Strategic Market Planning Chapter Eleven M arket-Based Management, 4 th edition.

Upload

mohammed-shefinCategory

view

61download

0

Dr.Sunitha.SAssistant Professor

School of Management Studies,National Institute of Technology (NIT) Calicut

MONETARY ECONOMICS:

Financial System

Financial system: Formal financial sector:presence of an

orgnaised,instituional and regulated system Informal financial sector Is an

unorganised,non instituional and noin regulated system

Resulting in “ financial dualism”

2

Formal sector comes under the purview of the misnitsry of finance(MoF),RBI and Securities and Exchange Board of India(SEBI) & Insurance Regulatory and Development Authority(IRDA).

Infrmal scetor :consists of moneylenders,pawn brokers,funds or associations doing finance business,chit fund companies,local brokers etc

3

4

Monetary Economics studies about…… Banks Money market Capital Market Non Bank Financial Intermediaries Unregulated Credit Markets

5

And aspects of stock market like………. Stock Exchanges BSE NSE NIFTY SENSEX Bulls &Bears

6

Some basic stuff

Credit Liquidity Inflation Monetary Policy Fiscal Policy

7

“Inflation is too much money chasing too few goods”

Demand pull or cost push inflation

8

Banking

Central Bank Commercial Banks Development Banks Cooperative banks

9

1. Accepting of deposits Current deposit Account - withdraw money at any time – no interest Fixed deposit - money deposited in the account is for very short

period. – high rate of interest – term deposit – matures at a definite period.

Savings deposit Account – some restrictions. – minimum amount of money – interest rate is low.

2. Granting of loans and advances Loans- Overdraft – draft in excess of credit balance – for the reliable

customer.

10

Reserve Bank of India

Currency Authority Banker to Govt Bankers’ Bank Controller of money supply & credit Exchange Management & control

11

Non Bank Financial Intermediaries (NBFIs) Mutual Funds (UTI) Insurance companies

(LIC & GIC) Provident/Pension

Funds Post Offices Savings Other NBFIs

Money Lenders Chit funds Hire Purchase/Leasing

companies

Regulated Unregulated

Financial System

13

Financial System

Financial institutions Commercial banks, RBI, NBFIs, companies

Financial Assets Currency, deposits, cheques, bills, bonds, shares, Equities, debentures, T-bills, certificates of deposits,

commercial papers

Financial markets Money market (short term funds) Capital market (medium & long term funds)

Primary Market (New Issue Market) Secondary Market (Stock Market)

14

Money Market

15

Money Market

Market in which short term funds are borrowed and lent ( maturity below one year) are called as money market.

Call Money Market Commercial Bill Market Treasury Bill Market Certificate of Deposit Commercial Paper

Submarkets

16

Call Money Market

Deals with one day loans (called as call loans or call money) as well as loans up to 15 days

Who are the Participants? usually banks, Mutual funds, large corporations

and insurance companies are able to participate in this market.

borrowers are banks who are temporarily short of funds

Suppliers are banks with temporary excess of cash

The rate at which the call loan is lent is called as call rate.

The rate of interest is always higher than savings account rate.

The loans in the call money market are very short, usually lasting no longer than a week and are often used to help banks meet reserve requirements.

17

Money lent for a day is called as call money and for a period more than a day is called as notice money and money lent for 15 days or more days is called term money.

Helps in maintaining liquidity, controlling inflation, fill the gaps or temporary mismatches in funds and also determining the interest rates in the economy

Need based market where in demand and supply of money shape in the market

18

19

Commercial Bill market

Bill of Exchange (BOE) is like a promissory note ,which has a maturity period of 3 months.

“I owe you so and so amount of money after 3 months from the present date.”

Either the BOE holder could wait till it gets matured or get it discounted or get encashed through the process of discounting

20

Treasury Bill market

T Bills are short term debt instruments issued by the Govt to get funds.

Who are the participants? Borrowers: mostly commercial banks Lender: Govt departments

Sold by RBI through auction Maturity: 91days,182 days,365 days Zero default risk and hence more safer

Treasury Bills

Treasury bills, commonly referred to as T-Bills are issued by Government of India against their short term borrowing requirements with maturities ranging between 14 to 364 days.

All these are issued at a discount-to-face value. For example a Treasury bill of Rs. 100.00 face value issued for Rs. 91.50 gets redeemed at the end of it's tenure at Rs. 100.00.

Who can invest in T-Bill Banks, Primary Dealers, State Governments, Provident

Funds, Financial Institutions, Insurance Companies, NBFCs, FIIs (as per prescribed norms), NRIs can invest in T-Bills.

• At present, the Government of India issues three types of treasury bills through auctions, namely, 91-day, 182-day and 364-day. There are no treasury bills issued by State Governments.

• Eligible to be included for SLR purpose• Amount• Treasury bills are available for a minimum

amount of Rs.25,000 and in multiples of Rs. 25,000. Treasury bills are issued at a discount and are redeemed at par.

Gilt Edged security Government security that is a claim on the government and is a secured financial instrument which guarantees certainty of both capital and interest. These securities are free of default risk or credit risk, which leads to low market risk and high liquidity.

23

24

Certificate of Deposit (CD)

CDs are short-term borrowings issued by banks and are freely transferable by endorsement and delivery.

Borrowed mainly by banks• Minimum period 7 days• Maximum period 1 year

CD s are issued generally when banks face tight liquidity,and are issued at relatively high interest rates.

CDs are issued when the deposit growth is sluggish but credit demand is high.

25

26

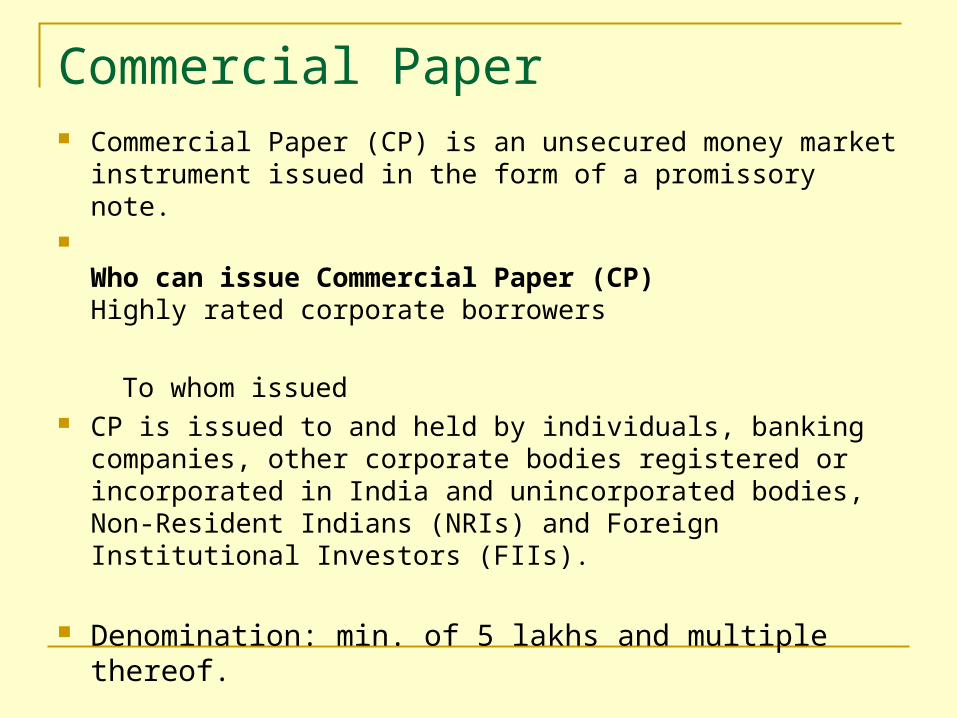

Commercial Paper(CP)

Direct short term finance issued by large creditworthy companies

Borrowed by banks, companies Maturity : 7 days to 3 months to one year Also known as Industrial paper,corporate

paper and industrial paper.

Commercial Paper Commercial Paper (CP) is an unsecured money market instrument

issued in the form of a promissory note.

Who can issue Commercial Paper (CP) Highly rated corporate borrowers

To whom issued CP is issued to and held by individuals, banking companies, other

corporate bodies registered or incorporated in India and unincorporated bodies, Non-Resident Indians (NRIs) and Foreign Institutional Investors (FIIs).

Denomination: min. of 5 lakhs and multiple thereof.

Some important Ratios

Bank rate CRR SLR Repo Rate Reverse Repo Rate

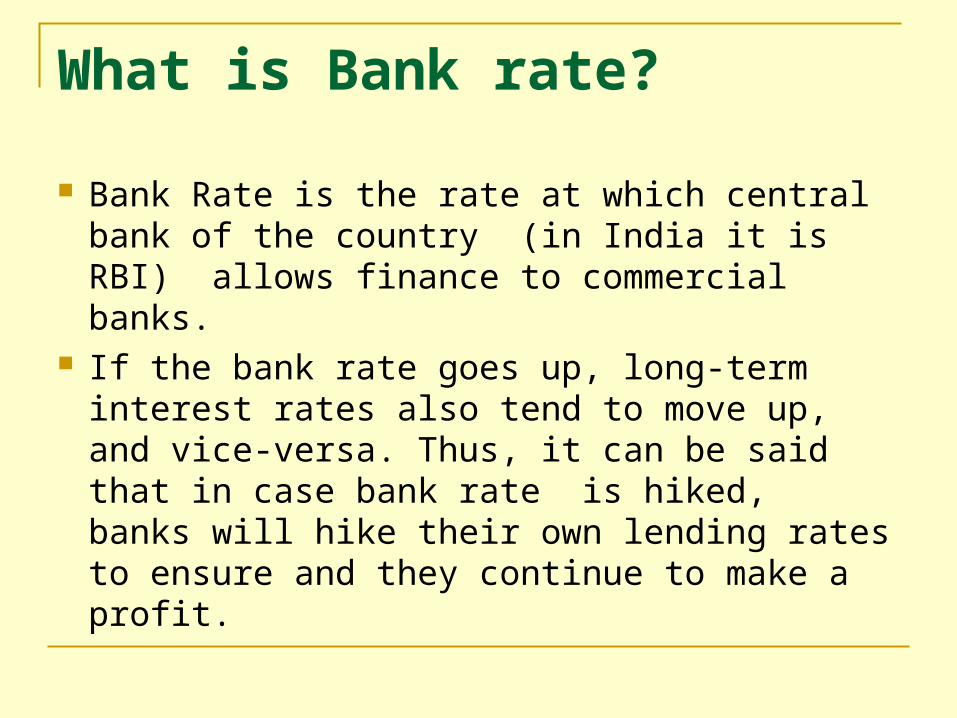

What is Bank rate?

Bank Rate is the rate at which central bank of the country (in India it is RBI) allows finance to commercial banks.

If the bank rate goes up, long-term interest rates also tend to move up, and vice-versa. Thus, it can be said that in case bank rate is hiked, banks will hike their own lending rates to ensure and they continue to make a profit.

What is CRR?

CRR means Cash Reserve Ratio. Banks in India are required to hold a certain

proportion of their deposits in the form of cash. However, actually Banks don’t hold these as cash with themselves, but deposit such case with Reserve Bank of India (RBI) / currency chests, which is considered as equivalent to holding cash with themselves..

CRR This minimum ratio (that is the part of the total deposits

to be held as cash) is stipulated by the RBI and is known as the CRR or Cash Reserve Ratio.

Thus, When a bank’s deposits increase by Rs100, and if

the cash reserve ratio is 9%, the banks will have to hold additional Rs 9 with RBI and Bank will be able to use only Rs 91 for investments and lending / credit purpose. Therefore, higher the ratio (i.e. CRR), the lower is the amount that banks will be able to use for lending and investment. This power of RBI to reduce the lendable amount by increasing the CRR, makes it an instrument in the hands of a central bank through which it can control the amount that banks lend. Thus, it is a tool used by RBI to control liquidity in the banking system

What is SLR?

SLR stands for Statutory Liquidity Ratio. indicates the minimum percentage of

deposits that the bank has to maintain in form of gold, cash or other approved securities.

Controls the credit growth in the economy

REPO RATE

Repo (Repurchase) rate is the rate at which the RBI lends short-term money to the banks. When the repo rate increases borrowing from RBI becomes more expensive. Therefore, we can say that in case, RBI wants to make it more expensive for the banks to borrow money, it increases the repo rate; similarly, if it wants to make it cheaper for banks to borrow money, it reduces the repo rate

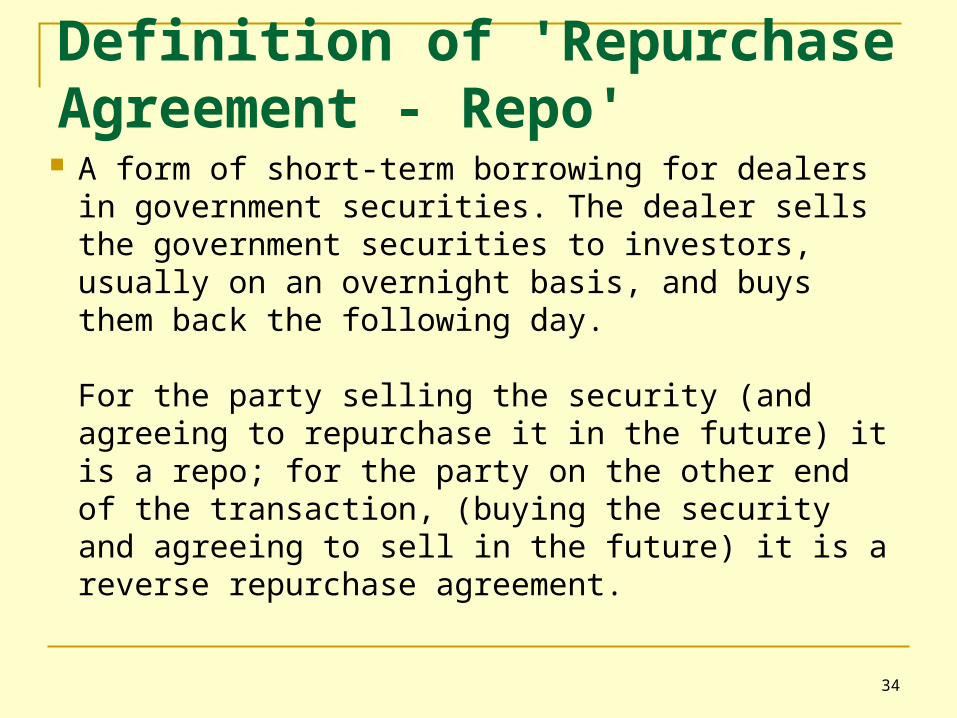

Definition of 'Repurchase Agreement - Repo' A form of short-term borrowing for dealers in

government securities. The dealer sells the government securities to investors, usually on an overnight basis, and buys them back the following day.

For the party selling the security (and agreeing to repurchase it in the future) it is a repo; for the party on the other end of the transaction, (buying the security and agreeing to sell in the future) it is a reverse repurchase agreement.

34

REVERSE REPO RATE

Reverse Repo rate is the rate at which banks park their short-term excess liquidity with the RBI. The RBI uses this tool when it feels there is too much money floating in the banking system. An increase in the reverse repo rate means that the RBI will borrow money from the banks at a higher rate of interest. As a result, banks would prefer to keep their money with the RBI

REPO RATE Vs REVERSE REPO RATE

Thus, we can conclude that Repo Rate signifies the rate at which liquidity is injected in the banking system by RBI, whereas Reverse repo rate signifies the rate at which the central bank absorbs liquidity from the banks.

Repo rate, also called repurchase rate, is the rate of interest that banks pay when they borrow money from the Reserve Bank of India to meet their short-term fund requirements. This is called repurchase rate because when they borrow money from the RBI, they keep government securities with the central bank as collateral. When they pay the money back to RBI, they take the collateral back.

37

Reverse repo rate is the rate of interest that banks get when they keep their surplus money with the RBI. Repo rate is always higher than the reverse repo rate. At present, the repo rate is 7.75% per annum and the reverse repo rate is 6.75%.

By controlling these rates, the RBI controls the rate of interest in the economy.

38

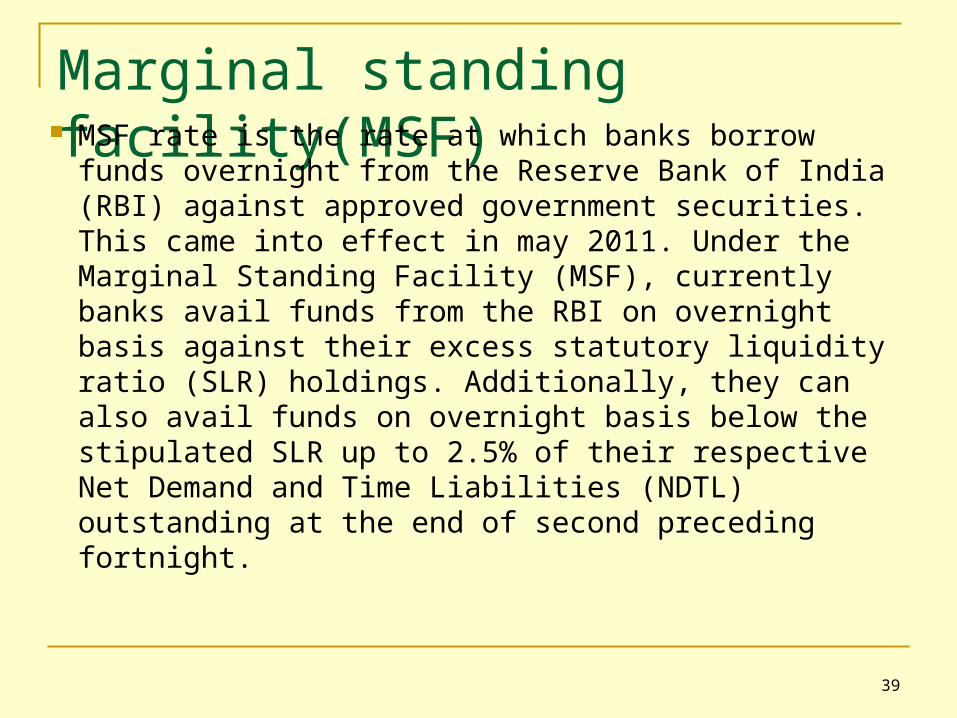

Marginal standing facility(MSF) MSF rate is the rate at which banks borrow funds

overnight from the Reserve Bank of India (RBI) against approved government securities. This came into effect in may 2011. Under the Marginal Standing Facility (MSF), currently banks avail funds from the RBI on overnight basis against their excess statutory liquidity ratio (SLR) holdings. Additionally, they can also avail funds on overnight basis below the stipulated SLR up to 2.5% of their respective Net Demand and Time Liabilities (NDTL) outstanding at the end of second preceding fortnight.

39

Recent Rates Issued by RBI(as of 31 October,2012 & 3 April 2013 & 11 November 2013) Bank rate 9% 8.5% 8.75 Repo rate 8% 7.5% 7.75 Reverse repo rate 7% 6.5% 6.75 CRR 4.5% 4.0 4.0 SLR 23% 23% 23 Marginal Standing 9% 8.75

Facility (MSF)

41

Thank You