Natural Phenomena and Human Economic Behavioral …

106

Natural Phenomena and Human Economic Behavioral Influence in Multi-Factor Predictive Modeling The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citable link http://nrs.harvard.edu/urn-3:HUL.InstRepos:37736810 Terms of Use This article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Other Posted Material, as set forth at http:// nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of- use#LAA

Transcript of Natural Phenomena and Human Economic Behavioral …

Natural Phenomena and HumanEconomic Behavioral Influence inMulti-Factor Predictive Modeling

The Harvard community has made thisarticle openly available. Please share howthis access benefits you. Your story matters

Citable link http://nrs.harvard.edu/urn-3:HUL.InstRepos:37736810

Terms of Use This article was downloaded from Harvard University’s DASHrepository, and is made available under the terms and conditionsapplicable to Other Posted Material, as set forth at http://nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of-use#LAA

Natural Phenomena and Human Economic Behavioral Influence in Multi-Factor

Predictive Modeling

Shawn J. Mushtaq

A Thesis in the Field of International Relations

for the Master of Liberal Arts Degree

Harvard University

November 2017

© Copyright 2017 Shawn J. Mushtaq. All Rights Reserved.

Abstract

This research investigates the impact of human economic behavioral activity and

the Earth’s magnetic field in the area of financial economics using the Fama-French 3-

Factor Model as a test subject. The research objective is to test whether human economic

and geomagnetic activity could improve quantifiable estimated outputs in the Fama-

French Model—and to discover if there are any relationships with these variables that

could have a profound influence in predicting financial market or economic activity.

After reviewing all data and research approaches, the concluding analysis

indicates that geomagnetic activity does not have strong enough influence to reasonably

predict equity and fund returns. For human economic behavior, the absolute change in

Money Velocity and U-3 Unemployment improves the original Fama-French 3-Factor

Model by nearly 3% and outpaces the 5-Factor model under an array of tests. Keywords

for this research are: (i) Financial Economics, (ii) Quantitative Methodology, (iii)

Investment Portfolio Management, (iv) Geophysics, and (v) Machine Learning. Research

supervision was directed under Muhammet Bas, Ph.D. at the Department of Government,

Harvard University Graduate School of Arts and Sciences.

iv

Table of Contents

I. Introduction….……………………………………………….…………………………1

Research Questions………………………………….…...………………………..2

Research Hypothesis……………………………………………...……….…...….2

Research Significance……………………………………….……...…………..…3

II. Definition of Terms…..…...............................................................................................4

III. Literature Review – Background of the Problem…..…................................................8

IV. Research Methodology……………………………………………..………………..16

V. Data Transformations…………………………………...…………………………….23

VI. Limitations…………………………………………………………………...………26

VII. Quantitative Modeling with Returns………..…………………………..………..…27

Original Approach: State Street Corporation Stock Returns……….....................27

Original Approach: Vanguard S&P 500 Fund Returns.…….…………….……..34

EMA Approach: State Street Corporation Stock Returns….……………..……...43

EMA Approach: Vanguard S&P 500 Fund Returns….…………....……...……..46

Concluding Analysis for Chapter VII…………………………………...…...…..50

VIII. Model Validation & Estimation ………………………………………...…………53

List of Qualifying Models………………………………………………..………53

Model Fitness Test: STT Observed verses Predicted Values…..……………..…54

Model Fitness Test: Vanguard Observed verses Predicted Values ………..……56

v

Robustness Analysis on Modeled Vanguard Returns: 2008-2009 Financial

Crisis..........................................................................................................58

Alternative 5-Factor Model verses the Fama-French 5-Factor Model…………..59

Concluding Analysis for Chapter VIII…………………………….......................62

IX. Research Conclusion………………………………………………...........................64

Appendix A: Experiential Modeling with Adjusted Closed Prices…………...…………67

Section A-1: Modeling with STT Stock Prices ………………….....…...………68

Section A-2: Modeling with Vanguard Fund Prices……………....……...……...69

Section A-3: STT Robustness Analysis & Model Fitness…………..…...…...….72

Section A-4: Vanguard S&P 500 Robustness Analysis & Model Fitness…….…75

Appendix B: Data Transformation Approach for Returns………………...……………..78

Section B-1: State Street Corporation Stock Returns…………………….…..….79

Section B-2: Vanguard S&P 500 Fund Returns……………………………..…..82

Appendix C: Causality of Earth’s Magnetic Field and Human Economic Behavior……85

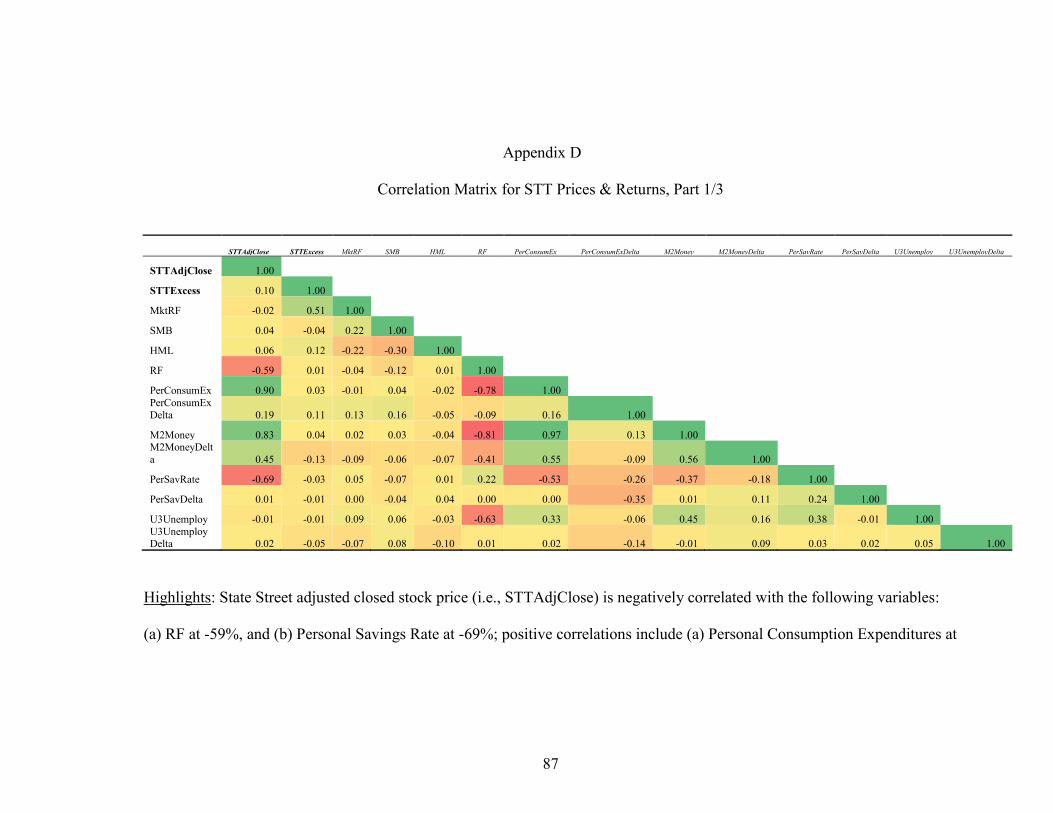

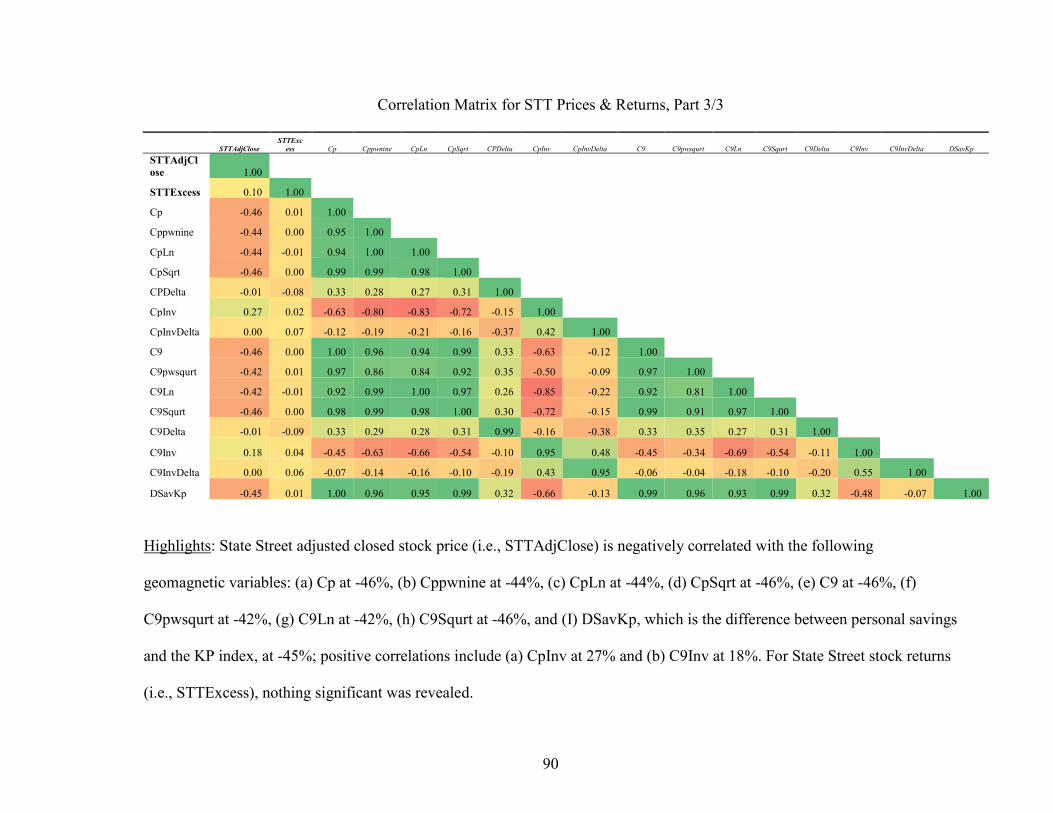

Appendix D: Correlation Matrix for STT Prices & Returns……………………….….…87

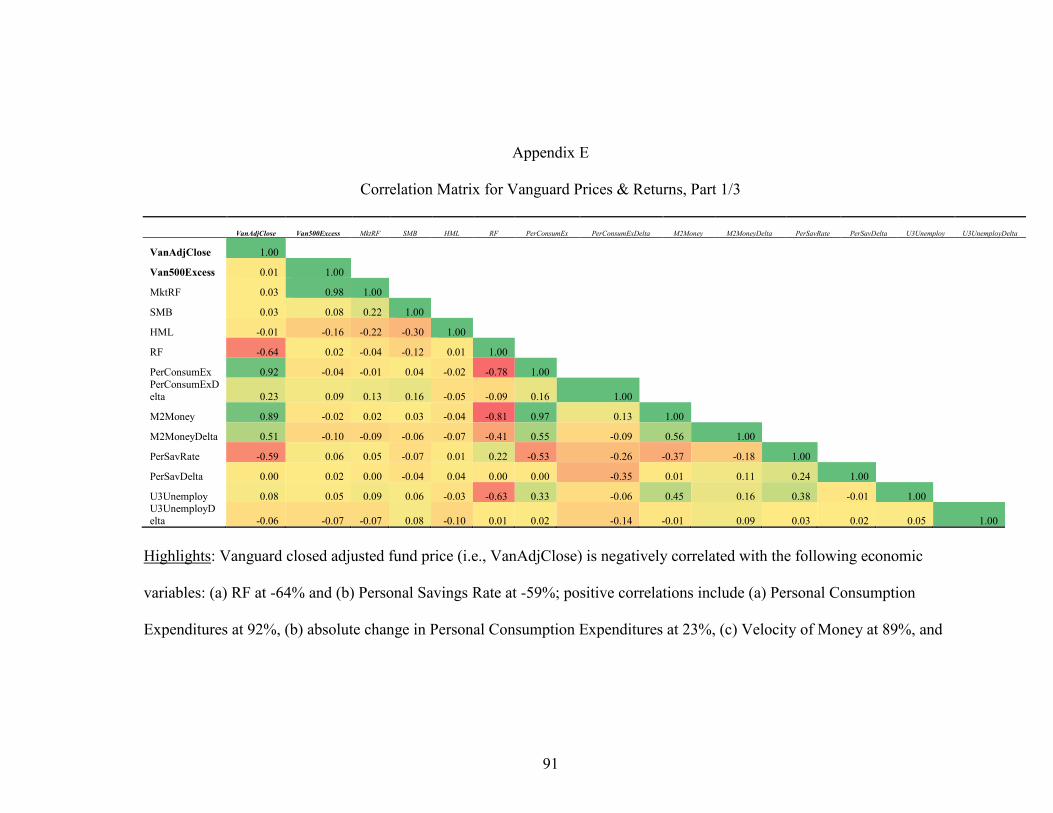

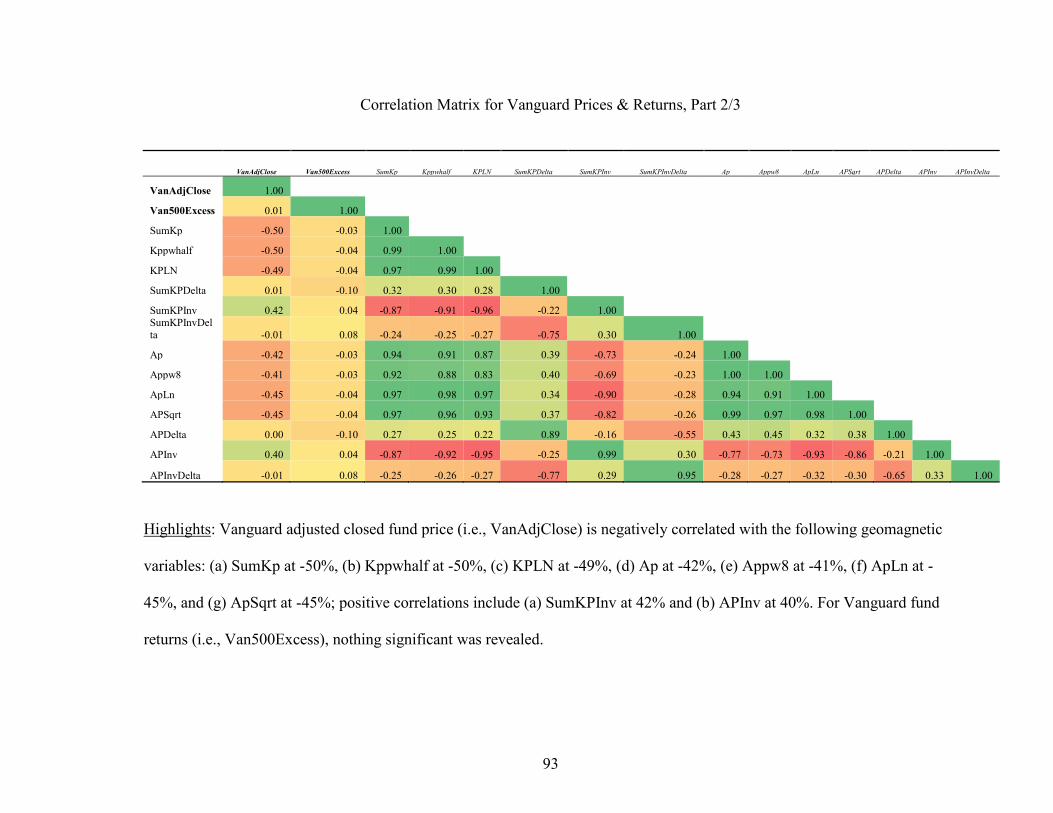

Appendix E: Correlation Matrix for Vanguard S&P 500 Fund Prices & Returns….…....91

X. References…………………………………………………………………...…..……95

vi

List of Tables

Table 5-1: Data Transformations………………………………………………………...23

Table 7-1: STT Original Model Regression Results, Part 1…………………………..…28

Table 7-2: STT Original Model Regression Results, Part 2…...……….………………..29

Table 7-3: STT Original Model Regression Results, Part 3.……...……………………..30

Table 7-4: STT Money Velocity Relationship Test...........................................................31

Table 7-5: STT Adjusted FFModel v. Original.................................................................32

Table 7-6: STT Original Model Regression Results, Part 4…..…………………………33

Table 7-7: Van500 Original Model Regression Results, Part 1……………………….…35

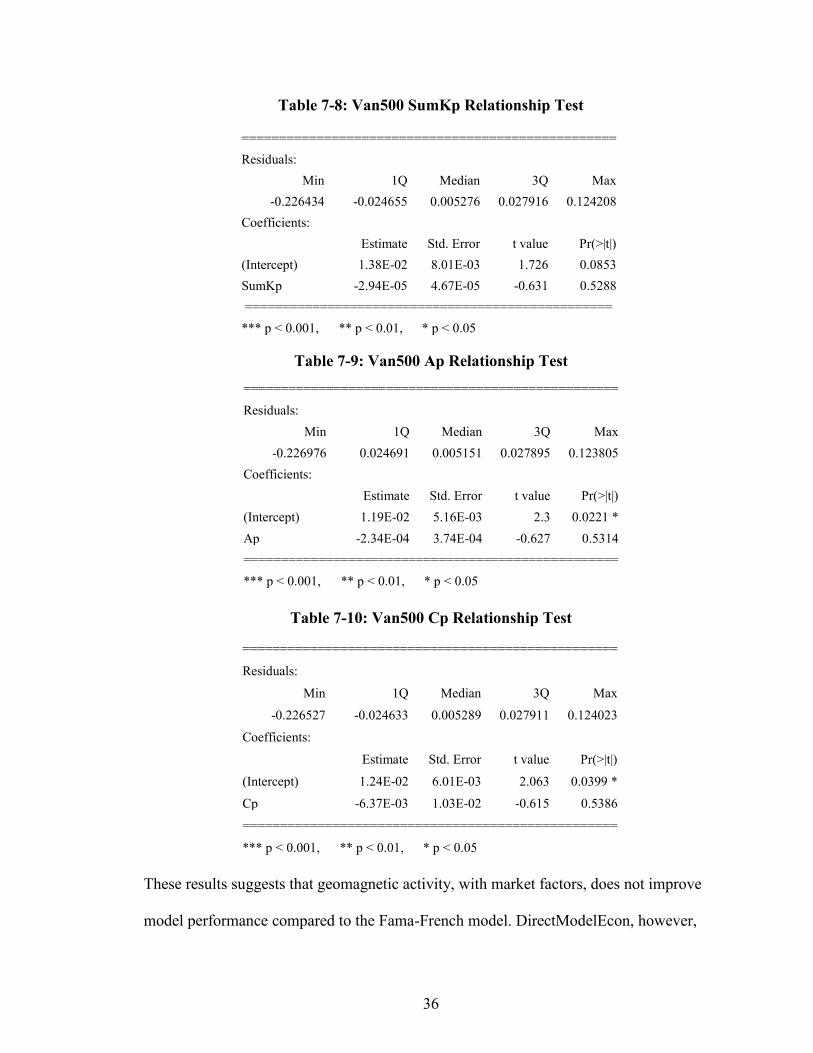

Table 7-8: Van500 SumKp Relationship Test……………………………………...……36

Table 7-9: Van500 Ap Relationship Test…………..………………………………..…..36

Table 7-10: Van500 Cp Relationship Test…………………………………………….…36

Table 7-11: Van500 Adjusted DirectModelEcon v. FFModel…………..…………....…37

Table 7-12: Van500 Original Model Regression Results, Part 2……………...…………38

Table 7-13: Van500 Adjusted Model 2 v. FFModel ……………..…………………...…39

Table 7-14: Van500 Original Model Regression Results, Part 3………………...………40

Table 7-15: Van500 Original Model Regression Results, Part 4……..……………….…41

Table 7-16: STT EMA Approach, Part 1…………...……………………………………44

Table 7-17: STT EMA Kp Index Relationship Test…………………………………..…45

Table 7-18: STT EMA Approach, Part 2...………………………………………………45

Table 7-19: Van500 EMA Approach, Part 1…...……………………………..…………47

vii

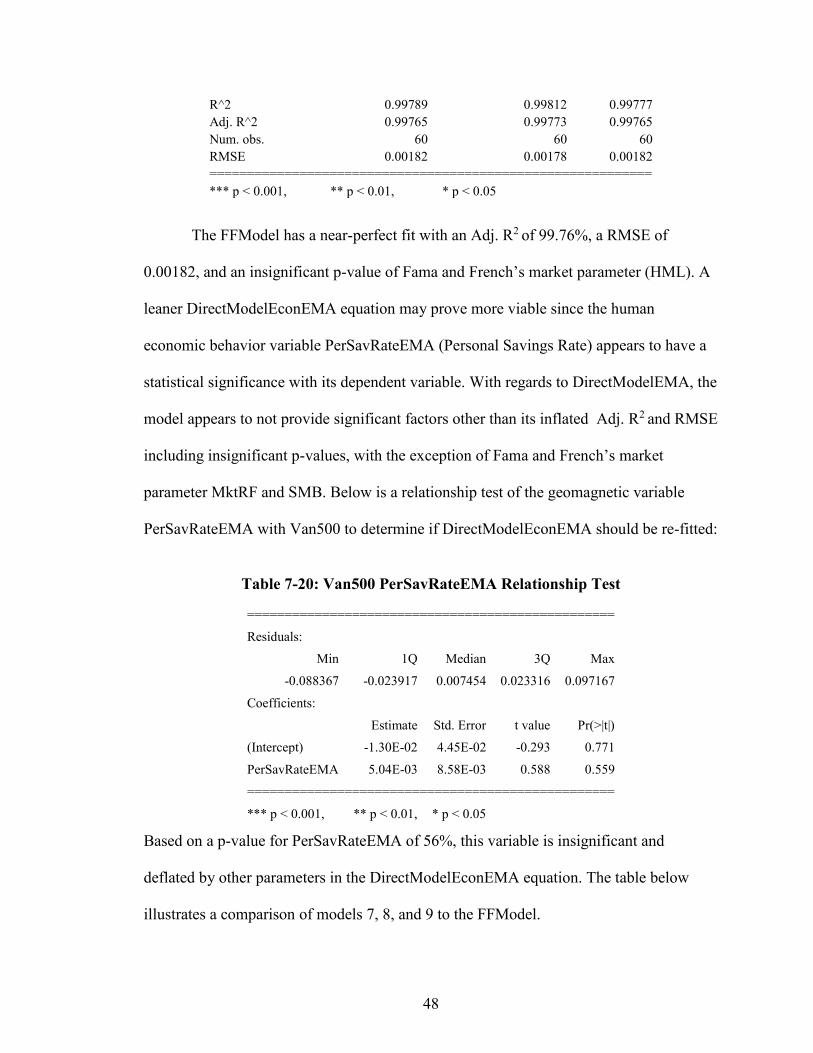

Table 7-20: Van500 PerSavRateEMA Relationship Test...………………………...……48

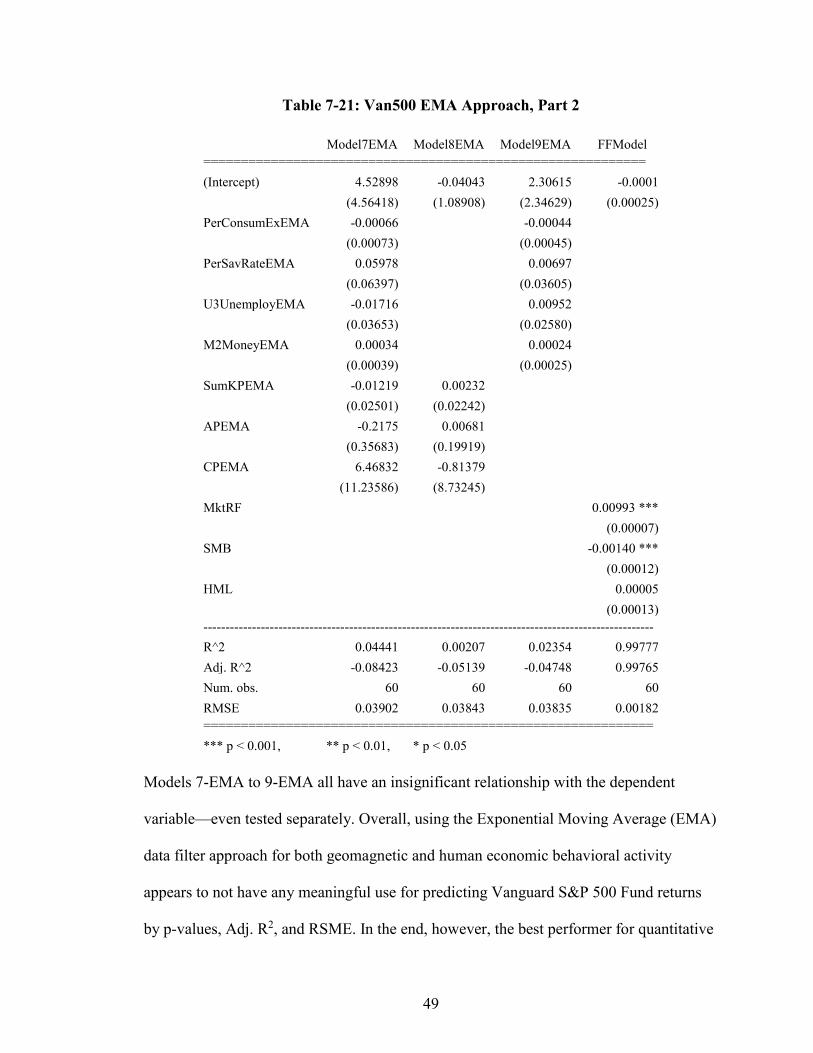

Table 7-21: Van500 EMA Approach, Part 2………………………………………….…49

Table 7-22: STT Short-Listed Models for Chapter VII……………………………….…51

Table 7-23: Van500 Short-Listed Models for Chapter VII…………………………...…53

Table 8-1: All Qualifying Models…………………………………………………..……54

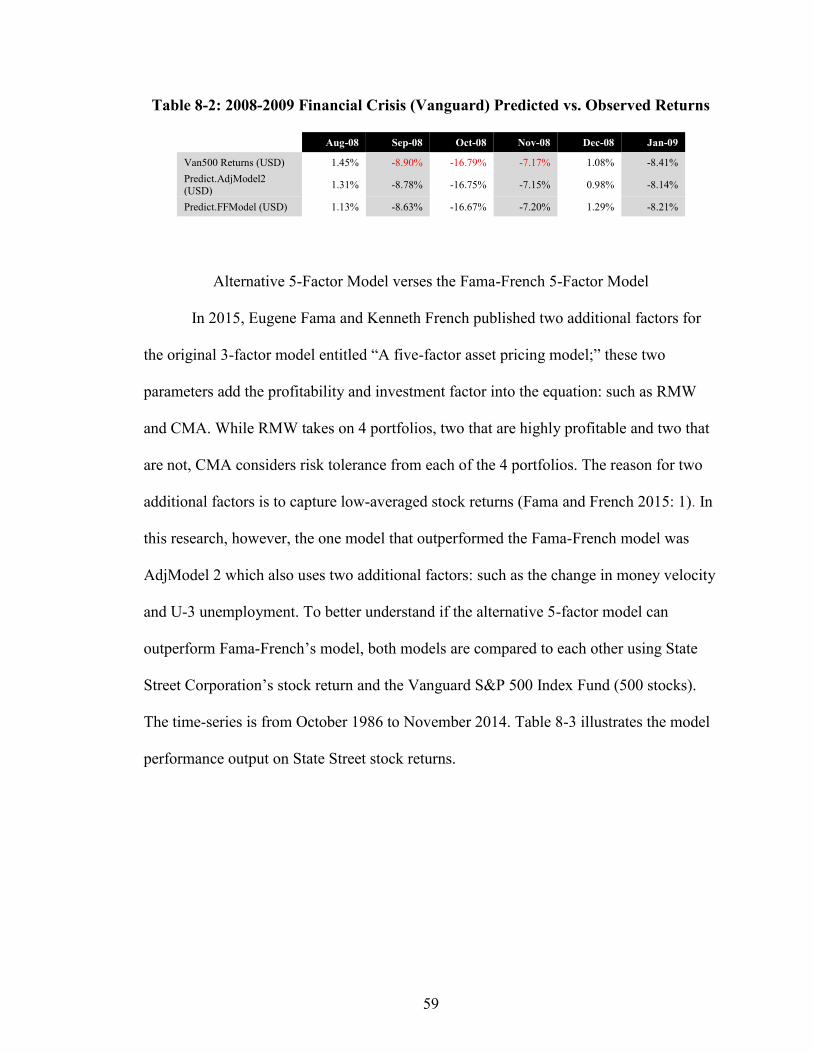

Table 8-2: 2008-2009 Financial Crisis (Vanguard) Predicted vs. Observed Returns……59

Table 8-3: Alternative 5-Factor v. Fama-French 5-Factor on STT Returns ………….…60

Table 8-4: Alternative 5-Factor v. Fama-French 5-Factor on Vanguard Returns ………61

Table A-1.1: STT Model Regression Results ………………………………………...…68

Table A-2.1: Van500 Regression Results……………………………………………..…69

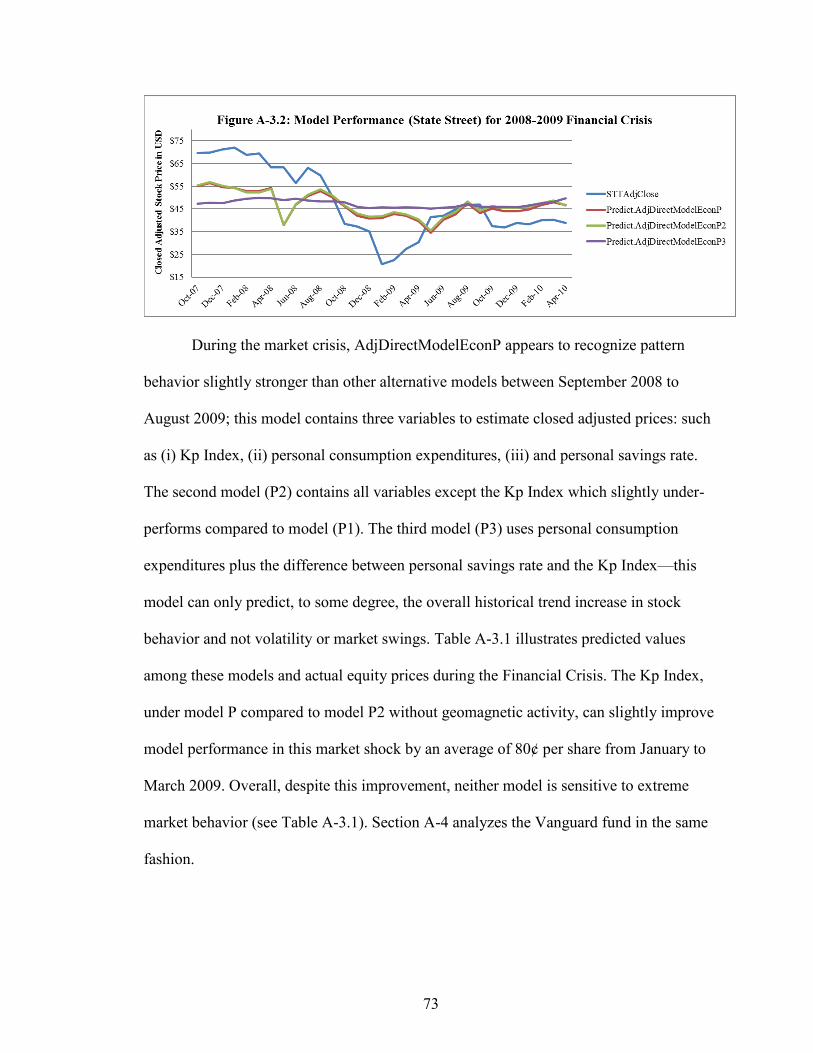

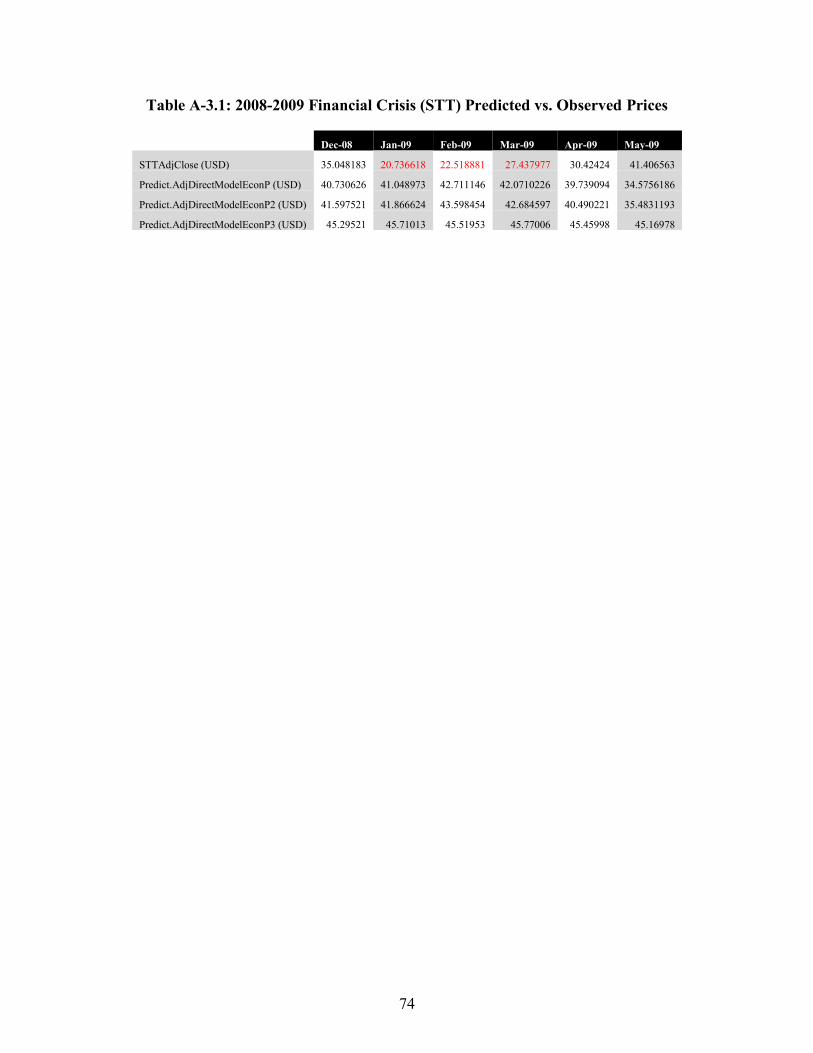

Table A-3.1: 2008-2009 Financial Crisis (STT) Predicted vs. Observed Prices…...……74

Table A-4.1: 2008-2009 Financial Crisis (Vanguard) Predicted vs. Observed Prices…..77

Table B-1.1: STT Transformed Data Approach, Part 1……………………………..…...79

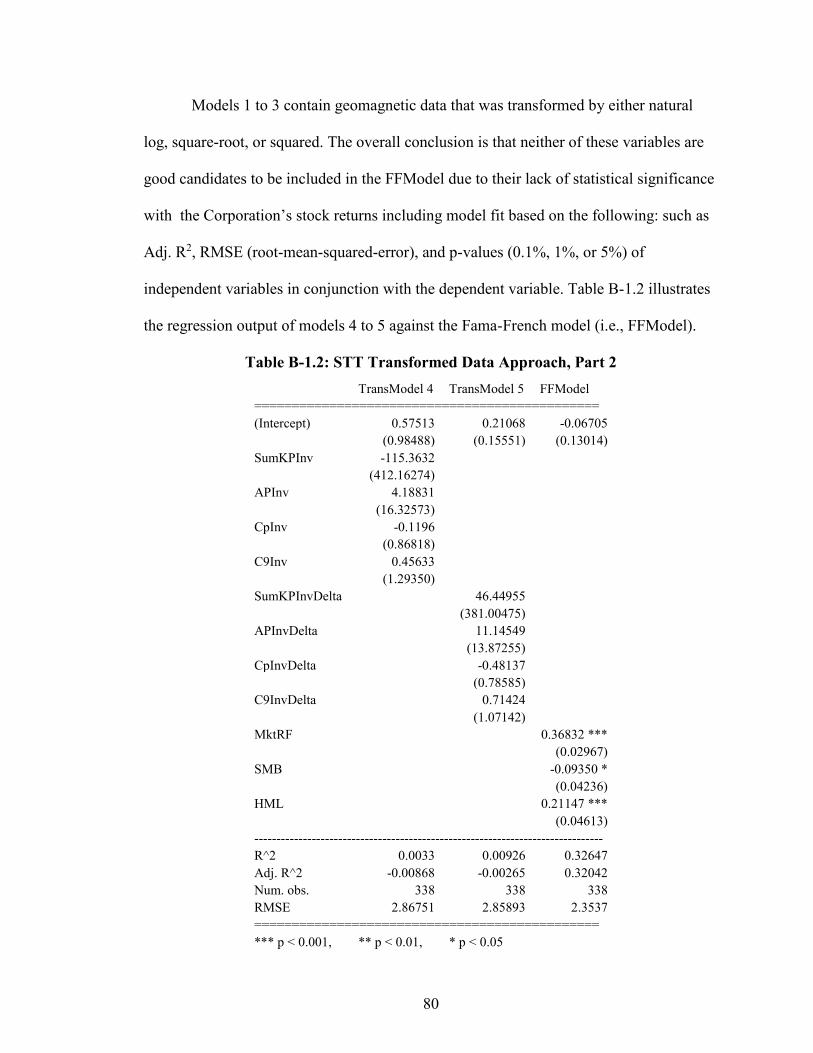

Table B-1.2: STT Transformed Data Approach, Part 2…………………………….....…80

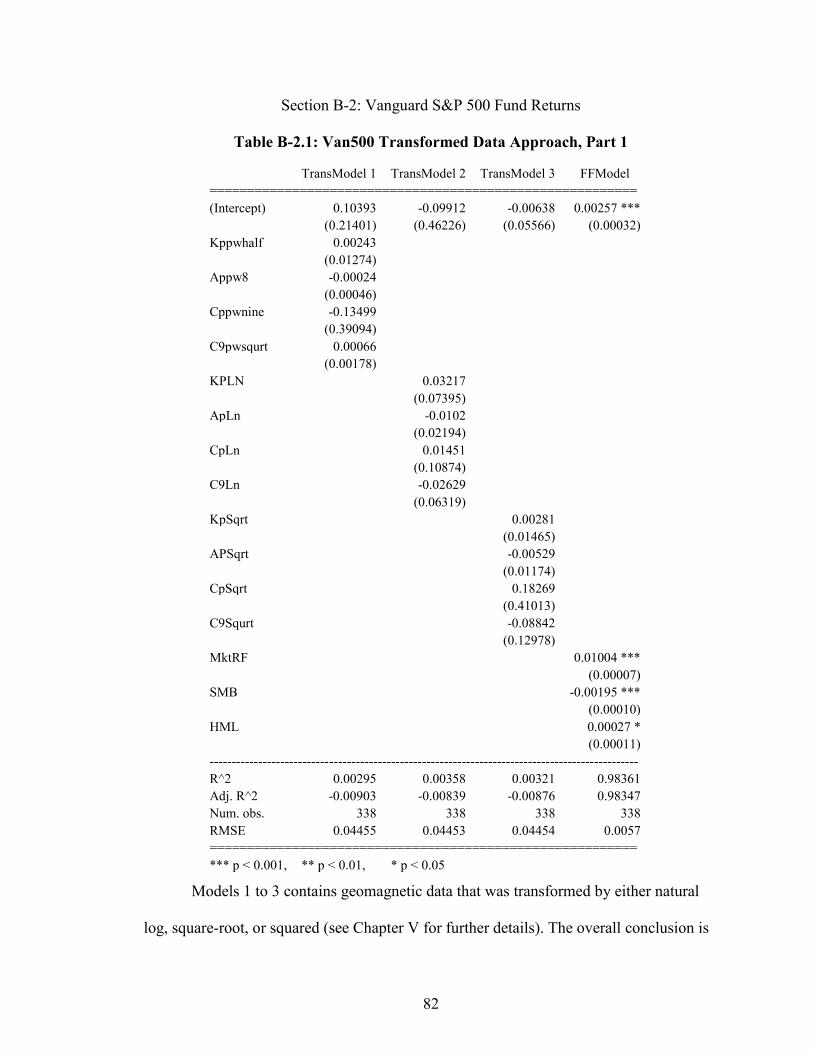

Table B-2.1: Van500 Transformed Data Approach, Part 1……………………..…….…82

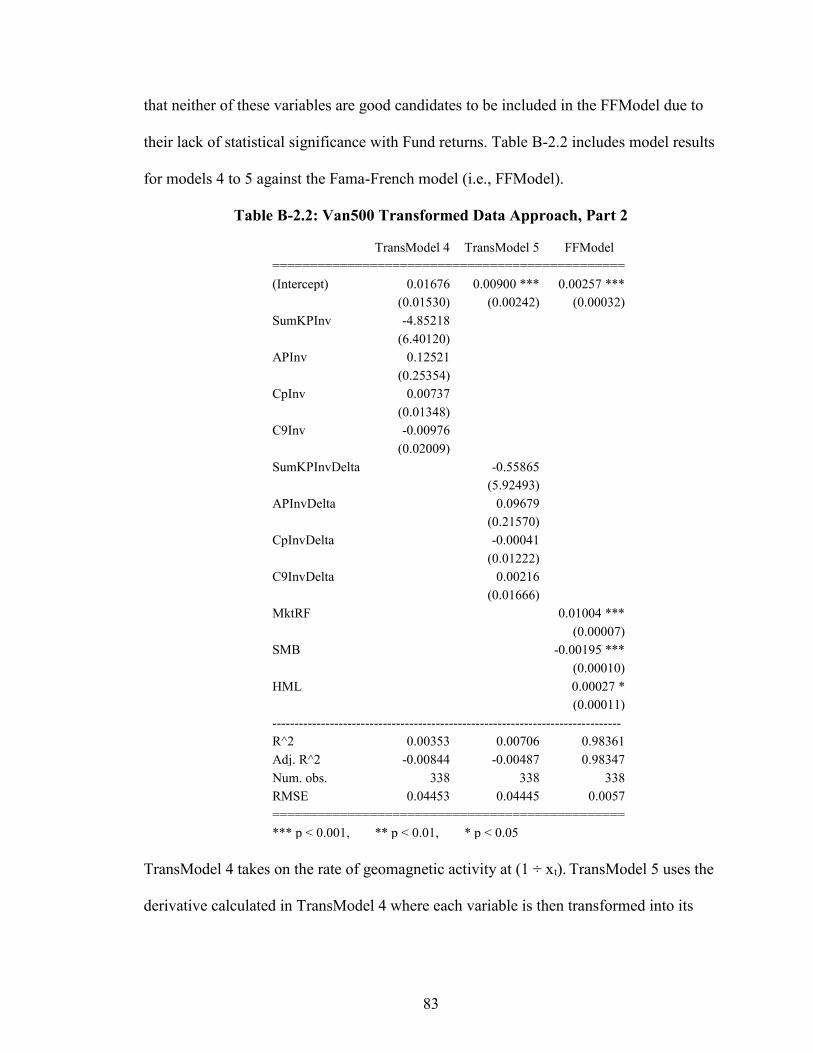

Table B-2.2: Van500 Transformed Data Approach, Part 2…………………………..….83

Table C-1: Results for Causality of Earth’s Magnetic Field and Human Economic

Behavior………………………………………………………………...…..……86

1

Chapter I

Introduction

The epic Sci-fi drama of George Lucas’s first Star Wars movie in May 1977 (Los

Angeles Times 2011) made headlines for decades with its subsequent releases thereafter.

The Star Wars story influenced ideas in science and technology—so much so, in fact, the

United States Government’s ballistic missile space defense system was nicknamed “Star

Wars” (Kreig 2008-2009: 1). What makes Star Wars an interesting topic in academia,

specifically within econometric modeling, is this quote from the 1977 movie by Obi-Wan

(Ben) Kenobi: “The Force is what gives a Jedi his power. It’s an energy field created by

all living things. It surrounds us and penetrates us. It binds the galaxy together” (IMDb

2016). Here, old Ben is describing natural phenomena influencing life—he is essentially

describing galactic magnetic fields (Han 2003: 3-12). Interestingly enough, the use of

natural phenomena in academic research has been investigated since the late nineteenth

century.

A multitude of researchers, from a variety of academic disciplines, researched (to

a limited extent) the influence of natural phenomena on the human body. In early

economic literature, scholars studied the interconnection between sunspot activity and

commercial collapses in addition to price fluctuations. Other studies have noted the

connection with sunspot activity, market behavior, and its use in equilibrium models.

Only recently, however, has some research investigated another natural phenomena

called the “Earth’s magnetic field” and its connection with political behavior that

2

potentially influences the outcome of market behavior in quantitative modeling (East

2014: 193-195). With such a colorful array of literature spanning physics to psychology,

however, this thesis will not continue to investigate how sunspot activity impacts

quantifiable societal outcomes, but use the natural phenomena of Earth’s magnetic field

to understand its influence and predictive power.

Research Questions

Since there is a research gap associating the Earth’s magnetic field with market

activity, this research will attempt to answer the following questions:

1. Although research has revealed the potential interconnection of geomagnetic

activity with market behavior, could this natural phenomena actually increase the

prediction power of quantitative models?

2. What about the human behavioral element—does that play a role in econometric

modeling?

Research Hypotheses

This research hypothesizes that, based on existing literature, the Earth’s magnetic

field might have a minute influence on improving quantifiable estimated outputs.

Although it can be hypothesized that magnetic activity could influence human economic

behavior, the use of the human behavioral element in econometric modeling might also

reveal some changes in predicted outputs. Despite the possibility of these variables

having some influence in quantitative estimation, the purpose of the thesis is to provide

grounded analysis for a better understanding of this research area—and contribute

3

meaningful findings that could give rise to new research areas outside the scope of

financial economics.

The thesis uses quantitative techniques to determine the variables’ possible impact

in estimated outputs. Additionally, this analysis relies on historical time-series data used

by an array of academic disciplines and institutions: such as geophysics, the social

sciences, and governmental agencies.

Research Significance

The significance of the final outcome in this research should reveal (a) the

relationships between or among the variables used in this research; (b) the influence of

geomagnetic activity in econometric outputs; (c) lastly, the impact of human economic

behavior, with and without geomagnetic activity, in quantitative estimation.

4

Chapter II

Definition of Terms

Chapter II defines all data used in this research. Applications, such as RStudio

(including packages) and Microsoft Excel, was utilized for data transformations,

adjustments, analysis, and storage:

Kp Index (abbreviation:“SumKp”): an independent variable of the Earth’s Magnetic

Field activity derived from the K Planetary Index which is transformed from its 3-

hourly range to a monthly average (NOAA 2016). Due to the lack of data quality from

the United States National Oceanic and Atmospheric Administration (NOAA), this data

was retrieved from the British Geological Survey in the United Kingdom. Chapter V

discusses additional transformations for this variable.

Ap Index (abbreviation:“Ap”): an independent variable measuring geomagnetic storm

events in a 24-hour time period derived from the Kp Index which aligns, to some

degree, with sunspot activity (NOAA 2016). For this research, the Index was

transformed to a monthly average. Due to the lack of data quality from the United

States National Oceanic and Atmospheric Administration (NOAA), this data was

retrieved from the British Geological Survey in the United Kingdom. The data is also

transformed using a variety of mathematical techniques to test its impact on market

activity—this is discussed later in Chapter V.

Cp & C9 Index (abbreviation:“Cp” & “C9”): both Cp and C9 are independent variables

measuring overall magnetic activity. The C9 Index, however, converts the Cp Index to

5

a single digit from 0 to 9 (Ivory 2016: 1). These variables were converted to a monthly

average for this research. Since this data is not provided by the United States National

Oceanic and Atmospheric Administration (NOAA) at the time of retrieval, the British

Geological Survey in the United Kingdom served as an access-point for this

information. Chapter V discusses additional transformations for these variable.

Personal Consumption Expenditure (abbreviation:“PerConsumEx”): an independent

human economic behavior variable representing spending on goods and services within

the United States. This data frequency is monthly and seasonally adjusted with

additional data transformations discussed in Chapter V. The information was retrieved

from the Federal Reserve Bank of St. Louis.

Velocity of M2 Money Stock (abbreviation:“ M2Money”): an independent human

economic behavior variable representing all U.S. currency in circulation which includes

investment, savings, and deposit accounts. The data frequency is monthly in billions of

U.S. Dollars and seasonally adjusted. This information was retrieved from the Federal

Reserve Bank of St. Louis. Additional data transformations were conducted for this

research study (See Chapter V).

Personal Savings Rate (abbreviation:“PerSavRate”): an independent human economic

behavior variable describing the percentage rate at which U.S. citizens save their

money from disposable income. This data has a monthly frequency, is seasonally

adjusted, and in billions of U.S. Dollars. The data was provided by the Federal Reserve

Bank of St. Louis. Additional data transformations were conducted for this research

study (See Chapter V).

6

Unemployment (abbreviation:“U3Unemploy”): an independent human economic

behavior variable that represents seasonally adjusted U-3 unemployment rate in the

United States. The data frequency is monthly and retrieved from the United States

Bureau of Labor of Statistics. Additional data transformations were conducted for this

research study (See Chapter V).

MktRF, SMB, HML, RMW, and CMA: independent variables representing factors used

in Fama-French’s model: such as MktRF, also abbreviated as (Rmt – Rft), which

represents the return for the New York Stock Exchange (NYSE), NASDAQ, and the

American Stock Exchange (AMEX) minus the U.S. Treasury Bill rate (at one month);

SMB reflects the mean return from a small portfolio minus large portfolios; HML is

calculated by subtracting the high book-to-market to the Small B/M value on value

portfolios and growth portfolios; RMW is calculated by subtracting two robust

portfolios from two weak operating portfolios in term of their mean return; lastly,

CMA’s calculation is similar to RMW, but considers the level of risk tolerance by

subtracting high and low risk portfolios (French 2016: 1). These variables were

retrieved from Kenneth French’s website at the Tuck School of Business, Dartmouth

College.

STT: a dependent variable representing State Street Corporation’s monthly closed-

adjusted stock price to incorporate dividends and splits (NYSE: STT). The data was

retrieved from Yahoo Finance.

Van500: a dependent variable representing Vanguard’s S&P 500 Index fund

(NASDAQ: VFINX) that closely tracks the S&P 500 Index. The fund consists of the

largest American corporations which accounts for 75% of the U.S. stock market’s value

7

(Vanguard 2016). The data frequency is monthly and incorporates adjusted closed

domestic stock price to account for dividends and splits. This data was retrieved from

Yahoo Finance.

8

Chapter III

Literature Review − Background of the Problem

The first academic literature documenting the Earth’s Magnetic Field was

published by William Gilbert in De Magnete. Gilbert (1600/1958) discussed the Earth’s

magnetic field as a force controlling the North and South Pole. In addition, Gilbert

(1600/1958) also explained how the geomagnetic field dictates the behavior of a

compass’s needle in terms of the true North, South, East, and West that is dependent on

the geographical location of the measurement being observed or recorded.

Lanza & Meloni (2006) has noted that the Earth’s magnetic field is divided into

three parts: (1) the internal field, also known as the Main Field; (2) the magnetosphere,

which is the external field; and (3) the ionosphere, which is responsible for global

variation in magnetism on Earth. Although the origins of the geomagnetic field are still

being studied, the Main Field is produced by the Earth’s fluid core; in addition, the

external field (i.e., magnetosphere) is produced by electric currents protecting Earth from

solar wind dictated by the Sun’s behavior (Lanza & Meloni 2006: 1). According to the

National Oceanic and Atmospheric Administration (NOAA), the Earth’s magnetic field is

measured by the following:

declination (D), inclination (I), horizontal intensity (H), the north (X) and

east (Y) components of the horizontal intensity, vertical intensity (Z), and

total intensity (F). The parameters describing the direction of the magnetic

field are declination (D) and inclination (I). D and I are measured in units

of degrees, positive east for D and positive down for I. The intensity of the

total field (F) is described by the horizontal component (H), vertical

component (Z), and the north (X) and east (Y) components of the

9

horizontal intensity. These components may be measured in units of gauss

but are generally reported in nanoTesla (1nT * 100,000 = 1 gauss). The

Earth’s magnetic field intensity is roughly between 25,000 - 65,000 nT (.25

- .65 gauss). Magnetic declination is the angle between magnetic north and

true north. D is considered positive when the angle measured is east of true

north and negative when west. Magnetic inclination is the angle between

the horizontal plane and the total field vector, measured positive into Earth.

In older literature, the term “magnetic elements” often referred to D, I, and

H (NOAA 2016).

NOAA (2016) also measures the magnetic field with indices: such as [K], [KP], and

[AP]; the [K] Index represents a 3 hour range of magnetic activity; the [KP] Index is a

planetary mean measurement of the [K] Index; the [AP] Index is similar to the [KP]

Index in that it measures the earliest maximum value in a 24-hour time period. Lastly, the

[Cp] Index is a qualitative estimate of overall magnetic activity, which aggregates daily

[AP] measurements—this index also has a counterpart called the [C9] Index that converts

the [Cp] Index to one digit ranging from 0 to 9 (Ivory 2016: 1). With this knowledge, the

question is: how influential could magnetic activity be in quantitative modeling? Since

there is limited information on the subject, history has shown that researchers have used

natural phenomena in a variety of studies.

Hyde Clarke’s “A Preliminary Inquiry into the Physical Laws Governing the

Periods of Famines and Panics” was one of the first publications describing how a natural

phenomenon could be interconnected with economic activity. After Clarke (1847)

introduced the concept of “physical economy,” he compared cycles of crops including

price fluctuations, famine periods, the influence of solar and lunar winds on Earth’s

weather, and harvest periods. The result was that speculation, famine, and panic can

occur in roughly ten or eleven year intervals (Clarke 1847: 157). Outside factors, such as

10

solar and lunar winds influencing weather trends on Earth leading to economic

fluctuations, prompted an investigation into the physical laws of sunspot behavior.

In “Commercial Crisis and Sun-Spots,” Jevons referenced Hyde Clarke’s

exploration on how nature can influence economic outcomes. Jevons (1878) focused his

research on sunspot activity and commercial collapses; the end result from his study

revealed a 10.8 year interval in the commercial collapse timeline of 1825, 1836-9, 1847,

1857, and 1866; when comparing that interval with the duration of sunspot activity, the

results revealed a difference of 0.3.1 The discovery of business cycles linking with

sunspot activity led to a quantitative standard in the twentieth century.

“Do Sunspots Matter?” introduced the sunspot equilibrium formulated by Karl

Shell and David Cass in response to the 1878 study by Jevons. The purpose of this

equilibrium model was to deviate away from the traditional models that yielded certainty

equilibria to a broader and more non-traditional approach (Shell and Cass 1983: 195).

Shell and Cass’s final overall result was that sunspots are an extrinsic random variable

that do not influence general economic principles; the equilibrium, however, can offer an

explanation of excess volatility.

Bizer et al. (2014) produced one of the first and most recent experimental studies

which explored strategic coordination and sunspot activity in economic forecasting. The

final result was that accurate predictions were finite with low payoffs under this model.

1 The commercial collapse interval (10.8) was deducted by the sunspot interval

(10.5). This calculation was intended to show the difference between actual verses

predicted results.

11

Bizer et al. (2014) suggested that more research should be conducted to reduce herding

for forecasters to support anti-herding.

“Sunspots, GDP, and the Stock Market” used raw data from the National

Aeronautics and Space Administration (NASA) that recorded the number of sunspots

over time. They analyzed the moving average of sunspot behavior, the Dow Jones

Industrial Average (DJIA), and the U.S. gross domestic product. The concluding results

were that the correlation between these variables is insignificant. Modis (2007), however,

noted that sunspot activity and its unusual similarity with the DJIA and U.S. GDP

warrants further investigation by scholars.

Russian academics Belkin & Poluyakhtov investigated the relationship between

solar activity cycles (i.e., sunspots), real U.S. GDP, and interest rates in “Unconventional

Cyclical Theory: Cyclical Solar Activity and the Cyclical Development of the Economy.”

Data used in their research was the annual indexes of real U.S. GDP and the number of

Wolf W—an indicator of solar activity. Belkin & Poluyakhtov (2011) analyzed extreme

deviations from the mean solar cycle activity including maximums and minimums in

correlation with GDP and interest rate growth. Belkin & Poluyakhtov (2011) concluded

that solar activity and interest rates appear to be correlated with a coefficient of 79%. In

addition, the authors (2011) also noted a possible economic decline from 2013-2015.

“Unemployment, and Recessions, or Can the Solar Activity Cycle Shape the Business

Cycle?” revisited solar activity maximums and their correlation with U.S. recessions—

roughly seven solar maximums revealed eight out of thirteen recessions plus low U.S

unemployment being preceded by six solar maximums with a rapid increase of

unemployment following a two to three year lag. Gorbanev (2012) methodology used

12

monthly data of sunspot numbers from the National Aeronautics and Space

Administration (NASA) and the U.S. National Oceanic and Atmospheric Administration

(NOAA).

In 2014, Jakie R. East published the first political science dissertation on how

natural phenomena, such as the Sun and Earth, could not only have a connection with

economics, but human behavior entitled “Natural Phenomena as Potential Influence on

Social and Political Behavior: The Earth’s Magnetic Field.” East’s ( 2014) dissertation

analyzed the baseline relationship between geomagnetic frequencies and an array of

societal outcomes within several social science disciplines.

For Political Science and Criminology, East (2014) illustrated that one area of the

natural phenomena effect on human behavior was expressed by the “opportunity and

motivation theory” under SAD (Seasonal Affective Disorder), where higher temperatures

correlates with less crime and the lack of sunlight is associated with depression and

suicide that influences the melatonin and serotonin areas of the brain (East 2014: 14-15).

Sociology, Psychology, and Biology has predominantly used a number of natural

phenomena variables to explain human behavior derived from Charles Darwin’s idea of

natural selection (East 2014: 16-17). For example, East (2014) noted that the New

Ecological Paradigm (NEP) uses natural phenomena variables to explain how human

behavior might be influenced by this environment (East 2014: 17). In addition, subfields

of psychology, such as environmental and evolutionary, examines how human behavior

and the environment interact with each other (East 2014: 17-18).

Although Economics has not heavily researched how geophysical variables are

interconnected with human behavior, which in turn, to some degree, could influence

13

market fluctuations, East (2014) analyzed how the Earth’s magnetic field could explain

swings in market prices. More specifically, for daily low & high numbers in the stock

market, an escalation in the [y] and [h] component of the magnetic field tends to increase

the distance between high and low numbers (East 2014: 193). In addition, East (2014)

also used the AP Index of the magnetic field to refine a model that analyzes U.S.

Presidential messages and its influence on the Dow Jones Industrial Average (DJIA) and

the National Association of Securities Dealers Automated Quotations (NASDAQ) index;

in East’s (2014) analysis, the magnetic variable did, in fact, slightly refine Martin’s (2008)

model (East 2014: 197-200).

Other literature, authored by Babayev & Allahverdiyeva (2007), noted that severe

magnetic disturbances can cause negative human emotional responses. Palmer, Rycroft,

and Cermack (2006) revealed that extreme low or high geomagnetic activity could affect

melatonin levels and cardiovascular health. Karasek et al. (1998) also published a study

revealing the effect of magnetic fields on melatonin levels within the human brain. East

(2014) also cited the interconnection between magnetic activity and the human brain’s

melatonin and serotonin levels. To better understand how both natural phenomena (i.e.,

magnetic activity) and human behavior could potentially influence outputs in quantitative

modeling, the Fama-French model is reviewed.

William F. Sharpe introduced the theory of the Capital Pricing Asset Model

(CAPM) in 1964 entitled “Capital Asset Prices: A Theory of Market Equilibrium under

Conditions of Risk,” with later contributions by John Linter (1965a, b), Jack Treynor

(1962), and Jan Mossin (1966); the CAPM model is described as:

Er= rf + βi(Em – rf) (1)

14

where:

Es = Expected return,

Rf = Risk free rate,

βi = Sensitive of a security,

Em = Expected market return,

(Em – rf) = Risk premium.

This model calculates the expected (predicted) return of a security or portfolio. In

equilibrium, the total risk is not priced—instead, it is market risk (systematic); in addition

the model also takes on specific risk (i.e., β)—meaning risk of the asset being estimated.

CAPM eventually became a benchmark for later quantitative equations to estimate

(predict) possible returns.

Following the contribution from Sharpe (1964), Linter (1965a, b), Treynor

(1962), and Mossin (1966) was the introduction of the three-factor model by Eugene

Fama and Kenneth French (1992, 1993) extending the CAPM model; the Fama-French

(1992, 1993) regression model is represented by the following equation:

Rit – Rft = αi + βi(Rmt – Rft) + siSMB +hiHMLt +ϵit ;

t = 1, 2..T for each i = 1, 2…N (2)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

Rft = Risk free return;

Rmt = Return on the value-weighted market portfolio;

βi = Sensitive of a security;

siSMB = Small minus big;

hiHMLt = High minus low B/M;

ϵit = Standard error of the estimate.

The extension of the CAPM model by Fama and French (1992, 1993) added two more

betas (β) to the equation: SMB and HML. HML (β2) is calculated by subtracting the high

15

book-to-market to the Small B/M value. The theory behind this Fama and French’s

(1992, 1993) beta allows the model to recognize additional risk exposure between growth

and valued stocks. For SMB (β3), this is calculated by the difference between small and

large stocks—Fama and French’s (1992, 1993) calculation is essentially trying to explain

excess returns on a portfolio by market capitalization making this beta a measure of size

risk—meaning that smaller firms are exposed to more risk due to their lack of

diversification.

Overall, these models are designed to predict an outcome based on market

behavior. Since there is literature suggesting the interconnection with geomagnetic

activity and its influence on human behavior, could this natural phenomena actually

increase the prediction power of this model? What about the human element—does that

play a role in econometric modeling? This research will attempt to answer these

questions and provide grounded analysis for real-world model owners.

16

Chapter IV

Research Methodology

The research design will use a scenario analysis with differing categories: such as

a direct, indirect, and alternative quantitative modeling approach for the Fama-French 3-

factor model—this analyzes any improvement of the original model’s prediction

capabilities—and investigates the possible impact of the added variables on expected

returns without the Fama-French’s 3-Factor Model. The output of expected (predicated)

returns also incorporates a two-fold comparative analysis for model performance—this

includes single stock returns (i.e., State Street Corporation) and fund returns representing

500 of America’s largest corporations closely tracking the S&P 500 Index (i.e., Vanguard

S&P 500 Index Fund). The reason for using the Vanguard S&P 500 Fund is because the

Fama-French model typically performs much stronger compared to the use of a single

stock due to most of the 3-factors being constructed on a microeconomic level—the Fund

is also used to better understand how added variables behave in a larger market

environment. These assets are analyzed to determine if the modeling approaches

mentioned below increase estimation performance of the original Fama-French output.

The following is the direct approach equation:

Rit = αi + βi(Rmt – Rft) + siSMB +hiHMLt + β4it + β5it + β6it + ϵit ;

t = 1, 2..T for each i = 1, 2…N (3)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

Rft = Risk free return;

17

Rmt = Return on the value-weighted market portfolio;

βi = Sensitive of a security;

siSMB = Small minus big;

hiHMLt = High minus low B/M;

β4it = SumKp activity for period t;

β5it = AP activity for period t;

β6it = Cp activity for period t;

ϵit = Standard error of the estimate.

The direct approach equation with human economic behavior variables is as follows:

Rit = αi + βi(Rmt – Rft) + siSMB +hiHMLt + β4it + β5it + β6it + β7it + β8it + β9it +

β10it + ϵit ; t = 1, 2..T for each i = 1, 2…N (4)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

Rft = Risk free return;

Rmt = Return on the value-weighted market portfolio;

βi = Sensitive of a security;

siSMB = Small minus big;

hiHMLt = High minus low B/M;

β4it = SumKp activity for period t;

β5it = AP activity for period t;

β6it = Cp activity for period t;

β7it = Personal Consumption Expenditure for period t;

β8it = Velocity of M2 Money Stock for period t;

β9it = Personal Savings Rate for period t;

β10it = U-3 Unemployment for period t;

ϵit = Standard error of the estimate.

Alternative Model 1 Equation:

Rit = αi + βi(Rmt – Rft) + siSMB +hiHMLt + ∆β4it + ∆β5it + ∆β6it + ϵit ;

t = 1, 2..T for each i = 1, 2…N (5)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

Rft = Risk free return;

18

Rmt = Return on the value-weighted market portfolio;

βi = Sensitive of a security;

siSMB = Small minus big;

hiHMLt = High minus low B/M;

∆β4it = SumKp activity for period t;

∆β5it = AP activity for period t;

∆β6it = Cp activity for period t;

ϵit = Standard error of the estimate.

Alternative Model 2 Equation:

Rit = αi + βi(Rmt – Rft) + siSMB +hiHMLt + ∆β4it + ∆β5it + ∆β6it + ∆β7it + ∆β8it

+ ∆β9it + ∆β10it + ϵit ; t = 1, 2..T for each i = 1, 2…N (6)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

Rft = Risk free return;

Rmt = Return on the value-weighted market portfolio;

βi = Sensitive of a security;

siSMB = Small minus big;

hiHMLt = High minus low B/M;

∆β4it = SumKp activity for period t;

∆β5it = AP activity for period t;

∆β6it = Cp activity for period t;

∆β7it = Personal Consumption Expenditure for period t;

∆β8it = Velocity of M2 Money Stock for period t;

∆β9it = Personal Savings Rate for period t;

∆β10it = U-3 Unemployment for period t;

ϵit = Standard error of the estimate.

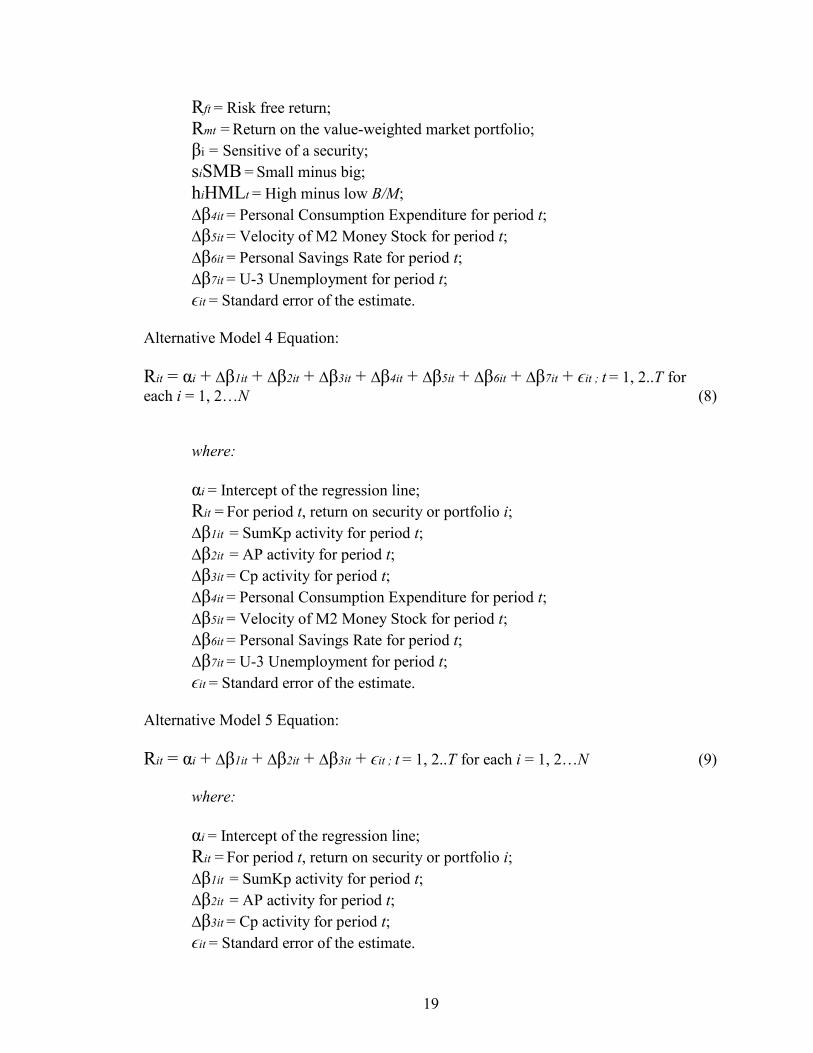

Alternative Model 3 Equation:

Rit = αi + βi(Rmt – Rft) + siSMB +hiHMLt + ∆β4it + ∆β5it + ∆β6it + ∆β7it + ϵit ; t =

1, 2..T for each i = 1, 2…N (7)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

19

Rft = Risk free return;

Rmt = Return on the value-weighted market portfolio;

βi = Sensitive of a security;

siSMB = Small minus big;

hiHMLt = High minus low B/M;

∆β4it = Personal Consumption Expenditure for period t;

∆β5it = Velocity of M2 Money Stock for period t;

∆β6it = Personal Savings Rate for period t;

∆β7it = U-3 Unemployment for period t;

ϵit = Standard error of the estimate.

Alternative Model 4 Equation:

Rit = αi + ∆β1it + ∆β2it + ∆β3it + ∆β4it + ∆β5it + ∆β6it + ∆β7it + ϵit ; t = 1, 2..T for

each i = 1, 2…N (8)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

∆β1it = SumKp activity for period t;

∆β2it = AP activity for period t;

∆β3it = Cp activity for period t;

∆β4it = Personal Consumption Expenditure for period t;

∆β5it = Velocity of M2 Money Stock for period t;

∆β6it = Personal Savings Rate for period t;

∆β7it = U-3 Unemployment for period t;

ϵit = Standard error of the estimate.

Alternative Model 5 Equation:

Rit = αi + ∆β1it + ∆β2it + ∆β3it + ϵit ; t = 1, 2..T for each i = 1, 2…N (9)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

∆β1it = SumKp activity for period t;

∆β2it = AP activity for period t;

∆β3it = Cp activity for period t;

ϵit = Standard error of the estimate.

20

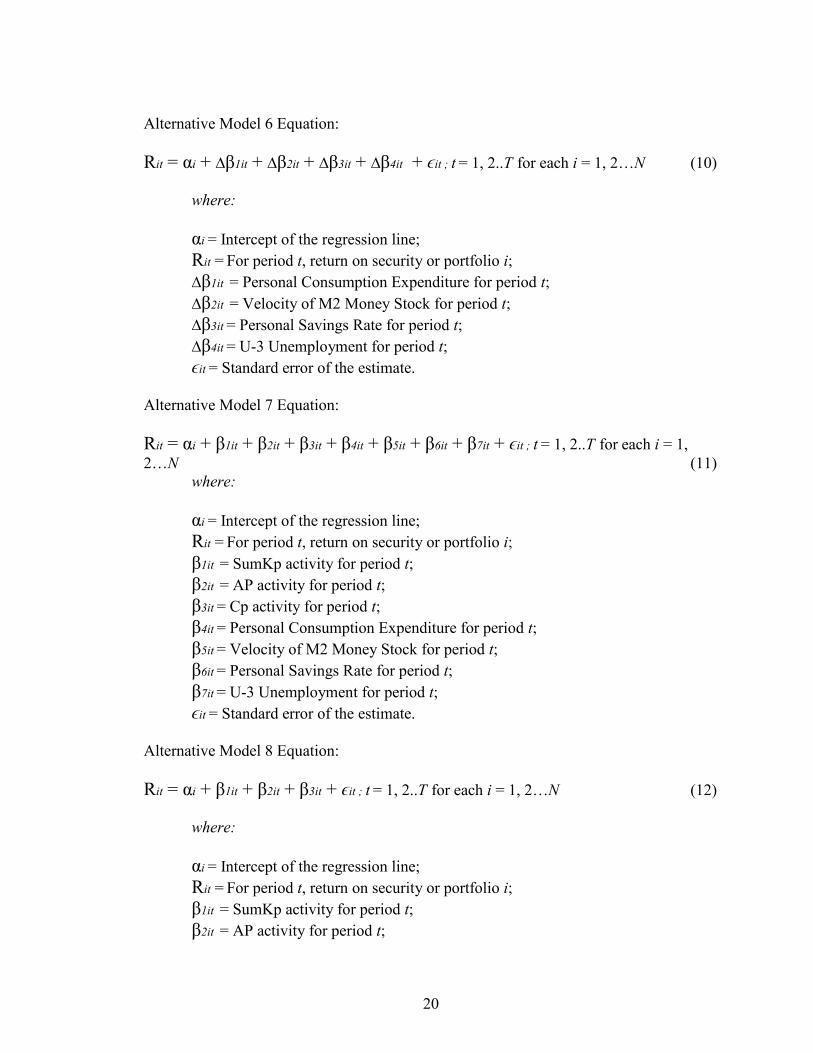

Alternative Model 6 Equation:

Rit = αi + ∆β1it + ∆β2it + ∆β3it + ∆β4it + ϵit ; t = 1, 2..T for each i = 1, 2…N (10)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

∆β1it = Personal Consumption Expenditure for period t;

∆β2it = Velocity of M2 Money Stock for period t;

∆β3it = Personal Savings Rate for period t;

∆β4it = U-3 Unemployment for period t;

ϵit = Standard error of the estimate.

Alternative Model 7 Equation:

Rit = αi + β1it + β2it + β3it + β4it + β5it + β6it + β7it + ϵit ; t = 1, 2..T for each i = 1,

2…N (11) where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

β1it = SumKp activity for period t;

β2it = AP activity for period t;

β3it = Cp activity for period t;

β4it = Personal Consumption Expenditure for period t;

β5it = Velocity of M2 Money Stock for period t;

β6it = Personal Savings Rate for period t;

β7it = U-3 Unemployment for period t;

ϵit = Standard error of the estimate.

Alternative Model 8 Equation:

Rit = αi + β1it + β2it + β3it + ϵit ; t = 1, 2..T for each i = 1, 2…N (12)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

β1it = SumKp activity for period t;

β2it = AP activity for period t;

21

β3it = Cp activity for period t;

ϵit = Standard error of the estimate.

Alternative Model 9 Equation:

Rit = αi + β1it + β2it + β3it + β4it + ϵit ; t = 1, 2..T for each i = 1, 2…N (13)

where:

αi = Intercept of the regression line;

Rit = For period t, return on security or portfolio i;

β1it = Personal Consumption Expenditure for period t;

β2it = Velocity of M2 Money Stock for period t;

β3it = Personal Savings Rate for period t;

β4it = U-3 Unemployment for period t;

ϵit = Standard error of the estimate.

In addition to the original modeling approach noted above, the research also utilizes two

other frameworks: such as the data transformation and exponential moving average

(EMA) approach. The transformation approach (see Appendix B) uses existing data to

better understand if any real impact may be viable for quantitative estimation; the data

transformation approach, however, will not use models located in the original approach.

Moreover, since geomagnetic data tends to be noisy, added betas are re-calculated to their

EMA form—human economic behavioral data is also transformed to understand their

impact in quantitative estimation. In addition, since both Cp and C9 are measurements of

the same geomagnetic frequency (with differing approaches), only Cp is utilized due to a

slight positive correlation increase with State Street stock returns—the same approach is

also applied to the Vanguard S&P 500 Fund. Lastly, data is correlated, using Pearson’s

correlation, to determine if any relationships exists between or among independent and

dependent variables (see Appendix D & E).

22

The variable selection process will have a p-value cap of 5%; a variance inflation

factor (VIF) analysis is also conducted to ensure that the selected variables are not

inflating model fitness metrics and to reduce multicollinearity; if a VIF analysis reveals

severe inflation, the removal of the variable will likely occur. Autocorrelation will be

addressed on a case-by-case basis—if severity is detected, generalized least square

regression or dependent variable differencing might occur. Data with the strongest

dependent variable relationship and model fit is tested against the Fama-French’s original

model (see Chapter VIII) to determine if there is any quantitative estimation

improvement—this includes conducting an analysis comparing actual verses estimated

outcomes to determine the model’s true reliability of predicted returns. Additionally, a

robustness analysis, during the 2008-2009 Financial Crisis, is used to test whether the

selected models can predict swings in the market. Lastly, human economic behavioral

and geomagnetic variables are tested for causality using the Granger test (see Appendix

C)—this is to determine if there are any underlying relationships among human

behavioral economic and geomagnetic variables (Granger 1988: 199-211). Although it is

not known if these variables reveal a relationship with each other for a predicted

outcome, it could be hypothesized that the unknown and known measurement error for

the time-series regression models should not reveal a significance of - 0 -.

23

Chapter V

Data Transformations

All variables used in Chapter II have undergone data transformations outside the

scope of absolute delta to better understand their impact in predicting returns; although a

select number of variables have already undergone a seasonality transformation from

their original source, this research did not adjust for seasonality. Table 5-1 below

illustrates the equation used to transform each independent variable including its name

and variable description ranging from September 1986 to November 2014.

Table 5-1: Data Transformations

Variable Name Variable

Equation Variable Description

PerConsumExDelta X2t - X1t

Personal Consumptions Expenditure transformed to express

the change (∆) from the current rate in time X2t minus the

previous rate X1t.

M2MoneyDelta X2t - X1t Velocity of Money transformed to express the change (∆)

from the current rate in time X2t minus the previous rate X1t.

PerSavDelta X2t - X1t Personal Savings Rate transformed to express the change (∆)

from the current rate in time X2t minus the previous rate X1t.

U3UnemployDelta X2t - X1t

U-3 unemployment rate transformed to express the change

(∆) from the current rate in time X2t minus the previous rate

X1t.

Kppwhalf √Xt The KP Index datum is square-rooted .

KPLN Ln(Xt) The KP Index datum transformed to its natural-logarithm.

SumKPDelta X2t - X1t The KP Index transformed to express the change (∆) from the

current rate in time X2t minus the previous rate X1t.

SumKPInv 1 ÷ Xt 1 divides the KP Index datum.

SumKPInvDelta X2t - X1t The derivative of SumKPInv transformed to express the

change (∆) from the current rate in time X2t minus the

24

previous rate X1t.

Appw8 Xt(1/0.8) The AP Index datum is squared by 1/0.8.

ApLn Ln(Xt) The AP Index datum transformed to its natural-logarithm.

APSqrt √ Xt The AP Index datum square-rooted for the data series.

APDelta X2t - X1t

The AP Index data series transformed to express the change

(∆) from the current rate in time X2t minus the previous rate

X1t.

APInv 1 ÷ Xt 1 divides the AP Index datum.

APInvDelta X2t - X1t

The derivative of APInv transformed to express the change

(∆) from the current rate in time X2t minus the previous rate

X1t.

Cppwnine Xt(1/9) The CP Index datum is squared by 1/9.

CpLn Ln(Xt) The CP Index datum transformed to its natural-logarithm.

CpSqrt √ Xt The CP Index datum square-rooted for the data series.

CPDelta X2t - X1t

The CP Index data series transformed to express the change

(∆) from the current rate in time X2t minus the previous rate

X1t.

CpInv 1 ÷ Xt 1 divides the CP index datum.

CpInvDelta X2t - X1t

The derivative of CpInv transformed to express the change

(∆) from the current rate in time X2t minus the previous rate

X1t.

C9pwsqurt Xt(2) The C9 Index datum is squared.

C9Ln Ln(Xt) The C9 Index datum transformed to its natural-logarithm.

C9Squrt √ Xt The C9 Index datum square-rooted for the data series.

C9Delta X2t - X1t

The C9 Index data series transformed to express the change

(∆) from the current rate in time X2t minus the previous rate

X1t.

C9Inv 1 ÷ Xt 1 divides the C9 Index datum.

C9InvDelta X2t - X1t

The derivative of C9Inv transformed to express the change

(∆) from the current rate in time X2t minus the previous rate

X1t.

25

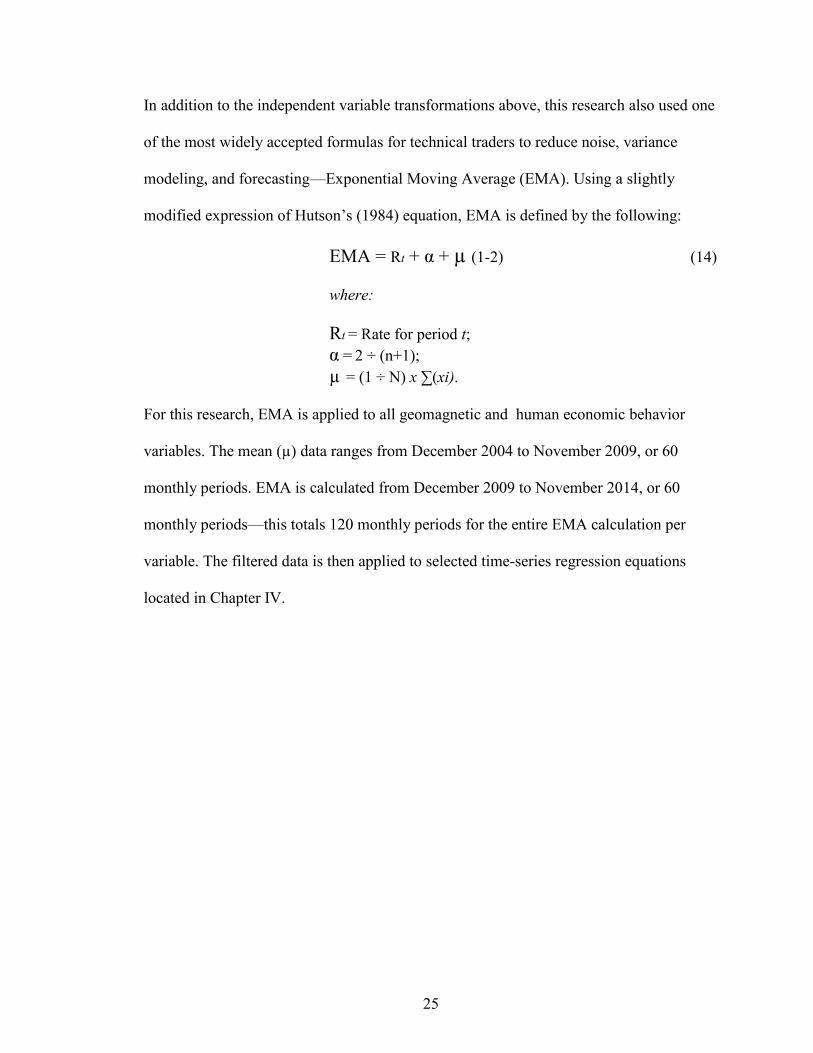

In addition to the independent variable transformations above, this research also used one

of the most widely accepted formulas for technical traders to reduce noise, variance

modeling, and forecasting—Exponential Moving Average (EMA). Using a slightly

modified expression of Hutson’s (1984) equation, EMA is defined by the following:

EMA = Rt + α + µ (1-2) (14)

where:

Rt = Rate for period t;

α = 2 ÷ (n+1);

µ = (1 ÷ N) x ∑(xi).

For this research, EMA is applied to all geomagnetic and human economic behavior

variables. The mean (µ) data ranges from December 2004 to November 2009, or 60

monthly periods. EMA is calculated from December 2009 to November 2014, or 60

monthly periods—this totals 120 monthly periods for the entire EMA calculation per

variable. The filtered data is then applied to selected time-series regression equations

located in Chapter IV.

26

Chapter VI

Limitations

This research design is limited by advanced knowledge of geophysics. Since there

are multiple variables involved outside the scope of this design, it would be improbable

to identity every aspect and element influencing the research outcome. Moreover, the use

of more advanced quantitative techniques, such as vector autoregression (VAR)

modeling, is limited. Research limitations may also extends to medical and psychology

research used to evaluate and explain human behavior. In addition, this research is

limited to the 13 observatories measuring magnetic activity worldwide. Human economic

behavior data is limited to the United States. Data quality is limited to selected sources

mentioned in this research and cannot guarantee 100% accuracy of the raw data used.

The processing component is limited to least squares regression due to Fama and

French’s methodology choice; moreover, time-series data is not adjusted for lag. Models

that use Fama-French factors may only be applied to the equities market, or funds

constructed with stocks due to the research approach used. If the model(s) does not

include Fama-French factors, this research may only be applied to asset classes being

bought or sold in economies comparable with the United States—this is due to the nature

of the data being used in the analysis.

27

Chapter VII

Quantitative Modeling with Returns

Chapter VII is comprised of all time-series regression model approaches using

data in the original approach illustrated on Chapter IV and EMA filtered data for both

State Street Corporation’s stock and the Vanguard S&P 500 Index Fund percent-returns;

correlation matrices are located in Appendix D to E.

Original Approach: State Street Corporation Stock Returns

This section uses all equations (3 – 13) located in Chapter IV. After all regression

outputs have been calculated with the selected data, the model’s parameters maybe

modified (if applicable) to meet the cut-off p-value of any measurement over 5%. The

monthly time-series range is from October 1986 to November 2014. The first table

reveals regression results for the Direct Model Equation 3 (“DirectModel”) and the

direct model with human economic behavior variables, Equation 4 (“DirectModelEcon”)

compared with the Fama-French model (“FFModel”) using State Street Corporation

adjusted stock returns. For variable elimination, the focus of the regression output

includes the following: (i) Adj. R2, (ii) RMSE (root-mean-squared-error), and (iii) p-

values (0.1%, 1%, or 5%). A variance inflation factor (VIF) analysis will typically occur

after the model’s parameters have been adjusted.

28

Table 7-1: STT Original Model Regression Results, Part 1

In both the DirectModel and DirectModelEcon, added variables have reduced the

models’ goodness-of-fit compared the FFModel by the decrease in Adj. R2. In addition,

RMSE has increased compared to the FFModel which suggests that these models have

less predictability. All added variables compared to the original FFModel have a p-value

above 5% regardless if they were tested separately or together—this suggests a weak

relationship with State Street Corporation’s stock return. In the DirectModel equation,

aggregating all geomagnetic indices creates multicollinearity with variance inflation

factors (VIF) ranging from 14 (min) to 502 (max). DirectModelEcon, which includes

both geomagnetic and human economic variables, revealed that the economic parameters

DirectModel DirectModelEcon FFModel

===============================================

(Intercept) 0.23272 0.97533 -0.06705

(0.86118) (1.29853) (0.13014)

MktRF 0.36905 *** 0.37291 *** 0.36832 ***

(0.02981) (0.02994) (0.02967)

SMB -0.09371 * -0.09492 * -0.09350 *

(0.04258) (0.04299) (0.04236)

HML 0.21288 *** 0.21666 *** 0.21147 ***

(0.04670) (0.04671) (0.04613)

SumKp -0.01097 -0.00385

(0.01889) (0.01983)

Ap 0.00214 -0.00456

(0.06268) (0.06380)

Cp 2.75657 1.81069

(4.86835) (5.10027)

PerConsumEx -0.00029

(0.00031)

M2Money 0.0004

(0.00031)

PerSavRate -0.11966

(0.14328)

U3Unemploy -0.13806

(0.12954)

-------------------------------------------------------------------------------

R^2 0.32797 0.33967 0.32647

Adj. R^2 0.31579 0.31948 0.32042

Num. obs. 338 338 338

RMSE 2.3617 2.35532 2.3537

===============================================

*** p < 0.001, ** p < 0.01, * p < 0.05

29

have inflation factors at 49 and 40 for personal consumption expeditors (PerConsumEx)

including money velocity (M2Money)—the results suggest that severe multicollinearity

exists when these parameters are used. The Fama-French model is the best model for

predicting State Street stock returns under this scenario based on Adj. R2, RMSE, and

probability values. Table 7-2 displays results for models 1 to 3 which includes the

absolute change (delta) in both geomagnetic and human economic behavior.

Table 7-2: STT Original Model Regression Results, Part 2

Model 1 Model 2 Model 3 FFModel

==========================================================

(Intercept) -0.06662 -0.05318 0.15167 -0.06705

(0.13064) (0.21847) (0.59268) (0.13014)

MktRF 0.36615 *** 0.36058 *** 0.36019 *** 0.36832 ***

(0.02995) (0.03035) (0.08190) (0.02967)

SMB -0.09061 * -0.10563 * 0.04623 -0.09350 *

(0.04272) (0.04336) (0.11671) (0.04236)

HML 0.21403 *** 0.20961 *** 0.31496 * 0.21147 ***

(0.04669) (0.04716) (0.12686) (0.04613)

SumKPDelta -0.00727 -0.00953

(0.02919) (0.02930)

APDelta -0.01159 -0.00677

(0.05243) (0.05248)

CPDelta 1.38283 1.73015

(6.10560) (6.12231)

PerConsumExDelta 0.00619 -0.01094

(0.00446) (0.01206)

M2MoneyDelta -0.00652 0.01342

(0.00471) (0.01270)

PerSavDelta 0.00559 -0.17342

(0.16921) (0.45808)

U3UnemployDelta 0.68023 -2.66238

(0.84619) (2.28092)

--------------------------------------------------------------------------------------------------

R^2 0.32746 0.33676 0.07174 0.32647

Adj. R^2 0.31527 0.31648 0.05211 0.32042

Num. obs. 338 338 339 338

RMSE 2.3626 2.36052 6.40795 2.3537

==========================================================

*** p < 0.001, **p < 0.01, * p < 0.05

Both models 1 and 2 has decreased performance compared to the Fama-French

model. Multicollinearity exists when geomagnetic indices are used in Model 1: such as

30

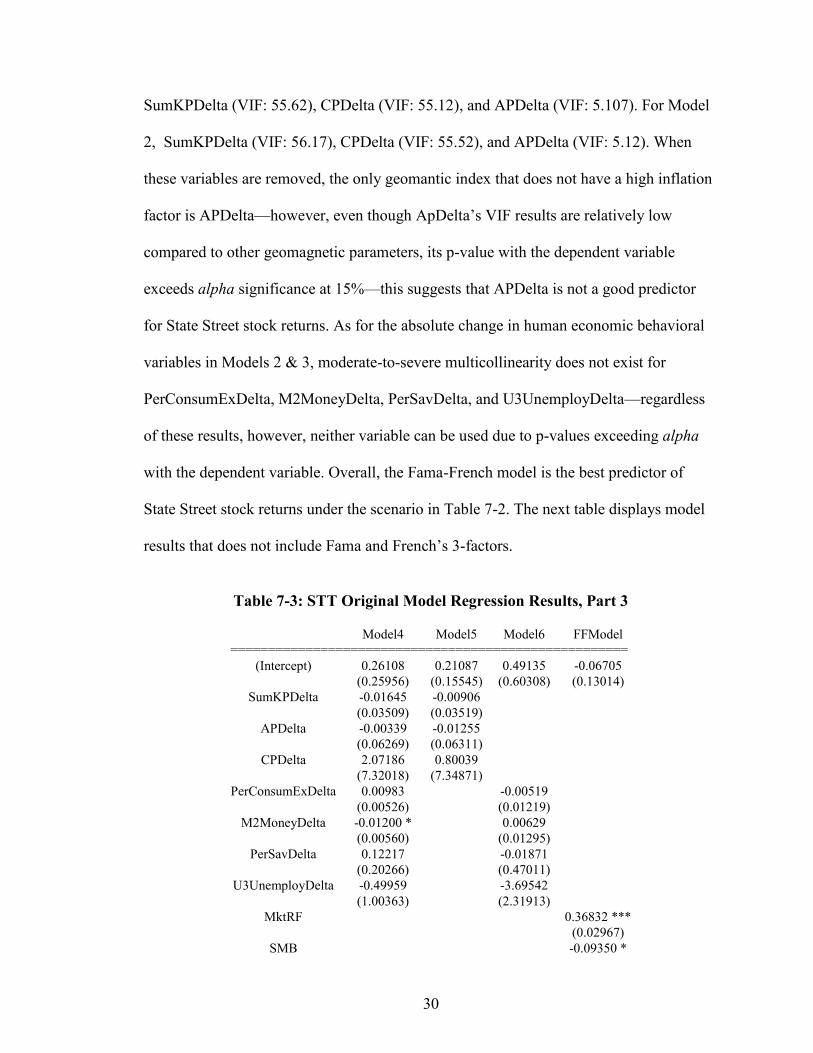

SumKPDelta (VIF: 55.62), CPDelta (VIF: 55.12), and APDelta (VIF: 5.107). For Model

2, SumKPDelta (VIF: 56.17), CPDelta (VIF: 55.52), and APDelta (VIF: 5.12). When

these variables are removed, the only geomantic index that does not have a high inflation

factor is APDelta—however, even though ApDelta’s VIF results are relatively low

compared to other geomagnetic parameters, its p-value with the dependent variable

exceeds alpha significance at 15%—this suggests that APDelta is not a good predictor

for State Street stock returns. As for the absolute change in human economic behavioral

variables in Models 2 & 3, moderate-to-severe multicollinearity does not exist for

PerConsumExDelta, M2MoneyDelta, PerSavDelta, and U3UnemployDelta—regardless

of these results, however, neither variable can be used due to p-values exceeding alpha

with the dependent variable. Overall, the Fama-French model is the best predictor of

State Street stock returns under the scenario in Table 7-2. The next table displays model

results that does not include Fama and French’s 3-factors.

Table 7-3: STT Original Model Regression Results, Part 3

Model4 Model5 Model6 FFModel

=====================================================

(Intercept) 0.26108 0.21087 0.49135 -0.06705

(0.25956) (0.15545) (0.60308) (0.13014)

SumKPDelta -0.01645 -0.00906

(0.03509) (0.03519)

APDelta -0.00339 -0.01255

(0.06269) (0.06311)

CPDelta 2.07186 0.80039

(7.32018) (7.34871)

PerConsumExDelta 0.00983 -0.00519

(0.00526) (0.01219)

M2MoneyDelta -0.01200 * 0.00629

(0.00560) (0.01295)

PerSavDelta 0.12217 -0.01871

(0.20266) (0.47011)

U3UnemployDelta -0.49959 -3.69542

(1.00363) (2.31913)

MktRF 0.36832 ***

(0.02967)

SMB -0.09350 *

31

The absolute change (delta) in geomagnetic activity, defined by SumKPDelta,

APDelta, CPDelta, and C9Delta under Model 5, does not have a deterministic

relationship with State Street Corporation’s stock returns based on probability values.

The change in human economic behavior variables, defined under Model 4 and 6 by

PerConsumExDelta (Personal Consumptions Rate), M2MoneyDelta (Money Velocity),

PerSavDelta (Personal Savings Rate), and U3UnemployDelta (U-3 Unemployment), does

not have probability significance with the dependent variable except M2MoneyDelta

(Money Velocity); this parameter, as illustrated on Table 7-4, has a p-value of 2.1% with

the dependent variable making the relationship significant.

Table 7-4: STT Money Velocity Relationship Test

The table below displays a comparison of the adjusted Fama-French Model

(AdjFFModel), which includes M2MoneyDelta and the original model (FFModel).

(0.04236)

HML 0.21147 ***

(0.04613)

-----------------------------------------------------------------------------------------

R^2 0.03463 0.00698 0.00816 0.32647

Adj. R^2 0.01415 -0.00194 -0.00372 0.32042

Num. obs. 338 338 339 338

RMSE 2.83488 2.85793 6.59396 2.3537

=====================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

===============================================

Residuals:

Min 1Q Median 3Q Max

-13.8415 -0.8245 -0.2493 1.1647 11.1416

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.549933 0.212255 2.591 0.00999 **

M2MoneyDelta -0.012830 0.005529 -2.320 0.02093 *

===============================================

*** p < 0.001, ** p < 0.01, * p < 0.05

32

Table 7-5: STT Adjusted FFModel v. Original

AdjFFModel FFModel

=================================

(Intercept) 0.11346 -0.06705

(0.18044) (0.13014)

MktRF 0.36421 *** 0.36832 ***

(0.02975) (0.02967)

SMB -0.09746 * -0.09350 *

(0.04238) (0.04236)

HML 0.20425 *** 0.21147 ***

(0.04633) (0.04613)

M2MoneyDelta -0.00667

(0.00463)

--------------------------------------------------------

R^2 0.33065 0.32647

Adj. R^2 0.32261 0.32042

Num. obs. 338 338

RMSE 2.34991 2.3537

=================================

*** p < 0.001, ** p < 0.01, * p < 0.05

Although the p-value for M2MoneyDelta is no longer significant due to inflation

from other parameters, the Adj. R2 and RMSE appears to have slightly improved model

performance at 32.26% (AdjFFModel) verses 32.04% (FFModel)—RMSE at 2.35

(AdjFFModel) verses 2.353 (FFModel). For all variables in the alternative model,

variance inflation factors are within reasonability at 1.09 (MktRF), 1.13 (SMB), 1.14

(HML), and 1.03 (M2MoneyDelta). The intercept of AdjFFModel suggests that the

expected State Street single stock return rate is 11% per month; the slope can be viewed

as the expected one-unit per share stock increase results in an escalation of MktRF’s

coefficient by 0.36, SMB by -0.097, and HML by 0.20 with the change in money velocity

by -0.006, respectively. The Fama-French model reveals that the expected State Street

single stock return rate decreases 7% per month; the slope can be viewed as the expected

one-unit per share stock return decrease results in an increase of MktRF’s coefficient by

33

0.37, SMB by -0.093, and HML by 0.21, respectively. To further study the model

performance between these models, AdjFFModel is back-tested against the Fama-French

model in Chapter VIII. Table 7-6 compares models 7, 8, and 9 to the FFModel.

Table 7-6: STT Original Model Regression Results, Part 4

Model7 Model8 Model9 FFModel

=================================================

(Intercept) 2.40213 0.52296 0.94714 -0.06705

(2.80791) (1.66798) (0.89970) (0.13014)

PerConsumEx -0.00054 -0.0003

(0.00040) (0.00028)

M2Money 0.0006 0.0004

(0.00039) (0.00032)

U3Unemploy -0.08371 -0.14236

(0.15862) (0.13432)

PerSavRate -0.15773

(0.17836)

SumKp -0.0092 -0.00658

(0.03800) (0.03535)

Ap 0.02239 0.02421

(0.07765) (0.07569)

Cp 1.68505 0.88542

(8.61664) (8.31994)

MktRF 0.36832 ***

(0.02967)

SMB -0.09350 *

(0.04236)

HML 0.21147 ***

(0.04613)

-----------------------------------------------------------------------------------

R^2 0.00921 0.00049 0.00596 0.32647

Adj. R^2 -0.01181 -0.00849 -0.00297 0.32042

Num. obs. 338 338 338 338

RMSE 2.87196 2.86725 2.85939 2.3537

=================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

Models 7, 8, and 9 all have insignificant performance results compared to the

FFModel in predicating single stock returns for the State Street Corporation in terms of p-

values, RMSE, and Adj. R2. Raw data, without any transformations for human economic

behavior and geomagnetic activity, has generally shown worse results compared to their

delta counterparts.

34

To conclude, neither model presented in this section has shown promising results

against the Fama-French model with the exception of AdjFFModel—this model slightly

exceeds model performance of the Fama-French model which qualifies for backtesting in

Chapter VIII. Lastly, the absolute change (delta) in money velocity appears to have

influence and significance, but that variable alone cannot accurately predict stock returns

for the Company. In the next section, the same scenario analysis is applied, but to a group

of equities that closely tracks the Standard & Poor’s Index (i.e., S&P 500)—this is to see

if the proposed parameters have any meaningful impact in quantitative estimation within

a larger market environment.

Original Approach: Vanguard S&P 500 Fund Returns

The Vanguard S&P 500 Index fund is used as the dependent variable in this

section. The rationale for the use of such a diversified mutual fund is due to the fact that

Fama and French’s three-factor model performs stronger since their equation contains

mostly microeconomic parameters: such as MktRF, SMB, and HML. This section uses

all equations (3 – 13) located in Chapter IV to analyze if alternative methods could

improve the original model. The monthly time-series range is from October 1986 to

November 2014. Table 7-7 displays regression results for the Direct Model Equation 3

(“DirectModel”) and the direct model with human economic behavior variables, Equation

4 (“DirectModelEcon”) compared with the Fama-French model (“FFModel”). For

variable elimination, the focus of the regression output includes the following: (i) Adj.

R2, (ii) RMSE (root-mean-squared-error), and (iii) p-values (0.1%, 1%, or 5%). A

35

variance inflation factor (VIF) analysis will typically occur after the model’s parameters

have been adjusted.

Table 7-7: Van500 Original Model Regression Results, Part 1

The DirectModel produces model performance results that is similar to the

FFModel by Adj. R2 and RMSE; however, after testing for significance at 5% or below

(Tables 7-8 to 7-10) with geomagnetic variables located below, these variables produce

inflated model performance metrics.

DirectModel DirectModelEcon FFModel

===============================================

(Intercept) -0.00290 0.00718 0.00257 ***

(0.00330) (0.00538) (0.00032)

MktRF 0.01005 *** 0.01006 *** 0.01004 ***

(0.00007) (0.00007) (0.00007)

SMB -0.00196 *** -0.00192 *** -0.00195 ***

(0.00010) (0.00010) (0.00010)

HML 0.00026 * 0.00024 * 0.00027 *

(0.00011) (0.00011) (0.00011)

SumKp 0.00008 -0.00002

(0.00007) (0.00007)

Ap -0.00001 0.00014

(0.00015) (0.00015)

Cp -0.01374 0.00075

(0.01649) (0.01650)

PerConsumEx 0.00000

0.00000

M2Money 0.00000

0.00000

PerSavRate 0.00052

(0.00034)

U3Unemploy -0.00087 **

(0.00030)

-------------------------------------------------------------------------------

R^2 0.98399 0.98521 0.98361

Adj. R^2 0.9837 0.98476 0.98347

Num. obs. 338 338 338

RMSE 0.00566 0.00547 0.0057

===============================================

*** p < 0.001, ** p < 0.01, * p < 0.05

36

Table 7-8: Van500 SumKp Relationship Test

==================================================

Residuals:

Min 1Q Median 3Q Max

-0.226434 -0.024655 0.005276 0.027916 0.124208

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.38E-02 8.01E-03 1.726 0.0853

SumKp -2.94E-05 4.67E-05 -0.631 0.5288

=================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

Table 7-9: Van500 Ap Relationship Test

Table 7-10: Van500 Cp Relationship Test ==================================================

Residuals:

Min 1Q Median 3Q Max

-0.226527 -0.024633 0.005289 0.027911 0.124023

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.24E-02 6.01E-03 2.063 0.0399 *

Cp -6.37E-03 1.03E-02 -0.615 0.5386

==================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

These results suggests that geomagnetic activity, with market factors, does not improve

model performance compared to the Fama-French model. DirectModelEcon, however,

==================================================

Residuals:

Min 1Q Median 3Q Max

-0.226976 0.024691 0.005151 0.027895 0.123805

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 1.19E-02 5.16E-03 2.3 0.0221 *

Ap -2.34E-04 3.74E-04 -0.627 0.5314

==================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

37

has an improved Adj. R2, decrease in RMSE, and only one variable (i.e., U3Unemploy)

with a p-value below 5%. Despite one variable being significant, the cause for majority of

the increase in model performance is due to the variance being inflated by additional

parameters having p-values exceeding alpha. The table below is the adjusted

DirectModelEcon model compared to the FFModel:

Table 7-11: Van500 Adjusted DirectModelEcon v. FFModel

RMSE has shown a noticeable decrease compared to the FFModel which suggest

stronger model predictability (i.e., -0.0016). In addition, Adj. R2 has increased by 0.095%

compared to the Fama-French model. The U3Unemploy (i.e., unemployment) variable

has significance with the Vanguard S&P 500 Fund returns where p < 0.001. Severe

multicollinearity does not exist with this particular model with variance inflation factors

at 1.08 (MktRF), 1.13 (SMB), 1.13 (HML), and 1.009 (U3Unemploy). The intercept of

AdjDirectModelEcon suggests that the expected Vanguard S&P 500 Fund return rate is

AdjDirectModelEcon FFModel

=======================================

(Intercept) 0.00823 *** 0.00257 ***

(0.00126) (0.00032)

MktRF 0.01006 *** 0.01004 ***

(0.00007) (0.00007)

SMB -0.00193 *** -0.00195 ***

(0.00010) (0.00010)

HML 0.00027 * 0.00027 *

(0.00011) (0.00011)

U3Unemploy -0.00093 ***

(0.00020)

-----------------------------------------------------------------

R^2 0.98461 0.98361

Adj. R^2 0.98442 0.98347

Num. obs. 3 38 338

RMSE 0.00554 0.0057

=======================================

*** p < 0.001, ** p < 0.01, * p < 0.05

38

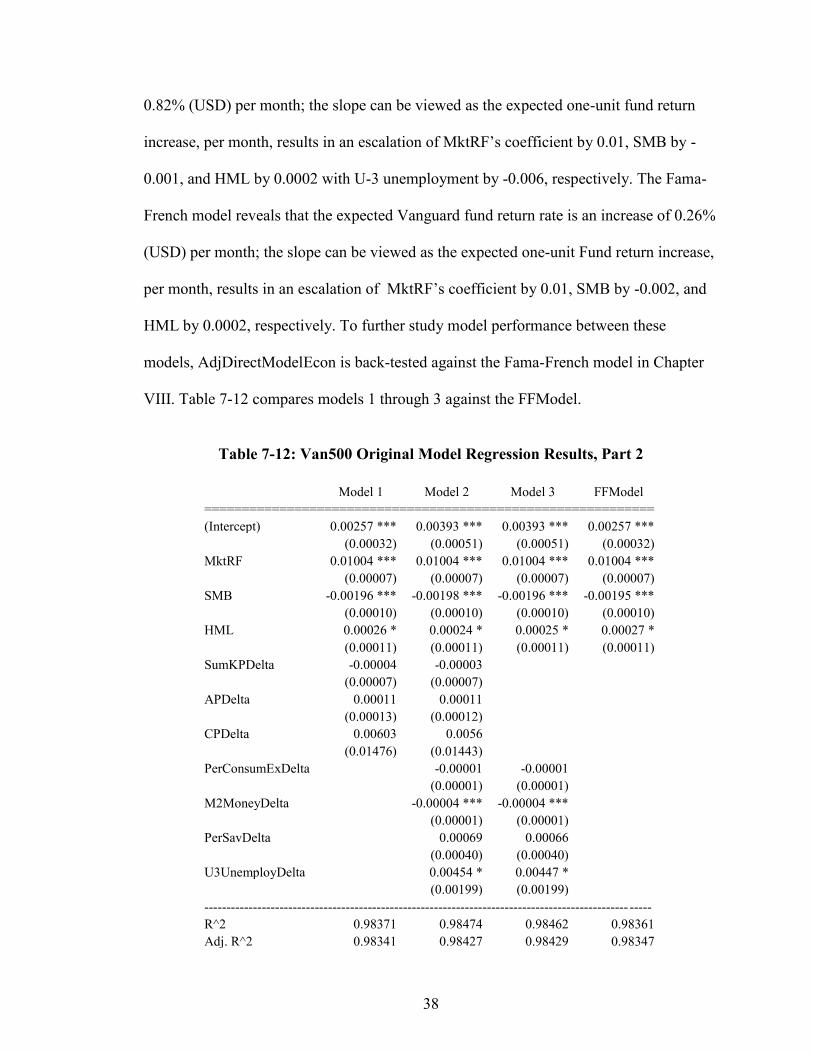

0.82% (USD) per month; the slope can be viewed as the expected one-unit fund return

increase, per month, results in an escalation of MktRF’s coefficient by 0.01, SMB by -

0.001, and HML by 0.0002 with U-3 unemployment by -0.006, respectively. The Fama-

French model reveals that the expected Vanguard fund return rate is an increase of 0.26%

(USD) per month; the slope can be viewed as the expected one-unit Fund return increase,

per month, results in an escalation of MktRF’s coefficient by 0.01, SMB by -0.002, and

HML by 0.0002, respectively. To further study model performance between these

models, AdjDirectModelEcon is back-tested against the Fama-French model in Chapter

VIII. Table 7-12 compares models 1 through 3 against the FFModel.

Table 7-12: Van500 Original Model Regression Results, Part 2

Model 1 Model 2 Model 3 FFModel

============================================================

(Intercept) 0.00257 *** 0.00393 *** 0.00393 *** 0.00257 ***

(0.00032) (0.00051) (0.00051) (0.00032)

MktRF 0.01004 *** 0.01004 *** 0.01004 *** 0.01004 ***

(0.00007) (0.00007) (0.00007) (0.00007)

SMB -0.00196 *** -0.00198 *** -0.00196 *** -0.00195 ***

(0.00010) (0.00010) (0.00010) (0.00010)

HML 0.00026 * 0.00024 * 0.00025 * 0.00027 *

(0.00011) (0.00011) (0.00011) (0.00011)

SumKPDelta -0.00004 -0.00003

(0.00007) (0.00007)

APDelta 0.00011 0.00011

(0.00013) (0.00012)

CPDelta 0.00603 0.0056

(0.01476) (0.01443)

PerConsumExDelta -0.00001 -0.00001

(0.00001) (0.00001)

M2MoneyDelta -0.00004 *** -0.00004 ***

(0.00001) (0.00001)

PerSavDelta 0.00069 0.00066

(0.00040) (0.00040)

U3UnemployDelta 0.00454 * 0.00447 *

(0.00199) (0.00199)

------------------------------------------------------------------------------------------------ -----

R^2 0.98371 0.98474 0.98462 0.98361

Adj. R^2 0.98341 0.98427 0.98429 0.98347

39

The change in geomagnetic activity (i.e., SumKPDelta, APDelta, and CPDelta),

as shown in Model 1, has decreased model performance in RMSE, p-values, and Adj. R2.

Human economic behavior variables M2MoneyDelta (i.e., the change in money velocity)

and U3UnemployDelta (i.e., the change in unemployment) all have promising results and

statistically significant. Table 7-13 represents the adjusted version of Model 2 compared

to the FFModel.

Table 7-13: Van500 Adjusted Model 2 v. FFModel

AdjModel 2 FFModel

====================================

(Intercept) 0.00354 *** 0.00257 ***

(0.00043) (0.00032)

MktRF 0.01003 *** 0.01004 ***

(0.00007) (0.00007)

SMB -0.00199 *** -0.00195 ***

(0.00010) (0.00010)

HML 0.00026 * 0.00027 *

(0.00011) (0.00011)

M2MoneyDelta -0.00004 **

(0.00001)

U3UnemployDelta 0.00489 *

(0.00198)

-------------------------------------------------------------

R^2 0.98434 0.98361

Adj. R^2 0.9841 0.98347

Num. obs. 338 338

RMSE 0.00559 0.0057

====================================

*** p < 0.001, ** p < 0.01, * p < 0.05

Model performance of AdjModel 2 has shown an increase in Adj. R2 by 0.063%.

In addition, RMSE has decreased by 0.0011 which indicates stronger estimation

performance (and absolute fit) compared to the FFModel when the absolute change

(delta) in both Money Velocity and U-3 unemployment is used in the model. Severe

Num. obs. 338 338 338 338

RMSE 0.00571 0.00556 0.00556 0.0057

============================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

40

multicollinearity does not exist with this particular model with variance inflation factors

at 1.10 (MktRF), 1.14 (SMB), 1.15 (HML), 1.027 (M2MoneyDelta), and 1.0031

(U3UnemployDelta). The intercept of AdjModel 2 suggests that the expected Vanguard

S&P 500 Fund return rate is 0.35% (USD) per month; the slope can be viewed as the

expected one-unit fund return increase, per month, results in an escalation of MktRF’s

coefficient by 0.01, SMB by -0.002, HML by 0.0003, and the change in money velocity

by -0.00004 with U-3 unemployment (delta) by 0.005, respectively. To further study the

model performance between these models, AdjDirectModelEcon is back-tested against

the Fama-French model in Chapter VIII. Table 7-14 compares models 4 to 6 against the

FFModel.

Table 7-14: Van500 Original Model Regression Results, Part 3

Model 4 Model 5 Model 6 FFModel

========================================================

(Intercept) 0.00940 * 0.00900 *** 0.00933 * 0.00257 ***

(0.00403) (0.00241) (0.00403) (0.00032)

SumKPDelta -0.00048 -0.00037

(0.00054) (0.00055)

APDelta -0.00037 -0.00051

(0.00097) (0.00098)

CPDelta 0.08572 0.06691

(0.11366) (0.11393)

PerConsumExDelta 0.00014 0.00014

(0.00008) (0.00008)

M2MoneyDelta -0.00016 -0.00016

(0.00009) (0.00009)

PerSavDelta 0.00325 0.00368

(0.00315) (0.00314)

U3UnemployDelta -0.01553 -0.01367

(0.01558) (0.01555)

MktRF 0.01004 ***

(0.00007)

SMB -0.00195 ***

(0.00010)

HML 0.00027 *

(0.00011)

----------------------------------------------------------------------------------------------- -

41

Models 4 to 6 do not contain any Fama-French factors (i.e., MktRF, SMB, and

HML). These models use absolute change (delta) in either geomagnetic activity, human

economic behavior, or both. Based on performance results, neither of these models would

be a candidate for backtesting against the FFModel. In addition, no statistical significance

was revealed in this scenario between each additional variable (aside from the Fama-

French factors) and the dependent variable. Table 7-15 includes results for models 7 to 9

against the Fama-French model.

Table 7-15: Van500 Original Model Regression Results, Part 4

R^2 0.03533 0.01072 0.02445 0.98361

Adj. R^2 0.01487 0.00184 0.01273 0.98347

Num. obs. 338 338 338 338

RMSE 0.04402 0.04431 0.04406 0.0057

========================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

Model 7 Model 8 Model 9 FFModel

==================================================

(Intercept) 0.05952 0.01761 0.02433 0.00257 ***

(0.04347) (0.02590) (0.02393) (0.00032)

PerConsumEx -0.00001 -0.00001

(0.00001) (0.00001)

M2Money 0.00001 0.00001

(0.00001) (0.00001)

U3Unemploy 0.00107 0.00166

(0.00246) (0.00237)

PerSavRate -0.00165 -0.00168

(0.00276) (0.00276)

SumKp -0.00038 -0.00012

(0.00059) (0.00055)

Ap -0.00001 -0.00019

(0.00120) (0.00118)

Cp 0.0678 0.02516

(0.13340) (0.12917)

MktRF 0.01004 ***

(0.00007)

SMB -0.00195 ***

(0.00010)

HML 0.00027 *

(0.00011)

42

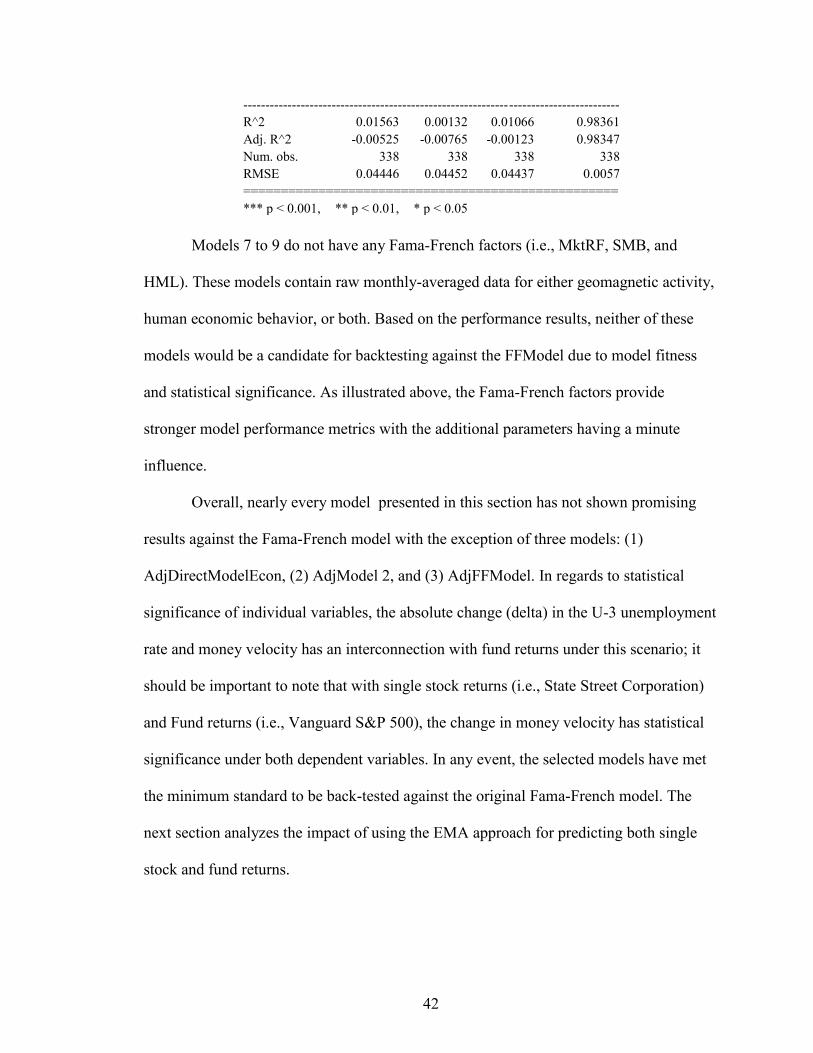

Models 7 to 9 do not have any Fama-French factors (i.e., MktRF, SMB, and

HML). These models contain raw monthly-averaged data for either geomagnetic activity,

human economic behavior, or both. Based on the performance results, neither of these

models would be a candidate for backtesting against the FFModel due to model fitness

and statistical significance. As illustrated above, the Fama-French factors provide

stronger model performance metrics with the additional parameters having a minute

influence.

Overall, nearly every model presented in this section has not shown promising

results against the Fama-French model with the exception of three models: (1)

AdjDirectModelEcon, (2) AdjModel 2, and (3) AdjFFModel. In regards to statistical

significance of individual variables, the absolute change (delta) in the U-3 unemployment

rate and money velocity has an interconnection with fund returns under this scenario; it

should be important to note that with single stock returns (i.e., State Street Corporation)

and Fund returns (i.e., Vanguard S&P 500), the change in money velocity has statistical

significance under both dependent variables. In any event, the selected models have met

the minimum standard to be back-tested against the original Fama-French model. The

next section analyzes the impact of using the EMA approach for predicting both single

stock and fund returns.

-------------------------------------------------------------------------------------

R^2 0.01563 0.00132 0.01066 0.98361

Adj. R^2 -0.00525 -0.00765 -0.00123 0.98347

Num. obs. 338 338 338 338

RMSE 0.04446 0.04452 0.04437 0.0057

==================================================

*** p < 0.001, ** p < 0.01, * p < 0.05

43

EMA Approach: State Street Corporation Stock Returns

In this section, the Exponential Moving Average (EMA) calculation is applied to

all geomagnetic and human economic behavior variables. The mean (µ) data ranges from

December 2004 to November 2009, or 60 monthly periods. EMA is calculated from

December 2009 to November 2014, or 60 monthly periods—this totals 120 monthly

periods for the entire EMA calculation per variable. The filtered data is then applied to

selected time-series regression equations without absolute delta (i.e., models 7, 8, and 9)

located in Chapter IV. After the time-series regression outputs have been calculated with

the selected data, the model’s parameters are later modified (if applicable) to meet the

cut-off p-value of any measurement over 5%. To meet this requirement, the focus of the

regression output includes the following: (i) Adj. R2, (ii) RMSE (root-mean-squared-

error), and (iii) p-values (0.1%, 1%, or 5%). A variance inflation factor (VIF) analysis

will typically occur after the model’s parameters have been adjusted (or removed). Table

7-16 includes the DirectModelEMA, where geomagnetic variables are included with the

Fama-French factors—and DirectModelEconEMA, which includes all variables from

DirectModelEMA, but with human economic behavior—these models are then compared