![UKCP Supervision Policy - UK Council for Psychotherapy UKCP_Supervision_DocumentAM[3].doc UKCP Supervision Policy Contents 1. Introduction: Generic UKCP Supervision Policy Supervision](https://static.fdocuments.in/doc/165x107/5b42cf1b7f8b9a14058b595a/ukcp-supervision-policy-uk-council-for-psychotherapy-ukcpsupervisiondocumentam3doc.jpg)

Monetary Policy and Banking Supervision: Is There a … · · 2018-03-08Monetary Policy and...

22

Monetary Policy and Banking Supervision: Is There a Conflict of Interest? * D. Lima * I. Lazopoulos † V. Gabriel † December 17, 2012 Abstract The objective of this paper is to empirically assess whether central banks are less ag- gressive in their inflation mandate when they are in charge of banking regulation, since tight monetary policy conditions could have an adverse effect on the stability of the bank- ing system. Due to this conflict of interest between the monetary policy makers and bank regulators, it has been argued that banking supervisory powers should be assigned to an independent authority to avoid an inflation bias. We perform an econometric analysis using panel data for 25 industrialised countries from 1975 to 2007 to analyse the impact of a country’s institutional mandate of monetary policy and banking supervision on in- flation outcomes. Using a fixed effects approach, the estimation results obtained do not provide evidence to suggest that separation of banking supervision and monetary policy has a significant effect on inflation outcomes. Nevertheless, results show that other insti- tutional factors, such as inflation targeting and deposit insurance schemes, are significant determinants of inflation outcomes. Key words: monetary policy, banking regulation, institutional mandates. 1 School of Economics, University of Surrey and Central Bank of Portugal. 2 School of Economics, University of Surrey. * Supported by FCT - Fundacao para a Ciencia e a Tecnologia, through project SFRH / BD / 69139 / 2010. 1

Transcript of Monetary Policy and Banking Supervision: Is There a … · · 2018-03-08Monetary Policy and...

Monetary Policy and Banking Supervision: Is Therea Conflict of Interest?∗

D. Lima∗ I. Lazopoulos† V. Gabriel†

December 17, 2012

Abstract

The objective of this paper is to empirically assess whethercentral banks are less ag-gressive in their inflation mandate when they are in charge ofbanking regulation, sincetight monetary policy conditions could have an adverse effect on the stability of the bank-ing system. Due to this conflict of interest between the monetary policy makers and bankregulators, it has been argued that banking supervisory powers should be assigned to anindependent authority to avoid an inflation bias. We performan econometric analysisusing panel data for 25 industrialised countries from 1975 to 2007 to analyse the impactof a country’s institutional mandate of monetary policy andbanking supervision on in-flation outcomes. Using a fixed effects approach, the estimation results obtained do notprovide evidence to suggest that separation of banking supervision and monetary policyhas a significant effect on inflation outcomes. Nevertheless, results show that other insti-tutional factors, such as inflation targeting and deposit insurance schemes, are significantdeterminants of inflation outcomes.

Key words: monetary policy, banking regulation, institutional mandates.

1School of Economics, University of Surrey and Central Bank of Portugal.2School of Economics, University of Surrey.∗Supported by FCT - Fundacao para a Ciencia e a Tecnologia, through project SFRH / BD / 69139 / 2010.

1

1 Introduction

The recent financial crisis raised the debate regarding the institutional architecture of mone-tary policy and banking regulation:1

“ In the clear light of morning, the legal or otherwise effective divorce be-tween central bank and supervisory agency, or monetary policy and regulatorypolicy, was a mistake. (...) The guards in the twin towers of monetary policyand regulatory policy surveyed their compounds as if the other did not exist. (...)Monetary policy was deliberately oblivious to the asset price boom – that wassomebody else’s problem. Regulatory policy was oblivious to macro risks – thatwas the central bankers’ job. (...) In booms there is a premium to new trends anda discount on old ideas and much good is abandoned for the sakeof modernity”.

- Avinash Persaud, Feb 21st 2011, The Economist

Historically, the institutional arrangements concerningthe monetary policy and banking reg-ulation were mainly influenced by two distinct traditions; the English influence where mon-etary policy and banking supervision are combined under thecentral bank, and the Germaninfluence where these functions are separated.2 According to Haubrich (1996), the origin ofthese different traditions is related to the evolution of the payment system. Countries thatadopted the English tradition experienced a rapid expansion of credit through the introduc-tion of alternative forms of money, where the central banks naturally became the guarantorsof the smooth functioning of the payment system and the regulators in these market-based fi-nancial systems. In contrast, countries that experienced aslow expansion of credit developeda bank-based financial system of well-capitalised banks that were regulated by an indepen-dent authority following the German tradition.However, in the late nineties there was a tendency for the separation of these functions fol-lowing the German tradition.3 According to Masciandaro (2009), in a sample of 91 countries,94% chose to reform their financial supervisory architecture between 1986 and 2006, whichsuggests that there has been a tendency to unify the financialsystem regulators within thesame agency that is different from the central bank. In particular, it is shown that the degreeof unification of financial regulators is inversely related to the central bank’s role in bankingregulation and supervision. More recently, the 2008 financial crisis questioned this apparentconsensus towards the separation of functions, and many countries, including the EuropeanUnion and the United Kingdom, are currently implementing reforms regarding the role of thecentral bank in banking supervision mandates (Dalla Pellegrina et al., 2010).Notwithstanding the institutional mandate trends around the world, there are strong argu-ments for and against separation of banking supervision from the central bank in the aca-demic literature. The aim of this paper is to empirically examine if monetary policy makersand bank regulators have conflicting interests by assessingwhether a combined institutionalmandate has led to higher inflation rates, on average, than a separate regime. This important

1In this paper, following the literature, we have opted to notdistinguish between the concepts of bankingregulation and banking supervision.

2For example, countries with an English influence include theUnited States, United Kingdom, Australia andHong Kong, whereas countries with German influence include Austria, Germany, Denmark, and Switzerland.

3Most notably, in 1999 the European Central Bank was assignedthe responsibility for the conduct of mon-etary policy in the euro-area and the national authorities became in charge of the banking regulation and super-vision. Likewise, United Kingdom and Australia had opted for the separation of these functions.

2

argument in favour of the separate regime states that a central bank responsible for bankingregulation will be more flexible in its inflation mandate if itfears that tight monetary condi-tions may cause bank distress due to adverse effects of high interest rates on the profitabilityand soundness of the banking sector (Goodhart and Schoenmaker 1993 and 1995).4 Underthese circumstances, it is likely that the flexibility in guiding monetary policy will lead tohigher inflation rates.There is evidence in the literature that supports the existence of a conflict of interest betweenmonetary policy makers and bank regulators. Using data fromthe United States over the pe-riod 1990-1998, Ioannidou (2005) examines whether monetary policy responsibilities haveimplications in the conduct of the bank supervision when theFederal Reserve System (Fed)is responsible for both functions.5 The results suggest that monetary policy influences Fed’ssupervisory actions as it turns out to be more flexible in its bank supervisory role when ittightens the monetary policy stance. Moreover, focusing on25 industrialised countries overthe period 1960-1996, Di Noia and Di Giorgio (1999) find evidence that average inflationrate is explained by countries’ institutional mandate whencontrolling for central bank inde-pendence from the government. The authors conclude that central banks are less effective incontrolling inflation when they are responsible for the regulation of the banking sector. In asimilar study, Copelovitch and Singer (2008) consider 23 industrial countries from 1975 to1999 and found empirical evidence that inflation rates have been significantly lower, on av-erage, in countries where the central bank and the banking supervisor are separate agencies.This effect is conditional on the choice of the exchange rateregime and the size of the do-mestic banking sector. In particular, the separation mandate has a significant negative effecton inflation under floating rates, but this effect is only observed at middle to high levels ofbanking sector size.Our analysis is based on the works of Di Noia and Di Giorgio (1999) and Copelovitch andSinger (2008), but we introduce a number of innovations. First, the time span of the sampleis enlarged from 1999 to 2007. The end date falls before the start of the recent recession of2008, because our aim is to capture normal times. Second, we suggest the use of appropriatemethods to estimate panels, such as fixed effects. In addition, we implement two differentdata specification approaches; one follows Copelovitch andSinger (2008)’s approach of five-year average inflation rate, while the other uses annual panel data. Fourth, we introduceadditional explanatory variables, such as inflation targeting, oil imports as percentage of GDPand bank concentration index.The estimation results show that the separation of banking supervision from the central bankdoes not have a significant impact on inflation. In this sense,the conflict of interest argumentagainst combination of monetary policy and banking supervision is not supported by ourempirical findings. More interestingly, we find that inflation targeting and deposit insuranceare the main institutional driving forces of low inflation rates. Bank concentration, as a proxyfor the market structure of the banking system, is also significant and it has a negative impacton inflation outcomes. External factors, such as trade and capital account openness, are also

4The impact of short-term interest rates on banks’ profitability and solvency does not only depend on the thelength of time for which high interest rates are likely to persist, but also on the structure of the banks’ balancesheet, i.e. the interest sensitivity difference between assets and liabilities and the weighted average maturity offixed rate assets relative to variable rate liabilities.

5Note that the regulatory architecture of the banking systemin the United States is such that the Fed alongwith the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation(FDIC), all share the supervisory powers, but the Fed is the only regulator responsible for monetary policy.

3

important determinants of inflation. In addition, our empirical evidence indicates that centralbank independence has only a negative significant impact on inflation rates when we are notcontrolling for the external factors.The paper proceeds as follows. Section 2 presents the data and describes the methodologyused. The estimation results are presented in Section 3, andSection 4 concludes.

2 Empirical Analysis

2.1 Data

We consider annual time series data for 25 OECD countries over the period 1975-2007. Thedependent variable is the annual inflation rate, in logarithmic form. The selection of explana-tory variables is based on Copelovitch and Singer (2008), but we also include a number ofvariables that we believe can be related to inflation. Appendix 1 provides the definition anddata sources for each explanatory variable considered in the econometric analysis.The banking supervisory separation variable (thereafterseparate) is the main explanatoryvariable we are interested in, since the purpose of this study is to measure the impact ofa separate banking supervision mandate on inflation behaviour. We defineseparateas adummy that takes value of 1 if, in a certain country, the functions of monetary policy andbanking regulation are conducted by two independent institutions, and value 0 in the op-posite case, which we classify as a combined mandate. The classification of countries intothese two groups (separate or combined) was based on information disclosed by the WorldBank Regulation and Supervision Survey (updated June 2008)6, which collected informationfrom supervisory authorities located in 142 countries for the year 2006. This informationwas complemented with other sources. We consulted Copelovitch and Singer’s classificationand in the cases for which there was uncertainty about the type of mandate, the central banksand supervisory agencies websites were also checked. The Courtis (2011) survey about thesupervision arrangements around the world was also used to confirm our previous classifica-tion. Table 1 shows the evolution of the institutional arrangements and inflation rates in the25 countries included in our sample along the period 1975-2007.

6In addition, we have also analysed the responses from an older version of the same survey (2000).

4

Table 1: Number of countries with separate and combined mandates per year and average inflation rates.

Year Separate Mandate Combined Mandate Inflation Rate1975 8 17 13.5%1980 8 17 13.4%1985 7 18 8.0%1990 7 18 6.1%1995 7 18 3.3%2000 12 13 2.5%2005 14 11 2.1%2007 14 11 2.2%

In 1975, the banking supervision responsibilities were assigned to the central bank in 17countries, whereas only 8 countries had preferred to allocate this policy to a different author-ity. This distribution remained stable until late 1990’s, when we observe an increase in thenumber of countries that have opted to separate their banking supervision functions from themonetary policy authority: in 2000, 12 presented a separateinstitutional mandate and 13 acombined one. In 2007, the last year considered in our sample, the majority of countries (14out of 25) had preferred to assign their banking supervisionpowers to a different authority.During the sample period, inflation rates also decreased substantially: in 1975, the globalsample inflation was 13,5% on average, and in 2007 it had decreased to 2,2%.The classification of countries in terms ofseparateandcombinedinstitutional mandates ispresented in Appendix 2. For the euro area member states, we assume a separate bank-ing supervision regime after their entrance in the EuropeanMonetary Union, in 1999,7 sincemonetary policy is centralised in the European Central Bank.8We expect that a separate bank-ing supervision regime will have a negative impact on inflation rates, as argued by the conflictof interest effect.A pool of additional regressors is considered and they are divided in four categories: insti-tutional, external, economic and banking structure. In addition to the variableseparate,weinclude as institutional factors central bank independence (CBI), explicit deposit insurance,inflation targeting, exchange rate regime, euro membershipand a dummy variable to accountfor the great moderation period.There is a large literature following Cukierman et al. (1992) that suggests a significant nega-tive impact of the degree of independence of the central bankon inflation outcomes. Thus, itis expected that a country with a higher degree of central bank independence will also have,on average, lower inflation rates. However, the empirical evidence is not conclusive, since al-though the first studies confirm a significant effect of CBI on inflation rates (Grilli et al., 1991and Cukierman et al., 1992), there are recent papers that do not find a strong effect (Mangano,1998 and Crowe and Meade, 2007). The CBI variable is based on the work of Arnone et al.(2007). In their study, they update the Cukierman et al. (1992) and Grilli, Masciandaro andTabellini (1991) measures for central bank political and economic autonomy. Political auton-omy is interpreted as the power of central banks to define and implement monetary policy,

7Except for Greece, that joined the European Monetary Union in 2001.8It can also be argued that the European Monetary Union is a combined mandate, in the sense that the

national central banks are part of the Euro System. We perform a sensitiveness analysis to assess for the oppositecase, in which we assume a combine institutional mandate between monetary policy and banking supervision,whenever the national central bank is in charge of supervisory responsibilities. The estimation results do notchange substantively.

5

whereas economic autonomy evaluates the central banks operational independence. The CBImeasures that we find in the literature are usually computed for certain periods of time. Thismeans that is not possible to find a time series for a CBI index.The way researchers circum-vent this problem is by assuming that CBI measures do not change significantly across time.We follow this approach, and we assume the CBI measures computed in the late 80’s do notvary till 2003, the year for which Arnone et al. (2007) updatethe index.Another institutional determinant of low inflation rates isassociated to depositors protection.A country with an explicit deposit insurance scheme with therole of protecting depositorsfrom losses in the event of a bank failure, will experience, on average, lower inflation rates,because the central bank can be aggressive on its inflation mandate as it is not concernedabout the effect of interest rates on banking stability. Thedeposit insurance variable takesvalue of 1 for countries with explicit deposit insurance andof 0 otherwise. The classificationuses information from the World Bank Deposit Insurance Around the World Dataset, from1975 to 2003, and from the International Association of Deposit Insurers (IADI), for theremaining years.To account for the effects of inflation targeting on inflationbehaviour we introduce a dummyvariable that takes value of 1 at the year that a country adopted inflation targeting and on-wards9 and value of 0 in the remaining cases. The classification is based on Roger (2010).Since this approach pursues an explicit public commitment to control inflation as the princi-pal policy goal we expect that a country that has adopted inflation targeting will experiencelower inflation rates. The exchange rate regime variable takes value of 1 for all varieties of“hard” fixed exchange rates and 0 for floating or managed floating regimes. Data is based onthe International Monetary Fund classification, by Ilzetzki, Reinhart and Rogoff (2008). TheGreat Moderation dummy variable is included to control for the persistent decline of inflationrates in the developed world since the early 1980’s. The structural breaking point is the year1984 following McConnell and Perez-Quiros (2000). Euro membership is controlling for theEuro Area countries’ specific monetary policy mandate and ittakes the value of 1 from 1999onwards for the Euro Area member countries, except for Greece, that entered the EuropeanMonetary Union in 2001.In order to capture for the impact of external factors, we consider trade openness, capital ac-count openness and oil imports as percentage of GDP. Trade openness is measured as the sumof imports and exports as a percentage of GDP and the data is taken from the ComparativePolitical Dataset (1960-2009). Theory predicts an inverserelation between trade opennessand inflation: more open economies will benefit from lower inflation, on average. The de-gree of openness affects inflation through two different channels (Romer, 1993). First, in atheoretical model of monetary policy without precommitment, a more closed economy has ahigher incentive to engage in surprise inflation since its impact on the real depreciation is lesscostly, given that the fraction of imported goods is lower inthis economy.10 Second, open-ness affects the output-inflation trade-off: for a given increase in output, the rise in domesticprices will be higher as more open the economy is, given the exchange rates disciplining ef-fect. Thus, monetary policymakers incentives to engage in expansionary policies are lower inmore open economies, and therefore inflation is expected to be smaller. Empirical evidence

9In our sample, the countries that use inflation targeting areNew Zealand (since 1990), Canada (since 1991),United Kingdom (since 1992), Sweden (since 1993), Australia (since 1993), Iceland (since 2001) and Norway(since 2001). Finland and Spain adopted inflation targeting, in 1993 and 1995 respectively, but abandoned itwhen they entered the Euro Area, in 1999.

10In these models it is assumed that domestic and foreign goodsare not perfect substitutes.

6

supports theory, by showing a strong and robust negative impact of openness on inflationoutcomes (Romer, 1993).Capital account openness is measured using the Chinn-Ito index, developed in Chinn and Ito(2006).11 This index accounts for restrictions on capital account transactions, current accounttransactions, requirements of the surrender of exports proceeds and the presence of multipleexchange rates. Similarly to trade openness, empirical evidence shows a negative relationshipbetween financial openness and inflation (Gruben and McLeod,2002 and Gupta, 2008). Foroil imports, we expect that an increase in oil prices will have a positive effect on inflationof oil importer countries. The data for the value of oil imports is from the World EconomicOutlook Database, published by the International MonetaryFund.To account for the effect of economic conditions on inflation, we include log of Gross Do-mestic Product (GDP), log of GDPper capita, currency crisis and banking crisis. Currencyand banking crisis are dummy variables that take value of 1 whenever the country is experi-encing a currency or a banking crisis.12 We expect that inflation will be higher on averagewhen the country is going through a banking or currency crisis. The log of GDP and GDPper capita were considered to control for the size and the level of development of countries,respectively.Lastly, to allow for the possibility that the magnitude of the influence of institutional man-dates of monetary policy and banking supervision on inflation outcomes may be affected bythe structure of the banking system, two variables were included: the size of the bankingsystem, measured by domestic credit over GDP, and the degreeof banking concentration,measured by the ratio of total assets held by the three largest banks in each country over thebanking system total assets.13 The size of the banking system may have a negative impacton inflation outcomes, since when the banking system contributes to a larger share of thedomestic economy, a supervisory central bank will be more concerned about the monetarypolicy effects on bank stability (Copelovitch and Singer, 2008). The impact of the degreeof bank concentration on inflation is not as straightforward. There are two distinct views inthe literature concerning the impact of banking concentration on the monetary policy trans-mission mechanism. One view, more common, states that higher concentration implies lesscompetition, higher profitability due to greater interest margins between deposits and loans,and therefore a less efficient transmission mechanism of monetary policy to the real economy.In this case, we would expect a positive impact of bank concentration measures on inflation.Alternatively, the efficient-structure theory (Demsetz, 1973) argues that cost-efficient bankscould drive cost-inefficient banks out of the market and increase their market share, whichwould lead to higher concentration and greater profitability. In this situation, profitabilityis generated due to cost efficiency and the transmission of monetary policy is not affectedas interest margins are also not affected. Therefore, according to this approach, a higherconcentration degree in the banking industry would lead to lower inflation rates.Table 2 summarises the expect impact of each explanatory variable on inflation rates.

11The Chinn-Ito index is taken from the Comparative PoliticalDataset (1960-2009).12For banking crisis, data is based on Glick and Hutchison (1999), except for Australia and USA, for which

data comes from Caprio and Klingebiel (2003). For the remaining years (2000-2007), data comes from Laevenand Valencia (2010). For currency crisis, data is based on Glick and Hutchison (1999), except for Australia andUSA, for which the data comes from Laeven & Valencia (2008). For the years 2000-2008, data comes fromLaeven and Valencia (2008).

13For the period 1988-1997, the data follows Beck, Demirguk-Kunt and Levine (2006). From 2002 onwards,we update the dataset using Orbis database to compute the index.

7

Table 2: Regressors’ expected impact on inflation.

Variable DescriptionExpected Impact

on Inflation

Institutional FactorsSeparate CB Yes = 1 −

CBI Central Bank Independence Index −

Inflation Targeting Yes = 1 −

Great Moderation 1975-83 = 0; 1984-2007 = 1 −

Deposit Insurance Yes = 1 −

Exchange Rate Regime Fixed = 1 +Euro Membership Yes = 1 ?

External FactorsTrade Openness Index −

Capital Accounts Openness Chinn-Ito Index −

Oil Imports (% GDP) Controls for oil importing countries +Economic Factors

GDP (log) Controls for size of the economies +GDP per capita (log) Controls for wealth of the economies −

Banking Crisis Yes = 1 +Currency Crisis Yes = 1 +

Banking Structure FactorsBank Concentration Index Controls for the banking sector degree of concentration + / −Domestic Credit (% GDP) Controls for the banking sector size −

2.2 Model Specification

In order to estimate the relationship between inflation rates and institutional arrangements ofbanking regulation and supervision, we adopt the followingregression model:

πi,t = β0+β1separatei,t +λXi,t +ui,t (1)

where,πi,t is the (logged) inflation rate for countryi in yeart, separatei,t is a binary variablethat takes value of 1 if the country is classified as separate at time t and value of 0 otherwise,Xi,t is a vector of control variables included in the model (see Section 3.1 for a description ofthe variables) andui,t is the error term.The econometric analysis is developed in two stages. First,we suggest the use of annualpanel data, that comprises a time-series component of 33 years, ranging from 1975 to 2007,and a cross-section pool of 25 advanced countries. Second, we follow Copelovitch and Singer(2008) that compute five-year averages for inflation rates, assuming that many of the institu-tional determinants of inflation rates included in their model change infrequently. It is formedby a time-series component of 7 time periods and a cross section component of 25 developedcountries.For each data specification, annual and 5 years average paneldata, we estimate a Full Model(Model 1), that includes all explanatory variables described previously. Then, we test forthe collective statistical significance of the exclusion ofeach block of explanatory variables(external, economic and banking structure regressors), bycalculating a F Test. The estimationresults are presented for each version of the model (Models 2, 3 and 4, respectively). In

8

addition, we estimate a reduced version of Model (1) that includes only institutional factors.14

The models are estimated by using a Fixed Effects approach.15 Panel data models have someadvantages over cross-section or time series models, because they integrate heterogeneityacross units (individuals, firms or countries) that is typical in microeconomic data. This het-erogeneity is taken explicitly into account by allowing forindividual-specific variables. Ifit is assumed that heterogeneity (individual effect) is correlated with the regressors, fixed-effects model may be appropriate, whilst if it is not assumedthat there is correlation, therandom-effects model may perform better. Since we assume that there are country-specificcharacteristics in this model that can be correlated with the explanatory variables, such as cul-ture, geographic location, language, among others, we consider that a Fixed Effects approachis more adequate than a Random Effects approach.Among the main weaknesses of using panel data are estimationand inference problems, suchas heteroskedasticity and autocorrelation, since it involves both cross-section and time seriesdata. In order to correct for heteroskedasticity problemswe use a fixed effects approach withcorrected standard errors.The estimation results are presented in section 3.3.

2.3 Estimation Results

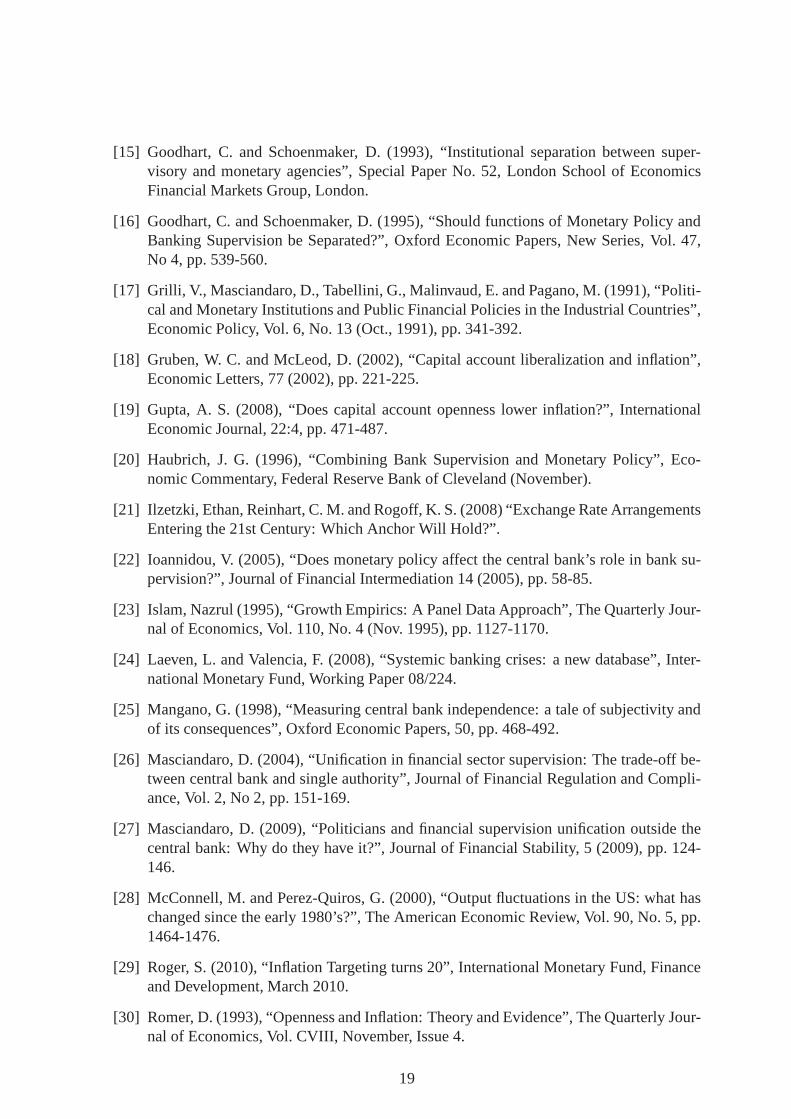

2.3.1 Annual Panel Data

Table 3 shows the regression results based on the estimationof the annual panel data speci-fication for the period 1975-2007. The econometric softwareadopted is STATA, version 12.Five model specifications are estimated: Model 1 is the full version of the model presentedin section 3.2 and, as described before, Models 2, 3, and 4 areconstrained versions of thesame model, in which external, economic and banking structure factors are excluded, respec-tively. F test statistics for the statistical significance of omiting each block of variables arealso presented. Model 5 only considers institutional factors. The F Test shows that the nullhypothesis is rejected for every group of variables, meaning that the collective inclusion ofeach group of variables is statistically relevant to explain inflation.The most striking result is that the variableseparate,in which impact we focus our analysis,is not statistically significant, in any of the models considered. In particular, even whenonly institutional variables are accounted for (Model 5),separateis still not significant andthe coefficient sign is contrary to our expectations. Therefore, our results do not provideempirical evidence for the conflict of interest argument.In what regards the inflation targeting variable, the previous empirical literature does not con-sider it as an explanatory variable. However, our findings show that this variable is relevantin determining inflation outcomes. In fact, inflation targeting is statistically significant inevery model specification and it has a negative impact on inflation rates, as predicted by theliterature. The estimated impact on inflation rates of usinginflation targeting as a monetarypolicy approach ranges from a minimum of -24% (Model 4) to a maximum of -34% (Model

14We also account for the interaction of some regressors withseparate, such as exchange rate regimes andbank concentration index. The estimation results do not change substantively and the majority of the interactionsconsidered are not statistically significant.

15In terms of estimation methods, Copelovitch and Singer (2008) adopt pooled Ordinary Least Squares withcorrected standard errors. This methodology is not the mostappropriate to estimate panel data, because it doesnot take into consideration unobserved effects.

9

5),16showing not only a large effect, but also its robustness since it does not vary considerablyacross different model specifications.Moreover, the estimation results reveal that deposit insurance, bank concentration index,trade and capital account openness are statistically significant variables. As for deposit insur-ance, its estimated impact on inflation rates is negative as expected and statistically significantacross all the regressions. The coefficients’ magnitudes ofdeposit insurance are lower thaninflation targeting, varying from a minimum of -14% to a maximum of -25%. This meansthat a country with an explicit deposit insurance scheme will have, all else equal, inflationrates that are at least 14% lower than a country without deposit protection.The variable bank concentration index enters the regressions with a negative sign, suggestingthat an increase in the degree of concentration in the banking sector has a negative impacton inflation rates. The variable is statistically significant in Model 1 and Model 3, but notin Model 2, where external factors are omitted, although thecoefficient maintains the neg-ative sign. The magnitude of the coefficient in Model 1 is identical to Model 3 and can beinterpreted as follows: a one percentage point increase in the bank concentration ratio is asso-ciated with a 30% decrease in inflation rates holding all other independent variables constant.As touched on in Section 3.1, the alternative explanation focusing on cost-efficiency offers abetter explanation to our results, since it suggests that a higher concentration in the bankingsystem does not seem to affect the transmission mechanism ofmonetary policy and, as aresult, inflation rates can be lower on average when concentration is higher.Finally, our results suggest that a more open economy in terms of trade and capital flowsseems to benefit from lower inflation rates, all else equal. These results are consistentwith previous empirical evidence (Romer, 1993; Gupta, 2008) and partly consistent withCopelovitch and Singer (2008), since their results also suggest a negative significant effect ofcapital account openness on inflation rates.

The remaining explanatory variables, such as central bank independence, exchange rateregime, domestic credit as a percentage of GDP, oil imports over GDP and the log of GDPand GDP per capita, are not significant determinants of inflation behaviour in industrialisedcountries. In particular, it is worth to discuss in more detail the results for central bank inde-pendence.There is a vast literature investigating the impact of central bank independence on inflationrates and stating that central bank independence is the maininstitutional factor affecting in-flation outcomes. In our regression models, although central bank independence enters theregression with the expected negative sign, it seems to be insignificant whenever bankingstructure variables are accounted for. Only when we are not controlling for the structure ofthe banking system, as in Model 2 and Model 5, central bank independence has a negativeand statistically significant effect on inflation rates. TheCBI variable is based on the work ofArnone et al. (2007), which update ade juremeasure of independence following Cukiermanet al. (1992), since it assesses regulations only. As suggested by Cukierman et al. (1992),de factomeasures of central bank independence are also important toassess how regula-tions work in practice. Our results seems to suggest that thedegree of legal independenceper seis not sufficient to guarantee a significant negative impact on inflation outcomes. Inaddition, it is interesting to note that its impact is statistically significant only when exter-

16Since the dependent variable in our model is the log of inflation, the interpretation of the magnitude of theseregression coefficients cannot be done directly. Thus, for dummy variables, we have to convert the estimated

values, using the formulaexp(

β̂)

−1.

10

Table 3: Estimation results for annual panel data 1975-2007.

Dependent Variable:Model 1 Model 2 Model 3 Model 4 Model 5

inflation

Constant10.371 5.923 1.400∗∗∗ 13.569∗ 1.193∗∗∗

(11.101) (14.639) (0.150) (7.135) (0.053)Separate BS -0.016 0.033 0.002 0.061 0.003

(1 = Yes) (0.099) (0.112) (0.094) (0.074) (0.069)Inflation Targeting −0.285∗∗∗ −0.327∗∗∗ −0.332∗∗∗ −0.276∗∗∗ −0.408∗∗∗

(1 = Yes) (0.077) (0.070) (0.064) (0.068) (0.055)CBI − 0.242 −0.227∗ −0.228 −0.137 −0.189∗

(index) (0.150) (0.117) (0.150) (0.140) (0.098)Deposit Insurance −0.194∗∗∗ −0.283∗∗∗ −0.200∗∗∗ −0.155∗∗∗ −0.179∗∗∗

(1 = Yes) (0.067) (0.079) (0.063) (0.046) (0.046)Exchange Rate Reg. −0.053 −0.037 −0.077 −0.071 −0.120

(1 = fixed) (0.065) (0.084) (0.062) (0.044) (0.073)Euro Area Member 0.241 0.202 0.293∗∗ 0.162 0.311∗∗∗

(1 = Yes) (0.166) (0.138) (0.132) (0.096) (0.074)

Great Moderation (omitted) (omitted) (omitted)−0.263∗∗∗ −0.364∗∗∗

(0.049) (0.049)Domestic Credit −0.000 −0.000 −0.000

- -(% of GDP) (0.001) (0.001) (0.001)

Bank Concentration −0.305∗∗ −0.180 −0.335∗∗∗- -

Index (0.120) (0.131) (0.113)GDP −0.780 −0.407

-−0.715

-(log) (0.841) (0.998) (0.532)

GDP per capita 1.151 0.572-

0.628-

(log) (1.175) (1.212) (0.716)Banking Crisis 0.056 0.069

-0.058∗

-(1 = Yes) (0.060) (0.063) (0.030)

Currency Crisis 0.094 0.098-

0.058-

(1 = Yes) (0.085) (0.080) (0.036)

Trade Openness−0.108∗∗∗

-−0.100∗∗∗ −0.100∗∗∗

-(0.023) (0.021) (0.027)

Capital Account −0.003∗-

−0.003∗ 0.003∗∗-

Openness (0.002) (0.002) (0.001)Oil imports 2.095

-2.151 2.450∗

-(% GDP) (1.600) (1.505) (1.323)

Observations 305 335 305 565 764No Countries 22 25 22 22 25

F Test 56.11∗∗∗ 55.00∗∗∗ 82.02∗∗∗ 201.96∗∗∗ 201.45∗∗∗

(global significance) (15, 21) (12, 24) (11, 21) (14, 21) (7, 24)F test

-14.16∗∗∗ 2.45∗ 3.99∗∗

-(exclusion) (3, 21) (4, 21) (2, 21)

R squared (within) 0.38 0.29 0.37 0.58 0.53* p < = .10; ** p < = .05; *** p < = .01Robust standard errors are in brackets.

nal factors are not considered in the model. In summary, the lack of significance of centralbank independence may be due to measurement issues (due to the fact that it does not assesshow regulations are implemented) or even due to theoreticalproblems with the associationbetween central bank independence and inflation. Our results also suggest that the relationbetween CBI and banking structure should be studied further.The Great Moderation variable is omitted in 3 out of 5 regressions due to collinearity prob-

11

lems. For the remaining models, the variable is statistically significant and the estimatedcoefficient enters the regression with the expected sign.In synthesis, estimation results in Table 3 suggest that inflation rates in industrialised coun-tries are mainly affected by institutional factors, such asinflation targeting and deposit insur-ance, but not by the separation of banking supervision powers from the central bank, evenwhen we are not controlling for banking structure, economicsize and wealth and externalfactors. Other factors, such as the degree of openness of theeconomy and the degree of bankconcentration are also important to assess inflation behaviour.Given the estimation results so far, in particular the insignificant effect of a separate bankingsupervisor in contrast with the significant impact of inflation targeting in every alternativespecifications of the regression models, they suggest that the interaction between thesepa-rate and inflation targeting should be studied more deeply. The decision of some countriestowards the separation banking supervision powers from thecentral bank was coincident intime with the assignment to monetary policymakers of a more transparent mandate in whichprice stability was considered a primary goal. Therefore, we assess the interactions betweenthe two variables and test the hypothesis that inflation is lower on average in developed coun-tries due to inflation targeting mandates and not because of different institutions mandates forbanking supervision.In order to test this hypothesis, we build three dummies. Thefirst dummy, Sep_Inftarg1, takesvalue of 1 whenever a particular country has inflation targeting and a combined mandate ina certain period in time. The second dummy, Sep_Inftarg2, takes value of 1 whenever acountry does not follow inflation targeting and has implemented a separate mandate. Finally,there is a third dummy, Sep_Inftarg3, that takes value 1 if a country targets inflation and hasa separate mandate.The dummies compare to a baseline case, in which a country hasa combined regime and noinflation targeting. For all dummy variables, we expect a negative impact on inflation out-comes. If this hypothesis is correct, we expect that Sep_Inftarg1 will be statistically signifi-cant, whereas Sep_Inftarg2 will not. Table 4 presents the estimation results for the interactionof separate central bank and inflation targeting.The estimation results show that the variable Sep_Inftarg1is statistically significant in everymodel specification and its impact on inflation rates is negative, as expected. This suggeststhat a country with inflation targeting and a combined regimewill have, on average, a lowerinflation outcome than a country with no inflation targeting and no separation of functions.In turn, Sep_Inftarg2 is not statistically significant in any regression, which suggests that acentral bank that an institutional mandate characterised by a central bank exclusively respon-sible for monetary policy and without an inflation target mandate has no significant impacton inflation rates. Lastly, the impact on inflation outcomes of Sep_Inftarg3 is significant andnegative.These findings provide empirical support to our argument that the main institutional driverof low inflation outcomes in industrialised countries may bethe fact that these countriesimplemented an inflation targeting approach. Therefore, there is additional evidence that theconflict of interest argument is not supported by our estimation results.The estimation results for the remaining explanatory variables are identical to the ones pre-sented in Table 4.

12

Table 4: Estimation results for annual panel data 1975-2007.

Dependent Variable:Model 1 Model 2 Model 3 Model 4 Model 5

(log) inflation

Constant10.491 5.924 1.425∗∗∗ 13.797∗ 1.198∗∗∗

(11.241) (14.672) (0.151) (7.040) (0.053)Sep_Inftarg1 −0.314∗∗∗ −0.348∗∗∗ −0.376∗∗∗ −0.230∗∗∗ −0.432∗∗∗

(1: Separate = 0, Inf. Targeting = 1) (0.077) (0.073) (0.063) (0.076) (0.087)Sep_Inftarg2 −0.036 0.020 −0.031 0.084 −0.006

(1: Separate = 1, Inf. Targeting = 0) (0.113) (0.127) (0.111) (0.078) (0.074)Sep_Inftarg3 −0.304∗∗ −0.296∗∗ −0.333∗∗∗ −0.222∗∗ −0.400∗∗∗

(1: Separate = 1, Inf. Targeting = 1) (0.143) (0.129) (0.104) (0.097) (0.060)CBI −0.248 −0.231∗∗ −0.242 −0.128 −0.193∗

(index) (0.146) (0.111) (0.143) (0.138) (0.095)Deposit Insurance −0.195∗∗∗ −0.284∗∗∗ −0.201∗∗∗ −0.147∗∗∗ −0.181∗∗∗

(1 = Yes) (0.069) (0.081) (0.063) (0.046) (0.047)Exchange Rate Reg. −0.048 −0.033 −0.068 −0.077∗ −0.118

(1 = fixed) (0.068) (0.087) (0.067) (0.044) (0.073)Euro Area Member 0.244 0.205 0.297∗∗ 0.170∗ 0.304∗∗∗

(1 = Yes) (0.165) (0.136) (0.131) (0.096) (0.071)

Great Moderation (omitted) (omitted) (omitted)−0.265∗∗∗ −0.364∗∗∗

(0.048) (0.049)Domestic Credit 0.000 0.000 0.000

- -(% of GDP) (-0.771) (0.001) (0.000)

Bank Concentration −0.315∗∗ −0.185 −0.342∗∗∗- -

Index (0.122) (0.133) (0.113)GDP −0.771 −0.396

-−0.742

-(log) (0.846) (1.001) (0.527)

GDP per capita 1.117 0.547-

0.673-

(log) (1.182) (1.218) (0.714)Banking Crisis 0.052 0.067

-0.059∗

-(1 = Yes) (0.063) (0.065) (0.030)

Currency Crisis 0.095 0.100-

0.063∗-

(1 = Yes) (0.085) (0.081) (0.036)Trade Openness −0.108∗∗∗

-−0.102∗∗∗ −0.100∗∗∗

-(0.024) (0.022) (0.028)

Capital Account −0.003∗-

−0.003∗ 0.004∗∗-

Openness (0.002) (0.002) (0.001)Oil imports 2.085

-2.112 2.463∗

-(% GDP) (1.617) (1.525) (1.311)

Observations 305 335 305 565 764No of Countries 22 25 22 22 25

F Test 72.20∗∗∗ 75.49∗∗∗ 94.15∗∗∗ 318.57∗∗∗ 287.99∗∗∗

(global significance) (16, 21) (13, 24) (12, 21) (15, 21) (8, 24)F test

-13.64∗∗∗ 2.60∗ 4.02∗∗

-(exclusion) (3, 21) (4, 21) (2, 21)

-R squared (within) 0.38 0.29 0.37 0.58 0.53

* p < = .10; ** p < = .05; *** p < = .01Robust standard errors are in brackets.

2.3.2 Five Years Panel Data

In Table 5, the estimation results for the five-year panel data specification are presented.Here we follow the data approach adopted by Copelovitch and Singer (2008). The 5 yearsaverage is calculated for the all pool of regressors considered in the model, including dummy

13

variables for which we adopt a different average criterion.The average of dummy variables isfirst computed and then it is converted into 0 whenever it is less than 0.5 and into 1 otherwise.Models 2, 3 and 4 consist of Model 1 (Full Model) excluding blocks of variables: externalvariables, economic variables and banking structure variables, respectively. A F Test wasperformed to test for the impact of the joint exclusion of each block. The F Test shows thatnull hypothesis that the coefficients for each group of variables are zero is rejected. Hence,the joint inclusion of each group of variables is statistically relevant to explain inflation.The findings using a 5 years panel do not differ substantivelyfrom the ones obtained by usingannual data. The estimation results for Model 1 show that thevariableseparatehas a negativeimpact on inflation rates but this effect is not statistically significant. Even when accountingsolely for institutional factors, the effect ofseparateon inflation is still insignificant. Thesame result applies to other model specifications. In conclusion, the separation of bankingsupervision from the central bank does not affect significantly inflation rates according toour results. This outcome differs from Copelovitch and Singer (2008) and Di Noia and DiGiorgio (1999), although they adopt the same data specification.As before, inflation targeting has a statistically significant negative impact on inflation rates.This result is consistent with the different model specifications presented in Table 5. Themagnitude of the estimated coefficient ranges from -35% (Model 4) to -52% (Model 2),meaning that an inflation targeter country will have, on average, 35% to 52% lower inflationoutcomes each five years than a country that does not target inflation. Furthermore, theseresults show once again that a country that provides explicit deposit insurance schemes willhave on average lower inflation outcomes.The institutional variables of central bank independence and exchange rate regime remainstatistically insignificant. The variable that controls for the period of the Great Moderation isnot omitted in this data specification and enters the regressions with the expected sign, thoughit is only statistically significant in Models 3, 4 and 5.In what concerns economic factors, currency crisis has a statistically significant impact oninflation behaviour in Models 1 and 2, whereas banking crisisis statistically significant inModels 2 and 4. Both regressors have a positive impact on inflation rates, although currencycrisis effect is stronger than banking crisis. The variables log of GDP and GDP per capita arenot relevant predictors of inflation.Moreover, external factors are important in the sense that trade openness has a statisticallysignificant negative effect on inflation. The remaining external factors, such as oil importsas percentage of GDP and capital account openness, are not relevant in explaining inflationbehaviour.Finally, bank concentration is an important determinant ofinflation outcomes. The degreeof concentration in the banking system has a negative and statistically impact on inflation.Conversely, the size of the banking system does not seem to berelevant to explain inflationand its impact is close to zero.As before, the interaction between a separate central bank and a inflation targeting centralbank is assessed using a 5 years average panel data. Table 6 shows the estimation results.The estimation results suggest the variable Sep_Inftarg1 is statistically significant in everymodel specification, except when there is no control for banking structure variables (Model4). The impact is negative, as predicted. On the contrary, Sep_Inftarg2, the variable thatassesses the impact on inflation rates of having a separate regime and no inflation targeting,is insignificant in every model specification, except Model 1, in which we control for external,economic and banking structure factors. Sep_Inftarg3 has astatistically significant negative

14

Table 5: Estimation results for five-year average panel data1975-2007.

Dependent Variable:Model 1 Model 2 Model 3 Model 4 Model 5

(log) inflation

Constant15.644 12.456 4.235∗∗∗ 16.165∗ 2.922∗∗∗

(10.277) (13.300) (0.526) (8.095) (0.157)Separate CB −0.351 −0.072 −0.297 0.301 −0.011

(1 = Yes) (0.227) (0.271) (0.258) (0.213) (0.123)Inflation Targeting −0.572∗∗∗ −0.733∗∗∗ −0.603∗∗∗ −0.429∗∗ −0.711∗∗∗

(1 = Yes) (0.161) (0.115) (0.168) (0.187) (0.125)CBI −0.245 −0.324 −0.480 −0.028 −0.886∗∗∗

(index) (0.522) (0.362) (0.576) (0.531) (0.276)Deposit Insurance −0.664∗∗∗ −0.701∗∗ −0.642∗∗∗ −0.371∗ −0.287∗∗

(1 = Yes) (0.223) (0.294) (0.205) (0.189) (0.112)Exchange Rate Reg. 0.215 0.173 0.074 −0.031 −0.222

(1 = fixed) (0.145) (0.194) (0.229) (0.144) (0.203)Euro Area Member 0.680∗∗∗ 0.443 0.723∗∗∗ 0.372∗∗ 0.563∗∗∗

(1 = Yes) (0.202) (0.270) (0.190) (0.173) (0.136)

Great Moderation−0.167 −0.468 −0.780∗ −0.638∗∗∗ −0.830∗∗∗

(0.477) (0.665) (0.379) (0.161) (0.109)Domestic Credit 0.002 0.001 0.000

- -(% of GDP) (0.001) (0.001) (0.001)

Bank Concentration −1.377∗∗∗ −1.173∗ −1.015- -

Index (0.454) (0.603) (0.634)GDP −0.395 0.254

-−0.433

-(log) (0.420) (0.497) (0.363)

GDP per capita −0.175 −0.246-

−0.206-

(log) (0.349) (0.182) (0.406)Banking Crisis 0.100 0.242∗∗

-0.200∗∗

-(1 = Yes) (0.091) (0.112) (0.094)

Currency Crisis 0.959∗∗∗ 0.714∗∗∗-

0.264-

(1 = Yes) (0.158) (0.146) (0.271)

Trade Openness−0.204∗

-−0.230∗∗ −0.186

-(0.113) (0.108) (0.114)

Capital Account 0.001-

−0.004 0.004-

Openness (0.004) (0.005) (0.005)Oil imports 0.107

-0.101 −0.488

-(% GDP) (1.590) (1.657) (1.797)

No of Observations 98 107 98 122 163No of Countries 22 25 22 22 25

F Test 585.08∗∗∗ 66,943∗∗∗ 109.15∗∗∗ 312.30∗∗∗ 142.07***(global significance) (16, 21) (13, 24) (12, 21) (14, 21) (7, 24)

F test-

2.76∗ 16.10∗∗∗ 5.21∗∗-

(exclusion) (3.21) (4,21) (2,21)R squared (within) 0.67 0.57 0.59 0.76 0.71

* p < = .10; ** p < = .05; *** p < = .01Robust standard errors are in brackets.

impact on inflation outcomes that is robust in different model specifications.Results are not as clear as in an annual panel data approach, but they still suggest that beingan inflation targeter is more important to assure lower levels of inflation in industrialisedcountries than having an independent banking supervision mandate.

15

Table 6: Estimation results for five-year average panel data1975-2007.

Dependent Variable:Model 1 Model 2 Model 3 Model 4 Model 5

(log) inflation

Constant17.575∗ 19.808 3.654∗∗∗ 13.911∗ 2.901∗∗∗

(9.850) (12.109) (0.500) (7.482) (0.122)Sep_Inftarg1 −0.609∗∗ −0.583∗ −0.847∗∗ −0.327 −0.752∗∗∗

(1: Separate = 0, Inf. Targeting = 1) (0.277) (0.305) (0.351) (0.200) (0.239)Sep_Inftarg2 −0.468∗ 0.037 −0.324 −0.024 0.001

(1: Separate = 1, Inf. Targeting = 0) (0.250) (0.294) (0.235) (0.253) (0.145)Sep_Inftarg3 −0.832∗∗∗ −0.537∗∗ −0.904∗∗∗ −0.472∗∗ −0.784∗∗∗

(1: Separate = 1, Inf. Targeting = 1) (0.277) (0.241) (0.229) (0.211) (0.164)CBI −0.022 −0.134 −0.135 0.173 −0.730∗∗∗

(index) (0.493) (0.331) (0.516) (0.482) (0.237)Deposit Insurance −0.471∗∗ −0.677∗∗ −0.442∗ −0.211 −0.355∗∗∗

(1 = Yes) (0.192) (0.310) (0.214) (0.167) (0.104)Exchange Rate Reg. −0.005 −0.117 −0.141 −0.153 −0.311

(1 = fixed) (0.174) (0.260) (0.145) (0.154) (0.182)Euro Area Member 0.963∗∗∗ 0.556∗∗ 0.976∗∗∗ 0.635∗∗∗ 0.776∗∗∗

(1 = Yes) (0.261) (0.267) (0.227) (0.208) (0.185)

Great Moderation0.065 −0.022 −0.288 −0.687∗∗∗ −0.887∗∗∗

(0.278) (0.490) (0.339) (0.163) (0.107)Domestic Credit 0.000 0.000 −0.001

- -(% of GDP) (0.001) (0.002) (0.001)

Bank Concentration −1.163∗∗∗ −0.896 −1.025∗∗- -

Index (0.363) (0.541) (0.436)GDP −0.751∗ −0.543

-−0.458

-(log) (0.391) (0.494) (0.300)

GDP per capita 0.576∗ −0.264-

0.100-

(log) (0.310) (0.195) (0.234)Banking Crisis −0.015 0.145

-0.120

-(1 = Yes) (0.116) (0.174) (0.118)

Currency Crisis 0.678∗∗ 0.359-

0.158-

(1 = Yes) (0.287) (0.412) (0.346)

Trade Openness−0.368∗∗∗

-−0.350∗∗∗ −0.292∗∗∗

-(0.088) (0.063) (0.075)

Capital Account −0.005-

−0.003 −0.001-

Openness (0.004) (0.004) (0.003)Oil imports −0.767

-−0.363 −1.165

-(% GDP) (1.630) (1.421) (1.890)

No of Observations 98 107 98 122 163No of Countries 22 25 22 22 25

F Test 313,801∗∗∗ 299.05∗∗∗ 132.60∗∗∗ 464∗∗∗ 160.92∗∗∗

(global significance) (17, 21) (14, 24) (13, 21) (15, 21) (8, 24)F test

-9.73∗∗∗ 3.00∗∗ 5.13∗∗

-(exclusion) (3, 21) (4, 21) (2, 21)

R squared (within) 0.63 0.45 0.59 0.75 0.69* p < = .10; ** p < = .05; *** p < = .01Robust standard errors are in brackets.

3 Conclusions

The estimation results show that the separation of banking supervision from the central bankdoes not have a significant impact on inflation. In this sense,the conflict of interest argumentagainst combination of monetary policy and banking supervision is not supported by our em-

16

pirical findings. These results are contrary to the empirical evidence of previous literature,due to two main reasons. First, we adopt a different methodology that assesses the countryspecific effects and their correlation with the explanatoryvariables. Second, we include ad-ditional explanatory variables to control for the effect oninflation rates of inflation targetingpractices, banking concentration and oil imports over GDP,among others.Monetary policymakers have a primary goal that is price stability. However, it is argued thatcentral banks are also concerned with financial stability, even when they are not responsiblefor banking supervision, since financial distress may affect the bank transmission channel ofmonetary policy. Being this the case, the institutional arrangements of banking supervisionwould not be considered a significant determinant of inflation rates behaviour. In fact, ourresults indicate that the most important institutional determinants of low inflation rates areinflation targeting and deposit insurance schemes. Moreover, external factors, such as tradeopenness, capital account openness and currency crisis have also strong effects on inflationbehaviour. Finally, our results show that higher levels of concentration in the banking struc-ture will have a negative impact on inflation, suggesting that the structure of the bankingsystem in important to assess how monetary policy impacts onthe level of prices.In the literature, some authors prefer to internalise the conflict of interest effect in the centralbank, instead of suggesting the separation of policies. Forexample, Goodhart and Schoen-maker (1993) and (1995), argue that, in an environment characterized by open, competitive,and market-driven banking system, the conflict of interest should be incorporated into thecentral bank in order to achieve a more efficient resolution of bank distress. In addition, Blin-der (2010) considers that the separation of policies may notmaximise the society outcome,because an independent banking supervisor would not be concerned about macroeconomicimpacts when disciplining the banks.Given our empirical evidence about this argument, the conflict of interest between monetarypolicy and banking supervision should not be a concern for central banks. Other arguments,such as reputation risks and organisational costs may pose higher concerns than the conflictof interest effect.We will expand this research in other directions. First, we will assess the impact of pastinflation on current inflation. The inclusion of lagged explanatory variables will require theuse of adequate estimation techniques to deal with dynamic panels. Second, we will test foran alternative perspective of the conflict of interest effect. The argument is the following: acentral bank with supervisory powers that is concerned withthe impact of monetary policy onbanking stability will increase interest rates by less thanit would if it was not responsible forbanking supervision. Thus, inflation volatility will also be lower in countries where bankingsupervision is located in the central bank. With this purpose, a model will be built in whichthe dependent variable will be given by measures of inflationand interest rate volatility.

17

References

[1] Armingeon, K., Weisstanner, D., Engler, S., Potolidis,P., Gerber, M. and Leimgru-ber, P. (2011), Comparative Political Data Set 1960-2009, Institute of Political Science,University of Berne

[2] Arnone, M., Laurens, B. J., Segalotto, J., and Sommer, M.(2007), “Central Bank Au-tonomy: Lessons from Global Trends”, International Monetary Fund, Working Paper07/88.

[3] Beck, T., Demirguc-Kunt, A. and Levine, R. (2006), “Bankconcentration, competition,and crises: first results”, Journal of Banking and Finance, Vol. 30, Issue 5, pp. 1581-1603.

[4] Blinder, A. S. (2010), “How Central Should the Central Bank Be?”, Journal of Eco-nomic Literature, 48:1, pp. 123-133.

[5] Caprio, G. Jr and Klingebiel, D., (2003), “Bank insolvency: bad luck, bad policy or badbanking?”, World Bank Policy Research Working Paper no. 1620.

[6] Chinn, M. D. and Ito, H. (2008), “A new measure of financialopenness”, Journal ofComparative Policy Analysis, Volume 10, Issue 3 September 2008 , p. 309 - 322.

[7] Copelovitch, Mark S. and Singer, David Andrew (2008), “Financial Regulation, Mone-tary Policy, and Inflation in the Industrialized World”, TheJournal of Politics, Vol. 70,no. 3, pp. 663-680.

[8] Courtis, Neil (2011), “How Countries Supervise their Banks, Insurers and Security Mar-kets 2011”, Central Bank Publications.

[9] Crowe, C. and Meade, E. E. (2007), “The evolution of central bank governance aroundthe world”, The Journal of Economic Perspectives, Vol. 21, No. 4, pp. 69-90.

[10] Cukierman, A., Webb, S. B., Neyapti, B. (1992), “Measuring the independence of Cen-tral Banks and its effect on policy outcomes”, The World BankEconomic Review, Vol.6, No. 3, pp. 353-398.

[11] Dalla Pellegrina, L., Masciandaro, D., Vega, R. (2010), “Governments, central bankers,and banking supervision reforms: Does independence matter?, Vox.

[12] Demsetz, H. (1973), “Industry Structure, Market Rivalry, and Public Policy”, Journalof Law and Economics, Vol. 16, No. 1, pp. 1-9.

[13] Di Noia, Carmine and Di Giorgio, Giorgio (1999), “Should Banking Supervision andMonetary Policy Tasks be Given to different Agencies?”, International Finance 2:3, pp.361-378.

[14] Docherty, Peter (2008), “Basel II and the Political Economy of Banking Regulation –Monetary Policy Interaction”, International Journal of Political Economy, Vol. 37, no.2, Summer 2008, pp. 82-106.

18

[15] Goodhart, C. and Schoenmaker, D. (1993), “Institutional separation between super-visory and monetary agencies”, Special Paper No. 52, LondonSchool of EconomicsFinancial Markets Group, London.

[16] Goodhart, C. and Schoenmaker, D. (1995), “Should functions of Monetary Policy andBanking Supervision be Separated?”, Oxford Economic Papers, New Series, Vol. 47,No 4, pp. 539-560.

[17] Grilli, V., Masciandaro, D., Tabellini, G., Malinvaud, E. and Pagano, M. (1991), “Politi-cal and Monetary Institutions and Public Financial Policies in the Industrial Countries”,Economic Policy, Vol. 6, No. 13 (Oct., 1991), pp. 341-392.

[18] Gruben, W. C. and McLeod, D. (2002), “Capital account liberalization and inflation”,Economic Letters, 77 (2002), pp. 221-225.

[19] Gupta, A. S. (2008), “Does capital account openness lower inflation?”, InternationalEconomic Journal, 22:4, pp. 471-487.

[20] Haubrich, J. G. (1996), “Combining Bank Supervision and Monetary Policy”, Eco-nomic Commentary, Federal Reserve Bank of Cleveland (November).

[21] Ilzetzki, Ethan, Reinhart, C. M. and Rogoff, K. S. (2008) “Exchange Rate ArrangementsEntering the 21st Century: Which Anchor Will Hold?”.

[22] Ioannidou, V. (2005), “Does monetary policy affect thecentral bank’s role in bank su-pervision?”, Journal of Financial Intermediation 14 (2005), pp. 58-85.

[23] Islam, Nazrul (1995), “Growth Empirics: A Panel Data Approach”, The Quarterly Jour-nal of Economics, Vol. 110, No. 4 (Nov. 1995), pp. 1127-1170.

[24] Laeven, L. and Valencia, F. (2008), “Systemic banking crises: a new database”, Inter-national Monetary Fund, Working Paper 08/224.

[25] Mangano, G. (1998), “Measuring central bank independence: a tale of subjectivity andof its consequences”, Oxford Economic Papers, 50, pp. 468-492.

[26] Masciandaro, D. (2004), “Unification in financial sector supervision: The trade-off be-tween central bank and single authority”, Journal of Financial Regulation and Compli-ance, Vol. 2, No 2, pp. 151-169.

[27] Masciandaro, D. (2009), “Politicians and financial supervision unification outside thecentral bank: Why do they have it?”, Journal of Financial Stability, 5 (2009), pp. 124-146.

[28] McConnell, M. and Perez-Quiros, G. (2000), “Output fluctuations in the US: what haschanged since the early 1980’s?”, The American Economic Review, Vol. 90, No. 5, pp.1464-1476.

[29] Roger, S. (2010), “Inflation Targeting turns 20”, International Monetary Fund, Financeand Development, March 2010.

[30] Romer, D. (1993), “Openness and Inflation: Theory and Evidence”, The Quarterly Jour-nal of Economics, Vol. CVIII, November, Issue 4.

19

A Appendix

Table A.1: Variables and respective definitions and sources.

Variables Sources and Definitions

Inflation Rate

(log)

"WORLD ECONOMIC AND FINANCIAL SURVEYS, World Economic Outlook database April 2003

(site IMF). Inflation (consumer prices; index and annual percent change). Data for inflation are averages for

the year, not end-of-period data. The index is based on 1995=100."

Separate and

Combined

Regimes

Copelovitch and Singer (2008); Di Noia and Di Giorgio (1999); World Bank - Banking Regulation Survey

2000 and 2008; Central Banks and Banking Supervisors webpages for the years missing. Dummy = 1 if a

country has separated mandates for monetary policy and banking regulation / supervision.

GDP per capita

(log)

World Bank (2011): World Development Indicators (Edition:September 2011). ESDS International,

University of Manchester. DOI: http://dx.doi.org/10.5257/wb/wdi/2011-09. GDP per capita is gross

domestic product divided by midyear population. GDP at purchaser’s prices is the sum of gross value added

by all resident producers in the economy plus any product taxes and minus any subsidies not included in the

value of the products. It is calculated without making deductions for depreciation of fabricated assets or for

depletion and degradation of natural resources. Data are inconstant local currency.

GDP Constant

Prices (log)

World Bank (2011): World Development Indicators (Edition:September 2011). ESDS International,

University of Manchester. DOI: http://dx.doi.org/10.5257/wb/wdi/2011-09. GDP (constant LCU): GDP at

purchaser’s prices is the sum of gross value added by all resident producers in the economy plus any product

taxes and minus any subsidies not included in the value of theproducts. It is calculated without making

deductions for depreciation of fabricated assets or for depletion and degradation of natural resources. Data

are in constant local currency.

Central Bank

Independence

Index

Follows Copelovitch and Singer: "Data on CBI are based on Cukierman’s (1992) methodology for

calculating legal independence” and are compiled from the Comparative Political Dataset for the period

1975–96 (Armingeon et al. 2005) and Polillo and Guillen (2003) for the remaining years (cbicwn and cbipd,

respectively). China and Singapore are missing. Central Bank Index 1971-1996 from Lijphart (1999).

Banking Crisis Glick and Hutchison (1999), "Banking and Currency Crises: How Common are Twins?" For Australia and

USA the data comes from Caprio and Klingebiel (2003), "Episodes of Systemic and Borderline Financial

Crises", World Bank. For the years 2000-2007, data comes from Laeven and Valencia (2010). Dummy = 1

when the country has a banking crisis.

Currency Crisis Glick and Hutchison (1999), "Banking and Currency Crises: How Common are Twins?"; For Australia and

USA the data comes from Laeven & Valencia (2008) "Systemic Banking Crises: A New Database", IMF

WP. For the years 2000-2008, data comes from Laeven and Valencia (2008). Dummy = 1 when the country

has a currency crisis, 0 otherwise.

Openness of the

economy

Comparative Political Dataset 23 OECD countries (1960-2008). Openness of the economy in current prices,

measured as total trade (sum of import and export) as a percentage of GDP. 1960-2007. Source: Penn World

Table 6.3, http://pwt.econ.upenn.edu/php_site/pwt_index.php (Download: 2010-02-01)

Capital Account

Openness Index

Comparative Political Dataset 23 OECD countries (1960-2008). Index for the extent of openness in capital

account transactions. Source: Chinn and Ito (2008); www.ssc.wisc.edu/~mchinn/research.html. Source:

OECD Economic Outlook Database, Economic Outlook: Annual and quarterly data, Vol. 2009, release 03

Deposit Insurance World Bank Deposit Insurance around the world dataset. Deposit Insurance Fund Dummy = 1 if a country

has deposit insurance, 0 if not

Exchange Rate

Regime

Dataset for Ilzetzki, Reinhart and Rogoff (2008). IMF Classification (Coarse). It takes the value o 0 for

floating or managed floating regime and 1 for all varieties of “hard” fixed exchange rates.

20

Table A.1: Variables and respective definitions and sources.

Inflation targeting Scott, R. (2010), "Inflation Targeting Turns 20", Finance & Development, March 2010, Vol. 47 No 1. For

Finland and Spain: Little, J. S. and Romano, T. F. (2009), "Inflation Targeting - Central Bank Practice

Overseas", Public Policy Briefs, No 08-1. Dummy = 1 if the country has Inflation Targeting, 0 otherwise.

We assume that the Member States of Euro zone have inflation targeting.

Table A.2: Separate variable classification by country.

Countries Time Period Dummy Values

Australia 1975-1997 01998-2007 1

Austria 1975-1998 01999-2007 1

Belgium - 01975-2007 1

Canada - 01975-2007 1

China 1975-2002 02003-2007 1

Denmark - 01975-2007 1

Finland 1975-1998 01999-2007 1

France 1975-1998 01999-2007 1

Germany 1975-1998 01999-2007 1

Greece 1975-2000 02001-2007 1

Iceland 1975-1998 01999-2007 1

Ireland 1975-1998 01999-2007 1

Italy 1975-1998 01999-2007 1

Japan 1975-1997 01998-2007 1

Luxembourg 1983-1998 01975-1982 / 1998-2007 1

Netherlands 1975-1998 01999-2007 1

New Zealand 1975-2007 0- 1

Norway - 01975-2007 1

Portugal 1975-1998 0

21

Table A.2: Separate variable classification by country.

1999-2007 1Singapore 1975-2007 0

- 1Spain 1975-1998 0

1999-2007 1Sweden - 0

1975-2007 1Switzerland - 0

1975-2007 1United Kingdom 1975-1997 0

1998-2007 1United States 1975-2007 0

- 1

22