Model Tax Conventions - Michael Honiball · 3 Model Tax Treaties • Read the introduction to the...

17

1 Model Tax Conventions © Webber Wentzel 2012 Lecture given by Professor Michael Honiball Partner, Webber Wentzel Presented at the University of Johannesburg 15 February 2012

Transcript of Model Tax Conventions - Michael Honiball · 3 Model Tax Treaties • Read the introduction to the...

1

Model Tax Conventions

© Webber Wentzel 2012

Lecture given by Professor Michael Honiball

Partner, Webber Wentzel

Presented at the University of Johannesburg

15 February 2012

2

Model Tax Treaties

• Introduction;

• Model Tax Treaties:

o General;

o Types of Treaties;

o Scheme of Model Treaties;

o Taxes Covered by Treaties

o Persons Covered;

o Entry into Force and Termination;

• South African Treaties:

o Treaties in Force;

o Procedure for Entering into Treaties;

• Eligibility for Treaty Benefits.

Overview

3

Model Tax Treaties

• Read the introduction to the OECD MTC Commentary;

• Need to standardise the fiscal treatment of taxpayers engaged in cross-border

transactions;

• OECD Council recommends that members conform to the OECD MTC;

• South Africa is not an OECD Member State;

• Historical background-leader and forerunner;

• Wide influence of the OECD MTC;

• Difference between bilateral and multilateral tax agreements;

• OECD MTC seeks to specify a single rule for each situation.

Introduction

4

Model Tax Treaties

• OECD MTC:

o Chapter 1: Scope of the Treaty;

o Chapter 2: Some Definitions;

o Chapter 3: Distributive Rules;

o Chapter 4: Taxation of Capital;

o Chapter 5: Double Tax Relief;

o Chapter 6: Special Provisions;

o Chapter 7: Entry into Force and Termination;

• UN MTC:

o Source country is awarded taxing rights in more instances

• US MTC;

• SA MTC.

General

5

Model Tax Treaties

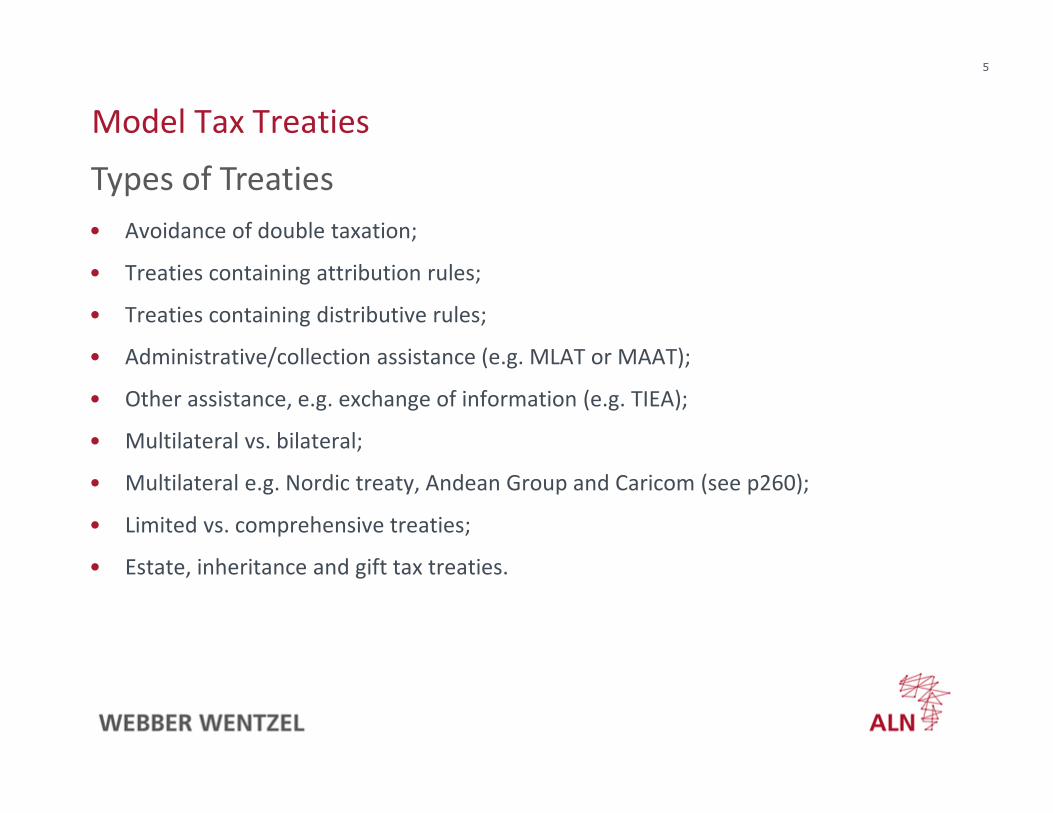

• Avoidance of double taxation;

• Treaties containing attribution rules;

• Treaties containing distributive rules;

• Administrative/collection assistance (e.g. MLAT or MAAT);

• Other assistance, e.g. exchange of information (e.g. TIEA);

• Multilateral vs. bilateral;

• Multilateral e.g. Nordic treaty, Andean Group and Caricom (see p260);

• Limited vs. comprehensive treaties;

• Estate, inheritance and gift tax treaties.

Types of Treaties

6

Model Tax Treaties

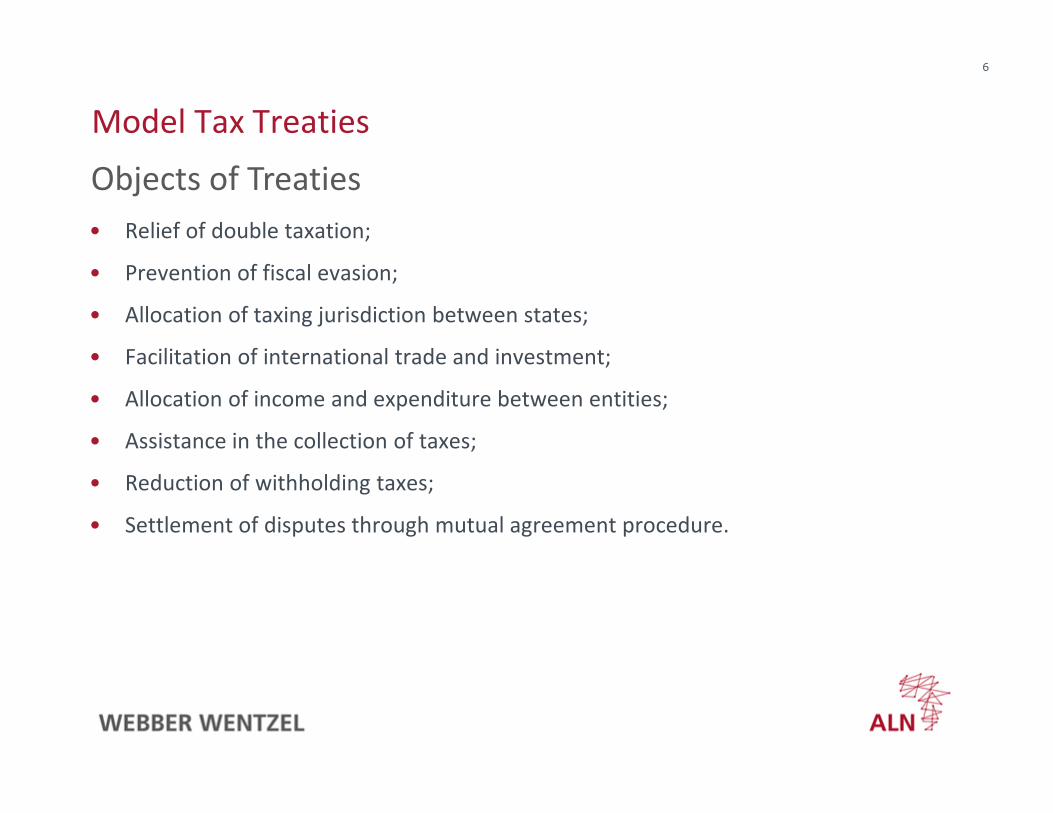

• Relief of double taxation;

• Prevention of fiscal evasion;

• Allocation of taxing jurisdiction between states;

• Facilitation of international trade and investment;

• Allocation of income and expenditure between entities;

• Assistance in the collection of taxes;

• Reduction of withholding taxes;

• Settlement of disputes through mutual agreement procedure.

Objects of Treaties

7

Model Tax Treaties

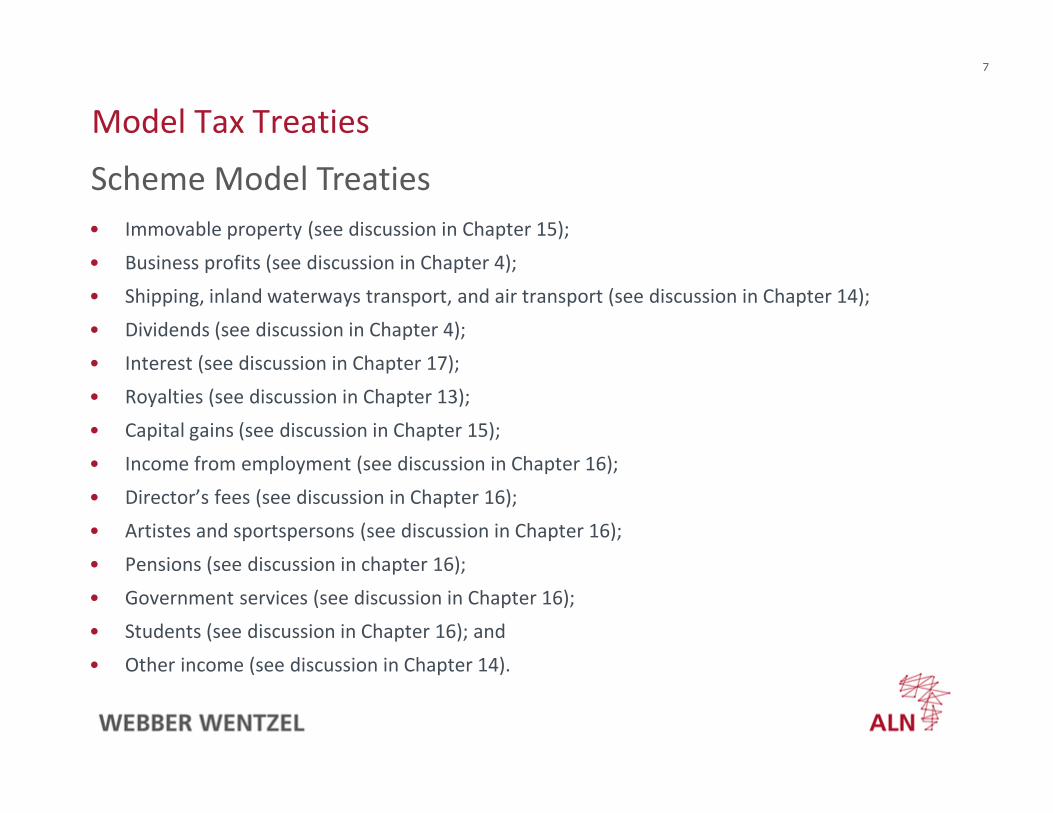

• Immovable property (see discussion in Chapter 15);

• Business profits (see discussion in Chapter 4);

• Shipping, inland waterways transport, and air transport (see discussion in Chapter 14);

• Dividends (see discussion in Chapter 4);

• Interest (see discussion in Chapter 17);

• Royalties (see discussion in Chapter 13);

• Capital gains (see discussion in Chapter 15);

• Income from employment (see discussion in Chapter 16);

• Director’s fees (see discussion in Chapter 16);

• Artistes and sportspersons (see discussion in Chapter 16);

• Pensions (see discussion in chapter 16);

• Government services (see discussion in Chapter 16);

• Students (see discussion in Chapter 16); and

• Other income (see discussion in Chapter 14).

Scheme Model Treaties

8

Model Tax Treaties

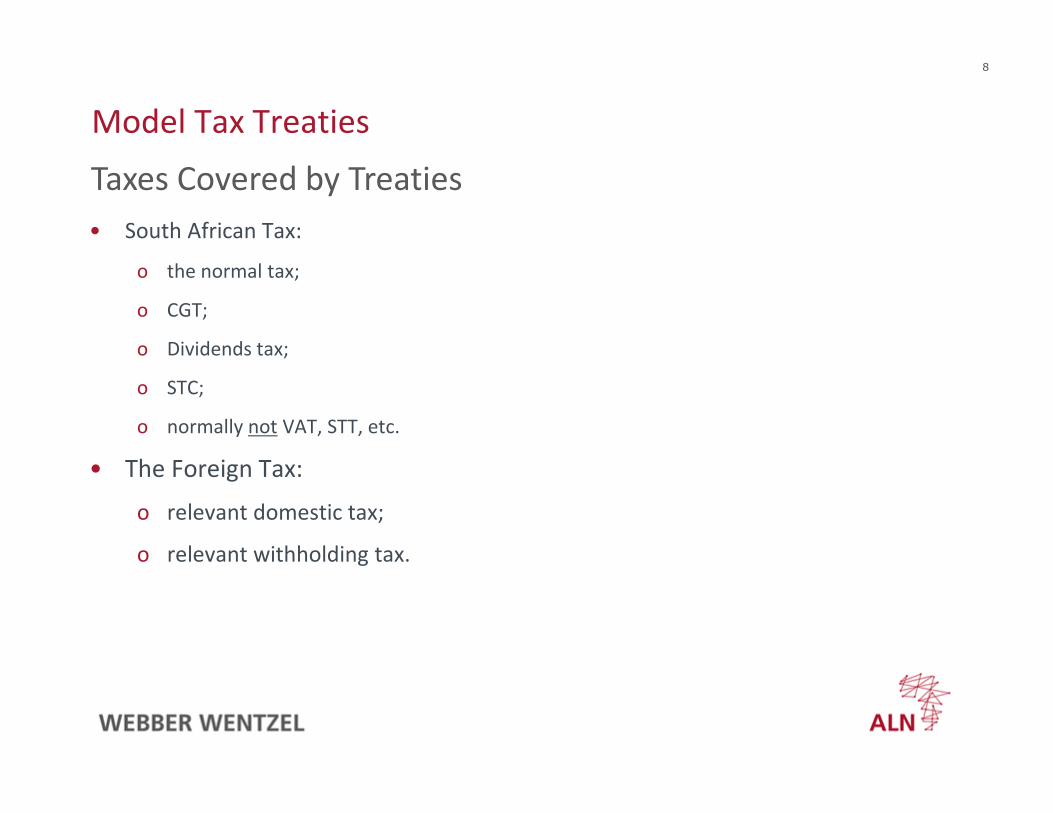

• South African Tax:

o the normal tax;

o CGT;

o Dividends tax;

o STC;

o normally not VAT, STT, etc.

• The Foreign Tax:

o relevant domestic tax;

o relevant withholding tax.

Taxes Covered by Treaties

9

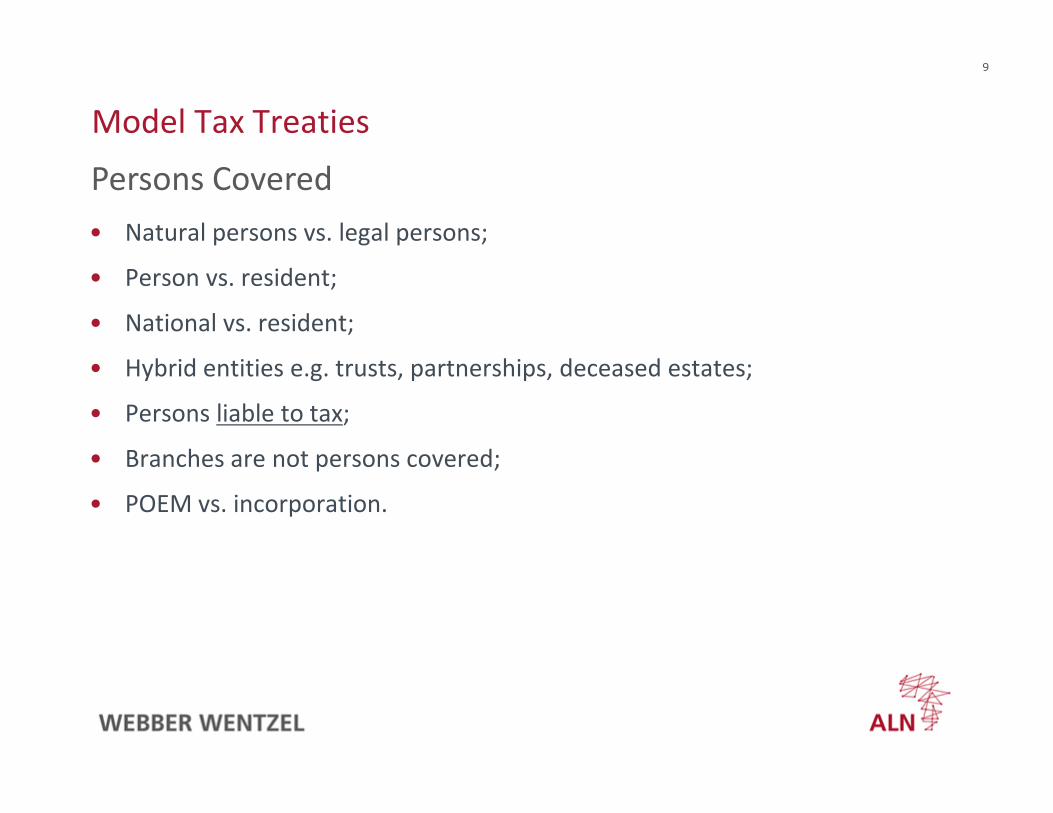

Model Tax Treaties

• Natural persons vs. legal persons;

• Person vs. resident;

• National vs. resident;

• Hybrid entities e.g. trusts, partnerships, deceased estates;

• Persons liable to tax;

• Branches are not persons covered;

• POEM vs. incorporation.

Persons Covered

10

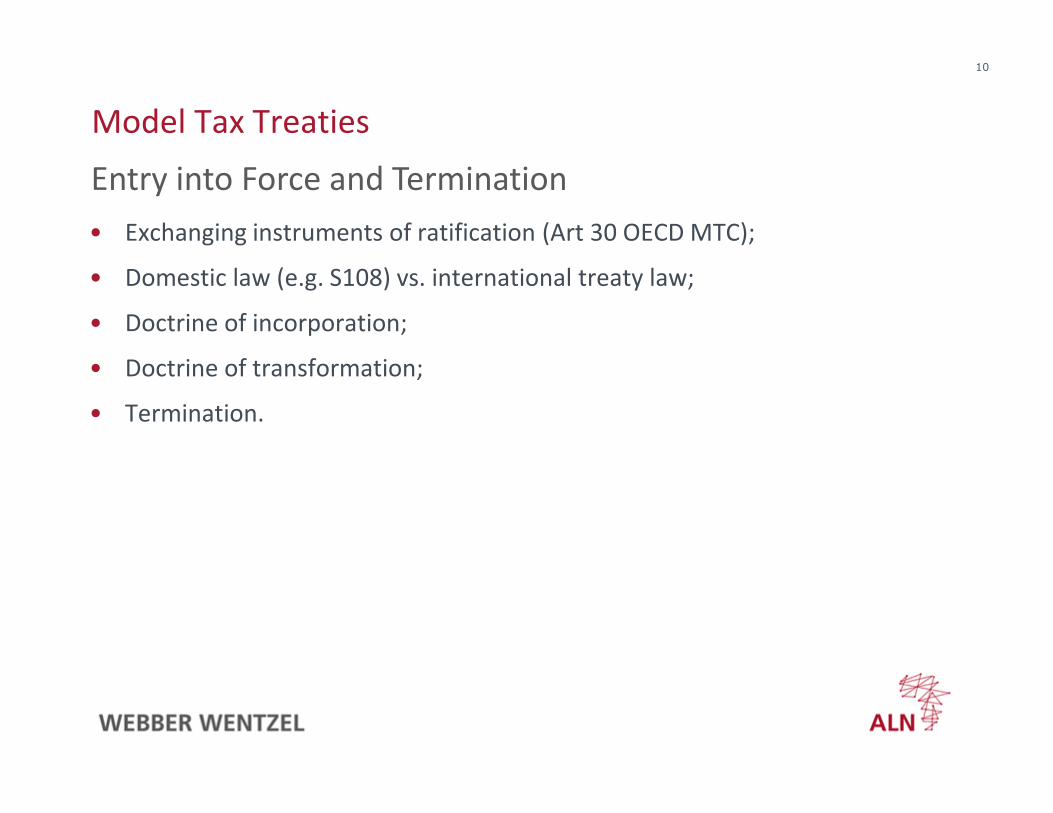

Model Tax Treaties

• Exchanging instruments of ratification (Art 30 OECD MTC);

• Domestic law (e.g. S108) vs. international treaty law;

• Doctrine of incorporation;

• Doctrine of transformation;

• Termination.

Entry into Force and Termination

11

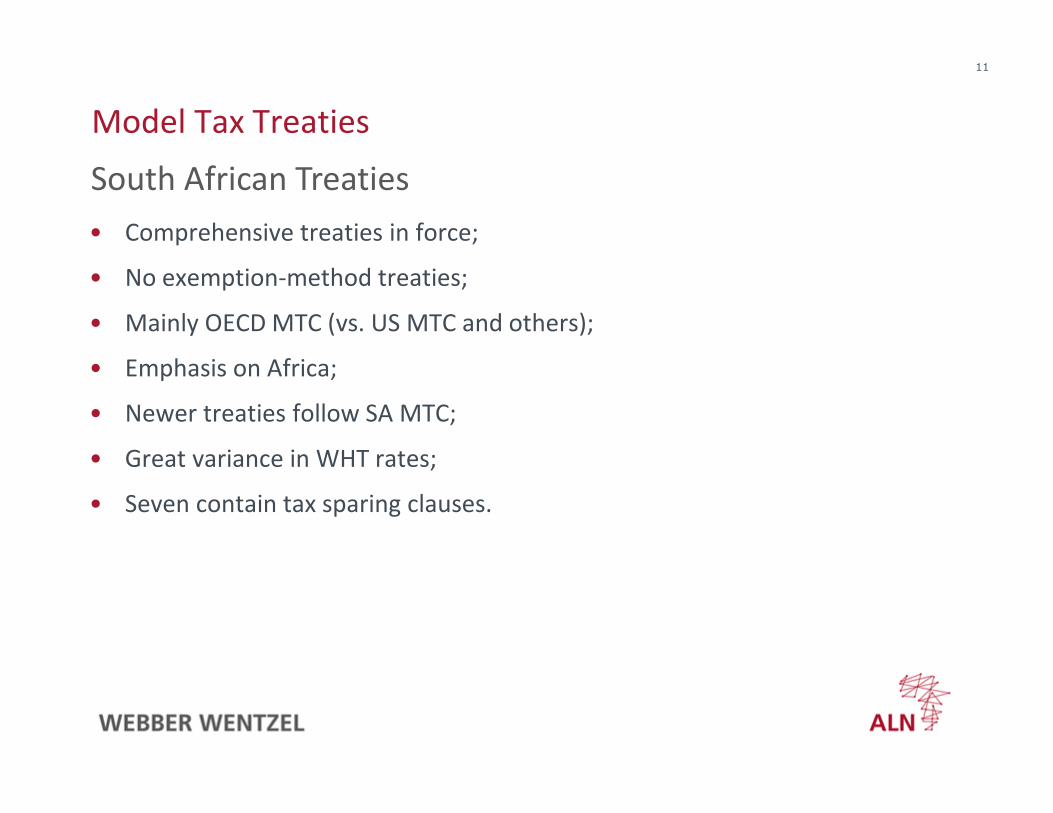

Model Tax Treaties

• Comprehensive treaties in force;

• No exemption-method treaties;

• Mainly OECD MTC (vs. US MTC and others);

• Emphasis on Africa;

• Newer treaties follow SA MTC;

• Great variance in WHT rates;

• Seven contain tax sparing clauses.

South African Treaties

12

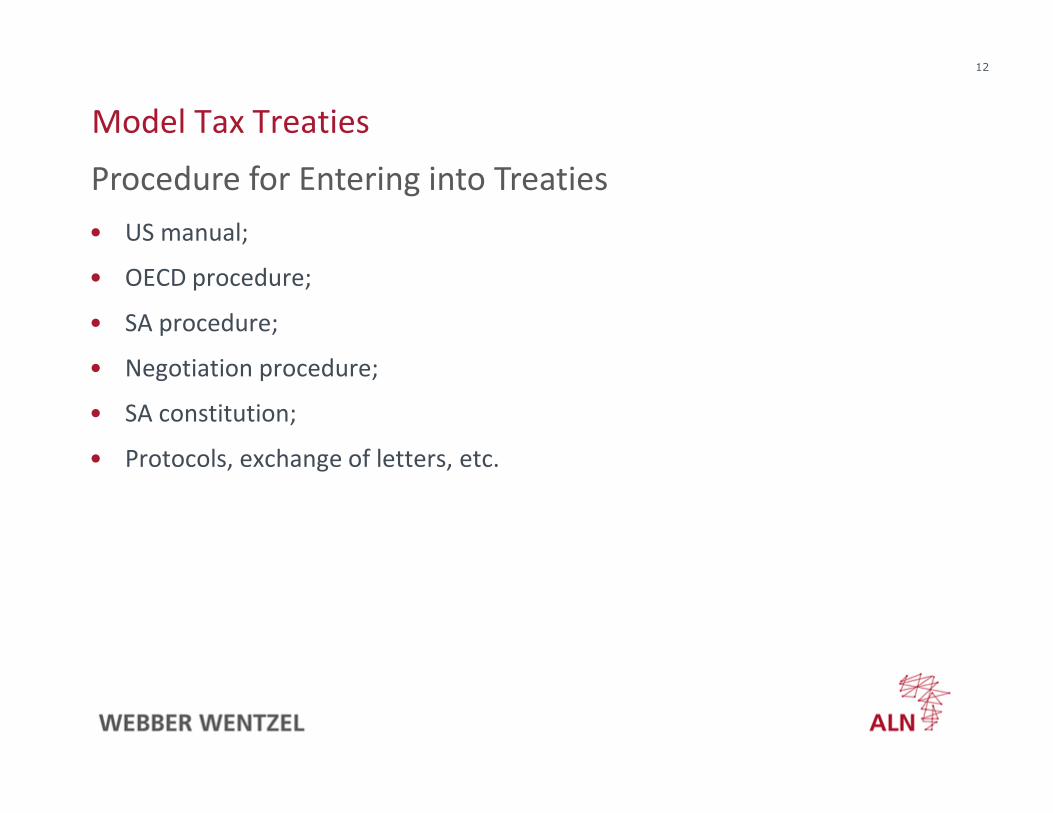

Model Tax Treaties

• US manual;

• OECD procedure;

• SA procedure;

• Negotiation procedure;

• SA constitution;

• Protocols, exchange of letters, etc.

Procedure for Entering into Treaties

13

Model Tax Treaties

• Usually restricted to residents;

• Third State/triangular situations;

• Triangular example;

• Overseas case law.

Eligibility for Treaty Benefits

14

Prescribed and Recommended Reading

• Olivier & Honiball : International Tax : A South African Perspective 2011

(Chapters 9 and 10) – prescribed;

• Roy Rohatgi: Basic International Taxation – 2nd Edition, Volume 1 (Richmond

2005) (Chapter 3) – recommended;

• OECD MTC and Commentary – highly recommended;

• Silke on International Tax (LexisNexis 2010) (Chapter 12) – recommended.

15

QUESTIONS?

16

Presenter’s Details:

Professor Michael Honiball

Partner, Webber Wentzel

Tel: +27 11 530 5269

Fax: +27 11 530 6269

Email: [email protected]

Websites: www.michaelhoniball.com

www.webberwentzel.com

17

BOTSWANA

BURUNDI

ETHIOPIA

KENYA

MALAWI

MAURITIUS

MOZAMBIQUE

RWANDA

SOUTH AFRICA

TANZANIA

UGANDA

ZAMBIA

Legal Notice: these materials are for training purposes only and do not constitute legal or other professional advice.

www.webberwentzel.com

JOHANNESBURG

10, 16 & 18 Fricker Road,

Illovo Boulevard,

Johannesburg, 2196, South Africa

PO Box 61771, Marshalltown,

Johannesburg, 2107, South Africa

T +27 11 530 5000

CAPE TOWN

15th floor, Convention Tower,

Heerengracht, Foreshore,

Cape Town, 8001, South Africa

PO Box 3667, Cape Town,

8000, South Africa

T +27 21 431 7000