NAPRA Annual Report forweb - nepra.org.pk Reports/Annual Report 2002... · Producers (SPPs) did not...

45

1

Transcript of NAPRA Annual Report forweb - nepra.org.pk Reports/Annual Report 2002... · Producers (SPPs) did not...

1

2

3

4

5

TABLE OF CONTENTS

S. No.

PARTICULARS Page Nos.

1. Foreword IX 2. Mission Statement XI

PART-I

3. Activities of the Year in Review 1 4. Regulatory Procedure 1 5. Licenses to Electric Power Generation Companies 2 6. Generation Licenses to Small Power Producers (SPPs) 2 7. Generation Licenses to Independent Power Producers (IPPs) 2 8. Generation Licenses to Chashma Nuclear Power Plant (Chashnup) 3 9. Transmission Licenses to the National Transmission and Dispatch

Company (NTDC) and Special Purpose Transmission License to KESC 3

10. Tariff 3 11. Automatic Tariff Adjustment (ATA) 3 12. Ex-WAPDA Distribution Companies (DISCOs) – (ATA) 4 13. KESC – (ATA) 4 14. Structural Adjustment of Tariff

Ex-WAPDA Distribution Companies (DISCOs) 5

15. KESC 5 16. Real Return on Assets 8 17. Tariff Determination for Small Power Producers (SPPs) 8 18. Privatization 8 19. Restructuring of WAPDA 10 20. Industry and Market Structure 11 21. Performance Standards for Transmission Company 13 22. Eligibility Criteria 13 23. Performance Standards for Distribution Companies 14 24. Performance Standards for Generation Companies 14 25. Grid Code Guidelines 14 26. Distribution Code Guidelines 15 27. Procedures and Standard for Investment Pogramme 15 28. Enviromental Standards 15 29. Complaints 15 30. Complaints/Court Cases handled during the year 16 31. Administration and Financial Organization of NEPRA

NEPRA Service Regulations 17

32. Computer Usage 18 33. Library Services 18

6

34. Recruitment/Appointment 18

35. Anticipated Development in 2003-2004 Licences

18

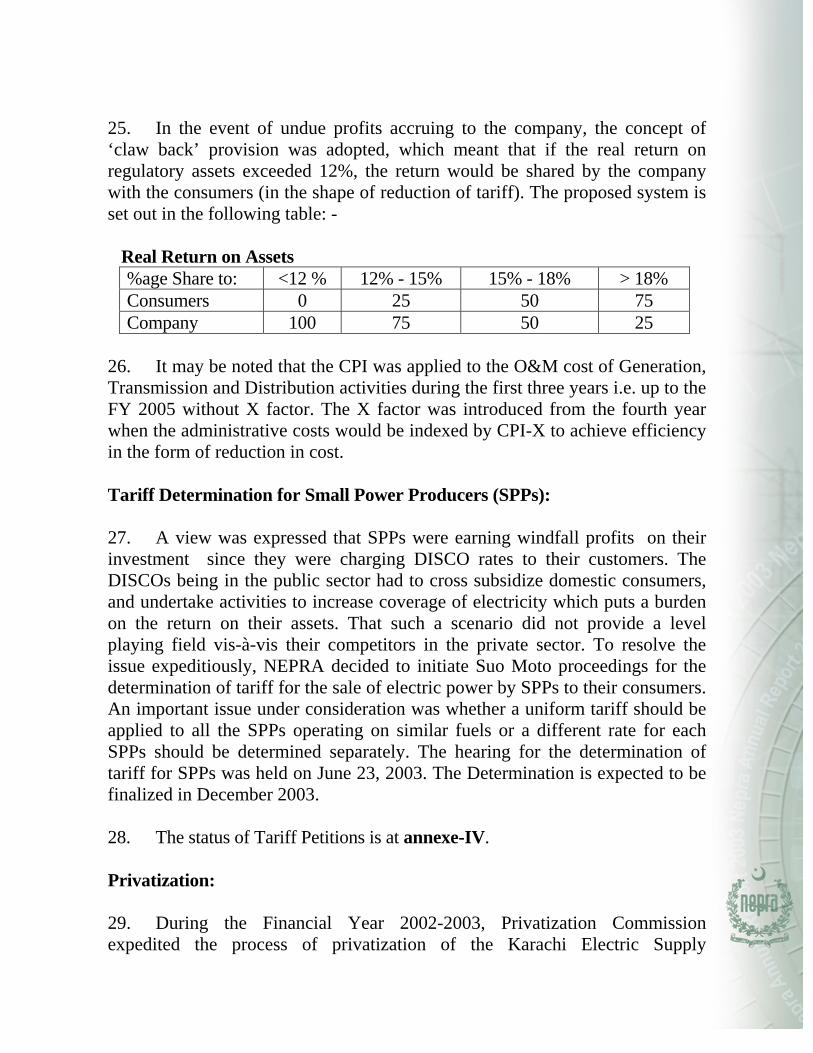

36. Tariff 18

PART-II

37. Regulatory Aspects of Power Sector Reform 20 38. Private Investment 21 39. Improving Energy Efficiency and Lowering Costs 22 40. Universal Service 23 41. Maximizing Government Revenue 24 42. Quality of Service 24 43. Research and Development 25 44. The Regulatory Framework 25 45. Capacity Building for Regulatory Institution 27 46. Federal and Provincial Regulatory Regime 29

Annexes

47. Annexe-I

List of Small Power Producers Granted Generation Licences 31

48. Annexe-II List of Independent Power Producers

32

49. Annexe-III List of Licenses Issued During July 1, 2002 to June 30, 2003

33

50. Annexe-IV Status of Tariff Petitions

34

7

GLOSSARY OF ABBREVIATIONS 1. ADB Asian Development Bank 2. BPC Bulk Power Consumer 3. DISCO Distribution Company 4. FESCO Faisalabad Electric Supply Company 5. GENCO Generation Company 6. GOP Government of Pakistan 7. GWh Gigawatt per hour 8. IBRD International Bank for Reconstruction and Development 9. ICI Imperial Chemical Industries 10. IEC International Electro-Technical Commission 11. IFC International Finance Corporation 12. IPP Independent Power Producer 13. IRG International Resources Groups 14. KESC Karachi Electric Supply Corporation (Ltd.) 15. kV Kilo Volt 16. kWh Kilowatt per hour 17. LAN Local Area Network 18. LUMS Lahore University of Management Sciences 19. MW Megawatt 20. NEPRA National Electric Power Regulatory Authority 21. NESPAK National Engineering Services of Pakistan 22. NGC National Grid Company 23. NTDC National Transmission and Dispatch Company 24. PC Privatization Commission 25. PEPCO Pakistan Electric Power Company Limited 26. PPIB Private Power and Infrastructure Board 27. PSDP Power Sector Development Project 28. PSI Pakistan Standards Institute 29. SPP Small Power Producer 30. TOKTEN Transfer of Knowledge Through Expatriate Nationals 31. UAAR University of Arid Agriculture Rawalpindi 32. UNDP United Nations Development Programme 33. WAPDA Water and Power Development Authority 34. WB World Bank

8

9

FOREWORD A desirable objective of a regulatory body is to develop the citizen’s confidence and trust in the law protecting his rights and interests. This has to be achieved while keeping in conformity with the demands of law i.e. the Act, NEPRA rules and the relevant clauses of the Constitution of Pakistan. The overall economic policy framework of the Government has to be taken into consideration in consistency with the Act. In performing its functions NEPRA has to maintain a wholesome balance between the most often conflicting interests of various stakeholders. In a short evolutionary period of eight years, NEPRA has achieved both. 2. In the absence of a Chairman during the year under review, NEPRA continued to function in pursuit of its regulatory objectives. It adopted consultative approach mainly through public hearings in which stakeholders participated with increasing interest. The quality of interventions has shown visible improvement from the advocacy groups and other stakeholders. The main focus of NEPRA’s activities during the year was on issue of licenses, tariff setting, development of standards for quality of service as well as measures for the competitive trading arrangement. Its approval of the Multi-Year Tariff (MYT) for KESC is the first ever in the electricity sector in South Asia. The pass through of fuel prices has been allowed on a quarterly basis to the public utilities. The foundations of competitive trading arrangements were worked out to be incorporated in the NTDC license. For achieving all this important work technical assistance was provided by the international consultants and donor agencies, which is duly acknowledged. Firm commitment by the Government to maintain the autonomy of the regulator as well as to provide assistance in its capacity building has provided encouragement to the Authority to pursue its regulatory objectives with a high degree of professionalism and integrity. 3. The report highlights some of the regulatory issues, which are important for the sustainability of the electricity reform. These have been included in the report to create an awareness of the reform issues and to provide a clear perspective among the stakeholders of the decisions taken by the regulator. The rationale of some of the hard policy decisions required to provide efficient services and affordable electricity to the country would lead to wider acceptability of the reform process. 4. It is hoped that with the expeditious restructuring of WAPDA into financially and administratively independent entities, and subsequent

10

privatization of some of these companies as well as KESC, the power producers shall now be able to tread the path of healthy competitive growth. Competition in the generation part of the power sector will thus be contributing positively towards national development as well as provision of reliable electricity at an affordable price. 5. We are conscious of the regulatory issues at the regional and international levels and their applicability in the development of an efficient power sector. We are also continuously providing our input in the formulation of power sector policies so that better coordination is established among the policy makers, regulators and utility managers. In order to meet this challenge the Authority is continuously striving for capacity building in which the World Bank has come forward with significant assistance as part of a package of assistance for human resource development to the Government of Pakistan. 6. The report gives the Council of Common Interests, Government of Pakistan, and the readers at large an overview of the NEPRA activities from 1st July 2002 to 30th June 2003, and some of the associated regulatory issues. January 21, 2004 Chairman

11

12

PART - I

ACTIVITIES OF THE YEAR IN REVIEW

Regulatory Procedure The regulatory framework consists of a quasi-judicial authority for the issue of licenses, tariff setting, maintaining standards for quality of service, introduction of measures which yield competition in the competitive segments of the power sector and to act as surrogate for competition in areas of natural monopoly. 2. The cornerstone of regulatory procedure is to adopt consultative approach mainly through public hearings in which all stakeholders are allowed to participate. The proceedings enable the general public to vent their feelings on the poor quality of service provided to them. The public utility is able to put across its’ viewpoint regarding its constraints to operate on the basis of commercial considerations, and that they are not in a position to cover their costs from the tariff allowed to them. This debate provides an avenue to balance the expectations of the service provider, and the general public on the basis of legitimate considerations. The regulator is provided a wider base of information on the basis of which it can makes its determinations. It also enables it to establish a pro-active contact with the stakeholders to achieve its’ objectives of growth, efficiency and equity. The Authority’s decisions contain reasons which are recorded in detail in its’ determinations. These are available for public upon request, in the manner prescribed by the rules. Licences: 3. NEPRA grants licences for generation, transmission and distribution of electricity. Licences are issued in conformity with the rules framed by the NEPRA, and notified by the Federal Government. Hearings are conducted prior to the grant of each licence and the views of all the stakeholders are duly addressed by NEPRA in its determinations.

13

Details of various licensing activities undertaken during the year are as follows: - Licences to Electric Power Generation Companies: 4. During the period July 2002 – June 2003, NEPRA granted generation licences to four companies. The three WAPDA successor generation companies (GENCOs), namely Jamshoro Power Company Limited (1054 MW), Central Power Generation Company Limited (1655 MW), and Northern Power Generation Company Limited (1921 MW) were granted licenses on July 1, 2002. The Karachi Electric Supply Company (KESC) was granted licence on November 18, 2002. Generation Licences to Small Power Producers: 5. The 1994 Power Policy, provided incentives to the private sector to invest in the generation of electricity. Consequently, a number of small power generating units were established by the industrial units to meet their own requirements, and in some cases their surplus power was sold to a few other industrial consumers in the adjoining areas. However, these Small Power Producers (SPPs) did not sign any bilateral contract with WAPDA for the sale of electricity. Until now, NEPRA has granted generation licences to 15 Small Power Producers for a total installed capacity of approximately 240 MW, and cases of remaining SPPs are under process. A List of Small Power Producers issued licences so far is at annexe-I. Out of the 15 SPPs granted the generation licence, 9 have also applied for the grant of distribution licence. Generation Licence to Independent Power Producers (IPPs): 6. NEPRA, upto 30th June 2003, received licence applications from 16 Independent Power Producers (IPPs), that were established in response to the GOP’s 1994 Power Policy. Four applications are yet to be admitted. For the processing of applications of the remaining twelve IPPs, 6 public hearings were held. Draft licence was circulated amongst all the stakeholders including the IPPs prior to these hearings. The licence based on the outcome of these hearings is expected to be issued by September 2003. The list of IPPs is at annexe-II.

14

Generation Licence to Chashma Nuclear Power Plant (Chashnup): 7. The NEPRA has received application for the grant of generation licence to the Chashnup. The same was admitted and hearing has been conducted in this case. The generation licence will be granted during the last quarter of the year 2003. Transmission Licence to the National Transmission and Dispatch Company (NTDC) and Special Purpose Transmission Licence to KESC: 8. A Transmission Licence was granted to National Transmission and Dispatch Company (NTDC) on 31 December 2002. Public hearing in the case was held on December 23, 2002, which was attended by all the stakeholders. The licence also included a road map of various phases with regards to the eventual shape the power market structure was expected to take. 9. The application from KESC for a Special Purpose Transmission Licence is under consideration. 10. A list of licences issued during the year is at annexe-III. Tariff: 11. NEPRA is exclusively responsible for determining tariffs, rates, charges and other terms and conditions for electric power services within the country. The procedure to be adopted by NEPRA in order to arrive at tariff determination has been prescribed in the Tariff Standards and Procedure Rules 1998. 12. The tariff setting aims to protect the consumers from monopolistic prices, ensure adequate revenue to the service provider to cover reasonable costs, and earn a reasonable return on its investment, encourage economic efficiency, improve quality of service, and minimize tariff distortions among different consumer categories. Automatic Tariff Adjustment (ATA): 13. The mechanism for adjusting consumer-end tariff of the distribution companies, in order to account for variations in the price of fuel, was notified in the official gazette on December 29, 2001. According to this mechanism, the

15

consumer-end tariff is reviewed every quarter for adjustments on the basis of changes in the fuel prices taken place in the previous quarter. During the year 2002-03, the tariff was adjusted thrice for Ex-WAPDA distribution companies (DISCOs) and twice in the case of KESC. Ex-WAPDA Distribution Companies (DISCOs) – (ATA): 14. Under the prescribed mechanism of ATA, consumer-end tariff of the DISCOs is reviewed on a quarterly basis adjusted for variations in the price of fuel. In FY 2002-03, the consumer-end average tariff was adjusted upward twice in October 2002, and in March 2003 by 6.49 paisa/kwh and 11.79 paisa/kwh respectively. The tariff was reduced by 13.47 paisa/kwh in December 2002, thereby reducing the upward adjustment in FY 2002-03 to only 4.81 paisa/kwh. KESC – (ATA): 15. According to the formula approved by NEPRA, KESC has been allowed quarterly adjustment not only on account of variation in fuel price, but also on the cost of power purchased. KESC in order to avail of this facility, is required to submit an application within the first week of the month succeeding the quarter for which adjustment is required. Within four working days of the receipt of request from KESC, NEPRA usually allows the proposed tariff adjustment. NEPRA, however, makes its determination as soon as possible but no later than one month of the receipt of the application, and intimates the same to the government for notification in the official gazette. The new ATA formula enables KESC to meet its’ revenue requirement on account of increase in its input costs on quarterly basis without any loss of time by following the prescribed regulatory procedure. 16. Two ATA tariff adjustments were made for KESC in the FY 2002-03. The first adjustment in January 2003 provided a relief to the consumers of KESC on account of reduction in tariff by paisa 5.5/kwh while the second adjustment in April 2003, provided an increase of paisa 18.76/kwh in the tariff.

16

Structural Adjustment of Tariff: Ex-WAPDA Distribution Companies (DISCOs): 17. Pursuant to Rule 3 of Tariff Standard and Procedure Rules-1998, WAPDA, on behalf of its distribution companies, filed a petition for upward revision of the base consumer-end tariff. NEPRA admitted the petition on May 10, 2002 and held public hearing on June 20-22, 2002. There were 17 interveners. The tariff determination for average increase of 40 paisa/kwh was made on July 17, 2002. The Government of Pakistan, however, filed a request to NEPRA to reconsider its determination of this tariff under Section 31(4) of NEPRA Act on account of their reasoning that the consumers were unable to bear such substantial increase in tariff in one setting. NEPRA as a result of this petition restricted the average increase in tariff to 33 paisa/kwh as against the original average increase of 40 paisa/kwh. KESC: 18. KESC on February 12, 2002 filed a tariff petition for an increase in its base tariff by 47.5%. Later, KESC requested that the proceedings of the petition may be put on hold as the petitioner wanted to submit a revised petition as directed by the Privatization Commission of the Government of Pakistan. The revised petition was filed on May 22, 2002, in which the petitioner requested for an increase of 16% in the average tariff, and approval for a Multi-year formula based tariff for the next 10 years. The Authority admitted the revised petition, and issued a notice on June 4 and 5, 2002 to seek the participation of the stakeholders on the tariff petition. In response thereof, 25 communications and 8 Intervention requests were received and accepted. The public hearing commenced on July 15 to 17, 2002 in Islamabad. 19. In view of the logistic problems of the general public from Karachi to participate in the public hearings held in Islamabad, the Authority held an open session at Karachi on 21st and 22nd of August 2002. 20. The salient features of the Multi-year formula based tariff are as under: -

(i) Indexation of O&M cost of generation (excluding fuel cost), transmission and distribution segments of the tariff by the application of CPI.

17

18

Application of CPI-X on O&M cost component of generation, transmission and distribution activities. (ii) Variations in fuel prices and cost of power purchased to be made

as pass-through on quarterly basis. (iii) Claw-back provision for sharing the profits of the company beyond

a certain limit, between the company and the consumers through reduction in tariff.

21. Against the demand by KESC for an average tariff increase of 16% in the existing base tariff, the Authority accorded approval for raise in average power tariff by 6.5% only. The overall percentage increase in tariff as demanded by KESC could not be imposed on the consumers at one time. It was anticipated that in case of privatization of KESC, the private investor would be able to not only reduce the T&D losses but also bring in the efficiency in the KESC system, particularly in the generation and distribution segments within 7 years (time initially allowed for MYT). As such, NEPRA showed a pragmatic approach to weigh up future profits against initial losses. 22. The approval of Multi-Year Tariff (MYT) as per Authority’s determination on September 10, 2002 is the firstever permitted in the power sector in South Asia. The World Bank has shown appreciation for adopting the new concept in Pakistan by describing it, “As the first serious attempt in South Asia to create a comprehensive MYT system for an electricity company”. 23. In its determination, the Authority fixed the tariff of KESC for the next 7 years subject to adjustment on account of the following: -

(i) Variation in fuel price (ii) Variation in cost of power purchased (iii) Indexation of Generation, Transmission and Distribution

component of the tariff excluding (i) above, as per CPI. (iv) Claw back provision.

24. The Transmission and Distribution (T&D) losses, which were recorded as 40% were assumed to be reduced by 5% annually during the next two years. The target of T&D losses was set at 15% over a 10-year period due to the expected investment in upgrading and modernization of the system by the prospective buyer, in case of privatization of KESC. The target of receivables was set to a level of 25% of annual revenue billed for the FY 2002-03 and 16% for the FY 2003-04.

19

25. In the event of undue profits accruing to the company, the concept of ‘claw back’ provision was adopted, which meant that if the real return on regulatory assets exceeded 12%, the return would be shared by the company with the consumers (in the shape of reduction of tariff). The proposed system is set out in the following table: - Real Return on Assets

%age Share to: <12 % 12% - 15% 15% - 18% > 18% Consumers 0 25 50 75 Company 100 75 50 25

26. It may be noted that the CPI was applied to the O&M cost of Generation, Transmission and Distribution activities during the first three years i.e. up to the FY 2005 without X factor. The X factor was introduced from the fourth year when the administrative costs would be indexed by CPI-X to achieve efficiency in the form of reduction in cost. Tariff Determination for Small Power Producers (SPPs): 27. A view was expressed that SPPs were earning windfall profits on their investment since they were charging DISCO rates to their customers. The DISCOs being in the public sector had to cross subsidize domestic consumers, and undertake activities to increase coverage of electricity which puts a burden on the return on their assets. That such a scenario did not provide a level playing field vis-à-vis their competitors in the private sector. To resolve the issue expeditiously, NEPRA decided to initiate Suo Moto proceedings for the determination of tariff for the sale of electric power by SPPs to their consumers. An important issue under consideration was whether a uniform tariff should be applied to all the SPPs operating on similar fuels or a different rate for each SPPs should be determined separately. The hearing for the determination of tariff for SPPs was held on June 23, 2003. The Determination is expected to be finalized in December 2003. 28. The status of Tariff Petitions is at annexe-IV. Privatization: 29. During the Financial Year 2002-2003, Privatization Commission expedited the process of privatization of the Karachi Electric Supply

20

21

Corporation, one GENCO and one DISCO namely Faisalabad Electric Supply Company (FESCO), and Jamshoro Power Company (JPC) Ltd., respectively. It is expected that private sector management will introduce the discipline required to improve the efficient supply of electric power as well as bring in financial and technical resources to upgrade the system. Unfortunately, the Iraq War and continued travel restrictions deterred investors, and the KESC sale notices received scant attention. The JPC has submitted a tariff petition that is under review, and is shortly expected to come up for hearing. The culmination of these efforts is expected to be an important opportunity for NEPRA to provide direction to the power sector reform. Restructuring of WAPDA: 30. The generation part of the restructured power wing of WAPDA comprises four thermal power companies, and one WAPDA hydro power organization as detailed below: -

(i) Jamshoro Power Company Limited (JPCL) (ii) Central Power Generation Company Limited (CPGCL) (iii) Northern Power Generation Company Limited (NPGCL) (iv) Lakhara Power Generation Company Limited (LPGCL) (v) The WAPDA Hydro Electric, will remain with WAPDA

31. The distribution part of the power wing has been restructured into the following distribution companies: -

(i) Lahore Electricity Supply Company Ltd. (LESCO) (ii) Faisalabad Electricity Supply Company Ltd. (FESCO) (iii) Gujranwala Electricity Power Company Ltd. (GEPCO) (iv) Multan Electricity Power Company Ltd. (MEPCO) (v) Islamabad Electricity Supply Company Ltd. (IESCO) (vi) Peshawar Electricity Supply Company Ltd. (PESCO) (vii) Hyderabad Electricity Supply Company Ltd. (HESCO) (viii) Quetta Electricity Supply Company Ltd. (QESCO) (ix) Tribal Electric Supply Company Ltd. (TESCO)

32. The transmission part of the power wing will be owned and controlled by the National Transmission and Despatch Company (NTDC) in the public sector.

22

Industry and Market Structure:

33. In order to facilitate the creation of competitive electricity market, NEPRA, in its NTDC license issued on 31 December 2002, incorporated a roadmap for it’s development besides issuing a draft Transition Order as a consultative document. 34. The NTDC licence and the supporting Draft Transition Order envisage the following market structure: Phase I: Existing Arrangement to Single Buyer Plus Arrangement 35. The existing arrangement will be transformed into the single buyer plus arrangement from July 1, 2004. The following operating environment and facilities should exist by that time.

• All GENCOs, DISCOs and Transmission Companies to be independent corporate entities having distinctly separate Financial and Management status.

• All Gencos, Discos and Transmission Companies to obtain license to operate from NEPRA.

• Separate costs and tariffs for Generation and Transmission Companies.

• NTDC to have no financial or management interest in Generation or Distribution business.

• Establish a System Operator, Central Power Procurement Agency(CPPA), Transmission Network Operator, Contract Registrar and Power Exchange Administrator within the NTDC.

36. Phase II and III: Moving from Single Buyer plus to a Competitive Bilateral Contract Market 37. The single buyer plus arrangement is expected to be transformed into a competitive trading arrangement by July 1, 2009. It is extendable to July 1, 2012, if considered appropriate by NEPRA in consultation with the Federal Government and all licensed pool operators. For the Competitive Trading Bilateral Contract market the following facilities will be completed:

23

• Metering facilities with DISCOs and Bulk Power

Consumers(BPCs) and in power purchase for NTDC. • Infrastrucure including hardware and software facilities to

prioritise and schedule contracts. • Human resources/skills to administer contracts.

38. The NTDC has been directed in the NTDC licence to facilitate the establishment and functioning of a “Single Buyer Plus”(SBP) trading arrangement by not later than July 1, 2004. The NTDC has also been directed to bring for the Authority’s approval its organisational restructuring plan within one hundred and eighty (180) days from the grant of the licence to establish:

(i) a “Central Power Purchasing Agency” (CPPA) for the procurement of power on behalf of ex-WAPDA DISCOs;

(ii) a “System Operator” for the safe and reliable operation, control switching and dispatch of transmission system and the generation facilities and provision of balancing services;

(iii) a “Transmission Network Operator” for the operation and maintenance (O&M) of transmission system including planning, design and capacity expansion of its transmission system, generation expansion, least cost planning and citing of new generation facilities;

(iv) a “Contract Registrar and Power Exchange Administrator”(CRPEA) for the recording and notification of contracts and other matters relating to bilateral trading between the generation licensees and the BPCs and between the generation licensees and the distribution companies for their future capacity needs. The CRPEA shall also handle a financial settlement system in close coordination with the System Operator for balancing the market and for settlement of differences arising with CPPA.

39. After the Competitive Market Operation Date (CMOD) the NTDC shall continue to be a party to the trading arrangements prior to the CMOD in its capacity as a system operator and ancillary services provider and comply with commercial code governing those arrangements which were undertaken during the transition period.

24

40. In order to finalise the determination for the NTDC licence, NEPRA requested early decision on the following issues from the Federal Government:

(i) Assignment of contracts of IPPs. (ii) Arrangement regarding capability of financially weak

DISCOs to discharge their payment obligation to the NTDC in case of uniform retail sale tariff.

(iii) Complete functional independence of ex-WAPDA DISCOs and GENCOs in financial and administrative terms.

41. NEPRA is of the view that clarification of above issues is important to enable it to undertake regulatory responsibilities for the restructuring of the power sector. Standards and Codes: PERFORMANCE STANDARDS FOR TRANSMISSION COMPANY: 42. As per NEPRA Act, NTDC is responsible for the transmission interconnection and services of electric power in a safe, efficient and reliable manner on a non-discriminatory basis. As per Section 34 and Section 7 (2) (c) of NEPRA Act, NEPRA has to prescribe Performance Standards for Transmission based upon the existing system conditions, planning and operating criteria as provided in the Grid Code, status of the transmission system, comparison with international standards, and considering the Stakeholders’ view point. The work on the development of Performance Standards for Transmission Companies started in July 2000. A draft report was prepared, and presented to the Authority for discussion and approval at the end of Year 2001. The report is under the Authority’s review for approval, and circulation among the Stakeholders for comments. The report is expected to be finalized by the end of June 2004. Eligibility Criteria: 43. For the non-discriminatory provision of distribution service and sale of power to all the consumers within the service territory of a distribution company, the Authority has laid down Consumer Eligibility Criteria, notified by the Federal Government. The Criteria recognizes the right to receive electricity supply of all those consumers who fulfill certain conditions and

25

follow specific procedural requirements as laid down in this criteria before applying for their electrical connections. The Criteria also makes the distribution company responsible to expand and reinforce its distribution system while allowing it to collect relevant connection charges subject to NEPRA approved terms and conditions. PERFORMANCE STANDARDS FOR DISTRIBUTION COMPANIES: 44. As per NEPRA Act, NEPRA has to prescribe Performance Standards for Distribution Companies with respect to reliability, quality, efficiency and safety of electric power services provided by the Distribution Companies. 45. After taking into consideration the comments of all the Stakeholders, a final draft was approved in April 2003. The prescribed Performance Standards (Distribution) along with the determination from the Authority are being forwarded to the Government for approval and notification in its official gazette. PERFORMANCE STANDARDS FOR GENERATION COMPANIES: 46. The Generation Companies are responsible for safe, efficient and reliable electric power at least cost for supply to NTDC for onward delivery and sale to DISCOs. As per Section 34 of the Act, NEPRA has to prescribe Performance Standards for Generation Companies. Work on the Performance Standards for Generation is expected to be completed by Mid-2004. GRID CODE GUIDELINES: 47. Under the provisions of its Transmission Licence, NTDC is responsible for developing a Grid Code for the smooth and effective functioning of its bulk transmission system, and that of other licensees that will be connected to its bulk transmission system. 48. PEPCO draft alongwith the BPI (ADB consultants) comments are under review and discussion by NEPRA and PEPCO at this stage. The final Grid Code is expected to be completed, and approved by NEPRA by March 2004.

26

DISTRIBUTION CODE GUIDELINES: 49. As per NEPRA Act and Distribution Licensing (Rules) 1999 and provision of distribution licences, Distribution Companies are responsible to prepare Distribution Code, covering all technical and operational aspects of distribution system, and their interface relationship with NTDC, other Distribution Companies, BPCs, and other Users connected to its distribution system. Distribution Code Guidelines were provided to PEPCO by NEPRA in April 2000. The PEPCO submitted its first draft in December 2000, which was commented upon by NEPRA, and reviewed by ADB/BPI Consultants. PEPCO re-submitted its revised (2nd) draft in September 2002 which is under consideration/ review by NEPRA, and is expected to be completed by June 2004. PROCEDURES AND STANDARD FOR INVESTMENT PROGRAMME: 50. Under NEPRA Act, the Authority is required to prescribe procedures and standards for the Transmission and Distribution Companies Investment Programmes. The purpose of prescribing the standards is to lay down criteria according to which the investment plan of various electric power network companies shall be examined, and approved by the Authority. The draft reports for Distribution and Transmission Companies have been prepared by the Authority for circulation among the stakeholders. ENVIRONMENTAL STANDARDS: 51. No separate environmental standards have been prescribed by NEPRA but have endorsed the standards prescribed by the Federal Government and all the licensees shall follow the Federal Government, Environmental Protection Agency's prescribed Standards. COMPLAINTS: 52. The Consumer Affairs Division of NEPRA has increased its usefulness in view of its positive role of resolving complaints of consumers against the Licensees. In due course, the Consumer Affairs Division would also monitor

27

the Industry Performance Standards that have been prescribed by NEPRA; and to entertain and redress any complaints in this regard. To achieve its objectives, an electronic system is expected to be established and maintained so as to record all the consumers complaints, the action taken on it and any follow up required. 53. In the FY 2002-2003, one hundred and seventy two (172) complaints were received by NEPRA from consumers all over the country. This was a significant increase in the number of complaints over the previous year, and may be attributed to increasing awareness amongst the public of NEPRA’s role in the handling of complaints. Most of the complaints filed with NEPRA came under the purview of the Provincial Offices of Inspection (POI) or the utility itself. NEPRA referred such complaints to the concerned offices and pursued them until the issues were resolved. Complaints/Court Cases Handled During the Year: 54. Details of the complaints and the court cases dealt with in the financial year 2002-2003 are given below: Complaints:

Area Complaints Received

Complaints Disposed Off

Lahore 15 15 Multan Nil Nil Faisalabad 14 14 Gujranwala 3 3 Islamabad/Rawalpindi 87 87 Karachi 18 18 Hyderabad 23 23 Peshawar 9 9 Quetta 3 3 Total 172 172

28

Detail of the Court Cases:

Court Notices Received from the Court

Disposed Off by the Court In Process

Lahore High Court

18 16 2

Senior Civil Judge 1 - 1 Civil Judge Faisalabad

1 - 1

Administration and Financial Organization of NEPRA: NEPRA Service Regulations: 55. In pursuance of Section 10(1) and 47(2) of the NEPRA Act, the Authority is empowered to make regulations consistent with the provisions of the Act, for defining the terms and conditions of the service of its staff. The Authority has approved NEPRA Service Regulations (2003) which were notified in the Official Gazette of Pakistan vide S.R.O. No. 544(1)/2003. NEPRA Service Regulations cover the following:

i. General Provisions ii. Service of the Authority iii. Appointments iv. Posting, Transfer and Training v. Promotion vi. Annual Assessment Report of Employees vii. Leave viii. Gratuity ix. Provident Fund x. Transportation xi. Travelling xii. Medical Care Facilities xiii. Efficiency and Discipline xiv. Other Benefits

29

Computer Usage: 56. NEPRA in order to make use of Information Technology has established a Local Area Network (LAN) of 48 nodes in its Main office. It is providing professionals a common platform of sharing information along with the facility of accessing internet and e-mail. Presently, NEPRA has one dedicated dial-up connection for Server and Five connections for independent users. The process to upgrade the connection through DSL (Digital Subscriber Loop) or satellite links is being undertaken. Library Services: 57. NEPRA Library has acquired books for the specialized needs of the regulator. The library, in addition to about 2500 books, subscribes 7 journals and 5 magazines. It has also obtained reference books such as International Electro-Technical Commission (IEC) standards, Pakistan Standard Institute (PSI), Pakistan Law references, and other legal documents. Recruitment/Appointment: 58. NEPRA has adopted a transparent procedure to recruit its’ professional staff. Posts are advertised with specific job requirements. The Authority however, faces difficulties in the recruitment of competent professional staff due to the shortage of skills in infrastructure regulation. Anticipated Developments in 2003-2004: LICENCES: 59. Applications for distribution licences by a number of SPPs are under consideration of the Authority and a decision is expected in 2003-04. Besides, a Special Purpose Transmission License to KESC alongwith generation licences to Chashnup and the remaining IPPs are also expected to be granted in 2003-04. TARIFF: 60. In pursuance of the requirement under the licence the licensees were required to get their tariffs approved from NEPRA. Accordingly three thermal generation companies, one hydro generation company and National Transmission

30

and Dispatch Company (NTDC) have filed petitions for determination of their tariffs pursuant to Rule 3(2) of Tariff Standards and Procedure Rules. The tariff determination on these cases by the Authority is expected in 2003-04. 61. The tariff petition filed by NTDC for determination of its wheeling charges has also been admitted, and notices to all stakeholders have been given. The determination, which is expected in FY 2003-04, would establish the transfer tariff from generation to distribution licensees through NTDC for the transition period from the existing arrangement to a competitive market. 62. The determination of tariff for Small Power Producers is expected in the year 2003-04 besides a determination on Security Deposits and System Development Charges for KESC.

31

PART-II

I. Regulatory Aspects of Power Sector Reform:

Power Sector Reform in Pakistan, as in other parts of the world, has led to organizational ‘unbundling’ of electricity supply into three productive activities generation, transmission and distribution. The reorganization has enabled the regulator to implement the NEPRA Act by developing alternative ‘market’ structure for each segment of the power sector. Accordingly, generation licence is issued to a person to construct, own or operate a connected generation facility (Section 15). Such an arrangement not only provides space for the private sector in the generation activity but also lays the foundation for the establishment of a competitive wholesale market for power. The transmission license is issued only to the National Grid Company (Section 17) in the public sector. The national grid company shall, however, be responsible to operate transmission and inter-connection services on a non-discriminatory basis (Section 18). The distribution licence contains exclusivity of distribution services over a period of time as determined by the Authority (Section 20, 21). The transmission and distribution facilities are therefore treated as ‘natural’ monopolies subject to regulatory oversight and control. The power sector reform has been initiated to attract private investment to improve the technical and financial performance of the sector, and to free budgetary resources for other development needs of the country. The reform process has created a flurry of activity as foreign and domestic investors, financial advisers, advocacy groups have all responded to seize opportunities arising out of a new liberal environment. 2. Our electric power sector owned and controlled by the government has remained constrained for various reasons and has not been able to meet the socio-economic needs of the country. In the last few years it has also tied up substantial budgetary resources to undertake extensive financial and capital restructuring of the public sector utilities. WAPDA and KESC are beset with problems associated with public utilities such as high electrical losses, collection inefficiency, over staffing, poor reliability of service, and in recent years yielding low or negative return on assets. The reform process has been initiated with an expectation that the power sector would eventually become an efficient engine of socio-economic development. This initiative, however, requires explicit articulation of the reform objectives and maintaining a balance

32

among competing interests for the benefit of all stakeholders. Some of the important issues for the sustainability of reform process are highlighted below:-

(i) Private Investment: Attracting private investment in the creation of new generation capacity is often the single most important objective of the initial phases of electricity reform. Our 1994 Power Policy has been successful in increasing thermal generation capacity through Independent Power Producers (IPPs), though the pricing arrangements and other clauses of the Implementation Agreements and Power Purchase Agreements have aroused substantial controversy. As a corollary to the increase in thermal generation capacity, the transmission and distribution systems have not received the much needed investment, thereby, creating constraints in the balanced development of the power system. The regulator has to stimulate investment by, inter alia, setting tariffs in each segment of the power sector which cover all prudently incurred costs. The regulator, during the transitional stage, has to walk on a tight rope to ensure that the consumers (with the assistance of the government) are not subjected to volatility in prices (frequent changes but not those related to tariff setting on account of economic principles), and the investors have been allowed a fair return on their investment. The full impact of the reform process could only be realized if the effort towards rational tariff adjustment moved in tandem with the speedy and efficient restructuring of the power sector.

The need to promote private sector is an important consideration in the reform process. This, inter-alia, stimulates market activity wherever it is possible. Any over regulation, however, needs to be avoided since it may prove counter productive. It is with this objective that NEPRA determined a uniform tariff for Small Power Producers (SPPs) instead of determining separate tariff for each licensee. The customers of SPPs therefore always have a choice to leave their supplier and move to the utilities if their prices were not competitive. The resetting of consumer end tariff should reflect cost of service. This is important since prices close to their cost of service provide appropriate signals on how electricity would be consumed, and by whom. It also gives appropriate signals to the suppliers when and

33

where to enter the market (to expand supply). Having no disagreement on this economic principle, the Authority, however, may initially adopt averaging of generation prices as cost of power purchase to the distribution companies to provide for stranded cost of IPPs. Such arrangement will, however, be of a very short duration (4-5 years) since it is only after this transitional phase, that all parameters will be fully established to maintain regulator’s fundamental role as market maker.

(ii) Improving Energy Efficiency and Lowering Costs:

Lowering energy cost through competition has been an important objective of reform effort. Competition puts a downward pressure on the profit margins of the generators and suppliers, and provides an incentive to reduce cost. As a result, electricity prices under competition tend to be lower. In fact, this has been the most impressive achievement of reform efforts in many parts of the world. The setting up of competitive trading arrangements in our system is going to be rather a long drawn out struggle. The situation in particular is made difficult by the existence of Independent Power Producers (IPPs), which presently constitute about 31% of the total installed generation capacity of 18,500 MW in the country, having guarantees by the government as security for their project agreements. This has imposed a level of inflexibility in the newly created electricity market. The other 30% generation capacity owned by the government is up for sale through breaking up into three separate legal entities (GENCOs). Of these Jamshoro Power Company (1054 MW installed capacity) is up for sale on fast track. It is anticipated that privatization effort would require a long term PPA with at least 5-7 years tariff decided up front. The market share of these GENCOs may allow them to play a dominant role in the market thereby limiting competition. The remaining 30% to 40% generation capacity is hydel, which as a policy decision of the government, is not to be privatized and constitutes cheapest source of electricity partly on account of its’ debt capital being substantially written off. The power sector, therefore, is a hybrid of low cost hydel electricity to high cost thermal generation. The generation cost of the public sector thermal generation plants available for sale can’t be expected to be reduced in the short to medium term on account of the requirements of substantial investment to upgrade the generation

34

facilities. This, however, does not imply that the regulator would wait for the competition to develop in the next few years whose benefits could then be passed on to the consumers. The regulator has to adopt a pro-active policy to make use of every available regulatory tool that can be used in our transitional electricity environment which may lead to superior performance by the regulated entities to the benefit of all key interest groups.

Section 31(2) of NEPRA Act states that the Authority would formulate standards for tariff determination which would, inter alia, ‘encourage economic efficiency in the electric power industry’. This implies that alongside the development of competitive market the regulator could make use of regulatory tools providing incentives (price caps, rate moratoria or earnings sharing etc.) to supply goods at least possible cost. Such an arrangement coupled with strict mandates and regulatory monitoring can benefit the consumer by sharing the cost savings in the form of lower rates or slower rate increase, increase the profitability of the regulated entities and encourage new entrants by minimizing regulatory risk on account of predictability of revenue stream over a reasonable period of time. There is no denying the fact that incentive regulation is aimed at bridging the gap between the restructuring of the regulated monopolies to the development of a fully competitive market economy of the electricity sector.

(iii) Universal Service: Pakistan has a large population which

remains un-served by electricity. There is no doubt that increasing electricity coverage is an important policy objective of the government, but it needs to be balanced with the requirements of restructuring and reform of the power sector. If expansion of service territory is left entirely to market forces, the potential load characteristics of new markets in the rural and far-flung areas, and the costs associated with grid expansion may not provide adequate incentives to the private sector. The government needs to give serious consideration of allocating public funds to increase coverage and exploring options of exploiting new and renewable sources of energy as well as providing electricity through distributed generation systems. The regulator has to ensure that the initiative to increase electricity coverage is not unduly restricted by

35

the exclusivity available to Distribution Licensees under Section 21 of NEPRA Act.

It is important to note that social dimensions of power policy should not be allowed to become a drag on the sustainability of the power sector. What good is low tariffs when there is no electricity in the wires? The reliability of the electricity service is far more important than the price per se. The issue of accessibility of electricity for vulnerable population should be treated as a financing issue and funds should be provided explicitly to support such access. This can be done in terms of tariff subsidies or allocation of development funds by the federal and provincial governments or by levying a surcharge on all consumers.

(iv) Maximizing Government Revenue: Privatization in a given

resource constraint is an attractive policy since alternative policies such as cutting expenditure or raising taxes are not popular. The revenue obtained by privatization, along with decline in the drainage of public funds on account of the deficits of state owned enterprises, can serve to implement development policies with an electoral pay off. The privatization needs of the power sector, however, need to be balanced with the objective of maintaining price stability while moving towards a market economy. The Privatization Commission may be under pressure to maximize sale proceeds of privatized units. It may, however, be noted that the revenue generation of the distribution companies is largely dependent on the price at which these entities are allowed to sell or distribute power by the regulator. Privatization of power sector may, however, not be viewed as a mere exercise in maximizing revenues of the government. The reform process should generate positive social and economic spillover effects. The induction of private sector on reasonable terms would increase competition, efficiency, introduce higher quality and relatively lower cost of electricity services.

(v) Quality of Service: Improving quality of service for consumers

is an important objective of power sector reform. The frequency and duration of outages, voltage and frequency fluctuations, are all problems that affect all types of consumers. There is no denying that

36

the goal has alluded the public utilities due to lack of priority to the issue and the need for additional resources needed to improve the quality of service.

The task before the regulator includes identifying quality of service and setting standards of performance. This is followed by establishing an effective mechanism for monitoring the standards set by the regulator. There is, however, need to be pragmatic in the assessment of local setting in which the performance standards have to operate. In particular, there may be local variation between urban and rural areas. It is important to bear in mind that the level of quality of service has a direct bearing on the cost of service. Improvements in the quality of service may require mobilization of additional resources which may have a direct bearing on the revenue requirement of the service provider. The regulator may use incentive regulation in its tariff determinations to provide incentives and penalties for maintaining quality of service.

(vi) Research and Development: As public ownership gives way

to private enterprise in the power sector, and as the deregulation of regulated segments of the market takes ground, public sector programmes pursuing social objectives are likely to be seriously affected. Such programmes may include new and renewable sources of energy which may have the potential to be installed in far flung and mountainous areas, energy efficiency research programmes, universal service policy initiatives particularly to low income customers and rural areas, consumer protection and awareness programmes etc. Due to hesitation by the private sector the immediate challenge for the regulator is how to expand the role of such programmes in the public sector for development of the power sector which is being increasingly owned and operated by the private sector.

(vii) The Regulatory Framework: GOP’s 1994 Power Policy was

implemented as an adhoc response to power shortages and the inability of the public sector to fund the required investment. There was no doubt that on the basis of liberal incentives provided in the policy, a number of IPPs were established which did increase thermal generation capacity and relieved power shortages. The

37

power purchase agreements guaranteed by the government were, however, expensive and subsequently proved to be politically divisive having an adverse impact on the investment climate in the power sector. The public finances were also subjected to increasing pressure since increasing capacity payments of the IPPs could not be supported by collections at the retail level. The budgetary sources had to substantially contribute towards the revenue requirements of the public utilities.

It is evident that proper sequencing of reform would reduce the chances of costly lapses. The importance of creating enabling conditions, particularly the development of autonomous regulatory institutions, are essential in promoting private investment which may otherwise be hesitant, unreliable and expensive. The regulator, however, has the difficult task of overcoming rigidity, lack of innovation, rent-seeking behavior, and other deficiencies arising out of regulation of public utilities by the government. The regulator has to remove barriers to entry and to actively facilitate competition on account of restructuring of existing power sector enterprises. In the long run, competition may also reduce the need for price regulation except in those segments of the power sector which continue to have substantial market power i.e. transmission grid. The application of the ‘incentive’ or ‘performance based’ price regulation is of growing interest to obtain superior performance from the sector. The monitoring of service quality is important from the point of view of environment, safety and other consumer protection concerns. The enforcement of higher standards may, however, reflect increased costs and higher prices. The regulator has to maintain an arm’s length relationship with the key stakeholders to maintain its autonomy (real or perceived) in its decision making. This is particularly important in its role of determining tariff which the government may be loath to sustain for political considerations. The regulated prices have to be maintained at economic levels. The public utilities, in the initial stages, will come into conflict with the regulator on account of not being used to monitoring or control. This often leads to efforts to ‘capture’ the regulator to undermine its’ ability to provide a level playing field. If such an effort succeeds, it is definitely a setback for the reform effort.

38

(viii) Capacity Building for Regulatory Institutions: The vast majority of regulatory commissions all over the world have three to five members with varied qualifications who are selected on the basis of each countries respected criteria. The State of Arizona of U.S.A requires that a candidate for commissioner “be able to speak, write and read English”. The State of Connecticut statute specifies that “at least three Commissioners must have training or experience in at least one of the following fields; economics, engineering, law, accounting or finance and further, at least two of these fields must be represented on the authority at all times”. The State of Alaska statute, for one, specifies that “one Member must be a graduate of an accredited school of law; one member shall be a graduate of an accredited university with a major in finance, accounting or business administration; and two members shall be consumers”

Section 3, Chapter II of NEPRA Act provides for the establishment of the Authority. Section 3(4) states ‘ Every Member shall be a professional of known integrity and competence with at least fifteen years of related experience in law, business, engineering, finance, accounting, economics or the electric utility business’. The NEPRA Act requires appointment of eminent persons by the Federal Government for Chairman and Members. Such persons may have the experience of public or private service. The government in the initial stages of regulatory experience is likely to be more comfortable with eminent persons retired from public service to be appointed as Members/Chairman of the Authority, as it invokes a trust of legislative responsibility being exercised in public interest. The public service provides diversity of experience with a level of institutional support for human resource development which is often beyond the reach of private sector. The disciplines specified in the Act, to represent in the Authority, are by and large available in abundance in the public service. The power sector has always been the focus of development policy of the government on account of its’ impact on social and economic development of the country. The economic agenda of the government invariably provides exposure of policy issues at the macro management level. They are required to look at achieving economic efficiency by deploying resources to their best use. The higher echelon of public service is invariably exposed to the best

39

available academic training in the world, in their respective area of interest. The personnel appointed from the public sector therefore, bring with them diversity of experience, high level of academic qualification, and a level of experience of dealing with economic and social issues, which may not otherwise be available in the private sector.

The moot point is that the Government should appoint the best persons with independent thinking who are capable of leading the regulatory authority. The Authority, irrespective of the background of its’ Members, need to quickly adapt itself to the objectives of the regulatory legislation. This is important since the regulatory arrangement should not be perceived by the stakeholders as a mere extension of the government, and not an independent body. The regulator has to develop a consultative approach with all the stakeholders particularly the government. It needs to build the confidence of the government to pursue the power sector reform by initiating a number of confidence building measures in that direction. This is important since the reform process has been initiated by the Breton Woods institutions lobby on account of increasing burden of the power sector on the budgetary resources. The leadership qualities of the Authority require regulatory skills to be used with impeccable level of integrity, and a measure of political acumen. Needless to say that the Authority is supported by regulatory staff which is drawn from the best available talent in their respective disciplines required in dealing with complex regulatory issues. Their recommendations provide the basis on which the Authority takes decisions on broader comprehension of issues. The Federal Government is required to appoint regulators as provided in the NEPRA Act from the best available talent in the country or from abroad. It is, however, important to realize that regulation of public utilities, being a new phenomenon, is desperately short in regulatory expertise. By the time a regulator may develop some understanding of the complexities of the sector, his tenure may be over. The hunt for a new regulator often involves long delays in selection of these posts. This seriously affects the smooth and effective functioning of the Authority. The Government may consider providing a period of succession in the

40

retirement of the regulator. This will provide an opportunity to the newly appointed regulators to learn from their more experienced colleagues. At the same time, the large majority of regulators may not retire at the same time since it can cause a void in regulatory expertise thereby causing delay and lowering the quality of regulatory decisions. Infrastructure regulation is a complex task requiring considerable resources. If the human resource is allowed to deplete, then regulation may create more distortions than the market failure which it is supposed to address. Indeed, a dearth of regulatory expertise in the Authority on account of certain legal restrictions may not be in public interest.

II. Federal and Provincial Regulatory Regime: 3. Electricity is on the Concurrent Legislative List of the Fourth Schedule (Entry 34) of the Constitution. Article 157 of the Constitution empowers the Federal Government to construct or cause to construct power generation plants in the country and inter-provincial transmission lines. At the same time the Provincial Governments may: (a) determine tariff for distribution of electricity in the province; (b) lay transmission lines in the province; and (c) to the extent electricity is supplied to a province from the national grid, require supply to be made in bulk for transmission and distribution in the provinces. Any framing of the law regulating electricity industry at the Federal level would have required satisfying the Provincial Governments of the protection of their interests as laid down in the Constitution. In the case of NEPRA Act, this was done by involving the provinces in the initial meetings held by the Minister for Water and Power in January 1997, and subsequently in July 1997 by a Cabinet Sub-Committee headed by the Minister for Finance to frame the NEPRA Act. The establishment of a regulatory Authority at the Federal level has the following advantages in the development of electricity sector at the national level: -

(i) The electricity industry structure was primarily developed at the federal level through funds substantially provided by international lending agencies. The interaction of aid giving agencies with the Federal Government and its public sector utilities for restructuring and privatization of the power sector entities would be easier at the federal level.

(ii) The proliferation of regulatory institutions at the Federal and Provincial level was not desirable on account of resource constraints, and the prospect of spreading too thin an undeveloped

41

regulatory expertise in the country. The restructuring of the power sector would have been affected by the inevitable contentious issues of jurisdiction between the Federal and Provincial authorities.

(iii) Foreign private investors in the electricity sector usually prefer dealing with a single regulatory agency in the country, rather than with multiple agencies with potentially different interpretations of rules and regulations and different perceptions of how the sector should evolve. The uncertainty and risks associated with such a regulatory regime may choke off a significant proportion of potential private investment; foreign or local.

(iv) The setting of rates at retail level in each province would have provided varied perceptions on issues of covering the cost of service. The provincial governments would have found it expedient to pursue social policies by keeping tariff artificially low to attract industry, and to provide relief to the household consumers. Such variation in distribution rates would have distorted the national electricity market.

4. The establishment of regulatory regime at the Federal level allows the provinces to be represented at the decision making level through the appointment of one Member from each province in the Authority. In the case of NEPRA Act, it calls for provincial governments to establish offices of inspection for monitoring safety and quality of electric power services as well as investigating consumer complaints. The NEPRA is providing technical assistance to the provincial governments on drafting of inspection procedures.

42

Annexe-I

List of Small Power Producers Granted Generation Licences

S. No. Name of Company Address Category

Date of Grant of

Licence 1. M/s. Maple Leaf Electric

Company Ltd. 42-Lawrence Road, Lahore SPP 28-07-2001

2. M/s. Sapphire Power Generation Ltd.

149 Cotton Exchange Building, I.I. Chundrigar Road, Karachi.98

SPP 27-08-2001

3. M/s. ICI Pakistan Power Gen Ltd.

ICI House, 63 Mozang Road, P.O. Box 198, Lahore

SPP 27-08-2001

4. M/s. Mahmood Power Generation Ltd.

Mehr Manzil, Lahore Gate, P.O. Box 28, Multan

SPP 22-10-2001

5. M/s. Crescent Powertec Ltd.

Sargodha Road, Faisalabad 7-B-III, Aziz Avenue, Gulberg V, Lahore

SPP 22-10-2001

6. M/s. Ellahi Electric Company Ltd.

Nagina House 91-B-1, M.M. Alam Road, Gulberg-III, Lahore-54660

SPP 22-10-2001

7. M/s. Gulistan Power Generation Ltd.

58-Main Gulberg, Lahore SPP 16-11-2001

8. M/s. Kohinoor Genertek Ltd.

42-Lawrence Road, Lahore SPP 08-12-2001

9. M/s. D.S. Power Ltd. 20-K, Gulberg II, Lahore SPP 08-12-2001

10. M/s. Monnoo Energy Ltd.

Monnoo House, 3- Montgomery Road, Lahore

SPP 08-12-2001

11. M/s. Century Power Generation Ltd.

Lakson Square, Building No. 2, Sarwar Shaheed Road, Karachi

SPP 02-01-2002

12. M/s. Sitara Energy Ltd. 5th Floor, Sitara Tower, Bilal Chowk, New Civil Lines, Faisalabad.

SPP 02-01-2002

13. M/s. Bhanero Energy Ltd.

31-K, Gulberg-II, Lahore 54660.

SPP 31-01-2002

14. M/s. Quetta Textile Mills Ltd.

Nadir House, G/F 1, I.I Chundrigar Road, Karachi.

SPP 31-01-2002

15. M/s. Ideal Energy Ltd. 1088/2 Jail Road, Faisalabad.

SPP 04-04-2002

43

Annexe-II

List of Independent Power Producers (IPPs) Sr. No.

Name of Company Date of Application

Date of Admission

Conference Held On

1. Fauji Kabirwala Power Co. Ltd. 3.5.2000 01.10.2002 ¾.02.2003

2. AES Lal Pir 18.9.2000 08.10.2002 27.02.2003 3. AES Pak Gen 18.9.2000 08.10.2002 27.02.2003 4. Gul Ahmed Energy Ltd. 02.04.2001 03.03.2003 07.04.2003 5. Tapal Energy Ltd. 10.05.2001 03.03.2003 07.04.2003 6. Saba Power 23.05.2001 03.03.2003 07.04.2003 7. TNB Liberty Power Ltd. 10.11.2001 24.03.2003 06.05.2003 8. Habibullah Coastal 25.05.2001 24.03.2003 06.05.2003 9. Uch Power Ltd. 30.07.2001 04.04.2003 24.05.2003 10. The Hub Power Co. Ltd. 17.07.2001 11.04.2003 24.05.2003 11. Rousch Pakistan Power Ltd. 30.7.2001 17.04.2003 05.06.2003 12. Kohinoor Energy Ltd. 15.08.2001 23.04.2003 05.06.2003 13 Kot Addu Power Co. Ltd. 21.06.2001 Not admitted 14. Southern Electric Power Co. Ltd. 15.04.2003 “ 15. Japan Power Ltd. 09.05.2003 “ 16. Altern Energy Ltd. 14.05.2003 “

44

Annexe-III

List of Licences Issued During July 1, 2002 to June 30, 2003 GENCOs: S. No.

Name of Company Date of Application

Date of Admission

Conference Held On

Licence Issued on

1.

Jamshoro Power Co. Ltd. GENCO - 1, TPS, Jamshoro

07-09-2001

18.03.2002 03.06.2002 01.07.2002

2. Central Power Generation Co. Ltd. GENCO-II (WAPDA) Guddoo Thermal Power Station, Kashmore.

23-08-2001 10.04.2002 03.06.2002 01.07.2002

3. Northern Power Generation Co. Ltd. (GENCO-III), 172-WAPDA House, Lahore.

25.05.2001 10.04.2002 03.06.2002 01.07.2002

4. Karachi Electric Supply Co. Ltd. Abullah Aimai House, Abdullah Haroon Road, Karachi.

11.09.2000 26.07.2002 09.09.2002 18.11.2002

NTDC: Sr. No.

Name of Company Date of Application

Date of Admission

Conference Held On

Licence Issued On

1. National Transmission & Despatch Co. Ltd.

10.04.2002 20.11.2002 23.12.2002 31.12.2002

45

Annexe-IV

Status of Tariff Petitions

Sr. #

Name of the

Petitioner

Case No. Date of Filing of Petition

Date of Admission

Determination Issued On

Gazette Notification No. / Issued

On

1 KESC NEPRA/TRF-14/KESC

12.02.2002 21.02.2002 10.09.2002 715(I)/2002 12.10.2002

716(I)/2002 12.10.2002

2 “ “ “ - 06.01.2003 46(I)/2003 3 “ “ - 16.04.2003 4 WAPDA NEPRA/TRF-

15/WAPDA-2002

27.03.2002 10.05.2003 29.07.2002 522(I)/2002 12.08.2002

5 “ NEPRA/TRF-10/MW&P

15.08.2000 - 17.10.2002 821(I)/2002 18.11.2002

6 “ “ “ - 18.12.2002 960(I)/2002 27.12.2002

7 “ “ “ - 29.03.2003 406(I)/2003 09.05.2003

8 Central Power Generation Co. Ltd.

NEPRA/TRF-16/CPGCL-2003

24.03.2003 03.04.2003 Awaited

9 Northern Power Generation Co. Ltd.

NEPRA/TRF-17/NPGCL-2003

28.03.2003 03.04.2003 “

10 Jamshoro Power Co. Ltd.

NEPRA/TRF-18/JPCL-2003

28.03.2003 03.04.2003 “

11 NTDC NEPRA/TRF-19/NTDC-2003

28.04.2003 29.05.2003 “

12 Hydropower – WAPDA

NEPRA/TRF-20/WAPDA(Hydro)-2003

29.04.2003 30.05.2003 “

13 SPPs Tariff NEPRA/TRF-21/SPPs-2003

- 08.04.2003 “

14 KESC NEPRA/TRF-22/KESC-2003

10.05.2003 14.05.2003 “