NACHA Operating Rules: What Do They Mean to...

30

© 2015 NACHA — The Electronic Payments Association. All rights reserved. No part of this material may be used without the prior written permission of NACHA. This material is not intended to provide any warranties or legal advice and is intended for educational purposes only. NACHA Operating Rules: What Do They Mean to You?

-

Upload

vuongkhanh -

Category

Documents

-

view

218 -

download

0

Transcript of NACHA Operating Rules: What Do They Mean to...

© 2015 NACHA — The Electronic Payments Association. All rights reserved. No part of this material may be used without the prior written permission of NACHA. This material is not

intended to provide any warranties or legal advice and is intended for educational purposes only.

NACHA Operating Rules:

What Do They Mean to You?

• Who is NACHA and What is ACH?

• Originator Obligations for Authorization

and Authentication

• Authorization Requirements by SEC Code

• Resources

Agenda

2

• As a not-for-profit association, NACHA represents more than

10,000 financial institutions – some are Members directly, and

some are represented via 16 Regional Payments Associations

– Direct Financial Institution Members

– Regional Payments Associations

• Through its industry councils and forums, NACHA brings

together payments system stakeholders to foster dialogue

and innovation to strengthen the ACH Network

– Affiliate Program

– Payments Innovation Alliance

NACHA as Industry Association

– Risk Management Advisory Group

– Government Relations Advisory

Group

– Communications & Marketing

Advisory Group

NACHA as Network Administrator

• ACH Logical Network

– ACH rules set, and associated payment types and formats owned by NACHA

– Allows counterparties to logically and confidently pass transactions to each other, knowing how they will be recognized and dealt with

• NACHA holds the role of the Network…

– Administrator

– Rules Creator

– Rules Enforcer

– Educator

– Supporter

– Protector

• ACH Physical Network

– The physical environment required to move transactions

– The technology and communications environment, and associated product set, needed to initiate, clear and settle ACH transactions between counterparties

• ACH Operators take the role of… – Processing and routing transactions

• Maintaining access to all sending and receiving endpoints

• Inter-operator exchanges

– Services to help financial institutions manage ACH volume and risk management

– Interbank settlement – Network reporting to NACHA

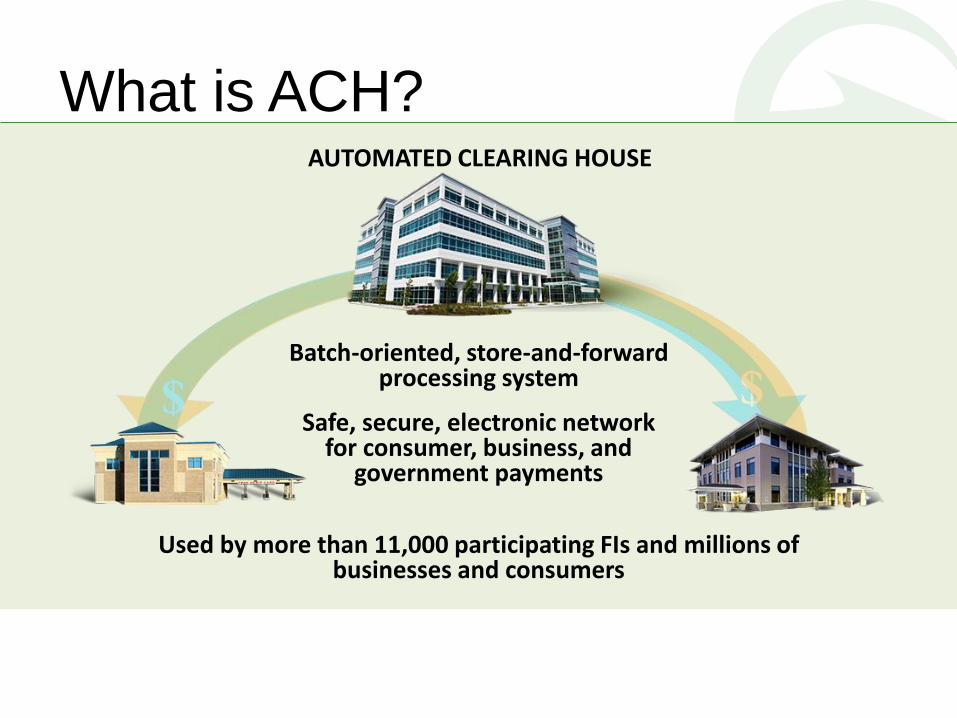

What is ACH?

Batch-oriented, store-and-forward processing system

Safe, secure, electronic network for consumer, business, and

government payments

AUTOMATED CLEARING HOUSE

Used by more than 11,000 participating FIs and millions of businesses and consumers

What is ACH?

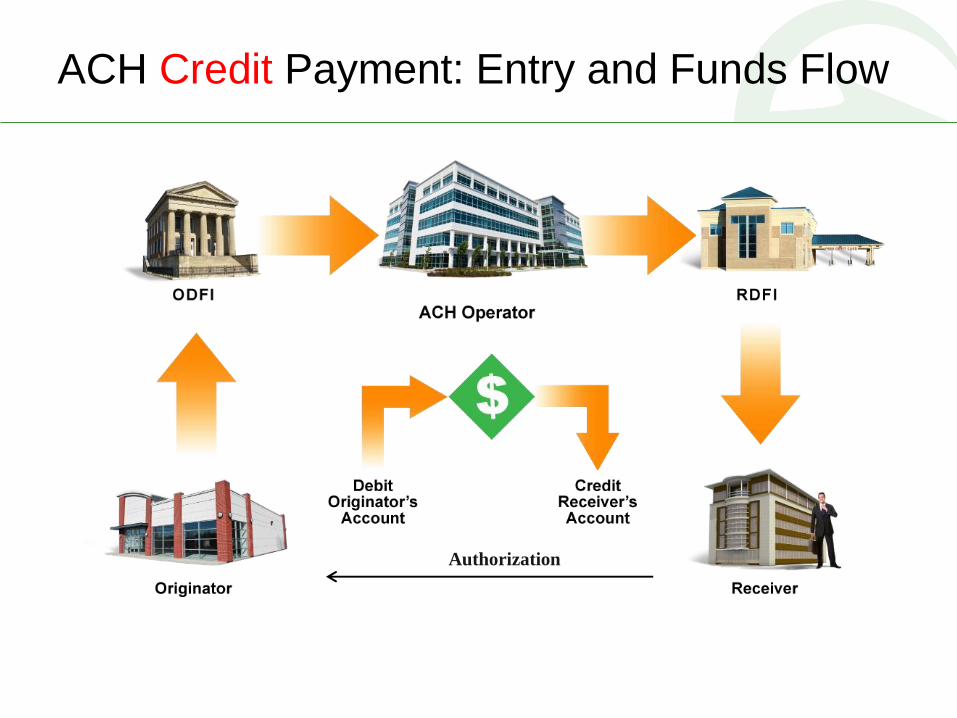

ACH Credit Payment: Entry and Funds Flow

Authorization

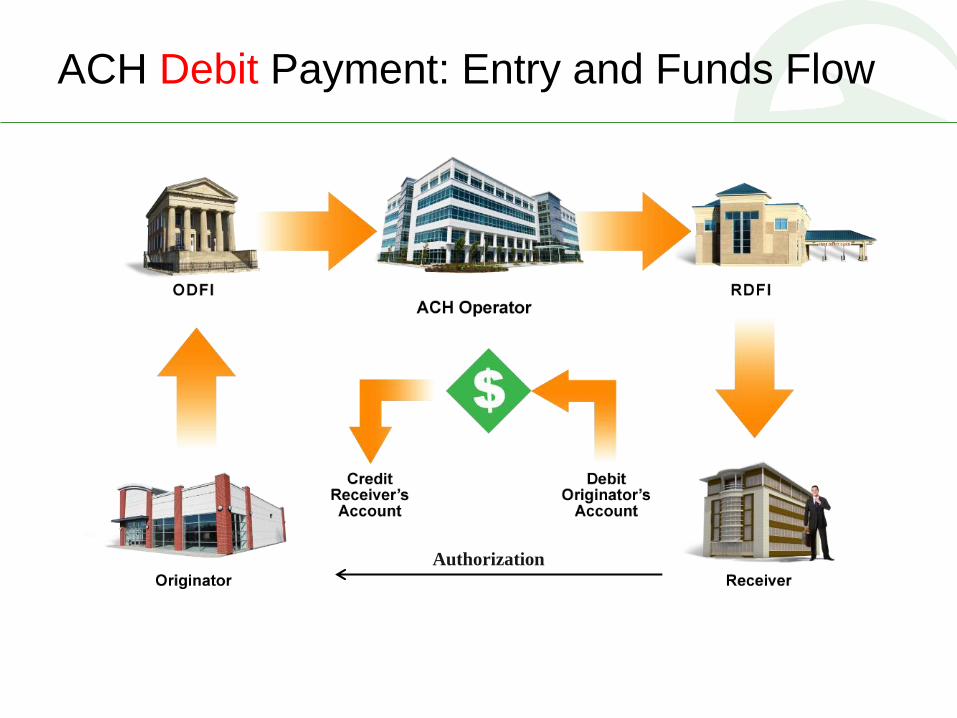

ACH Debit Payment: Entry and Funds Flow

Authorization

Authorizations

“An Originator must obtain authorization from

the Receiver to originate one or more Entries

to the Receiver’s account.”

2015 NACHA Operating Rules, Article Two, Subsection 2.3.1

9

Authorizations

• Authorization occurs when Originator and the Receiver enter into an agreement to allow the Originator to initiate a debit entry to the Receiver’s account

• An authorization to debit an account is only valid if the person who authorized the debit is an owner on the account

10

• Requirements specified

in the Rules are

MINIMUM

requirements

Electronic Authorizations • Similarly authenticated standard allows signed, written

authorizations to be provided electronically

• Writing and signature requirements in the NACHA

Operating Rules can be satisfied by compliance with the

E-sign Act (Electronic Signatures and Global National

Commerce Act)

11

• To satisfy Reg E and NACHA Rules,

must evidence both the customer’s

identity and assent to authorization -

should provide the same assurance

as a signature in the physical world

• Electronic authorizations must be

visually displayed in a way that

allows the consumer to read it

Corporate Authorizations • Corporate Authorizations

– Business Receiver must authorize all credits and debits

– Originator / Receiver must enter into agreement with each business receiver of ACH Entries (other than ARC, BOC and POP Entries to non-consumer accounts)

12

– Agreement must bind the Receiver to the NACHA

Rules

Consumer Debit Authorizations • Authorization must:

– Be readily identifiable

– Have clear and readily understandable terms

– Provide for revocation (for recurring payments or payments scheduled in advance)

• Authorization should contain: – Express authorization language

– Amount of transaction

– The date(s) and/or frequency of the transaction(s)

– The consumer’s account number and financial institution’s routing number

– Account Type

13

• Authorization of a debit entry must be in writing and signed

or similarly authenticated, except where expressly provided

in the Rules for specific types of Entries

Consumer Debit Authorizations

Originators must:

• Provide the Receiver with electronic or hard copy of

Receiver’s authorization

• Retain the original or a copy for two years from

termination or revocation of authorization

• At the request of the ODFI, provide original or copy to

ODFI in such time and manner as to allow the ODFI to

deliver it to the RDFI within 10 banking days of the

RDFI’s request for a copy of the authorization

14

Consumer Debit Authorizations

• Notice of Change of

Amount

• Written notification of

amount and date

• No notice required for

change within agreed

upon range

• Notice of Change to

Scheduled Date

• Written notification of

new date

15

7 CALENDAR DAYS

prior to debit date

10 CALENDAR DAYS

prior to debit date

Authorization Requirements by SEC Code

• Writing that is signed OR Receiver may similarly authenticate the written authorization previously delivered by Originator

• Example of similarly authenticated:

– Originator delivers written terms of authorization.

– Receiver authenticates agreement to terms of authorization by key entering into a VRU or speaking to a recorded line a PIN provided with the authorization that identifies the consumer

• Proof of authorization would be a copy of the written authorization and the consumer’s use of the authorization code provided by the Originator.

16 PPD

PPD Prearranged Payment or Deposit Entry Written Authorization Credit or Debit

PPD

debit

credit

Authorization Requirements by SEC Code

• Oral Authorization only

• Single Entry or recurring consumer

debits

• If no relationship exists, the

consumer must initiate the phone

call

• Record authorization and/or provide

written notice before settlement

17

TEL

TEL

Telephone Initiated Entry Electronic Authorization (Similarly Authenticated) Debit Only

Authorization Requirements by SEC Code

• Minimum Authorization Information – Date on or after which debit will occur (single) or timing –

including start date – number and/or frequency (recurring)

– Amount of the transaction(s) or method of determining amount

– Receiver’s Name and account to be debited

– Telephone number for Receiver inquiries

– Revocation method

– Date of oral authorization

– Statement by Originator that authorization is for single entry ACH debit (single only)

• REMEMBER: Key entry on a VRU to input data and respond to questions does not qualify as oral authorization. Actual authorization must be oral.

18

TEL Telephone Initiated Entry Electronic Authorization (Similarly Authenticated), Debit Only

Authorization Requirements by SEC Code

• Single or Recurring consumer debit and credit entries

• Use when authorization was given via the internet or entry was initiated via wireless device

• Use for P2P – Credit WEB only for payments exchanged between consumers

• Example of records of authorization – Screen shot of authorization language and

date/time stamp of the Receiver log-in and the authorization process that evidenced both the consumer’s identity and assent to the authorization

19

WEB Internet/Mobile Initiated Entry Electronic Authorization (Similarly Authenticated)

WEB

Authorization Requirements by SEC Code

• Consumer is Originator

• Used primarily for bill payment

• Credits only (except for reversal)

• Individual payments only

CIE Consumer Initiated Entry Electronic Authorization (Similarly Authenticated) Credit Only

CIE

Authorization Requirements by SEC Code

• Single entry debit initially presented as a paper check

• Consumer check must have been returned insufficient or uncollected funds and be less than $2,500

• Limited to a combination of three presentments (paper and ACH)

• Notice must be provided

21

RCK Re-Presented Check Entry Notice = Authorization, Debit Only

RCK

Authorization Requirements by SEC Code

• Single or recurring payments

• Agreement between trading parties

• One addenda record

• Used for the distribution or consolidation of funds intra-company or between two corporate entities

CCD Corporate Credit or Debit Written Authorization (recommended), Credit or Debit

CCD

Authorization Requirements by SEC Code

• Debit or credit transfer between trading partners, single or recurring

• Agreement between trading parties

• May contain up to 9,999 addenda records

CTX

CTX

Corporate Trade Exchange Entry Written Authorization (recommended) Credit or Debit

Authorization Requirements by SEC Code

• Regular lockbox check converted into an ACH transaction

• Must have been received through the mail or at a drop-box or in-person for bill payment

• “When you provide a check as payment, you authorize us either to use information from your check to make a one-time electronic fund transfer from your account or to process the payment as a check transaction”

• Must post/place in prominent and conspicuous location

24

ARC Accounts Receivable Entry Authorization = Notice + Receipt of Source Document, Debit Only

ARC

CHECK RECEIVED AT LOCKBOX

Authorization Requirements by SEC Code

• Requires written notice to Receiver prior to

receipt of each source document

• “When you provide a check as payment, you

authorize us either to use information from

your check to make a one-time electronic fund

transfer from your account or to process the

payment as a check transaction. For inquiries,

please call (retailer phone number).”

• Must post in prominent and conspicuous

location and provide copy of notice at the time

of transaction

25

BOC Back Office Conversion Entry Authorization = Notice + Receipt of Source Document, Debit Only

BOC

CHECK IS RECEIVED AT POINT OF SALE, BUT

CONVERTED AT A LATER TIME

Authorization Requirements by SEC Code

• Verification of Receiver’s Identity

– Must use commercially reasonable procedure to verify the Receiver’s identity

– Examples include:

• Photo identification

• Retailer preferred card

• Check verification services

26

BOC Back Office Conversion Entry Authorization = Notice + Receipt of Source Document, Debit Only

Authorization Requirements by SEC Code

• Merchant must provide notice and

consumer signs

authorization at point of purchase

• Check is scanned by merchant to capture

account information, voided, and returned

to the customer

• Must post in prominent and conspicuous

location and provide copy of notice at the

time of transaction

27

POP Point-of-Purchase Entry Authorization = Notice + Receipt of Source Document AND Written Authorization, Debit Only

POP

• NACHA Operating Rules – Board Policy Statements

– Formal Rules Interpretations

– Summary of Revisions from

previous year and any Supplements

– Operating Rules

• NACHA Operating Guidelines – do not supersede the Rules but provide

additional information

Resources

1. Online Rules access

With full-featured search, bookmarking, save search, and a host of FAQs!

2. NACHA’s Website

– Upcoming amendments

– Proposed changes

– eStore

– News and education

Resources

www.achrulesonline.org

www.nacha.org

QUESTIONS?

Danita Tyrrell, AAP

Director, Network Rules

NACHA-The Electronic

Payments Association