Monetary Policy in India - Macro/Finance,...

51

Monetary Policy in India Ila Patnaik Ajay Shah DEA, July 2007 Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 1 / 48

Transcript of Monetary Policy in India - Macro/Finance,...

Monetary Policy in India

Ila Patnaik Ajay Shah

DEA, July 2007

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 1 / 48

Part I

What is monetary policy and how does it work?

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 2 / 48

What is monetary policy?

Monetary policy is the management of money supply and interestrates by central banks to influence prices and employment.Monetary policy works through expansion or contraction ofinvestment and consumption expenditure.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 3 / 48

The uses of monetary policy

Monetary policy cannot change long-term trend growth.There is no long-term tradeoff between growth and inflation. (Highinflation can only hurt growth).What monetary policy – at its best – can deliver is low and stableinflation, and thereby reduce the volatility of the business cycle.When inflationary pressures build up:

raise the short-term interest rate (the policy rate)which raises real rates across the economywhich squeezes consumption and investment.

The pain is not concentrated at a few points, as is the case withgovernment interventions in commodity markets.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 4 / 48

How central banks of mature market economies work

Election cycle in interest ratesHence, political independence for the narrow task of monetarypolicyThe central bank sets the short rateThe market either explicitly or implicitly knows the inflation targetof the central bank.The short rate is unambiguously set by the central bank and isknown to everyone.The “monetary transmission” : the market process through whichchanges to the short rate lead to changes in all other interest ratesand financial prices.There is no contradiction between financial sector developmentand an effective monetary policy!Key words: focus, independence, transparency, predictability,accountability.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 5 / 48

Money creation

Reserve money is created when the central bank either lends tothe government, or buys foreign exchange thus adding toreserves.Reserve money (M0) induces broad money (M3) through the‘money multiplier’.India’s long-term reform agenda: drop CRR and SLR, whichwould increase the money multiplier.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 6 / 48

Instruments of monetary policy in India

Net loans to central government (i.e. open market operations)Net purchase of foreign currency assetsChange in cash reserve ratioChanges in repo rate and reverse repo rateBank rate

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 7 / 48

Part II

Impossible trinity

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 8 / 48

Monetary policy in an open economy

Impossible trinity:Open capital accountPegged currency regimeIndependent monetary policy

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 9 / 48

Monetary policy in an open economy

ExampleLet us say you have inflation and so want a contractionarymonetary policy.You raise interest rates.Since the capital account is open, capital flows in from abroad inresponse to the higher interest rates.This puts a pressure on the rupee to appreciate.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 10 / 48

But the exchange rate is pegged

ExampleThe Central Bank buys up the dollars coming in to prevent rupeeappreciation.This leads to an expansion in net foreign exchange assets of theCentral Bank and and thus of money supply.Classic symptom of impossible trinity difficulties: raising interestrates but money supply growth is surging.An expansion in money supply will lower interest rates.You cannot raise rates, and keep the exchange rate pegged at thesame time.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 11 / 48

Monetary policy in an open economy

ExampleIf the US hikes the Fed rate, and India stays still, capital will flowout and the currency will depreciate.If the RBI wants to prevent depreciation of the currency, it will haveto sell dollars or raise rates. Both these are contractionary.Currency pegging forces RBI to also raise rates.Thus having a peg means following US monetary policy.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 12 / 48

Monetary policy in an open economy

A country with an open capital account cannot hope to have anindependent monetary policy if it runs a pegged exchange rate.Pegging the exchange rate induces a loss of monetary policyautonomy.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 13 / 48

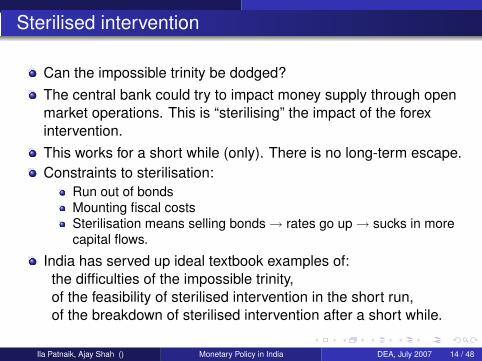

Sterilised intervention

Can the impossible trinity be dodged?The central bank could try to impact money supply through openmarket operations. This is “sterilising” the impact of the forexintervention.This works for a short while (only). There is no long-term escape.Constraints to sterilisation:

Run out of bondsMounting fiscal costsSterilisation means selling bonds→ rates go up→ sucks in morecapital flows.

India has served up ideal textbook examples of:the difficulties of the impossible trinity,of the feasibility of sterilised intervention in the short run,of the breakdown of sterilised intervention after a short while.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 14 / 48

Part III

The story of Indian monetary policy

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 15 / 48

Conceptual framework

1 What was happening in the exchange rate regime?2 How was the currency regime being implemented?3 What were the consequences of the implementation of the

exchange rate regime for monetary policy?

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 16 / 48

Four phases of the INR exchange rate regime0

510

1520

25

Squ

ared

wee

kly

retu

rns

1995 2000 2005

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 17 / 48

Four phases of the INR exchange rate regime35

4045

INR

/US

D r

ate

1995 2000 2005

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 18 / 48

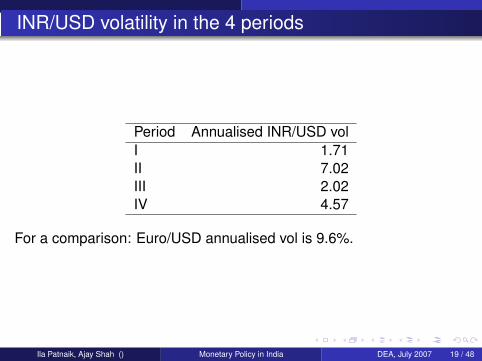

INR/USD volatility in the 4 periods

Period Annualised INR/USD volI 1.71II 7.02III 2.02IV 4.57

For a comparison: Euro/USD annualised vol is 9.6%.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 19 / 48

The evolution of the INR exchange rate regime

Period 1: April 1993 to February 1995 Period where trading in the INR firstbegan. For most of this period the exchange rate was Rs.31.37per dollar.

Period 2: February 1995 to August 1998 The period of the Asian crisis, therewas the highest-ever currency flexibility in India’s experience.

Period 3: August 1998 to March 2004 Tight pegging, with low volatility andsome appreciation.

Period 4: March 2004 - Greater currency flexibility.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 20 / 48

The evolution of the INR exchange rate regime

Period 1: April 1993 to February 1995 Period where trading in the INR firstbegan. For most of this period the exchange rate was Rs.31.37per dollar.

Period 2: February 1995 to August 1998 The period of the Asian crisis, therewas the highest-ever currency flexibility in India’s experience.

Period 3: August 1998 to March 2004 Tight pegging, with low volatility andsome appreciation.

Period 4: March 2004 - Greater currency flexibility.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 20 / 48

The evolution of the INR exchange rate regime

Period 1: April 1993 to February 1995 Period where trading in the INR firstbegan. For most of this period the exchange rate was Rs.31.37per dollar.

Period 2: February 1995 to August 1998 The period of the Asian crisis, therewas the highest-ever currency flexibility in India’s experience.

Period 3: August 1998 to March 2004 Tight pegging, with low volatility andsome appreciation.

Period 4: March 2004 - Greater currency flexibility.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 20 / 48

The evolution of the INR exchange rate regime

Period 1: April 1993 to February 1995 Period where trading in the INR firstbegan. For most of this period the exchange rate was Rs.31.37per dollar.

Period 2: February 1995 to August 1998 The period of the Asian crisis, therewas the highest-ever currency flexibility in India’s experience.

Period 3: August 1998 to March 2004 Tight pegging, with low volatility andsome appreciation.

Period 4: March 2004 - Greater currency flexibility.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 20 / 48

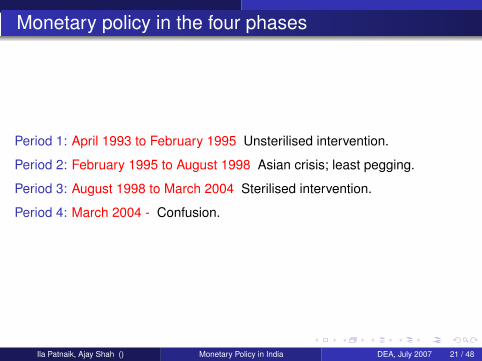

Monetary policy in the four phases

Period 1: April 1993 to February 1995 Unsterilised intervention.

Period 2: February 1995 to August 1998 Asian crisis; least pegging.

Period 3: August 1998 to March 2004 Sterilised intervention.

Period 4: March 2004 - Confusion.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 21 / 48

Period 1

1 Began as a surge in capital inflows.2 RBI bought USD to prevent appreciation beyond Rs.31.37.3 There was no bond market to speak of.4 NFA and M0 went up.5 M3 growth accelerated.6 Inflation rate rose to 16 percent.7 Monetary tightening through CRR and interest rate hikes started

when faced with high inflation. This was after a year of almost nosterlisation.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 22 / 48

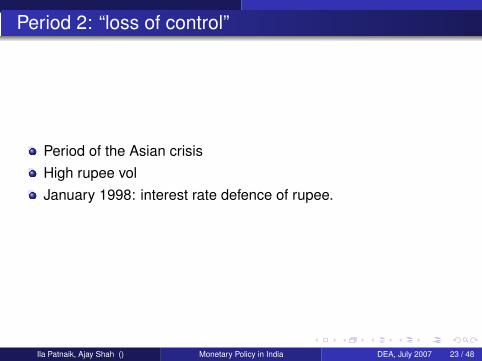

Period 2: “loss of control”

Period of the Asian crisisHigh rupee volJanuary 1998: interest rate defence of rupee.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 23 / 48

Period 3: Successful sterilised intervention

1 By now the bond market was much better developed.2 The bond market was actively used for OMO.3 CRR phaseout program stayed on course.4 M0 and M3 growth were contained5 Inflation remained below 10 percent.6 But the real rate dropped to negative numbers, thus setting the

stage for trouble after Period 3.7 Period 3 broke down when RBI ran out of government bonds for

OMO.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 24 / 48

Part IV

Current challenges to monetary policy (Period IV)

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 25 / 48

Challenge of open economy

Year Gross flowsTrillion rupees Percent to GDP

1999-00 9.16 51.282006-07 41.18 110.01

Measured in rupees: gross flows across the current and capitalaccounts grew by 4.5 times in seven years.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 26 / 48

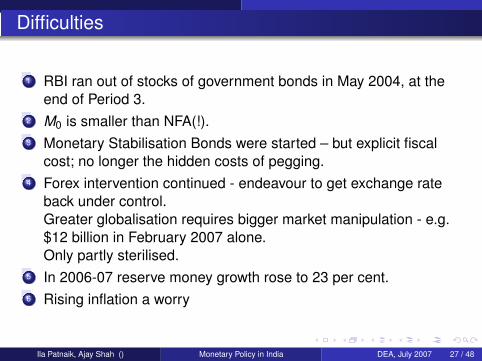

Difficulties

1 RBI ran out of stocks of government bonds in May 2004, at theend of Period 3.

2 M0 is smaller than NFA(!).3 Monetary Stabilisation Bonds were started – but explicit fiscal

cost; no longer the hidden costs of pegging.4 Forex intervention continued - endeavour to get exchange rate

back under control.Greater globalisation requires bigger market manipulation - e.g.$12 billion in February 2007 alone.Only partly sterilised.

5 In 2006-07 reserve money growth rose to 23 per cent.6 Rising inflation a worry

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 27 / 48

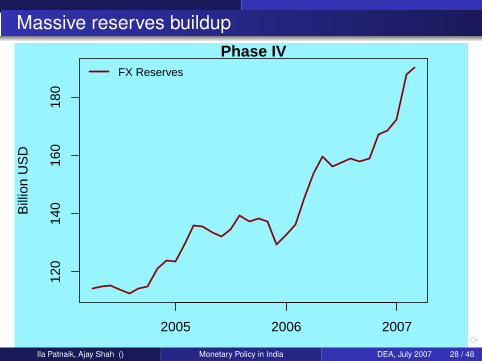

Massive reserves buildup

120

140

160

180

Phase IV

Bill

ion

US

D

2005 2006 2007

FX Reserves

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 28 / 48

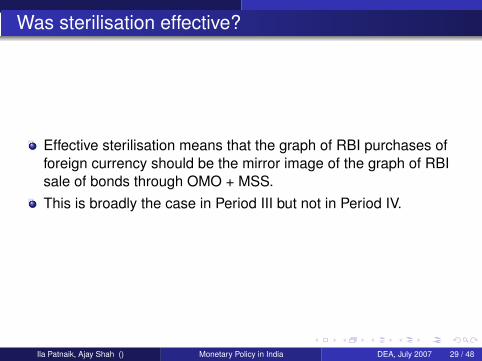

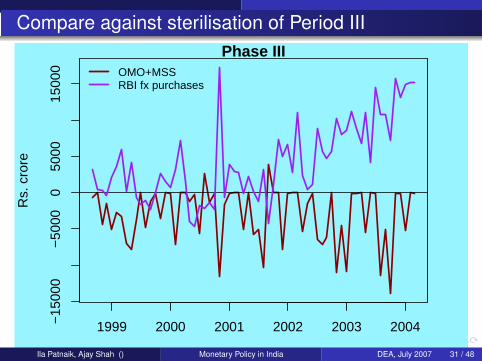

Was sterilisation effective?

Effective sterilisation means that the graph of RBI purchases offoreign currency should be the mirror image of the graph of RBIsale of bonds through OMO + MSS.This is broadly the case in Period III but not in Period IV.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 29 / 48

Ineffectual sterilisation - OMO + MSS

−20

000

020

000

4000

0Phase IV

Rs.

cro

re

2005 2006 2007

OMO+MSSRBI fx purchases

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 30 / 48

Compare against sterilisation of Period III

−15

000

−50

000

5000

1500

0Phase III

Rs.

cro

re

1999 2000 2001 2002 2003 2004

OMO+MSSRBI fx purchases

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 31 / 48

Movement of NFA and M0

−2e

+05

2e+

056e

+05

Phase IV

Leve

ls (

Rs.

cro

re)

2005 2006 2007

NFAM0NDA

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 32 / 48

Compare against the picture in Period III

−1e

+05

1e+

053e

+05

5e+

05 Phase III

Leve

ls (

Rs.

cro

re)

1999 2000 2001 2002 2003 2004

NFAM0NDA

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 33 / 48

Acceleration in M0 and M3 growth

1012

1416

1820

2224

Phase IV

Per

cent

age

chan

ge (

YO

Y)

2005 2006 2007

Growth in M0Growth in M3

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 34 / 48

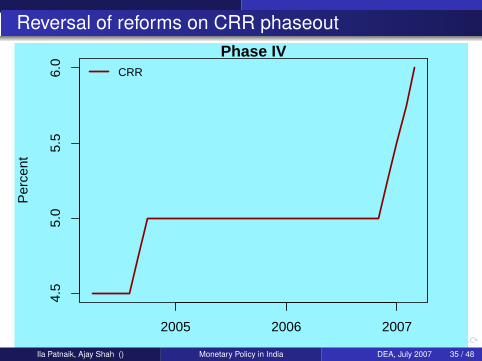

Reversal of reforms on CRR phaseout

4.5

5.0

5.5

6.0

Phase IV

Per

cent

2005 2006 2007

CRR

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 35 / 48

Compare against the fuller picture on CRR phaseout

68

1012

14Full Period

Per

cent

1995 2000 2005

CRR

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 36 / 48

Improvement of money multiplier got stalled

4.6

4.7

4.8

4.9

5.0 Phase IV

2005 2006 2007

M3/M0

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 37 / 48

Inflationary pressures

45

67

8Phase IV

Per

cent

2005 2006 2007

Inflation

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 38 / 48

Monetary policy has tried to tighten?

4.5

5.0

5.5

6.0

6.5

7.0

7.5

Phase IV

Per

cent

2005 2006 2007

CRR91−day rate

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 39 / 48

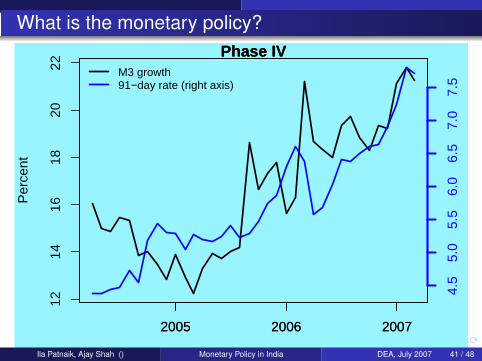

What is the monetary policy?

1012

1416

1820

2224

Phase IV

Per

cent

2005 2006 2007

Phase IV

2005 2006 2007

4.5

5.0

5.5

6.0

6.5

7.0

7.5

M0 growth91−day rate (right axis)

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 40 / 48

What is the monetary policy?

1214

1618

2022

Phase IV

Per

cent

2005 2006 2007

Phase IV

2005 2006 2007

4.5

5.0

5.5

6.0

6.5

7.0

7.5

M3 growth91−day rate (right axis)

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 41 / 48

Monetary policy has been behind the curve

45

67

8Phase IV

Per

cent

2005 2006 2007

91−day rateWPI inflation

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 42 / 48

Real rates remain too low to reduce inflation

−3

−2

−1

01

2Phase IV

Per

cent

2005 2006 2007

Real interest rate

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 43 / 48

What is the monetary policy?

In a mature market economy, the central bank unambiguouslypins down the short rate.The financial markets are told the ‘monetary policy rule’ so theyhave expectations about future values of the short rate.Using this, the market traces out the full yield curve.RBI has two short rates, not one: 6% and 7.75%.At 7.75% the transactions are roughly zero.At 6% the transactions are capped at Rs.3000 crore.The central bank has stopped performing its core function, that ofpinning down the short rate.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 44 / 48

Part V

Summary

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 45 / 48

Key messages

Monetary policy is supposed to be about pinning down the shortrate so as to achieve an inflation target, and thus stabilise themacroeconomy.Pegged exchange rate + de facto convertibility “uses up” the leverof monetary policy.There is a loss of autonomy in the conduct of monetary policy.India’s monetary regime is largely India’s exchange rate regime:

Period 1 MP was dominated by Rs.31.37 (unsterilised)Period 2 Currency flexibility + interest rate defencePeriod 3 Sterilised interventionPeriod 4 Confusion.

The biggest question today: What is the monetary policy?

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 46 / 48

Further reading

India’s experience with a pegged exchange rate by Ila Patnaik, in IndiaPolicy Forum 2004, Brookings Institution Press and NCAER, 2005,edited by Suman Bery, Barry Bosworth and Arvind Panagariya.http://openlib.org/home/ila/PDFDOCS/Patnaik2004_implementation.pdf

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 47 / 48

Thank you.

Ila Patnaik, Ajay Shah () Monetary Policy in India DEA, July 2007 48 / 48

![How China Lends [cover here] - Center for Global Development](https://static.fdocuments.in/doc/165x107/61878b32b973f64e8045e493/how-china-lends-cover-here-center-for-global-development.jpg)