NAIOP Northern Virginia 2017 Annual Forecast · No Update Reduce Corporate ... Cushman &...

88

NAIOP Northern Virginia 2017 Annual Forecast

Transcript of NAIOP Northern Virginia 2017 Annual Forecast · No Update Reduce Corporate ... Cushman &...

NAIOP Northern Virginia

2017 Annual Forecast

Today’s Discussion

U.S. Economic &Market Outlook

Ken McCarthy, Principal Economist

February 16, 2017

Today’s Discussion

The Longest Expansion Ever?

Cyclical Drivers

Long Term Drivers

Ranking Expansions by DurationThis is already the third longest in history

36

58

73

92

93

106

120

0 20 40 60 80 100 120 140

1970

1975

2001

1982

2009

1961

1991

Source: National Bureau of Economic Research

This Expansion Still Has LegsFew Excesses, No Trigger in Sight

50

60

70

80

90

100

110

120

130

140

150

Mill

ions

of P

erso

ns

1969-70Fed aggressively tightens as a tax surcharge is imposed

1973-75Price controls ended OPEC oil embargo, massive inflation

1981-82Second oil shock, Sharp Fed tightening (FF goes to 20%)

1990-91Iraq invades Kuwait, oil prices surge

2008-09Great Recession, financial crisis brought on by residential real estate collapse

1960Fed tightens from faulty seasonal adjustment

2001Equity markets collapse as dot-com boom ends. 9/11

Source: BLS, Cushman & Wakefield Research

No excesses in sight, Current expansion likely to last several more years.

Employment Growth Compared to Long-Term Recovery Average

Average Recovery: 2,081

0

500

1,000

1,500

2,000

2,500

3,000

Source: U.S. Bureau of Labor Statistics

After two strong years job growth has returned to trend.

Growth Driver: Tighter Labor Markets, Higher WagesU.S. Private Sector Job Openings and New Hires

Source: U.S. Bureau of Labor Statistics

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

Tho

usan

ds

Job Openings New Hires

Jobs are going unfilled

Getting tougher to find workers/labor costs and household income will rise/ real estate is a recruiting tool

Atlanta Fed Wage Growth TrackerY-O-Y

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

Per

cent

Cha

nge

from

1 Y

ear A

go 3

-mon

th m

ovin

g av

erag

e

Source: Federal Reserve Bank of Atlanta

Wages will continue to accelerate over the next two years, boosting income

U.S. Motor Vehicle SalesRecord-Setting Performance

9

11

13

15

17

19

21

23

Mill

ions

of U

nits

Best two years

Source: U.S. Bureau of Economic Analysis

When incomes rise, Americans buy cars

Now What?

Trump and ConfidenceBusiness and Consumers More Optimistic

December increase

largest on record

Optimism is high as the

new Administration

takes office, but

attitudes can change

quickly.

Since the election

consumer confidence

has surged to its highest

level since 2001.

If sustained, these

increases set the stage

for stronger growth in

revenue

80

90

100

110

20

60

100

140

Small Business Confidence Surge

Consumer Confidence Soars

Source: National Federation of Independent Businesses, The Conference Board

Trump and ConfidenceS&P 500 Stock Price Index Hits a Record

1,800

1,900

2,000

2,100

2,200

2,300

2,400

Source: S&P Dow Jones

Trump PoliciesStill a Lot We Don’t Know

TAX REFORM PROPOSALSNo Update

Reduce Corporate income tax from 35% to 15%

Top income tax bracket reduced from 39.6% to 33%, number of brackets from 7 to 3

Leave capital gains tax at 20%

Repeal the estate tax and eliminate the alternative minimum tax

Advocated for a one-off 10% tax rate on repatriated corporate earnings

REGULATION POLICIESExecutive Orders

Dismantle Dodd-Frank law

Repeal & Replace Obamacare

End the war on coal

American energy dominance declared strategic priority

SPENDING PROPOSALSNo Update

Spend $1 trillion on infrastructure over 10 years much of it privately funded

Eliminate the sequester on defense spending (boost troop levels, number of ships, aircrafts and bolster missile defense system

Eliminate government waste and budget gimmicks

Halt new trade deals like the Trans-Pacific Partnership

Enforce existing trade treaties more strictly

Potentially renegotiate existing treaties like NAFTA

Strengthen U.S. stance against currency manipulation

TRADE AND GLOBALIZATIONExecutive Orders

Trump and the Economy Stronger Growth Likely

1.6%

2.1%

1.7%

1.5%1.6%

2.3%

3.0%

2.0%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2016 2017 2018 2019

Pre-Election Baseline Post-Election baseline

Most businesses will benefit from stronger consumer and business spending growth

Source: Cushman & Wakefield

10-Year Treasury Yield

Source: U.S. Federal Reserve Board

1.25%

1.45%

1.65%

1.85%

2.05%

2.25%

2.45%

2.65%

Risk Free rate reset post-election. Market now in “wait and see” mode

The 35-Year Bull Run10-Year Treasury Yield

Source: U.S. Federal Reserve Board

By any historical standard interest rates are low. Is the bull market over? To soon to tell.

1.0%

3.0%

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

Fed Funds Target Forecast

Source: U.S. Federal Reserve Board, Cushman & Wakefield

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

Steady, Step by step tightening expected

FORECAST

Long-TermTrends Millennials and Real Estate:

The Urbanization Trend will Continue

0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00

15

18

21

24

27

30

33

36

39

42

45

48

51

54

57

60

63

66

69

Millions of Persons

Age

Millennials: 90.8 Million

Boomers: 79.1 Million

Millennials Are Now the Largest Component of the Labor Force

Source: U.S. Census Bureau

Millennial Characteristics

THEY DON’T DRIVE

% of 19 year olds with a drivers license

1983: 87%

2014: 69%

THEY GREW UP WITH THE INTERNET

1980: First Millennials

1993: First Web Browser

1980: First Gigabyte Hard Drive-weighed 550 lb and cost $40,000

2017 3.0 Terabyte drive (3,000 times as large) weighs 3 lb and costs $100

MOST EDUCATED GENERATION IN HISTORY

Larger % of millennials have a bachelors or higher than in any previous generation

And many are still in high school

Millennials are more likely to live in urban areas than earlier generations

URBAN-FOCUSED

They are Mostly in Their 20s

Source: U.S. Census Bureau

3,000

3,200

3,400

3,600

3,800

4,000

4,200

4,400

4,600

4,800

16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60 62 64

Num

ber

of P

eopl

e

Age

Population

Aged 20 to 29

Change in Employment Core Vs. Periphery

Source: CityObservatory Surging Center City Job Growth

0.10%

0.5%

1.2%

-0.1%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

2002-2007 2007-2011

Core Periphery

Today’s Discussion

Fact Checker

Millenials?

Trump Effect?

Top Private Sector Transactions 2014-2016New Deals, 50k SF +, Inside vs. Outside the Beltway

Inside the Beltway Outside the Beltway

CEB – 350k SF Capital One – 272k SF

Nestle – 200k SF NFCU – 235k SF

Marymount – 100k SF Fannie Mae – 186k SF

Applied Predictive – 100k SF Noblis – 150k SF

Am. Diabetes Assn – 78k SF Ellucian – 100k SF

Sands Capital – 78k SF AFCU – 93k SF

Grant Thornton – 76k SF Serco – 88k SF

MWAA – 74k SF MC Dean – 86k SF

Politico – 61k SF Alarm.com – 83k SF

Tegna – 70k SF

EIT – 65k SF

Carahsoft – 64k SF

TOTAL – 1.1 MSF TOTAL – 1.5 MSF

6%

48%32%

6%

10%

October 2016 – 60 Tours, 850k Sf

Contractor Tech PBS Medical Other

The Fact CheckerCushman & Wakefield’s Tour Tracker Beta – Tour Activity is Up 30%

Source: BLS

46%

21%

19%

4%

10%

January 2017 – 78 Tours, 900k SF

Contractor Tech PBS Construction/Engineering Other

Today’s Discussion

Northern Virginia Economic &Market Outlook

Nate Edwards, Regional Director

February 16, 2017

Today’s Discussion

NoVA Economy

The Trump Impact

Office Leasing

Capital Markets

Current Local Economy - Very Strong

DC Metro Employment% Growth YOY

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%1

99

1Q

21

99

1Q

41992Q

21

99

2Q

41

99

3Q

21

99

3Q

41

99

4Q

21

99

4Q

41

99

5Q

21

99

5Q

41

99

6Q

21996Q

41

99

7Q

21

99

7Q

41

99

8Q

21

99

8Q

41

99

9Q

21

99

9Q

42

00

0Q

22

00

0Q

42001Q

22

00

1Q

42

00

2Q

22

00

2Q

42

00

3Q

22

00

3Q

42

00

4Q

22

00

4Q

42

00

5Q

22005Q

42

00

6Q

22

00

6Q

42

00

7Q

22

00

7Q

42

00

8Q

22

00

8Q

42

00

9Q

22

00

9Q

42010Q

22

01

0Q

42

01

1Q

22

01

1Q

42

01

2Q

22

01

2Q

42

01

3Q

22

01

3Q

42

01

4Q

22

01

4Q

42

01

5Q

22

01

5Q

42

01

6Q

2

Washington DC, MSA US

DC MSA Now

Outperforming the US

Source: BLS

Job Growth in Major Markets2016 YOY

Source: BLS

162,483

126,642

119,033

73,933 73,09264,675 64,175

62,233

59,333 57,10852,243

44,96739,950

12,358

1.7%

2.2%

3.5%

2.9%

2.3%

3.4%

2.8%2.5%

1.3%

2.0%

2.0%

3.2%

2.1%

0.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

-10,000

40,000

90,000

140,000

190,000N

ew Y

ork

Los

An

gele

s

Dal

las

Atl

anta

Was

hin

gto

n, D

C

Seat

tle

San

Fra

nci

sco

Mia

mi

Ch

icag

o

Ph

ilad

elp

hia

Bo

sto

n

Den

ver

Det

roit

Ho

ust

on

Non Office-Using Office-Using % Growth YOY

DC – 15,000 (8,500 Typical)

NoVA – 33,000 (19,300 Typical)

SMD – 25,000 (4,500 Typical)

-2,090

390

4,760

7,400

8,810

11,110

12,220

20,510

-5,000 0 5,000 10,000 15,000 20,000

Information (75k)

Financial (156k)

Federal Government (370k)

Manufacturing & Construction (210k)

Retail (288k)

Leisure & Hospitality (321k)

Education & Healthcare (431k)

Professional & Business Services (742k)

# of Jobs

Employment by SectorDC Metro, 2016 YOY

(total sector employment)

Source: BLS

-110

90

1,640

490

4,920

3,840

3,580

12,220

-5,000 0 5,000 10,000 15,000 20,000

Information (42k)

Financial (70k)

Manufacturing & Construction (95k)

Federal Government (85k)

Retail (148k)

Leisure & Hospitality (142k)

Education & Healthcare (160k)

Professional & Business Services (400k)

# of Jobs

Employment by SectorNorthern Virginia, 2016 YOY

(total sector employment)

Source: BLS

NoVA Captures 54% of

the Region’s Office –

Using Job Growth

DC Metro Unemployment RateDC Metro vs. the US and Major Markets, Yearend 2016.

2.7%2.7%

3.7%3.7%

3.9%4.3%

4.5%4.7%4.8%4.9%

5.1%5.1%

5.5%5.6%5.7%

0% 2% 4% 6%

Boston

Denver

Washington, DC

San Francisco

Dallas

Seattle

New York

Los Angeles

United States

Philly

Atlanta

Miami

Houston

Detroit

Chicago

Source: BLS

2.8% 2.9%3.2% 3.3% 3.4%

3.9%4.2%

5.8%

0%

1%

2%

3%

4%

5%

6%

7%

Wealthiest Counties in the U.S.Median Household Income – 4 of 10 Wealthiest U.S. Counties are in the DC Metro Region

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Source: Census, Motley Fool

DC Metro Economic Indicators

0%

10%

20%

30%

40%

50%

60%

$0$10,000$20,000$30,000$40,000$50,000$60,000$70,000$80,000$90,000

$100,000

Was

hin

gto

n, D

C

San

Fra

nci

sco

Bo

sto

n

New

Yo

rk

Den

ver

Ch

icag

o

Los

An

gele

s

Dal

las

Ho

ust

on

Atl

anta

Un

ited

Sta

tes

Det

roit

Mia

mi

Incomes and Education

Median Incomes

Educational Attainment - % of Population with Bachelor's

21

5

4

Fortune 1,000 HQ’s

NoVA DC Maryland

The Smartest, most Well-Paid Workforce in the Nation with Great Companies to Work For

Source: US Census, Forbes

Forecasted MF Deliveries

0

1,000

2,000

3,000

4,000

5,000

6,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2017 2018 2019

DC SMD NoVA

Source: Delta

13,700 Units 8,600 Units

Class A Projected Quarterly Absorption - 2,400 units

DC Metro

MF AbsorptionDC Metro

2,379

4,063

2,589

1,574

735

7,741

1,776

2,646

4,436

8,081

6,782

5,176

6,849

5,926

10,14710,631

8,266

0

2,000

4,000

6,000

8,000

10,000

12,0002

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

DC MD VA

Source: REIS, CoStar

By 2025…

850,000

Additional People327,000 Households 33,000 Units/Year 13,000 MF Units/Year

Source: Cushman & Wakefield

Trump Policies Could Mean Big Things for NoVA

Federal Procurement in the DC MetroBy Market, $Billions

40

$8$11

$16$14

$19

$25

$39

$59

$70

$77

$82$80

$76

$69$71 $71

$74

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bill

ion

s

TOTAL NORTHERN VIRGINIA TOTAL DISTRICT OF COLUMBIA TOTAL SUBURBAN MARYLAND TOTAL WEST VIRGINIA

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

Bill

ion

s

DC Metro + $1 TN DC Metro + $500BN DC Metro CBO Baseline

Contracting Opportunities Could Surge With TrumpDC Metro Procurement with Trump Proposed Defense Spending Increases

Cyber – $11 Billion in Spending by 20203,200 Cyber Jobs Posted

Source: Cushman & Wakefield, FCEDA

Job Growth Forecast

73,100

56,55048,181 44,872

37,962

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2016 2017 2018 2019 2020

Cushman & Wakefield George Mason University Moody's Average Historical Average: 36,000

Source: Cushman & Wakefield, Moody’s, GMU-CRA

Washington MSA GDP

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

DC Metro U.S.

Source: Moody’s

Economic Growth Expected to AccelerateDC Metro: Gross Metro Product (GMP)

2.6%

3.7%

3.2%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

DC Metro GMP Growth (AR, right)

Source: Cushman & Wakefield Research, Bureau of Economic Analysis, NCREIF

Northern Virginia Leasing

Lease DistributionSince 2011 – 73% of Deals Below 15k SF

53%

20%

13%

8%3%

3%

< 8k SF

8-15k SF

15-25k SF

25-50k SF

50-100k SF

100k SF +

Concessions Remain ElevatedClass A Direct, 7+ Year Term

0.00

0.20

0.40

0.60

0.80

1.00

1.20

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Avg Starting Rent (FS) Avg TI PSF Avg Mos Free Rent Per Year of Term

Source: Cushman & Wakefield

Obsolete Product% of Inventory by Submarket that is Pre 1990 and less than 50% Leased

Source: Cushman & Wakefield

72%

20%14%

6% 8%3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

5

10

15

20

25

I-3

95

Eis

enh

ow

er

Fair

fax

/ O

/V

Cry

stal

/Pen

tago

n

RB

Co

rrid

or

Tyso

ns

Res

ton

/ H

ern

do

n

Inve

nto

ry (

MSF

)

Obsolete as a % of Total Inventory

Active Inventory Obsolete Inventory % of Total

13.1%

14.4%

17.2%

17.3%

19.5%

24.7%

16.2%

23.1%

21.7%

22.6%

11.6%

1.8%

5.9%

4.4%

3.1%

0% 10% 20% 30%

Fairfax/Oakton

Reston/ Herndon

Crystal

Tysons

RB Corridor

Quoted vs. True Vacancy

Quoted Vacancy True Vacancy

Differential

Deal Volume Concentrated in Silver Line Markets

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Leasing Activity Vacancy

Reston/Herndon & Tysons Experienced More New Leasing Activity than the Next 6 Submarkets Combined

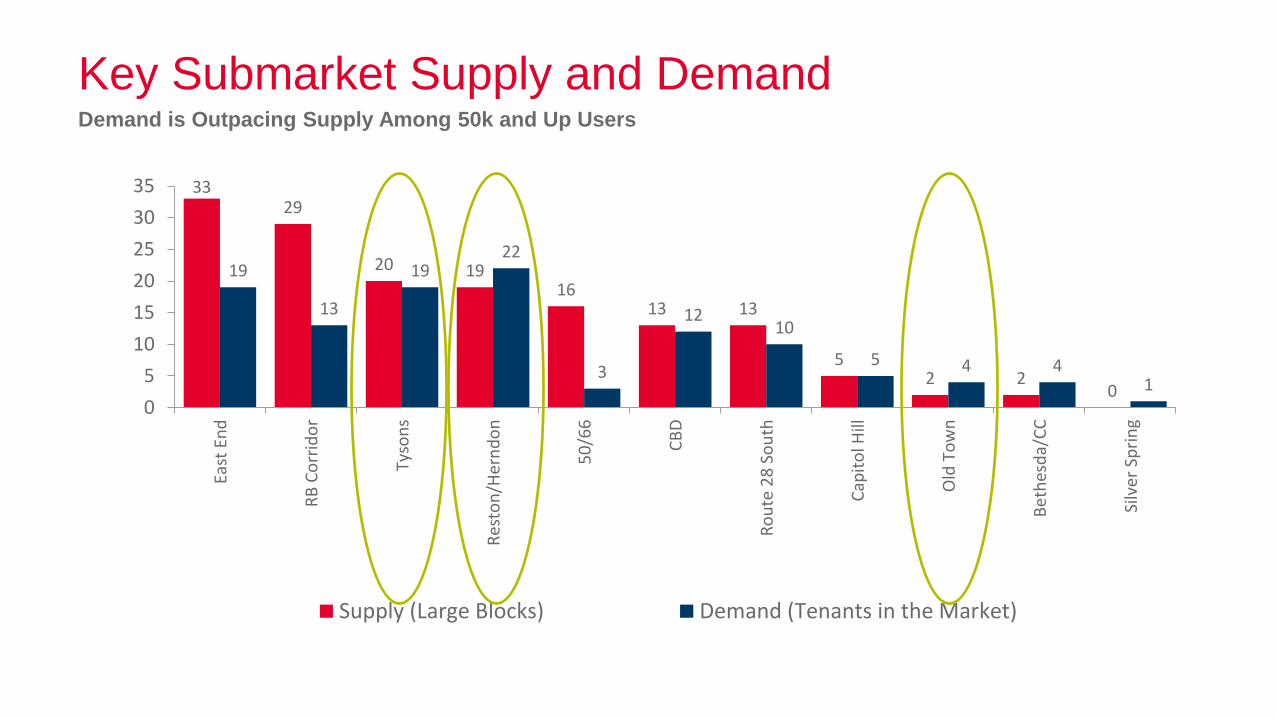

Key Submarket Supply and DemandDemand is Outpacing Supply Among 50k and Up Users

3329

20 1916

13 13

52 2

0

19

13

1922

3

1210

5 4 41

0

5

10

15

20

25

30

35

East

En

d

RB

Co

rrid

or

Tyso

ns

Res

ton

/Her

nd

on

50

/66

CB

D

Ro

ute

28

So

uth

Cap

ito

l Hill

Old

To

wn

Be

thes

da/

CC

Silv

er S

pri

ng

Supply (Large Blocks) Demand (Tenants in the Market)

Large BlocksReston/Herndon, Tysons, Ballston

37

18

7

4

29

9

7

2

43

11

5

3

0 5 10 15 20 25 30 35 40 45 50

20-50k SF

50-100k SF

100-200k SF

200k SF+

Tysons Corner Reston/Herndon RB Corridor

Large Blocks on MetroReston/Herndon, Tysons, Ballston, ¼ Mile From Metro/Future Metro

32

17

7

3

5

2

1

1

4

1

1

1

0 5 10 15 20 25 30 35 40 45 50

20-50k SF

50-100k SF

100-200k SF

200k SF+

Tysons Corner Reston/Herndon RB Corridor

Net New Growth 2015-2016 Real Growth is Being Seen for the First Time in 5 Years

65,000 SF

235,000 SF

100,000 SF

200,000 SF

120,000 SF

230,000 SF

300,000 SF60,000 SF

1.2 MSF

NoVA GSA ExposureGSA Northern Virginia Expirations 2017-2020 by Submarket

2,050,489

1,413,580

1,045,345980,768

880,776

698,465 659,550

270,599 266,436150,485

93,650 141,716 125,142 116,233 99,27224,209

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000C

ryst

al/P

enta

gon

Cit

y

Ro

ssly

n

Spri

ngf

ield

Bal

lsto

n

Her

nd

on

I-3

95

Eise

nh

ow

erA

ve Tyso

ns

Lou

do

un

Co

un

ty

Ro

ute

28

S

Res

ton

Cla

ren

do

n/

CH

Old

To

wn

Mer

rifi

eld

Fair

fax

Cen

ter

Pri

nce

Will

iam

Source: GSA

Capital Markets

Office Sales Volume YTD 2016Among Major Metros

$29.4

$14.4 $14.4

$7.8 $7.0$5.8 $5.4 $5.1 $4.5

$2.7 $1.9 $0.9

$272

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

NYC Metro SF Metro LA Metro Boston DC Metro Dallas Chicago Seattle Atlanta Philly Metro Denver Houston

$B

illio

ns

Sales Volume 2016 YTD Average Price Per SF

Source: C&W, RCA

Office Investment Sales VolumeWashington DC Metro

$10.2

$14.1

$12.5

$3.4

$2.3

$4.3

$7.2

$5.4

$6.8

$8.0

$9.7

$7.0

-$1.0

$1.0

$3.0

$5.0

$7.0

$9.0

$11.0

$13.0

$15.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bil

lio

ns

DC NoVA SMD Historical Average: $7.6 Billion

Source: Cushman & Wakefield

Office Pricing$/square foot

$484

$205

$167

$0

$100

$200

$300

$400

$500

$600

$700

$800

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

DC NoVa SMD

Source: Cushman & Wakefield

Office Cap RatesWashington, DC Metro Area, all classes

2.51%

5.66%

8.98%

6.55%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US 10 Yr Treasury DC Office Cap Rate MD Office Cap Rate VA Office Cap Rate

Source: C&W

Office Cap RatesWashington, DC Metro Area, all classes

2.22%

5.39%

6.99%

7.05%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US 10 Yr Treasury DC Office Cap Rate MD Office Cap Rate VA Office Cap Rate

Source: Cushman & Wakefield61

Where Foreign Buyers Are Most ActiveCross-border office sales as % of total sales volume – 2016

DC Metro 36%

New York 35%U.S. = 21%

Foreign acquisitionsunder 10% of investor composition YTD 2015

Dallas 28%

Miami 42%

Philly 32%

Source: Cushman & Wakefield, RCA

Boston 20%

Denver 15%

Seattle 22%

Los Angeles 17%

Chicago 10%

Austin 13%

San Francisco 21%

Atlanta 12%

Tampa 17%

Minneapolis 29%

Phoenix 12%

$0

$500

$1,000

$1,500

$2,000

$2,500 $2,287

$1,911

$1,720$1,381

$1,088

$850

$707$520

$364$161 $153

$22

Millio

ns

2012 2013 2014 2015 2016

Source: Cushman & Wakefield, RCA

Foreign Investment in DC Metro OfficeBy Country, DC Metro 2012-2016

Today’s Discussion

Fact Checker

Is the Local Recovery Helping the Office Market?

2011-2013 HeadwindsReal GDP, Y/Y % Change

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

GDP

GDP ex GCE

This was the important turning point for DC

• Jan 3rd 2011: Tea Party Movement Begins

• Aug 2011: Debt ceiling deal, cuts gov’t

spend by $2.4T

• 2012: Sequester kicks in

• 2012: Majority of Brac Moves Occur

• 2013: Fiscal Cliff Gov’t shutdown

Source: BEA

Northern Virginia Bounces off the Bottom Office Leasing Fundamentals

21.3%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

-3

-1

1

3

5

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Va

ca

nc

y R

ate

Sq

ua

re F

ee

t (M

illio

ns

)

New Deliveries Net Absorption

Average Deliveries: 1.6 msf Average Absorption 465k SF

Vacancy Rate Average Vacancy: 16%

Source: Cushman & Wakefield

The Bottom

• 9/2014: Federal Employment starts to

grow

• 10/2014: GDP hits 5% for the region

• 12/2014: First Budget in 6 Years Passed

• 2015: 58,000 Jobs Created

• 2016: 73,000 Jobs Created

• 2017: Real Net New Demand and Rent

Growth

Contractors Have Rightsized in the Suburbs

San Jose

Washington, DC

Detroit

Source: Cushman & Wakefield

Contractor Consolidations post-Recession

Company Name Pre-recession Footprint Current Footprint % Reduction

Lockheed Martin 4,321,527 2,802,698 35.15%

Mitre 975,331 964,742 1.09%

L-3/Engility 538,366 368,151 31.62%

Harris Corporation 451,806 351,369 22.23%

EADS/Airbus 312,547 248,495 20.49%

SRA International 898,141 406,571 54.73%

IBM Corporation 1,139,960 913,299 19.88%

CACI 993,611 632,323 36.36%

Average Reduction 27.69%

7 YEARS AGO TODAY

Department Finance Human Resources

Driver Expense Management Labor

Outlook Liability Asset

Criteria Pro-Forma Employee Experience

What’s Different Now?Tenant Leasing Decisions

Job Growth/ Confidence

Absorption

(75% Renew)

Rents Increase

New Development

Over Supply

Leasing Cycle

Historical Office Recovery

Job Growth/ Confidence

Efficiency Offsets

Absorption (50% Renew)

Flight to Quality

Obsolescence for Old /

Demand for New

Haves & Have Nots

Office Recovery – Past 7 Years

Today’s Discussion

Transactional Perspectives

Spencer Stouffer, Vice Chairman

February 16, 2017

Today’s Discussion

Demand

Supply

Tysons – the Bellwether

Predictions

DEMAND

San Jose

Washington, DC

Detroit

Source: Cushman & Wakefield

60%

The Core Markets – Arlington, Tysons, Reston/Herndon

And Tysons Continues to Attract Tenants from Other Submarkets

220k SF

29k SF

163k SF

29k SF

92k SF

140k SF

80k SF

Notable Private Sector Relocations

840,000 SF

86k SF

TYSONS

198k SF

40k SF

190k SF

161k SF

97k SF

160k SF

RESTON/HERNDON

818,000 SF

200k SF

34k SF

179k SF

76k SF

78k SF

35k SF

54k SF

ARLINGTON

656,000 SF

Non-Core Markets - the Other 40%

San Jose

Washington, DC

Detroit

Source: Spencer

Buildings will outperform given:• Captive Tenants• Pricing Advantage• Best in Show

The top half will capture the absorption

Supply

Source: Cushman & Wakefield

2014

Large Existing Blocks are Drying up – Tysons

Source: Cushman & Wakefield

2017

Large Existing Blocks are Drying up – Tysons

San Jose

Washington, DC

Detroit

Source: Cushman & Wakefield

2014

Large Existing Blocks are Drying up – Reston/Herndon

San Jose

Washington, DC

Detroit

Source: Cushman & Wakefield

Large Existing Blocks are Drying up – Reston/Herndon

2017

Demand for New SpaceNorthern Virginia New vs. Relet

(4,000,000)

(3,000,000)

(2,000,000)

(1,000,000)

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2008 2009 2010 2011 2012 2013 2014 2015 2016

Sq

uare

Fe

et

Deliveries New Space Absorption Relet Absorption Sublet Absorption

Since 200815.4 msf absorbed in New

-15.2 msf absorbed in Relet/Sublet

Development Pipeline2013-2018 New Development – Tysons, Toll Road and Inside the Beltway – 77% Leased

535

309 322

92

211

525

322

488 477

340

720

355

167

235

553

161

440

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100

200

300

400

500

600

700

800

18

12

N M

oo

re

14

00

Cry

stal

90

1 S

Cla

rk

30

01

Was

hin

gto

n

30

03

Was

hin

gto

n

79

00

Tys

on

s

79

40

Jo

ne

s B

ran

ch

Silv

erl

ine

Ce

nte

r

17

75

Tys

on

s

Mit

re IV

24

15

Eis

en

ho

wer

19

00

Re

sto

n M

etro

Pla

za

10

00

N. G

leb

e

10

41

Ele

ctri

c A

ve

Ce

ntr

al P

lace

23

11

Wils

on

The

Bo

ro

Cap

On

e H

Q

Rosslyn Crystal Clarendon Tysons Tysons Tysons Eisenhwr Reston Ballston Tysons Rosslyn Courthouse Tysons Tysons

2013 2014 2015 2016 2017 2018

SF (

Tho

usa

nd

s)

New SF Available New SF Leased Vacancy %

Tysons – the Bellwether

Source: DTZ Research, CoStar

$29.00$28.00

$30.50 $30.50

$32.00

$26.00

$31.00$32.25

$28.50

$32.50 $32.00

$35.50

$27.50

$38.00

$33.50

$31.00

$35.00$34.00

$37.50$38.50

$40.00

$20

$25

$30

$35

$40

$45

8180/8200Greenboro

American Center Tysons DullesPlaza

Tysons MetroCenter

1765 GreensboroStation

Westwood MetroTower

Silverline Center

16% 11% 15% 12% 17% 48% 29%

2014 2015 2016

Rent Growth – 2014 to NowAs Quality Space Becomes More Scare – Rents are Popping in Select Tysons Assets

The Metro EffectDemand is Outpacing Supply Among 50k and Up Users

7.2%

21.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2012 2013 2014 2015 2016

Tysons Corner

Metro Proximate All Properties

Predictions

Predictions

Source: Spencer

• 2017 – the best year in Northern Virginia since 2007

• 1 million square feet of positive absorption in 2017

• At least 2 new preleases signed

• Rents continue to increase in Tysons/Reston/Herndon

501 K Street, NW

Owner

Notes

Thank You