Natural Gas Demand Supply Trends in the Asia Pacificeneken.ieej.or.jp/en/data/pdf/210.pdf ·...

19

IEEJ:October 2003 1 Natural Gas Demand Supply Trends in the Asia Pacific Region *1 Takeo Suzuki, Group Manager, Gas Group, First Research Department Tetsuo Morikawa, Researcher, Gas Group, First Research Department *1 This report is the product of research in 2002 commissioned by the Ministry of Economy, Trade and Industry, which has approved disclosure of this report. We thank ministry staff members for their understanding and cooperation. As we prepared this report, a working group of experts in the natural gas businesses offered many helpful suggestions. The authors also wish to thank the members of Gas Group of IEEJ for their contributions, on which this report relies. This report was made based on information available as of March 2003. In August 2002, the players in Japan’s natural gas market received two items of interesting news. The first was that China had selected Australia to supply LNG for its first LNG receiving terminal to be constructed in Guangdong province; the second was that the company investigating the Sakhalin-Japan pipeline project had confirmed the project’s technical and commercial feasibility. Regarding the first one, China became a new importer in the Asia-Pacific LNG market, traditionally consisting of Japan, South Korea and Taiwan only. It was surprising that the LNG price for China was going to be 20 to 30% lower than that for the existing LNG importers in the region. The second one was important because building the Sakhalin pipeline could lead to the development of nation-wide gas pipeline network, which is a challenge for Japan’s gas market. This pipeline could improve the supply security through diversifying energy sources in addition to the form of LNG in natural gas supply in Japan and could increase bargaining power in pricing negotiations over LNG imports. Having begun to import LNG in 1969, Japan drastically increased import amount in the 1980s after two oil crises. Twenty years later, those LNG purchase contracts have reached or are reaching their renewal dates. Although it remains difficult to predict future LNG demand in an ongoing stagnant economy and deregulation, the demand for cheaper forms of energy (i.e., inexpensive LNG) has continued to grow as strong as ever. The LNG market has shifted from a seller's to a buyer's market since the early 1990s. Japan's energy companies, the world’s major LNG buyers, have tried to establish flexible trade conditions and to buy gas at lower prices. However, there is still much room for trade flexibility and price reduction. It is preferable for Japan that LNG prices will drop along with more flexible trade practices. This report summarizes the status of natural gas in the Asia-Pacific region with emphasis on LNG supply and demand as of spring 2003. 1. Reserves, production, and consumption of natural gas World natural gas reserves as of the end of 2001 were estimated to be 164.7 trillion cubic meters (TCM), with about 70% in the former Soviet Union and the Middle East. Conversely, the share of the Asia-Pacific region was a mere 14.9 TCM, accounting for less than 10%. World production in 2001 totaled 2.55 TCM, with North America and the former Soviet Union each accounting for about 30%, and the Asia-Pacific region for 11%.

Transcript of Natural Gas Demand Supply Trends in the Asia Pacificeneken.ieej.or.jp/en/data/pdf/210.pdf ·...

IEEJ:October 2003

1

Natural Gas Demand Supply Trends in the Asia Pacific Region*1

Takeo Suzuki, Group Manager,

Gas Group, First Research Department

Tetsuo Morikawa, Researcher, Gas Group, First Research Department

*1 This report is the product of research in 2002 commissioned by the Ministry of Economy, Trade and Industry, which

has approved disclosure of this report. We thank ministry staff members for their understanding and cooperation. As we prepared this report, a working group of experts in the natural gas businesses offered many helpful suggestions. The authors also wish to thank the members of Gas Group of IEEJ for their contributions, on which this report relies. This report was made based on information available as of March 2003.

In August 2002, the players in Japan’s natural gas market received two items of interesting news. The first was that China had selected Australia to supply LNG for its first LNG receiving terminal to be constructed in Guangdong province; the second was that the company investigating the Sakhalin-Japan pipeline project had confirmed the project’s technical and commercial feasibility. Regarding the first one, China became a new importer in the Asia-Pacific LNG market, traditionally consisting of Japan, South Korea and Taiwan only. It was surprising that the LNG price for China was going to be 20 to 30% lower than that for the existing LNG importers in the region. The second one was important because building the Sakhalin pipeline could lead to the development of nation-wide gas pipeline network, which is a challenge for Japan’s gas market. This pipeline could improve the supply security through diversifying energy sources in addition to the form of LNG in natural gas supply in Japan and could increase bargaining power in pricing negotiations over LNG imports. Having begun to import LNG in 1969, Japan drastically increased import amount in the 1980s after two oil crises. Twenty years later, those LNG purchase contracts have reached or are reaching their renewal dates. Although it remains difficult to predict future LNG demand in an ongoing stagnant economy and deregulation, the demand for cheaper forms of energy (i.e., inexpensive LNG) has

continued to grow as strong as ever. The LNG market has shifted from a seller's to a buyer's market since the early 1990s. Japan's energy companies, the world’s major LNG buyers, have tried to establish flexible trade conditions and to buy gas at lower prices. However, there is still much room for trade flexibility and price reduction. It is preferable for Japan that LNG prices will drop along with more flexible trade practices. This report summarizes the status of natural gas in the Asia-Pacific region with emphasis on LNG supply and demand as of spring 2003. 1. Reserves, production, and

consumption of natural gas World natural gas reserves as of the end of 2001 were estimated to be 164.7 trillion cubic meters (TCM), with about 70% in the former Soviet Union and the Middle East. Conversely, the share of the Asia-Pacific region was a mere 14.9 TCM, accounting for less than 10%. World production in 2001 totaled 2.55 TCM, with North America and the former Soviet Union each accounting for about 30%, and the Asia-Pacific region for 11%.

IEEJ:October 2003

2

World consumption in 2001 totaled about 2.55TCM. The major consumers include North America and the former Soviet Union, which are also major producers. Europe is a major consumer too, with well-developed pipeline networks, and also supplies natural gas within

the region, imports from Africa and the former Soviet Union. The Asia-Pacific region accounted for 12.5% of the world’s total consumption (see Table 1-1 and Figure 1-1).

Table 1-1 World natural gas reserves, production, and consumption (2001) Reserves Production Consumption

(BCM) Share (%) (BCM) Share (%) (BCM) Share (%)

North America 6,706 4.1 737.1 28.9 739.0 29.0

Latin America 8,046 4.9 137.4 5.4 137.4 5.4

Europe 7,997 4.9 305.7 12.0 497.1 19.5

Former Soviet Union 55,977 34.0 719.7 28.2 588.4 23.0

Africa 11,758 7.1 129.6 5.1 64.6 2.5

Middle East 59,351 36.0 233.6 9.2 206.6 8.1

Asia-Pacific 14,910 9.1 289.7 11.3 319.6 12.5

Total 164,745 100.0 2,552.7 100.0 2,552.7 100.0 Note: BCM = billion cubic meters, TCM = 1,000 BCM Source: Natural Gas in the World 2002, Cedigaz

Figure 1-1 Share of World natural gas reserves, production, and consumption by region (2001)

Source: Natural Gas in the World 2002, Cedigaz

���������������������

������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������

������������������������������������������

������������������������������������������

������������������������������������������

������������������������������������������

���������������������������������������������������������������

������������������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������

���������������������

��������������������� ���������������������

���������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������

���������������������������������������������������������������

0%

20%

40%

60%

80%

100%

埋蔵量 生産量 消費量

164,745BCM 2,552.7BCM 2,552.7BCM

Asia-Pacific region����

Middle East�������� Africa����

Former SovietUnion countries����Europe����

���� Latin America����

North America

Reserves Production Consumption

IEEJ:October 2003

3

In the Asia-Pacific region, 40% of gas reserves are in Malaysia and Indonesia, followed by 10.2% in China. In terms of production, Indonesia accounted for 23.8%, followed by Malaysia (18.5%) and Australia (11.7%). These countries export natural gas, mainly in the

form of LNG. In terms of consumption, Japan ranks first, accounting for 23.9%, followed by Indonesia (11.3%) and Malaysia (9.8%) that also consume domestic gas (see Table 1-2 and Figures 1-2 and 1-3).

Table 1-2 Natural gas reserves, production, and consumption

in the Asia-Pacific region (2001)

Source: Natural Gas in the World 2002, Cedigaz

Figure 1-2 Share of natural gas reserves, production, and consumption

in Asia-Pacific region by country (2001)

Source: Natural Gas in the World 2002, Cedigaz

(BCM) Share (%) (BCM) Share (%) (BCM) Share (%)

Japan 40 0.3 2.4 0.8 76.5 23.9

South Korea 0 0.0 0.0 0.0 21.8 6.8

Taiwan 76 0.5 0.8 0.3 6.6 2.1

Afghanistan 100 0.7 0.2 0.1 0.2 0.1

Australia 3,530 23.7 33.8 11.7 23.6 7.4

Bangladesh 332 2.2 9.9 3.4 9.9 3.1

Brunei 366 2.5 10.4 3.6 1.4 0.4

China 1,515 10.2 30.3 10.5 30.3 9.5

India 650 4.4 22.8 7.9 22.8 7.1

Indonesia 3,790 25.4 69.0 23.8 36.2 11.3

Malaysia 2,314 15.5 53.7 18.5 31.3 9.8

Myanmar 287 1.9 7.4 2.5 2.2 0.7

New Zealand 85 0.6 5.6 1.9 5.6 1.8

Pakistan 710 4.8 23.4 8.1 23.4 7.3

Papua New Guinea 428 2.9 0.1 0.0 0.1 0.0

Philippines 165 1.1 0.0 0.0 0.0 0.0

Thailand 352 2.4 18.7 6.5 23.9 7.5

Vietnam 170 1.1 1.3 0.4 1.3 0.4

Singapore 0 0.0 0.0 0.0 2.5 0.8

Total 14,910 100.0 289.7 100.0 319.6 100.0

Reserves Production Consumption

����������������������������������������������������������������������������

��������������������������������������

��������������������������������������������������������� �������������������

�������������������

���������������������������������������������������������

�����������������������������������������������������������������������������������������������

�����������������������������������������������������������������������������������������������

���������������������������������������������������������

���������������������������������������������������������

�������������������������������������� �������������������

�������������������

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

埋蔵量14,910BCM

生産量289.7BCM

その他�������� パキスタン��������

マレーシア����インドネシア����インド����

���� 中国

ブルネイ����オーストラリア

Other Pakistan Malaysia Indonesia India China Brunei Australia

Reserves Production

IEEJ:October 2003

4

Figure 1-3 Share of natural gas consumption in Asia-Pacific region by country (2001)

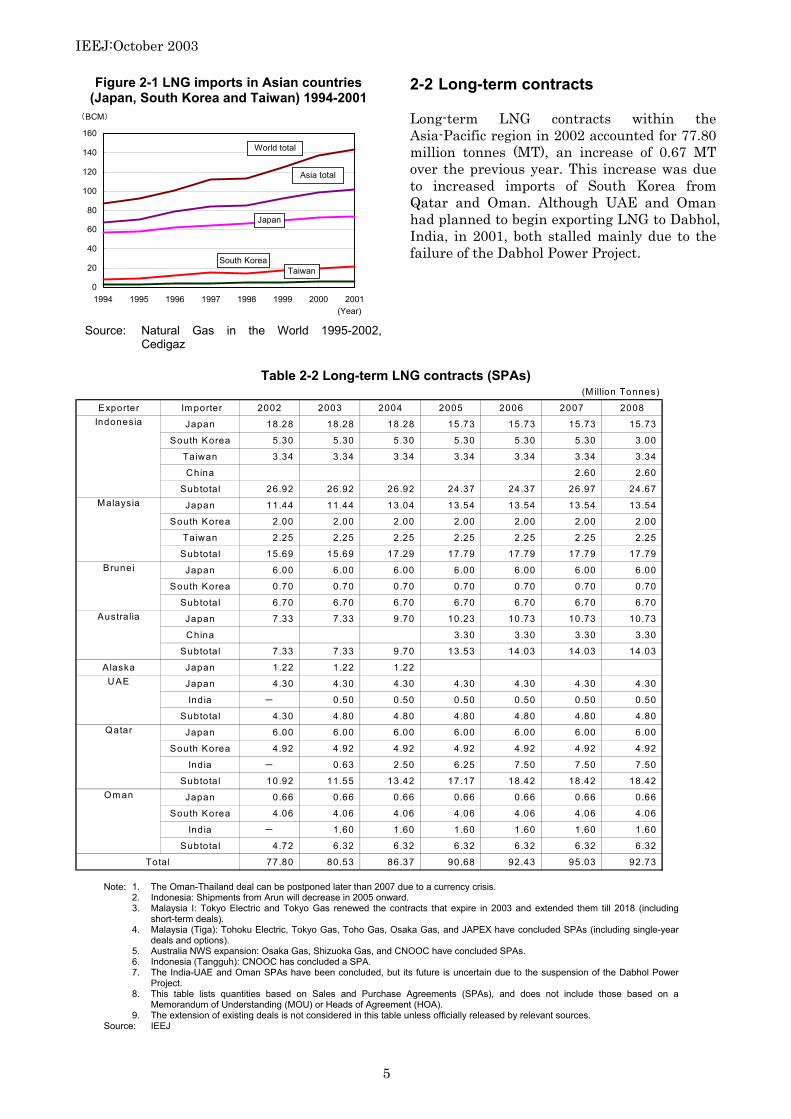

Source: Natural Gas in the World 2002, Cedigaz 2. LNG trade 2-1 Overview Of the total 554.3 billion cubic meters (BCM) world natural gas trade in 2001, 411.3 BCM (equivalent to 74%) was supplied via pipeline. Conversely, the share of LNG trades is increasing considerably, with 143 BCM worldwide in 2001 representing a 4.3% increase over 2000. The share of LNG imports by Asian countries (Japan, South Korea, and Taiwan) remained dominant, accounting for about 71.4% worldwide. Japan's LNG imports totaled 74.07 BCM in

2001 (up 2.0% from 2000), thus accounting for 51.8% of the world market. South Korea's share of LNG imports temporarily dropped in 1998 due to the economic crisis, but has since rebounded to reach 21.83 BCM (up 10.9% from 2000). Driven by strong demand for natural gas in the US and Europe, we can observe that new projects including in Nigeria and Trinidad-Tobago and existing projects with excess capacity supply the increasing amount of LNG to these markets (by about 1.4 times from 1998 to 2000).

Table 2-1 LNG imports in Asian countries (Japan, South Korea and Taiwan) 1994-2001

Source: Natural Gas in the World 1995-2002, Cedigaz

���������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

�������������������������������������������������������������������������������������������������������������������� �����

�������������������������

����������������������������������������������������������������������������������������������������������������������

������������������������������������������������������

������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������������������������������������

����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������������������������������������������������������������������������������������������������������������

�������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� ��������������������������������

������������������������������������������������������������������������������������������������

�����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

���������������������������������������������������������������������������

����������������������������������������������������������������������������������������������������

日本23.9%

韓国6.8%

オーストラリア7.4%中国

9.5%インド7.1%

インドネシア11.3%

マレーシア9.8%

パキスタン7.3%

タイ7.5%

その他9.3%

Japan

South Korea

Australia China India Indonesia

Others Thailand

Pakistan

Malaysia

1994 1995 1996

BCM % BCM % BCM % BCM %

Japan 56.80 64.7 57.92 62.3 61.94 61.5 64.34 57.4

South Korea 7.90 9.0 9.53 10.3 12.95 12.9 15.71 14.0

Taiwan 3.00 3.4 3.32 3.6 3.53 3.5 4.13 3.7

Asia total 67.70 77.2 70.77 76.2 78.42 77.9 84.18 75.1

World total 87.75 100.0 92.93 100.0 100.73 100.0 112.12 100.0

1998 1999 2000 2001

BCM % BCM % BCM % BCM %

Japan 66.22 58.5 69.42 55.8 72.59 52.9 74.07 51.8

South Korea 14.31 12.6 17.52 14.1 19.68 14.4 21.83 15.3

Taiwan 4.65 4.1 5.35 4.3 5.98 4.4 6.30 4.4

Asia total 85.18 75.2 92.29 74.2 98.25 71.7 102.20 71.4

World total 113.24 100.0 124.37 100.0 137.10 100.0 143.11 100.0

Importer

Importer

1997

IEEJ:October 2003

5

Figure 2-1 LNG imports in Asian countries (Japan, South Korea and Taiwan) 1994-2001

Source: Natural Gas in the World 1995-2002, Cedigaz

2-2 Long-term contracts Long-term LNG contracts within the Asia-Pacific region in 2002 accounted for 77.80 million tonnes (MT), an increase of 0.67 MT over the previous year. This increase was due to increased imports of South Korea from Qatar and Oman. Although UAE and Oman had planned to begin exporting LNG to Dabhol, India, in 2001, both stalled mainly due to the failure of the Dabhol Power Project.

Table 2-2 Long-term LNG contracts (SPAs)

Note: 1. The Oman-Thailand deal can be postponed later than 2007 due to a currency crisis. 2. Indonesia: Shipments from Arun will decrease in 2005 onward. 3. Malaysia I: Tokyo Electric and Tokyo Gas renewed the contracts that expire in 2003 and extended them till 2018 (including

short-term deals). 4. Malaysia (Tiga): Tohoku Electric, Tokyo Gas, Toho Gas, Osaka Gas, and JAPEX have concluded SPAs (including single-year

deals and options). 5. Australia NWS expansion: Osaka Gas, Shizuoka Gas, and CNOOC have concluded SPAs. 6. Indonesia (Tangguh): CNOOC has concluded a SPA. 7. The India-UAE and Oman SPAs have been concluded, but its future is uncertain due to the suspension of the Dabhol Power

Project. 8. This table lists quantities based on Sales and Purchase Agreements (SPAs), and does not include those based on a

Memorandum of Understanding (MOU) or Heads of Agreement (HOA). 9. The extension of existing deals is not considered in this table unless officially released by relevant sources. Source: IEEJ

(BCM)

0

20

40

60

80

100

120

140

160

1994 1995 1996 1997 1998 1999 2000 2001

Japan

Taiwan

World total

South Korea

Asia total

(Year)

(Million Tonnes)

Exporter Im porter 2002 2003 2004 2005 2006 2007 2008

Japan 18.28 18.28 18.28 15.73 15.73 15.73 15.73

South Korea 5.30 5.30 5.30 5.30 5.30 5.30 3.00

Taiwan 3.34 3.34 3.34 3.34 3.34 3.34 3.34

China 2.60 2.60

Subtotal 26.92 26.92 26.92 24.37 24.37 26.97 24.67

Japan 11.44 11.44 13.04 13.54 13.54 13.54 13.54

South Korea 2.00 2.00 2.00 2.00 2.00 2.00 2.00

Taiwan 2.25 2.25 2.25 2.25 2.25 2.25 2.25

Subtotal 15.69 15.69 17.29 17.79 17.79 17.79 17.79

Japan 6.00 6.00 6.00 6.00 6.00 6.00 6.00

South Korea 0.70 0.70 0.70 0.70 0.70 0.70 0.70

Subtotal 6.70 6.70 6.70 6.70 6.70 6.70 6.70

Japan 7.33 7.33 9.70 10.23 10.73 10.73 10.73

China 3.30 3.30 3.30 3.30

Subtotal 7.33 7.33 9.70 13.53 14.03 14.03 14.03

Alaska Japan 1.22 1.22 1.22

Japan 4.30 4.30 4.30 4.30 4.30 4.30 4.30

India - 0.50 0.50 0.50 0.50 0.50 0.50

Subtotal 4.30 4.80 4.80 4.80 4.80 4.80 4.80

Japan 6.00 6.00 6.00 6.00 6.00 6.00 6.00

South Korea 4.92 4.92 4.92 4.92 4.92 4.92 4.92

India - 0.63 2.50 6.25 7.50 7.50 7.50

Subtotal 10.92 11.55 13.42 17.17 18.42 18.42 18.42

Japan 0.66 0.66 0.66 0.66 0.66 0.66 0.66

South Korea 4.06 4.06 4.06 4.06 4.06 4.06 4.06

India - 1.60 1.60 1.60 1.60 1.60 1.60

Subtotal 4.72 6.32 6.32 6.32 6.32 6.32 6.32

Total 77.80 80.53 86.37 90.68 92.43 95.03 92.73

UAE

Qatar

Om an

Indonesia

Malaysia

Brunei

Australia

IEEJ:October 2003

6

_______________________________ *2 One-year or shorter-term deals *3 Tohoku Electric announced that it had procured 0.9MT from Bontang, 0.34MT from Malaysia, 0.4MT from Qatar,

and 0.06MT each from Oman and Australia (for a total of 1.7 MT) as alternative gas supplies.

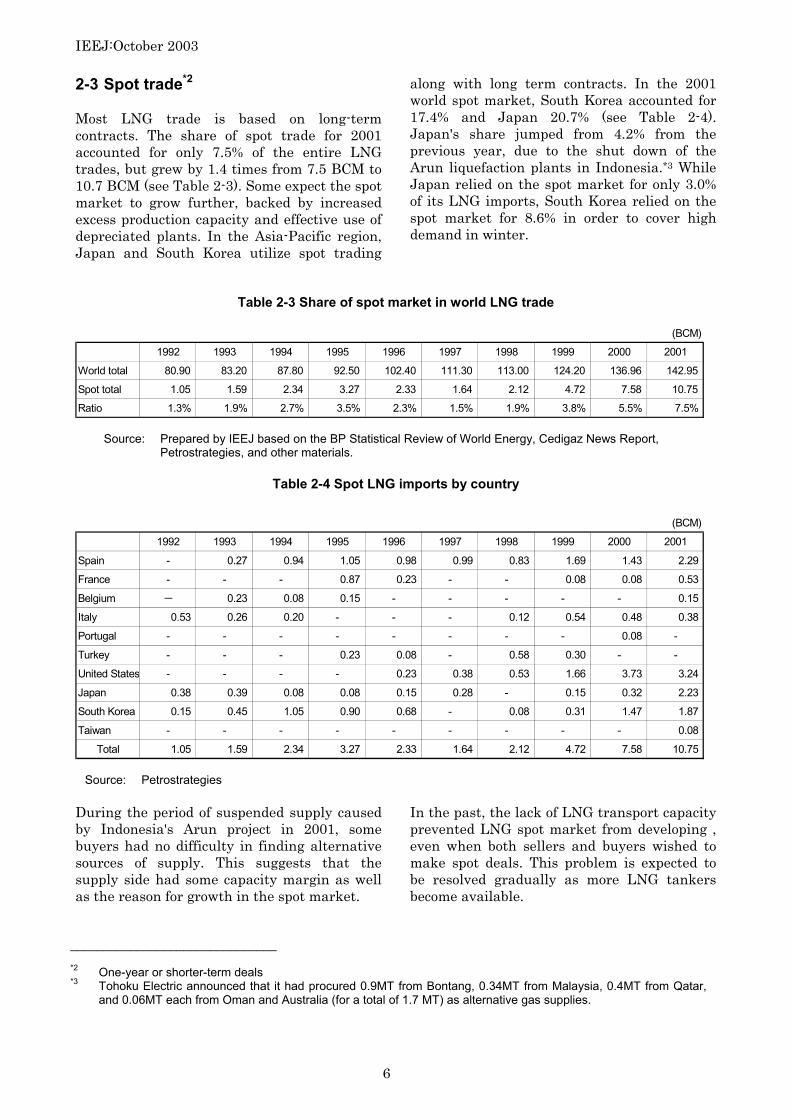

2-3 Spot trade*2 Most LNG trade is based on long-term contracts. The share of spot trade for 2001 accounted for only 7.5% of the entire LNG trades, but grew by 1.4 times from 7.5 BCM to 10.7 BCM (see Table 2-3). Some expect the spot market to grow further, backed by increased excess production capacity and effective use of depreciated plants. In the Asia-Pacific region, Japan and South Korea utilize spot trading

along with long term contracts. In the 2001 world spot market, South Korea accounted for 17.4% and Japan 20.7% (see Table 2-4). Japan's share jumped from 4.2% from the previous year, due to the shut down of the Arun liquefaction plants in Indonesia.*3 While Japan relied on the spot market for only 3.0% of its LNG imports, South Korea relied on the spot market for 8.6% in order to cover high demand in winter.

Table 2-3 Share of spot market in world LNG trade

Source: Prepared by IEEJ based on the BP Statistical Review of World Energy, Cedigaz News Report,

Petrostrategies, and other materials.

Table 2-4 Spot LNG imports by country

Source: Petrostrategies

During the period of suspended supply caused by Indonesia's Arun project in 2001, some buyers had no difficulty in finding alternative sources of supply. This suggests that the supply side had some capacity margin as well as the reason for growth in the spot market.

In the past, the lack of LNG transport capacity prevented LNG spot market from developing , even when both sellers and buyers wished to make spot deals. This problem is expected to be resolved gradually as more LNG tankers become available.

(BCM)

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

World total 80.90 83.20 87.80 92.50 102.40 111.30 113.00 124.20 136.96 142.95

Spot total 1.05 1.59 2.34 3.27 2.33 1.64 2.12 4.72 7.58 10.75

Ratio 1.3% 1.9% 2.7% 3.5% 2.3% 1.5% 1.9% 3.8% 5.5% 7.5%

(BCM)

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Spain - 0.27 0.94 1.05 0.98 0.99 0.83 1.69 1.43 2.29

France - - - 0.87 0.23 - - 0.08 0.08 0.53

Belgium - 0.23 0.08 0.15 - - - - - 0.15

Italy 0.53 0.26 0.20 - - - 0.12 0.54 0.48 0.38

Portugal - - - - - - - - 0.08 -

Turkey - - - 0.23 0.08 - 0.58 0.30 - -

United States - - - - 0.23 0.38 0.53 1.66 3.73 3.24

Japan 0.38 0.39 0.08 0.08 0.15 0.28 - 0.15 0.32 2.23

South Korea 0.15 0.45 1.05 0.90 0.68 - 0.08 0.31 1.47 1.87

Taiwan - - - - - - - - - 0.08

Total 1.05 1.59 2.34 3.27 2.33 1.64 2.12 4.72 7.58 10.75

IEEJ:October 2003

7

3. LNG facilities 3-1 Liquefaction plants The first LNG trade in the Asia-Pacific region involved LNG exports from Kenai, Alaska, to Japan in 1969. Lumut liquefaction plant in Brunei then began operations in 1972 as the first LNG plant in Asia. Other plants have since been constructed in Arun and Bontang in Indonesia, Bintulu in Malaysia and Karratha for the northwest continental shelf (NWS) project in Australia.

In the Middle East, LNG plants were constructed in Abu Dhabi, Qatar and Oman to serve the Asia-Pacific market. Liquefaction capacity in those countries reached about 88 MT at the end of 2001 (see Table 3-1). By 2010, a number of construction projects, such as MLNG III in Malaysia, NWS expansion project in Australia, Ras Laffan (Phase 2) in Qatar, Sakhalin II in Russia and Tangguh (Irian Jaya) in Indonesia, are to be ready to meet growing LNG demand in the Asia-Pacific region.

Table 3-1 Existing liquefaction plants in the Asia-Pacific region (as of 2002)

Source: IEEJ

Country Station name Number oftrains

Liquefying capacity(Million Tonnes)

Start ofoperation

United States (Alaska) Kenai 1 1.30 1969

Brunei Lumut 5 7.20 1972

Bontang A, B 2 1977

Bontang C, D 2 1983

Bontang E 1 18.69 1989

Bontang F 1 1993

Bontang G 1 1997

Bontang H 1 2.95 1999

Arun 4 7.90 1978

I (Satu) 3 8.10 1983

II (Dua) 3 7.80 1995

Australia Karratha 3 7.50 1989

Das Island 1 2 2.50 1977

Das Island 2 1 3.00 1994

Qatar Gas 3 7.70 1997

Ras Laffan 2 6.60 1999

Oman Qalhat 2 6.60 2000

Total 39 87.84

Abu Dhabi

Indonesia

Malaysia

Qatar

IEEJ:October 2003

8

Figure 3-1 LNG Production capacity growth in the Asia-Pacific region 1969-2000

Source: IEEJ

3-2 LNG receiving terminals With respect to the receiving terminals in importing countries, twenty five terminals are currently operating, two are being constructed and another two planned in Japan. In South Korea, three terminals at Pyeongtaek, Inchon and Tongyoung are operating, and Twangyang

terminal will be completed in 2005. In Taiwan, one terminal is operating at Yungan, and the second LNG terminal is planned in Taoyuan in northern Taiwan (see Table 3-2). Countries such as India, China and the Philippines are also planning to construct LNG receiving terminals.

0

10

20

30

40

50

60

70

80

90

100

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Million Tonnes

1969

IEEJ:October 2003

9

_______________________________ *4 Later in May 2003, Tokyo Gas and Tokyo Electric, and in July Kyushu Electric signed Heads of Agreement (HOA)

with Sakhalin Energy Investment Company, the business entity of the Sakhalin II Project for their LNG purchase.

Table 3-2 LNG receiving terminals in Japan, Korea, Taiwan, India, and China

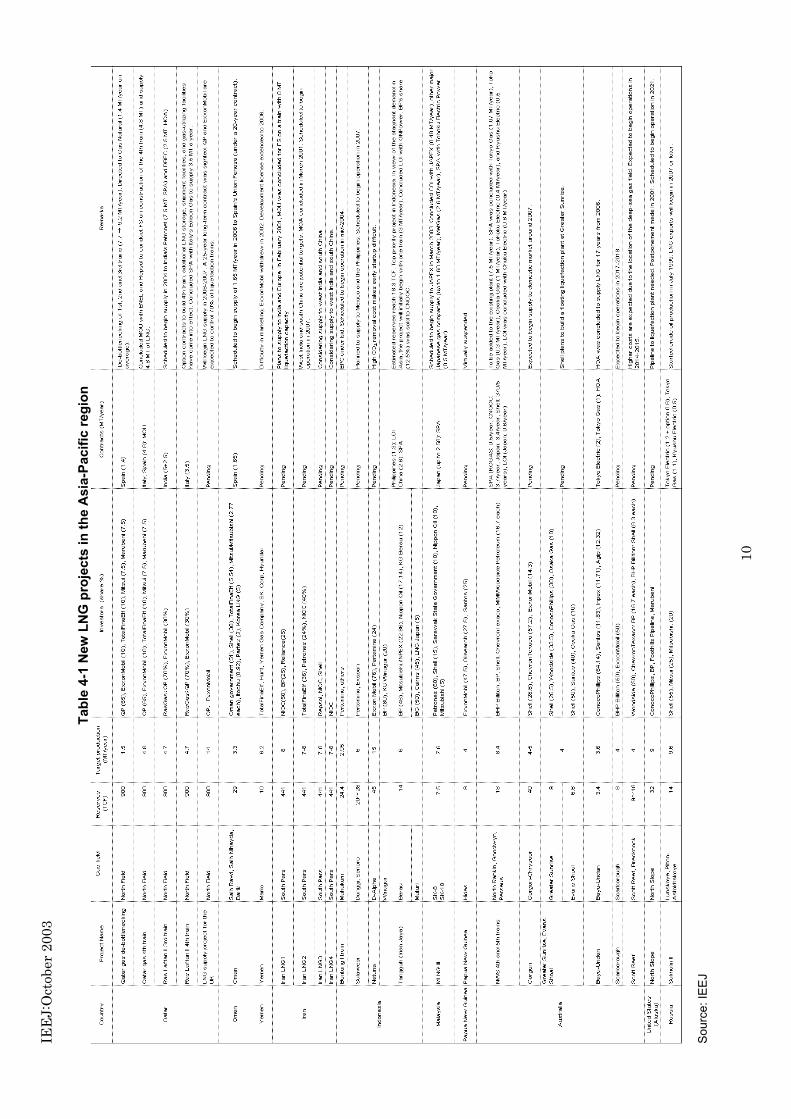

Source: IEEJ 4. LNG projects There are more than ten new and upgrading LNG projects being planned in the Asia-Pacific region, Middle East, North America and Russia to serve the Asia-Pacific market. However, the projects that have made meaningful progress are limited to those in Qatar (Ras Laffan phase 2), Malaysia (MLNG III) and Australia (NWS expansion). Due to sluggish demand in the Asian LNG market, operations are unlikely to begin until 2005 or later for the Gorgon project in Australia and

many other projects, which are still in the planning stage (see Table 4-1). Those projects aim to supply LNG to new markets such as China and India that are planning a number of LNG import projects, and to the existing markets such as Japan, South Korea and Taiwan. With respect to Sakhalin II in Russia, in February 2003, it was reported that more than one Japanese buyer was considering a deal, and that the start of commercial operation would be announced soon. 4

Country Receiving station Company name LNG exporter Storage (kl) Start-up

Sendai Sendai City Gas Bureau Malaysia 80,000 1997

Higashi Niigata Nihonkai LNG Indonesia, Malaysia, Qatar 720,000 1984

Futtsu Tokyo Electric Australia, Abu Dhabi, Malaysia, Indonesia, Brunei 860,000 1985

Sodegaura Tokyo Electric, Tokyo Gas Brunei, Malaysia, Australia, Indonesia, Alaska, Qatar 2,660,000 1973

Higashi Ohgishima Tokyo Electric Brunei, Malaysia, Australia, Indonesia, Alaska, Abu Dhabi, Qatar 540,000 1984

Negishi Tokyo Electric, Tokyo Gas Alaska, Brunei, Australia, Malaysia 1,250,000 1969

Sodeshi Shimizu LNG Malaysia 177,200 1996

Chita Kyodo Chubu Electric, Toho Gas Indonesia, Australia, Qatar, Malaysia 300,000 1977

Chita Chita LNG Indonesia, Australia, Qatar, Malaysia 640,000 1983

Yokkaichi LNG Center Chubu Electric Indonesia, Australia, Qatar 320,000 1987

Yokkaichi Toho Gas Indonesia 160,000 1991

Kawagoe Chubu Electric Indonesia, Australia, Qatar 480,000 1997

Senboku 1 Osaka Gas Brunei 180,000 1972

Senboku 2 Osaka Gas Indonesia, Australia, Malaysia, Qatar 1,585,000 1977

Himeji (Osaka Gas) Osaka Gas Indonesia, Australia, Malaysia, Qatar, Oman 560,000 1984

Himeji (Kansai Electric) Kansai Electric Indonesia, Australia, Malaysia, Qatar 520,000 1979

Hatsukaichi Hiroshima Gas Indonesia 85,000 1996

Yanai Chugoku Electric Australia, Qatar 480,000 1990

Oita Oita LNG Australia, Indonesia 460,000 1990

Tobata Kitakyushu LNG Indonesia 480,000 1977

Fukuoka Saibu Gas Malaysia 70,000 1993

Kagoshima Nihon Gas Indonesia 36,000 1996

Ohgishima Tokyo Gas Alaska, Brunei, Australia, Indonesia, Malaysia 400,000 1998

Chita Midorihama Toho Gas Indonesia, Australia, Malaysia 200,000 2001

Nagasaki Saibu Gas Malaysia 35,000 March, 2003

Sakai Sakai LNG N.A. 420,000 Planning (2005)

Mizushima Chugoku Electric, Nippon Oil N.A. 160,000 Planning (2006)

Wakayama Kansai Electric N.A. 840,000 Planning

Joetsu Chubu Electric, Tohoku Electric N.A. 720,000 Planning

Tsuruga Osaka Gas N.A. 1,800,000 Plan suspended

Pyeongtaek Korea Gas Corporation Indonesia, Malaysia 1,000,000 1986

Inchon Korea Gas Corporation Indonesia, Malaysia, Brunei, Australia 1,000,000 1996

Tongyoung Korea Gas Corporation N.A. 420,000 2002

Gwangyang Pohang Steel Corporation (POSCO) N.A. 200,000 2005

Yungan Chinese Petroleum Corporation (CPC) Indonesia, Malaysia 300,000 1990

Taoyuan (Northern Taiwan) Tung Ting Gas Corporation N.A. 420,000 Planning

Dabhol (West India) Dabhol Power/MetGas Oman, Abu Dhabi 480,000 N.A.

Dahej (West India) Petronet LNG Qatar N.A. 2003

Pipavav (West India) GPLCL/NTPC N.A. N.A. 2006

Kakinada (West India) Indian Oil Corp./Petronas N.A. N.A. 2006

Cochin (Southwest India) Petronet LNG Qatar N.A. 2007

Ennore (Southeast India) DBEC Qatar N.A. 2004

Hazira (West India) Shell Oman N.A. 2004

Gapalpur Al-Manhal/Ipicol N.A. N.A. N.A.

Shenzhen CNOOC, BP, others Australia N.A. Planning (2005)

Fuijian CNOOC, Fujian Investment and Development Indonesia N.A. Planning (2007)

Philippines Bataan GN Power Indonesia N.A. Planning

China

Japan

Korea

Taiwan

India

IEE

J:O

ctob

er 2

003

10

Tabl

e 4-

1 N

ew L

NG

pro

ject

s in

the

Asi

a-Pa

cific

regi

on

Sour

ce: I

EEJ

IEEJ:October 2003

11

_______________________________ *5 Construction of the liquefaction plants has begun for Sakhalin II. Therefore, this project progressed from

“Planning” to “Under construction or supply contracts concluded” in the Table 5-2.

5. LNG demand-supply balance 5-1 LNG demand forecasts Table 5-1 lists LNG demand forecasts by oil and gas companies, consulting firm and research institutes. While LNG demand for 2001 was 74.5 MT, the projection for 2010 will increase by 26.5-60.5 MT to reach 101-135 MT. Of this increase, new demand in India, China and other new importing countries account for 10-31 MT. Total regional demand growth from 2001 to 2010 is projected to be 3.4-6.8% per

year. Growth in existing LNG importers is expected to be 2.2-4.1% per year. Consequently, the new importers will have a significant impact on the region’s demand growth. The projected LNG imports by existing importers depend on the extent of economic states in each country and their policy towards CO2 emissions. Particularly for Japan and Taiwan, the construction of nuclear power plants will be one of the key factors on which natural gas demand and thus substantially LNG imports amount depend.

Table 5-1 LNG demand forecasts

Note: *1 Natural Gas in the World 2002, Cedigaz *2 Data was obtained in March 2001 for TotalFinaElf; July 2001 for Wood Mackenzie; November 2001 for

Cedigaz; July 2001 for OGJ; and February 2003 for Tokyo Gas *3 OGJ: Oil & Gas Journal Source: Cedigaz, TotalFinaElf, Wood Mackenzie, Oil & Gas Journal and Tokyo Gas

5-2 LNG supply forecast As shown in Table 5-2, the Asia-Pacific region (including the Middle East) has LNG plants capable of liquefying 87.84 MT a year (as of the end of 2002). The total liquefying capacity of projects under construction or soon-to-be constructed with supply contracts is 32 MT a year in the region. Since these projects are to come in reality with high possibility, we can expect an LNG supply capacity of 119.84 MT a year by 2010. Of this capacity, 2.10 MT a year from existing projects and 5.15 MT a year from projects under construction or soon-to-be constructed will be directed to Europe. The

remaining 112.59 MT a year may be considered a relatively reliable figure for LNG supply capacity for the Asia-Pacific market in 2010. Moreover, projects including Sakhalin II, Gorgon and many others are conducting gas reserve investigation and market research. Officially released figures reveal that another 72.35 MT can be added. Since 7.80 MT a year of those projects are to be exported to Europe, the remaining 64.55 MT a year may be directed to the Asia-Pacific market.*5

MT (Million Tonnes)

(High) (Low) (High) (Low)

Japan 54 66 60 69.1 66 62 60.9 60-68 1.2%-2.8%

South Korea 15.9 25 21 21.6 23 20 25.7 21-26 2.6%-5.6%

Taiwan 4.6 13 11 10.4 13 10 10.8 10-13 9.0%-12.2%

Subtotal 74.5 104 92 101.1 102 92 97.4 91-107 2.2%-4.1%

India 0 12 8 12 17 12 18 5-10 -

China 0 16 9 8 6 3 5 5-10 -

Others 0 3 0 0 3 0 - 0-2 -

Total 74.5 135 109 121.1 128 107 120.4 101-129 3.4%-6.8%

2001*1 2010*2

Annual growth from2001 to 2010TotalFinaElf Wood

MackenzieCedigaz OGJ*3

(Base)Tokyo Gas

IEEJ:October 2003

12

Table 5-2 Progress of LNG projects in the Asia-Pacific region

Source: IEEJ

Existing LNG liquefying plants

Asia-Pacific region 61.44 4,000~7,000 See Table 3-1 for details.

Abu Dhabi 5.50 12,000 Began operations in 1977.

Qatargas (Qatar) 7.70 12,000 Began operations in 1997.

Ras Laffan (Qatar) 6.60 12,000 Began operations in 1999.

Oman 6.60 11,800 Began operations in 2000.

Subtotal 87.84

Exports to Europe -2.10 Oman to Spain for Shell and Qatar to Spain for Gas Natural from 2002 onward.

Subtotal after subtraction 85.74

Under construction or supply contracts concluded

Ras Laffan II (Qatar) 4.70 12,000 Scheduled to begin operation in 2004. The 3rd train is to be built for Petronet in India.

Ras Laffan II (Qatat) 4.70 12,000 Scheduled to begin shipment in early 2006. 4th train is planned to supply for EdisonGas in Italy.

Qatargas (Qatar) 1.50 12,000 1st, 2nd and 3rd trains are being de-bottlenecked. To be completed in 2005.

MLNG III (Malaysia) 7.60 4,600 Scheduled to begin operation in March 2003.

Tangguh (Indonesia) 6.00 4,500 SPA concluded for Fujian province in China.

NWS 4th train (Australia) 4.20 6,800 Scheduled to begin operation in 2004.

Oman expansion 3.30 11,800 Scheduled to being operation in 2006.

Subtotal 32.00

Export to Europe -5.15 Oman to Spain for Union Fenosa and Qatar to Italy for Edison Gas from 2006 onward.

Subtotal after subtraction 26.85

Planning

Qatargas (Qatar) 4.80 12,000 MOU on 4th train FS concluded. Plannning to supply Enel (Italy) and Repsol (Spain).

Iran 8.00 12,000 Studying LNG supply possibility to India and China.

Yemen 6.20 12,000 Difficulty in marketing. ExxonMobil withdrew in 2002. Development license extended to2006.

Sakhalin II (Russia) 9.60 1,700 LNG exports will begin in 2007 or later.

Natuna (Indonesia) 15.00 4,200 Expected to begin operations in 2007 or later.

Bontang I (Indonesia) 2.95 4,600 Scheduled to begin operations in 2004.

Sulawesi (Indonesia) 6.00 - Scheduled to begin operations in 2007.

Bayu-Undan (East Timor) 3.60 6,800 HOA concluded for LNG supply for 17 years, beginning in 2006.

Greater Sunrise, Evans Shoal (Australia) 4.00 6,800 Shell planning to build a floating liquefying plant at Greater Sunrise. Expected to beginoperations around 2007.

NWS 5th train (Australia) 4.20 6,800 Scheduled to begin operations in 2006 or 2007.

Gorgon (Australia) 4.00 6,800 Expected to begin operations in 2005.

Papua New Guinea 4.00 6,700 Virtually suspended

Subtotal 72.35

Exports to Europe -7.80 4.8 MT a year for Enel (Italy) and Repsol (Spain), and 3 MT a year for Mexico.

Subtotal after subtraction 64.55

Total 177.14

Liquefyingcapacity

(MT)

Transportationdistance to Japan

(km)Remarks

IEEJ:October 2003

13

5-3 LNG demand-supply balance In the context above, in 2010, new capacity of 22.41 MT needs to be secured out of the 64.55 MT in “Planning” category of Table 5-2 to match the maximum estimated demand of 135 MT. For the lowest demand of 101 MT, this

demand can be met by the 112.59 MT capacity of existing and plants under construction. In that case, it will not be necessary to implement the LNG projects in the “Planning” category (see Figure 5-1).

Figure 5-1 LNG demand-supply balance in the Asia-Pacific region in 2010

Note: *The total capacity shown in this figure will not necessarily be realized. Source: IEEJ

6. International gas pipelines in

Asia In Asia, natural gas producing countries such as Indonesia, Malaysia, Australia and Brunei are geographically distant from countries such as Japan, South Korea and Taiwan, which import natural gas in the form of LNG. Thus, compared to the US and Europe, few cross-border pipelines have been constructed. It has been common practice to supply natural gas in the form of LNG in Asia instead of via pipeline. In fact, pipelines were only employed for domestic use within each gas-producing country. A growing trend in recent years shows more Asian countries are developing international pipeline infrastructures. Currently, the following international pipelines are operating in Asia: from Malaysia to Singapore (PGU: Peninsular Gas

Unitization), from the Yadana gas field in Myanmar to Thailand, from the Yetagun gas field in Myanmar to Thailand, from west Natuna in Indonesia to Singapore and from Natuna to Malaysia. There are also plans to construct gas pipelines from south Sumatra in Indonesia to Singapore and to west Java. These are constituent elements in the Trans-ASEAN pipeline scheme. The energy ministers of South East Asian countries reportedly signed an MOU on the construction of a gas pipeline network slated to begin in July 2002. Consequently, the cross-border pipeline project within South East Asia is making slow but steady progress. Looking at northeast Asia, Russia plans to construct a pipeline from Irkutsk (Kovykta gas field) to China and Korea. For Japan, there is Sakhalin I project that would transport gas from Sakhalin, which is located the shortest distance of 44 km north from Japan. In August

����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

������������������������������������������������������������������

8,5748,574

2,685

6,455

13,500

10,100

7,450

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2002年 2010年������������������������

既存・稼働中

������������������������

建設中

事業化検討中 * 需要見通し(高需要ケース)

需要見通し(低需要ケース)

(10,000 tons)

2002 2010

Existing

Planning *

Projected demand (Low demand case)

Under construction or supplycontracts concluded

Projected demand (High demand case)

IEEJ:October 2003

14

_______________________________ *6 The Mainichi Newspaper, January 18, 2003

2002, the Japan Sakhalin Pipeline Company, owned by JAPEX, Itochu and Marubeni, completed an FS on the Sakhalin pipeline in terms of the route, design standards and environmental and regulatory issues on the Japanese side, and announced the technical and commercial feasibility of a high-pressure natural gas pipeline to supply 8 BCM of gas via 26-28 inches (65-70 cm) diameter pipes. Under this project, Pacific route from Soya Cape in Hokkaido to the Kanto region (about 1,440 km) or Japan Sea route from Soya Cape to Niigata (about 1,120 km) is being considered. Regarding the issue of nuclear weapons in

North Korea, South Korea has reportedly proposed building a pipeline from the Sakhalin to Kyushu across the Korean peninsula under private sector management to offer a supply of natural gas to North Korea in exchange for totally giving up its nuclear weapons program. The US is now discussing this proposal in a positive manner, according to the report.*6 This could benefit North Korea in terms of securing a long-term energy supply and could virtually have a guarantee of not being attacked by the US since the pipeline would be a vested interest of Japanese and American companies. However, this proposal represents a highly charged political challenge.

Figure 6-1 International gas pipelines in

Asia-Pacific region

Source: IEEJ

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ���

��� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

Major Gas Fields

Operating

Constructing

Planning

Iran

Qatar

Oman

Turkmenistan

Russia

Pakistan

Ko vyk t a

India

China

Thailand

Singapore

Malaysia Indonesia

Sakh a l i n

Australia

Papua New Guinea

South

Korea

Japan

Yac h e n g 1 3 - 1

Yadan a

Ye t a g u n

Hong KongBangladesh

W e s t S i be r i a

N a t u n aJ D A

IEEJ:October 2003

15

_______________________________ *7 Please not that technology that affects the demand-supply balance not only the Asia-Pacific region. *8 In December 2002, the US Federal Energy Regulatory Commission (FERC) decided not to require terminal operators

for approval or specifying a price list based on net cost regarding the use of new LNG terminals by a third party. Detailsof contracts concluded with the customer(s) must still be reported to FERC before a new terminal can be constructed.However, this will enable terminal operators to lease excess station capacity to third party at any desired charge setthrough negotiations. Consequently, the advantages of this technology may be reduced in light of third party access toLNG receiving terminal.

Table 6-1 International gas pipelines under construction and planning in the Asia-Pacific

region

Source: IEEJ 7. Technology trends in LNG and

other natural gas relating issues*7

7-1 Energy Bridge™ El Paso of the US proposed a new technology called Energy Bridge in May 2002, which is a regasification system on LNG carrier to supply gas directly to the ground base. LNG would be regasified onboard, then the gas would be sent via subsea pipeline that would be connected with local pipeline network. Thus, this technology can eliminate receiving terminal of the conventional LNG chain. Eliminating the need for a receiving terminal provides advantages, especially for LNG

import/receiving terminal operators in the US that are relieved of this requirement of allowing third party access to their terminal's capacity.*8 It will also ease security concerns over the vulnerability of receiving terminal with high energy density to terrorist attacks, since gas can be unloaded offshore. This technology would prove useful in terms of efficient operation of LNG carrier and of being free from limitations of port conditions. Energy Bridge may also become a new element in the LNG chain on the receiving side. El Paso intends to use this technology in the Gulf of Mexico for the time being. This technology can be useful in the US where underground gas storage system is well-developed and where LNG regasification, unloading and transport can be conducted at the same time. However, in Japan, where receiving terminals have storage function, it may be difficult to employ this technology. Meanwhile, in February 2003, El Paso announced that it was pulling out of the LNG market. Therefore the future of this technology and its applications need to be closely monitored.

Stauts Pipeline length Supply Remarks

JDA (Malaysian and Thai territorialwaters) → Malaysia, Thailand

JDA (Malaysia and Thai territorialwaters) → Thailand, Malaysia About 350km 4.0-8.6 BCM/year Malaysia will take gas for the 1st phase. To be

completed by the end of 2004.

Indonesia → Singapore South Sumatra → Singapore 477km About 3.4 BCM/yearfrom 2003 onward

Pertamina and PowerGas signed an contract inFebruary 2001.

Qatar → UAE → Oman → Pakistan(Dolphin project) Qatar → UAE (1st phase) 350km 2 BCFD Examining candidates for equipment-related FEED

contract.

1.0-1.4 BCFD Also 500-700 MMCFD for Bahrain

Korsakov → Ishikari About 450kmIshikari → Niigata 884kmAomori → Kanto 860km

About 2,200km 18-20 BCM/year A subsea pipeline to avoid Pakistan is beingstudied. MOU on FSpostponed to December 2004.

Bangladesh → India Bangladesh → Orissa About 1,600km 5 BCM/year Difficulties related to political problems inBangladesh.

About 1,000km 500-770 MMCFD Part of the Trans-ASEAN pipeline. To be completedafter 2020.

About 1,460km 20 BCM/year Unocal withdrew

Indonesia → Thailand Natuna gas field → Thailand About 1,538km 500 MMCFD in 20051,000 MMCFD in 2007

Postponed to 2007 or later due to currency crisis inThailand and stagnant gas demand.

About 1,150km 20 BCM/year Project cancellation was reported in October 1996.

141km 1.5MMCMD Scheduled for completion in 2002, but delayed dueto financial problems.

Economics being reexamined after a change ofroute (Lianyungang → Shanghai).

Pipeline FS by ExxonMobil and Japex wascompleted in April 2002.

Routes

Oman → India

About 3,500km 30 BCM/year FS by Russia, China, and Korea will be completedin 2003.

Sakhalin → Japan 800-1000 BCFDpipeline capacity

Turkmenistan → China

Plans haltedor abandoned

Planning

FS

SPA, MOU

About 5,730km 30 BCM/year

Iran → Armenia

Qatar → Kuwait (Bahrain)

Iran → India

Irkutsk → China, Korea

Indonesia → Philippines

Turkmenistan → Pakistan (TPA project)

Turkmenistan → Shanghai

IEEJ:October 2003

16

_______________________________ *9 For the Qatar expansion project, LNG carrier with unprecedented capacity is reportedly considered. Cost

reduction can be expected regarding transport as well as liquefaction in the LNG chain. *10 Journal of the Japan Institute of Energy, vol. 81, 574 (2002)

7-2 Maximizing LNG production capacity per train

Table 7-1 lists the production capacity of selected liquefaction plants. The capacity per train has been on the increase over the past 25 years in order to reduce production costs by economics of scale. For example, production capacity of the Australia NWS project, which began operations in the late 1980s, was initially 2.1

MT per train, but later increased to 2.5-3.0 MT during the mid-1990s, then exceeded 3.0 MT by the end of the 1990s. For the projects in Trinidad and Tobago, Oman and RasGas of Qatar, the annual production capacity per train is 3.0-3.3 MT, 3.8 MT for the Malaysia Tiga (MLNG III), 4.8 MT for Sakhalin II and 7.8 MT for the expansion project in Qatar that will begin shipments in 2006 to the UK. This trend is likely to continue. *9

Table 7-1 Production capacity of selected LNG plants

Source: Journal of the Japan Institute of Energy, vol. 81, 574 (2002), except for Ras

Laffan Plant (the first cell from the bottom) expansion announced in a press release by ExxonMobil (July 2003)

7-3 Liquefaction process *10 The liquefaction system that was employed in Algeria and Alaska when LNG was first commercialized in the 1960s is called Cascade. However, the propane pre-cooled mixed refrigerant process (C3-MCR) of Air Products and Chemicals Inc. (APCI) later became dominant in many subsequent projects. That trend continued until the Cascade system was adopted in a project in Trinidad and Tobago. The Snoehvit LNG project of the North Sea will reportedly employ the Triple MR (Triple Mixed Refrigerant) of Linde. Shell's

proprietary Double Mixed Refrigerant (DMR) method will reportedly be used for the Sakhalin II project. Since the core technologies for the liquefying process (i.e., the liquefying process itself and associated equipments) show sign of departing from the dominant method, it is necessary to pay attention to trends in liquefaction technology and the impact on future LNG projects.

Arun Sumarta Indonesia 6 1.6 1978

NWS Karatha Australia 3 2.1 1989

MLNG 2 Bintulu Malaysia 3 2.9 1995

Qatargas Ras Laffan Qatar 3 2.5 1996

NLNG Bonny Nigeria 3 3.0 1999

OLNG Al Ghalilah Oman 2 2.9 1999

Rasgas 1-2 Ras Laffan Qatar 2 3.2 1999

Rasgas 3 Ras Laffan Qatar 2 4.7 2004

Sakhalin II Sakhalin Russia 1 4.8 2005

NLNG+ Bonny Nigeria 2 4.1 2004

Qatargas II Ras Laffan Qatar 1 (7.8) (2007)

CapacityMTPA Start upProject Location Country No. of

trains

IEEJ:October 2003

17

_______________________________ *11 Gas to Liquids (GTL): A new natural gas processing technology. Natural gas is first converted into a synthesis gas

(mixture of hydrogen and carbon monoxide), then is transformed to middle distillate such as kerosene and diesel oil,or liquid products such as dimethylether (DME) and ethanol. GTL also may be narrowly defined as technology tomanufacture petrochemical products (such as kerosene and diesel oil) by utilizing the Fischer-Tropsch (FT) process.

*12 15 member countries: According to GECF, Algeria, Brunei, Egypt, Indonesia, Iran, Libya, Malaysia, Nigeria, Norway(as an observer), Oman, Russia, Trinidad and Tobago, UAE, Venezuela, and Qatar. From the initial 11 countries,Turkmenistan left, while Egypt, Trinidad and Tobago, UAE, Venezuela, and Libya joined.

*13 A GECF meeting, held during the International Energy Forum in September 2002 in Osaka, is not considered as aministerial meeting.

*14 According to GECF, EU countries are pushing ahead with their gas market deregulation only at their ownconvenience without discussions with producing countries. The resulting advantages have only been directed toimporting countries with no share given to the exporters. Thus, what EU calls, competitive gas market policy maypose risks to investment incentives for developing natural gas resources. Such a policy will eventually cause asupply shortage and will undermine the benefit of importers too.

7-4 GTL projects Many GTL*11 projects are emerging recently. In addition to projects operating in South Africa and Malaysia, GTL has drawn attention as a new way of generating revenue from gas resources in Indonesia, Qatar and Australia (where natural gas is already developed and exported mainly in the form of LNG). Indeed, GTL is creating a new field in the processing industry. GTL plants currently operating in South Africa and Malaysia are based on Sasol and Shell technology respectively. Other GTL technologies developed by ExxonMobil, Syntroleum, Rentech and ConocoPhillips are being studied in many countries. 8. Cooperation among

gas-producing countries The meetings of Gas Exporting Countries Forum (GECF) were first held in May 2001 in Teheran, then in February 2002 in Algeria where the ministers of member countries participated. In February 2003, the third meeting was held involving the ministers from 15 countries*12 in Doha, Qatar.*13 Following a roundtable meeting in Algeria held in early September 2002 and taking into account of the GECF policy*14, the ministers apparently discussed gas marketing for Europe where deregulation is underway and the framework of destination clause and contracts of natural gas trades.

Prior to this meeting, in June 2002, three LNG exporters, Brunei, Indonesia and Malaysia, reportedly agreed to cooperate to ensure stabilized operation of their LNG plants. That is a multinational-cooperation to prevent incidents from affecting their LNG supply, drawn on the experience from the suspended LNG supply due to security problems in Indonesia’s Ache special autonomous region in March 2001. 9. LNG supply from the Middle

East to Europe In the past, Asian countries were the main customers for Middle Eastern LNG exporters such as the UAE, Qatar and Oman, while Europe was an LNG market only for spot or short-term deals. Given recent stagnant gas demand in the Asian market and increasing demand in Europe for power generation and concerns over the future of gas supply from the North Sea, mid and long term LNG supply contracts are increasingly concluded for European market. Traditional Asian importers such as Japan, to which the LNG was originally marketed, are closely monitoring the effects on the Asian market.

IEEJ:October 2003

18

10. Implications for Japan Reviewing the current LNG market, we can see the following points as worthy of note: In terms of supply and production: 1) Worldwide LNG production capacity is increasing due to expansion of existing plants in Trinidad and Tobago, Nigeria, Qatar, Malaysia and Australia, in addition to new projects in Norway, Russia and Iran; 2) LNG transport capacity is increasing; 3) Gas competitiveness is improving by cost reduction at liquefaction plants and LNG carriers; 4) LNG prices are falling. In terms of demand and consumption: 1) LNG supply from the Middle East to Europe is increasing due to growing demand; 2) New players have joined the market, thus changing the market structure. China is to be a new LNG importer. New LNG receiving terminal projects are planned in India and several locations along the Pacific coast in the US and Mexico; 3) There is a potential trend toward increased use of natural gas endorsed by GTL evolution for diesel oil market, in addition to a growing preference for natural gas for high efficiency power generation and for other sectors as an environmental measure. In terms of business models of market players, LNG sellers and buyers are expanding their roles in the LNG value chain to become more competitive in the mega-competition of energy industry. For example, Shell and BP are penetrating into LNG transport business adding to downstream markets. Meanwhile, some buyers (including Japanese power/gas companies) are strategically joining the upstream business such as LNG transport and gas exploration. With market deregulation, the competition among different forms of energy and different types of gas is likely to intensify. This will result in creating conflicts among existing LNG buyers and make it difficult to form a large-scale consortium of LNG buyers. This trend is illustrated by the fact that one consortium of Japanese buyers for NWS expansion project disbanded and entered individual negotiations. In the future, new types of players like LNG marketers and traders may appear in the Asia-Pacific market.

Uncertainty resulting from market deregulation enhances the need for further flexibility in LNG contractual practices. Since LNG projects require huge investments, the sellers claim the necessity of a long-term contract. Meanwhile, it is important for the buyers to assure stable supply. Therefore, basically, long-term contracts will continue to play the dominant role. Nevertheless, short-term and spot trading are likely to increase in response to the market requirements. As a means to enhance trading flexibility, easing LNG destination clause is to be considered. As LNG trading becomes more flexible, business opportunities will increase, enabling various forms of trading such as spot, swap and arbitrage. In particular, we must watch players with transport capability. Japanese players have already made efforts to improve flexibility in business practices. For instance, some of them change contractual conditions from Ex-ship to FOB and take some transport risk by themselves, use short-term and spot deals in combination with long-term deals to match supply with demand more precisely, and try to ease the destination clause when renewing existing contracts and concluding new ones. Regarding supply conditions based on pricing mechanism, as buyers push ahead with strategies for raising competitiveness in the gas market under ongoing deregulation, tailored contracts instead of unified ones for individual buyers can prevail. In terms of pricing, buyers may adopt a pricing formula less sensitive (though still linked) to crude oil prices, or tend to incorporate other variables to introduce a new index such as petroleum product prices and electricity prices, or adopt fixed prices. Driven by such pressures and the significant cost reduction in LNG chain, natural gas price level is expected to fall and the competitiveness of natural gas to rise. According to the news in August 2002 about the contract to supply LNG from the Australia NWS project to the new LNG receiving terminal in Guangdong, the price was going to be at least 20% lower than those for existing LNG buyers in Asia, with small price fluctuations because the link portion pegged to the crude oil price decreased from 85% in the conventional contracts to 30%, although details were kept confidential. For India, a price cap was reportedly set in the contract by which PetroNet would buy LNG from RasGas in Qatar. Evidently, buyers requests are

IEEJ:October 2003

19

increasingly influential in determining LNG prices. The current goals for Japanese LNG buyers are more flexible deals at lower cost, while ensuring supply security. Three LNG projects in Bayu-Undan, Sakhalin II and Tangguh are expected to start up by 2010. Natural gas can be supplied via pipeline from the Sakhalin I project to Japan after 2010. Experts predict that the LNG price will decrease by 10% or more in the years ahead, that pricing formula will feature not only prices of crude oil but prices of electricity and oil products and that fixed price can be an option, that short-term and spot deals can account for about 15% (currently 5 to 6%) of overall LNG deals by about 2010.*15 The worldwide LNG market shows signs of changing from a seller's market to a buyer's market. We expect that LNG prices will consequently drop and the trading flexibility will increase through talks with suppliers and cooperation with neighboring LNG importing countries, Korea and Taiwan, that share the same position and that the LNG market will then benefit Japan.

Contact: [email protected]

15 “Prospect of LNG Market in the Asia-Pacific region”, SPEC (Symposium on Pacific Energy Cooperation), February 2003.