The Black Swan: The Impact of the Highly Improbable by Nassim Nicholas Taleb

Nassim Nicholas Taleb on Accepting Uncertainty, Embracing VolatilityPublished : December 17, 2012 in Knowledge@Wharton

The day before a big game, regardless of the sport, a team's coach or starplayer is often asked, "How will you stop the opposing team tomorrow?"The answer typically goes something like this: "We can't worry about theother team. We just have to play our game."

That, in a very simplified nutshell, is the essence of Nassim NicholasTaleb's highly polemical, always thought-provoking new book, Antifragile:Things That Gain from Disorder. Here, though, the opponent is not anotherteam's slugger, quarterback or point guard, but the future and change. Thedefining characteristic of future change, according to Taleb (who continuesa line of argument developed in previous books like Fooled by Randomness and The Black Swan), is that it is impossible, and foolhardy, to try to predictit. Instead, the author argues, it is essential to make peace with uncertainty,randomness and volatility. Those who do not -- who insist not only ontrying to predict the future, but also on somehow trying to manage it -- hedisparagingly calls "fragilistas."

Antifragile is divided into seven sections that Taleb calls "books." In aprologue, he explains that each is, in a sense, a long personal essay, "mixing autobiographical musingsand parables with more philosophical and scientific investigations." The author introduces fictionalcharacters such as Fat Tony, who epitomizes the straight-talking "street" knowledge of the practitioner asopposed to the fragilista. In addition to "fragilista," he coins or adopts a number of other terms; delvesinto extended asides on Greek philosophy and mythology; and in general fashions a thoroughlyidiosyncratic approach to his subject matter. The result is a work that is readable and entertaining, if attimes a bit unwieldy.

A Future We Can't Predict

Taleb advocates what he calls "nonpredictive decision making" focused on the ability of the unit inquestion (whether that be an individual, institution, industry or society) to withstand unexpected change.Yet to simply survive is not enough. Taleb is interested in things that actually thrive on uncertainty. Tomerely avoid harm is, in his terms, to be robust -- and at times this is an acceptable result. Robustnessfalls in the middle of a continuum he calls The Triad. At the far left is fragility -- that which requirestranquility, certainty and predictability -- and at the far right, in the absence of a better word for it, is antifragility.

Antifragility, it should be pointed out, doesn't mean that volatility will always be experienced positively. Itsimply means that the antifragile has more of an upside than downside from random events. As Talebnotes, "Some things benefit from shocks; they thrive and grow when exposed to volatility, randomness,disorder, and stressors and love adventure, risk, and uncertainty."

Another sports analogy, one Taleb himself uses, effectively illustrates the idea of benefiting from shock.When we go the gym and lift heavy weights (barbells later become a key image in the book), weintentionally apply stress to our body. Muscle tissue is strained and even broken down. The body'sresponse is to overcompensate to the trauma and emerge stronger than before. This process ofoverreaction to stress and setbacks, the author argues, is intrinsic to our very being, to all of evolution, tonature and to every human system that has survived. It is the process of life itself. The reverse holds trueas well: Remove stress from a system, and that system grows weak; it becomes fragile. Stay in bed forthree weeks instead of lifting weights, and muscles atrophy.

This is a single/personal use copy ofKnowledge@Wharton. For multiple copies,custom reprints, e-prints, posters or plaques,please contact PARS International:[email protected] P. (212) 221-9595 x407.

All materials copyright of the Wharton School of the University of Pennsylvania. Page 1 of 4

Nassim Nicholas Taleb on Accepting Uncertainty, Embracing Volatility: Knowledge@Wharton( http://knowledge.wharton.upenn.edu/article.cfm?articleid=3136)

The Cat and the Washing Machine

A key distinction for Taleb is that between the organic and the mechanical, and the title concept is centralto this. Organic entities are intrinsically antifragile, while artificial creations are at best robust and likelyfragile. The split corresponds roughly, but not entirely, to the living and the non-living. Taleb argues thatcertain man-made things like ideas, technologies, businesses and even the economy operate more byorganic principles than mechanical ones: "They are closer to the cat than to the washing machine but tendto be mistaken for washing machines."

Nature and natural systems are an ongoing reference for Taleb -- not just as illustrative analogies, but aspart of the very fabric of his worldview. For him, nature is the ultimate model for how to deal withuncertainty. Nature does not need to predict the future in order to deal with its unexpected turns. Theinformation volatility provides is digested and adapted as part of the evolutionary process. In this sense,nature "loves small errors."

Nature is also not "safe." It accepts short-term loss for long-term gain. For example, Taleb cites thenatural cycle of forest fires that clear the forest of highly flammable material and weed out weak andvulnerable growth. Suppressing these fires artificially (i.e., suppressing volatility) imposes a falseshort-term stability while increasing long-term risk. We get fewer fires but more devastating ones. Thisbasic principle can be applied to human systems as well. Government bailouts that prevent certainbusinesses from going under, for example, only increase the possibility of system-wide collapse. Errorand failure, Taleb insists again and again, are essential sources of information as long as they are limitedand localized. Every plane crash brings us closer to safety. Attempts to eliminate error and volatility willbackfire in the long run. Paradoxically, there is no long-term stability without short-term volatility.

Black Swans

A concept Taleb developed in a previous book, Black Swans are game-changing, world-altering events hecontends are the driving force in history. Though they are impossible to predict, fragilistas (especially thepolicymakers and academics Taleb loves to ridicule) make the mistake of trying to impose a clearnarrative on them in retrospect. With that narrative in place, they tell themselves the Black Swan couldhave, and perhaps should have been, anticipated, and they set about trying to successfully predict the nextone. For example, events in the Middle East that have caught the U.S. government by surprise (such asthe 2011 Egyptian uprising or the 1979 Islamic Revolution in Iran) are labeled "intelligence failures." Thesolution, according to fragilistas, is simply better forecasting.

This approach misses the point, which is to assess the fragility of a system, not the particular event thatwill expose that fragility. In a discussion of the earthquake and tsunami that produced the 2011Fukushima nuclear disaster in Japan, Taleb writes: "Not seeing a tsunami or an economic event coming isexcusable; building something fragile to them is not." And in the case of the Fukushima disaster,authorities seem to be responding appropriately: not by developing better predictive models, but bybuilding smaller and less vulnerable reactors.

It is important to point out that Black Swans are not always negative, destructive events. The explosion ofthe Internet and the rise of Google are examples of positive Black Swans. What cultivating antifragilitydoes, Taleb says, is enable us to minimize the potential harm from negative Black Swans while capturingthe benefits of positive ones. It is all about developing a productive and flexible relationship withvolatility.

Nonetheless, the dominant impulse among policymakers and so-called experts is to try to reducevolatility, rather than deal with it more productively. These fragilistas overestimate the reach of scientificknowledge and the possibilities of human control. Intolerant of the messiness of trial-and-error volatility,they avoid small errors and the essential feedback those errors provide. The end result is to createsomething that is steadier and more predictable, but fundamentally fragile. Risks are hidden andsuppressed, and the stimulation of randomness and stressors is denied. But the effort to avoid smallmistakes and minor pains makes larger ones more severe. Ironically, the imposition of false stability withthe intention of avoiding Black Swans makes them more likely and more dangerous.

All materials copyright of the Wharton School of the University of Pennsylvania. Page 2 of 4

Nassim Nicholas Taleb on Accepting Uncertainty, Embracing Volatility: Knowledge@Wharton( http://knowledge.wharton.upenn.edu/article.cfm?articleid=3136)

Narrowly, the fragilista is marked by a preoccupation with theory, risk assessment and strategic planning-- all of which Taleb disdains. More broadly, the fragilista is symptomatic of the fundamentalshortcomings of modernity, which the author defines as "humans' large-scale domination of theenvironment, the systematic smoothing of the world's jaggedness, and the stifling of volatility andstressors." Modernity has made a religion of rationalism, optimization and efficiency. By contrast, Talebinvokes Nietzsche and his embrace of the "Dionysian": the "dark, visceral, wild, untamed, hard tounderstand."

Knowledge and Practice

Epistemology, the inquiry into the nature of knowledge, is a central concern for Taleb, and an eminentlypractical one as opposed to a theoretical one. In a world ruled by uncertainty and unpredictability, and inwhich precise causes are impossible to isolate, abstract and theoretical knowledge is of limited use. Hisown encounter with these limits came when, as a recent graduate of business school and then the recipientof a doctorate in management science, he did a stint on a foreign exchange trading floor. The professionaltraders he worked with had no background in theory, and they didn't read economic reports or forecasts;they simply had a nose for when to buy and when to sell. They knew what worked; they didn't need toknow why.

Ever since, Taleb has had a deep respect for practitioners as opposed to theorists. Real, usable knowledgeemerges from doing, not studying. Technology is often described as the application of scientificknowledge to practical projects, implying a hierarchy with priestly "science" on one level and mere"practice" far below. Taleb lists numerous examples in the development of technology, and medicine aswell, demonstrating how theory and knowledge emerge from practice, not the other way around. Keyadvances grow organically (and sometimes randomly) from individuals the author likes to call "tinkerers"engaged in hands-on trial-and-error experimentation.

Accordingly, Taleb embraces the apprenticeship model of learning as opposed to the academic model. Hedoesn't oppose formal education, but says its purpose should be learning for learning's sake, and thateducation should not be justified as an engine of economic growth. He cites studies by economists whocall into question an assumed causal link between education levels and productivity. Instead, he argues,wealth and economic growth eventually result in good education systems.

The logical conclusion of Taleb's preference for practice over theory is to question the classical Socraticideal of truth in the first place. Being right, knowing how to define things, understanding the differencebetween what is true and false: None of this is the point. What is important is to understand the results ofevents, not the events themselves. An even deeper implication of this approach is that real intelligencelies not in the individual, but in the evolutionary process -- the ongoing process of trial-and-error. In thisprocess, he argues, options (essentially, the freedom to experiment with uncertainty) can be moreimportant than knowledge or information. Options allow you to benefit from the feedback trial-and-errorprovides. And knowing how to apply that feedback to future decisions can be the highest form ofwisdom: "wisdom in decision making is vastly more important -- not just practically, but philosophically-- than knowledge."

Medicine and Barbells

The practice of modern Western medicine is a topic of great interest to Taleb in its own right. But it alsoprovides him with a set of clear examples of the perils of the fragilista's tendency toward what he terms"naïve interventionism." This is a category of intervention that produces small (or no) visible gains, whilecreating the possibility of large (but often not immediately visible) harm. Examples include statin drugs totreat high cholesterol (where fifty patients have to be treated, at uncertain cost, to prevent a singlecardiovascular event) and annual mammograms for women (which actually increase all-cause mortalityfor the test group).

In opposition to this approach, the author cites the part of the Hippocratic Oath that cautions, "First, do noharm." Unfortunately, the pervasiveness of professionalization in our society creates a bias towardintervention -- in other words, the restraint of inaction is not likely to be rewarded. Nonetheless, inmedicine and other areas, he asserts that the first rule should be to "avoid interference with things we don'tunderstand," which, in Taleb's view, covers a lot of ground.

All materials copyright of the Wharton School of the University of Pennsylvania. Page 3 of 4

Nassim Nicholas Taleb on Accepting Uncertainty, Embracing Volatility: Knowledge@Wharton( http://knowledge.wharton.upenn.edu/article.cfm?articleid=3136)

Taleb is a fan of barbells as an exercise tool. But he also uses the image to convey the "bimodal" approachhe suggests is the best way to deal with uncertainty and cultivate antifragility. In keeping with the imageof the barbell, the idea is to avoid the wishy-washiness of the supposed "Golden Middle" and insteadconcentrate on two contrasting but complementary strategies: extreme risk aversion on one side, andextreme risk loving on the other. For example, in the area of personal investment, you might invest 90%of your funds in something as radically safe as cash, while putting 10% toward extremely high-risk,high-reward investments. Your maximum loss would be capped at 10% of your assets, whereas putting100% of your assets in so-called "medium" risk securities carries a danger of losing everything. Strive tobe 90% accountant, 10% rock star, Taleb cheekily suggests.

He applies this model across a variety of arenas. For example, in medicine, we should treat the healthy ornear-healthy with an extremely conservative, less-is-more approach, while treating the seriously ill muchmore aggressively. In socio-economic policy, it would imply aggressive intervention for the very weakwhile letting the very strong alone -- in contrast to the current policy of focusing on the creation of minorgains for the middle class.

Skin in the Game

For Taleb, the barbell is a tool for engaging risk and uncertainty in a way that is both responsible andvigorous. He praises those who take risks, whether they be entrepreneurs or poets, as adventurers anddoers essential to the continued evolution of society and the economy. At the other end of the spectrumare those who talk or act without any risk or exposure. Taleb has nothing but disdain for policymakers orpundits who enter the fray of public policy without any personal stake in the issue at hand. They have no"skin in the game," as he likes to put it.

In a final section devoted to the ethics of fragility and antifragility, Taleb laments that this kind ofdisconnect between influence and personal risk is only growing: "At no point in history have so manynon-risk-takers, that is, those with no personal exposure, exerted so much control." Here, the author takesthe gloves off and names names -- with columnist Thomas Friedman and economist Joseph Stiglitzamong those singled out. Taleb is particularly troubled by corporate managers who don't own thebusinesses they run. They have incentives (bonuses) without disincentives (penalties), upside withoutdownside. Robert Rudin, for example, earned nearly $120 million in bonuses from Citibank, but sufferedno personal consequences when the bank collapsed and required a multi-billion--dollar governmentbailout.

Taleb characterizes this as essentially a "transfer of antifragility," with certain individuals exertinginfluence without cost (remaining antifragile) while others bear the consequences (increased fragility).Such a transfer is, he asserts, a kind of theft, and it raises a profound ethical question, perhaps thedominant one of our time. Somehow, he writes, we have to "make talk less cheap."

This is a single/personal use copy of Knowledge@Wharton. For multiple copies, custom reprints, e-prints, posters or plaques, please contactPARS International: [email protected] P. (212) 221-9595 x407.

All materials copyright of the Wharton School of the University of Pennsylvania. Page 4 of 4

Nassim Nicholas Taleb on Accepting Uncertainty, Embracing Volatility: Knowledge@Wharton( http://knowledge.wharton.upenn.edu/article.cfm?articleid=3136)

Connecting the dots December 12, 2012

INVESTMENT MANAGEMENT

Simhavalokana

As we bid adieu to the year 2012, it is time for our very own form of Simhavalokana. Wildlife enthusiasts, or should we say Indian philosophers, may well know the fact that as the lion walks some distance in the jungle, it looks back to examine the path it chose and how it covered that distance. Th is retrospective glance in Sanskrit is known as Simhavalokana.

It is human nature to obsess about the future. We don’t blame market forecasters for being pre-occupied in attempting to look at the crystal ball while trying to predict index targets for 2013. After all Charles Kettering1 once said, “My interest lies in the future, because I am going to spend the rest of my life there”. However, as lifelong students of the stock market we think it is as important to refl ect on the year gone by, as it is to try to make forecasts. We often get so absorbed in the daily noise surrounding investing, that we tend to forget the importance of refl ective Simhavalokana. In this year-end edition of Connecting the Dots, we make an attempt to summarise ten lessons learnt from the markets in 2012.

1. Market timing is dangerous

As investors, our holy grail for generating alpha is to look for through-cycle winners, who we call Th e Dependables (refer CTD: Th e Dependables). We don’t categorise stocks or sectors as defensives or cyclicals, but rather as those with dependable growth and capital allocation characteristics versus those without. We think market timing is a dangerous game and in 2012 we refrained from trying to time the market by avoiding tactical trades in high beta stocks in anticipation of a rally.

As Vitaliy Katsenelson2 said, “It is hard if not impossible to create a successful market timing process. Aside from the fact that it demands that you be correct twice – when you buy and when you sell – emotions are in the driver’s seat of the market especially at the tops and bottoms”.

Amay Hattangadi

Executive DirectorPortfolio Manager, Morgan Stanley Growth Fund

Swanand Kelkar

Vice President

Portfolio Manager, Morgan Stanley Growth Fund

1 An American inventor, engineer, businessman, and the holder of 186 patents; Credited with the invention of the electric motor.

2 The Little Book of Sideways Markets by Vitaliy Katsenelson.

Simhavalokana

2 |

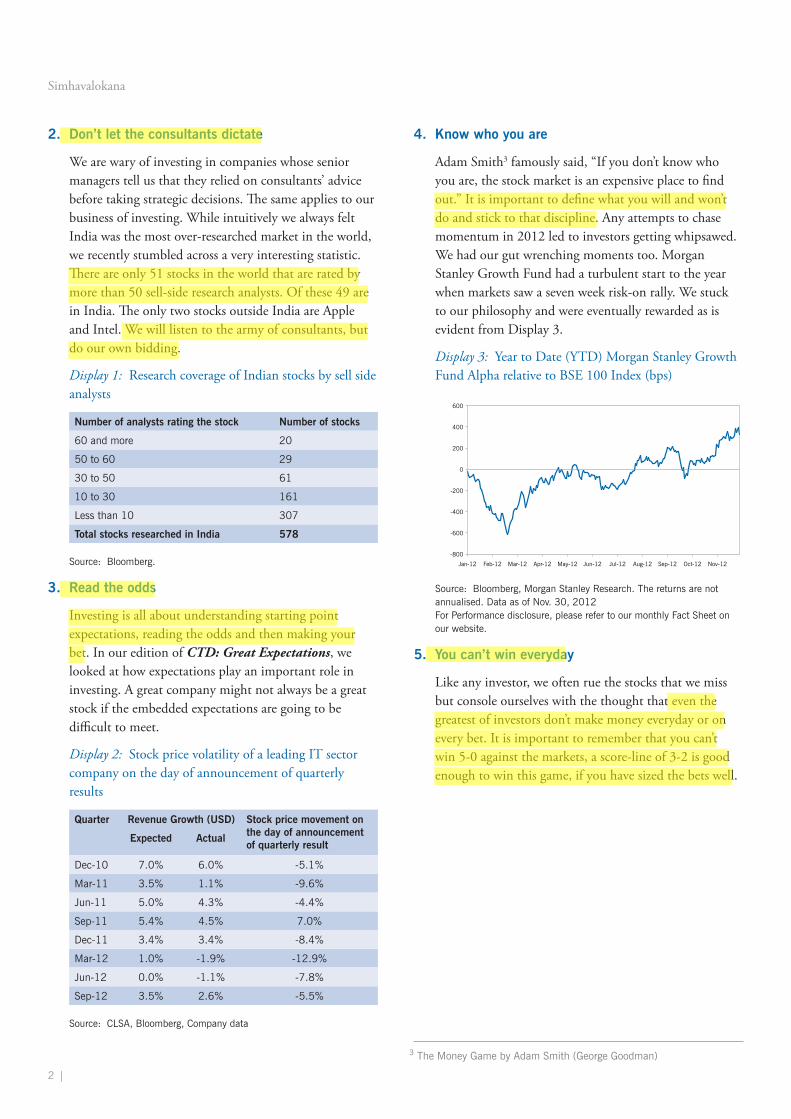

2. Don’t let the consultants dictate

We are wary of investing in companies whose senior managers tell us that they relied on consultants’ advice before taking strategic decisions. Th e same applies to our business of investing. While intuitively we always felt India was the most over-researched market in the world, we recently stumbled across a very interesting statistic. Th ere are only 51 stocks in the world that are rated by more than 50 sell-side research analysts. Of these 49 are in India. Th e only two stocks outside India are Apple and Intel. We will listen to the army of consultants, but do our own bidding.

Display 1: Research coverage of Indian stocks by sell side analysts

Number of analysts rating the stock Number of stocks

60 and more 20

50 to 60 29

30 to 50 61

10 to 30 161

Less than 10 307

Total stocks researched in India 578

Source: Bloomberg.

3. Read the odds

Investing is all about understanding starting point expectations, reading the odds and then making your bet. In our edition of CTD: Great Expectations, we looked at how expectations play an important role in investing. A great company might not always be a great stock if the embedded expectations are going to be diffi cult to meet.

Display 2: Stock price volatility of a leading IT sector company on the day of announcement of quarterly results

Quarter Revenue Growth (USD) Stock price movement on the day of announcement of quarterly result

Expected Actual

Dec-10 7.0% 6.0% -5.1%

Mar-11 3.5% 1.1% -9.6%

Jun-11 5.0% 4.3% -4.4%

Sep-11 5.4% 4.5% 7.0%

Dec-11 3.4% 3.4% -8.4%

Mar-12 1.0% -1.9% -12.9%

Jun-12 0.0% -1.1% -7.8%

Sep-12 3.5% 2.6% -5.5%

Source: CLSA, Bloomberg, Company data

4. Know who you are

Adam Smith3 famously said, “If you don’t know who you are, the stock market is an expensive place to fi nd out.” It is important to defi ne what you will and won’t do and stick to that discipline. Any attempts to chase momentum in 2012 led to investors getting whipsawed. We had our gut wrenching moments too. Morgan Stanley Growth Fund had a turbulent start to the year when markets saw a seven week risk-on rally. We stuck to our philosophy and were eventually rewarded as is evident from Display 3.

Display 3: Year to Date (YTD) Morgan Stanley Growth Fund Alpha relative to BSE 100 Index (bps)

Source: Bloomberg, Morgan Stanley Research. The returns are not annualised. Data as of Nov. 30, 2012For Performance disclosure, please refer to our monthly Fact Sheet on our website.

5. You can’t win everyday

Like any investor, we often rue the stocks that we miss but console ourselves with the thought that even the greatest of investors don’t make money everyday or on every bet. It is important to remember that you can’t win 5-0 against the markets, a score-line of 3-2 is good enough to win this game, if you have sized the bets well.

3 The Money Game by Adam Smith (George Goodman)

-800

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12

-600

-400

-200

0

200

400

600

Simhavalokana

| 3

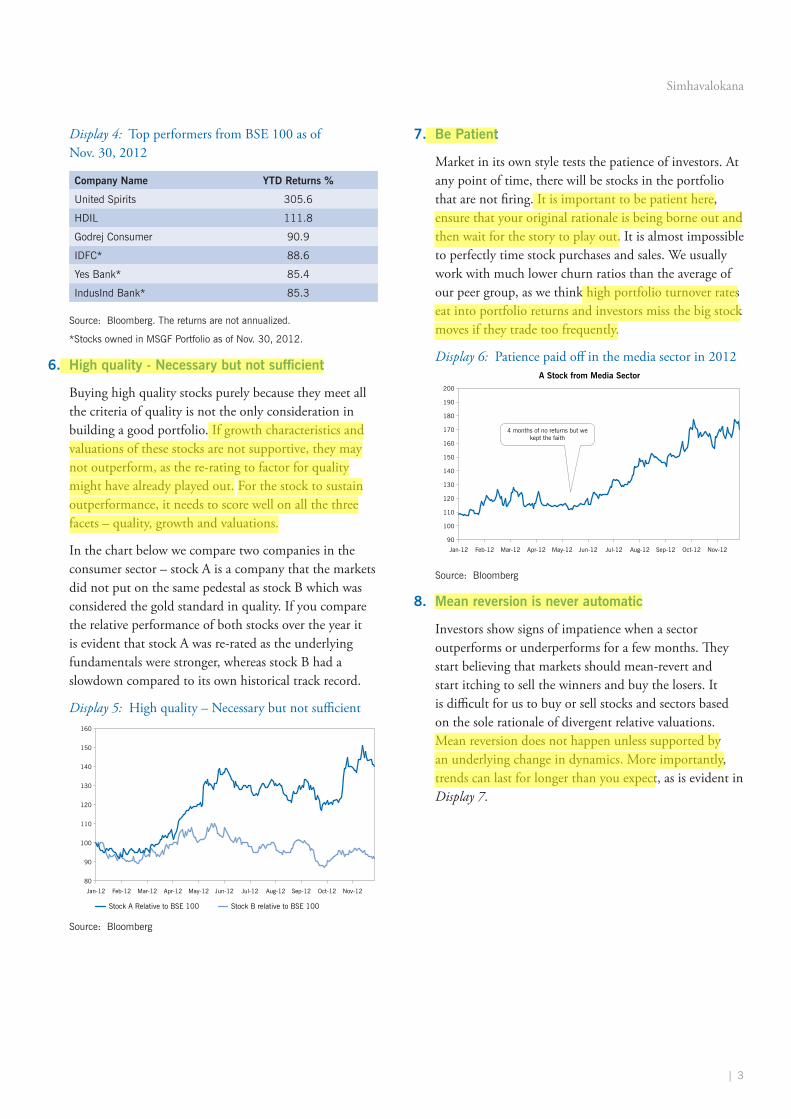

Display 4: Top performers from BSE 100 as of Nov. 30, 2012

Company Name YTD Returns %

United Spirits 305.6

HDIL 111.8

Godrej Consumer 90.9

IDFC* 88.6

Yes Bank* 85.4

IndusInd Bank* 85.3

Source: Bloomberg. The returns are not annualized.

*Stocks owned in MSGF Portfolio as of Nov. 30, 2012.

6. High quality - Necessary but not suffi cient

Buying high quality stocks purely because they meet all the criteria of quality is not the only consideration in building a good portfolio. If growth characteristics and valuations of these stocks are not supportive, they may not outperform, as the re-rating to factor for quality might have already played out. For the stock to sustain outperformance, it needs to score well on all the three facets – quality, growth and valuations.

In the chart below we compare two companies in the consumer sector – stock A is a company that the markets did not put on the same pedestal as stock B which was considered the gold standard in quality. If you compare the relative performance of both stocks over the year it is evident that stock A was re-rated as the underlying fundamentals were stronger, whereas stock B had a slowdown compared to its own historical track record.

Display 5: High quality – Necessary but not suffi cient

Source: Bloomberg

7. Be Patient

Market in its own style tests the patience of investors. At any point of time, there will be stocks in the portfolio that are not fi ring. It is important to be patient here, ensure that your original rationale is being borne out and then wait for the story to play out. It is almost impossible to perfectly time stock purchases and sales. We usually work with much lower churn ratios than the average of our peer group, as we think high portfolio turnover rates eat into portfolio returns and investors miss the big stock moves if they trade too frequently.

Display 6: Patience paid off in the media sector in 2012

Source: Bloomberg

8. Mean reversion is never automatic

Investors show signs of impatience when a sector outperforms or underperforms for a few months. Th ey start believing that markets should mean-revert and start itching to sell the winners and buy the losers. It is diffi cult for us to buy or sell stocks and sectors based on the sole rationale of divergent relative valuations. Mean reversion does not happen unless supported by an underlying change in dynamics. More importantly, trends can last for longer than you expect, as is evident in Display 7.

80

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12

90

100

110

120

130

140

160

150

Stock A Relative to BSE 100 Stock B relative to BSE 100

90

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12

100

110

120

130

140

200

4 months of no returns but wekept the faith

160

170

180

190

150

A Stock from Media Sector

Simhavalokana

4 |

Display 7: Cyclicals vs. Defensives

Source: Company data, MSCI, Credit Suisse estimates

Note: As per Credit Suisse, “Defensives” include Consumer Staples, Telcos, Utilities and Healthcare. “Cyclicals” include Energy, Materials, Industrials, Consumer Discretionary and Technology.

9. Don’t gamble

Market participants often spend disproportionate time and eff ort in trying to predict binary events. Th ese range from trying to guess when the Government might announce subsidy reduction measures to forecasting M&A activity. We resisted the temptation of participating in binary events such as chasing stocks on the back of rumoured M&A in the airlines and liquor sectors. While hindsight vision is a perfect 20-20 and some of these “event plays” might seem like misses in our portfolio, writing a convincing rationale without factoring in the event would have been diffi cult for us.

10. Bad Macro ≠ Bad Stock returns

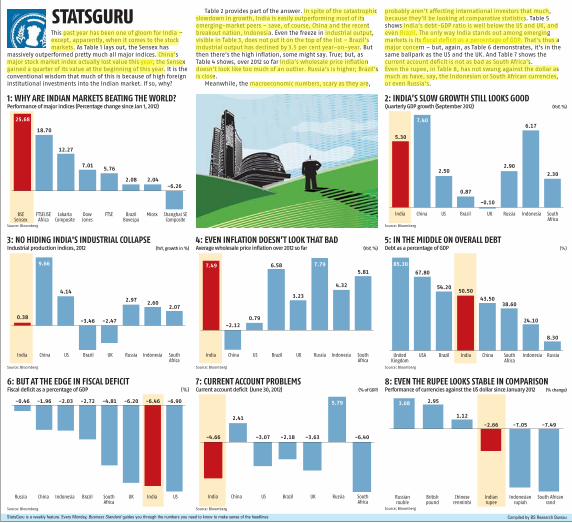

Market indices are up 30%4 this year as this edition of Connecting the Dots goes into print. If we look back at all the gloomy economic commentary at the beginning and through most of the year it would have been almost impossible to predict such respectable returns. Year to date, India is among the best performing markets in the world. Amongst the 45 countries included in the MSCI All Country World Index, India this year ranks at #5 in US Dollar performance. So while macro factors play an important role in defi ning the regime in which companies operate, it is incorrect to give up on a country just because its macro environment is challenged. We strongly believe that despite the macro vulnerabilities, India’s allure for investors lies in the bottom up micro stories.

Display 8: Strong markets despite slowing GDP Growth

Source: CEIC, FactSet, Morgan Stanley Research

We recently watched the movie Life of Pi5 and it set us thinking about the deeper philosophical message from a seemingly simple story. Th e protagonist who goes by the nickname Pi survives a shipwreck on a boat with a Bengal tiger. After narrating his bizarre, almost implausible story, he says to the doubting offi cials who are investigating the shipwreck, “I know what you want. You want a story that won’t surprise you. Th at will confi rm what you already know. Th at won’t make you see higher or further or diff erently.” He then tells an alternate, far more gruesome and tragic story about his survival. Even the hard-nosed offi cials in the end believe the fantastic yet happy narrative. Isn’t the India story similar? While the problems are well known, we need to dream of a story that does not confi rm what we already know. In a year where doubt and skepticism abound, the Indian markets are likely to end 2012 at the top of the heap. While there are multiple excuses for not investing in the market, we continue to believe that a well-constructed portfolio can give decent returns. Investors need to choose what they want to believe. As Pi says “To choose doubt as a philosophy of life is akin to choosing immobility as a means of transportation.” Happy investing.

5 The movie Life of Pi is based on a book by the same name by Yann Martel.

5.0%

Dec-11 Mar-12 Jun-12 Sep-12 Nov-12

5.2%

5.4%

5.6%

5.8%

6.0%

6.2%

90

95

100

105

110

115

120

130

125

Nifty (Indexed to 100)-RSQuarterly GDP Growth (y-o-y)-LS

-7.0

Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

-6.3x

-4.0

-5.0

-6.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

India Trailing PB - Cyclicals less defensives

4 YTD return for BSE 100 as on December 6, 2012

www.jpmorganmarkets.com

Asia Pacific Equity Research14 December 2012

India Equity StrategyThe Policy Reform Road - A Good Start

Indian Equity Strategy

Bharat Iyer AC

(91-22) [email protected]

J.P. Morgan India Private Limited

Bijay Kumar, CFA(91-22) [email protected]

J.P. Morgan India Private Limited

Gunjan Prithyani(91-22) [email protected]

J.P. Morgan India Private Limited

Emerging Market Equity StrategyAdrian Mowat(852) [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

See page 4 for analyst certification and important disclosures, including non-US analyst disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

! Combating accusations of “policy-paralysis” over the last two years, the Government has made a decisive comeback on the reforms front over the last quarter. Zest for reforms has also been backed by some shrewd political maneuvering. Policy initiatives have been the key driver for Indian equities performance over the last quarter. A revival in growth is expected to be gradual implying that the policy developments will continue to be the key driver for market performance over the near term.

! What’s been achieved so far? Key policy initiatives since September are: 1. Increase in Diesel price and capping the number of subsidized LPG cylinder per family per year to six 2. Increased FDI limit in multi-brand retail (51%), Aviation (49%) and Broad casting (74%) 3. Cabinet approvals– Companies bill, Insurance & PFRDA bills, Land acquisition bill, Cabinet Committee on Investments, Urea Investment Policy 4. Roadmap on Direct Cash Transfers 5. Reduction in withholding tax on Corporate bonds 6. Resolving 2G spectrum pricing and auction 7. SEB debt restructuring 8.Rajiv Gandhi Equity Savings scheme to encourage retail investor into Indian equities.

! What to expect? Parliamentary approval is required for Insurance, PFRDA and Companies Bill. More importantly, the real progress on Cabinet Committee on Investments, Land Acquisition Bill and GST (Goods and Services Tax) are extremely important for attaining higher growth trajectory.

! Implications for Indian equities. Despite the recent sharp rally, current market valuations are not reflecting any irrational exuberance. Our base case expectations are for Indian equities to deliver returns of 12-15% over the next year driven primarily by earnings growth. Momentum on reforms sustaining would open up the possibility of increased returns as the markets re-rate further.

Figure 1: MSCI India - 12 M Forward PE

Source: MSCI, Datastream

8

12

16

20

24

Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12

BSE Sensex

Source: Bloomberg (rebased performance).

MSCI India relative

Source: MSCI, Bloomberg

9095

100105110115120125

Nov 11 Feb 12 May 12 Aug 12 Nov 1

90

95

100

105

110

Dec 11 Apr 12 Aug 12 Dec 12

rel to EM

rel to APxJ

2

Asia Pacific Equity Research14 December 2012

Bharat Iyer(91-22) [email protected]

Policy Reforms: The Course Ahead. Combating accusations of “policy-paralysis” over the last two years, the Government has made a decisive comeback on the reforms front over the last quarter. Zest for reforms has also been backed by some shrewd political maneuvering. Policy initiatives have been the key driver for Indian equities performance over the last quarter. A revival in growth is expected to be gradual implying that the policy developments will continue to be the key driver for market performance over the near term.

Key policy initiatives / achievements since September 2012 are:

1. Increase in Diesel price and capping the number of subsidized cylinder per family: Diesel prices were increased by Rs 5 per liter, amounting to an 11% increase over the current price, effective from September 14. Also, the number of subsidized cooking gas cylinders that each family can avail has been capped at 6 per year. These measures are expected to reduce the fiscal deficit by a marginal ~ 0.1% of GDP.

2. Increased FDI limits. Foreign Direct Investment limit has been increased to 51% in multi-brand retail. This was an extremely contentious political issue and involved voting in both the parliament houses. Additionally, the CCEA (Cabinet Committee of Economic Affairs) approved a proposal that allows foreign-airlines to own up to 49% stake in India’s domestic carriers, increased FDI limits from 49% to 74% in the broadcasting sector, and introduced FDI into power exchanges.

3. Cabinet approvals: Companies’ bill, Insurance & PFRDA bill and Land Acquisition bill have been approved by the Cabinet but parliamentary approvals are required for these bills. Urea Investment Policy and Cabinet Committee on Investment don’t need parliamentary approval.

a. Companies’ bill’s objective is to modernize the structure for corporate regulation in India and also to promote better governance practices.

b. Higher FDI limit in Insurance (proposed 49%) & Pension Funds (in-line with Insurance sector) are expected to bring foreign capital and global expertise in these sectors.

c. Land Acquisition Bill aims to define an equitable framework for the compensation, resettlement and rehabilitation for land acquisition. The details are going to be debated in the parliament.

d. Cabinet Committee on Investment (CCI) has an objective of de-bottle necking key impediments in large projects (above Rs. 10 bn). The Committee is expected to oversee implementation of projects on a continuous basis.

Government has taken a number of policy initiatives to reviveeconomic growth momentum over the last three months.

3

Asia Pacific Equity Research14 December 2012

Bharat Iyer(91-22) [email protected]

e. Urea Investment Policy is expected to incentivize fertilizer firms setting up new plants and expanding existing capacity. India imports over 30 per cent of urea requirement and the policy aims at reducing that.

4. Roadmap of Direct Cash Transfers. Direct targeting of subsidies has been one of the focus areas for this government towards fiscal consolidation. The Finance Minister shared details of the cash transfer of subsidies starting 1st of January 2013. The rollout is expected to start in 51 districts across states in India. The key criterion of district selection was districts with over 80% UID (Aadhaar) coverage. There are 29 schemes of various ministries –HRD, Women & Child Welfare, Minority Affairs, and Labor etc. – which have been short-listed for the cash transfer.

5. Reduction in withholding tax on corporate bonds. Withholding Tax has been cut from 20% to 5 % for all foreign loans, ECBs and FCCBs. This is the tax retained by the corporate and paid to the Government from FII/ NRIs payout. Earlier in March this year, the tax rate was reduced from 20% to 5% for select sectors only - power, airlines, roads and bridges, ports and shipyards, affordable housing, fertilizer and dams.

6. Resolving 2G spectrum pricing and auction. Telecom sector has been oneof the key victims of regulatory uncertainty. The recently held 2G spectrum auction has reduced the regulatory overhang to some extent.

7. SEB debt restructuring. The Cabinet Committee on Economic Affairs (CCEA) approved restructuring of Rs 1.9 lakh crore debt of state electricity boards. The move is expected to benefit the lenders and power companies in the long-term if discipline is maintained. As per the scheme, 50% of the short-term outstanding liabilities would be taken over by state governments and balance 50% would be restructured by providing moratorium on principle and best possible terms for repayments. Additionally, SEBs are expected to reduce their deficit in a phased manner through timely hikes in electricity tariff and reducing T&D (Transmission & Distribution) losses.

8. Rajiv Gandhi Equity Savings scheme. Under this scheme, a one-time deduction for income tax purposes will be available to a “new retail investor.” The new retail investor will be eligible for a deduction on the actual amount invested in ‘eligible securities’ in the first financial year, subject to maximum deduction limit of Rs 50,000. Eligible securities will include equity shares falling in the list of equity declared as “BSE-100” or “CNX-100”; equity shares of public sector enterprises that are categorised as Maharatna, Navaratna or Miniratna by the Central Government.

The Road AheadDespite the recent sharp rally, current market valuations are not reflecting any irrational exuberance. Our base case expectations are for Indian equities to deliver returns of 12-15% over the next year driven primarily by earnings growth. Momentum on reforms sustaining would open up the possibility of increased returns as the markets re-rate further.

Sentiment in financial marketshas improved but bottoming out of growth and the pace of recovery remains uncertain as of now.

Manufacturing the future: The next era of global growth and innovation

McKinsey Global Institute

1

A decade into the 21st century, the role of manufacturing in the global economy

continues to evolve. We see a promising future. Over the next 15 years,

another 1.8 billion people will enter the global consuming class and worldwide

consumption will nearly double to $64 trillion. Developing economies will continue

to drive global growth in demand for manufactured goods, becoming just as

important as markets as they have been as contributors to the supply chain. And

a strong pipeline of innovations in materials, information technology, production

processes, and manufacturing operations will give manufacturers the opportunity

to design and build new kinds of products, reinvent existing ones, and bring

renewed dynamism to the sector.

The factors we describe point to an era of truly global manufacturing

opportunities and a strong long-term future for manufacturing in both advanced

and developing economies. The new era of manufacturing will be marked

by highly agile, networked enterprises that use information and analytics as

skillfully as they employ talent and machinery to deliver products and services

to diverse global markets. In advanced economies, manufacturing will continue

to drive innovation, exports, and productivity growth. In developing economies,

manufacturing will continue to provide a pathway to higher living standards.

As long as companies and countries understand the evolving nature of

manufacturing and act on the powerful trends shaping the global competitive

environment, they can thrive in this promising future.

The McKinsey Global Institute undertook the research and analysis that follows

to establish a clearer understanding of the role of manufacturing in advanced and

developing economies and the choices that companies in different manufacturing

industries make about how they organize and operate. We started with an

examination of how manufacturing has evolved to this point and then plotted

its likely evolution based on the key forces at work in the global manufacturing

sector. We also sought to understand the implications of these shifts for

companies and policy makers. Our research combined extensive macroeconomic

analyses with industry insights from our global operations experts. In addition,

we conducted “deep dive” analyses of select industries, including automotive,

aerospace, pharmaceuticals, food, steel, and electronics manufacturing.

We ind that manufacturing continues to matter a great deal to both developing

and advanced economies. We also see that it is a diverse sector, not subject

to simple, one-size-its-all approaches, and that it is evolving to include more

service activities and to use more service inputs. And we see that the role of

manufacturing in job creation changes as economies mature. Finally, we ind that

the future of manufacturing is unfolding in an environment of far greater risk and

uncertainty than before the Great Recession. And in the near term, the lingering

effects of that recession present additional challenges. To win in this environment,

companies and governments need new analytical rigor and foresight, new

capabilities, and the conviction to act.

Executive summary

2

ManufacTurInG MaTTers, buT ITs naTure Is chanGInG

Manufacturing industries have helped drive economic growth and rising living

standards for nearly three centuries and continue to do so in developing

economies. Building a manufacturing sector is still a necessary step in national

development, raising incomes and providing the machinery, tools, and materials

to build modern infrastructure and housing. Even India, which has leapfrogged

into the global services trade with its information technology and business

process outsourcing industries, continues to build up its manufacturing sector to

raise living standards—aiming to raise the share of manufacturing in its economy

from 16 percent today to 25 percent by 2022.1

how manufacturing matters

Globally, manufacturing output (as measured by gross value added) continues

to grow—by about 2.7 percent annually in advanced economies and 7.4 percent

in large developing economies (between 2000 and 2007). Economies such as

China, India, and Indonesia have risen into the top ranks of global manufacturing

and in the world’s 15 largest manufacturing economies, the sector contributes

from 10 percent to 33 percent of value added (Exhibit E1).

1 India’s national manufacturing policy, adopted in November 2011, calls for setting up national

manufacturing zones, creating 100 million manufacturing jobs, and raising manufacturing’s

contribution to GDP from 16 percent today to 25 percent by 2022.

exhibit e1

Large developing economies are moving up in global manufacturing

SOURCE: IHS Global Insight; McKinsey Global Institute analysis

1 South Korea ranked 25 in 1980.

2 In 2000, Indonesia ranked 20 and Russia ranked 21.

NOTE: Based on IHS Global Insight database sample of 75 economies, of which 28 are developed and 47 are developing.

Manufacturing here is calculated top down from the IHS Global Insight aggregate; there might be discrepancy with bottom-up

calculations elsewhere.

Top 15 manufacturers by share of global nominal manufacturing gross value added

Rank 1980 1990 2000 2010

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

United States

Germany

Japan

United Kingdom

France

Italy

China

Brazil

Spain

Canada

Mexico

Australia

Netherlands

Argentina

India

United States

Japan

Germany

Italy

United Kingdom

France

China

Brazil

Spain

Canada

South Korea1

Mexico

Turkey

India

Taiwan

United States

Japan

Germany

China

United Kingdom

Italy

France

South Korea

Canada

Mexico

Spain

Brazil

Taiwan

India

Turkey

United States

China

Japan

Germany

Italy

Brazil

South Korea

France

United Kingdom

India

Russia2

Mexico

Indonesia2

Spain

Canada

3Manufacturing the future: The next era of global growth and innovation

McKinsey Global Institute

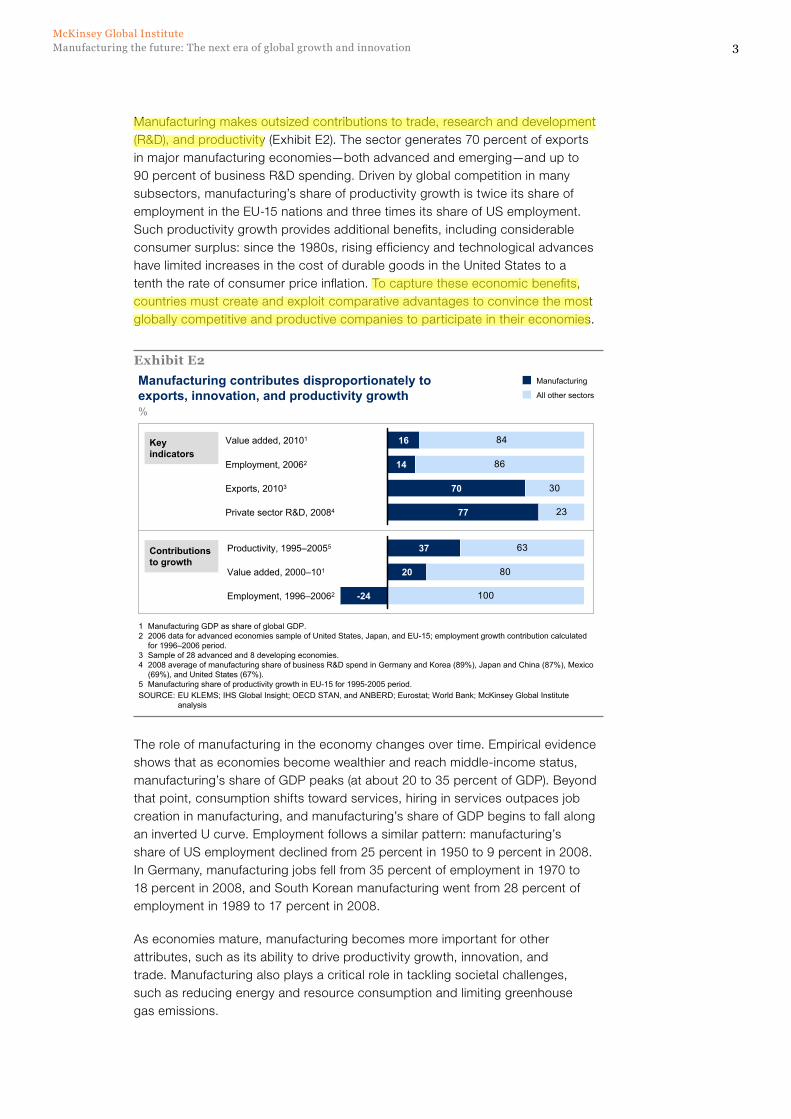

Manufacturing makes outsized contributions to trade, research and development

(R&D), and productivity (Exhibit E2). The sector generates 70 percent of exports

in major manufacturing economies—both advanced and emerging—and up to

90 percent of business R&D spending. Driven by global competition in many

subsectors, manufacturing’s share of productivity growth is twice its share of

employment in the EU-15 nations and three times its share of US employment.

Such productivity growth provides additional beneits, including considerable

consumer surplus: since the 1980s, rising eficiency and technological advances

have limited increases in the cost of durable goods in the United States to a

tenth the rate of consumer price inlation. To capture these economic beneits,

countries must create and exploit comparative advantages to convince the most

globally competitive and productive companies to participate in their economies.

The role of manufacturing in the economy changes over time. Empirical evidence

shows that as economies become wealthier and reach middle-income status,

manufacturing’s share of GDP peaks (at about 20 to 35 percent of GDP). Beyond

that point, consumption shifts toward services, hiring in services outpaces job

creation in manufacturing, and manufacturing’s share of GDP begins to fall along

an inverted U curve. Employment follows a similar pattern: manufacturing’s

share of US employment declined from 25 percent in 1950 to 9 percent in 2008.

In Germany, manufacturing jobs fell from 35 percent of employment in 1970 to

18 percent in 2008, and South Korean manufacturing went from 28 percent of

employment in 1989 to 17 percent in 2008.

As economies mature, manufacturing becomes more important for other

attributes, such as its ability to drive productivity growth, innovation, and

trade. Manufacturing also plays a critical role in tackling societal challenges,

such as reducing energy and resource consumption and limiting greenhouse

gas emissions.

exhibit e2

Manufacturing contributes disproportionately to exports, innovation, and productivity growth

SOURCE: EU KLEMS; IHS Global Insight; OECD STAN, and ANBERD; Eurostat; World Bank; McKinsey Global Institute

analysis

%

1 Manufacturing GDP as share of global GDP.

2 2006 data for advanced economies sample of United States, Japan, and EU-15; employment growth contribution calculated

for 1996–2006 period.

3 Sample of 28 advanced and 8 developing economies.

4 2008 average of manufacturing share of business R&D spend in Germany and Korea (89%), Japan and China (87%), Mexico

(69%), and United States (67%).

5 Manufacturing share of productivity growth in EU-15 for 1995-2005 period.

84

86

30

23

Exports, 20103 70

Employment, 20062 14

16Value added, 20101

77Private sector R&D, 20084

Manufacturing

All other sectors

63

80

100

Value added, 2000–101 20

Productivity, 1995–20055 37

-24Employment, 1996–20062

Contributions to growth

Key indicators

4

As advanced economies recover from the Great Recession, hiring in

manufacturing may accelerate. And the most competitive manufacturing nations

may even raise their share of net exports. Whether such a rebound can be

sustained, however, depends on how well countries perform on a range of

fundamental factors that are important to manufacturing industries: access to

low-cost or high-skill labor (or both); proximity to demand; eficient transportation

and logistics infrastructure; availability of inputs such as natural resources or

inexpensive energy; and proximity to centers of innovation.

Manufacturers in advanced economies will continue to hire workers, both in

production and non-production roles, such as design and after-sales service.

But in the long run, manufacturing’s share of employment will continue to be

under pressure in advanced economies. This is due to ongoing productivity

improvements, the continued growth of services as a share of the economy, and

the force of global competition, which pushes advanced economies to specialize

in more high-skill activities. Manufacturing cannot be expected to create mass

employment in advanced economies on the scale that it did decades ago.

Manufacturing is not monolithic

In order to craft effective business and policy strategies in manufacturing, it

is important to start with an understanding of the fundamental differences

between manufacturing industries. We identify ive broad segments that vary

signiicantly in their sources of competitive advantage and how different factors

of production inluence where companies build factories, carry out R&D, and go

to market. Depending on the industry, factors such as energy and labor costs or

proximity to talent, markets, and partners such as suppliers and researchers have

greater weight (Exhibit E3). Indeed, many manufacturing companies, including

in industries such as automotive and aerospace, are already concerned about a

skill shortage.

We ind this segmentation a helpful way to see the global nature of different

industries, anticipate where manufacturing activities are most likely to take place,

and understand the role of innovation in various industries. For companies, the

segmentation helps to explain the evolution of different parts of their operations,

from individual business units to various stages of their supply chains. The

segmentation can also clarify the differences between segments of the same

industry—why suppliers of automotive electronic components respond to

very different dynamics than suppliers of mechanical parts, for example. The

framework also helps explain why the needs and factors of success vary even

within the same industry; the carmaker that emphasizes its technological edge

and precision engineering has very different requirements than the producer of

low-cost models.

5Manufacturing the future: The next era of global growth and innovation

McKinsey Global Institute

The largest group is global innovation for local markets, which is composed of

industries such as chemicals (including pharmaceuticals); automobiles; other

transportation equipment; and machinery, equipment, and appliances. These

industries accounted for 34 percent of the $10.5 trillion (nominal) in global

manufacturing value added in 2010. Industries in this group are moderately to

highly R&D-intensive and depend on a steady stream of innovations and new

models to compete. Also, the nature of their products is such that production

facilities are distributed close to customers to minimize transportation costs. The

footprints of these industries may also be inluenced by regulatory effects (e.g.,

safety standards) and trade agreements.

Regional processing industries are the second-largest manufacturing group

globally, with 28 percent of value added, and the largest employer in advanced

economies. The group includes food processing and other industries that locate

close to demand and sources of raw materials; their products are not heavily

traded and not highly dependent on R&D, but they are highly automated. Energy-

and resource-intensive commodities such as basic metals make up the third-

largest manufacturing group. For these companies, energy prices are important,

but they are also tied to markets in which they sell, due to high capital and

transportation costs.

Global technology industries such as computers and electronics depend

on global R&D and production networks; the high value density of products

such as electronic components and mobile phones, make them economically

transportable from production sites to customers around the globe. Finally, labor-

intensive tradables, such as apparel manufacturing, make up just 7 percent of

exhibit e3

Group

Furniture, jewelry, toys, other

Textiles, apparel, leather

Medical, precision, and optical

Semiconductors and electronics

Computers and office machinery

Basic metals

Mineral-based products

Paper and pulp

Refined petroleum, coke, nuclear

Wood products

Printing and publishing

Food, beverage, and tobacco

Fabricated metal products

Rubber and plastics products

Machinery, equipment, appliances

Electrical machinery

Other transport equipment

Motor vehicles, trailers, parts

Chemicals

Value density

Trade intensity

Energy intensity

Capital intensity

Labor intensity

R&D intensityIndustry

Manufacturing is diverse: We identify

five broad groups with very different

characteristics and requirements

SOURCE: IHS Global Insight; OECD; Annual Survey of Manufacturers (ASM) 2010; US 2007 Commodity Flow Survey;

McKinsey Global Institute analysis

High

Upper-middle

Lower-middle

Low

% of global

manufacturing

value added

Labor-intensive tradables

Global technologies/ innovators

Energy-/ resource-intensive commodities

Regional processing

Global innovation for local markets

7

9

22

28

34

6

value added. The group’s goods are highly tradable and companies require low-

cost labor. Production is globally traded and migrates to wherever labor rates are

low and transportation is reliable.

We see that the ive segments make very different contributions to the global

manufacturing sector and have evolved in dramatically different ways. Industries

in just two of the ive segments—regional processing and global innovation

for local markets—together make up nearly two-thirds of manufacturing value

added and more than half of manufacturing employment, both in advanced and

emerging economies. Two other industry groups—global technologies and labor-

intensive tradables—are both highly traded globally, but exist at opposite ends of

the skill spectrum. Together, they make up only 16 percent of value added in both

advanced and emerging economies.

The evolution of these manufacturing groups has resulted in some specialization

across different types of economies. Advanced economies retain a lead in the

global innovation for local markets group and are less competitive in labor-

intensive manufacturing. In 2010, advanced economies ran a $726 billion surplus

in goods such as automobiles, chemicals, pharmaceuticals, and machinery, and

had a $342 billion trade deicit in labor-intensive tradables. While labor-intensive

industries in advanced economies have shed 37 percent of their jobs since 1995,

regional processing industries (e.g., food manufacturing) have lost only 5 percent

of their employment (Exhibit E4).

exhibit e4

Manufacturing employment in advanced economies has declined across all groups but has fallen most in the labor-intensive tradables group

SOURCE: EU KLEMS; OECD; McKinsey Global Institute analysis

100

90

85

80

75

70

65

0

Manufacturing overall

2000999897

95

04 05 06 2007

Global innovation forlocal markets

Regional processing

Global technologies/ innovators

Energy- and resource-Intensive commodities

Labor-intensivetradables

030201

105

961995

Manufacturing employment by group in selected advanced economies, 1995–20071

Index: 1995 = 100

Share of manufacturing employment%

1995

33

28

8

14

16 12

37

30

8

13

20072000

35

29

9

14

14

1 Sample of 17 advanced economies: EU-15, Japan, and United States.

NOTE: Numbers may not sum due to rounding.

7Manufacturing the future: The next era of global growth and innovation

McKinsey Global Institute

The distinction between manufacturing and services has blurred

Manufacturing has always included a range of activities in addition to production.

Over time, service-like activities—such as R&D, marketing and sales, and

customer support—have become a larger share of what manufacturing

companies do. More than 34 percent of US manufacturing employment is in such

service-like occupations today, up from about 32 percent in 2002. Depending on

the segment, 30 to 55 percent of manufacturing jobs in advanced economies are

service-type functions (Exhibit E5), and service inputs make up 20 to 25 percent

of manufacturing output.

Manufacturing companies rely on a multitude of service providers to produce

their goods. These include telecom and travel services to connect workers in

global production networks, logistics providers, banks, and IT service providers.

We estimate that 4.7 million US service sector jobs depend on business from

manufacturers. If we count those and one million primary resources jobs related

to manufacturing (e.g., iron ore mining), total manufacturing-related employment in

the United States would be 17.2 million, versus 11.5 million in oficial data in 2010.

Including outsourced services, we ind that services jobs in US manufacturing-

related employment now exceed production jobs—8.9 million in services versus

7.3 million in production.

Just as manufacturing creates demand for services inputs, services also create

demand for manufactured goods. For every dollar of output, US manufacturers

use 19 cents of service inputs, creating $900 billion a year in demand for

services, while services create $1.4 trillion in US manufacturing demand. In China

manufacturing creates $500 billion in services demand, and services demand

$600 billion a year in manufactured goods. And while manufacturing drives more

than 80 percent of exports in Germany, services and manufacturing contribute

nearly equal shares of value added to the country’s total exports.

exhibit e5

45

60

69

69

70

Labor-

intensive

tradables

30

Energy-/

resource-

intensive

commodities

31

Regional

processing31

Global

innovation for

local markets

40

Global

technologies/

innovators

55

Service type activities already make up 30 to 55 percentof manufacturing employment

SOURCE: US Bureau of Labor Statistics (BLS); McKinsey Global Institute analysis

10037

63

TotalService

type

Manufac-

turing

type

Manufacturing occupations in the United States in 20101

%

Service type

Manufacturing type

1 Manufacturing-type occupations refer to early-stage manufacturing and final assembly. Service occupations include R&D,

procurement, distribution, sales and marketing, post-sales service, back-office support, and management.

8

The role of manufacturing in job creation is changing

Manufacturing’s role in job creation shifts over time as manufacturing’s share of

output falls and as companies invest in technologies and process improvements

that raise productivity. Hiring patterns within manufacturing also change, with

hiring skewed toward high-skill production jobs and both high- and low-skill

service jobs, as hiring in production overall slows. At the same time, growth in

service-sector hiring accelerates, raising that sector’s share of employment. This

pattern holds across advanced economies and will hold for today’s developing

economies as they become wealthier. As manufacturing’s share of national output

falls, so does its share of employment, following an inverted U curve (Exhibit E6).

We ind that manufacturing job losses in advanced economies have been

concentrated in labor-intensive and highly tradable industries such as apparel

and electronics assembly. However, overall in the United States, trade and

outsourcing explain only about 20 percent of the 5.8 million manufacturing

jobs lost during the 2000-10 period; more than two-thirds of job losses can be

attributed to continued productivity growth, which has been outpacing demand

growth for the past decade.

Even strong manufacturing exporting nations have shed jobs in the past decade.

Germany’s manufacturing employment fell by 8 percent and South Korea’s by

11 percent. Our analysis indicates that while manufacturing output will continue

to rise and manufacturers will hire more high-skill production workers and

workers in non-production roles, overall manufacturing employment will remain

under pressure in advanced economies; if current trends persist, manufacturing

employment in advanced economies could fall from 45 million jobs today to fewer

than 40 million by 2030.

exhibit e6

SOURCE: GGDC 10-Sector Database: “Structural change and growth accelerations in Asia and Latin America: A new sectoral

data set,” Cliometrica, volume 3, Issue 2, 2009; McKinsey Global Institute analysis

Manufacturing’s share of total employment falls as the economy grows wealthier, following an inverted U pattern

0

5

10

15

20

25

30

35

40

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Manufacturing employment% of total employment

GDP per capita1990 PPP-adjusted dollars1

Germany

India

Mexico

Taiwan

United States

South Korea

Japan

United Kingdom

1 Adjusted using the Geary-Khamis method to obtain a 1990 international dollar, a hypothetical currency unit that allows

international comparisons adjusted for exchange rates and purchasing power parity (PPP).

9Manufacturing the future: The next era of global growth and innovation

McKinsey Global Institute

Manufacturing has been regarded as a source of “better” jobs than services,

offering higher levels of compensation. However, we ind that this distinction is

far less clear today. It is true that in aggregate, average compensation is higher

in manufacturing than in services (17 percent higher in 2006, measured as total

labor compensation including social security payments). But when manufacturing

and service jobs in industries that have similar factor intensity are compared, the

wage differences are small. The gap in average pay between manufacturing and

services also is seen in wage distribution. Manufacturing has a disproportionately

high number of well-paying jobs in the United States (700,000 more) compared

with services and a disproportionately small number of low-paying jobs (720,000

fewer). These wage differences may relect trade and offshoring effects,

unionization, and legacy wage arrangements.

new OPPOrTunITIes arIse In a MOre cOMPlex and

uncerTaIn envIrOnMenT

An exciting new era of global manufacturing is ahead—driven by shifts in

demand and by innovations in materials, processes, information technology,

and operations. The prospect is for a more “global” manufacturing industry, in

which developing economies are the source of new customers as well as the

source of low-cost production. It can also be a time of rapid innovation, based on

new technologies and methods. However, these opportunities arise in a global

environment that is strikingly different from that of the pre-recession period, with

shifts in the cost and availability of factor inputs (e.g., labor and natural resources)

and rising complexity, uncertainty, and risk.

Some forces are already being felt: the shift of global demand toward developing

economies, the proliferation of products to meet fragmenting customer demand,

the growing importance of value-added services, and rising wages in low-cost

locations. Other trends are now becoming more pronounced, such as a growing

scarcity of technical talent to develop and run manufacturing tools and systems,

and the use of greater intelligence in product design and manufacturing to boost

resource eficiency and track activity in supply chains.

demand is shifting and fragmenting

The shift in global demand for manufactured goods is happening at an

accelerating pace, driven by the momentum of emerging economies. In China,

per capita income for more than one billion citizens has doubled in just 12 years,

an achievement that took the United Kingdom 150 years with just nine million

inhabitants as it industrialized. And China is not alone. With industrialization and

rising productivity spreading to other parts of Asia and Africa, some 1.8 billion

people are expected to join the global consuming class by 2025, expanding

markets for everything from mobile phones to refrigerators and soft drinks.

These new consumers often require very different products to meet their

needs, with different features and price points, forcing manufacturers to offer

more varieties and SKUs (stock-keeping units). At the same time, customers

in more established markets are demanding more variety and faster product

cycles, driving additional fragmentation. Finally, customers increasingly look to

manufacturers for services, particularly in business-to-business (B2B) markets,

creating an additional demand shift.

10

Innovations create new possibilities

A rich pipeline of innovations promises to create additional demand and drive

further productivity gains across manufacturing industries and geographies. New

technologies are increasing the importance of information, resource eficiency,

and scale variations in manufacturing. These innovations include new materials

such as carbon iber components and nanotechnology, advanced robotics and

3-D printing, and new information technologies that can generate new forms of

intelligence, such as big data and the use of data-gathering sensors in production

machinery and in logistics (the so-called Internet of Things).

Across manufacturing industries, the use of big data can make substantial

improvements in how companies respond to customer needs and how they run

their machinery and operations. These enormous databases, which can include

anything from online chatter about a brand or product to real-time feeds from

machine tools and robots, have great potential for manufacturers—if they can

master the technology and ind the talent with the analytical skills to turn data into

insights or new operating improvements.

Important advances are also taking place in development, process, and

production technologies. It is increasingly possible to model the performance of a

prototype that exists only as a CAD drawing. Additive manufacturing techniques,

such as 3-D printing, are making prototyping easier and opening up exciting

new options to produce intricate products such as aerospace components and

even replacement human organs. Robots are gaining new capabilities at lower

costs and are increasingly able to handle intricate work. The cost of automation

relative to labor has fallen by 40 to 50 percent in advanced economies since

1990. In addition, advances in resource eficiency promise to cut use of materials

and energy (i.e., green manufacturing). An emerging “circular” economy will help

stretch resources through end-of-life recycling and reuse.

an uncertain environment complicates strategy

Even as new markets and technologies open up fresh opportunities for

manufacturing companies, a series of changes in the environment creates new

challenges and uncertainty. The growth of global value chains has increased

exposure of many companies to the impact of natural disasters, as Japan’s

2011 earthquake and Thailand’s looding have demonstrated. And after years

of focusing on optimizing their value chains for low cost, many manufacturing

companies are being forced to reassess the balance between eficiency gains

from globally optimized value chains and the resilience of less fragmented and

dispersed operations.

Catastrophic events are not the only sources of uncertainty facing manufacturing

companies. Manufacturers also face luctuating demand and commodity prices,

currency volatility, and various kinds of supply-chain disruptions that chip away

at proits, increase costs, and prevent organizations from exploiting market

opportunities. Price increases in many commodities in the past decade have

all but erased the price declines of the past century. Volatility in raw materials

prices has increased by more than 50 percent in recent years and is now

at an all-time high.2 Long-term shifts in global demand are accompanied by

2 Resource revolution: Meeting the world’s energy, materials, food, and water needs, McKinsey

Global Institute, November 2011 (www.mckinsey.com/mgi).

11Manufacturing the future: The next era of global growth and innovation

McKinsey Global Institute

signiicant upswings and downswings in demand, driven by changes in customer

preferences, purchasing power, and events such as quality problems.

Government action is another source of uncertainty. Governments continue to

be active in manufacturing policy, even as the path of economic growth and

the outlook for iscal and inancial market stability remain uncertain. All too

often government action (and lack of action) simply adds to uncertainty. This is

the case with unclear energy and carbon emissions policies. And, while trade

barriers continue to fall around the world with the proliferation of preferential trade

agreements, there are many exceptions. Government interventions persist—

sometimes with protectionist measures—in industries such as autos and steel,

which many governments regard as national priorities for employment and

competitiveness. Steel tariffs have fallen over the past 20 years, but governments

continue to favor domestic steel production in other ways.

As the world works through the aftermath of the inancial crisis with household,

banking, and public sector deleveraging; as rebalancing of trade propels

exchange rate swings; and as the momentum of emerging economies puts

friction on natural resource prices, uncertainty will prevail.

Implications for footprints, investment, and competition

Taken together, the opportunities and challenges described here have the

potential to shift the basis for how companies pursue new markets and how they

will expand their production and R&D footprints. Not only will companies compete

in different ways and build new production and supply networks as they respond

to new kinds of demand and forces of change in the global environment, but

nations also will learn to compete on a wider range of factors than labor cost or

tax rates.

For example, rather than simply responding to changing labor rates,

manufacturers will need to consider the full range of factor inputs as they weigh

the trade-offs between where they produce their goods and where they sell

them. Much has been made of rising Chinese labor costs and falling wages in the

United States. However, for most manufacturers, the more pressing workforce

issue likely will be the struggle to ind well-trained talent. Manufacturing is

increasingly high-tech, from the factory loor to the back ofices where big data

experts will be analyzing trillions of bytes of data from machinery, products in

the ield, and consumers. The global supply of high-skill workers is not keeping

up with demand, and the McKinsey Global Institute projects a potential shortage

of more than 40 million high-skill workers by 2020. Aging economies, including

China, will face the greatest potential gaps.

Global competition will also be affected by demand shifts and changes in the

cost and availability of various supply factors. The global footprint of regional

processing industries such as food processing will naturally follow demand,

but for other industries such as automobiles and machinery, transportation and

logistics costs or concerns about supply-chain resilience may trump labor costs.

Assessing the future pattern of costs and availability of resources such as raw

materials and energy has become more complex. Resource prices rose rapidly

before the recession and remain high by 20th-century standards. Yet access

to previously untapped sources, such as shale gas in the United States, can

change the relative costs of energy inputs and promote domestic production as

12

a substitute for imports. Then again, many energy-intensive processing industries

such as steel tend to be located near demand, and their footprints are “sticky”

due to high capital investments and high exit costs. In many industries, market

proximity, capital intensity, and transport and logistics matter as much as energy

and labor costs.

Finally, to compete, companies also may need to consider access to centers of

innovation. This applies to many industries, not just those that make high-tech

products. In the United States, for example, a new auto industry technology

cluster is emerging around South Carolina’s auto factories.

For companies, the new mindset for making footprint decisions is not just about

where to locate production, but also who the competitors are, how demand is

changing, how resilient supply chains have to be, and how shifts in factor costs

affect a particular business. As new geographic markets open up, companies

will be challenged to make location trade-offs in a highly sophisticated, agile way.

They will need to weigh proximity to markets and sources of customer insights

against the costs and risks in each region or country.

On their part, policy makers will need to recognize that every country is going

to compete for global manufacturing industries. Governments will need to invest

in building up their comparative advantages—or in acquiring new ones—to

increase their appeal to globally competitive and productive companies. As

governments compete, they can help tilt the decisions for these companies by

taking a comprehensive view of what multinational manufacturing corporations

need: access to talent, reliable infrastructure, labor lexibility, access to necessary

materials and low-cost energy, and other considerations beyond investment

incentives and attractive wage rates.

ManufacTurers wIll need deTaIled InsIGhTs InTO

new OPPOrTunITIes, aGIlITy, and new caPabIlITIes

To take advantage of emerging opportunities and navigate in a more challenging

environment, manufacturing companies need to develop new muscles. They

will be challenged to organize and operate in fundamentally different ways to

create a new kind of global manufacturing company—an organization that more

seamlessly collaborates around the world to design, build, and sell products

and services to increasingly diverse customer bases. These organizations will

be intelligent and agile enterprises that harness big data and analytics, and

collaborate in ecosystems of partners along the value chain, to drive decision

making, enhance performance, and manage complexity. They will have the vision

and commitment to place the big bets needed to exploit long-term trends such

as rising demand in emerging markets, but also will use new tools to manage the

attendant risks and near-term uncertainties.

conventional strategies will be increasingly risky; granularity is key

Companies that stick to business-as-usual approaches will be increasingly at risk.

Manufacturers will no longer succeed by “copying and pasting” old strategies into

new situations. They must develop a granular understanding of the world around

them—and plan the operations strategy to compete in it.

First, manufacturers must understand the dynamics of their segments (e.g., their

labor, energy, or innovation intensity), and how new trends play against those