MSME in Selected MENA Countries: Challenges and Way Forward 12th September-FINALUpdated 16th... ·...

35

Research & Statistics Department 1 MSME in Selected MENA Countries: Challenges and Way Forward Cairo, September 20 th , 2018 Dr. Magda Kandil A presentation to "MSMEs: Inspiring Growth Challenges & Opportunities in Access to Finance” conference.

Transcript of MSME in Selected MENA Countries: Challenges and Way Forward 12th September-FINALUpdated 16th... ·...

Research & Statistics Department

1

MSME in Selected MENA Countries:Challenges and Way Forward

Cairo, September 20th, 2018

Dr. Magda Kandil

A presentation to "MSMEs: Inspiring Growth Challenges & Opportunities in Access to Finance” conference.

Remaining Gaps and challenges

Rationale for Government Intervention

SME development in Morocco, Jordan and Egypt

TABLE OF CONTENTS

1

2

3

4

SMEs: Job Creation and Inclusive Growth

SME Action Plan in the UAE 5

2

SMEs: Job Creation and Inclusive Growth

1

3

1

3

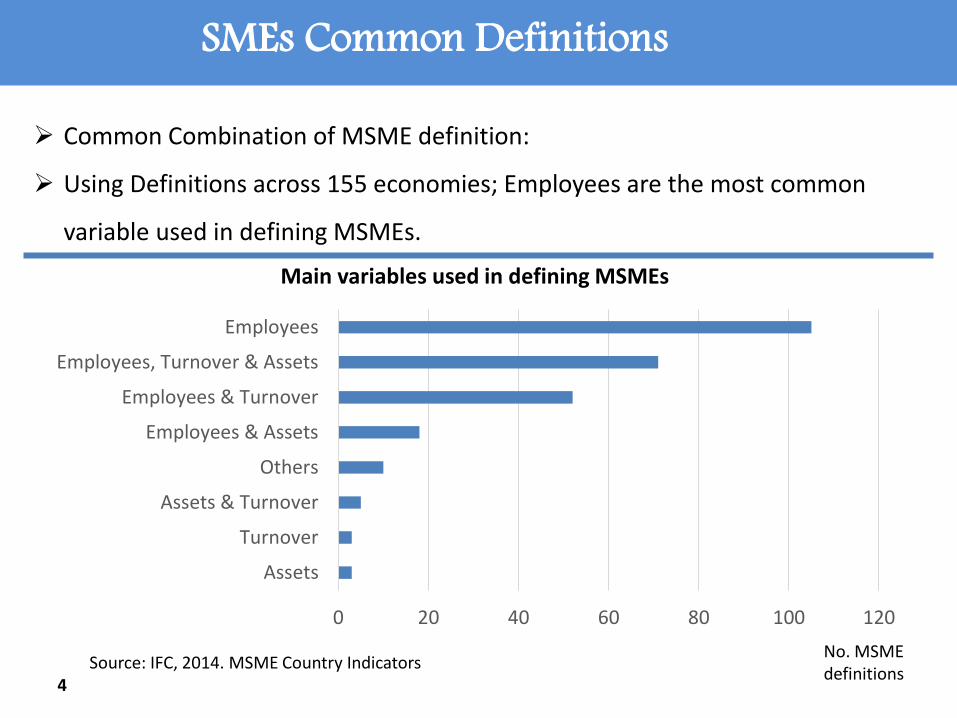

SMEs Common Definitions

1

3

4

0 20 40 60 80 100 120

Assets

Turnover

Assets & Turnover

Others

Employees & Assets

Employees & Turnover

Employees, Turnover & Assets

Employees

Common Combination of MSME definition:

Using Definitions across 155 economies; Employees are the most common

variable used in defining MSMEs.

Source: IFC, 2014. MSME Country Indicators

Main variables used in defining MSMEs

No. MSME definitions

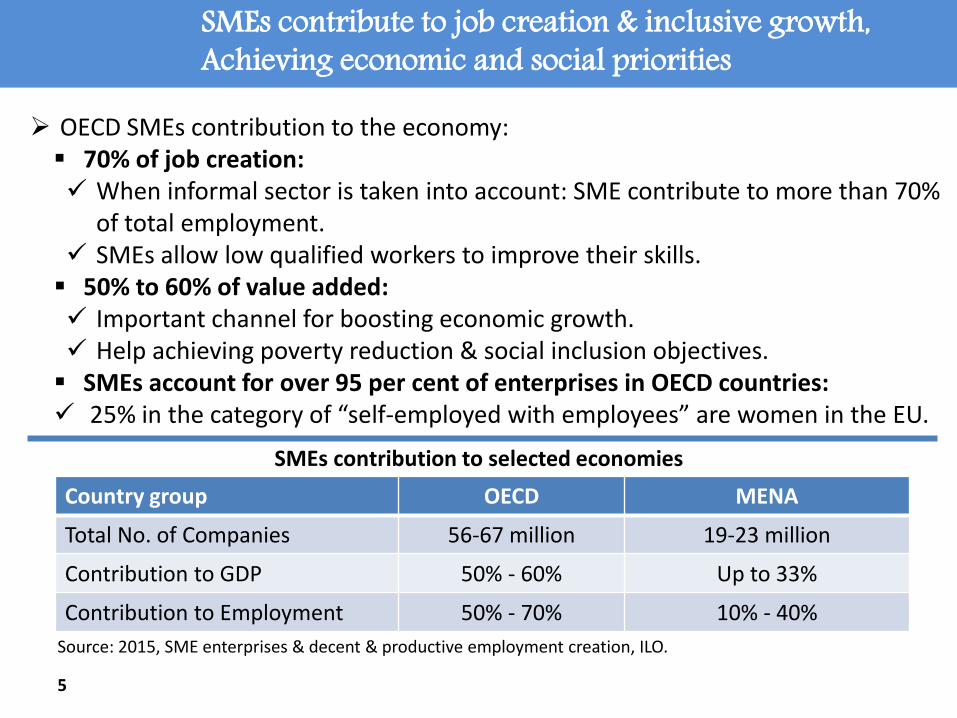

SMEs contribute to job creation & inclusive growth, Achieving economic and social priorities

1

3

OECD SMEs contribution to the economy: 70% of job creation: When informal sector is taken into account: SME contribute to more than 70%

of total employment. SMEs allow low qualified workers to improve their skills. 50% to 60% of value added: Important channel for boosting economic growth. Help achieving poverty reduction & social inclusion objectives. SMEs account for over 95 per cent of enterprises in OECD countries: 25% in the category of “self-employed with employees” are women in the EU.

5

Country group OECD MENA

Total No. of Companies 56-67 million 19-23 million

Contribution to GDP 50% - 60% Up to 33%

Contribution to Employment 50% - 70% 10% - 40%

SMEs contribution to selected economies

Source: 2015, SME enterprises & decent & productive employment creation, ILO.

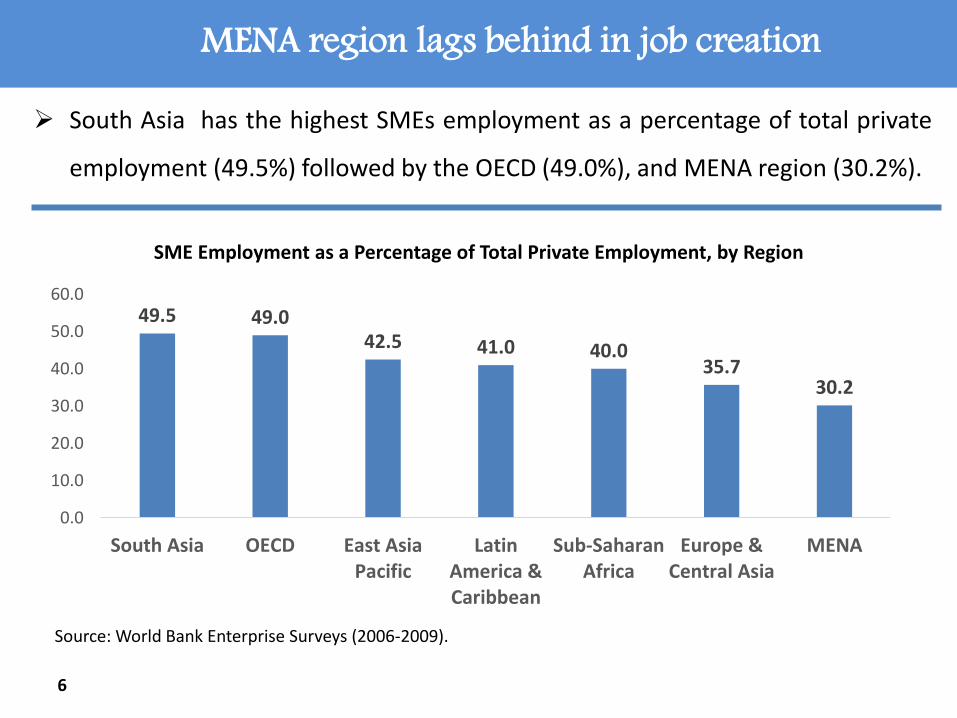

MENA region lags behind in job creation

1

3

6

49.5 49.042.5 41.0 40.0

35.730.2

0.0

10.0

20.0

30.0

40.0

50.0

60.0

South Asia OECD East AsiaPacific

LatinAmerica &Caribbean

Sub-SaharanAfrica

Europe &Central Asia

MENA

SME Employment as a Percentage of Total Private Employment, by Region

Source: World Bank Enterprise Surveys (2006-2009).

South Asia has the highest SMEs employment as a percentage of total private

employment (49.5%) followed by the OECD (49.0%), and MENA region (30.2%).

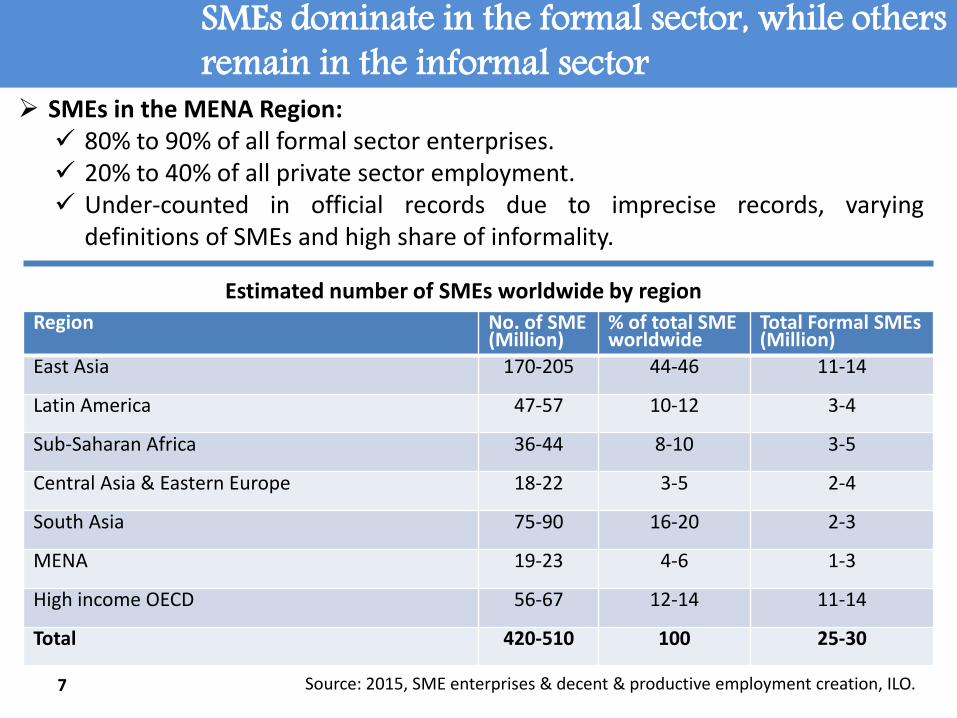

SMEs dominate in the formal sector, while others remain in the informal sector

1

3

SMEs in the MENA Region: 80% to 90% of all formal sector enterprises. 20% to 40% of all private sector employment. Under-counted in official records due to imprecise records, varying

definitions of SMEs and high share of informality.

7

Region No. of SME (Million)

% of total SME worldwide

Total Formal SMEs(Million)

East Asia 170-205 44-46 11-14

Latin America 47-57 10-12 3-4

Sub-Saharan Africa 36-44 8-10 3-5

Central Asia & Eastern Europe 18-22 3-5 2-4

South Asia 75-90 16-20 2-3

MENA 19-23 4-6 1-3

High income OECD 56-67 12-14 11-14

Total 420-510 100 25-30

Estimated number of SMEs worldwide by region

Source: 2015, SME enterprises & decent & productive employment creation, ILO.

Potential for SMEs’ Job creation in MENA countriesNonetheless, the region lags behind in SME employment.

1

3

SMEs are generally more labor-intensive compared to larger firms. Innovative enterprises report higher employment growth rates. The social benefits of job creation are higher for SMEs. SMEs increase the tax base. End result: Government support to SMEs may be more effective than alternative

policies (like unemployment benefits).

8

SMEs as Employers in Selected MENA Countries

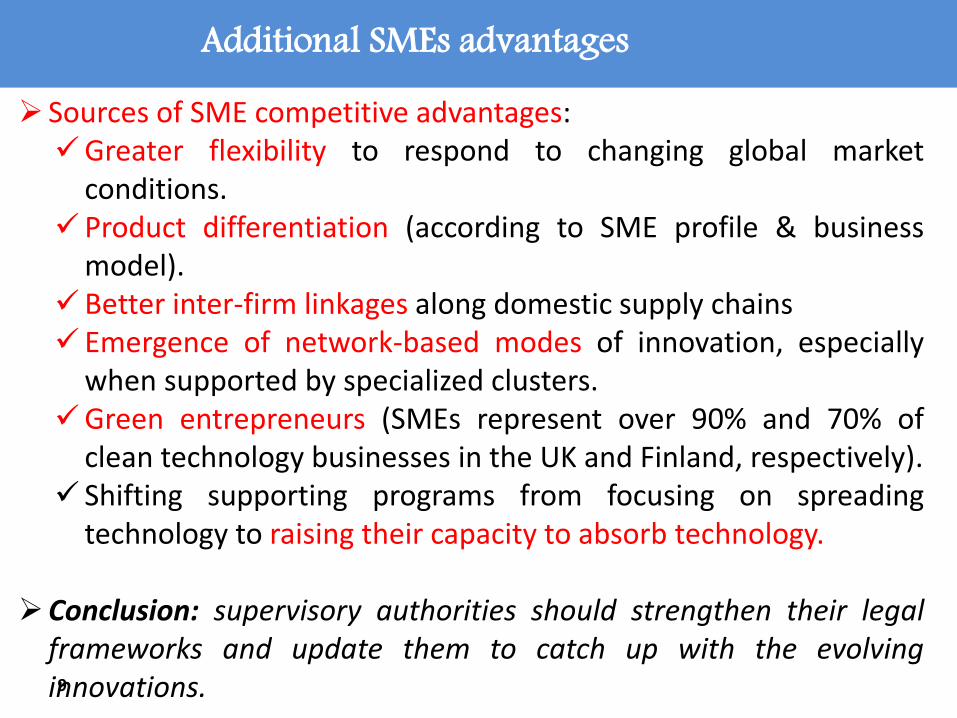

Additional SMEs advantages

1

3

Sources of SME competitive advantages:Greater flexibility to respond to changing global market

conditions.Product differentiation (according to SME profile & business

model).Better inter-firm linkages along domestic supply chains Emergence of network-based modes of innovation, especially

when supported by specialized clusters.Green entrepreneurs (SMEs represent over 90% and 70% of

clean technology businesses in the UK and Finland, respectively). Shifting supporting programs from focusing on spreading

technology to raising their capacity to absorb technology.

Conclusion: supervisory authorities should strengthen their legalframeworks and update them to catch up with the evolvinginnovations.9

Remaining Gaps and challenges

1

3

2

10

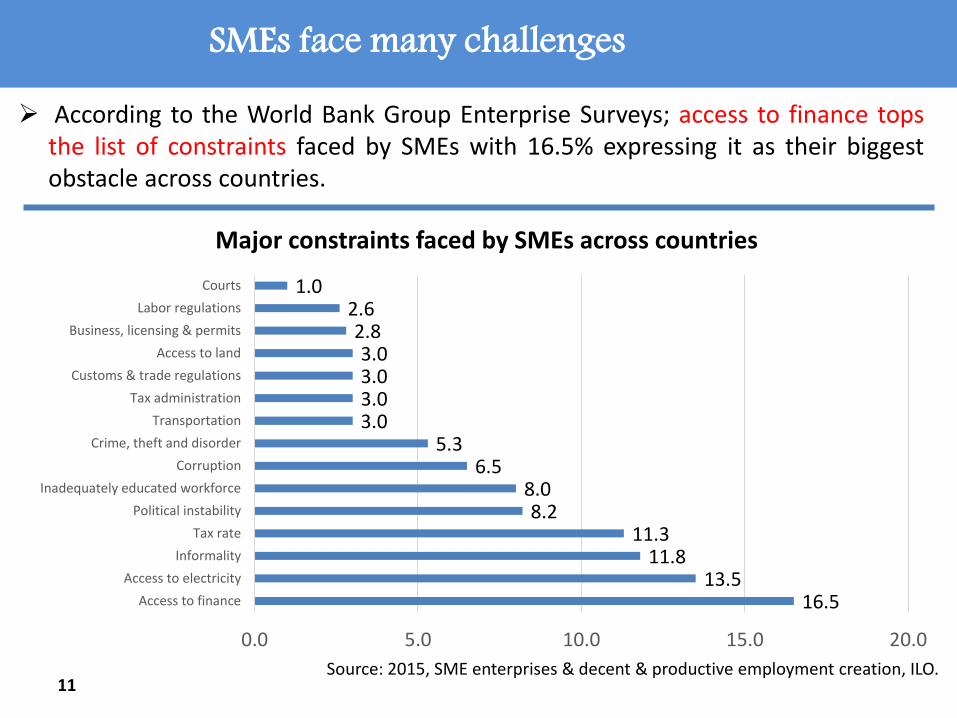

SMEs face many challenges

1

3

According to the World Bank Group Enterprise Surveys; access to finance topsthe list of constraints faced by SMEs with 16.5% expressing it as their biggestobstacle across countries.

11

16.513.5

11.811.3

8.28.0

6.55.3

3.03.03.03.0

2.82.6

1.0

0.0 5.0 10.0 15.0 20.0

Access to finance

Access to electricity

Informality

Tax rate

Political instability

Inadequately educated workforce

Corruption

Crime, theft and disorder

Transportation

Tax administration

Customs & trade regulations

Access to land

Business, licensing & permits

Labor regulations

Courts

Major constraints faced by SMEs across countries

Source: 2015, SME enterprises & decent & productive employment creation, ILO.

limited market access to global markets given their small size

1

3

Challenges: Access to financial services:

Difficult macroeconomic environment. Funding gap due to the lack of venture capital, financial skills and financial

literacy. Risk weighting in the realm of the implementation of Basel III accords.

SMEs are lagging behind in: Adopting Digital Technologies & participating in E-commerce. Investment in knowledge-based assets, such as R&D, human resources. Limited in-house innovation processes and organizational capabilities.

Participation in global markets and value chains is uneven across SME firms. Challenges are compounded by:

Internet connectivity issues and web presence. Lack of renting computer power (use of big data) High job turnover, which poses problems for employment security. Relying on external recruitment instead of investing in training. Regulatory burdens. High costs of tax compliance12

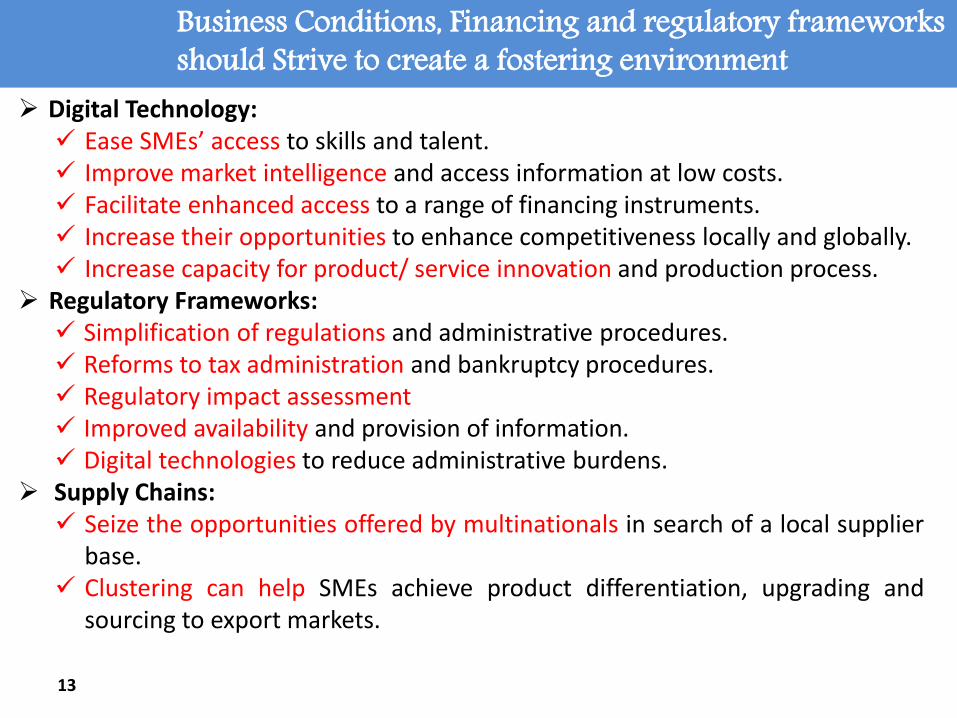

Business Conditions, Financing and regulatory frameworks should Strive to create a fostering environment

1

3

Digital Technology: Ease SMEs’ access to skills and talent. Improve market intelligence and access information at low costs. Facilitate enhanced access to a range of financing instruments. Increase their opportunities to enhance competitiveness locally and globally. Increase capacity for product/ service innovation and production process.

Regulatory Frameworks: Simplification of regulations and administrative procedures. Reforms to tax administration and bankruptcy procedures. Regulatory impact assessment Improved availability and provision of information. Digital technologies to reduce administrative burdens.

Supply Chains: Seize the opportunities offered by multinationals in search of a local supplier

base. Clustering can help SMEs achieve product differentiation, upgrading and

sourcing to export markets.

13

Business Conditions, Financing and regulatory frameworks should Strive to create a fostering environment

1

3

Access to finance:

Digital transformation holds potential to improve SME access tofinance.

Reduce the asymmetry of information between lenders andborrowers through credit bureaus and credit registries.

Broaden the range of financing instruments available to SMEsand entrepreneurs.

Increase SMEs’ resilience to changing conditions in creditmarkets through strengthen SME capital structures.

Broaden government financing and loan-guarantee initiatives.Adequate support for the emergence of “lean start-ups”

14

Rationale for Government Intervention

1

3

3

15

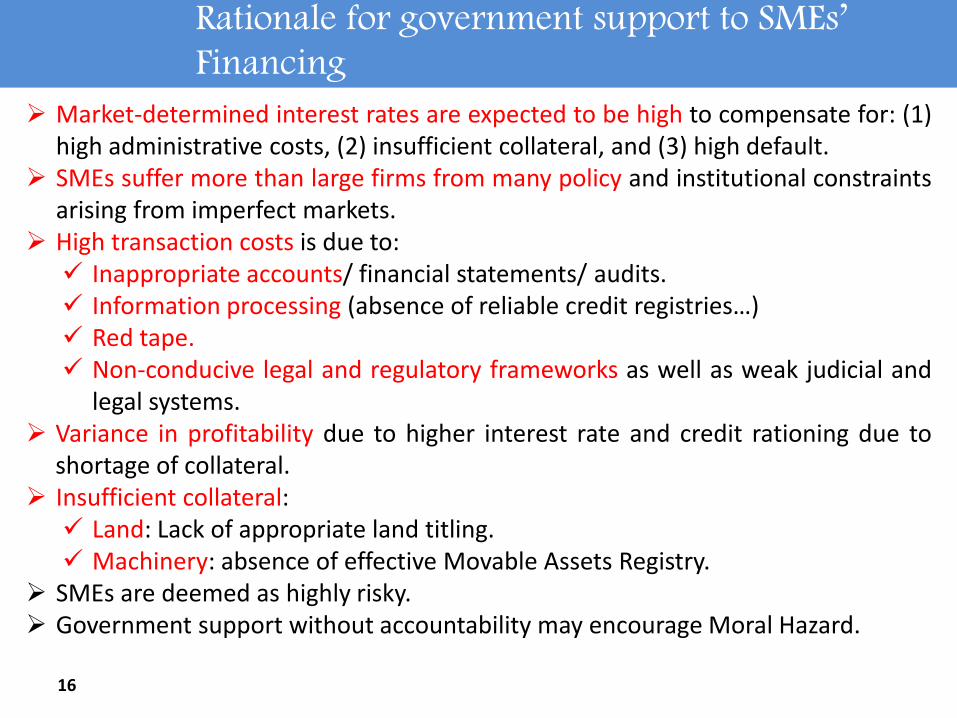

Rationale for government support to SMEs’ Financing

1

3

Market-determined interest rates are expected to be high to compensate for: (1)high administrative costs, (2) insufficient collateral, and (3) high default.

SMEs suffer more than large firms from many policy and institutional constraintsarising from imperfect markets.

High transaction costs is due to: Inappropriate accounts/ financial statements/ audits. Information processing (absence of reliable credit registries…) Red tape. Non-conducive legal and regulatory frameworks as well as weak judicial and

legal systems. Variance in profitability due to higher interest rate and credit rationing due to

shortage of collateral. Insufficient collateral:

Land: Lack of appropriate land titling. Machinery: absence of effective Movable Assets Registry.

SMEs are deemed as highly risky. Government support without accountability may encourage Moral Hazard.

16

Rationale for government support to SMEs’ Financing

1

3

Lack of sufficient financial track records. High fixed costs for banks for processing loan applications. The gap in credit costs between SMEs and large enterprises remains wide as the

decline in interest rates in the post crisis period benefited large enterprises morethan small ones.

17 Source: OECD, 2017.Enhancing the Contributions of SMEs in a Global and Digitalized Economy

Interest rate spreads between loans to SMEs and to large enterprises

Rationale for government intervention: The Social benefits of job creation & easing market access

1

Social benefits of Job creation: SMEs are generally more labor-intensive compared to larger firms. The social benefits of job creation are higher for of SMEs. Substantial fixed cost to tax regulatory requirements and compliance costs. End result: Government support to SMEs may be more effective than

alternative policies (like unemployment benefits). Easing Market access constraints: Credit Reporting Systems & Secured Transactions Frameworks (including

movable assets registries). Credit lines, Guarantee Schemes, State Banks, SME Exchanges, SME Funds,

Reforms to encourage leasing, factoring. Financial Education, Training, Awareness Campaigns. Improved access to capacity building support for SMEs & guide them through

red tape challenge. SME to obtain patents for new ideas/ techniques. Scaling up incubator operations to accelerate SMEs developments. Regulations should focus on creating enabling environment and compensating

SMEs of adverse externalities.18

SME development in Morocco, Jordan and Egypt

Chapter 1

1

3

4

Limits to SME Development in Arab Countries

1

3

AMF Main Findings (Arab Consolidated Economic Report, 2013): Limited access to finance Weak in guarantees and collateral Inadequate business environment Regulatory constraints Poor management systems

Bank funding of SMEs: Highest in Morocco (24%), followed by Egypt (13%), andJordan (8%).

SME listed Value on the stock markets remain limited

Egypt Morocco Jordan

Banking Sector Loans to SMEs (% of Total) 13% 24% 8%

SME Listed Value on the stock market (% of GDP) 0.1% 4.5% 1.0%

SMEs Financial indicators

Morocco: Current SME Landscape

1

3

Share of SMEs in economic activity

Central Bank of Morocco sponsored an agreement between banks and SMEassociation with focus on: Banks to adopt a standard loan file for SMEs Banks committed to take guarantees related only to companies Information such as accounting data to be provided by borrowers to the

authorities A National Committee was entrusted with follow-up and monitoring

implementation of SME development agenda

Total GDP Total Exports Total Employment

40% 30% 50%Source: Bank Al-Maghrib

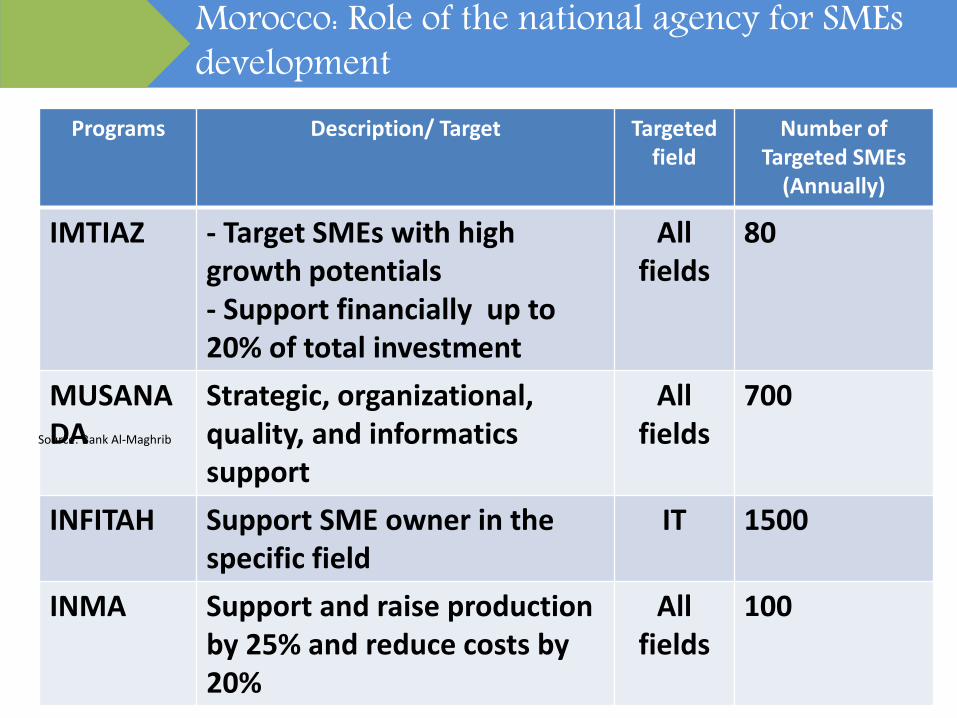

Morocco: Role of the national agency for SMEs development

1

3

Programs Description/ Target Targetedfield

Number of Targeted SMEs

(Annually)

IMTIAZ - Target SMEs with high growth potentials- Support financially up to 20% of total investment

Allfields

80

MUSANADA

Strategic, organizational, quality, and informatics support

Allfields

700

INFITAH Support SME owner in the specific field

IT 1500

INMA Support and raise production by 25% and reduce costs by 20%

All fields

100

Source: Bank Al-Maghrib

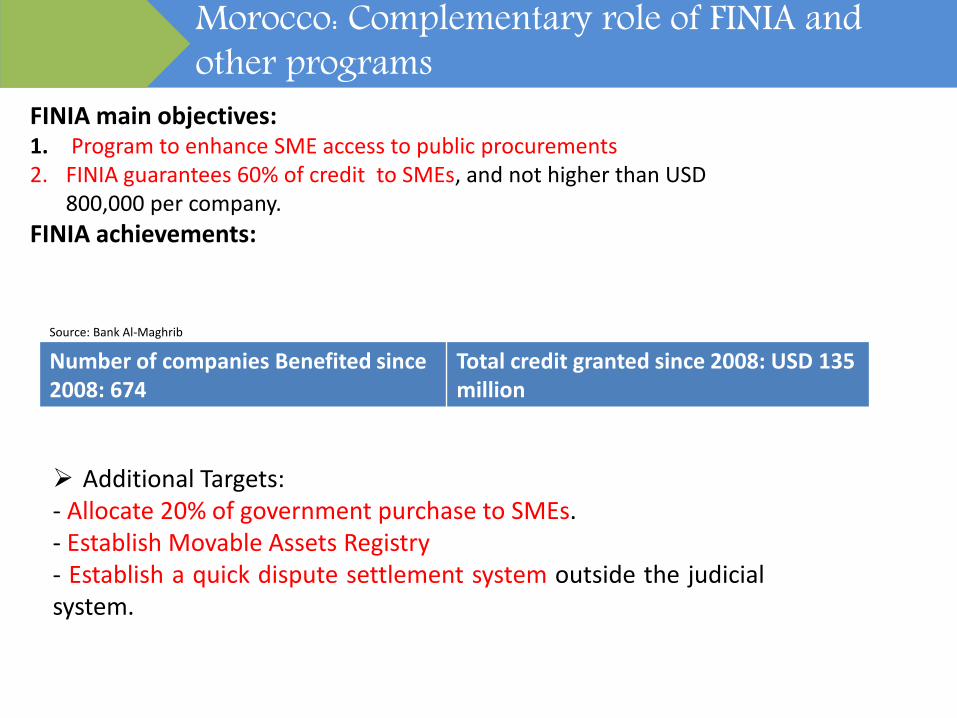

Morocco: Complementary role of FINIA and other programs

1

FINIA main objectives:1. Program to enhance SME access to public procurements2. FINIA guarantees 60% of credit to SMEs, and not higher than USD

800,000 per company.

FINIA achievements:

Number of companies Benefited since 2008: 674

Total credit granted since 2008: USD 135 million

Additional Targets:- Allocate 20% of government purchase to SMEs.- Establish Movable Assets Registry- Establish a quick dispute settlement system outside the judicialsystem.

Source: Bank Al-Maghrib

9/16/2018 24

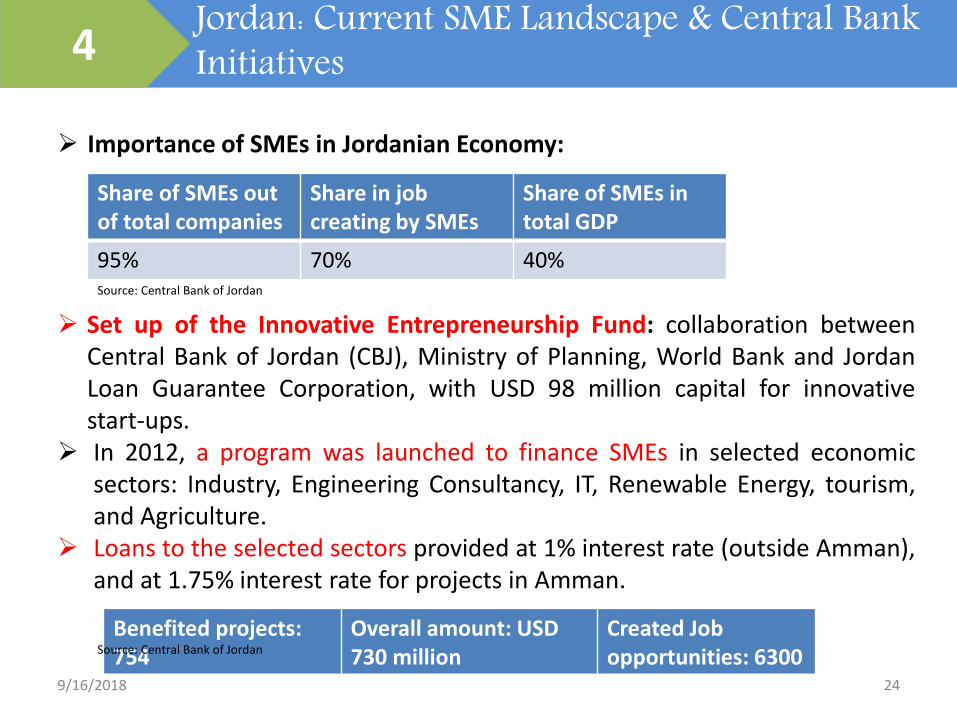

Jordan: Current SME Landscape & Central Bank Initiatives4

Importance of SMEs in Jordanian Economy:

Set up of the Innovative Entrepreneurship Fund: collaboration betweenCentral Bank of Jordan (CBJ), Ministry of Planning, World Bank and JordanLoan Guarantee Corporation, with USD 98 million capital for innovativestart-ups.

In 2012, a program was launched to finance SMEs in selected economicsectors: Industry, Engineering Consultancy, IT, Renewable Energy, tourism,and Agriculture.

Loans to the selected sectors provided at 1% interest rate (outside Amman),and at 1.75% interest rate for projects in Amman.

Share of SMEs out of total companies

Share in job creating by SMEs

Share of SMEs in total GDP

95% 70% 40%Source: Central Bank of Jordan

Benefited projects: 754

Overall amount: USD730 million

Created Job opportunities: 6300Source: Central Bank of Jordan

9/16/2018 25

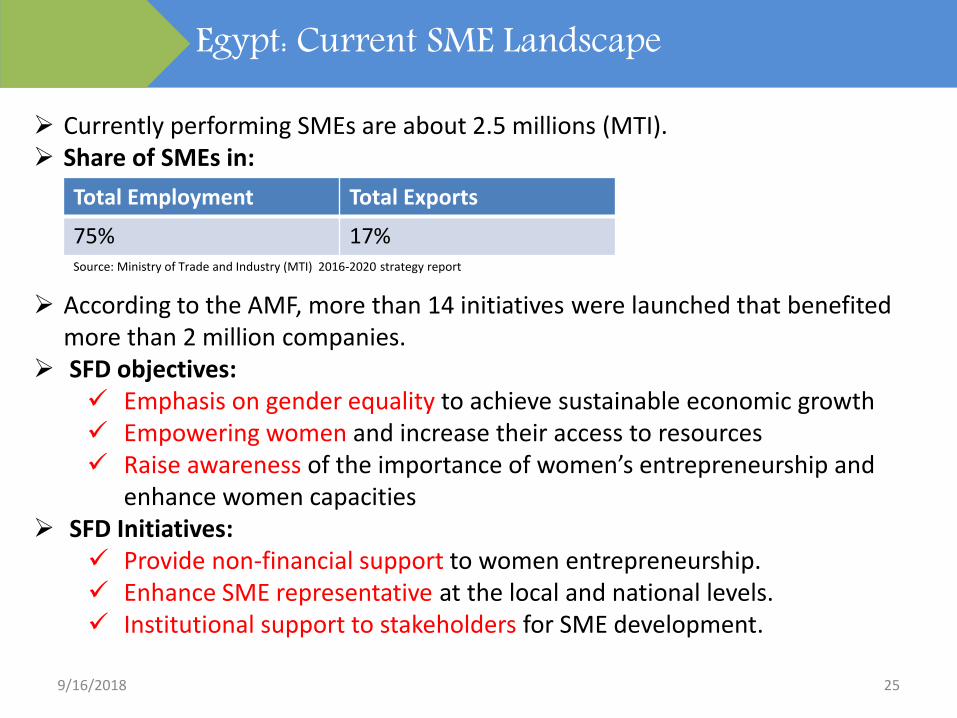

Egypt: Current SME Landscape

Currently performing SMEs are about 2.5 millions (MTI). Share of SMEs in:

According to the AMF, more than 14 initiatives were launched that benefited more than 2 million companies.

SFD objectives: Emphasis on gender equality to achieve sustainable economic growth Empowering women and increase their access to resources Raise awareness of the importance of women’s entrepreneurship and

enhance women capacities SFD Initiatives:

Provide non-financial support to women entrepreneurship. Enhance SME representative at the local and national levels. Institutional support to stakeholders for SME development.

Total Employment Total Exports

75% 17%Source: Ministry of Trade and Industry (MTI) 2016-2020 strategy report

UAE Action Plan to Enhance SME Finance and Development

Chapter 1

1

3

5

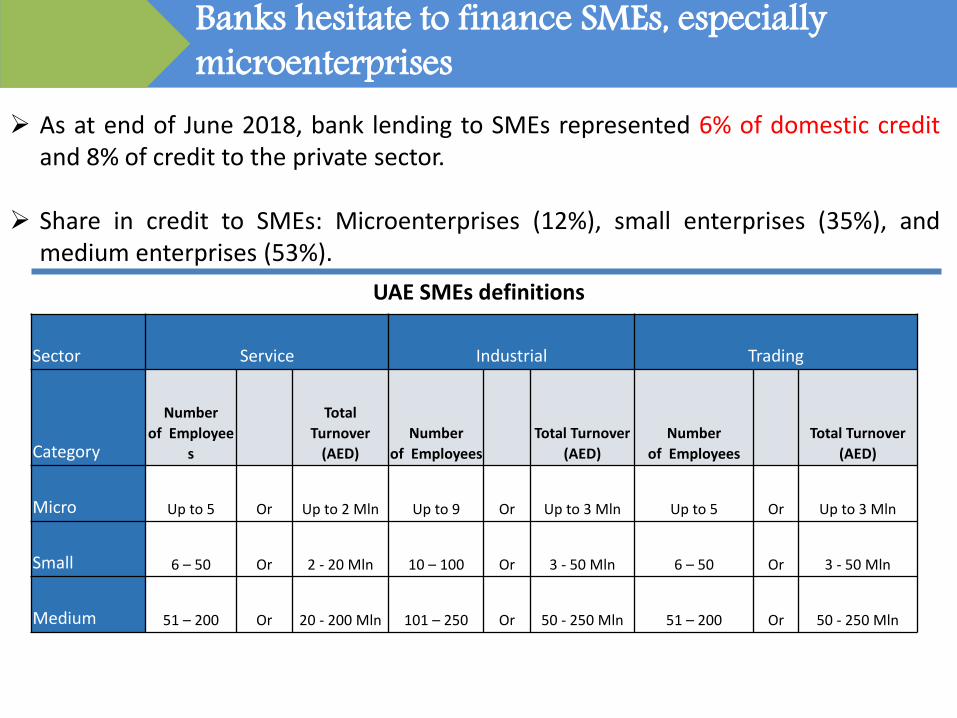

Banks hesitate to finance SMEs, especially microenterprises

1

3

As at end of June 2018, bank lending to SMEs represented 6% of domestic creditand 8% of credit to the private sector.

Share in credit to SMEs: Microenterprises (12%), small enterprises (35%), andmedium enterprises (53%).

Sector Service Industrial Trading

Category

Number

of Employee

s

Total

Turnover

(AED)

Number

of Employees

Total Turnover

(AED)

Number

of Employees

Total Turnover

(AED)

Micro Up to 5 Or Up to 2 Mln Up to 9 Or Up to 3 Mln Up to 5 Or Up to 3 Mln

Small 6 – 50 Or 2 - 20 Mln 10 – 100 Or 3 - 50 Mln 6 – 50 Or 3 - 50 Mln

Medium 51 – 200 Or 20 - 200 Mln 101 – 250 Or 50 - 250 Mln 51 – 200 Or 50 - 250 Mln

UAE SMEs definitions

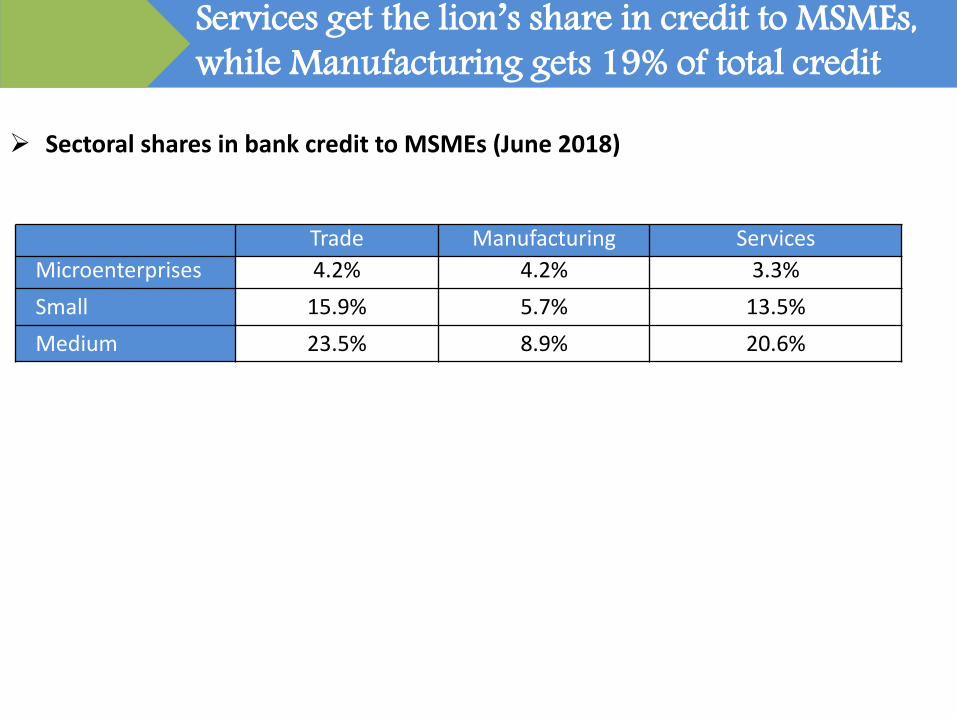

Services get the lion’s share in credit to MSMEs, while Manufacturing gets 19% of total credit

1

3

Sectoral shares in bank credit to MSMEs (June 2018)

Trade Manufacturing Services

Microenterprises 4.2% 4.2% 3.3%

Small 15.9% 5.7% 13.5%

Medium 23.5% 8.9% 20.6%

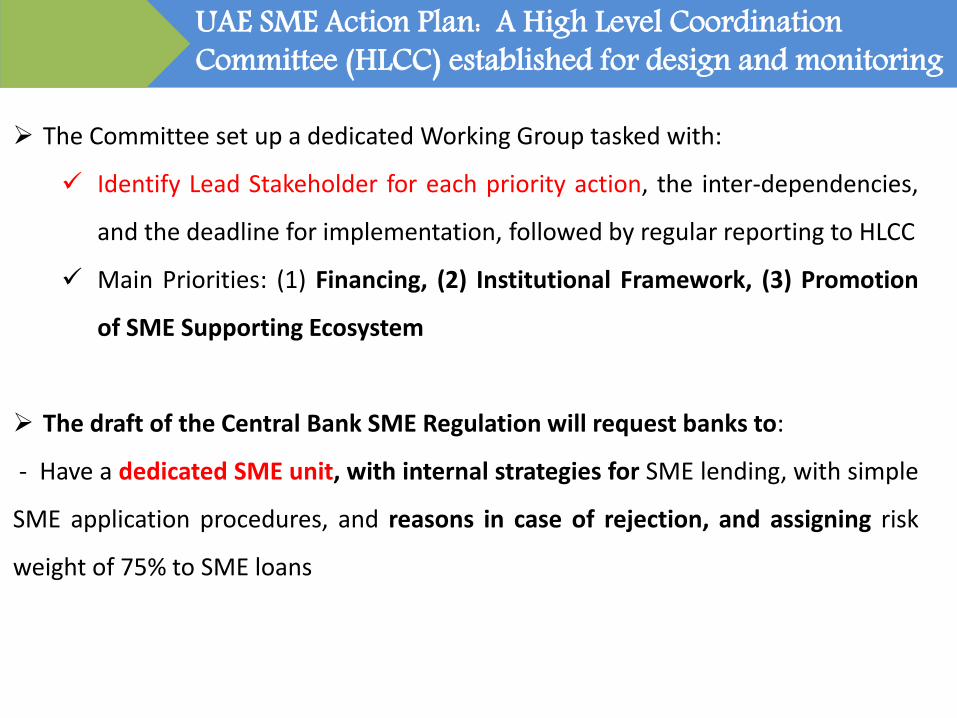

UAE SME Action Plan: A High Level Coordination Committee (HLCC) established for design and monitoring

1

3

The Committee set up a dedicated Working Group tasked with:

Identify Lead Stakeholder for each priority action, the inter-dependencies,

and the deadline for implementation, followed by regular reporting to HLCC

Main Priorities: (1) Financing, (2) Institutional Framework, (3) Promotion

of SME Supporting Ecosystem

The draft of the Central Bank SME Regulation will request banks to:

- Have a dedicated SME unit, with internal strategies for SME lending, with simple

SME application procedures, and reasons in case of rejection, and assigning risk

weight of 75% to SME loans

Enhancing SME access to credit at a lower cost

1

3

Emirates Development Bank set up the Electronic Movable Assets Securitization

Registry (for equipment, inventory, accounts receivable, cash flows…)

For effective use of the Registry: Need for low cost for registration by SMEs and

search by lenders.

Strengthen Al Etihad Credit Bureau: SME scores will constitute the basis toassess default and allow banks adopt risk-based pricing

Establishment of a Federal Credit Guarantee Scheme (FCGS) with contributionof the federal government, banks and SME borrowers

Fees will be designed so as to minimize moral hazard and risk-taking

Provide alternative financing and effective dispute settlement

1

3

Protect creditors and shareholders’ rights and remove constraints to

alternative financing:

Stock Exchange for SMEs: allow interested medium size SMEs to be listed on a

dedicated SME platform with less stringent conditions

Need effective implementation of The corporate Bankruptcy Law of 2016 and a

gradual decriminalization of bounced cheques, and reformed bankruptcy

regime for individuals

Establishment of the Credit Ombudsman Office.

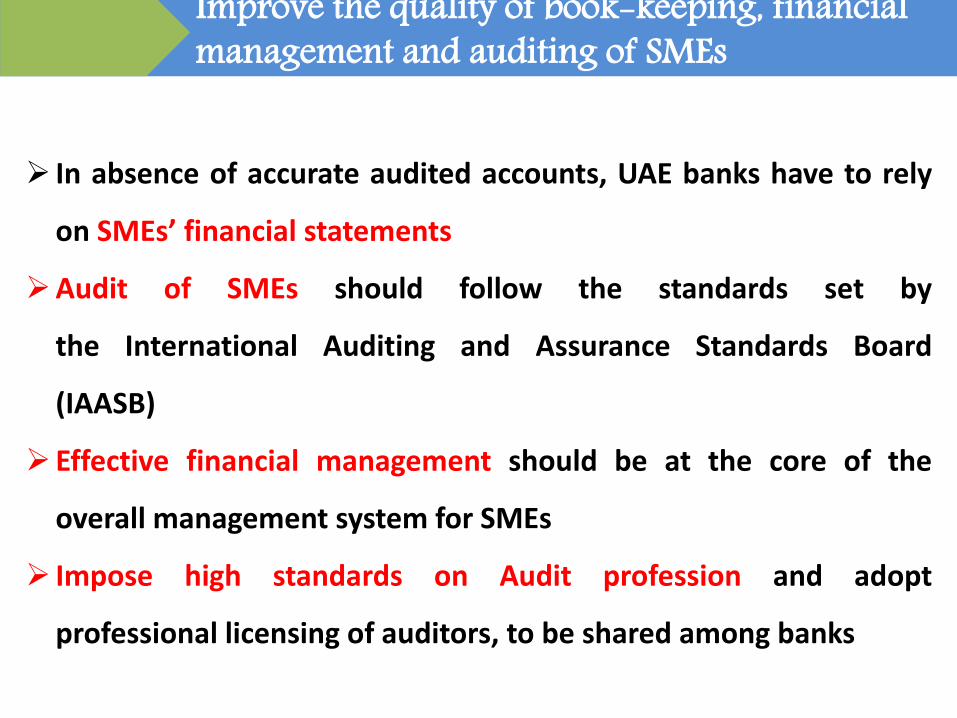

Improve the quality of book-keeping, financial management and auditing of SMEs

1

3

In absence of accurate audited accounts, UAE banks have to rely

on SMEs’ financial statements

Audit of SMEs should follow the standards set by

the International Auditing and Assurance Standards Board

(IAASB)

Effective financial management should be at the core of the

overall management system for SMEs

Impose high standards on Audit profession and adopt

professional licensing of auditors, to be shared among banks

Help SME business development and access to export markets

1

3

Establish the Federal Small Business Administration entrustedwith: Providing asset-based lending (like CAP lines program in the

US), which provides asset-based credit lines for a short-termpurposes

Coordinate with the Export Promotion Authority to help SMEaccess to export markets

Establish a Federal Export Promotion Agency, whose maintasks: Inform SMEs about export opportunities through

participation to exhibitions in the UAE and abroad Facilitate matching with foreign buyers Provide training on trade finance and export operations Connect SMEs to trusted global export portals

Promote Venture Capital and other specialized companies and facilitate access to public procurements

1

3

Initiatives to encourage:

Venture Capital to fund startups and SMEs with high growth

potential

Business Angels to fill the gap between startups and seed capital

Facilitate SME access to public procurements

Ministry of Finance has developed a system that allows all SMEs

to access federal tenders

Ensure timely payments to SMEs from the public sector at both

federal level and emirates level

More Efforts are needed to mobilize the development for the MSMEs for the Benefits of our Economic Agendas

1

3

Thank you!