Introduction to Agribusiness IAFNR Agribusiness ModuleIAFNR Agribusiness Module.

We recently revised our GDP forecasts and now expect flat growth in 2017 and 2.0% growth in 2018. Although

GDP growth reached 1% q/q in the first quarter, this was mostly driven by the agricultural sector, and both

manufacturing and the services sector remain sluggish. We forecast that GDP will contract by about 0.3% in the

second quarter, which if confirmed will likely raise questions about the performance of the economy in 2H17.

The outlook on Brazil’s sovereign credit rating was lowered to negative last month, with negative implications for

the BRL. However, FX intervention by the Central Bank, strong FX flows and a favorable external environment

helped offset the adverse domestic backdrop. We revised our YE exchange-rate forecasts from BRL/USD 3.10

to BRL/USD 3.20 in 2017 and from BRL/USD 3.25 to BRL/USD 3.30 in 2018. We also lowered our consumer

inflation forecasts to 3.4% in 2017 and 4% in 2018. Disinflation, meanwhile, will allow the Central Bank to

continue to cut the Selic policy rate, which we forecast will end the year at 8%, providing some support for the

BRL going forward.

While the U.S. and Chinese growth forecasts dipped slightly last month, the outlook for Europe has improved

marginally. Going forward, we see some asymmetric risks for additional slowdown of activity, albeit spread over

a longer horizon. Combined with improved inflation dynamics, this deceleration would slow the downward bias

for global liquidity, as the world’s leading economies are likely to keep their expansionary policies for a longer

period.

June 2017 Macroeconomic Research Department

Macroeconomic Outlook

MONTHLY AGRIBUSINESS BRAZIL MONTHLY AGRIBUSINESS BRAZIL

Executive Summary

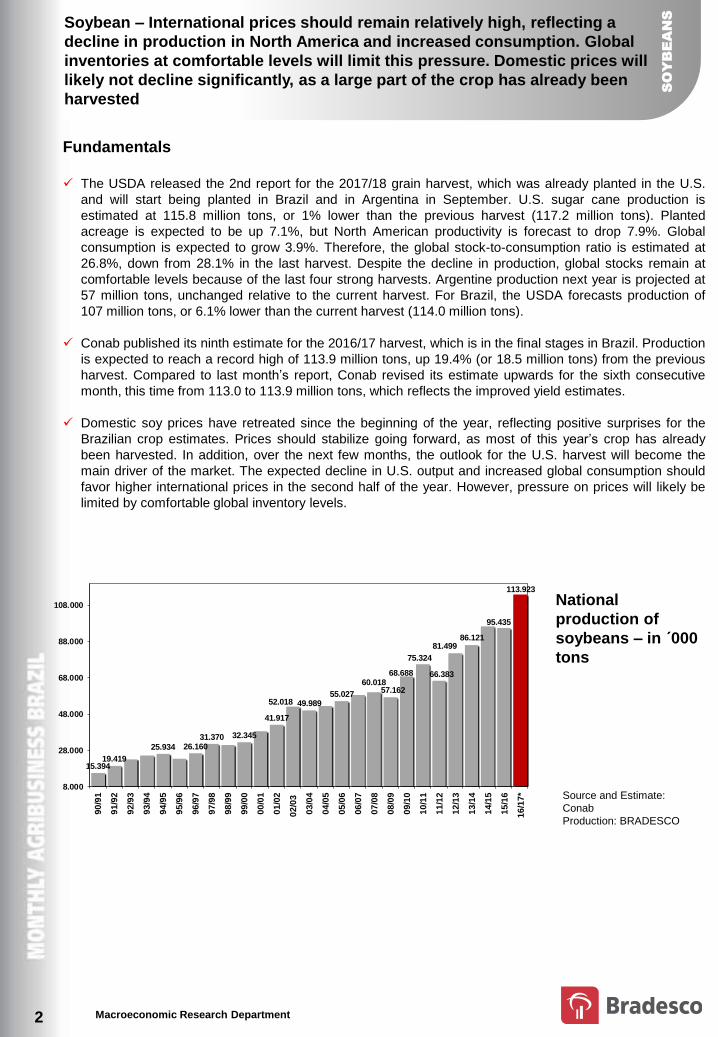

Soybeans – International prices should remain relatively high, reflecting a decline in production in North

America and increased consumption. Global inventories at comfortable levels will limit this pressure. Domestic

prices will likely not decline significantly, as a large part of the crop has already been harvested.

Corn – International prices continue rising in a controlled manner, due to the weaker harvest. Although lower

than the last harvest, comfortable inventory levels will limit this high. Domestic prices could drop further, as a

record Brazilian harvest moves into full swing and the second harvest intensifies in June.

Coffee – International prices should remain moderately high in the coming months, reflecting the reduced ratio

between inventories and global consumption and the Brazilian crop’s “off” year in the biennial production cycle.

Domestic prices will remain high due to the smaller Brazilian crop.

Cattle – Cattle prices will remain at low levels, reflecting the combination of low domestic demand, low export

volumes and increased numbers of animals ready for slaughter, which considers the retention of cows in recent

years.

Sugar and Ethanol – As a result of the global production surplus, international sugar prices should continue at

low levels, without any tendency to rise. Due to a lower ethanol production forecast, the prices should rise, but

the high will be limited by a drop in petroleum and consequent gas prices, and by ethanol import volumes.

Macroeconomic Research Department

15.39419.419

25.934 26.16031.370 32.345

41.917

52.018 49.98955.027

60.01857.162

68.688

75.324

66.383

81.49986.121

95.435

113.923

8.000

28.000

48.000

68.000

88.000

108.000

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

*

em mil toneladasFonte e Projeção: CONAB

Elaboração: BradescoProdução Nacional de Soja 1990 - 2012

2

SO

YB

EA

NS

Soybean – International prices should remain relatively high, reflecting a

decline in production in North America and increased consumption. Global

inventories at comfortable levels will limit this pressure. Domestic prices will

likely not decline significantly, as a large part of the crop has already been

harvested

Fundamentals

The USDA released the 2nd report for the 2017/18 grain harvest, which was already planted in the U.S.

and will start being planted in Brazil and in Argentina in September. U.S. sugar cane production is

estimated at 115.8 million tons, or 1% lower than the previous harvest (117.2 million tons). Planted

acreage is expected to be up 7.1%, but North American productivity is forecast to drop 7.9%. Global

consumption is expected to grow 3.9%. Therefore, the global stock-to-consumption ratio is estimated at

26.8%, down from 28.1% in the last harvest. Despite the decline in production, global stocks remain at

comfortable levels because of the last four strong harvests. Argentine production next year is projected at

57 million tons, unchanged relative to the current harvest. For Brazil, the USDA forecasts production of

107 million tons, or 6.1% lower than the current harvest (114.0 million tons).

Conab published its ninth estimate for the 2016/17 harvest, which is in the final stages in Brazil. Production

is expected to reach a record high of 113.9 million tons, up 19.4% (or 18.5 million tons) from the previous

harvest. Compared to last month’s report, Conab revised its estimate upwards for the sixth consecutive

month, this time from 113.0 to 113.9 million tons, which reflects the improved yield estimates.

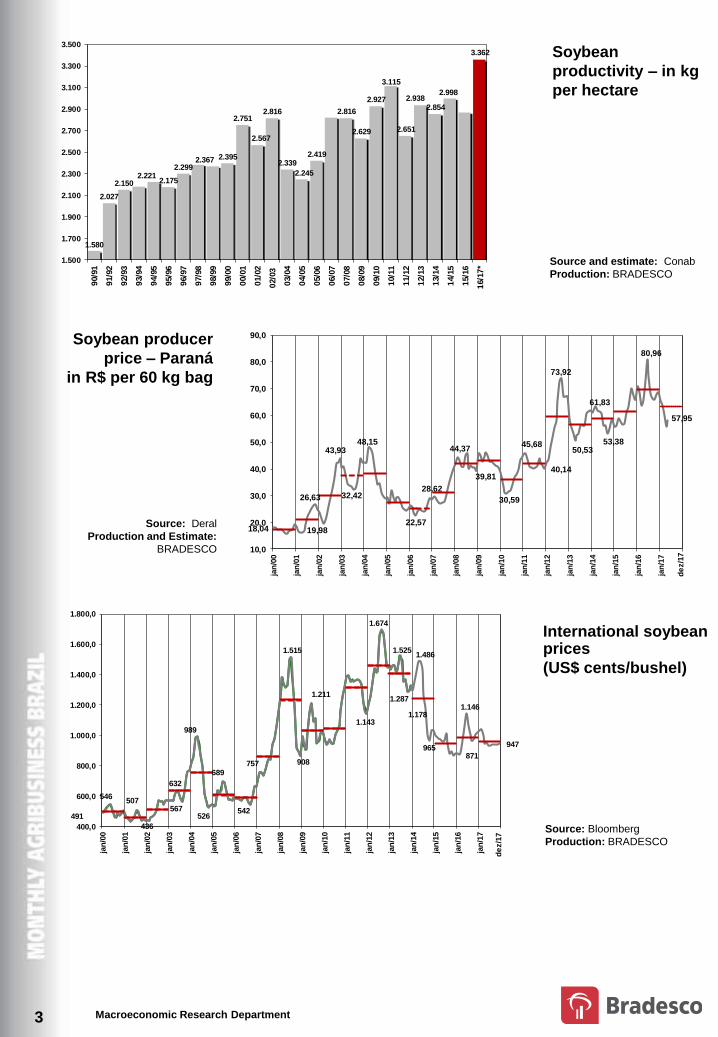

Domestic soy prices have retreated since the beginning of the year, reflecting positive surprises for the

Brazilian crop estimates. Prices should stabilize going forward, as most of this year’s crop has already

been harvested. In addition, over the next few months, the outlook for the U.S. harvest will become the

main driver of the market. The expected decline in U.S. output and increased global consumption should

favor higher international prices in the second half of the year. However, pressure on prices will likely be

limited by comfortable global inventory levels.

Source and Estimate:

Conab

Production: BRADESCO

National

production of

soybeans – in ´000

tons

Macroeconomic Research Department

18,04

26,63

19,98

43,93

32,42

48,15

22,57

28,62

44,37

39,81

30,59

45,68

40,14

73,92

50,53

61,83

53,38

80,96

57,95

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

SOJA EM GRÃO PREÇO AO PRODUTOR - PRAÇA PR

em R$ por saca de 60 kg Fonte: Deral PR Elaboração e Projeção: Bradesco

de

z/1

7

3

Source: Deral

Production and Estimate:

BRADESCO

Soybean producer

price – Paraná

in R$ per 60 kg bag

Source: Bloomberg

Production: BRADESCO

International soybean prices

(US$ cents/bushel)

491

546507

436

632

567

989

526

689

542

757

1.515

908

1.211

1.143

1.674

1.525

1.287

1.486

1.178

965871

1.146

947

400,0

600,0

800,0

1.000,0

1.200,0

1.400,0

1.600,0

1.800,0

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

PREÇOS INTERNACIONAIS DE SOJA - BOLSA DE CHICAGO - CBOT PREÇO FUTURO 1º VENCTO 2000 - 2010

em US$ cents por bushel

em US$ cents por bushel

Fonte: Bloomberg Elaboração: Bradesco•Projeção de preço: média dos preços futuros

de

z/1

7

Soybean

productivity – in kg

per hectare

Source and estimate: Conab

Production: BRADESCO

1.580

2.027

2.1502.221

2.175

2.2992.367 2.395

2.751

2.567

2.816

2.339

2.245

2.419

2.816

2.629

2.927

3.115

2.651

2.9382.854

2.998

3.362

1.500

1.700

1.900

2.100

2.300

2.500

2.700

2.900

3.100

3.300

3.500

90/9

1

91/9

2

92/9

3

93/9

4

94/9

5

95/9

6

96/9

7

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

09/1

0

10/1

1

11/1

2

12/1

3

13/1

4

14/1

5

15/1

6

16/1

7*

em kg por ha Fonte e Projeção: Conab Elaboração: Bradesco Produtividade da lavoura de soja - 1990 - 2012

Macroeconomic Research Department

Fundamentals

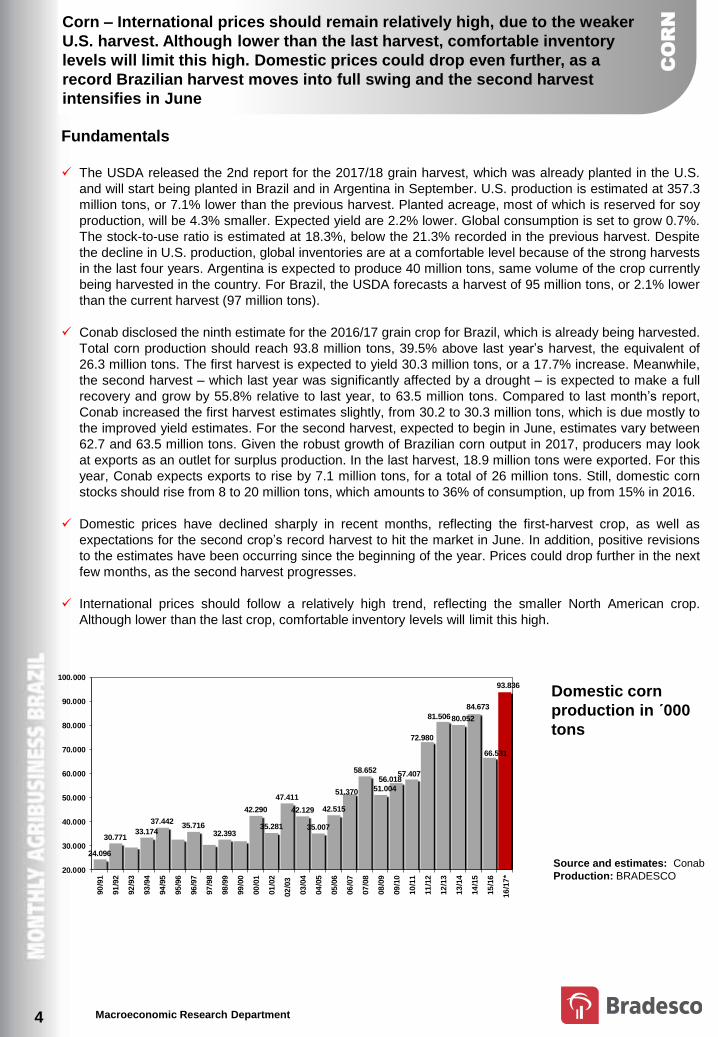

The USDA released the 2nd report for the 2017/18 grain harvest, which was already planted in the U.S.

and will start being planted in Brazil and in Argentina in September. U.S. production is estimated at 357.3

million tons, or 7.1% lower than the previous harvest. Planted acreage, most of which is reserved for soy

production, will be 4.3% smaller. Expected yield are 2.2% lower. Global consumption is set to grow 0.7%.

The stock-to-use ratio is estimated at 18.3%, below the 21.3% recorded in the previous harvest. Despite

the decline in U.S. production, global inventories are at a comfortable level because of the strong harvests

in the last four years. Argentina is expected to produce 40 million tons, same volume of the crop currently

being harvested in the country. For Brazil, the USDA forecasts a harvest of 95 million tons, or 2.1% lower

than the current harvest (97 million tons).

Conab disclosed the ninth estimate for the 2016/17 grain crop for Brazil, which is already being harvested.

Total corn production should reach 93.8 million tons, 39.5% above last year’s harvest, the equivalent of

26.3 million tons. The first harvest is expected to yield 30.3 million tons, or a 17.7% increase. Meanwhile,

the second harvest – which last year was significantly affected by a drought – is expected to make a full

recovery and grow by 55.8% relative to last year, to 63.5 million tons. Compared to last month’s report,

Conab increased the first harvest estimates slightly, from 30.2 to 30.3 million tons, which is due mostly to

the improved yield estimates. For the second harvest, expected to begin in June, estimates vary between

62.7 and 63.5 million tons. Given the robust growth of Brazilian corn output in 2017, producers may look

at exports as an outlet for surplus production. In the last harvest, 18.9 million tons were exported. For this

year, Conab expects exports to rise by 7.1 million tons, for a total of 26 million tons. Still, domestic corn

stocks should rise from 8 to 20 million tons, which amounts to 36% of consumption, up from 15% in 2016.

Domestic prices have declined sharply in recent months, reflecting the first-harvest crop, as well as

expectations for the second crop’s record harvest to hit the market in June. In addition, positive revisions

to the estimates have been occurring since the beginning of the year. Prices could drop further in the next

few months, as the second harvest progresses.

International prices should follow a relatively high trend, reflecting the smaller North American crop.

Although lower than the last crop, comfortable inventory levels will limit this high.

24.096

30.77133.174

37.44235.716

32.393

42.290

35.281

47.411

42.129

35.007

42.515

51.370

58.652

51.004

56.01857.407

72.980

81.50680.052

84.673

66.531

93.836

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

100.000

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

*

em mil toneladas Fonte e Projeção: ConabProdução Nacional de Milho - 1991 - 2012

4

CO

RN

Corn – International prices should remain relatively high, due to the weaker

U.S. harvest. Although lower than the last harvest, comfortable inventory

levels will limit this high. Domestic prices could drop even further, as a

record Brazilian harvest moves into full swing and the second harvest

intensifies in June

Source and estimates: Conab

Production: BRADESCO

Domestic corn

production in ´000

tons

Macroeconomic Research Department 5

Corn productivity

– in kg per hectare

Source and estimate: Conab

Production: BRADESCO

Source: Deral

Production and Estimate:

BRADESCO

Corn producer price

– Paraná

in R$ per 60 kg bag

Source: Bloomberg

Production: BRADESCO

International Corn prices

(US$ cents/bushel)

217

235

267

215

316

237

413

326

493

711

418

322

347

546

753

603

763

662

439

502

335

410

323

396

160

260

360

460

560

660

760

860

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

Milho - Bolsa de Chicago - CBOTPreço futuro 1º vencimento

Em US$ cents por bushelFonte: Bloomberg Elaboração e Projeção: Bradesco

de

z/1

711,95

7,05

11,40

22,28

18,96

16,26

10,44

14,14

24,94

13,07

26,92

17,26

23,29

19,17

24,34

39,98

20,77

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

Preço pago ao produtor de milho - Paraná Fonte: DeralElaboração e Projeção:

Em R$ por saca de 60 kg Fonte: DeralElaboração e Projeção: Bradesco

Em R$ por saca de 60 kg

1.791

2.1942.3492.344

2.622

2.356

2.5882.6502.5892.480

3.260

2.864

3.585

3.296

2.867

3.279

3.655

3.972

3.599

4.3114.158

4.808

5.1495.057

5.396

4.178

5.409

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

5.500

6.000

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

*

em kg por ha Produtividade - Milho - 1991 - 2012

Macroeconomic Research Department

Fundamentals

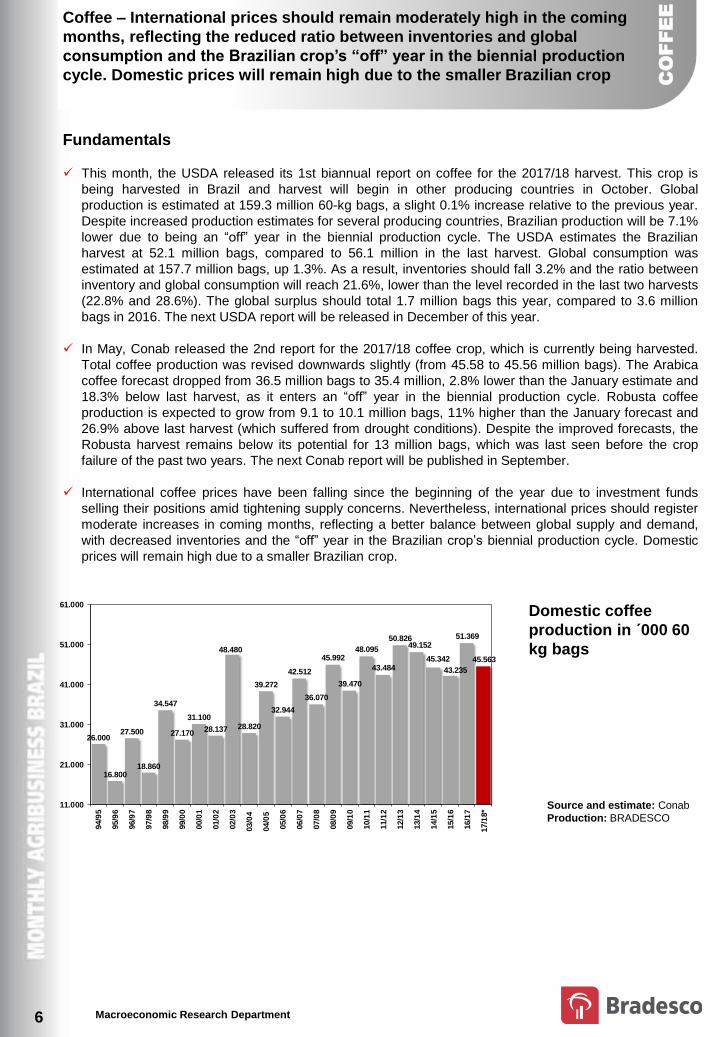

This month, the USDA released its 1st biannual report on coffee for the 2017/18 harvest. This crop is

being harvested in Brazil and harvest will begin in other producing countries in October. Global

production is estimated at 159.3 million 60-kg bags, a slight 0.1% increase relative to the previous year.

Despite increased production estimates for several producing countries, Brazilian production will be 7.1%

lower due to being an “off” year in the biennial production cycle. The USDA estimates the Brazilian

harvest at 52.1 million bags, compared to 56.1 million in the last harvest. Global consumption was

estimated at 157.7 million bags, up 1.3%. As a result, inventories should fall 3.2% and the ratio between

inventory and global consumption will reach 21.6%, lower than the level recorded in the last two harvests

(22.8% and 28.6%). The global surplus should total 1.7 million bags this year, compared to 3.6 million

bags in 2016. The next USDA report will be released in December of this year.

In May, Conab released the 2nd report for the 2017/18 coffee crop, which is currently being harvested.

Total coffee production was revised downwards slightly (from 45.58 to 45.56 million bags). The Arabica

coffee forecast dropped from 36.5 million bags to 35.4 million, 2.8% lower than the January estimate and

18.3% below last harvest, as it enters an “off” year in the biennial production cycle. Robusta coffee

production is expected to grow from 9.1 to 10.1 million bags, 11% higher than the January forecast and

26.9% above last harvest (which suffered from drought conditions). Despite the improved forecasts, the

Robusta harvest remains below its potential for 13 million bags, which was last seen before the crop

failure of the past two years. The next Conab report will be published in September.

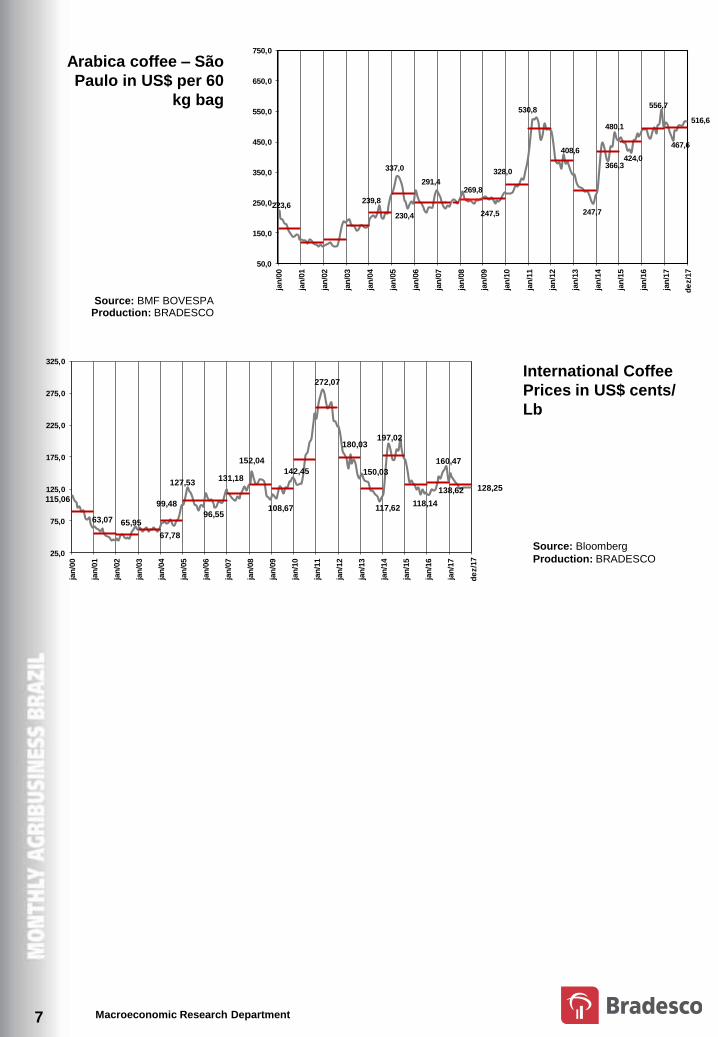

International coffee prices have been falling since the beginning of the year due to investment funds

selling their positions amid tightening supply concerns. Nevertheless, international prices should register

moderate increases in coming months, reflecting a better balance between global supply and demand,

with decreased inventories and the “off” year in the Brazilian crop’s biennial production cycle. Domestic

prices will remain high due to a smaller Brazilian crop.

6

CO

FF

EE

Domestic coffee

production in ´000 60

kg bags

Source and estimate: Conab

Production: BRADESCO

26.000

16.800

27.500

18.860

34.547

27.170

31.100

28.137

48.480

28.820

39.272

32.944

42.512

36.070

45.992

39.470

48.095

43.484

50.82649.152

45.342

43.235

51.369

45.563

11.000

21.000

31.000

41.000

51.000

61.000

94/9

5

95/9

6

96/9

7

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

09/1

0

10/1

1

11/1

2

12/1

3

13/1

4

14/1

5

15/1

6

16/1

7

17/1

8*

Fonte e projeção (*): Conab Elaboração: BradescoProdução Nacional de Café - 1994 - 2012mil sacas de 60 kg

Coffee – International prices should remain moderately high in the coming

months, reflecting the reduced ratio between inventories and global

consumption and the Brazilian crop’s “off” year in the biennial production

cycle. Domestic prices will remain high due to the smaller Brazilian crop

Macroeconomic Research Department 7

Source: Bloomberg

Production: BRADESCO

International Coffee

Prices in US$ cents/

Lb

Source: BMF BOVESPA Production: BRADESCO

Arabica coffee – São

Paulo in US$ per 60

kg bag

115,06

63,07 65,95

67,78

99,48

127,53

96,55

131,18

152,04

108,67

142,45

272,07

180,03

150,03

117,62

197,02

118,14

160,47

138,62 128,25

25,0

75,0

125,0

175,0

225,0

275,0

325,0

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

Projeção de preço: média dos preços futuros Café em grão - Bolsa de Nova York - NYBOT2000 - 2010Em US$ cents por libra peso

Fonte: Bloomberg Elaboração:

de

z/1

7

223,6239,8

337,0

230,4

291,4269,8

247,5

328,0

530,8

408,6

247,7

366,3

480,1

424,0

556,7

467,6

516,6

50,0

150,0

250,0

350,0

450,0

550,0

650,0

750,0

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

Café Arábica - Preço ao Produtor - Praça São Paulo 2000 - 2012Em R$ por saca 60 kg Fonte: Cepea EsalqElaboração e Projeção: Bradesco

de

z/1

7

Macroeconomic Research Department 8

BE

EF

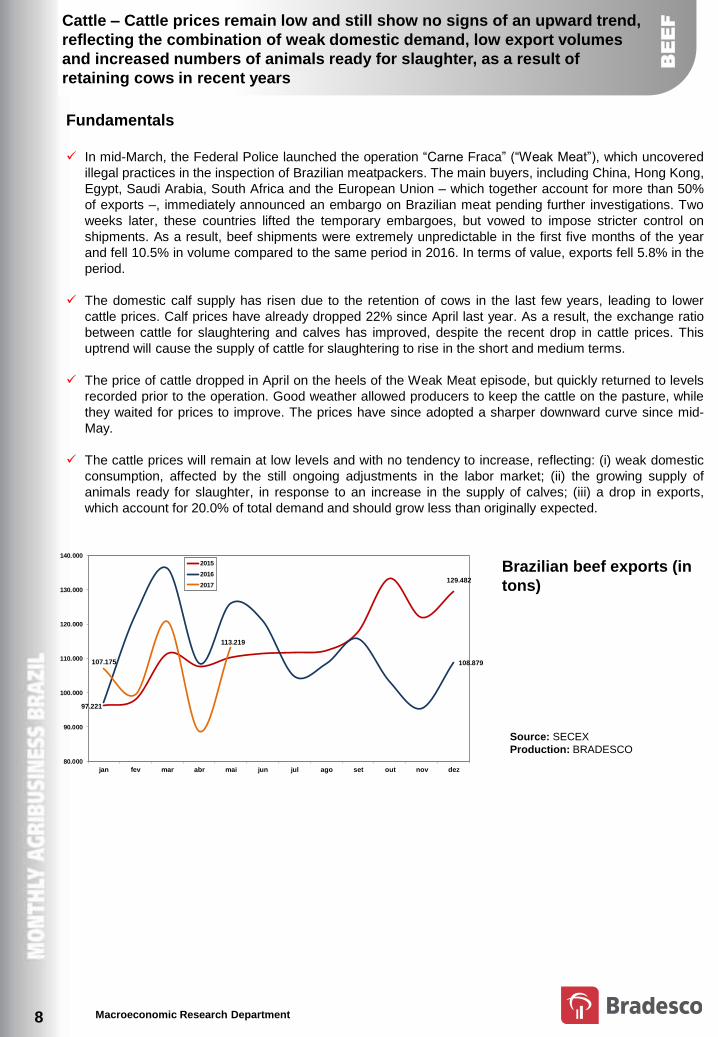

Brazilian beef exports (in

tons)

Source: SECEX

Production: BRADESCO

129.482

97.221

108.879107.175

113.219

80.000

90.000

100.000

110.000

120.000

130.000

140.000

jan fev mar abr mai jun jul ago set out nov dez

Exportações Brasileiras de carne bovina - 2010 - 2012 - Em toneladas Fonte: Secex Elaboração: Bradesco

2015

2016

2017

Cattle – Cattle prices remain low and still show no signs of an upward trend,

reflecting the combination of weak domestic demand, low export volumes

and increased numbers of animals ready for slaughter, as a result of

retaining cows in recent years

Fundamentals

In mid-March, the Federal Police launched the operation “Carne Fraca” (“Weak Meat”), which uncovered

illegal practices in the inspection of Brazilian meatpackers. The main buyers, including China, Hong Kong,

Egypt, Saudi Arabia, South Africa and the European Union – which together account for more than 50%

of exports –, immediately announced an embargo on Brazilian meat pending further investigations. Two

weeks later, these countries lifted the temporary embargoes, but vowed to impose stricter control on

shipments. As a result, beef shipments were extremely unpredictable in the first five months of the year

and fell 10.5% in volume compared to the same period in 2016. In terms of value, exports fell 5.8% in the

period.

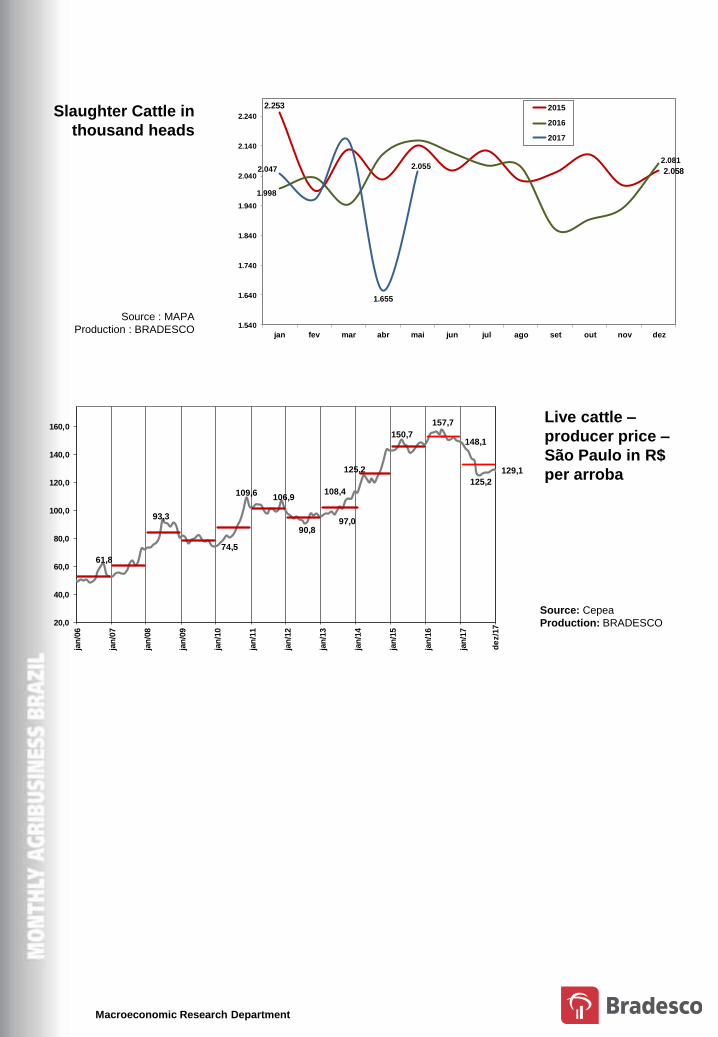

The domestic calf supply has risen due to the retention of cows in the last few years, leading to lower

cattle prices. Calf prices have already dropped 22% since April last year. As a result, the exchange ratio

between cattle for slaughtering and calves has improved, despite the recent drop in cattle prices. This

uptrend will cause the supply of cattle for slaughtering to rise in the short and medium terms.

The price of cattle dropped in April on the heels of the Weak Meat episode, but quickly returned to levels

recorded prior to the operation. Good weather allowed producers to keep the cattle on the pasture, while

they waited for prices to improve. The prices have since adopted a sharper downward curve since mid-

May.

The cattle prices will remain at low levels and with no tendency to increase, reflecting: (i) weak domestic

consumption, affected by the still ongoing adjustments in the labor market; (ii) the growing supply of

animals ready for slaughter, in response to an increase in the supply of calves; (iii) a drop in exports,

which account for 20.0% of total demand and should grow less than originally expected.

Macroeconomic Research Department

Live cattle –

producer price –

São Paulo in R$

per arroba

Source: Cepea

Production: BRADESCO

Slaughter Cattle in

thousand heads

Source : MAPA

Production : BRADESCO

2.253

2.058

1.998

2.0812.047

1.655

2.055

1.540

1.640

1.740

1.840

1.940

2.040

2.140

2.240

jan fev mar abr mai jun jul ago set out nov dez

Abates mensais de boi - 2010 - 2012 - Em toneladas Fonte: Secex Elaboração: Bradesco

2015

2016

2017

61,8

93,3

74,5

109,6106,9

90,897,0

108,4

125,2

150,7

157,7

148,1

125,2

129,1

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

BOI GORDO PREÇO AO PRODUTOR - PRAÇA SP

Em R$ por arroba (15 kg)Fonte: Cepea EsalqElaboração e Projeção: Bradesco

de

z/1

7

Macroeconomic Research Department

222.429240.944

287.810

314.969

257.592

320.650

359.316

431.413

474.800

559.432

604.514623.905

560.364

588.916

658.822

634.767657.184

647.626

150.000

250.000

350.000

450.000

550.000

650.000

90

/91

91

/92

92

/93

93

/94

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

17

/18

*

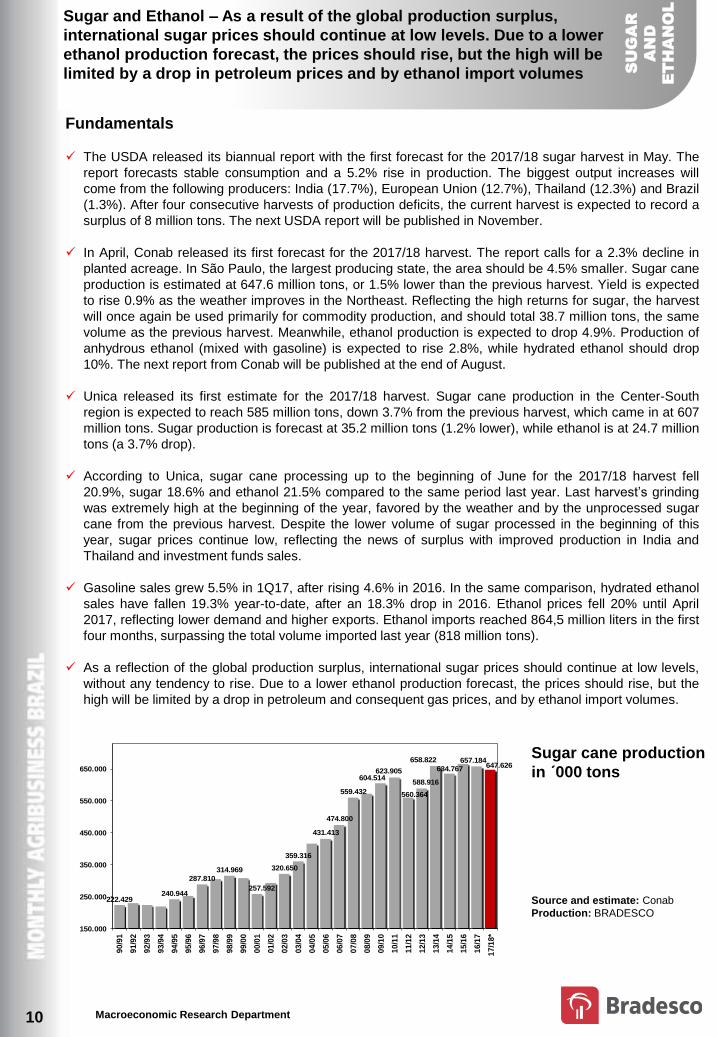

mil toneladasProdução Nacional de Cana-de-Açúcar - 1990 - 2013

Fonte e projeção : Conab Elaboração. Bradesco

Sugar cane production

in ´000 tons

Source and estimate: Conab

Production: BRADESCO

10

SU

GA

R

AN

D

ET

HA

NO

L

Sugar and Ethanol – As a result of the global production surplus,

international sugar prices should continue at low levels. Due to a lower

ethanol production forecast, the prices should rise, but the high will be

limited by a drop in petroleum prices and by ethanol import volumes

Fundamentals

The USDA released its biannual report with the first forecast for the 2017/18 sugar harvest in May. The

report forecasts stable consumption and a 5.2% rise in production. The biggest output increases will

come from the following producers: India (17.7%), European Union (12.7%), Thailand (12.3%) and Brazil

(1.3%). After four consecutive harvests of production deficits, the current harvest is expected to record a

surplus of 8 million tons. The next USDA report will be published in November.

In April, Conab released its first forecast for the 2017/18 harvest. The report calls for a 2.3% decline in

planted acreage. In São Paulo, the largest producing state, the area should be 4.5% smaller. Sugar cane

production is estimated at 647.6 million tons, or 1.5% lower than the previous harvest. Yield is expected

to rise 0.9% as the weather improves in the Northeast. Reflecting the high returns for sugar, the harvest

will once again be used primarily for commodity production, and should total 38.7 million tons, the same

volume as the previous harvest. Meanwhile, ethanol production is expected to drop 4.9%. Production of

anhydrous ethanol (mixed with gasoline) is expected to rise 2.8%, while hydrated ethanol should drop

10%. The next report from Conab will be published at the end of August.

Unica released its first estimate for the 2017/18 harvest. Sugar cane production in the Center-South

region is expected to reach 585 million tons, down 3.7% from the previous harvest, which came in at 607

million tons. Sugar production is forecast at 35.2 million tons (1.2% lower), while ethanol is at 24.7 million

tons (a 3.7% drop).

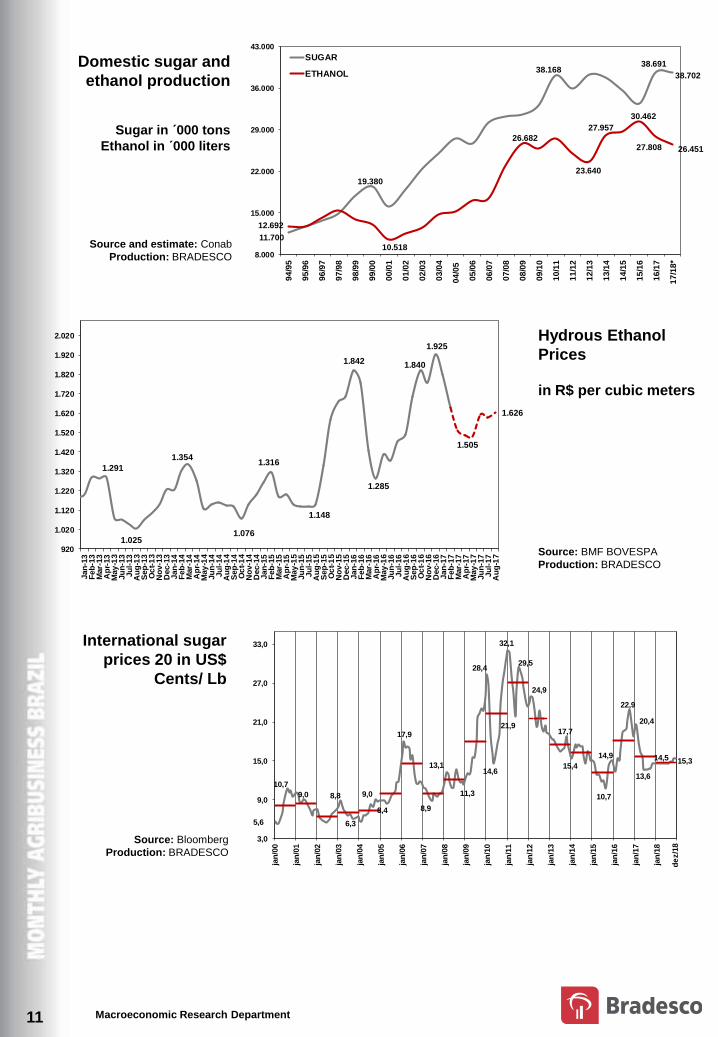

According to Unica, sugar cane processing up to the beginning of June for the 2017/18 harvest fell

20.9%, sugar 18.6% and ethanol 21.5% compared to the same period last year. Last harvest’s grinding

was extremely high at the beginning of the year, favored by the weather and by the unprocessed sugar

cane from the previous harvest. Despite the lower volume of sugar processed in the beginning of this

year, sugar prices continue low, reflecting the news of surplus with improved production in India and

Thailand and investment funds sales.

Gasoline sales grew 5.5% in 1Q17, after rising 4.6% in 2016. In the same comparison, hydrated ethanol

sales have fallen 19.3% year-to-date, after an 18.3% drop in 2016. Ethanol prices fell 20% until April

2017, reflecting lower demand and higher exports. Ethanol imports reached 864,5 million liters in the first

four months, surpassing the total volume imported last year (818 million tons).

As a reflection of the global production surplus, international sugar prices should continue at low levels,

without any tendency to rise. Due to a lower ethanol production forecast, the prices should rise, but the

high will be limited by a drop in petroleum and consequent gas prices, and by ethanol import volumes.

Macroeconomic Research Department

1.291

1.025

1.354

1.076

1.316

1.148

1.842

1.285

1.840

1.925

1.505

1.626

920

1.020

1.120

1.220

1.320

1.420

1.520

1.620

1.720

1.820

1.920

2.020

Jan

-13

Feb

-13

Mar-

13

Ap

r-13

May

-13

Ju

n-1

3Ju

l-13

Au

g-1

3S

ep

-13

Oc

t-1

3N

ov-1

3D

ec-1

3Jan

-14

Feb

-14

Mar-

14

Ap

r-14

May

-14

Ju

n-1

4Ju

l-14

Au

g-1

4S

ep

-14

Oc

t-1

4N

ov-1

4D

ec-1

4Jan

-15

Feb

-15

Mar-

15

Ap

r-15

May

-15

Ju

n-1

5Ju

l-15

Au

g-1

5S

ep

-15

Oc

t-1

5N

ov-1

5D

ec-1

5Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May

-16

Ju

n-1

6Ju

l-16

Au

g-1

6S

ep

-16

Oc

t-1

6N

ov-1

6D

ec-1

6Jan

-17

Feb

-17

Mar-

17

Ap

r-17

May

-17

Ju

n-1

7Ju

l-17

Au

g-1

7

em R$ por metro cúbico

11

Source: BMF BOVESPA

Production: BRADESCO

International sugar

prices 20 in US$

Cents/ Lb

Source: Bloomberg

Production: BRADESCO

Hydrous Ethanol

Prices

in R$ per cubic meters

5,6

10,7

9,0 8,8

6,3

9,0

8,4

17,9

8,9

13,1

11,3

28,4

14,6

32,1

21,9

29,5

24,9

17,7

15,4

10,7

14,9

22,9

20,4

13,6

14,5 15,3

3,0

9,0

15,0

21,0

27,0

33,0

jan

/00

jan

/01

jan

/02

jan

/03

jan

/04

jan

/05

jan

/06

jan

/07

jan

/08

jan

/09

jan

/10

jan

/11

jan

/12

jan

/13

jan

/14

jan

/15

jan

/16

jan

/17

jan

/18

Preços internacionais de açúcar – NYBOT – Preço futuro 1º Vencto 2000 – 2013Fonte: Bloomberg Elaboração: Bradesco

Em US$ cents por libra peso

de

z/1

8

Domestic sugar and

ethanol production

Sugar in ´000 tons

Ethanol in ´000 liters

Source and estimate: Conab

Production: BRADESCO

11.700

19.380

38.16838.691

38.702

12.692

10.518

26.682

23.640

27.957

30.462

27.808 26.451

8.000

15.000

22.000

29.000

36.000

43.000

94

/95

95

/96

96

/97

97

/98

98

/99

99

/00

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

17

/18

*

Açúcar em mil toneladasEtanol em mil litros

Fonte e (*) Projeção: Conab Elaboração: Bradesco

Produção nacional de açúcar e de etanol 1993 – 2013

SUGAR

ETHANOL

Macroeconomic Research Department 12

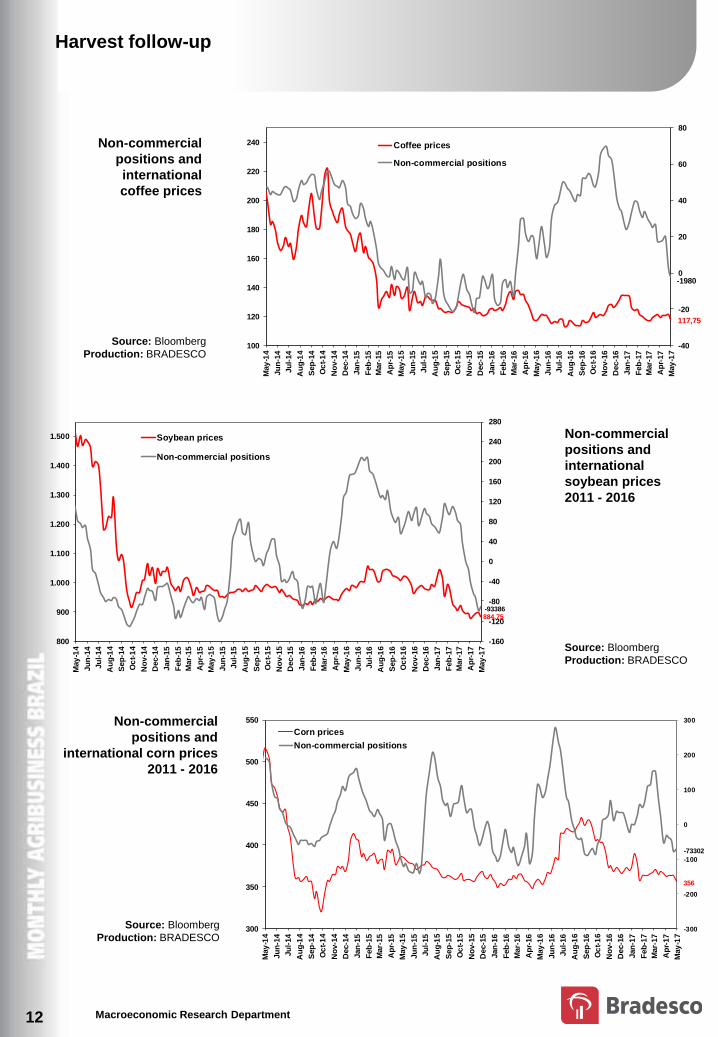

Harvest follow-up

Non-commercial

positions and

international

soybean prices

2011 - 2016

Non-commercial

positions and

international corn prices

2011 - 2016

Non-commercial

positions and

international

coffee prices

Source: Bloomberg

Production: BRADESCO

Source: Bloomberg

Production: BRADESCO

Source: Bloomberg

Production: BRADESCO

884,75-93386

-160

-120

-80

-40

0

40

80

120

160

200

240

280

800

900

1.000

1.100

1.200

1.300

1.400

1.500

May

-14

Ju

n-1

4

Ju

l-14

Au

g-1

4

Sep

-14

Oc

t-1

4

No

v-1

4

Dec-1

4

Jan

-15

Feb

-15

Mar-

15

Ap

r-15

May

-15

Ju

n-1

5

Ju

l-15

Au

g-1

5

Sep

-15

Oc

t-1

5

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May

-16

Ju

n-1

6

Ju

l-16

Au

g-1

6

Sep

-16

Oc

t-1

6

No

v-1

6

Dec-1

6

Jan

-17

Feb

-17

Mar-

17

Ap

r-17

May

-17

Soybean prices

Non-commercial positions

16-j

un

-

356

-73302

-300

-200

-100

0

100

200

300

300

350

400

450

500

550

May

-14

Ju

n-1

4

Ju

l-14

Au

g-1

4

Sep

-14

Oc

t-1

4

No

v-1

4

Dec-1

4

Jan

-15

Feb

-15

Mar-

15

Ap

r-15

May

-15

Ju

n-1

5

Ju

l-15

Au

g-1

5

Sep

-15

Oc

t-1

5

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May

-16

Ju

n-1

6

Ju

l-16

Au

g-1

6

Sep

-16

Oc

t-1

6

No

v-1

6

Dec-1

6

Jan

-17

Feb

-17

Mar-

17

Ap

r-17

May

-17

Corn prices

Non-commercial positions

117,75

-1980

-40

-20

0

20

40

60

80

100

120

140

160

180

200

220

240

May

-14

Ju

n-1

4

Ju

l-14

Au

g-1

4

Sep

-14

Oc

t-1

4

No

v-1

4

Dec-1

4

Jan

-15

Feb

-15

Mar-

15

Ap

r-15

May

-15

Ju

n-1

5

Ju

l-15

Au

g-1

5

Sep

-15

Oc

t-1

5

No

v-1

5

Dec-1

5

Jan

-16

Feb

-16

Mar-

16

Ap

r-16

May

-16

Ju

n-1

6

Ju

l-16

Au

g-1

6

Sep

-16

Oc

t-1

6

No

v-1

6

Dec-1

6

Jan

-17

Feb

-17

Mar-

17

Ap

r-17

May

-17

Posições Não Comerciais e Preços Internacionais de café - 2007 - 2014 - Fonte: Bloomberg Elaboração: Bradesco

Coffee prices

Non-commercial positions

Macroeconomic Research Department

SO

YB

EA

NS

Soybean Complex

Of soybean grain produced in Brazil, 43% is exported and 57% is destined to milling. The milling process

results in 72% bran and 18% oil. The remaining 10% are seeds and losses. Of bran produced, 50% is

exported and 20% of oil is exported.

Soybean is an exports culture, since the level of production exceeds consumption by around 40%. This

means that any growth of domestic production results in exportable surplus.

In the domestic market, soybean is used in the manufacturing of food, such as salami and sausages and

nearly 80% is employed to produce animal’s food. Soybean accounts for 25% to 30% of poultry and hog

food.

Countries of destination

Grain: 75% China, 25% Europe, 10% other Asian countries.

Bran: 70% Europe, 20% Asian countries.

Oil: 50% China, 20% India.

Seasonality

Summer crop: planting occurs between October and December and harvest is concentrated between

February and May.

Regionalization

Mid-west: 49%, south 33%, 8% northeast, 6% southeast

Ranking

Brazil is the world’s second largest player of production with 30.8%, behind the USA with 31.5%, but it is

the largest exporter with 40.7%, followed by USA with 39.3%.

Source: Usda

Production: BRADESCO

World ranking of

the soybean

complex 2011 –

2012 harvest

Snapshot of the market

13

Ranking Production Export Production Export Production Export

US 35,5% 44,2% 20,2% 14,0% 20,6% 12,9%

Brazil 26,4% 32,0% 15,1% 22,9% 15,8% 16,2%

Argentina 19,8% 12,8% 17,2% 49,3% 17,7% 54,6%

China 5,6% 0,0% 25,8% 0,0% 24,6% 0,0%

Grains Meal Oil

Macroeconomic Research Department

Corn is the basis of animal’s food for main types of breeding. In the animal’s food composition, corn accounts

for:

64% in poultry raising

65% in hog raising

23% in dairy cattle

Countries of destination

Corn exports account for 28% of volume produced. Main markets of destination are 14% Japan, 13%

South Korea, 8.5% Taiwan.

Seasonal factors

Corn has two crops:

Summer crop: planting occurs between October and December and harvest is concentrated between

February and May. It represents 40% of total harvest. It has the following regional distribution: 45% south,

26% southeast, 10% mid-west, 15% northeast.

Winter crop: planting occurs between February and June and harvest is concentrated between July and

November. It accounts for 60% of total crop. It has the following regional distribution: 64.3% mid-west,

23% south (only in Paraná), 6% northeast (only in Bahia), 5% southeast.

Ranking

Brazil is the world’s third largest corn producer, with 7% market share and the second largest exporter,

with 18% market share.

CO

RN

Snapshot of the market

14

Macroeconomic Research Department

Brazil exports 67% of coffee produced, 90% green coffee and 10% instant coffee.

Coffee cultivation has high workforce costs, which account for nearly 52% of total costs, since most part

of harvest is manual.

Countries of destination

Green coffee: 19.3% USA, 18.8% Germany, 10% Japan.

Instant coffee: 16.3% USA, 13.5% Russia, 6.4% Ukraine.

Regionalization

Regional distribution of coffea arabica:

71.5% state of Minas Gerais

10.5% state of São Paulo

9.1% state of Espírito Santo

4.3% state of Paraná

2.8% state of Bahia

Regional distribution of Robusta coffee production:

75.6% state of Espírito Santo

12.5% state of Rondônia

6.7% state of Bahia

2.6% state of Minas Gerais

Seasonality

Coffee flowerage occurs between September and November in Brazil. Harvest starts in May and extends

until September.

Ranking

Brazil is the world’s largest coffee player with 37% market share in production and 27% in exports. Other

players, such as Vietnam and Colombia have low domestic consumption, opposite to Brazil, which

accounts for 15% of global consumption.

Distribuição regional da produção de café robusta:

71,2% Espírito Santo

14,3% Rondônia

6,4% Bahia

2,4% Minas Gerais

CO

FF

EE

Snapshot of the market

15

Macroeconomic Research Department

Brazilian cattle is estimated in approximately 200 million heads. The commercial livestock for

slaughtering is estimated at 40 million heads, i.e., this is the volume of cattle at age and weight ideal for

slaughter. The remaining cattle is divided among dairy cows, male calf and unfinished cattle.

Exports accounts for 20% of beef national production.

Countries of destination

Russia is the main market of destination of Brazilian beef exports, accounting for 22%. Hong Kong

accounts for 18%.

Regionalization

Cattle slaughter has the following regional distribution: 36.4% mid-west, 20.4% southeast, 20.1% north,

12.3% south and 10.8% northeast.

Ranking

Brazil is the world’s second largest beef producer with 16.9% market share, preceded by the USA, which

holds 19.1%.

Brazil is the world’s largest exporter with 21% market share.

Seasonality

Cattle raising cycle is long – 2.5 years since when male calf is born until slaughter with approximately 15

arrobas.

Cattle breeding system in Brazil is the extensive cattle raising, i.e., bull is raised released in the pasture

and eats grass.

The confinement system, where bull is raised with animal’s food in small areas, accounts for only 5% of

total slaughter.

Cattle crop occurs in the first half of the year, during rainfall period, when pasture is plentiful. With a

greater cattle supply for slaughter, finished cattle prices during such period are lower.

The cattle intercrop occurs in the second half of the year, during drought period, when cold and white

frost dry pasture. Bull lose weight, with lower cattle supply for slaughter. However, cattle prices increase

during such period, as supply is higher for confined cattle, whose production cost is higher. During

intercrop peak (October) there is greater number of confined male cattle slaughter.

Confinements have two shifts:

1st shift: unfinished cattle is stored between May-June and delivered in August-September.

2nd shift: unfinished cattle is stored between August-September and delivered in November-December.

BE

EF

Snapshot of the market

16

Macroeconomic Research Department

Sugarcane Complex

Of sugarcane produced in Brazil, 46% is destined to produce sugar and 54% to produce ethanol.

Sugar has the following destination: 70% exports and 30% domestic market. Ethanol has the following

destination: 10% exports and 90% domestic market.

Out of total ethanol produced, 55% is hydrated (used as fuel in flex fuel vehicles) and 45% is used as

anhydrous (mixed to gasoline between 20% and 26%).

Sugar is an exports culture, since level of production exceeds consumption by approximately 70%. This

means any growth of national production generates exportable surplus.

Countries of destination

Raw sugar (73% of production) : 15% China, 8% Bangladesh;

Refined sugar (27% of production): Arabian and African countries;

Ethanol: 60% USA, South Korea 13%.

Seasonality

Cane is a continual culture, since period between cane planting and harvest is 18 months, and from

same plant, it is possible to make until six cuts, on average.

Cane harvest period occurs between April and November. During such period, mills operate 24 hours.

Between January and March, plants are disassembled for maintenance.

Brazil is the single large global player with crop in the first half of the year. Other countries are: USA,

Europe, India, Thailand and Australia start their crop from the second half of the year.

Regionalization

65% southeast, 16.8% mid-west, 10.3% northeast, 7.3% south.

Ranking

Brazil is the world’s largest sugar producer, with 22.2% market share. Other players are: India 15%,

European Union 9.2%, China 8.5%, Thailand 6.2%.

Brazil is the largest exporter, with 46% market share in the global market. Other exporters are: Thailand

15%, Australia 5.4%.

World’s largest ethanol producers are: 57% USA and 27% Brazil.

SU

GA

R

AN

D

ET

HA

NO

L

Snapshot of the Market

17

Complexo Sucroalcooleiro

Da cana-de-açúcar produzida no Brasil, 46% se destina à produção de cana e 54% à produção de

etanol (safra 2011/12).

O açúcar tem a seguinte destinação: 68% exportação e 32% mercado doméstico. O etanol tem a

seguinte destinação: 7% exportação e 63% mercado interno.

Do total de etanol produzido, 68% é hidratado (usado como combustível nos carros flex fuel) e 32% é

usado como anidro (misturado à gasolina na proporção de 20% a 26%).

O açúcar é uma cultura de exportação, visto que o nível de produção excede o consumo em torno de

70%. Isso significa dizer que qualquer crescimento da produção nacional gera excedente exportável.

Países de destino

Açúcar Bruto (73% da produção) : 16% Rússia, 10% China;

Açúcar Refinado (27% da produção): Países árabes e africanos;

Etanol: 34% EUA, Coreia do Sul 15%, Japão 14%.

Sazonalidade

A cana é uma cultura perene, pois o tempo entre o plantio e a colheita da cana é de 18 meses, e da

mesma planta é possível fazer até 6 cortes, em média.

O período de colheita da cana ocorre entre abril e novembro. Nesse período as usinas operam 24

horas. Entre os meses de janeiro e março as plantas são desmontadas para manutenção.

O Brasil é o único grande player mundial com safra no 1º semestre do ano. Os demais: EUA, Europa,

Índia, Tailândia e Austrália têm início de safra a partir do 2º semestre do ano.

Regionalização

65% Sudeste, 16,8% Centro-Oeste, 10,3% Nordeste, 7,3% Sul.

Ranking

O Brasil é o maior produtor mundial de açúcar com participação de 21,2%. Os demais players são: Índia

16,8%, União Europeia 9,9%, China 7%, Tailândia 6%.

O Brasil é o maior exportador, com participação de 42% no mercado global. Os demais exportadores

são: Tailândia 15,3%, Austrália 5,2%.

Os maiores produtores mundiais de etanol são: 45% EUA e 33,5% Brasil.

Macroeconomic Research Department

Source: IBGE, CEPEA

Production: BRADESCO

Seasonality of

slaugther of steers

and cows and live

cattle prices

1997 – 2010

in R$ per arroba

Fernando Honorato Barbosa

DEPEC - BRADESCO does not accept responsibility for any actions/decisions that may be taken based on the information provided in its publications and projections. All the data and opinions contained in these information bulletins is carefully checked and drawn up by fully qualified professionals, but it should not be used, under any hypothesis, as the basis, support, guidance or norm for any document, valuations, judgments or decision taking, whether of a formal or informal nature. Therefore, we emphasize that all the consequences and responsibility for using any data or analysis contained in this publication is assumed exclusively by the user, exempting BRADESCO from all responsibility for any actions resulting from the usage of this material. We all point out that access to this information implies acceptance in full of this term of responsibility and usage. The reproduction of the content in this report (partially or in full) is strictly forbidden except if authorized by BRADESCO or if the sources (the name of the authors, publication and BRADESCO) are strictly mentioned.

Team

Economists: Ana Maria Bonomi Barufi / Andréa Bastos Damico / Constantin Jancso / Daniela Cunha de Lima /

Ellen Regina Steter / Estevão Augusto Oller Scripilliti / Fabiana D’Atri / Igor Velecico / Leandro

Câmara Negrão / Marcio Aldred Gregory / Myriã Tatiany Neves Bast / Priscila Pacheco Trigo / Regina

Helena Couto Silva / Thomas Henrique Schreurs Pires

Internships: Alexandre Stiubiener Himmestein/ Christian Frederico M. Moraes / Felipe Alves Fêo Emery de

Carvalho / Felipe Yamamoto Ricardo da Silva / Gabriela Soares de Faria / Mariana Silva de Freitas /

Rafael Martins Murrer