Alternative Tax Apportionment Issues Confronting Multistate Companies

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no

longer permitted.

Navigating Multistate Tax Issues

With Pass-Through EntitiesReconciling State Recognition Rules and Overcoming Complexities

With the Taxation of S Corps and Partnerships

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, JUNE 14, 2018

Presenting a live 90-minute webinar with interactive Q&A

Christopher Beaudro, Attorney, Eversheds Sutherland (US), Atlanta

Justin T. Brown, Attorney, Eversheds Sutherland (US), Atlanta

Charles C. Capouet, Attorney, Eversheds Sutherland (US), Washington, D.C.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-328-9525 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the

problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone

listening is no longer permitted.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you

will receive immediately following the program.

For CPE credits, attendees must participate until the end of the Q&A session and

respond to five prompts during the program plus a single verification code. In addition,

you must confirm your participation by completing and submitting an Attendance

Affirmation/Evaluation after the webinar.

For additional information about continuing education, call us at 1-800-926-7926 ext. 2.

FOR LIVE EVENT ONLY

© 2017 Eversheds Sutherland (US) LLP

Navigating Multi-State Tax Issues with Pass-through Entities

June 14, 2018

Justin Brown

Associate

Charles Capouet

Associate

Chris Beaudro

Associate

Eversheds Sutherland

Introduction and overview

Outline

─ State conformity to federal treatment of pass-through entities (“PTEs”)

─ Jurisdiction to tax PTEs and their owners (Nexus)

─ Mechanisms for reaching income of nonresident owners of PTEs

─ Apportionment of PTE income

5

Eversheds Sutherland

State Conformity to Federal Treatment of PTEs

Eversheds Sutherland

State Conformity to Federal Treatment of PTEs

─ Check-the-box (CTB) regulations overview

─ CTB application to state income taxes

─ CTB application to other state taxes

─ State conformity, partial conformity and non-conformity

─ S corp. elections

─ PTE Level Taxes

─ New Partnership Audit Rules

7

Eversheds Sutherland

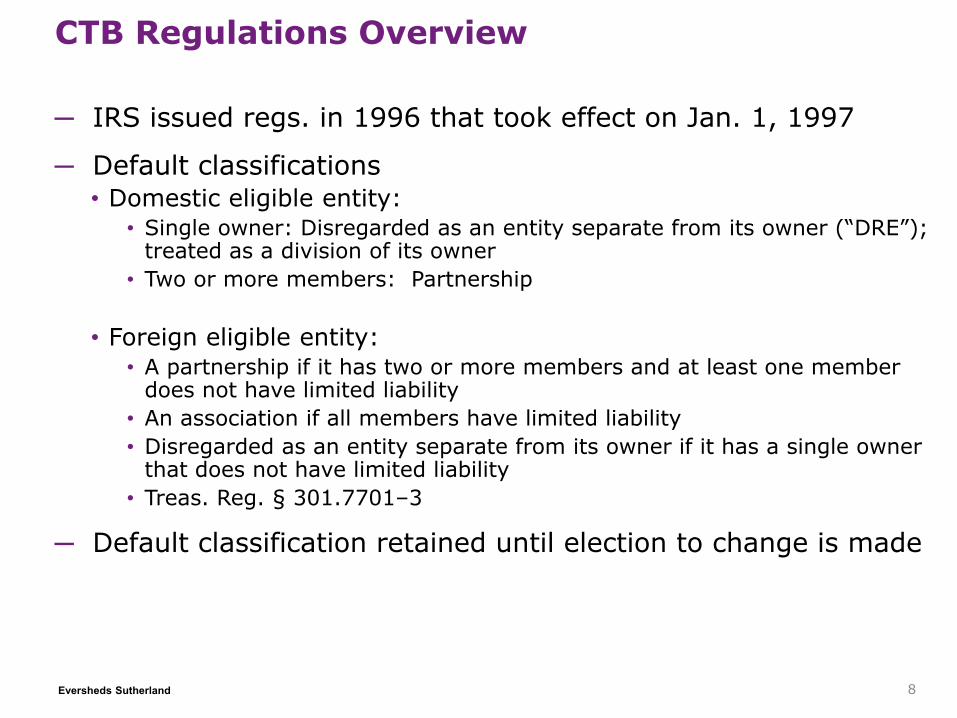

CTB Regulations Overview

─ IRS issued regs. in 1996 that took effect on Jan. 1, 1997

─ Default classifications• Domestic eligible entity:

• Single owner: Disregarded as an entity separate from its owner (“DRE”); treated as a division of its owner

• Two or more members: Partnership

• Foreign eligible entity:• A partnership if it has two or more members and at least one member

does not have limited liability

• An association if all members have limited liability

• Disregarded as an entity separate from its owner if it has a single owner that does not have limited liability

• Treas. Reg. § 301.7701–3

─ Default classification retained until election to change is made

8

Eversheds Sutherland

CTB Regulations Overview

─ CTB election necessary when an eligible entity chooses to be classified as something other than its default classification (or wants to change its classification)

─ CTB election options:• Single owner: Corporation or DRE

• Two or more members: Corporation or partnership

─ File Federal Form 8832, Entity Classification Election

9

CTB Application to State Income Taxes

─ State adoption of CTB regulations• Intended to simplify tax compliance and administration

• 25 or so states conformed in 1997; almost all comply now… but there are exceptions (discussed later)

─ State conformity is not as straight forward as it seems

─ States have conformed in a variety of ways:• Conformity statutes

• Bulletins

• Regulations

• Form instructions

─ States have varied in addressing the application of the CTB classification for all entities (some only address for certain entities, i.e., LLCs)

10

CTB Application to Other State Taxes

─ CTB regulations formulated for federal income tax purposes

─ Some states apply CTB to non-income taxes• E.g. Tennessee Franchise Tax. Notice No. 13-16 (Tenn. Dep’t of

Revenue Nov. 2013).

─ Varying treatment of CTB for sales and use tax purposes.• Alabama Revenue Ruling 98-005, 06/18/1998.

11

State Conformity, Partial Conformity and Non-Conformity

─ Conformity• Alaska. Instructions for Forms 6000, 2017 Alaska Corporation

Net Income Tax Return

• Arkansas. Ark. Code §§ 4-32-1313, 26-51-802(a)

─ Partial conformity and non-conformity• Pennsylvania. Franchise Tax: 72 Pa. Stat. Ann. § 7601(a)

• Rhode Island. R.I. Gen. Laws §§ 7-16-73(b), 44-11-2.2(a)(1); see Bulletin, “Q & A on Rhode Island Income Tax Changes Affecting Pass-through Entities Including: Partnerships and Limited Liability Companies (LLCs) with Nonresident Partners or Members; Trusts with Nonresident Beneficiaries; and S Corporations with Nonresident Shareholders,” (R.I. Div. of Taxation Dec. 28, 2004)

• Tennessee. Notice No. 13-16 (Tenn. Dep’t of Revenue Nov. 2013)

12

S Corporation Elections

─ State approaches vary

• Most states recognize federal S corp. election

• Some states have additional requirements

• Some states require a separate S corp. election

• Some states allow a federal S corp. to opt out for state purposes

• Some states do not follow federal S. corp. scheme

─ State consequences vary

13

PTE Level Taxes

─ California:• LLC fee imposed on each LLC that is doing business in the state.

This fee is based on the “total income” reportable to the state. The fee is capped at $11,790.

• Cal. Rev. & Tax. Cd. §17942(a).

─ New York City• Unincorporated business tax is imposed on the “business taxable

income” earned by each “unincorporated business” that is doing business in the state at a rate of 4%.

• NYC Administrative Code § 11-503.

─ Texas• Texas franchise tax is imposed on most PTEs.

• Texas allows DREs to be treated as disregarded separate from its corporate owner.

• Tex. Admin. Code 34 §3.581(c); Texas Form 05-908.

14

New Partnership Audit Rules

─ IRS may assess and collect from partnerships at the entity level for 1065 and Schedule K-1 issues • Collection from partnership (not partners) in “year of

adjustment” rather than “year of review”

─ Option to elect out for partnerships with 100 or fewer partners • Partners cannot be other partnerships, LLCs (including SMLLCs),

trusts or tax-exempt organizations

• Audit, assessment and collection at partner level – “Back to the Future” – Pre-TEFRA

• Election is the partnership’s (not the partners individually)

• Who’s going to decide?

15

New Partnership Audit Rules

─ After assessment, partnerships (that can’t elect out) can:

• Modify the proposed entity level assessment by presenting information specific to partners’ taxes — including amended returns

• “Push out” the entity level tax liability by providing Schedule K type reports to partners for their share of the tax imposed at the partnership level – current year

• Cost: 2% higher interest rate

16

New Partnership Audit Rules – State Issues

─ Will state law conform to the new federal changes?• Not automatically

─ New federal rules are primarily in IRC §§ 6221 to 6241 (administrative procedures)

─ States use the IRC only to compute taxable income and do not incorporate IRC administrative procedures• States usually have their own procedures

─ Practitioners need guidance for dealing with partnership and operating agreements

17

New Partnership Audit Rules – State Issues

─ Without automatic adoption, where does that leave states?

─ For partnerships assessed by the IRS at the entity level, how will states impose related state tax?

─ How are states to deal with the liability being assessed in “year of adjustment” rather than “year of review”?

─ Most states never conformed to TEFRA

18

Eversheds Sutherland

Jurisdiction to Tax PTEs and Their Owners (Nexus)

Jurisdiction to Tax PTEs and Their Owners

─ Jurisdiction (nexus) overview

─ Constitutional limitations

─ Nexus of nonresident partners

20

Jurisdiction (Nexus) Overview

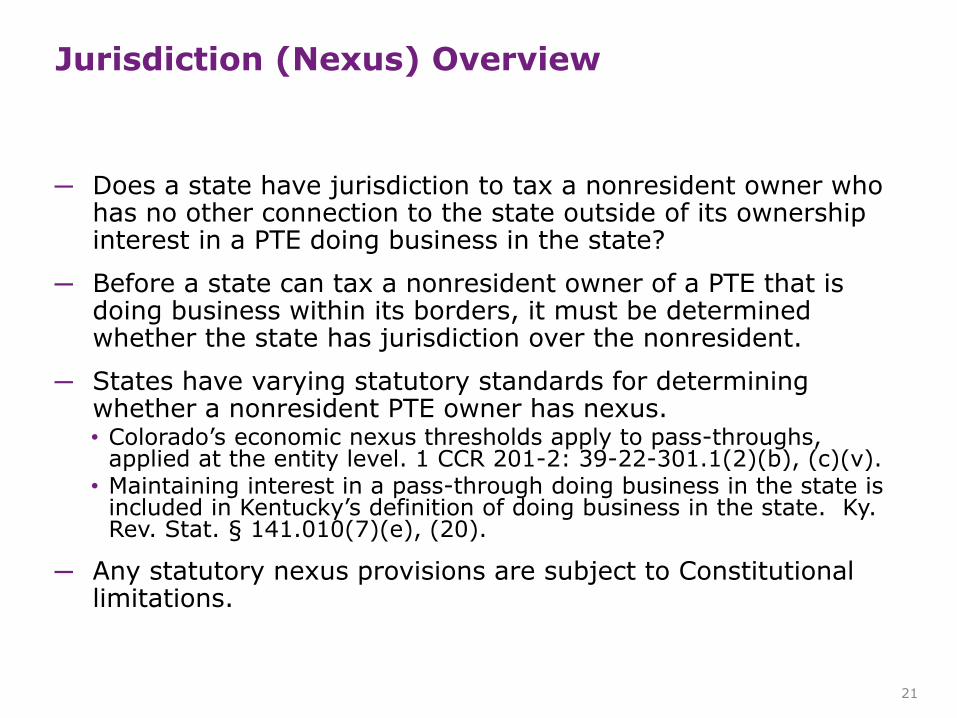

─ Does a state have jurisdiction to tax a nonresident owner who has no other connection to the state outside of its ownership interest in a PTE doing business in the state?

─ Before a state can tax a nonresident owner of a PTE that is doing business within its borders, it must be determined whether the state has jurisdiction over the nonresident.

─ States have varying statutory standards for determining whether a nonresident PTE owner has nexus.• Colorado’s economic nexus thresholds apply to pass-throughs,

applied at the entity level. 1 CCR 201-2: 39-22-301.1(2)(b), (c)(v).• Maintaining interest in a pass-through doing business in the state is

included in Kentucky’s definition of doing business in the state. Ky. Rev. Stat. § 141.010(7)(e), (20).

─ Any statutory nexus provisions are subject to Constitutional limitations.

21

Constitutional Limitations

─ States are limited in their ability to tax or impose a tax collection obligation on an out-of-state person or entity.

─ The Due Process Clause of the US Constitution requires minimum contacts with the taxing state.

─ The Commerce Clause of the US Constitution requires substantial nexus with the taxing state.• In contrast to ownership of a pass-through, it is rare for a state

to assert that a shareholder of a corporation is doing business in a state based on the activities of the corporation.

22

Nexus of Nonresident Partners

─ States generally assert that a partner in a partnership having property or personnel in the state has nexus based on its ownership interest in the partnership.

─ Must determine whether the nonresident partner has sufficient contacts with a state• Is the partner’s activity sufficient to be considered to be doing

business in the state?

• Does the nonresident partner have sufficient contacts with the state to satisfy U.S. Constitutional nexus standards?

• Is the analysis different for general versus limited liability partners?

23

Nexus of Nonresident Partners

─ An analysis of nonresident partner nexus requires consideration of the aggregate and entity theories of partnerships.

─ Aggregate theory:• Activities of the partnership are attributed to the individual

partners.• The partners are considered to be conducting the business of the

partnership.• This theory is based on common law treatment of partnerships.

─ Entity theory:• Partnerships are treated as an entity, distinct from the partners.• Partnership interests are treated like an ownership interest in a

corporation.• This theory is adopted by the Revised Uniform Partnership Act

(RUPA).

24

Nexus of Nonresident Partners

─ Recent Developments• Taxpayer victories:

• Corrigan v. Testa (Ohio May 4, 2016).• UTELCOM, Inc. and UCOM, Inc. v. Bridges (La. 2012) (cert. denied).• BIS LP, Inc. v. Director, Div. of Taxation (N.J. Super. Ct. App. Div.

2011).• Lanzi v. Ala. Dep’t of Revenue (Ala. Civ. App. 2006) (rejected by

Prince v. State Dept. of Revenue (Ala. Civ. App. 2010)).• DiBelardino v. Dep’t of Taxation (Va. Cir. Ct. 2007)

• This was a consolidated case involving two taxpayers. LLC member with no other connection to Virginia was held not to have sufficient nexus to be subject to Virginia tax but LLC member who also owned real estate in Virginia did have sufficient contact with the state.

• Taxpayer losses:• Sahi USA, Inc. v. Comm’r of Revenue (Mass. App. Tax Bd. 2006).• In re: Shell Gas Gathering Corp. #2 (N.Y. Tax App. Trib. 2010).• Prince v. State Dept. of Revenue (Ala. Civ. App. 2010).• Village Super Market of PA, Inc. v. Director, Div. of Taxation (N.J. Tax

Ct. 2013).• Preserve II, Inc. v. Director, Div. of Taxation (N.J. Tax 2017).

25

Eversheds Sutherland

Mechanisms for Reaching Income of Nonresident Owners of PTEs

State Entity-Level Taxes

─ Most states (like federal) do not tax disregarded entities, partnerships, LLCs, or S corporations• No annual net income

• No net worth

• No gross receipts taxes

─ However, there are exceptions…

28

State Entity-Level Taxes

─ Alabama• Net worth-based Business Privilege Tax (BPT) on:

• All corporations

• Limited liability entities (LLEs) (e.g., LLCs, LPs)

• Minimum tax of $100 up to maximum tax of $15,000 (except for financial institutions and insurance companies ($3,000,000))

• Applies even if the entity is disregarded for income tax

• But if a member of the SMLLC is also subject to the BPT, then the member counts the SMLLC’s net worth in computing its own tax, and the SMLLC takes a net worth of $0.00 (but still has to pay the minimum $100 BPT)

29

State Entity-Level Taxes

─ California• LLC “tax” and LLC “fee”

• Annual LLC “tax” is $800 (CA standard minimum tax)

• Annual LLC “fee” is based on “total income” apportioned to California

• Fee was originally unapportioned but was found unconstitutional in Northwest Energetic Services, LLC (2006)

• Due if California annual income is equal to or greater than $250,000

• Fee ranges from $900 to $11,790 (if CA total income is equal to or greater than $5MM)

• Applies to SMLLCs (not to LLCs electing to be taxed as corporations)

• Excludes allocations from another LLC already subject to the fee

• If the FTB determines multiple LLCs were formed to reduce fees, the total income could include the aggregate total income of all commonly controlled LLC members.

30

State Entity-Level Taxes

─ District of Columbia• Unincorporated Business Tax (UBT)

• 8.25% rate (same as corporate income tax)

• Minimum tax: $250; $1,000 if District gross receipts are greater than $1,000,000

• Base essentially the same as if the unincorporated business were a C corporation

• Exemptions:

• Entities with $12,000 or less in gross income exempt

• Certain service-based partnerships are exempt

• Qualified High Technology Companies

• Ballpark Fee• Funds the Nationals baseball stadium

• Entities with $5MM or greater in gross receipts

• Fee is between $5,500 to $16,500 per year

31

State Entity-Level Taxes

─ Illinois• Personal Property Tax Replacement Income Tax

• Funding used to eliminate the Illinois business personal property tax

• Applies to partnerships and multi-members LLCs

• Rate is 1.5% (C corporations pay 2.5%)

• Corporations receive credit for amount of tax paid by LLC of which they are members

• Deduction allowed for distributive shares of income of partners that are themselves subject to the tax

32

State Entity-Level Taxes

─ New York City• Unincorporated Business Tax (UBT)

• 4% of taxable income apportioned to NYC

• Corporate SMLLCs exempt (subject to corporate tax) but SMLLCs owned by individuals are not

• Residents receive credit for UBT paid by unincorporated business

• Special deductions and exemptions

• Real estate entities not subject to tax

• Dealing for one’s own account not taxable

• S corporations are subject to NYC’s corporation income tax

33

State Entity-Level Taxes

─ New York State• Annual filing fee

• Ranging from $25 to $4,500 (more than $25,000,000 New York source gross income) for LLPs and LLCs

• Ranging from $0 to $4,500 for regular partnerships

• Applies to LLPs and LLCs, including LLCs that are disregarded entities for federal income tax purposes

• Does not apply to LLPs or LLCs electing to be treated as a corporation for federal income tax purposes

34

State Entity-Level Taxes

─ Ohio• Commercial Activity Tax (CAT)

• Applies to all businesses regardless of form (e.g., corporations, partnerships, LLCs, S corporations – all subject to CAT)

• Rate is 0.26% of Ohio-sourced gross receipts

• Minimum tax is $150 (for receipts between $150,001 and $1MM)

• Combined v. Consolidated reporting

• Advantages of consolidated reporting – elimination of intercompany gross receipts

35

State Entity-Level Taxes

─ Texas• Margin Tax

• Applies to “limited liability entities,” including LLCs, LPs, and trusts

• General partnerships owned solely by individuals are exempt

• Exemption for “passive entities”

• Rate – 0.75% of taxable margin for most businesses

• 0.375% for retailers and wholesalers

• Margin Tax base is apportioned with a single receipts factor

36

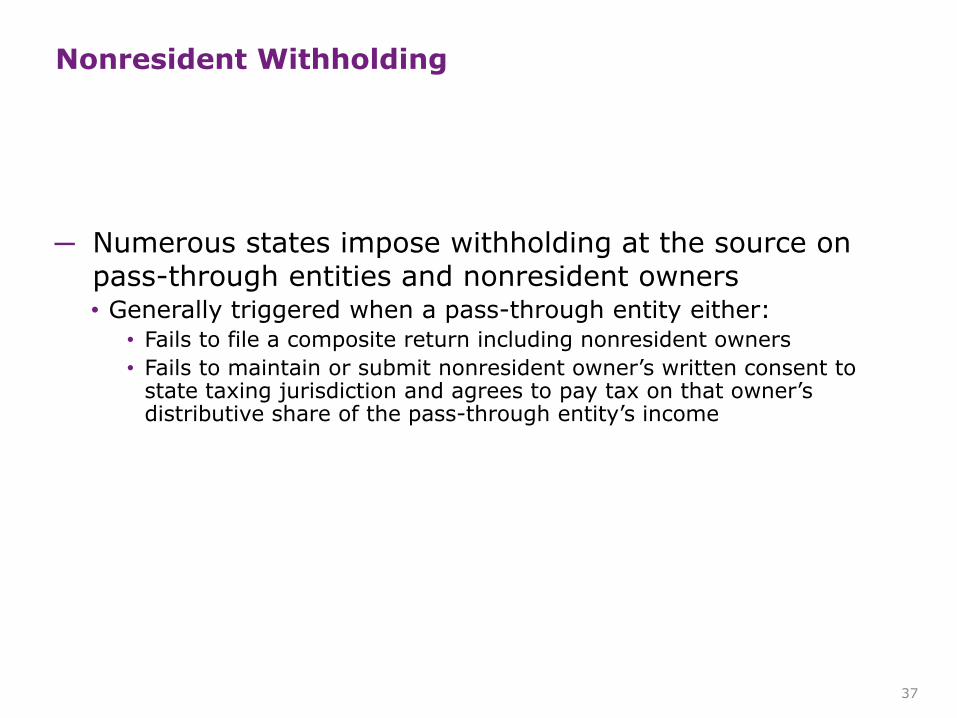

Nonresident Withholding

─ Numerous states impose withholding at the source on pass-through entities and nonresident owners• Generally triggered when a pass-through entity either:

• Fails to file a composite return including nonresident owners

• Fails to maintain or submit nonresident owner’s written consent to state taxing jurisdiction and agrees to pay tax on that owner’s distributive share of the pass-through entity’s income

37

Nonresident Withholding

─ If a state requires withholding, the pass-through entity generally pays tax at the highest individual or corporate tax rate multiplied by that owner’s distributive share of income attributable to the state• Some states require withholding only in connection with the

state’s allocable share of a distribution to a nonresident owner

• Some states except corporate partners from withholding • E.g., Idaho, Nebraska, Missouri

38

Nonresident Withholding

─ Four types of state nonresident withholding provisions:

39

•California, Colorado, Georgia, Idaho, Illinois, Indiana, Kentucky, Louisiana, Massachusetts, Missouri, Montana, South Carolina, West Virginia, Wisconsin

Composite return/Nonresident consent to taxation

•Alabama, California, Connecticut, Pennsylvania, Utah, Virginia

Nonresident withholding required

•Kentucky, New Jersey, New York, Oregon, Vermont, Wisconsin

Estimated tax payments required

• New Mexico, UtahPTE remains

contingently liable

Nonresident Withholding

─ California (it’s complicated!)• Withholding on distributions to foreign (non-US) persons

• Non-corporate partners – 12.3%; Corporate partners – 8.84%; Foreign bank and financial institution partners – 10.84%

• Highest marginal rate withholding required on distributions by LLCs to nonconsenting, nonresident members• Form 3832, Limited Liability Company Nonresident Members’

Consent – Must withhold regardless

• 7% withholding required on distributions of California-source income greater than $1,500 to domestic (nonforeign) partners• CA FTB Publication 1017 Resident and Nonresident Withholding

Guidelines (150 FAQs!!)

• Exception for payees meeting an exemption on FTB Form 590or the partner receives authorization from the FTB waiving or reducing withholding (Forms 588 and 589)

40

Nonresident Withholding

─ California – Foreign Partners/Members• Follows Treas. Reg. § 1.1446-6

• Foreign partners can request reduced or no withholding for distributions of effectively connected taxable income to foreign partners or members

• Foreign partner or member must sign and send IRS Form 8804-C to the partnership or LLC and then also sign and send Form 589, Nonresident Reduced Withholding Request, to the FTB with a signed copy of IRS Form 8804-C• The FTB will review the request within 21 days

• If approved, the partnership or LLC should submit Form 592-A, Payment Voucher for Foreign Partner or Member Withholding, with the reduced withholding amount to the FTB

41

Nonresident Withholding

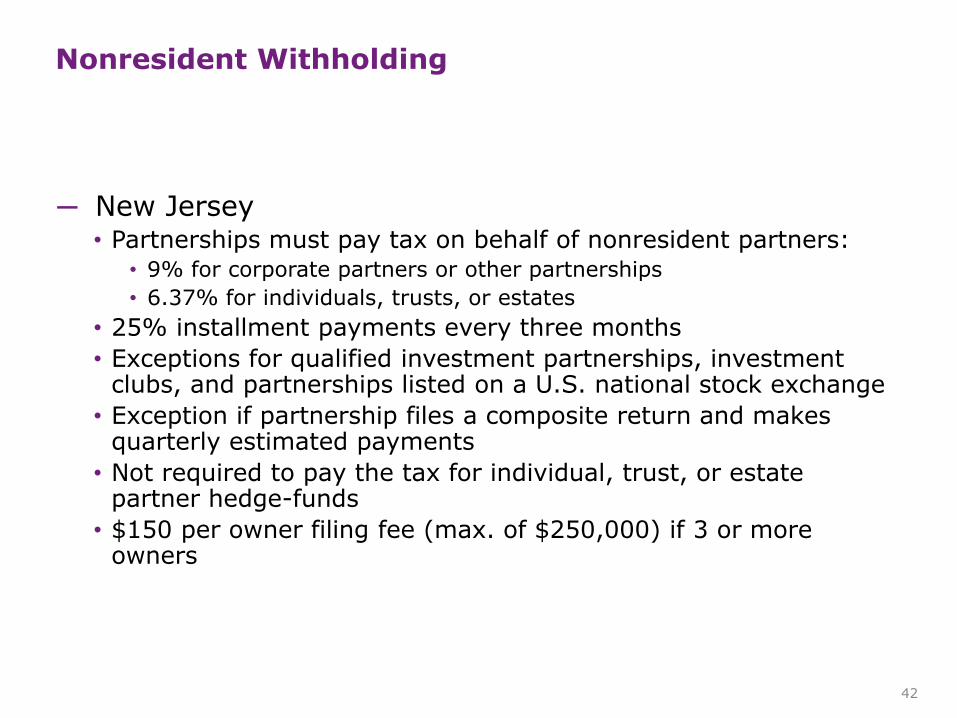

─ New Jersey• Partnerships must pay tax on behalf of nonresident partners:

• 9% for corporate partners or other partnerships

• 6.37% for individuals, trusts, or estates

• 25% installment payments every three months

• Exceptions for qualified investment partnerships, investment clubs, and partnerships listed on a U.S. national stock exchange

• Exception if partnership files a composite return and makes quarterly estimated payments

• Not required to pay the tax for individual, trust, or estate partner hedge-funds

• $150 per owner filing fee (max. of $250,000) if 3 or more owners

42

Nonresident Withholding

─ Illinois• Does not permit composite returns for nonresident owners

• Requires partnerships, S corporations, and trusts to withhold tax on both business and nonbusiness income and certain credits distributable to their respective nonresident partners, shareholders, and beneficiaries

• Entities are not required to pay the tax on behalf of owners that elect to make their own tax payments• Not applicable to individuals

• Must file the Form IL-1000-E

• The owner pledges to file all Illinois income tax returns, make timely payments of Illinois income taxes due, and be subject to Illinois personal jurisdiction for the collection of income tax due

43

Nonresident Withholding

─ New York• N.Y. Tax Law § 658(c)(4)

• Pass-through entities are required to make quarterly estimated tax payment on behalf of nonresident members or partners

• However, estimated payments are not required if:

• Any owner whose estimated tax required to be paid for the tax year by the entity is $300 or less;

• Any nonresident individual owner elects to be included in the group (composite) return that the entity has been authorized to file; or

• Any owner that provides the entity with an exemption certificate certifying that the owner will comply in their individual or corporate capacity with the New York State estimated tax and tax return filing requirements

44

Nonresident Withholding

─ California• CA FTB Public Service Bulletin 10-16 (May 20, 2010)

• If withholding was required but pass-through entity failed to withhold, the withholding agent is liable for 100% of the amount required to be withheld, plus interest

─ Utah• Utah Info. Pub. 68 (Sept. 1, 2014)

• Pass-through entities can request waivers of the Utah withholding requirement

• However, if a waived downstream entity or taxpayer fails to file a return and make required payments, the pass-through entity will not be eligible for the waiver and is liable for Utah withholding on the unpaid amounts, plus penalties and interest

45

Nonresident Withholding

─ States may not require withholding for investment partnerships or publicly traded partnerships:• California – Income arising through an investment partnership is

not “California source income.” Cal. Rev. & Tax Cd. § 23040.1.

• Doesn’t apply to corporations participating in management of the investment partnership’s investment activities

• New York – Excludes publicly traded partnerships, as defined in I.R.C. § 7704, from paying estimated tax on behalf of partners. N.Y. Tax Law § 658(c)(4)(A).

• Means any partnership if: (1) interests in the partnership are traded on an established securities market; or (2) interests in the partnership are readily tradable on a secondary market (or the substantial equivalent thereof).

46

Eversheds Sutherland

Apportionment of Pass-Through Entity Income

Apportionment Of Pass-Through Entity Income

48

PTE

Corp. Partner

Indiv.

Is the PTE unitary with the corp.

partner?

Is the individual a resident?

Is the entity or individual a general partner or a limited

partner?

Do the factors flow up?

Is the income the result of the sale of

an interest in a PTE?

Eversheds Sutherland

Apportionment of Pass-Through Entity IncomeBusiness/Non-Business Income

Corporate Partners – Business/Non-Business Income

─ Corporate Partners• Is business/non-business income determination made at:

• The partnership level?

• The partner level?

• Most states have not addressed this issue• Arizona guidance provides that determination of business income be

done at the partner level.

• Ariz. Corp. Tax Rul. No. 94-2 (Apr. 4, 1994).

• Illinois has provided direct guidance on this issue – requiring the determination of business/non-business income be done at the partnership level.• Ill. Admin. Code tit. 86, §§ 100.3500(a)(3), 100.3500(b)(1)

(“Trade or business activities of a partner or of any related party are irrelevant”).

50

Eversheds Sutherland

Apportionment of Pass-Through Entity IncomeAllocation and Apportionment

Corporate Partners – Apportionment Factors

─ Partner level approach• Partners combine their share of the pass-through entity’s

apportionment factors with their own apportionment factors. • Referred to as “flow-through” or “flow-up” apportionment.

• Also known as “partner-level” apportionment.

• Example:• Assume that a corporate partner has a 40% interest in a partnership

• The corporate partner would calculate its own apportionment factor by including 40% of the partnership’s sales, property, and payroll (assuming that the state uses a three-factor apportionment formula), but usually only if the partner and the partnership are unitary.

53

Corporate Partners – Apportionment Factors

─ Partnership level approach • The pass-through entity’s income is apportioned to the state

using only the pass-through entity’s own apportionment factors.

• Owners of the pass-through entity then allocate their distributive share of post-apportionment income to the appropriate state.

• Example:• Assume a corporate partner has a 40% interest in a partnership,

which earns $100 of income.

• If apportionment is calculated at the partnership level, and the partnership computes a 50% apportionment factor in a state, then the partner would include $20 of partnership income in its tax base in that state.

• $100 × 40% = $40, and $40 × 50% = $20

54

Corporate Partners – Apportionment Factors

─ California (Cal. Code Regs. tit. 18, §25137-1)• If partners are unitary with partnership, then partnership’s

factors “flow through” to the partners.

• If partners are not unitary with the partnership, then the factors do not “flow through” to the partners.

• If partners and partnership are not unitary, but the income is considered business income, then partners must apportion partnership income separately from their other business income.

─ Illinois (86 Ill. Admin. Code §100.3380(d) and 100.3500)• Follows California approach to corporate partner apportionment.

55

Corporate Partners – Apportionment Factors

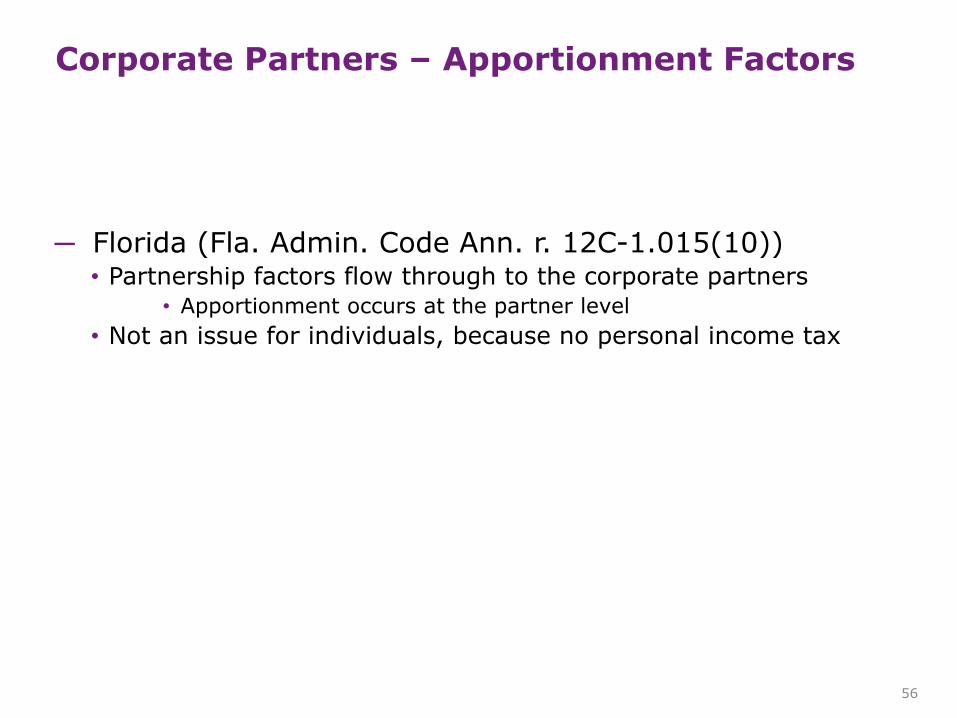

─ Florida (Fla. Admin. Code Ann. r. 12C-1.015(10))• Partnership factors flow through to the corporate partners

• Apportionment occurs at the partner level

• Not an issue for individuals, because no personal income tax

56

Corporate Partners – Apportionment Factors

─ Massachusetts (Mass. Regs. Code tit. 830, § 63.38.1)• Partnership factors flow through to corporate partners, if

partnership and corporate partners are engaged in “related business activities.”

• If they are not engaged in related business activities, corporate partners separately account for partnership income and apportion it using only the partnership’s factors.• If corporation owns less than 50% of an LP, it is presumed not to be

doing business in Massachusetts, and apportionment is done at the partnership level.

57

Corporate Partners – Apportionment Factors

─ New Jersey (NJ Rev. Stat.§54:10A-15.7(a); NJ Admin. Code tit.18, §18:7-7.6(g)(3)) • Partnership factors flow through to corporate partners, if the

partnership and partners are unitary.• There are special New Jersey rules of unity for corporate partners and

partnerships.

• Factors include:

• Amount of inter-company transactions

• Whether there is a substantial interest in the partnership relative to the corporate shareholder’s assets

• Relative income produced by interest to corporate shareholder’s total income

• Whether the entities are in the same line of business

• Substantial overlap of employees and offices

• Sharing of operational facilities, technology, or know-how

• If not unitary, apportion partnership income at the partnership level and report distributive share of apportioned taxable income without regard to the partners’ separate apportionment factors.

58

Corporate Partners – Apportionment Factors

─ Oklahoma (Okla. Stat. tit. 68, § 2358(A)(4)(b)(2); Okla. Admin. Code §710:50-17-51(15)(A))• Partnership factors do not flow through to the corporate partners.

• Instead, income is apportioned at the partnership level and separately allocated to the state by the corporate partners.

• Similar treatment in Arkansas, Louisiana, and Mississippi.

59

Individual Partners

─ Resident individuals generally are subject to tax on their entire distributive share of partnership income in their state of residence.

─ Nonresident individuals generally are subject to tax only on their share of partnership income earned within the state.

60

Eversheds Sutherland

Apportionment of Pass-Through Entity IncomeSale of an Interest

Sale of an Interest

─ What is the character of the interest being sold?• Partnership

• The sale of a partnership interest is generally treated as a sale of an intangible, and the gain is apportioned based on the usual rules for sales of intangibles.

• This treatment is based on the entity theory of partnerships.

• Disregarded Entity• When a disregarded entity is being sold, it is likely that the states

treat the seller as if it held the assets of the disregarded entity directly (i.e., it is like selling a division of the corporate owner).

• States have not provided much guidance on this issue.

62

Sale of an Interest

─ Is it business income? • Transactional Test

• If not in the business of buying and selling partnership interests, there is a strong argument that the sale of the interest generates nonbusiness income and that the gain should be sourced to its commercial domicile.

• Functional Test• If the interest is an operational asset used in the business, its sale

would likely be held to generate business income.

63

Sale of an Interest

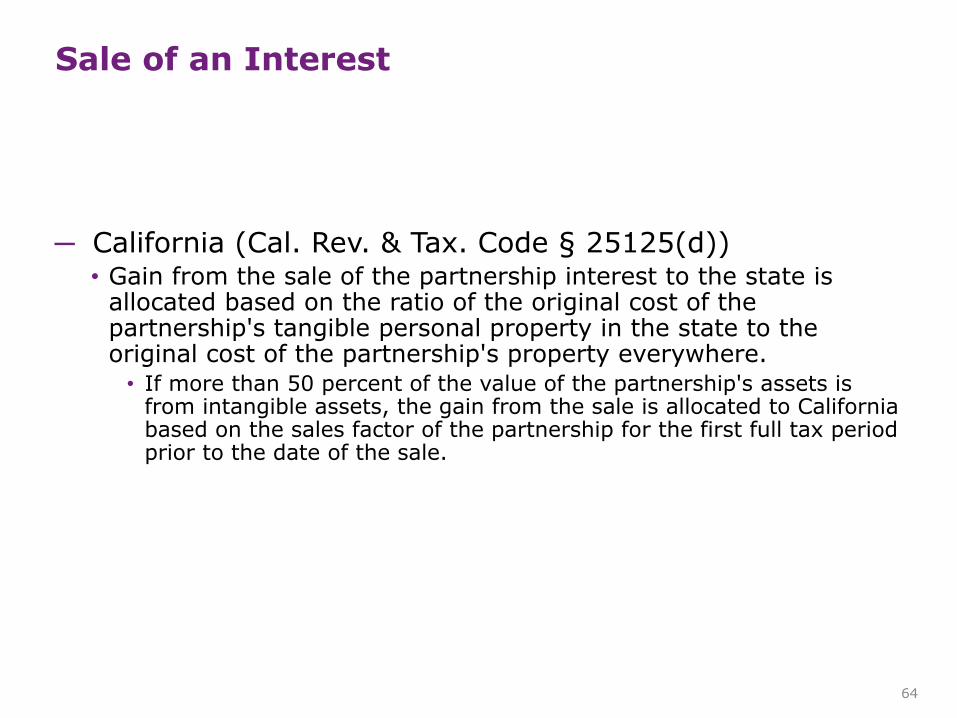

─ California (Cal. Rev. & Tax. Code § 25125(d))• Gain from the sale of the partnership interest to the state is

allocated based on the ratio of the original cost of the partnership's tangible personal property in the state to the original cost of the partnership's property everywhere. • If more than 50 percent of the value of the partnership's assets is

from intangible assets, the gain from the sale is allocated to California based on the sales factor of the partnership for the first full tax period prior to the date of the sale.

64

Sale of an Interest

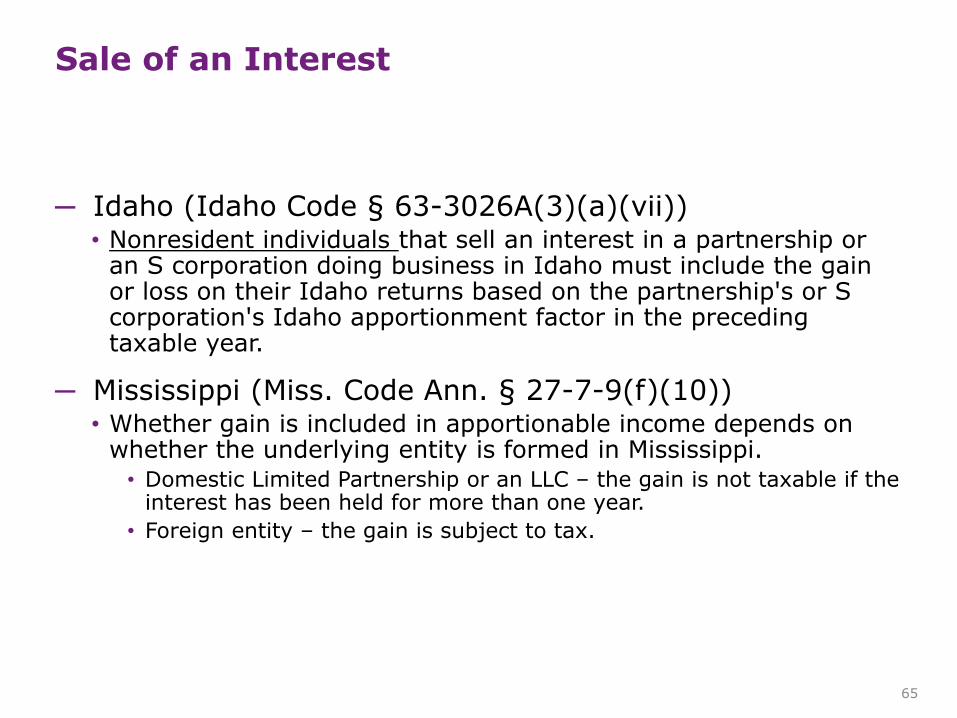

─ Idaho (Idaho Code § 63-3026A(3)(a)(vii))• Nonresident individuals that sell an interest in a partnership or

an S corporation doing business in Idaho must include the gain or loss on their Idaho returns based on the partnership's or S corporation's Idaho apportionment factor in the preceding taxable year.

─ Mississippi (Miss. Code Ann. § 27-7-9(f)(10))• Whether gain is included in apportionable income depends on

whether the underlying entity is formed in Mississippi.• Domestic Limited Partnership or an LLC – the gain is not taxable if the

interest has been held for more than one year.

• Foreign entity – the gain is subject to tax.

65

Sale of an Interest

─ New York (N.Y. Tax Law § 631(b))• Statute defines “income derived from New York sources” to

include gain from the sale of an interest in a partnership, LLC, S corporation or C corporation:• with 100 or fewer shareholders; and

• whose assets are comprised more than 50%, on a fair market basis, of New York real property.

─ Texas (34 Tex. Admin. Code § 3.591(e)(2))• Sales of intangibles are apportioned based on the “location of the

payor” rule. • Gain from the sale of a partnership interest would be included in the

numerator of the Texas receipts factor only if the buyer of the partnership interest were legally domiciled in Texas.

66

Sale of an Interest

─ Oregon (Or. Rev. Stat. 314.635(4))• Gain or Loss from is allocable to the state in the ratio of the

original cost of partnership tangible property in the state to the original cost of the property everywhere.

• If greater than 50% of the partnership’s property is intangibles, gain or loss from the sale of the interest is allocated to the state based on the sales factor for the preceding tax year.

67

Eversheds Sutherland

Thank You

68

Eversheds Sutherland

Be sure to also submit your pet

through our app to be featured as

Pet of the Month!

Download the Eversheds Sutherland SALT Shaker app today

Connect with us!

─ Apple App Store

─ Google Play

─ Amazon Appstore

69

@ESsaltlaw

eversheds-sutherland.com© 2017 Eversheds Sutherland (US) LLP

All rights reserved.

Contact Us

Chris F. Beaudro

AssociateEversheds Sutherland (US) [email protected]

stateandlocaltax.com

Charles C. Capouet

AssociateEversheds Sutherland (US) [email protected]

Justin T. Brown

AssociateEversheds Sutherland (US) [email protected]