MOMENTUM - bbnc.net · 2 bbnc fy2018 annual report message to our shareholders 3 message to our...

34

BBNC FY2018 ANNUAL REPORT MOMENTUM

Transcript of MOMENTUM - bbnc.net · 2 bbnc fy2018 annual report message to our shareholders 3 message to our...

B B N C F Y 2 0 1 8 A N N U A L R E P O R T

MOMENTUM

15BOARD AND MANAGEMENT

17FINANCIALS & MANAGEMENT DISCUSSION AND ANALYSIS

31INDEPENDENT

AUDITORS' REPORT

32CONSOLIDATED

FINANCIAL STATEMENTS

61AUDIT COMMITTEE REPORT

62STATEMENT OF

MANAGEMENT RESPONSIBILITY

MOMENTUMTABLE OF CONTENTS

02MESSAGE TO OUR

SHAREHOLDERS

04FY2018 HIGHLIGHTS

06OUR CULTURE

10OUR PEOPLE

12OUR LANDS

14ABOUT BBNC

2 3BBNC FY2018 ANNUAL REPORT MESSAGE TO OUR SHAREHOLDERS

MESSAGE TO OUR SHAREHOLDERS

FY2018 WAS A YEAR OF BOTH GAINING TRACTION AND STAYING THE COURSE.

“

here is a saying that those in Bristol

Bay’s communities know well: being

up on step. It’s when your boat

reaches a certain speed and levels out on the

water. It’s steadied, hitting its stride, on its way.

In FY2018, BBNC got up on step. One could

argue that we’ve been there—or close to it—for a

while now, but this year there was no question.

We delivered our best net income performance

in company history, introduced new initiatives

and enhanced existing ones, and marked our

20th consecutive year of sustaining a predictable

and increasing dividend. It was a year of both

gaining traction and staying the course. As a

result, our financial health is solid and our

momentum is strong.

We continued to push the envelope in FY2018 as

we have always done, approaching our work with

the innovative and bold spirit that has defined our

culture for generations. We have never been afraid

to do things differently, to be curious and creative

A YEAR OFMOMENTUM

in starting new programs or in exploring new ways

of doing business. This thinking has shaped our

purpose as an Alaska Native Corporation from

the beginning, and will continue to do so for

years to come.

BBNC’s history has been building to this time.

We got our start. Worked hard, took risks.

Learned from our successes and misses. Tried

and tried again. Expanded, diversified, scaled

back when it was the right thing to do. Built

experience and expertise, achieved financial

stability and growth, responded to the needs

of our shareholders and subsidiaries. Stood up

for what’s right as stewards of our lands, people,

and Native way of life. Through it all, gaining and

maintaining. Now we’re moving into the next

phase of BBNC’s journey, with clear-eyed

optimism and excitement for what comes next.

We won’t stop doing what got us here. There is

still much work to be done.

Joseph L. ChythlookCHAIRMAN OF THE BOARD

Jason MetrokinPRESIDENT & CHIEF EXECUTIVE OFFICER

As we close the book on FY2018 and move

headlong into the current fiscal year, we invite

you to keep your own momentum going. Keep

doing what makes our shareholder community

such a great and vibrant one. Keep celebrating

our shared traditions, history, and values. And as

always, keep making your voices heard, clear and

strong; Bristol Bay is counting on it and we are

listening, up on step together.

With appreciation,

T

OUR ANC

$103,063,000NET INCOME

Total FY2018 net income—a 151% increase over last year and the

strongest result in BBNC’s history

5OUR ANC4 BBNC FY2018 ANNUAL REPORT

10,376

20 YEARS

500+ TRAINING PROGRAMS

DIVIDENDS

SHAREHOLDERS

EDUCATION

WAGES

Of predictable and increasing dividends paid

Paid in shareholder wages by BBNC and its

subsidiaries in FY2018Shareholders took part in

employment and training

support services offered by

BBNC in FY2018

Total number of BBNC shareholders

FY2018 HIGHLIGHTS

$14.1 MILLION

Awarded to students through the BBNCEF

Higher Education/Vocational Education Scholarship

program and the Short-Term Vocational Education

program in FY2018.

$823,000

7OUR CULTURE

WE WANT TO HELP OUR COMMUNITIES OFFER ACTIVITIES THAT ARE MEANINGFUL AND RELEVANT TO OUR PEOPLE AND CULTURE.

SHARING OUR NATIVE WAY OF LIFE

“

Ricardo LopezBBNCEF Program Officer, Cultural Heritage Program

ake salt fish. Sew a kuspuk or dance

fan. Sing centuries-old songs and

learn the traditional names and

honored histories of places. Discover medicinal

plants, carve soapstone, build a sled or salmon net

from scratch. Gather with village Elders to share

old stories and hone new skills.

These are some of the many ways that our Alaska

Native culture has, and continues to, come to life

across the Bristol Bay region. It’s a culture that

has shaped our people for generations and is

at the heart of BBNC’s work; one that embodies

momentum in its forward-facing spirit and lasting

imprint on this place we call home.

The BBNC Education Foundation’s Cultural

Heritage and Native Place Names programs

work to strengthen this imprint by preserving,

celebrating, and promoting our cultural traditions

and Native way of life. The programs support

organizations in the Bristol Bay region that engage

BBNC shareholders, descendants, and community

members in a range of educational and cultural

activities. Grant awards through the programs

range from $1,000 to $5,000.

OUR CULTURE

M

6 BBNC FY2018 ANNUAL REPORT

8 BBNC FY2018 ANNUAL REPORT

“The grants we get to award are for very affirming,

positive, and joyful activities,” says Ricardo Lopez,

Cultural Heritage Program Officer, who joined the

BBNCEF staff in December 2017. “Whether it’s a

school project or a summer youth camp, it will help

strengthen our cultural identity. And we know that

even a modest grant can make a big impact.”

FY2018 saw both programs sustain and build that

impact throughout the region:

• A special grant cycle specifically for summer

youth culture camp activities throughout the

region was introduced, with nine camps taking

place as a result. Nine more culture camps

will take place in villages from Clark's Point to

Nondalton this summer.

• The programs now accept grant applications

on a rolling basis to be more responsive to

community needs and activities throughout

the calendar year.

• The Cultural Heritage Program began to

explore the concept of a regional culture camp,

working with BBNC, its land, shareholder

and corporate relations, and shareholder

development departments to explore

concepts and opportunities through culture

camps to sustain Alaska Native cultural identity

for shareholders and descendants.

• The Native Place Names program awarded

additional grants for activities dedicated to

Native language preservation, including a

series of hikes and discussions for youth and

Elders in Togiak.

• BBNCEF streamlined elements of program

guidelines to improve the accessibility and

ease of grant applications.

“As much as culture changes and evolves with

time, you’ve got to have good roots and continue

to grow,” says Lopez. “Our roots in Bristol Bay go

deep. The cultural activities supported by the

Foundation are a reminder of that. They say, ‘you’re

a strong person, we are resilient people, and you

come from a proud and vibrant culture that you

should know about.’ Even if you don’t practice

subsistence activities on a regular basis, even if

it’s just one week a summer, connecting with our

culture and sharing these experiences will build a

stronger community and future.”

$78,000 Total awarded in the Native Place Names and

Cultural Heritage grant in FY2018

28

9OUR CULTURE

Yup'ik place name signs in

Igiugig, funded by a BBNCEF

Place Names grant

10 BBNC FY2018 ANNUAL REPORT

iiculuten,” Francisca Demoski’s mom and grandparents

would tell her growing up in Togiak. In Yup’ik, it means

“be a good listener,” and this lesson has stuck with her

throughout her life. As BBNC’s Land Manager, Demoski has played

an essential role in the Place Names project, formed by the late Bristol

Bay leader, and former BBNC board member, Harvey Samuelsen in

an effort to preserve place names in the region that were only being

passed down orally. Today, over 950 names are in the Bristol Bay

Online database.

“This ongoing project tells a neat story and provides a history that

will be preserved and shared with the people from Bristol Bay for

generations to come,” said Demoski. “I hope schools, tribes and

other groups in the region use the resource to teach youth and locals.

There are a lot of great features on the website, and folks can even

learn the pronunciation of the names in all three languages spoken in

Bristol Bay: Yup’ik, Alutiiq, and Dena’ina.”

Demoski understands the importance of passing on traditional

knowledge to future generations. Through her work on the project,

she has learned how people have interacted with the land and how

the names were traditionally used, and has a deeper understanding

of her heritage. “This project reminds me why our land and resources

are so important to our people,” Demoski said.

STEWARDS OF OUR LAND AND OUR FUTURE

About 150 miles east of Togiak,

BBNC shareholder AlexAnna

Salmon has worked tirelessly

to advocate for Alaska Native

culture. She has worked through

multiple grants (from BBNC and

other entities) to revitalize her

local Yup’ik dialect, incorporate

Native place names throughout

her village of Igiugig, and revise

the cultural awareness standards

in 13 district schools. She

sees these initiatives as key to

building cultural momentum for

the next generation.

“I think it motivates students to

have the awareness that they

are part of a greater whole, and

know that we are looking to

them to carry on for our people,”

Salmon says. “If you grow up

knowing who you are, where

you’re from, if you know how

to speak some of your Native

language or how to harvest food

OUR PEOPLE

“N

11OUR PEOPLE

from the land, that all feeds into positive resilience

and confidence. Knowing our history, what we’ve

been through, and that we’re still here today is a

testament to our people and our potential.”

In FY2018, both Demoski and Salmon were accepted

to BBNC’s Training Without Walls (TWOW) program,

a three-year leadership development program for

shareholders and descendants with a commitment

to the advancement of the Native community. Since

1994, TWOW has provided BBNC shareholders with

opportunities to advance their skills and careers, and

assists them in pursuing board and council leadership

positions. They can earn college credits for their work

and receive mentoring from experienced leaders in

Bristol Bay and the Native community.

“TWOW has been such a wonderful opportunity

to network with others throughout the region and

beyond, while learning and building our leadership

skills together,” says Demoski. “We all learn from

each other’s experiences and bring the lessons to life

during our training sessions.”

Salmon also understands the value that programs like

TWOW provide to Bristol Bay. “Training and resources

help us hire from within our own communities, and

empower us to become stronger organizations and

develop better governance for our own people.

BBNC is investing in us so we can turn around and

make a living and a lasting difference here at home. It

just has an amazing ripple effect.”

By dedicating their energies towards Native language

and place names preservation, and participating in

TWOW, both Demoski and Salmon are honoring their

respective pieces of the earth, mirroring a reverence

for our land and hope for the future that has shaped

BBNC from the start.

13OUR LANDS

THE MORE LOCALLY-ACCESSIBLE MATERIAL SITES WE CAN HAVE, THE BETTER ABLE WE’RE GOING TO BE TO EFFECTIVELY AND COST-EFFICIENTLY SUPPLY THE MATERIAL NEEDS FOR INFRASTRUCTURE PROJECTS AROUND OUR REGION. BRISTOL BAY WILL BE BETTER OFF AS A RESULT.

40

The size of the Bristol Bay region. BBNC

is responsible for roughly 12 percent of

that expanse—3 million acres of subsurface

lands and 116,000 acres of surface lands.

$5.0 BBNC Land Department’s 5-year goal

for investing in land and infrastructure

projects throughout Bristol Bay.

50%BBNC reduced the Snake Lake Quarry

entry road’s incline from 16% to 8%, making

it much safer and easier for trucks to access

and transport rock.

MILLION

MILLIONACRES

LESS STEEP

PROTECTIONAND PROGRESS

bundant, sustaining, and pristine. Vast and breathtaking. Steeped in

heritage, history, and culture. Ours to celebrate and preserve.

A deep reverence for Bristol Bay’s lands and waters is shared by those who call this

place home, and has long guided BBNC’s values, policies, and operations. Our

Land Department continued to play a critical role in the protection and responsible

development of our region’s land in FY2018, balancing financial growth with the

respect that Bristol Bay deserves.

7,500 Total weight of a recent Snake Lake Quarry

sale of armor rock for an erosion project

in Mekoryuk, AK.

2.0The amount of rock that BBNC is currently

permitted for as part of its FY2018 re-opening

of the Snake Lake Quarry north of Dillingham.

The rock will be used for infrastructure and

construction projects across Bristol Bay and

beyond for years to come, including fortifying

creek and river banks to reduce erosion.

MILLION CUBIC YARDS

TONS

“

Daniel CheyetteBBNC Vice President, Land & Natural Resourceson the re-opening of the Snake Lake Quarry, BBNC’s largest Lands initiative of FY2018

OUR LANDS

A

12 BBNC FY2018 ANNUAL REPORT

15ABOUT BBNC

EXECUTIVE MANAGEMENT TEAM

BOARD OF DIRECTORS

Back row: Diedre Hill, Everette Anderson, Peter Andrew Jr., H. Robin Samuelsen Jr., Kimberly Williams,

and Karl Hill. Front row: Shawn Aspelund, Marie Paul, Russell S. Nelson, Joseph L. Chythlook,

Dorothy M. Larson, and Melvin C. Brown.

Left to right: Nancy Schierhorn,

Executive Vice President,

Chief Development Officer;

April Ferguson, Executive Vice

President & General Counsel;

Jason Metrokin, President &

Chief Executive Officer;

Scott Torrison, Executive

Vice President & Chief

Operating Officer; Ryan York,

Executive Vice President &

Chief Financial Officer.

MOMENTUMABOUT BBNC

14 BBNC FY2018 ANNUAL REPORT

CORPORATE PROFILEBristol Bay Native Corporation (BBNC) is

a responsible Alaska Native investment

corporation dedicated to the mission of

“Enriching Our Native Way of Life.” Established

through the Alaska Native Claims Settlement Act

of 1971 (ANCSA), BBNC works to protect the land

in Bristol Bay, celebrate the legacy of its people,

and enhance the lives of its shareholders.

VALUES• Respect the people, land and natural

resources that are the basis for our culture

and the Native way of life.

• Responsibly manage natural resources,

prioritizing the cultural and economic value

of the Bristol Bay fishery.

• Responsibly manage financial resources,

leading to a continuous source of dividends

and benefits for our shareholders.

• Maintain integrity and fairness in our

dealings with all stakeholders.

MISSIONEnriching Our Native Way of Life.

VISIONTo protect the land in the Bristol Bay region,

celebrate the legacy of its people, and

enhance the lives of BBNC shareholders.

GOALS• Build the financial strength of BBNC.

• Pay predictable and increasing

shareholder dividends.

• Balance responsible development

and protection of our lands, fisheries

and resources.

• Increase shareholder employment and

development opportunities.

• Support educational, cultural and

social initiatives that positively affect

shareholders and descendants.

• Help to develop economic opportunities

in the Bristol Bay region.

17ABOUT BBNC

MOMENTUMFINANCIALS FY2018

16 BBNC FY2018 ANNUAL REPORT 17FINANCIALS

MANAGEMENT’S DISCUSSION AND ANALYSISManagement’s Discussion and Analysis (MD&A) is intended to provide readers of the financial statements with a narrative of the company’s financial condition as seen through the eyes of management. The MD&A should be read together with the Consolidated Financial Statements and accompanying Notes included in this Annual Report. Within the MD&A, we make certain state-ments that are forward-looking in nature. In making these statements, we use current information and our expecta-tions of future events; these are subject to assumptions,

risks and uncertainties that could change at any time and could cause actual results to differ materially from those expressed or implied by such statements, and these should be considered with the understanding of their inherent uncertainty. Forward-looking statements included in the MD&A are made only as of the date of this MD&A, and we assume no obligation to update any written or oral forward-looking statements made by us or on our behalf as a result of new information, future events or other factors.

CORPORATE PROFILE

FISCAL YEAR

2018 2017 2016

BBNC revenues $ 1,659,345,000 1,525,181,000 1,512,022,000

BBNC earnings before interest, taxes, and noncontrolling interests $ 58,761,000 66,410,000 38,759,000

BBNC earnings after interest, taxes, and noncontrolling interests $ 103,063,000 41,021,000 43,689,000

Cash provided by operating activities $ 45,687,000 94,985,000 74,154,000

Regular dividends declared $ 20,200,000 18,796,000 17,499,000

Regular dividends per share $ 37 35 32

Regular shares outstanding 540,100 540,100 540,100

Average shareholder hire 198 202 171

Bristol Bay Native Corporation (BBNC or the Corporation) is an Alaska Native Regional Corporation created pursuant to the Alaska Native Claims Settlement Act of 1971 (ANC-SA). Congress enacted ANCSA to resolve longstanding conflicts surrounding aboriginal land claims in Alaska and to stimulate economic development throughout Alaska. The Corporation was incorporated as a for-profit corpo-ration to benefit Alaska Natives with ties to the Bristol Bay region and at March 31, 2018, the Corporation had 10,376 shareholders. ANCSA provided the Corporation with a monetary entitlement from the federal government of $32.7 million and the right to 3,079,553 acres of federal lands. At March 31, 2018, stockholders’ equity retained by the Corporation has grown to $480.0 million, and cash dis-tributions to shareholders have exceeded $220.0 million.

BBNC is primarily a holding company and as such derives substantially all of its cash flow from its subsidiaries and its portfolio of passive investments which are the Company’s primary two asset allocations. We rely on profits from both to repay our creditors, to fund shareholder dividends, to

fund shareholder education opportunities and to fund corporate general and administrative costs. BBNC’s ability to fund each of these cash uses and to simultaneously grow the Corporation’s assets is subject to the profitability of our subsidiary businesses and the portfolio.

The BBNC Board of Directors approved a five-year stra-tegic plan for FY2017 through FY2021. The plan and the Corporation’s efforts focus on the pursuit of the following six strategic goals:

• Build the financial strength of BBNC.

• Pay predictable and increasing shareholder dividends.

• Balance responsible development and protection of our lands, fisheries and resources.

• Increase shareholder employment and development opportunities.

18 19BBNC FY2018 ANNUAL REPORT FINANCIALS

In order to increase the footprint of the benefits afforded by 8(a) contracting opportunities to our shareholders, village corporations and tribes within the Bristol Bay region, the Corporation is currently implementing a strategic initia-tive that includes establishing joint ventures and mentor protégé arrangements between BBNC government con-tracting subsidiaries and participating village corporations and tribes within the Bristol Bay region.

Branded as BBNC’s In-Region Government Contracting (IGC) initiative, the goals are as follows:

• increase in-region federal contract awards and successful performance rates,

• leverage BBNC subsidiaries capacity, experience and knowledge,

• create returns for BBNC, tribes and village corporations, and

• develop and provide extensive training to village corporations and tribes and their managers to increase their knowledge of federal government contracting programs and regulations and corporate governance to ensure full compliance for government contracting requirements.

Through the IGC initiative, BBNC developed three module training programs consisting of three two-day segments on topics such as corporate governance and formation, understanding financial statements, govern-ment contracting 101, 8(a) eligibility and applications and SBA compliance. As part of the IGC initiative, BBNC brings its experience to bear in aiding the village corporations and tribes to prepare to bid, win and perform contracts all while providing a level of quality to our customers that is consistent with BBNC’s long history of being a valued contractor to the federal government.

Investment earnings from the Portfolio are expected to be below those of FY2018. However, it should be noted that FY2018 was an exceptionally strong year for the market. Our asset allocation strategy within the Portfolio is meant to accomplish a desired rate of return with the least risk possible. Nonetheless, the returns we will experience will be reflective of broader trends in world financial markets.

BBNC continues to seek out attractive investments in the form of new acquisitions and “bolt-on” acquisitions to our existing business lines. We anticipate financing acquisitions through a mix of equity and debt capital. The Corporation’s debt load remains modest and we continue to enjoy access to abundant, low-cost debt financing. Both factors enable the Corporation to take on additional debt for acquisitions if and when deemed appropriated by management.

• Support educational, cultural and social initiatives that positively affect shareholders and descendants.

• Help to develop economic opportunities in the Bristol Bay region.

In order to meet the strategic goals, the Corporation must generate sufficient earnings. To that end, BBNC’s assets have been allocated to a variety of businesses that operate throughout Alaska and across the United States. As noted above, the Corporation’s assets are primarily allocated in two key areas: to a passive portfolio of investments (the Portfolio) and to our operating subsidiary compa-nies. There is also a small allocation to corporate assets which includes the Corporation’s headquarters building in Anchorage, Alaska.

The Portfolio is comprised of a variety of assets including marketable securities and liquid and non-liquid alternative investments. Management classifies the operating subsidiaries into four distinct business lines which are:

• Construction

• Government Services

• Industrial Services

• Tourism

The Corporation also has earnings from natural resource activities that are primarily comprised of certain revenue sharing payments received from other Alaska Native cor-porations as required under ANCSA.

The following pages are management’s outlook for FY2019 and view of the Corporation’s FY2018 results in total, for the Portfolio and of the business lines. In order to improve readability, in some cases these results are presented in a different format than the Consolidated Financial Statements.

FY2019 OUTLOOKManagement expects FY2019 to bring both challenges and opportunities across the broad landscape of BBNC’s business activities. Management expects overall earnings before income taxes to be greater in FY2019, due to consis-tent profit in most business lines and a significant reduction of losses in Industrial Services.

One of the largest subsidiaries in the Industrial Services business line is Peak Oilfield Service Company LLC (Peak). Peak and the other subsidiaries in this business line conduct substantially all of their operations within the State of Alaska. Uncertainty in the Alaska oil and gas industry driven by the precipitous drop in oil prices during FY2016 negatively affected earnings of our companies in this business line in FY2018. To what extent we will see increased recovery of revenues and margins remains to be seen. However, risks have been somewhat mitigated by the strong position-ing of our subsidiaries within the industry, and significant reductions in operating costs. Our companies are some of the safest and most efficient contractors working in Alaska, providing many services that are essential to our custom-ers. Our large fleet of exceptionally maintained equipment stands ready to serve the needs of our customers and our

customer base includes some of the strongest oil and gas companies operating in the state.

The Construction business line is expected to generate earnings slightly below those seen in FY2018. The federal government is the largest customer in the business line. Downward pressure on earnings continues to come from a variety of sources including continued negative changes to the Small Business Administration’s 8(a) program and from an operating environment where competitors are willing to work for slim margins. Our goal is to provide work for our customers at a price that results in the overall best value to the customer but also provides a profit for our shareholders.

The federal government is the primary customer for the Government Services business line. Challenges to the 8(a) program previously mentioned form headwinds in the industry. Earnings in FY2019 are expected to remain consistent from levels seen in recent years. Last year, BBNC made certain changes to the strategic alignment and management team within the business line in order to respond to the needs of our customers.

20 21BBNC FY2018 ANNUAL REPORT FINANCIALS

INDUSTRIAL SERVICES

The following table displays results of Industrial Services earnings, before interest and taxes for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

REVENUES

Industrial Services $ 867,764 764,541 788,107

COSTS AND EXPENSES

Industrial Services 872,822 767,941 772,132

Earnings from Industrial Services $ (5,058) (3,400) 15,975

The Industrial Services business line consists of the hold-ing company Bristol Bay Industrial, LLC and its companies Peak, Kakivik Asset Management (Kakivik), CCI Industrial Services (CIS), Alaska Directional, LLC, PetroCard and Bristol Alliance Fuels, LLC (BAF). Peak provides specialty services to the oil and gas industry in locations includ-ing Alaska’s Prudhoe Bay, Anchorage, Kenai, Valdez, and Palmer, and to a small extent, North Dakota. Peak provides a wide variety of services including crane services, rig moving, ice road construction, drilling support, general civil work, construction, trucking, facility operations and maintenance support, tank cleaning, and power systems. Kakivik specializes in nondestructive testing and inspec-tion. CIS provides a diverse array of specialty services to the oil and gas industry. Alaska Directional, LLC provides project management, directional drilling, trenching, plow-ing, cellular towers, and communications infrastructure services. PetroCard, a reputable fuel distributor in the Pacific Northwest, is based in Kent, Washington and

distributes fuel products through cardlock sites, mobile fueling and wholesale sales to commercial customers through facilities located primarily in Washington and Oregon. BAF, a fuel distributor in Dillingham, Alaska, helps to fulfill BBNC’s strategic goals of developing econom-ic opportunities in the Bristol Bay region, building the financial strength of BBNC, and increasing sharehold-er employment and development opportunities. The success of the Industrial Services business line can be attributed to the focus on quality safety programs that customers demand in this industry.

The Industrial Services business line is the Corporation’s largest source of shareholder hire. Average shareholder hire for this business line was 115 individuals with wages in excess of $8.4 million paid to shareholders in FY2018. The Industrial Services business line is expected to continue to play a key role in pursuit of the goals established within the Corporation’s strategic plan.

RESULTS OF OPERATIONSCONSOLIDATED RESULTS

The following table displays Consolidated Results for the fiscal year ended (in thousands except earnings per share and weighted average shares outstanding):

FISCAL YEAR

2018 2017 2016

REVENUES

Operating business lines $ 1,619,162 1,491,404 1,503,960

Investment earnings 27,959 24,789 (63)

Natural resources and royalty income 10,677 6,904 5,954

Other 1,547 2,084 2,171

Total revenue 1,659,345 1,525,181 1,512,022

COSTS AND EXPENSES

Cost of operating business lines 1,573,247 1,436,309 1,446,837

Cost of investment management 1,432 962 1,765

Corporate general and administrative expense 23,385 19,266 21,248

Interest 1,885 1,714 (107)

Other 2,520 2,234 3,413

1,602,469 1,460,485 1,473,156

Earnings from operations 56,876 64,696 38,866

Income tax benefit (expense) 46,348 (23,564) 4,875

Net earnings 103,224 41,132 43,741

Less income attributable to noncontrolling interest (161) (111) (52)

Net earnings attributable to Bristol Bay Native Corporation $ 103,063 41,021 43,689

Earnings per share $ 191 76 81

Weighted average shares outstanding 540,100 540,100 540,100

BBNC’s FY2018 earnings from operations were less than experienced in the previous fiscal year. Revenues from the operating business lines were $127.8 million higher than the prior year, primarily due to the effect the increase in gallons sold and fuel price per gallon had on the rev-enues of Industrial Services. Revenues from our portfolio investment earnings were more than the prior year by $3.2 million and were primarily due to better than expected returns from Corporation’s liquid alternative holdings and U.S. equity holdings.

Costs of the operating business lines were more than the prior year by $136.9 million, which was primarily due to the effect of the increase in gallons sold and fuel price per gallon on the expenses of Industrial Services. BBNC’s net earnings were $62.0 million more than prior year which equates to an increase in earnings per share of $115 from the prior year.

22 23BBNC FY2018 ANNUAL REPORT FINANCIALS

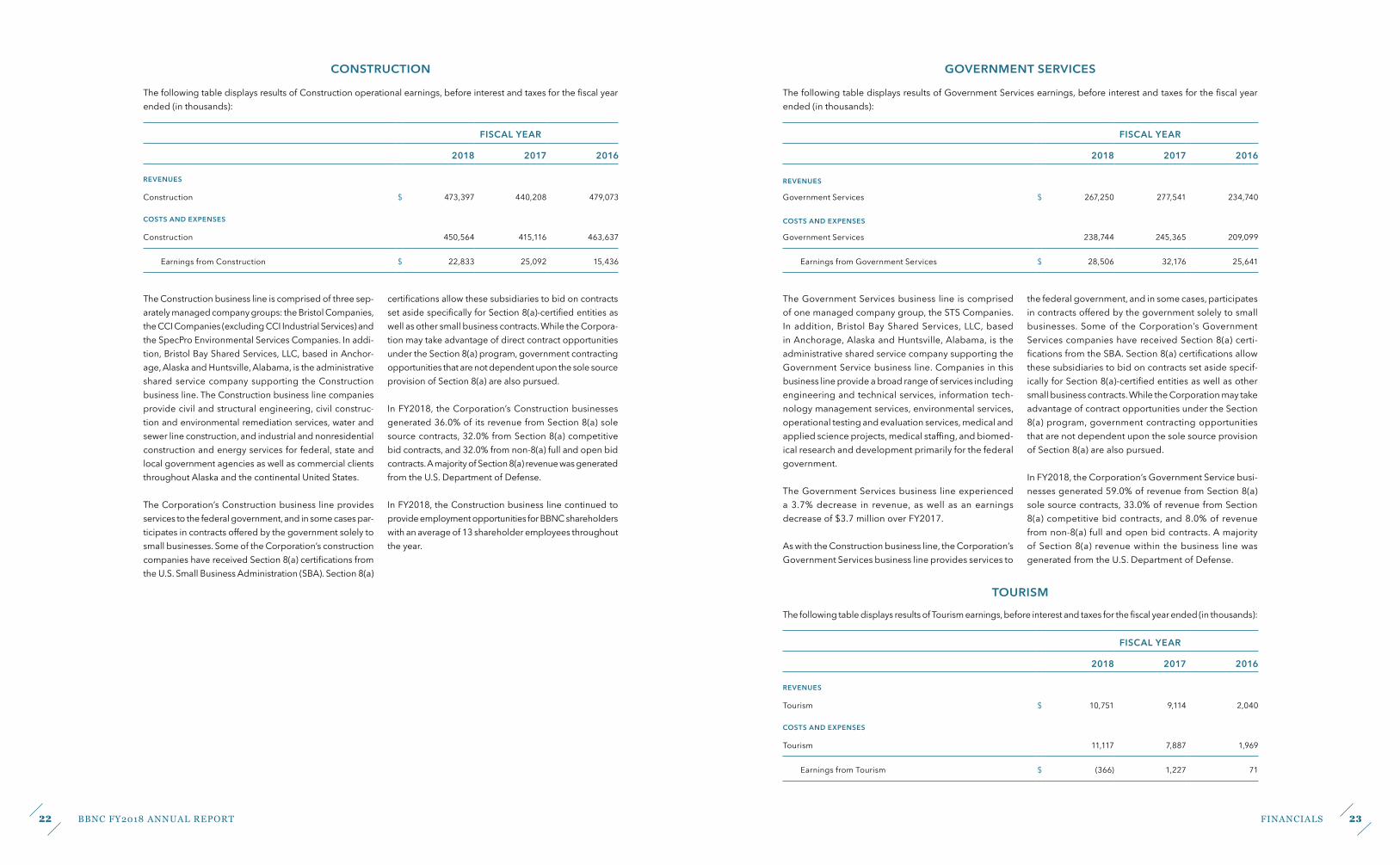

GOVERNMENT SERVICES

The following table displays results of Government Services earnings, before interest and taxes for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

REVENUES

Government Services $ 267,250 277,541 234,740

COSTS AND EXPENSES

Government Services 238,744 245,365 209,099

Earnings from Government Services $ 28,506 32,176 25,641

The Government Services business line is comprised of one managed company group, the STS Companies. In addition, Bristol Bay Shared Services, LLC, based in Anchorage, Alaska and Huntsville, Alabama, is the administrative shared service company supporting the Government Service business line. Companies in this business line provide a broad range of services including engineering and technical services, information tech-nology management services, environmental services, operational testing and evaluation services, medical and applied science projects, medical staffing, and biomed-ical research and development primarily for the federal government.

The Government Services business line experienced a 3.7% decrease in revenue, as well as an earnings decrease of $3.7 million over FY2017.

As with the Construction business line, the Corporation’s Government Services business line provides services to

the federal government, and in some cases, participates in contracts offered by the government solely to small businesses. Some of the Corporation’s Government Services companies have received Section 8(a) certi-fications from the SBA. Section 8(a) certifications allow these subsidiaries to bid on contracts set aside specif-ically for Section 8(a)-certified entities as well as other small business contracts. While the Corporation may take advantage of contract opportunities under the Section 8(a) program, government contracting opportunities that are not dependent upon the sole source provision of Section 8(a) are also pursued.

In FY2018, the Corporation’s Government Service busi-nesses generated 59.0% of revenue from Section 8(a) sole source contracts, 33.0% of revenue from Section 8(a) competitive bid contracts, and 8.0% of revenue from non-8(a) full and open bid contracts. A majority of Section 8(a) revenue within the business line was generated from the U.S. Department of Defense.

TOURISM

The following table displays results of Tourism earnings, before interest and taxes for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

REVENUES

Tourism $ 10,751 9,114 2,040

COSTS AND EXPENSES

Tourism 11,117 7,887 1,969

Earnings from Tourism $ (366) 1,227 71

CONSTRUCTION

The following table displays results of Construction operational earnings, before interest and taxes for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

REVENUES

Construction $ 473,397 440,208 479,073

COSTS AND EXPENSES

Construction 450,564 415,116 463,637

Earnings from Construction $ 22,833 25,092 15,436

The Construction business line is comprised of three sep-arately managed company groups: the Bristol Companies, the CCI Companies (excluding CCI Industrial Services) and the SpecPro Environmental Services Companies. In addi-tion, Bristol Bay Shared Services, LLC, based in Anchor-age, Alaska and Huntsville, Alabama, is the administrative shared service company supporting the Construction business line. The Construction business line companies provide civil and structural engineering, civil construc-tion and environmental remediation services, water and sewer line construction, and industrial and nonresidential construction and energy services for federal, state and local government agencies as well as commercial clients throughout Alaska and the continental United States.

The Corporation’s Construction business line provides services to the federal government, and in some cases par-ticipates in contracts offered by the government solely to small businesses. Some of the Corporation’s construction companies have received Section 8(a) certifications from the U.S. Small Business Administration (SBA). Section 8(a)

certifications allow these subsidiaries to bid on contracts set aside specifically for Section 8(a)-certified entities as well as other small business contracts. While the Corpora-tion may take advantage of direct contract opportunities under the Section 8(a) program, government contracting opportunities that are not dependent upon the sole source provision of Section 8(a) are also pursued.

In FY2018, the Corporation’s Construction businesses generated 36.0% of its revenue from Section 8(a) sole source contracts, 32.0% from Section 8(a) competitive bid contracts, and 32.0% from non-8(a) full and open bid contracts. A majority of Section 8(a) revenue was generated from the U.S. Department of Defense.

In FY2018, the Construction business line continued to provide employment opportunities for BBNC shareholders with an average of 13 shareholder employees throughout the year.

24 25BBNC FY2018 ANNUAL REPORT FINANCIALS

Natural Resource earnings consist primarily of 7(i) revenue sharing, net of the 50% distribution to village corporations and at-large shareholders that the Corporation receives from other regional Alaska Native Corporations. 7(i) receipts received are primarily from NANA Regional Corporation and Arctic Slope Regional Corporation. The Corporation distributes 50% of these receipts to village corporations and at-large shareholders as 7(j) payments.

Revenue from the sale of the Corporation’s natural resources, primarily gravel, rock and sand, is driven largely by resource development and infrastructure improvement activities in the Bristol Bay region. Revenues from the sale of natural resources tend to fluctuate from year-to-year. The Corpo-ration continues to advocate for responsible development of natural resources on BBNC lands and other lands within the BBNC region. We are committed to supporting a strong business climate that encourages investment in natural resource activities throughout the entire State of Alaska.

GENERAL AND ADMINISTRATIVE EXPENSESCorporate general and administrative expenses (G&A) increased from $19.3 million in FY2017 to $23.4 million in FY2018. G&A expenses are incurred by the Corporation in its efforts to provide corporate governance and oversight of its increasingly complex subsidiary operations, pursue new investments, protect the Corporation’s assets and

provide shareholder services. Corporate G&A increased by $4.0 million, primarily as a result of additional health insurance and workers compensation claims incurred on the Corporation’s self-insured plans in FY2018. G&A as a percentage of revenue was 1.4%, 1.3% and 1.4% in FY2018, FY2017 and FY2016, respectively.

TAXESThe following table displays our income tax (benefit) expense for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

Current income tax (benefit) expense $ (6,471) 21,160 (1,558)

Deferred income tax (benefit) expense (39,877) 2,404 (3,317)

Total income tax (benefit) expense $ (46,348) 23,564 (4,875)

Total tax (benefit) expense is comprised of current and deferred federal and state taxes which are primarily income based. To a lesser extent, the Corporation is subject to certain foreign income tax expense. Current tax expense represents expected taxes the Corporation will pay to taxing authorities on taxable income generated within the fiscal year plus or minus any prior year tax adjustments. Deferred tax expense represents the current year change in deferred tax assets net of changes in the Corporation’s deferred tax liabilities. Deferred tax assets and liabilities arise in the normal course of business and represent future differences between taxable income and book income

reported in the Corporation’s annual report. These differ-ences are expected and exist because of a lack of parity with respect to when certain items of income and expense are recognized under the tax code compared to treat-ment under Generally Accepted Accounting Principles. Our average blended tax rate is approximately 31.5% of earnings from operations.

During 2018, the Corporation sold oil and gas rights rec-ognizing a significant tax loss generating net operating losses, resulting in a deferred income tax benefit.

The Tourism business line consists of the holding company Bristol Bay Alaska Tourism, LLC and its companies Katmailand, Inc., Katmai Air, LLC, Katmai Lodge, LLC, Katmai Air Leasing, LLC, and Mission Lodge. The Katmai companies provide visitors with world renowned sport fishing, bear viewing, and lodging in Katmai National Park, located in Bristol Bay. Mission Lodge is an all-inclusive seasonal

fishing lodge on Lake Aleknagik near Dillingham in Bristol Bay. The Tourism business line provides opportunity for shareholder hire and development in the region. Management continues to seek opportunities to grow the Tourism business line through targeted acquisitions throughout the Bristol Bay region.

PORTFOLIO INVESTMENTS

The following table displays results of the Portfolio for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

REVENUES

Investment earnings (losses) $ 27,959 24,789 (63)

COSTS AND EXPENSES

Investment management 1,432 962 1,765

Earnings (losses) from Investments $ 26,527 23,827 (1,828)

The Corporation recognizes Portfolio earnings primarily from investments in public and private passive invest-ments including marketable securities, private equity placements and a number of commercial real estate investments located primarily in Anchorage, Alaska.

The Portfolio is managed pursuant to an investment policy which provides for a diversified asset allocation of equity securities, alternative investments, fixed income securi-ties, and cash. Real estate and alternative investments are often private, non-publicly-traded equity interests. The allocation to each of these four investment classes was developed with the help of the Corporation’s external investment advisor using modern portfolio theory. The

established policy allocation to different investment classes is designed to achieve a target annual return of 8.1% while exposing the Corporation to the lowest level of risk possible. At March 31, 2018, the total market value of the Portfolio was $223.1 million compared to $194.3 million at March 31, 2017. Portfolio holdings in private, non-publicly-traded investments were $72.4 million at March 31, 2018, compared to $54.7 million at March 31, 2017. The Corporation’s Portfolio generated investment earnings of $28.0 million, reflective of the broader trends in the equity markets, during 2018. The Corporation’s Portfolio returns are benchmarked against a custom index that approximates our investment allocation targets.

NATURAL RESOURCE MANAGEMENT

The following table displays results of Natural Resource earnings for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

REVENUES

Natural Resources

7(i) revenue sharing net of 7(j) distributions $ 10,375 6,713 5,671

Natural Resources 302 191 283

Earnings from Natural Resources $ 10,677 6,904 5,954

26 27BBNC FY2018 ANNUAL REPORT FINANCIALS

FISCAL YEAR

2018 2017 2016

Total available line of credit 53,582 32,307 59,077

Total liquidity $ 203,719 200,753 230,108

To meet both our short- and long-term liquidity require-ments we look to a variety of funding sources, both inter-nal and external. Our primary source of liquidity is cash generated from operating activities and from Portfolio earnings. In order to meet additional liquidity needs at the parent level, the Corporation has a line of credit with which it may draw upon to fund cash needs. The primary

line of credit has a ceiling of $75 million and is secured by marketable securities. If further acquisition opportunities arise, the Corporation will consider the costs and benefits of additional debt sources. Our cash flow from operations and access to short-term debt gives management confi-dence that the Corporation’s liquidity needs can be met in both the short- and long-term.

SIGNIFICANT SOURCES AND USES OF CAPITALThe following table displays sources/uses of cash and capital structure for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

SOURCES/USES OF CAPITAL

Cash flows from operating activities $ 45,687 94,985 74,154

Cash flows from investing activities (30,080) (53,726) (42,343)

Cash flows from financing activities (76,151) (28,427) (21,948)

Increase (decrease) in cash and cash equivalents $ (60,544) 12,832 9,863

CAPITAL STRUCTURE

Short and long-term debt $ 39,577 97,483 107,417

Total shareholders’ equity 480,031 397,315 374,676

Total capital $ 519,608 494,798 482,093

Debt to equity ratio 8.24% 24.54% 28.67%

OPERATING ACTIVITIES

The operating activity section of the statement of cash flows reconciles net income to the amount of cash provid-ed by operating transactions. Cash flows from operating activities was $45.7 million which was primarily comprised of net income of $103.2 million plus depreciation expense of $22.6 million less $26.1 million in gain on sale of marketable securities and $39.9 million in deferred tax benefits. For FY2017, cash flows from operating activities

was $95.0 million which was primarily comprised of net income of $41.1 million plus depreciation expense of $24.2 million and other changes in working capital. For FY2016, cash flows from operating activities was $74.2 million which was primarily comprised of net income of $43.7 million plus depreciation expense of $25.9 million and other changes in working capital.

BALANCE SHEETThe following table displays key balance sheet data as of March 31, for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

Cash and cash equivalents $ 24,615 85,159 72,327

Marketable securities 150,763 139,563 141,427

Other current assets 220,019 180,898 168,834

Investment in unconsolidated affiliates 29,994 19,187 21,421

Other investments 42,359 35,519 22,099

Other assets 3,139 3,994 3,604

Deferred taxes 14,096 0 0

Property, plant and equipment, net 148,344 155,240 161,012

Goodwill and intangible assets 66,531 66,942 52,326

Total assets 699,860 686,502 643,050

Current liabilities 185,254 179,365 151,501

Long-term liabilities 34,575 109,822 116,873

Total shareholders’ equity 480,031 397,315 374,676

Cash and cash equivalents decreased primarily due to the Corporation’s reinvestment in marketable securities and other investments. Other investments continue to increase as the Corporation increases its investments in alternative investments held in partnership and partner-ship-like entities where the Corporation owns less than 100% of the entity. Property, plant and equipment, net of depreciation, decreased from FY2017 to FY2018 due

to additional depreciation primarily at Peak and a write off of fixed assets in FY2018. Peak owns and operates a significant fleet of equipment and vehicles.

Long-term liabilities decreased from FY2017 to FY2018 as the Corporation continues to pay down long-term debt. BBNC shareholders equity continues to grow as a result of increased earnings net of dividends paid to shareholders.

LIQUIDITY AND CAPITAL RESOURCESThe following table displays total liquidity and capital resources as of March 31, for the fiscal year ended (in thousands):

FISCAL YEAR

2018 2017 2016

AVAILABLE FUNDS

Cash and cash equivalents $ 24,615 85,159 72,327

Marketable securities 150,763 139,563 141,427

Less: collateral on marketable securities (25,241) (56,276) (42,723)

Total available funds $ 150,137 168,446 171,031

AVAILABLE LINE OF CREDIT

Total line of credit 57,332 35,607 62,277

Less: outstanding letters of credit (3,750) (3,300) (3,200)

28 29BBNC FY2018 ANNUAL REPORT FINANCIALS

piloting, health and human services, occupational safety and health training, and medical assistant training. Provid-ing increased support for these types of programs is one of the Foundation’s long-term objectives.

Recognizing the value of job skills that do not require four-year college degrees, the Foundation also awards scholarships to help pay for vocational training and provides assistance for shareholders to attend various vocational training programs. This program specifically assists those that are in need of specialized certification or training in order to enhance their employment or career opportunities. In many instances, vocational assistance recipients, who are also shareholders, have used their certifications to be eligible for employment by the Cor-poration and its subsidiaries. The Corporation funded over $1.0 million in contributions to the BBNC Education Foundation in FY2018.

The Corporation further hosts the Bristol Bay Leadership Forum, a two-day session that provides Bristol Bay area vil-lage corporation, village council, borough, and city council leaders with an opportunity to meet with business, govern-

ment, and Native leaders, to share experiences, discuss issues affecting the people they represent, explore solutions to common problems and to consider new opportunities that may help lead to economic, educational and cultural benefits.

In FY2012, the Corporation initiated an Elder’s Benefit Program. Eligible original shareholders age 65 or older began receiving a benefit of $125 per quarter beginning in the third quarter of FY2012. In October 2013, share-holders approved establishment and funding of an Elders’ settlement trust, which was funded with a $10.8 million contribution from the Corporation in FY2015. Distributions from the trust to eligible shareholders are not taxable to the shareholders to the extent they are paid out of the current year or cumulative undistributed income of the trust.

The Corporation’s operations allow BBNC to provide meaningful career opportunities for our shareholders. During FY2018, our shareholder employment was a total of 198 shareholder employees. Total shareholder wages paid in FY2018 were $14.1 million. We continue to focus on expanding opportunities for shareholder employment.

CRITICAL ACCOUNTING ESTIMATESThe Corporation’s consolidated financial statements are prepared in accordance with generally accepted accounting principles. Significant accounting policies are discussed in note 1 Nature of Operations and Sum-mary of Significant Accounting Policies accompanying the consolidated financial statements of this report. In connection with the preparation of the financial state-ments, management is required to make assumptions and estimates about future events, and apply judgments that affect the reported amounts of assets, liabilities, revenues, expenses and related disclosures. Amounts recognized in the financial statements from such esti-

mates are necessary based on numerous assumptions involving varying and potentially significant degrees of judgment and uncertainty. Actual results may differ from management’s assumptions and estimates.

Areas in which accounting estimates could be different from the final results include accounts receivable, esti-mates of total contract costs for fixed price contracts, the fair value of investments, impairment of long-live assets, intangibles and goodwill, the tax valuation of oil and gas rights, and deferred tax assets, among others.

INVESTING ACTIVITIES

Net cash activity from investment activity is typically con-sistent unless significant acquisition activity occurs during a fiscal year. FY2018, FY2017 and FY2016 are reflective

of the Corporation’s normalized uses of cash for investing activities on a year-to-year basis.

FINANCING ACTIVITIES

Financing activities include transactions involving share-holder dividends, noncontrolling interests and borrowings and repayments of debt. Cash used by financing activities in FY2018 includes shareholder dividends of $20.1 mil-lion. FY2018 had increased cash flows used in financing activities due to increased payment on the line of credit compared to subsequent years.

Our total capital structure consists of the original monies received by the Corporation under ANCSA on behalf of its shareholders, funds provided by debt financing arrange-ments and accumulated earnings that have not been paid out in dividends. The overall increase in total capital in FY2018 is comprised of the fiscal year earnings offset by dividends paid.

We continue to monitor the Corporation’s debt-to-equity ratio and intend to maintain an appropriate balance of debt and liquidity. Management expects that doing so will enable us to both meet our financial obligations and ready the Corporation to take advantage of strategic opportunites in the future.

BBNC retains ownership of approximately 3.1 million acres of subsurface and approximately 100,000 acres of surface real estate. BBNC shareholder’s equity does not include the value of lands conveyed as a result of ANCSA, which cannot be readily estimated. Consistent with most Alaska Native Corporations, the Corporation did not record a value for such lands due to the inability to establish the value of those lands at the time of conveyance, especially considering the time and expense of obtaining appraisals.

DIVIDENDS AND SHAREHOLDER BENEFITSThe following table displays total dividends paid in each of the fiscal years ended (in thousands):

FISCAL YEAR

2018 2017 2016

Regular dividends declared $ 20,200 18,796 17,499

Cumulative dividends declared, since inception $ 220,872 200,672 181,876

Many of the benefits provided to our shareholders are a result of profits derived from federal government contract-ing. The Corporation’s long-term strategy is to enhance its financial strength while paying increasing shareholder dividends and promoting educational and employment opportunities. The core of our success is our focus on education and protecting our cultural heritage. We are committed to training our future generations. Since 1986, the Corporation has provided education scholarships to its shareholders pursuing both higher education degrees and vocational certifications.

In 1992, BBNC formally incorporated the BBNC Education Foundation (the Foundation) as a 501(c)(3) entity and has continued to invest in education and training through the Foundation. Scholarship recipients have graduated with bachelors, masters, and other advanced degrees, such as a Ph.D. in Anthropology, Doctors of Medicine, Doctors of Veterinary Medicine, Juris Doctor (Law), and degrees in engineering, business administration, education, nursing, guidance counseling, environmental science, economics and philosophy and associate degrees and other vocation-al certifications in dental therapy, culinary arts, professional

30 31BBNC FY2018 ANNUAL REPORT FINANCIALS

INDEPENDENT AUDITORS’ REPORTThe Board of Directors and Stockholders Bristol Bay Native Corporation:

We have audited the accompanying consolidated financial statements of Bristol Bay Native Corporation and its subsid-iaries, which comprise the consolidated balance sheets as of March 31, 2018 and 2017, and the related consolidated statements of operations, changes in stockholders’ equity, and cash flows for each of the years in the three-year period ended March 31, 2018, and the related notes to the consolidated financial statements.

MANAGEMENT’S RESPONSIBILITY FOR THE FINANCIAL STATEMENTS

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with U.S. generally accepted accounting principles; this includes the design, implementation, and main-tenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

AUDITORS’ RESPONSIBILITY

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consoli-dated financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OPINION

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Bristol Bay Native Corporation and its subsidiaries as of March 31, 2018 and 2017, and the results of their operations and their cash flows for each of the years in the three-year period ended March 31, 2018, in accordance with U.S. generally accepted accounting principles.

Anchorage, Alaska June 8, 2018

TEN YEAR FINANCIAL SUMMARY(In thousands except share data, ratios, and percentages)

2018 2017 2016 2015 2014 2013 2012 2011 2010 2009

REVENUES

Investment income $ 27,959 24,789 (63) 11,442 25,167 14,254 5,537 14,935 23,282 (34,293)

Industrial Services 867,764 764,541 788,107 1,069,079 1,153,597 1,136,637 1,212,609 986,510 825,659 1,041,693

Construction 473,397 440,208 479,073 414,033 404,907 517,799 449,868 401,608 375,776 268,503

Government Services 267,250 277,541 234,740 228,720 240,823 282,821 287,186 256,247 152,199 102,296

Tourism 10,751 9,114 2,040 1,861 1,890 1,493 0 0 0 0

Natural Resources 10,677 6,904 5,954 10,186 8,396 6,524 9,877 7,648 3,965 12,706

Other income (1) 1,547 2,084 2,171 763 1,114 2,252 430 252 1,515 666

TOTAL OPERATING REVENUE 1,659,345 1,525,181 1,512,022 1,736,084 1,835,894 1,961,780 1,965,507 1,667,200 1,382,396 1,391,571COSTS AND EXPENSES (1) 1,602,469 1,460,485 1,473,156 1,662,248 1,753,661 1,892,521 1,898,335 1,597,930 1,346,170 1,394,362

Earnings from operations 56,876 64,696 38,866 73,836 82,233 69,259 67,172 69,270 36,226 (2,791)

Income tax benefit (expense), net of extraordinary benefit

46,348 (23,564) 4,875 (28,000) (33,047) (27,941) 3,054 (26,253) (4,289) 8,853

Earnings applicable to noncontrolling interests

(161) (111) (52) (945) (36) 0 0 0 0 (888)

NET EARNINGS (LOSS) $ 103,063 41,021 43,689 44,891 49,150 41,318 70,226 43,017 31,937 5,174

CASH FLOW DATA

Net cash provided by operating activities

$ 45,687 94,985 74,154 89,618 120,534 30,489 36,975 17,484 5,631 56,439

Net capital expenditures 15,106 13,772 10,656 19,552 7,215 18,014 16,992 5,669 5,750 8,548

Addition (reduction) to long-term debt

(57,906) (9,934) (3,727) (862) 62,851 18,974 (11,648) (2,731) 6,884 (11,146)

Dividends paid 20,111 18,796 17,499 27,313 14,981 13,883 12,070 7,453 6,913 6,481

SHAREHOLDER DATA

Earnings (loss) per share $ 191.00 76.00 81.00 83.00 91.00 76.51 130.02 79.65 59.13 9.58

Dividends per share 37.40 34.80 32.40 30.00 27.00 25.00 22.00 13.80 12.80 12.00

Return on average stockholders’ equity

23.5% 10.6% 11.7% 12.9% 14.8% 14.6% 29.2% 22.2% 19.6% 3.4%

FINANCIAL POSITION

Cash and equivalents $ 24,615 85,159 72,327 62,464 49,471 38,214 46,135 35,118 25,521 26,170

Working capital (1) 59,380 86,692 89,660 89,135 59,827 37,931 71,655 10,469 27,479 34,340

Marketable equity securities at fair market value

150,763 139,563 141,427 133,445 136,807 176,781 115,202 97,830 84,820 59,645

Property, plant and equipment, at cost

148,344 155,240 161,012 170,630 174,337 70,263 56,940 46,481 46,748 47,170

Total assets 699,860 686,502 643,050 656,621 629,922 559,034 518,703 448,322 370,456 305,896

Long-term debt (including current maturities)

39,577 97,483 107,417 111,144 112,006 49,155 30,181 41,829 44,560 37,676

Stockholders’ equity 480,031 397,315 374,676 349,376 330,897 296,732 269,297 211,141 175,577 150,553

RATIOS

Current ratio (1) 1.3 1.5 1.6 1.5 1.3 1.2 1.3 1.1 1.2 1.3

Long-term debt to equity ratio 0.08 0.25 0.29 0.32 0.34 0.17 0.11 0.20 0.25 0.25

NOTES: (1) Marketable equity securities have not been included as part of current assets for this computation

32 33BBNC FY2018 ANNUAL REPORT FINANCIALS

BRISTOL BAY NATIVE CORPORATION AND SUBSIDIARIESCONSOLIDATED BALANCE SHEETS

March 31, 2018 and 2017 (In thousands, except shares)

LIABILITIES AND STOCKHOLDERS’ EQUITY

2018 2017

CURRENT LIABILITIES

Notes payable (note 9) $ 3,174 1,000

Accounts payable 77,819 54,832

Accrued liabilities (note 11) 76,516 86,930

Billings in excess of costs and earnings (note 1(m)) 21,341 21,848

Unclaimed dividends 1,402 1,313

Current maturities of long-term debt (note 10) 5,002 13,442

TOTAL CURRENT LIABILITIES 185,254 179,365

Long-term debt, less current maturities (note 10) 34,575 84,041

Deferred taxes (note 12) — 25,781

TOTAL LIABILITIES 219,829 289,187

Stockholders’ equity

Class A common stock, no par value. Authorized, 1,000,000 shares; issued and outstanding, 488,500 shares (note 2)

29,571 29,571

Class B common stock, no par value. Authorized, 300,000 shares; issued and outstanding, 51,600 shares (note 2)

3,124 3,124

Retained earnings 447,062 364,199

Total stockholders’ equity attributable to Bristol Bay Native Corporation 479,757 396,894

Noncontrolling interest 274 421

Total stockholders’ equity 480,031 397,315

Commitments and contingencies (notes 6, 9, 10, 11, 12, 13, 14, and 15)

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY $ 699,860 686,502

See accompanying notes to consolidated financial statements.

BRISTOL BAY NATIVE CORPORATION AND SUBSIDIARIESCONSOLIDATED BALANCE SHEETS

March 31, 2018 and 2017 (In thousands, except shares)

ASSETS

2018 2017

CURRENT ASSETS

Cash and cash equivalents $ 24,615 85,159

Marketable securities (notes 5 and 7) 150,763 139,563

Accounts receivable:

Trade, net (note 8) 180,799 144,602

Natural resources (note 1(l)) 252 4,424

Inventories 5,479 4,173

Costs and earnings in excess of billings (note 1(m)) 21,895 19,931

Prepaid expenses and refundable taxes 8,094 263

Notes receivable (note 1(g)) 3,500 7,505

TOTAL CURRENT ASSETS 395,397 405,620

Investments in unconsolidated affiliates (note 6) 29,994 19,187

Other investments (note 7) 42,359 35,519

Other assets 3,139 3,994

Deferred taxes (note 12) 14,096 —

Property, plant, and equipment, at cost (notes 1(i) and 10):

Land 14,719 13,660

Buildings 49,757 51,205

Leasehold improvements 26,883 22,126

Machinery and equipment 182,077 180,019

273,436 267,010

Less accumulated depreciation 125,092 111,770

148,344 155,240

Intangible assets, net (note 4) 24,812 26,323

Goodwill (notes 1(j) and 4) 41,719 40,619

TOTAL ASSETS $ 699,860 686,502

34 35BBNC FY2018 ANNUAL REPORT FINANCIALS

BRISTOL BAY NATIVE CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITYYears ended March 31, 2018, 2017, and 2016 (In thousands)

COMMON STOCKRETAINED EARNINGS

TOTAL SHAREHOLDERS’

EQUITY ATTRIBUTABLE

TO BRISTOL BAY NATIVE

CORPORATION

NON-CONTROLLING

INTERESTS

TOTAL STOCKHOLDERS’

EQUITY

CLASS A CLASS B

Balance, April 1, 2015 $ 29,571 3,124 315,784 348,479 897 349,376

Dividends ($32.40 per share)

— — (17,499) (17,499) — (17,499)

Net earnings — — 43,689 43,689 52 43,741

Distributions to noncontrolling interest — — — — (942) (942)

Balance, March 31, 2016 29,571 3,124 341,974 374,669 7 374,676

Dividends ($34.80 per share)

— — (18,796) (18,796) — (18,796)

Net earnings — — 41,021 41,021 111 41,132

Distributions to noncontrolling interest — — — — 303 303

Balance, March 31, 2017 29,571 3,124 364,199 396,894 421 397,315

Dividends ($37.40 per share) — — (20,200) (20,200) — (20,200)

Net earnings — — 103,063 103,063 161 103,224

Distributions to noncontrolling interest — — — — (308) (308)

Balance, March 31, 2018 $ 29,571 3,124 447,062 479,757 274 480,031

See accompanying notes to consolidated financial statements.

BRISTOL BAY NATIVE CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONSYears ended March 31, 2018, 2017, and 2016 (In thousands, except shares and per share data)

2018 2017 2016

REVENUES

Industrial services $ 867,764 764,541 788,107

Construction 473,397 440,208 479,073

Government services 267,250 277,541 234,740

Tourism 10,751 9,114 2,040

Investment earnings (notes 5, 6 and 7) 27,959 24,789 (63)

Natural resources 10,677 6,904 5,954

Other 1,547 2,084 2,171

1,659,345 1,525,181 1,512,022

COSTS AND EXPENSES

Cost of industrial services 872,822 767,941 772,132

Cost of construction 450,564 415,116 463,637

Cost of government services 238,744 245,365 209,099

Cost of tourism 11,117 7,887 1,969

Cost of investment management 1,432 962 1,765

Corporate general and administrative expense 23,385 19,266 21,248

Interest 1,885 1,714 (107)

Other 2,520 2,234 3,413

1,602,469 1,460,485 1,473,156

Earnings from operations 56,876 64,696 38,866

Income tax benefit (expense) (note 12) 46,348 (23,564) 4,875

NET EARNINGS 103,224 41,132 43,741

Less income attributable to noncontrolling interest (161) (111) (52)

NET EARNINGS ATTRIBUTABLE TO BRISTOL BAY NATIVE CORPORATION $ 103,063 41,021 43,689

Earnings per share $ 191 76 81

Weighted average shares outstanding 540,100 540,100 540,100

See accompanying notes to consolidated financial statements.

36 37BBNC FY2018 ANNUAL REPORT FINANCIALS

BRISTOL BAY NATIVE CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS (CONTINUED)Years ended March 31, 2018, 2017, and 2016 (In thousands)

2018 2017 2016

CASH FLOWS FROM INVESTING ACTIVITIES:

Acquisition of businesses, net of cash acquired (4,256) (23,087) (15,591)

(Issuance of) collection on notes receivable 4,005 (7,505) —

Return of capital from unconsolidated affiliates 3,679 1,752 —

Investment in unconsolidated affiliates (15,220) — (1,814)

Purchase of other investments (5,463) (18,695) (14,282)

Return of capital from other investments 2,281 7,581 —

Additions to property, plant, and equipment (15,106) (13,772) (10,656)

Net cash used in investing activities (30,080) (53,726) (42,343)

CASH FLOWS FROM FINANCING ACTIVITIES:

Proceeds from long-term debt 29,000 54,832 60,571

Repayment of long-term debt (86,906) (64,766) (64,298)

Proceeds of notes payable 2,174 — 220

Contributions from (distributions to) noncontrolling interests (308) 303 (942)

Dividends paid (20,111) (18,796) (17,499)

Net cash used in financing activities (76,151) (28,427) (21,948)

Increase (decrease) in cash and cash equivalents (60,544) 12,832 9,863

CASH AND CASH EQUIVALENTS:

Beginning of year 85,159 72,327 62,464

End of year $ 24,615 85,159 72,327

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION:

CASH PAID DURING THE YEAR FOR:

Interest $ 2,435 1,769 2,157

Income taxes paid 9,549 7,639 25,168

Income taxes refunded 3,234 — —

SUPPLEMENTAL SCHEDULE OF NONCASH INVESTING AND FINANCING ACTIVITIES:

Future payments based upon earnings in connection with acquisition 1,100 — —

Holdback payments in connection with acquisitions — 2,855 1,550

See accompanying notes to consolidated financial statements.

BRISTOL BAY NATIVE CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWSYears ended March 31, 2018, 2017, and 2016 (In thousands)

2018 2017 2016

CASH FLOWS FROM OPERATING ACTIVITIES:

NET EARNINGS $ 103,224 41,132 43,741

Adjustments to reconcile net earnings to cash provided by operating activities:

Equity in losses from unconsolidated affiliates 734 482 398

Unrealized depreciation (appreciation) of marketable securities and other investments 6,126 (15,864) 9,234

Depreciation and amortization 22,588 24,156 25,856

(Gain) loss on disposal of property plant and equipment (67) 74 (246)

Property and equipment abandonment and impairment losses 3,292 8,916 —

Gain on sale of marketable securities and other investments (26,074) (2,776) (1,540)

Gain on interest rate swap (156) (394) (65)

Deferred taxes (39,877) 2,404 (3,317)

Bad debt expense 135 248 357

Changes in operating assets and liabilities that provided (used) cash, net of acquisitions:

Accounts receivable (29,766) (14,553) 42,859

Costs and earnings in excess of billings (1,947) 1,246 1,927

Billings in excess of costs (962) 3,886 343

Recognition (reversal) of forward losses on construction contracts (2) 133 (1,585)

Net (purchase) sale of marketable securities 5,090 18,198 (15,676)

Inventories (1,306) 788 2,418

Accounts payable 22,987 (6,121) (6,589)

Accrued liabilities and other (18,332) 33,030 (23,961)

Net cash provided by operating activities 45,687 94,985 74,154

38 39BBNC FY2018 ANNUAL REPORT FINANCIALS

The Corporation consolidates majority owned subsidiaries that are not considered variable interest entities for which the Corporation exercises operational control. The Corporation will also consolidate any variable interest entities of which it is the primary beneficiary. The Corporation consolidates AN-AN, C, LLC as the primary beneficiary of a variable interest entity. Included in the Corporation’s consolidated balance sheet as of March 31, 2018, is $18,820,000 of assets and $12,541,000 of liabilities of AN-AN, C, LLC, consisting primarily of a building and the associated long-term loan payable for the building. The Corporation contributed $6,463,000 of equity and guarantees the long-term loan payable of AN-AN, C, LLC.

All significant intercompany accounts and transactions have been eliminated in consolidation.

(C) CASH AND CASH EQUIVALENTSCash and cash equivalents include cash and investments with initial maturities, at the time of purchase, of three months or less. Money market mutual funds that are part of the investment portfolio are not considered to be cash equivalents and are included in marketable securities.

(D) MARKETABLE SECURITIESMarketable securities are used to supplement cash provided by operations in order to fund corporate overhead and shareholder dividends. The marketable securities are recorded at fair value and are classified as trading. The Corporation includes net unrealized gains and losses as a part of investment earnings. Realized gains or losses resulting from the sale of securities are also included in investment earnings. Cost of securities is determined using the first-in, first-out method. Interest income is recorded on the accrual basis. Dividends are recorded on the ex-dividend date.

(E) INVESTMENTS IN UNCONSOLIDATED AFFILIATESInvestments in unconsolidated affiliates are accounted for using the cost or the equity method, depending on whether the Corporation has the ability to exercise significant influence over operating and financial policies of an investee. Under the cost method, investments are carried at acquisition cost and distributions are recognized as income when received. Under the equity method, the Corporation’s share of affiliate earnings is included in income when earned, and distributions are credited to the investment when received. For flowthrough entities (i.e., partnerships, limited liability companies, subchapter S corporations, etc.), the ability to exercise significant influence is presumed to exist if the percentage of ownership is equal to or greater than 3 to 5%. For other entities, significant influence is presumed to exist if the percentage of ownership is equal to or greater than 20%. The Corporation’s share of earnings or losses is determined either by its respective ownership percentage or, when appropriate, by using the hypothetical liquidation at book value method (HLBV). When using the HLBV, the Corporation evaluates at each balance sheet date, the amount it would receive or be obligated to pay if the investee were liquidated. The difference between this amount at the beginning of the period compared to end of the period plus cash received from the investments during the period and less amounts contributed to the investment during the period, represents the Corporation’s earnings or losses for the period from such investment.

Cost method investments are reviewed for impairment in the occurrence of a triggering event indicating impairment. Equity method investments are analyzed for impairment on an ongoing basis. An impairment charge is recorded whenever the fair value of the investment is considered to be less than the carrying amount and the impairment is considered other than temporary.

(F) TRADE ACCOUNTS RECEIVABLETrade accounts receivable are recorded at the invoiced amount and do not bear interest. The allowance for doubtful accounts is management’s best estimate of the amount of probable credit losses in existing accounts receivable. The Corporation determines the allowance based on its historical write off experience and current economic conditions. Past due balances over 60 days in a specified amount are reviewed individually for collectability. All other balances are reviewed in aggregate. Account balances are charged off against the allowance after all means of collection have been exhausted and the potential for recovery is considered remote. The Corporation does not have any off balance sheet credit exposure related to its customers. The allowance for uncollectible accounts was $828,000 and $716,000 at March 31, 2018 and 2017, respectively.

BRISTOL BAY NATIVE CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTSMarch 31, 2018 and 2017

(1) NATURE OF OPERATIONS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(A) NATURE OF OPERATIONSThe operations of Bristol Bay Native Corporation (Corporation) include the following business lines:

• Industrial services (includes petroleum distribution)

• Construction

• Government services

• Tourism

• Portfolio of public and private passive investments, some of which are managed by outside investment managers

• Subsurface and other natural resource management

(B) PRINCIPLES OF CONSOLIDATIONThe accompanying consolidated financial statements include the accounts of the Corporation and its wholly, and majority owned, subsidiaries:

Bristol Resources, Inc.Bristol Bay Corporate Services, Inc.Bristol Bay Architects, Inc.*Bristol Bay Parking, LLCBristol Bay Development LLCBristol Bay Development Fund, LLCAN-AN, C, LLCArctic Holdings, LLCPetroCard, Inc. (PC)Bristol Alliance Fuels, LLCBristol Bay Petroleum Properties, LLCKatmailand, Inc.Katmai Air, LLCKatmai Lodge, LLCKatmai Air Leasing, LLCBristol Bay Mission Lodge, LLCBristol Environmental Solutions, LLCBristol Construction Services, LLCBristol Design Build Services, LLCBristol Environmental Remediation Services, LLCBristol Engineering Services CorporationBristol General Contractors, LLCBristol Industries, LLCSES Electrical LLC

SES Civil Contractors LLCSES Energy Services LLCBadger Technical Services, LLCBristol Bay Shared Services, LLCDefendSafe, LLCEagle Applied Sciences LLCEagle Medical Services, LLCEagle Integrated Healthcare, LLCEagle Global Scientific, LLCGlacier Technical Solutions, LLCGlacier Technologies LLCMedPro Technologies, LLCBristol Infrastructure Design Services, LLCSpecPro, Inc.SpecPro Professional Services LLCBristol Site Contractors, LLC SES Infrastructure Services, LLCCCI Construction Services, LLC CCI Energy and Construction Services, LLCCCI Group, LLCCCI, Inc.CCI Mechanical, LLCCCI Solutions, LLCCCI General Contractors, LLC

CCI Utility Services, LLCCCI Facility Contractors, LLCCCI Facility Support Services, LLCAerostar SES LLCSES Construction and Fuel Services LLCSpecPro Environmental Services LLCWorkforce Resources, LLCSpecPro Technical Services LLCSpecPro Management Services, LLCSTS Systems Integration, LLCSTS Systems Support, LLCSTS Solutions and Training, LLCTekPro Services, LLCTekPro Support Services, LLCVista International Operations, Inc.Vista Technical Services, LLCVista Defense Technologies LLCBristol Bay Industrial, LLCPeak Oilfield Service Company LLCCCI Industrial Services, LLCKakivik Asset Management, LLCAlaska Directional, LLCBristol Bay Alaska Tourism, LLC

*No significant activity in 2018, 2017 or 2016.

40 41BBNC FY2018 ANNUAL REPORT FINANCIALS

The Corporation performs its annual impairment review of goodwill at March 31, and when a triggering event occurs between annual impairment tests. No impairment loss was recorded in 2018, 2017 or 2016. The reporting units assessed for impairment include Industrial Services Group (ISG) group, SpecPro Technical Services (STS) group, and SpecPro Environmental Services (SES) group.