Navigating the new world of IFRS 16 Leases€¦ · Lease accounting – Future • IFRS 16 issued...

30

Navigating the new world of IFRS 16 Leases CFLA Conference - September 22, 2016

Transcript of Navigating the new world of IFRS 16 Leases€¦ · Lease accounting – Future • IFRS 16 issued...

Navigating the new world of IFRS 16 Leases

CFLA Conference - September 22, 2016

© Deloitte LLP and affiliated entities.

IFRS 16 – Leases Agenda

This presentation and its contents are intended for informational purpose only.

Introduction and Background

Presentation and discussion on accounting under IFRS 16

• Lessee accounting

• Lessor accounting

Practical challenges and implications on leasing strategy

Wrap up / questions

This presentation and its contents are intended for informational purposes only.

Navigating the new world of IFRS 16 Leases 2

© Deloitte LLP and affiliated entities.

BackgroundSetting the stage

Navigating the new world of IFRS 16 Leases 3

© Deloitte LLP and affiliated entities.

The accounting frameworksSetting the stage

What are the GAAPs?

International Financial Reporting Standards“IFRS”

Accounting Standards for Private Enterprises“ASPE”

U.S. GAAP

Who does it apply to?

• Canadian public companies• International

public companies• Canadian private companies

who have chosen to use IFRS

• Canadian private companies• Certain subsidiaries of

U.S. parents

• U.S. parent (both public and private)

• Certain Canadian public companies who have chosen U.S. GAAP

Lease accounting –Current

• IAS 17 • CPA Handbook, CICA 3065 • FAS 13 (ASU 840)

• Distinction between finance and operating leases• For lessees, operating leases are off balance sheet and finance leases are on balance sheet• For lessors, assets relating to operating and finance leases are recognized on balance sheet

(although characterization differs)

Lease accounting –Future

• IFRS 16 issued January 2016 • No current changes proposed

• ASU 842 issued February 2016

Implementation date

• Annual periods on or after January 1, 2019

• Annual periods beginningJanuary 1, 2019, for public business entities,January 1, 2020, for all other entities

Navigating the new world of IFRS 16 Leases 4

© Deloitte LLP and affiliated entities.

The Canadian marketWho is impacted?

1,167,978

-

-

1,899

-356

SMALL TO MEDIUM SIZE ENTITIES (SME) PUBLIC COMPANIES

PUBLIC VS. PRIVATESMEs Public companies adopting IFRS Public companies adopting U.S. GAAP

A subset of these entities may use IFRS and US GAAP but most will likely use ASPE

5

The above chart is based on the data from Statistics Canada, Business Register, December 2015 and SEDAR. The chart is for illustration purposes. Actual numbers of businesses may vary based on market data sources used.

This is the subset impacted by IFRS 16

This is the subset impacted by ASC

842

Navigating the new world of IFRS 16 Leases

© Deloitte LLP and affiliated entities.

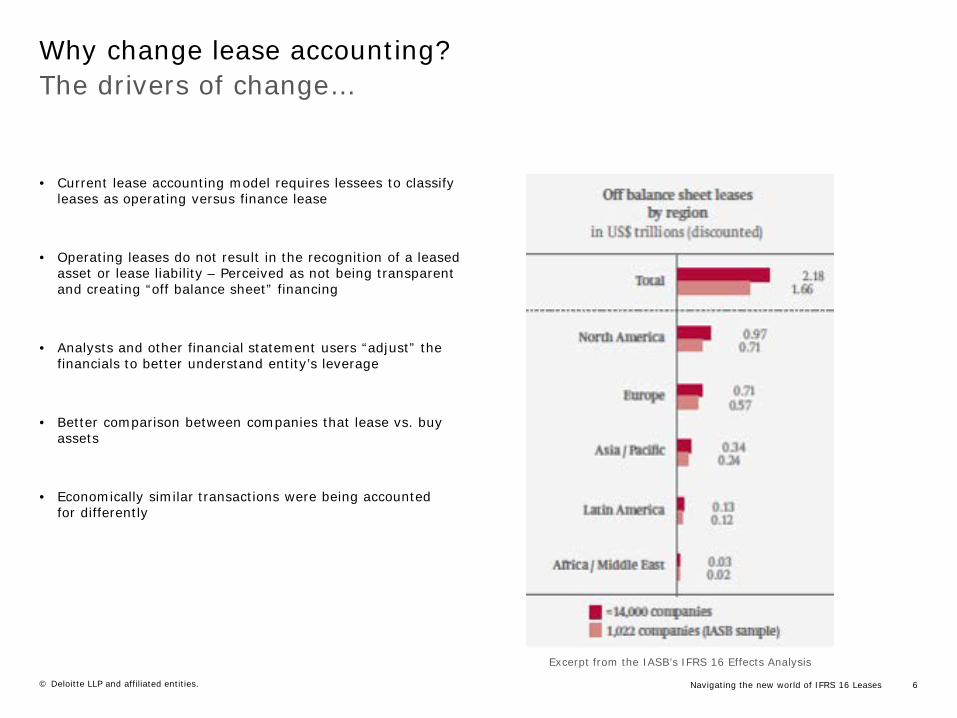

Why change lease accounting?The drivers of change…

• Current lease accounting model requires lessees to classify leases as operating versus finance lease

• Operating leases do not result in the recognition of a leased asset or lease liability – Perceived as not being transparent and creating “off balance sheet” financing

• Analysts and other financial statement users “adjust” the financials to better understand entity’s leverage

• Better comparison between companies that lease vs. buy assets

• Economically similar transactions were being accountedfor differently

Excerpt from the IASB’s IFRS 16 Effects Analysis

Navigating the new world of IFRS 16 Leases 6

© Deloitte LLP and affiliated entities.

IFRS 16 - LeasesThe accounting

7Navigating the new world of IFRS 16 Leases

© Deloitte LLP and affiliated entities.

The HighlightsIASB issues IFRS 16

8

Project concluded –long time in works

Joint project with US – converged in some respects but

not all

Most leases on balance sheet for

lessees

Lessor accounting largely unchanged

Data and systems may be impacted

2019 timeline but clock ticking now

Navigating the new world of IFRS 16 Leases

© Deloitte LLP and affiliated entities.

TimelinesTransition

Entities can elect to apply either

I. Full retrospective approach (as if always applied) or

II. A ‘modified’ retrospective approach with no restatement of comparatives (adjust opening retained earnings)

1 Jan 20191 Jan 2018

December year-ends:Retrospective application with restatement

December year-ends:Effective date

Comparative period

Navigating the new world of IFRS 16 Leases 9

© Deloitte LLP and affiliated entities.

Lessee accounting

Navigating the new world of IFRS 16 Leases 10

© Deloitte LLP and affiliated entities.

Lessee accountingIn a nutshell – “before” and “after”

Old standard New standard

Balance Sheet FY 20xx $

Lease assets xxx

Lease liabilities xxx

Income statement FY 2015 $

Low-value/short-term leases xxx

EBITDA xxx

Depreciation and amortisation xxx

Finance cost xxx

Profit before tax xxx

Balance Sheet FY 20xx $

Income statement FY 2015 $

Lease payments xxx

EBITDA xxx

Profit before tax xxx

Navigating the new world of IFRS 16 Leases 11

© Deloitte LLP and affiliated entities.

In a nutshellLessee accounting

EBITDA

Profit profile (lower in earlier years of lease)

Assets and liabilities

Impact on gearing

Operating cash inflows

Financing cash outflows

Balance sheet Income statement Cash flow statement

• Recognise lease assets and liabilities on balance sheet.

• Initially measured at the present value of unavoidable lease payments.

• Consider impact on KPIs, lending covenants, earn-outs, bonus programs, etc.

• Repayment of principal: finance activities

• Repayment of interest: finance or operating activities (depends on accounting policy for interest).

• Some variable payments, payments from short-term leases and from assets of low value: operating activities

• No change to total cash flows as no change to the economics. Pattern of recognition has changed.

Navigating the new world of IFRS 16 Leases 12

© Deloitte LLP and affiliated entities.

Initial measurement Lessee accounting

At commencement date: recognise right-of-use asset and lease liability

Lease liability Right-of-use asset

Present value of lease payments Cost

Rate implicit in the lease or Incremental borrowing rate

The capitalized asset and liability would likely still be lower than purchased asset and debt as it is only the economically unavoidable payments under the lease contract that come on balance sheet.

Navigating the new world of IFRS 16 Leases 13

© Deloitte LLP and affiliated entities.

Initial measurement Lessee accounting

14

Payments made less incentives receivable after commencement date

Commencement date

Payments made less incentives received beforecommencement date

Measurement of lease liability

Cost of right-of-use asset

Discounted at:Rate implicit in the lease or Incremental borrowing rate

Navigating the new world of IFRS 16 Leases

© Deloitte LLP and affiliated entities.

Lease paymentsLessee accounting

Fixed payments

less incentives

Exercise price of purchase

option (reasonably

certain)

Variable payments

(e.g., CPI/rate)

NPV =

Lease liability Right-of-use asset

Payments less incentives

before commence-ment date

Initial direct costs

Lease liability

Estimated cost for

dismantling restoring

asset

Expected residual value

guarantee Penalty for terminating

(if reasonably certain)

Navigating the new world of IFRS 16 Leases 15

© Deloitte LLP and affiliated entities.

Lease term – Extension and termination options Lessee accounting

Option to extend

Option to terminate

Non-cancellable period

Reassess significant event or change in circumstances that lessee controls and affects whether exercise ‘reasonably certain’. Revise: change in non-cancellable period.

‘Reasonably certain’

Consider all facts and circumstances that create an economic incentive, including expected changes:

• Contractual terms for optional periods

• Significant leasehold improvements

• Costs of termination and return

• Importance to operations (specialized, location, alternatives)

• Conditionality associated with option

Navigating the new world of IFRS 16 Leases 16

© Deloitte LLP and affiliated entities.

Right-of-use asset

Subsequent measurementLessee accounting

Lease liability

Navigating the new world of IFRS 16 Leases 17

Time

Expe

nse

prof

ile

Constant periodic rate of interest (P&L- finance cost)

Increase the lease liability to reflect the interest

Decrease the lease liability to reflect payments made

Time

Expe

nse

prof

ile

(P&L - depreciation)

Apply depreciation requirements in IAS 16

Depreciate over the useful life (taking extension options into consideration)

Impairment under IAS 36

© Deloitte LLP and affiliated entities.

Recognition exemptionsLessee accounting

Accounting policy choice:

Apply IFRS 16 or straight-line the expense

(if applying the exemption: Apply IAS 37 to assess onerous contracts)

Short-term leases (12 months or less)

Has a lease term at commencement of 12 months or less

Not highly dependent on, or highly interrelated with, other assets

Low-value leases

A lease that contains a purchase option is not a short-term lease

Assessment on an absolute basis (new asset value of < $5K)

Navigating the new world of IFRS 16 Leases 18

Election by class of underlying asset Election on a lease-by-lease basis

© Deloitte LLP and affiliated entities.

Combining or separating contracts Lease contracts

*Both lessees and lessors are required to separate lease components from non-lease components

Account for as a single contract Account for each component separately

Account for separately from non-lease components of a

contractor

Elect not to separate (by class) – Lessees

Non-lease

Combine two or more contracts Identify separate lease components*

Identify separate non-lease components (e.g., service)*

Navigating the new world of IFRS 16 Leases 19

The practical expedient is

only available to lessees, not lessors

Separating the non-lease components reduces the amounts recognized for the lease asset and liability

© Deloitte LLP and affiliated entities.

Portfolio application Lease contracts

Lease

Lease Lease

Lease

Lease

Lease

Lease

Lease

Practical expedient for leases with similar characteristics

20Navigating the new world of IFRS 16 Leases

• Should not be expected to result in materially different accounting

• Likely to apply to leases for items such as vehicles where they are all part of a master agreement

© Deloitte LLP and affiliated entities.

A comparison of IFRS 16 model with the FASB model (ASC 842)Lessee accounting

IFRS 16 U.S. GAAP (FASB model)

All leases Former on-B/S leases

Former off-B/S leases

Balance sheet

Recognition

All leases on balance sheet

Exemption for short-term leases

Exemption for leases of low-value assets --- ---

Measurement

Lease liabilities on a discounted basis

Initial lease asset = lease liability

Depreciation of lease assets Typically straight-line

Typically straight-line

Typically increasing

PresentationLease liabilities IAS 1 Separate

presentation (from former off b/s lease)

Separate presentation (from

former off b/s lease)Lease assets PPE or own line

Income statement

Operating costs Depreciation Depreciation Single expense

Finance costs Interest Interest ---

Cash flow statement

Operating activities Interest Interest Interest and principal

Finance activities Principal Principal

Navigating the new world of IFRS 16 Leases 21

© Deloitte LLP and affiliated entities.

Lessor accounting

Navigating the new world of IFRS 16 Leases 22

© Deloitte LLP and affiliated entities.

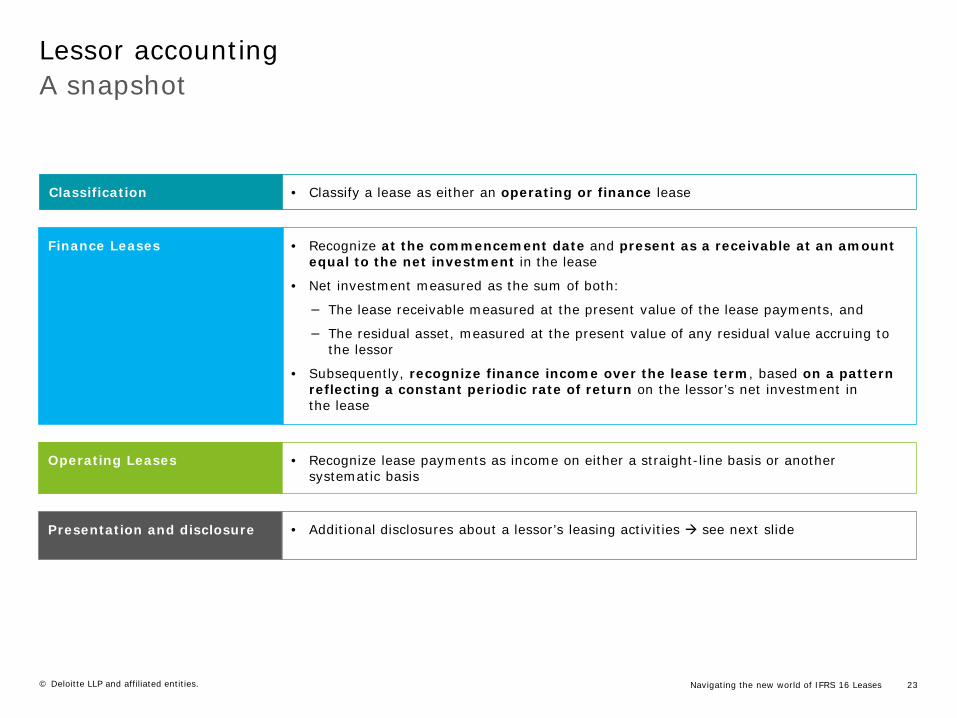

A snapshotLessor accounting

Classification • Classify a lease as either an operating or finance lease

Finance Leases • Recognize at the commencement date and present as a receivable at an amount equal to the net investment in the lease

• Net investment measured as the sum of both:

− The lease receivable measured at the present value of the lease payments, and

− The residual asset, measured at the present value of any residual value accruing to the lessor

• Subsequently, recognize finance income over the lease term, based on a pattern reflecting a constant periodic rate of return on the lessor’s net investment in the lease

Operating Leases • Recognize lease payments as income on either a straight-line basis or another systematic basis

Presentation and disclosure • Additional disclosures about a lessor’s leasing activities see next slide

Navigating the new world of IFRS 16 Leases 23

© Deloitte LLP and affiliated entities.

DisclosuresLessor accounting

Finance leases

• Selling profit or loss

• Finance income on the net investment in the lease

• Income relating to variable lease payments not included in the measurement of the net investment in the lease

• Qualitative and quantitative explanation of the significant changes in the carrying amount of the net investment in finance leases

• A maturity analysis of the lease payments receivable

Operating leases

• Lease income

• Income relating to variable lease payments that do not depend on an index or a rate

• Apply IAS 16 disclosure requirements for items of PPE

• Apply disclosure requirements in IAS 36, IAS 38, IAS 40 and IAS 41 for assets subject to operating leases if applicable

• A maturity analysis of lease payments

Other

• The nature of the lessor's leasing activities

• How the lessor manages the risk associated with any rights it retains in underlying assets

Navigating the new world of IFRS 16 Leases 24

© Deloitte LLP and affiliated entities.

Leasing strategyPractical challenges and implications

Navigating the new world of IFRS 16 Leases 25

© Deloitte LLP and affiliated entities.

Who is expected to be impacted?Leasing strategy

The above chart is based on the data from the IASB’s Effect Analysis

Navigating the new world of IFRS 16 Leases 26

Africa/ Middle East

Latin America

Asia/Pacific

Europe

North America

Total

Off-balance sheet leasesby region

in U.S.$ trillions (discounted)

≈ 14,000 companies

Excerpt from the IASB’s IFRS 16 Effects Analysis

Impact by industry

Airlines (23%) Retailers (21%)Travel & leisure (21%) Transport (12%)Telecommunicationns (6%) Energy (6%)Media (6%) Distributors (4%)Information technology (3%) Healthcare (3%)Other

© Deloitte LLP and affiliated entities.

How will these changes impact leasing?Leasing strategy

• Own vs lease strategy

− The cash flows and economics remain the same

− Impact to key metrics, covenants, cost of borrowing, etc will require consideration

− Credit ratings would not be expected to be impacted as analysts were already adjusting for operating leases

• Changes to lease structure and terms

− Lease terms will this mean shorter leases?

− Lease payments could we see more variable payment terms?

− May see unbundling of lease vs. service components to avoid allocation requirements

− Lessees may pay more attention to implicit interest rate vs borrowing rate (now that on balance sheet)

• Fewer overall structuring opportunities

Uncertainty on what this will mean to leasing strategies too early to tell but here are some considerations

Navigating the new world of IFRS 16 Leases 27

© Deloitte LLP and affiliated entities.

What does this mean for lessors? Leasing strategy

• Knowing your client matters

− Which ones are impacted i.e.. IFRS and US GAAP reporters with large operating lease portfolios

− Clients likely to require support (understanding impact, data, informational needs)

• The business benefits of leasing will remain, for example:

− Convenience

− Service

− Flexible terms matching payments to cash flow requirements

− Low cost financing

− Residual risk transfer avoid owning obsolete equipment

Navigating the new world of IFRS 16 Leases 28

© Deloitte LLP and affiliated entities.

Questions

Navigating the new world of IFRS 16 Leases 29

Deloitte, one of Canada's leading professional services firms, provides audit, tax, consulting, and financial advisory services. Deloitte LLP, an Ontario limited liability partnership, is the Canadian member firm of Deloitte Touche Tohmatsu Limited.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

The information contained herein is not intended to substitute for competent professional advice.

© Deloitte LLP and affiliated entities.