MSE608C – Financial and Cost Accounting Introduction.

27

MSE608C – Financial and Cost Accounting Introduction

-

date post

20-Dec-2015 -

Category

Documents

-

view

222 -

download

1

Transcript of MSE608C – Financial and Cost Accounting Introduction.

MSE608C – Financial and Cost Accounting

Introduction

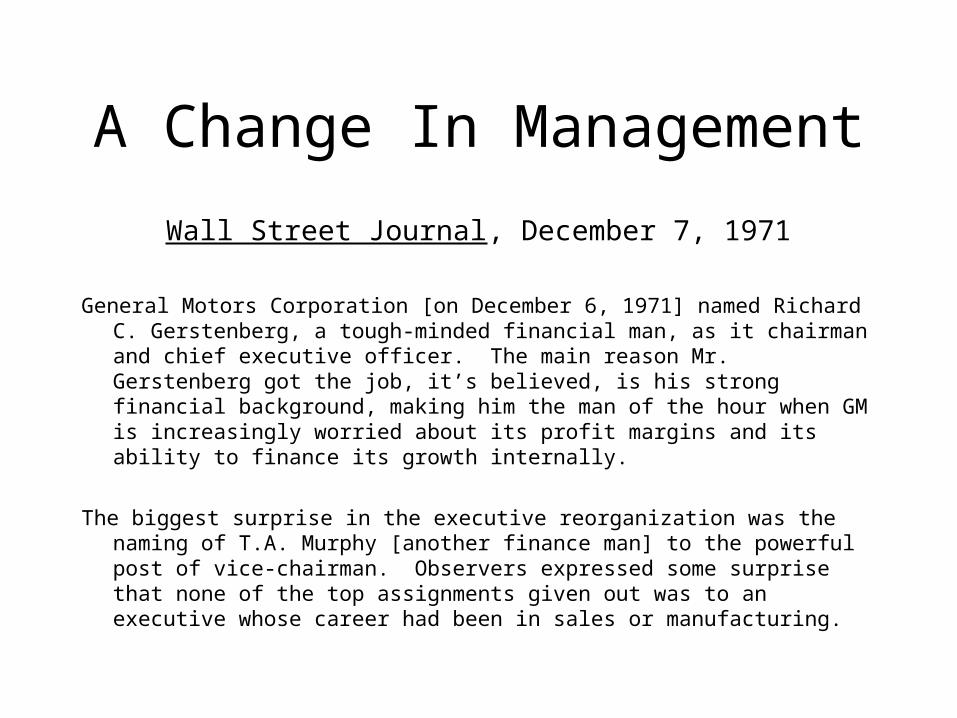

A Change In Management

Wall Street Journal, December 7, 1971

General Motors Corporation [on December 6, 1971] named Richard C. Gerstenberg, a tough-minded financial man, as it chairman and chief executive officer. The main reason Mr. Gerstenberg got the job, it’s believed, is his strong financial background, making him the man of the hour when GM is increasingly worried about its profit margins and its ability to finance its growth internally.

The biggest surprise in the executive reorganization was the naming of T.A. Murphy [another finance man] to the powerful post of vice-chairman. Observers expressed some surprise that none of the top assignments given out was to an executive whose career had been in sales or manufacturing.

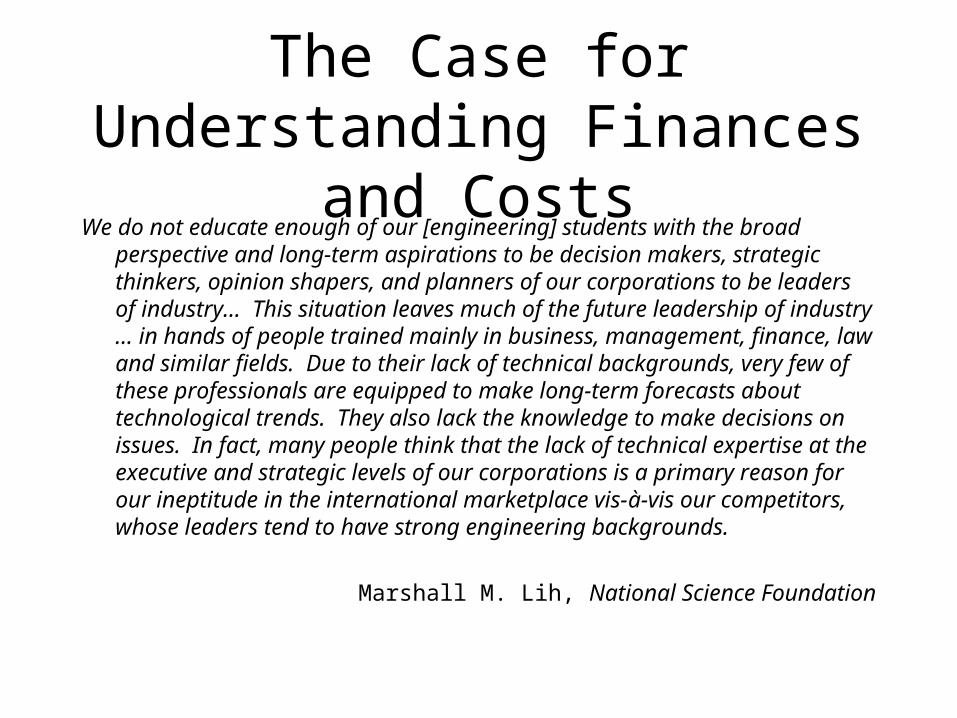

The Case for Understanding Finances and Costs

We do not educate enough of our [engineering] students with the broad perspective and long-term aspirations to be decision makers, strategic thinkers, opinion shapers, and planners of our corporations to be leaders of industry… This situation leaves much of the future leadership of industry … in hands of people trained mainly in business, management, finance, law and similar fields. Due to their lack of technical backgrounds, very few of these professionals are equipped to make long-term forecasts about technological trends. They also lack the knowledge to make decisions on issues. In fact, many people think that the lack of technical expertise at the executive and strategic levels of our corporations is a primary reason for our ineptitude in the international marketplace vis-à-vis our competitors, whose leaders tend to have strong engineering backgrounds.

Marshall M. Lih, National Science Foundation

WHY STUDY ACCOUNTING?

Why Study Accounting?

Part of the real world– It will provide useful knowledge and skills relevant to

understanding the successful operation of an organization. Many engineers tend to focus only on their task at-hand and ignore the financial implications; they see the forest and not the trees.

Why Study Accounting?

Requisite for high-level managementThe path to higher levels of management require a functional

understanding of accounting and how it is used to make decisions.

Beneficial to engineers at all levels• Manufacturing Engineer - analyze the value of equipment and

process changes; • Design Engineers - analyze the trade-offs required between

design and market demands;• Project Engineer - analyze the allocation of resources versus

scheduling using accounting information;• Senior-level Engineering Manager - monitor the gross financial

activities to ensure their profit centers are profitable.

Why Study Accounting?

Well-founded skepticismAccounting information is important in decision

making but it is at times inexact, subject to estimates, and can be open to interpretation.

Understanding is POWERBy understanding the accounting function the

engineer can fully participate in important business decisions.

What is Accounting?

The “language of business”– provides a common means for communicating

monetary information of an entity.

– Used by individuals and organizations inside and outside the entity.

What is Accounting?

• It is a organized and standardized process to observe, measure, record, classify and summarize activities of an organization into monetary terms.

• Not all important activities can be valued in monetary terms and thus cannot be included in reports and statements.

Who Are the Users of Accounting Information?

• Business managers– Plan; organize; direct; control; make decisions– Use historical data to plan for the future– Strategic (long-term) and Operational (short-term) planning

• Investors and owners– Financing the company– Payment of dividends– Capital purchases

• Creditors– What is the perceived risk (interest rate)– Collateral

• Government taxing and regulatory agencies– Taxes and compliance

What are Assets?

Assets– What a company OWNS

– Physical property, intangible rights and financial resources owned by the company.

– To be an asset it must: 1) possess future value,

2) be under the control of the business, and

3) have an assigned dollar value.

What are Liabilities?

Liabilities– What a company OWES

– Obligations owed to a creditor for a current benefit

– Must use assets to discharge liabilities.

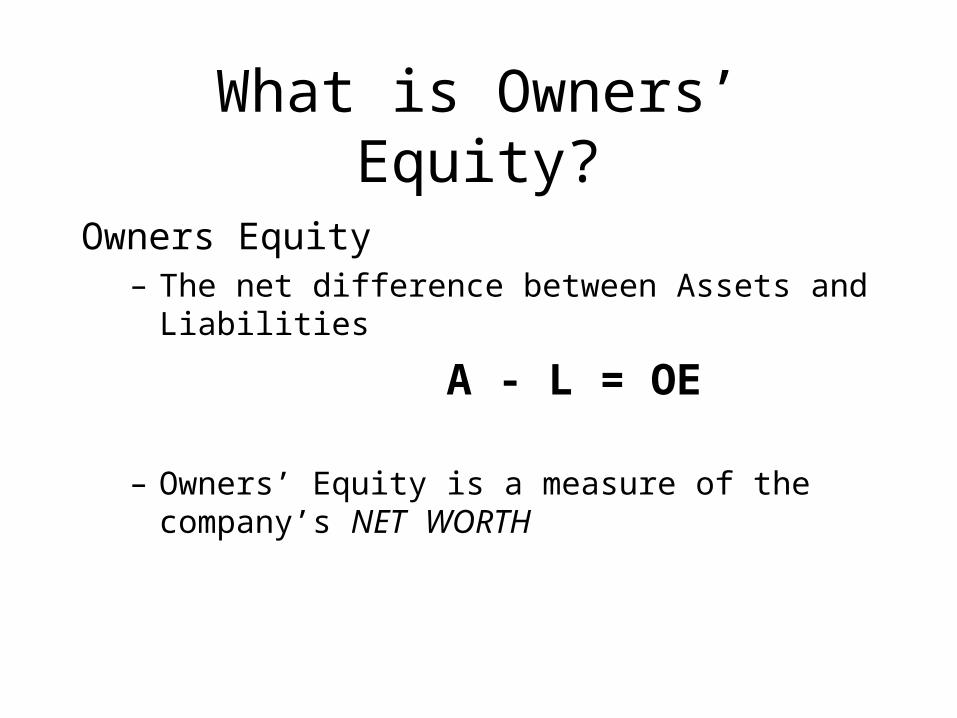

What is Owners’ Equity?

Owners Equity– The net difference between Assets and Liabilities

A - L = OE

– Owners’ Equity is a measure of the company’s NET WORTH

Fundamental Accounting Equation

A = L + OE

Valuing Assets

• Assets and must be valued in monetary terms.• Three valuation methods:

– Time-adjusted value method– Market value method– Cost value method

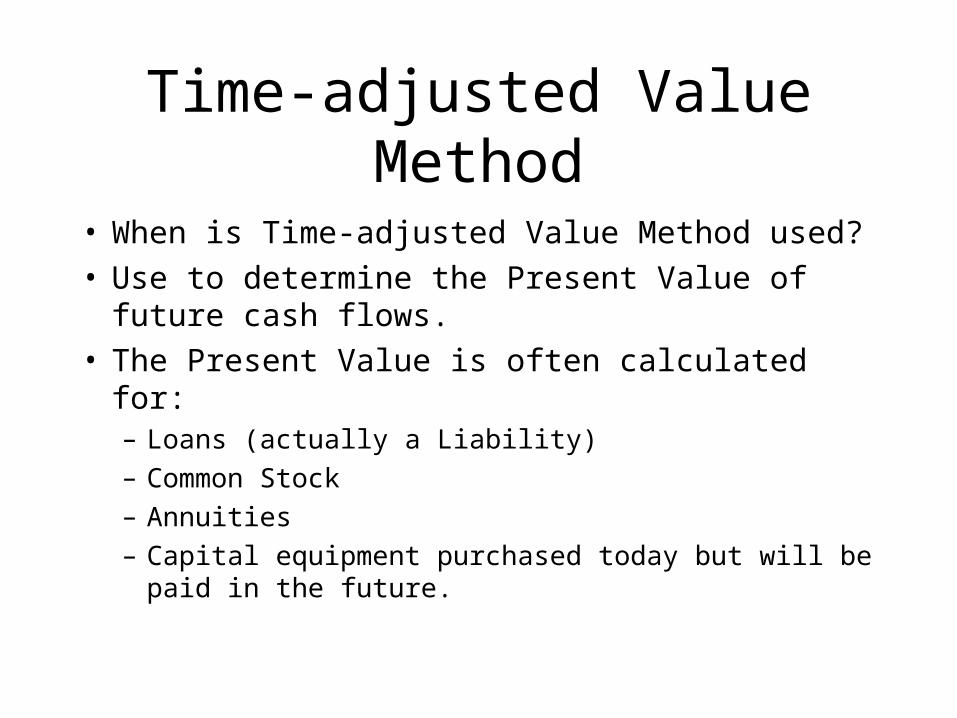

Time-adjusted Value Method

• When is Time-adjusted Value Method used?• Use to determine the Present Value of future cash

flows.• The Present Value is often calculated for:

– Loans (actually a Liability)

– Common Stock

– Annuities

– Capital equipment purchased today but will be paid in the future.

Time-adjusted Value Method

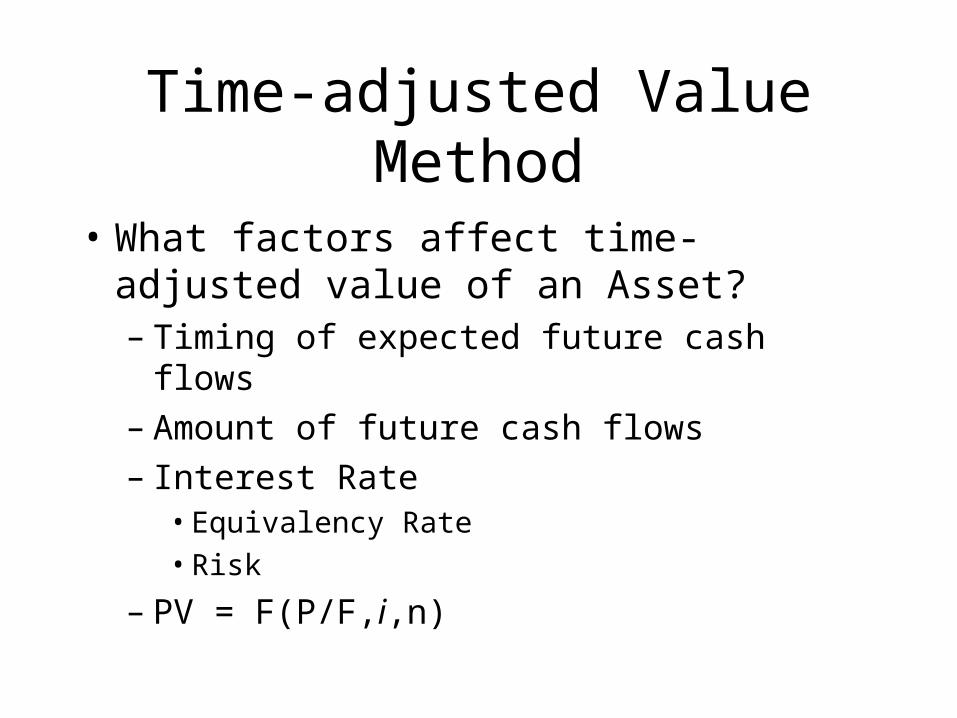

• What factors affect time-adjusted value of an Asset?– Timing of expected future cash flows– Amount of future cash flows– Interest Rate

• Equivalency Rate

• Risk

– PV = F(P/F,i,n)

Time-adjusted Value Method

• Advantages– Accurate for assets with long life and

predictable cash flows

• Disadvantages– Requires predictable cash flows.

Market Value Method

• The value of an Asset in the marketplace.– Established through second-hand markets

• Advantages– Easy to establish if efficient marketplace exists.

• Disadvantages– Difficult to establish if there is not an efficient

marketplace.

– Value can be unreliable if adequate information is not available (may be under- or over-valued)

Cost Value Method

• The value of an Asset is the price paid when it was acquired

• Advantages– Value clearly established

• Disadvantage– Does not account for appreciation or depreciation.

– Does not account for inflation

• Currently the most popular method

Intangible Assets

• Dictionary of Finance and Investment Terms:The right or nonphysical resource that is presumed to

represent and advantage to the firm’s position in the market place

• International Valuation Standards CommitteeAssets that manifest themselves by their economic

properties, they do not have physical substance, they grant rights and privileges to their owner and usually generate income for their owners.

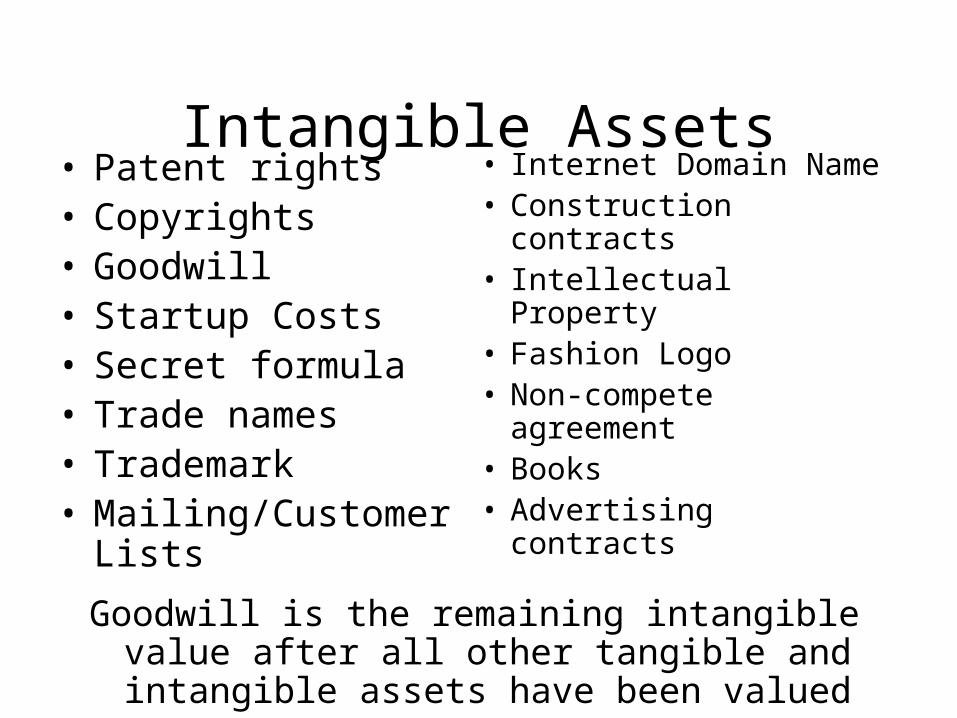

Intangible Assets• Patent rights• Copyrights• Goodwill• Startup Costs• Secret formula• Trade names• Trademark• Mailing/Customer Lists

• Internet Domain Name• Construction contracts• Intellectual Property• Fashion Logo• Non-compete agreement• Books• Advertising contracts

Goodwill is the remaining intangible value after all other tangible and intangible assets have been valued

Intangible Assets

• When are these valued– When an Intangible Asset is purchased– When a company is sold– When used as collateral for a loan– To obtain insurance

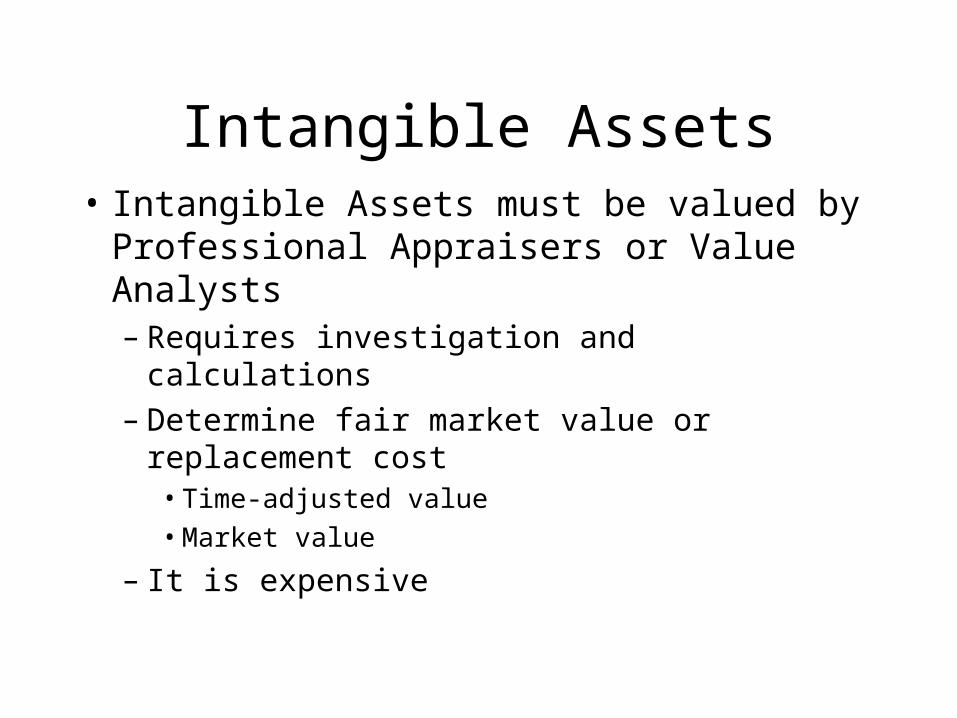

Intangible Assets• Intangible Assets must be valued by

Professional Appraisers or Value Analysts– Requires investigation and calculations– Determine fair market value or replacement

cost• Time-adjusted value

• Market value

– It is expensive

Intangible Assets

• Intangible assets are amortized (same as depreciated) if they have a limited life.

• Rule SFAS 142– Use straight-line method– 15 year asset class– Eliminated amortization of Goodwill

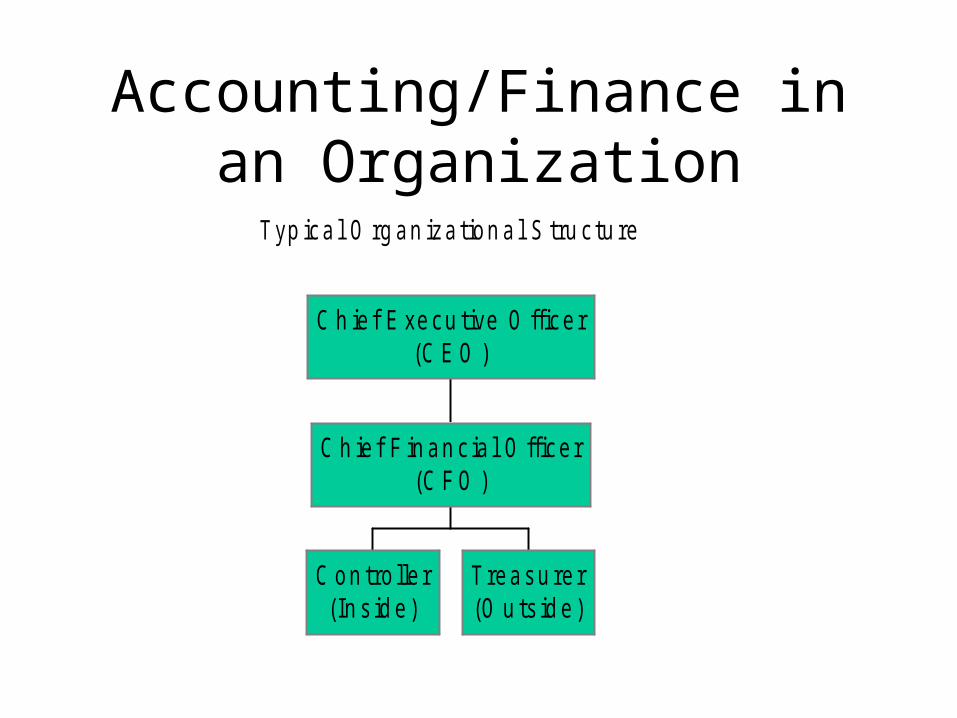

Accounting/Finance in an Organization

Typ ica l O rg an iza tion a l S tru c tu re

C on tro lle r(In s id e )

Treasu re r(O u ts id e )

C h ie f F in an c ia l O ffice r(C F O )

C h ie f E xecu tive O ffice r(C E O )

Assessment

1. What are the elements of the Fundamental Accounting Equation?

2. What is the definition of Owners Equity?

3. What are the three methods for Valuing Assets?