Montea Comm. VA. - ING Belgium Comm. VA. A partnership limited by shares, public closed-end real...

26

Montea Comm. VA. A partnership limited by shares, public closed-end real estate investment company under Belgian law, with registered office at Industrielaan 27, 9320 Erembodegem (Belgium), company registration no. 0417.186.211 (Montea or the Company) SUMMARY OF THE PUBLIC OFFERING TO SUBSCRIBE TO 1,945,416 NEW SHARES IN THE CONTEXT OF A CAPITAL INCREASE, IN CASH, WITH PREFERENTIAL RIGHTS, FOR A MAXIMUM AMOUNT OF EUR 52,526,232 (THE “OFFERING”) APPLICATION FOR ADMISSION TO TRADING OF THE NEW SHARES ON EURONEXT BRUSSELS AND EURONEXT PARIS PRIVATE PLACEMENT OF SCRIPS Subscriptions to the New Shares are, under the terms set out in the Prospectus, reserved for the existing shareholders and holders of Preferential Rights at an Issue Price of EUR 27 and at a subscription ratio of 2 New Shares for 7 existing shares. The Subscription Period will run from 3d June 2014 to 17th June 2014 inclusive. During the Subscription Period, the Preferential Rights can be traded on Euronext Brussels. WARNING Investing in shares involves significant risks. Investors are requested to examine the risks stated in section D of this Summary. Any decision to invest in the New Shares, Preferential Rights and scrips in the context of the Offering must be based on all of the information provided in the Prospectus. Joint Bookrunners Co-Lead Manager Summary dated 2nd June 2014

-

Upload

truongduong -

Category

Documents

-

view

215 -

download

1

Transcript of Montea Comm. VA. - ING Belgium Comm. VA. A partnership limited by shares, public closed-end real...

Montea Comm. VA.

A partnership limited by shares, public closed-end real estate investment company under Belgian law,

with registered office at Industrielaan 27, 9320 Erembodegem (Belgium), company registration no.

0417.186.211 (Montea or the Company)

SUMMARY OF THE PUBLIC OFFERING TO SUBSCRIBE TO 1,945,416 NEW SHARES IN THE CONTEXT OF A

CAPITAL INCREASE, IN CASH, WITH PREFERENTIAL RIGHTS, FOR A MAXIMUM AMOUNT OF EUR

52,526,232 (THE “OFFERING”)

APPLICATION FOR ADMISSION TO TRADING OF THE NEW SHARES ON EURONEXT BRUSSELS AND

EURONEXT PARIS

PRIVATE PLACEMENT OF SCRIPS

Subscriptions to the New Shares are, under the terms set out in the Prospectus, reserved for the existing

shareholders and holders of Preferential Rights at an Issue Price of EUR 27 and at a subscription ratio of

2 New Shares for 7 existing shares. The Subscription Period will run from 3d June 2014 to 17th June

2014 inclusive. During the Subscription Period, the Preferential Rights can be traded on Euronext

Brussels.

WARNING

Investing in shares involves significant risks. Investors are requested to examine the risks stated in

section D of this Summary. Any decision to invest in the New Shares, Preferential Rights and scrips in the

context of the Offering must be based on all of the information provided in the Prospectus.

Joint Bookrunners

Co-Lead Manager

Summary dated 2nd June 2014

This document (the “Summary”) forms, together with the Company’s 2013 annual financial report that was approved by the

Financial Services and Markets Authority (the “FSMA”) on 1st April 2014 as the registration document (the “Registration

Document”), and the securities note of 2nd June 2014 (the “Securities Note”), including all information incorporated by

reference, the prospectus (the “Prospectus”) in relation to (i) the public offering to subscribe to new shares in the Company

(the “New Shares”) in the context of a capital increase, in cash, with preferential rights (the “Preferential rights”) (the

“Offering”) and (ii) the admission to trading of the New Shares on Euronext Brussels and Euronext Paris. The Securities Note

may be distributed separately from the other two documents.

The Securities Note and the Summary were approved in their Dutch-language version by the FMSA on 2nd June 2014, pursuant

to article 23 of the Act of 16th June 2006. The approval of the FSMA does not imply any assessment of any kind of the earnings

or quality of the Offering, the New Shares or the Company.

The Summary has been drawn up in accordance with the requirements regarding the information contained in prospectuses as

well as the format, as stated in Commission Regulation (EC) nº 809/2004 of the European Commission dated 29th April 2004

implementing the Prospectus Directive. Under this commission regulation, summaries are drafted in accordance with the

disclosure requirements, known as “Elements”). These elements are numbered in Section A to E (A.1 – E.7).

The Summary contains all of the Elements required to be included in a summary for this type of security and issuer. Because

some Elements do not need to be discussed, there may be gaps in the sequence of the numbering of the Elements.

Although an Element is required to be inserted in the Summary on account of the type of security and issuer, it is possible that

no relevant information can be supplied about the Element. In this case, a short description of the Element will be included in

the Summary, with the statement “Not applicable”.

Section A — Introduction and warnings

Element Disclosure requirement

A.1 Warning - This summary must be read as an introduction to the prospectus. - Any decision to invest in the new shares, preferential rights or scrips being offered must be

based on an examination of the entire prospectus by the investor. - When a claim in relation to the information in the prospectus is lodged before a court, the

investor acting as the plaintiff, in accordance with the national legislation of the member state in question, must bear any costs for translating the prospectus before the legal proceedings are initiated.

- Only those persons who drafted the summary, including its translation, may be held legally liable if the summary, when read together with the other parts of the prospectus, is misleading, inaccurate or inconsistent, of if it, when read in conjunction with the other parts of the prospectus, does not contain the core facts for helping investors when they are considering investing in the new shares, preferential rights or scrips.

A.2 Consent to use the prospectus for later resale Not applicable.

Section B — Issuer and any guarantor

Eleme

nt

Disclosure requirement

B.1 Official name and trading name Montea.

B.2 Domicile, legal form, legislation under which the Company operates and country of establishment Montea is a partnership limited by shares (commanditaire vennootschap op aandelen/société en commandite par actions), incorporated under Belgian law. Its registered office is at Industrielaan 27, 9320 Erembodegem, Belgium. As a public fixed-capital real estate investment company, Montea is subject to the Act of 3rd August 2012 regarding certain forms of collective investment portfolio management (the “Act of 3rd August 2012”) and the Royal Decree of 7th December 2010 in relation to real estate investment companies (the “Royal Decree of 7th December 2010”), as well as under the relevant terms of the Belgian Companies’ Code.

B.3 Description of, and key factors relating to, the nature of the Company’s current operations and principal activities Montea is a real estate investment company that specialises in logistics and semi-industrial property in Belgium, France and the Netherlands. Montea provides more than just warehouses and aims to offer flexible and innovative property solutions to its tenants. Montea believes in the long-term value of logistics and semi-industrial property. Architectural requirements, technology and other specifications develop less quickly in this area than in other segments, such as office buildings. Yet when renovations need to be made to logistics or semi-industrial property, the cost of doing so in comparison with the total value of the building is lower than in other segments. This means that logistics and semi-industrial property is an attractive investment in the long term. Montea is positioned as an end-investor in the market. Montea works in conjunction with other parties in the sector, such as developers and landowners, using its expertise and experience, to be involved

from an early stage in the development of its buildings (known as build-to-suit projects). Core facts about Montea:

31.03.2014 31.12.2013 31.12.2012

Number of sites 37 35 32

Total floor space in m² 619,093 584,694 514,767

Fair value (excl. solar panels (K EUR)

336,466 311,936 283,678

Occupancy rate 95.0% 94.9% 96.3%

Contracted rent on an annual basis (K EUR)

27,113 26,048 22,641

B.4a Description of the most significant recent trends affecting the Company and the industries in which it operates “Expectations are that after the faltering recovery in 2013, the economy will improve further in 2014. Economic growth in 2013 ended up at around +0.1%. For 2014, forecasts are clearly more positive, with growth expected to be 1.1%. This means that while the recovery is continuing, it remains very fragile and is certainly insufficient to generate a genuine turnaround in the unemployment figures. Yet despite increasing unemployment, overall consumer confidence is on the rise. Clearly, consumers are living in the hope that things will get better and hence are getting in ahead of the expected recovery.

How these expectations will affect the semi-industrial and logistics market is hard to predict. Despite

Belgium’s central location and its relatively low rents, it is clear that there are many other parameters

that also play a role. These include the cost of wages and traffic congestion. Competition with our

neighbouring countries to attractive new distribution centres also remains very high. In the meantime,

little change is expected in terms of rents, yields and take-up. The arrival of a major e-commerce player

would be nice, but appears difficult to achieve in the short term.”1

B.5 Group of which the Company is part and its place within that Group Montea has one subsidiary in Belgium (Acer Park NV: 100%), seven subsidiaries in France (SCI Montea France: 100%, SCI 3R: 95%, SCI Antipole Cambrai: 100%, SCI Sagittaire: 100%, SCI Saxo: 100%, SCI Sévigné: 100% and SCI Socrate: 100%) and four subsidiaries in the Netherlands (Montea Nederland NV: 100%, Montea Almere NV: 100%, Montea Rotterdam NV: 100% and SFG BV: 100%). Montea also has a branch office (permanent establishment/établissement stable) in France (Montea SCA-SIIC: 100%).

B.6 Shareholding based on transparency declarations Based on the transparency declarations received by Montea prior to the date of the Securities Note, the major shareholders are as follows:

Shareholder Number of shares % of the capital

De Pauw Family

1,459,895 21.4%

Belfius Insurance 898,139 13.2%

Banimmo NV 833,934 12.2%

Federale Verzekering 690,058 10.1%

1 Source: De Crombrugghe & Partners NV for the property market in Belgium

De Smet Family 251,459 3.7%

Own shares 23,346 0.3%

Each share is entitled to one vote. At the present time, no control is exercised over Montea in the sense of article 5 of the Companies’ Code.

B.7 Important historical financial information for each financial year for the period covered by the historical financial information and for any later interim reporting period, and notes Consolidated balance sheet:

(EUR x 1.000) 31/03/2014 31/12/2013 31/12/2012

NON-CURRENT ASSETS 348 601 320 347 290 230

Goodwill 0 0

Intangible assets 106 114 141

Investment properties (incl. Development projects) 340 867 312 545 282 100

Investment properties 7 592 7 651 7 883

Development projects 0 0 0

Other tangible assets 0 0 0

Financial fixed assets 37 37 105

Financial lease receivables 0 0 0

Participations consolidated with the equity method 0 0 0

CURRENT ASSETS 21 087 19 450 17 268

Assets held for sale 0 0 2 225

Current financial assets 0 0 0

Financial lease receivables 0 0 0

Trade receivables 8 611 6 978 5 720

Tax receivables adn other current assets 1 960 638 844

Cash and cash equivalents 979 4 092 7 007

Deffered charges and accrued income 9 537 7 741 1 472

TOTAL ASSETS 369 688 339 797 307 498

SHAREHOLDERS' EQUITY 140 896 138 967 123 763

Shareholders' equity attributable to shareholders of parent company

140 798 138 869 123 663

Share capital 137 537 137 537 128 340

Share premiums 1 771 1 771 533

Reserves -484 -16 410 -2 108

Result 1 974 15 970 -3 102

Minority interests 98 98 100

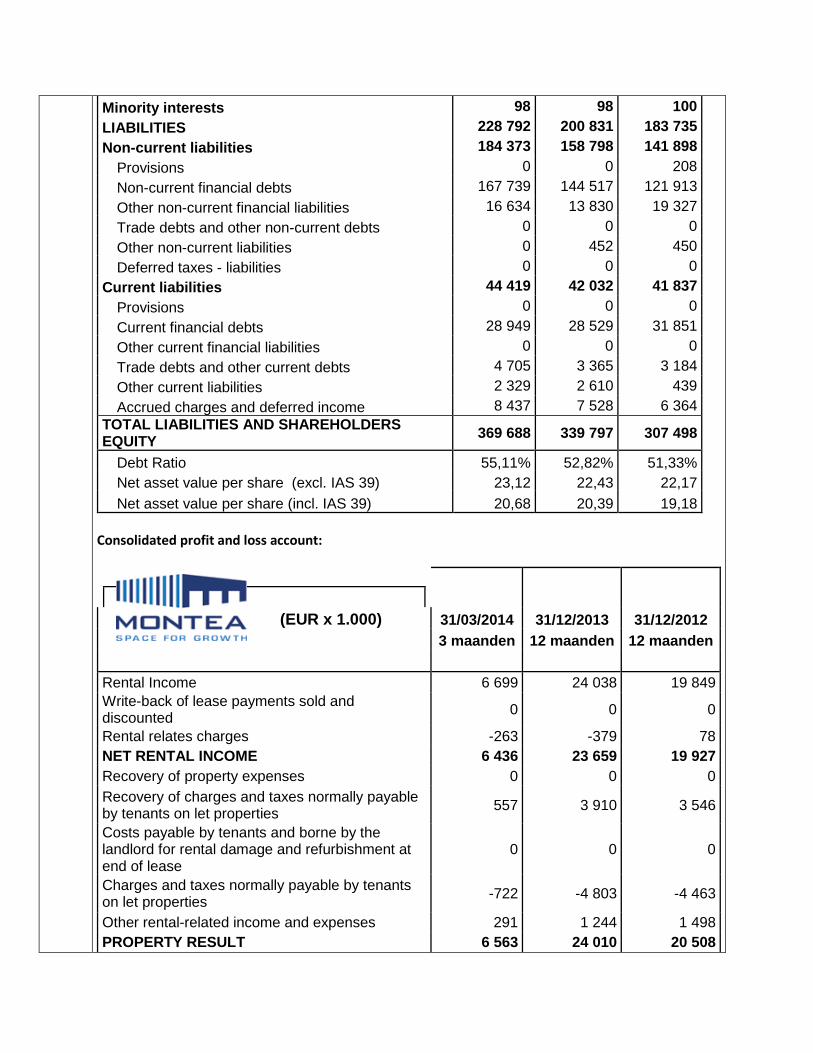

LIABILITIES 228 792 200 831 183 735

Non-current liabilities 184 373 158 798 141 898

Provisions 0 0 208

Non-current financial debts 167 739 144 517 121 913

Other non-current financial liabilities 16 634 13 830 19 327

Trade debts and other non-current debts 0 0 0

Other non-current liabilities 0 452 450

Deferred taxes - liabilities 0 0 0

Current liabilities 44 419 42 032 41 837

Provisions 0 0 0

Current financial debts 28 949 28 529 31 851

Other current financial liabilities 0 0 0

Trade debts and other current debts 4 705 3 365 3 184

Other current liabilities 2 329 2 610 439

Accrued charges and deferred income 8 437 7 528 6 364

TOTAL LIABILITIES AND SHAREHOLDERS EQUITY

369 688 339 797 307 498

Debt Ratio 55,11% 52,82% 51,33%

Net asset value per share (excl. IAS 39) 23,12 22,43 22,17

Net asset value per share (incl. IAS 39) 20,68 20,39 19,18

Consolidated profit and loss account:

(EUR x 1.000) 31/03/2014 31/12/2013 31/12/2012

3 maanden 12 maanden 12 maanden

Rental Income 6 699 24 038 19 849

Write-back of lease payments sold and discounted

0 0 0

Rental relates charges -263 -379 78

NET RENTAL INCOME 6 436 23 659 19 927

Recovery of property expenses 0 0 0

Recovery of charges and taxes normally payable by tenants on let properties

557 3 910 3 546

Costs payable by tenants and borne by the landlord for rental damage and refurbishment at end of lease

0 0 0

Charges and taxes normally payable by tenants on let properties

-722 -4 803 -4 463

Other rental-related income and expenses 291 1 244 1 498

PROPERTY RESULT 6 563 24 010 20 508

Technical costs -16 -14 -29

Commercial costs -87 -111 -91

Charges and taxes of unlet properties -92 -255 -174

Property management costs -167 -244 -637

Other property charges -2 -83 -115

TOTAL PROPERTY CHARGES -365 -708 -1 046

OPERATING PROPERTY RESULT 6 198 23 302 19 462

General costs -866 -3 573 -2 938

Other operating income and expenses -2 163 231

OPERATING RESULT BEFORE RESULT ON THE PORTFOLIO

5 330 19 892 16 756

Result on disposals of investment properties 0 1 107 362

Result on disposals of other non-financial assets 0 0 0

Result in the fair value of investment properties 1 239 -4 130 -6 692

Other results on the portfolio 0 0 0

OPERATING RESULT 6 569 16 870 10 425

Financial income 3 49 178

Net Interest charges -1 787 -6 219 -5 537

Other financial charges -7 -36 -110

Variations in the fair value of financial assets & liabilities

-2 804 5 497 -8 023

FINANCIAL RESULT -4 595 -708 -13 492

Income from participations consolidated with the equity method

0 0 0

RESULT BEFORE TAXES 1 974 16 161 -3 067

Corporate income tax 0 -193 -39

Exit tax 0 0 0

TAXES 0 -193 -39

NET RESULT 1 974 15 969 -3 106

NET CURRENT RESULT (1) 3 539 13 494 11 248

Number of shares entitled in the result of the period

6 808 962 6 587 896 5 634 126

NET RESULT PER SHARE 0,29 2,42 -0,55

NET CURRENT RESULT PER SHARE 0,52 2,05 2,00

GROSS DIVIDEND PER SHARE

1,97 1,93

NET DIVIDEND PER SHARE 1,48 1,45

Notes to the historical financial information The net rental result was EUR 23.66 million, a rise of 18.7% compared with the same period in 2012 (EUR 19.93 million). This increase of EUR 3.73 million is attributable to the EUR 4.19 million rise in rental income and the negative impact of lease-related costs amounting to EUR 0.46 million.

The operating result before the result on the property portfolio rose from EUR 16.76 million last year to EUR 19.89 at 31/12/2013. This increase of EUR 3.13 million (or 18.7%) in the operating result before the result on the property portfolio was due to: - the increase in the net rental result of EUR 3.73 million; - the smaller rise in the property result on top of the increase in the net rental result (impact of EUR -

0.23 million); - the increase in property costs, general company overheads and other operating income and costs of

EUR 0.37 million. The operating margin2 was 84.1% for the full year 2013, which was in line with the same period last year. The financial result at 31/12/2013 was EUR -6.21 million, a rise of 13.5% compared with the same period last year (EUR -5.47 million). The average debt increased by EUR 21.11 million (+15.4%). By contrast, there was a slight fall in the average financial cost (by 1.7%) to 3.92%3 for the 2013 financial year. The result on the property portfolio was EUR -3.02 million at 31/12/2013. This negative result was due to: - a positive gain of EUR 1.11 million; - a negative variation in the fair value of the real estate portfolio in Belgium of EUR -2.78 million; - a negative variation in the fair value of the real estate portfolio in France of EUR -1.70 million; - a positive variation in the fair value of the real estate portfolio in the Netherlands of EUR 0.35

million. The result on the hedging instruments was EUR 5.50 million at 31/12/2013. This positive result was due to the slight recovery in long-term interest rates during 2013. The net result was EUR 15.97 million, which was a rise of EUR 19.08 million compared with the previous year and was significantly affected by the positive variation in the value of the hedging instruments. The net operating result was EUR 2.05 per share and the distributable profit was EUR 2.08. As of 31/12/2013, the total assets (EUR 339.80 million) consisted of investment property (91.8% of the total) and the solar panels (2.2% of the total). The remaining amount of the assets (6.0% of the total) consisted of intangible, other tangible and financial fixed assets and current assets, including cash investments, trading and tax receivables. Total assets consisted of equity capital of EUR 138.97 million and total obligations of EUR 200.83 million.

B.8 Selected key pro forma financial information, to be identified as such. Not applicable.

B.9 Profit forecast or estimate In 2013, Montea achieved a net operating result of EUR 13.50 million (EUR 2.05 per existing share). Based on these results, the results of Q1 2014 and taking account of (i) the investments already announced (consisting mainly of “build-to-suit” projects that will only generate limited rental income for 2014), (ii) the acquisition of EUR 20 million of additional investments in 2014 that have not yet been announced, (iii) and estimate of the occupancy rate, and (iv) the issue of the 2014 bonds, and (v) the full placement of the intended capital increase, Montea aims to increase its net operating result by at least 10% to EUR 14.8 million. The forecasts above are based on various hypotheses and estimates of known and unknown risks, uncertainties and other factors reasonably assumed when the forecasts were made, but which subsequently could appear incorrect. As a consequence, the company’s results, financial situation, performance or achievements may differ significantly from the future results,

2 The operating result before the result on the property portfolio, compared with the net rental result. 3 This financial cost is an average for the whole year, including the lease debts in France, the Netherlands and

Belgium, and was calculated based on the total financial cost with regard to the average start and end balance of the financial debt for 2013, without taking account of the valuation of the hedging instruments.

financial situation, performance or achievements that such statements, outlooks and estimates previously described or proposed.

B.10 Reservation concerning the historical financial information Not applicable.

B.11 Statement about the working capital Montea funds its activities with long-term loans. The following loans expire within 12 months after the date of the Securities Note:

In 2014 (EUR 26.7 million): o A long-term loan of EUR 5 million with BNP Paribas Fortis NV (entered into on 30th

September 2011), which expires on 30th September 2014; o A long-term loan of EUR 6.7 million with Belfius Bank NV (entered into on 30th

September 2011), which expires on 30th September 2014; o A long-term loan of EUR 15 million with KBC Bank NV (entered into on 30th September

2011), which expires on 31st December 2014;

In the first half of 2015 (EUR 25 million); o A long-term loan of EUR 15 million with KBC Bank NV (entered into on 18th June 2012),

which expires on 18th June 2015; o A long-term loan of EUR 10 million with Belfius Bank NV (entered into on 31st May

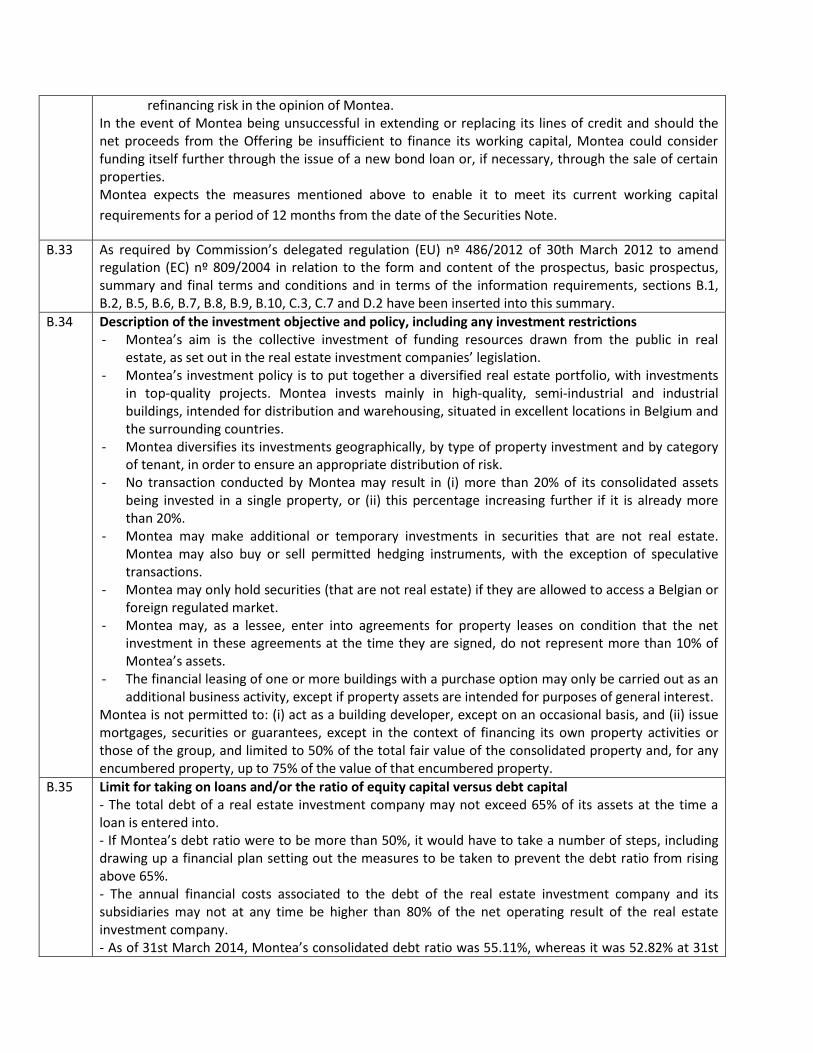

2012), which expires on 31st May 2015. As of the date of the Securities Note, these loans were completely drawn down. In addition, Montea has EUR 10.0 million of undrawn long-term loans available. Taking account of the net proceeds of this Offering and taking account of the (re)financing of the long-term funding arrangements stated above, Montea, as of the date of the Securities Note, has sufficient working capital (surplus of EUR 13.2 million) to meet its current needs under all circumstances for a period of 12 months from the date of the Securities Note. Without taking account of the net proceeds of this Offering and taking account of the (re)financing of the long-term funding arrangements stated above, Montea as of the date of the Securities Note, has insufficient working capital (shortfall of approximately EUR 87.6 million) to meet its current needs under all circumstances for a period of 12 months from the date of the Securities Note. The expiration of the above loans and complying with the obligations that Montea has entered into in the context of a number of ‘build-to-suit’ investment projects (subject to the usual suspensive conditions) will result in a shortfall in working capital from August 2014. Taking account of these due dates, the available lines of credit and the expected operating results, this shortfall will vary between the date of the Securities Note and 30th June 2015 between EUR 21.8 million on 31st August 2014 and a maximum of EUR 87.6 million on 30th June 2015. Montea expects to finance this shortfall as follows:

By way of the net proceeds from the Offering up to a maximum of EUR 51.6 million. Certain existing shareholders, in particular the De Pauw family, Belfius Insurance and Federale Verzekering have irrevocably undertaken to exercise all of their Preferential Rights, and the De Smet family has irrevocably undertaken to exercise a part of its Preferential Rights, (together for 46.6% of the shares) during the subscription period and to subscribe to the capital increase for a minimum amount of EUR 24.5 million.

In addition, Montea plans to renew or replace or extend its long-term loans. As of the date of the Securities Note, negotiations in relation to the renewal, replacement or extension of the lines of credit mentioned above had not yet begun. In the past, Montea has always been able to extend its loans. In addition, Montea obtains its funding from various banks, which reduces the

refinancing risk in the opinion of Montea. In the event of Montea being unsuccessful in extending or replacing its lines of credit and should the net proceeds from the Offering be insufficient to finance its working capital, Montea could consider funding itself further through the issue of a new bond loan or, if necessary, through the sale of certain properties. Montea expects the measures mentioned above to enable it to meet its current working capital

requirements for a period of 12 months from the date of the Securities Note.

B.33 As required by Commission’s delegated regulation (EU) nº 486/2012 of 30th March 2012 to amend regulation (EC) nº 809/2004 in relation to the form and content of the prospectus, basic prospectus, summary and final terms and conditions and in terms of the information requirements, sections B.1, B.2, B.5, B.6, B.7, B.8, B.9, B.10, C.3, C.7 and D.2 have been inserted into this summary.

B.34 Description of the investment objective and policy, including any investment restrictions - Montea’s aim is the collective investment of funding resources drawn from the public in real

estate, as set out in the real estate investment companies’ legislation. - Montea’s investment policy is to put together a diversified real estate portfolio, with investments

in top-quality projects. Montea invests mainly in high-quality, semi-industrial and industrial buildings, intended for distribution and warehousing, situated in excellent locations in Belgium and the surrounding countries.

- Montea diversifies its investments geographically, by type of property investment and by category of tenant, in order to ensure an appropriate distribution of risk.

- No transaction conducted by Montea may result in (i) more than 20% of its consolidated assets being invested in a single property, or (ii) this percentage increasing further if it is already more than 20%.

- Montea may make additional or temporary investments in securities that are not real estate. Montea may also buy or sell permitted hedging instruments, with the exception of speculative transactions.

- Montea may only hold securities (that are not real estate) if they are allowed to access a Belgian or foreign regulated market.

- Montea may, as a lessee, enter into agreements for property leases on condition that the net investment in these agreements at the time they are signed, do not represent more than 10% of Montea’s assets.

- The financial leasing of one or more buildings with a purchase option may only be carried out as an additional business activity, except if property assets are intended for purposes of general interest.

Montea is not permitted to: (i) act as a building developer, except on an occasional basis, and (ii) issue mortgages, securities or guarantees, except in the context of financing its own property activities or those of the group, and limited to 50% of the total fair value of the consolidated property and, for any encumbered property, up to 75% of the value of that encumbered property.

B.35 Limit for taking on loans and/or the ratio of equity capital versus debt capital - The total debt of a real estate investment company may not exceed 65% of its assets at the time a loan is entered into. - If Montea’s debt ratio were to be more than 50%, it would have to take a number of steps, including drawing up a financial plan setting out the measures to be taken to prevent the debt ratio from rising above 65%. - The annual financial costs associated to the debt of the real estate investment company and its subsidiaries may not at any time be higher than 80% of the net operating result of the real estate investment company. - As of 31st March 2014, Montea’s consolidated debt ratio was 55.11%, whereas it was 52.82% at 31st

December 2013.

B.36 Regulatory status of Montea and regulator As a public real estate investment company, Montea comes under the supervision of the FSMA.

B.37 Brief profile of the typical investor for whom Montea is designed Montea focuses on both private individual and institutional investors wanting an indirect investment in logistics and semi-industrial property (industrial estates) seeking a high dividend with an average risk profile.

B.38 Because Montea does not require any deviation from article 39, §1 of the RD of 7th December 2010, which states that none of the transactions carried out by Montea may result in it having over 20% of its consolidated assets invested in property that constitutes a single real estate property, element B.38 is not applicable.

B.39 Because Montea does not require any deviation from article 39, §1 of the RD of 7th December 2010, which states that none of the transactions carried out by Montea may result in it having over 20% of its consolidated assets invested in property that constitutes a single real estate property, element B.39 is not applicable.

B.40 Description of the service-providers, including the maximum amount of fees payable 1. Auditor

Montea’s auditor is Ernst & Young Bedrijfsrevisoren BCVBA, whose registered office is at De Kleetlaan 2, 1831 Diegem, represented by Mrs Christel Weymeersch, company auditor. The remuneration of the auditor for the 2013 financial year was EUR 42,805 (excl. VAT).

2. Real estate experts Montea’s real estate experts are (i) Crombrugghe & Partners, whose registered office is at Herman-Debrouxlaan 54, 1160 Brussels, represented by Mr Pascal van Humbeeck (for property in Belgium and the Netherlands), and (ii) Deloitte France, whose registered office is at avenue Charles de Gaulle 185, 92200 Neuilly-sur-Seine, France, represented by Olivier Gerarduzzy (for property in France). The total remuneration of the real estate experts for the 2013 financial year was EUR 119,100 (excl. VAT).

3. Financial services Financial services are provided by Euroclear Belgium for Belgium and by Société Générale for France. The total remuneration for financial services for the 2013 financial year was EUR 6,478 (excl. VAT).

4. External managers Montea does not use external managers.

B.41 Because Montea does not rely on investment managers, investment advisors, custodians, trustees or other counsellors, element B.41 is not applicable.

B.42 Frequency with which the intrinsic value of Montea is determined and description of the way in which this intrinsic value will be notified to investors The intrinsic value of Montea is determined each quarter (based on the valuation of Montea’s property portfolio by the real estate expert) and notified in a press release dealing with the annual, half-yearly and quarterly figures.

B.43 Because Montea does not qualify as “an undertaking for collective investment in other collective investment undertakings”, element B.43 is not applicable.

B.44 Because on the date of the Summary and the Securities Note, works have been commenced by Montea and financial overviews have been drawn up as stated above, element B.44 is not applicable.

B.45 Description of Montea’s portfolio See Item B.3 of this Summary.

B.46 Indication of the most recent intrinsic value per share As of 31st March 2014, the net inventory value was EUR 20.68 per share and EUR 23.12 (excluding IAS 39) per share.

Section C — Securities

Element Disclosure requirement

C.1 Description of the type and class of securities being offered and/or admitted to trading, including any security identification number All New Shares will be issued in accordance with Belgian law. These are ordinary shares that represent capital (in euro), are of the same category, are totally free to trade, are paid up in full, have voting rights and are without indication of par value. They will have the same associated rights and share in the profits as the existing shares, on the understanding that for the 2014 financial year, the New Shares will be entitled to a dividend from the time they are issued, i.e. from 24th June 2014. In the same way as the existing shares, the New Shares will be given the ISIN code BE0003853703, while Preferential Rights will be given the ISIN code BE0970132354.

C.2 Currency in which the securities will be issued. EUR.

C.3 Number of issued, fully paid-up shares and number of shares not paid up in full. Par value per share or statement that the shares have no par value. As of the date of the Securities Note, the company share capital was represented by 6,808,962 shares, without a par value stated and paid up in full.

C.4 Description of the rights attached to the securities. - Voting right: each share is entitled to one vote, subject to cases where the voting right is

suspended, as stated in the Companies’ Code. Shareholders may vote by proxy. - Dividends: the New Shares provide an entitlement to a (pro rata temporis) dividend per share

(if there is a distributable profit) from the date of issue, which in principle is 24th June 2014. For this purpose, just before the beginning of the subscription period, coupon nº 13 will be detached from the existing shares (after the markets close). This coupon represents the right to receive part of the dividend for the current financial year, calculated pro rata temporis for the period between 1st January 2014 and the issue date of the New Shares, in principle 24th June 2014, on which the shareholders’ meeting on 19th May 2015 will decide (if applicable). The coupon will be detached on 2nd June 2014, but at the same time will be paid out in the same way as the coupon that makes up the balance of the dividend (coupon nº 14 or, where appropriate, one of the subsequent coupons). It will be kept at the banking institution and outsourced in the same as this banking institution outsources other detached coupons. Its value will be estimated at the time of the prospectus, as set out below. The New Shares will be issued with coupons nº 14 and following attached. Coupon nº 14, or where appropriate one of the subsequent coupons, represents the right to part of the dividend (if there is one) for the current financial year, calculated pro rata temporis for the period between the issue date of the New Shares, in principle 24th June 2014, and 31st December 2014, to be received based on what the shareholders’ meeting of 2015 decides. The policy on distributable dividends adopted by the Company is discussed in more detail in Element C.7.

- Preferential rights on capital increase in cash: in accordance with the Royal Decree of 7th

December 2010, Montea’s articles of association state that with a capital increase by contribution in cash, the preferential right granted by the Companies’ Code to shareholders can be restricted or cancelled, but only if a preferential allocation right is granted to the existing shareholders in the allocation of new securities. Such a preferential allocation right does not need to be granted where a contribution in kind is involved in the context of paying out an optional dividend, on condition that this is made effectively payable for all shareholders.

- Rights in the event of liquidation: the balance after liquidation, specifically the net assets, will be distributed among the shareholders in proportion to the number of shares they own.

C.5 Description of any restrictions on the free transferability of the securities Montea’s articles of association contain no stipulations that restrict the transferability of the shares. However, see Element E.5 of this Summary regarding certain lock-up undertakings entered into in the context of the Offering.

C.6 Admission to trading and listing location The Preferential Rights (coupon nº 12) will be detached on 2nd June 2014 when the market closes and may be traded during the subscription period, i.e. from 3rd June 2014 to 17th June 2014 inclusive, on Euronext Brussels. Consequently, from 3rd June 2014, the existing shares will be traded ex-coupon nº 12 and 13. Permission to trade the New Shares on Euronext Brussels and Euronext Paris will be applied for. The New Shares will be listed in the same way as the existing shares with ISIN code BE0003853703; the Preferential Rights will be listed with ISIN code BE0970132354.

C.7 Description of the dividend policy As a public real estate investment company, Montea is required to pay out an amount as capital allowance that at least corresponds with the positive difference between the following amounts: - 80% of the amount equivalent to the sum of the adjusted result and the net profit on the sale of

properties that are not exempt from the payment obligation; and - the net reduction of Montea’s debts over the course of the financial year. Although Montea has the status of a real estate investment company, it still remains subject to article 617 of the Companies’ Code, which states that a dividend may only be paid if, at the closing date of the financial year in question, the net assets resulting from this payment do not fall below the amount of the paid-up capital, plus all of the reserves that may not be paid out pursuant to the law or the articles of association. Because Montea also comes under the status of a French SIIC, it must also comply with a number of payout terms, as defined by the French legislation on SIICs. At the proposal of the statutory manager of Montea (Montea Management NV), the general meeting of shareholders of Montea decided on 20th May 2014 to pay out a gross dividend of EUR 1.97 for the 2013 financial year. This represents an increase of 2.1% compared with the gross dividend for the 2012 financial year (EUR 1.93 per share). This corresponds with a net dividend of EUR 1.4775 per share for the 2013 financial year, compared with EUR 1.4475 per share for the 2012 financial year. The dividend for the 2013 financial year represents a payout percentage of 94.7% of the distributable profits and 96.1% of the net operating result.

Section D — Risks

Element Disclosure requirement

D.1 D.2

Main risks associated with Montea and its activities Applicant investors must take account of the fact that the risk factors summarised below on the

date of the Securities Note constitute the essential risks to be assessed by a potential investor when considering an investment in the New Shares. The risk factors relate to uncertain events that may or may not occur. Market risks

a. Risks associated with the economic situation Macroeconomic indicators have a certain effect on investments and rental incomes from companies operating in the sector for logistics and semi-industrial property and these may have a negative effect on Montea’s business activities. These macroeconomic indicators may also have an effect on the financing of existing and future investments.

b. Risks associated with the property market The level of rental income, property values and occupancy rates are affected significantly by supply and demand in the property market. In order to maintain its growth and yields, Montea must keep its occupancy rate up to the mark and retain its rental income and property values by entering into new lease agreements or renewing existing ones.

c. Concentration risk In view of the type of projects in which Montea invests, there is a risk that Montea may become too dependent on the continued existence of a specific site or contractual relationship with a particular client.

d. Inflation risk When interest percentages are at fixed rates, Montea is only exposed to a limited extent to the risk of inflation in view of the fact that rents are indexed annually (based on the health index). However, if there is a rise in the nominal interest rate, low inflation would lead to an increase in the actual interest rate. This in turn would result in financial costs rising more quickly than income from the indexing of rents.

II. Risks associated with Montea’s real estate portfolio a. Risks associated with rental income

Montea’s entire turnover consists of the rental income generated by the lease agreements that Montea signs with third parties. Non-payment by tenants and a fall in occupancy rates could have a negative impact on results.

b. Risks associated with the destruction of buildings There is a risk that the buildings in Montea’s property portfolio are destroyed as the result of fire, natural disasters, accidents, terrorism, etc. Montea is insured against these risks (cover for the cost of a new building, including additional guarantees, such as the loss of rental income).

c. The conditional nature of forthcoming build-to-suit projects The Company has signed an agreement for various build-to-suit projects with the developer in which the Company undertakes, at a pre-agreed price, to purchase the building in question (or the company to which the building belongs), subject to the fulfilment of a number of suspensive conditions. These suspensive conditions relate to items such as the handing over of the guarantee, the first rent payment, obtaining the necessary permits and the provisional handover of the building. If the building is handed over later than scheduled, or if one or more of the suspensive conditions are not fulfilled, the Company may decide not to acquire the building (or only later), which may have an impact on the Company’s planned results and its future property portfolio.

d. Public domain and airport zones For some property, the Company has concessions for public domain or building rights. These titles are by definition restricted in time and may be terminated early for reasons in the public interest due to the specific nature of the location or its legal status. In particular, reference is made to the building rights that the Company or its subsidiaries have stipulated with The Brussels Airport Company (TBAC) at Brucargo. These building rights may, as is customary in the airport zone, be

terminated early by The Brussels Airport Company for reasons of general interest or the proper operation of the airport. Should TBAC terminate the building rights for any of these reasons, it will pay full compensation to the Company. Should a competent authority (other than TBAC) terminate the building rights of reasons of public interest (expropriation), the Company will not receive any compensation from TBAC. If this should be the case, TBAC and the Company will strive to obtain appropriate compensation from the competent authority, in which TBAC undertakes to pass on any compensation it receives to the Company. In this latter case, there may be a discussion between the Company and the competent authority regarding the extent of the compensation, which in turn may have a negative impact on the Company’s activities and operating results.

III. Financial risks a. Debt structure

Under the law, neither the consolidated or simple debt ratio of the Company may exceed 65%4. The Company has signed covenants with the financial institutions that are in line with the market and which also state that the Company’s consolidated debt ratio (pursuant to the Royal Decree of 7th December 2010) may not exceed 60%. In addition, the terms of the 2013 bonds (totalling EUR 30 million) and 2014 bonds (totalling EUR 30 million) stipulate a maximum consolidated debt ratio of 65%. If the Company breaches these covenants, any bondholder can require that his/her/its bonds be immediately declared enforceable and repayable at face value, plus interest accrued (if there is any) to the date of payment, without further formalities, unless the breach is rectified prior to the Company receiving such notification. Article 54 of the Royal Decree of 7th December 2010 states that if the Company’s consolidated debt ratio exceeds 50%, the Company is required to draw up a financial plan containing an execution schedule stating the measures that will be taken to prevent this ratio exceeding 65%. As of 31st December 2013, the Company’s consolidated debt ratio was 52.82%, meaning that the Company was required to draw up a financial plan and execution schedule. The auditor has audited the financial plan and drafted a special report. On 31st March 2014, the Company’s consolidated debt ratio was 55.11%. A maximum consolidated debt ratio of 60% or 65% means that as of 31st March 2014, the Company’s property portfolio may grow by EUR 45 million or EUR 104 million respectively, fully funded by debt, whereby all of the other balance sheet items (with the exception of the property portfolio and long-term debts) remain the same, hence not taking account of the changes to the working capital and the net result for the period.

b. Liquidity risk The liquidity risk means that the Company runs the risk, at a certain moment, of not having the necessary cash resources and no longer being able to obtain the required funding to service its short-term debts.

- Lines of credit Given the legal status of real estate investment companies and the nature of the assets in which the Company invests (logistics and semi-industrial property), under the current circumstances, the risk of the non-renewal of the lines of credit (excluding unforeseen circumstances) is small, even in the context of a tightening of the terms of credit. However, it is the case that credit margins may increase at the time when the lines of credit expire and have to be renewed. There is also the risk of the termination of the bilateral lines of credit through the cancellation, termination or review of the financing contracts as the result of non-compliance with the undertakings (“covenants”) stipulated at the time these financial contracts were signed. For example, technically speaking, should the Company lose its status as a real estate investment company, this could constitute an event or default under the terms of most of the Company’s lines

4 Article 53 of the Royal Decree of 7th December 2010.

of credit. The Company’s undertaking stipulated with its financial institutions are in line with the market and state, among other tings, that the consolidated debt ratio may not exceed the ceiling of 60%5.

- The 2013 bonds and 2014 bonds Montea may not be able to repay the 2013 bonds and/or 2014 bonds when they mature. Pursuant to the general terms and conditions of both the 2013 bonds and the 2014 bonds, the Company may be obliged to make early repayment of the bonds issued should there be a change in control over the Company. If that should be the case, each bondholder will be entitled to demand that Montea buy back his/her/its bonds at 100.00 per cent of their face value, plus any interest due but not yet paid up to (but excluding) the date of early repayment.

c. Interest rates Short-term and/or long-term interest rates on the (international) financial markets are exposed to significant fluctuations. With the exception of its lease agreements6, the 2013 bonds7 and the 2014 bonds8, all of Montea’s financial debts are at a variable interest rate (bilateral lines of credit at the EURIBOR 3-month rate). This enables Montea to benefit from low interest rates. Total interest-bearing obligations (excluding the negative value of the hedging instruments under IAS 39) were 53% of Montea’s balance sheet total at 31st March 2014.

d. Credit risk If one of Montea’s clients or counterparties does not meet its contractual obligations, Montea runs the risk of incurring a financial loss.

IV. Regulatory risks a. Status as a real estate investment company/SIIC

Any unfavourable change in the system of real estate investment companies in Belgium or to SIICs in France would have negative consequences for the Company’s results and hence also for the remuneration of its shareholders. If the Company should lose its status as a real estate investment company or SIIC as the result of a serious shortcoming in its compliance with the obligations pursuant to the Act of 3rd August 2012 and the Royal Decree of 7th December 2010, as well as with the terms of its SIIC status, it may also mean the end to the system of fiscal transparency (exemption from tax on profits regarding the Company and taxation regarding the shareholders).

b. AIFMD, EMIR and the new status of regulated real estate company The Company should experience no effect from the European regulations and the transposition of European Directives into Belgian law, including (should the Company comes under its scope) the Alternative Investment Fund Managers Directive (AIFMD) and the Directive on OTC derivatives, central counterparties and transaction registers (the European Market Infrastructure Regulation, or EMIR). Given its status as a public real estate investment company, the Company is currently qualified under Belgian law as a self-managed collective investment undertaking. As a result of this, it will be considered as the manager of an alternative investment fund (AIF) under AIFMD, which will be

5 In addition to the main guarantee of not exceeding the 60% debt ratio, the other main covenants with the five banking institutions consist of (i) complying with all of the terms for the status of real estate investment company, (ii) not issuing guarantees, securities or mortgages on its property, (iii) an interest coverage ratio (defined as the operating margin compared with the net financial cash result) of a minimum of 2.00 to 2.25, (iv) retaining a minimum portfolio value of EUR 150,000,000. 6 Montea has financial debts of EUR 5 million (2.8% of the total financial debt) in relation to the current lease agreements. These leases (for 3 sites) expire between 2014 and 2017. They were entered into with a fixed payment per quarter (including interest). 7 Montea issued bonds in 2013 at a fixed interest rate of 4.107%. 8 Montea issued bonds in 2014 at a fixed interest rate of 3.355%.

transposed into Belgian law by the Act on alternative institutions for collective investment and their managers (AICB Act). In the meantime, the Belgian parliament will create a new legal status of public regulated real estate company, as provided for in Parliament’s draft bill DOC 53 n° 3497/001 that was approved on 22nd April 2014 (GVV Act). The GVV Act will come into effect on the date stated by the Royal Decree on public regulated real estate companies. This date was not known by the Company on the date of the Securities Note. The Company proposes to apply for a permit as a public regulated real estate company, as provided for in the GVV Act. In view of the fact that the legal status of the Company will change, although it will continue to be subject to the current regulatory supervision of the FSMA, it will not be considered as an AIF and hence will not be subject to the AIFMD regulatory framework. Part of the transformation procedure requires the FSMA to grant the permit as a public regulated real estate company and approval by the extraordinary General Meeting of the Company. If for any reason the Company should fail to obtain a permit and approval as a public regulated real estate company, it will still be required to comply with the stipulations of the AICB Act and EMIR. If the Company were to be considered as an AIF under AIFMD (as transposed into Belgian law), this would affect the Company’s activities, operating results, profitability, financial health and prospects. Any additional obligations that might arise from the application of AIFMD could have an impact on the Company’s operating management, among other things (such as the mandatory appointment of a custodian). The Company would have to modify its existing organisation structure, rules and procedures, which would hinder its current operating model and require additional resources to implement and monitor these new obligations. Also, should the Company be considered an AIF, it could be affected by the application of other European Regulations and the transposition into Belgian law of any European Directives which apply (or are expected to apply in a more stringent matter) to AIFs, such as EMIR. If the Company, as an AIF, were to be subject to EMIR, it would be exposed to loss-making margin calls on its hedging instruments in order to protect itself (for example) against fluctuating interest percentages. Other relevant European Directives and Guidelines that might have an impact on the Company if it were to be considered an AIF, include “Basel III” (Proposal of Capital Requirement Directive and Regulation) and the “Financial Transaction Tax”. If the Company were to be recognised as a public regulated real estate company, this would involve the following risk. The loss by the Company of its status would constitute an event of default under the terms of most of the Company’s lines of credit, which would lead to liquidity and solvency risks and could have a detrimental impact on the Company’s activities, operating results, profitability, financial health and prospects. It would also result in the loss of the transparent fiscal regime.

c. FBI status In September 2013, Montea filed a request with the Dutch Tax Office for its Dutch subsidiaries, Montea Nederland NV and Montea Almere NV, to be qualified as “Fiscale Beleggingsinstelling” or “FBI” as provided by article 28 of the Dutch corporate Income tax law (Wet vennootschapsbelasting 1969) in terms of its Dutch real estate investments. This request is currently pending before the Dutch Ministry of Finance. Montea has also applied for a fiscal unity for Dutch corporate income tax purposes between Montea Nederland NV and Montea Almere NV. Montea Nederland NV established Montea Rotterdam NV in 2014. The Dutch Tax Administration has been requested to add Montea Rotterdam NV to the fiscal unity for Dutch corporate income tax purposes of Montea Nederland NV. The decision regarding the application for the FBI status with respect to Montea Nederland NV and Montea Almere NV will also cover the status of Montea

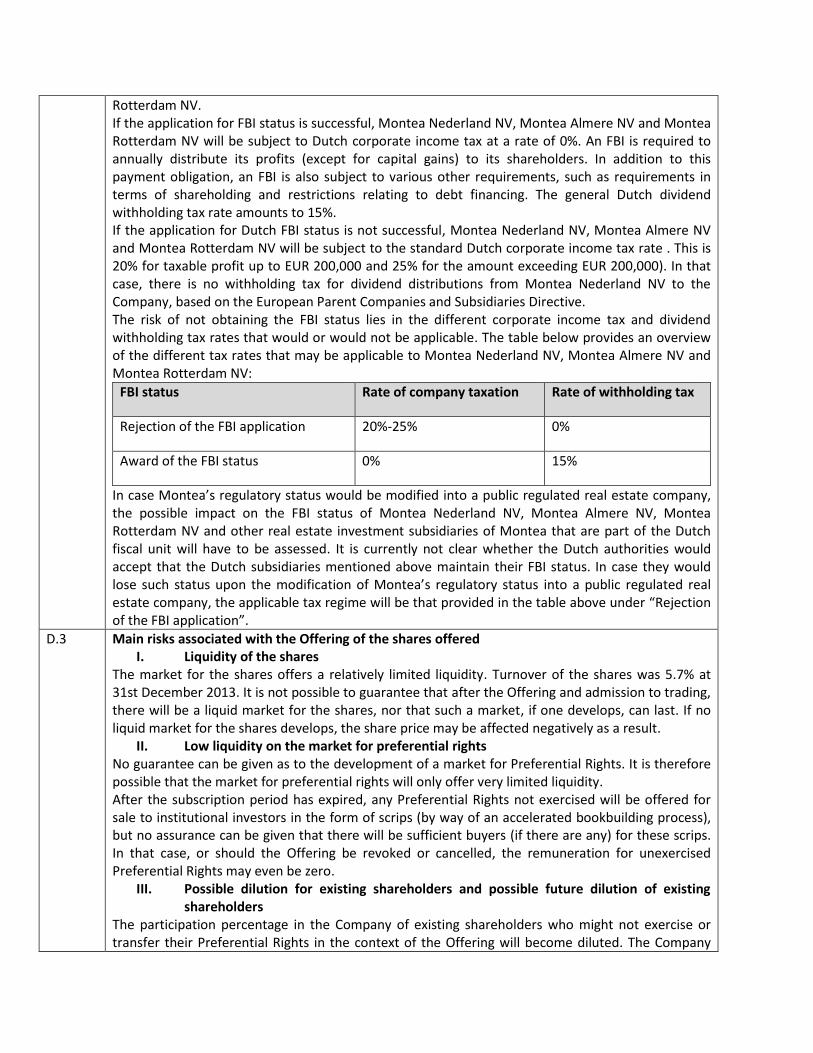

Rotterdam NV. If the application for FBI status is successful, Montea Nederland NV, Montea Almere NV and Montea Rotterdam NV will be subject to Dutch corporate income tax at a rate of 0%. An FBI is required to annually distribute its profits (except for capital gains) to its shareholders. In addition to this payment obligation, an FBI is also subject to various other requirements, such as requirements in terms of shareholding and restrictions relating to debt financing. The general Dutch dividend withholding tax rate amounts to 15%. If the application for Dutch FBI status is not successful, Montea Nederland NV, Montea Almere NV and Montea Rotterdam NV will be subject to the standard Dutch corporate income tax rate . This is 20% for taxable profit up to EUR 200,000 and 25% for the amount exceeding EUR 200,000). In that case, there is no withholding tax for dividend distributions from Montea Nederland NV to the Company, based on the European Parent Companies and Subsidiaries Directive. The risk of not obtaining the FBI status lies in the different corporate income tax and dividend withholding tax rates that would or would not be applicable. The table below provides an overview of the different tax rates that may be applicable to Montea Nederland NV, Montea Almere NV and Montea Rotterdam NV:

FBI status Rate of company taxation Rate of withholding tax

Rejection of the FBI application 20%-25% 0%

Award of the FBI status 0% 15%

In case Montea’s regulatory status would be modified into a public regulated real estate company, the possible impact on the FBI status of Montea Nederland NV, Montea Almere NV, Montea Rotterdam NV and other real estate investment subsidiaries of Montea that are part of the Dutch fiscal unit will have to be assessed. It is currently not clear whether the Dutch authorities would accept that the Dutch subsidiaries mentioned above maintain their FBI status. In case they would lose such status upon the modification of Montea’s regulatory status into a public regulated real estate company, the applicable tax regime will be that provided in the table above under “Rejection of the FBI application”.

D.3 Main risks associated with the Offering of the shares offered I. Liquidity of the shares

The market for the shares offers a relatively limited liquidity. Turnover of the shares was 5.7% at 31st December 2013. It is not possible to guarantee that after the Offering and admission to trading, there will be a liquid market for the shares, nor that such a market, if one develops, can last. If no liquid market for the shares develops, the share price may be affected negatively as a result.

II. Low liquidity on the market for preferential rights No guarantee can be given as to the development of a market for Preferential Rights. It is therefore possible that the market for preferential rights will only offer very limited liquidity. After the subscription period has expired, any Preferential Rights not exercised will be offered for sale to institutional investors in the form of scrips (by way of an accelerated bookbuilding process), but no assurance can be given that there will be sufficient buyers (if there are any) for these scrips. In that case, or should the Offering be revoked or cancelled, the remuneration for unexercised Preferential Rights may even be zero.

III. Possible dilution for existing shareholders and possible future dilution of existing shareholders

The participation percentage in the Company of existing shareholders who might not exercise or transfer their Preferential Rights in the context of the Offering will become diluted. The Company

could decide in the future to increase its capital, which could have a diluting effect for shareholders. IV. Withdrawal of the Offering – no minimum amount for the Offering

If the Offering is cancelled, the Preferential Rights will become invalid or without value. Accordingly, investors who have acquired these Preferential Rights will incur a loss given that transactions relating to these Preferential Rights will not be run down after the end of the Offering. The Company has the right to proceed with a capital increase for a maximum amount of EUR 52,526,232. However, no minimum amount is defined for the Offering. The ultimate number of New Shares subscribed to will be confirmed in the Belgian financial press. This means that the proceeds could be reduced or may have an effect on the intended appropriation of the proceeds. The minimum required free float of the shares of 30% must be respected at all times, regardless of the results of the Offering.

V. Volatility of the share price and yield The issue price can not be considered as indicative for the market price of the shares after the Offering.

VI. Fall in the price of the shares or the Preferential Rights on sale of the shares The sale of a number of shares or Preferential Rights on the market, or the impression of such sales taking place during the Offering with regard to the Preferential Rights, or during or after the Offering has taken place with regard to the shares, could have an unfavourable effect on the price of the shares or the Preferential Rights.

Section E — Offer

Element Disclosure requirement

E.1 Total net proceeds and estimated total costs of the issue/offer, including the estimated costs charged by the issuing institution or provider to the investor If the maximum Offering is subscribed to, the gross proceeds from the Offering (the issue price multiplied by the number of New Shares) will be a maximum of EUR 52,526,232. The costs associated with the Prospectus and the Offering are estimated at EUR 900,000 and include fees owed to the FSMA and Euronext Brussels, management fees, the cost for translating and distributing the Prospectus, legal and administrative fee and publication costs. The overall remuneration for the managers consists on the one hand of a fixed fee of EUR 175,000 and on the other hand of a variable fee equivalent to 1.75% of the gross proceeds of the Offering (the issue price multiplied by the number of New Shares, with the exception of those New Shares subscribed to by the major shareholders in accordance with their undertakings stated in the Securities Note). The overall remuneration for the managers is not capped. The net proceeds of the Offering are therefore estimated at approximately EUR 51.6 million. Subscription applications may be lodged free of charge with the managers or with those institutions via any other financial intermediaries. Shareholders are requested to obtain information about any costs charged by these other intermediaries.

E.2.a Reasons for the offer, use of the proceeds, estimated net proceeds The net revenue from the Offering, if it is subscribed to in full, is estimated at approximately EUR 51.6 million (after deduction of costs and expenses that the Company is required to pay). Montea plans to use the net proceeds from the Offering to continue its growth strategy and hence expand its real estate portfolio further within the debt ratio bracket of 50 to 55% that the board of directors is trying to achieve (this does not exclude this bracket being exceeded for brief periods of time). The Company’s debt ratio was 55.11% at 31st March 2014. The Company plans to use the majority of

the net proceeds from the Offering to fund an acquisition programme. Since the end of the 2013 financial year, the Company has already announced the following transactions for a total of EUR 80.2 million. In Belgium: acquisition of a building in Puurs, build-to-suit project for Dachser at MG Park De Hulst in Willebroek, build-to-suit project for Metro at the Montea site in Vorst, renovation and extension for Caterpillar at the Montea site (co-owned with WDP) in Grimbergen and a second and third build-to-suit project with MG Real Estate at Park De Hulst in Willebroek. In the Netherlands: acquisition of a building in Waddinxveen and a build-to-suit project in Oss for Vos Logistics. The investments that Montea will make in various build-to-suit, renovation and extension projects, as stated above, are expected in the final three quarters of 2014. In the meantime, Montea will use the surplus net income from the Offering to repay long-term loans that can be drawn down again later. At the date of the Securities Note, Montea is unable to say with certainty what the use of the proceeds from the Offering will be. The Company will, at its discretion, determine the amounts as well as the timing of the actual investments and this will depend on various factors, such as movements in the debt ratio, the availability of the various investment opportunities, the fulfilment of the suspensive conditions in the build-to-suit projects, the timing of handover in the build-to-suit projects and the actual net proceeds from the Offering, as well as Montea’s operating costs and expenses. This will give the Company’s management a high degree of flexibility in spending the net proceeds from this Offering. The Company will issue information about how the resources will be used at the appropriate time and will specify what the resources obtained will be spent on.

E.3 Description of the terms of the offer 1. General

The Company’s manager decided on 2nd June 2014 to increase the Company’s capital within the framework of the permitted capital via a maximum injection in cash of EUR 52,526,232, including any issue premium, in compliance with the Preferential Rights of the existing shareholders in the proportion of 2 New Shares for 7 existing shares owned. The issue price per New Share is EUR 27. The planned operation consists on the one hand of a public offer to subscribe to New Shares (by exercising Preferential Rights that are either already held by existing shareholders, or are acquired during the subscription period), and on the other of a private placement of the scrip. The New Shares can be subscribed to by exercising Preferential Rights or scrips. If all of the offered shares are not subscribed to, the capital increase will still proceed in the amount of the subscriptions received, unless the Company decides otherwise. The capital increase will also be decided on subject to the following suspensive conditions: - approval of the amendment to the articles of association, the Securities Note and the Summary

by the FSMA; - the underwriting agreement has been signed and is not terminated in accordance with its terms

and conditions; and - confirmation of the admission to trading of (i) the Preferential Rights on Euronext Brussels

(from the time of detachment of coupon nº 12) and (ii) the New Shares on Euronext Brussels and Euronext Paris from the time of issue. 2. Establishment of the issue price

The issue price for each New Share is EUR 27 and was set by Montea in consultation with the joint bookrunners, based on the price of the share on Euronext Brussels and Euronext Paris, including a

discount that will be applied in the usual way for this type of transaction. The issue price is 16.3% lower than the closing price of the share on Euronext Brussels on 30th May 2014 (which was EUR 33.20), adjusted to take account of the estimated value of coupon nº 139 which was detached on 2nd June 2014 (after the markets closed), i.e. EUR 32.26 after this adjustment. The issue price is 16.8% higher than the intrinsic value of the share, adjusted by the negative variation in the fair value of the hedging instruments as of 31st March 2014, which is EUR 23.12.

3. Total amount of the Offering The total amount of the Offering is a maximum of EUR 52,526,232, any issue premium included. However, there is not minimum defined for the Offering. The Company has the right to proceed with a capital increase for a lower amount.

4. Terms of subscription - Subscription period The subscription period will run from 3rd June 2014 to 17th June 2014 inclusive. - Subscription ratio The holders of Preferential Rights can subscribe to the New Shares at a subscription ratio of 2 New Shares for 7 existing shares or Preferential Right held. - Trading of Preferential Rights The Preferential Rights are materialised via coupon nº 12 of the existing shares. Each share gives an entitlement to one Preferential Right. The Preferential Rights, in the form of coupon nº 12 of the shares, will be detached on 2nd June 2014 after Euronext Brussels closes and can be traded throughout the entire subscription period on Euronext Brussels (ISIN code BE0970132354). Investors wishing to sign up for the Offering via a purchase of Preferential Rights can do so by lodging a purchase order for Preferential Rights with their financial institution with a simultaneous subscription order. Those existing shareholders who do not hold the exact number of Preferential Rights to be able to subscribe to the full number of New Shares can either buy the Preferential Rights lacking during the subscription period, or else sell any ‘surplus’ Preferential Rights. There can never be an undivided subscription: the Company will only acknowledge one owner per share. Existing shareholders who at the end of the subscription period, i.e. 17th June 2014, who have not used their Preferential Rights, can no apply it after this date. - Private placement of scrip Unexercised Preferential Rights will be represented by scrips, which will be sold by the managers to institutional investors by way of an accelerated bookbuilding process (i.e. a private placement in the form of a bookbuilding procedure). The private placement of the scrips will take place as soon as possible after the subscription period has closed, and in principle on 19th June 2014. Buyers of scrips may subscribe to New Shares at the same price and in the same proportion as subscribing via the exercise of Preferential Rights. The price at which the scrips are sold will be determined by the Company, assisted by the joint bookrunners, taking the results of the bookbuilding into account. The net proceeds from the sale of the scrisp, minus costs, will be made available by the Company to the holders of coupon nº 12 who did not exercise their Preferential Rights during the subscription period and will be paid to them on delivery of coupon nº 12 from 27th June 2014. If the net proceeds divided by the total number of

9 This estimated value is EUR 0.94 and of course remains subject to approval by the general meeting of shareholders on 19th May 2015, which will decide on the dividend to be paid out in relation to the 2014 financial year.

Preferential Rights exercised is less than EUR 0.05, they will not be distributed to holders of unexercised Preferential Rights, but transferred to the Company. The amount available for distribution will be published in the Belgian financial press on 20th June 2014.

5. Withdrawal or suspension of the Offering The Company has the right to proceed with a capital increase for a lower amount. The Company reserves the right, during or after the subscription period, to revoke or suspend the Offering if no underwriting agreement has been signed or if an event occurs after the beginning of the subscription period that enables the managers to terminate the underwriting agreement, on condition that the consequences of such an event would probably have a significant and negative effect on the success of the Offering or trade in the New Shares on the secondary markets. If the Company decides to revoke or suspend the Offering, a press announcement will be published by Montea and, insofar as this event requires the Company to publish an addendum to the Prospectus, an addendum will be published.

6. Option to reduce subscriptions Applications to subscribe with Preferential Rights will be implemented in full.

7. Withdrawal of orders Purchase orders are irrevocable subject to the stipulation that states that subscriptions may be withdrawn in the event of the publication of a supplement to the Prospectus within a period of two working days after this publication.

8. Payment and delivery of the shares offered Payment of the subscriptions via Preferential Rights or scrips will be made by debit from the purchaser’s account, with a value date of 24th June 2014. At the discretion of the buyer, the New Shares will be made available in dematerialised form in an account with a financial intermediary, or in registered form, depending on the preference of the buyer.

9. Publication of the results of the Offering The results of the subscriptions by exercise of Preferential Rights and scrips will be published in the Belgian financial press on 20th June 2014. The amount accruing to the holders of unexercised Preferential Rights will also be published in the Belgian financial press on 20th June 2014.

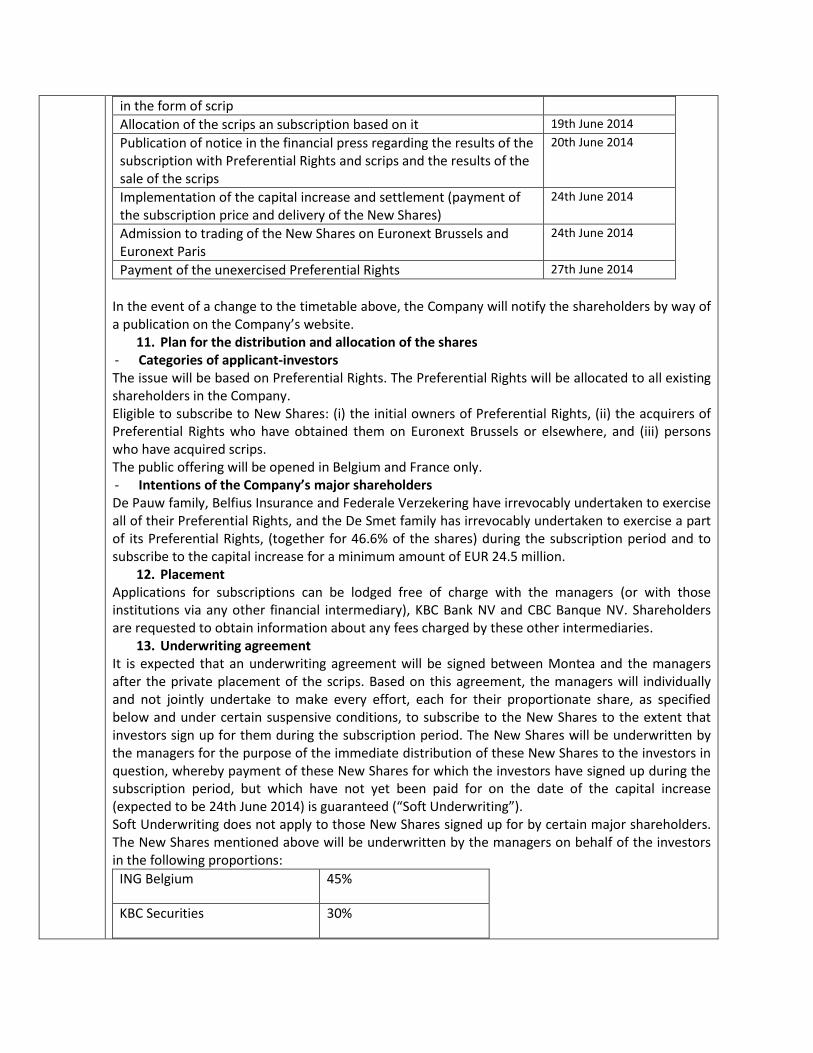

10. Planned timetable for the Offering

Publication of the announcement in the press and in the Belgian Official Gazette, as required by article 593 of the Companies’ Code

23rd May 2014

In-principle decision by the manager to increase the Company’s capital and establishment of the issue price/subscription ratio/amount of the Offering

2nd June 2014

Detachment of coupon nº 12 regarding Preferential Rights (post-closure of the market)

2nd June 2014

Detachment of coupon nº 13 regarding pro rata dividend (post-closure of the market)

2nd June 2014

Publication in the financial press of the notice regarding the Offering (issue price/subscription ratio/amount of the Offering)

3rd June 2014

Availability to the public of the Prospectus (with the issue price) 3rd June 2014

Opening of the subscription with Preferential Rights 3rd June 2014

Closure of the subscription with Preferential Rights 17th June 2014

Press release announcing the of the Offering of Preferential Rights 19th June 2014

Accelerated private placement of the unexercised Preferential Rights 19th June 2014

in the form of scrip

Allocation of the scrips an subscription based on it 19th June 2014

Publication of notice in the financial press regarding the results of the subscription with Preferential Rights and scrips and the results of the sale of the scrips

20th June 2014

Implementation of the capital increase and settlement (payment of the subscription price and delivery of the New Shares)

24th June 2014

Admission to trading of the New Shares on Euronext Brussels and Euronext Paris

24th June 2014

Payment of the unexercised Preferential Rights 27th June 2014

In the event of a change to the timetable above, the Company will notify the shareholders by way of a publication on the Company’s website.

11. Plan for the distribution and allocation of the shares - Categories of applicant-investors The issue will be based on Preferential Rights. The Preferential Rights will be allocated to all existing shareholders in the Company. Eligible to subscribe to New Shares: (i) the initial owners of Preferential Rights, (ii) the acquirers of Preferential Rights who have obtained them on Euronext Brussels or elsewhere, and (iii) persons who have acquired scrips. The public offering will be opened in Belgium and France only. - Intentions of the Company’s major shareholders De Pauw family, Belfius Insurance and Federale Verzekering have irrevocably undertaken to exercise all of their Preferential Rights, and the De Smet family has irrevocably undertaken to exercise a part of its Preferential Rights, (together for 46.6% of the shares) during the subscription period and to subscribe to the capital increase for a minimum amount of EUR 24.5 million.

12. Placement Applications for subscriptions can be lodged free of charge with the managers (or with those institutions via any other financial intermediary), KBC Bank NV and CBC Banque NV. Shareholders are requested to obtain information about any fees charged by these other intermediaries.

13. Underwriting agreement It is expected that an underwriting agreement will be signed between Montea and the managers after the private placement of the scrips. Based on this agreement, the managers will individually and not jointly undertake to make every effort, each for their proportionate share, as specified below and under certain suspensive conditions, to subscribe to the New Shares to the extent that investors sign up for them during the subscription period. The New Shares will be underwritten by the managers for the purpose of the immediate distribution of these New Shares to the investors in question, whereby payment of these New Shares for which the investors have signed up during the subscription period, but which have not yet been paid for on the date of the capital increase (expected to be 24th June 2014) is guaranteed (“Soft Underwriting”). Soft Underwriting does not apply to those New Shares signed up for by certain major shareholders. The New Shares mentioned above will be underwritten by the managers on behalf of the investors in the following proportions:

ING Belgium 45%

KBC Securities 30%

Belfius Bank 25%

100%

It is expected that the Company will declare certain representation & warranties in the underwriting agreement, will give guarantees and will indemnify the managers for certain liabilities. It is expected that the underwriting agreement will also state that if certain events occur, such as: - the suspension of trading on Euronext Brussels and Euronext Paris or a substantial and

detrimental change occurs in the financial situation or business activities of Montea or in the financial markets, or miscellaneous cases of force majeure; or

- some of the major shareholders have not exercised all of their subscription rights before the end of the subscription period and have validly subscribed to the corresponding number of New Shares or have not paid for these shares by the date of the capital increase; or

- the suspensive conditions in the underwriting agreement have not been or are no longer complied with;

the managers will have the right, under certain conditions and after consultation with Montea, to terminate the underwriting agreement prior to the date on which the capital increase was to take place. The Company may withdraw or suspend the operation. If this is the case, Montea will publish an addendum to the Prospectus that will be subject to the approval of the FSMA. In that case, subscriptions to the Offering with Preferential Rights and subscriptions to the private placement of scrips will automatically be withdrawn.

E.4 Description of all interests, including conflicting interests, of significance for the issue/offer 1. Interests of the managers

The managers have signed an engagement letter with the Company for the Offering and will, in principle, sign an underwriting agreement at the latest on the day after the private placement of the scrips. In addition: - they have granted, and will grant in the future, various banking services, investment services,

commercial and other services to the Company or its shareholders in the context of which they may collect remuneration; and

- the managers have agreed financing contracts and hedging instruments with the Company10. It is possible that the managers, from time to time, will retain shares, debt instruments or other financial instruments from the Company. In particular, Belfius Insurance, a subsidiary of Belfius Bank, owns 898,139 shares, representing 13.2% of the Company’s share capital. Belfius Insurance, whose permanent representative is Dirk Vanderschrick, is also a member of the Board of Directors of the manager. The managers are credit-providers as part of credit agreements and may in the future provide additional banking and commercial services to the Company for which they could receive remuneration and commission.

2. Conflicts of interest Federale Verzekering, Belfius Insurance, PSN Management BVBA and DDP Management BVBA, which are all directors of the manager, have indicated that they, or persons associated with them,

10 The financing contracts include long-term and short-term funding with variable interest rates. The Company has entered into lines of credit with the managers for a total of EUR 125,000,000, of which on the date of the Securities Note, EUR 105,500,000 was drawn down (i.e. EUR 23,166,667 in the short term and EUR 82,333,333 in the long term). The Company has insured itself against variable interest rates by taking out hedging contracts of the “IRS” (“Interest Rate Swaps”) type with the managers for a total contracted amount of EUR 138,425,000.

will subscribe to the Offering. The other directors of the manager own no shares in the Company. Pursuant to article 18 of the Royal Decree of 7th December 2010, the persons and entities

mentioned above have a conflict of interest with the Offering. Pursuant to article 18 §2 and §3 of

the Royal Decree of 7th December 2010, the manager declares that the Offering and the capital

increase arising therefrom (i) are in the interests of the Company, (ii) form part of the Company’s

investment policy, and (iii) is being carried out under normal market conditions. Pursuant to article

18 of the Royal Decree of 7th December 2010, the following persons and entities could have a

possible a conflict of interest in relation to the Offering if they intend to subscribe to New Shares

and/or acquire New Shares later: