MODULE 1 - The basics -...

54

MODULE 1 - The basics #1 Test taking strategies. The following section is not required portion of the salespersons curriculum, it is offered to advise the salesperson candidate with basic test taking techniques only. The responsibility to study and prepare for the salesperson exam rests solely with the candidate. None of the material in test taking strategies section of the textbook is the basis for any particular exam question. The material is this section is not part of the exam. As of April 1, 2016 the Massachusetts real estate salesperson exam is administered by PSI Exams on behalf of the Commonwealth nearby testing centers are in Fall River and Boston. Candidates making exam reservations after March 15, 2016 should visit psiexams.com or call 800 733-9267. Part One - General Section - 80 questions, Part Two - Massachusetts Law Section- 40 questions. Basically, 70% is a passing grade. Each part of the exam is administered separately. 150 minutes for the first part, 90 minutes for the second part. If you pass, you’ll only be told that you’ve passed. If you fail, you’ll be given your score. It is possible to pass one part, but not the other, if so you’ll only be required to retake the unpassed part. The exam is administered by computer, you will be issued with a writing implement and dry erase board to make notes and calculations. A basic calculator is built into the exam, you do not need to bring a calculator. 1

Transcript of MODULE 1 - The basics -...

MODULE 1 - The basics

#1 Test taking strategies.

The following section is not required portion of the salespersons curriculum, it is offered to

advise the salesperson candidate with basic test taking techniques only. The responsibility to

study and prepare for the salesperson exam rests solely with the candidate.

None of the material in test taking strategies section of the textbook is the basis for any

particular exam question. The material is this section is not part of the exam.

As of April 1, 2016 the Massachusetts real estate salesperson exam is administered by PSI

Exams on behalf of the Commonwealth nearby testing centers are in Fall River and Boston.

Candidates making exam reservations after March 15, 2016 should visit psiexams.com or call

800 733-9267.

Part One - General Section - 80 questions,

Part Two - Massachusetts Law Section- 40 questions.

Basically, 70% is a passing grade.

Each part of the exam is administered separately. 150 minutes for the first part, 90

minutes for the second part.

If you pass, you’ll only be told that you’ve passed. If you fail, you’ll be given your score. It is

possible to pass one part, but not the other, if so you’ll only be required to retake the unpassed

part.

The exam is administered by computer, you will be issued with a writing implement and dry

erase board to make notes and calculations. A basic calculator is built into the exam, you do not

need to bring a calculator.

1

During the exam you can flag questions you have trouble with for further review later. We

recommend however that you select the best answer you can while you are looking at the

question for the first time. Flag those questions you’d like to review if you find yourself with

extra time at the end of the section.

We also recommend taking the General Section sample test provided by PSI Exams here:

http://www.psilearningacademy.com/real-estate-salesperson-and-affiliate-broker-practice-e

xams/

In our experience the best time to take the sample exam is three-quarters through your

preparation time window. The exam will give you a good feel for the manner in which the

questions will be asked and guide you to parts of the curriculum you may wish to focus upon. If

you’ve been getting 90% or more on the sample questions in the textbook, don’t be surprised if

you score less than 90% on the sample exam.

Don’t worry, you still have time to study.

However, if you do very poorly on the sample exam now would be the time to reschedule your

exam reservation.

Note: There is only one sample test provided by PSI. Consequently there is little upside to

taking it twice. There is no PSI sample test for the Massachusetts portion of the test.

Lastly, always remember to read the whole question. Understand exactly what the question is

asking and solve only for the question asked. Any question left blank will be marked wrong.

#2 What is real estate?

There are two types of property: personal property and real estate.

2

Real estate, aka real property or realty, is land and certain items attached to the land. The

owner of real property has certain rights of ownership: ability transfer ownership, administer,

loan against and lease.

Most importantly an owner enjoys: possession, control, quiet enjoyment and disposition.

Personal property are moveable items like furniture, the bright line of difference is the nature by

which an item is attached to the land, with exceptions noted below. Personal property aka

personalty or chattel may also be sold by a receipt or bill of sale. Real estate is sold by deed.

As a general rule: items permanently affixed to real estate (land or building) are real estate.

Ask these questions:

How is the item attached to the real estate?

Is the item one of a kind or special built for the location?

What was the intent of the owner?

Can the parties agree to include the item inside or outside the real estate transaction?

Exemptions.

Crops or emblements. Can be removed by the seller and are considered personal property. The

harvest of the crops can also occur after the close of a real estate transaction.

Trade equipment or fixtures. The classic example are the chairs, sinks and cabinets of a barber

shop.

Consequence Cube.

What exactly is real estate and what is personal property can often be subject to dispute. As real

estate professionals it is our responsibility to foresee this potential conflict in the service of our

clients.

3

Question: A single family home with a concrete patio in the backyard is sold. The seller

installed a handmade cobblestone fireplace mortared on the patio. Is the fireplace real estate or

personal property?

A very large stone sits at the end of a driveway and is inscribed with the last name of the seller.

Is the stone real estate or personal property?

Consequently, a listing agent should always discuss with the client items that may be

misconstrued. Conversely a buyer agent should always seek to define what exactly is real estate

and what is personal property. Never assume that all parties have the same understanding.

State and write the obvious.

Real property rights are grouped as a bundle.

Surface rights: right to build and plant crops. Also the right not to have an abutting property

destabilized the subject property.

Air rights: to use the vertical airspace, subject to local, state and federal regulation.

Appurtenances: rights of access (beach rights)

Mineral rights: if minerals are vertically removed they become personal property (Law of

Capture). Mineral rights may be severed and transferred from ownership of the land surface.

Riparian rights. Use of water by a lake, river or similar body of water for recreation and

agriculture. On navigable water the rights extend to the water’s edge. On non-navigable water

rights extend to mid-point of water.

Littoral rights. Similar but in this case the body of water would be very large, like the Atlantic

Ocean or the Great Lakes. Rights end at the mean high water mark.

Methods of measurement of real estate.

4

Metes and bounds - metes are measured in feet from a known point, like a rock. Bounds is the

compass direction. Measurement returns to the point of beginning aka POB.

Lots and blocks - recorded plat plan of a subdivision. Street grid creates blocks, the divided by

lots.

#3 How real estate is owned.

In the US land is owned by individuals in a format called the allodial system. Pure allodial land

is not subject to government authority of any kind, as such, no such pure allodial land exists in

the US. In the United Kingdom, especially England and Wales all land is held by the Crown, a

vestige of the feudal land system. France disposed of the feudal land system as a result of the

French Revolution in the 1790’s.

Today, real estate ownership is owned by interest in an estate which defines the rights and

limits of the ownership.

Freehold estates are ownership. Non-freehold estates are possession.

Types of freehold estates.

1) Fee, fee simple, fee simple absolute. The type of estate interest that theoretically is not

subject to restrictions, hence it is the best form of ownership that can be granted from the

grantor to the grantee. The law assumes all estates are Fee unless otherwise noted.

2) Life estate. Three types:

a) Life estate in reversion. A grants to B, when B dies, estate reverts back to A.

b) Life estate in remainder. A grants to B, when B dies estate goes to X. X is the

remainderman. X is always named by A at the establishment of the life estate.

c) Pur autre vie (for the life of another). A grants to B, when Y passes, estate goes

to X. X is the remainderman, originally named by A. The life tenant B is

prohibited from laying waste to the property and must keep real estate taxes

current.

5

3) Fee simple subject to condition subsequent - title transferred upon condition a certain

activity does not occur in future.

4) Fee simple determinable - title transferred upon condition a certain activity continues.

An original property owner can file an action for forfeiture if a new owner violates the

condition subsequent or fee simple determinable.

Types of non-freehold estates.

1) Leasehold or lease. Renting for a fixed term. A leased fee, is a property held in fee

which has been leased.

2) Tenancy at will or tenant at will. Renting month to month.

3) Tenancy at sufferance. Remaining in a rental unit beyond a lease term.

OR or EE

A blankOR gives something. A blankEE receives something. Grantor gives title, grantee

receives it.

Title held by an individual such title is called severalty.

If a corporation, profit or nonprofit owns property, the corporation is considered a single

individual. Title can also be owned by two or more individuals, these forms of ownership are

commonly referred to as a tenancy but in this instance the tenancy is ownership and should not

be confused with the common usage of the term tenancy to connote renting.

Types of multi-party ownership.

6

1) Tenancy by the entirety. Reserved for married people. The interest cannot be divided

during the term of the marriage. Upon divorce parties become tenants in common. Upon

death of a spouse, the surviving spouse takes title as a fee simple estate aka survivorship.

2) Tenancy in common. Each owns the property in a separate but undivided interest, no

survivorship. In other words, if party A dies, party B does not inherit the interest of party

A. The interest of party A is granted to the heirs of party A.

3) Joint Tenancy. Equal interests, equal possession, acquired at the same time, by the same

deed. Upon death of owning party, the remaining parties acquire the interest equally, not

the heirs.

4) Syndication. Commonly referred to as a Real Estate Investment Trust or REIT. This is

basically owning stock in a real estate holding company.

5) Condominium. From the Latin con “together with” and dominium “right of ownership”.

The unit deed is recorded at the time of sale of a single unit. The master deed defines the

entire condo complex and governance. Single unit ownership with a joint undivided

interest and responsibility in the defined common areas. A buyer receives a 6D

certificate from the condo association stating that the condo unit is current with all condo

fees.

6) Cooperative. A corporate entity which owns the entire real estate, one deed, one

mortgage, only. Each “owner” is granted stock in the corporation and a lease for the

particular co-op unit.

#4 Transferring real estate ownership.

A deed written intent to transfer ownership. The Habendum clause “to have and hold” defines

the estate granted.

Purchase and Sale. The common real estate transaction often involving but not requiring real

estate agents and brokers.

Dedication. Voluntary gift of land to the government.

7

Eminent domain. The taking of land by government through a process called condemnation,

the government must prove that the land is needed for a public purpose. Not as common today,

but heavily used to construct the Interstate Highway system and to redevelop neighborhoods -

see the West End of Boston.

Foreclosure. The forced sale of an asset to satisfy a private debt.

Tax sale. The forced sale of an asset to satisfy a tax debt or back taxes. Aka a Sheriff's sale.

Escheat. When in the absence of heirs property ownership reverts to the state.

Involuntary alienation. Loss of ownership due to lack of funds: taxes, court judgements,

bankruptcy, suit for partition.

Adverse possession. Acquiring the land of another by open, continuous, and uninterrupted use

that is hostile and adverse to the owner. Private land will often be blocked off from public

access once a year to interrupt access. By use of a method called tacking claimants can defeat

the interruption efforts of the owner.

Will. Bequeath and devise real estate. Bequest and leave as a legacy personal property. The

person making the will is known as the testator, a will must be witnessed by two individuals not

named in the will. If an individual passes without a will the person is said to be intestate. The

Probate court will administer the property and distribute the property via the common law rules

of descent. Dower rights apply to the surviving spouse, male or female.

Accretion. The addition of net real estate by mother nature - wind and water, the additional land

is alluvium. Erosion the subtraction of net real estate by mother nature.

#5 Types of Deeds

8

General Warranty Deed protects buyer against any prior claim of title that occurred during or

before the seller’s term of ownership.

Special Warranty Deed protects buyer against any prior claim of title that occurred during the

seller’s term of ownership.

Quitclaim Deed, the most common for basic real estate transactions, transfers grantor’s

ownership interest in a property such as it existed at the time of closing. Provides grantee little

protection - hence the need to investigate the chain of title and secure title insurance, which in

Massachusetts must be handled by an attorney. Title insurance is needed even though under the

covenant of seisin the seller is asserting that they have not promised the property to any other

party.

Since the deed is evidence of title it is recorded at the Registry of Deeds, the government

collects a tax via the use of a Deed Stamp to fund the Registry. At closing the Deed Stamp is

typically paid for by the seller. Recording a deed at the Registry is not required for it to be valid

however doing so serves as constructive notice to all parties with or without actual notice of the

transaction and protects grantees against claims of title.

Title insurance is an type of insurance that protects against a possible defect or cloud on title.

Efforts to remove defects or cloud on title is called action to quiet title. Color of title is a term

used to describe ownership of title.

Registered Land in the Commonwealth is a different form of title which with the blessing of the

Land Court connotes indefeasible title. Registration of land provides the same or higher level of

grantee protection as does title insurance. Registration of land is often used to quiet title.

#6 Claims and restrictions on ownership.

Although you hold the color of title other parties may still file claims against your ownership aka

encumbrances.

9

Liens are a type of encumbrance representing a debt secured by an ownership stake in the

property.

Financial encumbrances:

1) A mortgage is a voluntary lien. While the mortgage lien is in place the mortgagor is said

to have equitable title, until the mortgage lien is released at which time legal title is

obtained.

2) A tax lien is an involuntary lien. Property taxes are factored by the value of the property

(ad valorem) and collected quarterly in most towns. A tax lien holds priority over any

other lien. If a property is sold by the town for non-payment of taxes, the prior owner has

six months to repay the taxes plus interest under the right of redemption.

3) Special assessments is a charge paid over time for the targeted expenditure of public

funds, the most common is for the improvement of roads and sewer. The improvement is

known as a betterment.

4) Mechanics lien. Protection for contractors and material suppliers.

5) Attachments. Legal seizure of a defendant's property to prevent asset transfer or hiding

of assets. Lis pendens from the Latin, pending action, is not a lien itself but notice of

pending legal action and hence it is a cloud on the title.

6) Judgements. Final determination by a court of a debt. Failure to pay a judgement may

result is the sale of the asset.

7) Super lien. Applies to unpaid condo fees and holds a position superior to any mortgage,

can force the sale for unpaid condo fees.

Non-financial encumbrances.

1) Easement. An irrevocable right “running with the land” which survives sale of the

property. “A right held by one property owner to make use of the land of another for a

limited purpose.”

a) Easement appurtenant. From the French ease of tenant and also the most

common type of easement is access to travel over the property to access another

property when the lots of property are adjoining. The dominant tenement is the

10

party with the right and receives the benefit aka an appurtenance. The

subservient tenement is the property which grants the easement/encumbrance.

b) Easement in Gross. Is a personal written right to granted to a non-abutter to

access land, for instance for hunting and fishing.

2) License. A personal, non-transferable, revocable permission to use the land of another.

3) Encroachments. The unapproved use of land by another. For instance, Mary

“accidentally” widens her driveway by paving over part of Bob’s land. Often resolved or

discovered by survey.

4) Covenants. Private agreements, usually in a neighborhood, to uphold certain visual or

value standards: each home shall have at least a garage or front porch. “Racially-based

restrictive covenants are not, on their face, invalid under the Fourteenth Amendment,”

under the 1948 US Supreme Court Case Shelley v Kraemer case.

11

MODULE 1 - Quiz

1. A ventilation fan is built into a wall, the unit is:

a. chattel b. real estate c. tenant property d. up for negotiation

2. A former owner returns to harvest annual crops, he is:

a. stealing b. trespassing c. collecting his personal property d. poaching

3. At low tide a property owner tells people walking on the beach to move along, at issue is:

a. sanding rights b. littoral rights c. riparian rights d. privacy rights

4. From Nicks Rock, to Smelt Pond, to Spooner Pond to Triangle Pond and back to the POB

is an example of: a. lots and blocks b. Kings Rule c. metes and bounds d. government land survey

5. Person A grants an estate to B. When B dies, X takes over the estate, this is an example

of: a. pur autre vie b. remainderman c. common law d. life estate in reversion

6. X sells an estate to Y with no strings attached, this is an example of:

a. life estate b. free simple estate c. fee d. simple absolute estate

12

7. Tenant B stays beyond his lease, an example of :

a. constructive eviction b. non-freehold estate c. tenancy at sufferance d. tenancy by the entirety

8. X and Y own property together, X dies and B inherits X share, the real estate is owned in:

a. tenancy by the entirety b. tenancy in common c. joint tenancy d. severalty

9. The government forces the sale of a property for the construction of a new civic center:

a. redevelopment b. re-zoned c. eminent domain d. foreclosure

10. X dies his estate reverts to the government:

a. adverse possession b. escheat c. involuntary alienation d. tax sale

11. Uncle Bob gives Nephew Ray a boat upon Bob’s death:

a. bequeath b. grant c. bequest d. devise

12. Q buys property and receives deed protecting him against events during X’s term of

ownership but encroachment began before X owned the property Q should have sought a: a. special warranty deed b. quitclaim deed c. general warranty deed d. de-registered land

13

13. Not a lien, but notice of a possible lien in future: a. mechanics lien b. lis pendens c. encumbrance d. betterment fee

14. Mary is allowed to drive over Sue’s land to access a boat dock on a non-abutting parcel.

Mary benefits from: a. shared driveway b. easement in gross c. encroachment d. dominant tenement

15. In selling a condo what proves that all the condos fees are current?

a. 21E certificate b. title 5 voucher c. the HUD d. 6D certificate

14

MODULE 2 - The law

#1 Real estate brokerage laws and practice.

The practice of real estate in Massachusetts is overseen by the Massachusetts Board of

Registration of Real Estate Brokers and Salespersons.

Established in 1960, the five member board serves without compensation and promulgates and

enforces real estate law that has been enacted by the legislature. An critically important principle

to remember is that a licensed agent cannot legally operate unless affiliated with an agency, nor

work for more than one agency at a time. A broker however, may work independently of an

agency as a sole proprietor. Anyone, licensed or unlicensed may own an agency, but they must

employ a Broker of Record.

Technically, an agent has no clients, all clients are connected to the agency only. The broker of

record is held liable for acts committed by agents affiliated with his agency under the concept of

vicarious liability. If an agent departs one agency for another they very may well not be able to

transfer buyer clients and most definitely will not be able to transfer listings.

Board membership:

a. One of the five members shall be a chairperson appointed by Governor.

b. Three members are licensed brokers with a minimum of seven years of experience, as

a broker.

c. Two members of the general public.

Board members serve five years, each year one member’s term expires. They convene at least

four times in a calendar year, a three member quorum is required.

Website: http://www.mass.gov/ocabr/licensee/dpl-boards/re/

15

All licenses are issued for two years, however the first license runs from the date of passing

the exam until the third birthday on a prorated basis. An individual may hold only one

license at a time and such license must be posted in a public place at your place of business.

Licensees who have an inactive license must contact the board to seek reinstatement.

An agent is obliged to constrain their practice of real estate to transactions and listings for which

they have a reasonable proficiency.

Board penalty for acting as an unlicensed real estate agent: up to $500. What constitutes

unlicensed? Acting: for a another, for a fee.

No commission is due, unless and until the transaction closes, according the 1975 SJC decision,

Tristram's Landing Inc. v Wait. Buyer’s broker shall only be due commission, if they are

determined to be the procuring cause of the sale.

A salesperson license does not allow a broker to arrange the purchase of real estate in an

investment pool.

A broker who wishes to engage salespersons to work for them must also acquire an agency

license. The most common structure for a real estate agency is a Limited Liability Company or

LLC. All real estate agencies must carry errors and omissions liability insurance.

No broker or agent should be engaged in the unlicensed practice of law. Whenever a client asks

if they should seek legal counsel, the answer should always be: Yes.

In the event of death, disability or severance of the broker of record, the brokerage may

continue for one year while it secures a new broker of record. In the event of a sole

proprietorship, the Board may grant a temporary license for one year (in practice this license is

often granted to the attorney handling the estate of the deceased).

16

Salesperson license requirements:

a. 40 hour salesperson class.

b. Pass the salesperson's exam.

c. At least 18 years of age.

d. Good moral character. The student handbook requires three upstanding citizens to verify

a candidate's good moral character. DO NOT ask classmates or people at the test

center to sign the handbook on your behalf.

e. If previously licensed, an individual must activate and resolve any issues with the

previous license and may not simply begin the process again.

f. A resident agent must maintain a legal address in the Commonwealth.

Non-residents may be agents if they empower the Board to receive legal summons on

their behalf.

Broker license requirements:

a. 40 hour broker class.

b. Be actively affiliated as a salesperson with a broker(s) for three years.

c. Pass the broker exam.

d. Post a $5000 surety bond.

e. Good moral character (see above).

Exemptions:

a. Attorneys may become brokers but are not required to take class or exam and may

upon posting a $5000 surety bond, letter of good standing from the Board of Bar

Overseers and licensing fee become a licensed broker.

b. Licensed brokers and salesperson from states that have reciprocal licensing agreements

with Massachusetts, subject to the licensing fee.

c. No license is needed to sell your own property, salaried property managers, auctioneer,

attorney on behalf of a client, individual acting under a legal power of attorney and the

executor of an estate.

17

#2 Board procedures.

The board may conduct a hearing on a matter of its own choosing or as a result of a complaint.

a. agents or broker must be given 10 days written notice if they are to be the subject of a

hearing

b. The board may subpoena records and witnesses.

c. Licensee may have legal counsel, but presence of legal counsel is not a legal entitlement.

d. Appeals must be filed within 20 days.

e. While under appeal a license must be surrender to the board within 7 days of notice by

the board.

Board may suspend or revoke a license:

1. If obtained by false representation

2. Represented more than one party in a transaction without informed consent of all parties.

3. Failure to account for funds in escrow (trust account).

4. Sharing commissions with a non-licensed individual who was required to be licensed.

5. Receiving an undisclosed commission.

6. Inducing any party to break a contract for the personal benefit of the agent/broker.

7. Commingling funds/uncashed checks. Mixing clients fund with any other funds.

8. Failing to produce a copy of a real estate contract for client.

9. Accepting a net listing which is an agreement to sell for a set amount and agent retains

balance for commission.

10. Acting in dual capacity as agent and undisclosed principal.

11. Proved violations of the Mass Fair Housing Law - immediate suspension.

#3 Disclosures and Requirements of Brokerage.

The following disclosures and requirements are relative to brokerage law, additional disclosure

relative to building materials and conditions of particular properties are covered in Modules 3

and 4.

18

All advertisements in print or elsewhere must name the brokerage or broker of record. No blind

advertisements. Listing the agent name is not sufficient, the brokerage must be named. Out of

state real estate marketed in the Commonwealth shall be registered by the Board and represented

by a licensed Massachusetts broker.

Broker must obtain permission to advertise listings and may not post sign without express

written permission.

No discriminatory advertisements are allowed. Records or advertisement must be kept for

three years. Bait and switch advertisements are not allowed.

Any financial interest of a broker or agent (or family/business partner) in any property subject

to sales, lease, rent or mortgage shall be fully and prominently disclosed in writing to all parties.

When in doubt disclose, even if the interest is indirect or minimal.

Escrow funds (trust accounts). One of the primary responsibilities of a broker is to hold in

escrow clients funds pending the sale of real estate. The seller brokerage is legal holder of such

funds and the broker for the seller hold the funds of the buyer in broker’s escrow account.

Funds in the escrow account shall not be commingled with any other funds of any kind. A

single escrow is sufficient for a brokerage, a separate account per transaction is not required.

Note: A salesperson shall never hold client funds. Clients funds are subject to immediate

deposit and hold no relation to commission that may or not be paid.

Escrow fund records shall be maintained for three years and are subject to inspection by the

Board at anytime. Disputes relative to escrow must be settled by agreement of the parties or

court order. Broker shall not resolve the dispute.

19

Three types of listing information:

a. Must be disclosed - known hidden defects (red flag issues), material facts, must be

disclosed.

b. Must not be disclosed - information about the client not material to the listing.

c. Must be disclosed upon questioning - stigmatized property. Note, the fact that a prior

occupant had a disease which would be highly unlikely to be transmitted to new occupant

is not a stigma, and shall not be disclosed, even if asked.

Agents may not withhold a material fact, nor may they over exaggerate or puff up the listing

aka puffing.

Withholding a material fact is a misrepresentation. An agent may not withhold a material

fact at the request of the seller.

#4 Agency Disclosures.

At the first personal meeting with a prospective buyer or seller during which the discussion of a

specific property is mentioned, the agent/broker must provide notice (provided by the Board)

which discloses the relationship. At this meeting the agent/broker should also disclose in writing

any financial interest they personally (or family/business partner). Like escrow records, these

disclosure forms shall be maintained for three years.

Rental fees must also be disclosed at the first personal meeting and a form clearly describing

the nature and amount of the rental fee be presented for client signature at the first meeting

discussing a specific property.

Under the Law of Agency, the broker/agent acts a fiduciary to the client. Fiduciary duties are:

a. Obedience. Follow lawful instructions.

b. Loyalty. Act in best interest of client. Client interest placed first.

20

c. Disclosure. Share all material information with client.

d. Confidentiality. Withhold certain information from others, for instance the lowest price

a seller would accept.

e. Accountability. Secure and account for all funds.

f. Reasonable care and diligence.

Further, the agent/broker cannot bind the principal. The scope of an agent/broker’s authority

is limited, the agent/broker only represents the principal as a special agent, not a general agent.

All transactional decisions (how much to list and sell the property, accept which offers) rest with

the principal. As noted, an agent may not withhold a material fact at the request of the

seller. All offers are to be presented forthwith to the principal.

Types of Agency.

a. Seller Agent. All fiduciary duties apply.

b. Buyer Agent. All fiduciary duties apply.

c. Disclosed Dual Agent. Broker may work on behalf of both parties with the informed

written consent of the parties. Loyalty is divided.

d. Designated Agent. A broker may appoint an agent of the firm to represent the buyer for

instance, especially if the listing agent also works for the broker. In such a case the

broker is a dual agent. Written consent of the parties is required. Professional driver on

a closed course, don’t try this at home.

e. Facilitator. An agent that does not represent either the seller or the buyer.

Types of Listings.

a. Open listing - held by more than one agency. For instance Boston rental listings

distributed to multiple rental agencies.

b. Exclusive agency - only one agency but owner can sell without the named agency and

not pay commission.

c. Exclusive right to sell/lease - all sales must go through named agency and commissions

paid. Most, not all MLS listings, remember the listing itself is not an offer, only a public

notice.

21

d. Entry Only. Broker enters seller's listing information into MLS for nominal fee and

takes no further action on behalf of seller. Seller acts as FSBO (for sale by owner)

thereafter.

To create a listing, a listing contract must be completed between the seller and the listing agency.

The commission, or brokerage fee, will be defined in the listing agreement.

Minimum Listing Agreement components:

Name the parties, identify the property, define the broker’s authority (often limited by time) and

compensation (almost always as a percentage of final sales price), establish a listing price

The listing agreement is the primary instrument detailing the relationship between seller and

brokerage. However, brokerages may also engage buyers in buyer representation agreements,

including exclusive right to represent agreements.

Hopefully, after the advertisement of a listing an offer will be made, that offer is often more

formally called an Contract to Purchase.

Minimum Offer requirements:

1. Identify the property, deed type, personal property inclusions and exclusion,

contingencies (typical for mortgage, home inspection and Title V), closing date, detail of

total offer amount, earnest money deposit.

Most offers include four documents: the offer, a copy of the deposit check, a copy of the

consumer disclosure and a mortgage letter.

22

MODULE 2 - Quiz

1. Brokers who serve on the Board of Registration must have how many years of

experience? a. 5 b. 3 c. 7 d. 10

2. How many days notice must an agent receive prior to a board hearing?

a. 5 b. 10 c. 7 d. 30

3. Who appoints the chairperson of the Board of Registration?

a. Board of Realtors b. Congress c. Governor d. General Court

4. How many members are required to form a quorum of the Board of Registration?

a. 3 b. 5 c. 2 d. 7

5. A broker who employs salespersons must obtain a:

a. waiver b. broker of record c. an agency license d. a LLC

6. A previously licensed individual must:

a. take the class and exam again b. contact the board to seek reinstatement c. pay the fee d. get errors and omissions insurance

23

7. Non-resident agents: a. Keep a Massachusetts address b. Empower the Board to receive legal summons on their behalf c. Hire a lawyer d. Cannot be licensed

8. Brokers must secure a bond of how much?

a. $7500 b. $10,000 c. $5000 d. $2000

9. Good moral standing is demonstrated by how many people signing your handbook?

a. 2 b. 3 c. 4 d. 5

10. No license is required for:

a. securities b. property manager c. out of state agents d. to sell out of state land

11. If the Board suspended a license, it must be surrendered within how many days?

a. 5 b. 7 c. 10 d. 20

12. A net listing:

a. Benefits the seller b. Benefits the buyer c. Benefits the both buyer and seller d. Is a conflict of interest

13. Violations of the Mass Fair Housing Law results in:

a. a board hearing b. $500 fine c. $1000 fine d. immediate suspension

24

14. Uncashed checks are examples of: a. escrow b. commingling c. IOLTA d. commissions

15. A house for sale is known for past drug activity should be disclosed:

a. always b. never c. if asked d. if sellers approves disclosure

16. An agent tells a buyer the lowest price the seller would accept. Agent violated:

a. Obedience b. Loyalty c. Disclosure d. Confidentiality

17. Homeowner lists home with broker, homeowner sells home but does not owe

commission, this is an example of: a. exclusive right to sell b. open listing c. exclusive agency d. fsbo

18. Agent must present broker disclosure:

a. when the first showing a house b. at first meeting to discuss a house c. before the open house d. after the open house

25

MODULE 3 - The money

#1 Contracts.

Contracts are enforceable agreements between two or more parties. Often a meeting of the

minds occurs before an offer is made in writing. All real estate contracts must be in writing

under the Statute of Frauds. A verbal contract is not enforceable.

Components of contracts:

a. By mutual and voluntary agreement via signature there must be an offer and acceptance.

b. Frequently an offer requires a response within a certain time, this is often referred to as:

time is of the essence.

c. The exchange of something of value, commonly referred to as consideration. The

market value of the consideration is not important, only that the seller deems the value

acceptable.

d. The contract must be for a legal product or service.

e. All parties must be competent to enter into the contract.

f. An atmosphere of reality of consent must exist, which must not include:

misrepresentation, fraud, undue influence or duress.

A contract once completed and closed is called executed. Completed but not fully performed

(closed) is executory. Contracts can also be implied or expressed. Expressed contracts

prohibit any additional implied provisions. A contract may be assigned or transferred to another

party.

A contract can exist in four states:

a. Valid, binding on the parties.

b. Void, no legal force, not binding.

c. Voidable, not yet void, but susceptible to challenge.

d. Unenforceable, for instance a verbal contract or a contract with a minor.

26

Contract configuration.

a. Unilateral. Party A is obliged to act when and if Party B performs a certain act. Option

to buy.

b. Bilateral. Party A and party B are required to act in tandem. For instance for the

exchange of goods or property.

Less than perfect outcomes.

a. Recission. Typically the buying party informs the seller within three business days.

b. Court orders one party to perform their portion of the contract, a court ordered legal

remedy - specific performance.

c. Party seeks funds to refund damages suffered.

d. Liquidated damages are damages predetermined by contract, should the one party fail to

perform.

e. Forfeit. Buyer surrenders good faith deposit or earnest money.

A common written unilateral contract is an option to purchase contract in which the Optionor

is the party who currently owns the parcel. The optionor gives the right to purchase the parcel at

a future date to the Optionee, who may or may not exercise the option. Similar to the right of

first refusal, but in a right of first refusal the owner retains control of market timing.

Often an option will be taken to grant the buyer sufficient time to conduct due diligence relative

to the suitability of the parcel. For instance a developer may seek permits.

Buyers can also protect themselves by including contingency clauses into offers to purchase.

For instance, a mortgage contingency clause.

Offers and counter offers are critical function of a salesperson and broker. Once an offer is

made, with stated time limit, the offer may be accepted by signature, rejected or counter offered

and time may be of essence or an express deadline may be included. Importantly, even if the

original offer deadline has not expired, the moment a rejection or counteroffer is made, the

original offer cannot be subsequently be accepted by the seller.

27

#2 Mortgages and Finance.

In common terms you hear the phrase: “We got a mortgage to buy the property.” In fact, the

buyer gave a mortgage to buy the property and the buyer is the mortgagor and the lender is the

mortgagee, which receives the mortgage in exchange for your promise to repay or ability to

collect the collateral in case of default. Promising the property but maintaining possession of the

property is known as hypothecation.

A promissory note is primary evidence of debt. Promissory notes can be bundled and sold in

the secondary mortgage market, a Note may or may not include a prepayment penalty clause.

A title theory state (Massachusetts) in which the mortgagor (borrower) retains equitable title

but gives legal title to the mortgagee (lender). In lien theory states, the mortgagor retains both

legal and equitable title.

Clauses in the Note.

1. Acceleration clause is the legal tool which allows a lender to foreclose prior to the

agreed upon closing date of the Note.

2. Defeasance clause allows the note and any subsequent lien to “be defeated” should the

terms of the mortgage be satisfied or discharged.

3. Due on sale clause, which requires satisfaction of the note prior to sale of the property.

4. Subordination clause allows the mortgagor to obtain future financing, like a HELOC.

Home Equity Line of Credit.

5. Estoppel clause bars the borrower from disputing the terms of the loan if the note is

transferred to a different lender.

Types of mortgages and payments:

1. Second mortgage. A second debt which is a lien subservient to the primary Note.

28

2. Private mortgage insurance or PMI required in situation of less than 20% equity (many

federal loan programs are exempted). As with any mortgage, the lender may require a

certain loan to value (LTV) ratio, the higher the ratio the more risk. Too much risk and

the lender may require PMI.

3. Purchase money mortgage. Fancy term for seller financing.

4. Balloon mortgage. Payments of interest and some principal, with total balance due at

end.

5. Package mortgage. Includes both real property and personal property.

6. Blanket mortgage. Covers multiple parcels allowing for partial release, via the partial

release clause, of legal title upon partial payment.

7. Construction loan. Funds are released to a developer upon the achievement of certain

construction benchmarks.

8. Reverse mortgage. Acts like an annuity paying the “owner” a fixed sum each month

until they cease to live in the property. Must be 62 plus to qualify.

Types of closings/Mortgage transfers..

a. Subject to original mortgagor is responsible for debt, even if new buyer defaults.

b. Assumption - both new and old buyers are responsible.

c. Novation - a new note between new buyer and lender, previous owner released.

Government loan programs.

The Department of Veteran Affairs guarantees the loan offered by a private lender to a certain

limit for owner occupied 1-4 family homes with up to a 100% financing or no down payment

required. Rates are capped. The VA appraises property and issues a Certificate of Value (CRV)

and a Certificate of Eligibility based upon the veteran's ability to pay. Loan can be assumed by

veteran or a non-veteran.

The Federal Housing Administration insures the loan offered by a private lender to certain

limit for owner occupied 1-4 family homes up to 97% value of first 25K in value and 95% of

remaining value. Rates are set by the market. A HUD appraiser estimates the value to determine

29

the maximum insurable loan value. The lender may charge points. Loan can be assumed by

buyer qualification.

Secondary mortgage market.

The secondary mortgage market is a means by which individual mortgage loans are bundled

together and sold as mortgage-backed securities. Fannie Mae or the Federal National

Mortgage Association, formerly a government agency, is the primary entity that buys mortgages

from private mortgage lenders for the purpose of bundling them into a securitized product.

Freddie Mac also buys private conventional mortgages. Ginnie Mae specializes in FHA and

VA mortgages.

#3 Appraisals.

An appraisal is an estimate or opinion of value. An appraisal does not set value.

Value is influenced by demand, utility, scarcity and transferability. Value can be influenced by

governmental action, the physical environment, economic factors and social interactions of

people.

Value is influenced by various economic pressures.

a. What is the highest and best use of a parcel. The greatest net return for the owner. No

three acre parking lots in downtown Manhattan.

b. Substitution. How much to acquire a similar or near equal property.

c. Conformity. Will the use remain constant for the foreseeable future?

d. Contribution. The net return on value added. A dock might cost $30K to build but add

$75K to the market price of a waterfront property.

e. Anticipation. Predicted impacts on value over time.

f. Competition. Direct relationship between profit levels and market entry.

g. Point of diminishing return. Avoid owning the nicest house of the street, especially if it

does not conform with uses in the foreseeable future.

30

h. Plottage. The purchase of multiple parcels (assemblage) to form a larger parcel. See

Boston University. The whole is greater than the sum of the parts.

Techniques to measure value:

a. Market value. The amount likely to be paid as market price in an arm’s length

transaction.

b. Cost approach to value.

c. Assessed value for taxation.

d. Liquidation value for the purpose to convert the property to cash.

e. Value in use, the value of holding a property.

f. Insurance value. What you might get in the worst case scenario.

These techniques are employed in full or in part by using one of three approaches to value:

1) Sales Comparison Approach.

2) Income Approach.

3) Cost Approach.

Sales Comparison, for single family homes.

Used to estimate market value of single family homes. Locating 3-5 similar, recently sold homes

and substituting estimated values to equalize for feature differentials. As a real estate

professional you’ll use this approach most often by employing a comparative market analysis

or CMA.

Income Approach, for investment property.

Value is determined as a derivative of annualized net income. Capitalization of the net income

reflects the final value. Using the following formula:

net operating income = (market value x cap rate)

$700,000 = $6,363,636 x 11%

31

Cost Approach, often used in non-profit and government applications. Formula:

(Estimate value of land + cost to reproduce existing improvements and buildings) - deduct

depreciation

#4 Renting and Leasing.

A lease is a contract between the lessor/owner and the lessee/tenant which establishes

possession but not title for a period of time in exchange for consideration/rent. The owner

retains a reversionary right of possession.

Three types of leasehold interest:

1) tenancy for years - common lease.

2) tenancy at will - often verbal aka TAW, can be terminated with 30 day notice.

3) tenancy at sufferance - lessee remains without permission beyond the term of the lease.

Lease essentials:

a. It must be in writing

b. Reasonable description of premises.

c. State term, not to exceed 99 years

d. State the term rent and monthly rent.

e. Clearly indicate the intent to lease.

f. Be signed by both parties.

A lease may be transferred if allowed under the terms of the lease by sublet, unlikely in

Massachusetts. It can also be terminated, the most common form of termination is eviction by

the lessor when the lessee has failed to pay rent. A 14-day written notice must be given to

commence an eviction. Tenant has ten days to pay arrears. Constructive eviction occurs when

the tenant departs the property because it is no longer fit for habitation. A lease may also be

terminated for eminent domain, mutual agreement, default, mortgage foreclosure, and

destruction. Death of a party to the lease does not terminate the lease unless stated in the lease.

32

Leases come in several forms the most common forms are:

a. Gross lease: fixed rent, owner pays all expenses. Common apartment lease, sometimes

used in smaller commercial leases.

b. Net lease: in addition to the base rent the tenant pays a portion of operating expenses of

building.

c. Percentage lease: base rent plus a percentage of gross sales. Often used in shopping

centers.

d. Graduated lease: rent amount moves up/down during term by a fixed schedule.

e. Index lease: rent amount fluctuates with a standardized factor, like the Consumer Price

Index, the escalator clause in the lease defines the fluctuation.

f. Reappraisal lease: rent increases are based upon appraised value.

g. Sale-leaseback: Owner sells property and leases back property at the same time.

h. Ground lease: long term leasing the land only. Any improvements (fast food restaurant)

become property of the owner at the end of the lease and are held in security for the lease.

i. Vacation rental: Under 100 day, exempt from many laws relative to leases.

Leases come with implied understanding of quiet enjoyment to protect the tenant and

prevention of waste to protect the owner. Ordinary wear and tear cannot be held against tenant,

only a decrease in value by deliberate act.

Often the property owner will require a security deposit to lease the property, the intent of the

security deposit is to prevent waste. Security deposits for residential leases traditionally do not

exceed one month’s rent and must be held in an interest bearing account by the landlord. The

tenant is entitled to an annual payment of interest from the landlord. To establish a baseline

understanding of the property condition, the owner must present tenant with property condition

statement within ten days of commencement of lease.

33

MODULE #3 Quiz

1. When all parties agree but nothing is yet on paper:

a. agreement in spirit b. meeting of the minds c. mutual consent d. offer and acceptance

2. A contract must include the exchange of something of value which is also known as:

a. money b. love and affection c. consideration d. earnest money

3. A contract is completed but not closed:

a. executed b. executory c. voidable d. express

4. If directed to complete a contract under court order:

a. unilateral b. specific performance c. bilateral d. implied

5. Optionee:

a. can buy real estate in the future b. can sell real estate in the future c. holds the right of first refusal d. awaits acceptance

6. A promissory note is:

a. evidence of title b. evidence of debt c. evidence of a mortgage d. evidence of deed

7. If you don’t pay your mortgage the lender may evoke:

a. defeasance clause b. subordination clause c. acceleration clause d. due on sale clause

34

8. A mortgage which covers multiple parcels allowing for partial release of legal title upon partial payment.

a. package mortgage b. blanket mortgage c. six-pack mortgage d. bundled mortgage

9. A buyer acquires property using the existing mortgage and the original owner is

responsible for the debt: a. novation b. hypothecation c. subject to d. assumption

10. An influence upon value based upon future events:

a. conformity b. substitution c. competition d. anticipation

11. Finding comparable properties and adjusting for material differences:

a. broker price opinion b. sales comparison c. cost approach d. assessed value

12. A landlord retains:

a. reversionary right of possession b. reversionary right of title c. equitable title d. adverse possession

13. A two year lease is for $1000 a month with a 5% monthly payment escalation clause in

year two. What is the term rent? a. $24,000 b. $24,600 c. $26,400 d. $25,200

35

14. How many days written notice must a landlord give before eviction starts? a. 7 b. 21 c. 14 d. 10

15. A tenant must pay for the rent plus other factors of ownership like taxes, this is an

example of: a. gross lease b. net lease c. index lease d. appraisal lease

16. A _____________________ is given by the landlord to the tenant within 10 days of a

tenancy? a. lease b. property condition statement c. accounting of funds d. security deposit interest statement

36

MODULE 4 - The government

#1 Fair Housing.

In Massachusetts there are very few housing applicants that can be discriminated against. In

fact, the only obvious and frequent party facing “discrimination” is college students. College

students may be declined for rental housing simply based upon their status as college students.

But college students are the distinct exception over the decades many protected classes have

secured fair housing protections via federal and state law.

Applicable federal fair housing laws, violators can face severe penalties.

a. Civil Rights Act 1866 passed after the Civil War prohibits discrimination based upon

race.

b. Civil Rights Act 1968 aka the Fair Housing Law bars discrimination based upon race,

color, religion, and national origin in almost all residential real estate transactions.

Gender discrimination was added in 1974.

c. The 1988 Civil Rights Act amendment protected mentally and physically handicapped

and families with school age children. Alcoholics can be considered handicapped.

Illegal drug users are not handicapped. Medical marijuana is source of considerable legal

dispute as states have moved to deregulate it and the federal government has not.

As a result of these laws federal fair housing law the following activities are prohibited:

a. decline a transaction or negotiation solely based upon a membership of a protected class.

b. alter terms based upon the class of applicant include mortgage terms and appraisal.

c. false representation of market conditions and listings.

d. Redlining - limiting beneficial loan terms by geography.

e. Blockbusting - induced panic selling

f. Steering - directing clients to a certain neighborhood based upon ethnicity, race or origin.

37

Consequently choose your words wisely, the following are unacceptable:

family neighborhood

changing neighborhood

“Where are you from?”

Five minute walk

Executive neighborhood

Exemptions:

1) Private sales of a owner occupied home, so long as the seller:

a) Sells no more than three a year.

b) No real estate broker is used.

c) No discriminatory advertising/verbal statements are used.

2) Rental in owner occupied home (up to two unit home) and religious and private

membership clubs, as long as:

a) No real estate broker is used.

b) No discriminatory advertising is used.

Enforcement. Federal penalty can include up to $10K or first violation, $25K for second

violation within 5 years and $50K for two or more violations within seven years.

Lesson in Capsule.

Steering, blockbusting and redlining occurred in Boston in the late 1960’s as official government

policy resulting in real estate agents using blockbusting techniques to generate sales listings.

Recommended reading: Death of a American Jewish Community, by Hillel Levine and

Lawrence Harmon.

http://www.amazon.com/The-Death-American-Jewish-Community/dp/0029138663

38

Massachusetts Fair Housing Laws further extend protections based upon age, sex, marital

status, sexual orientation, veteran status, race/color, religious creed, public assistance status,

ancestry, disability, genetic information, national origin or familial status. Complaints against

Massachusetts Fair Housing Laws are heard before the Massachusetts Commission Against

Discrimination and if found in violation agents face automatic suspension for 60 days and

automatic violation for 90 days for second offense within 2 years.

Tenants with service animals may also not be discriminated against or asked to place a larger

security deposit. They may however be liable for animal damages above and beyond the security

deposit.

Plus, like the federal penalty: up $10K or first violation, $25K for second violation within 5

years and $50K for two or more violations within seven years.

All fair housing laws apply if a real estate agent is used in the transaction or if

discriminatory oral statement or discriminatory written statements (advertising) is used.

The Massachusetts Consumer Protection Act aka Chapter 93A, protects consumers against

unfair and deceptive business acts, passed in 1967 it provides up to triple damages.

#2 Land Use.

The police power of the state includes the ability to regulate zoning as a means of controlling

land use by imposing:

a. purpose of usage: residential, commercial and even the type of commercial use.

b. building height.

c. setback from water, public ways, abutting property.

d. minimum lot size.

39

A property zoning can be considered:

a. a conforming use.

b. a nonconforming use (legal at the time of original use but now re-zoned).

c. Variance. A request made for a minor exemption to the zoning law.

d. Special permit use, an exemption allowed for the public good.

e. 40B. Allows non-conforming use and expedited permitting for projects that create at least

20% “affordable” units. Can only apply in towns that are considered to have less than

10% of “affordable” housing stock.

Duty to Disclose Zoning.

Agents have the duty to disclose zoning if it has a material bearing on the sale or lease of

property. Misrepresentation of zoning could face significant sanction.

Ruling: Agents have duty to exercise “Reasonable Care” in zoning representations

“The lawsuit was brought by a buyer of a hair salon business who relied upon what turned out to

be erroneous information supplied by the listing agent (through information provided by the

seller). The broker represented on the Multiple Listing Service (MLS) and newspaper advertising

that the property was zoned “Business B,” which allowed a hair salon. Further, the broker placed

at the property copies of pages from the town’s zoning by-law that listed hair salons as

“Permitted Business Uses” in the Business B District. The property was not, in fact, zoned for

business use; it was zoned residential, thereby prohibiting the hair salon the buyer wanted to

open at the property. The buyer sued for misrepresentation and violations of the Consumer

Protection Act, Chapter 93A.”

Read more here:

http://massrealestatelawblog.com/2013/04/19/sjc-rules-realtor-may-be-liable-for-erroneous-zoni

ng-info-in-mls/

40

#3 Regulated building materials, environmental laws and hazmat.

The Environmental Protection Agency (EPA) administers the Superfund Law aka the

Comprehensive Environmental Response, Compensation and Liability Act or CERCLA.

Chapter 21E is the Massachusetts Oil and Hazardous Material Prevention Act or State

Superfund and is related to the 1998 Brownfields Act or Act Relative to the Environmental

Cleanup and Promoting Redevelopment of Contaminated Property. The Brownfields Act

has allowed previously contaminated sites like gas stations to be cleaned and repurposed into

valuable real estate. Both 21E and the Brownfields Act are regulated the state Department of

Environmental Protection (DEP).

Lead paint is a substance that can cause lead paint poisoning to any individual exposed, but

especially vulnerable are children under 6 years of age. Lead paint was phased out in 1978.

In sales: the new owner, if sold to a family with a child under 6, is required to remove the

“mouthable” lead paint up to five feet off the floor within 90 days, including banks that

foreclose. Seller must allow prospective buyer 10 days to inspect.

In rentals: the owner, not the tenant, must remove the lead paint at no additional cost to the

tenant. The owner must provide accommodations for the tenant while the work is being

conducted. Must complete the lead paint notification paperwork. Of course, the owner or agent

cannot discriminate against any party based upon familial status. Tenant cannot opt out.

In vacation rentals: exempt if child is occupying less than 31 days a year, must complete the lead

paint vacation notification paperwork.

Penalties: $1K-$10K fine and possible criminal liability. 93A violation and possible triple

penalty.

41

Radon. A naturally occurring gas that enters the house via the foundation. Colorless and

odorless the EPA deems it unsafe at certain levels. Radon can be remediated through a venting

system to the outside.

Carbon Monoxide. Also colorless and odorless it is sourced typically, but not exclusively, from

natural gas, propane and kerosene burning appliances. Coal and wood can also produce CO. As

of 2006, all homes for sale must receive approval from the local fire department of smoke and

carbon monoxide detectors. Exemptions are homes without any source of CO. Some agents

carry spare CO detectors so if at the time of inspection they can replace a broken or missing

detector.

Asbestos. In its original (non-friable) state, wrapped around a pipe with a paper coating,

asbestos can be fairly harmless, but crumbled, flaky airborne asbestos (friable) can be extremely

hazardous to health. Must be removed by a professional.

UFFI. Used in the 1960’s as an insulator, its use was stopped in 1979. The formaldehyde gas

produced release posed certain health concerns. But over the passage of time the threat of UFFI

has faded. There is no requirement to affirmatively disclose.

Underground fuel tanks. Responsibility of owner to remove. “State law does not require the

removal of a residential underground tank if it isn't leaking, but there may be local requirements

in your community. Check with your fire department or health board.” Read more here:

http://www.mass.gov/eea/agencies/massdep/cleanup/regulations/removing-your-underground-he

ating-oil-tank.html

Agents are not required to disclose asbestos, leaky underground fuel tanks or radon. But failure

to knowingly disclose could be a misrepresentation subject to Chapter 93A.

Lastly, FEMA has recently redrawn flood maps up and down the east coast in response to

Hurricane Sandy. If a question arises relative to the floodplain, agents are advised to obtain an

up to date flood plain map.

42

#4 Closing Procedures and Requirements.

RESPA. The Real Estate Settlement Procedure Act is a federal law which requires an

information booklet covering the costs of settlement to potential borrowers within 3 days of loan

application. Must include good faith estimate of closing costs. Known charges must be

disclosed one day before closing. The disclosures are then included on the Uniform Settlement

Statement commonly referred to as The HUD.

Debits/Credits to the seller will be recorded on the HUD. Agents will need to understand what

constitutes a debit or credit and to whom.

Always debits to seller:

a. real estate commission

b. attorney fees for deed prep

c. total due existing mortgage and liens

d. recording fees to discharge liens

e. deed tax stamps

Always debits to buyer:

a. attorney fees relative to title

b. fees for lien certificate, plans and surveys

c. title insurance - remember is the buyer’s responsibility to determine if the seller has clear

title

d. loan points

e. recording fee of new mortgage

f. appraisal fee

g. prepaid interest

h. property tax reserves

The rule is:

Prepaid expenses are credits to the seller.

Expenses owed in arrears (accrued) are debits to the seller.

43

An element of time may also require calculation. For instance if a property owner pre-paid all

the real estate taxes for the full year, but the closing occurs October 31st. Or in the case of a

property with oil heat, the seller pre-paid for the oil in the tank.

Regulation Z, Truth in Lending (TIL/TILA), enforced by the Federal Trade Commission

applies to consumer loans. Requires full disclosure of all costs of credit so consumers can

compare by informing consumers of total cost in dollars in the form of Annual Percentage Rate

or APR. The APR is the total of interest, points, fees of any kind and disclosure of any

prepayment penalty. Not to include attorney fees, taxes, credit report fee and various other

closing fees. The following loans are excluded: commercial, construction, P&S, real estate

agents (unless offering credit), seller financing, buying subject to existing.

A buyer may rescind loan - except for a first mortgage - within three business days.

Advertisements with specific terms the APR must be displayed. General advertisements, like

“good rates” are not covered. But an ad like “0% down financing” without the APR stated is in

violation.

NEW TRID AS OF OCTOBER 3, 2015

TRID (TILA-RESPA Integrated Disclosures) took effect on October 3, 2015. In basic terms

TRID combines TILA and RESPA together under the supervision of the Consumer Financial

Protection Bureau (CFPB). The spirit of the law is for borrowers to “Know Before You Owe”.

Under TRID the HUD is now called the Closing Disclosure and the GFE is now the Loan

Estimate.

From the Mass Real Estate Law blog:

44

Under TRID, there will be a new settlement statement called a Closing Disclosure, which

must be issued to the borrower at least 3 days prior to closing. If that does not occur, the

closing will be delayed for up to 7 days. Lenders are requiring that the information

contained in the Closing Disclosure (fees, closing costs, taxes, insurance, escrows,

credits, etc.) be finalized no less than 7-14 days prior to closing, to give them enough

time to generate the new Closing Disclosure in a timely fashion. As with any major

regulatory change such as this, we can expect delays and speed bumps for closings

occurring after Oct. 3.

Learn more here:

http://massrealestatelawblog.com/2015/09/28/trid-rules-prompt-changes-to-mass-standard-form-

purchase-and-sale-agreement/

http://www.consumerfinance.gov/know-before-you-owe/

http://files.afncorp.com/WebTrac/Ratesheet/PNPs/AFN-F-Com_TRIDBasics.pdf

Direct Reduction Loan. Common home loan in which the monthly payments do not vary but

the amounts applied to interest and principal vary each month.

Points. Fees equal to 1% of the loan, paid to lender or mortgage broker, part of the APR,

typically the higher the points, the lower the interest rate aka discount points.

#5 Other Laws American with Disabilities Act, prohibits discrimination against disabled persons. “Disabled”

is “a physical or mental impairment that substantially limits a major life activity.” Requires

public accommodations and employers engaging in interstate commerce to make facilities

accessible.

45

Restraint of Trade (Sherman Antitrust Act) outlaws price fixing and geographic

non-competes between agencies. Price fixing can occur in the real estate industry when

brokerages collectively set commission prices/rates. Individuals face up to $1M fine and 10

years in jail. Corporations face up to $100M. Aggrieved parties may sue for treble damages,

court and attorney fees.

Do Not Call List

“A company with which a consumer has an established business relationship may call for up to

18 months after the consumer’s last purchase or last delivery, or last payment, unless the

consumer asks the company not to call again. In that case, the company must honor the request

not to call. If the company calls again, it may be subject to a fine of up to $16,000.”

Learn more here:

https://www.ftc.gov/tips-advice/business-center/guidance/qa-telemarketers-sellers-about-dnc-pro

visions-tsr

1031 Exchange

IRS code that defers gain or loss when parties exchange “like kind” properties, hence

delays/defers capital gains taxes.

Title 5 - Septic.

From the state website:

http://www.mass.gov/eea/agencies/massdep/water/wastewater/buying-or-selling-property-with-a

-septic-system.html

In general, Title 5 requires an inspection at the time of property transfer:

When a property is sold to new owners, or there otherwise is a transfer of title to new owners, or

when properties are divided or combined with certain exceptions.

46

"Title 5 does not require a system inspection if the transfer is of residential real property, and is

between the following relationships: (1) between current spouses; (2) between parents and their

children; (3) between full siblings; and (4) where the grantor transfers the real property to be held

in a revocable or irrevocable trust, where at least one of the designated beneficiaries is of the first

degree of relationship to the grantor". [REF: MGL Ch21A s. 13]

Even if there is not a sale or transfer of title, Title 5 requires an inspection when there is a change

in use or an expansion of the facility. For example, conversion of a retail store to a restaurant

requires an inspection. See Septic System Inspections for details.

Consequently, most offers and almost all P&S will contain a Title V contingency if applicable.

47

Module #4 Quiz

1) Gender discrimination was added to federal fair housing law in what year? a) 1966 b) 1866 c) 1968 d) 1974

2) An agent writes a letter to every home owner of the street warning of a “certain

undesirable ethnic group” moving into the area. This an example of: a) redlining b) steering c) blockbusting d) discrimination

3) A first violation of the Mass Fair Housing Law face immediate suspension of:

a) 30 days b) 60 days c) 90 days d) 120 days

4) An agency purposely fails to disclose a material fact of a property from a buyer, the

buyer sues for triple damages under: a) 93B b) 21E c) 40A d) 93A

5) An Inn operates on a residential street, a new owner buys the Inn and converts it to a

single family residence, the property lost its ___________________. a) conforming use as an Inn b) special permit use an Inn c) tax status as an Inn d) non-conforming use as an Inn

6) 40B is a state law that:

a) requires cleanup of underground fuel tanks b) promotes affordable housing c) requires a conforming use d) requires a septic inspection prior to property transfer

48

7) The CERCLA is overseen by: a) the DEP b) the DEQE c) the EPA d) the FDA

8) Landlord must remove the mouthable lead paint hazard up to how many feet off the

floor? a) 3 b) 4 c) 5 d) 6

9) Lead paint must be removed within how many days?

a) 30 b) 60 c) 90 d) 120

10) The threat of radon gas that emanates from the ground and may be mitigated:

a) by converting the gas to its friable state b) a detector and alarm c) a canary d) a ventilation system

11) A listing broker sees a vintage boiler in the basement wrapped in a white and yellow

insulating material, the agent during an open house tells possible buyers that it is not asbestos, even though the agent is aware that the boiler tested positive for asbestos:

a) disclosure b) misrepresentation c) reasonable care d) dual disclosure

12) This type of home would be exempt from the law requiring CO detectors:

a) a home heated by natural gas b) a home heated by fuel oil c) a home built before 2006 d) an electric home

49

13) The new HUD is called: a) Lending Estimate b) Good Faith Estimate c) Uniform Settlement Statement d) Closing Disclosure

14) Lender fails to provide loan estimate of closing costs within 3 days of application, this is

a violation of: a) CERCLA b) 21E c) TRID d) Regulation Z

15) An ad from a mortgage company touts “rates as low as 1.2%” but includes no

representation of the APR, it is a violation of: a) CERCLA b) 40B c) RESPA d) TIL

16) A $500,000 straight loan with a term of only one year and an interest rate of 5% also

requires 3 points, what is the APR? a) 7% b) 18% c) 8% d) 9%

17) The closing of a property being sold on August 1st includes a paid annual tax bill of

$1368, an outstanding water bill of $636, $1201 in deed stamps, 132 gallons of fuel oil at $2.88 gallon, the result is:

a) $887 debit to the seller b) $1515 credit to the seller c) $893 accrued to the seller d) $385 debit to the seller

50

Real Estate Math Calculations Square mile = 640 acres. Volume: Height x Width x Length Square or rectangle: Height x Length Area of 90 degree triangle: (Height x Length)/2 Commission calculations. Broker lists home for $335,000 with a 6% commission, split 3% for the listing agent, 3% for the buyer agent. Home sells for $287,700, what is the gross commission? How much does each agency get?

$287,700 x 6% = $17,262

$17,262 x .5 = $8,631 Straight line depreciation. Can also be used to factor appreciation Factory worth $11,500,000 depreciates 4% per year for 7 years, what is the value now?

4% x 7 = 28% 100% - 28% = 72%

$11,500,000 x 72% = $8,280,000 Obsolescence.

a. Functional obsolescence, loss of value due to changes in market standards. One bathroom home.

b. Economic obsolescence, changes outside the bounds of the property. Interest (assume a 360 year or 30 days/month). What is interest of the following loan for the first three years?

Loan of $45,263. Rate 5.5% $45,263 x .055 = $2,489 annual interest

$2,489 x 3yrs = $7,468.

51

Capitalization Rates: assumes property is owned outright, no mortgage.

net operating income = (market value x cap rate)

$700,000 = ($6,363,636 x 11%)

Net Operating Income Actual Gross Income -operating expenses = Net operating income (NOI) - mortgage = cash flow. Remember capital expenses like roof replacement is not an operating expense. Rate of Return: factors for mortgage payments. REIT purchased building for $7M, with $2M down. Annual debt service is $763,000 and net income is $1,566,777, what is the rate of return?

$1,566,777 - $763,000 = $803,777 delta $803,777 / $2,000,000 = 40% rate of return

Points. 1% of loan per point. An $80,000 loan with two points equals, $1600. Loan to Value (LTV). Critical risk factor used by lenders. The loan to value is the amount of the mortgage divided by the purchase price (or the appraisal, whichever is lower). The higher the LTV, the higher the risk.

$233,000 sale, with a 77% LTV, what is the loan amount? $233,000 x 77% = $179,410

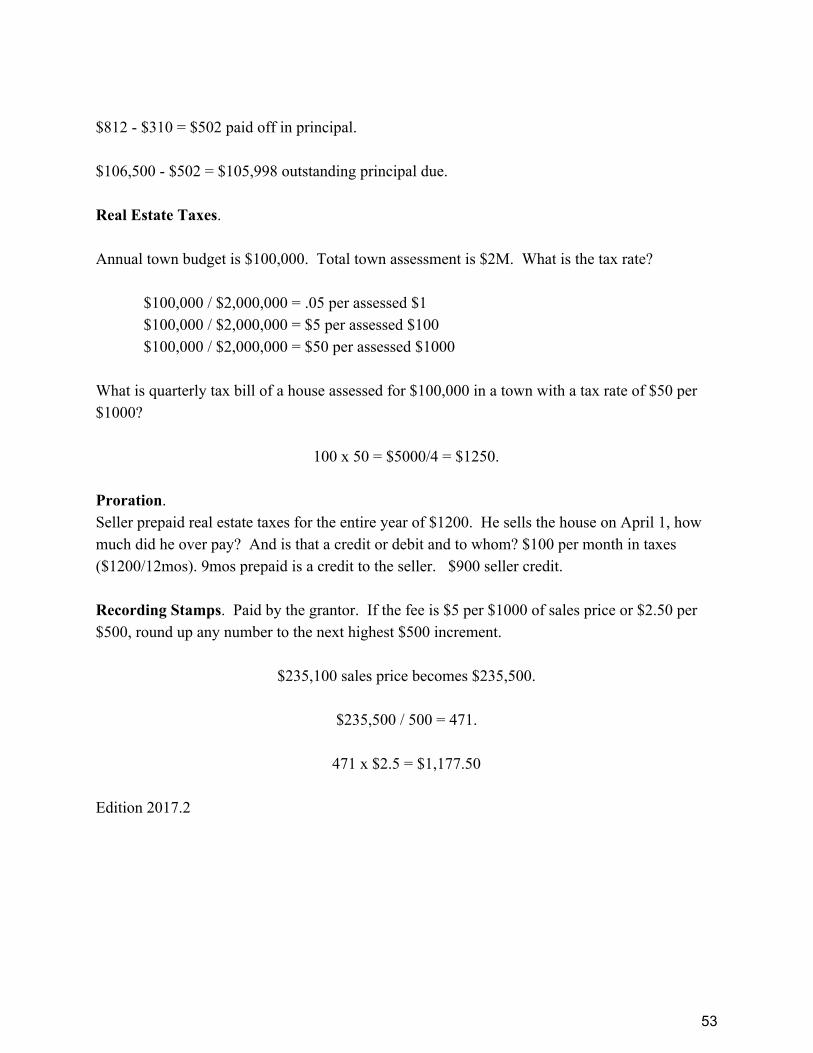

Direct Reduction Loan. Fixed monthly payment but the portion of payments that goes to principal and interest varies each month. A loan for $107,000 at 3.5% would total $3,745 in interest. After the first month what is the outstanding principal owed? The monthly payment is $812. $3,745 / 12 = $312 first month interest $812 - $312 = $500 paid off in principal. $107,000 - $500 = $106,500 outstanding principal due. Second month? $106,500 x .035 = $3,727 annual interest $3,727 / 12 = $310 second month interest.

52

$812 - $310 = $502 paid off in principal. $106,500 - $502 = $105,998 outstanding principal due. Real Estate Taxes. Annual town budget is $100,000. Total town assessment is $2M. What is the tax rate?

$100,000 / $2,000,000 = .05 per assessed $1 $100,000 / $2,000,000 = $5 per assessed $100 $100,000 / $2,000,000 = $50 per assessed $1000

What is quarterly tax bill of a house assessed for $100,000 in a town with a tax rate of $50 per $1000?