Modeling the Asymmetry of Stock Movements Using Price Ranges Ray Y. Chou Academia Sinica “ The...

36

Modeling the Asymmetry of Stock Movements Using Price Ranges Ray Y. Chou Academia Sinica “ The 2002 NTU International Finance Con ference” Taipei. May 24-25, 2002

-

Upload

anais-slee -

Category

Documents

-

view

214 -

download

0

Transcript of Modeling the Asymmetry of Stock Movements Using Price Ranges Ray Y. Chou Academia Sinica “ The...

Modeling the Asymmetry of Stock Movements Using Price

Ranges

Ray Y. Chou

Academia Sinica

“ The 2002 NTU International Finance Conference” Taipei.

May 24-25, 2002

Motivation

• Provide separate dynamic models for the upward-range and the downward-range to allow for asymmetries.

• Factors driving the upward movements and the downward movements maybe different.

• Upward range applications: market rallies, call options, historical new highs, limit order to sell

• Downward range applications: Value-at-Risk, put options, limit order to buy

Main Results• ACARR is similar to CARR and ACD but

with a different limiting distribution and with new interpretations and implications.

• Properties: QMLE, Distribution• Empirical results using daily S&P500 index

show asymmetry in dynamics, leverage effect, periodic patterns and interactions of upward and downward movements.

• Volatility forecast accuracy: ACARR>CARR>GARCH

Range as a measure of the “realized volatility”

• Simpler and more natural than the sum-squared-returns (measuring the integrated volatility) of Anderson et.al.(2000)

• Parkinson (1980) and others have established the efficiency gain of range over standard method in estimating volatilities

• Chou (2001) proposed CARR, a dynamic model for range with satisfactory performance

Discrete sampling from a continuous process

Let Pt be the logarithmic price of a speculative asset observed at

time t, t =1,2,…T. Pt are taken to be realizations of a price

process {P}, which is assumed to be a continuous process.

Let OPENtP , CLOSE

tP , HIGHtP , LOW

tP be the opening, closing, high and

low prices, in natural logarithm, between t-1 and t.

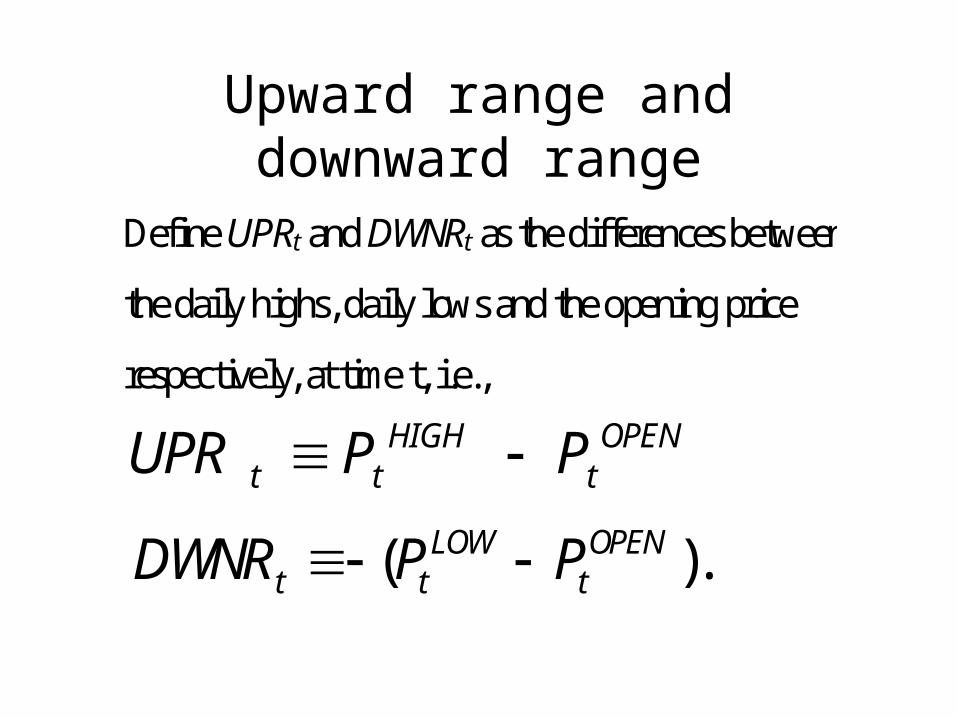

Upward range and downward range

Define UPRt and DWNRt as the differences between

the daily highs, daily lows and the opening price

respectively, at time t, i.e.,

OPENt

HIGHtt PPUPR

).( OPENt

LOWtt PPDWNR

Range and one-sided ranges

Note that these two one-sided ranges, UPR t and

DWNR t, represent the maximum returns and the

m inimum returns (in percentage size) respectively

over the unit time interval [t-1, t]. Further, the

range R t, is defined to be

LO Wt

H IG Htt PPR

, or

ttt DWNRUPRR .

The Conditional Autoregressive Range Expectation (CARR) model in Chou

(2001)

tttR

jt

q

jjit

p

iit R

11

t ~ iid f(.)

The Asymmetric Conditional Autoregressive Range Expectation -ACARR(p,q) model

ut

uttUPR

dt

dttDWNR

u

jt

q

j

ujit

p

i

ui

uut UPR

11

d

jt

q

j

djit

p

i

di

ddt DWNR

11

Distribution assumptions in ACARR

ut ~ iid fu(.),

dt ~ iid fd(.)

It is shown that the limiting distributions

fu(.) and fd(.) are identical but are different from the error distribution for the CARE model in Chou (2000b).

ACARRX(p,q) – ACARR(p,q) with exogenous variables

Let be some variables measurable at time t-1,

the ACAREX(p,q) model is defined to be

,1111

ltl

L

l

u

jt

q

j

ujit

p

i

ui

uut XUPR

,1111

ltl

L

l

d

jt

q

j

djit

p

i

di

ddt XDWNR

Explanatory variables in the ACARRX(p,q) model

• Lagged returns – leverage effect

• Periodic (weekday) pattern

• Transaction volumes

• Interaction tems – lagged DWNR in expected UPR and lagged UPR in expected DWNR

Properties of ACARR

• Same as ACD of Engle and Russell (1998) but with a known limiting distribution for the error term

• A conditional mean model

• An asymmetric model for volatilities

Sources of asymmetry for an ACARRX(1,1) model

– short term shock impact – long term persistence of shocks – speed of mean-reverting ‘s – effects of leverage, periodic pattern,

interaction terms, among others

A special case of ACARR: Exponential ACARR(1,1) or EACARR(1,1)

• It’s useful to consider the exponential case for f(.), the distribution of the normalized range or the disturbance.

• Like GARCH models, a simple (p=1, q=1) specification works for many empirical examples.

ACARR vs. ACD identical formula

• ACARR• Range data, positive

valued, with fixed sample interval

• QMLE with EACARR• Known limiting

distribution• A new volatility

model

• ACD• Duration data, positive

valued, with non-fixed sample interval

• QMLE with EACD• Unknown limiting

distribution• Hazard rate

interpretation

The QMLE property

• Assuming any general density function f(.) for the disturbance term t, the parameters

in ACARR can be estimated consistently by estimating an exponential-ACARR model.

• Proof: see Engle and Russell (1998), p.1135

The QMLE Estimation

• Consistent standard errors are obtained by employing the robust covariance method in Bollerslev and Wooldridge (1987).

• See Engle and Russell (1998).

Empirical example: S&P500 daily index

• Sample period: 1962/01/03 – 2000/08/25

• Data source: Yahoo.com

• Models used: EACARR(1,1), EACARRX(p,q)

• Both daily and weekly observations are used for estimation

• Forecast comparison of CARR and ACARR

-30

-20

-10

0

10

2000 4000 6000 8000

UPR DWNR

Figure 1: Daily UPR and Daily DWNR, S&P500, 1962/1-2000/8

Series: MAX

Sample 1 9700

Observations 9700

Mean 0.737026

Median 0.635628

Maximum 9.052741

Minimum 0.000000

Std. Dev. 0.621222

Skewness 2.110659

Kurtosis 15.76462

Jarque-Bera 73055.13

Probability 0.0000000

400

800

1200

1600

2000

2400

0.00 1.25 2.50 3.75 5.00 6.25 7.50 8.75

Series: MAX

Sample 1 9700

Observations 9700

Mean 0.737026

Median 0.635628

Maximum 9.052741

Minimum 0.000000

Std. Dev. 0.621222

Skewness 2.110659

Kurtosis 15.76462

Jarque-Bera 73055.13

Probability 0.000000

Figure 2: Daily UPR of S&P500 Index, 1962/1-2000/8

Series: AMIN

Sample 1 9700

Observations 9700

Mean 0.727247

Median 0.598360

Maximum 22.90417

Minimum 0.000000

Std. Dev. 0.681298

Skewness 5.456951

Kurtosis 128.1277

Jarque-Bera 6376152.

Probability 0.0000000

1000

2000

3000

4000

5000

6000

7000

8000

0 2 4 6 8 10 12 14 16 18 20 22

Series: AMIN

Sample 1 9700

Observations 9700

Mean 0.727247

Median 0.598360

Maximum 22.90417

Minimum 0.000000

Std. Dev. 0.681298

Skewness 5.456951

Kurtosis 128.1277

Jarque-Bera 6376152.

Probability 0.000000

Figure 3: Daily DWNR of S&P500 Index, Unsigned, 1962/1-2000/8

Series: AMIN

Sample 1 9700

Observations 9699

Mean 0.724960

Median 0.598329

Maximum 8.814014

Minimum 0.000000

Std. Dev. 0.643037

Skewness 2.271508

Kurtosis 15.61285

Jarque-Bera 72630.55

Probability 0.0000000

400

800

1200

1600

2000

2400

0.00 1.25 2.50 3.75 5.00 6.25 7.50 8.75

Series: AMIN

Sample 1 9700

Observations 9699

Mean 0.724960

Median 0.598329

Maximum 8.814014

Minimum 0.000000

Std. Dev. 0.643037

Skewness 2.271508

Kurtosis 15.61285

Jarque-Bera 72630.55

Probability 0.000000

Figure 4: Daily DWNR w/o Crash, Unsigned, 1962/1-2000/8

Nobs Mean Median Max Min Std Dev 1

12 Q(12)

Full sample

RANGE 1/2/62-8/25/00 9700 1.464 1.407 22.904 0.145 0.76 0.629 0.575 0.443 30874

UPR 1/2/62-8/25/00 9700 0.737 0.636 9.053 0 0.621 0.308 0.147 0.172 3631

DWNR 1/2/62-8/25/00 9700 -0.727 -0.598 0 -22.9 0.681 0.326 0.181 0.162 4320

Before structural shift

RANGE 1/2/62-4/20/82 5061 1.753 1.643 9.326 0.53 0.565 0.723 0.654 0.554 21802

UPR 1/2/62-4/19/82 5061 0.889 0.798 8.631 0 0.581 0.335 0.087 0.106 1199

DWNR 1/2/62-4/19/82 5061 -0.864 -0.748 0 -6.514 0.559 0.378 0.136 0.163 2427

After structural shift

RANGE 4/21/82-8/25/00 4639 1.15 0.962 22.904 0.146 0.818 0.476 0.414 0.229 11874

UPR 4/21/82-8/25/00 4639 0.572 0.404 9.053 0 0.622 0.189 0.089 0.125 651

DWNR 4/21/82-8/25/00 4639 -0.578 -0.388 0 -22.9 0.767 0.247 0.147 0.101 994

Table 1: Summary Statistics of the Daily Range, Upward Range and Downward Range of

S&P500 Index, 1/2/1962-8/25/2000

0.05

0.10

0.15

0.20

0.25

0.30

0.35

20 40 60 80 100 120 140 160 180 200

RHO_UPR RHO_DWNR RHO_DWNR(w/o crash)

Figure 5: Correlograms of Daily UPR and DWNR

T ab le 2 : Q M L E E st im a tion of A C A R R Using D a ily U pw ar d R an ge of S& P 5 00 Ind ex

1/2 /1 96 2-8 /25 /2 00 0

t ~ iid f( .)

E s tima tio n is c a rr ied ou t us in g th e QM L E m e th od h enc e it 's equ iva lent to e stim a t in g a n E xp on en tia l AC A R R( X ) (p, q) or a nd E A C AR R (X ) (p ,q) m o de l . N u mbe rs in p a re nthe ses a re t-ra t ios ( p-v a lu es) w ith ro bu st stan da rd e rr ors fo r the m od el co ef fi cients ( Q sta t ist ic s). L L F is th e log l ike l ih oo d fun c tion .

A C A R R( 1,1 ) A C A R R( 2,1 ) A CA RR X ( 2,1 )-a A CA RR X ( 2,1 )-b A CA RR X ( 2,1 )-c

L L F -1 20 35 .2 0 -1 20 11 .8 6 -1 19 55 .7 8 -1 19 49 .6 4 -1 19 50 .3 2

con stan t 0. 00 2 [ 3.2 16 ] 0. 00 1 [ 3.1 45 ] -0. 00 2 [-0.6 10 ] -0. 00 3 [-0.5 51 ] -0. 00 4 [-0.9 73 ]

UP R( t-1 ) 0 .0 3 [ 8.8 73 ] 0. 14 5 [1 0.8 37 ] 0. 20 3 [1 4.0 30 ] 0. 17 9 [1 1.8 56 ] 0. 18 6 [1 2.8 45 ]

UP R( t-2 ) -0. 12 6 [-9.1 98 ] -0. 11 7 [-9 ..4 48 ] -0. 11 2 [-8.8 79 ] -0. 11 5 [-9.2 45 ]

( t-1 ) 0. 96 8 [ 26 7.9 93 ] 0. 97 8 [ 34 1.9 23 ] 0. 90 3 [ 69.6 43 ] 0. 87 1 [4 8.4 26 ] 0. 87 7 [5 2.9 42 ]

r( t-1 ) -0. 05 7 [-8.4 31 ] -0. 01 8 [-1.9 59 ] -0. 02 3 [-2.7 34 ]

T U E 0. 05 8 [ 3.4 23 ] 0. 05 9 [ 3.4 75 ] 0. 05 9 [ 3.4 81 ]

W E D 0 .0 2 [ 1.2 71 ]

SD 0 .0 00 0 [ 0.2 01 ] -0. 00 3 [-1 .6 47 ]

DW NR (-1 ) 0. 04 6 [ 4.8 68 ] 0. 04 2 [ 4.8 03 ]

Q (12 ) 18 4. 4 [ 0.0 00 ] 2 2. 34 6 [ 0.0 34 ] 2 2. 30 4 [ 0.0 34 ] 2 0. 28 2 [ 0.0 62 ] 2 0. 50 3 [ 0.0 53 ]

tttU P R

,1111

ltl

L

l

u

jt

q

j

ujit

p

i

ui

uut XU P R

T able 3 : Q M L E Es tim at io n o f ACA RR U sin g D aily Do wnw ard Rang e of S& P5 00 In dex

1/2 /1 9 62-8 /25 /2 0 00

t ~ iid f(.)

Estim atio n is carried ou t usin g th e QM LE m eth od h en ce it's equ ivalent to es timatin g an Ex po n en tial AC A RR (X )(p,q) or and EA CA R R(X)(p ,q) m odel. N um bers in p arentheses are t-ra tio s(p-values) with rob ust stan dard er ro rs for the m od el co eff icients ( Q statistics). LLF is the log likelihoo d fun ctio n.

A C AR R(1,1) A C AR R(2,1) AC A RR X(2,1)-a AC A RR X(2,1)-b AC A RR X(2,1)-c

LLF -11 92 9.39 -11 889.61 -11 87 3.54 -11 86 8.55 -11 87 0.14

con stan t 0 .0 14 [5.905] 0 .0 04 [4.088] 0 .0 17 [4.373] 0 .0 17 [3.235] 0 .0 17 [4.417]

DW N R (t-1) 0 .0 84 [11.834] 0 .2 29 [1 6.277] 0 .2 52 [1 6.123] 0 .2 33 [1 4.770] 0 .2 39 [1 6.364]

DW N R (t-2) -0 .1 95 [-1 3.489] -0 .1 89 [-1 2.811] -0 .1 85 [-1 2.594] -0 .1 86 [-1 2.897]

t-1 0 .8 97 [1 01 .02] 0 .9 61 [1 99 .02] 0 .9 27 [8 7.639] 0 .9 06 [6 1.212] 0 .9 11 [6 3.893]

r (t-1) 0 .0 23 [4.721] -0 .0 09 [-1.187]

TU E -0 .0 08 [0.503]

W ED -0 .0 51 [-3.582] -0 .0 53 [-3.617] -0 .0 52 [-3.587]

SD -0 .0 02 [-2.124] 0 .0 01 [0.904]

UP R(-1) 0 .0 37 [4.164] 0 .0 28 [5.084]

Q (12) 192 .8 [0.000] 18.94 [0.009] 22 .2 27 [0.035] 14 .4 22 [0.275] 14 .7 74 [0.254]

tttD W N R ltl

L

l

d

jt

q

j

djit

p

i

di

ddt XD W N R 1

111

-10

-8

-6

-4

-2

0

2

4

2000 4000 6000 8000

UPR_NEG LAMBDA_UPR

Figure 6: Expected and Observ ed Daily UPR, 1962/1-2000/8

-25

-20

-15

-10

-5

0

5

10

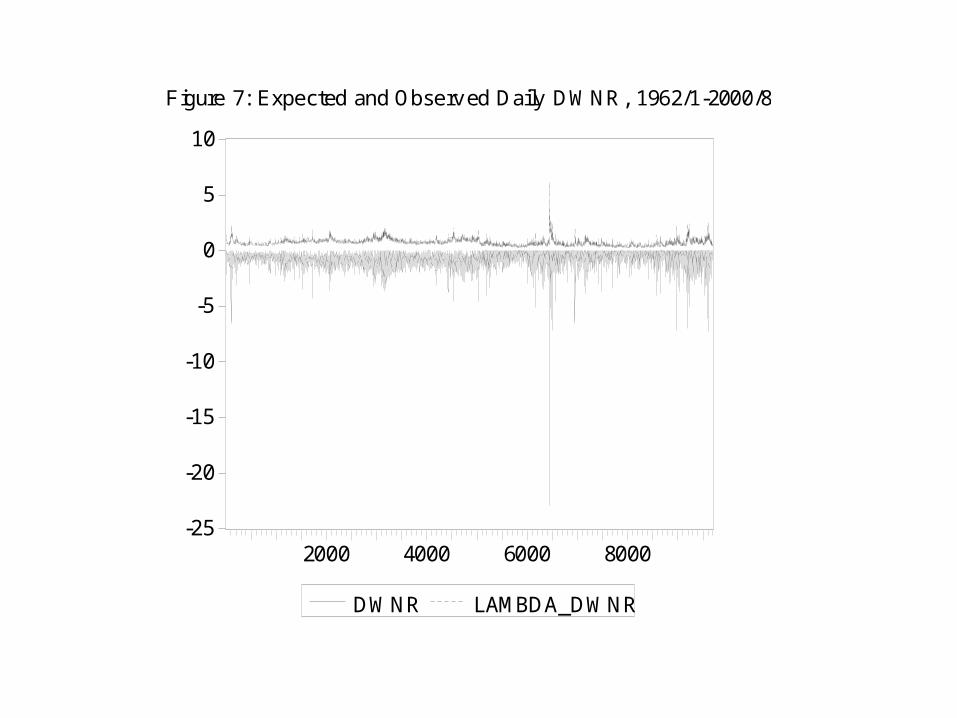

2000 4000 6000 8000

DWNR LAMBDA_DWNR

Figure 7: Expected and Observ ed Daily DWNR, 1962/1-2000/8

Series: ET_MAXSample 1 9700Observations 9700

Mean 1.233526Median 1.040290Maximum 29.61918Minimum 0.000000Std. Dev. 1.093848Skewness 3.854160Kurtosis 59.76949

Jarque-Bera 1326553.Probability 0.000000

0

1000

2000

3000

4000

5000

0 5 10 15 20 25 30

Series: ET_MAXSample 1 9700Observations 9700

Mean 1.233526Median 1.040290Maximum 29.61918Minimum 0.000000Std. Dev. 1.093848Skewness 3.854160Kurtosis 59.76949

Jarque-Bera 1326553.Probability 0.000000

Figure 8: Histogram of Daily et_UPR, 1962/1-2000/8

Series: ET_MIN

Sample 1 9700

Observations 9700

Mean 0.837894

Median 0.735879

Maximum 11.63559

Minimum 0.000000

Std. Dev. 0.688907

Skewness 2.306857

Kurtosis 18.96869

Jarque-Bera 111665.3

Probability 0.0000000

500

1000

1500

2000

2500

3000

3500

0 2 4 6 8 10 12

Series: ET_MIN

Sample 1 9700

Observations 9700

Mean 0.837894

Median 0.735879

Maximum 11.63559

Minimum 0.000000

Std. Dev. 0.688907

Skewness 2.306857

Kurtosis 18.96869

Jarque-Bera 111665.3

Probability 0.000000

Figure 9: Histogram of daily et_DWNR, 1962/1-2000/8

0

2

4

6

8

10

0 2 4 6 8 10

ET_UPR

Ex

po

ne

ntia

l Qu

an

tile

Figure 10: Q-Q Plot of et_UPR

0

2

4

6

8

1 0

0 2 4 6 8 1 0

E T _ D W N R

Exp

on

en

tia

l Q

ua

nti

leF ig u re 1 1 : Q -Q p lo t o f e t-D W N R

Figure 11: Q-Q plot of et-DWNR

Ta ble 4: A C A R R v e rsu s C A R R

In -s am p le V ola ti l ity For ec a st Co m pa r iso n U sin g T hre e M ea su re d V ola ti l it ie s as Be nc h m a rks.

T he thre e m e a sur e s of vo la t il i ty a re R N G , R ET S Q a nd A R E T : re spe c tiv ely,

da i ly ra n ge s, sq ua re d -da i ly -re turn s , a n d a bso ul te da i ly - r etu rn.

A CA R R (1 ,1) m od e l i s f it t ed fo r th e ra ng e ser ie s a n d a A CA RR m o de ls a re fi t te d fo r the u pw ar d r an ge

an d th e do w nw a rd ra ng e ser ie s. F V (C A R R) (F V (A CA R R )) is th e for e ca ste d v ola ti li ty u s ing CA RR ( A CA RR ).

( FV ( A CA RR )) i s th e fo re ca ste d ra ng e using the su m o f the f orc a sted u pw a rd r an ge a nd d ow n w a rd ra n ge .

P ro pe r tr an sfo rm a t io ns a r e m ad e fo r a d ju sting the d if fe re nc e b etw e e n a va ria nc e e stim a to r

an d a s ta n da rd -de v ia t io n e st im ator . N u m be rs in p ar en the se s a re t -ra tios .

M V t = a + b FV t(C A R R) + ut

M V t = a + c F V t(A C A R R) + ut

M V t = a + b FV t(C A R R) + c F V t(A C A R R) + ut

M e as ure d V o la t il i ty E x plan a to ry V a ria ble s

c o nsta nt FV (C A R R) FV ( A C A R R) A d j . R -sq. S .E .

R N G -0. 06 7 [-0 .36 6] 1 .0 05 [9 6.2 9] 0 .4 89 0 .5 43

R N G -0 .0 06 [-4 .14 8] 1 .0 47 [ 10 1.0 2] 0 .5 13 0 .5 31

R N G -0 .0 67 [0 .63 2] 0 .0 21 [ 0.4 6] 1 .0 26 [2 1.8 3] 0 .5 13 0 .5 31

RE T SQ -1 .2 03 [-1.3 5] 0 .3 97 [1 4.2 5] 0. 02 5 .7 25

RE T SQ -0 .2 65 [-2.9 4] 0 .4 59 [1 6.0 2] 0 .0 26 5 .7 09

RE T SQ -0 .2 49 [-2.7 6] -0 .1 91 [-2.3 2] 0 .6 44 [ 7.6 1] 0 .0 26 5 .7 08

A R E T 1 .1 42 [ 7.4 1] 0 .3 34 [2 7.0 7] 0. 07 0 .6 42

A R E T 0 .1 13 [ 5.8 5] 0 .3 54 [2 8.2 8] 0 .0 76 0 .6 39

A R E T 0 .1 15 [ 5.9 5] -0 .1 06 [-1.9 1] 0 .4 58 [ 8.0 9] 0 .0 76 0 .6 39

Extensions

• Robust ACARR – Interquartile range

• Multivariate ACARR

• Nonparametric or semiparametric ACARR

• Other data sets and simulations

• Long memory ACARR’s – IACARR, FIACARR,…

• ACARR and option price models

Conclusion

• ACARR is effective in modeling upward and downward market movements.

• Asymmetry found: dynamics, leverage effect, periodic patterns, interaction terms

• CARR provides more accurate volatility forecasts than GARCH (Chou (2001)) and ACARR gives further improvements.