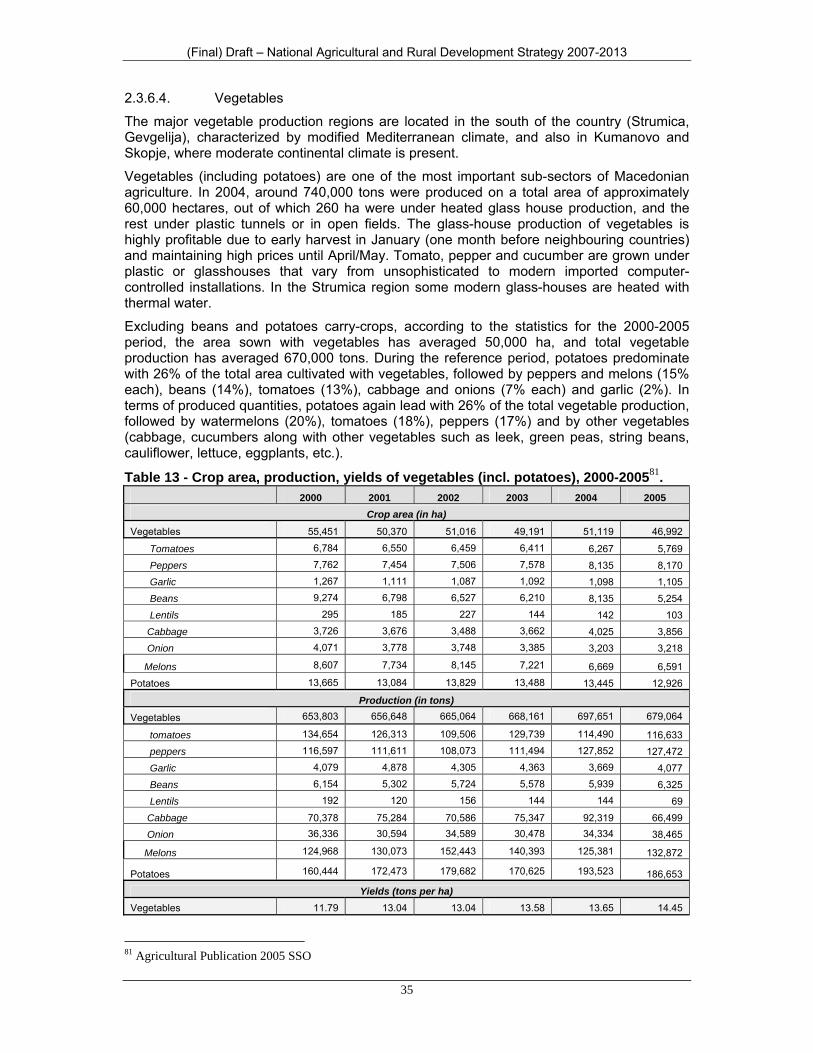

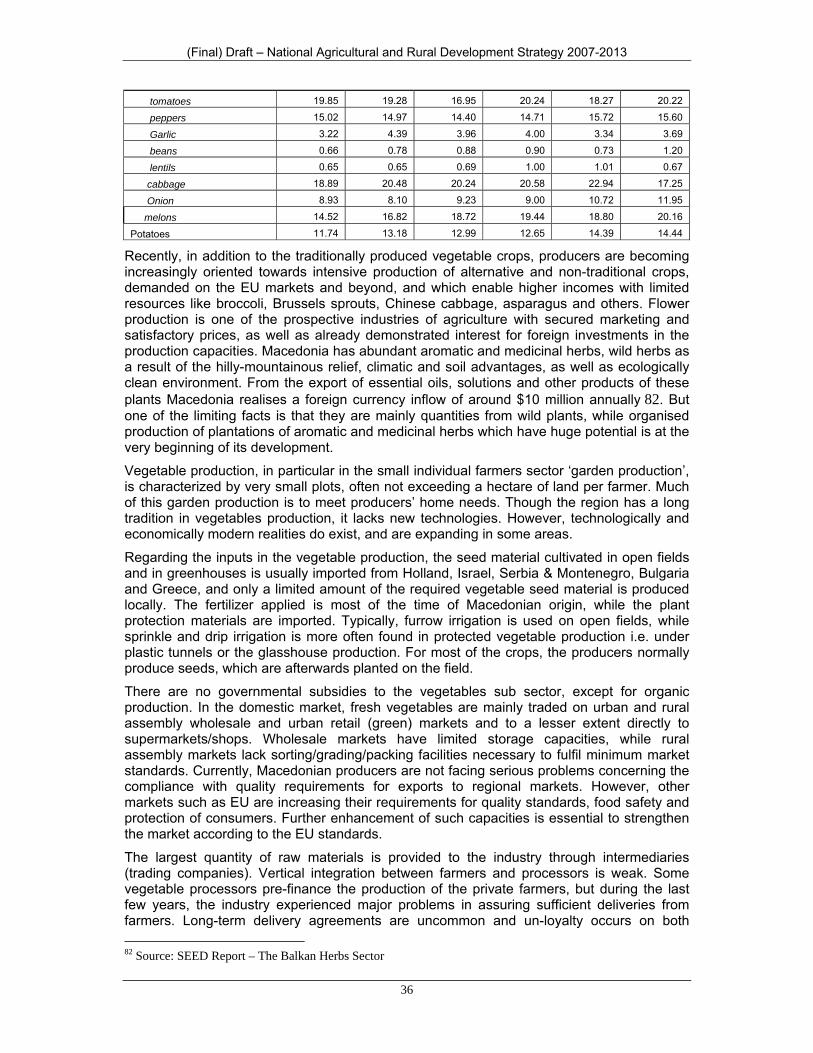

NATIONAL AGRICULTURAL AND RURAL DEVELOPMENT STRATEGY …faolex.fao.org/docs/pdf/mac147994.pdf ·...

132

REPUBLIC OF MACEDONIA Ministry of Agriculture, Forestry and Water Economy NATIONAL AGRICULTURAL AND RURAL DEVELOPMENT STRATEGY (NARDS) FOR THE PERIOD 2007-2013 Skopje, June 2007

Transcript of NATIONAL AGRICULTURAL AND RURAL DEVELOPMENT STRATEGY …faolex.fao.org/docs/pdf/mac147994.pdf ·...

REPUBLIC OF MACEDONIA Ministry of Agriculture, Forestry and Water Economy

NATIONAL AGRICULTURAL AND RURAL DEVELOPMENT STRATEGY (NARDS)

FOR THE PERIOD 2007-2013

Skopje, June 2007

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

2

TABLE OF CONTENTS

ACRONYMS AND ABBREVIATIONS ..................................................................... 4

1. PURPOSES AND STRUCTURE OF THE DOCUMENT .............................. 6 1.1. Purposes ..................................................................................................................... 6 1.2. Structure of the document ........................................................................................ 6 2. CURRENT SITUATION ................................................................................ 7 2.1. Role of Agriculture in the Economy .................................................................... 7

2.1.1. Geographic, Political and Administrative Background 7 2.1.2. Macroeconomic Framework 8 2.1.3. Role of Agriculture in the Economy 9

2.2. Rural Sector Analysis ......................................................................................... 10 2.2.1. Characterisation of Rural Areas. 10 2.2.2. Rural Demography and Education. 13 2.2.3. Employment (including SMEs, Crafts and Rural Tourism). 14 2.2.4. Social Care Infrastructure. 17 2.2.5. Technical Infrastructure. 17 2.2.6. Rural Development policies. 18

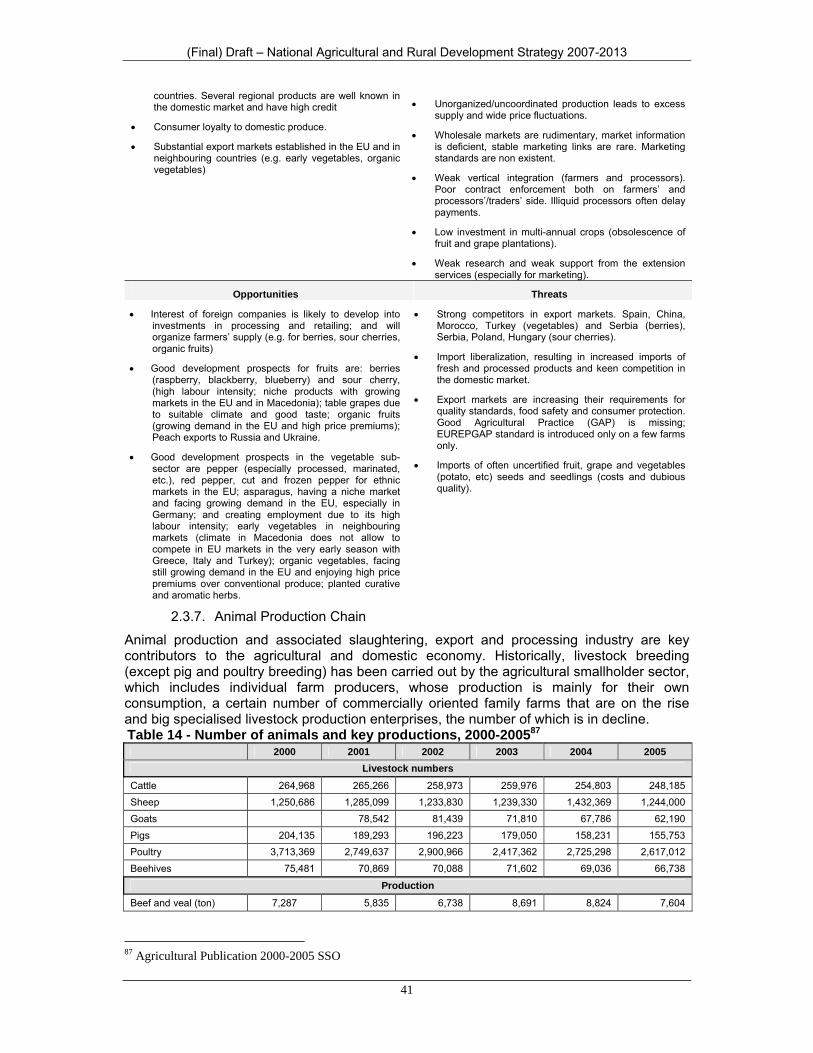

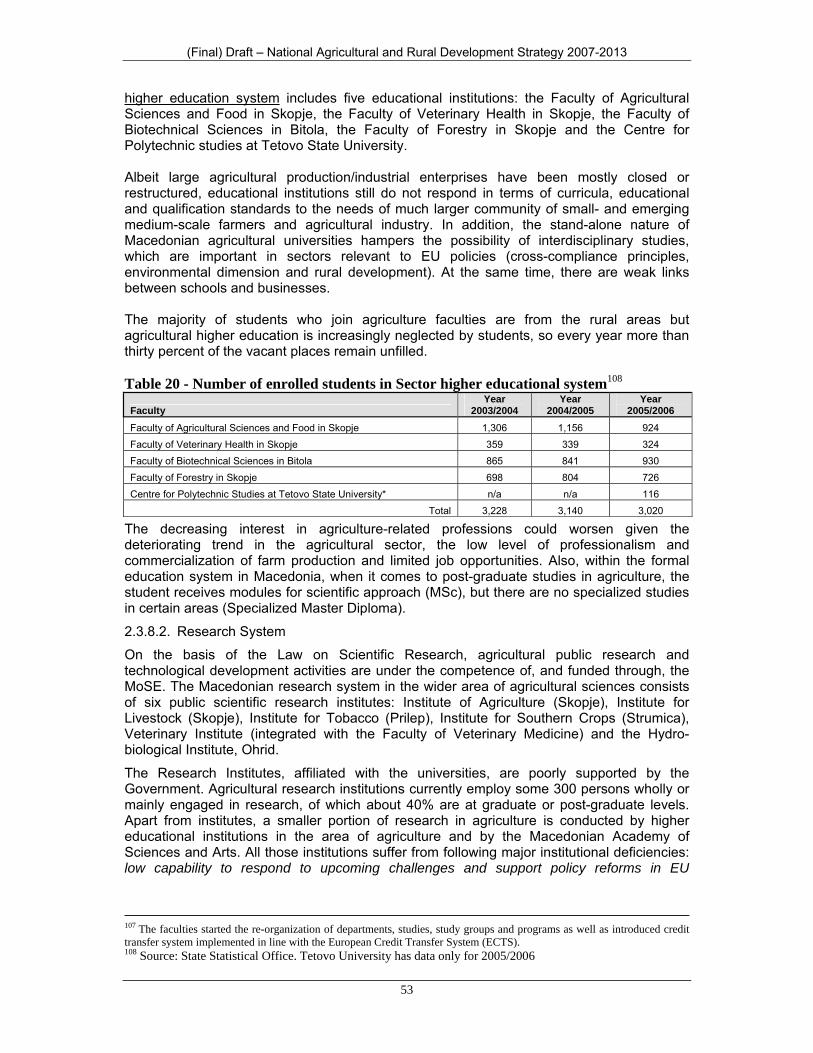

2.3. Sector Analysis: Agriculture .............................................................................. 19 2.3.1. Land Resources, Land Use and Main Agricultural Areas. 19 2.3.2. Land Ownership, Farm Structure and Productivity. 19 2.3.3. Agricultural Labour 21 2.3.4. Foreign Trade of Agricultural and Food Products 21 2.3.5. Main Agricultural Sub-sectors. 24 2.3.6. Crop Production Chain 24 2.3.7. Animal Production Chain 41 2.3.8. Education, Research and Extension Services in Agriculture 51 2.3.9. Biodiversity, Agriculture and the Environment 57

2.4. Sector Analysis: Fishery and Aquaculture ....................................................... 65 2.4.1. Fishery and Aquaculture Resources 65 2.4.2. Fishery and Aquaculture Policies and Programs 66

2.5. Sector Analysis: Forestry ................................................................................... 66 2.5.1. Forest Resources 66

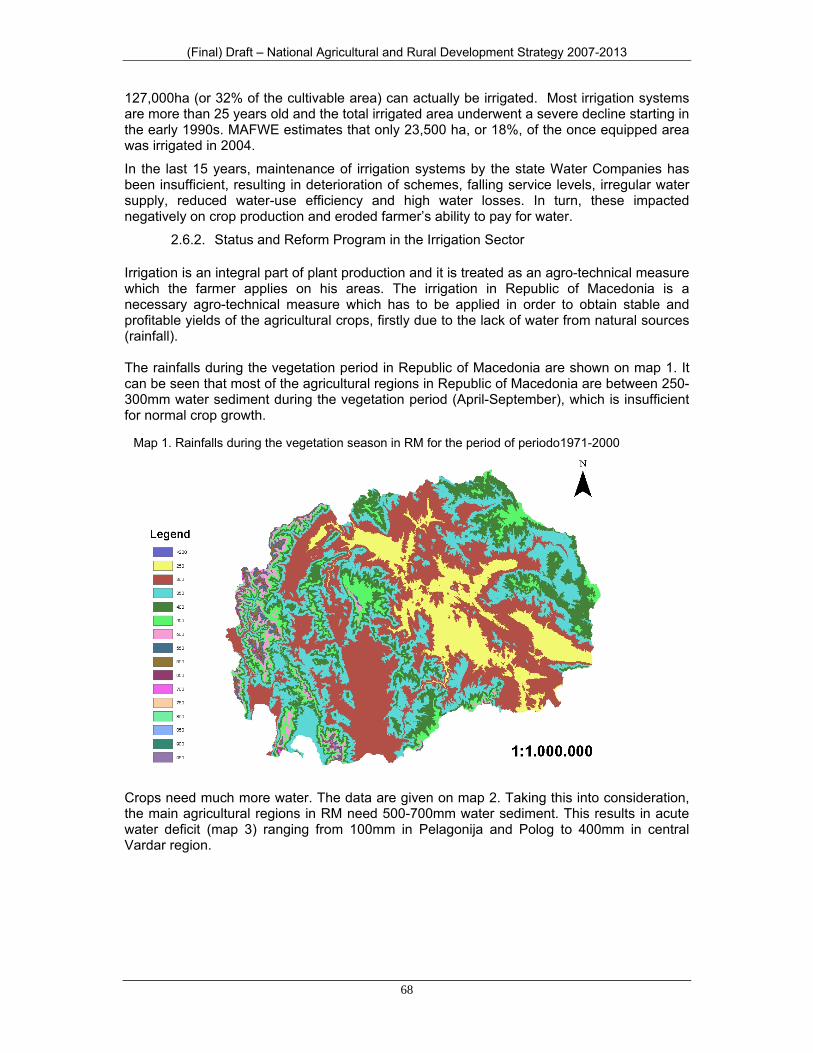

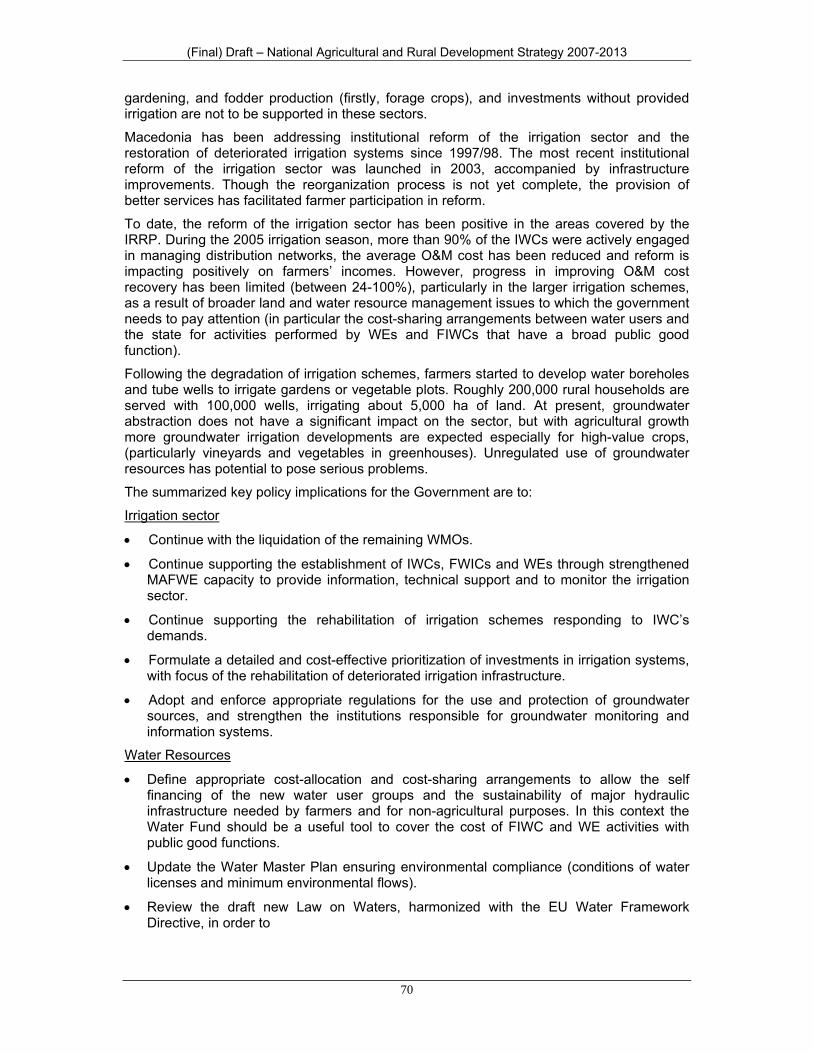

2.6. Sector Analysis: Water Economy ...................................................................... 67 2.6.1. Linkages between agriculture and water resources 67 2.6.2. Status and Reform Program in the Irrigation Sector 68

2.7. Legislative and Institutional Framework ........................................................... 71 2.8. Key Factors Hampering Agricultural and Rural Development ........................ 72 3. AGRICULTURAL AND RURAL DEVELOPMENT STRATEGY ............... 73 3.1. National Strategic Objective ............................................................................... 73 3.2. Strategic Policy Focal Issues ............................................................................. 74 3.3. Agricultural Support Policies ............................................................................. 81

3.3.1. Direct Payments in Crop Production 82 3.3.2. Livestock Production Chain Policies and Measures 92

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

3

3.4. Rural Development Policies ............................................................................. 100 3.4.1. AXIS 1 - Market efficiency and implementation of EU standards 101 3.4.2. AXIS 2 - Agri-environmental measures and local rural development 104 3.4.3. AXIS 3 - Development of the rural economy 104 3.4.4. AXIS 4 - Technical Assistance 105

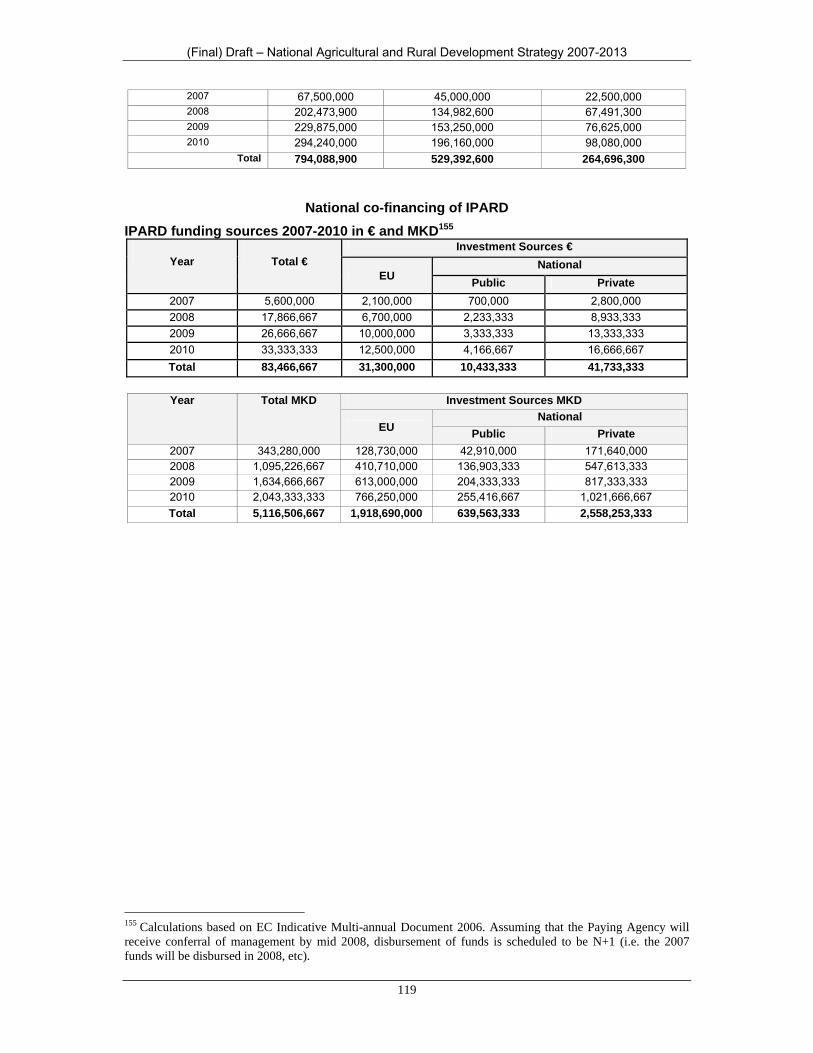

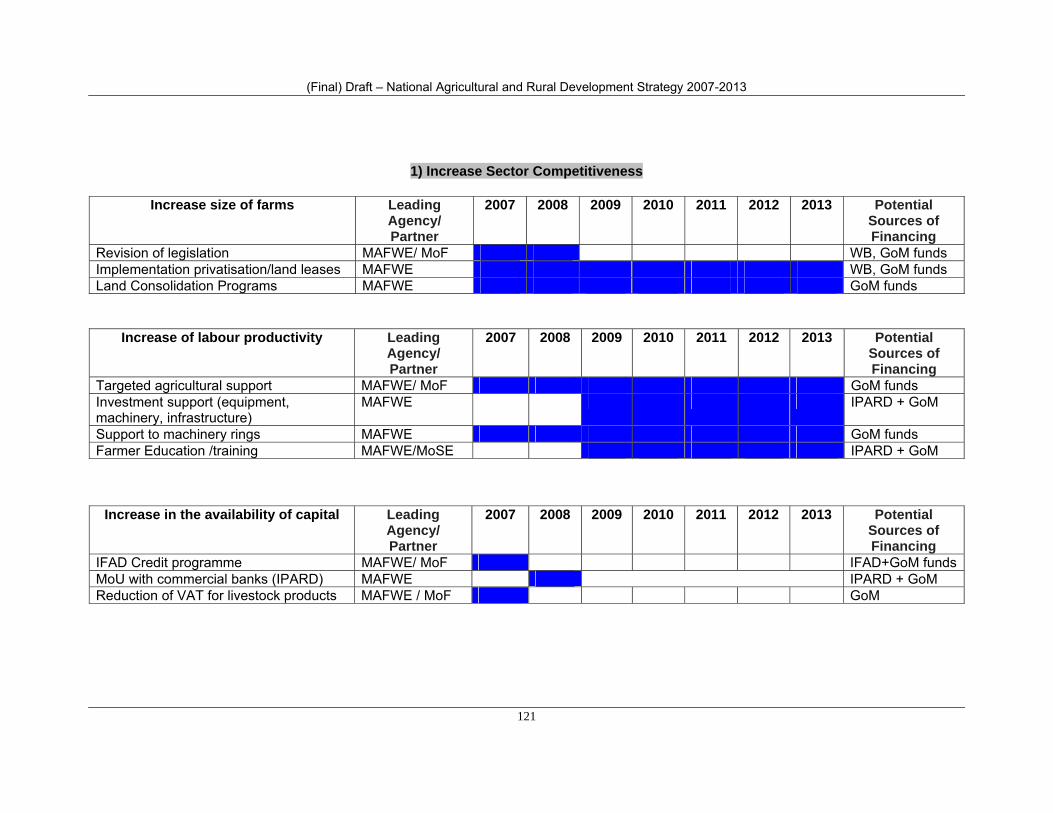

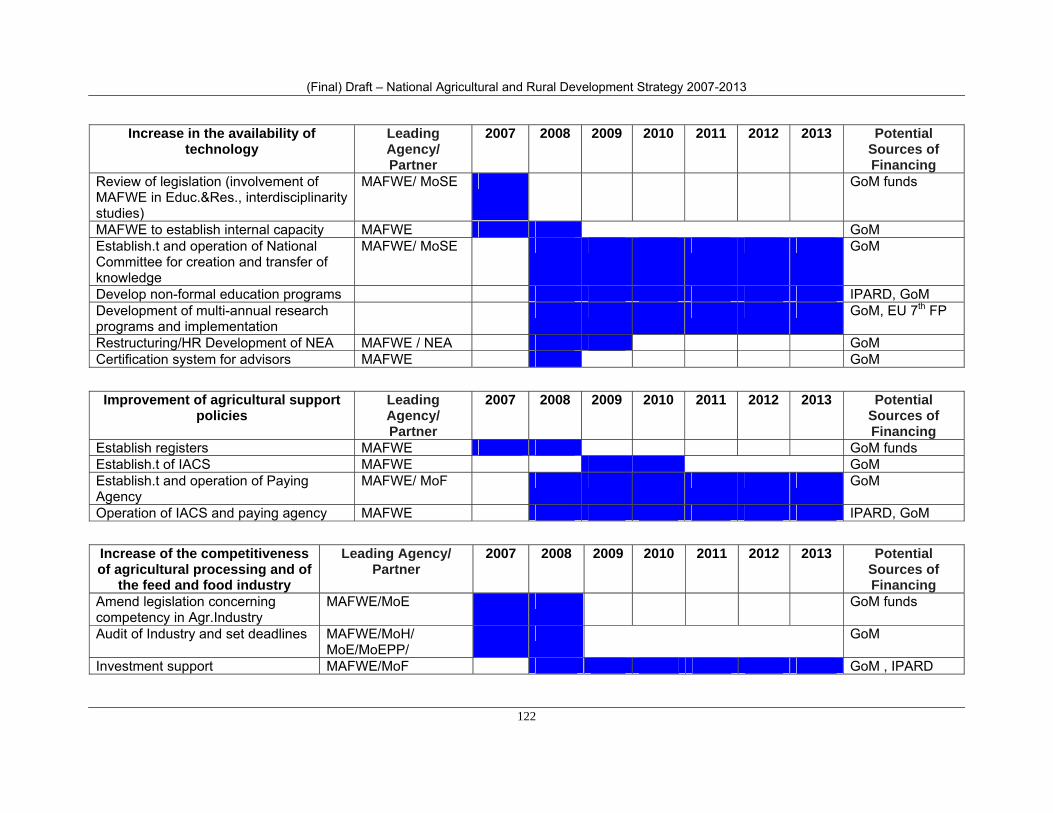

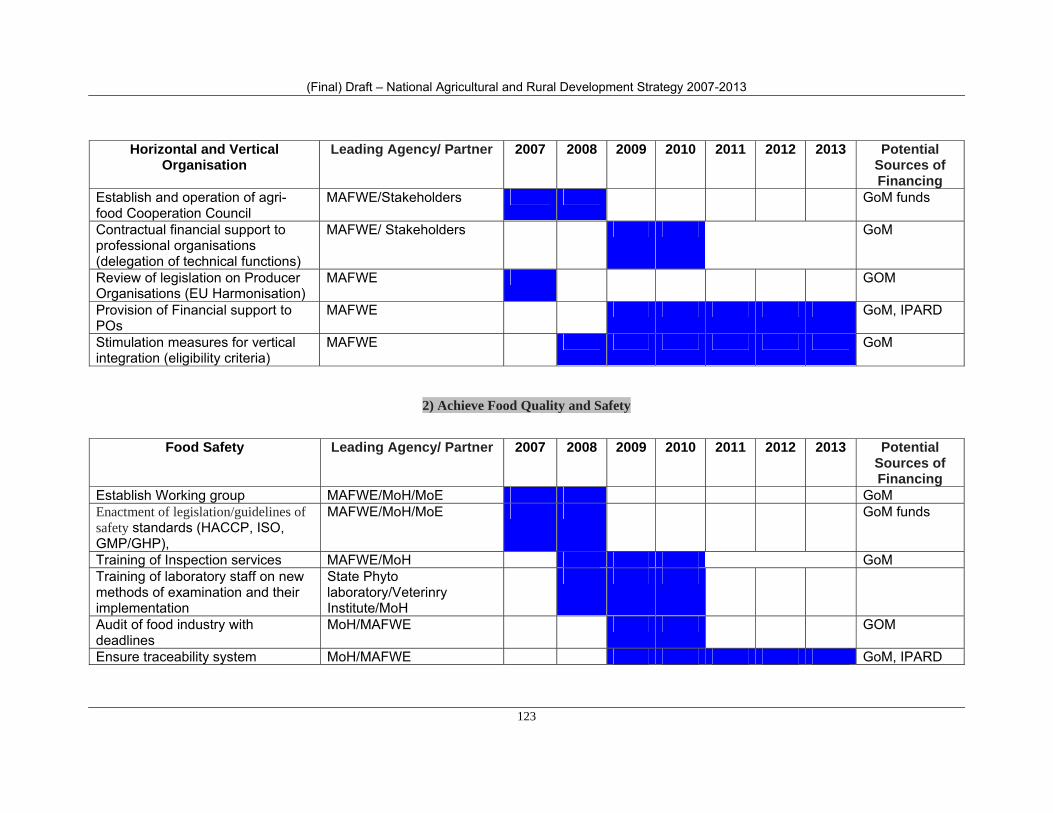

3.5. Legislative Harmonisation and Institutional Reform Policies ....................... 106 3.6. Budgetary resources for agriculture and rural development ....................... 118 4. IMPLEMENTATION PLAN OF PROPOSED policies ............................. 120

5. LAND POLICY ................................................................................................. 127

6. FORESTRY ...................................................................................................... 128 6.1. Vision ...................................................................................................................... 129 6.2. General objectives ................................................................................................. 130 6.3. Main directions: ...................................................................................................... 130 7. WATER ECONOMY ......................................................................................... 130 7.1 Strategic Water Economy Determinations ........................................................... 130 7.2. Strengthening the capacity of the Water Economy Directorate (WED) ............ 131 7.3 Irrigation measures ................................................................................................. 131

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

4

ACRONYMS AND ABBREVIATIONS

AE Agro-environmental AI Artificial Insemination AIS Agricultural Information System AMIS Agricultural Market Information System CAP Common Agricultural Policy (of the EU) CARDS Community Assistance for Reconstruction, Development and Stability CEFTA Central European Free Trade Agreement CMO Common Market Organisation (of the EU CAP) EU European Union EU-15 European Union of 15 Member States EU-25 European Union of 25 Member States (without Bulgaria and Romania) EU-27 European Union of 27 Member States Eurostat European Statistical Office EC European Community FADN Farm Accountancy Data Network FMS Farm Monitoring System FTA Free Trade Agreement FAO Food and Agriculture Organization (of the UN) FIWC Federation of Irrigation Water Committees GAO Gross Agricultural Output GAP Good Agriculture Practice/Cross Compliance (EUREPGAP) GDP Gross Domestic ProductGHP Good Hygiene Practice GIS Geographic Information System GHG Glass House effect Gases GMO Genetically Modified Organisms GMP Good Manufacturing Practice GoM Government of RM ha Hectares (10,000 sq.m) HACCP Hazard Analysis and Critical Control Points hl Hectolitres (100 liters) IFAD International Fund for Agricultural Development (of the UN) IACS Integrated Administrative Control System IICB Inter-Institutional Coordination Body IPA Instrument for Pre-Accession assistance IPARD Rural Development component of IPA IBRD International Bank for Reconstruction and Development ICT Information and Communication Technology I&R Animal Identification and Registration System ISO International Standards Organisation IWC Irrigation Water Committee kg Kilogram LFA Less Favoured Areas LPIS Land Parcel Identification System MAFWE Ministry of Agriculture, Forestry and Water Economy (of RM) MAASP Macedonian Agricultural Advisory Support Programme (SIDA funded) MAP Medicinal and Aromatic Plants MEPP Ministry of Environment and Physical Planning MLSG Ministry of Self GovernmentMKD Macedonian Denar MoC Ministry of Culture MoE Ministry of Economy

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

5

MoF Ministry of Finances MoH Ministry of Health MoLSG Ministry of Local Self Government MoSE Ministry of Science and Education MoTC Ministry of Transport and Communication n.a. Not Available NARDS National Agricultural and Rural Development Strategy NEA National Extension Agency (Agency for Promoting Agricultural Development) NUTS Nomenclature of Statistical Territorial Units OECD Organisation Economic Co-operation and Development OG Official Gazette of RM O&M Operation and Maintenance PGI Protected Geographical Indication PDO Protected Designation of OriginPO Producer Organisation RM Republic of Macedonia SEA Secretariat of European Affairs (of the RM) SEE South Eastern Europe SEUROP European Carcass Classification System SIDA Swedish Bilateral Aid SME Small and Medium Enterprise sq. km Square Kilometre SSO State Statistical Office of RM SWOT Strengths, Weaknesses, Opportunities and Threats analysis ton Tons TSG Traditional Specialty Guaranteed UHT Ultra High Temperature (for milk) UN United Nations VAT Value Added Tax VET Vocational Educational Training VMMS Vineyards Monitoring and Management System WB World Bank WE Water Economy WHO World Health Organization WMO Water Management Organization WTO World Trade Organisation

Macedonian Denar (MKD) Exchange rate used € 1 = MKD 61.3

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

6

1. PURPOSES AND STRUCTURE OF THE DOCUMENT

1.1. Purposes The National Strategy for Rural and Agricultural Development 2007-2013 (NARDS) has two interlinked purposes.

The first one is to provide the Macedonian Government (and, more in particular, the Ministry of Agriculture, Forestry and Water Economy - MAFWE) and to the stakeholders (rural dwellers, farmers and their associations, producer groups and processors) a multi-annual reference material – strategy and a tool for the development of Macedonian agriculture and rural areas.

The second one is to establish a base for supporting the drafting of the hierarchically lower-level agricultural and rural development operational plans, in particular the Instrument for Pre-Accession for Agricultural and Rural Development (IPARD) plan, and for their discussion with the European Commission.

In fact, according to the EU Council Regulation no. 1085 dated 2006, establishing an Instrument for Pre-Accession Assistance (IPA) -– the Preamble, point 16 stipulates that: “Assistance should be provided on the basis of a comprehensive multi-annual strategy that reflects the priorities of the Stabilisation and Association Process, as well as the strategic priorities of the pre-accession process”. This is reinforced in Title 1, article 6 Planning of assistance – “For countries listed in Annex I, assistance shall be based in particular on the Accession Partnerships. Assistance shall cover the priorities and overall strategy resulting from a regular analysis of the situation in each country and on which preparations for accession must concentrate …”. The mentioning of the strategic document for IPA reflects and resemble the provisions for EU Member States, that are included in the EU Regulation no. 1698 of the year 2005, that requires – specifically for rural development – that “each Member State should prepare its rural development national strategy and plan constituting the reference framework for the preparation of the rural development programmes…”.

1.2. Structure of the document The National Agricultural and Rural Development Strategy (NARDS) for the period 2007-2013 carries out in Chapter 2, an analysis of the situation of the range of responsibilities of the Ministry of Agriculture, Forestry and Water Economy. The strategy, however, does not set the strategy for all sub-sectors under MAFWE responsibility. By decision of the Strategic Planning Group, certain parts are not included because produced by other donors, namely:

- Forestry policy, already produced by FAO, and

- Water management because object of analysis and projects financed by the World Bank.

However the above are presented in summary form (background) and their implications with the IPARD co-financing are outlined. At the end of the chapter, the key factors hampering agricultural and rural development are identified.

Chapter 3 identifies the agricultural and rural development strategic objectives, sets the policy specific objectives and determines the measures to be implemented during the period.

Chapter 4 provides the implementation plans for the proposed measures.

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

7

2. CURRENT SITUATION

2.1. Role of Agriculture in the Economy 2.1.1. Geographic, Political and Administrative Background

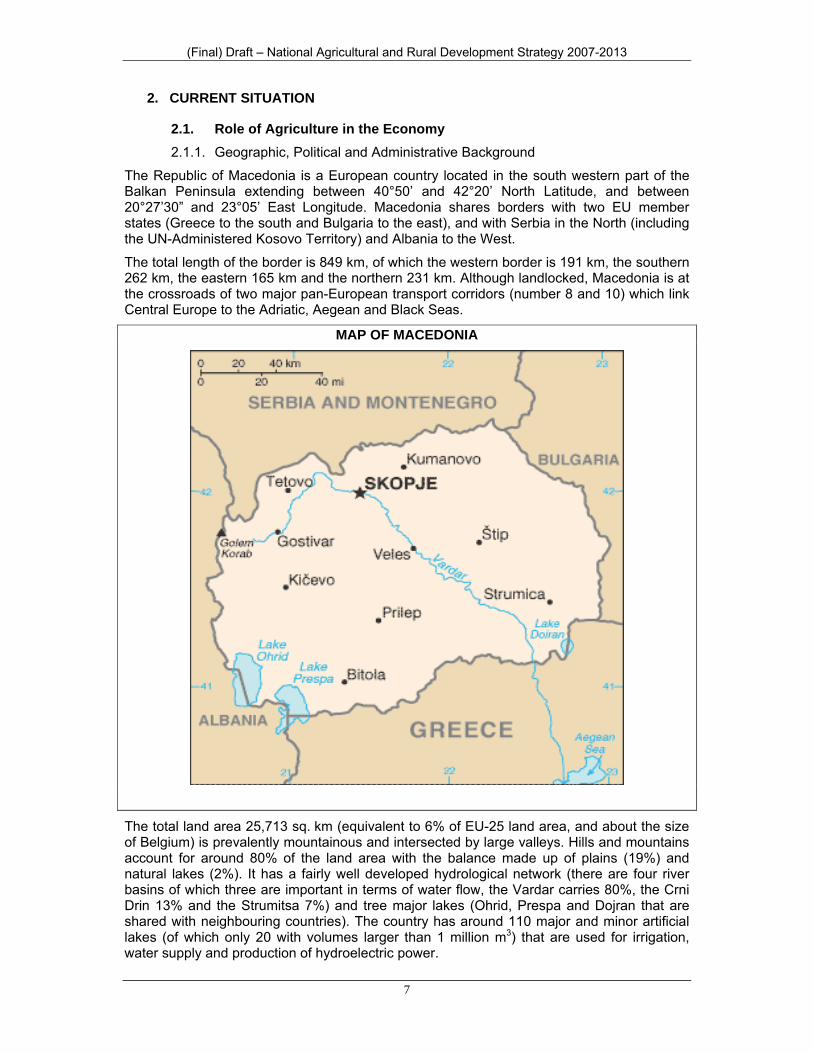

The Republic of Macedonia is a European country located in the south western part of the Balkan Peninsula extending between 40°50’ and 42°20’ North Latitude, and between 20°27’30” and 23°05’ East Longitude. Macedonia shares borders with two EU member states (Greece to the south and Bulgaria to the east), and with Serbia in the North (including the UN-Administered Kosovo Territory) and Albania to the West. The total length of the border is 849 km, of which the western border is 191 km, the southern 262 km, the eastern 165 km and the northern 231 km. Although landlocked, Macedonia is at the crossroads of two major pan-European transport corridors (number 8 and 10) which link Central Europe to the Adriatic, Aegean and Black Seas.

MAP OF MACEDONIA

The total land area 25,713 sq. km (equivalent to 6% of EU-25 land area, and about the size of Belgium) is prevalently mountainous and intersected by large valleys. Hills and mountains account for around 80% of the land area with the balance made up of plains (19%) and natural lakes (2%). It has a fairly well developed hydrological network (there are four river basins of which three are important in terms of water flow, the Vardar carries 80%, the Crni Drin 13% and the Strumitsa 7%) and tree major lakes (Ohrid, Prespa and Dojran that are shared with neighbouring countries). The country has around 110 major and minor artificial lakes (of which only 20 with volumes larger than 1 million m3) that are used for irrigation, water supply and production of hydroelectric power.

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

8

Soil structures in R. Macedonia are very heterogeneous (there are more than thirty types of soils) as consequence of the varied natural conditions for the soil creation (topography, climate, flora, geological formation and anthropogenic influence).

About half of the total land area is classified as agricultural (1.26 million ha), out of which 560,000 ha (44%) are cultivated land and 704,000 ha (56%) as permanent pastures. Upland or mountainous forests cover 37% of the country.

As a result of the geographic position and topography, Macedonia is at the crossroads of continental and Mediterranean climates which causes a wide variety of weather conditions. Eight climate-vegetation–soil regions have been identified with significantly heterogeneous climatic, vegetation and soil conditions1. The land used for agriculture production is located in the Sub-Mediterranean, Continental-Sub-Mediterranean and warm Continental areas with an altitude of 50-900 m. The summer-autumn seasons are dry and hot, while winters are snowy and with short but intense freezing spells. Higher precipitation is characteristic in the period from October to December and weaker from March to May. The spring and autumn rains are intensive and cause landslides, soil erosion and local floods. During the vegetation period, drought is rather common which points out that the water is limiting factor for intensive agriculture production. Late spring freezing and early autumn frosts are not infrequent.

According to latest census (2002), the total population is around two million divided into around 650 thousand households (with 3 persons per household). Population density is 79 inhabitants/sq. km which is low compared to the EU average of 115. Around 43% of population lives in rural areas. Urban population is mainly concentrated in the capital city Skopje (23.1%, with about 600 thousand inhabitants) and the rest is distributed in the other cities (Kumanovo 105, Bitola 88, Tetovo 72 and Veles 58 thousand respectively). Macedonia’s population has a multi-ethnic structure including Macedonians (64.18%), Albanians (25.17%), Turks (3.85%) and Roma (2.66%). The remaining balance of 4.14% is made up by other ethnic groups.

The Republic of Macedonia became independent in November 1991 and is a parliamentary Democracy with elections held every four years. It became member of the UN (1993), of the World Trade Organization (WTO) in 2003 and of CEFTA in 2006. Macedonia has signed in April 2001 the Stabilisation and Association Agreement with the EC and it’s member States which entered into force in April 2004. In addition, the country has signed ten Free Trade Agreements with different countries from the region. In December 2005 the European Council granted the Republic of Macedonia the status of candidate country for membership to the EU. As regards the possible opening of accession negotiations, the Commission considered that these could be opened once the country has reached a sufficient degree of compliance with the membership criteria.

According to the EU Nomenclature of Statistical Territorial Units (NUTS) Macedonia as a country is classified in the NUTS I and II, and it is divided into 8 Statistical Regions (corresponding to EU Classification NUTS III), and into 34 groups of Municipalities (equivalent to districts - corresponding to EU classification NUTS IV) and into 84 Municipalities and the city of Skopje (corresponding to EU classification NUTS IV)2.

2.1.2. Macroeconomic Framework

The Gross Domestic Product (GDP) of the Republic of Macedonia has grown in the 2000-2005 period, notwithstanding a drop in 2001 due to political instability. In 2005, the GDP stood at €4.46 billion, or around one percent of the EU-25 GDP. Per capita GDP stands at around 38% of the EU-25. Low standard of living, increasing poverty, high unemployment

1 Source: Gj. Filipovski, R.Rizovski,P.Ristevski 1996: Characteristics of the climate-vegetation-soil zones (regions) in Republic of Macedonia. MANU (Macedonian Academy of Sciences and Arts), Skopje) 2 Law on Territorial Organisation of Local Self Governments (RM OG 55/2004 and 12/2005)

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

9

rate (at around 36% of the workforce in 2005) and a relatively low economic growth rate remain central economic issues.

Since 2002, macroeconomic stability has been ensured by conservative fiscal and monetary policies and by the gradual liberalisation of international trade (decrease in average tariff rates) which maintained a low level of inflation (less than one percent in 2005) as well as a stable the nominal exchange rate of the currency. Foreign Direct Investment was at around two percent of GDP in recent years, quite low in general.

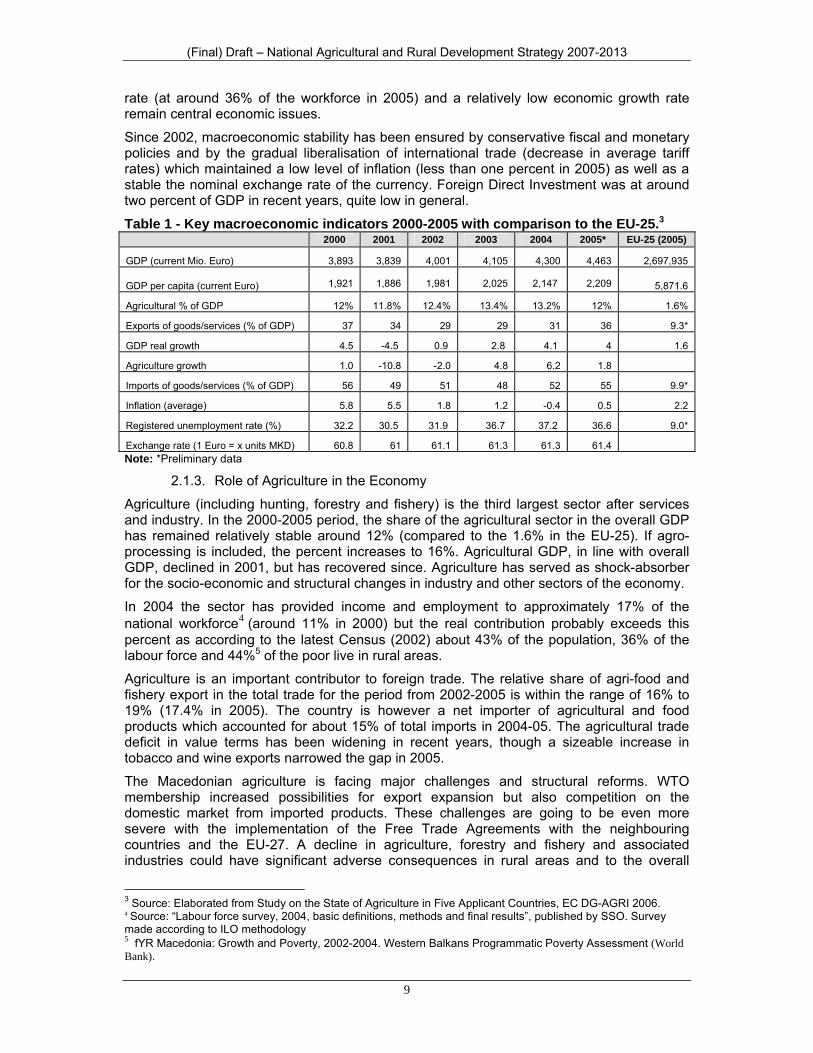

Table 1 - Key macroeconomic indicators 2000-2005 with comparison to the EU-25.3 2000 2001 2002 2003 2004 2005* EU-25 (2005)

GDP (current Mio. Euro) 3,893 3,839 4,001 4,105 4,300 4,463 2,697,935

GDP per capita (current Euro) 1,921 1,886 1,981 2,025 2,147 2,209 5,871.6

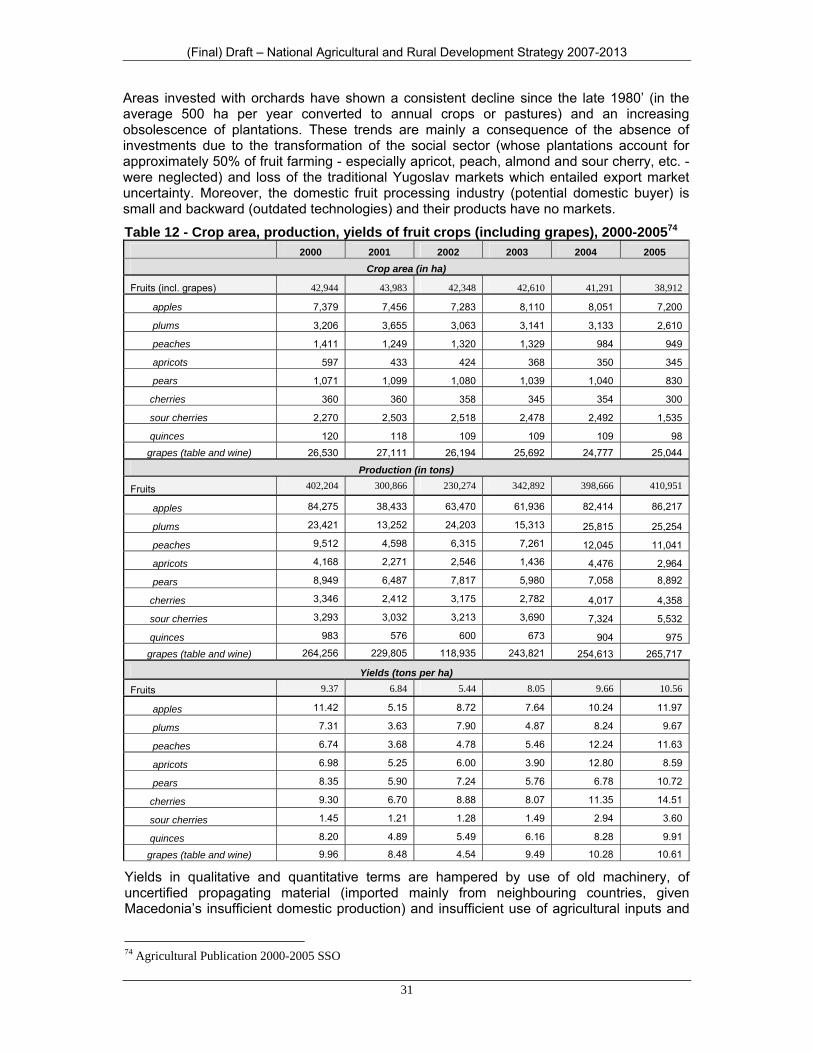

Agricultural % of GDP 12% 11.8% 12.4% 13.4% 13.2% 12% 1.6%

Exports of goods/services (% of GDP) 37 34 29 29 31 36 9.3*

GDP real growth 4.5 -4.5 0.9 2.8 4.1 4 1.6

Agriculture growth 1.0 -10.8 -2.0 4.8 6.2 1.8

Imports of goods/services (% of GDP) 56 49 51 48 52 55 9.9*

Inflation (average) 5.8 5.5 1.8 1.2 -0.4 0.5 2.2

Registered unemployment rate (%) 32.2 30.5 31.9 36.7 37.2 36.6 9.0*

Exchange rate (1 Euro = x units MKD) 60.8 61 61.1 61.3 61.3 61.4 Note: *Preliminary data

2.1.3. Role of Agriculture in the Economy

Agriculture (including hunting, forestry and fishery) is the third largest sector after services and industry. In the 2000-2005 period, the share of the agricultural sector in the overall GDP has remained relatively stable around 12% (compared to the 1.6% in the EU-25). If agro-processing is included, the percent increases to 16%. Agricultural GDP, in line with overall GDP, declined in 2001, but has recovered since. Agriculture has served as shock-absorber for the socio-economic and structural changes in industry and other sectors of the economy.

In 2004 the sector has provided income and employment to approximately 17% of the national workforce4 (around 11% in 2000) but the real contribution probably exceeds this percent as according to the latest Census (2002) about 43% of the population, 36% of the labour force and 44%5 of the poor live in rural areas.

Agriculture is an important contributor to foreign trade. The relative share of agri-food and fishery export in the total trade for the period from 2002-2005 is within the range of 16% to 19% (17.4% in 2005). The country is however a net importer of agricultural and food products which accounted for about 15% of total imports in 2004-05. The agricultural trade deficit in value terms has been widening in recent years, though a sizeable increase in tobacco and wine exports narrowed the gap in 2005.

The Macedonian agriculture is facing major challenges and structural reforms. WTO membership increased possibilities for export expansion but also competition on the domestic market from imported products. These challenges are going to be even more severe with the implementation of the Free Trade Agreements with the neighbouring countries and the EU-27. A decline in agriculture, forestry and fishery and associated industries could have significant adverse consequences in rural areas and to the overall

3 Source: Elaborated from Study on the State of Agriculture in Five Applicant Countries, EC DG-AGRI 2006. 4 Source: “Labour force survey, 2004, basic definitions, methods and final results”, published by SSO. Survey made according to ILO methodology 5 fYR Macedonia: Growth and Poverty, 2002-2004. Western Balkans Programmatic Poverty Assessment (World Bank).

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

10

economic and social stability of the country. Strengthening the competitiveness of the Macedonian agribusiness is the focal point for its survival. This must be supported by the reform of the public institutions and by the implementation of well targeted support policies and rural development measures.

2.2. Rural Sector Analysis 2.2.1. Characterisation of Rural Areas.

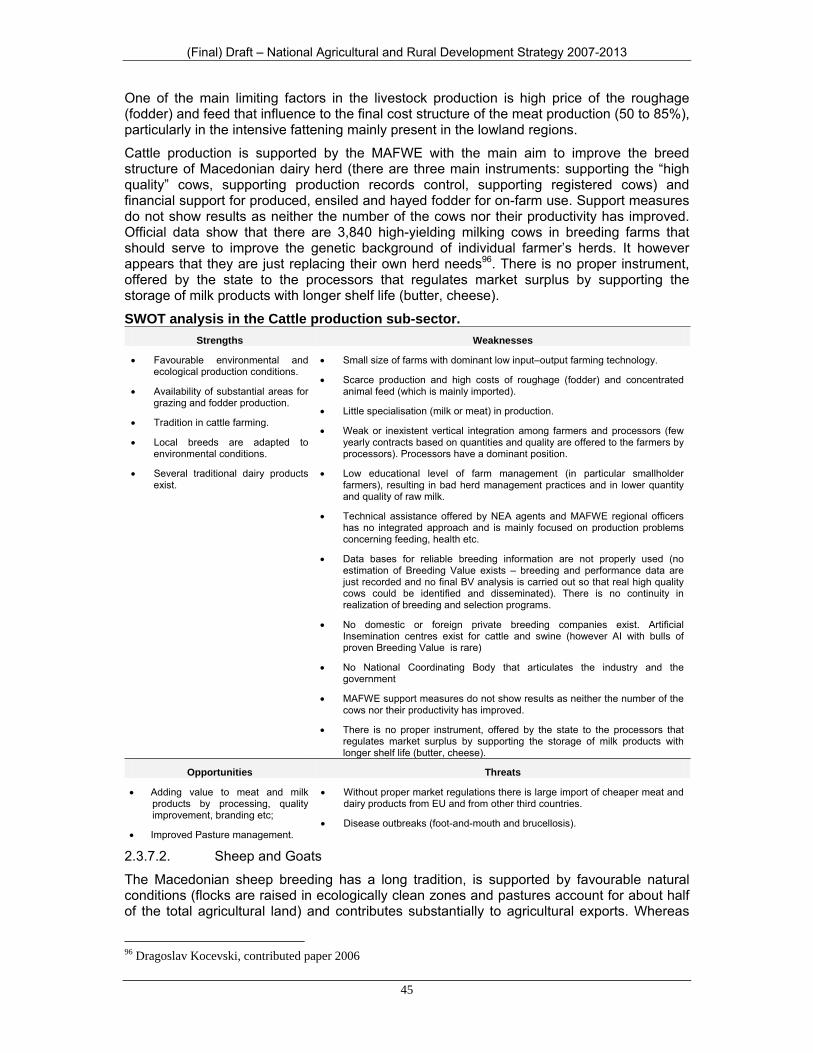

Available data necessary for the socio-economic characterisation of rural areas in Macedonia is limited and the picture is thus incomplete.

There is no clear definition of rural areas as well as well as classification based on the population density in the Republic of Macedonia. In 2002 the UNDP, the SSO and the Ministry of local self government carried out a socio-economic mapping of the disparities among Municipalities in Macedonia which delineated six zones based on population concentration on the territory of the country: a weak concentration zone (up to 50 inhabitants per sq. km), medium concentration zone (51-100 inhabitants per sq. km), overpopulated zone (101-150 inhabitants per sq. km), significantly overpopulated zone (151-500 inhabitants per sq. km), very significantly overpopulated zone (501 – 1,000 inhabitants per sq. km), and massively overpopulated zone (more than 1,000 inhabitants per sq. km). In 2002, almost half (61) of the municipalities belonged to the weak concentration zone, 26 municipalities had medium concentration, 7 were overpopulated, 19 were significantly overpopulated, 4 very significantly overpopulated, and 6 municipalities had more than 1,000 inhabitants per sq. km6.

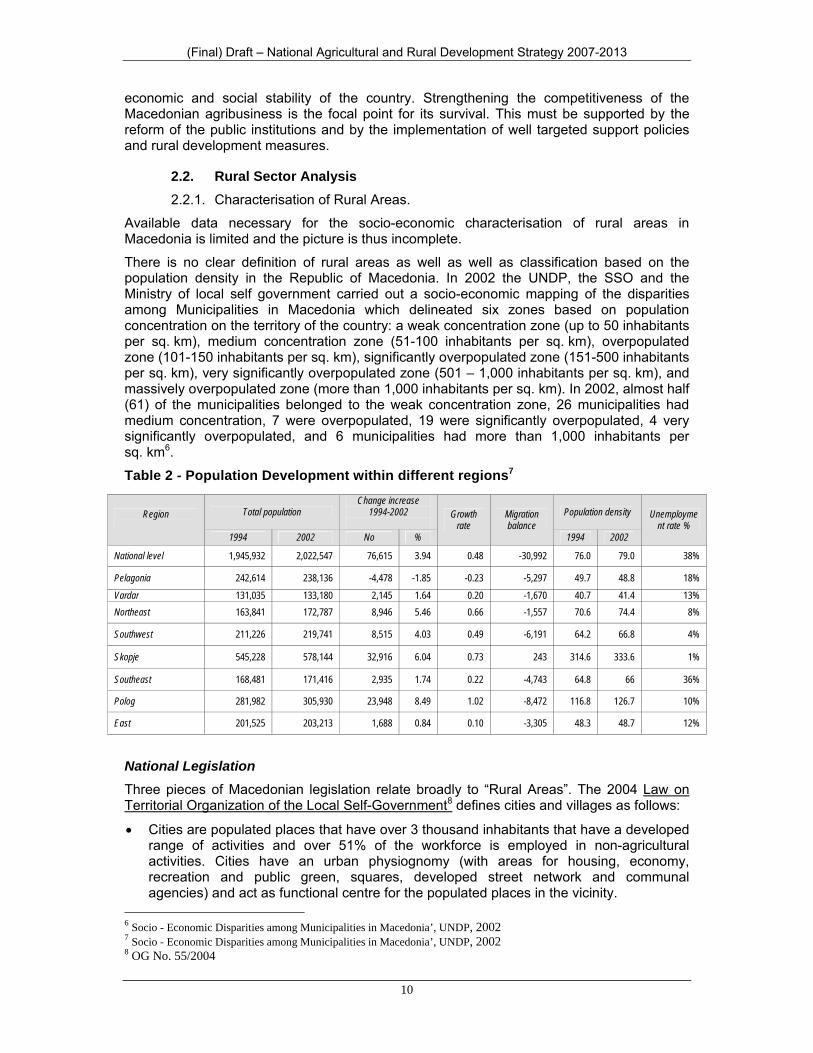

Table 2 - Population Development within different regions7

National Legislation Three pieces of Macedonian legislation relate broadly to “Rural Areas”. The 2004 Law on Territorial Organization of the Local Self-Government8 defines cities and villages as follows:

• Cities are populated places that have over 3 thousand inhabitants that have a developed range of activities and over 51% of the workforce is employed in non-agricultural activities. Cities have an urban physiognomy (with areas for housing, economy, recreation and public green, squares, developed street network and communal agencies) and act as functional centre for the populated places in the vicinity.

6 Socio - Economic Disparities among Municipalities in Macedonia’, UNDP, 2002 7 Socio - Economic Disparities among Municipalities in Macedonia’, UNDP, 2002 8 OG No. 55/2004

Region

Total population Change increase

1994-2002

Growth rate

Migration balance

Population density Unemployment rate %

1994 2002 No % 1994 2002

National level 1,945,932 2,022,547 76,615 3.94 0.48 -30,992 76.0 79.0 38%

Pelagonia 242,614 238,136 -4,478 -1.85 -0.23 -5,297 49.7 48.8 18%

Vardar 131,035 133,180 2,145 1.64 0.20 -1,670 40.7 41.4 13% Northeast 163,841 172,787 8,946 5.46 0.66 -1,557 70.6 74.4 8%

Southwest 211,226 219,741 8,515 4.03 0.49 -6,191 64.2 66.8 4%

Skopje 545,228 578,144 32,916 6.04 0.73 243 314.6 333.6 1%

Southeast 168,481 171,416 2,935 1.74 0.22 -4,743 64.8 66 36%

Polog 281,982 305,930 23,948 8.49 1.02 -8,472 116.8 126.7 10%

East 201,525 203,213 1,688 0.84 0.10 -3,305 48.3 48.7 12%

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

11

• Villages are defined as mono-functional populated areas, in which one business activity is predominant, whereas the ground has agricultural physiognomy and function.

According to the law, the principal difference between villages and towns lays in the main activity orientation of their communities (agriculture in the case of villages and secondary and tertiary sectors in the case of towns). There are also other differences, such as the size of the community, level of structures, environmental surroundings, etc.

Macedonia has a total of 84 Municipalities (33 with seat in a city, 49 with seat in a village, and 10 in the capital city of Skopje), and 1,715 villages covering 86.7% of the national territory and hosting 43% of the total population (2002 census).

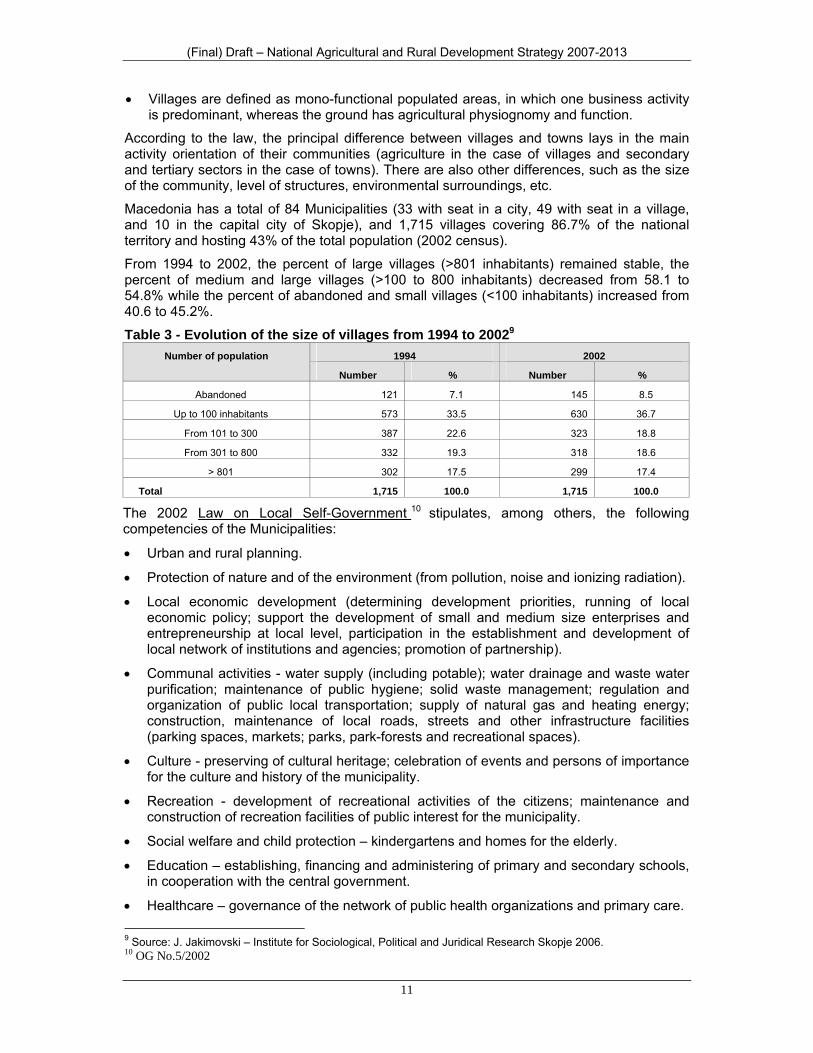

From 1994 to 2002, the percent of large villages (>801 inhabitants) remained stable, the percent of medium and large villages (>100 to 800 inhabitants) decreased from 58.1 to 54.8% while the percent of abandoned and small villages (<100 inhabitants) increased from 40.6 to 45.2%.

Table 3 - Evolution of the size of villages from 1994 to 20029 Number of population 1994 2002

Number % Number %

Abandoned 121 7.1 145 8.5

Up to 100 inhabitants 573 33.5 630 36.7

From 101 to 300 387 22.6 323 18.8

From 301 to 800 332 19.3 318 18.6

> 801 302 17.5 299 17.4

Total 1,715 100.0 1,715 100.0

The 2002 Law on Local Self-Government 10 stipulates, among others, the following competencies of the Municipalities:

• Urban and rural planning.

• Protection of nature and of the environment (from pollution, noise and ionizing radiation).

• Local economic development (determining development priorities, running of local economic policy; support the development of small and medium size enterprises and entrepreneurship at local level, participation in the establishment and development of local network of institutions and agencies; promotion of partnership).

• Communal activities - water supply (including potable); water drainage and waste water purification; maintenance of public hygiene; solid waste management; regulation and organization of public local transportation; supply of natural gas and heating energy; construction, maintenance of local roads, streets and other infrastructure facilities (parking spaces, markets; parks, park-forests and recreational spaces).

• Culture - preserving of cultural heritage; celebration of events and persons of importance for the culture and history of the municipality.

• Recreation - development of recreational activities of the citizens; maintenance and construction of recreation facilities of public interest for the municipality.

• Social welfare and child protection – kindergartens and homes for the elderly.

• Education – establishing, financing and administering of primary and secondary schools, in cooperation with the central government.

• Healthcare – governance of the network of public health organizations and primary care. 9 Source: J. Jakimovski – Institute for Sociological, Political and Juridical Research Skopje 2006. 10 OG No.5/2002

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

12

Regarding less favourable areas (LFA), the 1994 Law for stimulation of the Development of Economically Insufficiently Developed Regions11 provides determination criteria for three types of specific regions and for the rural centres as follows:

• Hilly-mountainous regions are the inhabited areas located at more than 800 meters above sea level that have distinct mountainous terrain configuration or, exceptionally, inhabited areas at more than 600 meters above the sea level, if they are with distinguished mountainous characteristics.

• Border regions are the inhabited areas in the regions that are up to 5 km from the state borders, including the inhabited areas that are farther than 5 km from the borderline, but are the first inhabited areas near the border. The inhabited areas with developed economic activity and built infrastructure do not have the status of border regions.

• Extremely undeveloped inhabited area have a low level of economic activity, are more than 10 km away from the city centre, without road access and basic infrastructure, high migration and small population density.

• Rural centres are the larger inhabited areas located in the centre of the economically underdeveloped regions where there are conditions for performing diversified economic activities which makes them "centre" of the development in that region. Municipalities may be rural centres, except for the ones with characteristics of cities.

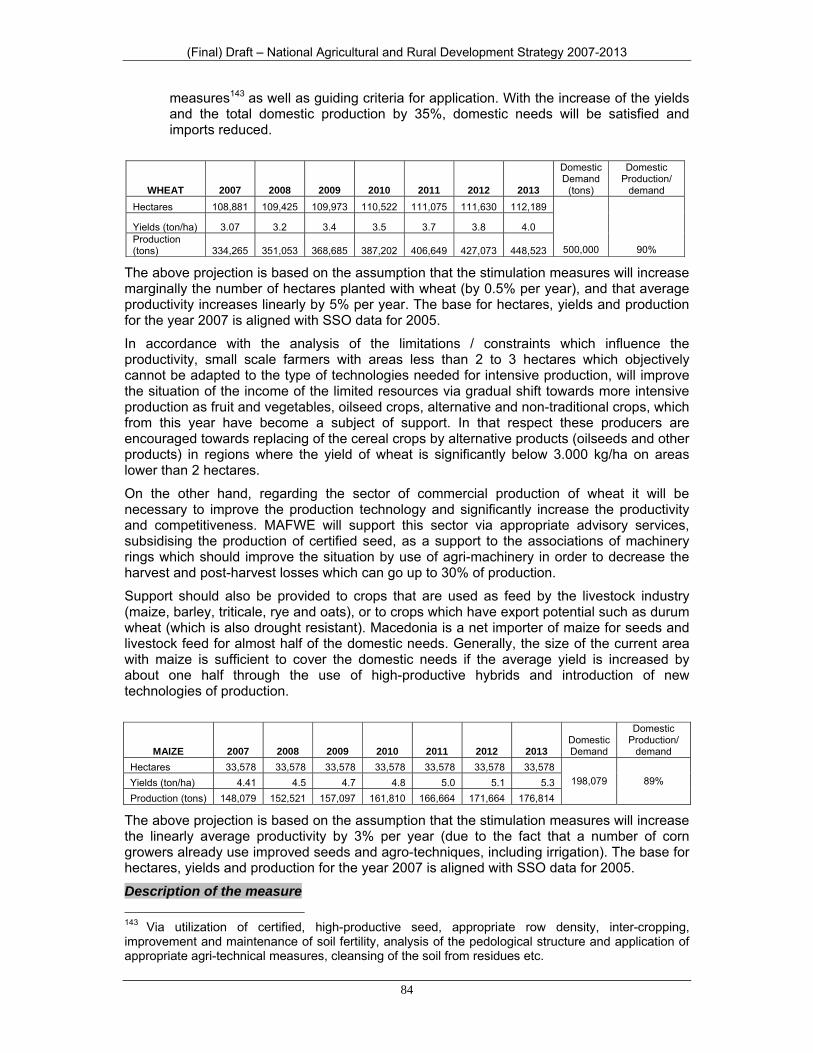

The law further determines the:

• Institutional set-up (it establishes the Bureau for Economically Underdeveloped Regions, under the Ministry of Local Self Government).

• National budget funding (up to one percent of the country’s GDP). At its peak in 2002, the Agency operated with annual budget of approximately € 9 million while in 2006 the budget was down to €3.3 million, far below the real needs, and

• Eligible measures (grants for economic and non-economic infrastructure projects, partial interest refund on domestic and foreign loans, investment support for economic activities/projects, employment creation, training and pensions, disability and health insurances, and for research related to economically underdeveloped areas).

According to the 2006 Decision for Determining the Economic Underdeveloped Areas12, 64% of the total Macedonian villages are eligible to be supported under the above Law. The total number of Rural Centres is 113 (out of which 20 have the status of Specific Regions also). The total number of villages with status of Specific Regions is 1,005 delineated as follows:

• 51% are hilly-mountainous villages, mainly spread in the South-West region, followed by Polog and Pelagonia, North-East and East and the smallest number of them is located in the Vardar and South-West regions and Skopje.

• 33% are extremely undeveloped villages, largely located in the East, Vardar and Pelagonia regions and in the North-East region.

• 15% are border villages located along the border lines.

Under the current decision, around 69% of the national territory and around 17% of the total population are covered. However, the criteria for determination of economically undeveloped regions are questionable, as some Macedonian villages with high migration rate, insufficient public utilities and economic infrastructure haven’t acquired the status of extremely undeveloped villages and vice versa.

11 OG No. 2/94 as amended by OG No. 39/99 12 OG No. 17/2006 and 54/2006

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

13

2.2.2. Rural Demography and Education.

According to latest census (2002), the total population of the Republic of Macedonia is around two million. Population density is 79 inhabitants/sq. km which is low (68%) compared to the EU average of 115 inhabitants/sq. km.

Around 43%13 of the population lives in rural areas distributed over 86.7% of the total land area. Urban population is mainly concentrated in the capital city Skopje (23.1%) and the rest is distributed in the other cities.

The average age of the population in Macedonia is approximately 33 years, and almost 68% of the population is in working age (between 15 and 64 years). The net rate of population growth has been roughly estimated at 0.4% for 2004, while the birth rate is almost twice as big as the mortality rate. Still, Macedonia has an unfavourable net average migration rate 5-1.45/1,000 inhabitants°.

From 1981 to 2002, the number of young people (0 to 19 years) declined from 41 to 32.2%, while population aged 65 and above increased from 8 to 32.2%. Unsatisfactory rural age structure is particularly found in the Pelagonia (18.8%), East (15.5), Vardar (12.9) and North-East (12.7%) regions14.

In Macedonia 96% of the total population of over 10 years is literate. There is gender equality in the literate population, but around two thirds of the illiterate population is female15.

If the overall literacy situation is good, there appears to be a difference between urban and rural areas in the educational structure. According to the 1994 census, a sizeable share (37.9%) of village and farming population above the age of 15 have insufficient or total lack of primary education: 10.5% are illiterate and 27.4% have not completed primary education. The low rate of education in the rural areas is due to the: “moving out of young and capable population for work, … the lack or small number of education facilities, not sufficient care for improvement of the school education of the young population, isolation of the undeveloped villages, etc”16.

The educational problem is obvious among the unemployed, since only 8% of them have higher or university education, the majority (54%) has secondary education, and the remaining 38% are unskilled. Young population (age 15-25) participate with 23% of the unemployed, however this percentage amounts up to 82% among the young working capable population17.

Education is a driving force of the economic and social development. It is also a factor for innovative readiness. The educational system certainly plays an important role in the young people’s ability to value the local product and the local tradition. The quality of education and life-long learning could reduce the disparities between urban and rural areas which are striking in Macedonia.

Small holder farmers (especially in backward areas) have the weakest educational and professional level among agricultural producers. In the country, apart from formal secondary and university education, there is a lack of additional (non-formal) education and training for farmers. Existing media programs (radio and television) relating to agriculture are limited in duration and are very general in scope. There are no specialised agricultural magazines. The Macedonian agro-web (all official national web pages supplying useful information for agricultural stakeholders) is very poor and offers obsolete information18. There are also a

13 According to the last census from 1994, rural population in the country was 40.2 %. 14 Contributed paper - J. Jakimovski (Institute for Sociological Political and Juridical Research , Skopje, Macedonia) 15 Source: State Statistical Office, 2002 Population Census, Book 13 16 Rural Social Structure, J. Jakimovski 2004. 17 Statistical Yearbook of the Republic of Macedonia, 2005 18 Agricultural Knowledge and information system in Macedonia, Master thesis, Rusev Trajce, 2005.

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

14

limited number of programs teaching about local culture and history, especially about the local public resources which can encourage and improve the quality of life.19

2.2.3. Employment (including SMEs, Crafts and Rural Tourism).

According to the latest statistics20, out of the total active population (885,609) of the country, 36.1% are unemployed (of which 82% are long-term unemployed). This does not compare favourably with the EU-25 average of 8.6% in 2005. Unemployment is worse in urban (68%) than in rural areas (32%)21 but the gap is narrowing. Furthermore, 44%22 of the poor live in rural areas.

Available statistics do not provide adequate details on rural employment by branches. Indeed the majority of rural population is engaged in the agricultural sector (mainly subsistence/household farming) and other activities, if any. Agricultural wages tend to be significantly lower than in other sectors, and almost half of all agricultural workers are unpaid family workers. Agricultural employment is also highly seasonal. The 2005 WB Poverty Assessment report concludes that agricultural employment serves as a social buffer, helping alleviate poverty and unemployment particularly in times of high off-farm unemployment.

A comparison of exclusively agricultural households, mixed households (those engaged in agriculture on private holdings and where at least one household member is employed outside agriculture), and household with no agricultural holdings, shows that mixed households have the highest incomes, followed by agricultural households. Non-agricultural rural households are worst off23. Studies have shown a trend towards diversification into non-farm employment as a result of economic need (and, to a lesser extent, attitudes towards farming), and confirm a positive correlation between income and the number of non-farm activities households engage in. Full-time farms earn 88% of their net income from farming (the remainder is largely unearned income such as pensions). Part-time farms earn around 50% of their income from wage or self-employment, with the remainder from farming and unearned income24.

Small and Medium Enterprises (SMEs) The law on Trade Companies (2004) sets the criteria for the determination of micro, small, medium and large enterprises. In terms of number of employees, the criteria are compatible with EU ones, but are different with regards to turnover and balance sheet values25. The Ministry of Economy is working to eliminate the discrepancies.

The number of private sector enterprises is increasing over time which shows that they play an increasingly important role in relation to the contribution to GDP, employment, export, etc.

The total number of registered enterprises is approximately 180,000, however in 2005 only 1/5 were active (44,424) and of these the great majority (98.8%) are SMEs.

Table 4 - Number of Active SMEs (1991 and 2000-2005)26 1991 2000 2001 2002 2003 2004 2005

19 MAFWE- Annual Agricultural Report 2005. 20 Survey for labour force N; 2.1.6.26 of 9 Oct 2006 SSO 21 Unemployment report from 31 August 2006 published 18 Sept 2006 from the Agency for Employment of RM 22 Growth and Poverty, 2002-2004. Western Balkans Programmatic Poverty Assessment (World Bank). 23 Source: State Statistical Office mentioned in WB document Agriculture and EU Accession: Achieving FYR Macedonia’s Agricultural Potential (November, 2006). 24 The main non-farm income-creating activities are trade, transport and car repair (accounting for 17.5% of all non-farm activities), followed by restaurant work, construction, food processing, tailoring, and tourism (Buchenrieder, G., J. Mollers and F. Heidhues. 2002). This analysis is based on survey data comprising households in rural areas that are employed full time in agriculture and households which have diversified or shifted away from agriculture as a source of income. 25 Source: Central Registry MoE 26 Source: Central Registry MoE

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

15

SMEs 9,703* 33,151 34,991 36,963 39,096 41,517 44,300 All 10,270 33,269 35,110 37,074 39,199 41,590 44,424

The number of active enterprises translates into an SME density of 22 per 1,000 inhabitants. This compares favourably with the SEE region (23), but unfavourably with the EU-15 average (45). SMEs are also important in terms of employment creation. In 200527 their share in total employment stood at 80% while contributing for only 50% of the GDP. The sectors in which most SMEs are operating are also the biggest contributors to employment (65%).

Three sectors alone comprise over 75% of the total active enterprises (and therefore also of SMEs). The wholesale and retail trade sector accounts for 48.7%, manufacturing for 16.4%, transport, storage and communication for 10.13%. Agricultural enterprises account for 2% of the total.

Table 5 - Active Enterprises by Sector (2005)28

Sector Small Medium and

Large Total Agriculture, hunting and forestry 934 32 966Fishing 28 0 28Mining and quarrying 86 7 93Manufacturing 7,069 222 7,291Electricity, gas and water supply 57 22 79Construction 3,061 52 3,113Wholesale and retail trade 21,511 121 21,632Hotels and restaurants 1,937 19 1,956Transport, storage and communication 4,468 32 4,500Financial intermediation 34 2 36Real estate, renting and business activities 2,150 18 2,168Public administration and defence 2 1 3Education 294 0 294Health and social work 1,387 3 1,390Social and personal services 859 16 875Total 43,877 547 44,424

Craftsmanship In 2001, 7,500 crafts were registered according to the Law on Craftsmanship. The annual growth rate of this sector was 1.4% within the period 1995-200129. More recent statistics are unavailable, as craftsmanship according to the new nomenclature, is not separated from the industry. Recent statistics30 show that sole proprietors in 2004 were 19,736 entities, but on the other hand self-employed are 53,252 persons. The need for joint evidence of all micro-businesses in the country is evident. The register on trade companies and register of farmers should be merged into one register of micro-businesses. Recent legislative changes to the Law on Craftsmanship and the Law on Trade Companies have greatly simplified the conditions for start-ups. For registration within the Craftsman chambers, it is necessary to have a crafts diploma and office/work facilities. No deposit is required for start-up. Moreover, there is a tax free period of three years after the establishment and thereafter a lump sum tax of progressive rates 15-18-24% applies.

27 EBRD – Annual Country Report –FYR Macedonia - 2005 28 Source: Central Registry (2005) 29 Study on the craftsmanship – Institute of Economics-Skopje for the Ministry of Economy, 2002 30 Statistical Yearbook of the Republic of Macedonia, 2005

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

16

Crafts are organized in 11 regional Crafts Chambers, the most active being those located in Skopje, Strumica, Prilep, Bitola, Tetovo and Kumanovo. In 2005 a National Crafts Chamber was registered in Gevgelija, however, it is not yet operational31

According to the Law on Vocational Education (2005) crafts licence is provided by Vocational Educational Training (VET) Centre for final examination of the craftsmen (so called master’s exam).

Craftsmen licences will be provided by the craftsmen chambers. However the education and practice will be joined through education in vocational schools and practice in certified craftsmen shops. Certification of the craftsmen shops for educational purposes will be provided by the craftsmen chambers upon passed master’s exam that includes pedagogy, theory of the activity and business economics. Also, after three years craftsmen education, students might continue their studies at the University level at so called higher specialist studies.

The average number of businesses per thousand inhabitants in rural municipalities in the country is 40.43 compared to 78.89 in urban municipalities (national average is 86.8). In 2005, according to the State Statistical Office32, 10% of total number of business entities’ headquarters was located in rural municipalities and 2.9% of the total number of registered enterprises is in the area of agriculture, hunting, forestry and fishery (5,024)33 – of which 21.4% are based in the rural municipalities.

Generally, rural areas are not attractive to businesses for several reasons: property right problems, lack of concentration of population, poorer educational achievements, lesser flexibility of the potential workforce, and distances from potential markets (for both inputs and outputs), all putting businesses in rural areas at a cost disadvantage. Poorly developed and diversified economic infrastructure and the consequent lack of quality jobs are common features of rural areas in Macedonia. These are also the main causes of development lag typical of these areas.

Rural Tourism Rural tourism in all its forms (agri-tourism, eco-tourism, cultural and ethno-village, mind/body tourism, wilderness sports, eno-gastronomic, hunting, etc. and, more in general the tourism industry in Macedonia) is small and well below the potential.

After halving in 2001 compared to the previous year, the annual number of tourists has been growing gradually but slowly. In the 2000-2005 period, Macedonia’s official statistics show that the average number of tourists (both inbound and domestic) is around 470 thousand per year34, of which only one third (around 150 thousand/year) is from foreign countries. Of these, 50% is from the neighbouring countries. The average number of nights spent per tourist is 4, but foreign tourists spent about half of this figure. During the period, the leading tourist destination is Ohrid, which absorbs approximately 60% of Macedonia's tourist visitors, followed by Skopje (20%), alpine areas (9%) and SPAs (4%).

Official Statistics do not provide data focused specifically on rural tourism in all its forms. According to a study carried out in 200235, the main reasons for coming to Macedonia are business trips, mainly in Skopje and seminars mostly in Ohrid; vacation and recreation; and 31 Statistical Yearbook of the Republic of Macedonia, 2005 31 Executive director at the Skopje Craftsman Chamber , Ms. Snezana Denkovska 32 State Statistical Office, Statistical report 6.1.1.02 33 The statistical report 6.1.1.02 34 SSO 2000 to 2005 annual reports. 35 Ministry of the Economy - Master Plan for tourism in Republic of Macedonia, Louis Berger S.A, April 2003. The study is being currently updated and reviewed.

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

17

cultural tourism mostly as a part of package offer along the visit to neighbouring countries. Foreign tourists arrive mainly by road or regular air flight. In 2002, foreign tourists spent an average of €72.5 per day, while average daily expenditure on rural/eco tourism was € 26.

The competent government authority for tourism is the Tourism Sector in the Ministry of Economy. Coordination between the Ministries involved in tourism related issues (MoE, MoEPP, MAFWE, MoC, MoT) is very weak and there is no national inter-sector body that monitors tourism development policies. The tourism activities are organised and supported by different organisations and associations, the most important one being the Chamber of Commerce and the Chamber of Tourism36 (Association of tourist agencies in Macedonia, Association of hotels in Macedonia, Tourism association of Skopje.

The National Development Plan (2007-2009) states that the development of tourism is regarded as an important development priority of Macedonia both because it offers numerous business opportunities and jobs, but also because it supports the country's objectives in the area of trade, export and investment. The NDP further states that rural or country tourism is often considered an indicator of good quality regional development and that Macedonia does have the potential for development of this tourism, because of the characteristic traditional architecture, favourable environment, diversity of sites to see, visit and do and the hospitality of people. According to the National Development Plan (2007-2009), the planned investment needs for rural tourism development for the three year period total € 3 million (or about 2.8% of the total planned investments).

Considering Macedonia’s diversity and quality of cultural/historical treasures and archaeological sites (over 4.200 archaeological sites, over 1.000 churches and monasteries and over 700 monuments of culture), of the environment/natural beauty (wealth of mountains, rivers and lakes, vast uninhabited stretches, unique flora and fauna) and diverse landscapes/attractions (authentic old villages, traditional houses, winter sport centres, mineral and termo-mineral springs, hunting sites, etc.), and varied traditions (traditional foods, wines, crafts, events, etc), it is a priority to promote the integrated development of a sustainable rural tourism in Macedonia, to be carried out in cooperation by all relevant Ministries and stakeholders (private sector, associations, etc).

2.2.4. Social Care Infrastructure.

Rural social care infrastructure (kindergartens, schools, public community centres – libraries, clubs) was developed in the past, but in the majority of cases is in serious disrepair and or abandoned.

Most of the population from rural areas, especially those living in high-mountainous villages, are lacking fundamental health services, including primary health services.

2.2.5. Technical Infrastructure.

Technical infrastructure in rural areas is far from satisfactory with the exception of electrical supply which is available to 99.75% of rural population (transmission and distribution network is fairly well developed and capacity of electric energy sources is 1,430 MW that largely satisfies domestic requirements).

In Macedonia, all municipal centres have public water supply systems, but water supply remains insufficient for the needs. The percent of the rural population with public water pipeline installation is 72.3 (compared to 87.7% of the total population), 18.7 have access to water under pressure from cisterns (compared to 8% of the total population), and 8.96% of the rural population lack water supply installation (4% for total population). The state of water supply in Macedonia, even though there has been considerable construction, is not yet satisfactory. The existing water supply capacities cannot supply sufficient quantities of high quality water, which is particularly noticeable in the highly populated areas of East

36 Master Plan for tourism in Republic of Macedonia, Louis Berger S.A, April 2003

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

18

Macedonia. Generally waterworks are poorly equipped and there is insufficient protection of the sources of hygiene.

Wastewater treatment plants have been built in Ohrid/Struga in Doyran and in Resen. Sewerage systems exist or are being completed in the cities and major settlements. The remaining settlements do not have any sewerage systems37. The share of rural population with a public sewage installation is low and is estimated at 17.7% (for total population it is 60.1%). Total rural population without any installation for sewage is 8.9% (total population 4%). Only 10% of rural population is covered by public municipal collection of solid waste (against 70% of total population).

The Macedonian road infrastructure (including the network of feeder roads) was fairly developed in the past, and contains 9,573 km of roads in a categorised road network (1995 data), of which 909 km are motorways, 3,058 km are regional roads and the remaining 5,606 km are local roads38. Of the latter around 50% are either soil based or unimproved at all and regular maintenance and extraordinary repair are a problem. Railroad transportation in Macedonia is poorly developed and includes network of 699 km of open railway lines, 226 km of rail yards and 102 km of industrial tracks.

Residents of many rural settlements, especially in mountain and remote villages, experience poor public transportation services (bus lines) to modern roads and thus to stores, schools, markets, etc. The telephone network (both fixed lines and GSM) covers the great majority of the territory; however access to information and communication technology is low in rural areas. Postal services have degraded in the recent years and small villages are often uncovered. National and local television, including cable and satellite, and radio are available throughout the country.

Municipal centres and larger villages generally have retail (green) market infrastructure working once per week. Access to market (for selling agricultural produce or for purchasing raw materials/ input supplies) is more time consuming and costly for people living in isolated villages.

2.2.6. Rural Development policies.

Rural Development in the EU policy meaning is new for the MAFWE and, more in general, for the Government of Macedonia. To date, several institutions are implementing in a non-coordinated fashion a range of public support programmes which can be broadly categorised under the heading of “rural development”. MAFWE has been running two small annual programs for agricultural investments and revitalisation of villages (amounting in average to €1.5 million per year, but which have been reduced, starting from 2004, to an average of €0.3 million per year). Similarly other sector-dedicated institutions conducted programs (SME’s by the Ministry of Economy, etc.). The economically underdeveloped areas are covered by the Bureau for Economically Underdeveloped Regions (under the Ministry of Local Self Government). However, these un-coordinated schemes are stand-alone, rather than integrated Programs.

In January 2004, a Department for Financial Support and Rural Development has been established within the MAFWE, which includes a Unit for Financial Support in Agriculture and a Unit for Rural Development, whose task is to plan, design and monitor rural development policies and measures.

At the end of 2005, MAFWE has been officially appointed by the Government39 to be the Managing Authority for Rural Development in Macedonia. In accordance with this Decision,

37 Country Study for Biodiversity of the Republic of Macedonia (First National Report) Skopje, July, 2003 Ministry of Environment and Physical Planning 38 Country Study for Biodiversity of the Republic of Macedonia (First National Report) Skopje, July, 2003 Ministry of Environment and Physical Planning 39 Decision of the Government of R. Macedonia, no.19-4070/1 of 18.11.2005 (OG of RM no. 5/2006),

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

19

MAFWE has been appointed to plan, monitor and assess the activities and programs, to coordinate the activities of the various institutions of the sector and to supervise the financial functions which apply to rural development. The managing institution shall be the partner responsible for the entire cooperation with EC in the area managing the agriculture and the rural development. The overall objective is to put in place systems of support for facilitating rural development measures according to EU measures and to build administrative systems capable to meet EU pre-accession IPARD funds.

In 2006, MAFWE introduced a separate budget programme of MKD 45 million (around € 0.73 million), to fund integrally and implement a pilot IPARD-like Rural Development programme. The programme was managed by the Department for Financial Support and Rural Development. Specific program goals are the following:

• Rural area development support in accordance with the existing programs for the target users to improve agriculture and rural areas competitiveness and sustainability.

• Establishment of necessary administrative systems in the framework of MAFWE to manage the EU pre-accession rural development funds.

The programme includes one measure “Investment in Agricultural Holdings” and three sub-measures:

• Purchasing of equipment and machinery for crop production • Purchasing of equipment and machinery for livestock production • Purchasing of equipment and machinery for calibration, sorting and packaging of fresh

agricultural products.

Eligible beneficiaries were physical and legal entities (registered farmers and agricultural enterprises).

2.3. Sector Analysis: Agriculture 2.3.1. Land Resources, Land Use and Main Agricultural Areas.

In 2004, the surface of Macedonia’s agricultural land40 amounted to 1.26 million ha or about 49% of the total land area, while forests covered an area of 947,653 ha or 37%.

Agricultural land includes 700,000 ha of pastures (or 55.6%) located mainly in the highlands, and 560,000 ha of cultivated land (or 44.2%) mainly concentrated in valleys. From the total cultivated land, 461,000 ha (82%) was arable land41 and gardens, 58,000 ha meadows (10%), 26,000 ha vineyards (5%) and 15,000 ha orchards (3%). Each year, one third of total arable land is estimated to be left fallow. Per capita arable land is 0.625 ha which is higher than the EU-25 average (0.35 ha).

Cultivated land shows a decreasing trend from 633,000 ha in 1999 to 560,000 ha in 2004, mainly due to land abandonment (rural-to-urban population migration) and urban/industrial developments which occur at the expense of agricultural lands.

2.3.2. Land Ownership, Farm Structure and Productivity.

Macedonia’s land is partly privately and partly state owned. Around 80% of cultivable lands (463,000 ha) is owned or leased by around 180 thousand private farms. The balance is made up of state owned lands which are rented to 136 agricultural enterprises42. The

40 Agricultural land includes cultivable and pasturelands. Cultivable land includes land for arable crops, orchards, vineyards and improved pastures. State Statistical Office, Statistical Yearbook 2005 41 Arable land includes land planted to annual crops (cereals, industrial, vegetable and fodder crops), nurseries and fallow land. 42 Privatized and not yet privatised former agro-kombinats and farm co-operatives. Agro-Kombinats are vertically integrated agri-businesses managed by the state, which have large land holdings and operate on state owned land on usufruct rights basis, while the state holds the effective property rights. AKs are diversified in primary production, input production, agro-food processing activities, commercial storage and marketing services. Very

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

20

majority of pasturelands is owned by the state and managed by the Public Enterprise for Pastures.

The 1996 Law on Transformation of Enterprises Managing Agricultural Land defines agricultural land as a public good or national treasure, and thus the majority of land is still state owned. The law initiated the privatisation process of public agricultural enterprises (not the land) and in 2003 about 95% of the agricultural enterprises were privatised, but the process is not completed yet43. State owned land is rented to agricultural enterprises without compensation for a limited period of time, or to individual farmers with compensation.

Effective use of agricultural land in Macedonia is hampered by parcelling and fragmentation stemming from previous limitations on usable areas and ownership44, inheritance customs, as well as a tradition of informal relations in the land market. The 1994 General Census registered around 178,000 private farms with average size of 2.5-2.8 ha fragmented into parcels of 0.3-0.5 ha. About 40% of the private farms are smaller household farms with less than 2 ha (also parcellised) that produce mainly for household subsistence and for selling surpluses to supplement other sources of income45.

The weak land market, which failed to contribute to farm consolidation, as well as the low economic growth and lack of social security, keeps feeding the process of fragmentation and diversification of production in small lots in order to offset market fluctuations and satisfy food needs.

Despite a significant fall in 2001 and 2002, between 1990 and 2004 agricultural production value grew by 6% (largely determined by the performance of the crop sub-sector which accounts for around 70% of agricultural GDP). Over the same period production from the farm sector grew by 30% while production from the enterprises sector fell by about 50%. The success of small individual farms is due to the transfer of effective land ownership rights (late 1980s/early 1990s) which became profit-oriented and introduced business strategies mainly focused on production diversification to reduce risks46.

However, in the long run, the existence of small and very fragmented farms, even if with medium intensity production levels, does not allow for a stronger modernization and mechanisation which results in lower competitiveness.

Since 2000, the gross agricultural output (GAO) has been increasing with net growth of 3.8%. Growth of agricultural GDP (or agricultural value-added) exceeded that of GAO, increasing by 29% between 2001 and 200447 which suggests rising agricultural productivity during this period. In the past few years (2002-2004) also the production index of agricultural enterprises has been rising slightly, as a result of privatization, organizational strengthening and the inception of market-oriented production strategies48.

Information is lacking concerning agricultural mechanisation, irrigated areas and use of fertilisers and agrochemicals for the smallholder farming sector. The only available data relates to agricultural enterprises, which from 2000 to 2005 show a reduction trend in the number of tractors, in irrigated area and in fertiliser and agrochemical use49.

often they were input suppliers and main buyers from the private farmers but indirectly through the Socially Owned Agriculture Cooperative, which have smaller land holdings and engage only in primary production 43 MAFWE- Annual Agricultural Report 2005. 44 Until 1984, the maximum amount of land allowed to be owned by a single farmer was 10 ha or 20 ha in hilly and mountainous regions. 45 MAFWE - 2004 Annual Agricultural Report: Agricultural Sector Complementary Information; Statistical Tables. 46 “The Influence of Economic Reform on Agricultural Production in Macedonia in the Transition Period” (M. Deleva, P. Ivanovski - unpublished paper presented at the Scientific Assembly of the Association of Agricultural Economists of RM, December 2005). 47 Agricultural GDP is defined as GAO minus intermediary consumption of variable inputs. 48 MAFWE 2005 Annual Agricultural Report. 49 Source: State Statistical Office, 2005

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

21

2.3.3. Agricultural Labour

During the 2000-2005 period, on the average 21% of the active labour force in Macedonia was employed in the agricultural sector (about four times more than in the EU-25). In 2005, the percentage was 19.5%, of which 93% on private farms and the remaining were employed by agricultural enterprises. In total approximately 100,000 people are engaged in agriculture (including enterprise employees and full-time farmers) and an additional 20,000 part-time farmers and significant seasonal employment (particularly in the fruit and vegetable sector) for which accurate data is very limited. More than half of the total engaged labour is employed in crop production with the remainder is in the livestock sector.

Total income from agricultural activities of all agricultural households and companies shows constant annual growth in the 1998-2004 period (in 2004, it is estimated at MKD 25,123 million)50. In the same year, the net salaries of labour involved in agriculture amounted to MKD 9,692 a month (approximately MKD 460 a day or about €7.5).

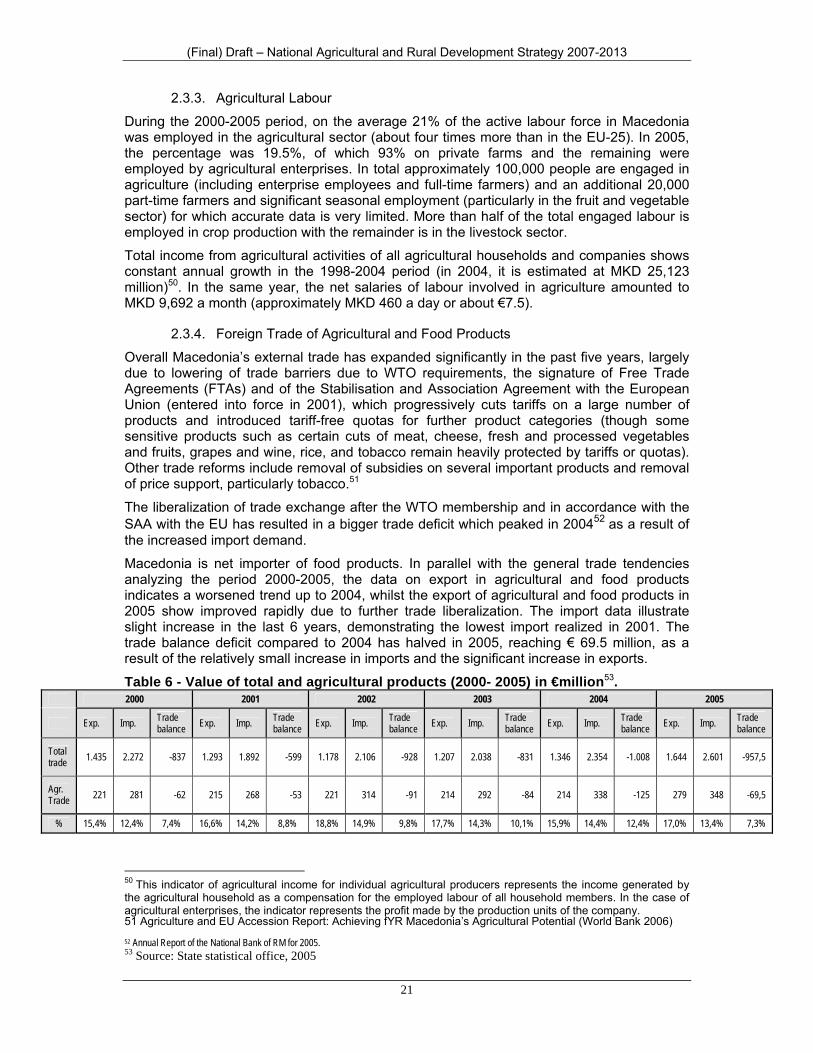

2.3.4. Foreign Trade of Agricultural and Food Products

Overall Macedonia’s external trade has expanded significantly in the past five years, largely due to lowering of trade barriers due to WTO requirements, the signature of Free Trade Agreements (FTAs) and of the Stabilisation and Association Agreement with the European Union (entered into force in 2001), which progressively cuts tariffs on a large number of products and introduced tariff-free quotas for further product categories (though some sensitive products such as certain cuts of meat, cheese, fresh and processed vegetables and fruits, grapes and wine, rice, and tobacco remain heavily protected by tariffs or quotas). Other trade reforms include removal of subsidies on several important products and removal of price support, particularly tobacco.51

The liberalization of trade exchange after the WTO membership and in accordance with the SAA with the EU has resulted in a bigger trade deficit which peaked in 200452 as a result of the increased import demand.

Macedonia is net importer of food products. In parallel with the general trade tendencies analyzing the period 2000-2005, the data on export in agricultural and food products indicates a worsened trend up to 2004, whilst the export of agricultural and food products in 2005 show improved rapidly due to further trade liberalization. The import data illustrate slight increase in the last 6 years, demonstrating the lowest import realized in 2001. The trade balance deficit compared to 2004 has halved in 2005, reaching € 69.5 million, as a result of the relatively small increase in imports and the significant increase in exports.

Table 6 - Value of total and agricultural products (2000- 2005) in €million53. 2000 2001 2002 2003 2004 2005

Exp. Imp. Trade balance Exp. Imp. Trade

balance Exp. Imp. Trade balance Exp. Imp. Trade

balance Exp. Imp. Trade balance Exp. Imp. Trade

balance

Total trade 1.435 2.272 -837 1.293 1.892 -599 1.178 2.106 -928 1.207 2.038 -831 1.346 2.354 -1.008 1.644 2.601 -957,5

Agr. Trade 221 281 -62 215 268 -53 221 314 -91 214 292 -84 214 338 -125 279 348 -69,5

% 15,4% 12,4% 7,4% 16,6% 14,2% 8,8% 18,8% 14,9% 9,8% 17,7% 14,3% 10,1% 15,9% 14,4% 12,4% 17,0% 13,4% 7,3%

50 This indicator of agricultural income for individual agricultural producers represents the income generated by the agricultural household as a compensation for the employed labour of all household members. In the case of agricultural enterprises, the indicator represents the profit made by the production units of the company. 51 Agriculture and EU Accession Report: Achieving fYR Macedonia’s Agricultural Potential (World Bank 2006) 52 Annual Report of the National Bank of RM for 2005. 53 Source: State statistical office, 2005

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

22

In comparison with 2004, the export of agro-food products in 2005 increased considerably by 30%. In the same way, the share of exported agro-food products showed an increase from 15.9% to 17% in 2005 in the total exports, which confirms the significance of agricultural products in the total trade in Macedonia. In comparison with total imports, imports of agricultural and food products in the last 6 years have been stable at approximately 14% of the total value of imports in Macedonia.

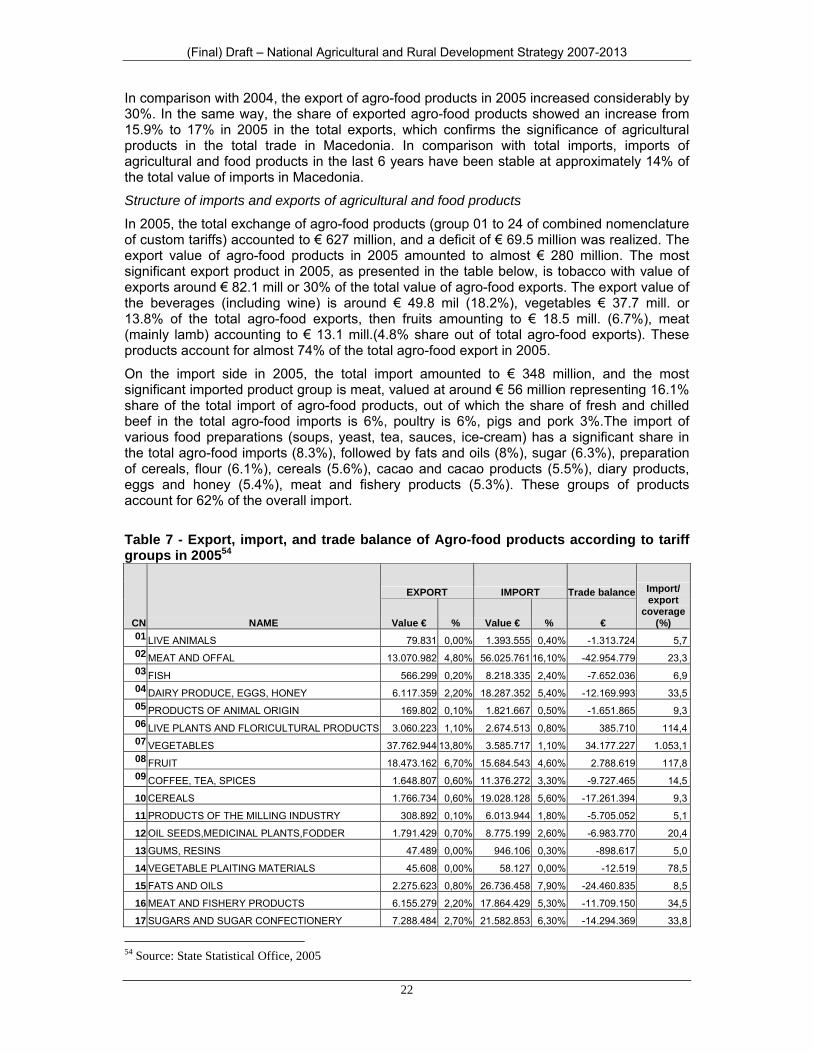

Structure of imports and exports of agricultural and food products

In 2005, the total exchange of agro-food products (group 01 to 24 of combined nomenclature of custom tariffs) accounted to € 627 million, and a deficit of € 69.5 million was realized. The export value of agro-food products in 2005 amounted to almost € 280 million. The most significant export product in 2005, as presented in the table below, is tobacco with value of exports around € 82.1 mill or 30% of the total value of agro-food exports. The export value of the beverages (including wine) is around € 49.8 mil (18.2%), vegetables € 37.7 mill. or 13.8% of the total agro-food exports, then fruits amounting to € 18.5 mill. (6.7%), meat (mainly lamb) accounting to € 13.1 mill.(4.8% share out of total agro-food exports). These products account for almost 74% of the total agro-food export in 2005.

On the import side in 2005, the total import amounted to € 348 million, and the most significant imported product group is meat, valued at around € 56 million representing 16.1% share of the total import of agro-food products, out of which the share of fresh and chilled beef in the total agro-food imports is 6%, poultry is 6%, pigs and pork 3%.The import of various food preparations (soups, yeast, tea, sauces, ice-cream) has a significant share in the total agro-food imports (8.3%), followed by fats and oils (8%), sugar (6.3%), preparation of cereals, flour (6.1%), cereals (5.6%), cacao and cacao products (5.5%), diary products, eggs and honey (5.4%), meat and fishery products (5.3%). These groups of products account for 62% of the overall import.

Table 7 - Export, import, and trade balance of Agro-food products according to tariff groups in 200554

CN NAME

EXPORT IMPORT Trade balance Import/ export

coverage (%) Value € % Value € % €

01 LIVE ANIMALS 79.831 0,00% 1.393.555 0,40% -1.313.724 5,7 02 MEAT AND OFFAL 13.070.982 4,80% 56.025.761 16,10% -42.954.779 23,3 03 FISH 566.299 0,20% 8.218.335 2,40% -7.652.036 6,9 04 DAIRY PRODUCE, EGGS, HONEY 6.117.359 2,20% 18.287.352 5,40% -12.169.993 33,5 05 PRODUCTS OF ANIMAL ORIGIN 169.802 0,10% 1.821.667 0,50% -1.651.865 9,3 06 LIVE PLANTS AND FLORICULTURAL PRODUCTS 3.060.223 1,10% 2.674.513 0,80% 385.710 114,4 07 VEGETABLES 37.762.944 13,80% 3.585.717 1,10% 34.177.227 1.053,1 08 FRUIT 18.473.162 6,70% 15.684.543 4,60% 2.788.619 117,8 09 COFFEE, TEA, SPICES 1.648.807 0,60% 11.376.272 3,30% -9.727.465 14,5

10 CEREALS 1.766.734 0,60% 19.028.128 5,60% -17.261.394 9,3

11 PRODUCTS OF THE MILLING INDUSTRY 308.892 0,10% 6.013.944 1,80% -5.705.052 5,1

12 OIL SEEDS,MEDICINAL PLANTS,FODDER 1.791.429 0,70% 8.775.199 2,60% -6.983.770 20,4

13 GUMS, RESINS 47.489 0,00% 946.106 0,30% -898.617 5,0

14 VEGETABLE PLAITING MATERIALS 45.608 0,00% 58.127 0,00% -12.519 78,5

15 FATS AND OILS 2.275.623 0,80% 26.736.458 7,90% -24.460.835 8,5

16 MEAT AND FISHERY PRODUCTS 6.155.279 2,20% 17.864.429 5,30% -11.709.150 34,5

17 SUGARS AND SUGAR CONFECTIONERY 7.288.484 2,70% 21.582.853 6,30% -14.294.369 33,8

54 Source: State Statistical Office, 2005

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

23

18 CACAO 5.203.114 1,90% 18.615.520 5,50% -13.412.406 28,0

19 PREPARATIONS OF CEREALS,FLOUR,STARCH 11.584.923 4,20% 20.625.938 6,10% -9.041.015 56,2

20 PRESERVED VEGETABLES AND FRUIT 14.279.869 5,20% 14.803.233 4,40% -523.364 96,5

21 MISCELLANEOUS FOOD PREPARATIONS 10.355.057 3,80% 28.338.069 8,30% -17.983.012 36,5

22 BEVERAGES, WINE, SPIRITS AND VINEGAR 49.783.696 18,20% 12.837.753 3,80% 36.945.943 387,8

23 ANIMAL FEED 184.915 0,10% 12.276.857 3,60% -12.091.942 1,5 24 TOBACCO AND MANUFACTURED TOBACCO 82.100.465 30,00% 12.569.994 3,70% 69.530.471 653,1

274.120.987 100% 340.140.321 100% -66.019.334 80,6

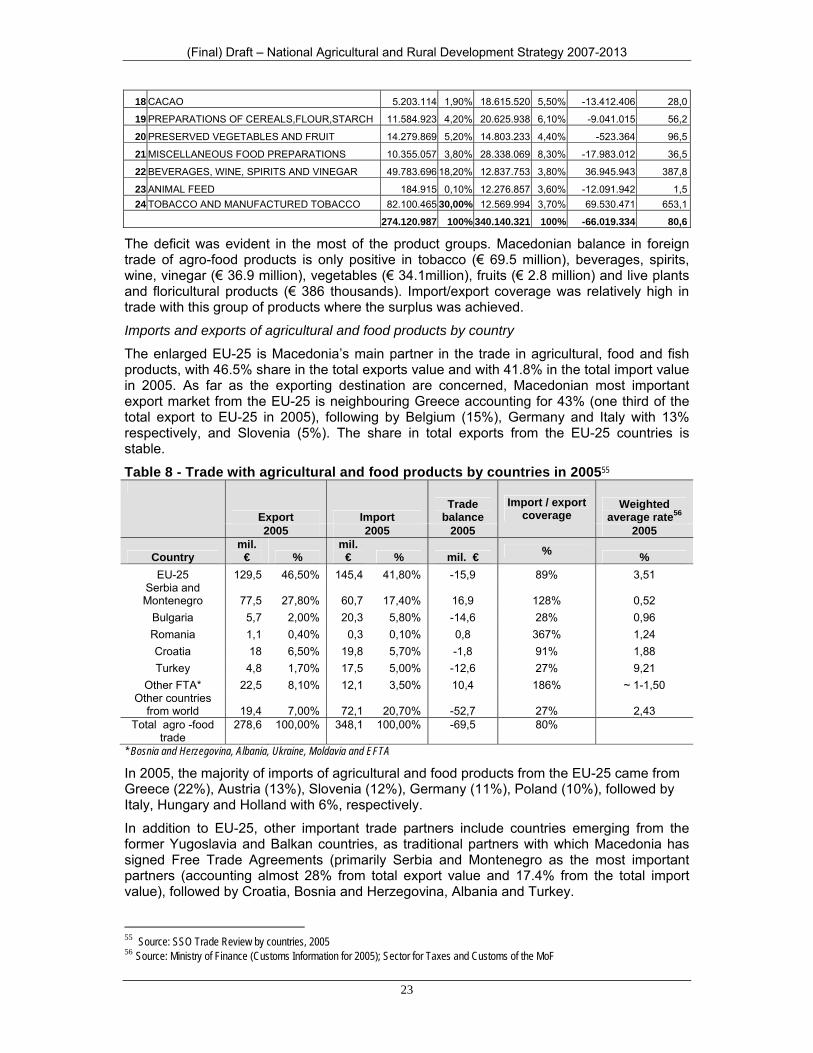

The deficit was evident in the most of the product groups. Macedonian balance in foreign trade of agro-food products is only positive in tobacco (€ 69.5 million), beverages, spirits, wine, vinegar (€ 36.9 million), vegetables (€ 34.1million), fruits (€ 2.8 million) and live plants and floricultural products (€ 386 thousands). Import/export coverage was relatively high in trade with this group of products where the surplus was achieved.

Imports and exports of agricultural and food products by country

The enlarged EU-25 is Macedonia’s main partner in the trade in agricultural, food and fish products, with 46.5% share in the total exports value and with 41.8% in the total import value in 2005. As far as the exporting destination are concerned, Macedonian most important export market from the EU-25 is neighbouring Greece accounting for 43% (one third of the total export to EU-25 in 2005), following by Belgium (15%), Germany and Italy with 13% respectively, and Slovenia (5%). The share in total exports from the EU-25 countries is stable.

Table 8 - Trade with agricultural and food products by countries in 200555

Export Import Trade

balance Import / export

coverage Weighted

average rate56 2005 2005 2005 2005

Country mil.

€ % mil.

€ % mil. € % % EU-25 129,5 46,50% 145,4 41,80% -15,9 89% 3,51

Serbia and Montenegro 77,5 27,80% 60,7 17,40% 16,9 128% 0,52

Bulgaria 5,7 2,00% 20,3 5,80% -14,6 28% 0,96 Romania 1,1 0,40% 0,3 0,10% 0,8 367% 1,24 Croatia 18 6,50% 19,8 5,70% -1,8 91% 1,88 Turkey 4,8 1,70% 17,5 5,00% -12,6 27% 9,21

Other FTA* 22,5 8,10% 12,1 3,50% 10,4 186% ~ 1-1,50 Other countries

from world 19,4 7,00% 72,1 20,70% -52,7 27% 2,43 Total agro -food

trade 278,6 100,00% 348,1 100,00% -69,5 80%

* Bosnia and Herzegovina, Albania, Ukraine, Moldavia and EFTA

In 2005, the majority of imports of agricultural and food products from the EU-25 came from Greece (22%), Austria (13%), Slovenia (12%), Germany (11%), Poland (10%), followed by Italy, Hungary and Holland with 6%, respectively.

In addition to EU-25, other important trade partners include countries emerging from the former Yugoslavia and Balkan countries, as traditional partners with which Macedonia has signed Free Trade Agreements (primarily Serbia and Montenegro as the most important partners (accounting almost 28% from total export value and 17.4% from the total import value), followed by Croatia, Bosnia and Herzegovina, Albania and Turkey.

55 Source: SSO Trade Review by countries, 2005 56 Source: Ministry of Finance (Customs Information for 2005); Sector for Taxes and Customs of the MoF

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

24

Positive trends with foreign markets occurred only in trade agro-food products with Serbia and Montenegro, achieving surplus of € 16.9 million; then Romania ( € 800 thousand) and other countries with which Macedonia has signed FTA with (Bosnia and Herzegovina, Albania, Ukraine, Moldavia and EFTA).

The general conclusion is that Macedonia depends on imports mostly for meat, processed products and other food preparation as well as for cereals. The analysis of the foreign trade sends a clear signal to domestic agro-food producers to work on restructuring of production and to create conditions to overcome the deficit. A small number of exported products emphasize the problem of competitiveness of domestic products, considering the quality, price competitiveness and potential quantities that may be sold outside Macedonia.

2.3.5. Main Agricultural Sub-sectors.

The structure of agricultural production has been stable in the last ten years and in the 2000-2005 period production has remained at the same level or has increased for the majority of agricultural products. In 2004, the agricultural gross production value (in current prices) amounted to MKD 59.510 million (approx. € 970 million).

The biggest contributor is plant production, including wine (79%), and the balance is made up by livestock products (21%). The production of fruits and vegetables (including wine) experienced the biggest gross value in 2004, with a share of 32 and 18.5% respectively in the overall value of the gross product in agriculture, or with around 40 and 23% of the total value of field crops. The biggest share of the gross product of the livestock sector in 2004 goes to livestock products with a 52% share (of which, dairy products participated with some 36% in the total value of livestock products) and livestock breeding with 48%.

2.3.6. Crop Production Chain

Crop production is analysed in four main groups, namely Cereals, Industrial (including Fodder) Crops, Fruits (including grapes) and Vegetables (including potatoes).

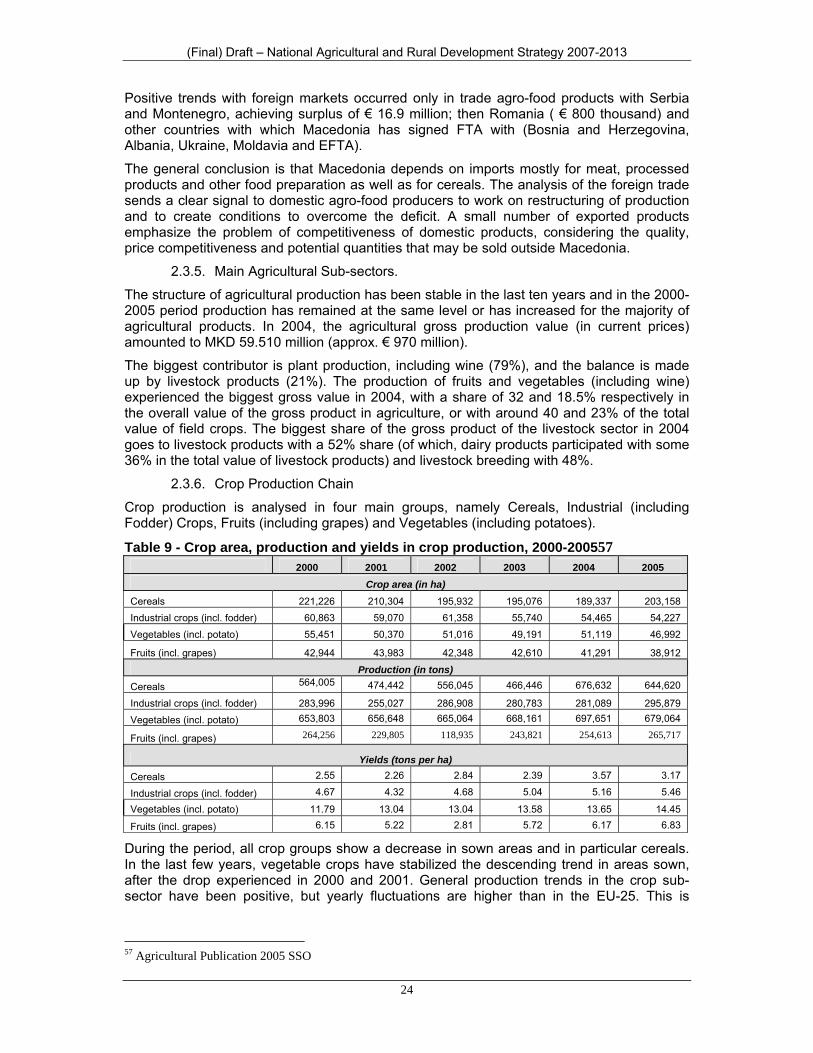

Table 9 - Crop area, production and yields in crop production, 2000-200557 2000 2001 2002 2003 2004 2005

Crop area (in ha) Cereals 221,226 210,304 195,932 195,076 189,337 203,158 Industrial crops (incl. fodder) 60,863 59,070 61,358 55,740 54,465 54,227 Vegetables (incl. potato) 55,451 50,370 51,016 49,191 51,119 46,992

Fruits (incl. grapes) 42,944 43,983 42,348 42,610 41,291 38,912

Production (in tons) Cereals 564,005 474,442 556,045 466,446 676,632 644,620

Industrial crops (incl. fodder) 283,996 255,027 286,908 280,783 281,089 295,879 Vegetables (incl. potato) 653,803 656,648 665,064 668,161 697,651 679,064

Fruits (incl. grapes) 264,256 229,805 118,935 243,821 254,613 265,717

Yields (tons per ha) Cereals 2.55 2.26 2.84 2.39 3.57 3.17

Industrial crops (incl. fodder) 4.67 4.32 4.68 5.04 5.16 5.46

Vegetables (incl. potato) 11.79 13.04 13.04 13.58 13.65 14.45

Fruits (incl. grapes) 6.15 5.22 2.81 5.72 6.17 6.83

During the period, all crop groups show a decrease in sown areas and in particular cereals. In the last few years, vegetable crops have stabilized the descending trend in areas sown, after the drop experienced in 2000 and 2001. General production trends in the crop sub-sector have been positive, but yearly fluctuations are higher than in the EU-25. This is

57 Agricultural Publication 2005 SSO

(Final) Draft – National Agricultural and Rural Development Strategy 2007-2013

25

possibly due to the lack of application of improved farm technologies (including irrigation) to mitigate climate variations and to shifting targets of past agricultural support policies.

2.3.6.1. Cereals

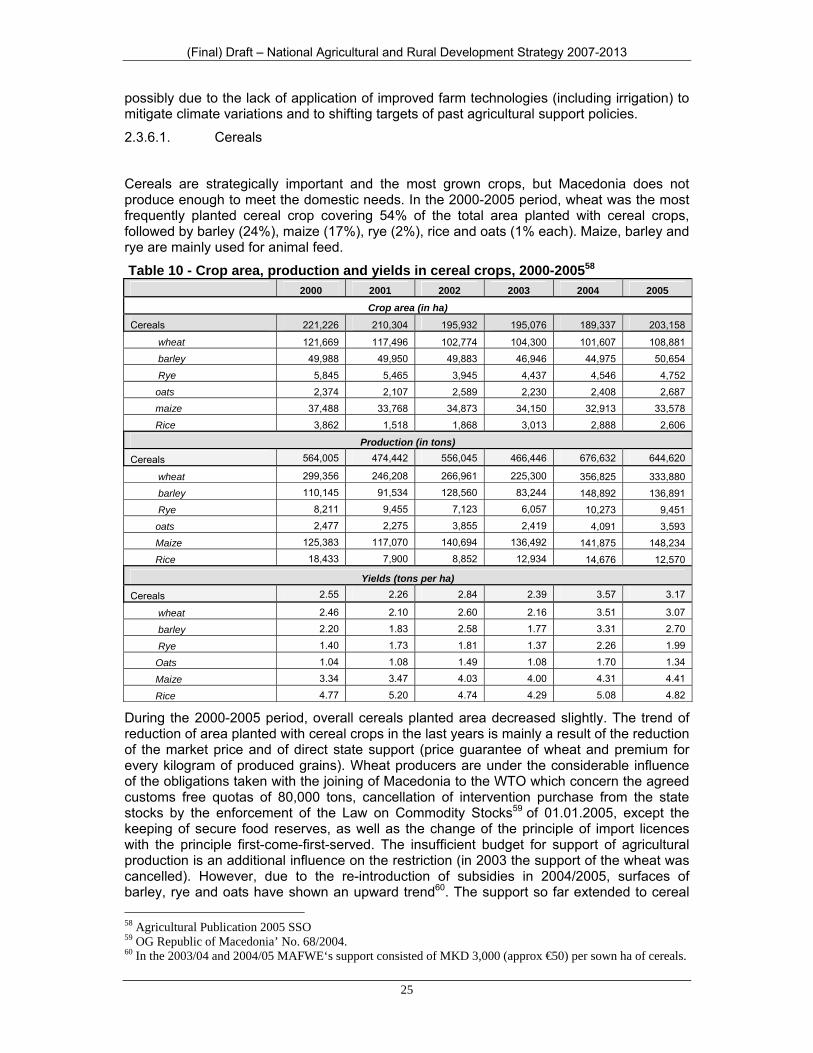

Cereals are strategically important and the most grown crops, but Macedonia does not produce enough to meet the domestic needs. In the 2000-2005 period, wheat was the most frequently planted cereal crop covering 54% of the total area planted with cereal crops, followed by barley (24%), maize (17%), rye (2%), rice and oats (1% each). Maize, barley and rye are mainly used for animal feed.

Table 10 - Crop area, production and yields in cereal crops, 2000-200558 2000 2001 2002 2003 2004 2005

Crop area (in ha)

Cereals 221,226 210,304 195,932 195,076 189,337 203,158

wheat 121,669 117,496 102,774 104,300 101,607 108,881 barley 49,988 49,950 49,883 46,946 44,975 50,654 Rye 5,845 5,465 3,945 4,437 4,546 4,752 oats 2,374 2,107 2,589 2,230 2,408 2,687 maize 37,488 33,768 34,873 34,150 32,913 33,578 Rice 3,862 1,518 1,868 3,013 2,888 2,606

Production (in tons)

Cereals 564,005 474,442 556,045 466,446 676,632 644,620