NAIC Bulletin: September 2016 - EYFILE/NAICBulletin_02855-161US_14September2016.pdf · September...

23

The National Association of Insurance Commissioners (NAIC) recently held its Summer National Meeting in San Diego. This publication highlights issues that various NAIC groups have addressed since the 2016 Spring National Meeting. We hope you find it informative, and we welcome your comments. Please contact your local EY professional for more information. What you need to know • The Executive Committee and Plenary approved an implementation date of 1 January 2017, for principle-based reserving as a national standard. • The Reinsurance (E) Task Force adopted the Term and Universal Life Insurance Reserve Financing Model Regulation (i.e., XXX/AXXX Credit for Reinsurance Model Regulation), which will be sent to the Financial Condition (E) Committee for approval later this year. • The Reinsurance (E) Task Force referred to the Qualified Jurisdiction (E) Working Group a request for the Working Group to review the European Union (EU) member state implementation of Solvency II and its potential effect on the status of certain EU jurisdictions deemed qualified jurisdictions under the US system of state-based insurance regulation. • The Cybersecurity (EX) Task Force exposed a revised draft of the Insurance Data Security Model Law that would establish uniform standards on data security and the investigation and notification of a data breach. September 2016 NAIC Bulletin Highlights of the National Association of Insurance Commissioners meeting Summer 2016 update In this issue: Executive Committee and Plenary .......... 2 Cybersecurity (EX) Task Force .................2 Principle-Based Reserving....................... 2 PBR pilot project .......................................3 Valuation Manual amendments................3 PBR methodology for non-variable deferred annuities ................................4 XXX/AXXX Reinsurance Framework ....... 4 Variable Annuity Framework ................... 5 Quantitative impact study ........................5 Effect on statutory accounting and reporting...............................................5 Accounting Practices and Procedures (E) Task Force........................................ 6 Statutory Accounting Principles (E) Working Group......................................6 Restricted Assets (E) Subgroup................7 Blanks (E) Working Group .........................7 Life Insurance and Annuities (A) Committee ............................................. 7 Life Actuarial (A) Task Force ....................8 VM-22 (A) Subgroup ................................8 Unclaimed Life Insurance Benefits (A) Working Group......................................8 Health Insurance and Managed Care (B) Committee ............................................. 8 Health Actuarial (B) Task Force ................9 Long-Term Care Actuarial (B) Working Group......................................9 Property and Casualty Insurance (C) Committee ............................................. 9 Financial Condition (E) Committee ........ 10 Capital Adequacy (E) Task Force ............10 Investment RBC (E) Working Group........10 Group Capital Calculation (E) Working Group.................................... 11 Group Solvency Issues (E) Working Group.................................... 11 ORSA Implementation (E) Subgroup ......11 Reinsurance (E) Task Force .................... 12 Risk-Focused Surveillance (E) Working Group.................................... 12 Valuation of Securities (E) Task Force ....12 Financial Regulation Standards and Accreditation (F) Committee ............... 13 International Insurance Relations (G) Committee ........................................... 13 ComFrame Development and Analysis (G) Working Group .............................. 14 Appendix A – Statutory Accounting Principles Working Group .................... 15 Appendix B – Blanks Working Group ...... 20 Appendix C – Capital Adequacy (E) Task Force ........................................... 22

Transcript of NAIC Bulletin: September 2016 - EYFILE/NAICBulletin_02855-161US_14September2016.pdf · September...

The National Association of Insurance Commissioners (NAIC) recently held its Summer National Meeting in San Diego. This publication highlights issues that various NAIC groups have addressed since the 2016 Spring National Meeting. We hope you find it informative, and we welcome your comments. Please contact your local EY professional for more information.

What you need to know • The Executive Committee and Plenary approved an implementation date of 1 January 2017, for

principle-based reserving as a national standard.

• The Reinsurance (E) Task Force adopted the Term and Universal Life Insurance Reserve Financing Model Regulation (i.e., XXX/AXXX Credit for Reinsurance Model Regulation), which will be sent to the Financial Condition (E) Committee for approval later this year.

• The Reinsurance (E) Task Force referred to the Qualified Jurisdiction (E) Working Group a request for the Working Group to review the European Union (EU) member state implementation of Solvency II and its potential effect on the status of certain EU jurisdictions deemed qualified jurisdictions under the US system of state-based insurance regulation.

• The Cybersecurity (EX) Task Force exposed a revised draft of the Insurance Data Security Model Law that would establish uniform standards on data security and the investigation and notification of a data breach.

September 2016

NAIC Bulletin Highlights of the National Association of Insurance Commissioners meeting

Summer 2016 update

In this issue: Executive Committee and Plenary .......... 2

Cybersecurity (EX) Task Force ................. 2 Principle-Based Reserving....................... 2

PBR pilot project ....................................... 3 Valuation Manual amendments ................ 3 PBR methodology for non-variable

deferred annuities ................................ 4 XXX/AXXX Reinsurance Framework ....... 4 Variable Annuity Framework ................... 5

Quantitative impact study ........................ 5 Effect on statutory accounting and

reporting ............................................... 5 Accounting Practices and Procedures (E) Task Force ........................................ 6 Statutory Accounting Principles (E)

Working Group...................................... 6 Restricted Assets (E) Subgroup ................ 7 Blanks (E) Working Group ......................... 7

Life Insurance and Annuities (A) Committee ............................................. 7 Life Actuarial (A) Task Force .................... 8 VM-22 (A) Subgroup ................................ 8 Unclaimed Life Insurance Benefits (A)

Working Group...................................... 8 Health Insurance and Managed Care (B) Committee ............................................. 8 Health Actuarial (B) Task Force ................ 9 Long-Term Care Actuarial (B)

Working Group...................................... 9 Property and Casualty Insurance (C) Committee ............................................. 9

Financial Condition (E) Committee ........ 10 Capital Adequacy (E) Task Force ............ 10 Investment RBC (E) Working Group........ 10 Group Capital Calculation (E)

Working Group.................................... 11 Group Solvency Issues (E)

Working Group.................................... 11 ORSA Implementation (E) Subgroup ...... 11 Reinsurance (E) Task Force .................... 12 Risk-Focused Surveillance (E)

Working Group.................................... 12 Valuation of Securities (E) Task Force .... 12

Financial Regulation Standards and Accreditation (F) Committee ............... 13

International Insurance Relations (G) Committee ........................................... 13 ComFrame Development and Analysis

(G) Working Group .............................. 14 Appendix A – Statutory Accounting Principles Working Group .................... 15

Appendix B – Blanks Working Group ...... 20 Appendix C – Capital Adequacy (E) Task Force ........................................... 22

EY AccountingLink | ey.com/us/accountinglink

2 | NAIC Bulletin August 2016

Executive Committee and Plenary The Executive Committee and Plenary adopted the Market Regulation Certification Program to establish and maintain standards that promote sound practices for market regulation activities related to insurance consumer protection.

The Executive Committee and Plenary also adopted the provisions for reinsurance ceded to certified reinsurers in Part A: Laws & Regulations — Traditional Insurers of the general accreditation standards as a required and uniform accreditation standard applicable to all NAIC accredited jurisdictions with an effective date of 1 January 2019.

Refer to the Principle-Based Reserving and XXX/AXXX Reinsurance Framework sections in this publication for more information.

Separately, the Executive Committee and Plenary adopted an NAIC Model Bulletin on federal Gramm-Leach-Bliley Act (GLBA) privacy notices. The NAIC Model Bulletin is intended to clarify that a licensee of the insurance department is not required to provide the annual privacy notices, provided the conditions under the Fixing America’s Surface Transportation (FAST) Act are met. The FAST Act includes amendments to the GLBA, which eliminated the requirement for financial institutions to provide GLBA annual notices if certain conditions are met.

Cybersecurity (EX) Task Force After discussing the significant number of comments received on the initial draft of the Insurance Data Security Model Law, the Task Force exposed a revised draft to address the issues raised.1 If adopted, the new cybersecurity model law would establish uniform standards for data security and the investigation and notification of a data breach applicable to any person or entity licensed, authorized to operate, registered or required to be licensed, authorized or registered pursuant to the insurance laws of the state. Comments are due by 16 September 2016.

The initial feedback on the revised draft of the proposed model law continues to indicate support for uniformity in data security and data breach notification requirements among the states. However, the proposed model law still needs significant development, input and revision before the industry can support its adoption in state legislature. Concerns were raised about the broad nature of industry-specific mandates in the revised draft and the potential conflicts with the existing requirements of federal and state cybersecurity laws and state privacy laws. Other concerns included a potential lack of clarity on coordination among states for data breach responses, the need for uniform application in the notification requirements from different parties so that the consumer would not be notified multiple times for the same data breach and the broad definition of personal information. The Task Force will schedule an interim conference call to further discuss feedback on the revised draft, with the goal of recommending the adoption of a final standard by the end of 2016.

Principle-Based Reserving The Executive Committee and Plenary approved Principle-Based Reserving (PBR) as a national standard with an implementation date of 1 January 2017, based on the NAIC’s determination that the requisite thresholds had been met by the states that enacted legislation to adopt the revised Standard Valuation Law (#820) with substantially similar terms and conditions to those in the NAIC model law.

Model #820 incorporates the various sections of the Valuation Manual (VM) that establish the minimum reserve and related requirements for PBR (for life products and variable annuities) and minimum reserve requirements (for health insurance and credit life and disability insurance) , which include:

• VM-20, Requirements for Principle-Based Reserves for Life Products

• VM-21, Requirements for Principle-Based Reserves for Variable Annuities

• VM-25, Health Insurance Reserves Minimum Reserve Requirements

• VM-26, Credit Life and Disability Reserve Requirements

Insurers that write life products subject to the Valuation Manual can elect to apply a PBR methodology to new policies and contracts issued in those states with enacted legislation on or after 1 January 2017. However, the provisions of the Valuation Manual include a three-year transition period during which the application of PBR is optional (i.e., required implementation no later than 1 January 2020). At the end of

EY AccountingLink | ey.com/us/accountinglink

3 | NAIC Bulletin August 2016

the transition period, an insurer that writes life products may assess whether it meets the PBR small company exemption provided by VM-20 and request approval from the insurance commissioner of its state of domicile each year to be exempt from its application.

Various NAIC groups have continued to address PBR implementation initiatives such as evaluating the results of a PBR pilot project for life products, clarifying the PBR requirements in the various sections of the Valuation Manual and developing a PBR methodology for non-variable deferred annuities. Other actions taken to implement PBR include the following:

• The Executive Committee and Plenary adopted amendments2 to the Valuation Manual that were proposed by the Life Insurance and Annuities (A) Committee and the Health Insurance and Managed Care (B) Committee. These amendments primarily clarified the application of PBR requirements related to life products in VM-20 and resolved a timing issue in the reserve requirements for health insurance in VM-25.

• The Statutory Accounting Principles (E) Working Group (SAPWG) adopted substantive revisions to Statement of Statutory Accounting Principles (SSAP) No. 51, Life Contracts, to address how to record a change in valuation basis under PBR and clarify that the initial application of PBR is not expected to result in a day one impact to surplus (Ref #2016-15), and to incorporate references to the Valuation Manual in SSAP No. 51 that will assist in the implementation of PBR (Ref #2015-47).

• SAPWG exposed the Implementation of Principle-Based Reserving issue paper to document the substantive revisions adopted in SSAP No. 51 related to PBR (Ref #2015-47). The issue paper will be updated upon adoption of other changes to statutory guidance that facilitate the implementation of PBR.

• The PBR Review Procedures (EX) Subgroup agreed to evaluate edits to the content of the Financial Condition Examiners Handbook and consider adding a separate chapter on PBR to Section 1 of the Financial Condition Examiners Handbook. The Subgroup also agreed to work with the Financial Analysis Handbook (E) Working Group (FAHWG) to reorganize and enhance the Financial Analysis Handbook by incorporating a risk-focused assessment for reserves. FAHWG has requested input from the Subgroup on potential changes to the content of specific chapters in the Financial Analysis Handbook by 31 October 2016.

• The NAIC continued its work to develop and implement technology to collect company experience data on behalf of individual states and protect the confidentiality of the data submitted. This data will be used to create industry experience tables for PBR and assess the credibility of an insurer’s own assumptions in the application of PBR.

PBR pilot project The PBR Review (EX) Working Group is conducting a PBR pilot project to help insurers and regulators prepare for the implementation of PBR for life products. As of 25 August 2016, six of the 12 participating companies have submitted the required information (e.g., PBR calculations and related supplement required by VM-20 and the deliverables required by VM-31, PBR Actuarial Report Requirements For Business Subject to a Principle-Based Reserve Valuation) for review by their state of domicile, and one company has dropped out of the pilot. The Working Group will evaluate the information received and discuss the results in regulator-only conference calls later this fall.

Valuation Manual amendments The Life Actuarial (A) Task Force (LATF) continued its work on amending the Valuation Manual included in Model #820 to clarify the minimum reserve and related requirements for life insurance, accident and health insurance and deposit-type contracts. The Valuation Manual amendments adopted by LATF (and subsequently proposed by the Life Insurance and Annuities (A) Committee for adoption by the Executive Committee and Plenary) included the following:

• Amendments to VM-G, Corporate Governance Guidance for Principle-Based Reserves, to exclude business subject to the requirements of Actuarial Guideline XLIII — CARVM for Variable Annuities (AG43) from PBR as those contracts are issued prior to 1 January 2017

• Amendments to VM-01, Definitions for Terms in Requirements, and VM-20 to clarify the definition of secondary guarantees, net premium reserve (NPR) and cash flows, since those terms are used in PBR requirements

EY AccountingLink | ey.com/us/accountinglink

4 | NAIC Bulletin August 2016

• Amendments to VM-20 to require that minimum reserves for term life and universal life with secondary guarantee products be determined separately when considering product aggregation

• Amendments to VM-20 to eliminate the use of post-level term period profits in the deterministic reserve calculation

• Amendments to VM-M, Mortality Tables, to incorporate the 2012 Individual Annuity Reserving Valuation Table for use in PBR calculations

Separately, LATF adopted the required amendments to VM-20 to publish updated data for investment spreads as of 30 June 2016 and 31 March 2015, and default costs as of 31 December 2015.

LATF directed a joint mortality table development team formed by the American Academy of Actuaries (Academy) and the Society of Actuaries (SOA) to make a technical correction to the 2017 Commissioners Standard Ordinary (CSO) mortality tables that would cap the composite mortality rates at the smoker mortality rates for certain ages where the composite rate exceeded the smoker rate.

LATF also discussed the development of an annual calendar for the adoption of Valuation Manual amendments and the publication of the VM-20 investment spread tables. LATF expressed its support for establishing a process to submit amendment proposals that would implement updates to the application of PBR requirements for consideration by regulators. The requisite timing for implementation will be determined with input from the Health Actuarial (B) Task Force (HATF).

PBR methodology for non-variable deferred annuities The VM-22 (A) Subgroup provided an update to LATF on its progress in developing a PBR methodology for non-variable deferred annuities. The Subgroup reported that it is currently considering an approach that would consist of a floor (i.e., formulaic) reserve and a modeled reserve with an exclusion test for the modeled reserve. Potential methodologies under consideration for the floor reserve include a proposal from the Academy’s Annuity Reserve Working Group (ARWG) and a “simplified method” proposed by the Subgroup. The American Council of Life Insurers (ACLI) is conducting a small field test of the simplified method floor reserve. The Subgroup also reported that the Academy’s ARWG will attempt to leverage the work currently being performed by the Variable Annuities Issues (E) Working Group (VAIWG) on various aspects of AG43 to develop a methodology for the modeled reserve that is consistent with the requirements of VM-21 based on Conditional Tail Expectation and Greatest Present Value of Accumulated Deficiencies concepts like those prescribed by AG43.

XXX/AXXX Reinsurance Framework The NAIC is finalizing its work to develop the XXX/AXXX Reinsurance Framework aimed at addressing changes in the regulation of term life (i.e., XXX) and universal life with secondary guarantees (i.e., AXXX) reserve financing transactions.

The Reinsurance (E) Task Force adopted the revised draft of the Term and Universal Life Insurance Reserve Financing Model Regulation (i.e., XXX/AXXX Credit for Reinsurance Model Regulation) that was exposed on 4 August 2016.3

The revised draft considered the recommendation of the LATF Drafting Group on the requirements in Section 4A that address scope exemptions (i.e., the previously exposed Options A and B were merged into a single option and incorporated reference to assumed yearly renewable term reinsurance) and Section 6 that address the actuarial method to establish the required level of primary security for each reinsurance treaty subject to its provisions (i.e., the previously exposed Option B with modification that will require LATF to synchronize the language in the Valuation Manual with the XXX/AXXX Credit for Reinsurance Model Regulation). The Task Force also approved technical edits to modify the language on the application of the actuarial method in Section 6 and the prohibition against avoidance of the requirements of the model regulation to covered policies in Section 9. The Task Force directed the NAIC staff to develop a project history memorandum to be submitted with the XXX/AXXX Credit for Reinsurance Model Regulation for consideration by the Financial Condition (E) Committee.

The Executive Committee and Plenary adopted amendments to Actuarial Guideline XLVIII — Actuarial Opinion and Memorandum Requirements for the Reinsurance of Policies Required to be Valued Under Sections 6 and 7 of the NAIC Valuation of Life Insurance Policies Model Regulation (AG48) to eliminate the use of NPR percentages for valuation dates after 31 December 2015. The NPR percentages are no longer necessary, since the Valuation Manual now references the use of the 2017 CSO tables.

EY AccountingLink | ey.com/us/accountinglink

5 | NAIC Bulletin August 2016

Other actions taken by various NAIC groups to implement the XXX/AXXX Reinsurance Framework include the development of proposals to revise the requirements for annual statement reporting and the risk-based capital (RBC) calculation for 2016. Refer to Appendix B and Appendix C in this publication for additional information on the related proposals.

Variable Annuity Framework The VAIWG continued working to identify potential changes to the NAIC statutory framework (i.e., statutory accounting, reserving and RBC requirements) for variable annuities. These changes are intended to encourage strong risk management practices by insurers and eliminate the need to reinsure variable annuity business through captive reinsurance transactions.

The VAIWG received a report from Oliver Wyman on the results of the 2016 Quantitative Impact Study (QIS) of 12 participating companies and their related considerations and recommendations for reserve and capital reform through proposed revisions to AG43 and the C3 Phase II requirements of the RBC calculation. The VAIWG also adopted revisions to the disclosure requirements for variable annuity products included in the annual statement and the disclosure requirements for transactions with variable annuity captives included in SSAP No. 61R, Life, Deposit-Type and Accident and Health Reinsurance.

Quantitative impact study The VAIWG exposed an Oliver Wyman report on 14 proposals aimed at addressing the complexities in the NAIC statutory framework for variable annuities. Comments are due by 14 November 2016.

The proposals can be grouped into the following categories:

• Align economically focused hedge assets with liability valuations

• Reform standard scenarios (AG43 and C3 Phase II)

• Align total asset requirement and reserves

• Revise asset admissibility for derivatives and deferred tax assets

• Standardize capital markets assumptions

Oliver Wyman affirmed eight of the proposals included in their preliminary report and subsequently tested as part of the QIS. The remaining six proposals represent new improvements to the reserving and RBC requirements for variable annuities that were identified by Oliver Wyman in the performance of the QIS. Concerns have been raised by industry representatives about the viability of these new proposals because many of the recommended improvements were not tested as part of the QIS.

The VAIWG will evaluate feedback to determine which of the proposals should be considered for adoption and will make sure those proposals are tested prior to implementation.

Effect on statutory accounting and reporting SAPWG exposed the following items referred by the VAIWG:

• An issue paper proposing special accounting treatment for certain limited derivatives hedging variable annuity guarantees (SAPWG Ref # 2016-03): The issue paper is meant to allow hedge accounting treatment under SSAP No. 86, Derivatives, for certain limited derivative contracts that otherwise would not meet the requirements for hedge accounting. However, the resulting accounting treatment will be covered in a new SSAP that is separate and distinct from the guidance in SSAP No. 86.

• Revisions to SSAP No. 56, Separate Accounts, removing the requirement to disclose total maximum guarantees for separate account products (SAPWG Ref # 2016-27): VAIWG is recommending adding more meaningful disclosures through additional interrogatories and modifications to the actuarial opinion.

• Revisions to the variable annuities captive disclosure required by SSAP No. 61R (SAPWG Ref # 2016-28): These are based on the VAIWG’s recommendations to update the disclosures for 2016 reporting and thereafter and include requiring disclosure of permitted practices that apply to captive reinsurers.

EY AccountingLink | ey.com/us/accountinglink

6 | NAIC Bulletin August 2016

Separately, the Blanks (E) Working Group (BWG) exposed an amendment to create a new variable annuities supplement and remove a variable annuity interrogatory in the annual statement (Ref #2016-27BWG). The VAIWG recommended this new supplement because it believes it will provide a more meaningful disclosure of the liabilities associated with variable annuity guarantees.

Refer to Appendix A and Appendix B in this publication for further information on the proposals’ comment periods.

Accounting Practices and Procedures (E) Task Force The Accounting Practices and Procedures (E) Task Force (AP&PTF) directed the SAPWG to develop statutory accounting guidance for certain limited derivative contracts used to hedge variable annuity guarantees that are subject to the reserve requirements of AG43. This guidance would focus on the reduction in non-economic surplus volatility caused by fluctuations in the value of these hedges as a result of interest rate sensitivity. The guidance would provide adequate safeguards to promote appropriate financial statement presentation and disclosures, sufficient transparency and regulatory oversight over the use of these hedges. The development of the specific hedge accounting guidance will be coordinated with the work currently being performed by the VAIWG to develop changes in the reserving methodology for variable annuities.

Statutory Accounting Principles (E) Working Group SAPWG took the following steps, in addition to those discussed in the Principle-Based Reserving and Variable Annuity Framework sections in this publication:

• SAPWG adopted revisions to SSAP No. 1, Accounting Policies, Risks & Uncertainties, and Other Disclosures, to clarify that the disclosure of permitted or prescribed practices should include all practices that affect statutory accounting (e.g., gross or net presentation of reported amounts or the use of different financial statement reporting lines) and not just those practices that affect net income or surplus (Ref #2015-52). An example to clarify the permitted practice disclosure was also adopted. The revisions are effective immediately.

• SAPWG adopted revisions to SSAP No. 97, Investments in Subsidiary, Controlled and Affiliated Entities, to incorporate the filing guidance for subsidiary, controlled or affiliated (SCA) entities from the Purposes and Procedures Manual of the NAIC Investment Analysis Office (P&P Manual) in an appendix (Ref #2015-25). The revisions, effective immediately, will remove conflicts with the content in SSAP No. 97.

• SAPWG also submitted a referral to the Valuation of Securities Task Force (VOSTF) to request changes to the P&P Manual that would retain a filing requirement and reference to SSAP No. 97 but remove the detailed SCA filing instructions.

• SAPWG adopted revisions to SSAP No. 2, Cash, Drafts, and Short-Term Investments, following the removal of money mutual funds from the Class 1 bond list to clarify that these investments are considered to be short term and are reported on Schedule DA (Ref #2016-05). However, the statutory accounting for these investments will continue to follow the applicable guidance in SSAP No. 26, Bonds, or SSAP No. 30, Unaffiliated Common Stock, based on the nature and characteristics of the investment. The revisions are effective immediately.

• SAPWG exposed an issue paper and substantive revisions to SSAP No. 2 that would require investments in money market mutual funds to be classified as cash equivalents. Comments are due by 10 October 2016 (Ref # 2016-18). The revised statutory accounting guidance would require prospective application as of 1 January 2018. Interested parties have requested an earlier effective date.

• SAPWG reexposed revisions to SSAP No. 3, Accounting Changes and Corrections of Errors, to clarify the existing guidance on recognition of the correction of an accounting error (Ref #2015-46). Comments are due by 10 October 2016. The proposed changes would address the actions to be taken when the reporting entity becomes aware of a material accounting error in previously issued financial statements and how all accounting errors should be corrected if an amended financial statement is not filed.

EY AccountingLink | ey.com/us/accountinglink

7 | NAIC Bulletin August 2016

• SAPWG exposed revisions to Appendix A-010, Minimum Reserve Standards for Individual and Group Health Insurance Contracts, to incorporate the use of the 2013 individual disability income valuation table (Ref #2016-17). Comments are due by 10 October 2016. Entities would have to adopt this table as of 1 January 2020, with early adoption allowed beginning on 1 January 2017. The requirements of Appendix A-010 are incorporated into SSAP No. 54, Individual and Group Accident and Health Contracts.

• SAPWG exposed additional options for reporting investment information in the quarterly statement blank (Ref #2015-27). Comments are due by 10 October 2016. The proposed alternatives would expand on the three previously exposed options and include the possibility of a semiannual collection of investment data and a data-only (non-PDF) submission of Schedule D investments, with information detailing CUSIP, par value, book/adjusted carrying value and fair value to be received with the quarterly statement blank for the second quarter.

• SAPWG exposed BlackRock’s suggested systematic valuation methodology and the responses to questions raised on their calculated valuation proposal (Ref #2013-36). Comment are due by 10 October 2016. SAPWG agreed to submit a referral to the VOSTF requesting a review of BlackRock’s suggested calculation.

• SAPWG also directed the NAIC staff to prepare an issue paper for bond-approved exchange-traded funds and bond mutual funds in scope of SSAP No. 26 to require measurement at fair value (using net asset value as a practical expedient), unless the reporting entity elects to use a documented “systematic value” approach that has been approved by the domiciliary state. The issue paper would also include the definition of a “security” along with definitions for investments that are not included in the proposed bond definition (e.g., loan participation, loan syndication) for treatment as bond-like investments. These proposals are also part of the investment classification review project (Ref #2013-36).

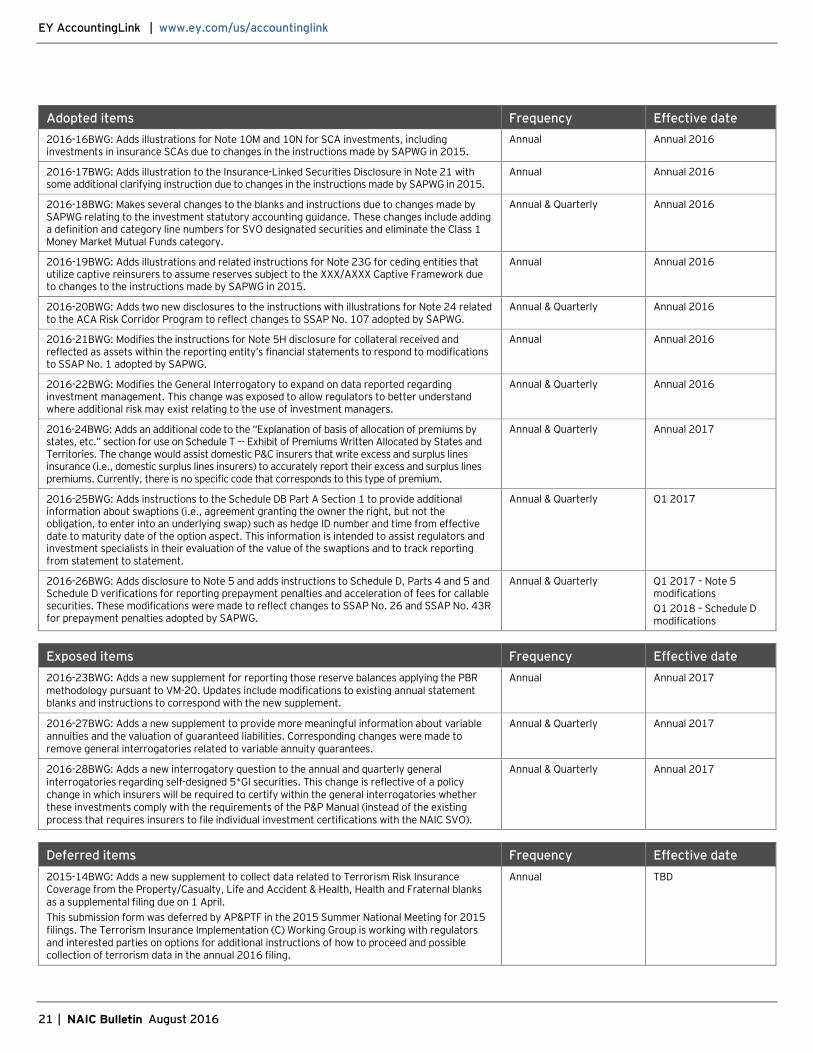

Appendix A in this publication summarizes the actions taken by SAPWG since the 2016 Spring National Meeting.

Restricted Assets (E) Subgroup The Subgroup finalized its work to develop enhanced disclosure requirements for repurchase and reverse repurchase transactions in SSAP No. 103R, Transfers and Servicing of Financial Assets and Extinguishments of Liabilities, and referred the updated guidance to SAPWG. SAPWG exposed the proposed revisions to SSAP No. 103 and related disclosure templates developed by the Subgroup for a comment period ending 10 October 2016.

Blanks (E) Working Group Appendix B in this publication summarizes the actions taken by the BWG since the 2016 Spring National Meeting.

Life Insurance and Annuities (A) Committee The A Committee received a report of the Life Insurance Illustration Issues (A) Working Group and adopted its recommendation to move forward with developing a short consumer-oriented document to explain key components of life insurance products. The A Committee will also develop a plan to revise the content of the Life Insurance Buyer’s Guide that will assist consumers in making informed decisions when buying a policy.

Additionally, the A Committee discussed ways to promote state adoption and compliance with the Suitability in Annuity Transactions Model Regulation (#275), which has been adopted by 37 states as of 4 August 2016.

The A Committee will also review and revise as necessary the following annuity-related illustration and sales guidance:

• Section 6. Standards for Annuity Illustrations in the Annuity Disclosure Model Regulation (#245), which has been adopted by seven states as of 15 August 2016. Specific consideration will be given to disclosures that are necessary to inform consumers given the innovations in products currently in the marketplace.

EY AccountingLink | ey.com/us/accountinglink

8 | NAIC Bulletin August 2016

• Model Regulation on the Use of Senior-Specific Certifications and Professional Designations in the Sale of Life Insurance and Annuities (#278), which has been adopted by 39 states as of 15 August 2016.

• The NAIC’s Producer and Insurer Bulletin and Consumer Alert — Preventing Abusive Practices: The Misuse of Senior Designations and “Free Lunch” Seminars, which has been adopted by five states as of 15 August 2016.

Life Actuarial (A) Task Force LATF received the report of the Longevity Risk (A/E) Subgroup, which continues its work to “provide recommendations for recognizing longevity risk in statutory reserves and/or RBC, as appropriate.” The Subgroup provided an update on the results of its survey on the reflection of longevity risk in asset adequacy testing and proposed an approach to a voluntary field testing process with the ACLI to size longevity risk in reserves and capital. LATF also heard a presentation from the Academy Longevity Risk Task Force on research and results of testing it had completed around longevity risk.

LATF received a report from the SOA on the development of the 2017 Generally Recognized Expense Table (GRET), which is used in policy illustrations. LATF voted to expose the 2017 GRET for a comment period ending 28 September 2016.

LATF voted to disband the Contingent Deferred Annuity (A) Subgroup, since it had completed its charges.

VM-22 (A) Subgroup The Subgroup proposed modifying the process for determining the maximum statutory valuation interest rates for income annuities. The proposed methodology seeks to address shortcomings of the current methodology and tie the prescribed valuation data more closely to the time of annuity contract inception. Comments are due by 11 November 2016.

The Subgroup also received a proposal from the Academy for revisions to the Separate Accounts Funding Guaranteed Minimum Benefits Under Group Contracts Model Regulation (#200), to achieve consistency with the revisions to the Synthetic Guaranteed Investment Contracts Model Regulation (#695), adopted in 2015. Members of the Subgroup (except its New York member) expressed their support for the proposed revisions to Model #200. The Subgroup will schedule an interim conference call to present the proposed revisions to LATF.

Unclaimed Life Insurance Benefits (A) Working Group The Unclaimed Benefits Model Drafting (A) Subgroup completed its work to develop a draft of the Unclaimed Life Insurance and Annuities Model, which includes provisions that are similar to the National Conference of Insurance Legislators Model Unclaimed Life Insurance Benefits Act and the requirements in the regulatory settlement agreements reached with a number of insurers. The proposed model act is intended to establish a uniform process for life insurance companies to identify deceased insured individuals and perform meaningful searches for beneficiaries entitled to receive unclaimed life insurance (i.e., death) benefits. The Subgroup referred the draft of the proposed model act to the Unclaimed Life Insurance Benefits (A) Working Group. The Working Group will schedule interim conference calls to discuss and consider its requirements.

Health Insurance and Managed Care (B) Committee The B Committee adopted revisions to VM-25 to address a timing issue with the reserve requirements for health insurance. The revisions replace the current language in the Valuation Manual with a provision indicating that the reserve requirements for group accident and health insurance certificates issued on or after 1 January 2017, are the applicable requirements found in the Accounting Practices and Procedures Manual (AP&P Manual).

The B Committee adopted revisions to the Health Insurance Reserves Model Regulation (#10) that replace the 1985 Commissioners Individual Disability Table with the 2013 Individual Disability Income Table. The B Committee also adopted Actuarial Guideline L — 2013 Individual Disability Income Valuation Table (AG 50), which provides instructions for the use of the 2013 Individual Disability Income Valuation Table.

EY AccountingLink | ey.com/us/accountinglink

9 | NAIC Bulletin August 2016

The B Committee adopted the model law development request from the Senior Issues (B) Task Force to revise the Long-Term Care Insurance Model Act (#640) and the Long-Term Care Insurance Model Regulation (#641). The revisions will update the disclosure provisions in Model #640 and Model #641 to reflect the large and multiple rate increases on policyholders, including those holding policies sold under the rate stabilization standards, which have occurred since the models were last updated.

Health Actuarial (B) Task Force HATF adopted revisions to the NAIC Guidance Manual for Rating Aspects of the Long-Term Care Insurance Model Regulation, which is used to evaluate compliance with the rating requirements under Model #641.

HATF exposed the final report from the Academy and SOA on their development of the updated cancer claims cost tables, which will replace the 1985 cancer claim cost tables. Comments are due by 6 October 2016.

Long-Term Care Actuarial (B) Working Group The Working Group proposed a new actuarial guideline (i.e., Actuarial Guideline Long-Term Care) to provide uniform guidance for insurers with a major block of long-term care contracts, effective 31 December 2017. The proposal would require standalone asset adequacy testing for inforce business and new issues, along with documentation of assumptions and a uniform approach to establish the assumption for future rate increases. Deficiencies identified as a result of the testing would be recorded as additional reserves in the statutory-basis financial statements. Comments are due by 5 November 2016.

Property and Casualty Insurance (C) Committee The C Committee discussed the feedback on its previously exposed draft document of principles for recommended reforms to the National Flood Insurance Program (NFIP). The C Committee will schedule an interim conference call to receive additional comments, with the goal of recommending the adoption of final principles for NFIP reforms by the end of 2016.

The C Committee also discussed the 2016 Workers’ Compensation Large Deductible Study performed by the NAIC/IAIABC Joint (C) Working Group. Previous discussions by the Workers Compensation (C) Task Force on the recent insolvencies of workers’ compensation insurers, the growth of the large deductible market and the increased number of workers affected by large deductibles were contributing factors that resulted in the decision to update the original study performed in 2006.

The updated study is intended to educate readers on the use, business practices and potential risks of large deductible policies in workers’ compensation with a focus on six key areas:

• Employer insurance buying trends

• Solvency concerns

• Claims

• State filing requirements

• Special considerations for workers’ compensation underwriters

• Unique concerns of professional employer organizations (PEOs)

Unlike the original study, which was designed largely by regulators for regulators, the updated study provides a snapshot of the large/mega-deductible landscape. It is intended to serve as a resource for all affected parties, including employers, workers’ compensation insurance underwriters, injured workers, advisory organizations, guaranty funds, PEOs and regulators. The updated study also provides a comprehensive overview of large deductibles and the issues related to successfully underwriting and regulating these accounts and can be used as a practical guide for regulators, insurance underwriters and employers with deductible products. The C Committee will schedule an interim conference call to consider adoption of the updated study.

The C Committee approved a second request to extend the deadline for revisions to the Creditor-Placed Insurance Model Act (#375). The Creditor-Placed Insurance Model Act Review (C) Working Group is currently reviewing Model #375 to determine whether it should be retained as a model law, amended, converted to a guideline or archived.

EY AccountingLink | ey.com/us/accountinglink

10 | NAIC Bulletin August 2016

Financial Condition (E) Committee The E Committee previously agreed to develop contingency plans that would continue to protect US consumers and US ceding insurance companies under the US system of state-based insurance regulation from the potential adverse effects of the covered agreement that the US Department of the Treasury and the Office of the US Trade Representative are negotiating with the EU. Three methods to mitigate the potential loss of consumer protection collateral have been suggested by the E Committee: (1) expanding the certified reinsurance process, (2) requiring consumer protection in the form of added required capital for US ceding companies or (3) requiring all reinsurers to file certain limited information with the NAIC under new authority created by a new NAIC model. These methods will be considered by the E Committee in a future meeting.

The E Committee adopted revisions to the Life and Health Guaranty Association Model Act (#520) to clarify that guaranty association coverage isn’t applicable to factored structured settlement annuity benefits, which are structured settlement annuity benefits that have been sold to a third party by the original annuitant.

Capital Adequacy (E) Task Force Appendix C in this publication summarizes the actions taken since the 2016 Spring National Meeting by the Task Force and the various NAIC groups that report to it.

The Task Force formed an ad hoc group to evaluate affiliated investment risks in all of the RBC formulas in response to an issue raised by the P&C RBC (E) Working Group (PCRBC) that affiliated investment risks were not easy to understand. Separately, the PCRBC will make a related modification to the Type 7 affiliated investment instructions to correct a mismatch with the RBC formula.

The Health RBC (E) Working Group (HRBC) withdrew a previously adopted modification to the 2016 Health RBC calculation on Medicaid pass-through payments (Ref #2015-26 H). The modification was withdrawn as concerns were raised by industry representatives about potential issues that may exist in the RBC calculation if the modified requirements are implemented. The HRBC elected to extend its temporary correction to the 2015 Health RBC guidance for Medicaid pass-through payments to 2016 (Ref #2015-27 H) while it reconsiders the effect of the withdrawn modifications.

The Operational Risk (E) Subgroup continued to evaluate the inclusion of operational risk in all of the RBC formulas. Two primary approaches are under consideration by the Subgroup to apply an operational risk charge in the RBC formula: an exposure proxy approach (i.e., apply a factor to net premiums and net reserves reported by the insurer) and an RBC add-on approach (i.e., apply a factor to the RBC calculated by the insurer). To further evaluate operational risk, the Subgroup adopted a new “informational only” amendment for the 2016 RBC filings to collect more information by applying operational risk factors to the RBC calculation (Ref #2016-05 O).

Investment RBC (E) Working Group The Investment RBC (E) Working Group (IRBC) started its project to assess the RBC charges for investment risk in all of the RBC formulas using the guiding principles included in the previously exposed “Way Forward” document. The IRBC determined it would first assess the structure of the RBC formulas for investment risk (e.g., determine number of designations) to determine the appropriate factors to apply to a specific investment risk.

The IRBC has made the following tentative decisions on the structure of the Life RBC formula:

• NAIC bond designations should be expanded from six to 20 in the C1 corporate bond factors. However, for statutory accounting and regulatory (i.e., state law) purposes, the current system of six designations would not be changed.

• Asset valuation reserve (AVR) designations for corporate bonds would also increase from six to 20 for purposes of the RBC calculation. However, no changes would be made to the calculation of realized gains/losses relating to AVR, which would continue to use the current system.

• Other assets that currently use corporate bond factors (e.g., Schedule BA assets, preferred stock) would maintain the six designations.

EY AccountingLink | ey.com/us/accountinglink

11 | NAIC Bulletin August 2016

• Designations for structured securities (including modeled and non-modeled securities) that are recorded based on statutory guidance in SSAP No. 43R, Loan-backed and Structured Securities, should be expanded from six to 20.

• Blanks and instructions will need to be updated for these decisions on the structure of the RBC formulas for investment risk.

The Working Group also intends to assess the portfolio adjustments (i.e., asset concentration factor and bond size factor) included in the Life RBC investment risk calculation as part of its project. In future meetings, the Working Group will discuss the factors to assign to these designations and consider the investment risk for assets such as common stock and real estate.

The Academy is also running the bond model for Health and P&C RBC considerations that include known adjustments from the Life RBC formula such as tax adjustments and risk premium offset. This analysis will help to inform the IRBC in its considerations of whether the structure and factors should be modified in the Health and P&C RBC calculations for investment risk.

The Working Group continues to progress toward its goal to have the updated structure and factors for investment risk ready for use in each of the RBC formulas by the end of 2017.

Group Capital Calculation (E) Working Group The Working Group continued its work on the development of a US group capital calculation. The calculation will be applicable to US-domiciled insurance groups and provide information intended to enhance the ability of state insurance regulators to monitor insurer solvency at the group level. The calculation is not meant to establish a US group capital calculation but rather is another assessment tool a regulator may use when assessing an insurance company.

The Working Group has determined that the inventory method (i.e., identify a specific charge for each company in the group) is the most appropriate approach to use in developing the calculation. The Working Group exposed an NAIC staff memorandum to solicit feedback on a number of key questions about the use of the inventory method, including: the scope of the calculation (e.g., which entities in an insurance holding company structure would be subject to the calculation); how to determine and apply charges to different types of companies that are not insurance entities and may or may not already be subject to other capital requirements; and the use of scalars (i.e., factors) for non-US insurance companies that are subject to regulatory requirements in their domicile jurisdiction. Comments are due by 25 October 2016.

Group Solvency Issues (E) Working Group The Working Group reviewed and discussed the results of a survey on the use and effectiveness of Enterprise Risk Report (i.e., Form F) filings. The responses provided by 36 state insurance regulators indicated that many are not satisfied with the information currently being provided in Form F filings. The Working Group discussed options for improving the process, such as guidance on what to include in Form F filings and how their scope differs from the scope of Own Risk and Solvency Assessment (ORSA) filings. The Working Group directed the NAIC staff to begin drafting this guidance for review and consideration by the Working Group in a future meeting.

ORSA Implementation (E) Subgroup The Subgroup developed and previously exposed a “best practice” document to promote consistency among state insurance regulators on the sharing of information included in ORSA filings. ORSA filings often apply to a number of large groups with domestic insurers in various states, and regulators are encouraged to rely on the lead state to perform the primary review and assessment of the information submitted. Regulators have also recognized a need to establish some best practices for this process to preserve confidentiality while reducing redundant review efforts. The Subgroup will schedule an interim conference call to discuss the comments received on the exposed document.

EY AccountingLink | ey.com/us/accountinglink

12 | NAIC Bulletin August 2016

Reinsurance (E) Task Force The Task Force adopted revisions to the Uniform Application Checklist for Certified Reinsurers to address the timeliness of issued financial strength ratings, the appropriate disclosure of material International Financial Reporting Standards (IFRS) to GAAP adjustments, a notation regarding the funding of trust accounts and the jurisdictional requirements regarding actuarial reporting.

The Task Force referred a request to the Qualified Jurisdiction (E) Working Group to study and report on EU member state implementation of Solvency II and its potential effect on Qualified Jurisdiction status. Regulators have expressed a desire to better understand the effect of recent actions taken by certain EU jurisdictions that restrict the ability of US-domiciled insurance and reinsurance companies to conduct business in those jurisdictions, and any other actions taken by other EU member states that would affect reinsurance and group solvency.

Risk-Focused Surveillance (E) Working Group The Working Group referred proposed guidance for gaining an understanding of an insurance company in support of a risk-focused financial analysis to the Financial Analysis Handbook (E) Working Group. The Working Group suggested that the proposed guidance be included in the framework section of the Financial Analysis Handbook. The guidance would outline procedures and the topics on which regulatory filings and public sources of information may not be sufficient for an analyst to develop an adequate understanding of the entity.

The Working Group previously exposed guidance to be included in the Financial Analysis Handbook to promote greater uniformity and consistency in the prioritization framework used by state insurance regulators. The proposed guidance would encourage all states to use a prioritization scale of 1–5, with priority 1 representing the highest priority company for solvency monitoring purposes, and further define each priority rating. The Working Group will schedule an interim conference call to discuss the comments received on the exposed guidance.

Valuation of Securities (E) Task Force The Reporting Exceptions Analysis (E) Working Group of the VOSTF was formed to evaluate the cause of certain reporting exceptions that appear on the NAIC Jumpstart Exception Report (i.e., the population of securities reported by insurance companies that possibly should have been filed with the Investment Analysis Office (IAO)) and recommend ways to address these exceptions. The Working Group discussed a listing of the reporting anomalies identified to date that have caused these exceptions with the intention to complete its evaluation in September.

VOSTF revised the content of the P&P Manual after recent actions by SAPWG, as follows:

• VOSTF adopted an amendment to modify the guidance on surplus notes included in various sections of the P&P Manual to correspond with adopted revisions to SSAP No. 41R, Surplus Notes.

• VOSTF adopted a revised definition for “loan-backed and structured securities” to be included in the P&P Manual, which was considered necessary due to questions that have been raised by interested parties as a result of the changes to SSAP No. 43R adopted in 2010. This revised definition was referred back to SAPWG.

• VOSTF exposed an amendment to delete the reporting instructions for money market mutual funds to correspond with the adopted clarifications to statutory accounting and reporting guidance for a comment period ending 30 September 2016.

VOSTF also acted on several proposals to amend the P&P Manual as follows:

• VOSTF adopted a policy change for 5* securities, which requires an insurer to self-certify that it is receiving and expects to continue receiving interest and principle on the security. Previously, the Securities Valuation Office (SVO) was tasked with performing due diligence over these certifications. This policy change required removal of guidance from the P&P Manual and created a new general interrogatory for the self-certification that was exposed by the BWG (Ref #2016-28BWG).

• VOSTF exposed an SVO recommendation to amend the P&P Manual to clarify the definition and purpose of NAIC designations. The SVO’s initial report concluded the use of the NAIC designation is clear in the P&P Manual; however, a user of the P&P Manual could conclude that NAIC designations are only associated with credit risk as a result of certain language that exists in the P&P Manual, which is not appropriate as the designation process is focused on a quality of a security assessment. Comments on the SVO report and recommendation are due by 21 November 2016.

EY AccountingLink | ey.com/us/accountinglink

13 | NAIC Bulletin August 2016

• VOSTF adopted an amendment to include Italian GAAP as a National Financial Presentation Standard, which will allow insurers to file securities with the IAO that have audited financial statements prepared on this basis of accounting without including a reconciliation to US GAAP or IFRS.

• VOSTF exposed an amendment to include Belgian GAAP as a National Financial Presentation Standard for a comment period ending 30 September 2016.

• VOSTF adopted an amendment to include H.R. Ratings de Mexico, S.A. de C.V. as a credit rating provider on the NAIC Credit Rating Provider List, meaning that credit ratings issued to certain securities by H.R. Ratings de Mexico, S.A. de C.V. must be used by insurers in the administration of the filing exempt process.

• VOSTF adopted an amendment that eliminates a requirement for public meetings to be held as part of the assumption setting phase of the financial modeling methodology (i.e., determining assumptions for RMBS and CMBS), after the IAO staff indicated that insurers already understand the methodology and process.

Financial Regulation Standards and Accreditation (F) Committee The F Committee adopted revisions to the Review Team Guidelines and the Accreditation Review Process and Procedures to enhance the accreditation program and related guidance, effective 1 January 2017. The revisions shift the focus of the accreditation standards from compliance toward substance and quality of work performed. The F Committee also exposed revisions to the Self-Evaluation Guide, Interim Annual Review intended to update and align its content with the adopted enhancements to the accreditation program and related guidance. Comments are due by 28 October 2016.

The F Committee also adopted the revisions made to the Financial Condition Examiners Handbook by the Financial Examiners Handbook (E) Technical Group in 2015 that would affect the accreditation standards and/or review team guidelines, effective 1 January 2017. The revision identified by the Task Force as “significant” for accreditation purposes clarifies the responsibility for state insurance department oversight of contract examiners. Other revisions include allowing the use of interim work, enhancing the examiner’s ability to address cybersecurity risks, clarifying the required elements to review related party transactions and permitting the use of a single exam report when multiple entities that are part of the insurance company group are domiciled in the same state.

The F Committee received an update on the status of the 2009 revisions to Model #820 related to PBR. The F Committee indicated that LATF would be sending a referral regarding significant elements of Model #820 to be included in Part A: Laws and Regulations Accreditation Preamble of the general accreditation standards, during the 2016 Fall National Meeting.

The F Committee exposed the recommendation from the Risk Retention Group (E) Task Force to revise the CPA audits standard in Part A: Laws and Regulations-Risk Retention Groups (RRGs) Organized as Captives of the general accreditation standards for a comment period ending 28 September 2016. The revisions address the overlap between the audit partner rotation requirements included in the Annual Financial Reporting Model Regulation (#205) and the Model Risk Retention Act (#705) and provide guidance on how to appropriately apply each standard for accreditation purposes.

International Insurance Relations (G) Committee The G Committee continued discussing the activities of the International Association of Insurance Supervisors (IAIS) and their potential effect on the US system of state-based insurance regulation. Specific updates were provided on the work of the IAIS in the following areas:

• Standard-setting activities – The G Committee submitted the NAIC comments to the IAIS on the following draft application papers related to supervision: the Application Paper on Approaches to Supervising the Conduct of Intermediaries and the Application Paper on the Regulation and Supervision of Mutuals, Cooperatives and Community-based Organisations in Increasing Access to Insurance Markets. The IAIS will vote to adopt final versions of each application paper at its meetings in November. The G Committee also submitted the NAIC comments to the IAIS on the Issues Paper on Cyber Risk to the Insurance Sector, which is intended to raise awareness for insurers and supervisors of the challenges presented by cyber risk, including current and contemplated supervisory approaches for addressing this risk.

EY AccountingLink | ey.com/us/accountinglink

14 | NAIC Bulletin August 2016

• Financial stability – The IAIS released its updated assessment of the methodology to determine globally systemically important insurers (G-SIIs). The 2016 methodology is based on the following five-phase approach: (1) the collection of data from insurers subject to the assessment; (2) quality control and scoring of the data submitted to determine the quantitative threshold to be used for further analysis; (3) an assessment of quantitative and qualitative considerations related to the heterogeneity of an insurer’s structure, activities, products, exposures and global activities within the insurance industry with consideration for differences in data quality reported across insurers and across jurisdictions; (4) information exchange with potential G-SIIs; and (5) IAIS list of G-SIIs recommended to the Financial Stability Board.

• Implementation – The IAIS self-assessment reports for market conduct and solvency are currently being drafted, with the self-assessment reviews for reinsurance and macroprudential standards currently in process.

• Stakeholder engagement – The IAIS has indicated that recommended improvements will be forthcoming to its procedures to providethe appropriate level of transparency, communication and ability for stakeholder engagement.

The G Committee also discussed the experience of US-domiciled insurance and reinsurance companies with the implementation of Solvency II by the 28 EU member states, including perceived barriers to doing business in EU jurisdictions. Concerns about the level of uncertainty on the ability to conduct business in certain of these jurisdictions were raised, since the US system of state-based insurance regulation is not considered an equivalent jurisdiction for Solvency II. Other concerns were raised on the ability of a covered agreement negotiated to gain equivalency being able to preempt state law.

ComFrame Development and Analysis (G) Working Group The Working Group discussed the IAIS consultation document to solicit feedback on valuation, qualifying resources and a method for setting the capital requirement in Version 1.0 of the risk-based global insurance capital standard, which is expected to be released in mid-2017, with the final version (i.e., Version 2.0) expected to be adopted in 2019. Specific questions in the consultation document have been targeted for NAIC responses with initial views provided by the NAIC staff. The Working Group will schedule an interim conference call to discuss these questions and the related responses to be submitted to the IAIS. The proposed responses will then be sent to the G Committee for its review and consideration prior to the comment deadline of 19 October 2016.

The Working Group also received an update on the field testing and development of the IAIS Common Framework for the Supervision of Internationally Active Insurance Groups (ComFrame), which is a set of international supervisory requirements focusing on the effective group-wide supervision of internationally active insurance groups. ComFrame has been developed based on the requirements and guidance currently established in the IAIS Insurance Core Principles, which are globally accepted requirements for the supervision of the insurance sector. The IAIS expects to release revisions to the modules of ComFrame related to governance, supervisory process and resolution for public consultation in November (i.e., after completion of the IAIS meetings).

Stay tuned The 2016 Fall National Meeting is scheduled for 10–13 December 2016, in Miami. Conference calls or other meetings will be held before then. A list of meetings can be found at http://naic.org/meetings_calendar.htm.

Endnotes: _______________________ 1 The revised draft of the proposed model law can be found on the NAIC’s website at

http://www.naic.org/committees_ex_cybersecurity_tf.htm. 2 The amended Valuation Manual as of 29 August 2016, can be found on the NAIC’s website at

http://www.naic.org/committees_a_latf.htm. 3 The draft version of the XXX/AXXX Credit for Reinsurance Model Regulation is on the NAIC’s website at

http://www.naic.org/committees_e_reinsurance.htm.

EY | Assurance | Tax | Transactions | Advisory

© 2016 Ernst & Young LLP. All Rights Reserved.

SCORE No. 02855-161US

ey.com/us/accountinglink

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US. This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

EY AccountingLink | www.ey.com/us/accountinglink

15 | NAIC Bulletin August 2016

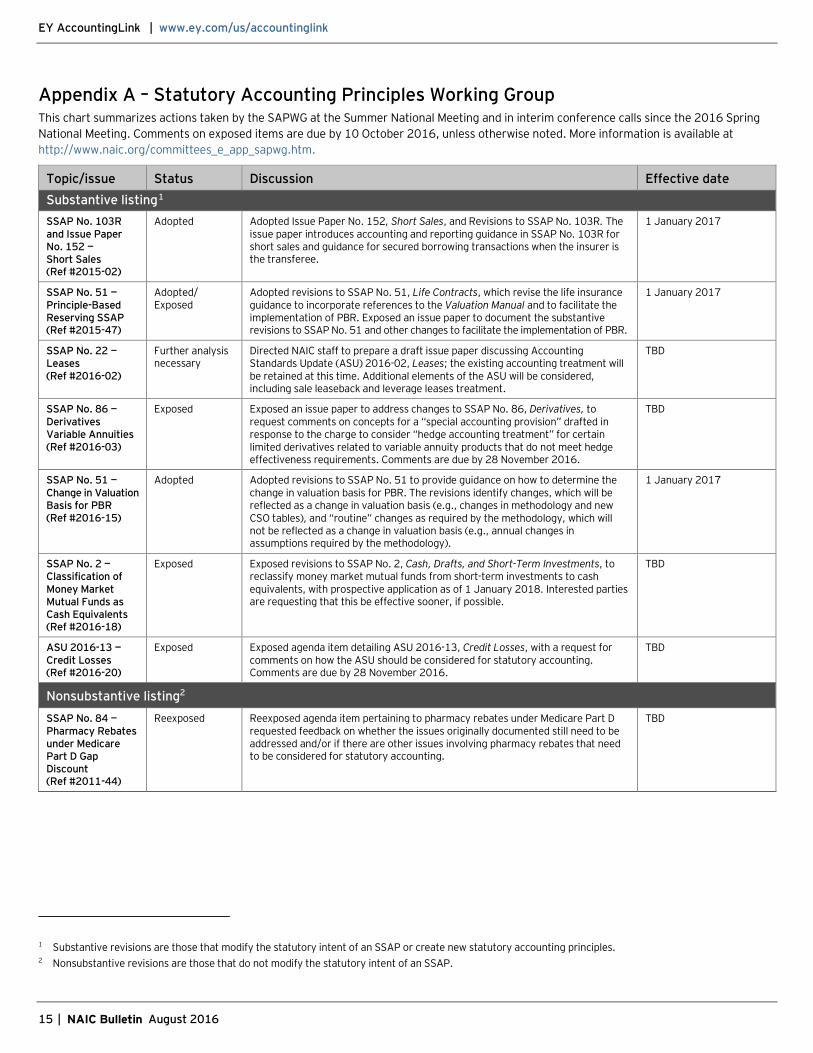

Appendix A – Statutory Accounting Principles Working Group This chart summarizes actions taken by the SAPWG at the Summer National Meeting and in interim conference calls since the 2016 Spring National Meeting. Comments on exposed items are due by 10 October 2016, unless otherwise noted. More information is available at http://www.naic.org/committees_e_app_sapwg.htm.

Topic/issue Status Discussion Effective date Substantive listing1 SSAP No. 103R and Issue Paper No. 152 — Short Sales (Ref #2015-02)

Adopted Adopted Issue Paper No. 152, Short Sales, and Revisions to SSAP No. 103R. The issue paper introduces accounting and reporting guidance in SSAP No. 103R for short sales and guidance for secured borrowing transactions when the insurer is the transferee.

1 January 2017

SSAP No. 51 — Principle-Based Reserving SSAP (Ref #2015-47)

Adopted/ Exposed

Adopted revisions to SSAP No. 51, Life Contracts, which revise the life insurance guidance to incorporate references to the Valuation Manual and to facilitate the implementation of PBR. Exposed an issue paper to document the substantive revisions to SSAP No. 51 and other changes to facilitate the implementation of PBR.

1 January 2017

SSAP No. 22 — Leases (Ref #2016-02)

Further analysis necessary

Directed NAIC staff to prepare a draft issue paper discussing Accounting Standards Update (ASU) 2016-02, Leases; the existing accounting treatment will be retained at this time. Additional elements of the ASU will be considered, including sale leaseback and leverage leases treatment.

TBD

SSAP No. 86 — Derivatives Variable Annuities (Ref #2016-03)

Exposed Exposed an issue paper to address changes to SSAP No. 86, Derivatives, to request comments on concepts for a “special accounting provision” drafted in response to the charge to consider “hedge accounting treatment” for certain limited derivatives related to variable annuity products that do not meet hedge effectiveness requirements. Comments are due by 28 November 2016.

TBD

SSAP No. 51 — Change in Valuation Basis for PBR (Ref #2016-15)

Adopted Adopted revisions to SSAP No. 51 to provide guidance on how to determine the change in valuation basis for PBR. The revisions identify changes, which will be reflected as a change in valuation basis (e.g., changes in methodology and new CSO tables), and “routine” changes as required by the methodology, which will not be reflected as a change in valuation basis (e.g., annual changes in assumptions required by the methodology).

1 January 2017

SSAP No. 2 — Classification of Money Market Mutual Funds as Cash Equivalents (Ref #2016-18)

Exposed Exposed revisions to SSAP No. 2, Cash, Drafts, and Short-Term Investments, to reclassify money market mutual funds from short-term investments to cash equivalents, with prospective application as of 1 January 2018. Interested parties are requesting that this be effective sooner, if possible.

TBD

ASU 2016-13 — Credit Losses (Ref #2016-20)

Exposed Exposed agenda item detailing ASU 2016-13, Credit Losses, with a request for comments on how the ASU should be considered for statutory accounting. Comments are due by 28 November 2016.

TBD

Nonsubstantive listing2 SSAP No. 84 —Pharmacy Rebates under Medicare Part D Gap Discount (Ref #2011-44)

Reexposed Reexposed agenda item pertaining to pharmacy rebates under Medicare Part D requested feedback on whether the issues originally documented still need to be addressed and/or if there are other issues involving pharmacy rebates that need to be considered for statutory accounting.

TBD

1 Substantive revisions are those that modify the statutory intent of an SSAP or create new statutory accounting principles. 2 Nonsubstantive revisions are those that do not modify the statutory intent of an SSAP.

EY AccountingLink | www.ey.com/us/accountinglink

16 | NAIC Bulletin August 2016

Nonsubstantive listing2 (continued)

SSAP No. 26 — Investment Classification Review (Ref #2013-36)

Further analysis necessary/ Exposed

Directed NAIC staff to prepare an issue paper for bond-approved exchange-traded funds and bond mutual funds in scope of SSAP No. 26 to require measurement at fair value (using net asset value as a practical expedient), unless the reporting entity elects to use an approved documented “systematic value” approach. Exposed BlackRock’s suggested systematic value calculation for comment.

TBD

SSAP No. 16R — ASU 2015-05: Fees Paid in a Cloud Computing Arrangement (Ref #2015-15)

Reexposed Requested comments to the revisions of SSAP No. 16R, Electronic Data Processing Equipment and Software, on whether guidance on cloud computing arrangements is necessary for statutory accounting.

TBD

SSAP No. 26 and SSAP No. 43R — Measurement Method for NAIC 5 Designations (Ref #2015-17)

Deferred* Deferred revisions to require AVR filer investments designated as an NAIC 5 to be reported at the lower of amortized cost or fair value until Ref # 2015-41 on NAIC 5* securities is complete.

TBD

SSAP No. 55 — Clarification of Accounting Treatment for Fees Incurred for Salvage/Subrogation Recoveries (Ref #2015-21)

Adopted Adopted the proposed revisions to SSAP No. 55, Unpaid Claims, Losses and Loss Adjustment Expense, to clarify the reporting of anticipated and received salvage and subrogation amounts.

Immediately

SSAP No. 86 Appendix D — FAS 133 EITFs (Ref #2015-22)

Further analysis necessary*

Directed the NAIC staff to note specified Financial Accounting Standard (FAS) 133 Emerging Issues Task Force issuances as pending in Appendix D and to prepare subsequent agenda items for review and consideration.

TBD

SSAP No. 26 and SSAP No. 43R —Prepayment Penalties on Callable Bonds (Ref #2015-23)

Adopted Adopted amendments to SSAP No. 26 and SSAP No. 43R to add a new disclosure to capture the number of CUSIPs and aggregate amount of investment income generated as a result of prepayment penalties and/or acceleration fees. Additional revisions clarify the amount of investment income and/or realized gain/loss to be reported upon disposal of an investment. The revisions are effective on a prospective basis.

1 January 2017

SSAP No. 97 —Inclusion of Filing Guidance (Ref #2015-25)

Adopted Adopted a new appendix to SSAP No. 97, Investments in Subsidiary, Controlled and Affiliated Entities, detailing the SCA reporting and filing process. The appendix matches SSAP No. 97, paragraph 18, as recommended by interested parties. With the adoption, NAIC staff recommend a referral to the VOSTF requesting the Task Force to proceed with amending the P&P Manual to delete the SCA instructions; retaining a filing requirement for SCAs and to add reference to the statutory accounting guidance.

Immediately

Quarterly Reporting of Investment Schedules (Ref #2015-27)

Reexposed Expanded the alternatives for quarterly investment reporting; new options include the possibility of a semiannual collection of investment data and a data-only (non-PDF) submission of Schedule D investments, with information detailing CUSIP, par value, book/adjusted carrying value and fair value to be received with the quarterly statement blank for the second quarter.

TBD

Aging and Revenue Recognition of Multi-Peril Crop Policies (Ref #2015-33)

Further analysis necessary*

Directed NAIC staff to work with interested parties, regulators and key stakeholders to develop recommendations for updating SSAP No. 78, Multiple Peril Crop Insurance, regarding (1) the use of the billing date for application of the 90-day rule, (2) defining the processing date or updating the term, (3) providing more specificity regarding the period of risk for purposes of earning revenue and (4) developing a glossary of terms.

TBD

EY AccountingLink | www.ey.com/us/accountinglink

17 | NAIC Bulletin August 2016

Nonsubstantive listing2 (continued)

ASU 2015-09: Financial Services — Insurance, Disclosures about Short-Duration Contracts (Ref #2015-37)

Deferred* Deferred consideration of the requirements of ASU 2015-09, Financial Services — Insurance, Disclosures about Short-Duration Contracts, since the industry has formed a group to review the applicability of the ASU for statutory accounting. SAPWG is waiting for the industry to submit comments on the US GAAP disclosures for short-duration insurance contracts before proceeding.

TBD

SSAP No. 1 — 5*/6* Securities (Ref #2015-41)

Adopted Adopted revisions to require disclosures to capture current and prior-period information on the number of 5* securities and the book adjusted carrying value and fair value for those securities. For non-AVR filers, the disclosure should also capture details on the securities that are reported at amortized cost and those that are reported at fair value.

Immediately

SSAP No. 86 — EITF 99-02: Accounting for Weather Derivatives (Ref #2015-43)

Adopted Adopted the US GAAP language from Accounting Standards Codification 815-45-15-2, with illustration, to clarify that the guidance on weather derivatives does not apply to insurance contracts that entitle the holder to be compensated only if, as a result of an insurable event, the holder incurs a liability or there is an adverse change in the value of a specific asset or liability for which the holder is at risk.

Immediately

SSAP No. 3 — Correction of an Error in SSAP No. 3 (Ref #2015-46)

Reexposed Reexposed revisions to clarify that the existing guidance in SSAP No. 3 pertains to the correction of accounting errors. The proposed changes also address the actions to be taken when the reporting entity becomes aware of a material accounting error in previously issued financial statements and how all accounting errors should be corrected if an amended financial statement is not filed.

TBD

SSAP No. 86 — Definition of a Notional (Ref #2015-51)

Reexposed Exposed two approaches to define “notional” in SSAP No. 86 for comment. The options include: calculate notional based on type of contract or calculate notional based on type of underlying item.

TBD

SSAP No. 1 — Clarification of Permitted Practice Disclosure (Ref #2015-52)

Adopted Adopted clarifications to the disclosure requirements for prescribed or permitted practices, identifying that disclosure should occur for practices that affect statutory surplus or RBC or that result in a different statutory accounting reporting (i.e., gross or net presentation).

Immediately

SSAP No. 97 — SCA Data Captured Disclosure (Ref #2016-04)

Adopted Adopted a data-capture disclosure template for all SCA investments within the scope of SSAP No. 97 for detailing the reported value for SCAs, as well as information received after filing the SCA with the NAIC. The exclusion for 8.b.i entities has been retained.

Immediately

Removal of the Class 1 List from the P&P Manual (Ref #2016-05)

Adopted Adopted necessary revisions to SSAP No. 26, SSAP No. 30, SSAP No. 32, Preferred Stock, and SSAP No. 2 to reflect the removal of the Class 1 Money Market Mutual Fund List from the P&P Manual. The revisions also clarify that Money Market Mutual Funds are to be reported as short-term investments within the guidance of SSAP No. 2.

Immediately

SSAP No. 100 — Disclosures about Fair Value of Financial Instruments (Ref #2016-06)

Adopted Adopted revisions to SSAP No. 100, Fair Value, to exclude deposit liabilities with no defined or contractual maturities from the fair value financial instruments disclosure.

Immediately

SSAP No. 92 and SSAP No. 102 — Method for Applying Discount Rates to Measure Net Periodic Benefit Cost (Ref #2016-08)

Adopted Adopted revisions to SSAP No. 92, Postretirement Benefits Other than Pensions, and SSAP No. 102, Pensions. The revisions incorporate amendments to allow an alternative (i.e., spot rate) method for measuring service cost and interest cost components of net periodic benefit cost.

Immediately

SSAP No. 1 — Collateral Received (Ref #2016-09)

Adopted Adopted a new disclosure to capture the aggregate total of collateral assets received and reported as assets on the insurer’s financial statements as well as the corresponding liability to return the collateral.

Immediately

EY AccountingLink | www.ey.com/us/accountinglink

18 | NAIC Bulletin August 2016

Nonsubstantive listing2 (continued)

Changes to Appendix A-820 Standard Valuation Law for Principle-based Reserving (Ref #2016-10)

Adopted Adopted revisions to Appendix A-820, Minimum Life and Annuity Reserve Standards, which incorporate relevant aspects of the 2009 revisions to Model #820. The revisions include references to the Valuation Manual in Appendix A-820.

1 January 2017

Insurance Linked Securities (ILS) Data Capture Disclosure (Ref #2016-11)

Adopted Adopted revisions to the annual statement instructions to include the data-capture disclosure template for insurance-linked securities and language clarifying how disclosure components should be completed.

Immediately

Appendix F — Policy Statement (Ref #2016-12)