Models for Banks' Loan Impairment Charges in Stress Tests ...€¦ · Models for Banks' Loan...

45

57 Models for Banks' Loan Impairment Charges in Stress Tests of the Financial System Kim Abildgren, Economics, and Jannick Damgaard, Financial Markets 1 1. INTRODUCTION AND SUMMARY In an international perspective, the financial crisis has led to renewed focus on development of models for assessing financial stability. A case in point is macro stress testing of banks' capitalisation. A key element of macro stress testing is to calculate banks' loan im- pairment charges in macroeconomic scenarios with severe negative shocks to the economy. Loan impairment charges are often the decisive factor determining the banks' financial performance and excess capital adequacy in periods of unfavourable macroeconomic developments. This is because credit is at the core of banking activities, so naturally it is also the major source of potential losses. The current accounting principles entail considerable cyclical variation in the banks' loan impairment charge ratios. Loan impairment charges are relatively high in years when the economy is slowing down and bank earnings are under pressure, while they are relatively low in years with high economic growth and sound bank earnings. This link between the banks' loan impairment charges and the business cycle should be re- flected in the models used for calculating loan impairment charges in stress tests. Detailed statistics on the banks' loan impairment charges are very scarce. This article presents approximate calculations of the banks' loan impairment charges by industry and sector since 1992, based on the Dan- ish Financial Supervisory Authority's statistics on the banks' losses and accumulated loan impairment charges. For all industries/sectors, loan im- pairment charges tend to be made 1-2 years before realisation of the losses. Moreover, for all industries the loan impairment charge ratios were relatively high in connection with the economic crisis in the early 1990s and the financial crisis from 2008 onwards. However, the level of 1 The authors thank Christian Møller Dahl, The University of Southern Denmark, for valuable sugges- tions and comments in connection with the preparation of the analyses in this article. Any remaining deficiencies in the article as well as views and conclusions are solely the responsibility of the authors. Monetary Review, 1st Quarter 2012 - Part 2

Transcript of Models for Banks' Loan Impairment Charges in Stress Tests ...€¦ · Models for Banks' Loan...

57

Models for Banks' Loan Impairment Charges in Stress Tests of the Financial System

Kim Abildgren, Economics, and Jannick Damgaard, Financial Markets1

1. INTRODUCTION AND SUMMARY

In an international perspective, the financial crisis has led to renewed focus on development of models for assessing financial stability. A case in point is macro stress testing of banks' capitalisation.

A key element of macro stress testing is to calculate banks' loan im-pairment charges in macroeconomic scenarios with severe negative shocks to the economy. Loan impairment charges are often the decisive factor determining the banks' financial performance and excess capital adequacy in periods of unfavourable macroeconomic developments. This is because credit is at the core of banking activities, so naturally it is also the major source of potential losses.

The current accounting principles entail considerable cyclical variation in the banks' loan impairment charge ratios. Loan impairment charges are relatively high in years when the economy is slowing down and bank earnings are under pressure, while they are relatively low in years with high economic growth and sound bank earnings. This link between the banks' loan impairment charges and the business cycle should be re-flected in the models used for calculating loan impairment charges in stress tests.

Detailed statistics on the banks' loan impairment charges are very scarce. This article presents approximate calculations of the banks' loan impairment charges by industry and sector since 1992, based on the Dan-ish Financial Supervisory Authority's statistics on the banks' losses and accumulated loan impairment charges. For all industries/sectors, loan im-pairment charges tend to be made 1-2 years before realisation of the losses. Moreover, for all industries the loan impairment charge ratios were relatively high in connection with the economic crisis in the early 1990s and the financial crisis from 2008 onwards. However, the level of

1 The authors thank Christian Møller Dahl, The University of Southern Denmark, for valuable sugges-

tions and comments in connection with the preparation of the analyses in this article. Any remaining deficiencies in the article as well as views and conclusions are solely the responsibility of the authors.

Monetary Review, 1st Quarter 2012 - Part 2

58

loan impairment charges in crisis periods compared with non-crisis periods varies strongly across industries. Very high loan impairment charge ratios were observed for particularly agriculture, etc. construc-tion, etc. and real estate, etc. in the crisis years.

All else equal, loan impairment charges under the current accounting principles increase the banks' lending capacity during booms and reduce their lending capacity during recessions. Hence the accounting rules for loan impairment charges are procyclical, i.e. they amplify cyclical fluc-tuations. In the wake of the most recent financial crisis it has therefore been discussed whether there is a need to amend the accounting rules so as to ensure that banks build up buffers in good times against losses in bad times.

There are various approaches to modelling the banks' loan impairment charges in connection with macro stress testing of the financial system. These approaches have different characteristics in terms of both degree of detail and methodology. This article presents and compares two spe-cific econometric models for banks' loan impairment charges.

A macro factor model is first estimated, modelling the loan impair-ment charge ratio for Danish banks' loans and guarantees to each indus-try/sector as a function of a number of macroeconomic variables. This enables calculation of loan impairment charge ratios by industry and sector in the projection period for each macroeconomic scenario in a stress test. Combining this information with the individual bank's credit exposures by industry and sector over the projection period makes it possible to calculate the individual bank's loan impairment charges for each scenario. The calculation of each bank's loan impairment charges in the scenarios can then allow for the distribution of each bank's credit exposures to households and various industries.

An accounts-based failure-rate model is then estimated for the loan impairment charge ratios of Danish banks on corporate credit exposures. The model is estimated on the basis of financial statements presented by around 96,000 firms on average in the period 1995-2009. In general, stress testing using this type of model implies constructing a number of macroeconomic scenarios for the future economic development. The development in each firm's financial ratios is then projected in the vari-ous scenarios, followed by calculation of each firm's probability of de-fault and the banks' loan impairment charges.

Both of the estimated models provide a good description of the histor-ical patterns of loan impairment charges and are able to explain the high loan impairment charge ratios during the crisis in the years from 2008 onwards. This is an important feature of models that are to be used for macro stress testing.

Monetary Review, 1st Quarter 2012 - Part 2

59

By definition, all models are simplified presentations of reality. So when constructing model-based projections, it is customary to include extra information besides that contained in the model's estimated relations. During the most recent financial crisis, for example, the Danish govern-ment has implemented extensive measures to support financial stability. Without these initiatives, the economic crisis would undoubtedly have been worse, and the banks' loan impairment charges would have been larger than they actually were. This should be borne in mind if the models are to be used for simulating loan impairment charges in stress scenarios without such massive government support.

The period from the mid-1990s has been characterised by increased focus on financial stability among central banks worldwide, not least in the wake of the most recent financial crisis. So it is likely that focus in the coming years will still be on refining the approaches and methods used for modelling the banks' loan impairment charges in connection with macroeconomic stress tests with a view to improving the basis for assessments of financial stability.

2. CREDIT LOSSES IN THE BANKS' LOAN PORTFOLIOS

The fundamental risk in connection with credit extension is that the borrower is unable or unwilling to meet its payment obligations to the bank in the form of interest and redemptions, cf. Andersen et al. (2001).

The size of a bank's credit losses can be regarded analytically as a product of three factors:

.defaultgivenLossratioeperformancNonexposureCreditlossCredit (2.1) The first factor is the size of the banks' credit exposure in terms of loans and guarantees. Normally, the banks' credit exposure tends to follow the economic development, and the period since 1980 has been characterised by considerable growth in the banks' credit exposure relative to the gross domestic product, GDP, cf. Chart 2.1. This trend has been observed not only in Denmark, but also in other advanced econ-omies with high income levels, cf. Levine (1997) and Andersen (2001). Moreover, credit exposure tends to rise particularly strongly during boom periods.

The second factor is the non-performance ratio, i.e. non-performing loans as a share of credit exposures. The non-performance ratio will nor-mally depend on macroeconomic developments since experience shows that borrowers find it more difficult to service their loans in periods of economic downturn. For example, the non-performance ratio on loans

Monetary Review, 1st Quarter 2012 - Part 2

60

to export firms will depend on international cyclical developments, while the non-performance ratio on loans to domestically oriented in-dustries will depend on developments in domestic consumption and investment.

The third factor is loss given default, i.e. the share of the non-per-forming loans that should be regarded as lost. It depends on e.g. the extent and quality of the collateral pledged by the debtor in connection with the loan, or on the ranking of the loan in the event of default. The ratio may be zero if the entire loan is collateralised, or e.g. 0.5 if half of the loan is collateralised. Loss given default will normally also depend on macroeconomic factors, e.g. property prices if the collateral for a loan consists of real estate.

The loss ratio on the banks' loans and guarantees is the product of the general non-performance ratio and loss given default, cf. Chart 2.2. A clear tendency is seen for the loss ratio to rise in periods of economic downturn and economic crisis.

3. THE BANKS' LOAN IMPAIRMENT CHARGES

Like the loss ratios, banks' loan impairment charge ratios show consid-erable cyclical variation, cf. Chart 3.1.

DANISH BANKS' LOANS AND GUARANTEES AS A PERCENTAGE OF NOMINAL GDP Chart 2.1

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Per cent

Note: Source:

The grey fields indicate economic downturns, cf. Abildgren et al. (2011). There is a data break in 2005, marking the change of accounting principles, cf. Box 3.1. Statistics Denmark, Danish Financial Supervisory Authority, Baldvinsson et al. (2005) and Busch-Nielsen et al. (1996).

Monetary Review, 1st Quarter 2012 - Part 2

61

DANISH BANKS' LOSSES ON LOANS AND GUARANTEES Chart 2.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

10

Per cent

Note: Source:

The grey fields indicate economic downturns, cf. Abildgren et al. (2011). Danish Financial Supervisory Authority, Baldvinsson et al. (2005) and Busch-Nielsen et al. (1996)

DANISH BANKS' LOSSES AND LOAN IMPAIRMENT CHARGES ON LOANS AND GUARANTEES Chart 3.1

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent

Note: Source:

Loan impairment charges have been stated net of reversal of previous loan impairment charges as revenue. There is a data break in the series for loan impairment charges in 2005, when the accounting principles were amended, cf. Box 3.1. Danish Financial Supervisory Authority, Baldvinsson et al. (2005) and Busch-Nielsen et al. (1996).

Monetary Review, 1st Quarter 2012 - Part 2

62

Under the present accounting rules from 2005, exposures are not to be charged to impairment expenses until there is objective evidence of impairment, e.g. the borrower fails to pay the instalments stipulated in the loan document. In that case, the loan must be written down to the present value of the expected future payments on the loan, allowing for realisation of collateral, cf. Box 3.1. In good times, with low unemploy-ment and sound corporate earnings, the number of non-performing loans, etc. is relatively small, resulting in low loan impairment charge ratios. Conversely, the number of non-performing loans is relatively high in a recession, entailing high loan impairment charge ratios.

Before 2005, a prudential principle applied, whereby the banks had to make provisions for expected future losses even though objective evi-dence of impairment had not yet been established.

There was also considerable cyclical variation in the banks' loan impairment charges before 2005. Loan impairment charges made in the years up to the early 1990s helped to ensure that the banks had buffers which they could use to meet losses during the economic crisis in the first half of the 1990s. This was one of the reasons why Denmark wea-thered the crisis much better than the other Nordic countries. In Finland, profit and loss accounts were, until 1990, based on expensing actual losses only. In Norway and Sweden, provisions had to be made for ex-pected losses, but in Sweden the requirements in this respect had been eased when the banking crisis began, and in Norway the requirements had by no means been observed in practice, cf. Abildgren et al. (2010).

Since the mid-1980s, there has been a tendency to make loan impair-ment charges 1-2 years before realisation of the losses. So far, this does not seem to have changed since the transition to the new accounting rules in 2005.

Detailed statistics on the banks' loan impairment charges are very scarce. But it is possible to approximate the banks' loan impairment charge ratios by industry and sector since 1992 on the basis of the Danish Financial Supervisory Authority's statistics on the banks' losses and accumulated loan impairment charges, cf. Box 3.2.1

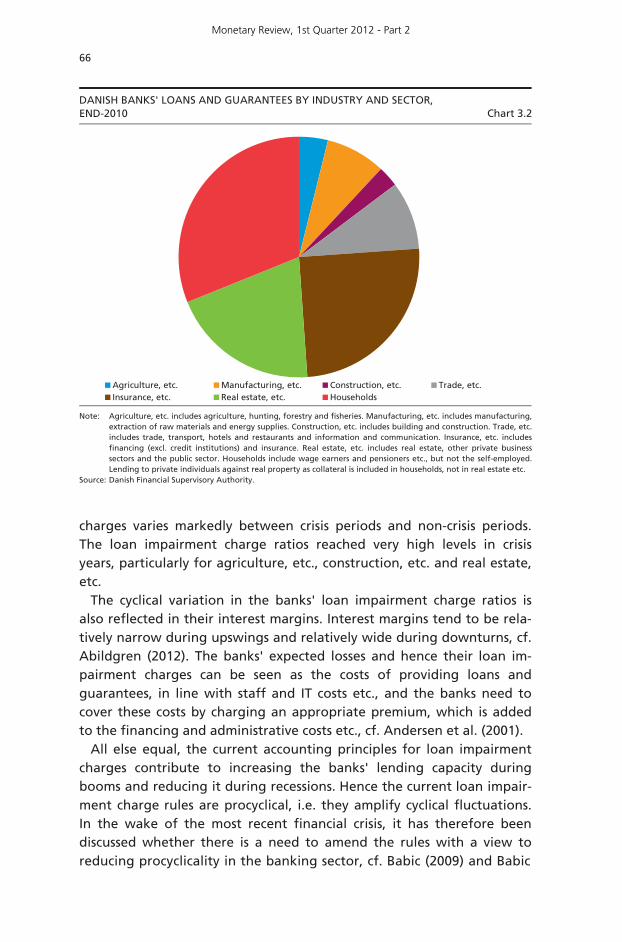

Chart 3.2 shows the banks' exposures by industry at end-2010, while Chart 3.3 shows the approximate loan impairment charge ratios by in-dustry/sector since 1992. It should be noted that for each industry/sector the loan impairment charge ratio relates to the banks' total credit ex-posure to the relevant industry/sector – whether or not the customer is a Danish resident. According to Danmarks Nationalbank's MFI statistics,

1 With effect from 2010, the banks have reported loan impairment charges by industry/sector to the

Danish Financial Supervisory Authority. However, the statistics for 2010 have not been released yet.

Monetary Review, 1st Quarter 2012 - Part 2

63

RULES FOR LOAN IMPAIRMENT CHARGES IN BANKS' FINANCIAL STATEMENTS Box 3.1

Before 2005, the banks' loan impairment charges (provisions on loans) were to be

made on the basis of a probable risk of loss according to a prudential principle.

With effect from 2005 new accounting rules were introduced, reflecting the Inter-

national Financial Reporting Standards, IFRS, cf. Thygesen and Ullersted (2005). The

new rules are based on a principle of neutrality and there must be objective evidence

of impairment before the loan impairment charge is made.

According to the rules in force since 2005, a bank must individually assess all loans

of a considerable size for the bank. Moreover, the bank may choose to assess any

other loans individually. In terms of individual assessment, objective evidence of

impairment is, as a minimum, deemed to exist in the following cases:

The borrower has considerable financial problems.

The borrower is in breach of contract, e.g. due to default on payment obligations

regarding interest and redemptions.

The bank eases the conditions for the borrower, and such easing would not have

been considered if the borrower had not had financial problems.

It is probable that the borrower will be subject to liquidation or other financial

reconstruction.

All loans not written down after individual assessment must be subject to group assess-

ment. To this end, the bank must group its loans according to credit risk characteristics.

As regards group assessment, objective evidence of impairment is found to exist when

observable data indicates a fall in the expected future payments from the group in

question which cannot be attributed to individual loans in the group. Examples of such

data could be:

Deterioration of the payment pattern for the relevant group of loans.

Change in circumstances that tend to be related to the extent of non-performance

in a group of loans, according to experience.

If the bank finds that there is objective evidence of impairment for a loan (or a group

of loans), it must make loan impairment charges corresponding to the difference

between the book value and the present value of the expected future payments. The

value of any collateral should be taken into account when calculating the present

value.

Although the purpose of the current rules was to lay down an objective criterion

for loan impairment charges, the calculation of the banks' loan impairment charges

will, in practice, depend on a number of estimates by the management. For example,

it will not always be clear whether or not a borrower has considerable financial

problems. If that is the case, the size of the loan impairment charges will depend on

the bank's specific estimates of the expected future payments, including the bank's

estimate of the realisation value of any collateral received.1

1 In February 2012, the Danish Financial Supervisory Authority tabled proposals for stricter rules for the banks' loan impairment charges. The new rules are to discourage recognition of uncertain payments far into the future in the calculation of the need for impairment charges on distressed loans for real estate. The proposal also contains more specific criteria for when objective evidence of impairment exists, cf. the Danish Financial Supervisory Authority's press release of 6 February 2012 (in Danish only).

Monetary Review, 1st Quarter 2012 - Part 2

64

APPROXIMATE DATA FOR DANISH BANKS' LOAN IMPAIRMENT CHARGE RATIOS BY INDUSTRY AND SECTOR Box 3.2

Let Nj,t describe loan impairment charges1 in year t in kr. billion related to loans and

guarantees to industry (or sector) j, ANj,t accumulated loan impairment charges2 at the

end of year t in kr. billion related to loans and guarantees to industry j, and Tj,t losses

in year t in kr. billion related to loans and guarantees to industry j. Then the

following identity applies in principle:

.,1,,, tjtjtjtj TANANN (3.1)

If loans and guarantees to industry j at the end of year t in kr. billion are stated as Uj,t,

the loan impairment charge ratio in year t related to loans and guarantees to industry

j, NPj,t, is given as:

.100

,

,,

tj

tjtj U

NNP

(3.2)

The Danish Financial Supervisory Authority has published breakdowns by industry and

sector of the banking sector's losses, accumulated loan impairment charges and

outstanding loans and guarantees for the period since 1994. These statistics can be

taken back to 1991 on the basis of Ministry of Economic Affairs (1994). Against this

background, loan impairment charge ratios by industry and sector for the banking

sector as a whole can, in principle, be calculated all the way back to 1992 by applying

(3.1) and (3.2).

Such calculations are by nature only approximated, because changes in the statistics

of accumulated loan impairment charges from year to year may, in practice, be

influenced by other factors than loan impairment charges and losses. For example, the

banks' accumulated loan impairment charges will show an extraordinary increase if a

bank restructures a foreign subsidiary bank as a branch. The reason is that the subsidiary

bank's accumulated loan impairment charges – which were not included in the statistics

before the restructuring – are added to the parent bank's accumulated loan impairment

charges after the restructuring. An extraordinary change in the accumulated loan

impairment charges will also appear if a bank is taken over by the Financial Stability

Company, which establishes a new subsidiary bank to continue the activities of the

acquired bank. The explanation is that the accumulated loan impairment charges of the

new subsidiary bank are set at zero on establishment. Another example is the strong

extraordinary fall in the accumulated loan impairment charges in connection with the

transition to the new accounting principles in 2005. The calculation method described

above therefore needs to be supplemented with assumptions of the distribution of such

extraordinary changes on industries and sectors. The loan impairment charge ratios

presented in this article are based on the assumption that the distribution on industries

and sectors of the extraordinary changes in the accumulated loan impairment charges in

a given year corresponds to the distribution on industries and sectors of the

accumulated loan impairment charges in that year.

1 Net of reversal of previous loan impairment charges as revenue. 2 Accumulated loan impairment charges consist of the sum of previously made loan impairment charges

(provisions) on exposures that have not yet been written off as losses.

Monetary Review, 1st Quarter 2012 - Part 2

65

non-residents – particularly residents of Sweden, Norway, Ireland, the UK, the Baltic States and the USA – are counterparties to around 40 per cent of lending to non-MFIs by Danish banks and their foreign branches. However, the existing statistics do not provide a basis for breaking down loan impairment charge ratios by customer geographies.

Although the approximate loan impairment charge ratios are subject to some uncertainty, several clear trends nevertheless emerge. For all industries/sectors there is a tendency to make loan impairment charges 1-2 years before realisation of the losses. It is also seen that loan im-pairment charge ratios were relatively high for all industries/sectors in connection with the economic crisis in the early 1990s and the financial crisis in the years from 2008 onwards. The level of loan impairment

CONTINUED Box 3.2

Given this calculation method, the loan impairment charge ratios by industry and

sector which can be calculated directly using the method mentioned above will add

up to the aggregated loan impairment charge ratios when weighted by loans and

guarantees. The aggregated loan impairment charge ratios are not calculated, but

based directly on the accounts statistics of the Danish Financial Supervisory Authority.

The directly calculated loan impairment charge ratios by industry and sector are,

however, characterised by some fluctuations that do not seem to be real in light of

the relatively smooth pattern of the aggregated loan impairment charge ratios, cf.

also Chart 3.1. The loan impairment charge ratios have therefore been smoothed out

subsequently, taking into account that the smoothed series must be relatively close to

the non-smoothed loan impairment charge ratios and that they must also add up to

the aggregated loan impairment charge ratios when weighted by loans and guaran-

tees.

If the smoothed loan impairment charge ratio in year t related to loans and guar-

antees to industry j is stated as NPSj,t, and NPt describes the aggregated loan impair-

ment charge ratio in year t, the smoothed loan impairment charge ratios are found as

the solution to the following minimisation problem:

,2010...,,1992

:

1

,

,

,

2

,,

2

1,,

tforNPNPSU

U

tosubject

NPNPSaNPSNPSa

Minimise

t

j

tj

j

tj

tj

j t

tjtj

j t

tjtj

(3.3)

where a is a parameter of importance to the degree of smoothing. Specifically, a has

been set at 0.5.

Monetary Review, 1st Quarter 2012 - Part 2

66

charges varies markedly between crisis periods and non-crisis periods. The loan impairment charge ratios reached very high levels in crisis years, particularly for agriculture, etc., construction, etc. and real estate, etc.

The cyclical variation in the banks' loan impairment charge ratios is also reflected in their interest margins. Interest margins tend to be rela-tively narrow during upswings and relatively wide during downturns, cf. Abildgren (2012). The banks' expected losses and hence their loan im-pairment charges can be seen as the costs of providing loans and guarantees, in line with staff and IT costs etc., and the banks need to cover these costs by charging an appropriate premium, which is added to the financing and administrative costs etc., cf. Andersen et al. (2001).

All else equal, the current accounting principles for loan impairment charges contribute to increasing the banks' lending capacity during booms and reducing it during recessions. Hence the current loan impair-ment charge rules are procyclical, i.e. they amplify cyclical fluctuations. In the wake of the most recent financial crisis, it has therefore been discussed whether there is a need to amend the rules with a view to reducing procyclicality in the banking sector, cf. Babic (2009) and Babic

DANISH BANKS' LOANS AND GUARANTEES BY INDUSTRY AND SECTOR, END-2010 Chart 3.2

Agriculture, etc. Manufacturing, etc. Construction, etc. Trade, etc.Insurance, etc. Real estate, etc. Households

Note: Source:

Agriculture, etc. includes agriculture, hunting, forestry and fisheries. Manufacturing, etc. includes manufacturing, extraction of raw materials and energy supplies. Construction, etc. includes building and construction. Trade, etc.includes trade, transport, hotels and restaurants and information and communication. Insurance, etc. includes financing (excl. credit institutions) and insurance. Real estate, etc. includes real estate, other private business sectors and the public sector. Households include wage earners and pensioners etc., but not the self-employed. Lending to private individuals against real property as collateral is included in households, not in real estate etc. Danish Financial Supervisory Authority.

Monetary Review, 1st Quarter 2012 - Part 2

67

DANISH BANKS' LOSSES AND LOAN IMPAIRMENT CHARGES ON LOANS AND GUARANTEES – BY INDUSTRY AND SECTOR Chart 3.3

-1

0

1

2

3

4

5

6

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Agriculture, etc.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Manufacturing, etc.

0

2

4

6

8

10

12

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Construction, etc.

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Trade, etc.

-0.5

0.0

0.5

1.0

1.5

2.0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Insurance, etc.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Real estate, etc.

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Households

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Loan impairment charge ratio Loss ratio

Per cent Total

Note: The aggregate loan impairment charge ratios have not been calculated but are based directly on the accounts statistics of the Danish Financial Supervisory Authority.

Monetary Review, 1st Quarter 2012 - Part 2

68

and Rasmussen (2010). One element of the debate has been the "Spanish model" for making provisions. This model entails that Spanish credit institutions must make loan impairment charges not only ac-cording to the principle of objective evidence of impairment ("specific provisions"), but also on the basis of average historical loss ratios over a business cycle ("dynamic provisions"). In periods with low specific pro-visions, the dynamic provisions are increased, while they are reduced in periods with high specific provisions. This means that a bank's total loan impairment charges in a given period become less cyclical, and in good times the bank builds up a buffer against losses in bad times.

In July 2009, the European Commission published its deliberations con-cerning implementation of dynamic provisions in accordance with the Spanish model as a supplement to loan impairment charges under the existing international accounting standards. In the European Commis-sion's consultation paper from February 2010, the thoughts about dynamic provisions had made way for contemplations about "counter-cyclical provisions" also aimed at ensuring that the banks, via loan im-pairment charges, build up buffers against their expected losses over a business cycle. The Commission has not followed up these proposals subsequently. So far, the regulatory response to the financial crisis in re-lation to the issue of procyclicality in the banking sector has mainly fo-cused on introducing countercyclical capital buffers, cf. Harmsen (2010) and Babic (2011).

Currently, the international accounting standards boards, IASB1 and FASB2, are working on proposals for new accounting standards to ensure that loan impairment charges are made at an earlier point than under the current principles. However, the proposals from the IASB and the FASB do not envisage smoothing of loan impairment charges over the business cycle.

4. LOAN IMPAIRMENT CHARGES AND MACRO STRESS TESTING OF THE BANKS' CAPITALISATION

Central banks and supervisory authorities have a number of different approaches to modelling loan impairment charges in connection with macro stress testing of the financial system, cf. e.g. Sorge (2004), Sorge and Virolainen (2006), Chan-Lau (2006), Foglia (2009) and Plesner (2012).

1 The International Accounting Standards Board, an independent organisation working to make

financial statements comparable across countries. 2 The Financial Accounting Standards Board, which develops accounting standards that are generally

accepted in the USA.

Monetary Review, 1st Quarter 2012 - Part 2

69

These approaches have different characteristics in terms of both degree of detail and methodology.

A basic distinction is often made between "top-down" and "bottom-up" stress testing. In top-down stress tests, the authorities perform all stress test calculations, while bottom-up stress tests are performed in cooperation with the banks whose resilience is to be tested. Conse-quently, in top-down stress tests, loan impairment charges are calculated using the authorities' macro stress testing models, while the calculations in bottom-up stress tests are based on the credit risk models of the indi-vidual banks.

This article focuses on models for calculation of the banks' loan impair-ment charges according to the top-down approach. Overall, the models can be divided into two groups: simultaneous models and satellite models. Simultaneous models This model type provides for simultaneous calculation of the macro-economic stress scenarios and the banks' loan impairment charges in the scenarios. This approach uses a simultaneous macroeconomic model that models not only macroeconomic variables such as economic growth, interest rates and house prices, but also both the banks' loan impair-ment charges (pass-through from the real economy to the banking sector) and the impact of the banks' lending capacity on the macro-economy (feedback effects from the banking sector to the real econ-omy), cf. Chart 4.1.

The simultaneous macroeconomic model may be a relatively small vector autoregressive (VAR) model or a larger structural macroeco-nometric model with relations describing the interaction between the banking system and the rest of the economy.

Small VAR models are relatively easy to maintain in step with eco-nomic developments, but since they are aggregated, their results could be difficult to interpret in depth in conformity with economic theory, cf. Abildgren (2012), Avouyi-Dovi et al. (2009) and Shahnazarian and Åsberg (2008).

OVERALL MODEL ARCHITECTURE – SIMULTANEOUS MODEL Chart 4.1

Real economy Banking sectorReal economy Banking sector

Monetary Review, 1st Quarter 2012 - Part 2

70

It requires far more resources to estimate and maintain large, structural macroeconometric models with a built-in financial sector. On the other hand, large structural models can make it easier to provide a description of the interaction between the financial and the real sectors which conforms to theory.

Given the relative complexity of simultaneous models, it may be neces-sary in practice to aggregate the modelling of the banking sector rather than modelling the profit and loss accounts and balance sheets of indi-vidual banks. This means that it is not possible to stress test the capital-isation of the individual banks – only the capitalisation of the banking system as a whole.

Satellite models Under this approach, various macroeconomic scenarios are constructed using a macroeconometric model, followed by modelling of the effects of the scenarios on the banks' loan impairment charges using a satellite model, cf. Borio et al. (2012). Danmarks Nationalbank applies the satel-lite approach in macro stress testing, and the relevant scenarios are constructed using Danmarks Nationalbank's macroeconometric model, MONA, cf. Danmarks Nationalbank (2003a, 2007a).

Typically, this stress testing approach implies construction of scenarios for both the expected economic development ("baseline scenario") and for hypothetical developments with adverse shocks to the economy ("stress scenarios"). The purpose of the scenarios is to throw light on the banks' resilience to possible, but not very probable, shocks to the econ-omy. The banks' capitalisation in the various scenarios is then calculated using a satellite model ("stress test model") with modules for calculation of the banks' loan impairment charges as well as their operating profit, etc. in the various scenarios, cf. Chart 4.2.

The strength of satellite models is their less complex model architec-ture, even in connection with a very detailed level of calculation based on modelling of the profit and loss accounts and balance sheets of indi-vidual banks. For example, in detailed satellite models, variations in the individual banks' exposures to different industries and sectors can be taken into account, which may be difficult in more aggregated models.

Modelling of loan impairment charges in satellite models There are a number of different approaches to modelling loan impair-ment charges in satellite models. Two main model types are examined in the following: macro factor models and accounts-based failure-rate models. In sections 5 and 6, these two model types are estimated on Danish data.

Monetary Review, 1st Quarter 2012 - Part 2

71

Macro factor models This model type is based on econometric relations that explain the banks' loan impairment charge ratios against the backdrop of develop-ments in a number of macroeconomic variables of importance to credit risk, according to generally accepted economic theory, cf. Bunn et al. (2005) and Haldane et al. (2007) for an example from the Bank of Eng-land.

Typical explanatory variables for the loan impairment charge ratio for corporate lending could be real economic growth, real interest rates, debt as a ratio of earnings, real prices of commercial properties, real unit labour costs, real commodity prices, etc. Examples of explanatory vari-ables for lending to households are unemployment, real income, real interest rates, debt as a ratio of income and real house prices.

As regards the level of aggregation, the modelling may relate to total loan impairment charges or loan impairment charges by industry or sector in the banking sector as a whole or for the individual banks.

Accounts-based failure-rate models Bernhardsen and Larsen (2007) and Bernhardsen and Syversten (2009) describe the use of an accounts-based failure-rate model for macro stress testing purposes at Norges Bank. In general, this approach implies con-structing a number of macroeconomic scenarios for the future economic development. Against this background, the development in each firm's financial ratios is projected in the various scenarios, followed by calcula-tion of each firm's probability of default and the banks' loan impair-ment charges. Carling et al. (2007) have estimated a similar model for

OVERALL MODEL ARCHITECTURE – SATELLITE MODEL Chart 4.2

Macro-economicscenarios

Market risk module

Operating profit module

Credit risk module

The banks’ excesscapital adequacy, etc. in the variousscenarios

Stress test model

Macro-economicscenarios

Market risk module

Operating profit module

Credit risk module

The banks’ excesscapital adequacy, etc. in the variousscenarios

Stress test model

Monetary Review, 1st Quarter 2012 - Part 2

72

Sweden. In addition to accounting variables, this model also includes macroeconomic variables in the description of the probability of default.

The strength of this model type is the detailed data material, which provides for very sophisticated examination of credit risk in the banks' lending portfolios. For example, it is possible to throw light on the banks' loan impairment charges broken down by the firms' industry, size, age, geographical location, etc.

On the other hand, accounts-based failure-rate models may contain variables that could be difficult to project to a satisfactory extent on the basis of macroeconomic indicators such as real GDP, e.g. auditors' quali-fications, cf. below.

5. MACRO FACTOR MODEL FOR DANISH BANKS' LOAN IMPAIRMENT CHARGES

This section estimates a macro factor model for Danish banks' loan impairment charge ratios by industry and sector. For each industry/sector the loan impairment charge ratio is modelled as a function of a number of macroeconomic variables. This enables calculation of loan impairment charge ratios by industry and sector in the projection period for each scenario in the stress test. Combining this information with the indi-vidual bank's credit exposures by industry and sector over the projection period makes it possible to calculate the individual bank's loan impair-ment charges for each scenario. The calculation of each bank's loan im-pairment charges in the scenarios can then allow for the distribution of each bank's credit exposures to households and various industries.1 But this model approach does not take into account any differences in the credit quality of the individual banks' loans and guarantees to a given industry.

Data The model is estimated on the basis of annual observations for the period 1992-2010. Observations for loan impairment charge ratios by industry and sector are described in section 3, while observations of the explanatory macroeconomic variables are from the MONA data bank.

1 The data constructed in section 3 for the banks' loan impairment charges by industry and sector

enables direct modelling of loan impairment charge ratios for the banks' loans and guarantees by industry and sector. The macro factor model defined in this section thus differs from the model described in Danmarks Nationalbank (2008, 2009a). Here, the banks' loan impairment charge ratios are estimated in two steps. The first step is to estimate a relation between loss ratios at industry/sector level and macroeconomic trends. The second step is to estimate a relation between the banks' aggregated loan impairment charge ratio relative to the loss ratios on the one hand and a set of macroeconomic variables on the other. Assuming that this relation is identical for all industries/sectors, it is possible to calculate the loan impairment charge ratios by industry/sector.

Monetary Review, 1st Quarter 2012 - Part 2

73

The explanatory macroeconomic variables are collected from the subset of MONA variables normally included in Danmarks Nationalbank's stress tests, cf. Appendix 1 in Stress tests, 2nd half 2011. Such limitation of the potential explanatory variables rules out the application of many variables that could be relevant in the modelling of loan impairment charge ratios (e.g. the debt levels of households and various industries or the prices of commercial or agricultural properties) since these vari-ables are not included in MONA. Moreover, the limitation implies that the potential explanatory variables are to be taken from among the relatively few aggregated "main variables" in Danmarks Nationalbank's stress tests and not from among the over 500 variables in MONA. The reason is that the detailed development in a number of specific vari-ables, such as agricultural exports, rent, etc., is not compiled separately in the stress scenarios.

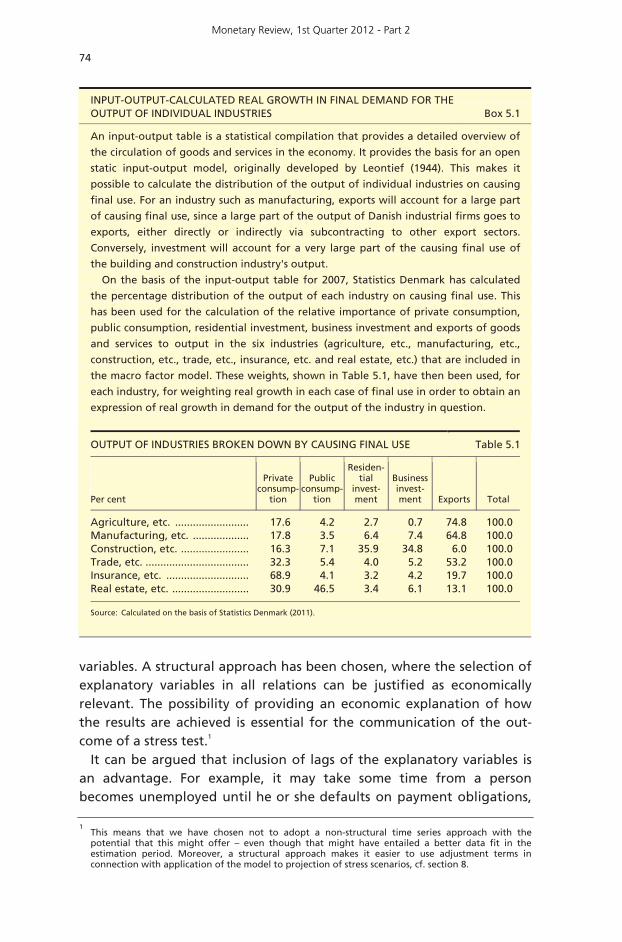

In general, MONA does not contain variables broken down by Indus-try, such as real growth in demand for the output of various industries, which should otherwise be regarded as more relevant to loan impair-ment charges on credit exposures by industry, compared with e.g. the development in total GDP. However, for each industry it is possible to obtain an expression of real growth in demand for that industry's out-put by weighting together real growth in private consumption, public consumption, residential investment, business investment and exports of goods and services using industry-specific weights based on input-output multipliers, cf. Box 5.1. As a result, the individual demand components are included with their direct or indirect impact on the output of the industry in question. Real growth in the demand for e.g. manufactured output that is directly or indirectly (via subcontractors) highly dependent on exports is thus given a high weight to real growth in exports, while real growth in demand for output from domestically oriented industries, such as building and construction, is given a high weight to real growth in investment.

Chart 5.1 shows the industry-specific expressions of real growth in de-mand for the output of the individual industries, while the other ex-planatory variables applied appear from Chart 5.2.1

Model specification For each industry and for households, the loan impairment charge ratio is modelled as a function of a number of explanatory macroeconomic

1 Besides the explanatory variables mentioned above, it has also been attempted to include real

growth in the export markets for manufactured output as a proxy of economic development abroad, given that non-residents are counterparties in around 40 per cent of Danish banks' lending to non-MFIs. However, since export market growth did not figure to any significant extent in the loan impairment charge relation for any industry, it has not been included in Chart 5.2.

Monetary Review, 1st Quarter 2012 - Part 2

74

variables. A structural approach has been chosen, where the selection of explanatory variables in all relations can be justified as economically relevant. The possibility of providing an economic explanation of how the results are achieved is essential for the communication of the out-come of a stress test.1

It can be argued that inclusion of lags of the explanatory variables is an advantage. For example, it may take some time from a person becomes unemployed until he or she defaults on payment obligations, 1 This means that we have chosen not to adopt a non-structural time series approach with the

potential that this might offer – even though that might have entailed a better data fit in the estimation period. Moreover, a structural approach makes it easier to use adjustment terms in connection with application of the model to projection of stress scenarios, cf. section 8.

INPUT-OUTPUT-CALCULATED REAL GROWTH IN FINAL DEMAND FOR THE OUTPUT OF INDIVIDUAL INDUSTRIES Box 5.1

An input-output table is a statistical compilation that provides a detailed overview of

the circulation of goods and services in the economy. It provides the basis for an open

static input-output model, originally developed by Leontief (1944). This makes it

possible to calculate the distribution of the output of individual industries on causing

final use. For an industry such as manufacturing, exports will account for a large part

of causing final use, since a large part of the output of Danish industrial firms goes to

exports, either directly or indirectly via subcontracting to other export sectors.

Conversely, investment will account for a very large part of the causing final use of

the building and construction industry's output.

On the basis of the input-output table for 2007, Statistics Denmark has calculated

the percentage distribution of the output of each industry on causing final use. This

has been used for the calculation of the relative importance of private consumption,

public consumption, residential investment, business investment and exports of goods

and services to output in the six industries (agriculture, etc., manufacturing, etc.,

construction, etc., trade, etc., insurance, etc. and real estate, etc.) that are included in

the macro factor model. These weights, shown in Table 5.1, have then been used, for

each industry, for weighting real growth in each case of final use in order to obtain an

expression of real growth in demand for the output of the industry in question.

OUTPUT OF INDUSTRIES BROKEN DOWN BY CAUSING FINAL USE Table 5.1

Per cent

Private

consump-tion

Public

consump-tion

Residen-tial

invest-ment

Business invest-ment

Exports

Total

Agriculture, etc. ......................... 17.6 4.2 2.7 0.7 74.8 100.0 Manufacturing, etc. ................... 17.8 3.5 6.4 7.4 64.8 100.0 Construction, etc. ....................... 16.3 7.1 35.9 34.8 6.0 100.0 Trade, etc. ................................... 32.3 5.4 4.0 5.2 53.2 100.0 Insurance, etc. ............................ 68.9 4.1 3.2 4.2 19.7 100.0 Real estate, etc. .......................... 30.9 46.5 3.4 6.1 13.1 100.0

Source: Calculated on the basis of Statistics Denmark (2011).

Monetary Review, 1st Quarter 2012 - Part 2

75

REAL GROWTH IN FINAL DEMAND FOR THE OUTPUT OF VARIOUS INDUSTRIES Chart 5.1

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

14

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Agriculture, etc. Manufacturing, etc. Construction, etc.Trade, etc. Insurance, etc. Real estate, etc.

Per cent year-on-year

Source: See Box 5.1.

UNEMPLOYMENT, REAL GROWTH IN HOUSE PRICES AND SHORT-TERM AND LONG-TERM REAL INTEREST RATES Chart 5.2

Unemployment

0

2

4

6

8

10

12

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Per cent Real growth in house prices

-15

-10

-5

0

5

10

15

20

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Per cent year-on-year

Short-term real interest rate

-2

0

2

4

6

8

10

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Per cent p.a. Long-term real interest rate

-2

0

2

4

6

8

10

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Per cent p.a.

Source: MONA data bank.

Monetary Review, 1st Quarter 2012 - Part 2

76

when the loan impairment charges are made. One reason could be that the person in question has private means to use. But with only 19 annual observations, inclusion of one or two lags of just a few explanatory variables may soon give rise to problems with lack of degrees of freedom. Instead of including lags of the explanatory variables in the model, we have chosen to include the response variable (loan impairment charge ratio) as an explanatory variable with a lag of one year.1

The macro factor model is therefore specified as the following linear regression equations:

,eXbbNPSaNPS tj

k

nn,tnjjj,tjj,t ,

1,0,1

(5.1)

where NPSj,t is the loan impairment charge ratio in year t related to loans and guarantees to industry j, bj,0 is a constant term, X1,t ,…, Xk,t are explanatory variables2 and aj, bj,1, …, bj,k are parameters. Finally, ej,t are serially uncorrelated error terms with a mean value of zero and time-invariant variance.3

For the loan impairment charge ratio on loans and guarantees to households, the basic potential explanatory variables are the unemploy-ment rate, real interest rates and real growth in house prices. A priori, rising unemployment is expected to increase the loan impairment charge ratio since it reduces the households' ability to pay. Correspond-ingly, rising real interest rates are expected to increase the loan impair-ment charge ratio, since a higher level of interest rates increases the interest burden of the households. Conversely, rising real house prices are, all else equal, expected to reduce the loan impairment charge ratio since a considerable number of bank loans are based on real property as collateral.

1 This corresponds to the mindset behind the "Koyck lag", i.e. transforming an equation with an

infinite number of lags of the explanatory variables with geometrically declining coefficients into an equation including a one-period lag of the response variable as an explanatory variable together with the original explanatory variables without lags, cf. Koyck (1954) and Griliches (1967). Theoretically, the parameter of the autoregressive term in a Koyck lag will be between 0 and 1. An alternative approach to parsimonious modelling is panel data estimation with parameter restrictions across industries. Since our aim is the widest possible modelling of cross-industry variations in credit risk, this method has not been selected.

2 All explanatory variables are in real terms, e.g. real interest rates, real growth in house prices, etc.,

given the assumption that the debtor's income/ability to pay rises in step with inflation. 3 The model (5.1) can be perceived as an ARX model, i.e. an autoregressive (AR) model expanded to

include exogenous variables (X). The model (5.1) is estimated using the single-equation Ordinary Least Squares, OLS, method. Thus, any problems with endogeneity are disregarded. We have chosen a linear model specification which is easy to interpret. We have not chosen a logit approach since loan impairment charge ratios can be negative and hence outside the set interval between 0 and 1. Deterministic trends have not been used in the regression equations, because the estimated model is designed for stress scenario projection. In addition, all of the applied response and explanatory variables must be presumed to be stationary in a structural economic perspective.

Monetary Review, 1st Quarter 2012 - Part 2

77

For loan impairment charge ratios on loans and guarantees to the six industries, the basic potential explanatory variables are real growth in demand for the output of the industry, real interest rates and real growth in house prices. A priori, an increase in real growth in demand for the output of the industry is expected to reduce the loan impairment charge ratio, since higher turnover improves firms' ability to pay. Rising real interest rates are assumed to increase the loan impairment charge ratio, because a higher level of interest rates implies a larger interest burden for the firms. Conversely, rising real house prices are, all else equal, expected to reduce the loan impairment charge ratio, since a considerable number of bank loans are based on commercial properties as collateral, which normally display correlation with house prices, cf. Chart 5.3.

Estimation results Table 5.2 shows the estimated loan impairment charge relations. With a few exceptions, the individual relations include only the explanatory variables for which the parameter estimates differ significantly from zero.1 All of the estimated parameters have the expected signs, and

1 This choice was made in light of the modest number of degrees of freedom. In principle, the

exclusion of relevant explanatory variables may give rise to bias in the estimated parameter coefficients, but, as mentioned, only insignificant variables have been excluded.

PROPERTY PRICES Chart 5.3

30

40

50

60

70

80

90

100

110

120

13019

92

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Single-family houses Commercial properties

2006 = 100

Note: Source:

Annual averages. Statistics Denmark.

Monetary Review, 1st Quarter 2012 - Part 2

78

there are no problems with autocorrelation in the relations at a signifi-cance level of 5 per cent. The high values of the determination coeffi-cient (R2) should be viewed in light of the use of smoothed loan impairment charge ratios, cf. Box 3.2.1

According to the estimated relation for loans and guarantees to households, an increase in unemployment by 3 percentage points will, all else equal, cause the loan impairment charge ratio to rise by 0.25 percentage point, while a drop in real house prices by 10 per cent will, all else equal, increase the loan impairment charge ratio by 0.5 percentage point. It should be noted, however, that the estimated coefficient of unemployment is not significantly different from zero, and that the unemployment rate has shown a clear downward trend since the early 1990s in step with the reduction of structural unemployment, cf. Andersen and Rasmussen (2011). In the estimation period 1992-2010 there have been no instances of a 3-percentage-point increase in unemployment from year to year. It is therefore uncertain whether the estimated effect on loan impairment charges from lending to house-holds will apply also in the event of a sharp increase in unemployment over a short period of time. This should be kept in mind if the relation is used for macro stress testing purposes, cf. also section 8 about model application.

In all of the estimated loan impairment relations for industries, real growth in demand for the industry's output is included as an explana-tory variable. For example, a 10-per-cent drop in real demand for the industry's output entails, all else equal, a rise of 1.5 percentage points in the loan impairment charge ratio, as regards loans and guarantees to construction, etc., Moreover, the development in real interest rates or real house prices has been found to have a significant effect on loan impairment charges for certain industries. For example, a 1-percentage-point increase in long-term real interest rates will, all else equal, cause the loan impairment charge ratio to rise by 0.2 percentage point as regards loans and guarantees to real estate, etc. When interpreting the relations for loan impairment charges on corporate lending, it should be borne in mind that both short-term and long-term real interest rates have shown a clear downward trend since the early 1990s. Consequent-ly, if there is a considerable increase in the level of interest rates, there is

1 If non-smoothed loan impairment charge ratios, described in Box 3.2, are used, almost the same

variables become significantly different from zero, with the same sign. R2 becomes somewhat lower, however, but the estimated loan impairment charge ratios do not differ to any noticeable extent from the ratios shown in Chart 5.4. Attempts have been made to include non-linear transformations of the explanatory variables (unemployment and interest rates) and asymmetrical treatment of increases and falls in house prices in alternative models. Inclusion of such terms did not result in better data fit.

Monetary Review, 1st Quarter 2012 - Part 2

79

a risk that the effect on loan impairment charges will differ from the effect that can be calculated directly on the basis of the relations.

Chart 5.4 compares actual and estimated loan impairment charge ratios. With the exception of manufacturing, etc. in the middle of the period, the actual and estimated loan impairment charge ratios are relatively closely related. This is also reflected in the relatively high deter-

ESTIMATED LOAN IMPAIRMENT RELATIONS Table 5.2

Response variable: Loan impairment charge ratio for loans and guarantees to

House-holds

Agricul-ture, etc.

Manufac-turing, etc.

Construc-tion, etc.

Trade, etc.

Insurance, etc.

Real estate, etc.

Explanatory variables:

Parameter estimate (standard error)

Constant .................. 0.0561 (0.193)

0.564***

(0.132) 0.401*** (0.135)

1.150*** (0.271)

0.430***

(0.0939) 0.467*** (0.0661)

0.692** (0.322)

Response variable, 1-year lag ................

0.355* (0.175)

0.601*** (0.0601)

0.608*** (0.143)

0.467*** (0.0720)

0.592***

(0.0784) 0.501*** (0.0805)

0.525*** (0.124)

Unemployment, per cent1 .........................

0.0829 (0.0494)

... ... ... ... ... ...

Real growth in house prices, per cent year-on-year ....................

-0.0484***

(0.0108) ... ... ... -0.0234*

(0.0128) ... ...

Short-term real interest rate, per cent p.a.2 ...........

... ... ... ... 0.0593* (0.0316)

... ...

Long-term real interest rate, per cent p.a.3 ...........

... ... ... ... ... ...

0.210** (0.0947)

Real growth in demand, per cent p.a.4 ..........................

...

-0.0917***

(0.0213)

-0.0447**

(0.0159)

-0.149***

(0.0338)

-0.0585**

(0.0266)

-0.144*** (0.0168)

-0.416*** (0.0833)

Number of observations ............ 18 18 18 18 18 18 18 R2 ............................. 0.842 0.887 0.676 0.847 0.929 0.905 0.817 Adjusted R25 ............ 0.808 0.872 0.633 0.826 0.907 0.893 0.778 AR(1)6 ....................... 0.452 0.975 0.896 0.248 0.142 0.0321 0.490 AR(1-2)6 .................... 2.345 1.001 1.418 0.324 0.0988 0.0215 0.442 JB7 ............................. 1.065 0.499 4.000 0.117 5.231* 0.639 2.058

1 Number of unemployed persons as a percentage of the labour force. 2 3-month collateralised money-market interest rate less year-on-year growth in the Harmonised Index of Consumer

prices, HICP. 3 Average bond yield less year-on-year growth in HICP. 4 Input-output-calculated real growth in final demand for the output of each industry, cf. Box 5.1. 5 Adjusted for the number of degrees of freedom. 6 LM test for autocorrelation (F form) with the order in brackets. The null hypothesis is no autocorrelation. 7 Jarque-Bera normality test with small sample adjustment. The null hypothesis is normality. Note: Estimated using the OLS method. * indicates rejection of the null hypothesis at a significance level of 10 per cent. ** indicates rejection of the null hypothesis at a significance level of 5 per cent. *** indicates rejection of the null hypothesis at a significance level of 1 per cent The null hypothesis on testing (double-sided) for significance of parameter estimates is that the parameter is equal

to zero. The delimitation of households and the individual industries is described in the note to Chart 3.2.

Monetary Review, 1st Quarter 2012 - Part 2

80

ACTUAL AND ESTIMATED LOAN IMPAIRMENT CHARGE RATIOS ON LOANS AND GUARANTEES FROM DANISH BANKS – MACRO FACTOR MODEL Chart 5.4

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Agriculture, etc.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Manufacturing, etc.

-1

0

1

2

3

4

5

6

7

8

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Construction, etc.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Trade, etc.

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Insurance, etc.

-2

-1

0

1

2

3

4

5

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Real estate, etc.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Households

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Actual Estimated

Per cent Total

Note: The estimated values of the total loan impairment charge ratio have been calculated by weighting loan impairment charge ratios by industry and sector using the weights of loans and guarantees. The actual total loanimpairment charge ratio has not been calculated, but is based directly on the accounts statistics of the DanishFinancial Supervisory Authority.

Monetary Review, 1st Quarter 2012 - Part 2

81

mination coefficients in Table 5.2. The estimated macro factor model is also able to explain the high levels of loan impairment charges during the crises in the early 1990s and the years from 2008 onwards. This is an important feature of models that are to be used for macro stress testing.

The calculations in Chart 5.4 are normally characterised as an "in-sample" test of the model, with the applied parameter estimates in all years being based on data for the entire period 1992-2010, and with actual lagged loan impairment charge ratios being applied in the calcu-lation of estimated loan impairment charge ratios. Since this is a very short data set that includes only few observations with a crisis in the banking sector, it makes no sense to perform a full "out-of-sample" test, calculating the parameter estimates on the basis of a subset of the observations in the data set. A partial out-of-sample test for the years 2007-09 – in which the parameter estimates are based on data for 1992-2010, but the estimated loan impairment charge ratios are used as lagged loan impairment charge ratios in the calculation of estimated loan impairment charge ratios in the projection period – results in an average absolute deviation from the actual loan impairment charge ratios in the three years of 0.3 percentage point for the sector as a whole. This corresponds to the average absolute prediction error in the in-sample test. The calculations thus illustrate that, also in a partial out-of-sample test, the model is able to generate high loan impairment charge ratios in a period of strong economic downturn.

6. ACCOUNTS-BASED FAILURE-RATE MODEL FOR THE LOAN IMPAIRMENT CHARGES OF DANISH BANKS

In this section, an accounts-based failure-rate model is estimated for Danish banks' loan impairment charge ratios for corporate credit expos-ures. In general, stress testing using this type of model implies construc-ting a number of macroeconomic scenarios for the future economic development. Against this background, the pattern of each firm's finan-cial ratios is projected in the various scenarios, followed by calculation of each firm's probability of default and the banks' loan impairment charges.

Data The data material behind the model consists of annual observations since 1995. Observations of the loan impairment charge ratios by Indus-try are described in section 3, while observations of the explanatory macroeconomic variables are from the MONA data bank and from the

Monetary Review, 1st Quarter 2012 - Part 2

82

subset of MONA variables included in Danmarks Nationalbank's stress test, cf. section 5.

The source of financial statements at micro level is a database consisting of the published financial statements of all Danish public and private limited liability companies with a balance-sheet total exceeding kr. 125.000, collected by Experian A/S. Credit institutions are excluded from the data set, since exposures vis-à-vis credit institutions are not included in the loans and guarantees that are the subject of the modelling of loan impairment charges. Moreover, a few special firms with large balance-sheet totals are excluded as they constitute only a limited risk to the banks. Cases in point are the Great Belt Bridge and Øresund Landworks as their debt is guaranteed by the government. Sole proprietorships are not comprised by the database. The data set consists of around 1,435,000 financial statements presented by around 96,000 firms on average for the financial years 1995-2009. The database also contains information about the number of failures and other firm-specific characteristics, such as age, geographical location, form of ownership, etc.

Estimation of the failure-rate model First, a modified version of Danmarks Nationalbank's failure-rate model is estimated.1 The model describes the probability of firm i failing2 in year t (PDi,t) on the basis of information on the firm's return on assets, debt, industry, geographical location, etc. in year t-2 (X1,i,t-2 ,…, Xk,i,t-2 ) as well as growth in real GDP in year t-1 (Z1,t-1).

3 This can be formally written as:

,ZaXbbFPD ,t

k

ntn,inti

111

12,0,

(6.1)

where b0 is a constant term, and b1, …, bk, a1 are parameters. The ex-planatory variables in the basic model are described in more detail in Table 6.1.

1 Danmarks Nationalbank's failure-rate model has not previously been used directly for macro stress

testing purposes. It is described in Danmarks Nationalbank (2003b, 2007b), Lykke et al. (2004) and Dyrberg (2004). The model estimated in this article contains the same variables as Danmarks Nationalbank's failure-rate model except for one variable indicating whether the financial statements of the firm in question have one or more auditors' qualifications. This variable has been excluded because it is difficult to project on the basis of macroeconomic variables.

2 Given the ultimate aim of modelling the banks' loan impairment charges, a broad-based definition

of "failure" is applied. A firm is regarded as having failed when one of the following events has occurred: (a) It is subject to compulsory liquidation or is being liquidated; (b) it has been or is being dissolved by the courts; (c) it is subject to a compulsory deed of arrangement with creditors or to a compulsory scheme of arrangement with creditors; or (d) it has been subject to enforced sale.

3 We have one comment in relation to the recording of failures in the data behind the equations

estimated in this section. All failures are placed two years after the end of the last year for which the firm presented financial statements as a going concern. The reason is that it, on average, takes 19 months from the presentation of the last financial statements as a going concern to the official affirmation of the compulsory liquidation, cf. Lykke et al. (2004).

Monetary Review, 1st Quarter 2012 - Part 2

83

EXPLANATORY VARIABLES IN (6.1) Table 6.1

Explanatory variables

Expected effect on probability

of default

Description

Firm-specific variables (included with a 2-year lag): Return on assets ......... - The firm's return on assets less the median return

on assets for the relevant industry. The return on assets is calculated as the profit for the year before interest (primary operating result) as a ratio of total assets at year-end.

Debt ratio (short-term) ................

+ Short-term debt as a ratio of the balance-sheettotal, year-end.

Debt ratio (long-term) .................

+ Long-term debt as a ratio of the balance-sheettotal, year-end.

Size ............................. - The logarithm of the balance-sheet total in kr. 1,000 at year-end deflated by the GDP deflator (1995 = 1).

Eroded capital base .... + The dummy variable is set at 1 if the firm has made a loss over the last year, and if another loss will mean that the firm's equity capital falls below the statutory requirement for capital size in new companies. Otherwise, the dummy vari-able is set at 0.

Form of ownership .... + The dummy variable is set at 1 if the firm is a private limited liability company (ApS) at year-end. Public limited liability companies (A/S) con-stitute the reference group (with the value 0). The statutory capital requirement for establish-ment of public limited liability companies is higher than for private limited liability com-panies.

Age - Dummy variables representing the firm's age at year-end measured as the number of full years. Newly established firms aged less than 1 year constitute the reference group (with the value 0).

Industry ...................... +/- Dummy variables for each industry. They are to capture industry-specific differences in the level of probability of default.

Municipality group .... - Dummy variables indicating the firms' domiciles at year-end by municipality group, with Greater Copenhagen as the reference group (with the value 0). Greater Copenhagen is normally more sensitive to cyclical fluctuations than the prov-inces.

Macroeconomic variables (included with a 1-year lag): Real GDP growth ....... - Year-on-year growth in real GDP. This variable is

to capture general cyclical developments.

Monetary Review, 1st Quarter 2012 - Part 2

84

ESTIMATION OF FAILURE-RATE MODEL (6.1) Table 6.2

Coefficient estimate

Standard error

Change in odds ratio

when explanatory variable changes by

one unit

Constant .................................................... -1.271*** 0.0391 ... Return on assets, percentage points ....... -0.00148*** 0.000111 0.999 Debt (short-term), ratio ............................ 0.267*** 0.00714 1.306 Debt (long-term), ratio ............................. 0.0427*** 0.0127 1.044 Size, log 1000 1995-kr. ............................. -0.310*** 0.00404 0.733 Form of ownership, dummy (1=private;0=public) ................................................... 0.238*** 0.0151 1.268 Eroded capital base, dummy (1=YES; 0=NO) ........................................... 1.121

***

0.0116

3.097

Real GDP growth, per cent p.a. ............... -0.0937*** 0.00172 0.911

Note: The explanatory variables are described in Table 6.1. The response variable in the estimated equation is the logarithm of the "odds ratio", i.e. the probability of "failing" divided by the probability of "continuing as a goingconcern". The figures in the column "change in odds ratio when explanatory variable changes by one unit" arethe antilogarithms of the figures in the column of coefficient estimates.

Besides the variables shown in the table, the estimated model contains dummy variables for industry, municipalitygroup and age.

* indicates that a coefficient is significantly different from zero at a significance level of 10 per cent. ** indicates that a coefficient is significantly different from zero at a significance level of 5 per cent. *** indicates that a coefficient is significantly different from zero at a significance level of 1 per cent.