Monetary Policy and Stock Market Booms and Busts in the 20th Century

Upload

cruz-raymondCategory

view

38download

0description

11

Natural Resources in LAC: Beyond Booms and Busts?

Americas Conference Miami Herald September 13, 2010

Chief Economist OfficeLatin America and the Caribbean RegionThe World Bank

Beyond booms and busts?

Boom-bust cycles are nothing new for LAC … from Potosi to the Lost Decade of the 1980s …

… its history has been punctuated by wasted commodity bonanzas

The “natural resource curse” is not destiny

“Natural resource blessings” can be seized through good policies

The commodity bonanza is less likely to end badly for LAC this time around

2

First, six stylized facts…

3

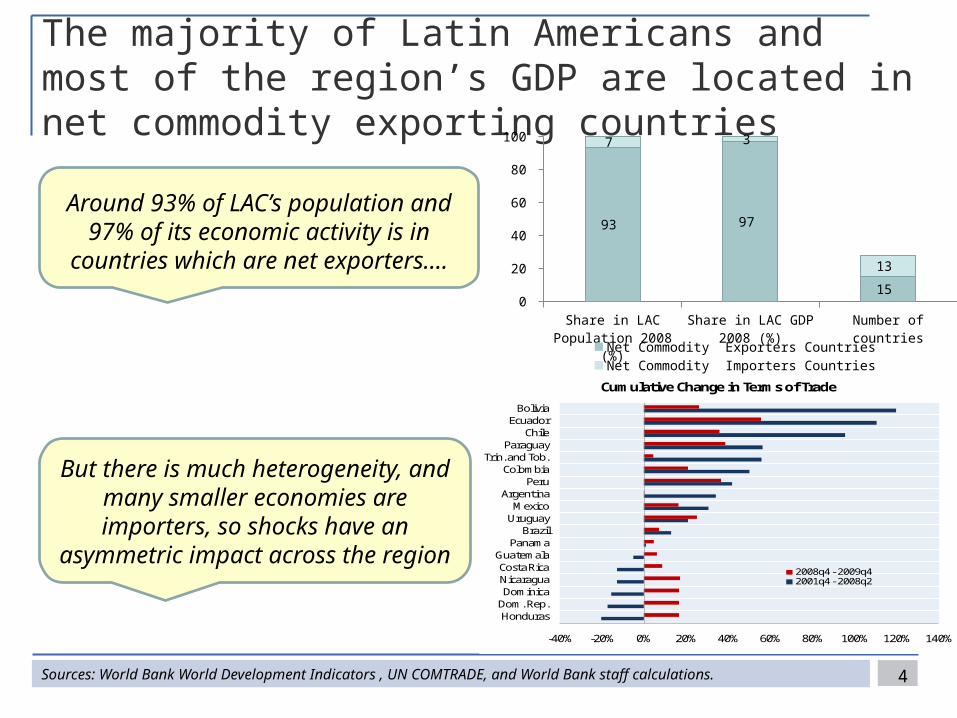

The majority of Latin Americans and most of the region’s GDP are located in net commodity exporting countries

4

Share in LAC Popula-tion 2008 (%)

Share in LAC GDP 2008 (%)

Number of countries0

10 20 30 40 50 60 70 80 90

100

93 97

15

7 3

13

Net Commodity Exporters Countries Net Commodity Importers Countries

-40% -20% 0% 20% 40% 60% 80% 100% 120% 140%

HondurasDom. Rep.Dominica

NicaraguaCosta Rica

GuatemalaPanama

BrazilUruguay

MexicoArgentina

PeruColombia

Trin. and Tob.Paraguay

ChileEcuador

Bolivia

Cumulative Change in Terms of Trade

2008q4 - 2009q42001q4 - 2008q2

Around 93% of LAC’s population and 97% of its economic activity is in

countries which are net exporters….

But there is much heterogeneity, and many smaller economies are importers, so shocks have an asymmetric impact

across the region

Sources: World Bank World Development Indicators , UN COMTRADE, and World Bank staff calculations.

5

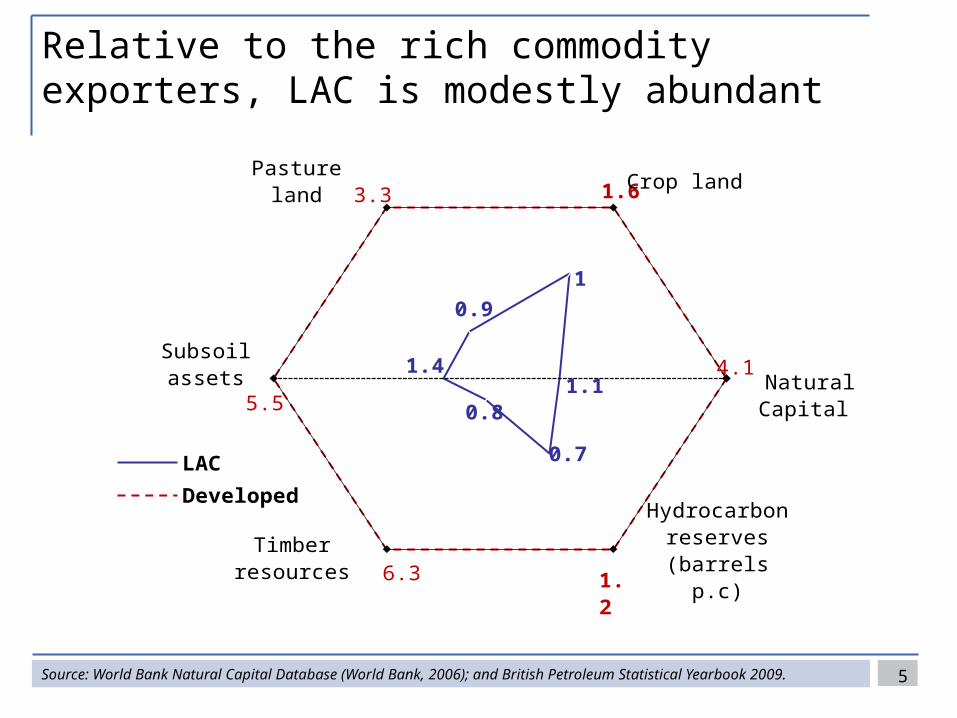

Relative to the rich commodity exporters, LAC is modestly abundant

Source: World Bank Natural Capital Database (World Bank, 2006); and British Petroleum Statistical Yearbook 2009.

4.1

1.63.3

6.3

5.5 0.81.1

0.7

1.4

1

0.9

Crop landPasture land

Subsoil assets

Timber resources

Hydrocarbon reserves (barrels

p.c)

Natural Capital

LAC

Developed

1.2

6

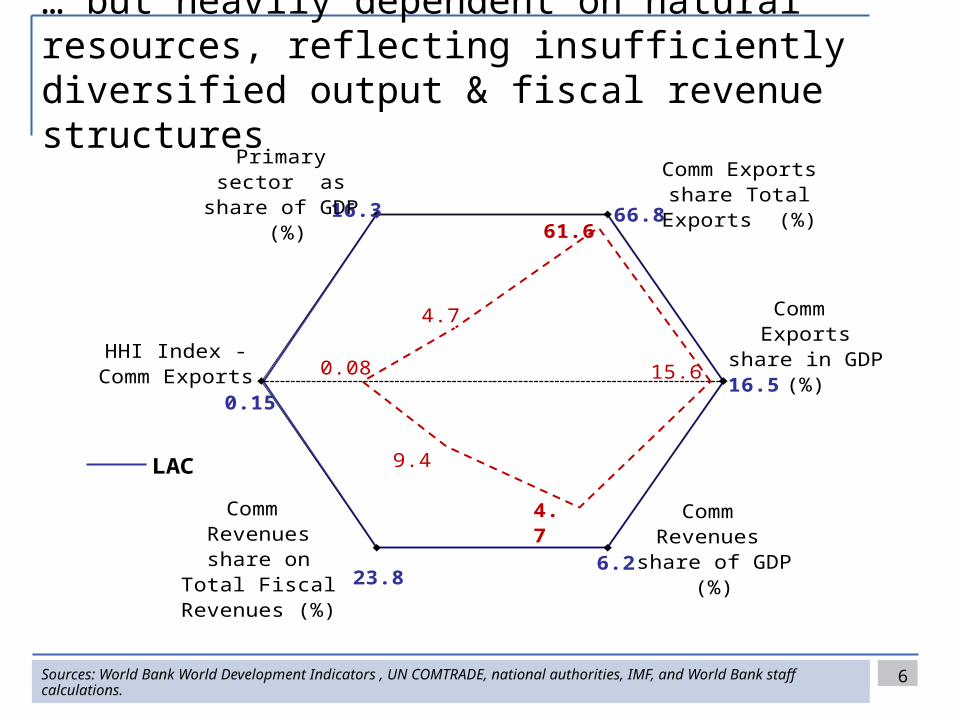

… but heavily dependent on natural resources, reflecting insufficiently diversified output & fiscal revenue structures

Sources: World Bank World Development Indicators , UN COMTRADE, national authorities, IMF, and World Bank staff calculations.

15.6

61.6

4.7

9.4

0.0816.5

66.816.3

0.15

23.86.2

Comm Exports share Total

Exports (%)

Primary sector as share of GDP (%)

HHI Index - Comm Exports

Comm Revenues share on Total

Fiscal Revenues (%)

Comm Revenues share of GDP (%)

Comm Exports share in GDP (%)

LAC

Developed 4.7

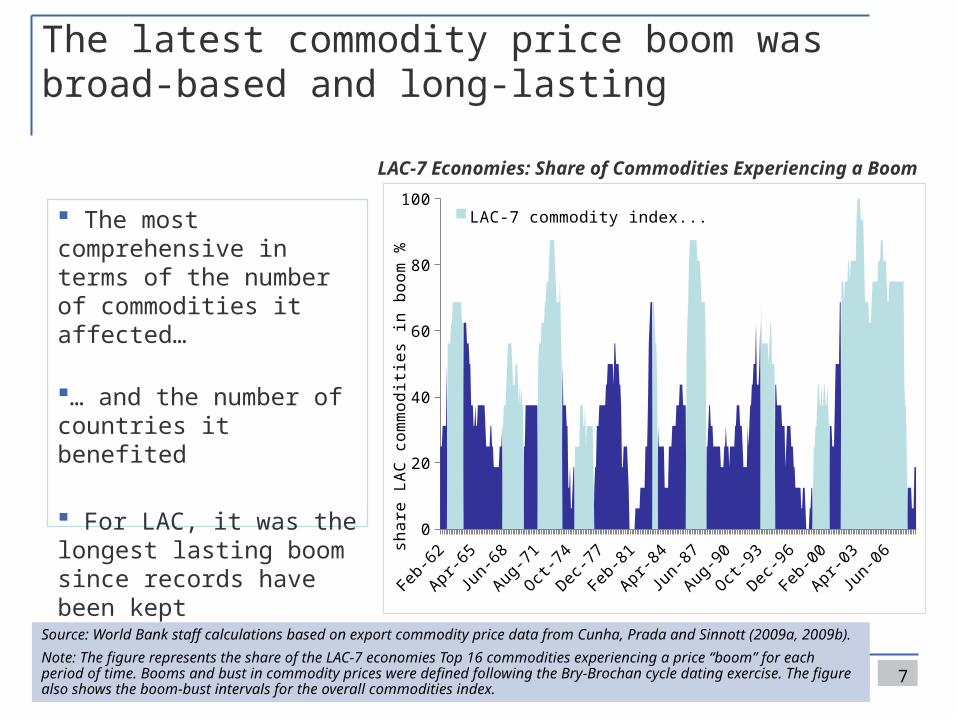

The latest commodity price boom was broad-based and long-lasting

The most comprehensive in terms of the number of commodities it affected…

… and the number of countries it benefited

For LAC, it was the longest lasting boom since records have been kept

7

Source: World Bank staff calculations based on export commodity price data from Cunha, Prada and Sinnott (2009a, 2009b).

Note: The figure represents the share of the LAC-7 economies Top 16 commodities experiencing a price “boom” for each period of time. Booms and bust in commodity prices were defined following the Bry-Brochan cycle dating exercise. The figure also shows the boom-bust intervals for the overall commodities index.

LAC-7 Economies: Share of Commodities Experiencing a Boom

Jan-

62

Sep-6

6

May

-71

Jan-

76

Sep-8

0

May

-85

Jan-

90

Sep-9

4

May

-99

Jan-

04

Sep-0

80

20

40

60

80

100 LAC-7 commodity index in boomLAC-7 commodity index in bust

shar

e L

AC

com

mod

ities

in b

oom

%

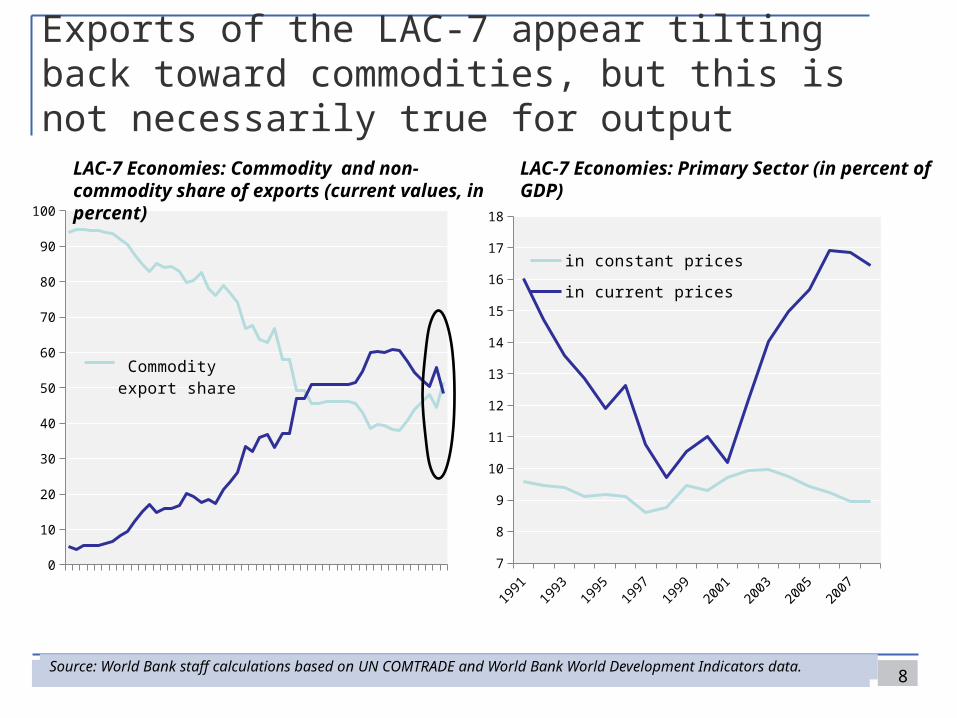

Exports of the LAC-7 appear tilting back toward commodities, but this is not necessarily true for output

8Source: World Bank staff calculations based on UN COMTRADE and World Bank World Development Indicators data.

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1991

1993

1994

1996

1999

2002

2005

2008

0

10

20

30

40

50

60

70

80

90

100

Commodity export share

Non-commodity export share

LAC-7 Economies: Primary Sector (in percent of GDP)LAC-7 Economies: Commodity and non-commodity share of exports (current values, in percent)

1991

1993

1995

1997

1999

2001

2003

2005

2007

7

8

9

10

11

12

13

14

15

16

17

18

in constant prices

in current prices

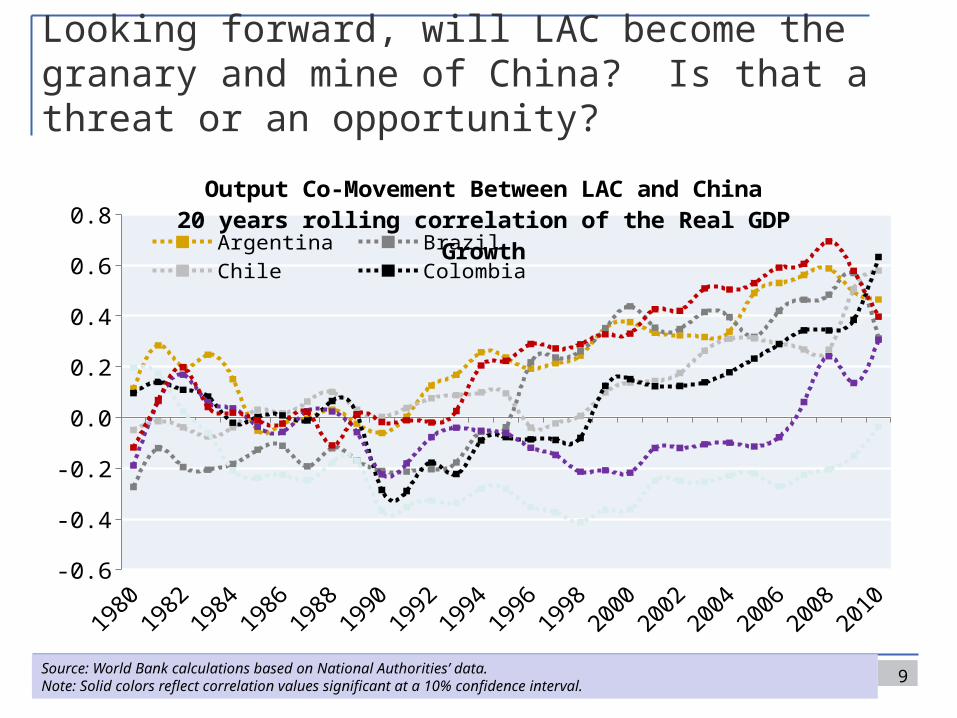

Looking forward, will LAC become the granary and mine of China? Is that a threat or an opportunity?

9

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8Output Co-Movement Between LAC and China20 years rolling correlation of the Real GDP

GrowthArgentina BrazilChile Colombia

Source: World Bank calculations based on National Authorities’ data. Note: Solid colors reflect correlation values significant at a 10% confidence interval.

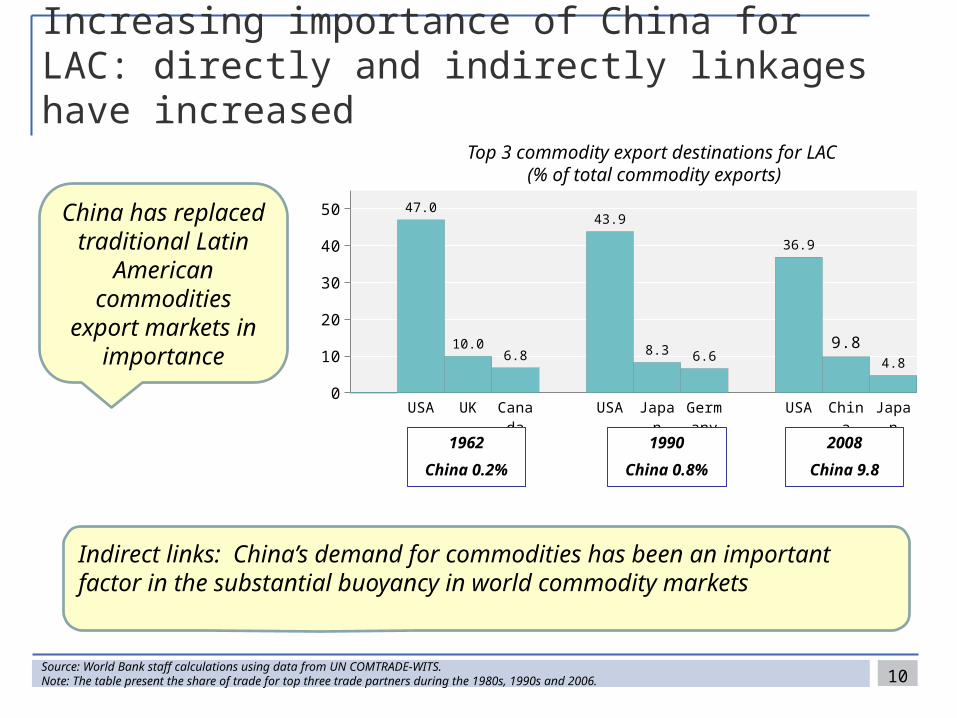

Increasing importance of China for LAC: directly and indirectly linkages have increased

10Source: World Bank staff calculations using data from UN COMTRADE-WITS. Note: The table present the share of trade for top three trade partners during the 1980s, 1990s and 2006.

USA UK Canada

USA Japan Ger-many

USA China Japan0

10

20

30

40

50 47.0

10.06.8

43.9

8.3 6.6

36.9

9.84.8

1962

China 0.2%

1990

China 0.8%

2008

China 9.8

Top 3 commodity export destinations for LAC (% of total commodity exports)

China has replaced traditional Latin

American commodities export

markets in importance

Indirect links: China’s demand for commodities has been an important factor in the substantial buoyancy in world commodity markets

The “natural resource curse” hypothesis: much ado about nothing?

11

12

We can’t ignore the curse hypothesis… some very wise people have believed it!

“Ten years from now, twenty years from now,

you will see: oil will bring us ruin … Oil is the Devil’s excrement’’ (early 1970s)

– Juan Pablo Pérez, Venezuelan Minister of Energy and founder of

OPEC

“Neither now nor in former ages have the nations possessing the best

climate and soil been either the richest or the most powerful; but …

generally among the poorest” (1848) – John Stuart Mill

“Oil is a curse. Natural gas, copper, and

diamonds are also bad for a country’s health” (2009) – Moisés Naím, Foreign Policy editor-

in-chief

“Projects of mining… are the projects… to which of all others a prudent law-giver, who desired

to increase the capital of his nation, would least choose to

give any extraordinary encouragement” (1776) –Adam

Smith

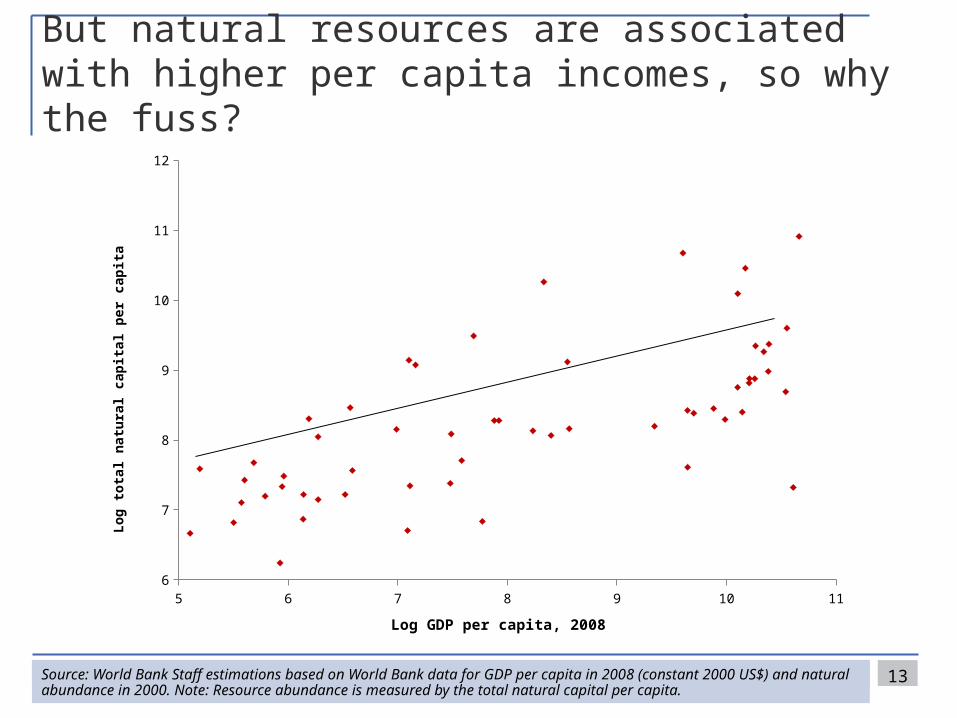

13Source: World Bank Staff estimations based on World Bank data for GDP per capita in 2008 (constant 2000 US$) and natural abundance in 2000. Note: Resource abundance is measured by the total natural capital per capita.

5 6 7 8 9 10 116

7

8

9

10

11

12

Log GDP per capita, 2008

Log

tota

l nat

ural

capi

tal p

er ca

pita

But natural resources are associated with higher per capita incomes, so why the fuss?

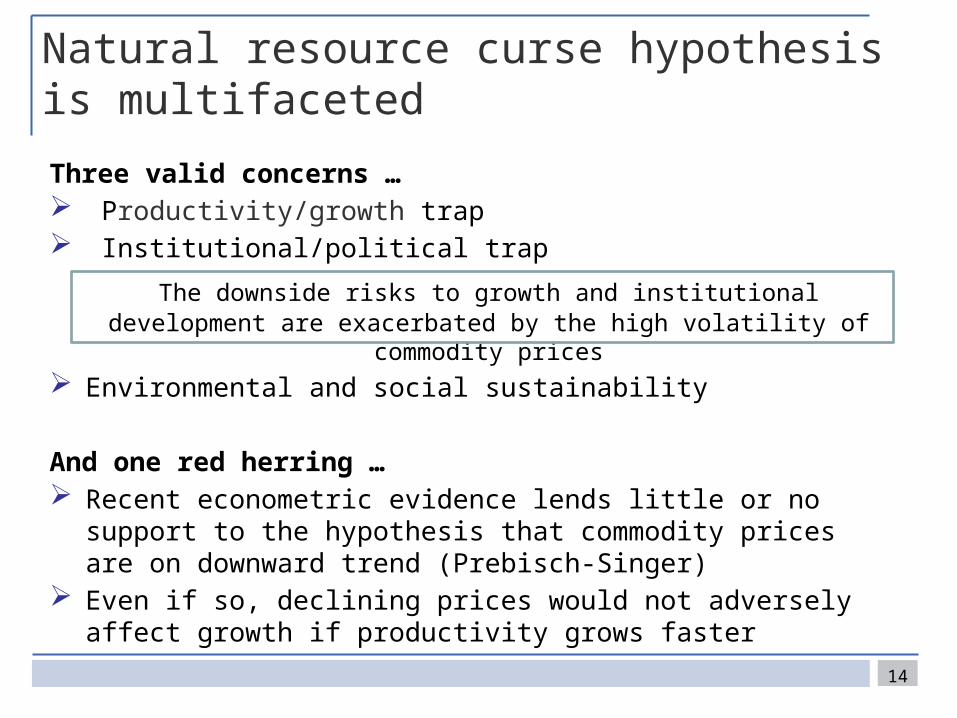

Natural resource curse hypothesis is multifaceted

Three valid concerns … Productivity/growth trap Institutional/political trap

The downside risks to growth and institutional development are exacerbated by the high volatility of commodity prices

Environmental and social sustainability

And one red herring … Recent econometric evidence lends little or no support to the hypothesis

that commodity prices are on downward trend (Prebisch-Singer) Even if so, declining prices would not adversely affect growth if

productivity grows faster

14

Dutch Disease: does commodity specialization undermine growth?

Some evidence seems to say yes Enclave production in many countries in the past, with few linkages and

minimal employment generation Via a strong currency (Dutch Disease), commodities can displace industries

where potential spillovers are higher (Hausmann, Rodrik)

But …. Careful econometric evidence contradicts early finding of a curse effect Many high-income countries developed by exploiting natural resources Commodity sectors can be of high productivity with much innovation Many cases of linkages & upgrading with significant employment effects

Bottom line: issues are more complicated than commonly thought, with much space for policies to determine outcomes

15

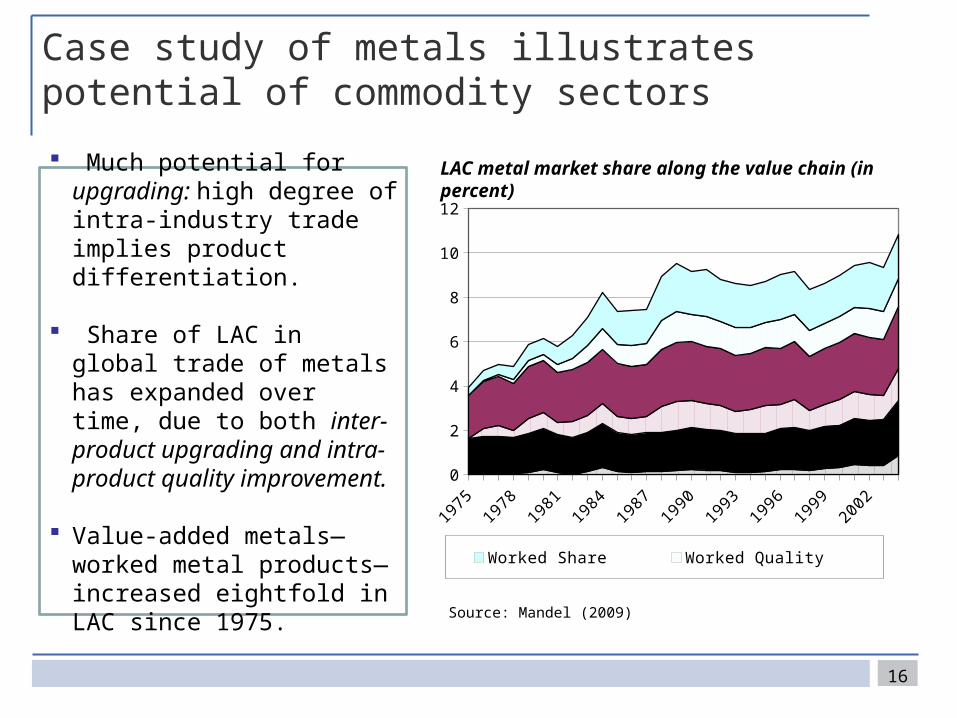

Case study of metals illustrates potential of commodity sectors

16

LAC metal market share along the value chain (in percent)

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

0

2

4

6

8

10

12

Worked Share Worked Quality Unwrought ShareUnwrought Quality Ore Share Ore Quality

Much potential for upgrading: high degree of intra-industry trade implies product differentiation.

Share of LAC in global trade of metals has expanded over time, due to both inter-product upgrading and intra-product quality improvement.

Value-added metals—worked metal products—increased eightfold in LAC since 1975.

Source: Mandel (2009)

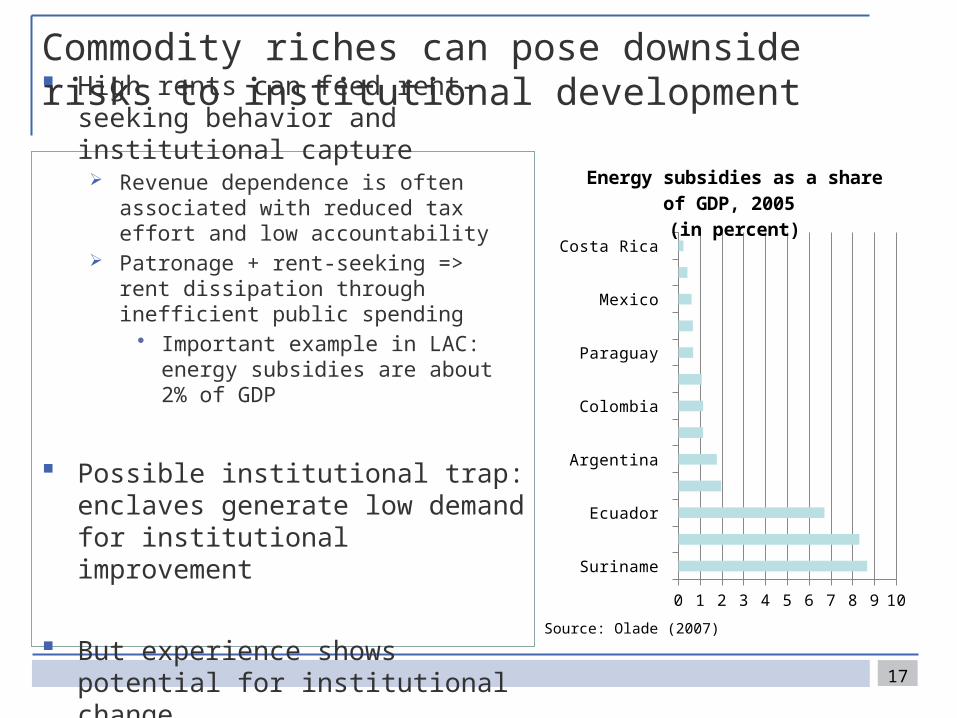

Commodity riches can pose downside risks to institutional development

High rents can feed rent-seeking behavior and institutional capture Revenue dependence is often associated with

reduced tax effort and low accountability Patronage + rent-seeking => rent dissipation

through inefficient public spending• Important example in LAC: energy

subsidies are about 2% of GDP

Possible institutional trap: enclaves generate low demand for institutional improvement

But experience shows potential for institutional change

17

Suriname

Venezuela

Ecuador

Bolivia

Argentina

Guyana

Colombia

Nicaragua

Paraguay

Trinidad & Tobago

Mexico

Guatemala

Costa Rica

0 1 2 3 4 5 6 7 8 9 10

Energy subsidies as a share of GDP, 2005

(in percent)

Source: Olade (2007)

Two institutional dimensions in which LAC seems to suffer less from the resource curse than other regions

No systematic effect in undermining democracy But some recent backsliding in quality of democracy in hydrocarbon

producing states

No tendency for increased large-scale violent conflict in resource-rich states Fewer secessionist movements in LAC – perhaps because these were

worked out over the longer history of independence

Institutions in many LAC countries are improving, but greater decentralization may create special problems

18

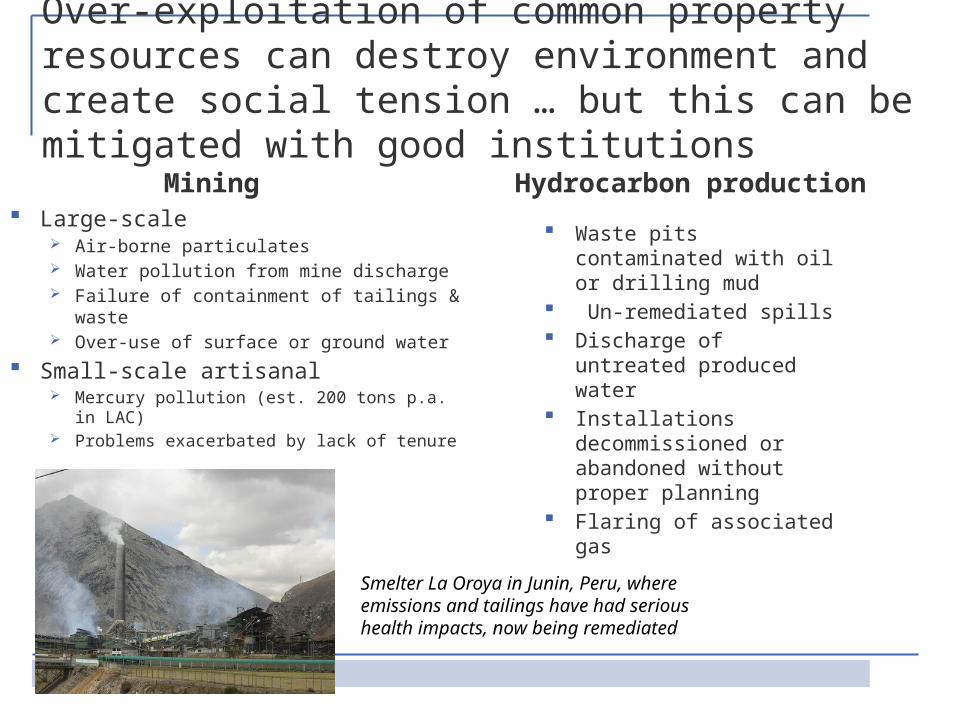

Over-exploitation of common property resources can destroy environment and create social tension … but this can be mitigated with good institutions

Mining Large-scale

Air-borne particulates Water pollution from mine discharge Failure of containment of tailings & waste Over-use of surface or ground water

Small-scale artisanal Mercury pollution (est. 200 tons p.a. in LAC) Problems exacerbated by lack of tenure

Hydrocarbon production

Waste pits contaminated with oil or drilling mud

Un-remediated spills Discharge of untreated

produced water Installations

decommissioned or abandoned without proper planning

Flaring of associated gas

Smelter La Oroya in Junin, Peru, where emissions and tailings have had serious health impacts, now being remediated

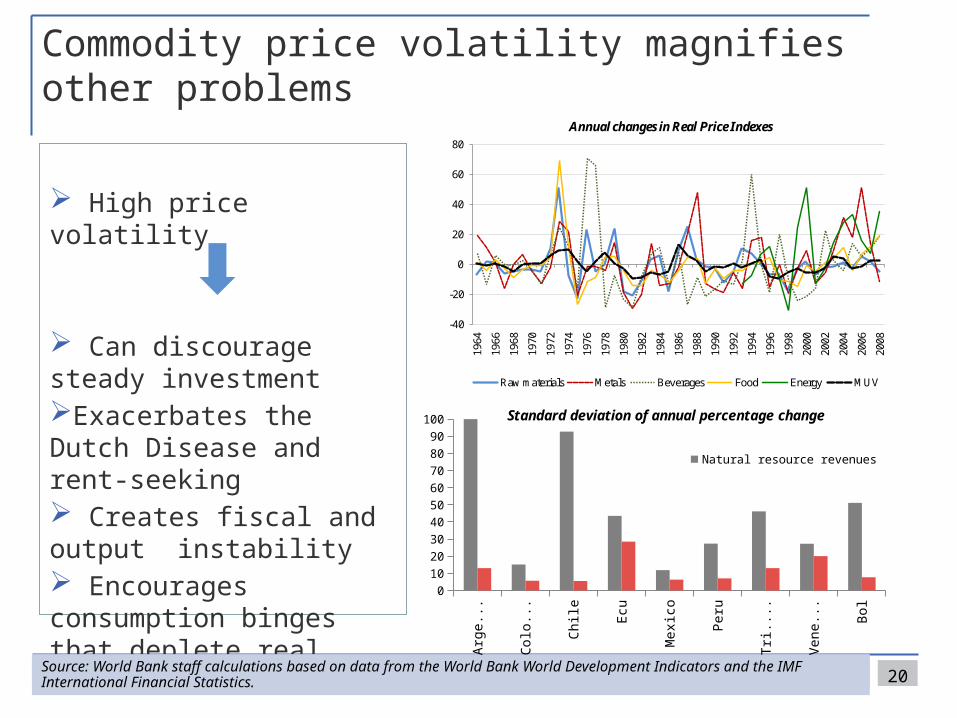

Commodity price volatility magnifies other problems

High price volatility

Can discourage steady investment Exacerbates the Dutch Disease and rent-seeking Creates fiscal and output instability Encourages consumption binges that deplete real wealth

20Source: World Bank staff calculations based on data from the World Bank World Development Indicators and the IMF International Financial Statistics.

Arge

ntina

Colo

mbi

a

Chile

Ecua

dor

Mex

ico

Peru

Tri.

& T

ob.

Vene

zuel

a

Boliv

ia

0102030405060708090

100 Standard deviation of annual percentage change

Natural resource revenues

Non-natural resource revenues

-40

-20

0

20

40

60

80

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Annual changes in Real Price Indexes

Raw materials Metals Beverages Food Energy MUV

Managing commodity abundance and commodity price volatility…

It’s all about saving, insurance, andgood regulation

21

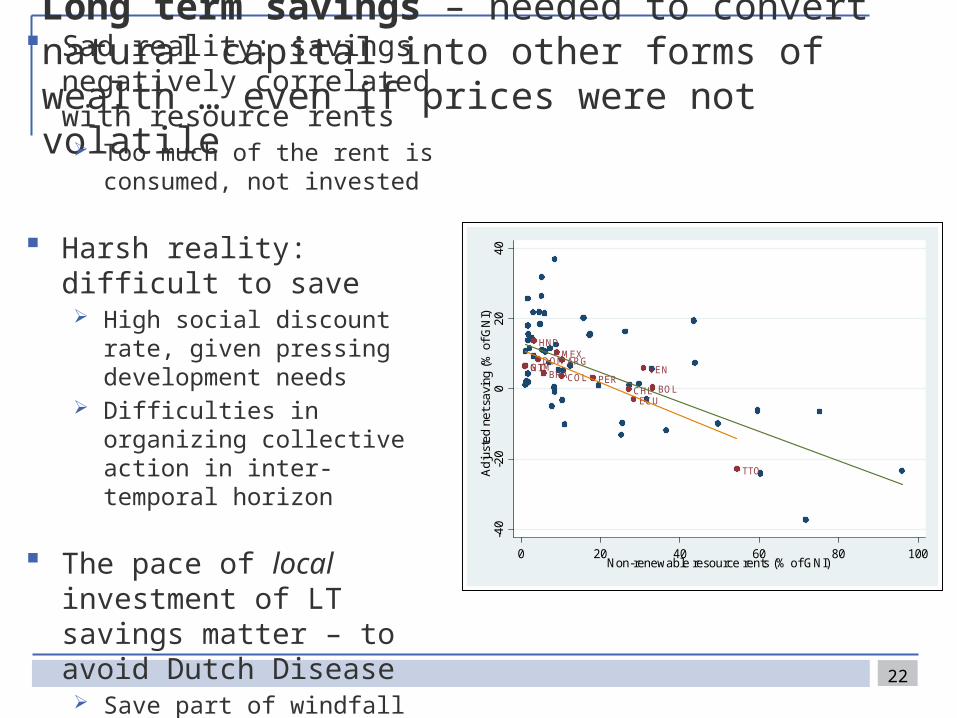

Long term savings – needed to convert natural capital into other forms of wealth … even if prices were not volatile

Sad reality: savings negatively correlated with resource rents Too much of the rent is consumed,

not invested

Harsh reality: difficult to save High social discount rate, given

pressing development needs Difficulties in organizing collective

action in inter-temporal horizon

The pace of local investment of LT savings matter – to avoid Dutch Disease Save part of windfall abroad

22

BRA PERNIC

ARG

COL

ECU

MEX

TTO

DOM

BOL

HND

GTM VEN

CHL

-40

-20

020

40A

djus

ted

net s

avin

g (%

of G

NI)

0 20 40 60 80 100Non-renewable resource rents (% of GNI)

And short term volatility requires other strategies

Self protection: reduce income volatility through diversification Tradable sector diversification (requires avoiding excessive real

appreciation through saving and gradual local investment of windfall) Don’t forget to nurture the goose that lays golden eggs!

• Diversification of commodity production also reduces income volatility Fiscal revenue diversification Buffer adverse impact on the poor through targeted transfers

Market insurance to hedge price volatility Market for hedges and insurance products is incomplete, especially for the

long-term … … but emerging successful experiences in hedging (Mexico, Panama) Political and legal risks hinder the use of market instruments

23

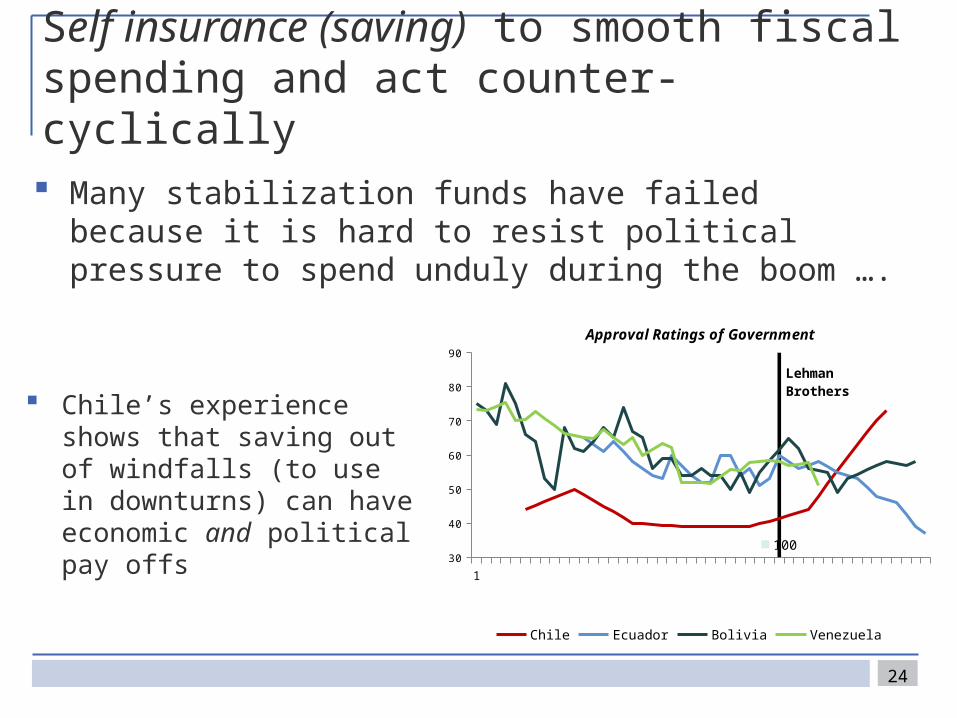

Self insurance (saving) to smooth fiscal spending and act counter-cyclically

Many stabilization funds have failed because it is hard to resist political pressure to spend unduly during the boom ….

24

Chile’s experience shows that saving out of windfalls (to use in downturns) can have economic and political pay offs

130

40

50

60

70

80

90

100

Chile Ecuador Bolivia Venezuela

Lehman Broth-ers

Approval Ratings of Government

Address environmental and social problems with up-front actions and new tools

Reduce environmental impact:

Don’t subsidize environmental destruction!

Take advantage of market-based approaches (tradable permits, PES)

Use strategic environmental assessments

Build local government and civil society capacity to help enforce environmental regulations

25

Reduce social impact:

Grant secure land title in advance of large projects

Educate residents to avoid unrealistic expectations

Strengthen local capacity to negotiate

Promote transparency (EITI) Avoid resettlement if possible

26

Thank you