NAS and operating performance FINAL - University of … · [email protected] W....

60

1 Non-Audit Services and Improvements in Clients’ Operating Performance and Risk Management William A. Ciconte III University of Florida [email protected] W. Robert Knechel ‡ University of Florida [email protected] Michael A. Mayberry University of Florida [email protected] August 2014 _____________________________________________________________________________________ ‡ Corresponding author: P.O. Box 117166, 325 Gerson Hall, Gainesville, FL 32611-7166. The authors appreciate the helpful comments of Matthew Ege, Devin Williams, Ying Zhou, and participants of the 2013 EARNet Symposium Ph.D. round table.

Transcript of NAS and operating performance FINAL - University of … · [email protected] W....

1

Non-Audit Services and Improvements in Clients’ Operating Performance and Risk

Management

William A. Ciconte III University of Florida

W. Robert Knechel‡ University of Florida

Michael A. Mayberry University of Florida

August 2014 _____________________________________________________________________________________ ‡Corresponding author: P.O. Box 117166, 325 Gerson Hall, Gainesville, FL 32611-7166. The authors appreciate the helpful comments of Matthew Ege, Devin Williams, Ying Zhou, and participants of the 2013 EARNet Symposium Ph.D. round table.

2

Non-Audit Services and Improvements in Clients’ Operating Performance and Risk

Management

Abstract

We examine whether, and when, non-audit services (NAS) purchased jointly with the audit

provide economic value to clients through improvements in operating performance and risk

management. Our investigation is important as it contributes to the ongoing debate between

critics and proponents of the joint provision of auditing and NAS. Using DuPont analysis, we

find NAS are positively related to subsequent increases in operating performance, consistent

with NAS providing access to human capital and other organizational resources. We further find

that NAS are negatively related to future operating risk, indicating that NAS enhance client

firms’ risk management. We find no evidence of NAS that are related to improvements in

operating performance increasing earnings management. Regulators considering whether to

further restrict NAS provided by a client’s auditor should exercise caution as restrictions could

result in unintended, negative consequences as they would be forcing firms to unbundle the

purchase of such services.

Key words: non-audit services; operating performance; risk; audit quality

JEL Classification: M41; M42; L84

3

Non-Audit Services and Improvements in Clients’ Operating Performance and Risk

Management

I. Introduction

The topic of auditor-provided non-audit services (NAS) is one of the most highly studied

issues affecting the audit profession (Simunic [1984], Palmrose [1986]). While the volume of

research is large, the focus has primarily been on one of two aspects of NAS that might influence

the audit directly: (1) economic bonding that reduces auditor independence (a cost) or (2)

knowledge spillovers that improve the quality or efficiency of the audit (a benefit). While it is

certainly valid to consider the cost and benefits of NAS as they influence the audit itself, little

research has addressed the benefits of NAS to the organization purchasing those services

independent of the effect on the audit.1 An audit firm’s expertise could have benefits to the

client that go beyond knowledge spillovers during the audit itself. To the extent that auditor-

provided NAS are the subject of regulation, a full cost/benefit tradeoff should consider the effect

of NAS on the organization as well as the effect on the audit process.2

In this paper, we take the perspective that economically-beneficial NAS may lead to at

least two positive and related outcomes: (1) improvements in overall performance and (2) a

reduction of future risk. The former connects NAS to the operations of an organization, while

the latter connects NAS to the risk management and internal control function of an organization.

Improvements in operating performance can arise because the company has improved access to

1 Theory also states that there are potential benefits that will accrue to the NAS production process from the provision of the audit (Simunic [1984]). However, we do not perform such an analysis due to data limitations. 2 We focus on NAS purchased from a firm’s auditor because we cannot observe purchases of NAS provided by firms other than the auditor. Our focus is not on the decision whether or not to purchase NAS from the auditor. Instead, we examine the costs and benefits of the NAS given their joint production. With respect to the decision to purchase multiple services from a single provider, extant literature posits that obtaining additional services from a firm with which the client is familiar can lead to the selection of higher quality services because the client has more information about the provider (Gustafson and Di Marco [1973], Gallouj [1997]). Another potential reason for a firm to purchase multiple services from a single provider is that by bundling the services together the provider can offer a discount relative to other service providers, increasing consumer surplus (Guiltinan [1987]).

4

reliable and precise information on which to make investment decisions,3 better access to human

capital and expertise not available internally, or increased tax-efficiency in the firm’s supply

chain. Improvements in risk management can flow from experience navigating unfamiliar

markets, compliance consulting, more effective information collection and dissemination, and

greater protection from downside risk due to enhanced internal controls. On the latter point,

while the Public Company Accounting Oversight Board (PCAOB) requires an audit opinion on

the internal control over financial reporting for SEC registrants, the benefits of NAS for internal

control are likely to extend significantly beyond the PCAOB’s focus.

Since the Foreign Corrupt Practices Act of 1977, and reinvigorated by the Committee on

Sponsoring Organizations (“COSO”) Framework in 1992 and the Sarbanes-Oxley Act of 2002

(“SOX”), both client organizations and their public accounting firms have increasingly been

cognizant of the need to manage business risk (Knechel [2007]). Risk management, through

differing types of assurance, information collection, and controls shields firms from downside

outcomes and improves the allocation of resources towards strategic objectives within the firm,

thus potentially improving performance and smoothing volatility (Baxter et al. [2013]). We

therefore expect that the incremental assurance, better information, access to technical experts,

identification of risks, and improvements in control systems arising from NAS should lead to

subsequent improvements in operating performance and decreases in operating risk. For

example, assurance provided by NAS with respect to acquisitions or pension plans can provide

better information to managers so they can better forecast future funds flows. Similarly, tax

consulting can yield a greater understanding of international operations and the tax and reporting

3 This point refers to the general information environment of an organization in contrast to the actual accounting system used by a client. Management advisory services can be related to either the context or quality of information (AICPA [1992]). Examples include supply chain strategies or methods for evaluating internal investments. Prior research documents a similar link between the audit and a client’s investment opportunity set (Cahan et al. [2008]).

5

consequences of repatriating funds allowing managers to improve international expansion

decisions while decreasing the risk of failure. While assessing control risk and considering

business risk are part of the financial statement audit, it is unlikely that the audit process alone

fully complements a client firm’s risk management function because the audit is highly-

structured, compliance-driven, and commoditized (Knechel [2007]). However, an organization’s

discretionary choices related to assurance-, control-, and information system-related NAS

represent deliberate choices beyond the mandated audit framework.4

While we argue that NAS are likely to be embedded in a firm’s risk management

function and framework, there are also reasons to question whether auditor-provided NAS will

result in a net economic benefit to an organization. First, NAS may be sold as part of a bundle of

services with the audit engagement. Bundling is defined as packaging two or more services

together for a single price (Guiltinan [1987]). If the objective of the bundle is to only improve

audit efficiency then it is less likely that NAS will lead to future improvements in operating

performance or subsequent reductions in risk for the client. Second, the potential for rent-

extraction by public accounting firms could result in the cost of services exceeding the benefit

(Schneider [2012], Wolinsky [1993]). Third, even if NAS are an effective mechanism for risk

management, to the extent that NAS compromise the independence of the audit decreased levels

of core financial-statement assurance could offset any potential benefits that accrue to client

firms from resource flexibility and improved risk management.

4 For example, Marathon Petroleum Corporation maintains a policy statement that outlines permissible audit-related, tax, and other NAS. Examples of audit-related services include due diligence related to pre-business combinations, employee benefit plan audits, and audits of pools of assets. Tax services include advice on restructuring, transfer pricing assistance, and customs audits. Lastly, the firm lists assistance with statutory and governmental filings among its permissible other services. Many of these types of services can have a direct impact on future operating performance and risk management.

6

Using a sample of publicly-traded firms from the post-SOX time period (2003-2013) that

purchase non-audit services from their auditor,5 we use DuPont Analysis models (Soliman

[2008], Patatoukas [2012], Dickinson [2011]) to forecast improvements in return on net

operating assets (RNOA), controlling for the underlying, fundamental changes in operations

arising from changes in after-tax profit margin (PM) and asset turnover (ATO).6 We supplement

these models with the dollar-value of NAS purchased by clients. We document a positive and

significant relation between current period NAS and subsequent improvements in operating

performance (RNOA) and asset turnover (ATO). We provide further evidence that risk

management is one mechanism linking NAS with improvements in operating performance by

examining how improvements vary with preexisting risk. We find that improvements in

operating performance due to NAS are greater for firms with relatively greater cash flow

volatility or stock return volatility, suggesting that when the opportunity for auditors to improve

risk management is greatest, the increase in performance is similarly greater. We also consider

whether firms benefit from purchasing NAS through improvements in risk management. We

document a negative relation between NAS and subsequent operating risk proxies, consistent

with NAS facilitating more effective risk management. Moreover, the negative relation suggests

that NAS’ relation to increases in operating performance does not arise as a result of clients

taking on more operating risk and, in fact, NAS fees are associated with improved risk

management in the future.

5 We limit our sample to the post-SOX time period to ensure consistent and reliable reporting of NAS. We omit firms that do not purchase any NAS to decrease the likelihood that our results are due to self-selection issues. We consider self-selection issues in Section V. 6 Focusing on operating performance allows us to abstract away from any financing effects that NAS may have. NAS have been related to increased costs of equity capital (Nam and Ronen [2012]), potentially influencing how firms rely on debt vs. equity financing. Our DuPont analysis omits financing effects from performance (Soliman [2008], Patatoukas [2012], Dickinson [2011]).

7

While improvements in operating performance are arguably beneficial to client firms,

such benefits must be offset against any potential costs or negative effects that might arise.

Specifically, we consider whether the positive relation between NAS and subsequent operating

performance represents a loss of audit quality. We thus examine the association between NAS

and subsequent earnings management, proxying for earnings management with signed

discretionary accruals. If the provision of NAS leads to an impairment of auditor independence

then the positive relation we find between NAS and future operating performance could be

driven by income-increasing earnings management. Holding constant the determinants of

operating performance, we fail to find any evidence consistent with NAS compromising audit

quality and resulting in greater income-increasing earnings management in subsequent periods.

Our results indicate that a client's decision to purchase NAS from their auditor yields

benefits that extend beyond the audit production process and we do not find any evidence that

the client's decision is driven by a desire (or ability) to reduce the quality of the audit by

undermining the independence of the auditor. Rather, our evidence clearly shows that some

clients can obtain demonstrable economic benefits by acquiring NAS from their auditor. While

similar benefits might be obtainable from other service providers, the fact that these firms

voluntarily choose their auditor for such services indicates that such transactions are

economically beneficial to the client organization. Obviously, firms that do not expect to benefit

in a similar fashion can choose to not purchase NAS from their auditors. In short, the voluntary

purchase of NAS suggests an economically informed decision that benefits the client

organization without damaging the auditor-client relationship or undermining audit quality.

8

To shed additional light on our results, we decompose NAS into three types: audit-related

fees, tax service fees, and other fees (SEC [2000]).7 We find that the positive relation been NAS

and subsequent improvements in operating performance are a function of audit-related services

improving asset turnover and tax services improving after-tax profit margins. As a supplemental

analysis, we allow the effect that NAS have on improvements in operating performance and

reductions in risk to vary by client-firm size. We estimate our models by asset-tercile and find

that the NAS purchased by smaller and midsize firms generally result in performance

improvements whereas the NAS obtained by midsize and larger firms result in reductions in

future risk.

Our findings are important for several reasons. First, standard-setters and regulators are

concerned that NAS may undermine audit quality. While much of the previous research on NAS

has failed to find a negative association between such services and audit quality (Kinney et al.

[2004], Paterson and Valencia [2011], Ashbaugh et al. [2003], DeFond et al. [2002], Chung and

Kallapur [2003], Hay et al. [2006]), our findings provide evidence that client firms appear to

benefit from the joint provision of NAS and that further restrictions on the currently permissible

bundle of NAS may have unintended, negative consequences. Second, our study is important to

academics seeking to understand the underlying costs and benefits of NAS. Previously, research

has primarily focused on outcomes such as tax avoidance (Cook et al. [2008]), audit efficiency

(Simunic [1984]), and earnings management (Kinney et al. [2004]). We offer a broader

perspective in which all costs and benefits are netted out through overall firm performance.

7 The SEC defines audit-related fees as “assurance and related services (e.g., due diligence services) that traditionally are performed by the independent accountant… employee benefit plan audits, due diligence related to mergers and acquisitions, accounting consultations and audits in connection with acquisitions, internal control reviews, attest services that are not required by statute or regulation and consultation concerning financial accounting and reporting standards.” Tax fees are “fees for tax compliance, tax planning, and tax advice.” Other fees capture any services not fitting into the above two-categories (Asthana and Krishnan [2006]).

9

Third, our research is important to managers of firms as we document the viability of NAS as a

mechanism to address gaps in human capital and improve risk management especially for firms

with high preexisting risk.8

The remainder of the paper is structured as follows: First, we develop our hypotheses in

Section II and elaborate on our research design in Section III. We then present our main findings

in Section IV and discuss additional analysis in Section V. Section VI summarizes our results

and conclusions.

II. Hypothesis Development

Organizations create value when they strategically identify and place into service

resources that can be leveraged to their advantage (Hitt and Ireland [1986]). Resources can be

broadly classified as physical capital, organizational capital, or human capital (Barney [1991]).

Physical capital resources include property, plant, and equipment, as well as raw materials, that

the firm possesses and uses in conducting its operations (Williamson [1975]). Organizational

capital resources include a firm’s control systems, the structure of the organization, and informal

interactions among divisions within the firm (Tomer [1987]). Human capital resources are

composed of the knowledge, experience, education, and perspective of each manager or worker

(Becker [1964]). NAS provide a potential source of organizational or human capital that could

be economically beneficial to an organization.

Hypothesis 1: NAS and Future Performance

The success of any organization depends on its ability to marshal and utilize appropriate

resources given its objectives and strategic plans. Fundamental to achieving success is the need

8 The potential for an audit firm to benefit a client in various ways beyond fundamental assurance over financial statements has been previously documented in the small and medium enterprises (SME) market where most companies are not publicly listed (Knechel et al. [2008]).

10

for effective decision making and resource management by the managers of the organization.

Many organizational failures can be directly traced to failures in management planning and

decision making (Denis and Denis [1995], Perez-Gonzalez [2006]). Consequently, all

organizations seek to acquire and develop the best human capital, consistent with the resource

based view of the firm (Conner [1991]). However, decisions about human capital often are based

on implicit tradeoffs between the costs and benefits of adding human resources to an

organization, as well as alternatives that may be available for gaining access to needed labor

(e.g., outsourcing). For example, the cost of some labor may be high due to short-term frictions

in labor markets. Labor market frictions that create inefficiencies when hiring new employees

include labor unions (Earle and Pencavel [1990]), wage rigidity (Gali et al. [2007]), supplier

market power or preferences (Hall [1997]; Chang and Kim [2007]), and inefficiencies in the

search for qualified candidates (Sterling [2014]). Further, once an employee is hired into an

organization, the cost associated with that individual becomes “sticky” (Anderson et al. [2003]).

One option for supplementing internal skills and expertise is to hire outside consultants

for specific tasks, especially if the task is highly technical such that obtaining the necessary skill

level via internal hires may not be cost effective. Nippa and Petzold [2002] note that hiring a

consultant with specific expertise facilitates knowledge transfer in a manner that may be less

costly than the client firm hiring and training employees to gain specialized knowledge. Further,

an internal solution may not be as effective as that provided by a consultant because the external

consultant is likely to have more experience in specific, highly technical areas. Thus, consulting

firms deliver value through improvements in the organizational resources of the firm and the

efficient deployment of human capital. The professionals that comprise a consulting engagement

team have generally obtained a considerable amount of formal education and training in order to

11

enter their field (Hitt et al. [2001]). The overall high level of auditor provided NAS in the

economy clearly indicates that the independent auditor is one possible source of external

expertise that a company can access.

The breadth and depth of NAS offered by public accounting firms continues to expand

consistent with the diversification of their human capital. These services are broadly classified as

audit-related, tax, and other. Audit-related services are assurance and associated services not

specifically required by statute such as due diligence pertaining to a merger or acquisition or

employee benefit plan audit (SEC [2000]).9 Tax services are performed by an accounting firm’s

tax department and include tax compliance or planning but do not include assurance work done

in conjunction with the audit (Kinney et al. [2004]). Lastly, other services are any services which

are not classified as audit-related or tax (SEC [2000]). Examples of other services include

consulting that improves information reporting, accuracy, and security; risk and compliance

services; and forensic accounting.10 Many of these services are sold to non-audit clients but

many are also actively marketed to audit clients as evidenced by the high average NAS fee

observed in our sample ($627,000).

NAS not only provide firms with resource flexibility in order to address operational

challenges, they can also improve a firm’s risk management. Risk management is important

because it facilitates a firm achieving its strategic objectives (COSO [2004]). Firms must

evaluate the risk and return on their investment options in order to ensure that they allocate

9 Note that if the employee benefit plan is large enough there is a statutory requirement that it be audited. Per the U.S. Department of Labor, a plan with fewer than 100 participants can receive a small pension plan audit waiver. If a plan is subject to a mandatory audit requirement, however, such an audit does not have to be conducted by the same auditor. 10 While SOX has imposed restrictions on the types of NAS that can be provided to public companies, there are still several types of permissible services that may be purchased to address clients’ needs subject to audit committee approval. SOX prohibits audit firms from providing bookkeeping, financial information systems design and implementation, appraisal or valuation, actuarial, internal audit outsourcing, management function or human resource, broker or dealer, legal, or expert services to their audit clients (Messier et al. [2014]).

12

capital efficiently across lines of business (Nocco and Stulz [2006], McShane et al. [2011]).

Consistent with expectations, Baxter et al. [2013] find that high quality enterprise risk

management is positively related to future operating performance. NAS addressing a firm’s risks

should similarly result in subsequent increases in firms’ operating performance. For example,

improved accuracy in information should allow managers to tailor strategies to their particular

competitive environment more effectively and with shorter response times. Tax consulting can

allow firms to better structure and source their supply chain in a manner that minimizes taxes

(e.g., via transfer prices), potentially freeing up resources for investment that would have

otherwise been remitted to taxing authorities. Assurances provided about pension plans and

acquisitions should allow managers to form better estimates of future financial needs and

payoffs, allowing managers to better allocate resources within the firm and minimize

unnecessary resource slack.

While the ability of NAS to provide resource flexibility and improve risk management

suggests a positive relation between NAS and subsequent improvements in operating

performance, there are at least four reasons why such an association may not occur. First, NAS

could be sold as a bundle of services with the audit solely to gain efficiencies in the audit.

Second, NAS could be purchased in order to improve financial reporting quality or to ensure

regulatory compliance. Neither of these two outcomes would necessarily lead to an improvement

in operating performance for the client. Third, the sale of NAS can be the result of rent extraction

by the audit firm due to a lack of bargaining power for the client or significant information

asymmetry between the audit firm and the client (Chen et al. [2010]). Fourth, the provision of

NAS can result in auditor independence impairment which reduces the value of the audit and

13

lowers audit quality (Simunic [1984]).11 A company could choose to purchase NAS from any of

a number of suppliers. The fact that they purchase specific NAS from their auditor suggests that

they perceive a net economic value in the services. Therefore, it follows that for public

accounting firms to maintain their NAS practices over the long term, they must provide value to

their clients (Klein and Leffler [1981]). This leads to our first hypothesis:

H1: There is a positive relationship between auditor-provided NAS and subsequent

changes in performance.

For the purposes of this paper, we proxy for future operating performance using the change in

the return on net operating assets. We also decompose our performance measure into its DuPont

components—asset turnover and after-tax profit margin—in our supplemental analysis to

provide a greater understanding as to the types of performance improvements provided by NAS.

Hypothesis 2: NAS and Risk

Services focusing on risk management are a significant component of NAS marketed to

audit clients (KPMG [2012], EY [2013]). Such services can have a beneficial effect on

mitigation of a firm’s future risk. Specifically, NAS that facilitate more effective risk

management can aid a firm in avoiding riskier investments and more accurately measuring the

potential for downside outcomes including the tax consequences of expanding into new

jurisdictions. For example, firms that engage in complex transactions such as mergers and

acquisitions are likely to benefit from due diligence work performed by the advisory practice of

their current auditor.12

11 The level of audit quality can have a significant impact on an organization’s cost of capital because high quality financial reporting is associated with lower cost of debt (Pittman and Fortin [2004]) and improved investment efficiency (Biddle and Hilary [2006]). 12 The assurance provided by NAS with regard to mergers and acquisitions (typically through audit-related fees) are particularly relevant in this setting as empirical evidence indicates that most acquisitions suffer from a winner’s curse where the acquiring firm experiences a loss in value after completing the transaction (Harford [1999], Gilberto and Varaiya [1989], Moeller et al. [2004]).

14

Risk management has been formally established as an important element of

management’s responsibilities since the Foreign Corrupt Practices Act of 1977 set forth that

managers must implement an effective system of internal control. Risk management was greatly

broadened by COSO in 1992 by establishing a framework for evaluating internal control. The

1992 COSO framework was subsequently extended to reflect a much more comprehensive

approach to enterprise risk management (COSO [2004]). Following the framework of COSO,

managers and auditors have placed a greater emphasis on a broad understanding of business risk

(Knechel [2007]). Risk management has also moved to the forefront of the agenda for audit

committees (KPMG [2012]). Such a change in focus toward risk management among corporate

officers and directors has led to substantial changes in auditing practice (IFAC [2009], PCAOB

[2010]). It has also served as an impetus for the further development of NAS that focus on

identifying and addressing risk.13

While some NAS have been developed to assist firms in their risk management, whether

purchases of NAS by audit clients actually influences the level of subsequent client risk is an

open question. First, following the implementation of SOX, firms changed the level and types of

NAS that they obtained from their auditors (Gaynor et al. [2006], Abbott et al. [2011]). Such

shifts in the demand for NAS could mitigate any association if valuable services were statutorily

prohibited or those charged with governance (i.e. the audit committee) opted not to purchase

NAS due to a perceived impairment of independence. Second, consistent with the discussion of

the impact of NAS on future operating performance, NAS could be the result of bundling these

services with the sale of the audit only to obtain audit efficiencies as opposed to reducing a

13 For example, in their 2012 Global Annual Review, PwC discussed the importance of providing assistance with risk management for several clients. The audit firm emphasizes that risk management will continue to be an important consideration for its clients going forward and that it will continue to work to serve client needs in this area.

15

client’s future risk. Given that specific types of NAS are sold to explicitly improve a firm’s risk

management, and that managers and board members are increasingly concerned with reducing

risk, it is more likely that NAS will be negatively related to future firm risk. We, therefore, state

our second hypothesis as follows:

H2: There is a negative relationship between auditor-provided NAS and subsequent

client risk.

We proxy for future risk using the standard deviation of operating cash flows for years t+1

through t+5 and daily stock return volatility for the subsequent calendar year.

Hypothesis 3: Effect of Different Types of NAS

Our first two hypotheses make no distinction between different types of NAS. Initial

theory proposed in the auditing literature treated NAS as essentially homogenous (Simunic

[1984]). Empirical research that has not accounted for potential differences across various types

of NAS has produced mixed results when examining the impact of the joint provision of audit

and NAS on financial reporting quality (Prawitt et al. [2012]). Recent research has begun to

consider the heterogeneous effects that different types of NAS have on audit quality and auditor

effort (Kinney et al. [2004], Davis et al. [1993], Bell et al. [2014]). Such findings are likely to

influence our analysis as well. For example, assurance services, such as audit-related services,

could improve a firm’s risk management processes so we might expect a positive (negative)

relation between audit-related services and future operating performance (risk). On the other

hand, such services may simply improve audit efficiency or yield a higher level of assurance on

the financial statements. Similarly, tax services could be positively (negatively) related to future

operating performance (risk) if they pertain to tax planning which reduces the likelihood of

negative unintended consequences from expansion into a new tax jurisdiction. However, tax

services focused solely on tax compliance may not have any future benefit for a client. While we

16

expect that there will be differences between the different types of NAS (i.e. audit-related, tax

and other), we do not have a priori expectations as to the effect of different types of NAS on

operating performance and future risk, leading to our third hypothesis:

H3: The effect of auditor-provided NAS on future operating performance and risk will

depend on the type of NAS provided by an audit firm.

III. Research Design

Subsequent Performance Model

To test our first hypothesis, we model subsequent improvements in operating

performance using a DuPont model based on prior literature (Soliman [2008], Patatoukas [2012],

Dickinson [2011], Fairfield and Yohn [2001]) which we supplement with measures of non-audit

fees and audit-fees. We estimate the following OLS regression, clustering standard errors by firm

and including year and industry fixed effects (two digit SIC) (Petersen [2009]):14

∆RNOAt+1 = β0 +β1 TOTNASt + β2 AUD_FEESt + β3 RNOAt + β4 ∆RNOAt + β5 ∆ATOt +

β6∆PMt + β7 GrNOAt +e (1)

The dependent variable is the change in the return on net operating asset (∆RNOAt+1) and is

measured as the difference between operating income after depreciation and amortization

(OIADP) scaled by lagged net operating assets from year t to year t+1. We define net operating

assets as the difference between operating assets and operating liabilities.15 The advantage of

using return on net operating assets is that we can analyze performance after removing the

effects of financing such as leverage or the cost of equity.

14 In additional analysis we make modifications to rule out two alternative explanations. First, we rule out the remediation of internal control weaknesses by removing all observations where a firm has an internal control weakness according to Audit Analytics. Second, we split our sample into three terciles by client size to ensure that our results are not driven solely by size. 15 Following Soliman [2008], we measure operating assets as total assets (AT) less cash (CHE) and short term investments (IVA). Operating liabilities are total assets less interest bearing debt (DLTT, DLC), common equity (CEQ), preferred stock (PSTK), and minority interest (MIB).

17

Our variable of interest is total non-audit fees which includes all non-statutory fees paid

to the independent auditor (TOTNAS), captured from Audit Analytics. To ease interpretation, we

rank TOTNAS into deciles and scale such that it varies between zero and unity.16 Consistent with

Hypothesis H1, we expect a positive and significant coefficient for TOTNAS (β1 > 0). We also

include the decile-rank of AUD_FEES in Equation (1) in order to accommodate any potential

cross-determination of audit and non-audit fees (Simunic [1984], Whisenant et al. [2003]) as

well as to control for any assurance or risk-reduction associated with a financial statement audit

(Simunic [1980]).

Our control variables are identified from prior literature (Soliman [2008]). We include

contemporaneous operating performance (RNOAt) as well as the change in operating

performance (∆RNOAt) to control for persistence of profitability and mean reversion over time.

We also include the contemporaneous changes in RNOA’s two components: asset turnover

(ATO) and after-tax profit margin (PM). Both serve as fundamental signals of operating

performance (Soliman [2008]). Asset turnover, sales divided by lagged net operating assets,

captures the extent to which firms are able to utilize assets to generate operating profits, with

changes indicating increases in efficiency of production or asset utilization. After-tax profit

margin, operating income divided by sales, captures the extent to which a firm is able to contain

costs within its sales as well as to set prices above marginal cost. We include growth in net

operating assets (GrNOA) to control for changes in the denominator of our performance measure

arising from differential growth rates across firms.

16 Unlike prior auditing literature (with the exception of Ferguson et al. [2004]), we rely on the decile-rank of non-audit fees and audit-fees rather than their natural log. This is to facilitate economic interpretation consistent with non-auditing studies that have variables of interest with significant skewness (Affleck-Graves and Mendenhall [1992], Battalio et al. [2012]). In Section V, we replicate all results, in direction and significance, using the natural log of non-audit fees and audit-fees as well as the ratio of NAS to total fees. We find qualitatively similar results using both measures.

18

We also employ Equation (1) in the test of our third hypothesis. Specifically, we

disaggregate TOTNAS into its three types: AR_FEES, TAX_FEES, and OTH_FEES (SEC [2000],

Asthana and Krishnan [2006]), which are the decile-ranks for audit-related, tax, and other fees,

respectively.17

Decomposing NAS into its three types allows us to determine which type(s) of

NAS are economically beneficial to clients. Hypothesis H3 predicts the coefficients on each type

of NAS will be different from one another, suggesting that each type of NAS has a unique

impact on firms’ subsequent operating performance.

Finally, we also provide evidence as to how NAS improves subsequent performance.

DuPont analysis suggests that operating performance can be driven by two components, asset

turnover and after-tax profit margin. We therefore replace the dependent variable of Equation (1)

with subsequent changes in ATO and PM.

Subsequent Operating Risk Model

To test our second hypothesis, we model the relation between subsequent operating risk

and NAS using the following OLS regression:

Riskt+k = γ0 +γ1 TOTNASt + γ2 AUD_FEESt + γ3 Riskt + γk CONTROLSj +e (2)

We employ two proxies of future operating risk: (1) the future five-year volatility of operating

cash flows (STDCFO) and (2) daily stock return volatility for the following year (STDRET). We

measure STDCFO as the five-year, rolling-window standard deviation of operating cash flows

scaled by total assets for years t+1 to t+5 (Minton and Schrand [1999], McGuire et al. [2012]).

We measure STDRET as the standard deviation of daily returns over the following calendar year

(Callen et al. [2010], Lara et al. [2011], Comprix et al. [2011]).

17 Note that when we form the deciles we assign all observations with a zero dollar value for a specific type of service into a single decile and then split the remaining observations across the nine remaining deciles. This is done to ensure that all observations with a zero dollar amount are treated the same.

19

Consistent with Hypothesis H2, we expect negative and significant coefficients for

TOTNAS (γ1 < 0). We also include contemporaneous levels of risk (RISK) to ensure TOTNAS is

not simply capturing firms with preexisting high or low levels of operating risk. We include the

same control variables as in Equation (1) to determine whether the subsequent increases in

operating performance related to NAS are related to subsequent increases in risk, which would

call into question the potential value of NAS to risk-averse shareholders, or subsequent decreases

in risk, enhancing the value of NAS. As with our analysis of operating performance, we also

explore the extent to which the relation between NAS and subsequent risk holds for the three

types of NAS (i.e., H3). Again, we cluster standard errors by firm and include year and industry

fixed effects (two digit SIC) (Petersen [2009]).

Sample Selection and Descriptive Statistics

We initially draw our sample from the intersection of Compustat’s Annual File, Audit

Analytics, and CRSP for the years 2003-2013. We begin in 2003 to ensure consistent reporting of

non-audit fees as well as a consistent set of SOX-allowed NAS. We end in 2013 because of the

requirement of one year of subsequent operating performance and risk. Next, we remove firms

in the financial industry or utilities because these firms operate in a highly regulated

environment. We then exclude any firm-year without the necessary data to estimate Equation (1),

requiring that observations have the data necessary to calculate current levels of, and future

changes in, RNOA, PM, and ATO. Next, we remove observations where denominators (lagged

net operating assets, sales) are less than one million to avoid small denominator problems. We

further restrict our sample by requiring firm-years to purchase a positive, nonzero amount of

NAS to decrease self-selection issues arising from the decision to purchase or not to purchase

20

NAS.18 Our final sample consists of 22,775 firm-year observations for our performance analysis

and 18,898 for our cash-flow (12,846 for our returns) based risk tests. We winsorize all

continuous variables by year at the 1% level.

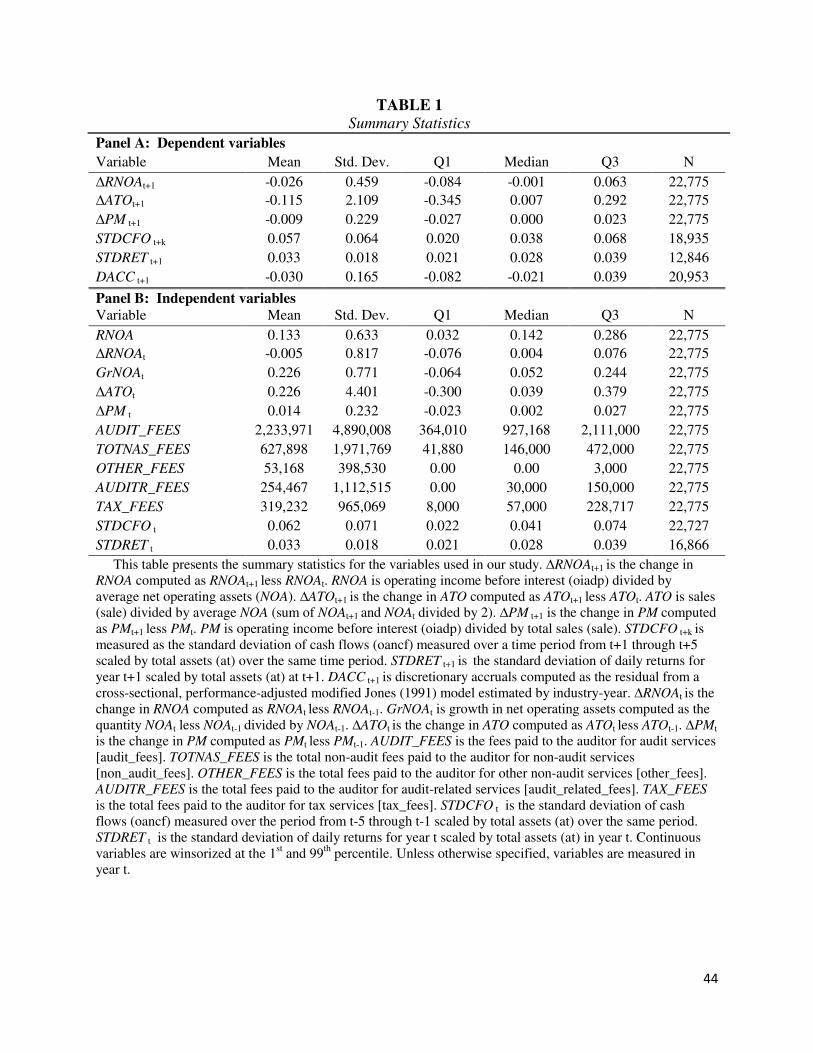

Table 1 contains descriptive statistics of our sample. Consistent with mean reversion of

performance, we find the average change in subsequent RNOA, ATO, and PM are all negative

(Fairfield and Yohn [2001], Soliman [2008]). Audit fees average $2.2 million while total non-

audit fees average $627 thousand. Tax fees are the largest type of non-audit fees, followed

closely by audit-related fees. Other fees are the smallest type of non-audit fees. Table 2 contains

the correlation matrix for the variables in our models. We find insignificant correlations between

non-audit fees and subsequent ∆RNOA and ∆PM. We find a modestly negative, but statistically

significant, correlation between TOTNAS and subsequent changes in asset turnover. Variance

inflation factors do not indicate any problems arising from multicollinearity.

<<<<< Insert Tables 1 and 2 about here >>>>>

IV. Main Results

Hypothesis 1: Subsequent Performance

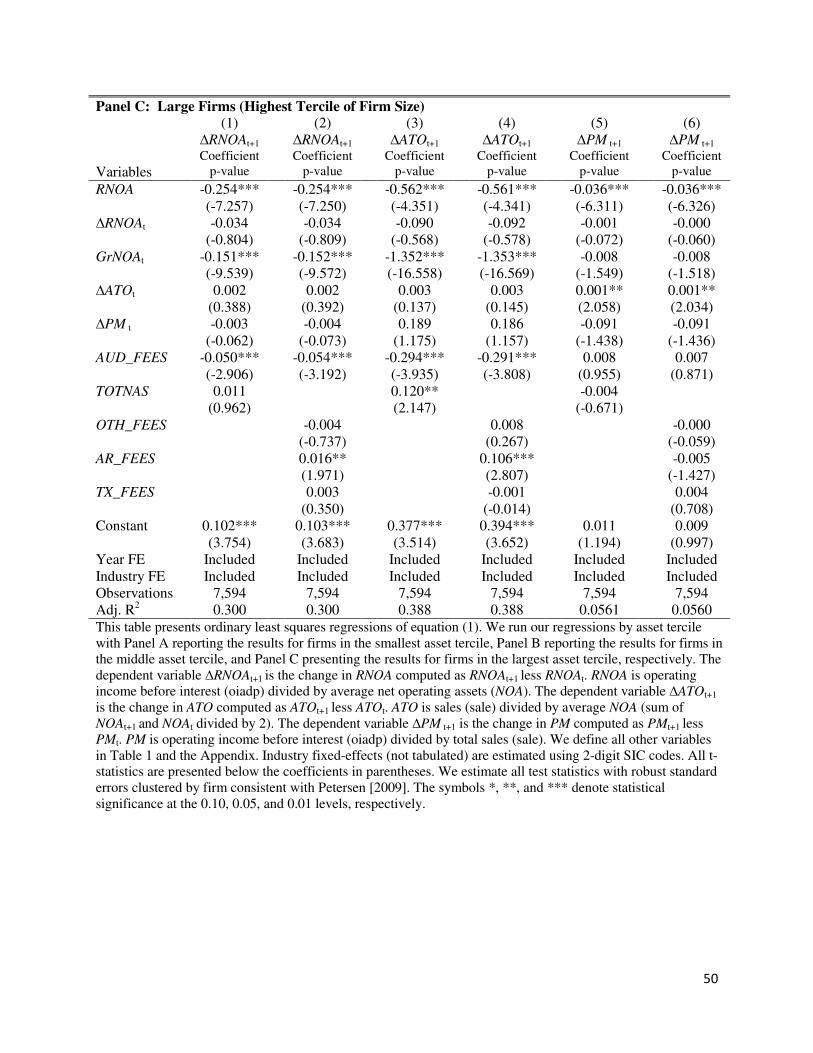

Table 3 presents the results of estimating Equation (1). The dependent variable in

Columns (1) and (2) is ∆RNOA. Columns (3) and (4) present the results for ∆ATO, while the

dependent variable for Columns (5) and (6) is ∆PM. Odd numbered columns contain TOTNAS

and even numbered columns contain the three types of TOTNAS. We find that AUD_FEES are

positively related to subsequent increases in operating performance (0.062, p<.01), suggesting 18 Consistent with Donohoe and Knechel [2013], we also confirm our findings are robust to removing firms purchasing a de minimis amount of NAS, where de minimis is defined as less than $10,000. Imposing these additional screens removes an additional 1,670 firm-years. We continue to find NAS are related to subsequent improvements in operating performance and subsequent reductions in operating risk. In untabulated additional analysis, we reperform all of our tests including all observations that do not purchase NAS (i.e. purchase a zero value). Our results continue to hold, namely we find NAS is positively and significantly related to subsequent increases in operating performance and negatively and significantly related to future reductions in operating risk.

21

that the improvements in organizational resources and assurances provided by the audit create

economic value for clients that also purchase NAS.19 Consistent with H1, the coefficient for

TOTNAS is positive and significant (0.053, p<.01) in Column (1), suggesting that NAS are

related to subsequent improvements in operating performance. A one-decile increase in fees is

associated with a 0.5% increase in return on net operating assets.20 Given that the average

subsequent change in operating performance is -2.6 percent, a one-decile increase in non-audit

fees results in about a 20% change in performance. The coefficients for AUD_FEES and

TOTNAS are statistically indistinguishable, suggesting the economic value provided by audits

and NAS are, on average, similar in magnitude. We also find that the coefficient for TOTNAS is

positive and significant in Column (3) (0.169, p<.01) while the coefficient for TOTNAS is

insignificant in Column (5), suggesting that the improvement in operating performance is

primarily attributable to improvements in asset turnover rather than after-tax profit margins.21

<<<<< Insert Table 3 about here >>>>>

Hypothesis 2: Subsequent Risk

Table 4 presents the results of estimating Equation (2). The dependent variable in

Columns (1) and (2) is the subsequent standard deviation of operating cash flows, while the

dependent variable in Columns (3) and (4) is the subsequent standard deviation of daily stock

returns. The coefficient for TOTNAS is negative and significant in both Columns (1) (-0.012,

p<.01) and (3) (-0.002, p<.01) consistent with Hypothesis H2 and suggests that NAS are related

to lower levels of future operating risk. Moreover, the negative coefficient is also evidence that

19 We also consider clients that do not purchase NAS in a supplemental analysis below. 20 Given that we decile-rank and transform such that NAS range from zero to one, a one unit increase in our context equals 0.1. 21 We confirm that improvements in operating performance and asset turnover persist into the second year. Namely, when replacing the dependent variable in Equation (1) with the average change in RNOA from year t+1 to t+2, we continue to find a positive and significant coefficient on TOTNAS.

22

the subsequent improvements in operating performance among firms that purchase NAS

documented in Table 3 does not simply occur because of increases in risk eliciting an

improvement in return. A one decile increase in NAS decreases subsequent operating cash flow

volatility by 0.12% (0.02%), or 2.1% (0.6%) of the average firm’s future cash flow volatility

(daily return volatility). Auditing services are also related to lower levels of future operating risk

as we find a negative and significant coefficient for AUD_FEES in Columns (1) and (3) (-0.034,

p<.01; -0.006, p<.01, respectively). This result is encouraging as it suggests that the statutorily-

mandated audit creates economic value by reducing future risk. Comparing the coefficients on

TOTNAS with AUD_FEES reveals that the assurances provided by auditing have a significantly

greater influence on reducing subsequent operating risk (p<.01 in Column (1) and p<.05 in

Column (3)). While the audit provides benefits in risk reduction, the joint provision of NAS

augments these benefits. In combination, our results suggest that NAS are related to subsequent

improvements in operating performance and decreases in operating risk, consistent with auditor-

provided NAS providing economic value to a client.

<<<<< Insert Table 4 about here >>>>>

Hypothesis H3: Analysis by Type of NAS

We report the results of tests of Hypothesis H3 relating to subsequent operating

performance in the even-numbered columns of Table 3. Disaggregating TOTNAS into its three

types reveals that audit-related services are positively related to subsequent improvements in

operating performance (Column (2), 0.018, p<.10). This finding suggests that the assurance

provided by audit-related services is beneficial to future operating performance via

improvements in asset turnover (Column (4), 0.102, p<.01). Tax services are also positively

related to subsequent improvements in operating performance (Column (2), 0.038, p<.01) via

23

improved after-tax profit margins (Column (6), 0.010, p<.05). Other types of NAS do not appear

to be related to improvements in firm performance, i.e., the coefficient for OTH_FEES is

insignificant in all three specifications.22 Taken together, the evidence is consistent with

hypothesis H3 which proposes that different types of NAS have different relations with client’s

future operating performance.

We present the results concerning the relation between types of NAS and subsequent

reductions in future risk in the even-numbered columns of Table 4. We find that audit-related

services are negatively and significantly related to future volatility in operating cash flows

(Column (2), -0.005, p<.01) and the future standard deviation of daily stock returns (Column (4),

-0.001, p<.01). We find a similar significantly negative relation between tax fees and firm risk

(Column (2), -0.009, p<.01; Column (4), -0.001, p<.01). Consistent with our analysis of future

operating performance, we do not find a significant association between other fees and future

risk. The collective evidence supports hypothesis H3 that different types of NAS have different

relations with future client risk.

Analysis of NAS based on Company Size

We do not explicitly control for client size in our primary analysis consistent with the

prior literature using DuPont Analysis (Soliman [2008], Patatoukas [2012], Dickinson [2011],

Fairfield and Yohn [2001]).23 However, we now consider the possibility that NAS can be related

to firm-size (Hay et al. [2006]). In order to examine the influence of size on our findings, we

estimate Equations (1) and (2) by yearly asset tercile. Table 5 presents the results of our analysis

concerning size and subsequent operating performance for small (Panel A), medium (Panel B)

22 We acknowledge that the frequency of non-zero other fees is significantly lower than for audit-related or tax fees as evidenced by the median amount of other fees being $0 in our sample. We cannot rule out the alternative explanation that the failure to find an association for other fees is driven by this lack of variation. 23 We implicitly control for size differences in Equations (1) and (2) by scaling RNOA by net operating assets.

24

and large (Panel C) firms. A pattern emerges suggesting that small firms primarily reap

improvements in operating performance from NAS as TOTNAS is significant and positive in

Column (1) in Panel A (0.104, p<.01) and Column (3) in Panel A (0.295, p<.05).24 Table 6

presents the results of our analysis concerning size and cash flow volatility (Panel A) and return

volatility (Panel B). Reductions in risk primarily occur among the midsize and large firms as

TOTNAS is negative and significant in Panel A, Column (3) (-0.012, p<.01) and Column (5) (-

0.007, p<.01), and in Panel B, Column (3) (-0.007, p<.05) and Column (5) (-0.008, p<.05).25

Overall, the results in Tables 5 and 6 suggest that smaller firms that have fewer resources

primarily gain from purchases of auditor-provided NAS through increases in performance (i.e.,

by obtaining access to external expertise), while larger firms benefit from NAS through reduced

risk which suggests that their issues have more to do with complex systems of risk management.

<<<<< Insert Tables 5 and 6 about here >>>>>>

V. Additional Analysis

Additional Risk Management Evidence

Our argument assumes that NAS influences subsequent performance and risk. We

provide further evidence that risk management is one mechanism through which this occurs by

examining the extent the relative magnitude of preexisting operating risk influences the relation

between operating performance increases and NAS. We assume that relatively higher levels of

operating risk reflect poorer firm-level risk management and greater opportunities for NAS to

improve risk management. Therefore, to the extent that risk management is a mechanism through

24 We obtain qualitatively similar (0.053, p<.01) results when we conditionally rank NAS into deciles within separate asset size quintiles rather than terciles. Following Kubick et al. [2014], we first sort all firms by total assets into five distinct quintiles. Next, within each size quintile, we form decile ranks of NAS purchases. By measuring NAS in this manner we treat observations in the highest decile of NAS in the highest quintile of asset size as equivalent to observations in the highest decile rank of NAS in the lowest quintile of asset size. Thus, we effectively remove the influence of size from the analysis. 25 We find qualitatively similar results (-0.012, p<.01) when we follow Kubick et al. [2014] to form decile ranks of NAS within asset quintiles.

25

which NAS work, we expect significantly greater improvements in operating performance

among firms with the greatest preexisting risk.

To test this, we augment Equation (1) with one of two risk proxies. For our first risk

proxy, we create an indicator variable (HIGH CF RISK) equaling one when a firm has above-

median operating cash flow volatility over the five years prior to the purchase of NAS. For our

second risk proxy, we create an indicator variable (HIGH RET RISK) equaling one when a firm

has above-median daily return volatility in the year prior to the purchase of NAS. We include the

main effect in Equation (1) (i.e., either HIGH CF RISK or HIGH RET RISK) and interact it with

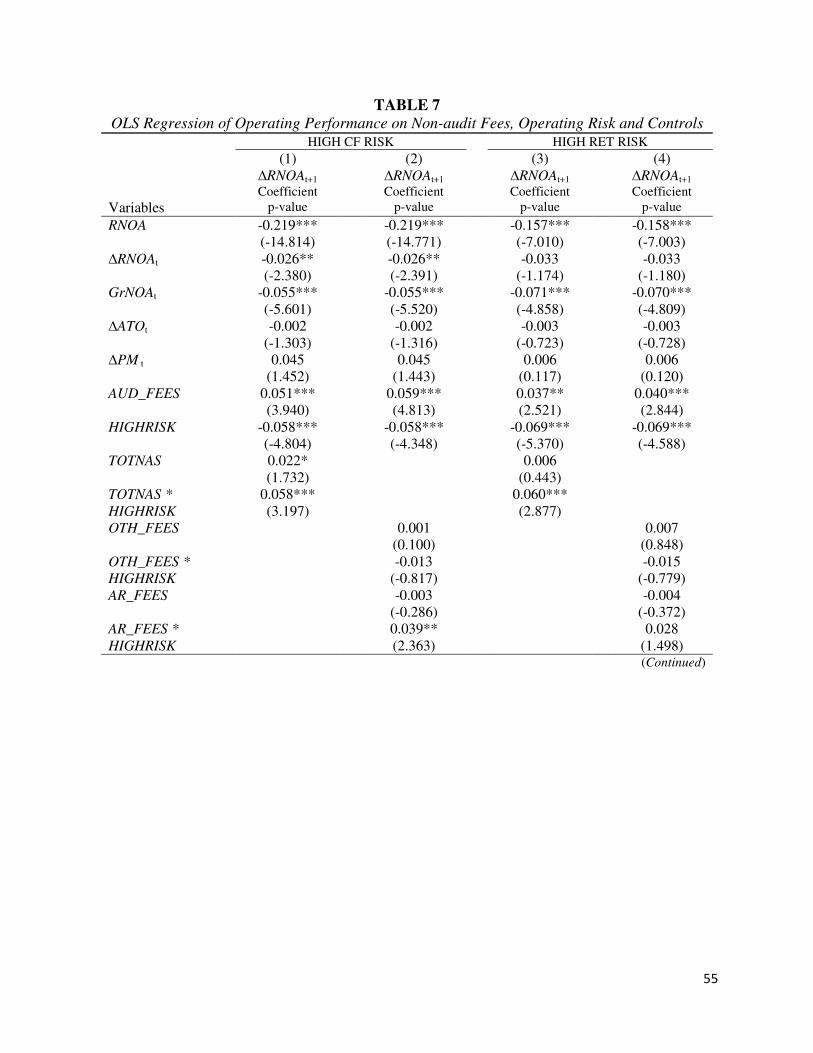

TOTNAS.26 Table 7 presents these results. The first two columns use HIGH CF RISK as our risk

proxy while the last two use HIGH RET RISK. We find a significant coefficient for TOTNAS in

Column (1) (0.022, p<.042) and an insignificant coefficient in Column (3) (0.006, p<.328),

providing some evidence that among firms that already have relatively low levels of operating

risk, NAS provides future improvement in operating performance. In contrast, we find robust

evidence of a positive and significant relationship of the interaction of TOTNAS and HIGH CF

RISK in Column (1) (0.058, p<.01) and TOTNAS and HIGH RET RISK in Column (3) (0.060,

p<.01), consistent with firms operating in relatively high risk environments benefiting the most

from their purchase of NAS.

<<<<< Insert Table 7 about here >>>>>

Audit Quality

Whether, and the extent to which, NAS may impair auditor independence and audit

quality is a contentious issue among researchers and regulators. There is mixed evidence within

prior literature as studies have documented a positive relation between NAS and audit quality

(Kinney et al. [2004], Paterson and Valencia [2011]), a negative relation (Frankel et al. [2002],

26 In both models, we cluster standard errors by firm and include year and industry fixed effects (Petersen [2009]).

26

Ferguson et al. [2004]), or no relation (Ashbaugh et al. [2003], DeFond et al. [2002], Chung and

Kallapur [2003]). In this paper, a concern may arise that the improvements in future

performance may simply be the result of earnings management. If the provision of NAS leads to

impaired auditor independence, then the auditor may be more willing to allow the client to book

positive accruals which could appear to be superior future performance (DeAngelo [1981],

Simunic [1984], Ashbaugh et al. [2003]). Given our hypotheses concern subsequent operating

performance, we test for evidence of earnings management in subsequent periods.27 We use

discretionary accruals (Jones [1991], Kothari et al. [2005]) as our proxy for earnings

management.28 We modify Equation (1) in two important ways in order to examine whether

earnings management drives our results. First, we substitute subsequent period discretionary

accruals at t+1 for our dependent variable ∆RNOAt+1. Second, we include current period

discretionary accruals at time t to control for any persistence in firm-specific accrual policies

unrelated to earnings management.

We report our results for discretionary accruals in subsequent periods in Table 8. Odd

numbered columns include the variable IMPPERF, an indicator variable equaling one when a

firm’s subsequent performance as measured by ∆RNOAt+1 is above the median for its given year,

and zero otherwise. We interact IMPPERF with non-audit fees to investigate the extent to which

firms with increased operating performance differ from those whose performance is below the

median. Panel A’s dependent variable is discretionary accruals for year t+1, while Panel B

27 There also remains the possibility that our results are an artifact of compromised audit quality leading to cookie jarring in year t. For this to be the case, however, the negative discretionary accruals of year t would need to reverse as positive discretionary accruals in year t+1 or later. Therefore, our subsequent period tests address this scenario and provide no evidence in support of it. In untabulated analysis, we find that current period discretionary accruals are also negatively and significantly related to NAS among firms with subsequent improvements in operating performance. 28 We calculate discretionary accruals as the residual from a cross-sectional, performance-adjusted modified Jones [1991] model estimated cross-sectionally by industry-year (McGuire et al. [2012], DeFond and Jiambalvo [1994], Dechow et al. [1995]). We use two-digit SIC for our industry-definition.

27

reports our results for the year t+2. The dependent variable in Columns (3) and (4) of both panels

is positive discretionary accruals. We therefore estimate a truncated regression in these columns,

rather than an OLS regression.

<<<<< Insert Table 8 about here >>>>>

We find an insignificant coefficient for TOTNAS when we use subsequent discretionary

accruals (year t+1) as our dependent variable in Column (1) of Table 8. When conditioning on

subsequent improvements in operating performance in Column (2), we find a positive coefficient

on TOTNAS among firms without subsequent improvements in operating performance (0.016;

p<.01), suggesting that NAS are related to increased discretionary accruals among firms that lack

improvements in operating performance. However, when summing the coefficients on TOTNAS

(0.016) and IMPPERF*TOTNAS (-0.037), we find current NAS are negative and significantly

related to subsequent discretionary accruals (p<.01) in year t+1, suggesting that the relation

between NAS and subsequent period’s discretionary accruals is negative among firms that

experience an increase in subsequent operating performance. We find a similar pattern of

coefficients when examining subsequent positive discretionary accruals at time t+1. Namely, the

coefficient for IMPPERF*TOTNAS is negative and significant (-0.017, p<.05). When we

examine discretionary accruals at time t+2, we find a negative and significant coefficient for

TOTNAS in Columns (1), (3), and (4) (p<.05) and insignificant coefficients on the IMPPERF by

TOTNAS interactions.

Taken together, these findings suggest there is a negative relation between NAS and

future, positive discretionary accruals. The negative association is even more pronounced for

firms with subsequent improvements in operating performance in year t+1. Overall, our evidence

from examining subsequent (positive) discretionary accruals is not consistent with firms’

28

improvements in operating performance arising from greater earnings management in future

periods.

Analysis of Self-selection

In our primary analysis, we exclude all firms that do not purchase NAS from their auditor

because of the endogeneity inherent in the choice to buy additional services. Prior literature

documents that the purchase of NAS along with the audit is likely jointly determined (Whisenant

et al. [2003]). To test for the effect of endogeneity, we perform additional analysis where we

include all observations that had zero NAS and that have the requisite data to calculate Equations

(1) and (2). To control for the selection issue, we employ a Heckman procedure (Heckman

[1979]) and specify the following probit model consistent with Ruddock et al. [2006]:29

PURCHASEt = ν0 + ν1BIG4t + ν2 NEGt + ν3 MRETt + ν4 CFOt + ν5 LEVt + ν4 INVRECt

+ ν4 LMVEt + ν4 MKTBKt + ν4 MERGERt + Σνj INDt +e (3)

where PURCHASE is an indicator variable taking a value of one if a firm engages its auditor for

NAS, zero otherwise. Our instruments are the auditor’s size (BIG4) as well as the client’s choice

of financing (LEV) as, a priori, there is no reason to expect that these variables should be related

to ∆RNOAt+1. We include controls for the client’s financial health (NEG, CFO), growth

prospects (MRET, MKTBK), size (LMVE), acquisition activity (MERGER), and industry

membership. All variables are defined in the Appendix.

We obtain the inverse-Mills ratio from Equation (3) and include this when we re-estimate

Equation (1). All other variables in the second stage are as previously defined. The inverse-Mills

ratio is significant (-0.098, p<.01) indicating that controlling for self-selection of firms that do

29 We exclude return on assets from our model because it is significantly correlated with our dependent variable ∆RNOA in the second stage of the Heckman procedure.

29

not purchase NAS is important when they are included in the analysis.30 In untabulated analysis,

we find that our results hold after controlling for self-selection. Namely, TOTNAS is positively

and significantly related to future return on net operating assets (0.049, p<.01). Similarly, when

we re-estimate Equation (2) after controlling for self-selection we find that TOTNAS is

negatively and significantly related to future cash flow volatility (-0.01, p<.01) and future stock

return volatility (-0.001, p<.10).

Analysis by Firm Life-Cycle

In our primary analysis, we follow prior DuPont analysis literature in building a

parsimonious empirical model (Soliman [2008], Patatoukas [2012], Dickinson [2011], Fairfield

and Yohn [2001]). This is particularly appealing as we are able to efficiently control for the key

determinants of the change in the return on net operating assets, our measure of operating

performance. In this section, we perform additional untabulated analysis to examine whether a

firm’s life cycle stage influences the relation between future operating performance (risk) and

NAS. We follow Dickinson [2011] and classify firms into one of five mutually exclusive life

cycle stages based on the signs of operating, investing, and financing cash flows.31 We then re-

estimate Models (1) and (2) for each unique life cycle stage.

An interesting pattern emerges from this analysis. First, we find that TOTNAS is

positively and significantly related to future RNOA only for firms in the introductory (0.168,

p<.01) or growth (0.051, p<.05) stages of the life cycle. We do not find any relation between

30 In untabulated analysis, we also test the validity of our instruments consistent with Larcker and Rusticus [2010] by regressing the residual from our second-stage estimation on all the explanatory variables in the first and second stages, including our instruments. We find that BIG4 is a valid instrument as it is insignificant (-0.003, p=.718) while LEV is significantly related to the residual (0.072, p<.01). Evidence of a valid instrument provides some assurance that our methodology addresses endogeneity concerns. 31 The five life cycle stages are defined by Dickinson [2011] as “(1) introduction where innovation is first produced; (2) growth where the number of producers increases dramatically; (3) maturity where the number of producers reaches a maximum; (4) shake-out where the number of producers begins to decline; and (5) decline where there is essentially a zero net entry.”

30

TOTNAS and future RNOA for the remaining three life cycle stages. These results are consistent

with our previously reported analysis of the influence of firm size in that we observe firms that

likely have the greatest need for external resources (relative to mature firms) obtain the greatest

operating performance benefits from their NAS purchases.

Second, we find consistent evidence that mature firms benefit from NAS purchases

through future decreases in risk as the coefficient on TOTNAS is negative and significantly

related to future cash flow volatility (-0.010, p<.01) and future stock return volatility (-0.002,

p<.01). Additionally, TOTNAS is negative and significantly related to future cash flow volatility

(-0.012, p<.01) and future stock return volatility (-0.005, p<.01) for growth and shake-out firms,

respectively. The results of our re-estimation of Equation (2) are largely consistent with our

analysis by firm size in that as firms mature and face increasingly complex operations they

benefit from the purchase of NAS in the form of a reduction in operating risk.32

Internal Control Weaknesses

Prior research has documented that the remediation of weaknesses in internal controls

over financial reporting disclosed under Section 404 of SOX are associated with improvements

in investment quality (Cheng et al. [2013]) and the purchase of NAS (Elder et al. [2008]). To

verify the extent to which our findings are attributable to the subsequent improvements arising

from the remediation of internal control weaknesses related to financial reporting, we exclude

from our sample the firm-year (t) and the following year (t+1) for all observations which Audit

Analytics identifies as having an internal control weakness and re-estimate Equations (1) and

32 We also find a weakly significant negative association between TOTNAS and future stock return volatility (-0.005, p<.10) for firms in the introduction life cycle stage. Thus there is some evidence that the purchase of NAS by immature firms can yield reductions in future operating risk as well.

31

(2).33 As this subsample lacks internal control weaknesses, results cannot be attributed to the

remediation of internal control weaknesses. In untabulated analysis, we continue to find positive

and significant coefficients for TOTNAS (p<.01) in Equation (1). This is consistent with the

benefits provided through NAS leading to subsequent increases in operating performance and

inconsistent with our findings being the result of internal control weakness remediation. We also

find a negative and significant coefficient for TOTNAS when re-estimating Equation (2),

suggesting that the negative relation between current NAS and future operating risk is not

attributable to internal control weaknesses. Overall, our results appear distinct from the

previously documented effects of internal control remediation.

Analysis using Other Measures of NAS Fee

For our primary analysis, we utilize the decile rank of NAS purchases in order to

facilitate interpretation of the economic significance of the coefficients from our tests. We

perform several robustness tests to ensure that our measure of NAS does not lead to spurious

inference. First, consistent with prior literature that examines NAS, we re-estimate Equations (1)

and (2), substituting the natural log of one plus the dollar value of non-audit fees in lieu of our

decile rank measure of NAS (Ashbaugh et al. [2003]).34 Our results are qualitatively similar to

our primary analysis with NAS being positively and significantly related to the future return on

net operating assets (0.011, p<.01) and negatively and significantly related to future changes in

cash flow volatility (-0.002, p<.01) as well as future changes in the standard deviation of stock

returns (-0.002, p<.01).

33 Remediation is defined as the process of fixing a material weakness or a significant deficiency during management’s assessment of internal controls (Messier et al. [2014]). Prior literature finds that internal control deficiencies are related to lower financial reporting quality, that remediation of previously reported internal control deficiencies is associated with improvements in accrual quality (Ashbaugh-Skaife et al. [2008]), and that the failure to remediate material weaknesses is related to increased abnormal accruals (Bedard et al. [2012]). 34 We also substitute the natural log of one plus the dollar value of audit fees paid as opposed to the decile rank of audit fees.

32

Second, we examine the relation between total fees paid to the auditor and future

operating performance and risk. In order to examine total fees, we modify Equations (1) and (2)

by removing our measures for audit fees (AUD_FEES) and NAS (TOTNAS) and including the

decile-rank of total fees (TOTAL_FEES) and scale so that it varies between zero and unity. Our

untabulated analysis shows that TOTAL_FEES are positively and significantly related to future

changes in return on net assets (0.107, p<.01) and negatively and significantly related to future

standard deviation of cash flows (-0.043, p<.01) and future standard deviation of returns (-0.032,

p<.01). These results are consistent with our primary analysis (Tables 3 and 4).

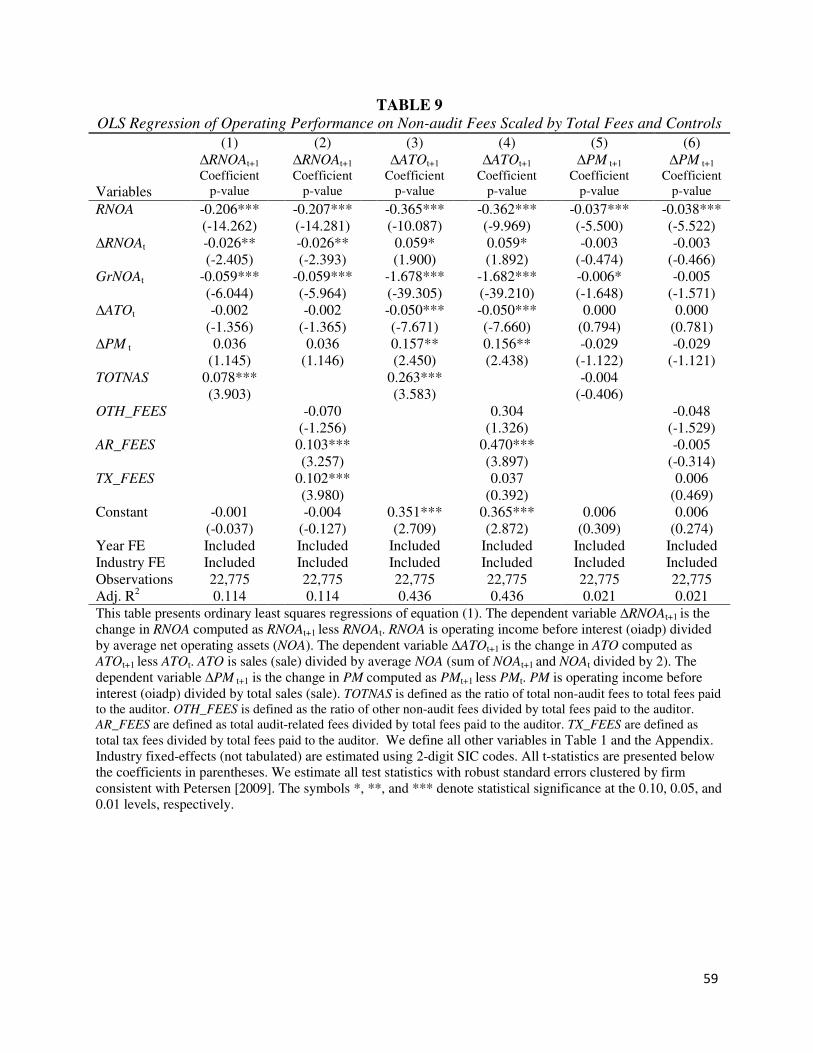

Lastly, we measure the relationship between NAS and future operating performance

(risk) using the ratio of NAS to total fees consistent with some prior literature (Frankel et al.

[2002], Ashbaugh et al. [2003]). We modify and re-estimate Equations (1) and (2) by

substituting the ratio of non-audit fees to total fees as our variable of interest and exclude audit

fees. We report the results of this analysis in Tables 9 and 10. We find that the ratio of non-audit

fees to total fees is positively and significantly associated with future return on net operating

assets (0.078, p<.01). We also document a negative and significant association between the ratio

of non-audit fees and future cash flow volatility (-0.008, p<.05) or future standard deviation in

returns (-0.011, p<.05). These results are consistent with our primary analysis. Additionally, we

find results for audit-related fees and tax fees consistent with our primary analysis. However, we

do find one notable difference from our primary results: the ratio of other fees to total fees now

has a positive and significant association with future cash flow volatility (0.041, p<.01) and

future standard deviation of returns (0.031, p<.05). Other services was not significant in our

primary analysis and this result may suggest that a large proportion of services that are unrelated

33

to the core services of an accounting firm—assurance and tax—may not have a positive impact

on risk management for the client.

<<<<< Insert Tables 9 and 10 about here >>>>>

VI. Conclusion

Numerous parties, such as regulators, investors, and corporate boards, must evaluate the

costs and benefits of the joint provision of auditing and NAS as part of the role that each plays in

the capital market. Prior academic research into NAS has considered the potential trade-off

between economic bonding reducing audit quality via independence impairment (cost) and

knowledge spillovers enhancing audit quality or efficiency (benefit). We expand the prior

literature’s exploration of the costs and benefits of NAS by considering two potential economic

benefits accruing to the client firm, namely improvements in operating performance and risk

management.

In general, we find that total NAS purchased in conjunction with the audit are positively

related to subsequent increases in operating performance and asset turnover. More specifically,

we find that audit-related fees are positively associated with future improvements in asset

turnover and tax fees are positively associated with future changes in after-tax profit margin.

These results suggest NAS provide economic benefits to client firms through operating

performance. We also find that total NAS fees, audit-related fees, and tax fees are negatively

related with future risk, suggesting that NAS also provide economic value to client firms through

improved risk management. In supplemental analysis, we provide evidence that firms with high

preexisting levels of operating risk appear to benefit the most from the purchase of NAS.

Additionally, we find that NAS purchased by firms that have fewer resources available (i.e.

smaller firms) are positively associated with future performance while NAS purchased by firms

that likely have more human capital available (i.e. larger firms) are associated with reductions in

34

future risk. We fail to find evidence of NAS compromising audit quality, suggesting the joint

provision of NAS and audit services do not appear to systemically impair audit quality

In spite of extensive sensitivity testing and supplemental analyses, our paper is still

subject to some limitations. First, our analysis of operating performance does not preclude NAS

impairing independence in appearance. If shareholders and debt-holders believe NAS

compromises audit quality, they may increase the financing costs of firms that purchase NAS.

Therefore, overall performance, net of financing costs, may not increase to the same extent as

operating performance. Second, we are only able to observe services purchased from auditors as

part of a bundle. We are therefore unable to comment on the economic benefits of the assurance-

related, internal control-related, tax, and other services purchased from other professional firms.

Lastly, we use common empirical proxies, such as discretionary accruals, to measure the

constructs we are interested in studying and to the extent that these proxies are measured with

error this may introduce bias into our analysis.

Overall, our study provides evidence that NAS provide economic benefits to client firms.

Our results are of interest to several stakeholders. Regulators that are currently weighing whether

or not to further restrict the bundling of NAS by audit firms should consider whether such

restrictions could have unintended, negative consequences for client firms. Those charged with

firm governance will be interested in our results that suggest that certain types of NAS can

improve firm operations and lower risk without sacrificing financial reporting quality. Lastly,

academics interested in studying the relation between auditing and NAS will be interested in our

study as it underscores the importance of more broadly considering the potential costs and

benefits to the client firm of the joint provision of audit and NAS in future research.

35

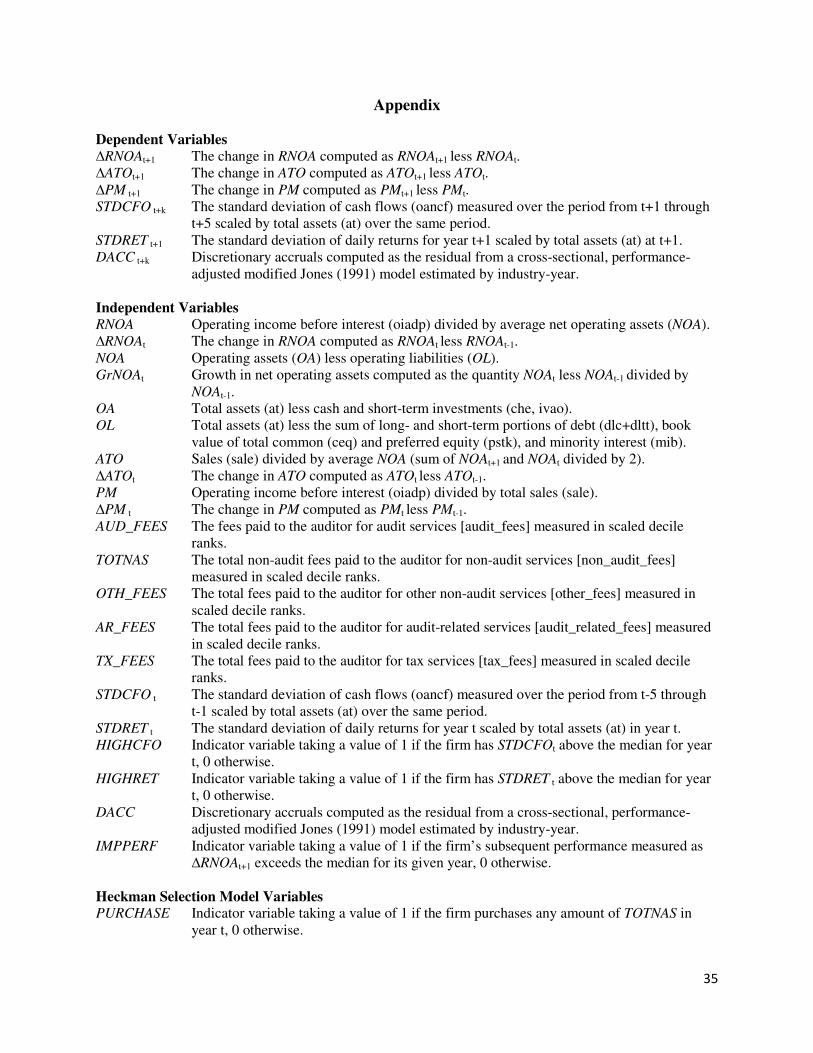

Appendix

Dependent Variables

∆RNOAt+1 The change in RNOA computed as RNOAt+1 less RNOAt. ∆ATOt+1 The change in ATO computed as ATOt+1 less ATOt. ∆PM t+1 The change in PM computed as PMt+1 less PMt. STDCFO t+k The standard deviation of cash flows (oancf) measured over the period from t+1 through

t+5 scaled by total assets (at) over the same period. STDRET t+1 The standard deviation of daily returns for year t+1 scaled by total assets (at) at t+1. DACC t+k Discretionary accruals computed as the residual from a cross-sectional, performance-

adjusted modified Jones (1991) model estimated by industry-year. Independent Variables

RNOA Operating income before interest (oiadp) divided by average net operating assets (NOA). ∆RNOAt The change in RNOA computed as RNOAt less RNOAt-1. NOA Operating assets (OA) less operating liabilities (OL). GrNOAt Growth in net operating assets computed as the quantity NOAt less NOAt-1 divided by

NOAt-1. OA Total assets (at) less cash and short-term investments (che, ivao). OL Total assets (at) less the sum of long- and short-term portions of debt (dlc+dltt), book

value of total common (ceq) and preferred equity (pstk), and minority interest (mib). ATO Sales (sale) divided by average NOA (sum of NOAt+1 and NOAt divided by 2). ∆ATOt The change in ATO computed as ATOt less ATOt-1. PM Operating income before interest (oiadp) divided by total sales (sale). ∆PM t The change in PM computed as PMt less PMt-1. AUD_FEES The fees paid to the auditor for audit services [audit_fees] measured in scaled decile

ranks. TOTNAS The total non-audit fees paid to the auditor for non-audit services [non_audit_fees]

measured in scaled decile ranks. OTH_FEES The total fees paid to the auditor for other non-audit services [other_fees] measured in

scaled decile ranks. AR_FEES The total fees paid to the auditor for audit-related services [audit_related_fees] measured

in scaled decile ranks. TX_FEES The total fees paid to the auditor for tax services [tax_fees] measured in scaled decile

ranks. STDCFO t The standard deviation of cash flows (oancf) measured over the period from t-5 through

t-1 scaled by total assets (at) over the same period. STDRET t The standard deviation of daily returns for year t scaled by total assets (at) in year t. HIGHCFO Indicator variable taking a value of 1 if the firm has STDCFOt above the median for year

t, 0 otherwise. HIGHRET Indicator variable taking a value of 1 if the firm has STDRET t above the median for year