NCOP PRESENTATION, 19 MARCH 2013

30

1 NATIONAL ROAD BASED PUBLIC TRANSPORT TRANSFORMATION PLAN: from bus to public transport subsidisation NCOP PRESENTATION, 19 MARCH 2013

description

NATIONAL ROAD BASED PUBLIC TRANSPORT TRANSFORMATION PLAN: from bus to public transport subsidisation. NCOP PRESENTATION, 19 MARCH 2013. Presentation Outline. Background Information Provincial Status Quo Investment in Public Transport Way Forward Funding Requirements - PowerPoint PPT Presentation

Transcript of NCOP PRESENTATION, 19 MARCH 2013

1

NATIONAL ROAD BASED PUBLIC TRANSPORT TRANSFORMATION

PLAN: from bus to public transport subsidisation

NCOP PRESENTATION, 19 MARCH 2013

2

Presentation Outline Background Information Provincial Status Quo Investment in Public Transport Way Forward Funding Requirements Implementation Programme Key Success Factors (Risks) Conclusion

3

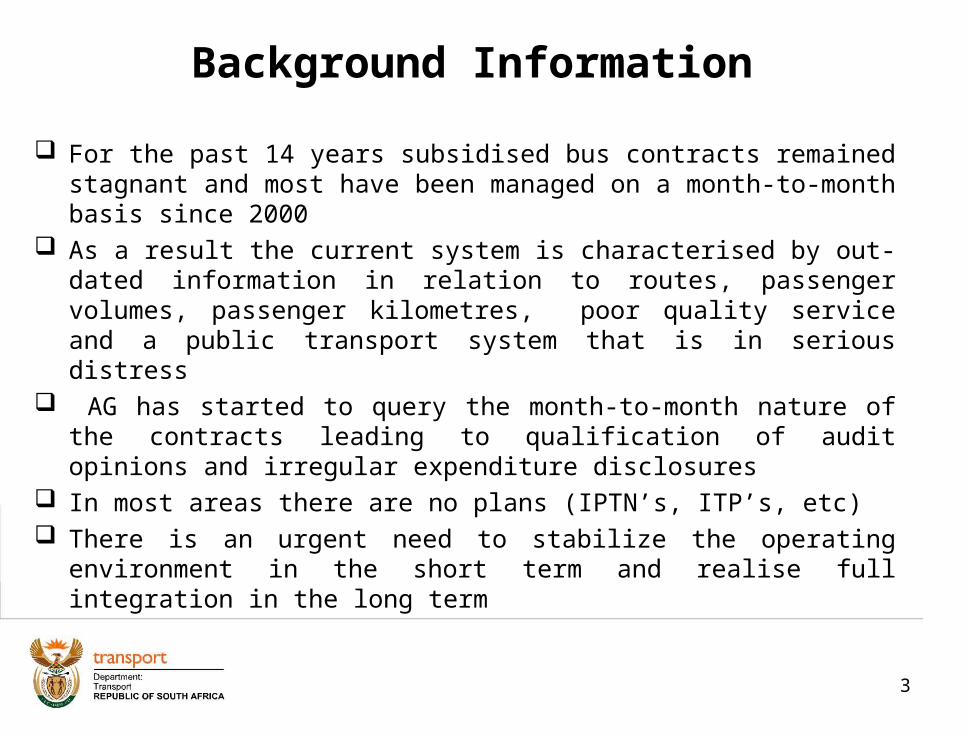

Background Information

For the past 14 years subsidised bus contracts remained stagnant and most have been managed on a month-to-month basis since 2000

As a result the current system is characterised by out-dated information in relation to routes, passenger volumes, passenger kilometres, poor quality service and a public transport system that is in serious distress

AG has started to query the month-to-month nature of the contracts leading to qualification of audit opinions and irregular expenditure disclosures

In most areas there are no plans (IPTN’s, ITP’s, etc) There is an urgent need to stabilize the operating environment in the

short term and realise full integration in the long term

4

Background Information

Provided for in Section 41 of the NLTA (No. 5 of 2009:

41. (1) Contracting authorities may enter into negotiated contracts with operators in

their areas, once only, with a view to—

(a) integrating services forming part of integrated public transport networks in

terms of their integrated transport plans;

(b) promoting the economic empowerment of small business or of persons

previously disadvantaged by unfair discrimination; or

(c) faciltating the restructuring of a parastatal or municipal transport operator to

discourage monopolies.

(2) The negotiations envisaged by subsections (1) and (2) must where appropriate include operators in the area subject to interim contracts, subsidised service contracts, commercial service contracts, existing negotiated contracts and operators of unscheduled services and non-contracted services.

5

Background Information…(modal split -road based)

Worldwide extensive funding support for public. Grounds: Economic: Vital for functioning and most economically efficient

means of (urban) travel Society: Equity, basic right of access Environmental / sustainability - least cost

Government funding to improve transport system effectiveness & sustainability and help achieve (spatial) development policy goals.

Background Information (Economic Rationale for Funding Support &

Subsidisation)

6

International Review-Total Cost of Transport Strategies

7

% local GDP on transportDeveloped cities High density, pro-public transport & NMT 5-7%

Low density, car based 12-15%Developing cities Low density sprawling 20% - 25%+

% M

etr

op

olit

an

GD

P

Source UITP 2006

Source UITP 2000

Conclusion: Compact cities with strong bias to public transport spend much less on transport with significant social and economic benefits

Richard Gordge

What do the red bars represent ?

Conclusion:Making public transport attractive (to all) requires major investments and subsidy. Only with increased corridor densities are operating cost

recovery likely to improve significantly.

International Review :Urban Densities and Operating Cost Recovery

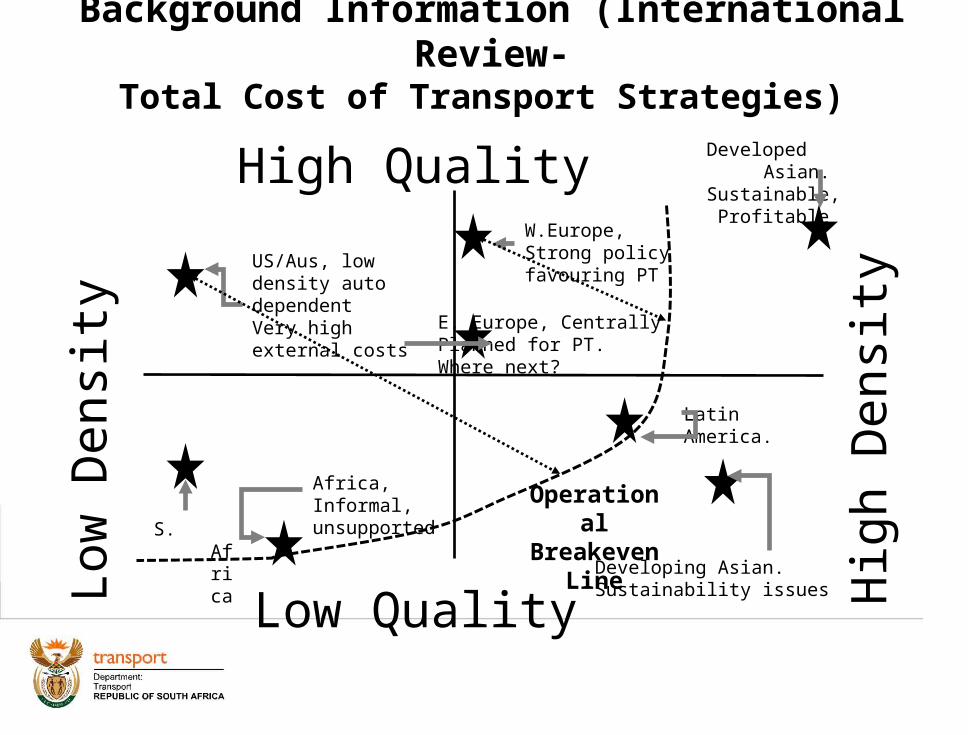

8Background Information (International Review-Total Cost of Transport Strategies)

High Quality

Low Quality

Low

Den

sity

Hig

h D

ensi

ty

Developing Asian. Sustainability issues

Developed Asian. Sustainable, Profitable

Latin America.

W.Europe, Strong policy favouring PT

E. Europe, Centrally Planned for PT. Where next?

US/Aus, low density auto dependent Very high external costs

S. Africa

Africa, Informal, unsupported Operational

Breakeven Line

International Review :Plot of Systems based on Quality & Density

9Background Information (International Review-Total Cost of Transport Strategies)

Comparators: PTOG Subsidy

Exclusively intra-urban routes

Rural settlements linkage to regional centres

• Rural linkage to regional centres

• Intra-Urban Routes

Ex-homeland to main urban routes

•Transport to mines•Some rural to urban routes

•Long urban commuter routes•Long distance rural to urban commuter trips

Background Information…(subsidized services spread) Source: GIPTN

11

Background Information… (subsidy funding history)

12

Provincial Status Quo (PTOG Contracts)

Province Nature and number of contracts 2012/13 BudgetTotal Interim Tendered Negotiated

Eastern Cape 1 1 0 0 174,466

Free State 7 0 5 2 192,872

Gauteng 34 8 26 0 1,625,746

Kwazulu Natal 39 2 36 1 808,279

Limpopo 11 7 1 3 260,725

Mpumalanga 7 7 0 0 439,003

Northern Cape 6 1 0 5 39,255

North West 4 0 1 3 80,686

Western Cape 1 1 0 0 696,237

GRAND TOTALS 110 27 69 14 4,317,269

13

PTOG split per Province

2012/13 PTOG allocation R4,317,269,000

14

PTOG split per contract type

About R2.9billion of the R4,3billion annual bus subsidy (PTOG) goes to interim contracts

The amount exclude provincial allocations (Limpopo, North West and Eastern Cape)

METROS TOWNSHIPS INTO METROS RURALPutco

SowetoGolden Arrow

Putco Sandfontein

NWS Botlhaba Interstate

Ripple Effect(KZN )

Av trip distance 46 26 73 81 48 82Trips / bus/ day 2.0 4.2 5.4 2.2 3.9 1.7Km/bus/day 81 129 225 160 165 152Pax/bus/day 136 166 203 157 176 130Pax/bus/km 1.67 1.29 0.90 0.98 1.06 0.85% subsidy 60% 63% 62% 61% 81% 69%Subsidy/pass. R 13 R 12 R 13 R 18 R 13 R 25Average fare R 8 R 7 R 8 R 12 R 3 R 11Cost/km 36 25 19 30 17 31

Contract Cost Analysis

World Bank

250

1000+

4.5

1 rtn tripv low pax/bus.High cost/km

Less dist.low pax/busHigh sub.

Long tripsInter-work

Better cost/km1 rtn Long tripHigh cost/km

V low fare !

High per tripSubsidy

Long distance.

18

South Africa – Current Funding PictureN

atio

nal G

over

nmen

t Fun

ding

(R

m)

14

Cap

ital

: B

ench

mar

k +

B

ackl

og

= 1

6 to

24

Op

erat

ing

:

Ben

chm

ark

= 8

to

16

(12

Cit

ies)

(Rbn

)

Current PT Investments

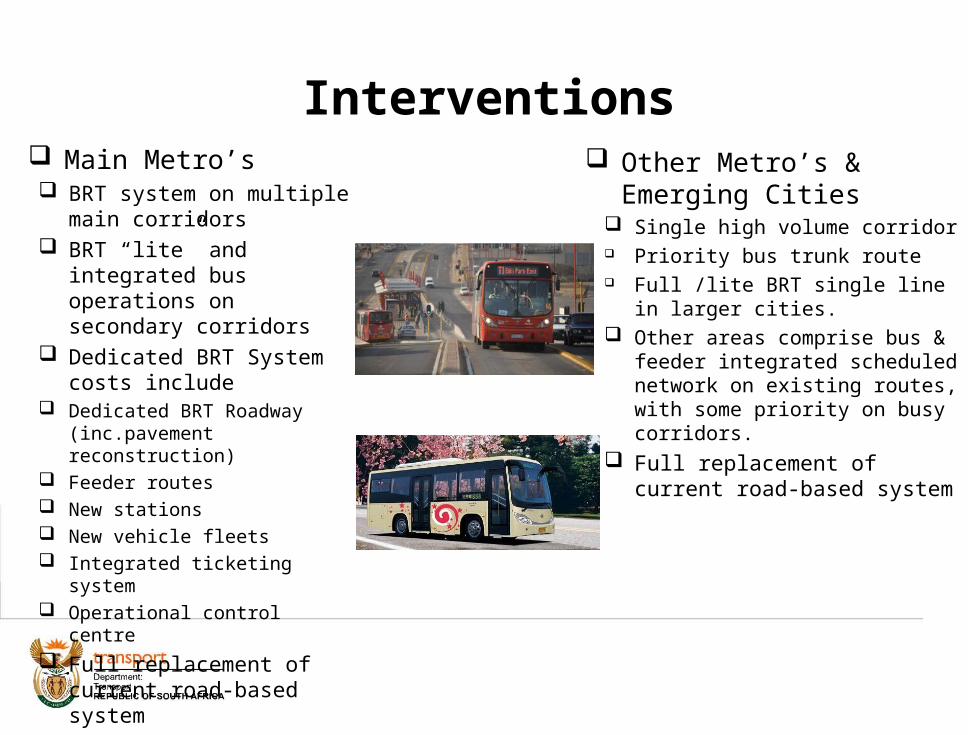

Interventions

23

Main Metro’s BRT system on multiple main

corridors BRT “lite” and integrated bus

operations on secondary corridors

Dedicated BRT System costs include

Dedicated BRT Roadway (inc.pavement reconstruction)

Feeder routes New stations New vehicle fleets Integrated ticketing system Operational control centre

Full replacement of current road-based system

Other Metro’s & Emerging Cities

Single high volume corridor Priority bus trunk route Full /lite BRT single line in larger

cities. Other areas comprise bus & feeder

integrated scheduled network on existing routes, with some priority on busy corridors.

Full replacement of current road-based system

Interventions24

Towns Formal bus system Inter-town services Mixed fleets including

Buses Midi buses Taxis

Full replacement of current road-based system

Scheduled services

High Density Rural and Rural Formalised mixed operations Vehicle re-cap Scheduled daily services to main centres Weekly services to regional towns Minimal infrastructure investments

Sparse Rural Selected interventions where viable Weekly & monthly services to towns Sharing services with health transport

and scholar transport Brokering, flexible scheduling and

confirmation of travel services No infrastructure costed

19

Way Forward

Why the need to transform: For the past 14 years subsidised bus contracts remained stagnant

and most have been managed on a month-to-month basis since 2000 As a result the current system is characterised by out-dated

information in relation to routes, passenger volumes, passenger kilometres, poor quality service and a public transport system that is in serious distress

AG has started to query the month-to-month nature of the contracts leading to qualification of audit opinions and irregular expenditure disclosures

In most areas there are no plans (IPTN’s, ITP’s, etc) There is an urgent need to stabilize the operating environment in the

short term and realise full integration in the long term.

20

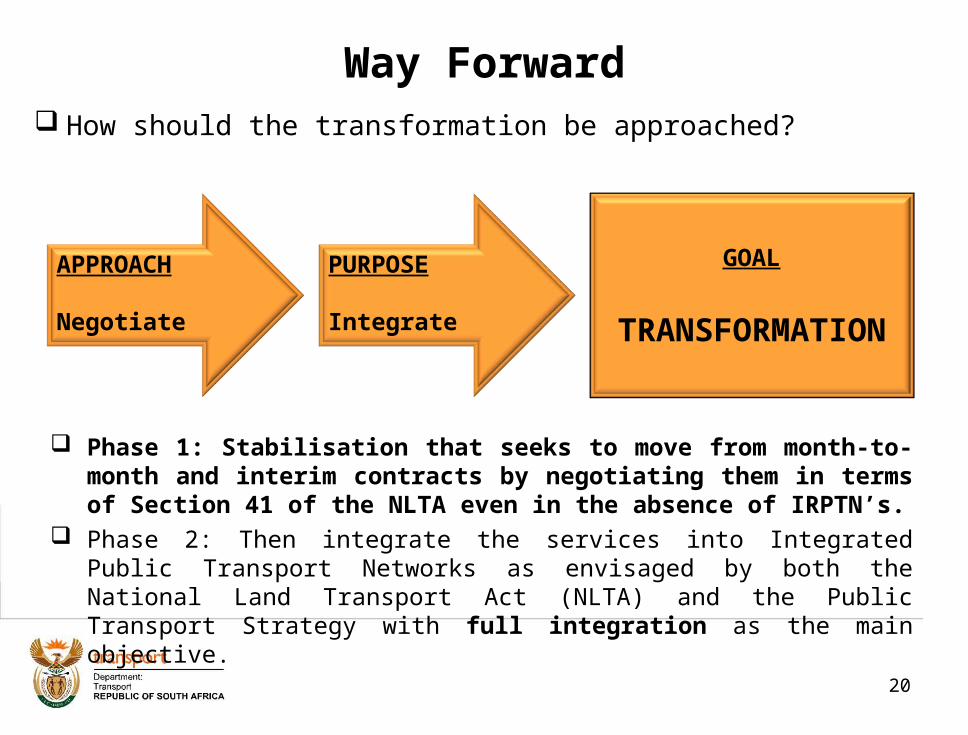

How should the transformation be approached?

Phase 1: Stabilisation that seeks to move from month-to-month and interim contracts by negotiating them in terms of Section 41 of the NLTA even in the absence of IRPTN’s.

Phase 2: Then integrate the services into Integrated Public Transport Networks as envisaged by both the National Land Transport Act (NLTA) and the Public Transport Strategy with full integration as the main objective.

APPROACH

Negotiate

PURPOSE

Integrate

GOAL

TRANSFORMATION

Way Forward

21

Phase 1: Stabilisation Funds permitting identify interim and/or old order contracts to be

negotiated. Initially target those that need to be unbundled and ensure that at least one such contract per province is negotiated.

Identify role players (mainly industry role players whose operations will be affected by the targeted contracts/ routes)

Develop an national implementation work programme and involve the municipalities.

Fast track the removal of impediments; notably legislation obstacles (develop a cooperation framework to deal with the contracting authority challenges)

Integrate the different funding sources, starting with the soon to expire TRP allocation (as taxis will be integrated into mainstream formal public transport system).

Mobilise more funding

Way Forward

22

High Density Urban Setup (travel demand, congestion, travel time, etc

Low Density Rural Setup (availability, access etc.)

Dedicated infrastructure & services (BRT?)

Quality PT services to enable access and mobility

Phase 2: Full integration based on IPTN’s Address the contracting authority challenges in the NLTA. Review the Public Transport expectations in relation to the “12 cities”

requirements with regard to IRPTN’s Adopt a differentiated approach for different PT challenges in the country

Ensure the modes (rail, bus and taxi) compete for the road and not on the road. Integrate (merge) the funding streams ( PTIS, PTOG, TRP, Green Fund, etc.). MinMec approved the plan (concept) in principle

Way Forward

23

Subsidy Requirement (Stabilisation)

24

Funding Requirements (full integration)

Province 2012/13 Allocation‘000

Taxi/SBO integration‘000

Eastern Cape 174,466 523,398

Free State 192,872 578,616

Gauteng 1,625,746 4,877,238

Kwazulu Natal 808,279 2,424,837

Limpopo 260,725 782,175

Mpumalanga 439,003 1,317,007

Northern Cape 39,255 117,765

North West 80,686 242,058

Western Cape 696,237 2,088,711

TOTAL 4,317,269 12,951,805

25

Proposed programme per provinceImplementation Programme for MTEF period 2014/15 to 2016/17

Province2014/15 2015/16 2016/17

Contract Funding required ContractFunding required Contract

Funding required

Eastern Cape AB350 Phase 2 119,466,000 Algoa Bus Service 57,985,012

Mayibiye Bus

Service 89,404,900 Total 208,870,900 57,985,012 Free State IBL 50,424,139 Maluti Bus Service 10,849,884 Thebeyagae 143,905 Total 50,568,044 10,849,884

Gauteng North West Star 126,315,607 Putco Mamelodi 8,168,867Brakpan Bus

Service 3,939,927

Putco Soweto 88,269,829 Putco Kwandebele 163,862,569Putco

Soshanguve 67,319,861

Boksburg

Operations 9,797,808South Western

Areas 34,419,242 Atteridgeville BS 17,353,511 Eldorado Park 9,483,947 Vaal Operations 24,775,684 Total 224,383,244 215,934,625 113,388,983

Kwazulu Natal Impendhle 4,075,077Combined Transport 8,905,084 BTI (Ulundi) 9,896,966

Sizananimazulu 16,194,338 Ikhwezi 25,476,666 TansnatAfrica 12,430,322 Duzi Bus Service 985,250 TansAfrica 34,735,982 Nondweni BS 3,327,414 Thembekile 1,334,750 Emondlo 8,401,122 RippleEffect 7,189,715 Dumbe 1,298,864 Darnall 1,364,175 Maphumulo 1,112,452 Total 29,779,130 81,294,345 25,654,702

26

Implementation Programme for MTEF period 2014/15 to 2016/17

Province2014/15 2015/16 2016/17

Contract Funding required ContractFunding required Contract

Funding required

LimpopoGreat North Transport 83,085,555 Risaba 2,349,907 Putco 131,079

Mabirimisa 8,895,020Lowveld Bus

Service 7,013,468

Bahwaduba 12,105,064Swangi's Transport 9,918,162

Magwaba 8,691,662 Mukondeleli 4,088,084 R Phadziri 4,703,564 Netshituni 9,543,173 G Phadziri 12,239,699 Mulaudzi 5,730,988 Enos 9,917,489 Mabidi 784,345 Total 83,085,555 58,902,405 37,209,299Mpumalanga Buscor 116,108,991 Megabus 14,358,051 Tilly's 2,279,075 Thembalethu 1,527,971 Putco 782,175 GNT 5,456,581 Total 116,108,991 15,886,022 8,517,831Northern Cape Phumatra 3,339,478 Unitrans 6,145,026 Total 9,484,504 North West Atamelang 29,803,582 Bojanala 69,529,999 Phumatra 6,284,887 Thari Bus Service 54,346,413 Total 90,434,882 69,529,999 Western Cape 0 Golden Arrow 231,399,282 Total 0 231,399,282

Grand Total 812,715,250 741,781,574 184,770,815

Proposed programme per province

27

Implementation Programme for MTEF period 2014/15 to 2016/17

Province2014/15 2015/16 2016/17

Contract Funding required ContractFunding required Contract

Funding required

LimpopoGreat North Transport 83,085,555 Risaba 2,349,907 Putco 131,079

Mabirimisa 8,895,020Lowveld Bus

Service 7,013,468

Bahwaduba 12,105,064Swangi's Transport 9,918,162

Magwaba 8,691,662 Mukondeleli 4,088,084 R Phadziri 4,703,564 Netshituni 9,543,173 G Phadziri 12,239,699 Mulaudzi 5,730,988 Enos 9,917,489 Mabidi 784,345 Total 83,085,555 58,902,405 37,209,299Mpumalanga Buscor 116,108,991 Megabus 14,358,051 Tilly's 2,279,075 Thembalethu 1,527,971 Putco 782,175 GNT 5,456,581 Total 116,108,991 15,886,022 8,517,831Northern Cape Phumatra 3,339,478 Unitrans 6,145,026 Total 9,484,504 North West Atamelang 29,803,582 Bojanala 69,529,999 Phumatra 6,284,887 Thari Bus Service 54,346,413 Total 90,434,882 69,529,999 Western Cape 0 Golden Arrow 231,399,282 Total 0 231,399,282

Grand Total 812,715,250 741,781,574 184,770,815

Proposed programme per province

28

THE PLAN

Adequate (additional)

and sustainable

funding

Good, strong inter-sphere

relations

Uniform standards

and guidelines.

Effective M & E

From leadership,

management and

stakeholders. Communicate

all the time

Contracting role

clarification; legal

justification to negotiate v competition

TRANSFORMATION

Funding Institutional Structures

Support Commitment Legislation

(un)certainty

Key Success Factors

All of the above can also be viewed as RISKS if not attended to

29

The Plan was approved by MinMec. FUNDING remains the main impediment to achieve total

transformation and integration. The Taxi Recapitisation Programme will continue until taxis are fully

integrated in mainstream PT. In its current form the programme has to run for a further 2 years to allow for: Finalisation of the option analysis Securing adequate funding

Efficiencies will have to be introduced into the programme

Conclusion

THANK YOU