NBAA 2011 Tactics to Avoid and Survive an IRS Audit · Document taxpayer’s intentions with leases...

78

Wolcott Aviation Seminars, LLC NBAA 2011 Tactics to Avoid and Survive an IRS Audit October 10, 2011 Jed R. Wolcott Certified Public Accountant

Transcript of NBAA 2011 Tactics to Avoid and Survive an IRS Audit · Document taxpayer’s intentions with leases...

Wolcott Aviation Seminars, LLC

NBAA 2011

Tactics to Avoid andSurvive an IRS Audit

October 10, 2011

Jed R. WolcottCertified Public Accountant

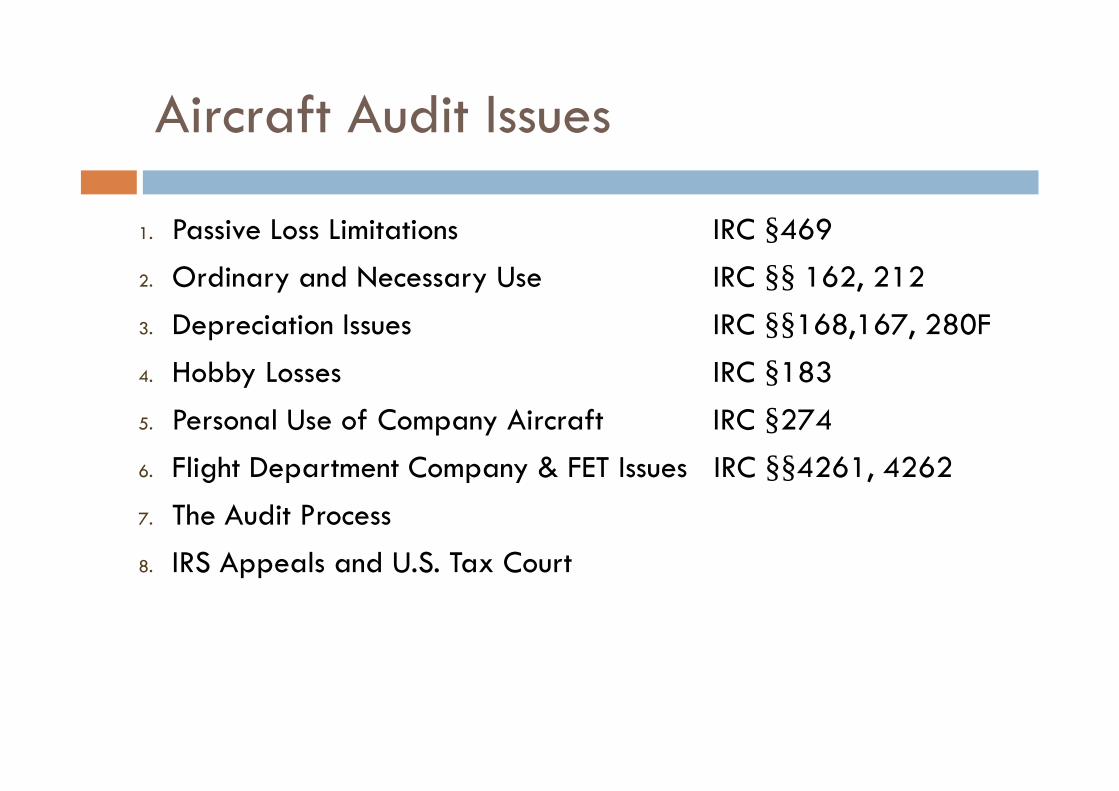

Aircraft Audit Issues

1. Passive Loss Limitations IRC §469

2. Ordinary and Necessary Use IRC §§ 162, 212

3. Depreciation Issues IRC §§168,167, 280F

4. Hobby Losses IRC §183

5. Personal Use of Company Aircraft IRC §274

6. Flight Department Company & FET Issues IRC §§4261, 4262

7. The Audit Process

8. IRS Appeals and U.S. Tax Court

Resource Materials

Copies of today’s materials are available at ourwebsite at www.aviation-cpa.com. Look for greenlookup bar

This PowerPoint presentation –

IRS code references on each slide

50101

Resource lookup

Audit Defense – Necessary Elements

Facts andCircumstances

IRS Code & Regulations

Tax CourtCases

Aircraft Audit Issues

Passive Loss LimitationsIRC § 469

Passive Loss Limitations (PAL) IRC §469

IRS limits use of losses from: Rental activities

Inadequate participation of owner

Causes: Lease to 135, rental company

Dry leases

Aircraft owner does not participate in activity

Result: Passive losses can only be used to offsetpassive income and often can not be used bytaxpayer

PAL Income

PAL Income includes:

Rental income

Income from activities where owner does not have material participation

Gain on sale of property used in a passive activity

Passive income generator (PIG)

PAL Income does NOT include:

Operating company income

Portfolio income (interest, dividends, annuities)

Income from working interests in oil and gas

Royalties from self-created intangibles

PAL Rules, Exceptions, and Grouping

There are 6 exceptions to the PAL leasing rules.Treas. Reg. § 1.469-1T(e)(3)(ii)(A)-(F)

There are 7 “tests” in the PAL material participationrules. Treas. Reg. §1.469-5T(a)(1)-(7)

PAL grouping rules provide a defense to the materialparticipation rules. Treas. Reg. § 1.469-4

Note, as of January 25, 2010, grouping election must be in writing, filedwith each tax return in the group

10601

10603

10604

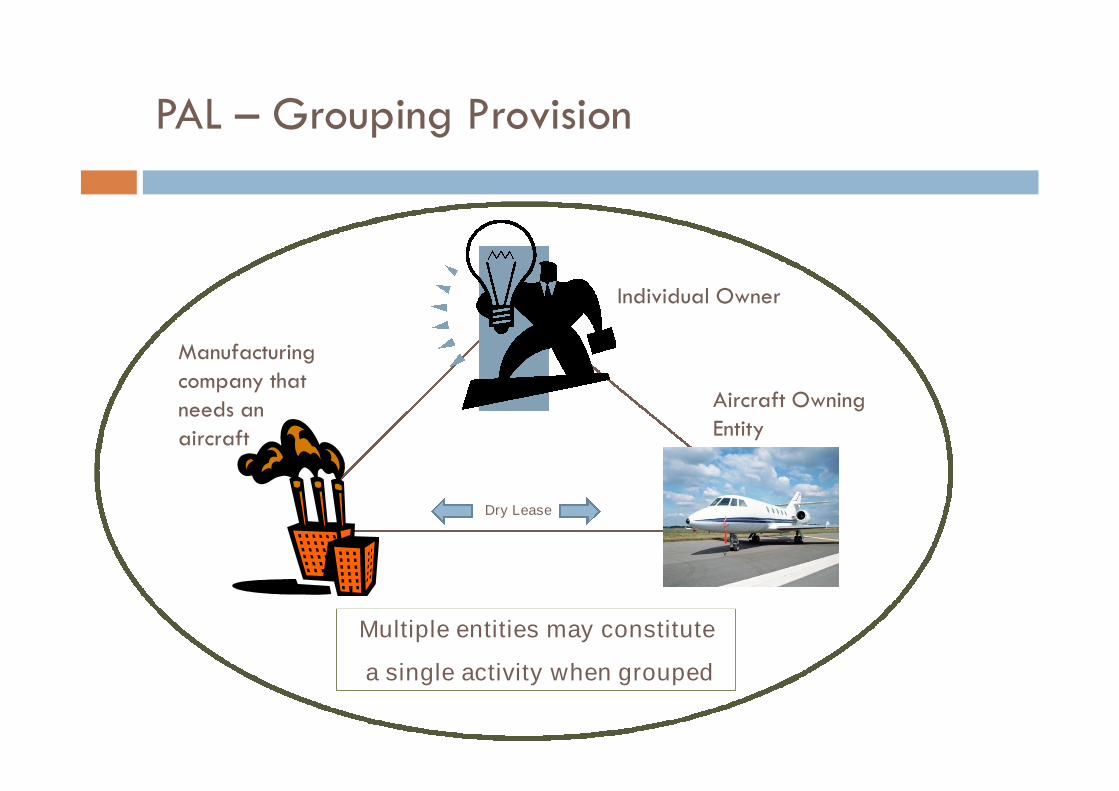

PAL – Grouping Provision

Dry Lease

Multiple entities may constitute

a single activity when grouped

Manufacturingcompany thatneeds anaircraft

Aircraft OwningEntity

Individual Owner

What to do Before the Audit

Separate active and passive activities to limitpassive effects

Amend returns to include grouping election

Restructure assignment of duties, prepare timelogs

Look for passive income opportunitiesRental real estate

Passive income generators (PIG)

Document taxpayer’s intentions with leases andin corporate minute books with annual meetings

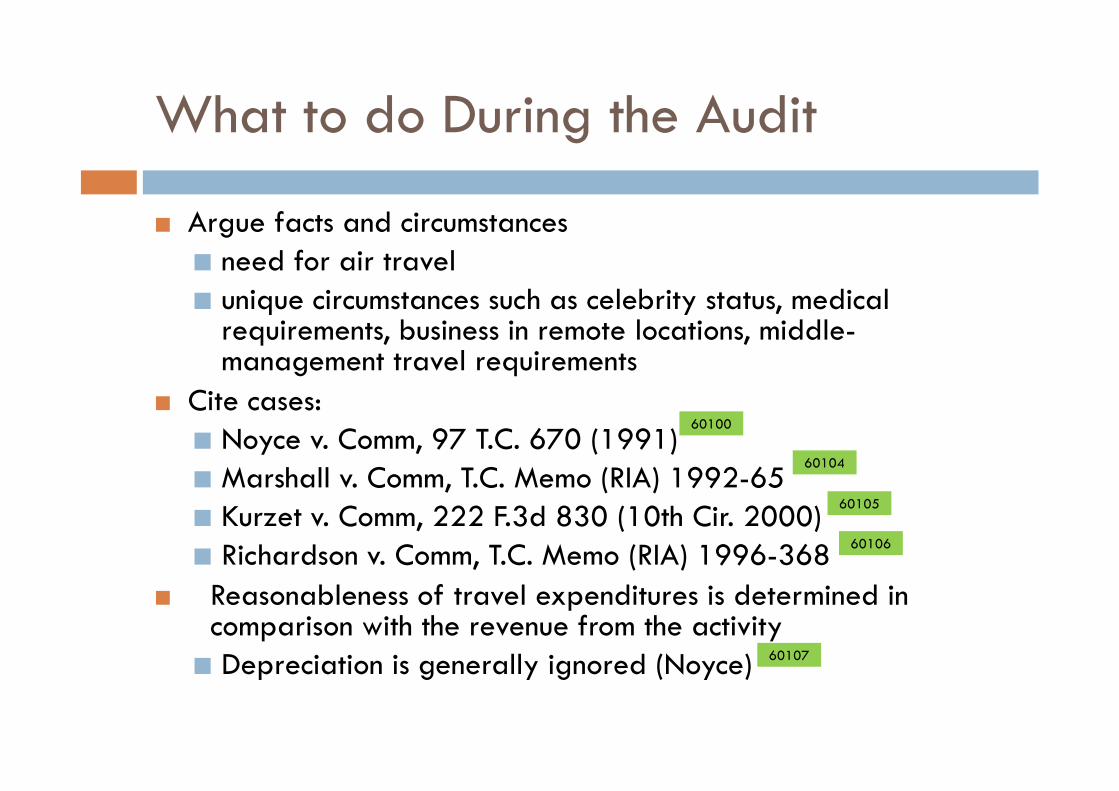

What to do During the Audit

Claim grouping if circumstances permit (new rulesafter Jan 25, 2010)

Prepare analysis of active and passive income andexpenses and request auditor allow restating

Test to see if insubstantial use criteria exists 80/20 test Candelaria vs. United States

Less than 2% aircraft FMV or other comparisons Treas. Reg. §

1.469-4(d)

Regulations give taxpayer substantial latitude toestablish material participation

Stress facts and circumstances

11003

60101

PAL/IRC§ 469 Cases

Leroy Candelaria and Elena Candelaria, Plaintiffs vs. UnitedStates of America, Defendant U.S. District Court, West. Dist ofTexas, El Paso Division, Civil Action No. EP-06-CV-0216-KC

Eugene J. and Kathryn A. Schumacher vs. Commissioner DocketNo. 18776-02S. 7/23/2003

Thomas Kenvill, Plaintiff v. U.S.A: U.S. District Court, Dist. N.D.,Northwestern Div., Civ. A3-96-135 11/06/97.

60103

60102

60101

Aircraft Audit Issues

Ordinary and NecessaryIRC §§ 162, 212

Ordinary and Necessary Business Expense -IRC §162

The IRS ordinary and necessary business expensestandard requires that an expense be: Appropriate Helpful in carrying on the taxpayer’s business A common and accepted practice Reasonable in amount Incidental to the business Not “lavish” or “exorbitant”

I.R.C. § 162(a)(2): 10101

Ordinary and Necessary Business Expense -IRC §162

Aircraft must be ordinary and necessary to thenormal course of business

Three hurdles must be overcome:

Air transportation is a business requirement

Air transportation need may only be met by privateaircraft

The aircraft is

appropriate for the

company’s use

Ordinary and Necessary Business Expense -IRC §162

IRS may try to limit deduction because aircraftwas inappropriate for specific travel requirement

Could limit deduction to first class airfare equivalent

May substitute reduced hourly operating rate

Ordinary and Necessary Business -Defenses

Little guidance in IRS regulations defining “Ordinaryand Necessary” use for aircraft

Arguments for and against “Ordinary andNecessary” use are often subjective and rely onfacts and circumstances

Court cases often helpful in defending taxpayerposition

No limitations on ordinary and necessary use citedin Sutherland , Midland Financial orNational Bankcorp cases

60110 60111

60112

What to do Before the Audit

Analyze company need for private air transportation

Consider trading if current aircraft is inappropriatefor company’s use

Document business use with corporate minutesapproving purchase and explaining businesspurpose. Prepare business plan and adopt inminutes

Maintain logs tracking business use, non-business use,training

What to do During the Audit

Argue facts and circumstances need for air travel unique circumstances such as celebrity status, medical

requirements, business in remote locations, middle-management travel requirements

Cite cases: Noyce v. Comm, 97 T.C. 670 (1991) Marshall v. Comm, T.C. Memo (RIA) 1992-65 Kurzet v. Comm, 222 F.3d 830 (10th Cir. 2000) Richardson v. Comm, T.C. Memo (RIA) 1996-368

Reasonableness of travel expenditures is determined incomparison with the revenue from the activity

Depreciation is generally ignored (Noyce) 60107

60106

60105

60104

60100

Aircraft Audit Issues

Depreciation IssuesIRC §§168, 167, 280F

Depreciation Audit Issues:

Non-compliance with Listed Property rules

Incorrect application of depreciation rates

Failure to follow 1031 tax free exchangeregulations

Failure to follow bonus depreciation rules

11000

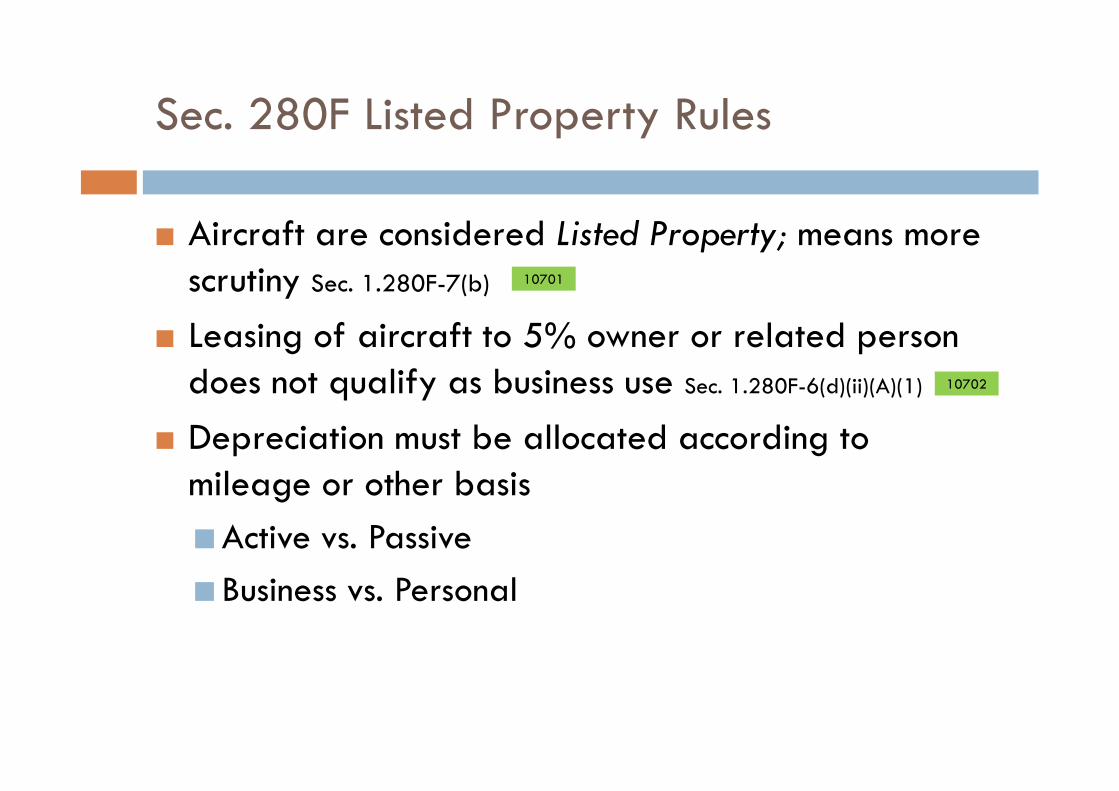

Sec. 280F Listed Property Rules

Aircraft are considered Listed Property; means morescrutiny Sec. 1.280F-7(b)

Leasing of aircraft to 5% owner or related persondoes not qualify as business use Sec. 1.280F-6(d)(ii)(A)(1)

Depreciation must be allocated according tomileage or other basis

Active vs. Passive

Business vs. Personal

10702

10701

Depreciation Rates for Aircraft

Only two tax depreciation methods available forbusiness aircraft:

+50% business use - taxpayer may use optionalModified Accelerated Cost Recovery System(MACRS)

-50% business use - taxpayer must use AlternativeDepreciation system (ADS)

Depreciation Rates for Aircraft - MACRS

Modified Accelerated Cost Recovery System(MACRS)

5 Year rate for Part-91 aircraft

7 Year rate for Part-135 aircraft

Depreciation rate must reflect predominant use each yearif use is split between Part-91 andPart-135

BIG GOTCHA: If MACRS is adopted andbusiness use falls below 50% taxpayer mustrecapture previous year’s excess depreciation

Depreciation Rates for Aircraft - ADS

Alternative Depreciation System (ADS) Straight LineDepreciation

6 Year rate for Part-91 aircraft

12 Year rate for Part-135 aircraft

Once ADS is elected, taxpayer cannot change

Bonus Depreciation Issues

Typical bonus depreciation audit issues: Not meeting contract requirements

Not meeting deposit requirements

Incorrect application of 1st year business-userequirements

Purchasing existing contracts

Failure to meet +50% business use in allsubsequent years

If you claim bonus depreciation,EXPECT TO BE AUDITED

1031 Tax-Free ExchangeRegulations IRC §1031

Rules for “Forward” and “Reverse” exchanges arecomplex

Completing the transactions within the specifieddeadlines is crucial

Failure to meet stat deadlines will cause gain on therelinquished aircraft to be recognized in the year ofsale

Suggestion: Use exchangecompany

11000

Single-Purpose Companies Have HighAudit Exposure

SPC’s are companies formed to only own an aircraft

Often used to shelter from potential liability, leaseaircraft back to owner

Typically S-Corps and multi-member LLC’s

Cash in equals cash out

Depreciation expense remains, very prominent

Very high audit selection rate

What to do Before the Audit

Consider restructuring SPCownership to limit auditexposure

Review 91 vs. 135 use to seeif rate is appropriate

If leasing, review use by 5%owners; amend if necessary

Consider the “visibility” ofbonus depreciation

What to do During the Audit

Depreciation is governed by statute andregulations, leaving little “wiggle room” duringaudit

Facts and circumstances of little value Ordinary and necessary rules prevail

Auditor satisfied that substantiation rules are met

Tax court cases won’t help much Noyce v. Commissioner 60100

Aircraft Audit Issues

Hobby LossesIRC §183

10500

Hobby Loss Rules – IRC §183

Restricts use of losses against other taxable incomeif activity is not “for profit”

IRS presumes activity is not a hobby if company hasprofits in 3 out of 5 years

If not 3 profitable years, IRS applies facts andcircumstances test

Hobby Loss Rules are dangerous because they allowIRS to disallow all operating costs, ownership costs,and depreciation. Can be big win for IRS

Hobby Loss Rules

IRS often cites Hobby Loss rules whenaircraft is owned by a single-purposecompany (SPC) Includes S-corps, multi-member LLC’s, and

Schedule C’s for individually-owned aircraft

Cash in often equals cash out, meaning no profitfrom day-to-day operations

SPC’s often have consistent loss years due todepreciation

Single Purpose Companies – Audit Targets

Copyright © 2009 Wolcott Aviation Seminars, LLC

Dry Lease

SPC

Owner

OperatingCompany

AircraftCompany

Example of Single-Purpose Company

ReportsLosses

Files Tax Return

Hobby Loss RulesTreas. Reg. §1.183-2(b)

IRS regulations provide a list of nine factors to test if anactivity is for profit, such as

1. Manner in which taxpayer carries on the activity

2. Expertise of the taxpayer or advisors

3. Time and effort expended

4. Expectation of future profits

5. Expectation that assets will appreciate in value

IRS also permits grouping of “hobby” activity with otherprofitable activityTreas. Reg. § 1.469-4(d) and Candeleria vs. Unites States

10502

11003 60101

Hobby Loss Rules (Continued)

Taxpayer might aggregate “hobby” activity with profitableactivity, 1.183-1(d)

Dry Lease

Owner

AircraftCompanyOperating

Company

NOTE: Include grouping decision reference in each taxreturn

10501

What to do Before the Audit

Hobby Loss Rules: Change ownership structure to

place aircraft in a profitableoperating company, or

Change ownership to makecompany a disregarded SM-LLC

Amend returns to include groupingelection

Create business plan, recordin Corporate Minute Book

Document, document, document

What to do During the Audit

Review the nine factors IRS uses to test if activity is forprofit

Other arguments:

Positive cash flow

Do not include depreciation in calculation or determiningIRC §183 loss test (see Noyce v. Commissioner)

Aircraft tend not to lose value, make good investment

Rental or charter use of aircraft pays down loan, buildsequity

Depreciation only defers taxes; gain or loss will resultwhen aircraft is sold

60100

IRC § 183 “Not Engaged in for Profit”

Bernard Cornfeld, Appellant, v. Commissioner, US Courtof Appeals D.C. Circuit 85-1243, 8/12/86.

Louismet v. Commissioner Dec. 39.054 43 T.C.M. 1496(1982)

Donald R. Campbell and Patricia A. Campbell v.Commissioner; US Court of Appeals, 6th Circuit 87-1892,2/23/1989, 868 F2d 833 60107

60109

60108

Aircraft Audit Issues

Personal Use ofCompany AircraftIRC § 274Reg § 1.61

10400

10304

Personal Use of Company Aircraft

For individual-owned aircraft, including aircraft ina single-member LLC owned by an individual:

Apply primary purpose test, similar to howindividual-owned autos are reported

Deduct pro-rata portion of direct costs, ownershipcosts and depreciation for non-business flight use

No distinction between non-business andentertainment flights; use is either business or non-business

10100

Personal Use of Company Aircraft

For aircraft owned by a Corporation, S-Corp orPartnership and provided with pilot(s):

Employees must report SIFL1 taxable income for non-business flights

Cash reimbursements may satisfy this requirement

Company must apply American Jobs Creation Act of2004 cost limitations for entertainment flights by“specified individuals” and guests

1Standard Industry Fare Level rates published by DOT

10400

10300

Personal Use of Company Aircraft -Defenses

Use of SIFL valuation provides “safe harbor”

Application and use of SIFL – Cases

Sutherland Lumber-Southwest v. Commissioner: US-CT-APP-8th Circuit 00-2827, 7/3/2001

Midland Financial Co. & Subs. v. Commissioner:Docket Nos.12302-99, 4574-00;TCM 371,8/1/2001

National Bankcorp of Alaska, Inc. v. Commissioner:Docket No. 6388-00 TCM 369, 8/1/2001 60112

60111

60100

Personal Use Of Company Aircraft –Defenses (continued)

Entertainment Cost Limitations

No “safe harbor” rules

Follow Notice 2005-45

Follow proposed Reg. 1.274-10

No cases yet (legislation is too recent)

10307

10300

What to do Before the Audit

Personal Use of Company Aircraft:

Amend employee personal tax returns to include SIFL

Amend company returns to recognize the entertainmentcost disallowance rules for aircraft-owning entity

Amend returns for non-business use deduction forindividually-owned and flown aircraft

Document business flights; make sure flight logs supportbusiness and non-business use IRC § 274(d)(4) 10305

What to do During the Audit

Expect the auditor to disallow all costs, expenses anddepreciation until taxpayer proves business use

If SIFL overlooked, request auditor permit amending the1040 returns

If entertainment cost disallowance deductions wereoverlooked, request auditor permit amending companyreturns

Key strategy is to get business use of the aircraft deducted(think about the future aircraft use)

Aircraft Audit Issues

Flight DepartmentCompanyIRC §§4261, 4262

1080110800

Flight Department Company Issue –IRC § 4261

Entity only owns and operates the aircraft

Pays DOC’s including pilots

Only purpose is to provide air transportation

Commercial says IRS!!!! – Excise tax owed:

7.5% of all costs, plus

$3.70 per passenger (2011)

6.25% for freight

See Notice 2005-62

10800

10804

Typical Flight Department CompanyStructure

Provides

Aircraft

IndividualOwner

OperatingCompany

AircraftCompany

Owner says:

“I’m simplyproviding my

company with anaircraft”

IRS says:

“You are providingair transportation

services. FETapplies”

Pilot(paid byaircraft

company)

Flight Department Company – How toRestructure – Pros and Cons

Convert “wet lease” to “dry lease”

Create separate management company to employpilots?

OK, providing the lessee pays the pilots

Note potential problem: This strategy could convertactivity to passive

Key issue – who controls the pilot?

Caution: It is too late to restructure after the audithas commenced

Affiliated Group Exemption as a FlightDept. Co. Audit Defense – IRC 4282

Allows large company with many subsidiaries toform an “aircraft operations” entity to operate thecompany aircraft without incurring FET liability

Must be a common parent owning at least 80% ofeach includable subsidiary

Certain entities are not includable, including S-corporations (IRC Sec. 1504)

Exemption does not apply to flights provided tothird parties outside of the affiliated group

10802

11001

What to do Before the Audit

Convert wet leases to dry leases (canbe as simple as changing whichcheckbook is used)

Have written leases making clear whopays the pilots

Hire (or create) a managementcompany to provide pilots

If claiming affiliated groupexemption, be sure all entities usingthe aircraft qualify

What to do During the Audit

Argue facts and circumstances

Examine the flight logs for exempt flights

Aircraft with MTOW < 6,000 lbs are exempt

If the aircraft was operated between subsidiaries,see if the Affiliated Group Exemption applies

Analyze all IRS findings and positions and considera negotiated settlement

If settling, depreciation is not included as expense;only cash amounts paid are subject to FET

If required to pay FET, claim fuel tax credits10803

Flight Department Company – Cases

Petit Jean Air Service v. United States; US District Court, East Ark.LR-71-6-216, 2/7/1974. Winthrop Rockefeller (formerGovernor of Arkansas) leased aircraft to corporation for liabilitypurposes. Corporation employed pilots, operated aircraft forowner and others. IRS imputed FET per Sec. 4262 on all travel.Court reversed for owner use, held for FET on 3rd party use ofaircraft.

60113

The Audit Process

Every Issue Won at Field Audit Level is aVictory!

Consider the field auditor the “Traffic Cop”

Easier to argue a ticket on the street than in TrafficCourt

Any issue eliminated at the audit level is gone

THE FIELD EXAMINATION IS THE MOSTCRUCIAL PORTION OF THE AUDIT

At This Stage

EVERYTHING IS NEGOTIABLE

If you can’t settle the case at the audit level, thensomeone is being unreasonable

Supervisor Negotiations

Negotiations become more difficult as the auditprogresses

Taxpayer can always request a supervisor meeting Supervisor is obligated to attend final meeting if

taxpayer requests

Strategy: Probably nothing to lose to demand meeting

Make auditor and supervisor aware by your actionsthat you are prepared to take the case to court if asettlement can’t be reached at Appeals

Always request that supervisor abate penalties

30-Day Letter

Notifies taxpayer of right to appeal to proposedadjustments within 30 days

Package will include a copy of auditor’sexamination report and Notice of ProposedAdjustments

For individual - Form 4549-E and Letter 3605-A

For corporation or partnership - Letter 1085

If Taxpayer intends to take case to Appeals, IRSrules permit 30 days to file Protest Letter

Note that the 30-day period is strictly enforced

90-Day Letter

If taxpayer does not respond to 30-day letter, IRSsends 90-day letter

Also known as Statutory Notice of Deficiency

Gives taxpayer 90 days (150 days if out ofcountry) to file a petition with Tax Court

If taxpayer still does not respond, the case isclosed, and the Notice of Deficiency is sent toCollections

Note that the 90-day period is strictly enforced

The Appeals Process

The Appeals Process

Appeal level formed over 60 years ago

Provides administrative alternative to litigating atax dispute

Appeals Hearing Officer has authority to determineaudit liabilities

Stays the collections process

Appeals office goal is to “settle” disputes betweenthe IRS and taxpayer

The Appeals Process

Appeals typically settles 70% of cases filed

Appeals settlement typically results in a 40%reduction of taxes calculated in the audit

Use FOIA to request auditor files and field notes

Bringing CPA and/or attorney shows the IRS thatyou are serious

Make clear that you are prepared to take the caseto court

Advantages in Appealing

Appeals Hearing Officer is hired to settle cases, andmost do so

Hearing Officers are generally more experienced thanfield auditors

Hearing Officer must weigh “hazards of litigation”

Allows taxpayer to keep open the option of Tax Court

Appeals “tolls” the collection process

Allows the taxpayer time and additional information onIRS position to develop court case more completely

Limitations to IRS Appeals

Appeals Office must follow IRS Revenue Rulings

In cases involving a refund or overpayment in excess of$200,000, report must be made to Joint Committee onTaxation of Congress before refund can be issued Reg.

§601.106(g)

Appeals agents are required to protect thegovernment in “whipsaw” cases where settlementcould effect another case, such as alimony

Additional limitations apply

11003

The Appeals Hearing

Informal conference usually handled in HearingOfficer’s office

May involve multiple meetings (don’t be hesitant toask)

Case may require additional information

Hearing may be held by phone or in person

IRS tries to hold appeals in the District, but taxpayerhas no control over where the Hearing Officer islocated

Fast Track Options

Fast Track Mediation

Small Business/Self Employed (SB/SE) option

Most disputes resolved within 40 days

Designed to settle disputes during the audit (prior to30- day letter issuance)

Available for:

Examinations (audits)

Offers in compromise

Disputes over trust fund recovery penalties

Other collection actions

Fast Track Settlement (FTS) IRC 6103(c)

Process for prompt resolution of Large and Mid-Size(LMSB) Business Tax Issues

FTS jointly administered by LMSB Division and Office ofAppeals

When appropriate, FTS may resolve audit issues in lessthan 120 days, rather than LMSB/Audit-Appealsprocess that averages 2 years

Brings Appeals Office resources to the audit site

Optional to taxpayer

Also available at selective locations for SmallBusiness/Self Employed (SB/SE)

COURT OPTIONS

U.S. Tax Court

U.S. Tax Court is under the jurisdiction of the HouseWays and Means and Senate Finance Committees

The Tax Court is the preferred forum for litigatingtax disputes

Most cases are represented pro se

Taxpayer may be represented by practitionersadmitted to the bar of the Tax Court

Attorneys admitted to practice before the SupremeCourt are admitted by application

CPA’s and Enrolled Agents admitted by passing anexamination

U.S. Tax Court

Once a case is docketed, the IRS assigns the caseback to Appeals Division to try and settle

80% of docketed cases are settled prior to trial

Most cases do not require witnesses; many casescan be argued on brief

The taxpayer, a CPA, or lawyer may prepare aTax Court petition to preserve a client’s rights to aredetermination

District Court and the Court of FederalClaims

Can take your case here only after tax is paid -as opposed to Tax Court where you are disputingthe deficiency before paid

Optional trial by jury

Procedures for filing claims are available at

U.S. District Court www.uscourts.gov

U.S. Court of Federal Claims www.cofc.uscourts.gov

Final Points

Be sure to incorporate all 3 foundation elements inyour defense:

IRS Code and Regulations

Tax Court cases

Facts and circumstances

Fight all IRS positions at the field-audit level; don’twait until later to begin to build your defense

Cases become more expensive to fight at Appeals orTax Court levels

Don’t be intimidated by Appeals or Tax Court options.

Resources:

www.aviation-cpa.com

Flight Tax Systems, Inc. – Coming Soon

Copyright © 2011 Wolcott Aviation Seminars, LLC

Aviation software created to assist aircraft ownersand operators in properly recording anddocumenting business flight use. Calculates: Primary purpose flights

SIFL

Entertainment cost disallowance

And Much More!

Call for more information 954-763-9363

Thank You Very Much!

Jed R. Wolcott, MBACertified Public Accountant

Wolcott Aviation Seminars, LLC5525 NW 15th Avenue, Suite 203Fort Lauderdale, Florida 33309

954-763-9363www.aviation-cpa.com