Money, Banking and Financial Market Statistics - European Central

297

MONEY, BANKING AND FINANCIAL MARKET STATISTICS IN THE ACCESSION COUNTRIES VOLUME I May 2003 EUROPEAN CENTRAL BANK BCE ECB EZB EKP EKT MONEY, BANKING AND FINANCIAL MARKET STATISTICS IN THE ACCESSION COUNTRIES METHODOLOGICAL MANUAL VOLUME I May 2003

Transcript of Money, Banking and Financial Market Statistics - European Central

MO

NE

Y, B

AN

KIN

G A

ND

FIN

AN

CIA

L M

AR

KE

T S

TA

TIS

TIC

S I

N T

HE

AC

CE

SS

ION

CO

UN

TR

IES

V

OL

UM

E I

M

ay 2

003

E

UR

OP

EA

N C

EN

TR

AL

BA

NK

BC

E

EC

B

EZ

B

EK

P

EK

T

MONEY, BANKING ANDFINANCIAL MARKETSTATISTICS IN THE

ACCESSION COUNTRIES

METHODOLOGICAL MANUAL

VOLUME I

May 2003

THE CURRENT DEFINITIONAND STRUCTURE OF MONEYAND BANKING STATISTICS

IN THE ACCESSION COUNTRIES

May 2003

© European Central Bank, 2003

Address Kaiserstrasse 29

D-60311 Frankfurt am Main

Germany

Postal address Postfach 16 03 19

D-60066 Frankfurt am Main

Germany

Telephone +49 69 1344 0

Internet http://www.ecb.int

Fax +49 69 1344 6000

Telex 411 144 ecb d

All rights reserved.

Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

ISBN 92-9181-342-7 (print)

ISBN 92-9181-343-5 (online)

3ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

Contents

List of Contributors .................................. 9

Foreword ....................................................... 11

Introduction to the countrychapters ......................................................... 13

Summary of progress ............................... 16

Bulgaria ....................................................... 27

List of abbreviations .................................. 28

1 Legal and institutionalbackground .......................................... 29

1.1 Organisational structure ....................... 29

1.2 Legal background .................................... 29

1.3 Institutional aspects ............................... 29

2 Monetary statistics .......................... 33

2.1 Legal background and statisticalstandards .................................................. 33

2.2 Concepts and definitions ...................... 34

2.3 Monetary institutions ............................ 38

2.4 Banking business: generaldeposits/other products ....................... 39

2.5 Statistical balance sheets ofthe monetary institutions ..................... 39

2.6 Measure(s) of money: definitionsand remarks ............................................. 41

2.7 Counterparts of money ........................ 42

2.8 Reserve money ....................................... 43

2.9 Reporting procedures ........................... 43

2.10 Data processing and compilationmethods .................................................... 44

2.11 Publications .............................................. 45

3 Contacts at the BulgarianNational Bank ..................................... 46

Cyprus ......................................................... 49

List of abbreviations .................................. 50

1 Legal and institutionalbackground .......................................... 51

1.1 Organisational structure ....................... 51

1.2 Legal background .................................... 51

1.3 Institutional aspects ............................... 54

2 Monetary statistics .......................... 61

2.1 Legal background and statisticalstandards .................................................. 61

2.2 Concepts and definitions ...................... 61

2.3 Population of monetaryinstitutions ............................................... 65

2.4 Banking business: generaldeposits/other products ....................... 66

2.5 Statistical balance sheets of themonetary institutions ............................ 66

2.6 National measure(s) of money:definitions and remarks ......................... 69

2.7 Counterparts of money ........................ 69

2.8 Reserve money ....................................... 70

2.9 Reporting procedures ........................... 70

2.10 Data processing and compilationmethods .................................................... 72

2.11 Publications .............................................. 72

3 Contacts at theCentral Bank of Cyprus ................ 73

Annexes ......................................................... 74

Central Bank of Cyprus OrganisationStructure ........................................................... 74

Annexes ......................................................... 47

Organisation chart of the BulgarianNational bank (BNB) ........................................ 47

Statistics Directorate ....................................... 48

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 20034

Estonia ......................................................... 101

List of abbreviations .................................. 102

1 Legal and institutionalbackground .......................................... 103

1.1 Organisational structure ....................... 103

1.2 Legal background .................................... 103

1.3 Institutional aspects ............................... 104

2 Monetary statistics .......................... 109

2.1 Legal background andstatistical standards ................................ 109

2.2 Concepts and definitions ...................... 109

2.3 Population of monetaryinstitutions ............................................... 109

2.4 Banking business: generaldeposits/other products ....................... 113

2.5 Statistical balance sheets of themonetary institutions ............................ 114

2.6 Measure(s) of money: definitionsand remarks ............................................. 115

2.7 Counterparts of money ........................ 116

2.8 Reserve money ....................................... 117

2.9 Reporting procedures ........................... 117

2.10 Data processing and compilationmethods .................................................... 119

2.11 Publications .............................................. 119

3 Contacts at the Bankof Estonia ............................................. 120

Annexes ......................................................... 121

Organisation chart of the Bankof Estonia ........................................................... 121

Organisation chart of the StatisticsDepartment and Financial StabilityDepartment of the Bank of Estonia .............. 122

Hungary ....................................................... 123

List of abbreviations .................................. 124

1 Legal and institutionalbackground .......................................... 125

1.1 Organisational structure ....................... 125

Czech Republic ....................................... 75

List of abbreviations .................................. 76

1 Legal and institutionalbackground .......................................... 77

1.1 Organisational structure ....................... 77

1.2 Legal background .................................... 77

1.3 Institutional aspects ............................... 79

2 Monetary statistics .......................... 82

2.1 Legal background and statisticalstandards .................................................. 82

2.2 Concepts and definitions ...................... 84

2.3 Population of monetaryinstitutions ............................................... 85

2.4 Banking business: generaldeposits/other products ....................... 87

2.5 Statistical balance sheets of themonetary financial institutions ............. 88

2.6 Measure(s) of money:definitions and remarks ......................... 89

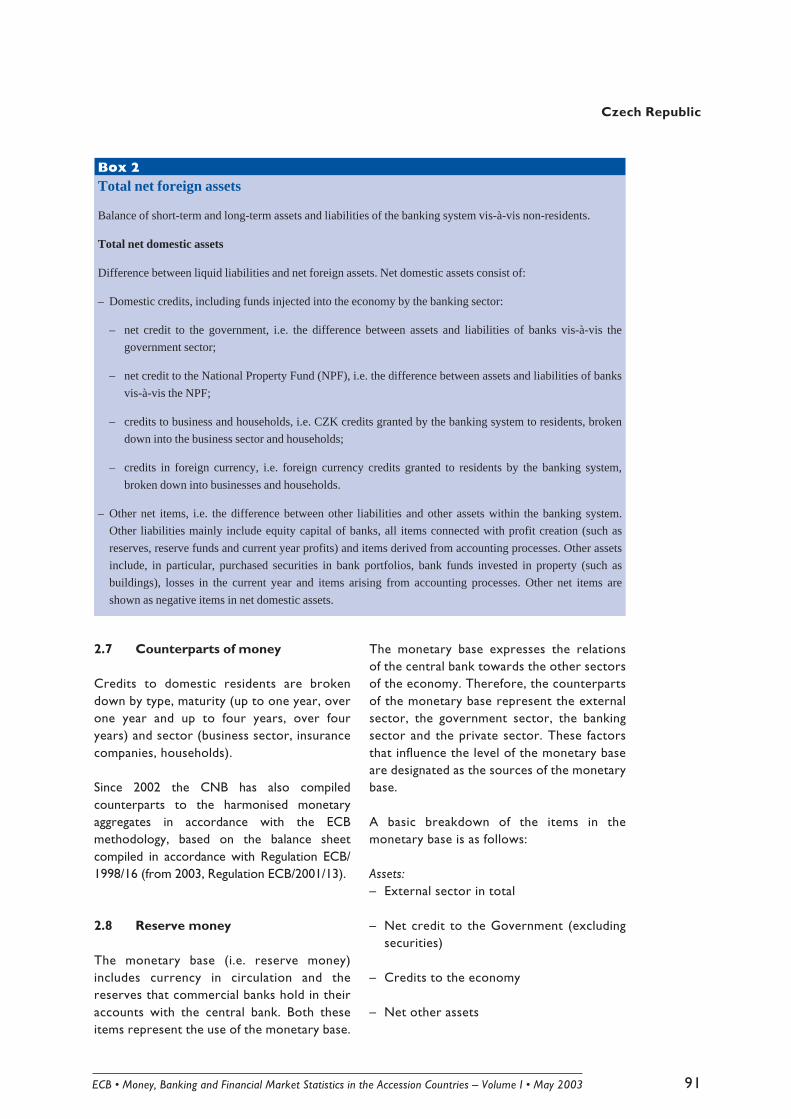

2.7 Counterparts of money ........................ 91

2.8 Reserve money ....................................... 91

2.9 Reporting procedures ........................... 92

2.10 Data processing and compilationmethods .................................................... 95

2.11 Publications .............................................. 96

3 Contacts at theCzech National Bank ..................... 97

Annex .............................................................. 98

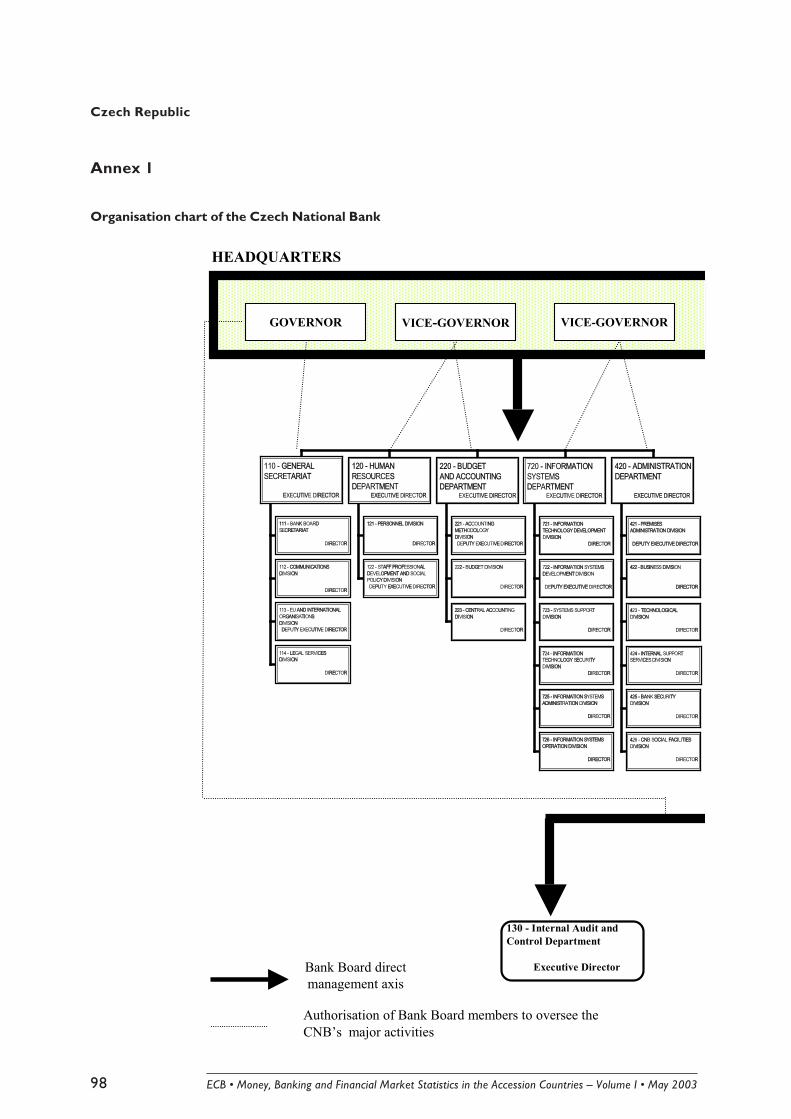

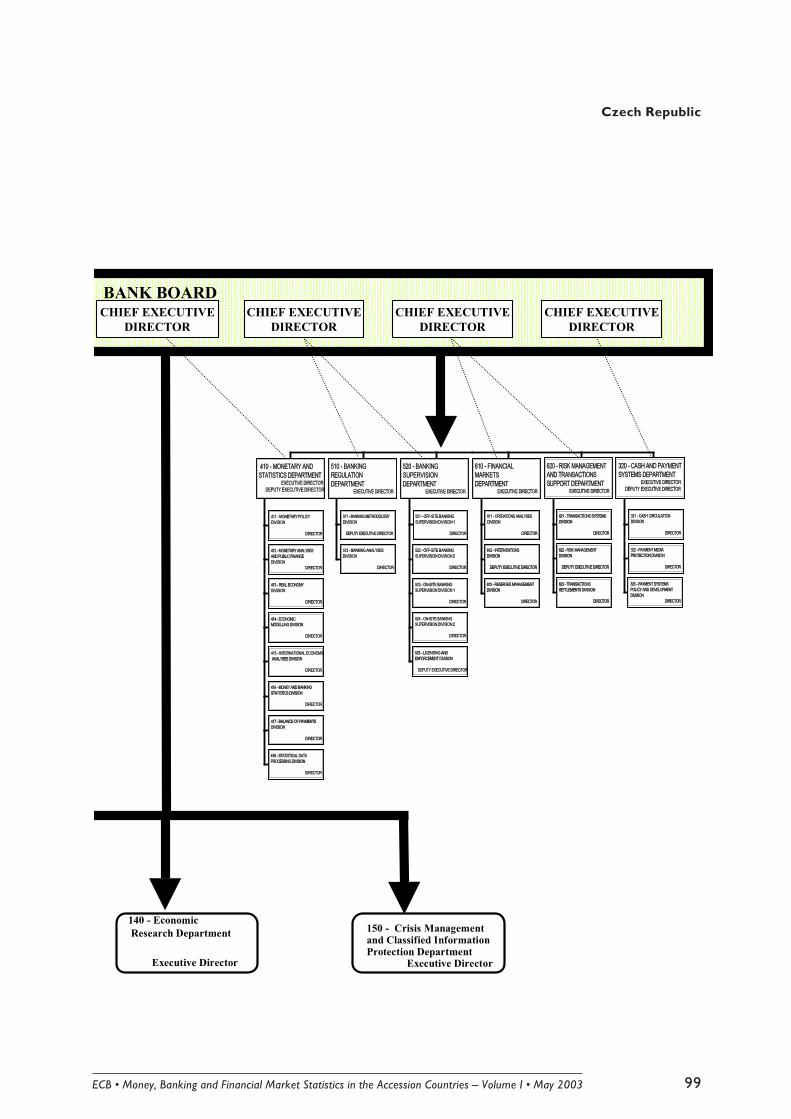

Organisation chart of theCzech National Bank ....................................... 99

5ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

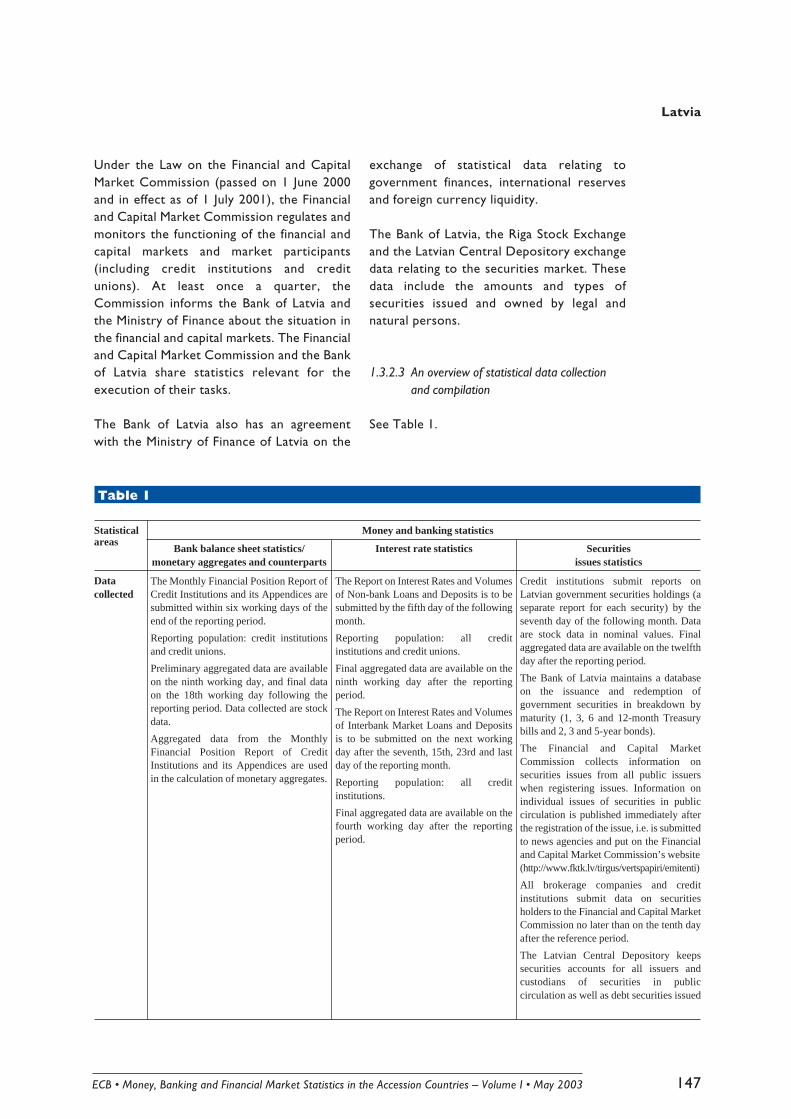

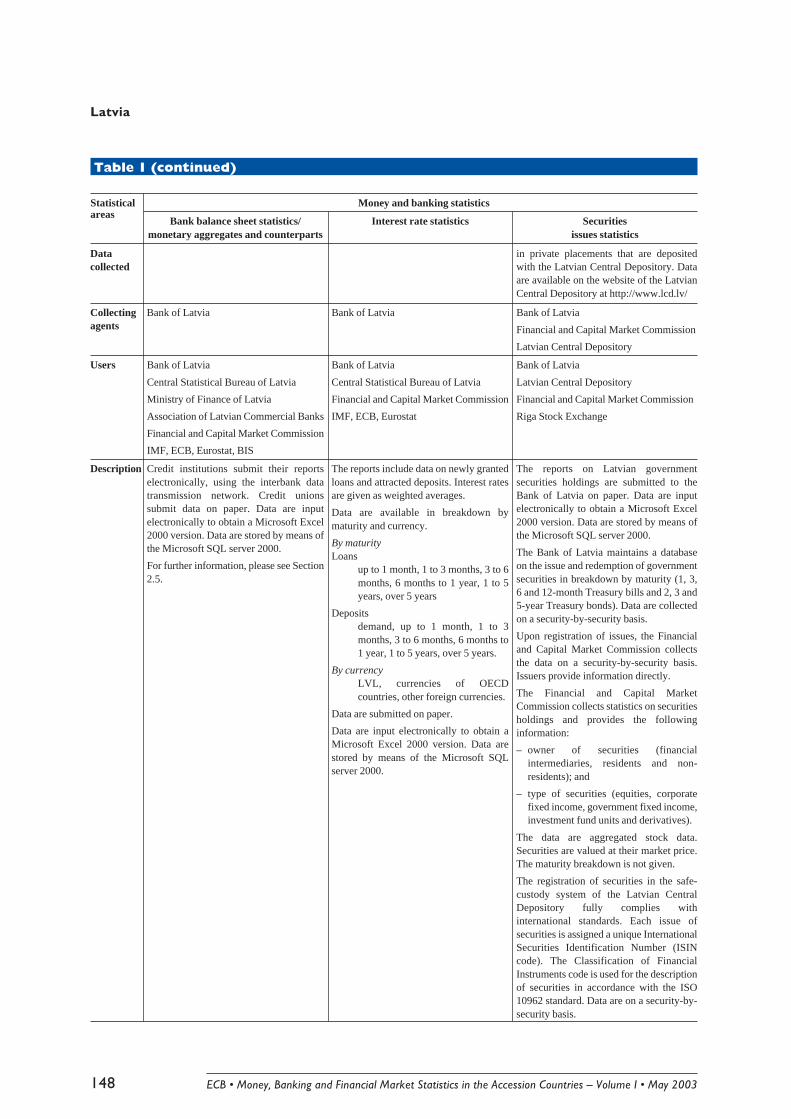

Latvia ............................................................ 143

List of abbreviations .................................. 144

1 Legal and institutionalbackground .......................................... 145

1.1 Organisational structure ....................... 145

1.2 Legal background .................................... 145

1.3 Institutional aspects ............................... 145

1.2 Legal background .................................... 125

1.3 Institutional aspects ............................... 126

2 Monetary statistics .......................... 129

2.1 Legal background and statisticalstandards .................................................. 129

2.2 Concepts and definitions ...................... 130

2.3 Population of monetaryinstitutions ............................................... 133

2.4 Banking business: generaldeposits/other products ....................... 133

2.5 Statistical balance sheets of themonetary institutions ............................ 134

2.6 National measure(s) of money:definitions and remarks ......................... 135

2.7 Counterparts of money ........................ 136

2.8 Reserve money ....................................... 136

2.9 Reporting procedures ........................... 136

2.10 Data processing and compilationmethods .................................................... 138

2.11 Publications .............................................. 138

3 Contacts at theNational Bank of Hungary ........... 139

Annexes ......................................................... 140

Organisation chart of the National Bankof Hungary (NBH) ............................................ 140

Organisation chart of the StatisticsDepartment of the NBH ................................. 141

2 Monetary statistics .......................... 150

2.1 Legal background andstatistical standards ................................ 150

2.2 Concepts and definitions ...................... 151

2.3 Population of monetaryinstitutions ............................................... 155

2.4 Banking business: generaldeposits/other products ....................... 155

2.5 Statistical balance sheets of themonetary institutions ............................ 156

2.6 Measure(s) of money: definitionsand remarks ............................................. 158

2.7 Counterparts of money ........................ 159

2.8 Reserve money ....................................... 159

2.9 Reporting procedures ........................... 159

2.10 Data processing and compilationmethods .................................................... 161

2.11 Publications .............................................. 162

3 Contacts at the Bankof Latvia ................................................ 163

Annexes ......................................................... 164

The Bank of Latvia’s Structure ....................... 164

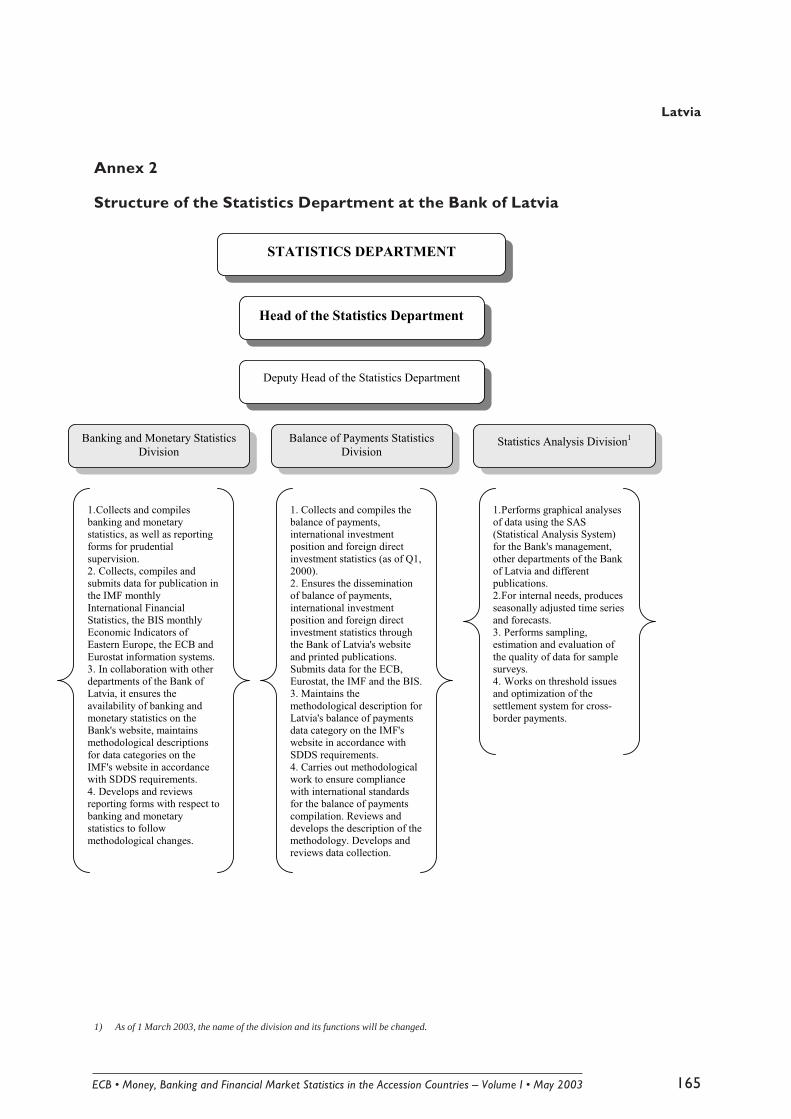

Structure of the Statistics Departmentat the Bank of Latvia ......................................... 166

Lithuania ...................................................... 167

List of abbreviations .................................. 168

1 Legal and institutionalbackground .......................................... 169

1.1 Organisational structure ....................... 169

1.2 Legal background .................................... 169

1.3 Institutional aspects ............................... 170

2 Monetary statistics .......................... 175

2.1 Legal background andstatistical standards ................................ 175

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 20036

Malta ............................................................. 187

List of abbreviations .................................. 188

1 Legal and institutionalbackground .......................................... 189

1.1 Organisational structure ....................... 189

1.2 Legal background .................................... 190

1.3 Institutional aspects ............................... 190

2 Monetary statistics .......................... 194

2.1 Legal background and statisticalstandards .................................................. 194

2.2 Concepts and definitions ...................... 195

2.3 Population of monetaryinstitutions ............................................... 198

2.4 Banking business: generaldeposits/other products ....................... 199

2.2 Concepts and definitions ...................... 176

2.3 Population of monetaryinstitutions ............................................... 178

2.4 Banking business: generaldeposits/other products ....................... 178

2.5 Statistical balance sheets of themonetary institutions ............................ 179

2.6 National measure(s) of money:definitions and remarks ......................... 180

2.7 Counterparts of money ........................ 180

2.8 Reserve money ....................................... 181

2.9 Reporting procedures ........................... 181

2.10 Data processing and compilationmethods .................................................... 182

2.11 Publications .............................................. 193

3 Contacts at the Bankof Lithuania .......................................... 184

Annex ............................................................. 185

Organisation chart of the Bankof Lithuania ....................................................... 185

2.5 Statistical balance sheets of themonetary institutions ............................ 199

2.6 Measure(s) of money: definitionsand remarks ............................................. 200

2.7 Counterparts of money ........................ 201

2.8 Reserve money ....................................... 201

2.9 Reporting procedures ........................... 201

2.10 Data processing and compilationmethods .................................................... 204

2.11 Publications .............................................. 205

3 Contacts at the CentralBank of Malta ..................................... 206

Annexes ......................................................... 207

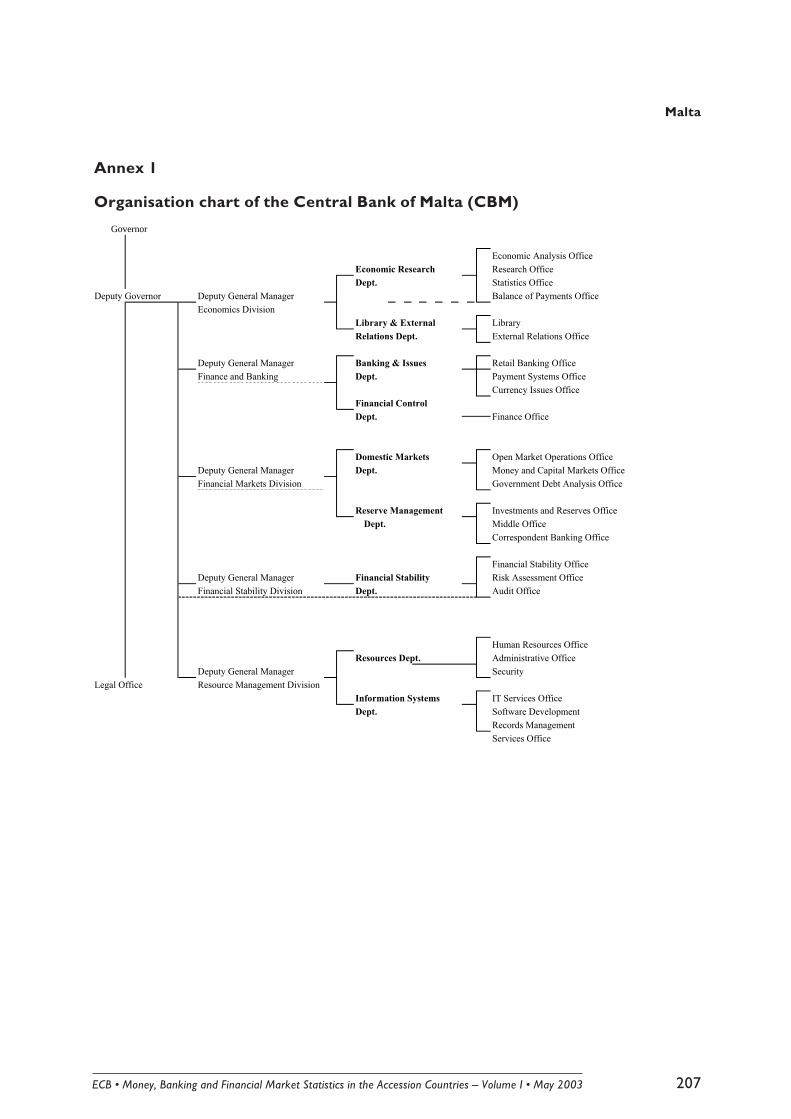

Organisation chart of the Central Bankof Malta (CBM) .................................................. 207

Organisation chart of the Statistics Section(within the Economics Department) ............ 208

Organisation chart of the Balanceof Payments Office ........................................... 209

Organisation chart of the Financial StabilityOffice .................................................................. 209

Poland ........................................................... 211

List of abbreviations .................................. 212

1 Legal and institutionalbackground .......................................... 213

1.1 Organisational structure ....................... 213

1.2 Legal background .................................... 214

1.3 Institutional aspects ............................... 214

2 Monetary statistics .......................... 217

2.1 Legal background andstatistical standards ................................ 217

2.2 Concepts and definitions ...................... 218

2.3 Population of monetaryinstitutions ............................................... 223

7ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

2.4 Banking business: generaldeposits/other products ....................... 223

2.5 Statistical balance sheets ofthe monetary institutions ..................... 224

2.6 Measure(s) of money: definitionsand remarks ............................................. 225

2.7 Counterparts of money .......................... 226

2.8 Reserve money ....................................... 227

2.9 Reporting procedures ........................... 227

2.10 Data processing andcompilation methods ............................. 229

2.11 Publications .............................................. 230

3 Contacts at the NationalBank of Poland .................................. 231

Annexes ......................................................... 232

Organisation chart of the National Bankof Poland (NBP) ................................................ 232

Organisation chart of the StatisticsDepartment of the National Bank ofPoland (NBP) ..................................................... 233

Slovakia ....................................................... 253

List of abbreviations .................................. 254

1 Legal and institutionalbackground .......................................... 255

1.1 Organisational structure ....................... 255

1.2 Legal background .................................... 255

1.3 Institutional aspects ............................... 256

2 Monetary statistics .......................... 262

2.1 Legal background andstatistical standards ................................ 262

2.2 Concepts and definitions ...................... 263

2.3 Population of monetaryinstitutions ............................................... 266

2.4 Banking business: generaldeposits/other products ....................... 267

2.5 Statistical balance sheets of themonetary institutions ............................ 267

Romania ....................................................... 235

List of abbreviations .................................. 236

1 Legal and institutionalbackground .......................................... 237

1.1 Organisational structure ....................... 237

1.2 Legal background .................................... 237

1.3 Institutional aspects ............................... 239

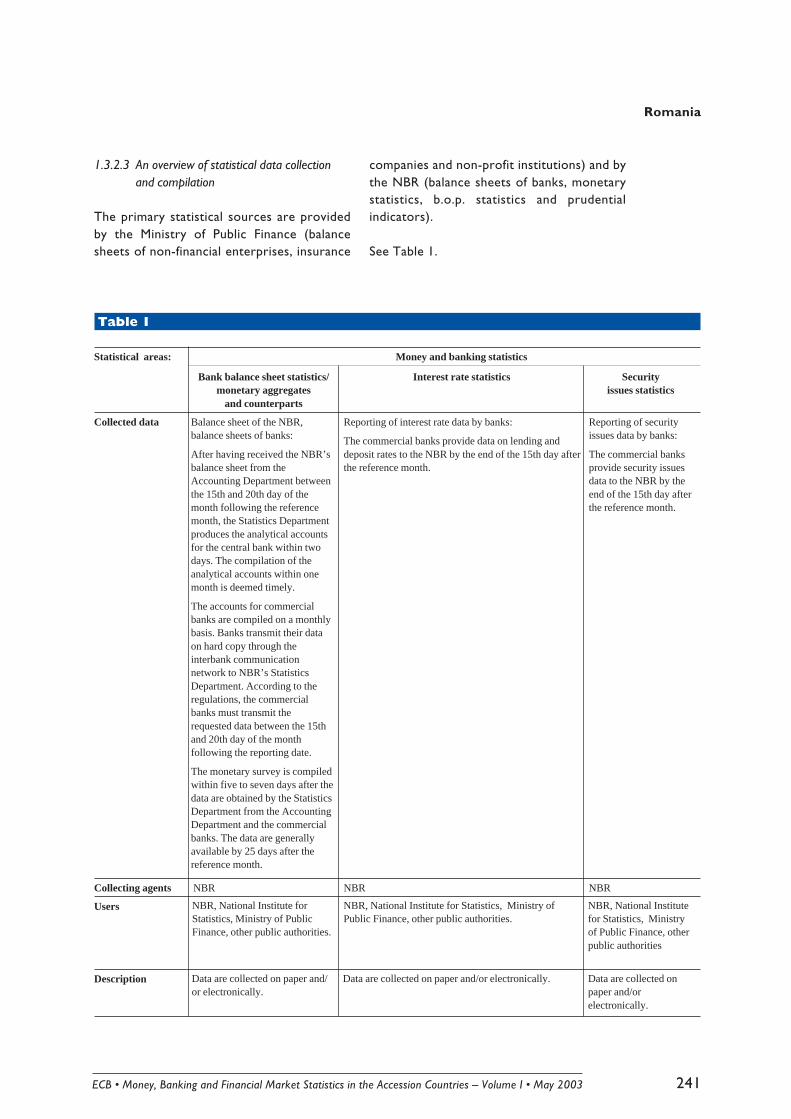

2 Monetary statistics .......................... 242

2.1 Legal background andstatistical standards ................................ 242

2.2 Concepts and definitions ...................... 242

2.3 Population of monetaryinstitutions ............................................... 246

2.4 Banking business: generaldeposits/other products ....................... 246

2.5 Statistical balance sheets of themonetary institutions ............................ 246

2.6 Measure(s) of money: definitionsand remarks ............................................. 247

2.7 Counterparts of money ........................ 247

2.8 Reserve money ....................................... 247

2.9 Reporting procedures ........................... 248

2.10 Data processing andcompilation methods ............................. 249

2.11 Publications .............................................. 249

3 Contacts at the NationalBank of Romania .............................. 250

Annexes ......................................................... 251

Organisation chart of theNational Bank of Romania (NBR) ................. 251

Organisation chart of the StatisticalDepartment of the NBR.................................. 252

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 20038

Slovenia ....................................................... 277

List of abbreviations .................................. 278

1 Legal and institutionalbackground .......................................... 279

1.1 Organisational structure ....................... 279

1.2 Legal background .................................... 279

1.3 Institutional aspects ............................... 280

2 Monetary statistics .......................... 281

2.1 Legal background and statisticalstandards .................................................. 281

2.2 Concepts and definitions ...................... 284

2.3 Population of monetaryinstitutions ............................................... 286

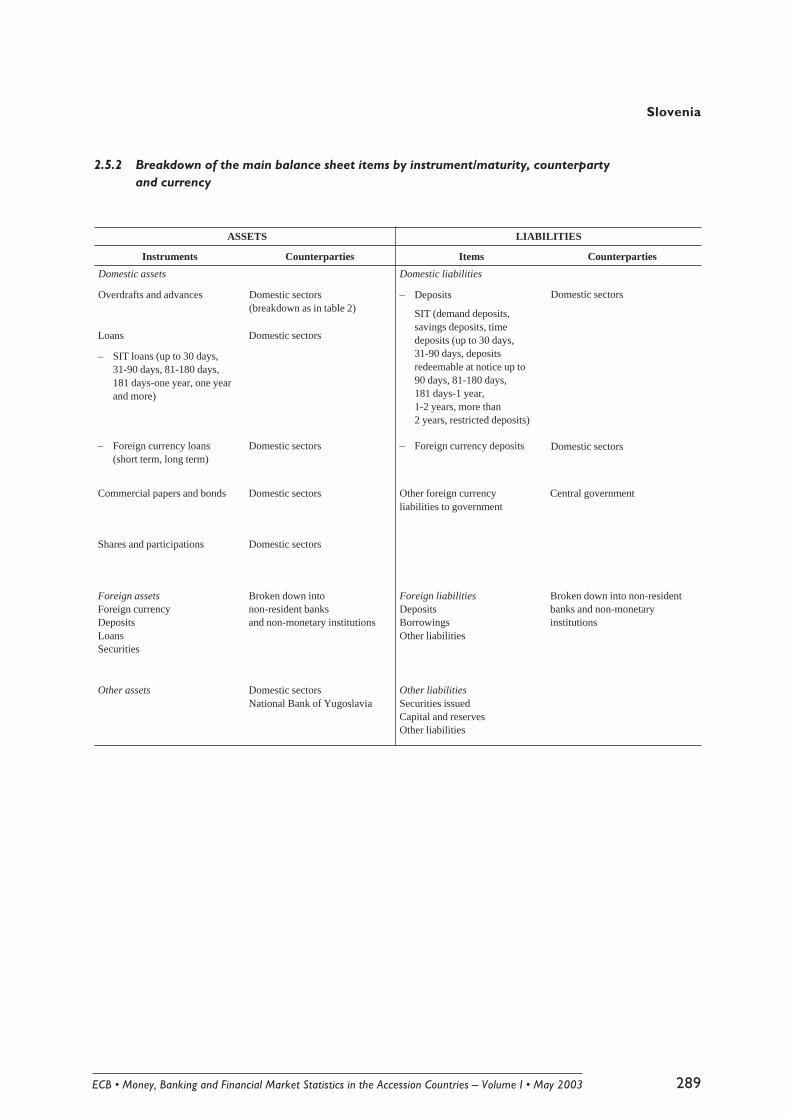

2.4 Banking business: generaldeposits/other products ....................... 288

2.5 Statistical balance sheets of themonetary institutions ............................ 288

2.6 Monetary aggregates: definitionsand remarks ............................................. 290

2.7 Counterparts of money ........................ 290

2.8 Reserve money ....................................... 290

2.9 Reporting procedures ........................... 291

2.10 Data processing andcompilation methods ............................. 292

2.11 Publications .............................................. 293

3 Contacts at theBank of Slovenia ................................ 294

Annexes ......................................................... 295

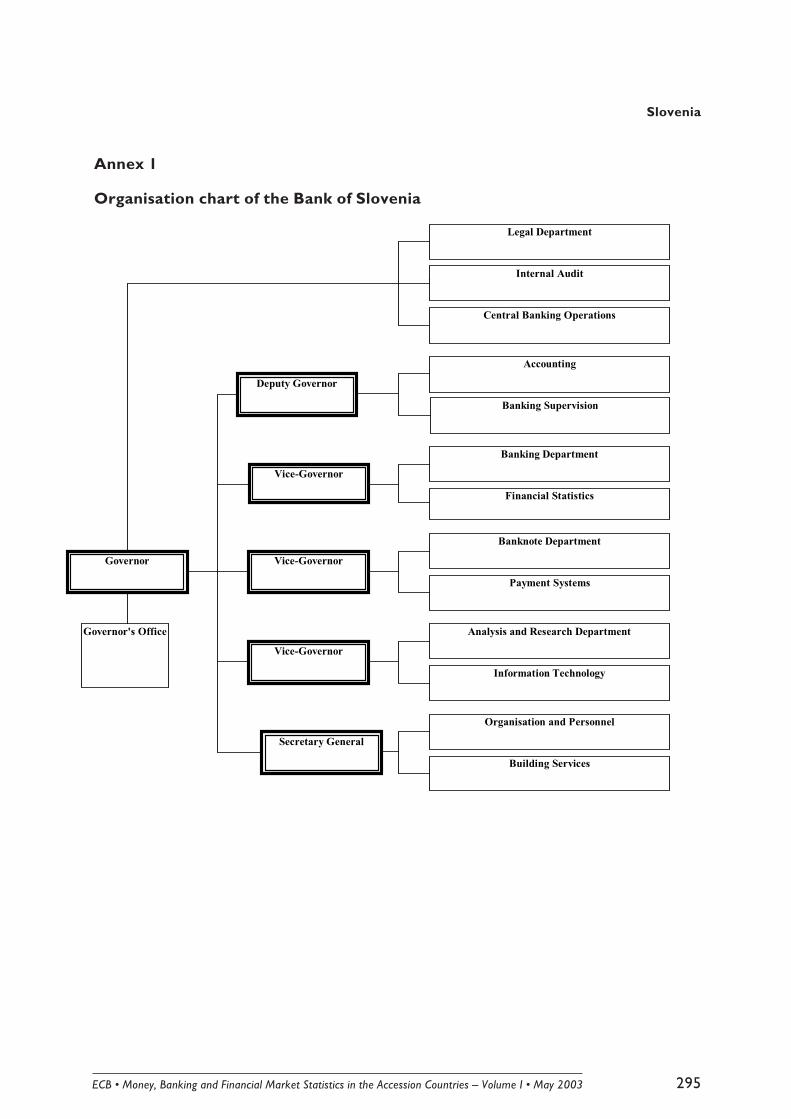

Organisation chart of theBank of Slovenia ................................................ 295

Organisation chart of the Statistics Departmentof the Bank of Slovenia ................................... 296

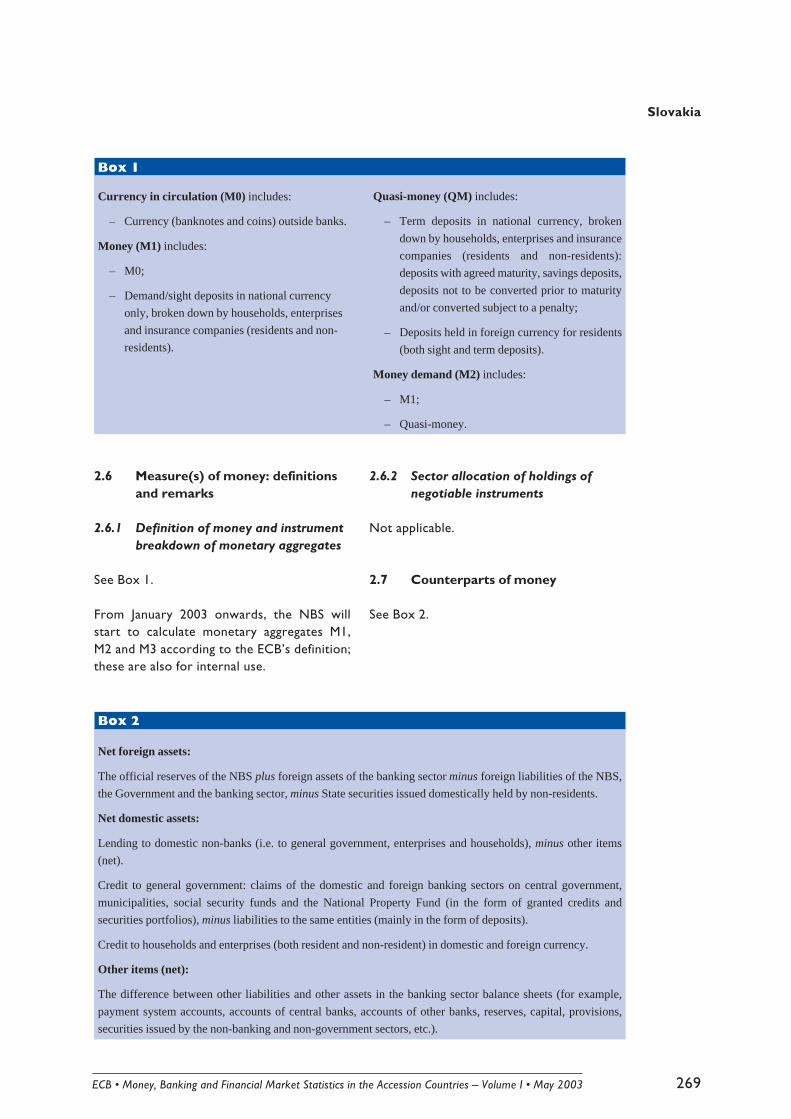

2.6 Measure(s) of money: definitionsand remarks ............................................. 269

2.7 Counterparts of money ........................ 269

2.8 Reserve money ....................................... 270

2.9 Reporting procedures ........................... 270

2.10 Data processing andcompilation methods ............................. 272

2.11 Publications .............................................. 273

3 Contacts at the NationalBank of Slovakia ................................ 274

Annexes ......................................................... 275

Organisation chart of the National Bankof Slovakia (NBS) .............................................. 275

Organisation chart of the Statistical workat the NBS ....................................................... 276

9ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

List of contributors

Bulgaria

Bulgarian National Bank Violeta PeichevaBoyka ZagorovaKatia Mincheva

Cyprus

Central Bank of Cyprus Eliana PsimolophitouAndroulla MelifronidouChristina Nicolaidou

Czech Republic

Czech National Bank Zbynek KarnetIva ChrtkovaMagda Gregorova

Estonia

Bank of Estonia Liina Seestrandt

Hungary

National Bank of Hungary Szilvia Veres

Latvia

Bank of Latvia Zigrida AustaInara LindeGunta Andersone

Lithuania

Bank of Lithuania Gintaras DaugëlaRomas Karaliûnas

Malta

Central Bank of Malta Jesmond PuleRoderick Psaila

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200310

Poland

National Bank of Poland Anna LewandowskaJoanna Glowala

Romania

National Bank of Romania Virgil Stefanescu

Slovakia

National Bank of Slovakia Ivana BrziakovaKarol MachacekDaniela MarekovaAndrea Bernathova

Slovenia

Bank of Slovenia Dušan MurnTomo Narat

European Central Bank Alda Morais

11ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

Foreword

Background

The initiative to compile a Manual on thecurrent definition and structure of moneyand banking statistics in the Accession Countries(hereinafter referred to as the”Methodological Manual”) was launched atthe inaugural money and banking statisticsseminar with the national central banks(NCBs) of the 12 Accession Countries1 heldat the European Central Bank (ECB) inFrankfurt am Main on 15 and 16 December1999.

The Manual is divided into two Volumes. Thisvolume (Volume I) presents the currentframework for the collection and compilationof monetary statistics and providesinformation on the legal and institutionalbackground to the compilation of thesestatistics2. It also describes the extent towhich the Accession Countries already meet(or will in the near future) the ECB’sstatistical requirements and compile statisticsthat are conceptually consistent with the euroarea monetary statistics.

The legal framework for the provision ofstatistics on the balance sheets of monetaryfinancial institutions (MFIs) in the euro areais set out in ECB Regulation ECB/2001/13 of22 November 2001 concerning theconsolidated balance sheet of the MFI sector,as amended, and in ECB Guideline ECB/2003/2 of 6 February 2003 concerning certainstatistical reporting requirements of the ECBand the procedures for reporting by theNCBs of statistical information in the field ofmoney and banking statistics. ECB RegulationECB/2001/13 is addressed to the reportingagents located in the euro area, and sets outin detail the statistical information they arerequired to submit to the NCB of theircountry of residence regarding MFI balancesheet statistics in order to meet the ECB’srequirements. The Guideline addresses theNCBs located in the euro area (”participatingNCBs”) and specifies the information (onboth MFI balance sheet statistics and on other

money and banking statistics) which must besubmitted to the ECB as well as the technicalprocedures to be followed in the datasubmissions.

Although the ECB’s main tasks relate to theeuro area, the ECB also has responsibilitiesunder the Treaty towards Member States ofthe European Union (EU) which have not yetjoined the euro area. It is acknowledged that,on average under “fast track” conditions, itmay take two years to implement statisticalchanges in reporting systems from the timethe Member States start discussing therequirements with reporting institutions totheir full implementation. Therefore, thework on the changes in the statistical systemsneeded to meet the requirements for euroarea money and banking statistics shouldbegin well in advance, in order to ensure thatstatistics are available by the time MemberStates join the euro area.

In order to provide the ECB with harmonisedmoney and banking statistics, the AccessionCountries will be required to modify, tovarying degrees, the structure of the statisticsthey currently collect from reportinginstitutions and to extend their coverage toall those financial institutions that fall underthe MFI definition.

It is in this connection that the compilationand regular update of a methodologicalmanual on money and banking statistics inthe Accession Countries is seen as aparticularly important task that is part of thework necessary to prepare countries foraccession to the EU and eventual membershipof the euro area.

1 Cyprus, the Czech Republic, Estonia, Hungary, Latvia, Lithuania,Malta, Poland, Slovakia, Slovenia, Bulgaria and Romania.

2 The first edition of the Methodological Manual, Volume I, waspublished in April 2001. The first edition of Volume II (entitled”Current framework for statistics on other financialintermediaries, financial markets and interest rates in theAccession Countries”) is being published in conjunction with thisVolume.

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200312

Aim

The aim of this second edition of theMethodological Manual (Volume I) is to assessdevelopments in the statistical framework forthe collection and compilation of money andbanking statistics in the Accession Countries(namely the extent to which they areprogressively becoming compliant with ECBstatistical standards), and thereby to support

the conceptual and practical harmonisationwork necessary to prepare these countriesfor membership of the EU and, eventually,the euro area. The present edition containsinformation as at end-December 2002,although anticipated changes up to the end ofJune 2003 are also mentioned.

Structure

The Methodological Manual (Volume I) isdivided into 12 country chapters, one chapterper country. Each chapter consists of threeparts: Part I deals with the legal andinstitutional background, Part II withmonetary statistics and Part III with thecontacts at the NCBs of the AccessionCountries.

Part One briefly describes the legal andinstitutional structure of the NCBs of theAccession Countries and their statisticaldepartments/work. This overview containsinformation on the further sources ofinformation that are available at the nationallevel, namely the websites where the basictext of the national laws and regulationsmentioned can be found.

Part Two presents the national frameworksfor the collection and compilation ofmonetary statistics in the AccessionCountries, describing in detail the collectionof balance sheet data from monetaryinstitutions and the compilation of thenational monetary aggregates andcounterparts. Any future plans to adapt thenational collection systems to ECB standardsare also mentioned.

Part Three lists the contacts at the NCBs towhom any queries concerning the issuesdescribed in the respective country chaptershould be addressed.

Status of the Manual

In the Accession Countries, theMethodological Manual is available to thegeneral public from the NCB of the countryconcerned. Other interested parties mayrequest copies from the ECB, at the followingaddress:

European Central Bank,Press DivisionKaiserstrasse 29, D - 60311 Frankfurt am MainFax: + 49 (69) 13 44 7404

The Methodological Manual is also availableon the ECB’s website (http://www.ecb.int).

The Methodological Manual is available onlyin English, with translations into nationallanguages left to the discretion of the NCBsof the Accession Countries.

13ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

1 Legal and institutional background

Introduction to the country chapters

This part provides a short overview of thelegal and institutional structure of the NCBsof the Accession Countries and, in particular,their statistical departments/work.

1.1 Organisational structure

This section provides a brief description ofthe organisation of the NCBs (see theorganisation chart(s) at the end of eachcountry chapter). It also gives a detaileddescription of the organisation of thestatistical departments/work at the NCBs,focusing on those areas responsible for thecompilation of money and banking statistics.

1.2 Legal background

This section analyses the national legalbackground for the activities of the NCBs,indicating the most important national laws,regulations and specific provisions thatprovide the framework for their activities.Where applicable, the website is indicatedwhere the basic text of the laws and

regulations mentioned in this section can befound.

1.3 Institutional aspects

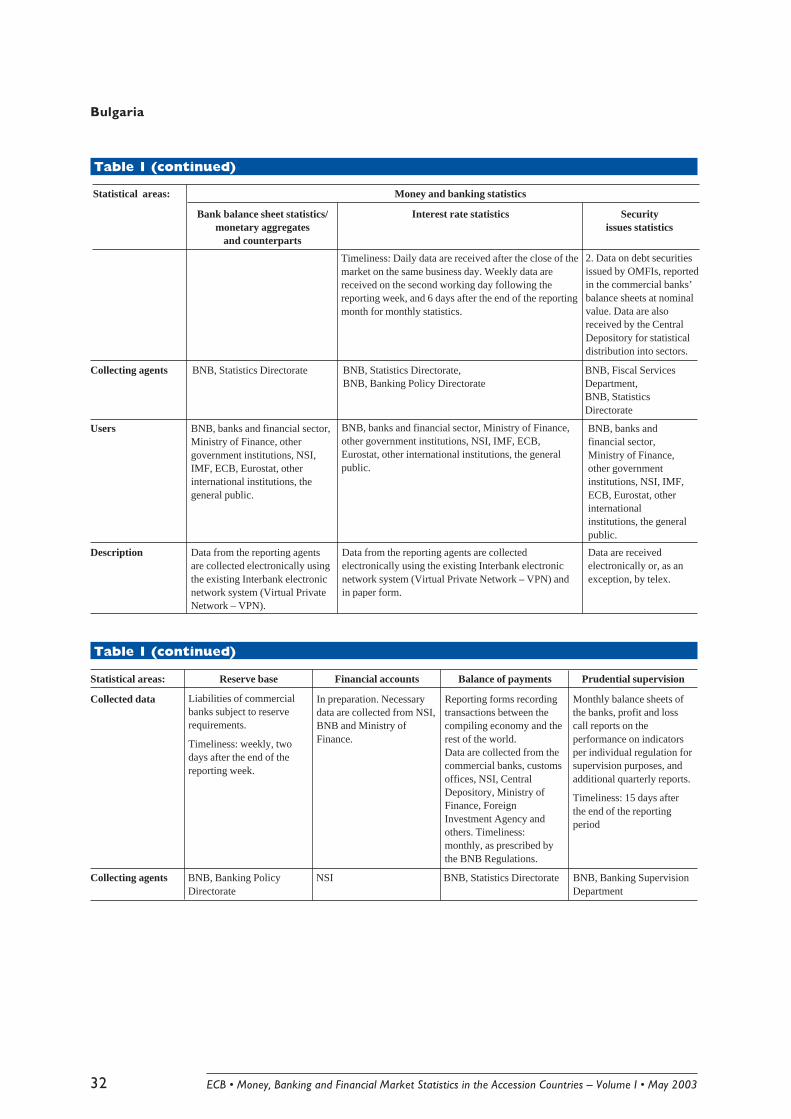

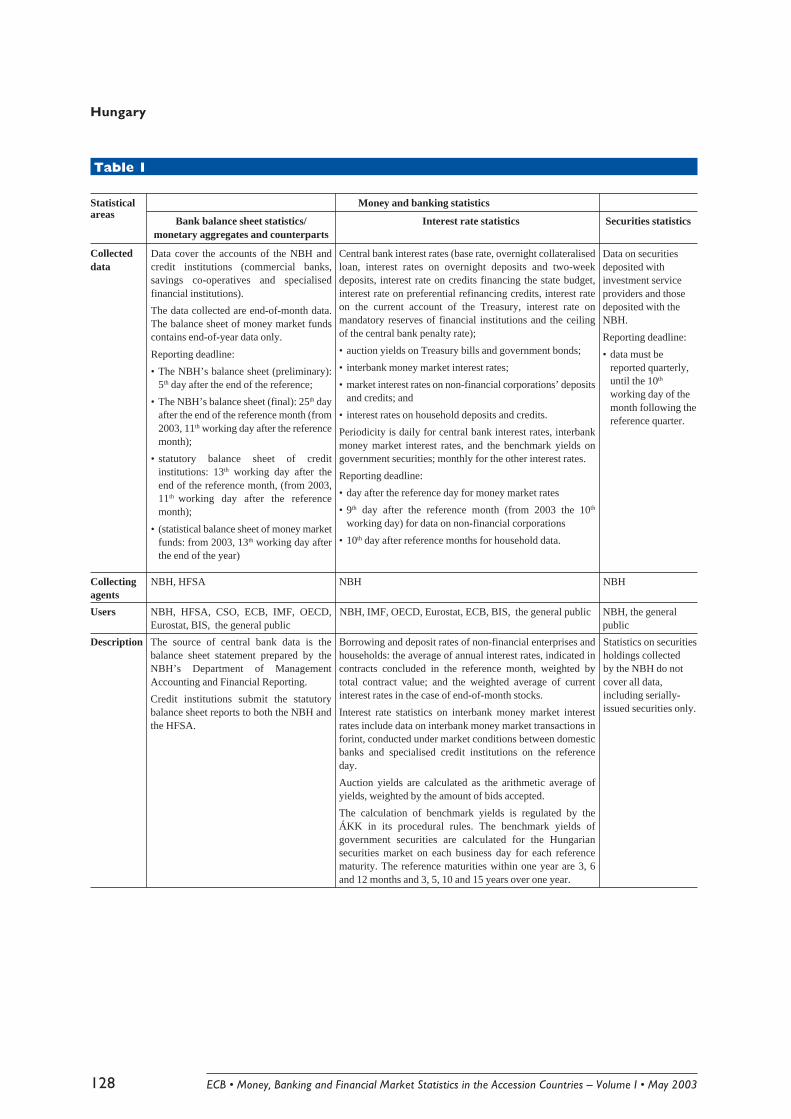

This section introduces the NCBs and brieflydescribes their role, functions andresponsibilities (e.g. statutory responsibility,banking supervision and activities vis-à-vis theGovernment and other public bodies). The mainactivities relating to macroeconomic statisticscarried out by the NCBs and by other publicauthorities (including the co-operation betweenthem) in the area of money and bankingstatistics, reserve base statistics, financialaccounts, balance of payments statistics andprudential supervision are also indicated. Thestatistical data collection and compilation of theabove-mentioned areas of statistics aredescribed (as shown in Table 1). This descriptioncovers the type of data collected, the frequencyand timeliness, the relevant sources of data, thecollecting agents, the users of the statisticsproduced and an overview of the statistical datacollection and compilation systems (e.g. themedia of data collection).

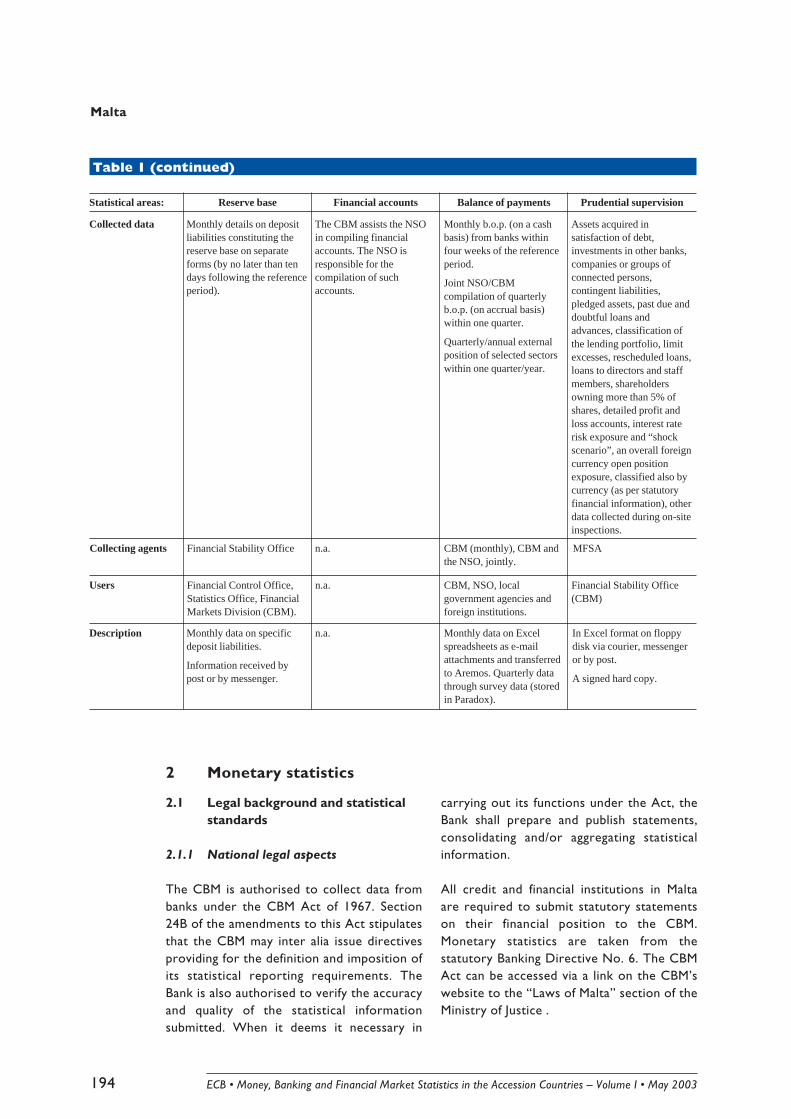

2 Monetary statistics

This part presents the current frameworkfor the collection and compilation ofmonetary statistics in the AccessionCountries. It describes in detail the collectionof balance sheet data from monetaryinstitutions and the compilation of nationalmonetary aggregates and counterparts.

2.1 Legal background and statisticalstandards

This section analyses the national legalbackground to monetary statistics, indicatingthe national laws, regulations and specificprovisions that apply to monetary statistics.Where applicable, the website is mentionedwhere the basic text of the laws and

regulations mentioned in this section can befound. It also indicates the statisticalstandards followed in the field of monetarystatistics, including international statisticalstandards (ESA 95, SNA 1993 and the IMFManual on Monetary and Financial Statistics).

2.2 Concepts and definitions

This section analyses a number of concepts anddefinitions for monetary statistics. Regarding theresidency principles for the purposes ofmonetary statistics, it presents the definition ofthe economic territory and provides the exactboundaries of the economic territory comparedwith the geographic territory. It also defines theconcept of residency for both natural persons

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200314

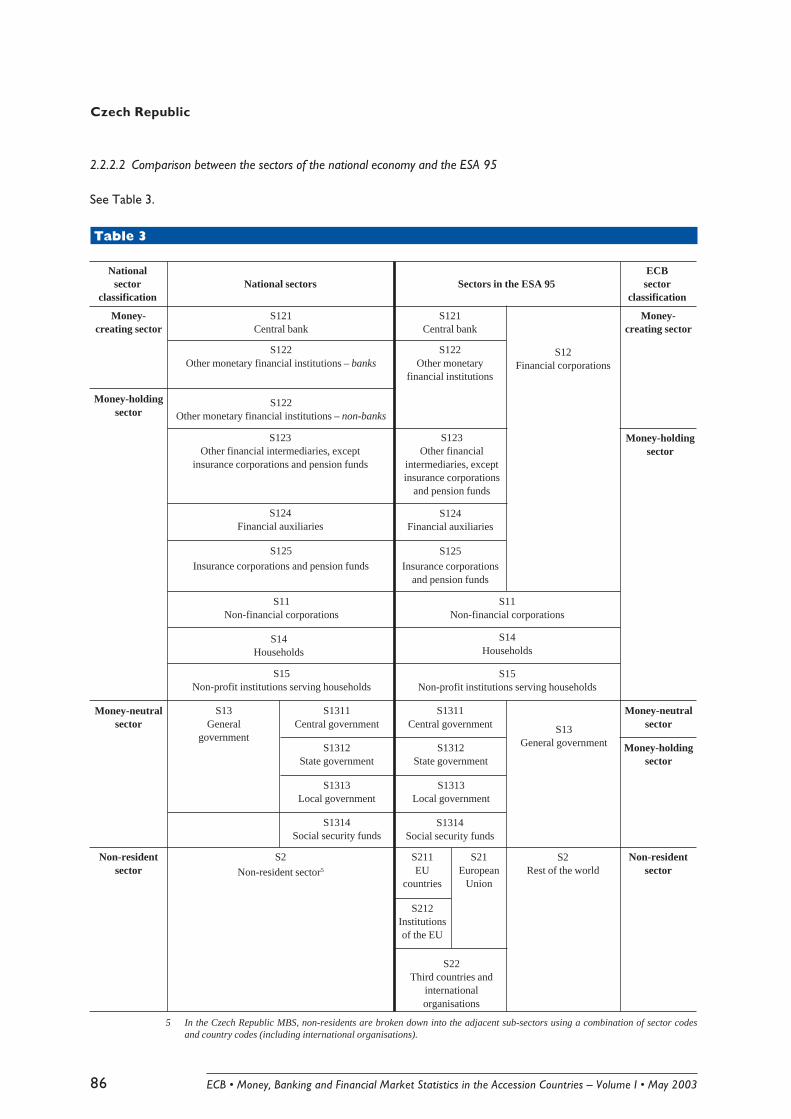

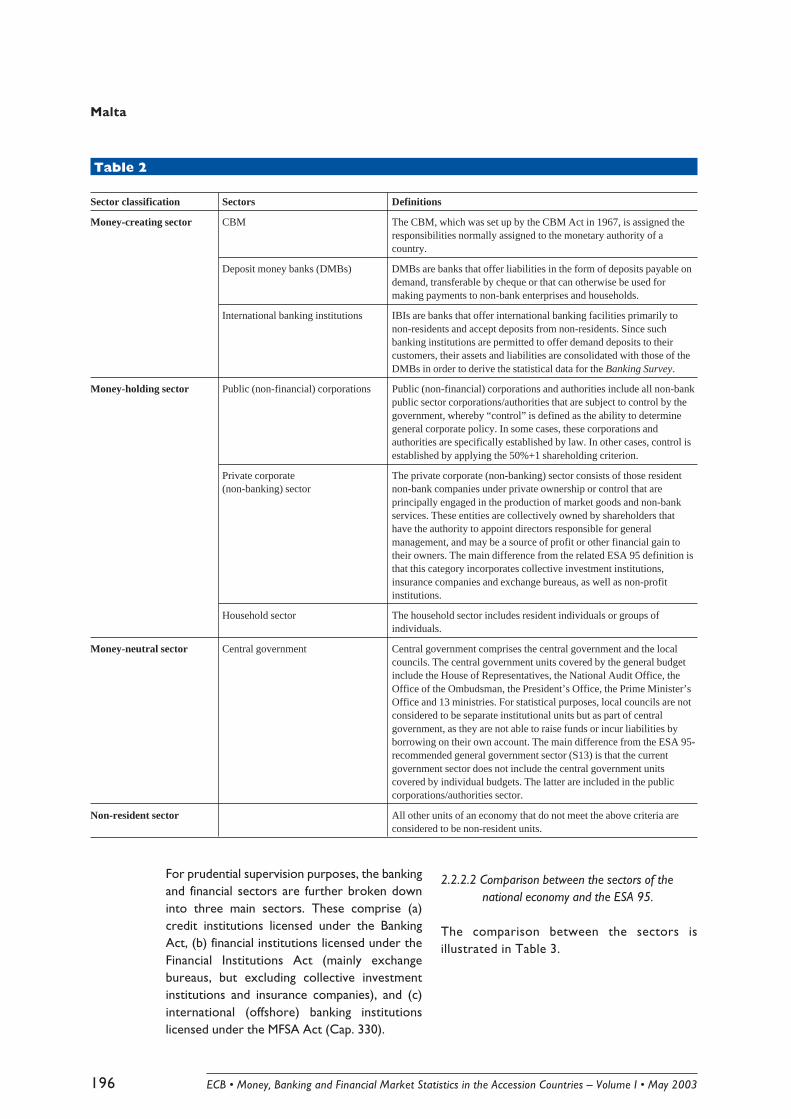

and enterprises (in particular, the residency offoreign branches of domestic banks and theresidency of domestic branches of foreignbanks). With respect to the sectorisationprinciples of monetary statistics, it presents thesectors into which the national economy is splitfor the purposes of compiling monetary statistics(as shown in Table 2). It also indicates how thisbreakdown corresponds to the ESA 95 and tothe ECB classification of ESA 95 sectors intomoney-creating, money-holding, money-neutraland non-resident sectors (as shown in Table 3).Where relevant, deviations between the sectorsof the national economy and the ESA 95 arebriefly explained.

2.3 Population of monetary institutions

This section describes the money-creatingsector within monetary statistics. The nationaldefinition of a credit institution (bank) and thelegal references to the definition are given. Anyother monetary institutions which are notcommonly known as credit institutions (banks),but which are nevertheless included in themoney-creating sector (e.g. money marketfunds), are also defined. For each category ofcredit institutions and of other monetaryinstitutions indicated, the number of institutionsis provided in Table 4. It is also indicatedwhether deposit liabilities of central governmentunits (e.g. Post Office savings accounts of theTreasury or the Post Office) are included in themeasures of money.

2.4 Banking business: general deposits/other products

This section outlines the general deposit andother banking products offered by creditinstitutions and by other monetaryinstitutions.

2.5 Statistical balance sheets of themonetary institutions

This section describes the main statisticalbalance sheet items (liabilities and assets) and

their breakdown by instrument/maturity,counterparty and currency.

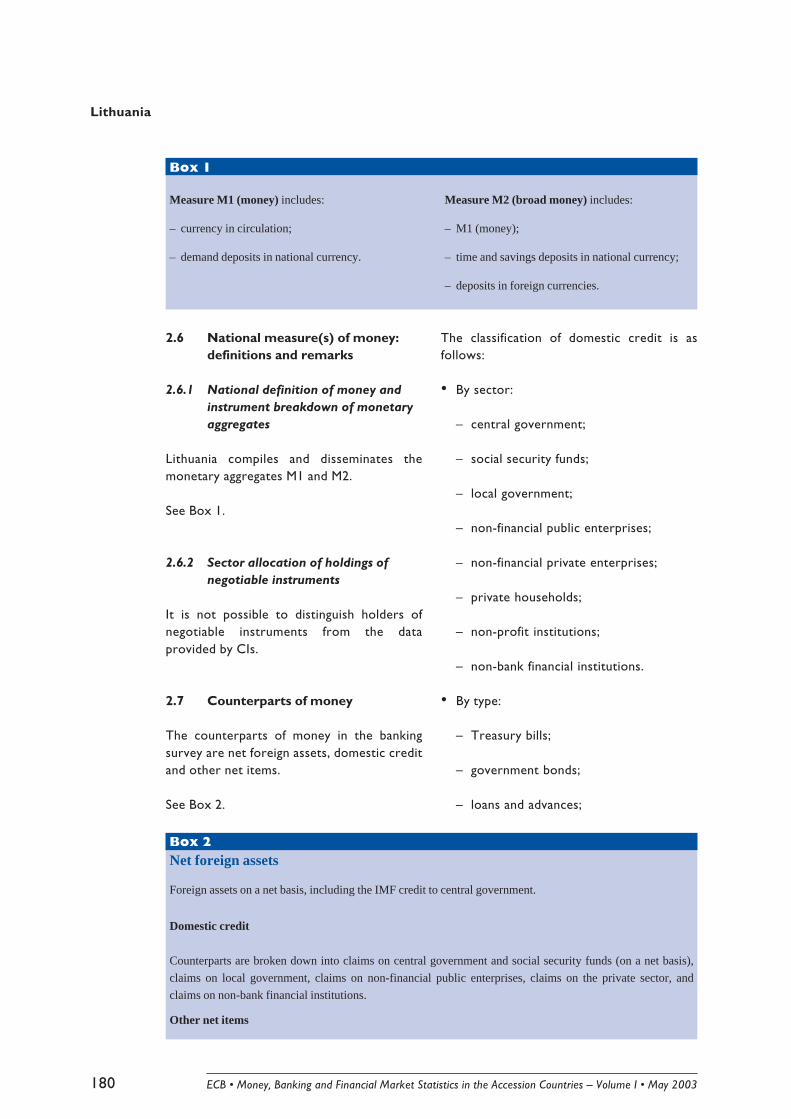

2.6 Measure(s) of money: definitionsand remarks

This section defines the main measures ofmoney, from the narrowest to the broadestaggregates. The corresponding instrumentbreakdown for each aggregate is listed in Box1. It also describes how holdings of negotiableinstruments issued by monetary institutions(i.e. any negotiable instruments which arefreely transferable, such as cash, certificatesof deposit, commercial bills and other bearerpaper), are explicitly or implicitly allocatedbetween the various economic sectors.

2.7 Counterparts of money

This section analyses the counterparts ofmoney (net external assets, domestic credit– net claims on the central government,claims on the private sector – other netitems). This information is shown in Box 2.The classification available on credit todomestic residents (by sector, type andmaturity) is also provided.

2.8 Reserve money

This section describes the relevant conceptsof reserve money (reserve money, basemoney, monetary base) compiled by theNCBs of the Accession Countries.

2.9 Reporting procedures

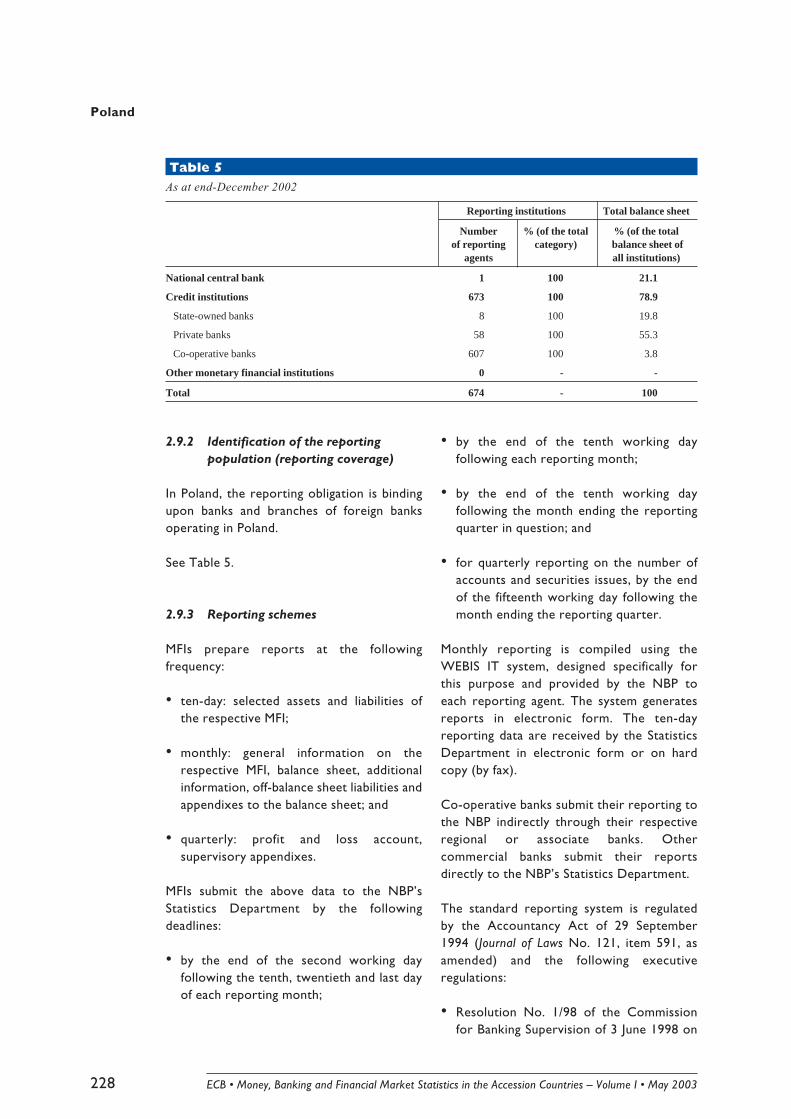

This section describes the reporting proceduresfor the compilation of monetary statistics. Itcovers the specific legal or other regulatorypowers granted to the NCB and to other agentswith respect to collecting data from themonetary institutions for the compilation ofmonetary statistics. It also describes thereporting coverage of the population ofmonetary institutions for the balance sheet data.

15ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

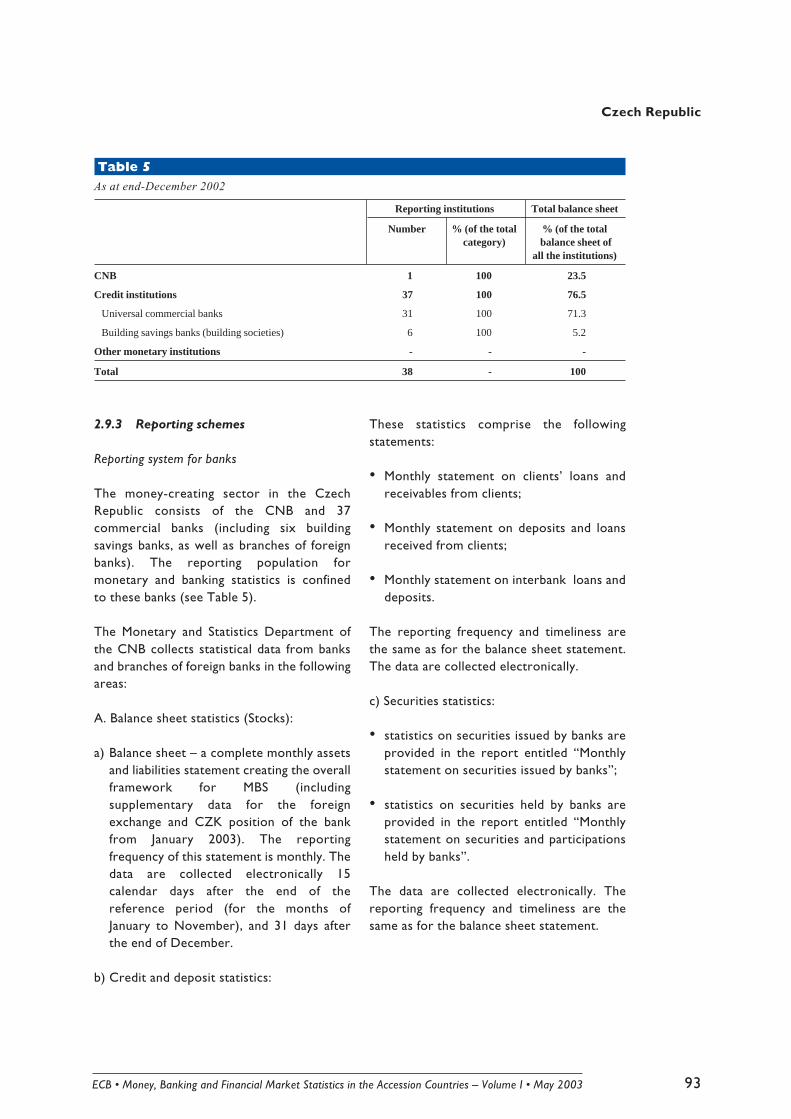

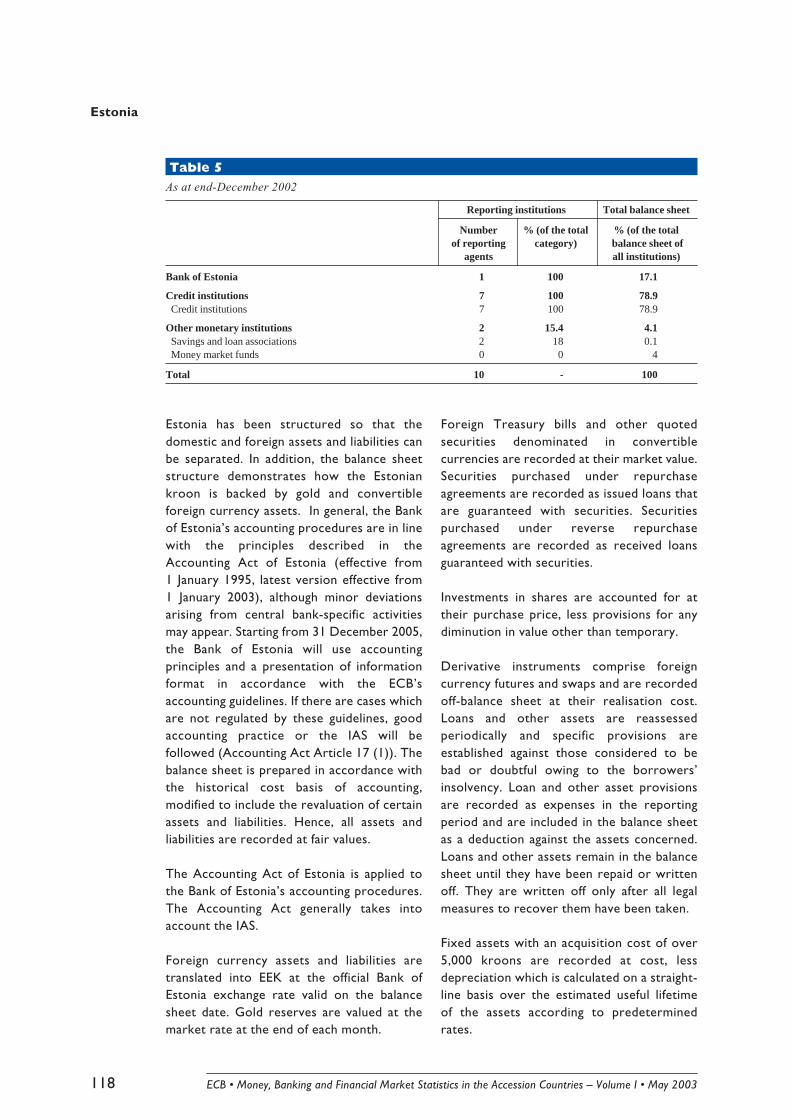

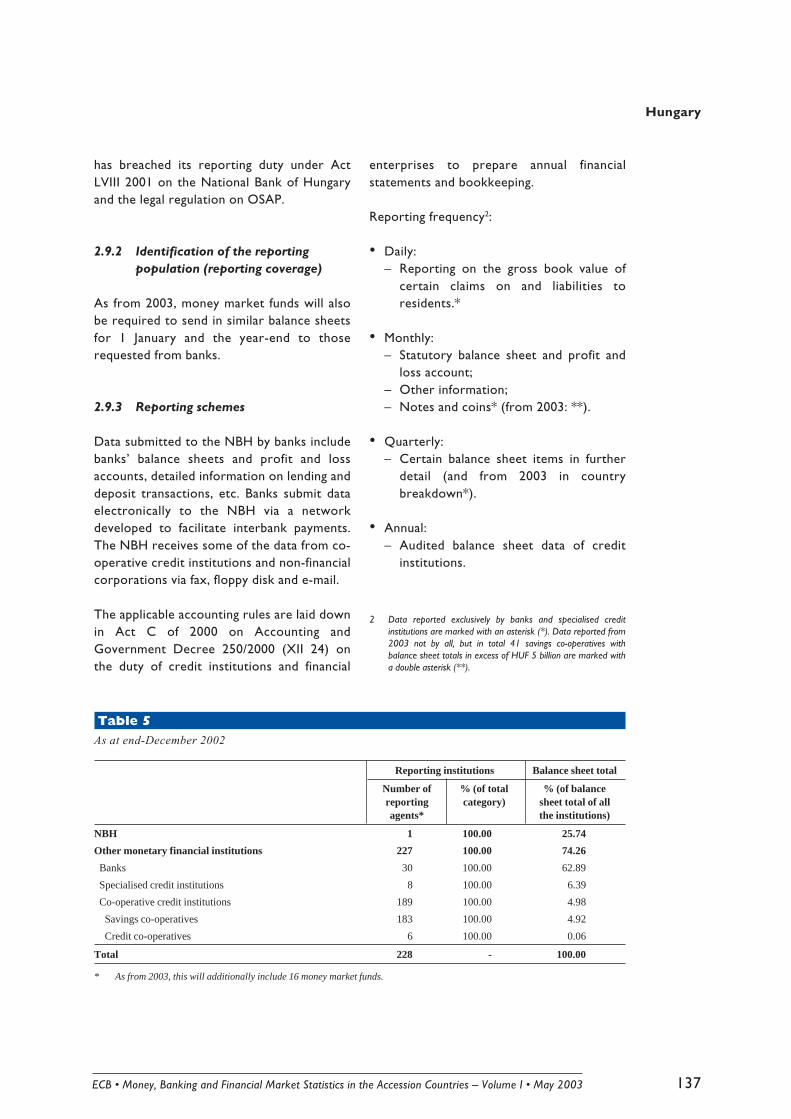

Table 5 shows the number of reportinginstitutions per category of monetary institutionand their contribution to the total of thecategory and to the total balance sheet of allinstitutions. This section also describes thereporting schemes for monetary statistics bytype of monetary institution. This descriptioncovers the reporting population (the reportingcoverage), the data collected (e.g. full balancesheet data or selected components), thefrequency and timeliness, the methodologicaland accounting rules and the medium of datacollection (e.g. paper, electronic).

2.10 Data processing and compilationmethods

This section provides information on the basisof calculation (e.g. end-of-period data, mid-

period, average data), the revision proceduresapplicable to monetary statistics and thecompilation of flows statistics, whereapplicable (in particular how adjustments forbreaks in series and other adjustments aremade). This section also addresses theseasonal adjustment of data.

2.11 Publications

This section indicates how monetary statisticsare first released to the public (e.g. source,type of data released, format, time andmedium of the publications). It also indicatesthe main weekly/monthly publications formonetary statistics, where these differ fromthe first publication, as well as any otherrelevant statistical publications for monetarystatistics.

3 Contacts at the national central bank of the Accession Country

This part lists the contacts at the NCBs ofthe Accession Countries, to whom anyqueries concerning the issues described in

the respective country chapter should beaddressed.

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200316

Summary of progress made in terms ofimplementation of the ECB’s statisticalreporting requirements

Introduction

This chapter provides a summary assessmentof recent progress made by the AccessionCountries in the implementation of the ECB’sstatistical requirements. It highlights a numberof key issues in the statistical practicesfollowed by the Accession Countries in thecompilation of their national statistics when

compared to the statistical requirements ofthe ECB. References to practices in theAccession Countries correspond to thesituation as at end-December 2002, butreflect, where appropriate, existing plans forchanges to the statistical systems up to theend of June 2003.

Statistical standards followed in the Accession Countries

ECB requirements. The ECB Regulation ECB/2001/13 concerning the consolidated balancesheet of the MFI sector (as amended) sets out indetail the ECB’s requirements for euro areamoney and banking statistics. The Regulationestablishes the statistical standards according towhich statistical data must be collected andcompiled in order to meet ECB requirements.The Regulation comprises two main elements:(i) the definition of the reporting population formonetary statistics; (ii) a specification of thestatistical information that reporting agentslocated in the euro area are required to submitto the NCB in their country of residence in orderto meet those requirements. Where appropriate,the ESA 95 constitutes the main reference workfor euro area money and banking statistics, interms of the classification by instrument andsector. In respect of the classification by sector, avery close link between ESA 95 and euro areamoney and banking statistics is ensured by theinclusion of the MFI sector as defined by the ECBin the ESA 95. Hence, the definition of thereporting population for monetary statistics (theMFI population) is fully transposed into theESA 95 sectorisation, corresponding to the sub-sectors S121 (The central bank) and S122 (Othermonetary financial institutions). The accountingrules followed by MFIs in drawing up theiraccounts comply with the national transpositionof the EU Bank Accounts Directive together withany other applicable international accountingstandards, such as the International AccountingStandards (IAS) developed by the InternationalAccounting Standards Board (IASB). Furtherrecommendations to national compilers regardingthe standards to be followed in euro area money

and banking statistics (valuation of instruments,netting procedures, time of recording, etc.) maybe found in the Guidance Notes to the ECBRegulation ECB/2001/13 (ECB, November2002).

Several Accession Countries have alreadyadopted the statistical recommendations ofthe ESA 95 and have broadly harmonised thecompilation of monetary statistics in line withECB requirements (this refers only to stocks;progress is less well advanced with regard toflow statistics – see below). This is the casein the Czech Republic, Estonia, Hungary, Latvia,Poland and Slovakia. Individual developmentsindicated by some of the countries concernedare as follows:

• The Czech Republic has indicated that therequirements in the field of balance sheetstock statistics contained in ECB/2001/13have already been adopted for banks (infact, the national requirements cover morethan what is required by the ECB). Table 1is compiled on a regular basis, while thepreparatory work on the compilation ofthe other tables on stocks is progressingwell.

• In Hungary, monetary statistics will satisfythe ECB criteria related to monetarystatistics in the course of by 2003.

• Latvia is also already compiling monetaryand banking statistics in accordance withECB/2001/13 (only the sector classificationused still differs slightly from the

17ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

institutional breakdown in the ESA 95), asthis country has adopted a new Regulationrequiring the information needed toprepare Tables 1 to 4 of ECB/2001/13.

• The same applies to Slovakia, which hasbeen receiving stock data fully in line withECB/2001/13 since January 2003.

In terms of accounting rules, a number ofAccession Countries (Bulgaria, Cyprus, CzechRepublic, Malta, Latvia, Estonia, Poland, Slovakiaand Slovenia) have indicated that theircountries have already adopted the EUDirectives on accounting3 and the IAS.

The other Accession Countries still lack fullharmonisation of their monetary statisticswith the ECB requirements. However, thework towards harmonisation in this area is ingeneral already well underway (only Romaniahas not indicated any plans about theimplementation of ECB requirements):

• In Bulgaria, 2003 will be a transitional yearfor the implementation of the ECBrequirements regarding stock data, withwork on the full harmonisation with ECBstandards having already started. Theenvisaged changes aim at obtaining fullcompliance with the sector classificationof the ECB, the identification of thebalances dominated in euro, USD andother foreign currencies, and the maturitybreakdown used by the ECB. Indeed, insome aspects the national requirementswill cover more than what is required bythe ECB.

• In Cyprus, a Sector Manual in accordancewith the ESA 95 is now being finalised,which will be used both to implement theECB’s statistical requirements and tocompile the financial accounts. The workon the harmonisation of monetary statisticswith ECB requirements has already begunwith the creation of a joint working

committee in charge of the design andintroduction of a new reporting scheme.This scheme will permit the collection ofall the necessary data from MFIs, thussatisfying both the ECB’s statisticalrequirements and the supervisory needsof the Central Bank of Cyprus (CBC).Harmonised data is scheduled to becompiled upon accession. The revision ofthe statistical framework will allow fullcompliance with the Regulations andGuidelines of the ECB, the IMF Manual onMonetary and Financial Statistics (2000),as well as with the statistical requirementsof the Bank for International Settlements.

• Malta plans to achieve full harmonisationwith the ESA 95 and the latest ECBstatistical standards by mid-2003. Theperiod between mid-2001 and mid-2003has been dedicated to designing and makingthe necessary preparations for theimplementation of new reporting returnsthat will satisfy the current ECBrequirements.

• Lithuania has developed draft versions ofnew reporting returns and instructions inline with the ECB requirements set out inECB/2001/13. These reporting returns areaddressed to credit institutions subject tominimum reserves and are expected to beadopted in 2003.

• Slovenia has adopted a Regulationintroducing the classification ofinstitutional sectors in line with theESA 95. Since 2000, a gradual alignment tothe ECB standards has taken place,including major changes to the reportingscheme, which already enables thecalculation of harmonised monetaryaggregates and their counterparts.

3 e.g. the Council Directive of 8 December 1986 on the “Annualaccounts and consolidated accounts of banks and other financialinstitutions” (86/635/EEC).

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200318

The residency principle

ECB requirements. The residency principlesapplied by the respective countries also followthe ESA 95 and SNA 1993 (and, consequently,the IMF Balance of Payments Manual, 5th edition),whereby the country of residence of aninstitutional unit is determined by its centre ofeconomic interest.

In terms of the application of the residencyprinciples within money and banking statistics,particular attention should be paid to thetreatment of financial institutions located inoffshore centres (understood as territories withbanking sectors dealing primarily with non-residents and/or in foreign currency, on a scaleout of proportion to the size of the host country).In the framework of euro area money andbanking statistics, offshore institutions are treatedstatistically as residents of the territories in whichthey are located, just like any other residentinstitution.

International or administered banking units(IBUs/ABUs) in Cyprus, which are mainlybranches of foreign banks or subsidiaries offoreign banks incorporated in Cyprus, havealways been considered as non-residentinstitutions because they are required toconfine themselves to transactionsdenominated in currencies other than CYP,and primarily to customers that are notresidents of Cyprus4. For this reason, theseinstitutions are not currently part of the

4 As from 1 January 2001, IBUs and ABUs have been permittedto grant medium and long-term loans in foreign currencies toresidents.

reporting population for the compilation ofmonetary statistics. However, since January2002, when the new statistical definition ofresidency set out in a new directive enteredinto force, IBUs/ABUs have been consideredas resident for b.o.p. and internationalinvestment position (i.i.p.) statisticalpurposes. This definition will also be adoptedfor monetary statistics, in the context of thefull implementation of the ECB’s statisticalrequirements (scheduled to be completedupon accession). The full harmonisationprocess will be facilitated by the abolition ofthe Exchange Control Law upon accession.

Until recently, most offshore non-bankinginstitutions in Malta were treated as non-residents because, although the place ofregistration of such companies was Malta,they were not seen as having a centre ofeconomic interest in the country. As from2003, any firm that either prepares a set ofaccounts, pays income tax in the country orexpects to have a presence there for oneyear or more, is seen as having a centre ofeconomic interest in Malta and, consequently,considered as resident. Thus, there will nolonger be a distinction between offshore andonshore companies. In fact, according to thelaw, all licensed offshore business may onlycontinue to operate until 2004 at the latest. Forthe moment, there is only one international(offshore) bank operating in Malta.

The population of monetary institutions and some borderline cases

ECB requirements. The ECB calculates the euroarea monetary aggregate M3 as the amount ofcurrency in circulation plus other monetaryliabilities issued by the resident money-issuingsector (in the case of deposits, also certainliabilities issued by central government) that areheld by the resident money-holding sector. In thiscontext, the resident money-issuing sectorcorresponds to the euro area monetary financialinstitutions (MFIs), the resident money-neutralsector to the euro area central government, andthe resident money-holding sector to the euro

area residents except MFIs and centralgovernment. The MFI sector comprises, inaddition to central banks, credit institutions asdefined in Community Law and other MFIs, withthe other MFIs in practice comprising moneymarket funds (MMFs) plus a few otherinstitutions.

19ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

The MFI definition is currently beingimplemented by all Accession Countries inthe context of the compilation of theprovisional List of MFIs in the AccessionCountries5. In respect of the first part of thedefinition concerning credit institutions, theongoing integration of the acquiscommunautaire into national legislationensures that the EU concept of creditinstitutions is either already applicable or willsoon be so in the Accession Countries.Furthermore, regarding MMFs, manyAccession Countries have taken steps toimplement this concept into their statisticalsystems.

Credit institutions: some borderlinecases

For the reasons mentioned above, IBUs/ABUsin Cyprus are still considered as non-residentwith regard to monetary statistics. Currently,they are not included in the reportingpopulation for monetary statistics and do notbelong to the money-creating sector(although they are banks, licensed to carryout banking business from within Cyprus). Theabolition of the Exchange Control Law willenable the CBC to consider IBUs/ABUs asresident institutions with regard to monetarystatistics by accession. Co-operative creditand savings societies (CCSSs) in Cyprus arealso currently not included in the reportingpopulation for the compilation of monetarystatistics (although they account for aboutone-third of the total deposits in Cyprus)6.The other financial institutions (OFIs) sector,which used to include specialised banks anddesignated financial institutions, ceased toexist in Cyprus in September 2001. Theseinstitutions have been reclassified as creditinstitutions within the domestic bank (DB)sector. Hence they are included in both themoney-creating sector and the monetaryaggregates. Finally, it should be noted thatthere are two DBs that hold a restrictedbanking licence and are not currently includedin the money-creating sector. IBUs, ABUs,CCSSs and the two DBs with a restrictedbanking licence (which are included in the

provisional List of MFIs because they fulfil thedefinition of credit institutions) will, uponaccession, form part of the reportingpopulation in the area of money and bankingstatistics.

In the Czech Republic, credit unions (calledsavings and credit co-operatives) are classifiedas belonging to the MFI sector and included inthe provisional List of MFIs, but will only beincluded in the money-creating sector in themoney and banking statistics as from 2004.However, the number of active credit unions isconstantly declining7. As the amount of depositswith credit unions is approximately only 0.1%of the total bank deposits of the resident money-holding sector, it might be more cost-effectiveto apply the cutting-off-the-tail principle to theseinstitutions.

As from 2003, credit co-operatives in Romaniawill no longer be excluded from monetarystatistics coverage because they are nowsubject to the central bank’s regulations andsupervision. The central bodies of such creditco-operatives (covering a network of severalhundred individual co-operatives) will startreporting the necessary monetary data. Sofar, only one central body has beenauthorised, but the process of grantinglicenses to other such bodies will continue inthe near future.

In Slovenia, the 2 savings banks and 28 savingsand loan undertakings (which provide servicesto a limited circle of clients) are not includedin the money-creating sector in nationalmonetary statistics, because of the partly

5 A provisional List of MFIs in the Accession Countries was firstpublished in 2001, with the reference date end-December 2000.Updated versions have been published since then on an annualbasis.

6 The main reason being that they are neither subject to thesupervision of the NCB nor to the prudential standards thatapply to credit institutions. CCSSs have indirect access tomonetary credit through the Co-operative Central Bank (whichacts as their central bank) but are not subject to the regulationsissued by the Central Bank of Cyprus.

7 As at December 2002, there were only 46 credit unionsoperating without restrictions and one operating undercompulsory management. The number of credit unions includedin the provisional List of MFIs in December 2000 was 79.

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200320

incomplete breakdown of their accounts inthe past and non-compliance with the bankinglaw. These are indeed very small monetaryfinancial institutions, whose aggregatedbalance sheet has never exceeded 2% of thebalance sheet of the commercial banks. Theharmonisation of these institutions with thebanking law provisions will be achieved in2004, making it feasible to include them inthe money-creating sector in line with theECB requirements.

Credit unions in Latvia do not fall under thecategory of credit institutions. These are co-operative associations with a variable numberof members and capital, established toprovide financial services to their membersas stipulated by the Law on Credit Unions.They are, however, included in the reportingpopulation for money and banking statistics.

Co-operative-type institutions in Estonia alsodo not fall under the category of creditinstitutions. They cannot receive depositsfrom the public, only from their members.They may also only grant loans to members,and their activities are restricted to a certainterritory. Although there are currently 11such institutions, only two of them voluntarilysubmit balance sheet data on a monthly basis.These two are included in the calculation ofEstonian monetary aggregates.

Money market funds

A preliminary analysis made by Poland hasshown that the criteria of the MMF definitionare fulfilled by some investment funds,although the NCB still does not collect anyinformation from them and they are notincluded in the provisional List of MFIs. Thevalue of their assets (total) is beingmonitored, but at present this business ismarginal in comparison with the depositsplaced with the banking sector.

In Hungary, MMFs have been identified andincluded in the provisional List of MFIs since

June 2002, but have been included in themoney-creating sector of money and bankingstatistics since the beginning of 2003. Thenational definition of an MMF is identical tothe ECB definition.

In the Czech Republic, MMFs are identifiedand included in the provisional List of MFIsbut will only be included in the money-creating sector of money and bankingstatistics as from 2004. The value of totalfunds collected by MMFs is approximately 4%of the total bank deposits of the residentmoney holding sector (this share has beenrising constantly over the last two years).The national definition of MMFs should befully harmonised with the ECB definition inthe Czech legal system as from 2004. In themeantime, MMFs have started to harmonisetheir statutes with the ECB definition.

A legal definition of an MMF has not yet beenimplemented in Estonia. For statisticalpurposes, i.e. for the compilation of theprovisional List of MFIs in the AccessionCountries, the NCB has analysed a numberof mutual investment funds in order to selectthe ones that correspond to the ECBdefinition of an MMF. Data on the selectedMMFs are, however, not yet included in thecalculation of monetary aggregates.

Along the same lines, the five MMFs operatingin Malta are also not yet included in theprocess of compiling money and bankingstatistics, but have been included in theprovisional List of MFIs in the AccessionCountries.

Currently no MMFs have been identified inCyprus. However, in the context of theongoing co-operation between the CBC andthe Securities and Exchange Commission, thelatter will inform the CBC whenever it issuesa licence to an MMF.

At present no MMFs have been identified inBulgaria, Lithuania, Latvia, Slovenia, Slovakia andRomania.

21ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

Statistical balance sheets of monetary institutions

ECB requirements. ECB Regulation ECB/2001/13 (as amended) requires MFI balance sheetstatistics to be collected with the followingbreakdown by instrument: on the liabilities side,currency in circulation / deposits / debt securities/ money market fund units and shares / capital& reserves / remaining liabilities. The instrumentbreakdown on the asset side is very similaralthough a different terminology is used, resultingin the following categories: cash / loans /securities other than shares / shares & otherequity / fixed assets / remaining assets. Thisbreakdown is broadly consistent with the ESA95. A further breakdown by counterpart sector(ESA 95-consistent), maturity (at 1 and 2 years)or period of notice (at 3 months and – optionally– 2 years notice) and currency (euro / other) isrequired in respect of liability items in order tocalculate monetary aggregates. Variousbreakdowns are also required in respect of assetitems.

The statistical balance sheets of the money-issuing sector in the Accession Countriesgenerally follow the basic categorisationrequired for the purposes of compiling theconsolidated balance sheet of the MFI sector.In most cases, there is a sufficiently high levelof detail available by instrument, maturity andcounterpart sector to compile data consistentwith the breakdowns required in ECB/2001/13. In some cases, the national requirementseven go beyond what is required by the ECB(e.g. the Czech Republic). As the statisticalbalance sheets reflect national financialmarket conditions and are adapted to meetspecific national requirements, there are ofcourse a number of breakdowns andcategories that still differ from thoseidentified in ECB/2001/13. However,countries where this is the case are, ingeneral, planning to require breakdownsconsistent with ECB/2001/13 from reporting

agents (cf. Poland and Slovenia, for example,as from the end of 2003 and 2004,respectively).

A vital issue is the breakdown of depositliability items vis-à-vis the (potential) moneyholding sector by original maturity. Originalmaturity is a concept used by almost allAccession Countries. Until recently, thenotable exception was Cyprus, but most banksno longer use residual maturity, with theremaining banks expected to adopt originalmaturity, upon implementation of RegulationECB/2001/13. Examples of the originalmaturity cut-off points used are as follows:Bulgaria (at 2 years), Czech Republic (at 3months and 1, 2, 4 and 5 years), Estonia (at 1,2, 3 and 6 months and 1, 2, 3, 5 and 10years), Hungary (at 1 and 2 years), Latvia (at 6months and 1, 2 and 5 years), Malta (at 3 and6 months and 1, 2, 3, 4 and 5 years), Romania(simply ‘short-term’ and ‘long-term’), Poland(at 1, 3 and 6 months and 1 and 2 years),Slovakia (at 1, 3, 6, 9 months and 1, 2, 3, 4, 5and over 5 years) and Slovenia (at 1, 3 and 6months and 1 and 2 years).

The currency breakdown is also important.The currency breakdown of liabilities isgenerally restricted to the separateidentification of balances denominated in localcurrency and those in all foreign currenciescombined (except for deposits in Malta,which are broken down into variousdenominations). Balances denominated ineuro are usually not separately identified. Theexceptions are the Czech Republic, Slovakiaand Hungary (where a split between domestic/ euro / other foreign currency has alreadybeen introduced), Estonia and Latvia (whichhave introduced a breakdown by individualcurrency – including the euro – for the mainbalance sheet items).

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200322

8 A distribution by sector of actual holders based on data from theCentral Depository of Bulgaria is planned for the future.

9 However, due to their full transferability, it is not possible tohave an accurate breakdown of the current holders.

Sector allocation of holdings of negotiable instruments

ECB requirements. ECB Regulation ECB/2001/13does not require reporting institutions to identify theactual holders of their issues of negotiableinstruments (except MFI holdings), in view of thedifficulties in tracking their trade on secondarymarkets. However, in the compilation of euro areamonetary aggregates, an adjustment (for theholdings by non-residents) is made to debt securitieswith a maturity of up to two years. This adjustmentis made using aggregated information on holdersprovided by NCBs (where available) and security-by-security information provided by the two majorinternational securities settlement systems. A similaradjustment, using memo item data supplied byNCBs, was until recently made to deduct non-resident holdings of money market fund shares/units from M3 in the published monetarystatistics. However, ECB Regulation ECB/2002/8 of21 November 2002, amending ECB/2001/13,requires MFIs (and OFIs, when acting in the contextof financial activities involving MMF shares/units) asfrom May 2003 to provide NCBs with necessarydata on the residency breakdown of holders ofMMF shares/units.

In most Accession Countries (e.g. Estonia,Latvia, Lithuania, Malta, Slovenia), nationalbanknotes and coins (in all cases issued bythe NCB and by the government,respectively) are the only “transferableinstruments” included in monetaryaggregates. The amount held by the public is

usually determined as the difference betweenbanknotes and coins issued and those held bythe monetary institutions. Further allocationof banknotes and coins among sectors is notmade. Therefore, national notes and coinsheld by non-residents are usually consideredas being held by residents and are included inthe monetary aggregates. The circulation ofbanknotes denominated in other currencies(euro, US dollar) is not measured.

Other types of transferable instruments areincluded in the monetary aggregates in anumber of Accession Countries. These maycover certificates of deposit, commercialpaper and bank bearer bonds. Usually a fullsector breakdown of their holders cannot bederived. At best, a breakdown by the sectorof the first holder is made, such as for debtsecurities issued in Bulgaria8 or certificates ofdeposits in Romania9. In Cyprus, debt securitiesissued by domestic banks and traded on theCyprus Stock Exchange are mainlydistinguished into those held by providentfunds, legal and natural persons. In the CzechRepublic, data on all securities issued by bankshave been collected. However, a sectorbreakdown by current holder is not availablefor some types of securities. Finally, the Bankof Latvia, in collaboration with the LatvianCentral Depository, plans to start collectingdata on holders of securities in 2003.

Compilation of flow statistics

ECB requirements. The ECB publishes a widerange of euro area statistics in the ECB MonthlyBulletin and on its website, both as amountsoutstanding and as flows. These flow statisticsallow monetary analysis to focus on the actualfinancial transactions between the MFI sectorand the other economic sectors. For this purpose,the ECB removes purely statistical phenomenafrom stock data (i.e. non-transactions) which donot imply a transfer of financing between sectors.The framework for the derivation of euro areamoney and banking flow statistics consists ofadjusting the difference between stocks at the

end of the current and the previous end-monthsfor the non-transactions that have occurredduring this period. There are three types of non-transactions:

• Reclassifications and other adjustments (e.g.changes in the composition of the statisticalreporting population, changes in structure,

23ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

changes in the sector classification of MFIcounterparties, other changes arising from thereclassification of assets and liabilities,corrections of reporting errors), as reportedby the NCBs to the ECB according to ECBGuideline ECB/2003/210;

• Exchange rate changes (changes in the valueof assets and liabilities denominated in aforeign currency due to a change in theexchange rate of the euro vis-à-vis foreigncurrencies) – the ECB calculates a “standardadjustment” using quarterly data reported tothe ECB under ECB/2001/13; and

• Price revaluations (e.g. changes in the valuationof negotiable instruments caused by a changein their price – except the effect of exchangerate changes) and loan write-offs/write-downs.MFIs provide the ECB with data on revaluationadjustments according to ECB/2001/13.

Only a limited number of AccessionCountries have already started preparing (orare further improving) flow statistics usingthe methodologies set by the ECB:

• During 2003, a new data collection systemfor flows statistics will be implemented inEstonia. Data on non-financial transactions(divided into reclassifications, otheradjustments and price revaluation changes)will be collected directly from reportingagents; all the necessary breakdownsneeded to compile ECB flows statisticsshould be available.

• Hungary eliminates from the differences instocks the effects of write-off/write-downsreported by credit institutions and theeffects of exchange rate changes. Themethodology of calculating flows is underrevision because it is not uniform acrossversions of published statistics. As from2003, credit institutions will be able tosubmit all tables relating to the breakdownof flows requested in ECB/2001/13.

• The Czech Republic completed in 2002 thepreparatory work for the data collectionand compilation of flow statistics derived

from the MFI balance sheet stock statisticsin compliance with ECB/2001/13. Data willinitially be collected in a testing regimeand the full changeover to the standardreporting regime is envisaged for mid-2003.The collection of flow data from MMFs incompliance with ECB/2001/13 is, however,not yet under consideration.

• Poland is finalising the statisticalpreparations necessary to compile flowstatistics as far as possible in accordancewith the requirements set out in ECB/2001/13.

• In Lithuania, a new data collection systemfor flows statistics is being developed. Thissystem should cover data on pricerevaluations and loan write-offs/write-downs, as well as on reclassifications andother adjustments collected directly fromreporting agents. The new reportingreturns and instructions in line with theECB regulatory framework, which will beaddressed to credit institutions subject tominimum reserves, will in principle beadopted in 2003.

The remaining Accession Countries in generalonly produce flow data for analyticalpurposes, although some of them havealready indicated plans to adopt the ECBmethodology in the near future:

• Bulgaria also performs some statisticaladjustments of data (changes inclassification, write-offs, etc.), but foranalytical purposes only (these data arenot part of the published official monetarystatistics).

• Malta and Slovenia have indicated thatcurrently flow statistics are not compiled,although major breaks in published dataare usually identified and explained. Malta

10 Guideline of the ECB concerning certain statistical reportingrequirements of the ECB and the procedures for reporting byNCBs of statistical information in the field of money and bankingstatistics (ECB/2003/2).

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200324

has, however, indicated plans to compileflow statistics as from mid-2003.

• In Slovakia, the methodological aspects ofdata collection will be under preparationduring the first half of 2003.

• In the case of Latvia, the data is intended forthe NCB’s own use only and not forpublication. In order to obtain true flows formonetary analysis purposes, this countryadjusts the main items of the creditinstitutions’ aggregated balance sheet forvaluation effects arising from changes in theexchange rates of the national currencyagainst foreign currencies. Where changesoccur due to reclassification or changes inthe reporting population, the stocks of datacan also be adjusted according to thecharacteristics of the time series. In caseswhere adjustments are difficult, they are notmade for past periods. In 2003, Latvia plans

to remove effects arising from changes in theprices of securities and write-offsand write-downs of loans from statisticaldata.

• In Cyprus, during the process of monthlymonitoring of banks’ balance sheets,certain changes due to reclassifications,revaluations and write-offs/write-downsare identified and used for internal analysis.As far as reclassifications are concerned,stocks of data for past periods are adjustedaccordingly if the need arises. The ECB’srequirements for the derivation of flowstatistics will be fulfilled in the context ofthe implementation of Regulation ECB/2001/13. The first harmonised flowstatistics are scheduled to be compiledupon accession to the EU.

Only Romania has not indicated any plans toimprove and/or start compiling flow data.

11 For internal purposes, multiplicative models of TRAMO-SEATSare also used.

Seasonal adjustment of series

ECB practice. Besides the publication of series onnon-seasonally adjusted monetary aggregates(both as levels outstanding and flows), the ECBalso publishes seasonally adjusted levels and flowsof these aggregates using X-12-ARIMA11. Theseasonally adjusted series comprise M1, M2-M1,M2, M3-M2, M3 and “Loans to other euro arearesidents (excluding government)” (for furtherdetails on these seasonally adjusted series, seethe technical notes to Table 2.4 in the ECBMonthly Bulletin and the ECB publication“Seasonal adjustment of monetary aggregatesand Consumer Price Indices (HICP) for the euroarea”. August 2000).

Almost all Accession Countries performsome type of seasonal adjustment of data,although sometimes only for analyticalpurposes and, therefore, not intended forpublication. The only countries not usingtechniques for the seasonal adjustment ofdata are Romania and Estonia.

• Hungary intends to start publishing seasonallyadjusted data for monetary aggregates at the

latest in June 2003. The seasonal adjustmentwill be carried out using the TRAMO/SEATSsoftware package.

• Data in Bulgaria are seasonally adjusted foranalytical purposes only and do not formpart of the officially published monetarystatistics.

• Cyprus publishes (on an annual basis only)seasonally adjusted growth rates for thefollowing series (using the X-11 method ofthe Bureau of the Census, WashingtonDC): currency in circulation, demanddeposits, primary liquidity, quasi-money,total liquidity and claims on the privatesector.

• The Czech Republic seasonally adjustsreserve money and credit issuance data inits banking statistics. However, theseadjusted time series data are not published

25ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

regularly, except for the increment in thenational monetary aggregate M2 and theincrements in adjusted credits in inflationreports. The adjustment procedure coversseasonal factors, which are calculated asaverage relative deviations from the series,smoothed by the centred average method.These factors are checked once every twoyears and, in the event of significantchanges, are corrected. Seasonaladjustment is applied for analyticalpurposes. The current method was chosenbecause of its simplicity. More complexmethods – X-12-ARIMA and TRAMO/SEATS – have been tested with similarresults. The regular official publication ofseasonally adjusted data is underpreparation.

• Latvia seasonally adjusts monetaryaggregates (M1, M2D and M2X inaccordance with the national definitions)using the automated software packagesTRAMO/SEATS for WINDOWS andDEMETRA. Since time series are too short,seasonally adjusted time series are notpublished, but are used internally for thepurpose of analysis.

• In Lithuania, officially published data onmonetary aggregates and theircounterparts are not seasonally adjusted.The possibility of official publication isunder investigation.

• In Malta, published data are not seasonallyadjusted, but occasionally seasonally

adjusted series (using Census-X11) areused in the graphical illustration of certainmonetary statistics.

• Poland has been publishing seasonallyadjusted figures since December 1999 forthe following series: monetary aggregatesM0, M1 and M3, claims of commercialbanks on total domestic sectors,households and non-financial corporations,liabilities of commercial banks to totaldomestic sectors, households and non-financial corporations. Seasonally adjustedtime series are calculated with the SASsystem using the X-11 method of seasonalcorrelation and decomposition.

• The seasonal adjustment of time seriesfrom the relational database using TRAMO/SEATS has been automated in Slovenia sincethe beginning of 2001. Seasonally adjustedseries on national monetary aggregates arepublished in monthly bulletin charts.

• Slovakia has started producing seasonallyadjusted time series of currency incirculation and overnight deposits, atpresent for internal use only. Owing tothe insufficient length of existing timeseries, a multiplicative seasonaldecomposition method was applied foreach time series, separating them intotrend-cycle, seasonal, and randomcomponents. Regular publishing and theuse of a higher-quality tool (TRAMO/SEATS or X-12-ARIMA) are underpreparation for 2003.

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200326

Bulgaria

ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 200328

Bulgaria

List of abbreviations

BISERA Banking Integrated System for Electronic Transfer

b.o.p. balance of payments

BGN Bulgarian leva

BNB Bulgarian National Bank

ECB European Central Bank

ESA 95 European System of Accounts 1995

EUR euro

GDDS General Data Dissemination System

IMF International Monetary Fund

n.a. data are not available

n.c. data have not been collected

NSI National Statistical Institute

OMFIs other monetary financial institutions

RINGS Real-time Interbank Gross Settlement System

SDDS Special Data Dissemination Standard

SNA 1993 System of National Accounts 1993

USD US dollar

VPN Virtual Private Network

29ECB • Money, Banking and Financial Market Statistics in the Accession Countries – Volume I • May 2003

Bulgaria

1 Legal and institutional background

1.1 Organisational structure

1.1.1 Organisation chart of the nationalcentral bank

The main governance body of the BulgarianNational Bank (BNB) is the Managing Board,consisting of a Governor, three DeputyGovernors and three other members. Thereare three main departments in the BNB -Issue, Banking, and Banking Supervision. Themain function of the Issue Department is tomaintain the full foreign exchange reservecoverage of the total amount of the BNB’smonetary liabilities by taking the necessaryactions to effectively manage the Bank’sinternational foreign exchange assets. Shoulda systemic risk emerge that may affect thewhole banking system, the BankingDepartment assumes the functions of acreditor of last resort under the conditionsset forth in the BNB Law. The BankingSupervision Department supervises thebanking system.

See Annex 1.

1.1.2 Organisation of the statistical workat the national central bank

The statistical functions of the BNB areconcentrated in the Statistics Directorate,which is part of the Banking Department.

The Statistics Directorate consists of theMoney and Banking Statistics Division, theBalance of Payments and External DebtDivision, and the General Economic Statisticsand Publications Division. Money and bankingstatistics, as well as interest rates statistics,are compiled by the Money and BankingStatistics Division, which as of January 2003consists of the Monetary Statistics, InterestRates Statistics and Methodology Sections.

See Annex 2.

1.2 Legal background

The legal framework for the BNB isprincipally provided by:

• the Law on the Bulgarian National Bank(June 1997, as amended and supplementedin 1998, 1999, 2001 and 2002);

• the Law on Banks (June 1997, as amendedand supplemented in 1998, 1999, 2000,2001 and 2002).

Certain issues concerning the activities of theBNB are also covered by: