Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008 NON-LINEAR WORLD LINEAR MODELS? Nasir...

21

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008 NON-LINEAR WORLD LINEAR MODELS? Nasir Afaf Disclaimer: The views expressed here are those of the author and not Commerzbank AG

-

Upload

vivien-walters -

Category

Documents

-

view

231 -

download

2

Transcript of Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008 NON-LINEAR WORLD LINEAR MODELS? Nasir...

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

NON-LINEAR WORLD

LINEAR MODELS?Nasir Afaf

Disclaimer:

The views expressed here are those of the author and not Commerzbank AG

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

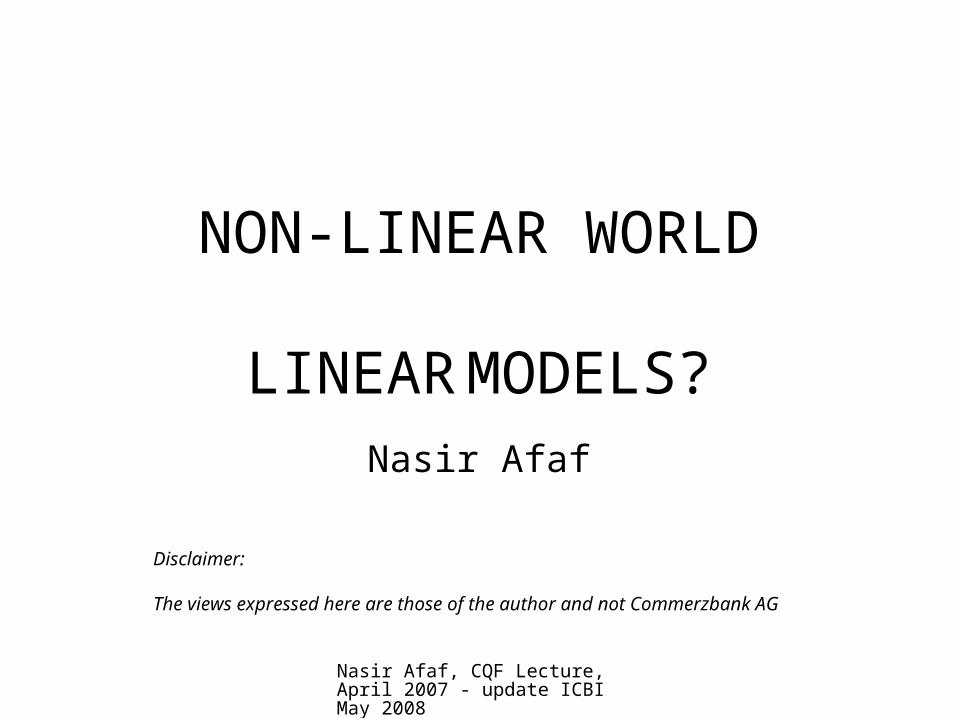

Pyramid of Modern Finance

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Real Markets

• Different classes of market participants

• Characterised by different– End objectives– Time horizons– Risk appetite– Response to market dynamics

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Market Participants

• Corporates – hedgers

• Market making institutions

• Investors:– Hedge funds/Proprietary Trading Desks– Real money managers – asset managers,

pension funds etc– CTA’s– Retail

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

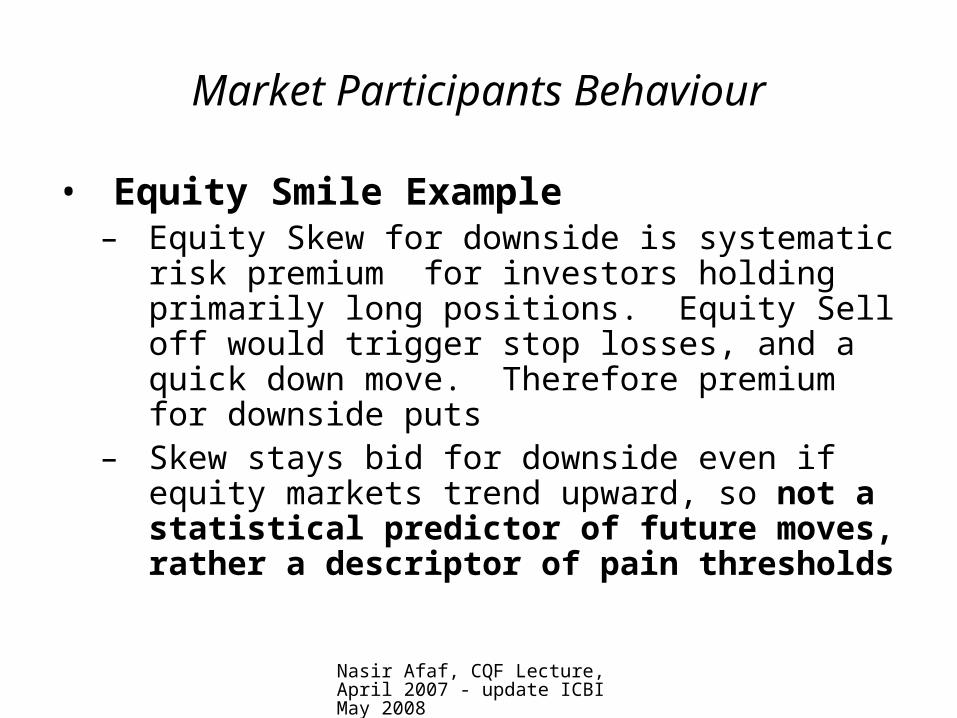

Market Participants Behaviour

• Equity Smile Example– Equity Skew for downside is systematic risk

premium for investors holding primarily long positions. Equity Sell off would trigger stop losses, and a quick down move. Therefore premium for downside puts

– Skew stays bid for downside even if equity markets trend upward, so not a statistical predictor of future moves, rather a descriptor of pain thresholds

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

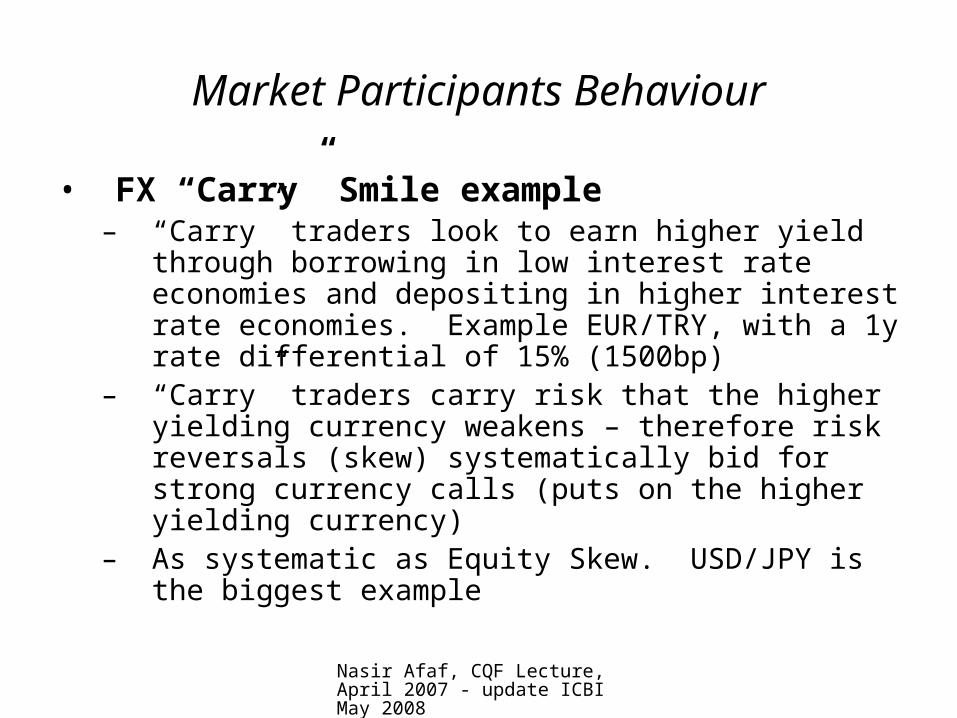

Market Participants Behaviour

• FX “Carry” Smile example– “Carry” traders look to earn higher yield through

borrowing in low interest rate economies and depositing in higher interest rate economies. Example EUR/TRY, with a 1y rate differential of 15% (1500bp)

– “Carry” traders carry risk that the higher yielding currency weakens – therefore risk reversals (skew) systematically bid for strong currency calls (puts on the higher yielding currency)

– As systematic as Equity Skew. USD/JPY is the biggest example

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Market Participants Behaviour

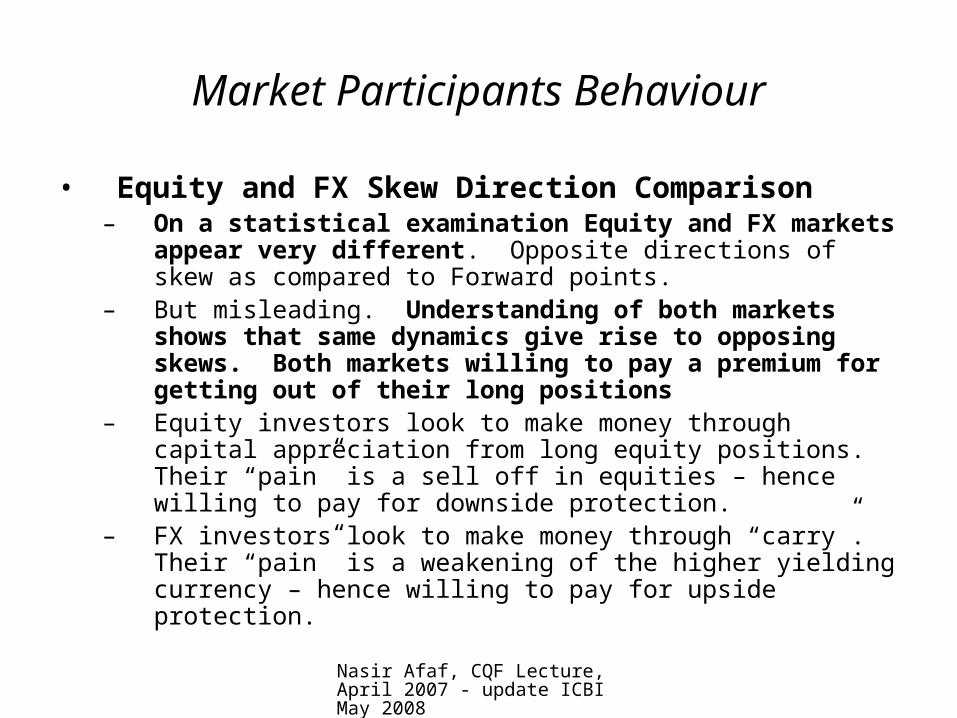

• Equity and FX Skew Direction Comparison– On a statistical examination Equity and FX markets

appear very different. Opposite directions of skew as compared to Forward points.

– But misleading. Understanding of both markets shows that same dynamics give rise to opposing skews. Both markets willing to pay a premium for getting out of their long positions

– Equity investors look to make money through capital appreciation from long equity positions. Their “pain” is a sell off in equities – hence willing to pay for downside protection.

– FX investors look to make money through “carry”. Their “pain” is a weakening of the higher yielding currency – hence willing to pay for upside protection.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Markets are non-linear – the weak part

• Interaction amongst market participants is key. He (unknown) did this, so I do that…..

• To understand how that interaction occurs you have to understand each type of participant.

• For example, asset managers do not adjust their holdings frequently. Certain types of hedge funds may do (“Renaissance”?)

• This gives rise to price dynamics in short term.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Markets are non-linear – the strong part

• Interaction is played out against a backdrop of liquidity, credit lines, levels of permitted risk, introduction of new financial instruments

• This generates price dynamics. Perfectly random to a pure statistician with no insight into what constitutes a market. Structured randomness for an insightful market participant. Information and insight is the key.

• Resulting price dynamics strongly feed back into liquidity, credit lines, levels of permitted risk, introduction of new financial instruments. This never ending feedback loop is what we call a market.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Using Derivatives Models

• Model first, or think first

• Linear SDE etc…

• Linear models highly idealised – though useful. Easiest to model.

• Real pricing is non-linear. Price can never be independent of risk limits, and the risk in your book. You always have to make mental adjustments.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

So who is a Derivatives Trader

• Linear model• Non-linear markets with feedback effects• Non-linear pricing with respect to mental

adjustments to account for risk in book, and risk limits etc

• A derivatives trader is a non-linear control hired by the bank to trade non linear instruments valued using linear models. This non-linear control is generally far from optimal!

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Ingredients in non-linear control

• Specific

– Mkt risk limits– Credit limits– Performance year to date!– Current book profile– Availability (and understanding!) of “useful

models”

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Ingredients in non-linear control

• General (Market Specific)

– Regulatory framework– Liquidity (Depth of market)– Transaction costs– Aggregate “market maker” positioning

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Missing ingredient in models

• Liquidity– Derivatives Models assume an infinite sea of

liquidity– Economic concepts of liquidity?– My concept of liquidity: All price changes

are due to the ebb and flow of liquidity. It is only meaningful to speak of liquidity at a certain price level and at a certain time. Every price movement is a liquidity squeeze.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Feedback effects

• Feedback– Derivatives Models (“no arbitrage”) valuations

are based on hedging recipes– Superiority of a model based on how well

“recipe” can be executed in practise– Can divide products/models into different

classes. Easy to hedge recipe (“fwd”), difficult to hedge recipe (“short date digital”).

– Market risk aggregation due to popularity of products/ideas/structures.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Feedback from derivatives “recipes” into liquidity

• Pyramid of modern finance (slide 1). Not so one way!

• Each popular product creates its own feedback

• Ever changing nature of liquidity, creates new opportunities, and more products

• Sometimes best way to trade cash is to be on top of complex exotics (“know the top of the pyramid, trade the base”)

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Modeling liquidity - 1

• Tangible Inputs– Tangibles (available to all)

• Bid-offer spreads in market• Volatility levels and other such information• “Sea” of all available market data• “Theory of everything model” or specific

“phenomenological model” from observable market data. Trade-offs between model choices.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Modeling liquidity - 2

• Intangibles– Effective “information set” and analysis– Modelling “interaction”– Modelling non-linear feedback– Distinction between market-makers and

market takers. Claim: over emphasised. Market makers are often market takers. “Inventory management” is best analogy for market making activity.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

Successful liquidity modelling

• Any reasonable liquidity model (understanding) must be dynamic rather than static.

• Be able to explain some phenomenon not amenable to traditional approaches (“wisdom” rather than “proof”)

• Must then imply a dynamical statement for price dynamics – and produce observed “statistical signatures”

• As in “chess” feedback and adaptive responses, tactical and strategic, must appear. These are subjective ingredients.

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

What it comes down to

• Derivatives valuations cannot be expected to be unique.

• Different “information set”, different “subjective analysis of interaction”, different “strategy”, for each participant is key.

• Traders attempt to “control” this non-linearity heuristically. At least the thoughtful (successful?) ones do!

Nasir Afaf, CQF Lecture, April 2007 - update ICBI May 2008

What it comes down to – BIG PICTURE

• All comes down to “predicting” and modeling Order Flow.

• Order Flow is driven by liquidity dynamics, which then translates into price changes.

• Shorter term as opposed to longer term positioning.

• Modeling becomes “Cause and Effect” rather than “Blind Statistical descriptions”