Naturals in Indonesia IFEAT Conference Shanghai Oct2009

15

“Naturals in Indonesia ” Sandeep Tekriwal Van Aroma Jl.Raya Bypass, KM 20, Padang, Indonesia [email protected] A very good morning to all the IFEAT Members & Delegates present today. My name is Sandeep Tekriwal and I am from PT. Van Aroma, Padang, Indonesia. I would like to take this opportunity to share some information on the World of Naturals in Indonesia. This lecture will highlight some of the major developments and concerns of the essential oils industry during the past two or three years especially in regard to violent price fluctuations in patchouli. As is known within the industry worldwide, Indonesia is a major supplier of patchouli, nutmeg, vetivert, cananga, citronella, massoi bark, sandalwood, cajuput, ginger, clove and its derivatives. Almost 85 % of the volume / turnover comes mainly from three products i.e. patchouli, nutmeg and clove. But first and foremost some basic information on Indonesia, its location and a SWOT analysis of the country relevant to the naturals industry worldwide.

-

Upload

christian-adi -

Category

Documents

-

view

55 -

download

5

Transcript of Naturals in Indonesia IFEAT Conference Shanghai Oct2009

“Naturals in Indonesia”

Sandeep Tekriwal

Van Aroma

Jl.Raya Bypass, KM 20, Padang, Indonesia

A very good morning to all the IFEAT Members & Delegates present today.

My name is Sandeep Tekriwal and I am from PT. Van Aroma, Padang, Indonesia. I would like to take this opportunity to share some information on the World of Naturals in Indonesia.

This lecture will highlight some of the major developments and concerns of the essential oils industry during the past two or three years especially in regard to violent price fluctuations in patchouli.

As is known within the industry worldwide, Indonesia is a major supplier of patchouli, nutmeg, vetivert, cananga, citronella, massoi bark, sandalwood, cajuput, ginger, clove and its derivatives.

Almost 85 % of the volume / turnover comes mainly from three products i.e. patchouli, nutmeg and clove.

But first and foremost some basic information on Indonesia, its location and a SWOT analysis of the country relevant to the naturals industry worldwide.

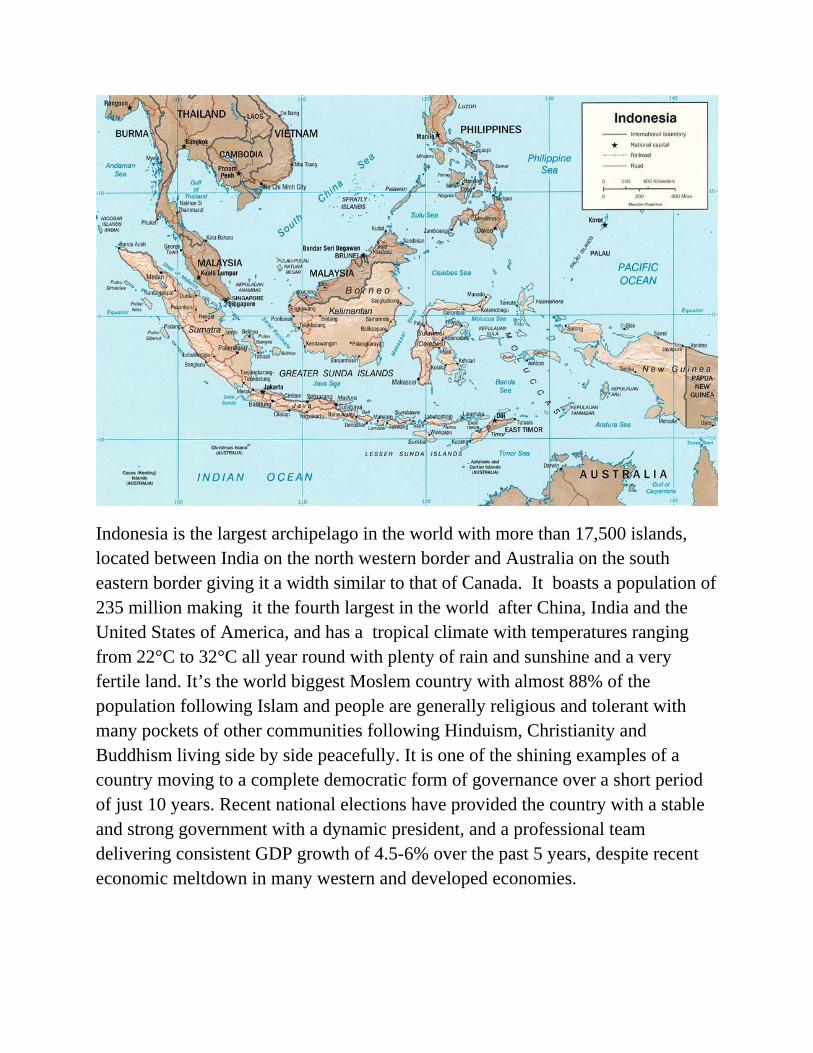

Indonesia is the largest archipelago in the world with more than 17,500 islands, located between India on the north western border and Australia on the south eastern border giving it a width similar to that of Canada. It boasts a population of 235 million making it the fourth largest in the world after China, India and the United States of America, and has a tropical climate with temperatures ranging from 22°C to 32°C all year round with plenty of rain and sunshine and a very fertile land. It’s the world biggest Moslem country with almost 88% of the population following Islam and people are generally religious and tolerant with many pockets of other communities following Hinduism, Christianity and Buddhism living side by side peacefully. It is one of the shining examples of a country moving to a complete democratic form of governance over a short period of just 10 years. Recent national elections have provided the country with a stable and strong government with a dynamic president, and a professional team delivering consistent GDP growth of 4.5-6% over the past 5 years, despite recent economic meltdown in many western and developed economies.

SWOT ANALYSIS OF INDONESIA IN NATURALS

STRENGTHS

1) Supplying 90% of the world patchouli oil requirement. Exporting 1400 MT of the 1500 MT/year world consumption. Other countries producing patchouli are India and China, but the Indonesian quality is more acceptable in the world markets.

2) Supplying 80% of the world nutmeg oil requirement. Exporting about 500 MT out of the total demand of 600 MT/Year. Other countries producing nutmeg oil are Grenada, Sri Lanka, India, but the quality and quantity are insignificant.

3) Supplying 50% of the world’s demand in crude clove oil & 75% of the world’s clove oil derivatives such as eugenol, iso eugenol, methyl eugenol etc. Indonesia exports close to 2500 MT of the world demand of 3500 MT/ Year of crude clove oil and its derivatives.

4) Having the 2nd highest biodiversity in the world after Brazil, making it suitable for the production of many other varieties of naturals.

5) Competitive labour costs for labour intensive industries makes it one of the low cost production bases for naturals such as vetivert, cananga, massoi bark, ginger, sandalwood oil etc...

WEAKNESSES

1) Unorganized field distillation industry and production of raw material with hardly any significant contribution from the organized sector.

Current Patchouli Oil Supply Chain

2) Crude field distillation technology thereby giving poor and inferior quality and yield.

3) Long supply chain between farmers and exporters adding to the overall cost of the end product.

4) Poor infrastructure facilities. 5) Lack of current international market information, demand and supply

situations for the farmer distillers. 6) Non availability of working capital from banks, forcing farmers to

borrow from the unorganized sector at very high interest rates, thereby depriving farmers of their due share of profit margins.

OPPORTUNITIES

1) Develop partnerships between farmers and exporters and educate them about modern distillation and farming techniques.

2) Develop partnerships between local and overseas buyers so as to encourage new investments, latest technical know-how and better market access.

3) Increasing trend in developed countries for shifting high cost production base to low cost economies like China, India and Indonesia.

4) Develop local Indonesia flavour & fragrance industry like China and India.

5) Increase in purchasing power of the Indonesian middle class.

6) Shift in the trend from synthetic to naturals.

THREATS

1) Global warming and changing weather patterns- El Nino/La Nina weather effects.

2) Violent price fluctuations - Viz patchouli can kill a products long-term prospect.

3) Competition from other plantation products like palm, cacao, coffee etc... This can easily grab the arable farmland if prices of these commodities move up.

The total value of exports of natural essential oils (HS-3301) from Indonesia has been estimated to be about USD 105 Million, while imports of essential oils stand at USD 380 million.

Table 1: Indonesia: Imports and Exports of Essential Oils 2003-2008 (US$)

380,670,130

381,940,000

350,758,000

320,152,000

289,574,000

193,125,000

IMPORT

104,320,120

101,140,080

67,324,969

93,320,585

70,732,539

59,766,299

EXPORT

2003

49.9418.342004

10.56 31.932005

(0.33)3.102008

8.8950.232007

9.56(27.85)2006

% CHANGE% CHANGEYEAR

380,670,130

381,940,000

350,758,000

320,152,000

289,574,000

193,125,000

IMPORT

104,320,120

101,140,080

67,324,969

93,320,585

70,732,539

59,766,299

EXPORT

2003

49.9418.342004

10.56 31.932005

(0.33)3.102008

8.8950.232007

9.56(27.85)2006

% CHANGE% CHANGEYEAR

Source: Indonesian Bureau of Statistics

Indonesia exports the basic raw naturals without much value addition while it imports the flavour and fragrance formulations and compounds after value addition from overseas. The top 5 countries/regions accounting for almost 80% of the total exports of naturals from Indonesia are:

1) United States of America 2) EU- France/Germany/Italy/Spain 3) China 4) Japan 5) India

PATCHOULI OIL

Traditionally patchouli had been cultivated predominantly in the island of Sumatra and recently Java, these together accounting for 90% of the production, mainly coming from areas such as Aceh, the Nias Islands, the Mentawai Islands, Bengkulu, and Jambi in Sumatra and Kuningan, Malang, Blitar and Garut area in Java. Over the past couple of years, there has been a significant development in patchouli oil production in Java and it would be safe to say that in the very near future Java may overtake Sumatra in total production. Other areas which have been developing fast are some pockets of Sulawesi and Kalimantan. Most of the patchouli produced in Sumatra is of the dark variety, while Java produces the light iron free patchouli, basically due to the use of stainless steel distillation vessels, while in Sumatra, the traditional small Iron drums are still in use. Sumatra quality patchouli is still much preferred due to its superior odour value.

We are all aware of the violent price fluctuations which have taken place in patchouli oil over the past three years (Diagram No: 1).

As one can see from Diagram 1, illustrating patchouli prices during the last 5 years, the prices bottomed to a level of USD 22 in Nov’2006 and then peaked to a level of USD 170 in January 2008 falling to USD 95 in April 2008. Prices fell further to USD 65 by November 2008 and came close to bottoming out at USD 32-35 in August 2009. Nobody will disagree that this is not a healthy phenomenon for the industry and we all wish to see a more stable and sustainable price, both for the producers and the consumers. Most of us are probably still not convinced about the exact reasons why such fluctuations took place, and we at the Indonesian Essential Oil Council tried to study some of the probable causes and the effect of these fluctuations. Some of them are as follows:

PROBABLE CAUSES

1) Global warming/ El Nino weather patterns in the middle of 2006 when a long dry spell affected the plantation and distillation activities and supplies dwindled drastically while demand remained consistent.

2) The speculative trading mentality of some of the players in the market including some of those in the middle who look for short term profits, thereby damaging long-term prospects for the product.

3) The very poor state of farming techniques being followed in Indonesia, thereby making it unsustainable for farmers.

4) The very steep jump in production costs for farmers because of the steep increase in energy prices, thereby increasing the overall cost of production.

5) Crop damage due to the spread of a new disease in farming areas affecting patchouli leaves.

6) The nomadic farming system in Sumatra whereby no one particular area is used permanently for cultivating patchouli.

7) The production system- perennial crop farming where the farmers plant crops which give better returns.

8) During the boom times, prices of all commodities kept moving up sharply while patchouli prices were still quiet, resulting in farmers moving to other crops, and thereby reducing production.

9) Global economic meltdown resulted in severe reduction in demand for patchouli.

EFFECT

1) When prices peaked out at levels of USD 170, the actual users

drastically slashed the % consumption of patchouli in their formulations, thereby reducing demand and the sudden drastic fall in prices.

2) New product development based on patchouli formulation does not take place due to very high uncertainty, resulting in demand not keeping pace with production.

3) Confidence of global consumers is shaken and they shift the formulations to more stable supplies.

4) Extreme shifts of production take place during severe fluctuations thereby creating unstable market conditions.

We feel that both exporters and importers of patchouli need to play a joint and responsible role so that possible this situation can be reduced in future. We had started to address this problem during the IFEAT Budapest Conference in 2007 where Mr. Gunawan mentioned about the “Cultiva” system of cluster farming and developing partnerships between international buyers and Indonesian exporters.

This concept of “Cultiva” has been implemented initially in 5 potential areas (Aceh, North Sumatra, West Sumatra, West Java, and East Java) and we are seeing a good level of success because of the support from the Indonesian government and the Indonesian Essential Oil Council (IEOC).

Cultiva Patchouli Oil Supply Chain

IEOC would like to propose some steps which have been discussed during its meetings, and we believe that this may help in bringing a sense of stability in the market. More than 75% of the consumption of patchouli is done by the top 10

players in this industry, and similarly more than 85% of exports by volume are concentrated in the hands of the top 10 exporters from Indonesia. Their role in this product is crucial for ensuring stability, and that can probably be achieved by taking the following steps:

1) Determine sustainable price levels at both ends. This can be achieved if both concerned parties are willing to study the production process and cost of production by making field trips in major production areas so as to understand the ground realities. Both parties must enter into a meaningful and open dialogue on pricing so that farmers, exporters and importers can have a continued and sustainable supply of patchouli. We at IEOC are of the view that a price ranging between USD 40 - USD 55 CNF shall be a long term sustainable price.

2) Develop partnerships so as to know the actual supply and demand scenario and developments taking place in the world market.

NUTMEG OIL

Unlike patchouli oil, price, demand and supply of nutmeg oil have been pretty stable, ranging between USD 40 to USD 55 per kg, but recently prices have started firming upwards towards levels of USD 65. Farming and distillation methods for nutmeg oil are far more organised and concentrated in few pockets in Aceh and west Java.

Traditionally, prices for nutmeg oil have always been higher than patchouli, but during the past couple of years, the price of nutmeg oil has been lower than patchouli, thereby discouraging farmers from distilling nutmeg oil. Prices are

expected to further firm in coming months because of an expected shortfall in crops for the following reasons:

1) Decreasing yields from nutmeg trees in producing areas of Aceh and West Java.

2) Deadly disease, attack by stem borer bug (Batocera) destroying the nutmeg trees in the main producing areas of Aceh.

3) Smaller number of new plantations for nutmeg trees coming up, thereby reducing the supply of raw material available for distillation.

4) Strengthening of the Indonesian currency.

5) Increase in demand by consumers of almost 15%.

6) Higher prices for nutmeg and mace as a spice discourage farmers from producing raw material for distillation, as only tender nutmegs are used for distillation oils.

Nutmeg stainless steel distillation unit

CLOVE OIL & ITS DERIVATIVES

Indonesia is the world’s biggest producer and consumer of clove bud and most of the production is used in the clove cigarette industry. Most of the time, demand for clove bud is more than production so Indonesia needs to import clove buds from Madagascar and Zanzibar.

Clove leaf and clove stems are mostly used for distillation of clove oil and its derivatives and the leadership of Indonesia in this is bound to continue in times to come.

Prices are quite stable and the majority of production is centralised in the Java and Sulawesi regions. Because of the strengthening price of cloves recently, prices of clove oil and derivatives have started firming up and are expected to go up further in coming months.

SOME NEW DEVELOPMENTS IN NATURALS IN INDONESIA

1) Alpinia Malaccensis Oil

This oil is grown mainly in the wild areas of Java and Maluku islands. The annual production of this oil is approximately 12-15 MT per annum and international prices are ranging from USD 35-40 per kg world ports.

It is used to produce Methyl Cinnamate crystals which are used in cosmetics and pharmaceutical industries.

Since Alpina Malaccensis is grown in the wild, it has tremendous potential for organic certification if the demand can be generated.

2) Aetoxylon Sympetalum Oil

This oil is mainly grown again in the wild in the Kalimantan islands of Indonesia and distillation takes place in Kalimantan and Java islands. Annual production of this oil is about 5-6 MT per annum and international prices range from USD 130-140 per KG world ports.

Aetoxylon Symetalum is mainly used in the fragrance industry and the main component is Alfa Eudesmol, which has a sweet woody note like that of agarwood oil.

3) Sandalwood Papua ( Santalum Macgregorii) Oil

Papua Sandalwood oil is mainly produced and distilled in west Papua.

The international price for this oil ranges between USD 300-350 and is mainly used in the fragrance industry. Production of this oil is 2-3 MT per annum but it can easily be scaled upwards if additional demand can be generated. It has good potential for growth as iis much cheaper than the other varieties of Sandalwood oils.

t

MAIN ISSUES RELATED TO ORGANIC CERTIFICATION OF NATURALS IN INDONESIA

Unlike other developing countries viz: Egypt, Sri Lanka, India, and China, exports of organic certified naturals have not been able to make significant growth in the international markets because of the following issues:

1) Total lack of education and information on the benefits of organic certification within the naturals industry in Indonesia, both to the farmer distillers and exporters.

2) Very high cost of certification, especially when the majority of plantations do not exceed few hectares/acres of land and the distillation units are small scale.

3) Very few local companies are internationally accredited to certify organic products unlike India, China and Egypt.

4) Lack of focus on the part of big exporters in educating the farmers on the benefits of organic certification.

5) Non availability of supporting organic certified material for farming, viz: fertilizers, pesticides, composts etc...

Keeping in mind all the above issues related to naturals in Indonesia, I can confidently state that the future for naturals in Indonesia is wide open with unlimited opportunities for future growth. With the support and guidance from major industry players worldwide, and active participation by local exporters, there is no reason why Indonesia cannot be one of the top five players in the world of naturals. Thank you.

Sandeep Tekriwal is the President of PT. Van Aroma, having more than 14 years of experience in exports of agro products, spices and essential oils from Indonesia. Having done his Masters in Business from Mumbai University, he has travelled extensively in the south east Asian countries especially Indonesia trying to carve a niche name for the company’s portfolio of products in international markets. He is working closely with the Indonesian Essential oil Association (DAI) to implement sustainable farming techniques in Patchouli in Indonesia.