Natura, January 2017 Stanley -Jan17.pdf · Sources: Euromonitor 2015, IMF WEO Oct 2016 (2016f data)...

43

Natura, January 2017 Morgan Stanley 9th Annual Latin America Executive Conference

Transcript of Natura, January 2017 Stanley -Jan17.pdf · Sources: Euromonitor 2015, IMF WEO Oct 2016 (2016f data)...

Natura, January 2017

Morgan Stanley9th Annual Latin America Executive Conference

Context, strategies & priorities

José Roberto Lettiere, CFO & IROMarcel Goya, Financial Director & IR

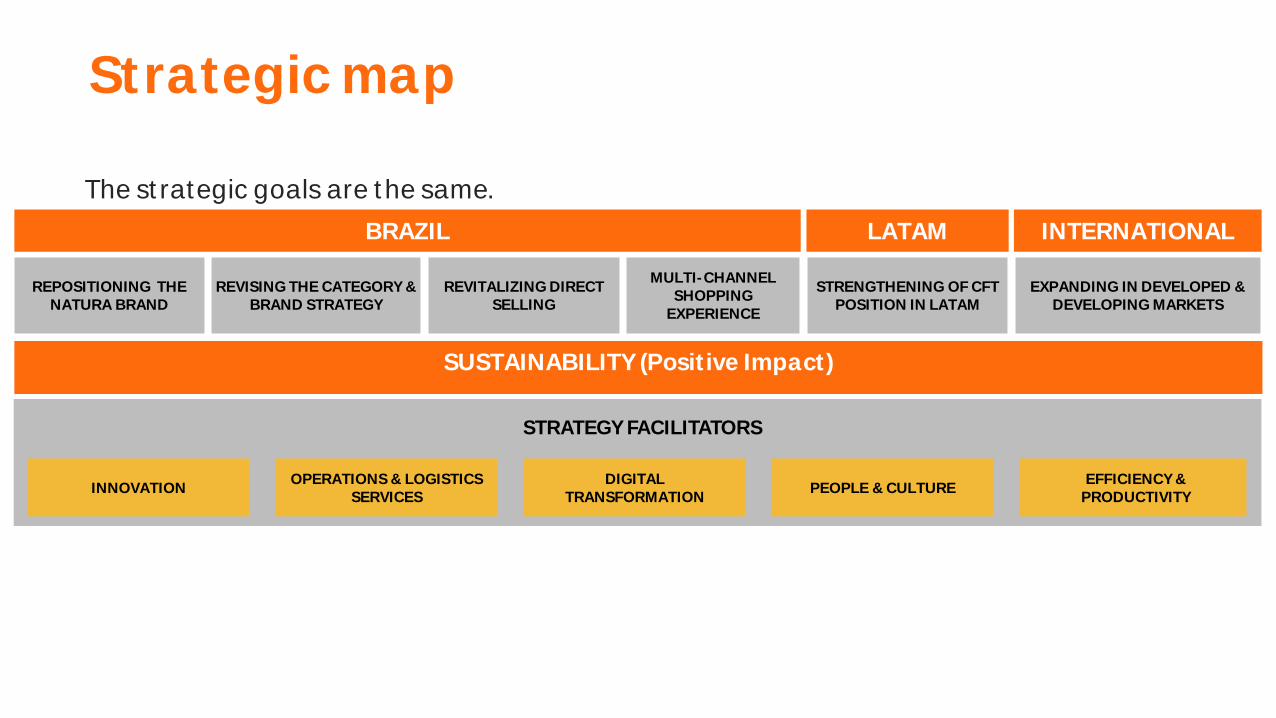

BRAZIL LATAM INTERNATIONAL

REPOSITIONING THE NATURA BRAND

REVITALIZING DIRECT SELLING

REVISING THE CATEGORY & BRAND STRATEGY

MULTI-CHANNEL SHOPPING

EXPERIENCE

EXPANDING IN DEVELOPED & DEVELOPING MARKETS

STRENGTHENING OF CFT POSITION IN LATAM

SUSTAINABILITY (Positive Impact)

INNOVATIONOPERATIONS & LOGISTICS

SERVICESDIGITAL

TRANSFORMATIONPEOPLE & CULTURE

EFFICIENCY & PRODUCTIVITY

STRATEGY FACILITATORS

Strategic map

The strategic goals are the same.

2017 Priorities

Brazil

Fragrances & gifts

Relaunching direct selling

Accelerating digitalization

New Channels

Maintaining Latam momentum

Culture & Organization Program

9M YTD - 2016 RESULTS

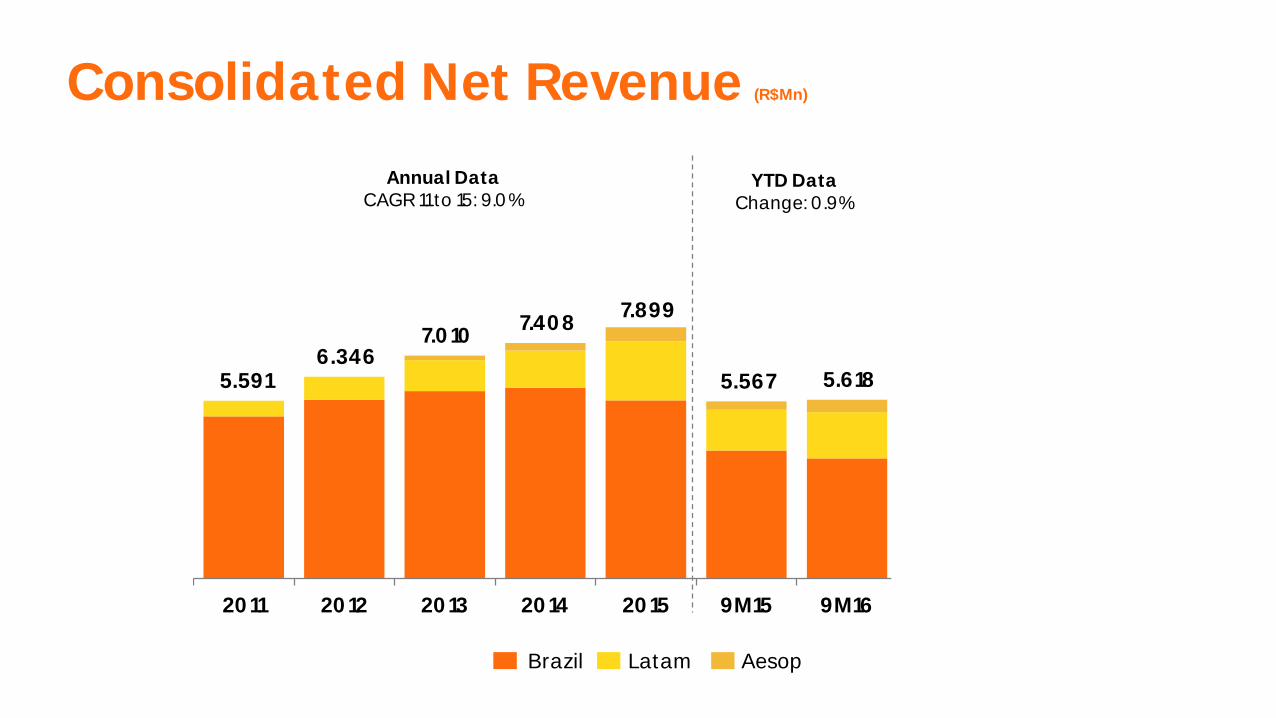

5.591 6.346

7.010 7.408

7.899

5.567 5.618

1.996 1.903

2011 2012 2013 2014 2015 9M15 9M16 3Q15 3Q16

Consolidated Net Revenue (R$Mn)

Annual DataCAGR 11 to 15: 9.0%

YTD DataChange: 0.9%

LatamBrazil Aesop

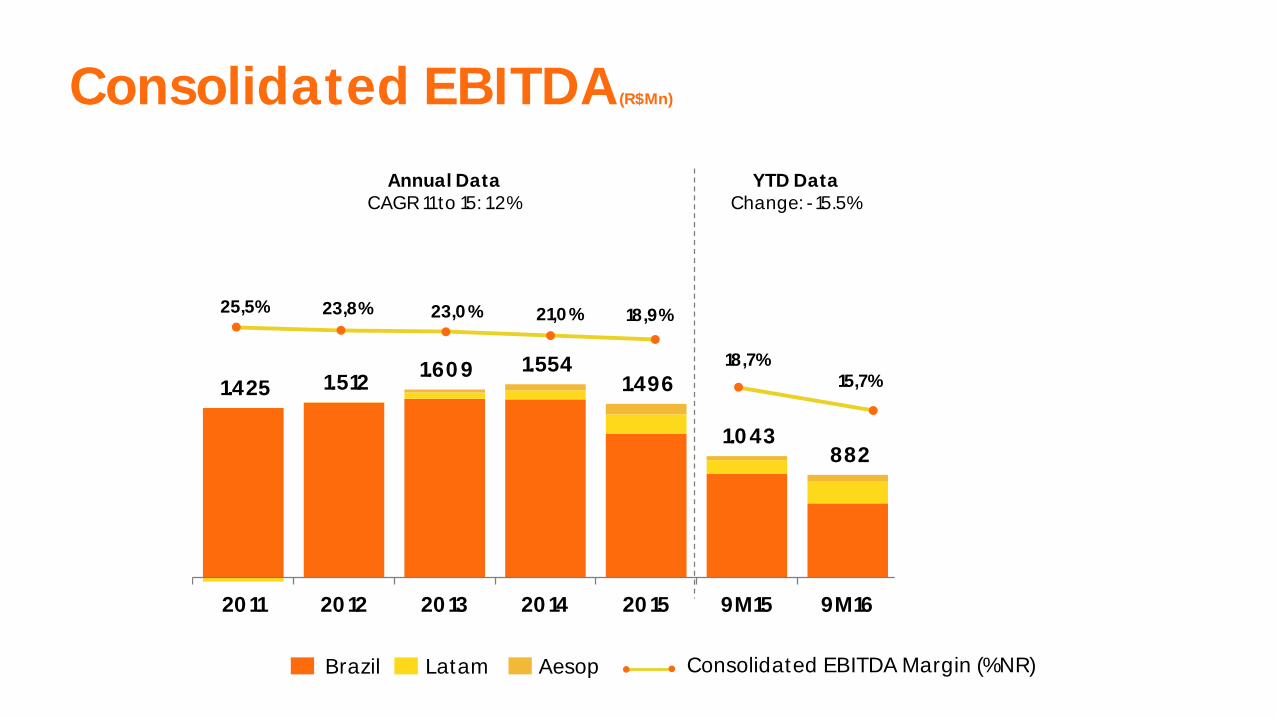

1.425 1.512 1.609 1.554

1.496

1.043 882

400 320

2011 2012 2013 2014 2015 9M15 9M16 3Q15 3Q16

25,5% 23,8% 23,0% 21,0% 18,9%

18,7%15,7%

20,0% 16,8%

Consolidated EBITDA (R$Mn)

Consolidated EBITDA Margin (%NR)

Annual DataCAGR 11 to 15: 1.2%

YTD DataChange: -15.5%

LatamBrazil Aesop

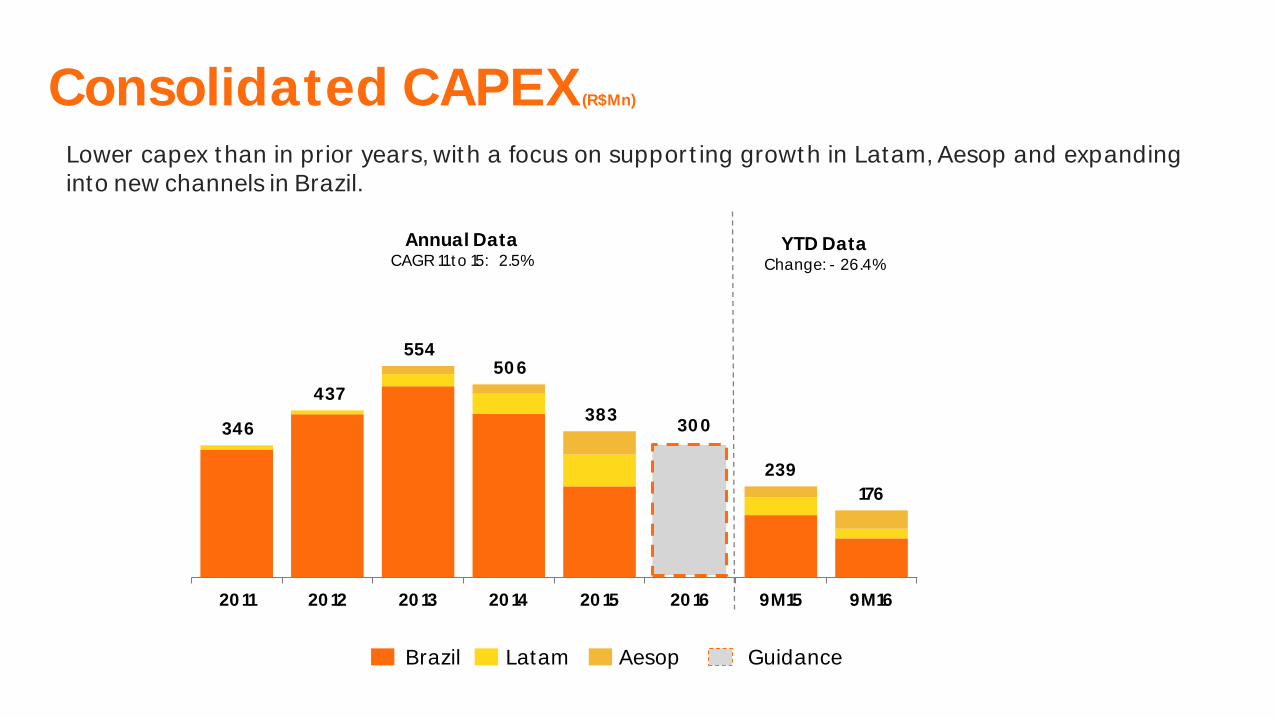

346

437

554 506

383 300

239

176

9865

2011 2012 2013 2014 2015 2016 9M15 9M16 3Q15 3Q16

Annual DataCAGR 11 to 15: 2.5%

YTD DataChange: - 26.4%

Guidance

Consolidated CAPEX (R$Mn)

Lower capex than in prior years, with a focus on supporting growth in Latam, Aesop and expandinginto new channels in Brazil.

LatamBrazil Aesop

Sustainability

Sustainable use of Brazil's social biodiversity (UEBT* re-certification)

Relaunch of Ekos with packaging made from 100% recycled PET

Launch of Natura Amazonia Challenge: Businesses for the Standing Forest

Carbon Neutral Program

Natura Consultant HDI and benefits for our consultants

Crer para Ver product Line

Environmental Accounting (EP&L)

* Union for Ethical BioTrade

Fragrances

Fragrances

Natura is world's tenth largest player and is:

» Leader in fragrances for men in Brazil

» Second in fragrances for women in Brazil

Largest CFT category in Brazil

Source: Euromonitor/ Kantar

Natura Day 2016 [Confidencial]

Sustainable Innovations

Natura FragrancesOur differentials

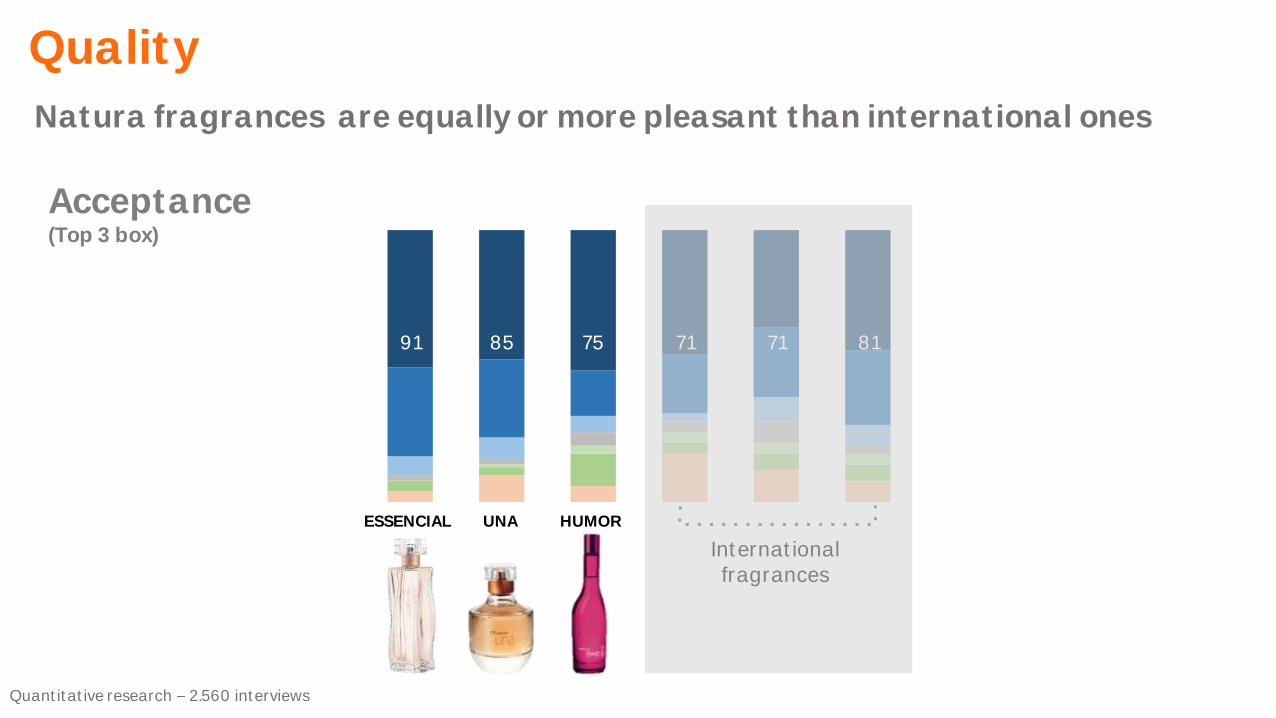

Quality Our BrandsArt of Perfumery

91 85 75 71 71 81

ESSENCIAL UNA HUMOR

Natura fragrances are equally or more pleasant than international ones

Quality

Acceptance(Top 3 box)

Quantitative research 2.560 interviews

International fragrances

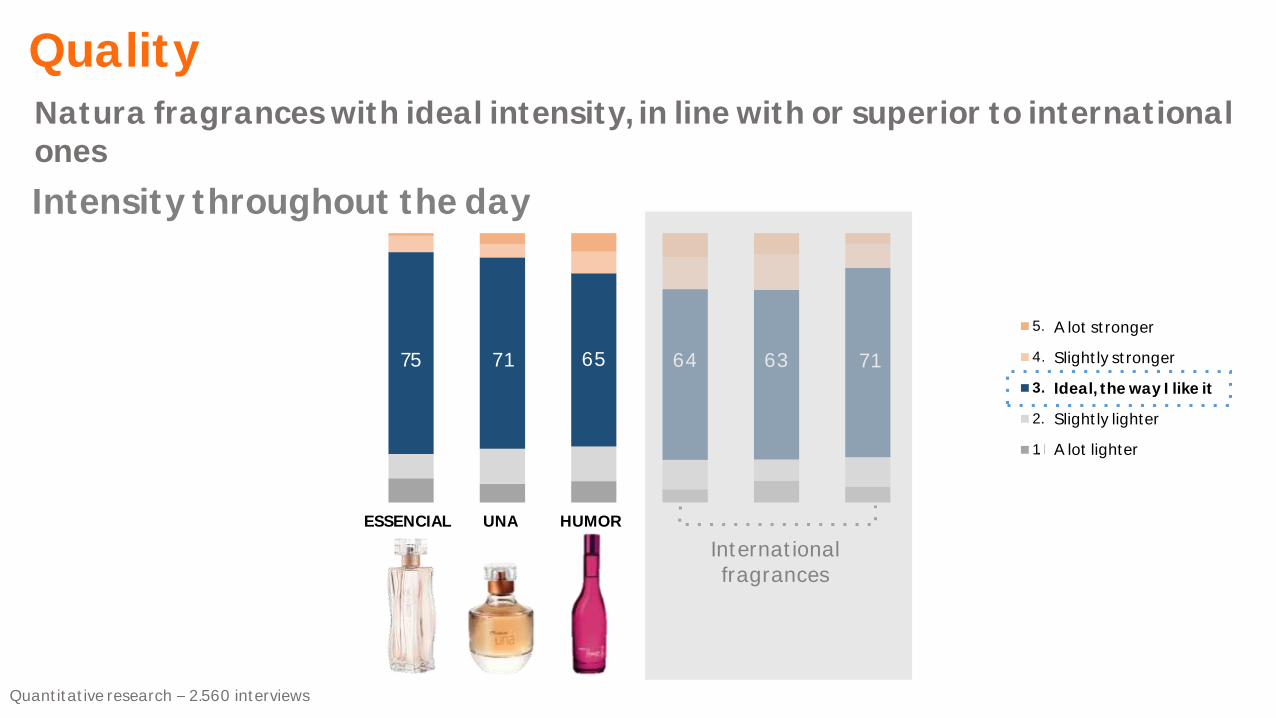

67 66 73 75 71 65 64 63 71

5. Muito mais forte

4. Um pouco mais forte

3. Ideal, como eu gosto

2. Um pouco mais fraca

1. Muito mais fraca

Quality

Intensity throughout the day

Natura fragrances with ideal intensity, in line with or superior to international ones

Quantitative research 2.560 interviews

International fragrances

ESSENCIAL UNA HUMOR

A lot stronger

Slightly stronger

Ideal, the way I like it

Slightly lighter

A lot lighter

Revised marketing strategy

Regional initiatives

Sales force incentives

Portfolio improvement

New style of communication

2017

Revitalizing direct selling

Natura Beauty Specialists

Channel segmentation

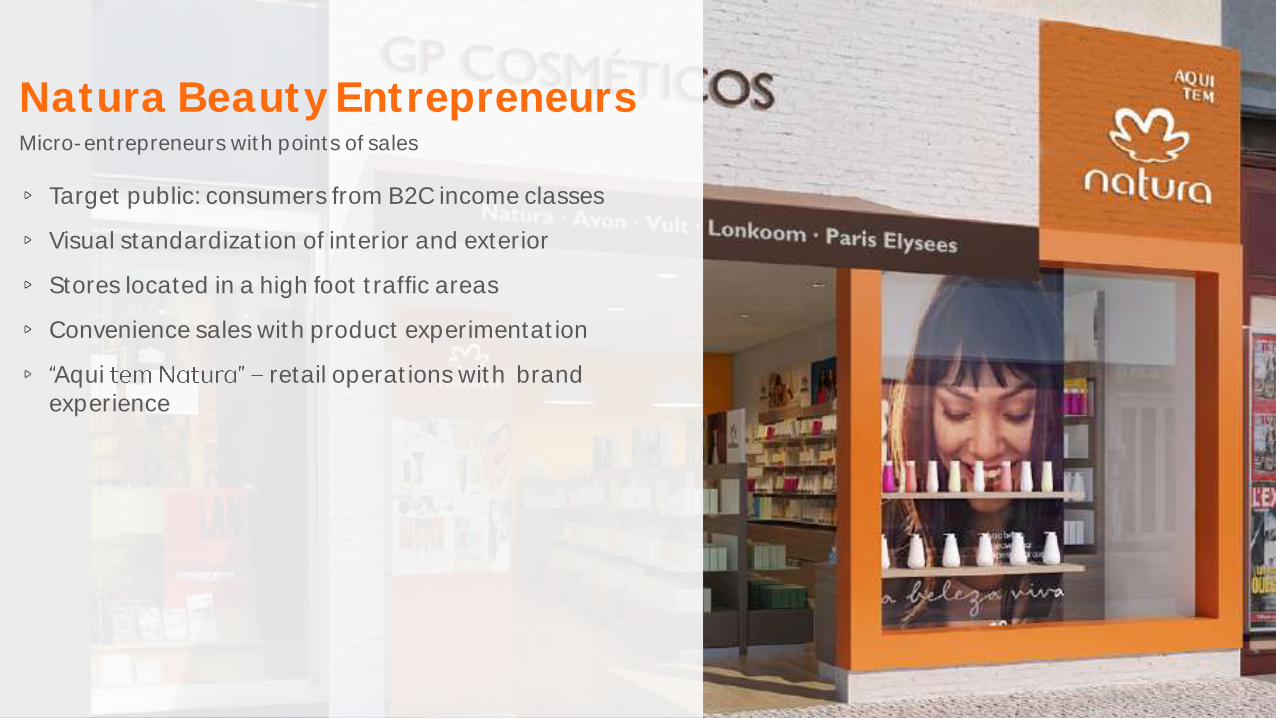

Natura Beauty Entrepreneurs

Natura Beauty Consultants

Natura Beauty Entrepreneurs Micro-entrepreneurs with points of sales

Target public: consumers from B2C income classes

Visual standardization of interior and exterior

Stores located in a high foot traffic areas

Convenience sales with product experimentation

Aqui retail operations with brand experience

Previous store New store

Natura Beauty SpecialistsProfessionals connected to the universe of beauty, with higher education levels and ideal profile for selling "core beauty"

Consulting as a career: self-fulfillment and pleasure

Focus on face care and makeup

Unique experience: assistance and experimentation

Exclusive opportunities :

Training in partnership with Anhembi MorumbiUniversity

Independent career development

Demonstration kit and samples

Specific recruitment and selection

Digital tool for service level improvement

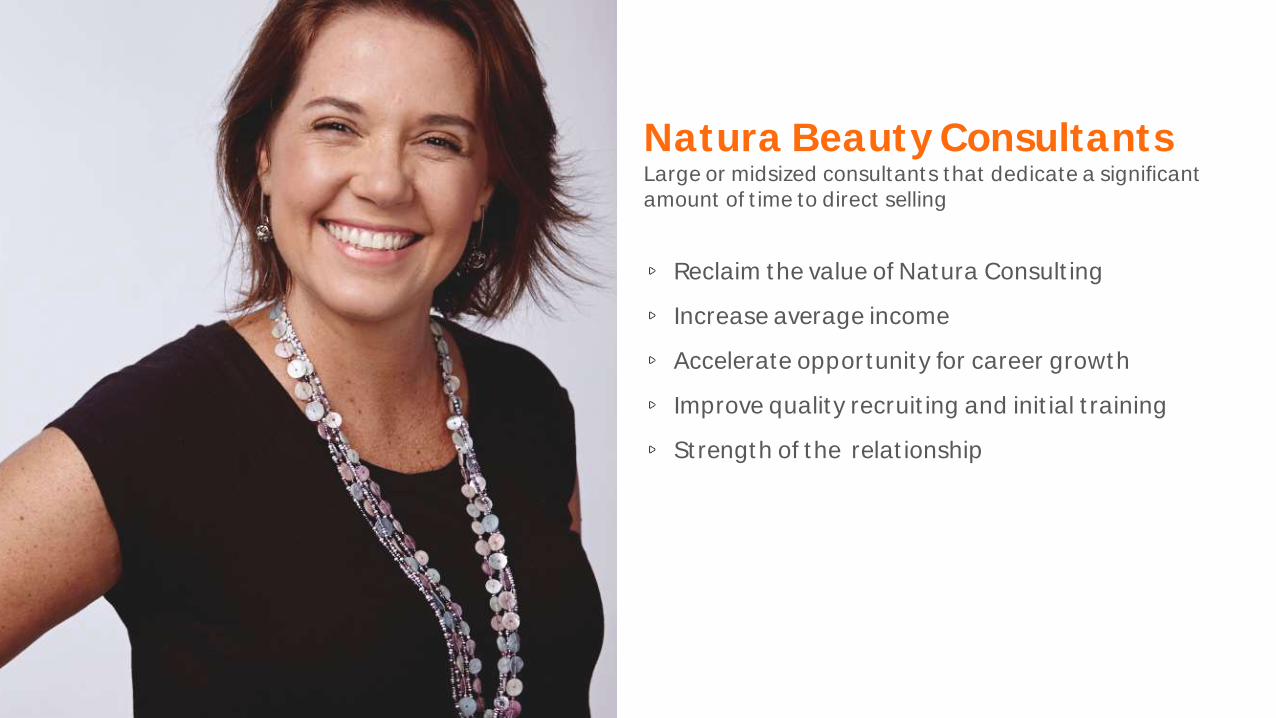

Natura Beauty ConsultantsLarge or midsized consultants that dedicate a significant amount of time to direct selling

Reclaim the value of Natura Consulting

Increase average income

Accelerate opportunity for career growth

Improve quality recruiting and initial training

Strength of the relationship

Digitalization

Rede Natura

One of Brazil's largest beauty e-commerce retailers

Diamond Ebit Certification and most admired cosmetics and fragrance store

• 1,5MM consumers registered

• 90K Digital Natura Consultants

• 50% of channel is incremental: Purely digital Natura Digital Consultant

• 2x revenue in 2016 vs. 2015 (forecast)

Natura is a digital business: 99,65% of all orders are captured digitally.

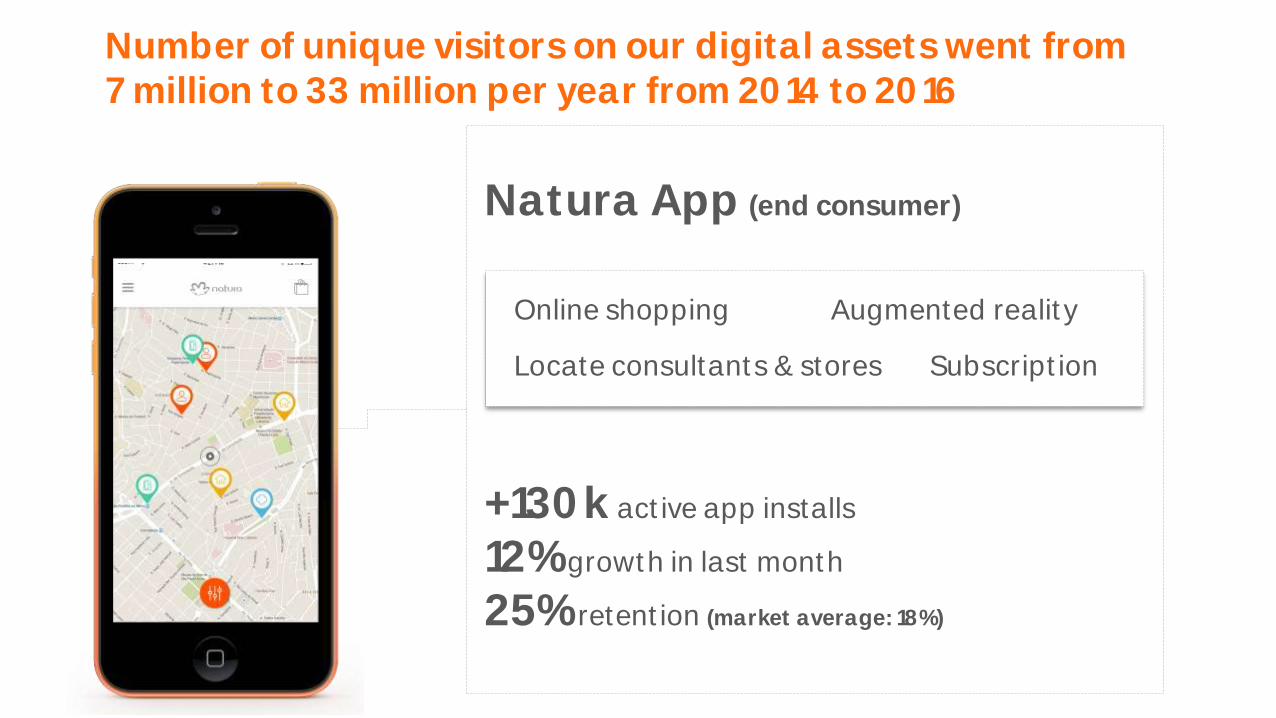

Consulting App

8,3% average productivity gain

270k active consultants

12% of orders placed via app

2% average sales growth with activation via push

70% of traffic to order capture systems

Order Capture

Promotions / Digital Magazine

Voice Orders

Payments

Natura App (end consumer)

+130k active app installs

12% growth in last month

25% retention (market average: 18%)

Number of unique visitors on our digital assets went from 7 million to 33 million per year from 2014 to 2016

Online shopping

Locate consultants & stores

Augmented reality

Subscription

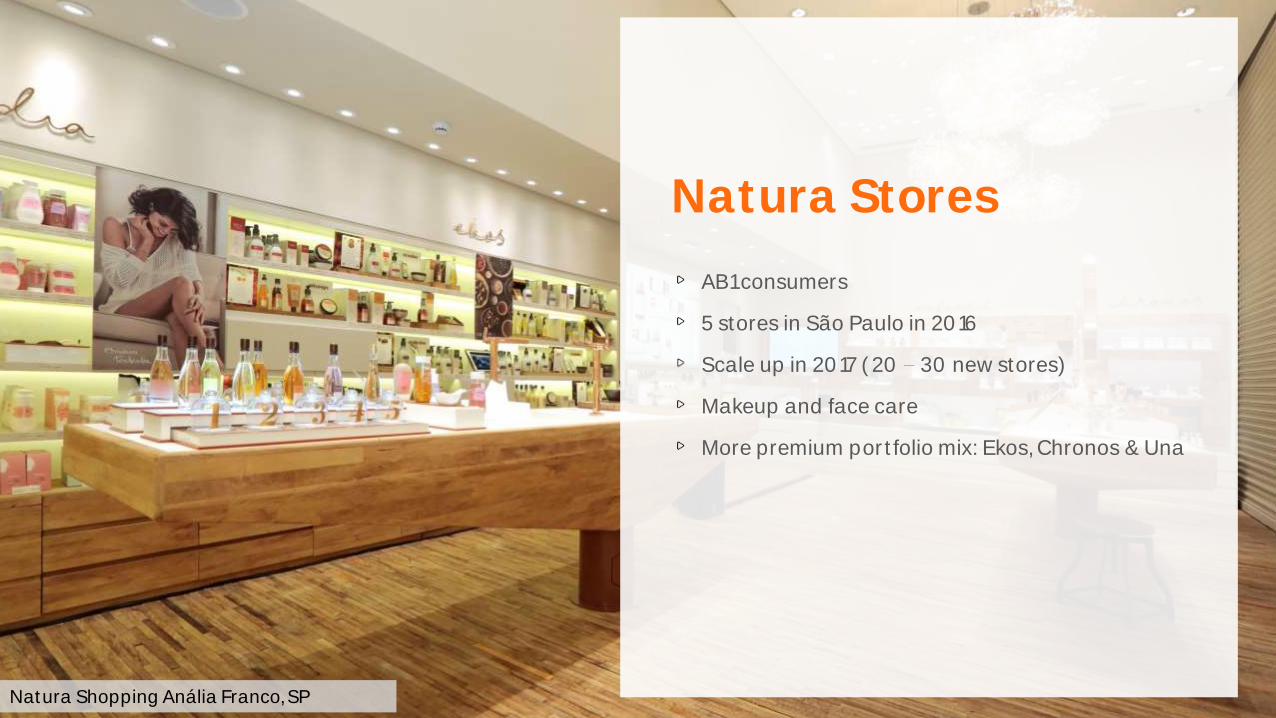

Brazil Retail

Natura Shopping Anália Franco, SP

Natura Stores

AB1 consumers

5 stores in São Paulo in 2016

Scale up in 2017 ( 20 30 new stores)

Makeup and face care

More premium portfolio mix: Ekos, Chronos & Una

Natura Shopping Anália Franco, SP

Drugstores

Sou Line in ~2,000 stores

Expansion to other chains in 2017

Tez Pilot launched

Latam

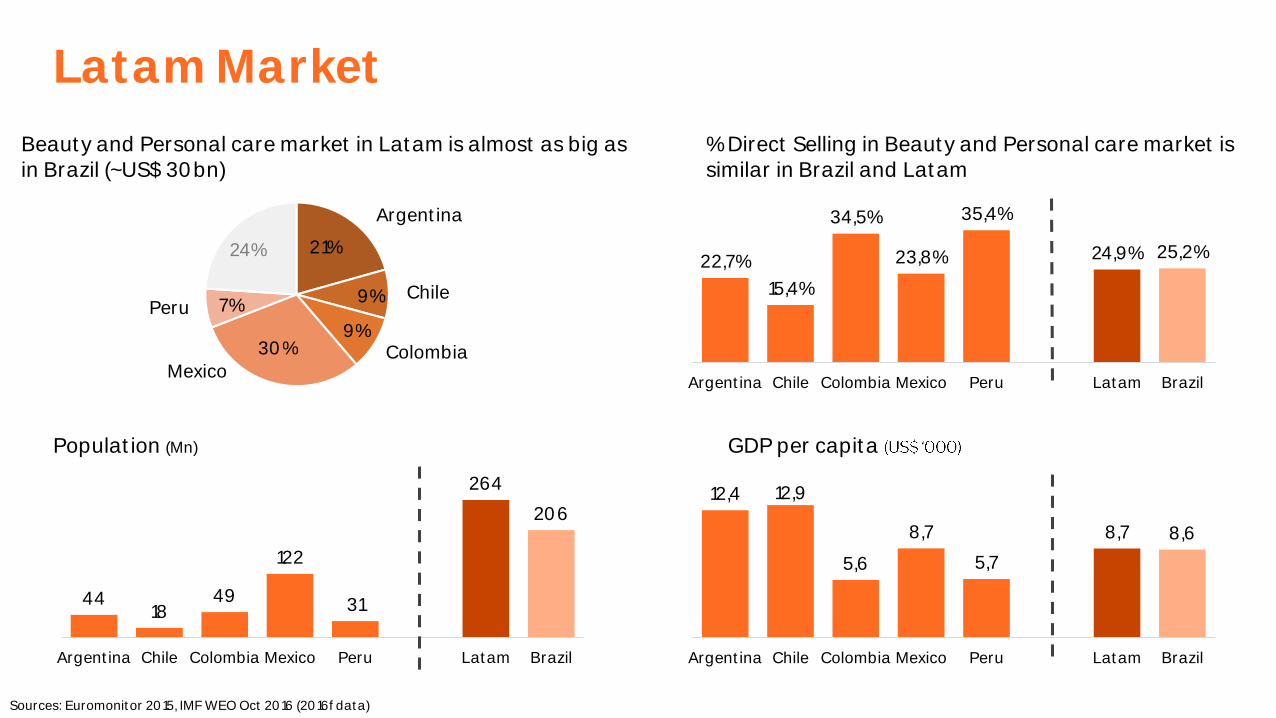

4418

49

122

31

264

206

Argentina Chile Colombia Mexico Peru Latam Brazil

Latam Market

21%

9%

9%30%

7%

24%22,7%

15,4%

34,5%

23,8%

35,4%

24,9% 25,2%

Argentina Chile Colombia Mexico Peru Latam Brazil

Sources: Euromonitor 2015, IMF WEO Oct 2016 (2016f data)

Beauty and Personal care market in Latam is almost as big as in Brazil (~US$ 30bn)

% Direct Selling in Beauty and Personal care market is similar in Brazil and Latam

Population (Mn) GDP per capita

Argentina

ChilePeru

MexicoColombia

12,4 12,9

5,6

8,7

5,7

8,7 8,6

Argentina Chile Colombia Mexico Peru Latam Brazil

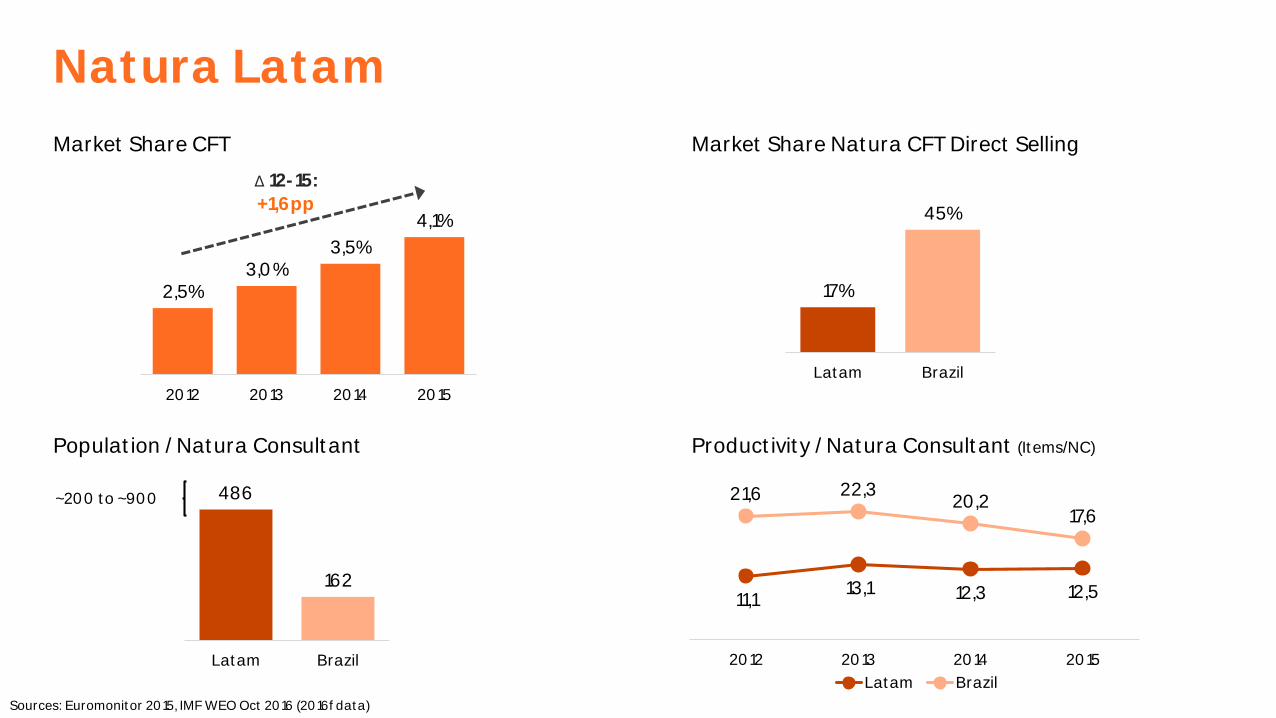

Natura Latam

Market Share CFT Market Share Natura CFT Direct Selling

Population / Natura Consultant Productivity / Natura Consultant (Items/NC)

2,5%3,0%

3,5%

4,1%

2012 2013 2014 2015

∆ 12-15:

+1,6pp

Sources: Euromonitor 2015, IMF WEO Oct 2016 (2016f data)

17%

45%

Latam Brazil

486

162

Latam Brazil

~200 to ~900

11,113,1 12,3 12,5

21,6 22,320,2

17,6

2012 2013 2014 2015

Latam Brazil

Natura Latam

Brand Preference

1

53 65

170 117

189 9,1%

13,0%

0,1%

5,4% 5,6%9,1%

-0,1

-0,05

0

0,05

0,1

2012 2013 2014 2015 9M15 9M16

-

50

100

150

200

250

EBITDA Latam

EBITDA (R$ Mn) EBITDA Margin

Profitability

2015

24% 1º

35% 1º

26% 1º

5% 6º

11% 5º Latam Preference20,5% (2015)

Source: Brand Essence (IPSOS) 2015

Strong construction of attributes of "Brazilianness" and "Connection with nature"

Natura is ready to sustain strong pace growth

- Operation and logistics services (34% regional production)

- Local team and positive reputation

- Multi-channel shopping experience

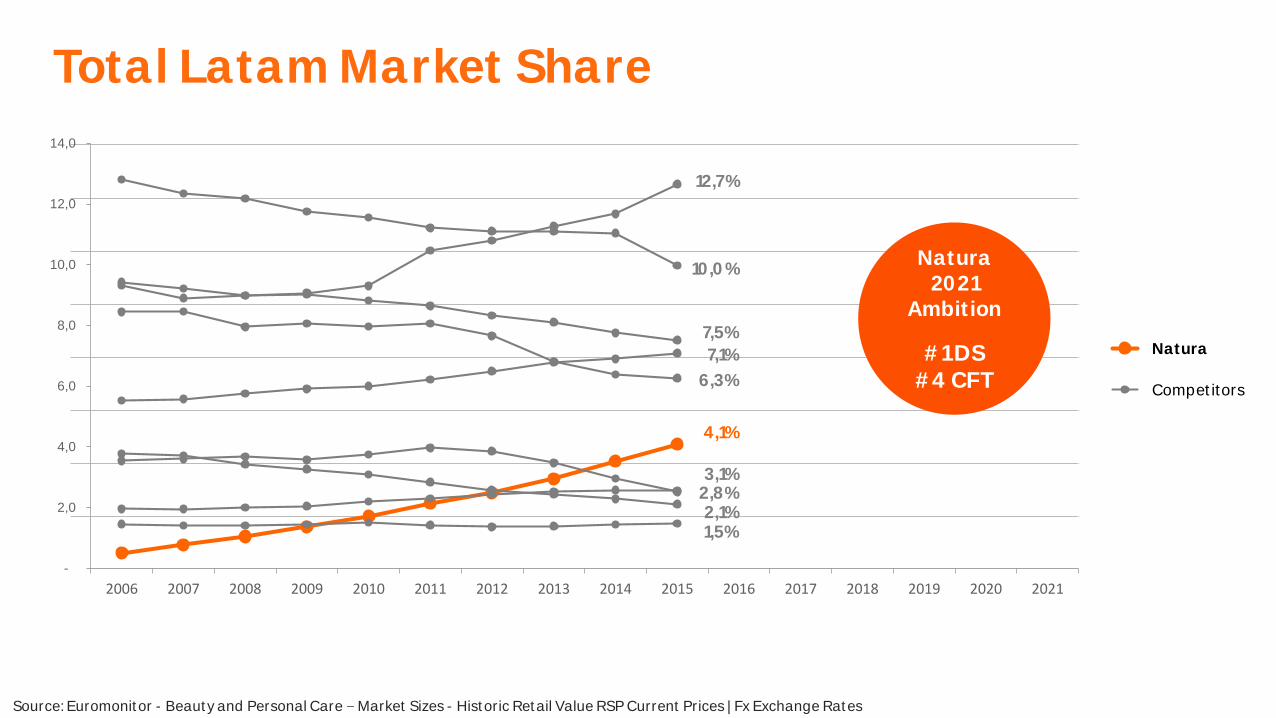

-

2,0

4,0

6,0

8,0

10,0

12,0

14,0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Unilever

P&G

L'Oréal

Colgate

Avon

Natura

Belcorp

BeiersdorfJafra

J&J

Natura 2021

Ambition

#1 DS#4 CFT

1,5%

10,0%

12,7%

7,5%

4,1%

3,1%

6,3%

2,1%2,8%

Source: Euromonitor - Beauty and Personal Care Market Sizes - Historic Retail Value RSP Current Prices | Fx Exchange Rates

Natura

Competitors

7,1%

Total Latam Market Share

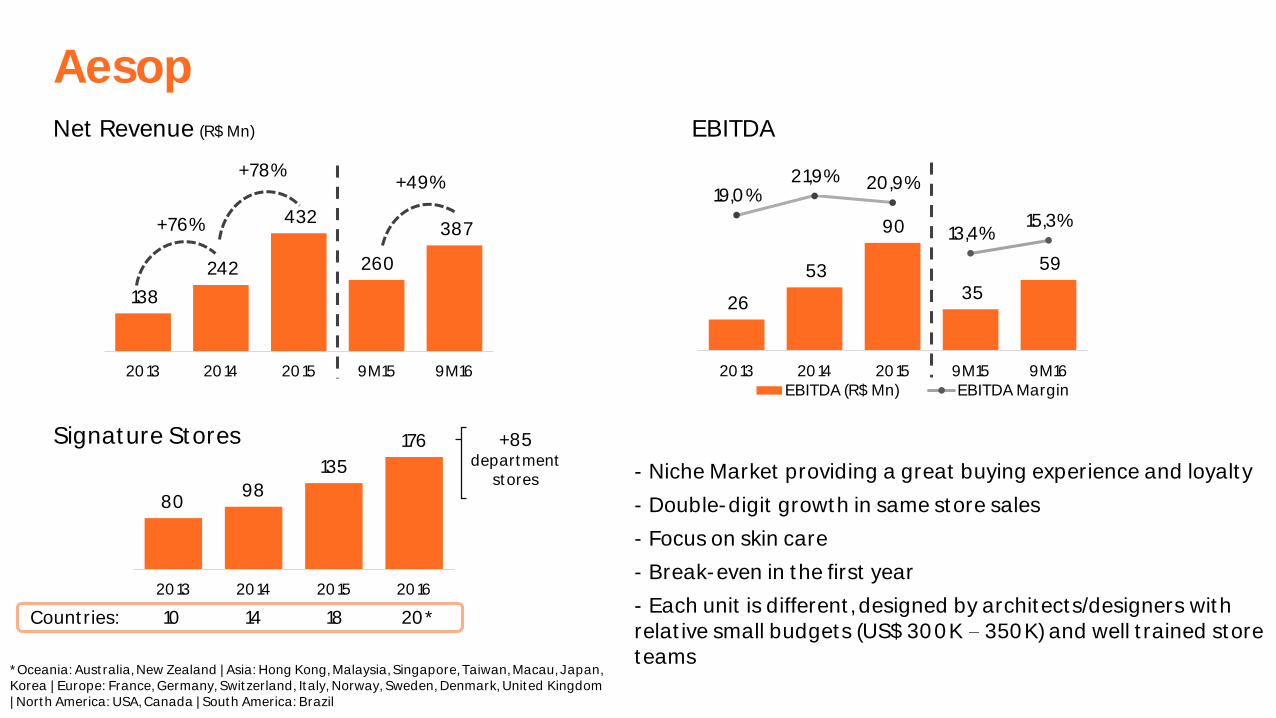

Aesop

26

53

90

35

59

13,4%15,3%

19,0%21,9% 20,9%

-0,03

0,02

0,07

0,12

0,17

0,22

-10

10

30

50

70

90

110

130

2013 2014 2015 9M15 9M16EBITDA (R$ Mn) EBITDA Margin

AesopNet Revenue (R$ Mn)

138

242

432

260

387

2013 2014 2015 9M15 9M16

+76%

+78%+49%

8098

135

176

2013 2014 2015 2016

Signature Stores

14 18 20*Countries:

* Oceania: Australia, New Zealand | Asia: Hong Kong, Malaysia, Singapore, Taiwan, Macau, Japan,Korea | Europe: France, Germany, Switzerland, Italy, Norway, Sweden, Denmark, United Kingdom| North America: USA, Canada | South America: Brazil

10

EBITDA

- Niche Market providing a great buying experience and loyalty

- Double-digit growth in same store sales

- Focus on skin care

- Break-even in the first year

- Each unit is different, designed by architects/designers with relative small budgets (US$ 300K 350K) and well trained store teams

+85 department

stores

Thank you

![IMF 2014 WEO data Sampler 3 [kompatibilitätsmodus]](https://static.fdocuments.in/doc/165x107/55a77e2b1a28abc9668b48a2/imf-2014-weo-data-sampler-3-kompatibilitaetsmodus.jpg)