Mortgage Enforcement ESSENTIALS 2016 - LSUC Store · Continuing Professional Development ......

117

*CLE16-0090401-A-PUB* chair Doug Bourassa Chaitons LLP September 13, 2016 Mortgage Enforcement ESSENTIALS 2016 Pracce Gems

Transcript of Mortgage Enforcement ESSENTIALS 2016 - LSUC Store · Continuing Professional Development ......

*CLE16-0090401-A-PUB*

chair

Doug Bourassa Chaitons LLP

September 13, 2016

Mortgage Enforcement ESSENTIALS 2016

Practice Gems

DISCLAIMER: This work appears as part of The Law Society of Upper Canada’s initiatives in Continuing Professional Development (CPD). It provides information and various opinions to help legal professionals maintain and enhance their competence. It does not, however, represent or embody any official position of, or statement by, the Society, except where specifically indicated; nor does it attempt to set forth definitive practice standards or to provide legal advice. Precedents and other material contained herein should be used prudently, as nothing in the work relieves readers of their responsibility to assess the material in light of their own professional experience. No warranty is made with regards to this work. The Society can accept no responsibility for any errors or omissions, and expressly disclaims any such responsibility.

© 2016 All Rights Reserved

This compilation of collective works is copyrighted by The Law Society of Upper Canada. The individual documents remain the property of the original authors or their assignees.

The Law Society of Upper Canada 130 Queen Street West, Toronto, ON M5H 2N6Phone: 416-947-3315 or 1-800-668-7380 Ext. 3315Fax: 416-947-3991 E-mail: [email protected] www.lsuc.on.ca

Library and Archives Canada Cataloguing in Publication

Practice Gems: Mortgage Enforcement Essentials 2016

ISBN 978-1-77094-768-9 (Hardcopy)ISBN 978-1-77094-769-9 (PDF)

1

Chair: Doug Bourassa, Chaitons LLP

Chair: Doug Bourassa, Chaitons LLP

September 13, 2016 1:00 p.m. – 4:00 p.m.

Total CPD = 2 h 30 m Substantive + 30 m Professionalism

The Law Society of Upper Canada

130 Queen, Street West Toronto, ON

SKU CLE16-00904

Agenda 1:00 p.m. – 1:10 p.m. Welcome and Opening Remarks

Doug Bourassa, Chaitons LLP

1:10 p.m. – 1:35 p.m. The Latest Law Affecting Mortgagees (Including

Additional Charges and Fees)

Doug Bourassa, Chaitons LLP

PRACTICE GEMS:

MORTGAGE ENFORCEMENT

ESSENTIALS 2016

2

1:35 p.m. – 2:00 p.m. NSIs (Notices of Security Interest) and other Title Issues

on Enforcement

Amanda Jackson, Gowling WLG (Canada) LLP 2:00 p.m. – 2:20 p.m. Collateral Mortgages: Special Documentary Issues, Rights

and Remedies Simon Crawford, Bennett Jones LLP 2:20 p.m. – 2:30 p.m. Go Ahead and Ask Us (Question and Answer Session) 2:30 p.m. – 2:45 p.m. Coffee and Networking Break 2:45 p.m. – 3:10 p.m. Mortgagees in Possession: Drawbacks and Benefits

Jerry Udell, C.S., McTague Law Firm LLP 3:10 p.m. – 3:40 p.m. Things I May Have Forgotten but Really Need to Know:

Protecting yourself in a Scary Market (30 minutes )

James Butson, Agueci & Calabretta

Joel Kadish, Kadish Law Professional Corporation

3:40 p.m. – 3:55 p.m. Procedure for Assessing of Accounts, Fees, and Expenses Robert Macdonald, Fogler, Rubinoff LLP 3:55 p.m. – 4:00 p.m. Go Ahead and Ask Us (Question and Answer Session) 4:00 p.m. Program Ends

September 13, 2016 SKU CLE16-00904

Table of Contents

TAB 1 Can a Mortgagee Sell to Itself Under Power of Sale? …….. 1 - 1 to 1 - 9

Doug Bourassa, Chaitons LLP Tushar Sabharwal, Chaitons LLP TAB 2 Title Issues: Notices of Security Interest and

Lodgements of Title …………………………………………………….. 2 - 1 to 2 - 18

Amanda Jackson, Gowling WLG (Canada) LLP James Riewald, Gowling WLG (Canada) LLP

TAB 3 Collateral Mortgages (including, but not limited to,

Mortgages on collateral) ……………………………………………… 3 - 1 to 3 - 30 Simon Crawford, Bennett Jones LLP Nicholas Arrigo, Student-at-Law, Bennett Jones LLP TAB 4 Mortgagees in Possession: Drawbacks and Benefits …….. 4 - 1 to 4 - 7

Jerry Udell, C.S., McTague Law Firm LLP Omar Raza, Barrister and Solicitor Adam Bulkiewicz, Student-at-Law, McTague Law Firm LLP Samuel Atkin, Student-at-Law, McTague Law Firm LLP

PRACTICE GEMS:

MORTGAGE ENFORCEMENT

ESSENTIALS 2016

TAB 5 Things I May Have Forgotten but Really Need to Know:

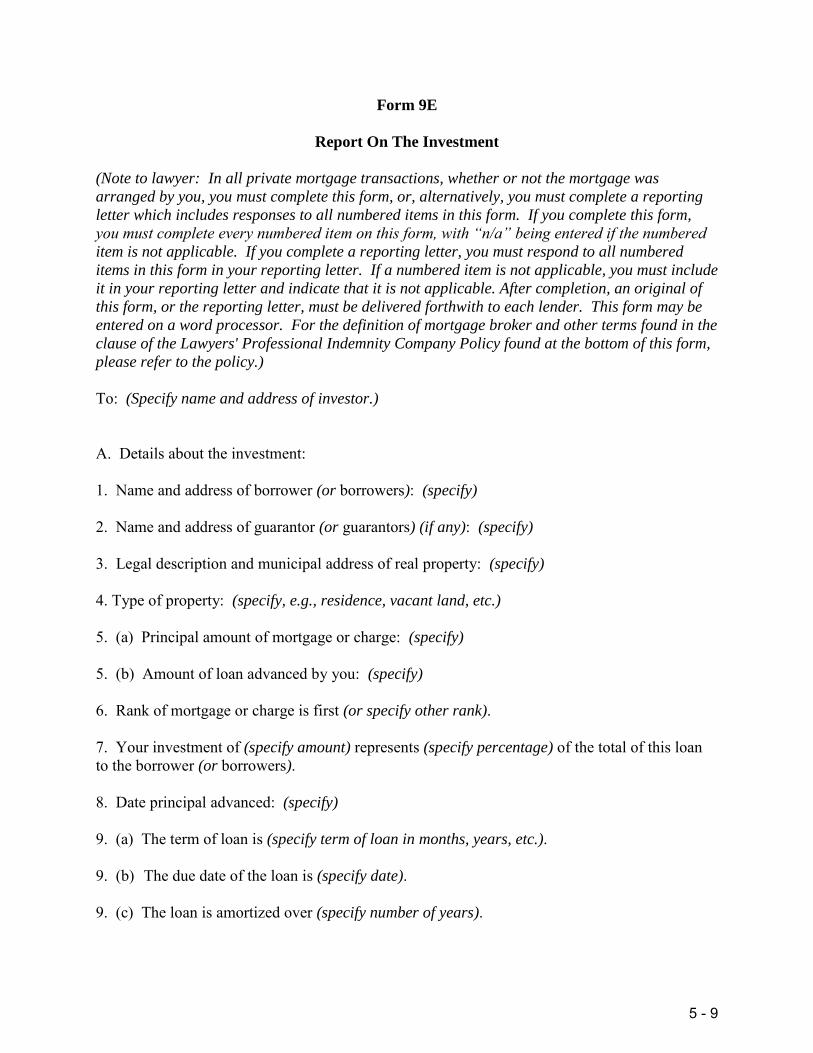

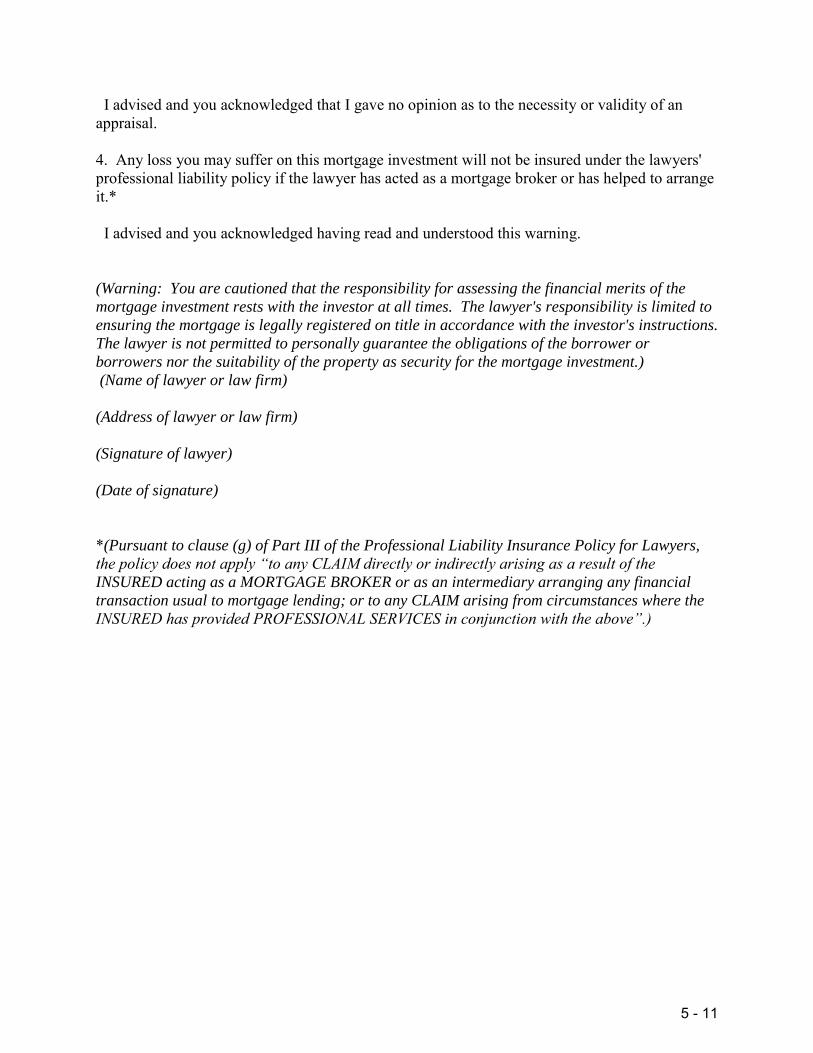

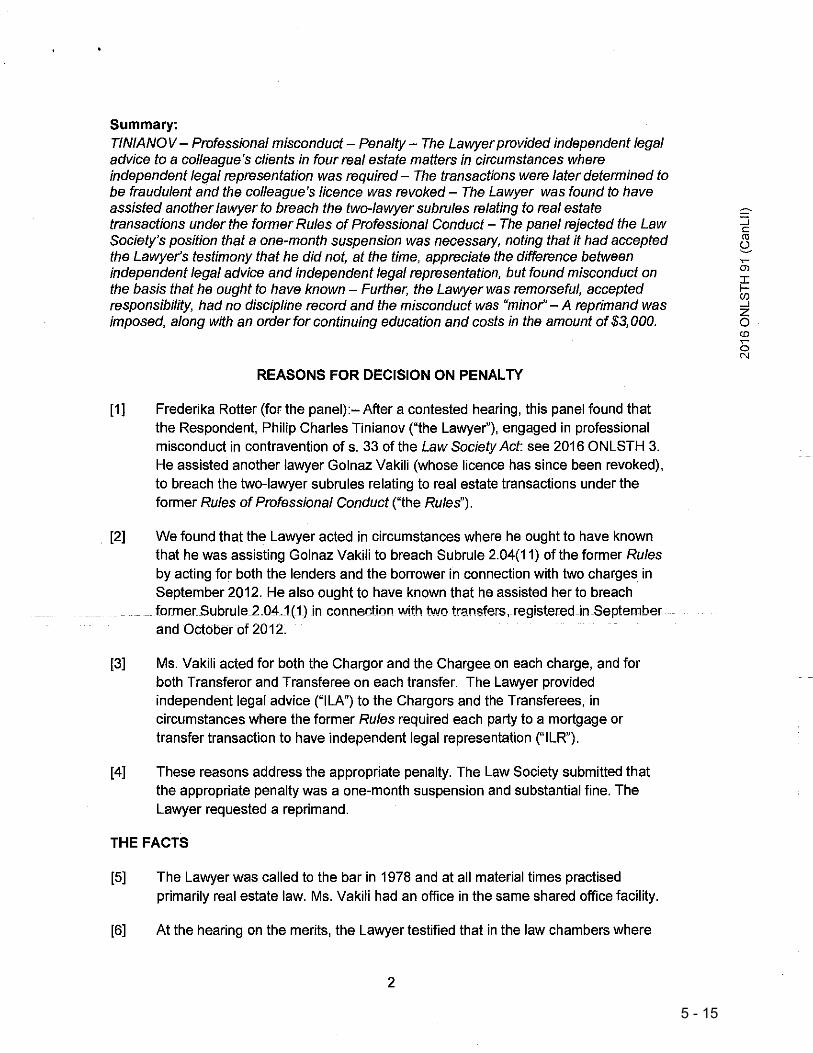

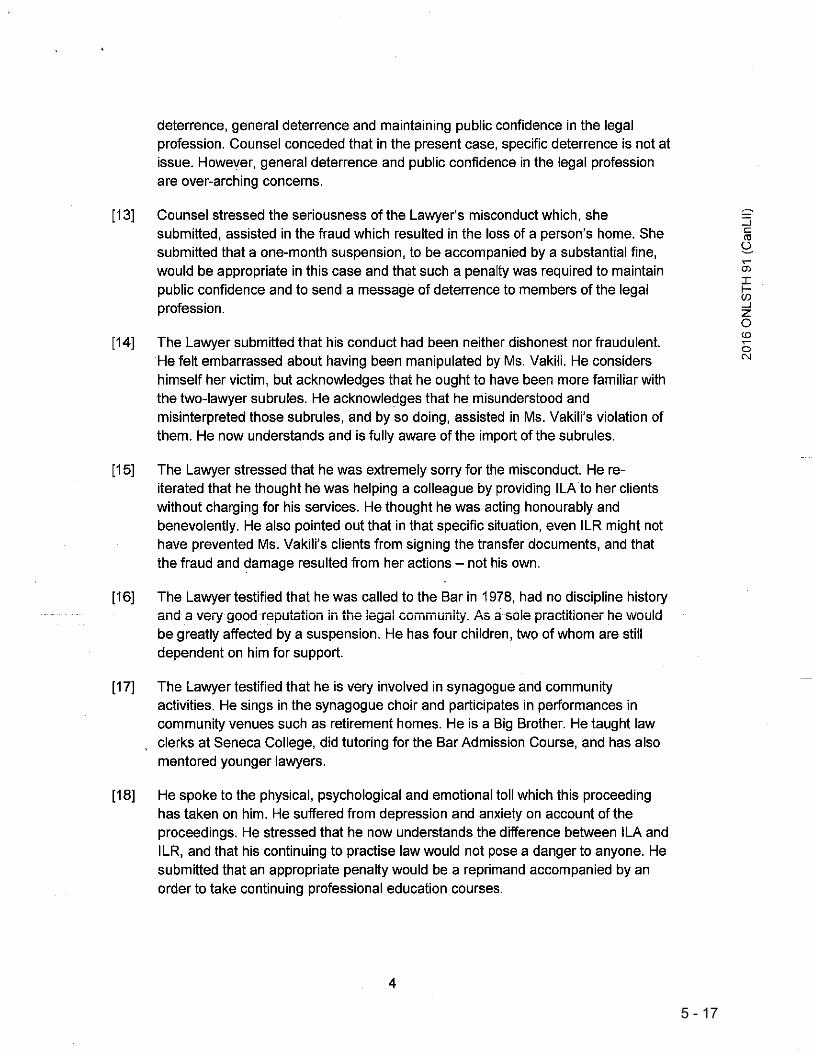

Protecting yourself in a Scary Market …………………………… 5 - 1 to 5 - 35 Investment Authority Investment Authority – Form 9D Report on Investment – Form 9E Mortgages and Record Keeping Requirements – By-Law 9 - Q&A (CanLII) Law Society of Upper Canada v. Tinianov Resource Links James Butson, Agueci & Calabretta Joel Kadish, Kadish Law Professional Corporation

TAB 6 Procedure for Assessing of Accounts, Fees and

Expenses ……………………………………………………………………… 6 - 1 to 6 - 5 Robert Macdonald, Fogler, Rubinoff LLP

TAB 1

Can a Mortgagee Sell to Itself Under

Power of Sale?

Doug Bourassa Chaitons LLP

Tushar Sabharwal

Chaitons LLP

September 13, 2016

Practice Gems:

Mortgage Enforcement

ESSENTIALS 2016

CAN A MORTGAGEE SELL TO ITSELF UNDER POWER OF SALE?

Doug Bourassa and Tushar Sabharwal

Chaitons LLP

Introduction

In today’s real estate market, aggressive and entrepenurial mortgagees are often concerned not

only with collecting their loaned monies, but will gaze longingly at the substantial equity upside

of owning the mortgaged property. The natural enforcement remedy would be foreclosure.

However, that remedy brings with it a lack of control over the process that is rarely attractive to a

lender. Instead, the question that is more often heard in today’s environment is whether the

lender can purchase the property itself under power of sale. Pejoratively, this is known as the

‘loan-to-own’ strategy.

The answer to this basic question turns out to be highly fact specific. As a starting point, one

must be familiar with a fundamental legal principle, which is that an individual cannot sell to

himself, including to a trustee for himself. Such a sale would be improvident and accordingly set

aside. An early, yet frequently cited decision from England, Farrar v. Farrars (“Farrar”)1,

succinctly summarized this basic proposition:

“A mortgagee cannot sell to himself, nor can two mortgagees sell to one of themselves,

nor to one of themselves and another. The reasons for this are obvious, and are not

merely formal but substantial. A man cannot contract with himself, and in the cases

supposed there cannot be any independent bargaining as between opposite parties. For

similar reasons a mortgagee cannot sell to a trustee for himself; he cannot buy in the

name of another”2

The passage above, though it may seem conclusive, actually raises further questions. Most

importantly, what are the parameters of “himself”? Will the courts uphold a sale by a mortgagee

to a spouse or a relative? What about a sale to corporation where the mortgagee is a shareholder?

Finally are there any special provisions for banks and financial institutions?

This paper will canvass the jurisprudence beginning from some of the earliest to some of the

most recent reported decisions on this question. This paper concludes that the principle from

Farrar is not absolute and as long as certain “duties” are followed by the mortgagee, the sale will

1 (1888) 40 Ch. D 396 2 Ibid at para 5 (lower court decision)

1 - 1

likely survive the court’s scrutiny. Whether it will attract litigation from the mortgagor is an

entirely different question.

Mortgagee as Shareholder of the Purchasing Corporation

(a) Farrar v Farrars Limited (1888) 40 Ch. D 396

The Farrar decision was referred to earlier for the legal principle that a mortgagee cannot sell to

himself. However, Farrar is also noteworthy because it opened to door for mortgagees to sell to

a corporation in which they held equity.

In Farrar, the defendant was one the three mortgagees of a property. The plaintiffs, being the

mortgagors, were in default and subsequently, the mortgagees took possession of the property.

Despite good faith endeavours to seek buyers for the property, the mortgagees failed to receive a

single offer. The mortgagees were advised by a “very competent person” named Mr. Hepper that

there was no prospect of a sale3. Accordingly, the defendant formed a limited company, in which

he was a significant shareholder, in order to use it as a vehicle to purchase the property. The

defendant successfully completed the transaction through the company; however, the plaintiffs

commenced an action to have the sale set aside on the grounds that the company was formed by

the defendant to purchase the property from the mortgagees at undervalue and as a result, the

transaction was fraudulent.

Despite outlining the principle that a mortgagee cannot sell to himself, the court decided in

favour of the defendant and the transaction was upheld. In arriving at its decision, the court was

cognizant of the deep-seated legal distinction between a natural person and a corporation at law:

“A sale by a person to a corporation of which he is a member is not, either in form or in

substance, a sale by a person to himself. To hold that it is, would be to ignore the

principle which lies at the root of the legal idea of a corporation body, and that idea is

that the corporate body is distinct from the persons composing it. A sale by a member of

a corporation to the corporation itself is in every sense a sale valid in equity as well as

law. There is no authority for saying that such a sale is not warranted by an ordinary

power of sale, and in our opinion, such a sale is warranted by such a power, and does not

fall within the rule to which we have at present referred.”4[Emphasis added]

3 Ibid at para 3 (lower court decision) 4 Farrar v Farrars Limited (1888) 40 Ch. D 396 at para 5 (court of appeal)

1 - 2

Even though the sale to the company was held not to offend the principle, the court in Farrar

created boundaries under which this exception to the principle could apply. The boundaries are

essentially the “duties” that the mortgagee selling under a power of sale as to abide by.

Essentially, the corporation has the burden of upholding the sale by demonstrating its fulfilment

of its duties. In Farrar, the duties outlined by the court included the duty to act in good faith and

the duty to take reasonable precautions to obtain a proper price. The defendant in Farrar fulfilled

his duties by doing his best to induce the mortgagors to pay him off, advertising the property in

the newspapers, putting the property up to auction and taking advice from a Mr. Hepper. In its

disposition on the issue of validity, the court stated the following:

“The evidence shows that the transaction was thoroughly honest and fair, and,,

notwithstanding its suspicious appearance, the company has proved its validity”5

This presents an interesting commingling of two different legal principles: (a) the validity of a

sale; and (b) the lender’s liability for an improvident sale. In Farrar, the purchaser was a risk of

having the sale set aside as invalid, whereas in a normal improvident sale transaction, the risk is

of a damages award, not usually a vacation of title. This additional risk can be understood as

premised on the principal of actual notice. A purchaser with knowledge of the sale at an

improvident basis takes title subject to that knowledge, and may therefore be liable to losing title.

(b) Ostrander v Niagara Helicopters Ltd6 [“Ostrander”]

The Ostrander decision is particularly interesting because it dealt with the validity of a sale of a

property by a mortgagee to a corporation in which the receiver-manager had a shareholding

interest.

In Ostrander a receiver-manager named Bawden was appointed privately by the debenture

holder, Roynat, upon default by the debtor. Ultimately, the debenture holder entered into an

agreement to sell the assets to New Unisphere, a corporation in which the receiver-manager held

a 2% interest. The debtor subsequently petitioned the court to declare the transaction void

because it alleged that the receiver and other defendants conspired against him, and that the

defendants wrongfully converted assets, thereby committing fraud.

5 Ibid at 17 6 1973 CanLII 467 (Ont. H.C.J.)

1 - 3

The court was of the view that even though the receiver-manager was an agent for the mortgagee

in possession and had a shareholding interest in the purchasing corporation, the transaction was

“While I find that the purchase by Mr. Bawden of the shares in New Unisphere, in the

amounts and at the times when he did, were purchases which he should better not have

made, I cannot find anything in these transactions to impugn the validity of the final sale

by tender. I am satisfied that Mr. Bawden and his principal Roynat did the very best they

could to protect their own security but at the same time went out of their way to assist

Ostrander in so far as his private negotiations had any hopes of success. Other than the

tactless purchase of these shares and the minor misjudgment with respect to certain

payments with which I have already dealt, I can find nothing censurable in Mr. Bawden's

conduct. I am satisfied that the power of sale was exercised in a fair and proper manner

and that in the opinion of Roynat and its advisers the better offer was obtained.”7

The court found that the transaction in question was completed only after other avenues to

sustain the business in receivership were exhausted. Further, even though there was another

competing offer, the court was of the view that such decisions were to be made at Roynat’s

discretion. Again, despite the suspicious circumstances surrounding the transaction, it was

ultimately upheld. Roynat and the receiver-manager had discharged themselves of the burden

placed upon them by demonstrating that they acted in good faith and took reasonable precautions

to obtain a proper price.

(c) 665456 Ontario Ltd. v. Barelan Management Inc.8[“Barelan”]

Barelan, is a more recent Ontario Court of Appeal decision and is another example of the courts

dealing with a transaction under a power of sale where a mortgagee is a shareholder of the

purchasing corporation.

The basic facts in Barelan were that the assignee of a mortgage exercised its power of sale and

sold the property to a numbered corporation at a price in excess of the appraised value. Most

importantly, it should be noted that the same person controlled the assignee and the purchasing

corporation. Prior to the closing of the sale, the mortgagor sought to redeem the mortgage. The

lender refused, asserting that, since a firm agreement to sell had been entered into, the right to

redeem had been extinguished.

7 Ibid at para 12 8 1990 CanLII 6907 (Ont. C.A.)

1 - 4

At trial, the court followed the reasoning in Farrar and decided to uphold the transaction entered

into by the assignee of the mortgage and the numbered company. The court was of the view that

the transaction amounted to a valid financing scheme by the assignee and the purchaser to

protect its investment, much as a company must often resort to a plan to overcome a hostile take-

over bid. Also working in their favour was the fact that the purchase price was in excess of the

appraised value. Similar to Farrar and Ostrander, this transaction at the trial stage passed the

scrutiny of the courts as the assignee had discharged the burden placed upon it.

The decision was appealed and the impugned transaction was set aside, albeit for reasons

unrelated to the validity of the sale. The Court of Appeal reasoned that, since on the particular

facts of this case, the sale agreement provided that the mortgage was to remain in force, the

mortgagor’s equity of redemption also remained in force:

“Under this agreement, the mortgage is to remain in effect and survive this sale. The

mortgagor’s equity of redemption is therefore not extinguished nor is its right to redeem.

The mortgagee has, to all intents and purposes, simply postponed payment of the

mortgage”9

Accordingly, the Court of Appeal’s decision must be viewed as restricted to its specific (and

unusual facts). Yet, the decision should not take away from the overarching theme from

Barelan, which is that the courts in Ontario are receptive to sales to related corporations under

power of sale.

(d) Lay v. 1222055 Ontario Inc10 [“Lay”]

The Lay decision can be considered the seminal authority on the duties of mortgagees during a

power of sale. Unlike Farrar, Barelan and Ostrander, Lay is an example of a case where the

mortgagee failed to fulfill its duties. As a consequence of that failure, the impugned transaction

was set aside. At issue in this case was the sale of a golf course by a mortgagee to a purchaser

under power of sale. The mortgagee owned a 60% interest in the purchasing company, which

served as the vehicle for completing the transaction.

Further, in Lay, the court articulated and expanded on the duties of a mortgagee acting under a

power of sale: 9 Ibid at para 16 10 2006 CanLII 30865 (ONSC).

1 - 5

“In Broos v. Robinson (1984) 23 A.C.W.S. (2nd) 556 (H.C.J.) the court set out a list of

specific “duties” that should be followed, or at least considered by the mortgagee during

the power of sale procedure. Not all of these steps will be necessary or appropriate in

every case. The list is, however, helpful to flesh out in greater detail the scope of the

mortgagee’s duty “to take reasonable precaution to obtain the true market value of the

mortgaged property” at the date of sale. “True” market value is synonymous with “fair

market value” for these purposes. These steps include:

(1) act bona fides in the exercise of the power of sale;

(2) attempt to realize fair market value in the sale;

(3) give some consideration to the interests of the mortgagor as well as the

mortgagee’s own interests;

(4) do not conduct the sale in bad faith (which is the reverse side of (1));

(5) see that the property comes to the attention of a wide segment of the market;

(6) obtain proper appraisals;

(7) advertise the property for sale;

(8) place “For Sale” signs on the property;

(9) place the property with the Multiple Listing Service; and

(10) ensure that efforts are conducted over a reasonable period of time.”11

In Lay, a number of factors outlined above were not followed and were ultimately detrimental to

the interests of the mortgagee and purchaser. First, the mortgagee made no serious effort to test

the public market for the sale of the golf course. The marketing effort of the mortgagee consisted

of a single fax broadcast to the Golf Course Owners Association (Canada), a relatively small

segment of the potential market. This was considered a mere “Token Effort”12. Second, they

took no steps independently to establish the fair market value of the golf course. The failure of

the mortgagee to obtain an appraisal or to even seek the advice of real estate professionals was

also considered damaging to its interests. Third, the mortgagees created a document named “a

business scenario”, which outlined their long-term plan to take over the golf course and make it

profitable. Of utmost importance, was the fact that this document was made in anticipation of the

default by the mortgagor. The existence of the plan spoke volumes of the mortgagees’ intentions

under the power of sale. The mortgagees were not interested in protecting their investment;

rather, they were interested in acquiring the golf course for themselves. In the eyes of the court,

this amounted to bad faith. The combination of failures by the mortgagees resulted in the

transaction being labeled a sham by the court and ultimately set aside.

11 Ibid at para 31. 12 Ibid at para 38.

1 - 6

In summary, from the Farrar decision to the Lay decision, it is clear that sales under power of

sale to related parties, such as corporations controlled by the principals of the lender, are not

strictly prohibited. The court will place the burden on the mortgagee to demonstrate the

fulfillment of its duties, to act in good faith to canvass the market and obtain an approximation of

market value. If these duties are complied with in good faith, there is no reason why such a

transaction would be set aside by the courts.

Mortgagee’s Spouse and Relatives

The mortgagee’s spouse and relatives may purchase the mortgaged property. Generally speaking,

the rationale is that the mortgagee is not “selling to himself”. In Bell v Smith (1916), 10 O.W.N.

414 (H.C.), it was held:

“The mortgagee was entitled to find a purchaser, if she did it fairly; and her husband did

not, in the absence of any suggestion to the contrary, come within the prohibited classes,

mentioned in Farrar v. Farrars, Ltd. (1888), 40 Ch. D. 395 (C.A.)." [Emphasis added]

As such, absent any indication of fraud or a failure of the mortgagee to perform one of his/her

duties, the transaction will be upheld. In Lake Apartments Ltd. v. Bootwala13, a decision from

Newfoundland, the mortgagee dealt with transactions between two brothers, one being the

mortgagee and the other the purchaser. The sale in this case was undervalued; however, it was

still upheld by the court. In its reasoning, the court was of the view that in such transactions,

without corruption or collusion between the mortgagee and purchasers, the court will not

interfere. The court was unable to find any evidence of collusion in this case.

Sale to a Third Party and Subsequent Reconveyence

There can be no doubt that a transaction valid in form and not in substance will not stand up to

judicial scrutiny. For example in the early Ontario case McLaren v. Fraser14, the mortgagee

exercised the power of sale contained in his mortgage by improperly selling to his own clerk who

13 37 D.L.R. (3d) 523. 14 1870 CarswellOnt 100

1 - 7

bought the property and subsequently conveyed it back to the mortgagee. Not surprisingly, the

transaction was set aside and the court in its reasons stated:

“The purchase made by Fraser (the defendant) under the power of sale was set aside upon

the application of that politic rule of equity which forbids the purchase by a trustee for

sale”15

Therefore, anyone who may think they have outsmarted the principle outlined in Farrar, by

creating a transaction which is in form compliant, but not in substance will be disappointed. It is

clear that such transactions will be met with equal scrutiny.

Are There Any Special Considerations for Banks?

Interestingly, if one looks at s. 433 of the Bank Act, it may lead to the conclusion that banks are

immune from the strictures of the Farrar decision and thus, have a free reign to purchase

property that it is selling under power of sale proceedings. The relevant parts of the section have

been reproduced below:

Purchase of realty

433 A bank may purchase any real property offered for sale

(c) by the bank under a power of sale given to it for that purpose, notice of the sale by

auction to the highest bidder having been first given by advertisement for four weeks in a

newspaper published in the county or electoral district in which the property is situated,

in cases in which, under similar circumstances, an individual could so purchase, without

any restriction as to the value of the property that it may so purchase, and may acquire

title thereto as any individual, purchasing at a sheriff’s sale or sale for taxes or under a

power of sale, in like circumstances could do, and may take, have, hold and dispose of

the property so purchased.16

However, it is important to note three factors that undermine the conclusion that banks are

immune from the common law principle in Farrar. First, there are no reported decisions

considering the provisions of s. 433(c) of the Bank Act. It is therefore unclear how s. 433(c) of

15 Ibid 16 Bank Act, SC 1991, c. 46, s. 433(c)

1 - 8

the Bank Act would be applied in light of the well established legal principle in Farrar. Second,

the requirements under this section are quite stringent. The requirements include four weeks of

advertising in a newspaper and going through an auction process. Auctions are a rare method of

conducting a power of sale in Canada. Third, the Bank Act only applies to Canadian Chartered

Banks and to some Canadian subsidiaries of foreign Banks. By no means does this provision

apply to all mortgage lenders across Ontario or to individual mortgagees.

Conclusion

There can be no doubt that a direct sale to oneself clearly offends the common law rule

established in Farrar. However, when a mortgagee purchases under a power of sale as a

shareholder of a corporation, the courts will not set aside the transaction automatically; rather,

the transaction will be scrutinized. So long as the mortgagee fulfills its duties under a power of

sale, the transaction should stand. Similar considerations apply to sales to spouses or other

relatives. Further, there can be no doubt that transactions compliant in form but not in substance

will clearly fail. On the other hand, although s. 433 of the Bank Act may seem to provide some

assistance to banks, the provision has yet to be considered by the judiciary. As it stands, s. 433

provides a very restrictive and unattractive means of completing a power of sale.

For the entrepeneurial lender, it may be able to successful complete this ‘backdoor foreclosure’.

It is not a strategy without risk. Related party transactions often attract litigation from

mortgagors who feel, rightly or wrongly, that the lender has not fulfilled its duties to obtain

market value. In assessing the value of the property as a potential purchase, a lender should add

a legal fee component to its cost/benefit analysis. There will be little chance of collecting any

costs award against a mortgagor who unsuccessfuly challenges a sale. After all, they couldn’t

pay their debts in the first place.

1 - 9

TAB 2

Title Issues: Notices of Security Interest

and Lodgements of Title

Amanda Jackson Gowling WLG (Canada) LLP

James Riewald

Gowling WLG (Canada) LLP

September 13, 2016

Practice Gems:

Mortgage Enforcement

ESSENTIALS 2016

TITLE ISSUES: NOTICES OF SECURITY INTEREST AND LODGEMENTS OF TITLE

James Riewald and Amanda Jackson Gowling WLG (Canada) LLP September, 2016

Introduction

It is not uncommon for equipment such as furnaces and air conditioners to be sold to a

consumer with a payment plan stretching over several years. A financier will typically

protect the priority of its security by registering a Notice of Security Interest. A less

popular registration achieving a similar purpose is a Lodgement of Title. These

registrations can often create priority issues between a mortgagee and the financier and

lead to title problems when a mortgagee seeks to convey a property under power of

sale. The purpose of this paper is to identify both types of registration, analyze typical

priority issues and discuss the treatment of both in the sale process.

Notice of Security Interest

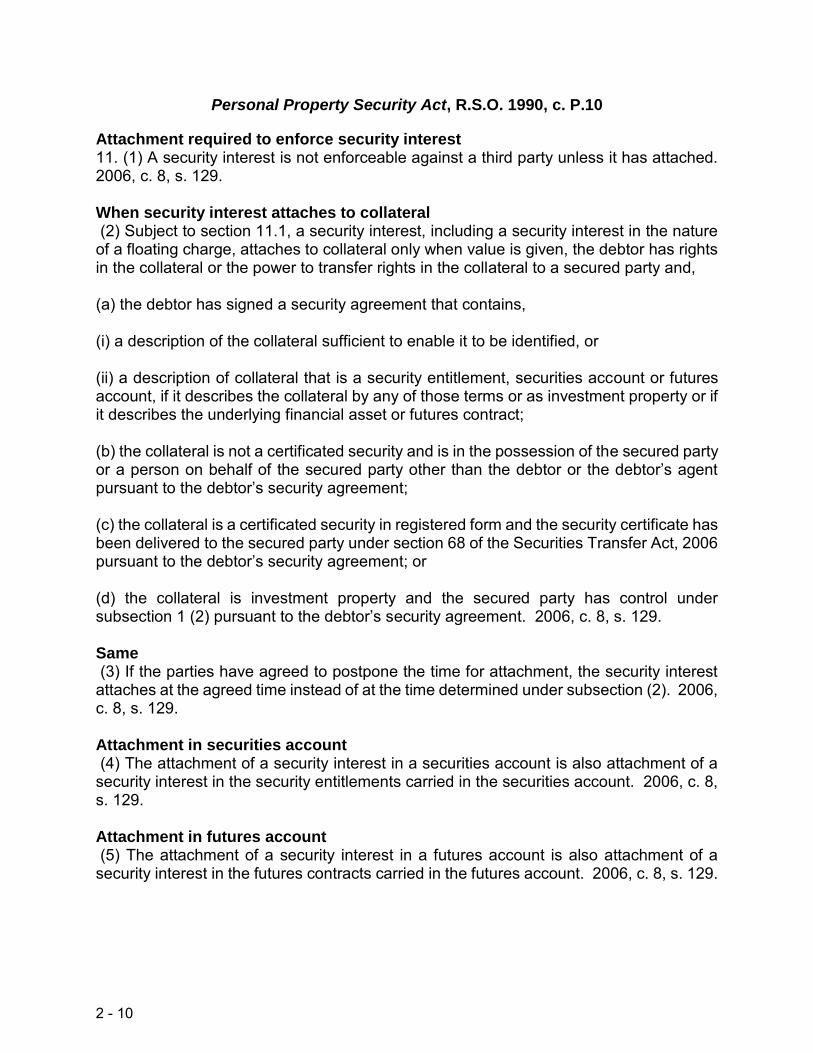

A Notice of Security Interest is a creature of statute. The Personal Property Security

Act1 permits the registration of a notice of security interest (in the required form) in the

proper land registry office where the collateral is or includes fixtures or goods that may

become fixtures.2 The form of notice is prescribed by Minister’s Order, pursuant to

section 25 of the PPSA.

By registering the notice in the land registry office, a secured party is able to give notice

of its interest in the collateral to subsequent mortgagees and purchasers. Where a

1 R.S.O. 1990, c. P10

2 Ibid., s. 54(1)

2 - 1

notice has been registered, every person dealing with the collateral is deemed to have

knowledge of the security interest for the purpose of s. 34(2) of the PPSA.3

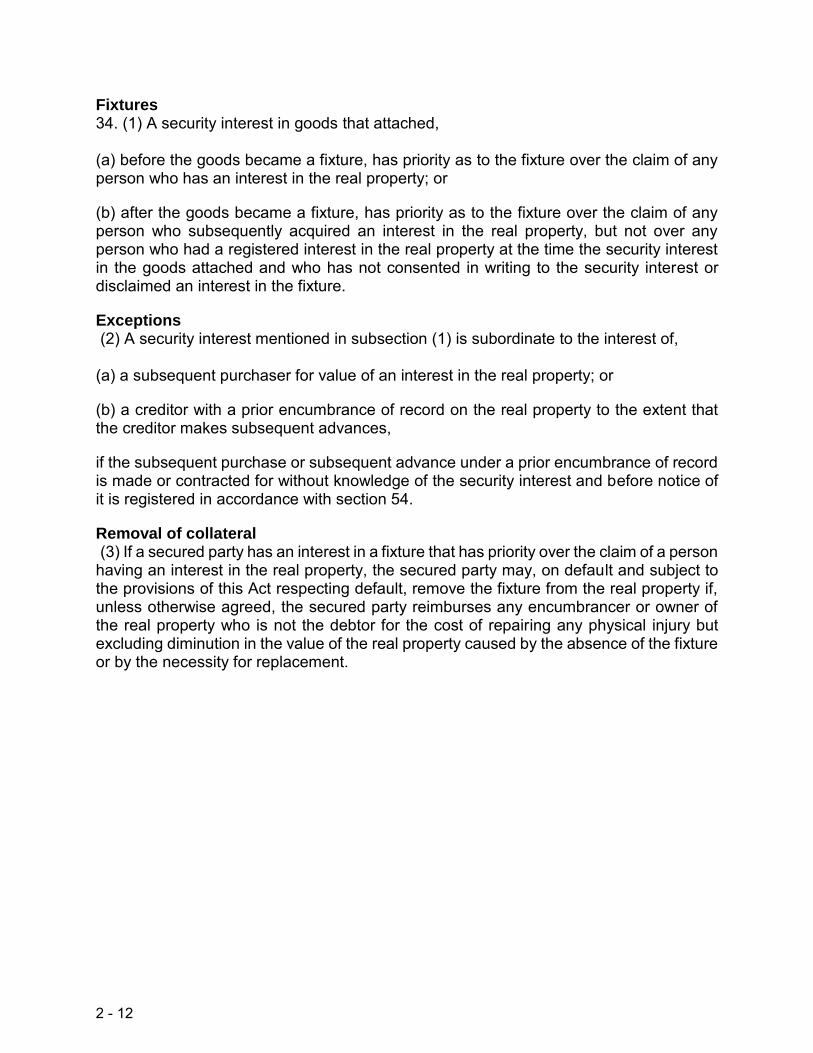

Section 34 of the PPSA is the starting point for determining priorities between secured

creditors and persons with an interest in the real property on which the fixture is located.

The general rule is that where the security interest in goods attaches before the goods

become a fixture, the security interest has priority over the claim of any person with an

interest in the real property (i.e., mortgagees). Where the security interest attaches

after the goods become a fixture, the security interest will have priority over

subsequently acquired interests in the real property but not over persons with registered

interests in the real property at the time the security interest attached and who have not

consented in writing to the security interest or disclaimed an interest in the fixture.4

Generally, the key issue for determining priorities is the timing of when the security

interest attaches to the goods. A security interest attaches when value is given, the

debtor has rights in the collateral or the power to transfer rights in the collateral to a

secured party and the debtor has signed a security agreement that contains certain

legislated information.5

The exceptions to the general rule stated above are twofold: (i) subsequent purchasers

for value of an interest in the real property; or (ii) creditors with prior encumbrances to

the extent that subsequent advances are made, if the purchase or subsequent advance

is made without knowledge of the security interest and before notice of the security

interest is registered in accordance with s. 54.6

3 Ibid., s. 54(5)

4 Ibid., s. 34(1)

5 Ibid., s. 11

6 Ibid., s. 34(2)

2 - 2

The deemed knowledge provision of s. 54 is important because by registering a notice

of security interest, a secured creditor is able to extend its priority over the fixture to

persons that would otherwise fall within the two exceptions set out above. Registration

of the notice protects the secured party’s priority over the fixture as against the claims of

subsequent purchasers or creditors making subsequent advances who might otherwise

claim they had no knowledge of the security interest.

The usual process when registering a transfer under power of sale is that the land

registrar will delete the entry of instruments (such as mortgages) that rank subsequent

to the mortgage under which the land is sold.7 However, there are a number of

instruments and entries that will not automatically be deleted even where notice of the

sale has been given.8 A Notice of Security Interest is one such instrument.

A Notice of Security Interest will not be deleted unless the mortgagee or its solicitor

make a statement attesting to the following:

1. That to the best of his/her knowledge and belief the security interest was

attached to the goods after they became fixtures and that the mortgagee did

not consent in writing to the security interest nor disclaim any interest in the

goods as fixtures; or

2. That to the best of his/her knowledge and belief the security interest was

attached to the goods before they became fixtures and that to the best of

his/her knowledge and belief a subsequent advance, as set out in the PPSA,

was made or contracted for under the mortgage without actual notice of the

security.9

7 Land Titles Act, R.S.O. 1990, c. L.5, s. 99(2)

8 Electronic Registration Procedures Guide, Version 11, January 2016, pp. 68 and 69

9 Electronic Registration Procedures Guide, Version 11, January 2016, p. 68

2 - 3

The statements set out above attest to the priority of the mortgage over the security

interest. In the case of the first statement, a person with an existing mortgage

registered on title will have priority over a secured creditor where the security interest

attaches to the goods after they become fixtures where the mortgagee did not consent

to the security interest or disclaim any interest in the goods as fixtures.10 In the case of

the second statement, the mortgage will have priority, even where the security interest

attached before the good became a fixture, where a subsequent advance was made

under the mortgage without actual notice of the security.11

Essentially, if a mortgagee can attest to the priority of its mortgage over the security

interest by making the above statements, the land registrar may delete the Notice of

Security Interest. The difficulty from a mortgagee’s perspective is that priorities

between a secured party and a mortgagee are often complicated. Consider, for

instance, the case of G.M.S. Securities & Appraisals Ltd. v. Rich-Wood Kitchens Ltd.12

The Ontario Court of Appeal considered the relative priorities between a first

mortgagee, a secured creditor whose security interest attached before the goods

became fixtures and a third mortgagee (a second mortgage had been previously paid

out). Subsequent to the registration of the first mortgagee, the goods became affixed to

the property. After the date the goods became attached, the first mortgagee made a

subsequent advance and the third mortgagee registered its mortgage. The secured

creditor registered a Notice of Security Interest after registration of the third mortgage.

The scenario created a circular priority problem. The first mortgagee had priority over

the secured creditor as to the amount of its subsequent advance only, the third

mortgagee had complete priority over the secured creditor but the first mortgagee had

priority over the third mortgagee for its mortgage.

10 PPSA, s. 34(1)(b); Home Trust Company v. Kitchener (City), 2013 ONSC 2190 (CanLII) at para. 29.

11 PPSA, s. 34(2)(b)

12 [1995] O.J. No. 44 (ONCA)

2 - 4

Practical Options

There are several other practical options for dealing with a Notice of Security Interest in

the context of a power of sale.

In the case of a Notice involving a security interest in goods subject to a rental

agreement (such as a furnace or water heater), the Agreement of Purchase and Sale

should make provision for the assumption by the purchaser of the rental agreement. In

such a case, provided the purchaser agrees, the Notice of Security Interest will simply

remain on title and there will be no issues.

In the case of a sale where there will be a surplus sufficient to pay out the interest of the

secured creditor, the sale transaction may close if the parties agree to an undertaking

by the mortgagee’s solicitor to obtain a discharge of the Notice of Security Interest.

Where there is likely to be a deficiency on sale, the mortgagee may want to consider

negotiating with the secured creditor to accept something less than what is owed in

respect of the security interest.

A final option is to insist that the secured creditor remove the fixture and discharge the

Notice of Security Interest. While the PPSA grants rights to a secured creditor to

remove a fixture13 there is no provision granting rights to a person with an interest in the

real property to insist that the secured creditor remove the fixture. The absence of a

provision does not necessarily mean that a person with an interest in the land does not

otherwise have such a right. The PPSA is clear that the principles of law and equity

shall supplement the PPSA and continue to apply unless they are inconsistent with the

express provisions of the PPSA. In Gari Holdings Ltd. v. Langham Credit Union Ltd.14,

the Saskatchewan Court of Appeal did not rule out that a person with an interest in land

13 See PPSA, s. 34(3)

14 2005 SKCA 97

2 - 5

who wished to have a fixture removed could seek a mandatory injunction against the

financier to do so. Moreover, the Court held that there was no reason why a person

should not be able to recover for loss occasioned by a commercially unreasonable

failure on the part of a financier to remove a fixture after having given notice of its

intention to do so. The Court reasoned that denying a remedy in such a situation would

effectively allow financiers to store fixtures on the property of others at no cost.15 In

G.M.S. Securities, supra, the Ontario Court of Appeal reasoned that a first mortgagee

converted the right of a financier to remove its fixture when it sold the subject property

under power of sale and held that against the first mortgagee when considering what

the reasonable commercial expectations of the parties were in resolving a priority

dispute. Perhaps it is within the reasonable commercial expectations of a mortgagee

and financier that if a mortgagee insists that a financier remove or waive its right to a

fixture, the financier will do so allowing the mortgagee to sell the property under power

of sale free and clear of any Notice of Security Interest.

The PPSA sets out circumstances where a person can demand that a secured party

register a discharge of a Notice of Security Interest (i.e., where all the obligations under

the security agreement have been performed).16 However, there is no provision for the

discharge of a Notice of Security Interest where the fixture once located on the subject

property is no longer present. In Home Trust Company v. Kitchener (City), supra, the

mortgagee took possession of the mortgaged property. At the time it took possession,

there was no air conditioner, which was subject to a security agreement, located on the

property. The mortgagee sold the property and the financier insisted on payment under

its Notice of Security Interest. The Court held that a Notice of Security Interest was not

an interest in land and that the reasonable commercial expectations of the parties

dictated that the financier should bear the loss.17 Accordingly, in situations such as the

15 Ibid, at paras. 25-28

16 PPSA, s. 56

17 Home Trust Company v. Kitchener (City), supra, at paras. 25 and 33

2 - 6

above, a mortgagee ought to be entitled to a discharge of the Notice of Security

Interest.

Lodgement of Title/Deposit of Title Deeds

A lesser known instrument sometimes found on title is a Lodgement of Title or Deposit

of Title Deeds.

A Lodgement of Title will typically provide that the borrower has delivered to the creditor

the title deeds to a property and that the creditor will have security over the property

until all obligations under an agreement have been performed. Security over real

property by way of Lodgement of Title is a recognized form of equitable mortgage in

Ontario.18 There does not have to be actual delivery of the title deeds - an agreement to

deliver the deeds is sufficient.19

Pursuant to s. 71 of the Land Titles Act20, any person entitled to or interested in any

unregistered estates, rights, interests or equities in registered land may protect same by

registering a notice under the section as authorized by the Director of Titles. A Notice of

Lodgement is a notice for which approval has been given by the Director Titles.21

In contrast to a Notice of Security Interest, a Notice of Lodgement is an entry that will be

deleted upon the registration of a transfer by a mortgagee under power of sale provided

that the Notice is registered subsequent to the mortgage under which the property is

conveyed. Any priority issues between the holder a Notice of Lodgement and a

mortgagee will be the typical priority issues as between mortgagees and order of

registration will prevail.

18 Walter M. Traub. Falconbridge on Mortgages, Fifth Edition, pages 5-7 and 5-8; Budzyk v. Thunder Bay Ventures, [1997] O.J. No. 658 at paras. 16 and 17.

19 Ibid.

20 R.S.O. 1990, c. L.5

21 Electronic Registration Procedures Guide, Version 11, January 2016, p. 106

2 - 7

Upon deletion of the Notice of Lodgement in a power of sale, the interest of any person

claiming under the Notice of Lodgement ceases to affect the land.22

Notwithstanding that the Notice of Lodgement will be deleted in a power of sale if it

ranks subsequent to the mortgage under which the property is conveyed, a purchaser

may want to consider if the Notice of Lodgement and/or communications from the

mortgagee or mortgagee’s lawyer in the course of the sale transaction puts the

purchaser on notice of some knowledge of a security interest. It may be that the

Lodgement of Title is part of a larger, multi-faceted consumer sale contract and that the

financier also has a security interest in a good affixed to the property.

A subsequent purchaser only obtains priority over a fixture if the purchase is made or

contracted for without knowledge of the security interest and before a Notice of Security

Interest is registered. The registration of the Notice of Security Interest deems a

purchaser to have knowledge but the registration is not necessary for the financier to

retain priority. While a financier may choose to register a Lodgement of Title in

accordance with the provisions of its consumer sale contract, it may be that the

consumer sale contract also creates a security interest. It could be argued by the

financier that the Notice of Lodgment also provides notice to a purchaser of an interest

in a fixture located on the property. Such an argument would be factually dependent on

the wording of the Notice of Lodgement and any other knowledge a purchaser may

have gained in the course of the sale negotiations. If a financier can successfully argue

that the purchaser had knowledge of the security interest then it would maintain priority

as against the purchaser.

However, it is unclear what level of knowledge is required. Arguably, the purchaser

would have to have knowledge of the security interest in the goods and that the security

interest had attached. The purchaser would need to have knowledge of each of the

conditions required for attachment:

22 Land Titles Act, s. 99(2)

2 - 8

a) value given;

b) the debtor has rights in the collateral or the power to transfer rights in the

collateral to a secured party; and

c) the debtor has signed a security agreement that contains a description of the

collateral sufficient to enable it to be identified.23

It seems unlikely that a purchaser would have such knowledge but, as stated above,

such a finding would be factually dependent on the particular transaction and the

wording of the Notice of Lodgement.

Conclusion

In conclusion, registrations of a Notice of Security Interest or Notice of Lodgement can

create complications where a property is being conveyed under power of sale. Where

there are sufficient proceeds to satisfy the financier’s interest or where the purchaser

agrees to assume the existing contract, problems are avoided. Where there are

insufficient proceeds a priority dispute between the interested parties may arise.

23 PPSA, s. 11(2)

2 - 9

Personal Property Security Act, R.S.O. 1990, c. P.10

Attachment required to enforce security interest 11. (1) A security interest is not enforceable against a third party unless it has attached. 2006, c. 8, s. 129. When security interest attaches to collateral (2) Subject to section 11.1, a security interest, including a security interest in the nature of a floating charge, attaches to collateral only when value is given, the debtor has rights in the collateral or the power to transfer rights in the collateral to a secured party and, (a) the debtor has signed a security agreement that contains, (i) a description of the collateral sufficient to enable it to be identified, or (ii) a description of collateral that is a security entitlement, securities account or futures account, if it describes the collateral by any of those terms or as investment property or if it describes the underlying financial asset or futures contract; (b) the collateral is not a certificated security and is in the possession of the secured party or a person on behalf of the secured party other than the debtor or the debtor’s agent pursuant to the debtor’s security agreement; (c) the collateral is a certificated security in registered form and the security certificate has been delivered to the secured party under section 68 of the Securities Transfer Act, 2006 pursuant to the debtor’s security agreement; or (d) the collateral is investment property and the secured party has control under subsection 1 (2) pursuant to the debtor’s security agreement. 2006, c. 8, s. 129. Same (3) If the parties have agreed to postpone the time for attachment, the security interest attaches at the agreed time instead of at the time determined under subsection (2). 2006, c. 8, s. 129. Attachment in securities account (4) The attachment of a security interest in a securities account is also attachment of a security interest in the security entitlements carried in the securities account. 2006, c. 8, s. 129. Attachment in futures account (5) The attachment of a security interest in a futures account is also attachment of a security interest in the futures contracts carried in the futures account. 2006, c. 8, s. 129.

2 - 10

Perfecting as to proceeds 25. (1) Where collateral gives rise to proceeds, the security interest therein, (a) continues as to the collateral, unless the secured party expressly or impliedly authorized the dealing with the collateral free of the security interest; and

(b) extends to the proceeds. R.S.O. 1990, c. P.10, s. 25 (1); 2000, c. 26, Sched. B, s. 16 (3).

Idem (2) Where the security interest was perfected by registration when the proceeds arose, the security interest in the proceeds remains continuously perfected so long as the registration remains effective or, where the security interest is perfected with respect to the proceeds by any other method permitted under this Act, for so long as the conditions of such perfection are satisfied. R.S.O. 1990, c. P.10, s. 25 (2). Idem (3) A security interest in proceeds is a continuously perfected security interest if the interest in the collateral was perfected when the proceeds arose. R.S.O. 1990, c. P.10, s. 25 (3). Idem (4) If a security interest in collateral was perfected otherwise than by registration, the security interest in the proceeds becomes unperfected ten days after the debtor acquires an interest in the proceeds unless the security interest in the proceeds is perfected under this Act. R.S.O. 1990, c. P.10, s. 25 (4). Motor vehicles classified as consumer goods (5) Where a motor vehicle, as defined in the regulations, is proceeds, a person who buys or leases the vehicle as consumer goods in good faith takes it free of any security interest therein that extends to it under clause (1) (b) even though it is perfected under subsection (2) unless the secured party has registered a financing change statement that sets out the vehicle identification number in the designated place. R.S.O. 1990, c. P.10, s. 25 (5).

2 - 11

Fixtures 34. (1) A security interest in goods that attached, (a) before the goods became a fixture, has priority as to the fixture over the claim of any person who has an interest in the real property; or

(b) after the goods became a fixture, has priority as to the fixture over the claim of any person who subsequently acquired an interest in the real property, but not over any person who had a registered interest in the real property at the time the security interest in the goods attached and who has not consented in writing to the security interest or disclaimed an interest in the fixture.

Exceptions (2) A security interest mentioned in subsection (1) is subordinate to the interest of, (a) a subsequent purchaser for value of an interest in the real property; or

(b) a creditor with a prior encumbrance of record on the real property to the extent that the creditor makes subsequent advances,

if the subsequent purchase or subsequent advance under a prior encumbrance of record is made or contracted for without knowledge of the security interest and before notice of it is registered in accordance with section 54.

Removal of collateral (3) If a secured party has an interest in a fixture that has priority over the claim of a person having an interest in the real property, the secured party may, on default and subject to the provisions of this Act respecting default, remove the fixture from the real property if, unless otherwise agreed, the secured party reimburses any encumbrancer or owner of the real property who is not the debtor for the cost of repairing any physical injury but excluding diminution in the value of the real property caused by the absence of the fixture or by the necessity for replacement.

2 - 12

Notice in land registry office 54. (1) A notice of security interest, in the required form, may be registered in the proper land registry office, where, (a) the collateral is or includes fixtures or goods that may become fixtures or crops, or minerals or hydrocarbons to be extracted, or timber to be cut; or

(b) the security interest is a security interest in a right to payment under a lease, mortgage or charge of real property to which this Act applies. R.S.O. 1990, c. P.10, s. 54 (1); 1998, c. 18, Sched. E, s. 198 (1).

Consumer goods, registration period (2) Where the collateral is consumer goods, a notice registered under clause (1) (a) or an extension notice registered under subsection (3), as the case may be, shall set out an expiration date, and the notice or extension notice is effective until the end of the expiration date. 2015, c. 20, Sched. 35, s. 2. Idem (3) A registration to which subsection (2) applies may be extended before the end of the registration period by the registration of an extension notice. R.S.O. 1990, c. P.10, s. 54 (2, 3).

Discharge (4) A notice registered under subsection (1) may be discharged or partially discharged by a certificate in the required form and the certificate may be registered in the proper land registry office. R.S.O. 1990, c. P.10, s. 54 (4); 1998, c. 18, Sched. E, s. 198 (2). Effect of registration (5) Where a notice has been registered under subsection (1), every person dealing with the collateral shall be deemed for the purposes of subsection 34 (2) to have knowledge of the security interest. Loss of claim (6) Where the collateral is consumer goods and the expiration date set out in a notice registered under clause (1) (a) has passed and an extension notice has not been registered or has expired, the land described in the notice is not affected by any claim under the notice but this subsection does not prevent the registration of a new notice under clause (1) (a). R.S.O. 1990, c. P.10, s. 54 (5, 6).

2 - 13

Discharge or amendment

Discharge where security interest existed 56. (1) Where a financing statement or notice of security interest is registered under this Act, and, (a) all the obligations under a security agreement to which it relates have been performed; or

(b) it is agreed to release part of the collateral covered by a security agreement to which it relates upon payment or performance of certain of the obligations under the security agreement, then upon payment or performance of such obligations,

any person having an interest in the collateral covered by the security agreement may deliver a written notice to the secured party demanding registration of a financing change statement referred to in section 55 or a certificate of discharge or partial discharge referred to in subsection 54 (4), or both, and the secured party shall register the financing change statement or the certificate of discharge or partial discharge, or both, as the case may be. R.S.O. 1990, c. P.10, s. 56 (1); 2006, c. 34, Sched. E, s. 18 (1).

Discharge where no security interest acquired (2) Where a financing statement or notice of security interest is registered under this Act and the person named in the financing statement or notice as the secured party has not acquired a security interest in the property to which the financing statement or notice relates, any person having an interest in the property may deliver a written notice to the person named as the secured party demanding registration of a financing change statement referred to in section 55 or a certificate of discharge referred to in subsection 54 (4), or both, and the person named as the secured party shall register the financing change statement or the certificate of discharge, or both, as the case may be. R.S.O. 1990, c. P.10, s. 56 (2); 2006, c. 34, Sched. E, s. 18 (2). Amendment (2.1) If a financing statement is registered under this Act and the collateral description or collateral classification in the financing statement includes personal property that is not collateral under the security agreement, the person named in the financing statement as the debtor may deliver a written notice to the person named as the secured party demanding registration of a financing change statement referred to in section 49 to provide an accurate collateral description, and the person named as the secured party shall register the financing change statement. 2006, c. 34, Sched. E, s. 18 (3). Removal of collateral classifications (2.2) If a financing statement is registered under this Act and the person named in the financing statement as the secured party has not acquired a security interest in any property within one or more of the collateral classifications indicated on the financing statement, the person named in the financing statement as the debtor may deliver a written notice to the person named as the secured party demanding registration of a financing change statement referred to in section 49 to correct the collateral

2 - 14

classifications by removing any collateral classification in which the person named as the secured party has not acquired a security interest, and the person named as the secured party shall register the financing change statement. 2010, c. 16, Sched. 5, s. 4 (4). Limiting collateral classification (2.3) If a financing statement is registered under this Act and the person named in the financing statement as the secured party has not included words limiting the scope of the collateral classification within the meaning of subsection 46 (2.1) and has acquired a security interest only in particular property within the classification, the person named in the financing statement as the debtor may deliver a written notice to the person named as the secured party demanding registration of a financing change statement referred to in section 49 to add words limiting the scope of the collateral classification, and the person named as the secured party shall register the financing change statement. 2010, c. 16, Sched. 5, s. 4 (4). (2.4) Repealed: 2006, c. 34, Sched. E, s. 18 (3).

Definition (3) For the purposes of subsections (4) and (5), “secured party” includes a person named in a financing statement or notice of security interest as the secured party to whom subsection (2) applies. R.S.O. 1990, c. P.10, s. 56 (3).

Failure to deliver (4) Where the secured party, without reasonable excuse, fails to register the financing change statement, or certificate of discharge or partial discharge, or all of them, as the case may be, required under subsection (1), (2), (2.1), (2.2) or (2.3) within 10 days after receiving a demand for it, the secured party shall pay $500 to the person making the demand and any damages resulting from the failure; the sum and damages are recoverable in any court of competent jurisdiction. 2006, c. 34, Sched. E, s. 18 (4); 2010, c. 16, Sched. 5, s. 4 (5). Security or payment into court (5) Upon application to the Superior Court of Justice, the court may, (a) allow security for or payment into court of the amount claimed by the secured party and such costs as the court may fix, and thereupon order the secured party to discharge or partially discharge, as the case may be, the registration of the financing statement or notice of security interest; or

(b) order upon any ground that the court considers proper that,

(i) the registrar amend the information recorded in the central file of the registration system to indicate that the registration of the financing statement has been discharged or partially discharged, as the case may be, or

2 - 15

(ii) the land registrar delete any entry in the books of the land registry office related to the notice of security interest or that the land registrar amend the books of the land registry office to indicate that the security interest has been discharged or partially discharged, as the case may be. R.S.O. 1990, c. P.10, s. 56 (5); 2000, c. 26, Sched. B, s. 16 (1).

Successors in interest (6) Where the person receiving a notice under clause (1) (a) did not have a security interest in the collateral immediately before all the obligations under the security agreement to which it relates were performed, the person shall, within fifteen days after receiving the notice, disclose the name and address of the latest successor in interest known to the person, and, if without reasonable excuse, the person fails to do so or the answer is incomplete or incorrect, the person shall pay $500 to the person making the demand and any damages resulting from the failure which sum and damages are recoverable in any court of competent jurisdiction. R.S.O. 1990, c. P.10, s. 56 (6).

No outstanding secured obligation (7) Where there is no outstanding secured obligation, and the secured party is not committed to make advances, incur obligations or otherwise give value, a secured party having control of investment property under clause 25 (1) (b) of the Securities Transfer Act, 2006 or subclause 1 (2) (d) (ii) of this Act shall, within 10 days after receipt of a written demand by the debtor, send to the securities intermediary or futures intermediary with which the security entitlement or futures contract is maintained a written record that releases the securities intermediary or futures intermediary from any further obligation to comply with entitlement orders or directions originated by the secured party. 2006, c. 8, s. 139.

2 - 16

Land Titles Act, R.S.O. 1990, c. L.5

Protection of unregistered estates 71. (1) Any person entitled to or interested in any unregistered estates, rights, interests or equities in registered land may protect the same from being impaired by any act of the registered owner by entering on the register such notices, cautions, inhibitions or other restrictions as are authorized by this Act or by the Director of Titles. R.S.O. 1990, c. L.5, s. 71 (1). Note: On a day to be named by proclamation of the Lieutenant Governor, subsection (1) is amended by striking out “of Titles”. See: 2012, c. 8, Sched. 28, ss. 45, 98.

Agreement of purchase and sale (1.1) An agreement of purchase and sale or an assignment of that agreement shall not be registered, but a person claiming an interest in registered land under that agreement may register a caution under this section on the terms specified by the Director of Titles. 1998, c. 18, Sched. E, s. 129. Note: On a day to be named by proclamation of the Lieutenant Governor, subsection (1.1) is amended by striking out “of Titles”. See: 2012, c. 8, Sched. 28, ss. 45, 98.

2 - 17

Effect of registration 99. (2) Where a notice, caution, inhibition or restriction is registered, every registered owner of the land and every person deriving title through the registered owner, excepting owners of encumbrances registered prior to the registration of such notice, caution, inhibition or restriction, shall be deemed to be affected with notice of any unregistered estate, right, interest or equity referred to therein. R.S.O. 1990, c. L.5, s. 71 (2). Note: A caution registered under section 71 or a predecessor of that section before June 16, 1999 ceases to have effect five years from June 16, 1999, if the date that the caution ceases to have effect is not specified in the caution or by subsection 128 (4) of this Act, as it read immediately before June 16, 1999, or if there is a date specified in the caution or by subsection 128 (4) of this Act, as it read immediately before June 16, 1999, the earlier of that date and five years from the date of registration of the caution. See: 1998, c. 18, Sched. E, s. 151 (2).

Effect of sale by chargee (2) Upon the registration of a transfer under subsection (1) and upon satisfactory evidence being produced, the land registrar may delete from the register the entry of an instrument or writ appearing to rank subsequent to the charge under which the land is sold, and thereupon the interest of every person claiming under such subsequent instrument or writ ceases to affect the land. R.S.O. 1990, c. L.5, s. 99 (2). Note: On a day to be named by proclamation of the Lieutenant Governor, subsection (2) is repealed and the following substituted:

Effect of sale by chargee (2) Upon the registration of a transfer under subsection (1) and upon evidence satisfactory to the Director being produced, the entry of an instrument or writ appearing to rank subsequent to the charge under which the land is sold may be deleted from the register and in that case the interest of every person claiming under the subsequent instrument or writ ceases to affect the land. 2012, c. 8, Sched. 28, s. 57 (2).

2 - 18

TAB 3

Collateral Mortgages

(including, but not limited to, mortgages

on collateral)

Simon Crawford Bennett Jones LLP

Nicholas Arrigo, Student-at-Law

Bennett Jones LLP

September 13, 2016

Practice Gems:

Mortgage Enforcement

ESSENTIALS 2016

Collateral Mortgages

(including, but not limited to, mortgages on collateral)

Simon Crawford, Partner, Bennett Jones LLP

Nicholas Arrigo, Student at Law, Bennett Jones LLP

I. What is a Collateral Mortgage?

Good question. There is the broad sense of the term and there is the technical sense of the term.

In common banking parlance, a collateral mortgage is one type of security document over so-

called collateral security, which The Court of Appeal in Royal Bank of Canada v Slack1 defined as

"any property which is assigned or pledged to secure the performance of an obligation and as

additional thereto, and which upon the performance of the obligation is to be surrendered or

discharged".

And, of course, this is where we want to make a distinction, because the use of the word

"collateral" is not, in our intended usage, referring to the asset (in the sense of the house charged

was collateral), but rather is referring to the security interest itself (in the sense that the charge

granted is collateral to something else).

Nor do we, in this paper, mean that a collateral mortgage means (only) an additional mortgage

given in support of a so-called "primary" mortgage, such as when one charges a second house as

additional credit support for the "primary" mortgage on one's main house. This is the usage

referred to in Falconbridge on Mortgages:

"Collateral security is a commercial rather than a legal term. It is a question of

construction in each case with particular reference to the course of dealings between the

parties, the type of transaction and the nature of the securities whether one mortgage is

to be resorted to first as the primary security or whether they are all to be considered as

parallel security."2

1 [1958] OR 262, 11 DLR (2d) 737. 2 Walter M. Traub, Falconbridge on Mortgages (Toronto: Thomson Reuters, April 2016), 1-11.

3 - 1

What we do mean, however, by the term "collateral mortgage", in the context of this discussion,

is any mortgage that is not a self-contained conventional mortgage. A self-contained

conventional mortgage is a mortgage that, within the four corners of the document, contains the

primary obligation to repay a debt, the terms of such repayment and the grant of the security

interest over the real estate as security therefor.

In contrast, therefore, in our usage, a collateral mortgage, is any mortgage which stands as

security for an obligation created outside of the mortgage, or for an obligation wherever or

howsoever created, that is a performance and not a payment obligation. So to get our heads in

the right space for this, a collateral mortgage may include but is not limited to:

(a) a mortgage delivered as security for the repayment of a grid promissory note;

(b) a mortgage delivered as security for the payment and performance of a

guarantee;

(c) a mortgage delivered as additional security for the primary debt borrowed under

another mortgage;

(d) a mortgage delivered as security for an indemnity; and

(e) a mortgage delivered to secure the performance of a transactional obligation,

such as an undertaking to perform environmental work or to hold the seller of a

property harmless under an assumed mortgage that it was not released under.

Stated simply, although there may be arguable exceptions, collateral mortgages are (generally

speaking), security documents only. Their purpose is to create a security interest in real estate to

support a primary obligation that (more often than not) is contained in another unregistered

instrument or contract. As a consequence, the obligations secured by a collateral mortgage can,

generally speaking, more easily be amended from time to time without affecting or amending

the mortgage itself.3

3 Daniel Kofman, "Collateral Mortgages and Revolving Loan Facilities: What Makes Collateral Mortgages Different?", Commercial Mortgage

Transactions 2013, p 2.

3 - 2

Although purists will no doubt balk at this, I am (again for the purposes of this discussion) also

going to lump in real property debentures in the collateral mortgage category, because they

satisfy my definition. While admittedly they secure both real and personal property, they are

invariably used (most often in the context of real estate bond issuances) only for the purposes of

creating a security interest in the property as security for obligations otherwise located.

When we think of mortgage enforcement or mortgage remedies, we don't generally think to

differentiate between conventional and collateral mortgages. More often, we think only of

ranking and priorities. But there are some concepts that we would do well to think of from time

to time as they are specific to collateral mortgages.

With that convoluted introduction behind us, let's consider our first collateral mortgage scenario

and issue.

II. Guarantees

A Co. borrows money from the bank and provides to the bank a conventional mortgage over its

office building. However, the bank is dissatisfied with the loan-to-value and so asks that A Co.'s

sister company, B Co. provide additional security over its manufacturing plant in support of the

loan. B Co. provides a mortgage over its manufacturing plant to the bank. You will note that I

have been intentionally cheeky and ambiguous about the nature of B Co.'s mortgage.

Questions that arise from this fact scenario are:

1. Is B Co.'s mortgage a collateral mortgage?

2. If it is a collateral mortgage, does B Co. have to provide a guarantee to the bank of A Co.'s

debt?

3. If it is not a collateral mortgage, does B Co. have to provide a guarantee to the bank of A

Co.’s debt?

4. Upon default, can the mortgagee enforce against the B Co.'s mortgage before enforcing

against A Co.'s mortgage?

3 - 3

(a) Is a guarantee necessary?

Our first question was, "is B Co.'s mortgage a collateral mortgage?", and the

answer to that very much depends on the drafting of both A Co.'s mortgage and

B Co.'s mortgage. Arguably, if B Co.'s mortgage states only that it is provided as

security for the debt incurred under A Co.'s mortgage, then it is quite clearly a

collateral mortgage. However, if B Co.'s mortgage is, on its face a conventional

mortgage that appears in all respects to be a "mirror" of the mortgage granted by

A Co., it may in fact be that what has been created is a "co-borrower" situation in

which both A Co. and B Co. have agreed to be primarily liable for the repayment

of the same debt and to satisfy that debt from the security of their respective

charged assets, if need be.

In the context of a co-borrower situation, there is little controversy over the

structure of the loan, as both mortgagors have not only created a charge, but have

promised to repay the primary debt as primary obligor. However, if B Co. has

created a collateral charge, then what is its relation to A Co., and what is the

nature of the debt secured?.

Obviously, the best answer would be if B Co. had delivered a written guarantee in

favour of the bank, guaranteeing the payment by A Co. of the debt created under

A Co.'s mortgage. But what if no such guarantee exists?

Steven Pearlstein has taken the position that a guarantee is not required.4 His

reasoning is that a collateral mortgage itself creates a surety relationship. To

support this, he points to a line of arguments found in the 1938 case Re Conley,5

in which Clauson LJ of the English Court of Appeal wrote that suretyship may be

based on a simple pledge deposited with a lender, and that a collateral mortgage,

viewed as a pledge of land deposited with the primary obligor's creditor, is

4 Steven I. Pearlstein, "Collateral Mortgages – Do you need a Guarantee?", 8th Annual Real Estate Law Summit 2011. 5 [1938] 2 All ER 127.

3 - 4

arguably analogous. Clauson LJ runs through the history of suretyship, tracing the

concept back to its inception as a pledge of property:

“… there is no reason to believe that in its inception the idea of suretyship

necessarily involved the idea of the surety making himself generally liable

in person and property for the satisfaction of the obligation he undertook.

His obligation in its inception seems to have been limited to the pledge

deposited or indicated. In the gradual development of suretyship, the

obligee, as one would expect, would call for a simpler and wider obligation

on the part of a surety – namely, the obligation to satisfy the principal debt

to the full by his person or property, without regard to the value of the

pledge or gage – and more and more the delivery or indication of a

particular piece of property as a pledge tended to become a form. If this

be a correct account of the development of the law of suretyship, it is quite

intelligible that the terms surety and guarantor should become associated

mainly with cases where the sanction for the obligation of the surety or

guarantor was not limited to the pledge, but consisted of the surety’s

liability to answer his obligation in person or in any property available for

execution.”

So we might reason that, if suretyship exists by virtue of delivery as a pledge of

property for the obligations of another, it includes a charge of property likewise

delivered.

But what if Steven is wrong (sorry Steven, I'm just saying "what if"…)? Generally

speaking, you have to have an obligation to a third party in order for that third

party to be able to enforce a security interest against you. So in the absence of the

surety "at law" argument, a guarantee is required in order for the collateral

mortgage to be enforceable…..a written guarantee. Guarantees are part of a

3 - 5

special class of deeds and contracts subject to the Statute of Frauds,6 which

provides as follows:

Writing required for certain contracts

4. No action shall be brought to charge any executor or administrator

upon any special promise to answer damages out of the executor's or

administrator's own estate, or to charge any person upon any special

promise to answer for the debt, default or miscarriage of any other person,

or to charge any person upon any contract or sale of lands, tenements or

hereditaments, or any interest in or concerning them, unless the

agreement upon which the action is brought, or some memorandum or

note thereof is in writing and signed by the party to be charged therewith

or some person thereunto lawfully authorized by the party.

While there is no common law requirement that a guarantee be evidenced in

writing, Section 4 of the Statute of Frauds imposes a formal requirement that

either a guarantee itself, or some memorandum or note thereof, be evidenced in

writing.7 The application of the Statute of Frauds turns on whether the agreement

(or such portion of the agreement at issue) gives rise to a primary obligation or

rather a "special" secondary or collateral obligation that constitutes a guarantee.

In short, every agreement which is a guarantee in substance must comply with the

Statute of Frauds in form and, while the Statute of Frauds does not require that

any particular form be adhered to, the essential elements of the agreement

generally must be in writing.8

As an aside, the law of guarantee does not require that consideration given by the

creditor benefit the guarantor directly. As Kevin McGuinness notes, "the

6 R.S.O. 1990, c. S. 19 (the "Statute of Frauds"). 7While there are a number of situations in which the requirement for written evidence may be dispensed with, the starting point of the analysis is

that such written evidence is required. 8 A. MacDonald & Co. v. Fletcher, [1915] 22 BCR 298.

3 - 6

consideration given by the creditor is to act in accordance with the request of the

guarantor in respect of the principal".9

That's all well and good, but in the context of collateral mortgages, it is not a bad

idea to always ensure that the consideration flowing to B Co (the second entity

providing the additional security by way of collateral mortgage) is sufficient. It is a

contract, after all.

The consideration for a guarantee may take the form of a benefit flowing from

lender directly to the guarantor, and oftentimes guarantees (as well as other

contracts) will include a statement to the effect that some nominal payment has

been exchanged which, together with other "good and valuable consideration",

constitutes sufficient consideration. More often than not (or dare I say, nearly

always) the nominal consideration never actually changes hands and so, if the

nominal consideration is all you've got (or rather, purport to have), you may find

yourself a few peppercorns shy of an enforceable bargain. Furthermore, while

courts will generally not inquire as to the adequacy of consideration, some courts

have recognized a distinction between "nominal consideration" and "valuable

consideration" and have held that, notwithstanding the freedom of parties to

make bad bargains, nominal consideration which is not "real" consideration of

some value in the eyes of the law does not constitute sufficient consideration.10

In most instances the reference to nominal consideration is simply boilerplate

language that does not reflect the actual consideration changing hands, and the

presence of such boilerplate language certainly does not render a guarantee

unenforceable: the consideration for a guarantee need not be set out in writing,11

nor is it necessary that consideration flow to the guarantor,12 as the consideration

9 Kevin McGuinness, The Law of Guarantee, 3rd ed (Markham, ON: LexisNexis, 2013), p 161. 10 See, for example, Glenelg Homestead Ltd v Wile, 2003 NSSC 155 (CanLII) at para. 26. 11 Statute of Frauds, at s. 6. 12 Canada Mortgage and Housing Corp. v. Elbarbari, 1996 CanLII 6712 (SK QB) per MacLean, J.

3 - 7

may simply be the lender suffering some detriment or providing some benefit to

a third party, such as the granting of credit by the lender to the borrower.

However, a potential issue arises where a guarantee (and associated collateral

mortgage) are provided in circumstances where a borrower has defaulted or is on

the brink of default under an existing loan. The potential issue is that, while it is

generally sufficient that the lender has granted some specific type forbearance in

consideration for a guarantee and/or collateral mortgage, for example refraining

from commencing legal proceedings against the borrower or granting an

extension for repayment of the underling debt, mere voluntary inaction on the

part of the lender does not constitute sufficient consideration.13

So what's to be made of all of this? Although a collateral mortgage need not

explicitly describe the consideration for which it is granted, it is prudent to