Natural Gas Vehicle Market Whitepaper USA 2013-2014

44

For more information, visit www.ngvevent.com Natural Gas Vehicle Market Whitepaper USA 2013-2014 Whitepaper highlights include: NGV USA Market Overview: Comprehensive analysis of the North American NGV Market Government Policies: How they will impact the NGV market over the next 5 years Converting to Natural Gas: Key considerations to address when converting your fleet to NGV’s Infrastructure Development: How to successfully plan and build NGV infrastructure

-

Upload

marcellus-drilling-news -

Category

News & Politics

-

view

1.894 -

download

0

Transcript of Natural Gas Vehicle Market Whitepaper USA 2013-2014

For more information, visit www.ngvevent.com

Natural Gas Vehicle Market Whitepaper USA2013-2014

Whitepaper highlights include:

NGV USA Market Overview: Comprehensive analysis of the North American NGV Market

Government Policies: How they will impact the NGV market over the next 5 years

Converting to Natural Gas: Key considerations to address when converting your fleet to NGV’s

Infrastructure Development: How to successfully plan and build NGV infrastructure

WELCO

ME

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 2

Welcome

Dear Colleague

Thank you for your interest in this FC Gas Intelligence Whitepaper on the Natural Gas Vehicle market in North America, 2013-14, I hope you find it valuable.

Natural Gas Vehicle’s (NGV) are at a seminal moment in the United States currently, with a range of stakeholders driving the development of the market. To get a thorough overview the report interviewed over 20 industry experts, drawing their combined expertise into this document to better inform your strategies over the next few years.

This Whitepaper is only the beginning of the debate on Natural Gas Vehicle’s, it has been created in conjunction with the 3rd Natural Gas Vehicle USA Conference & Exhibition (June 11-13, Houston) more info can be found here www.ngvevent.com

I hope you find the report useful and I look forward to speaking to you soon,

With very best wishesJoshua BullSector Head | FC Gas Intelligence

AB

OU

T FC BU

SINESS IN

TELLIGEN

CE

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 3

About FC Gas Intelligence

A business intelligence and networking company we help leading corporations define their future strategy and direction, develop growth opportunities and solve the problems facing their sectors. The engines of our business are growth and change. We focus on two types of industry:

■ Those arising from technology developments which are moving into full global commercialisation. ■ Those needing to change in order to respond to disruptive technologies or global events.

Our aim is to provide companies with insights into strategic options for the future in order that they can capitalise on opportunity.

Disclaimer FC Business Intelligence Ltd and its partners prepared the information and opinions in this report. FC Business Intelligence has no obligation to tell you when opinions or information in this report change. FC Business Intelligence Ltd makes every effort to use reliable, comprehensive information, but it makes no representation that the information is accurate or complete. In no event shall FC Business Intelligence Ltd and its partners be liable for any damages, losses, expenses, loss of data, loss of opportunity or profit caused by the use of the material or contents of this report.

No part of this document may be distributed, resold, copied or adapted without FC Business Intelligence Ltd ‘s prior written permission.

© FC Business Intelligence Ltd © 2013

Author

CON

TENTS

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 4

Contents

Welcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

About FC Gas Intelligence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

List of Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7-8

Chapter 1: NGV Industry Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.0 Market Size and Growth Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

1.1 Growth drivers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

1.2 NGVs on the Road . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.3 Locations of Existing CNG and LNG Stations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1.4 Proposed expansion of CNG and LNG fueling networks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

1.5 Expansion of Small and Midsize LNG Liquefaction Plants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

1.6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Chapter 2: Government policies: How they will shape the NGV market over the next 5 years . . . . .22

2.0 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

2.1 Policy in context . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

2.2 Subsidies and tax incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

2.3 Procurement policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

2.4 CAFÉ standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

2.5 Environmental regulation: potential risk? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.6 Export policy: potential risk? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.8 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Chapter 3: Converting to Natural Gas, Vehicle issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

3.0 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.1 Passenger automobiles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

3.2 Light and medium duty trucking vehicle options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.3 State subsidies for light-duty NGVS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

3.4 Heavy duty trucking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

3.5 Factors to consider in HD fleet conversions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

3.6 State subsidies for heavy-duty fleet conversion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

3.7 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Chapter 4: Building Dedicated Fuelling Infrastructure, CNG and LNG . . . . . . . . . . . . . . . . . . . .38

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

4.2 Basic cost considerations, CNG compared to LNG . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

4.3 Design, planning, and siting of CNG fuelling stations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

4.4 Design, planning, and siting of LNG fuelling stations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

FIGU

RES

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 5

Figures

Figure 1 Natural gas consumption by sector, 1990-2040 (trillion cubic feet) . . . . . . . . . . . . . . . . . . . . . . 9

Figure 2 U .S . Natural Gas Vehicle Fuel Consumption MMcf . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 3 Average diesel, gasoline, and CNG prices, 2000-2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 4 Price differential CNG to diesel, by state . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 5 PCT . Growth in public access CNG stations 7/11-8/13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Figure 6 Regional Transportation Corridors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Figure 7 Locations of CNG stations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Figure 8 Locations of LNG Stations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Figure 9 United States truck traffic volumes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Figure 10 Projected expansion of Trillium CNG station network, 2013-2016 . . . . . . . . . . . . . . . . . . . . . . 17

Figure 11 Projected expansion of Love’s CNG network . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Figure 12 Projected rollout of Clean Energy’s America’s Natural Gas Highway of LNG and LCNG stations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Figure 13 Projected network of LNG stations proposed by Shell and TravelCenters of America partnership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Figure 14 Blu LNG operational and pending LNG fuelling network (as of end 2013) . . . . . . . . . . . . . . 19

Figure 15 Small and Mid Scale LNG Liquefaction plants* . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Figure 16 Calculation of light-duty truck payback, based on various fuel price and truck premium assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Figure 17 Map of states offering various incentives for light-duty CNG vehicles . . . . . . . . . . . . . . . . . . 32

Figure 18 Natural gas engine comparison-- power (hp) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Figure 19 Natural gas engine comparison – torque (ft-lb) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Figure 20 Sample calculation of expected payback for HD fleet conversion . . . . . . . . . . . . . . . . . . . . . . 34

Figure 21 Sample CNG range calculation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Figure 22 Calculation of Heavy-duty truck payback, based on various fuel price and truck premium assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Figure 23 Heavy-duty incentives, Canada and US (as of August 2013) . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Figure 24 GE CNG in a Box . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Figure 25 GE LNG in a Box™ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Figure 26 Micro LNG . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

TAB

LES

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 6

List of Tables

Table 1 CNG average prices per region . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11

Table 2 Reduction of pollutants from CNG use, as compared with reformulated gasoline . . . . . . . . .12

Table 3 Small and Mid Scale LNG Liquefaction plants in the United States* . . . . . . . . . . . . . . . . . . . . . .20

Table 4 LNG Export facilities approved . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Table 5 Home fuelling specifications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

Table 6 Ford CNG model options (as of model year 2014) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

Table 7 Chrysler CNG model options (as of model year 2014) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

Table 8 GMC and Chevrolet CNG model options (as of model year 2014) . . . . . . . . . . . . . . . . . . . . . . . .30

Table 9 Summary of state incentives for light-duty CNG vehicles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Table 10 Heavy-Duty engine options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

Table 11 Weight diesel truck compared to CNG truck and LNG truck (full tanks in lbs) . . . . . . . . . . . . .35

Table 12 CNG to LNG compared . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39

EXECU

TIVE SU

MM

ARY

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 7

FC Gas Intelligence’s Natural Gas Vehicles Market Report USA 2013-2014 provides an up-to-the-minute summary of current conditions in this fast-growing market segment. The report’s four chapters summarizes the latest business intelligence vital to understanding issues currently confronting stakeholders in this market, and provides direct guidance for fleet managers looking for first-hand advice on key issues to consider when deciding whether to switch to cheaper, cleaner-burning natural gas.

Chapter 1: NGV USA Market Overview: Comprehensive Analysis of the North American NGV Market

Natural gas has significant potential to transform the transportation sector, particularly for fleets and commercial trucking, due to its cheaper, less volatile price, compared diesel or gasoline. The fuel is largely sourced in North America, in contrast to petroleum-based fuels, which are largely sourced from politically unstable and potentially hostile regions of the world, especially the Middle East. The fuel is also cleaner burning than traditional transportation fuels, and can help provide a bridge to a greener, lower-carbon future.

The chapter lays out in detail how the number of CNG and LNG public access fuelling stations is expanding rapidly, with several companies rolling out new NG infrastructure. Detailed information is provided about ambitious expansion plans, launched by companies such as Trillium and Love Travel Stops, in the era of CNG infrastructure, and Clean Energy, Shell, and ENN- Blu LNG on the LNG side. In partnership with Pilot Flying J Truck S, Clean Energy is also exploring LCNG options. The

net effect of these expansion plans is that some fleets—particularly heavy-duty trucks servicing major interstate transportation corridors may soon be able to convert to natural gas without having to develop independent fuelling infrastructure.

Chapter 2: Government Policies: How they will impact the NGV market over the next 5 years

Federal and state government policies have been crucial to fostering the development of NG as a transportation fuel. Stakeholders currently operating in this market, as well as companies considering undertaking fleet conversions, need to understand how government policies will continue to shape the future development of the NGV sector in both positive and potentially negative ways over the next five years. The chapter provides an overview of current federal and state policies to promote NGVs, and provides information on what government and private resources are available for getting the latest information about these rapidly evolving policies. Detailed discussion follows of two significant policy areas— environmental regulation, both state and federal, and export policy— that could thwart or at minimum slow development of NGVs. Understanding potential policy risks is important for companies undertaking or continuing significant investments in NGVs or infrastructural development.

Executive Summary

EXECU

TIVE SU

MM

ARY

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 8

Chapter 3: Converting to Natural Gas: Key Considerations to address when converting your fleet to NGVs

The higher relative costs of NGVs compared to traditionally-fuelled vehicles has thus far presented a major obstacle to wider use of NG as a transportation fuel. This chapter summarises the current state of the NGV market. OEMs have started to offer a wider range of NG options, from automobiles, to vans—both passenger and cargo—and light and medium-duty truck options. These vehicles cost more than conventionally fuelled models, but some of these costs can be offset by state incentives available for converting to NG. All major heavy-duty truck manufacturers now offer NG options, either in CNG or LNG formats, prodded by customers responding to the potential significant fuel costs savings. The chapter walks through specific examples of how to evaluate the value proposition for fleet conversions, looking at both light-duty, and heavy-duty, examples.

Chapter 4: Infrastructure Development: How to successfully plan and build NGV infrastructure

Infrastructural considerations continue to loom large in decisions to convert all or part of a fleet’s vehicles to NGV. The future U.S. NG infrastructure will combine a network of CNG, LNG, and LCNG stations. This chapter analyses issues fleet managers need to consider in deciding whether to opt for CNG of LNG, based on where their fleets will operate, and what their range needs are. Although more CNG and LNG infrastructure is continually coming on-line, most fleets must still construct or secure access to independent fuelling infrastructure, as existing public access infrastructure alone cannot support fleet range needs. This chapter discusses the issues companies must consider when deciding whether, where, and how to construct CNG or LNG fuelling stations. Infrastructural specialists are expanding their product offerings, focusing on modular, and lower-cost options that reduce the necessary up-front investments and also lower on-going operational and maintenance costs, for companies constructing both CNG and LNG fuelling infrastructure.

Executive Summary

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 9

Chapter 1: NGV Industry Overview

1.0 Market Size and Growth ForecastsPetroleum-based fuels currently dominate the U.S. transportation market, and this lack of fuel diversity makes this market particularly vulnerable to price shocks. The United States currently consumes 35 billion gallons of diesel fuel per year. Analysts disagree about how much of this current energy demand could be displaced by cheaper alternative fuels such as natural gas (NG), particularly in the industrial, power generation, and transportation sectors.

Citigroup forecasts NG demand in transportation alone to reach 2.2 billion cubic feet per day (Bcf/d) by 2020, while a Reuters poll of analysts is less bullish, expecting NG demand in this sector to reach only 1.2 Bcf/d over the same period. The United States Energy Information Administration (EIA) predicts a gradual rise in NG usage in the transportation sector over the next decade, as shown in Figure 1, as a more comprehensive NG sourcing and fuelling infrastructure is developed, comprising both compressed natural gas (CNG) and liquefied natural gas (LNG).

Figure 1 Natural gas consumption by sector, 1990-2040 (trillion cubic feet)

The use of NG as a transportation fuel has increased steadily over the last decade, reaching 32,000 Million cubic feet (MMcf ) in 2012. Most of this consumption is currently concentrated in the heavy-duty trucking sector. The American Clean Skies Foundation suggests that NG provides a promising opportunity to diversify fuel sources for both the heavy and medium duty trucking sector, which, taken together, account for 22% of the U.S. transportation sector’s fuel

use. This diversification would come with another benefit, for the cost of fueling with NG is substantially cheaper than buying petroleum-based fuels, even when necessary costs are included, both buying relatively more expensive NGVs, and developing fueling infrastructure, Fleet operators have a potential opportunity to capitalize on a major cost-saving opportunity, since fuel accounts for their second-highest cost.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 10

Figure 2 U .S . Natural Gas Vehicle Fuel Consumption MMcf

1.1 Growth drivers

Fuel priceThe principal factor driving growth in interest in NGVs is the lower overall price of NG compared to the cost of either gasoline or refined diesel fuels. Over the last decade, NG prices have dropped dramatically as new North American sources of supply have opened up, with the United States moving from a potential NG importer to a potential significant NG exporter over this time period.

Oil prices, by contrast, have been especially volatile over the same time period. Since 2000, refined diesel prices as measured by Diesel Gallon Equivalents (DGEs) have always exceeded NG prices, sometimes by as much as $2, but usually by at least $1.50, per DGE. Similarly, gasoline prices have always exceeded NG prices, when measured by Gasoline Gallon Equivalents (GGEs), by as much as $1.50 per unit.

Figure 3 Average diesel, gasoline, and CNG prices, 2000-2012

Source: Clean Cities Alternative Fuel Price Report, July 2013

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 11

Politically stable source of supplyIn addition to the comparative price advantage, NG supplies are more stable and certain, and virtually all demand can be supplied either domestically, or by turning to Canada or Mexico; the three countries are linked in a fully integrated NG transportation and distribution system. About 85% of the NG consumed in the United States is sourced domestically, from one of the 32 U.S. states that currently produce NG. Overall, 97% of the NG used in the U.S. comes either from the United States, Canada, or Mexico.

By contrast, oil is sourced from politically unstable or potentially hostile places, including Latin America, Russia, and especially the Middle East. Political instability in the Middle East often translates into price volatility and also raises periodic concerns about supply interruptions. Increased use of NG would translate into lessened dependence on energy imports from these politically unstable parts of the world.

Price stabilityIn addition to their more attractive absolute price levels, NG prices also have another advantage for corporate planning purposes in that they have in recent years traded in a much narrower band than either diesel or gasoline prices, with the prices varying since 2000 about $1 from lowest to highest price. Since late 2004, this price spread has been even tighter, varying by no more than $0.75.

It has not always been the case that NG prices have traded in such a narrow band, and in fact, until technology increased the domestically produced supply, NG prices had been among the most volatile commodities traded on the New York Mercantile Exchange (NYMEX). Future forecasts of NG supply suggest that future volatility will follow the recent pattern of tighter trading spreads.

Regional price variationsAs Table 1 indicates, CNG currently has a lower average price than diesel for all regions of the country, with the largest difference ($1.83 per DGE) being in the Rocky Mountain region. CNG costs on average about $1.52 less than diesel on a DGE basis.

Table 1 CNG average prices per region

Region CNG Price ($/DGE) Diesel Price ($)

New England $2.86 $4.07

Central Atlantic $2.48 $3.81

Lower Atlantic $2.24 $3.82

Midwest $2.08 $3.86

Gulf Coast $2.26 $3.82

Rocky Mountain $2.03 $3.86

West Coast $2.71 $4.08

National Average $2.39 $3.91

Source: Clean Cities Alternative Fuel Price Report, July 2013

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 12

Figure 4 illustrates price differentials by state for CNG relative to diesel. In this map, negative numbers represent prices for CNG lower than prices for diesel. States not highlighted with a colour did not have any CNG data points in the latest Clean Cities Alternative

Fuel Price Report, published in July 2013. For all states for which pricing data are available, CNG prices were cheaper than diesel, with the most favourable relative CNG prices found in states located in the Midwest, Rocky Mountain, and West Coast regions.

Figure 4 Price differential CNG to diesel, by state

CNG Price Difference Relative to Diesel

($1.99) - ($1.50)($1.49) - ($0.95)($2.30) - ($2.00)($1.99) - ($1.50)($0.94) - ($0.55)

Source: Clean Cities Alternative Fuel Price Report, July 2013

Environmental benefitsThere are considerable environmental benefits to wider adoption of NG as a transportation fuel, whether in CNG or LNG form. The United States Environmental Protection Agency (EPA) recognizes that natural gas vehicles (NGVs) produce lower levels of harmful emissions, including greenhouse gases, carbon dioxide, nitrogen oxide, particulate matter, and toxic and carcinogenic pollutants. The exact degree of emissions benefits depends on the type and model of the vehicle used, as well as the choice of the conventionally fueled vehicle benchmark. The Alternative Fuels Data Center (AFDC) of the United States Department of Energy (DoE) provides tools for performing detailed emissions comparisons. Many fleet operators are as attracted to NG’s potential to enable them to meet their emissions targets as they

are to the potential for fuel cost savings compared to using diesel or gasoline.

Table 2 Reduction of pollutants from CNG use, as compared with reformulated gasoline

Volatile Organic Compounds 10%

Carbon Monoxide 20-40%

Nitrogen Oxides 0%

Particulate Matter 80%

Source: A Full Fuel-Cycle Analysis of Energy and Emissions Impacts of Transportation Fuels Produced From Natural Gas, Wang, M.Q. and Huang, H.S., 1999

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 13

1.2 NGVs on the Road

The DoE as of September 2013 estimated that about 112,000 NGVs operate in the United States. Market observers say that these DoE figures lag the actual state of play, and that the number of NGVs currently on the road is probably approaching 150,000. Transit buses currently form the largest category of NGVs, and are powered by either CNG or LNG. Waste collection vehicles comprise the second largest category of NGVs, with roughly half of all such vehicles fueled by NG. Airports are the third largest NGV users, with about 35 using NGVs, either by operating their own fleets or promoting the use of private fleets that burn NG.

Wider use of NG in both short-haul fleets and long distance trucking is being facilitated by the development of CNG, LNG, and LCNG fueling networks. Technological innovation is producing more affordable light-duty, medium-duty, and heavy-duty NG truck options, as well as NG-fueled passenger vehicles, largely for fleet use, although the premium for all such vehicles remains high. These premiums are expected to drop as demand for these vehicles increases, but even on current estimates, a viable model for heavy-duty trucks driving 125,000 miles a year suggests that payback on CNG fleet conversion can occur in fewer than 2 years (as described more fully in section 3.__ below).

1.3 Locations of Existing CNG and LNG Stations

CNG stationsAs of September 4, 2013, 602 public access CNG stations operate across the United States, and 633 private access stations. These stations are substantially concentrated regionally. California and Utah have been at the forefront of adopting NG as a transportation fuel, and now each of these two states is covered with a network of stations, with 157 stations operating in California, serving a population of about 38 million, and 42 in Utah, serving a population of approximately 2.9 million. (The state of Utah owns natural gas production facilities and has promoted NG use in transportation; in contrast to other states, Utah has eschewed direct subsidies to this end, and has instead concentrated on building NG infrastructure.)

Other states with significant concentrations of CNG stations include the key NG producing states of Louisiana, Oklahoma, and Texas, as well as urban states such as New York. Pennsylvania and Ohio have shown the highest growth rate in building CNG stations in the last two years, and now have 21 and 13 public access stations operating, respectively.

Figure 5 PCT . Growth in public access CNG stations 7/11-8/13

Source: NGV Today, August 19, 2013, p. 9

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 14

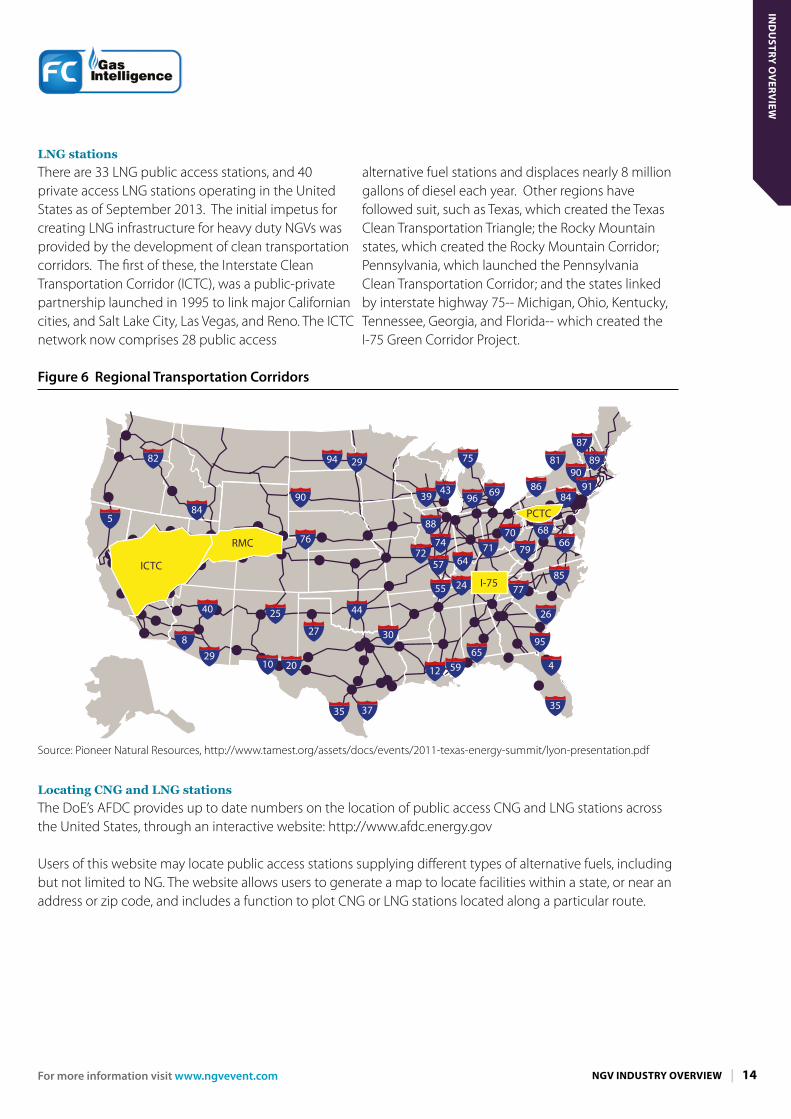

LNG stationsThere are 33 LNG public access stations, and 40 private access LNG stations operating in the United States as of September 2013. The initial impetus for creating LNG infrastructure for heavy duty NGVs was provided by the development of clean transportation corridors. The first of these, the Interstate Clean Transportation Corridor (ICTC), was a public-private partnership launched in 1995 to link major Californian cities, and Salt Lake City, Las Vegas, and Reno. The ICTC network now comprises 28 public access

alternative fuel stations and displaces nearly 8 million gallons of diesel each year. Other regions have followed suit, such as Texas, which created the Texas Clean Transportation Triangle; the Rocky Mountain states, which created the Rocky Mountain Corridor; Pennsylvania, which launched the Pennsylvania Clean Transportation Corridor; and the states linked by interstate highway 75-- Michigan, Ohio, Kentucky, Tennessee, Georgia, and Florida-- which created the I-75 Green Corridor Project.

Figure 6 Regional Transportation Corridors

82

845

90

76

2540

829

10 20

27

44

30

35 37

12 5965

4

95

26

55 24

57 64

35

39 43 699686

84

7170

79

7785

6866

88

7472

94 75 81

87

8990

29

ICTC

RMC

PCTC

I-75

91

Source: Pioneer Natural Resources, http://www.tamest.org/assets/docs/events/2011-texas-energy-summit/lyon-presentation.pdf

Locating CNG and LNG stationsThe DoE’s AFDC provides up to date numbers on the location of public access CNG and LNG stations across the United States, through an interactive website: http://www.afdc.energy.gov

Users of this website may locate public access stations supplying different types of alternative fuels, including but not limited to NG. The website allows users to generate a map to locate facilities within a state, or near an address or zip code, and includes a function to plot CNG or LNG stations located along a particular route.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 15

Figure 7 Locations of CNG stations

Source: http://www.afdc.energy.gov/locator/stations/results?utf8=✓&location=&filtered=true&fuel=CNG&owner=all&payment=all&ev_level1=true&ev_level2=true&ev_dc_fast=true&radius_miles=5

Some companies have stepped in to make publicly available via the internet not only station location and tracking tools, but other relevant information. CNGprices.com, for example, supplies up-to-the-minute information on CNG prices at a particular station, as well as crowd sourced information about station reliability, opening hours, and payment information.

http://www.cngprices.com/index.php CNGnow.com incorporates a GPS application. http://www.cngnow.com

LNG suppliers, such as Blu LNG, have incorporated station finder features in their websites, which also include pricing information, opening hours, and payment options. http://blulng.com

Figure 8 Locations of LNG Stations

Source: http://www.afdc.energy.gov/locator/stations/results?utf8=✓&location=&filtered=true&fuel=LNG&owner=all&payment=all&ev_level1=true&ev_level2=true&ev_dc_fast=true&radius_miles=5

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 16

1.4 Proposed expansion of CNG and LNG fueling networks

In the past two years, several companies have announced ambitious efforts to construct public

access NG infrastructure. These plans generally closely track major U.S. trucking routes and patterns. In general, to date CNG fuelling station networks have been designed largely to serve local and regional fleets. The thrust of LNG station development has been to connect these regional hubs.

Figure 9 United States truck traffic volumes

CNG stationsIn the CNG area, for example, Trillium announced an expansion project in June 2013 to construct and open 101 new CNG stations in 29 states within three years. This project includes plans to build new stations in states that already have extensive CNG infrastructure-- including California, New York, Ohio,

and Pennsylvania, Texas—and will also locate many new stations in states that currently have few public access CNG stations, including Florida and Georgia, but are nonetheless high-volume parts of current U.S. trucking networks.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 17

Figure 10 Projected expansion of Trillium CNG station network, 2013-2016

06/13

Existing Trillium Stations

Stations Opening 2013-2016 Projected

Stations Opening2013-2016 Projected

Existing Trillium Stations

Source: Trillium CNG, http://www.trilliumcng.com/fuel/pdf/expansion_map.pdf

Love’s Travel Stops and Country StoresLove’s Travel Stops & Country Stores, a family-owned, Oklahoma City-based company, currently operates more than 300 travel stops across 39 states that include fueling facilities and restaurants. The company has provided NG fueling capabilities at some of its locations for light and medium—duty vehicles since 2010. In 2012, Love’s constructed

its first heavy-duty CNG station in its home city of Oklahoma City, specifically for Class 8 vehicles, and the company is adding fast-fill CNG fueling capability to service Class 8 trucks at eight of its travel stops on highways along the Texas Triangle of Dallas, Houston and San Antonio, each intended to be operational by the fourth quarter of 2013.

Figure 11 Projected expansion of Love’s CNG network

85

WASHINGTON

OREGON

IDAHO

MONTANA

WYOMING

NEVADA

UTAH

ARIZONA

COLORADO

NEW MEXICO

NEWYORK VT

NH

MA

CT RI

NJ

MD DE

TEXAS

OKLAHOMA

CALIFORNIA

NEBRASKA

SOUTH DAKOTA

NORTH DAKOTAMINNESOTA

WISCONSIN

IOWA

MISSOURIKANSAS

ARKANSAS

LOUISIANA

MISSISSIPPI

ALABAMAGEORGIA

FLORIDA

NORTHCAROLINA

SOUTHCAROLINA

MAINE

VIRGINIA

WESTVIRGINIA

TENNESSEE

KENTUCKY

MICHIGAN

OHIO

INDIANA

ILLINOIS

PENNSYLVANIA

COTTONDALECOTTONDALE

HEYBURNHEYBURN

IDAHO FALLSIDAHO FALLS

INAINA

De MOTTEDe MOTTE

MATTHEWSMATTHEWS

McCOMBMcCOMB

TUPELOTUPELO

BILOXIBILOXI

DUNNDUNN

MILANMILAN

SANTA ROSASANTA ROSA

WELLSWELLS

CHOUTEAUCHOUTEAU

HAMBURGHAMBURG

FAIR PLAYFAIR PLAY

CHRISTIANACHRISTIANA

EDINBURGEDINBURG

THREE RIVERSTHREE RIVERS

LAMBSBURGLAMBSBURG

OAKDALEOAKDALE

TOOMSUBATOOMSUBA

LEELEE

AMARILLOAMARILLO

TIFTONTIFTON

SWEETWATERSWEETWATER

LOXLEYLOXLEY

EVERGREENEVERGREEN

McCALLAMcCALLA

STEELESTEELE

CLANTONCLANTON

FALKVILLEFALKVILLE

JASPERJASPER

MORRILTONMORRILTON

OZARKOZARK

PALESTINEPALESTINEWEST MEMPHISWEST MEMPHIS

LITTLE ROCKLITTLE ROCK

KINGMANKINGMAN

QUARTZSITEQUARTZSITE

GILA BENDGILA BEND

CHANDLERCHANDLER

YUMAYUMA

LAKE HAVASULAKE HAVASU

BENSONBENSON

COACHELLACOACHELLA

RIPONRIPON

LOST HILLSLOST HILLS

TULARETULARE

TEHACHAPITEHACHAPI

CORNINGCORNING

SANTA NELLASANTA NELLA

LAMARLAMAR

BENNETTBENNETT

HUDSONHUDSON

PUEBLOPUEBLO

FT. PIERCEFT. PIERCEAUBURNDALEAUBURNDALE

OCALAOCALA

JASPERJASPER

EMERSONEMERSON

JACKSONJACKSON

THOMSONTHOMSON

HOGANSVILLEHOGANSVILLE

RICHMOND HILLRICHMOND HILL

BRUNSWICKBRUNSWICK

DUBLINDUBLINDUBLINDUBLINDUBLINDUBLINDUBLINDUBLIN

NEWTONNEWTON DAVENPORTDAVENPORT

SIOUX CITYSIOUX CITY

CLIVECLIVE

POSTFALLSPOSTFALLS

GREENVILLEGREENVILLE

WILLIAMSVILLEWILLIAMSVILLE

UTICAUTICA

ROSCOEROSCOE

DWIGHTDWIGHT

KANKAKEEKANKAKEE

MARIONMARION

RICHMONDRICHMONDPITTSBOROPITTSBORO

ST. PAULST. PAUL

MEMPHISMEMPHIS

BELLEVILLEBELLEVILLE

GARYGARY

HAUBSTADTHAUBSTADT

WHITESTOWNWHITESTOWN

OTTAWAOTTAWA

ELLISELLIS

RICHMONDRICHMOND

CORBINCORBIN

HORSE CAVEHORSE CAVECALVERT CITYCALVERT CITY

SHEPHERDSVILLESHEPHERDSVILLE

WADDYWADDY

GRAYSONGRAYSON

PORT ALLENPORT ALLENLAKE CHARLESLAKE CHARLESVINTONVINTON

GREENWOODGREENWOOD MINDENMINDEN TALLULAHTALLULAH

ALBERT LEAALBERT LEAALBERT LEAALBERT LEA

MARSHALLMARSHALL

ST. JOSEPHST. JOSEPH

JOPLINJOPLIN

ROLLAROLLAROLLAROLLA

CANTONCANTON

BATESVILLEBATESVILLE

FLOWOODFLOWOOD

FARGOFARGO

WILLISTONWILLISTON

NORTH PLATTENORTH PLATTE

AURORAAURORA

BORDENTOWNBORDENTOWN

ALBUQUERQUEALBUQUERQUE

CLAYTONCLAYTON

LAS CRUCESLAS CRUCES

LORDSBURGLORDSBURG

GALLUPGALLUP

CLOVISCLOVIS

FERNLEYFERNLEY

LAS VEGASLAS VEGAS

BINGHAMTONBINGHAMTON

JEFFERSONVILLEJEFFERSONVILLE

HUBBARDHUBBARD

N. BALTIMOREN. BALTIMORE

ZANESVILLEZANESVILLE

BURBANKBURBANK

CLINTONCLINTONELK CITYELK CITY

NORMANNORMAN

LAWTONLAWTON

BOISE CITYBOISE CITY

ERICKERICK

EUFAULAEUFAULA

PAULS VALLEYPAULS VALLEY

TONKAWATONKAWA

WEBBERS FALLSWEBBERS FALLS

HOOKERHOOKER

ATOKAATOKA

HINTONHINTON

OKEMAHOKEMAH

COLBERTCOLBERT

ROSEBURGROSEBURG

ONTARIOONTARIO

TROUTDALETROUTDALE

JONESTOWNJONESTOWN

CARLISLECARLISLE

BLACKSBURGBLACKSBURGFT. MILLFT. MILL

NEWBERRYNEWBERRY

SIOUX FALLSSIOUX FALLS

COLUMBIACOLUMBIA

JACKSONJACKSON

MEMPHISMEMPHIS

DANDRIDGEDANDRIDGE

CHARLESTONCHARLESTON

LENOIR CITYLENOIR CITYBAXTERBAXTERNASHVILLENASHVILLE

CLAUDECLAUDE

DENTONDENTON

EL PASOEL PASO

HILLSBOROHILLSBORO

MIDLOTHIANMIDLOTHIAN

WALLERWALLER

MEMPHISMEMPHIS

VAN HORNVAN HORN

WICHITA FALLSWICHITA FALLS

RANGERRANGERWEATHERFORDWEATHERFORD

LULINGLULING

VANVAN

LUFKINLUFKIN

CLEVELANDCLEVELAND

EDNAEDNA

FAIRFIELDFAIRFIELD

HUTCHINSHUTCHINS

KINGSVILLEKINGSVILLE

LAREDOLAREDO

RHOMERHOME

HEARNEHEARNE

ODESSAODESSA

BAYTOWNBAYTOWN

MT. VERNONMT. VERNON

ANTHONYANTHONY

COMFORTCOMFORT

NATALIANATALIA

DEER PARKDEER PARKWEIMARWEIMAR

CEDAR CITYCEDAR CITY

SALT LAKE CITYSALT LAKE CITY

TOMSBROOKTOMSBROOK

SKIPPERSSKIPPERSSOUTH HILLSOUTH HILL

NAPAVINENAPAVINE ELLENSBURGELLENSBURG

TACOMATACOMA

WAMSUTTERWAMSUTTER

OAK CREEKOAK CREEK

N. LITTLE ROCKN. LITTLE ROCK

JOSEPH CITYJOSEPH CITY

BARSTOWBARSTOW

WHITELANDWHITELAND

TUCUMCARITUCUMCARI

PERRYSBURGPERRYSBURG

ARDMOREARDMORE

ORANGEBURGORANGEBURG

DICKSONDICKSON

LEARYLEARY

CHEYENNECHEYENNE

MAX MEADOWMAX MEADOW

PRESCOTTPRESCOTT

ANNAANNA

MARIONMARION

WACOWACO

ORMOND BEACHORMOND BEACH

BOONVILLEBOONVILLE

RIPLEYRIPLEY

SPARTASPARTA

CONNEAUTCONNEAUT

RUTHERGLENRUTHERGLEN

STRAFFORDSTRAFFORDSTRAFFORDSTRAFFORD

BUCKEYEBUCKEYE

MIFFLINVILLEMIFFLINVILLE

DILLONDILLON

LEROYLEROY

ELOYELOY

KATYKATYSAN ANTONIOSAN ANTONIO

FT. WORTHFT. WORTH ROCKWALLROCKWALL

DALLASDALLAS

SEGUIN

WILLISWILLIS

HOUSTONHOUSTON

OKLAHOMA CITYOKLAHOMA CITY

CNG AVAILABLE NOW

CNG COMING SOON

FEASIBLE CNG STATIONS

CNG UNLIKELY

FA

Source: Love’s Travel Stops and Country Stores, August 3, 2013 presentation

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 18

America’s Natural Gas HighwayClean Energy Fuels, the largest provider of NG fuel for transportation in North America, in July 2011 was the first private company to jump aggressively into supplying NG infrastructure when it announced plans to construct America’s Natural Gas Highway, a network of 150 public access LNG-fuelling stations, across 33 states. So far, about 70 stations have been completed, although rollout is proceeding slower than originally anticipated, partly due to Clean Energy’s desire to secure anchor tenants before construction of new facilities. Using two liquefaction plants, one planned and one operational, Clean Energy will supply both

stages of the supply chain, production and marketing.

Clean Energy has also entered into a partnership with Pilot Flying J Truck Travel Centers, which will allow Clean Energy to add NG fuelling options to the services already offered at Pilot Flying J’s extensive network of existing truck stops throughout the United States. Clean Energy also intends to add CNG-fuelling capacity at selected locations on the network, as and where it determines there will be sufficient demand to support such facilities.

Figure 12 Projected rollout of Clean Energy’s America’s Natural Gas Highway of LNG and LCNG stations

Source: Clean Energy Fuels

Shell and TravelCenters of America partnershipShell and TravelCenters of America announced in April 2013 that they would partner to provide a nationwide network of LNG fueling stations for heavy-duty road transportation customers. The companies intend to construct at least two LNG fueling lanes and a storage facility at 100 existing TravelCenters of America or Petro Stopping Centers full service travel centers located along the U.S. interstate highway system. Shell anticipates that the first of these stations will be operational within a year and intends to make it a priority to develop LNG fueling infrastructure along the main trucking corridors. Shell is also investing in both LNG liquefaction and refuelling infrastructure, and plans to build two

liquefaction plants. These will supply the basis for two new LNG refuelling networks, in the Gulf Coast Corridor (Texas and Louisiana) and the Great Lakes Corridor. These Shell-fueled networks have the potential to link up with planned or existing clean transportation corridors, including the Texas Triangle and the I-75 Clean Transportation Corridor. Market observers suggest that Shell’s entry into the NG market is serving as a wake-up call signaling the growing importance of NG as a transportation fuel, as Shell is a major multinational player with the scale and resources to transform this domestic U.S. LNG market substantially.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 19

Figure 13 Projected network of LNG stations proposed by Shell and TravelCenters of America partnership

Source: Shell

ENN initiativesChinese-owned ENN is also investing heavily in U.S. LNG fuelling infrastructure, with plans to build up to 500 LNG stations. ENN has partnered with a small

Utah company, CH4 Energy, to create a joint venture trading as Blu LNG. ENN has ambitions of building LNG plants in the future.

Figure 14 Blu LNG operational and pending LNG fuelling network (as of end 2013)

Source: Blu LNG, http://blulng.com/station-finder/

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 20

1.5 Expansion of Small and Midsize LNG Liquefaction Plants

Crucial to the rollout of a wider use of LNG as a transportation fuel is increasing geographic access

to its supply, which is partly being achieved by developing small and midscale LNG liquefaction infrastructure. Gas producers, suppliers, utilities, and public companies are planning and building new facilities.

Figure 15 Small and Mid Scale LNG Liquefaction plants*

*Planned and operational small and mid scale liquefaction facilities in the United States, where the location has been made public or disclosed directly to FC Business Intelligence.

Table 3 Small and Mid Scale LNG Liquefaction plants in the United States*

P = Planned E = Expansion O = Operational S = Site Selection C = Construction R = Reg . approvals*Details disclosed/available

Small-Mid Scale LNG Liquefaction Faciliies in the US*

Map Key Name Location LNG production Stage

1 Noble Energy Weld County, Colorado 100,000 gal/day P

2 APNG Topock LNG Plant Arizona 86,000 gal/day E

3 Clean Energy California Plant Boron, California 160,000 gal/day O

4 The Pickens Plant Willis, Texas 100,000 gal/day O

5 Shell, Geismar Geismar, Louisiana 250,000 P

6 Shell, Sarnia Sarnia, Ontario 250,000 P

7 Stabilis Energy Eagle Ford Shale 100,000/250,000 R

8 Stabilis Energy West Texas 100,000/250,000 S

9 Stabilis Energy The Bakken 100,000/250,000 S

10 Stabilis Energy Western Oklahoma 100,000/250,000 S

11 Stabilis Energy Haynesville, East Texas 100,000/250,000 S

12 Grande Prairie Elmworth, Canada 190,000 litres/day C

13 Colony Energy Partners Reno 180,000 gal/day (initial) P

14 Spectrum LNG Prudhoe Bay, Alaska 100,000 gal/day P

15 Spectrum LNG Ehrenberg, Arizona 60,000 gal/day O

16 Exxon LaBarge Shute Creek, WY 60,000 gal/day O

17 Prometheus Bowerman LFG to LNG California 5,000 gal/day O

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 21

1.6 Conclusion

Natural gas has significant potential to displace diesel and gasoline usage in the transportation sector. NG prices are both cheaper than either diesel or gasoline, and are also less volatile. NG is largely sourced in North America, especially the U.S., in contrast to oil and diesel, which are largely foreign-sourced, from politically unstable and potentially hostile regions of the world, especially the Middle East.

The number of CNG and LNG public access fuelling stations is expanding rapidly. Several companies have committed themselves to rolling out new NG infrastructure. On the CNG side, Trillium and Love Travel Stops have announced extensive plans, while on the LNG side, Shell, and ENN in a joint venture with Blu LNG, are major players. Clean Energy has also announced an extensive LNG plan, America’s Natural Gas Highway, and in partnership with Pilot Flying J truck stops is also exploring LCNG options.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 22

Chapter 2: Government policies: How they will shape the NGV market over the next 5 years

2.0 Introduction

Government policies, at both federal and state levels, have played a significant role in fostering the development of NG as a transportation fuel. The following chapter describes how such policies will continue to shape the future development of the NGV sector, focusing on the next five years. The chapter begins by discussing various state and federal policies to promote NGVs, including subsidies, tax incentives, procurement policies, and emissions standards. The chapter concludes by discussing two potential policy risk factors that could thwart or at minimum slow development of NGVs—environmental regulation, and export policy.

2.1 Policy in context

The DoE in 1993 launched the Clean Cities initiative, the flagship federal program designed to reduce petroleum consumption for transportation uses by promoting the use of alternative fuel vehicles. This program created a national network of more than 100 Clean Cities coalitions, which link fuel suppliers, private companies, original equipment manufacturers (OEMs), federal and state agencies, national laboratories, and local governments, among others, in designing and implementing alternative transportation policies for their local communities. Clean Cities seeks to reduce the use of fossil fuels by measures such as using alternative and renewable fuels, making improvements in fuel economy, and promoting emerging transportation technologies.

2.2 Subsidies and tax incentives

The significant and sustained lower relative cost of NG compared to petroleum-based fuels provides a strong incentive for fleets and individuals to shift to NGVs. Yet those who seek to make such a switch face two significant obstacles: the higher upfront cost of NGVs, whether automobiles, vans, or light, medium,

or heavy-duty trucks, compared to diesel or gasoline-powered vehicles; and the lack of a comprehensive fuelling infrastructure for either CNG or LNG vehicles.

Both the federal government and many state governments provide a plethora of subsidies, tax incentives, and loan programs to address these two obstacles (some of these incentive programmes are discussed more fully below—see sections 3.__ and 3.__, and 4.__ and 4.__). These public policies promote the use of NGVs (and other alternative fuel vehicles) by defraying their higher upfront costs and also support build-out of more NG fuelling stations. Other policies provide incentives to use alternative fuel vehicles—such as the ability to use high occupancy vehicle (HOV) lanes regardless of the number of passengers in a vehicle.

Most of the NG-specific policies the United States has in place promote the use of NG. But one federal excise tax policy currently disadvantages LNG, and this measure has attracted many reform calls among various NGV stakeholders. The federal excise tax on both LNG and diesel is currently 24.3 cents per gallon, but since it takes 1.7 gallons of LNG to produce the same amount of energy that a gallon of diesel produces, LNG is effectively taxed at a rate 70% higher than that of diesel. Both gasoline and CNG are also taxed according to energy output, leaving LNG as the odd fuel out.

Taxing the fuels on an energy content basis rather than on a volume basis would create a level playing field for LNG, and Mac Thornberry, a member of the United States House of Representatives from Texas in 2013 introduced the LNG Excise Tax Equalization Act of 2013 (H.R.2202), to achieve that goal. Thornberry believes that this reform would promote expanded private-sector investment in LNG infrastructure and production.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 23

Senator Michael Bennet of Colorado has introduced a companion bill, S. 1103, l into the United States Senate, but as of October 2013, the measures had been referred to their respective committees for consideration, and no further action has been taken on these measures.

The federal government currently has twenty-seven NG promotion policies in place, covering a range of areas, including infrastructural development, HOV lane use, aftermarket conversions, public transportation, and technological development. The DoE’s AFDC regularly updated website provides current summaries of existing federal policies: http://www.afdc.energy.gov/laws/laws/US/tech/3253

All states currently have at least one NG promotion policy in place, and the DoE’s AFDC website allows to search current such policies by fuel, and by state. Many urban states are strong NG supporters, including California (with 27 NG policies in place), Virginia (16), and Indiana (18). States that produce NG also promote its use, these include Colorado (11), Oklahoma (14) Texas (15), and Utah ( 10). http://www.afdc.energy.gov/laws/matrix/tech.

Policies fall to three broad areas: those that offset the incremental costs of NGV purchase; those that provide fuel incentives; and those that provide special privileges to NGV users (e.g., access to HOV lanes, additional parking, concessions on emissions inspections).

California has led the way in promoting clean air policies, and adopted its Air Pollution Control Act in 1947—nearly a decade before the federal government began to address air quality issues. The state has been at the forefront of promoting the use of alternative fuels, and currently has 27 NG state incentives in place—more than any other state— and these include policies to promote NGVs, to encourage NG infrastructural development, to advance the use of NG for public transit, and to foster NG-related technological development.

The DoE’s AFDC website summarises the state’s current policies http://www.afdc.energy.gov/laws/laws/CA/tech/3253

California has pioneered some innovative alternative fuel promotion policies, including parking incentives, and the ability to use HOV lanes regardless of the number of passengers in a vehicle. Drivers of qualifying alternative fuel vehicles—including CNG, hydrogen, electric, and plug-in hybrids-- that meet specified state and federal emissions standards are given special stickers. Vehicles are also exempted from certain toll charges, unless prohibited by federal law.

On September 28 Governor Jerry Brown signed into law a bill that will extend various other clean vehicle incentive programs until 2023. He also signed another piece of legislation that will extend for HOV lane access for certain alternative fuels vehicles until January 1, 2019.

2.3 Procurement policy

Both federal and state governments can advance the use of NGVs via the procurement policies they enact.

Federal policy President Obama issued a Presidential Memorandum in May 2011 directing all federal agencies to purchase or lease only alternative fuel passenger vehicles or LD trucks by 2015. This policy required no congressional action to be implemented and took immediate effect upon announcement. Mandating the use of alternative fuel vehicles for federal fleets was expected to have the direct effect of stimulating demand for such vehicles and, by creating economies of scale, reducing the upfront costs of such vehicles, thus increasing their attractiveness to a wider market. Further, in the case of NGVs, placing more of them on the road was also intended to increase utilization of existing NG infrastructure, and promote demand for additional fuelling stations. The policy was also expected to have indirect effects, as drivers of these vehicles will increase their familiarity with these vehicles and, in the case of NGVs, become aware of their far lower fuelling cost compared to petroleum-fuelled vehicles.

State policy States have followed the federal lead in developing their own NGV procurement policies. The governors of Colorado, Wyoming, Pennsylvania, and Oklahoma

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 24

announced a Memorandum of Understanding (MOU) in November 2011 to work together to convert their state vehicle fleets to NG. The MOU calls for a joint, multistate request for proposal for purchasing NGs for state fleets, and commits each state to purchase a specific number of NGVs. Many state fleets standing alone are not large enough convince OEMs that the vehicle needs of individual states represent a viable, stable, long-term market upon which to base product launch decisions. By developing a common proposal for NGV purchases and pooling their resources, the states hope to encourage OEMs to offer a wider range of NGVs. More than 20 states are now committed to follow this NGV sourcing approach.

These procurement policies have already influenced product offerings. The three major U.S.-headquartered OEMs – Chrysler, Ford, and GM (Chevrolet) – have all launched bi-fuel pickup trucks, and GM and Ford offer a bi-fuel van for commercial and fleet customers. Honda is the first OEM to offer a NG-fuelled automobile, the Civic NG, nationwide to non-fleet customers, and Chevrolet intends to offer its Impala model in a bi-fuel option for model year 2015. Various other companies offer competitive NG-conversion options.

Private initiativesThese public procurement initiatives have inspired the American Clean Skies Foundation to develop a wider procurement plan for the third-party transportation services used by the federal government. Every year, federal agencies spend roughly $150 billion on such transportation services.

The foundation has proposed requiring federal agencies to apply to third-party transportation providers the same kinds of alternative fuel targets, efficiency standards and reporting practices they currently apply to their own vehicle fleets. Such a policy would reduce overall oil consumption—and its associated economic and environmental costs. The foundation estimates that the programme it outlined in an August 2012 report could deliver approximately $7 billion in annual cost savings; cut petroleum consumption by billions of gallons each year; stimulate the introduction of tens of thousands of new alternatively fuelled vehicles; and reduce

greenhouse gas emissions by over 20 million metric tons annually. Moreover, the foundation emphasizes that by leveraging its influence with freight carriers and other suppliers, such a programme would allow the federal government an opportunity to create very large multiplier effects, and thus effectively reduce the dependence of the trucking industry and other private sector transportation providers on petroleum imports.

2.4 CAFÉ standards

The United States in 1975 first implemented Corporate Average Fuel Economy (CAFÉ standards) to encourage manufacturers to produce more fuel-efficient cars. The Obama administration and thirteen OEMs on August 28, 2012 announced new standards for automobiles, and light and medium duty trucks, levelling the playing field between NG and other alternative fuels for these categories of vehicles. These standards cover model years 2017-2025. The standards are ambitious ones, which by setting an average fuel economy standard of 54.5 miles per gallon (MPG) by 2025—double the 27.3 MPG 2011 average-- are intended to push OEMs toward technological innovation. The standards include tax incentives for purchase of certain types of alternative fuel vehicles, and an incentive multiplier to encourage adoption of fuel. The highest multiplier, 2.0, applies to electric vehicles; NGVs and hybrids enjoy a multiplier of 1.6—a significant improvement on the previous standard.

The Obama administration was the first to launch emissions standards for heavy-duty vehicles in 2011. These are due to be revised and extended soon, with a proposed rule expected imminently, which will be finalized sometime in 2015.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 25

2.5 Environmental regulation: potential risk?

One potential risk factor for broader NGV development is whether additional environmental restrictions will be imposed on fracking operations. At the federal level, the Bureau of Land Management sets drilling standards for federal lands, and the Environmental Protection Agency (EPA) has broad influence over fracking due to its authority to set air and water quality standards. The EPA in 2012 set air quality standards for fracking operations, requiring companies to capture gases released in the process—but these measures only codified best industry practices. The EPA is expected to announce fracking-related water quality standards in 2014, and is expected to take a similar approach.

The fracking industry remains vulnerable to the risk of lawsuits, which are largely brought under state law. Landowners have targeted energy companies in many states where fracking is widespread, in some cases, via class action lawsuits. But the United States Supreme Court has in recent years made it much more difficult for private plaintiffs to succeed in such lawsuits, especially, in class actions. So far, no company has lost a fracking suit, and the barriers to prevailing in such litigation for alleged harms including groundwater contamination, triggering of earthquakes, or environmental degradation, are formidable. The possibility exists that lawsuits or state-level policy changes could slow the spread of fracking in certain states. Yet absent a major shift in the composition of either Congress or the Supreme Court, it is unlikely that fracking lawsuits will impose major constraints on energy producers nationwide.

2.6 Export policy: potential risk?

United States NG export policy could also have a significant impact on the development of NG as a transportation fuel. Until recently, NG from domestic sources was not traded widely outside North America, and the United States did not export significant quantities of NG. In fact, before the shale gas revolution began, plans were underway to allow importation of substantial quantities of NG, and these

included proposals to develop the infrastructure to achieve this goal. Some of the NG export terminals discussed below were originally intended to be import facilities.

Now, as domestic NG reserves continue to be developed, and the spread between NG and world oil prices continues to be so wide, this situation has reversed itself. Yet U.S. NG exports are subject to a complex export regime, which requires federal government approval of NG export facilities and involves separate permitting processes undertaken by the DoE and the Federal Energy Regulatory Commission (FERC). To date, the DoE has approved four applications to permit export of U.S.-produced LNG have been approved, and more than twenty are pending. In 2011, the DoE approved Cheniere Energy’s Sabine Pass project, located on the Sabine River in the Louisiana/Texas border, thus clearing the way for the first new LNG construction in forty years (this project had originally been planned as an import terminal). Final clearance for this project led to a pause in consideration of other export applications. During this period, two studies were undertaken that examined the expected impact of NG exports on domestic prices, and in this interim period, NG exports were authorized to countries with which the US has free trade agreements, such as Canada and Mexico -- both members of the North American Free Trade Agreement (NAFTA).

In 2013, the DoE has approved three projects for export to non free-trade agreement destinations: Freeport LNG’s in Quintana Island, Texas, in May; Lake Charles LLC’s in Lake Charles, Louisiana, in August; and Dominion Resources’s Cove Point facility on Maryland’s Chesapeake Bay, in September. The DoE has seemingly accelerated its review process in response to political and company complaints about previous delays, and is currently reviewing expansion of Freeport LNG’s terminal in Freeport, Texas; Sempra Energy’s proposed project in Cameron, Louisiana; and Veresen’s Jordan Cove project in Coos Bay, Oregon.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 26

Table 4 LNG Export facilities approved

Company Location State Date

Cheniere Energy

Sabine Pass Louisiana/Texas border

Apr 2012

Freeport LNG Quintana Island

Texas May 2013

Lake Charles LLC

Lake Charles Louisiana Aug 2013

Dominion Resources

Cove Point (Chesapeake Bay)

Maryland Sep 2013

NG producers view exports as a way to earn higher prices than are available for NG in either the domestic U.S. or wider North American market. Yet significant LNG exports could distort the domestic supply/demand relationship, and thereby raise domestic NG prices. As long as NG is largely traded within North America, prices remain insulated from the volatility (and outright manipulation) that occurs in the world oil market.

The acceleration of export procedures is already provoking a backlash. Cove Point’s conditional approval to export up to 0.77 Bcf/d of NG raises the overall amount of permitted NG exports, breaching the export levels of 6 Bcf/d — the “low export scenario” — set forth in an earlier report commissioned by the DoE that examined the impact of NG exports on domestic prices and on which the agency relied in approving three previous LNG export applications.

America’s Energy Advantage (AEA), a coalition of manufacturers and consumers, is working to reserve US NG to promote a US manufacturing renaissance. AEA members include domestic-headquartered companies such as Alcoa, Celanese, Dow Chemical, Eastman, Huntsman, and Nucor, and trade associations, such as the American Public Gas Association (APGA). Its membership also includes firms such as Incitec Pivot, a global explosives and fertilizer manufacturer based in Australia, that recently began construction of an $850 million ammonia plant in Waggaman, Louisiana.

In September 2013, AEA filed a formal motion to intervene in the DOE’s proceeding evaluating Freeport LNG’s export application for its Freeport, Texas terminal. This application, if authorized would raise the cumulative volume of authorized LNG exports to 8.31 Bcf/d.

AEA seeks to encourage the DoE to develop a more formal rulemaking process based on current data and assessments of the current supply and demand environment. AEA asserts that current LNG export applications are being granted based on guidelines developed for NG imports in the 1980s. AEA’s motion also alleges that the legal standards the DOE used to analyse the public interest in two previous permitting applications were not “adequate, appropriate, or sustainable.”

APGA and the Industrial Energy Consumers of America (IECA) are working toward developing a responsible production policy, arguing that while exporting NG might maximize the price domestic producers receive for their product, it will reduce the price advantage NG currently enjoys relative to refined diesel or gasoline, and thus reduce the attractiveness of NG as a transportation fuel. If that occurs, these organizations emphasize, NG’s full potential to reduce America’s energy dependency will not be achieved.

The DOE may choose to undertake another pause in its permitting procedures, but this is unlikely to occur before year-end 2013, when new data should be available from the Energy Information Administration’s preliminary annual energy outlook for 2014.

A lively debate is raging on how America’s NG reserves should be deployed—to maximize producer revenues, or to support domestic manufacturing and encourage energy self-sufficiency. Opponents of increased NG exports emphasise that if all pending export applications were to be approved, half of current NG supply would be exported. Instead, they advocate building necessary infrastructure to consume NG domestically, not only for transportation uses, but for power generation as well.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 27

2.8 Conclusion

Government policies, both federal and state, have played a major role in promoting the development of NG as a transportation fuel, and will continue to do so both in the near-term ad over the coming decades.

California has been a leader in developing alternative fuels, and currently has the most comprehensive NG fuelling infrastructure. While the state continues to lead the way in policy innovation, many other states are also on the NG bandwagon, and are providing various incentives as well as setting their own procurement policies, to promote NG use.

Although it at this point appears unlikely that environmental regulations or public or private lawsuits, may significantly slow U.S. shale gas production, the long-term shape of U.S. NG export policy is a cause for some concern, as it has the potential to equalise somewhat domestic and world NG prices, and thereby, reduce the economic case for fleets to switch to NG. A lively debate is brewing over whether NG should be reserved for domestic uses, pitting conflicting interests of NG producers against other among NG stakeholders. Since the setting of export policy requires federal government action, this debate will require political resolution at the highest level.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 28

Chapter 3: Converting to Natural Gas, Vehicle issues

3.0 Introduction

Despite the relative cost advantage for fuelling NGVs compared to traditional diesel or gasoline-fuelled models, the higher relative costs of NGVs compared to traditionally-fuelled vehicles has presented a major obstacle to wider use of NG as a transportation fuel. This chapter focuses on costs and other issues that should be considered when contemplating switching to NGVs, while the next discusses the equally important issue of ensuring access to adequate fuelling infrastructure.

OEMs have started to offer a wider range of NG options, from automobiles, to vans—both passenger and cargo—and light and medium-duty truck options. Total sales have been modest but growing, and each OEM has announced plans for expansion of NG product offerings in forthcoming model years. At least twenty-one states provide some form of incentive for fleets to convert to light-duty CNG vehicles, in the form of grants or rebates, loans, state tax credits, or combinations of these policies. With OEMs now offering a wider range of NGVs, the impact of these incentive policies may now be more pronounced. All major heavy-duty truck manufacturers offer NG options, either in CNG or LNG formats.

3.1 Passenger automobiles

The US market lags significantly behind the European market in the number of NG options offered as passenger vehicles. Currently, only Honda offers a CNG option, the Civic NG, nationwide in the US, compared to Europe, where many automakers, including Fiat, GM, Mercedes, Peugeot, Toyota and Volkswagen, offer CNG options. Honda is strongly committed to develop the US NGV market and has offered a CNG automobile option since 1998 in the US.

Chevrolet announced in October 2013 that it will launch a bi-fuel Impala, beginning with the 2015 model year, to both passenger and fleet customers. The vehicle will include both a CNG tank in the trunk, and a gasoline tank, allowing for a total range of up to 500 miles by switching between the two fuels-- 150 miles on CNG and 350 miles on gasoline. GM has neither announced an expected price, nor projected fuel economy figures, and expects to sell as many as 1000 vehicles, largely to fleets, during its first model year.

Despite a lack of strong consumer demand, OEMs recognize that shifting to NG provides immediate emissions benefits, without any need for further technological innovation, and thus help fulfil their obligations to meet emissions standards for their product offerings.

Two major obstacles have prevented wider consumer adoption of NGVs. Although the costs of operating CNG vehicles are much lower, consumers must first pay the higher incremental cost of buying a CNG vehicle. The actual break-even point depends on the higher incremental cost for the CNG vehicle, and average number of miles driven. Moreover, passenger cars face greater infrastructural obstacles, for unlike fleets, they do not necessarily drive in consistent and familiar patterns, and they lack access to dedicated fuelling arrangements—either company-owned, or third-party— that are available to fleets.

Use of NG is impractical, at present, for non-fleet passenger vehicles, outside of states that have well-developed CNG infrastructure, such as California, New York, Oklahoma, Texas, and Utah. In the near-term, there are other pockets where use of such vehicles might catch on, especially in bi-fuel options, which can reduce fuelling and range anxiety.

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 29

One looming technological innovation might promote popularity of NG as a transportation fuel for passenger vehicles: the development of a cheap, widely available home refuelling option. At present, consumers are making a switch in how they view fuelling options. Outside of remote rural areas, drivers are not accustomed to considering refuelling possibilities when they drive passenger cars. But this is changing, with the hybrids such as Toyota’s Prius and Chevrolet’s Volt.

Wider use of such vehicles may promote a shift in how drivers think about fuelling their cars. Electric vehicles have limited range, and are generally most useful for commuting short distances. Drivers are able to charge their batteries when the vehicle returns home.

The lack of a cost-effective home fuelling appliance is seen as a major impediment to the development

of the NGV passenger automobile market, one which the federal government has devoted part of $30 million in research funds to finance proposals to create such appliances. The Drive Natural Gas Initiative (DNGI), a major industry trade association launched its Home Fueling Appliance Task Force determine specifications for such a product. The appliance should be able to provide a fuelling rate of 1 GGE per hour, should provide for 6,000 hours of service, and should cost less than $1,500. This translates to a fuelling cost per GGE of CNG of $0.25 (in addition with the cost of the fuel itself and the cost of the electricity to run the compressor). The task force decided that the cost of the appliance, plus the premium paid for the CNG vehicle (compared to the same non-CNG model), must payout in 3 years or less, in order to support a sustainable market. Several utilities, and manufacturers, are joining to develop products that meet these specifications. The timeframe for launch remains at least eighteen months away.

Table 5 Home fuelling specifications

Source: America’s Natural Gas Alliance

3.2 Light and medium duty trucking vehicle options

The major OEMs have responded to demand for CNG-fuelled vehicles, and either now offer, or plan to offer for model year 2014, a mix of vans, and light and heavy duty pick-up trucks.

FordFord expects to sell 15,000 CNG/LPG-prepped vehicles in 2013, representing a 25% increase on its 2012 sales

of similar vehicles. Beginning with model year 2014, Ford intends to extend its product range and offer its F-150 truck with a gaseous-fuel prep option on the 3.7-liter V6 engine, enabling the vehicle to run on CNG or LPG. This prep package includes hardened valves, valve seats, pistons and rings so it can operate on either CNG/LPG or gasoline through separate fuel systems, and from the factory costs approximately

TCO

Base Case Miles % CNG NGV Cost HFA Cost High-Miles /High CNG %

Actual miles 13,476 26,583 18,719

Daily miles 37 73 51

CNG percent 55% 106% 80%

NGV Premium $4,000 723 -$1,277

HFA (installed) $2,000

Simple Payout (yrs) 8.0 3.0 3.0 3.0 3.0 3.0

Market of 10 millioncommuters

IND

USTRY O

VERV

IEW

For more information visit www.ngvevent.com NGV INDUSTRY OVERVIEW | 30