![MODEL GST LAW - eicmai.orgeicmai.org/Uploaded-Files/Chapters/31.pdfProposed Indirect Tax Structure under GST 1] ... Optional Compounding scheme for taxpayers having taxable ... MODEL](https://static.fdocuments.in/doc/165x107/5abff9a07f8b9ac6688b95ec/model-gst-law-indirect-tax-structure-under-gst-1-optional-compounding-scheme.jpg)

Model GST Law - Manupatra ELP/2016/ELP...Section 2(7) of the Sales of Goods Act, 1930. Also by way...

45

An Analysis Model GST Law AN ANALYSIS

Transcript of Model GST Law - Manupatra ELP/2016/ELP...Section 2(7) of the Sales of Goods Act, 1930. Also by way...

A n A n a ly s i s M o d e l G S T La w

0 | P a g e © E c o n o m ic L a w s P r a c t i c e

Model GST Law

AN ANALYSIS

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 1

CONTENTS

Preface ....................................................................................................................................................................... 2

Preliminary ................................................................................................................................................................. 3

Levy of, and Exemption From, Tax ..............................................................................................................................10

Time and Value of Supply ..........................................................................................................................................12

Input Tax Credit .........................................................................................................................................................16

Compliances ..............................................................................................................................................................19

Refunds .....................................................................................................................................................................24

Electronic Commerce .................................................................................................................................................26

Assessment and Audit ............................................................................................................................................... 27

Inspection, Search, Seizure, Arrest; Offences & Penalties; Prosecution & Compounding ...........................................28

Appeals & Revision ....................................................................................................................................................32

Advance Ruling ..........................................................................................................................................................34

Settlement of Cases ...................................................................................................................................................35

Other Provisions ........................................................................................................................................................36

Transitional Provisions ............................................................................................................................................... 37

Schedules ..................................................................................................................................................................39

The Integrated Goods and Services Tax Act, 2016 ......................................................................................................40

Glossary of Terms ......................................................................................................................................................43

A n A n a ly s i s M o d e l G S T La w

2 | P a g e © E c o n o m ic L a w s P r a c t i c e

PREFACE

Dear Reader,

In what is a watershed event on the road to the Goods and Services Tax in India, the Government has released a draft

version of the ‘Model GST Law’ into the public domain earlier this week. With this development, while the passage of

the GST Constitution (122nd) Amendment Bill during the monsoon session is awaited, industry and other stakeholders

will be able to provide their inputs and comments on the draft, which will form the basis for the eventual GST

legislations.

Spanning nearly 200 pages, comprising the CGST/ SGST Act, GST

Valuation (Determination of Value of Supply of Goods and Services)

Rules and the IGST Act, the model law has made a laudatory attempt

to codify the existing indirect tax provisions under Customs law,

Central Excise law, Service tax law, VAT laws, etc. Notably, some of the

very latest amendments introduced as recently as in the Union Budget

2016-17 have found their way into the model law. And, it is also

significant that certain new concepts that the GST, by its nature,

necessitates, have been introduced (e.g. ‘continuous supply of goods’,

‘business vertical’, ‘recipient’, ‘zero-rated supply’ etc.) and varied

scenarios/ transactions have been envisaged and legislatively

addressed (e.g. taxability of intangibles, taxability of barter, job work,

transactions in respect of deemed export etc.).

At the same time, there is some distance to cover in terms of ironing

out the wrinkles in the draft and addressing areas of incompleteness,

as well as absorbing inputs that industry will come to provide,

especially where the particularities of a sector warrant special

dispensation under the law. Industry must endeavor that an impactful

contribution to the shaping of the GST law is made at this critical

juncture, so as to transition to a statutory framework that is expected

to govern all aspects of the levy (on all transactions) for the

foreseeable future.

While the Empowered Committee has given its in-principle nod to the present draft of the model law, once the draft is

in its final form, the next important challenge will lie in ensuring that States adopt and enact the model law in its fullest

form, to ensure uniformity of the levy and its consistent administration, as also the concept of “unified market” that

has been central to the proposed GST regime since its inception.

We, at ELP, have undertaken an analysis of the various provisions under the model law and we hope you find this

analysis informative and useful. Please revert with your comments and questions.

Thank you, as always, for your support.

Warm Regards,

Rohan Shah | Managing Partner

Outstanding Firm for Tax in India - Asialaw

Profiles 2016

Winner of Best Tax Firm in India Award -

LegalEra Awards 2014 & 2015

Winner of Taxation Firm of the Year Award -

India Business Law Journal’s Indian Law Firm

Awards 2009 to 2015

Top Tier firm for Tax in India - Chambers Asia-

Pacific 2011 to 2016

Top Tier firm for Tax in India - The Legal500

Asia-Pacific 2014 to 2016

Recommended as a Tier 1 law firm in Mumbai,

India - Tax Director’s Handbook 2014 to 2016

Recommended as a Tier 2 firm in India - World

Tax 2013 to 2016

Winner of Best Transfer Pricing Firm in India

Award - World Finance Legal Awards 2014

Our Achievements

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 3

PRELIMINARY

S H O RT T I T L E , E X T E N T A N D CO M M E N C E M E N T [ S E C T I O N 1 ]

The Model Goods and Services Tax Act, 2016 applies to the whole of India and the respective State, as the case may

be.

Analysis

For the first time, the State of Jammu and Kashmir has not been excluded as regards the application of the tax regime

that is applicable to the rest of India.

D E F I N I T I O N S [ S E C T I O N 2 ]

Some of the key and new definitions are:

Term Definition Analysis

address of delivery [Section 2(2)]

The address of the recipient of goods and/or services indicated on the tax invoice issued by the taxable person for delivery of such goods and / or services.

Definition is now used in the Model law.

The “address on record” may be different.

aggregate turnover [Section 2(6)]

Aggregate value of all taxable and non taxable supplies, exempt supplies, and export of goods and / or services of a person having the same PAN, but excludes: taxes paid under GST, if any, inward supplies (defined to mean receipt of goods

and/or services whether by purchase, acquisition or any other means and whether or not for any consideration), and

tax paid under reverse charge basis.

The definition is wide enough to include all the supplies by a person whether liable to tax or exempt.

Such turnover is required to be computed on pan-India basis for a PAN.

turnover in a State [Section 2(104)]

“turnover in a State” means the aggregate value of all taxable and non-taxable supplies, including exempt supplies and exports of goods and / or services made within a State by a taxable person and inter-state supplies of goods and / or services made from the State by the said taxable person excluding taxes, if any charged under the CGST Act, SGST Act and the IGST Act, as the case may be.

The definition is wide enough to include all the supplies by a person within the State and inter-state supplies.

business [Section 2(17)]

Includes: any trade, commerce, manufacture, profession,

vocation or any other similar activity, whether or not it is for a pecuniary benefit, any transaction in connection with or incidental or

ancillary thereto any transaction in the nature specified above,

whether or not there is volume, frequency, continuity or regularity of such transaction.

supply or acquisition of goods including capital assets and services in connection with commencement or closure of business,

provision by a club, association, society, or any such body (for a subscription or any other consideration) of the facilities or benefits to its members as the case may be,

admission, for a consideration, of persons to any premises, and

While the definition of ‘business’ does not exist in the present Excise / Service tax Law, the same has been defined under the CST Act / State VAT legislations.

The Model law appears to have borrowed the term from the latter. This definition assumes significance as the proposed levy is qua activities undertaken in the course or furtherance of business.

Profession and vocation has also now been included within the definition of business.

A n A n a ly s i s M o d e l G S T La w

4 | P a g e © E c o n o m ic L a w s P r a c t i c e

Term Definition Analysis

services supplied by a person as the holder of an office which has been accepted by him in the course or furtherance of his trade, profession or vocation.

business vertical [Section 2(18)]

The term ‘business vertical’ shall have the meaning assigned to a ‘business segment’ in the AS-17 issued by the Institute of Chartered Accountants of India.

The AS-17 prescribes principles for segmental reporting in the financial information for different types of products and services that an enterprise produces. The said AS defined ‘business segment’ to mean a distinguishable component of an enterprise that is engaged in providing an individual product or service or a group of related products or services and that is subject to risks and returns that are different from those of other business segments. The said AS further provides factors that should be considered in determining whether products or services are related.

This definition is relevant since there may be separate registrations for different business verticals.

This definition is also relevant in respect of input service distribution.

capital goods [Section 2(20)]

The definition of ‘capital goods’ under the Model law is similar to the definition under Rule 2(a) of the CCR.

composite supply [Section 2(27)]

Means a supply consisting of – Two or more goods; Two or more services; or A combination of goods and services. Provided in the course of furtherance of business, whether or not the same can be segregated

This is a new concept that has been introduced, which inter alia includes any combination of supplies of two or more goods and / or services.

Relevance: Goods or services combined but bearing differential rates

No usage of the definition in present draft

This provision is silent in respect of transactions which include immovable property. In a recent decision of the Hon’ble Delhi High Court [Suresh Kumar Bansal & Others vs. Union of India & Others, Judgement dated 03-06-2016 in W.P. (C) 2235/2011 and W.P. (C) 2971/2011], it was held that there is no effective machinery provision to tax the service element in composite construction services, as the valuation provisions in their

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 5

Term Definition Analysis

present form refer to exclusion of goods from the value of composite contracts to arrive at the services value, but do not contain any provisions to exclude the value of immovable property while arriving at the value of services in a composite contract having elements of transfer of goods/immovable property and provision of services.

Consideration [Section 2(28)]

The term ‘consideration’ has been defined to include: any payment made or to be made, whether in money

or otherwise, the monetary value of any act or forbearance, whether

or not voluntary, in respect of, in response to, or for the inducement of, the supply of goods and/or services, whether by the person or by any other person.

A deposit, whether refundable or not, given in respect of the supply of goods and/or services shall not be considered as payment made for the supply unless the supplier applies the deposit as consideration for the supply.

Deposits whether refundable or not will not be treated as consideration till the time such deposit is appropriated towards consideration for supply by the supplier.

Payment made “otherwise” than in money would also constitute consideration.

continuous supply of goods [Section 2(30)]

A supply of goods on a continuously or on recurrent basis under a contract whether or not, by means of a wire, cable, pipelines or other conduit the supplier issue invoices on regular or periodic basis.

This phrase has been defined for the first time.

deemed exports [Section 2(37)]

‘Deemed exports’ as notified by the Central Government / State Government on the recommendation of the GST Council, refer to transactions: Where goods supplied do not leave India, and Payment for such supplies is received either in Indian

Rupees, or in convertible foreign exchange.

The definition of ‘deemed exports’ has been incorporated from the Foreign Trade Policy 2015-2020.

goods [Section 2(48)]

Means every kind of movable property other than actionable claim and money, and includes securities, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under the contract of supply. For the purpose of this clause, the term ‘movable property’ shall not include any intangible property.

This definition is identical to the definition of ‘goods’ contained in Section 2(7) of the Sales of Goods Act, 1930. Also by way of explanation, it has been clarified that intangible properties will not fall under the category of goods.

Inputs [Section 2(54)]

Means any goods other than capital goods, subject to exceptions as may be prescribed, used or intended to be used by a supplier for making an outward supply In the course or furtherance of business.

This definition provides that the goods are to be actually used for the purpose of outward supply or are intended to be used for the purpose of outward supply to qualify as inputs. Further, similar to the present exclusion in the inputs as defined under Rule 2(l) of CCR, once a good qualifies as capital goods, it will not be considered as inputs. The requirement that inputs be used at the place of business has not been specified under the above definition. No exceptions have been prescribed

A n A n a ly s i s M o d e l G S T La w

6 | P a g e © E c o n o m ic L a w s P r a c t i c e

Term Definition Analysis

as yet.

market value [Section 2(67)]

Means full amount which a recipient of a supply is required to pay in order to obtain the goods and/or services of like kind and quality at or about the same time, and at the same commercial level where the recipient and the supplier are not related.

This definition has been adopted from certain State VAT legislations.

place of business [Section 2(75)]

Includes: a place from where the business is ordinarily carried

on, and includes a warehouse, a godown or any other place where a taxable person stores his goods, provides or receives goods and/or services; or

a place where a taxable person maintains his books of account; or

a place where a taxable person is engaged in business through an agent, by whatever name called.

Hitherto, place of business was not defined. The definition broadly borrows from the definition of ‘place of removal’ under the CE Act, while expanding the same to include a place where a person maintains his books of account.

Recipient (Section 2(80)]

‘Recipient of supply of goods and/or services’ has been defined to mean: where a consideration is payable for the supply of

goods and/or services, the person who is liable to pay that consideration,

where no consideration is payable for the supply of goods, the person to whom the goods are delivered or made available, or to whom possession or use of the goods is given or made available, and

where no consideration is payable for the supply of a service, the person to whom the service is rendered,

and any reference to a person to whom a supply is made shall be construed as a reference to the recipient of the supply; Explanation.- The expression “recipient” shall also include an agent acting as such on behalf of the recipient in relation to the goods and/or services supplied.

The term recipient has been defined for the first time. In the past there have been issues as regards who would be considered to be the service recipient where the beneficiary of services differs from the person making payment for such services. This definition puts to rest these issues, and is in line with the judgements of the CESTAT in the cases of Paul Merchants Ltd. v. CCE, Chandigarh [2013 (29) S.T.R. 257 (Tri. - Del.)], GAP International Sourcing (India) Pvt. Ltd. v. CST, Delhi [TS-61-Tribunal-2014-ST] and Vodafone Essar Cellular Ltd. vs. CCE, Pune-III [2013 (31) STR 738 (Tri-Mum).

related persons [Section 2(82)]

Persons shall be deemed to be ‘related persons’ only if: they are officers or directors of one another’s

businesses, they are legally recognized partners in business, they are employer and employee, any person directly or indirectly owns, controls or holds

five per cent or more of the outstanding voting stock or shares of both of them,

one of them directly or indirectly controls the other, both of them are directly or indirectly controlled by a

third person, together they directly or indirectly control a third

person, they are members of the same family. It is clarified that (i) the term ‘person’ also includes legal persons; and (ii) persons who are associated in the business of one another in that one is the sole agent or sole distributor or sole concessionaire, howsoever described, of the other shall be deemed to be related.

This definition has been adopted from the Customs Valuation Rules. The only modification appears to be that under the Customs Valuation Rules persons who are associated in the business of one another where one is the sole agent or sole distributor or sole concessionaire, have to meet one of the eight specified criteria to qualify as being ‘related’; however, under the Model law persons associated in the business of one another shall qualify as ‘related persons’ merely by virtue of being the sole agent or sole distributor or sole concessionaire.

reverse charge [Section 2(85)]

Means the liability to pay tax by the person receiving goods and/or services instead of the person supplying the goods and/or services in respect of such categories of supplies as the Central or a State Government may, on the recommendation of the Council, by notification, specify.

This term has been defined for the first time.

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 7

Term Definition Analysis

Services [Section 2(88)]

‘Services’ has been defined to mean anything other than goods. Explanation to the definition provides that services include transactions in intangible property and actionable claim but does not include money.

Whether a transaction in intangible property constitutes goods or services has been a recurring issue under the present indirect tax law. The Model law leaves no scope for such disputes, since the definition of ‘goods’ expressly excludes, and the definition of ‘service’s expressly includes, ‘intangible property’. ‘Intangible property’ is defined to mean any property other than tangible property, and ‘tangible property’ has been defined to mean any property that can be touched or felt.

works contract [Section 2(107)]

Means an agreement for carrying out for cash, deferred payment or other valuable consideration, building, construction, fabrication, erection, installation, fitting out, improvement, modification, repair, renovation or commissioning of any moveable or immovable property.

The definition has been adopted from State VAT enactments.

zero-rated supply [Section 2(109)]

Refers to a supply of any goods and/or services on which no tax is payable but credit of the input tax related to that supply is admissible. It is clarified that exports shall be treated as zero-rated supply.

This term has been defined for the first time.

M EA N I N G A N D S CO P E O F ‘ S U P P LY ’ [ S EC T I O N 3 ]

Supply of Goods and/or services to include:

all forms of supply of goods/ services such as sale, transfer, barter, exchange, license, rental, lease or disposal, for

consideration

importation of services whether or not for a consideration, and whether or not in the course or furtherance of

business

supplies specified in Schedule I, made or agreed to be made without consideration, viz.

Permanent transfer/disposal of business assets

Temporary application of business assets to a private or non-business use

Services put to a private or non-business use

Assets retained after deregistration

Supply of goods and/ or services by a taxable person to another taxable or non-taxable person in the course

or furtherance of business

supply of goods by a registered taxable person to a job-worker not to be treated as supply of goods

Schedule II is to be applied for determining ‘what is or is to be treated as a supply of goods or services’.

Particulars of Supply

Nature of Transactions To be Treated as Supply of

Transfer Title in goods. Goods

Goods or of right in goods or of undivided share in goods without the transfer of title thereof.

Services

Title in goods under an agreement which stipulates that property in goods will pass at a future date upon payment of full consideration as agreed.

Goods

Transfer of business assets

Where goods forming part of the assets of a business are transferred or disposed of by or under the directions of the person carrying on the business, whether or not for a consideration.

Goods

A n A n a ly s i s M o d e l G S T La w

8 | P a g e © E c o n o m ic L a w s P r a c t i c e

Particulars of Supply

Nature of Transactions To be Treated as Supply of

Goods held or used for the purposes of the business are put to any private use or are used, or made available to any person for use, for any purpose other than a purpose of the business, whether or not for a consideration.

Services

Where any goods, forming part of the business assets of a taxable person, are sold by any other person to recover any debt owed by the taxable person.

Goods

Where a person ceases to be a taxable person, any goods forming part of the assets of any business carried on by him shall be deemed to be supplied by him in the course or furtherance of his business immediately before he ceases to be a taxable person, unless— the business is transferred as a going concern to another person; or the business is carried on by a personal representative who is deemed to

be a taxable person.

Goods

Land and Building

Any lease, tenancy, easement, licence to occupy land. Services

Any lease or letting out of the building including a commercial, industrial or residential complex for business or commerce, either wholly or partly.

Services

Treatment or process

Any treatment or process which is being applied to another person’s goods. Services

Declared list of services

Similar to clause 66E of the Finance Act, except for clause (j) of 66E introduced w.e.f 14.05.2016 stating that, assignment by the government of the right to use the radio frequency spectrum and subsequent transfer thereof.

Services

By unincorporated association or body of person to its members

Any supply of goods for cash, deferred payment or other valuable consideration.

Goods

Where a person, acting as an agent, for an agreed commission or brokerage, either supplies or receives any goods

and/or services on behalf of any principal, the transaction between such principal and agent shall be deemed to

be a supply.

Subject to the provisions of Schedule II, the Central or a State Government may, upon recommendation of the

Council, specify by notification, the transactions that are to be treated as—

a supply of goods and not as a supply of services; or

a supply of services and not as a supply of goods; or

neither a supply of goods nor a supply of services.

The supply of any branded service by an aggregator under a brand name or trade name owned by him shall be

deemed to be a supply of the said service by the said aggregator.

Analysis

This is a critical provision which sets out the scope of transactions that qualify as supplies liable to tax under the

GST regime (under Section 7 - charging Section).

To fall within the scope of Section 3, all forms of supply in course or furtherance of business, require consideration

for it. The exceptions, i.e. where consideration is not required for tax to apply are:

Supplies specified under Schedule I

Import of services, whether or not in the course or furtherance of business.

Aggregators are liable for payment of tax on the services rendered under the brand / trade name of the

aggregator, by suppliers to potential customers who are connected on the electronic platform owned and

managed by such aggregator.

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 9

This provision was also included under the Service Tax Rules, 1994 w.e.f. 1-3-2015, so as to bring to tax the

amounts paid for the services provided under the brand/ trade name of the aggregator.

Schedule I

A computer, company car, when put to non-business use would be covered under the schedule. Similarly, any

services provided by the company for private or non-business use, for which no consideration is received, will

be treated as supply.

The assets retained after deregistration of the company under GST regime, would be considered as supply.

Supply of goods / service by a taxable person to another taxable or non-taxable person in course of business,

is treated as supply. The supply of goods / service to self i.e. inter-unit supply or branch transfers will not be

considered as supply. However, free of cost supplies, such as a supply of physician samples, distribution of

goods for sales promotion, etc. will be considered supplies.

Schedule II

Schedule II demarcates supply of goods and supply of services. This will hopefully put to rest some of the

current tax issues involving dual levy of Service tax and VAT on certain transactions.

A n A n a ly s i s M o d e l G S T La w

1 0 | P a g e © E c o n o m ic L a w s P r a c t i c e

LEVY OF, AND EXEMPTION FROM, TAX

C H A RG I N G P ROV I S I O N [ S E C T I O N 7 ]

CGST and SGST will be levied and collected on all ‘intra-state supplies’ of goods and/ or services at the specified rate.

CGST/ SGST will be paid by the ‘taxable person’. For certain notified categories of goods/ services, per the

recommendation of the GST Council, the tax will be payable on reverse charge basis.

Analysis

The charging provision levies CGST/ SGST on all ‘intra-State supplies’; however, this term is undefined under the

CGST/ SGST Act and instead is defined in the IGST Act.

Importantly, the rate of GST continues to remain a mystery.

The reverse charge mechanism, which shifts the liability to discharge tax to the recipient, has been extended to

supplies of goods, unlike the existing regime where the reverse charge only extends to services.

TA X A B L E P E RS O N [ S E C T I O N 9 ]

Taxable person has been defined to mean a person carrying on any business at any place in India/ State of India who is

registered or required to be registered for CGST/ SGST, subject to the following exclusions:

Person with an aggregate turnover equal to or less than INR 10,00,000 in a financial year (INR 5,00,000 for NE

States including Sikkim).

Government or local authorities to be considered a ‘taxable person’ qua activities or transactions carried out by

them as public authorities subject to specified exceptions under Schedule IV.

Services provided by an employee to the employer in the course of/ in relation to employment, or by any other

ties creating a relationship of employer and employee as regards working conditions, remunerations and

employer’s liability.

Persons engaged in the business of exclusively supplying goods and/or services that are not liable to CGST/ SGST.

Persons receiving services of value not exceeding an annual threshold (to be specified) for personal use, other

than for use in the course of furtherance of business.

Analysis

The exclusion for services provided by an employee to employer, which was previously under the definition of

‘service’, now finds place under the concept of ‘taxable person’.

Various other exclusions from the requirement to register, such as the threshold exemption and exemptions for

persons engaged solely in non-taxable activity, have been continued under the concept of ‘taxable person’.

The reverse charge mechanism for goods marks an important deviation, whereby businesses may be required to

discharge a levy akin to the ‘purchase tax’ imposed by certain States under the extant VAT laws.

ELP Comments

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 1 1

P OW E R TO G R A N T E X E M P T I O N F R O M TA X [ S EC T I O N 1 0 ]

The Central/ State Governments are empowered to grant exemptions from CGST/ SGST by way of issuance of

notification (or by special order in circumstances of an exceptional nature), on the recommendation of the GST

Council.

Where exemptions are granted absolutely, no tax shall be paid on such goods/ services.

For the purpose of clarifying the scope or applicability of any notification, an explanation may be inserted within

one year of issuance of the notification, which will have effect as if it had always been part of the said notification.

Analysis

The mandate under Section 5A of the CE Act has been extended to this law to ensure that no tax is collected and

paid on certain goods/ services enjoying absolute exemption (i.e. such exemptions will have to be compulsorily

availed).

The power to insert an Explanation within one year of issuance of a Notification, which would apply ab initio, runs

counter to the law declared by the Supreme Court in Union of India vs. Martin Lottery Agencies Ltd. [2009 (14)

S.T.R. 593 (S.C.)] and SEDCO Forex International Drill Inc. vs. Commissioner of Income Tax [(2005) 12 SCC 717],

which is to the effect that an Explanation does not automatically take effect retrospectively even if it is stated to

be “for the removal of doubts”. On the contrary, where an Explanation effects a substantive alteration of the

provision, it can only apply prospectively. This amendment has similarly been enacted vide the Finance Act, 2016.

A n A n a ly s i s M o d e l G S T La w

1 2 | P a g e © E c o n o m ic L a w s P r a c t i c e

TIME AND VALUE OF SUPPLY

T I M E O F S U P P LY [ S E C T I O N S 1 2 & 1 3 ]

Time of supply is to be the earliest of the following:

Category Goods Services

Forward charge Date of removal of goods / making available the goods to the buyer (where not required to be removed)

Date of issuance of invoice Date of receipt of payment Date on which recipient shows receipt of

goods in books of account

Date of issuance of invoice Date of receipt of payment Date of completion of service (if invoice

not issued within prescribed period) Date on which recipient shows receipt of

service in books of account (where there is no invoice or payment)

Reverse charge Date of receipt of goods Date of receipt of invoice Date of making payment Date of debit in the books of accounts

Date of receipt of services Date or receipt of invoice Date of making payment Date of debit in the books of accounts

For the following cases the time of supply is as specified:

Scenario Goods Services

Continuous supply Where successive statements of accounts/ payments are involved - date of expiry of period to which such statements relate

Where no such statements of account are involved – date of issuance of invoice or receipt of payment, whichever is earlier

Where due date of payment is ascertainable from the contract – date on which payment is liable to be made by recipient, whether or not invoice issued or payment received by supplier

Where due date of payment is not ascertainable from the contract – each time when the supplier receives payment or issues an invoice, whichever is earlier

Where payment is linked to completion of an event – time of completion of event

Specific scenarios Where it is not possible to determine when the supply will take place (e.g. sale on approval basis) – when it becomes known that the supply has taken place or, 6 months from date of removal, whichever is earlier

Where supply of services ceases under a contract before the completion of the supply – when the supply ceases

Residuary Where a periodical return is to be filed, the date on which such return is to be filed In any other case, the date on which CGST/ SGST is paid

Note: In all the above cases, receiving/ making payment refers to the date on which the payment is entered into books

of account or date on which payment is credited/ debited to bank account, whichever is earlier.

C H A N G E I N R AT E O F TA X FO R S E RV I C ES [ S EC T I O N 1 4 ]

The existing Rule 4 of the POT Rules is incorporated in the model law. For the purpose of this Section, the date of

receipt of payment is the date of credit in the bank account if such credit occurs after 4 working days from the date of

change in effective rate of tax.

Analysis

It is important to note that the aforesaid provision applies only to services. Hence, qua goods, it appears that scenarios

of rate change will fall under the default provision for time of supply of goods, viz. Section 12.

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 1 3

VA LU E O F TA X A B L E S U P P LY [ S E C T I O N 1 5 ]

The value of a supply of goods and/or services will be the ‘transaction value’, i.e. price actually paid or payable for

the said supply of goods and/or services, subject to the condition that:

the supplier and recipient of the supply are not related; and

the price is the sole consideration for the supply.

Specific inclusions which shall form part of the ‘transaction value’:

any amount the supplier is liable to pay but which has been incurred by the recipient of the supply, to the

extent not already included;

the value, apportioned as appropriate, of goods and/or services supplied directly or indirectly by the recipient

of the supply free of charge or at reduced cost for use in connection with the supply of goods and/or services

being valued, to the extent not already included;

royalties and license fees related to the supply of goods and/or services being valued that the recipient of

supply must pay, either directly or indirectly, as a condition of the said supply, to the extent not already

included;

any taxes, duties, fees and charges levied under any statute other than the SGST Act or the CGST Act or the

IGST Act

incidental expenses such as commission, packing, charged by the supplier to the recipient of a supply,

including any amount charged for anything done by the supplier in respect of the supply of goods and/or

services at the time of, or before delivery of the goods/ services;

subsidies provided in any form or manner, linked to the supply;

any reimbursable expenditure or cost incurred by or on behalf of the supplier and charged in relation to the

supply of goods and/ or services;

any discount or incentive that may be allowed after the supply has been effected.

Specific exclusions from ‘transaction value’:

any discount allowed before or at the time of supply, provided such discount is allowed in the course of

normal trade practice and has been duly recorded in the invoice issued in respect of the supply;

Post-supply discount which is established as per the agreement and is known at or before the time of supply

and specifically linked to the relevant invoices;

Analysis

Valuation for goods and services is pegged to transaction value, which concept has been taken from the existing

provisions under the Customs/ Central Excise laws. Further, the specific inclusions are largely aligned with Rule 10

of the Customs Valuation Rules.

The requirement that pre-supply discounts should be reflected in the invoice is currently envisaged under various

VAT statutes.

As regards reimbursable expenditure or cost being included in the transaction value, this is in line with the recent

amendment to Section 67 of the Finance Act.

Service providers, who were hitherto taxable on the basis of ‘gross amount’, will, under the GST regime, be

subjected to tax on the ‘transaction value’ concept; which concepts are un-tested in the context of rendition of

services.

ELP Comments

A n A n a ly s i s M o d e l G S T La w

1 4 | P a g e © E c o n o m ic L a w s P r a c t i c e

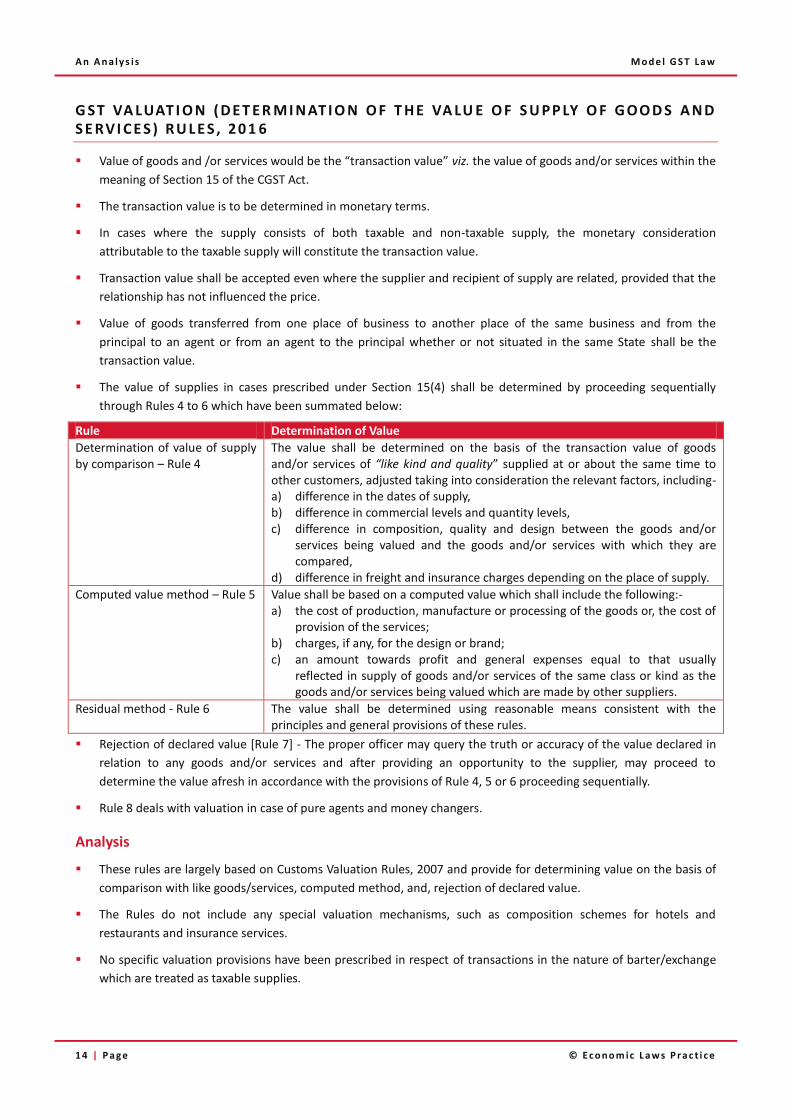

G ST VA LUAT I O N ( D E T E R M I N AT I O N O F T H E VA LU E O F S U P P LY O F G OO D S A N D S E RV I C E S ) R U L E S , 20 1 6

Value of goods and /or services would be the “transaction value” viz. the value of goods and/or services within the

meaning of Section 15 of the CGST Act.

The transaction value is to be determined in monetary terms.

In cases where the supply consists of both taxable and non-taxable supply, the monetary consideration

attributable to the taxable supply will constitute the transaction value.

Transaction value shall be accepted even where the supplier and recipient of supply are related, provided that the

relationship has not influenced the price.

Value of goods transferred from one place of business to another place of the same business and from the

principal to an agent or from an agent to the principal whether or not situated in the same State shall be the

transaction value.

The value of supplies in cases prescribed under Section 15(4) shall be determined by proceeding sequentially

through Rules 4 to 6 which have been summated below:

Rule Determination of Value

Determination of value of supply by comparison – Rule 4

The value shall be determined on the basis of the transaction value of goods and/or services of “like kind and quality” supplied at or about the same time to other customers, adjusted taking into consideration the relevant factors, including- a) difference in the dates of supply, b) difference in commercial levels and quantity levels, c) difference in composition, quality and design between the goods and/or

services being valued and the goods and/or services with which they are compared,

d) difference in freight and insurance charges depending on the place of supply.

Computed value method – Rule 5 Value shall be based on a computed value which shall include the following:- a) the cost of production, manufacture or processing of the goods or, the cost of

provision of the services; b) charges, if any, for the design or brand; c) an amount towards profit and general expenses equal to that usually

reflected in supply of goods and/or services of the same class or kind as the goods and/or services being valued which are made by other suppliers.

Residual method - Rule 6 The value shall be determined using reasonable means consistent with the principles and general provisions of these rules.

Rejection of declared value [Rule 7] - The proper officer may query the truth or accuracy of the value declared in

relation to any goods and/or services and after providing an opportunity to the supplier, may proceed to

determine the value afresh in accordance with the provisions of Rule 4, 5 or 6 proceeding sequentially.

Rule 8 deals with valuation in case of pure agents and money changers.

Analysis

These rules are largely based on Customs Valuation Rules, 2007 and provide for determining value on the basis of

comparison with like goods/services, computed method, and, rejection of declared value.

The Rules do not include any special valuation mechanisms, such as composition schemes for hotels and

restaurants and insurance services.

No specific valuation provisions have been prescribed in respect of transactions in the nature of barter/exchange

which are treated as taxable supplies.

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 1 5

The pure agent conditions and valuation mechanism for money changes is identical as existing under the Service

tax legislation.

Currently, a number of products are covered under MRP based assessment under Section 4A of CE Act. These

products will now be taxed on their transaction value.

Under the present indirect tax regime, varied valuation mechanisms are prescribed. With the above Rules, the

valuation processes places far greater onus on the supplier.

ELP Comments

A n A n a ly s i s M o d e l G S T La w

1 6 | P a g e © E c o n o m ic L a w s P r a c t i c e

INPUT TAX CREDIT

M A N N E R O F TA K I N G I N P U T TA X C R E D I T ( S EC T I O N 1 6 )

Every registered taxable person shall be entitled to take credit of input tax admissible to him, subject to such

conditions as may be prescribed. The key aspects in this regard are set out below:

Timelines:

Credit in respect of any invoice pertaining to a financial year can be taken only up to:

the filing of return for the month of September following the said financial year; or

filing of the relevant annual return

whichever is earlier

Conditions:

Possession of a tax invoice, or other tax-paying document issued by a supplier

Goods / services have been received or deemed to be received by the registered taxable person

Tax charged in respect of said supplies has been actually paid to the credit of the appropriate Government

Return has been furnished by the registered taxable person

Credit for goods against an invoice, which are received in lots or installments can be taken only upon receipt

of the last lot or installment

Restrictions:

Particulars Restrictions

Goods or services used partly for

business and partly for non-taxable

/ exempted / other purposes

Credit shall be restricted to input tax attributable to the purposes of business,

in the manner as may be prescribed by notification. Restriction does not apply

to credits pertaining to zero-rated supplies

Motor vehicles Credit not available in respect of motor vehicles, except when supplied in the usual course of business or are used to provide taxable services viz., transportation of passengers, transportation of goods and imparting training on motor driving skills

Goods / services used for personal

consumption

Credit not available in respect of: - goods or services (such as outdoor catering, beauty treatment, health

services, membership of a club, life and health insurance etc), when used primarily for personal use or consumption of any employee

- goods or services used for private or personal consumption

Works contract resulting in

immovable property (other than

plant and machinery)

Credit not available in respect of: - Goods / services acquired by a principal in the execution of works contract

resulting in the construction of an immovable property - Goods acquired by a principal, the property in which is not transferred

(whether as goods or in some other form) to any other person, used in the construction of immovable property

Capital Goods - Credit not admissible on such tax component of the cost of capital goods, for which depreciation has been claimed under the Income Tax Act, 1961

- In case of supply of capital goods on which input tax credit has been taken, payment is required to be made for an amount equal to input tax credit reduced by percentage as may be specified or tax on the transaction value of such capital goods, whichever is higher

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 1 7

Particulars Restrictions

Goods / services suffering

composition levy

Credit is not available on procurement of goods / services, on which tax has been paid under composition scheme as per Section 8

I N P U T TA X C R E D I T I N R E S P E C T O F I N P U T S / C A P I TA L G OO D S S E N T FO R J O B WO R K ( S EC T I O N 1 6 A )

Principal shall be be entitled to take credit of input tax on inputs / capital goods sent to a job-worker (either by

principal or directly), if the said inputs / capital goods, after completion of job-work, are received back by the

principal:

within 180 days in case of inputs

within 2 years in case of capital goods

In case inputs / capital goods are not received in the aforesaid time frame, credit shall be reversed (along with

interest), which can be re-claimed at the time when inputs / capital goods are received back.

M A N N E R O F D I ST R I B U T I O N O F C R E D I T ( S EC T I O N 1 7 )

Input service distributor may distribute the credits by way of prescribed document in the following manner:

Nature of input

tax

Credit may be

distributed as

Situation

CGST or

SGST or

IGST

IGST Where the distributor and the recipient of credit are located in the different States

CGST or

IGST

CGST Where the distributor and the recipient of credit, being a business vertical, are

located in the same State

SGST or

IGST

SGST

Distribution of credits by an input service distributor is subject to the following key conditions:

Credit of input services attributable to a supplier shall be distributed only to that supplier

Credit of input services attributable to more than one supplier shall be distributed on pro-rata basis amongst

such supplier(s) to whom the input service is attributable

O R D E R O F U T I L I Z AT I O N ( S E C T I O N 3 5 )

Amount of credit available with the taxable person shall be credited to his ‘electronic credit ledger’ and is

permitted to be utilized in the following order:

Particulars Order of Utilization of ITC

IGST - IGST

- CGST

- SGST

CGST - CGST

- IGST

SGST - SGST

- IGST

A n A n a ly s i s M o d e l G S T La w

1 8 | P a g e © E c o n o m ic L a w s P r a c t i c e

Input tax credit of CGST shall not be utilized towards payment of SGST and similarly input tax credit of SGST shall

not be utilized towards payment of CGST.

Analysis

The amalgam of existing CENVAT Credit and State VAT laws would ensure greater availability of credits since

deficiencies existing in the contemporary Central laws, such as reversal with respect to trading of goods or the

State VAT laws, such as retention of credit pertaining to inter-state branch transfer of goods, will be eliminated.

Condition of “receipt of services” for availment of credit is a departure from the present CENVAT Credit provisions

which, for input services, allows availment of credit on the basis of “receipt of invoice / bill”.

Credit continues to be restricted for non-taxable and exempted services except in case of exports.

Outer timelines for availment credit continue to exist under the model law, with certain modifications as

compared to the present scheme. The present CENVAT Credit provisions prescribe a time limit of one year from

the date of tax invoice and the State VAT laws of certain States (such as Maharashtra) require setting off of input

tax credits in the same financial year.

Credit records have to be maintained on a electronic register (which appears will be facilitated by the GSTN).

Various important aspects of existing CENVAT credits / VAT credit laws such as, credit on capital goods on 50:50

basis, sector specific provisions such as banking sector / financial sector, negative list / retention items under the

State VAT laws, etc. are presently absent in the model law.

The model law prescribes onerous condition for availability of credits only when tax has been actually paid into the

coffers of the respective Government. Imposing such a condition is a clear departure from the present practice

under the Central laws and seeks to follow the scheme provided under the certain State VAT laws.

ELP Comments

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 1 9

COMPLIANCES

R EG I ST R AT I O N [ S EC T I O N 1 9 – 2 2 ]

The threshold limit for registration has been prescribed to be INR 9 lakhs. A reduced threshold limit of INR 4 lakhs

has been prescribed for North Eastern States including Sikkim. This limit includes all supplies, whether on own

account or on behalf of principal, except supplies in the capacity of a registered job-worker, which shall be treated

as supplies by the principal. The said threshold is to be computed on an all India basis.

A person shall not be liable to registration if his aggregate turnover consists of only goods and / or services which

are not liable to tax.

A person having multiple business verticals in a State may obtain a separate registration for each business vertical,

subject to such conditions as may be prescribed.

A person, though not liable, may get himself registered voluntarily.

Every person shall have a Permanent Account Number issued under the Income Tax Act, 1961, in order to be

eligible for grant of registration.

The following categories of persons shall be mandatorily required to obtain registration, irrespective of the

threshold limit-

persons making any inter-State taxable supply;

casual taxable persons;

persons who are required to pay tax under reverse charge;

non-resident taxable persons;

persons who are required to deduct tax under section 37;

persons who supply goods and/or services on behalf of other registered taxable persons whether as an agent

or otherwise;

input service distributor;

persons who supply goods and/or services, other than branded services, through electronic commerce

operator;

every electronic commerce operator;

an aggregator who supplies services under his brand name or his trade name;

Such other person or class of persons as may be notified by the Central Government or a State Government

on the recommendations of the Council.

If a person, other than an Input Service Distributor, is already registered under an earlier law, it shall not be

necessary for him to apply for fresh registration and he shall follow the procedure as may be prescribed in this

regard.

A causal taxable person or a non resident taxable person shall, at the time of submission of application for

registration, make an advance deposit of tax of an amount equivalent to the estimated tax liability for the period

for which the registration is sought. The certificate of registration issued to such class of persons shall be valid for

a period of 90 days, which may be extended upto 90 days.

Powers have been provided for cancellation of registration if the assessee contravenes the provisions or obtains

the registration by fraudulent means. However, such cancellation may be revoked, in terms of the prescribed

procedure.

Analysis

The concept of a single/centralised registration for multiple places of business has not been provided.

A n A n a ly s i s M o d e l G S T La w

2 0 | P a g e © E c o n o m ic L a w s P r a c t i c e

Inapplicability of threshold limits to inter-state supplies runs counter to having uniform taxing principles for intra-

state and inter-state transactions.

TA X I N VO I C E , C R E D I T A N D D E B I T N OT ES [ S EC T I O N 2 3 – 2 4 ]

A registered taxable person supplying taxable goods, shall issue, at the time of supply, a tax invoice showing the

description, quantity and value of goods, the tax charged thereon and such other particulars as may be prescribed.

A registered taxable person, supplying services, shall issue a tax invoice within the prescribed time; showing the

description, the tax charged thereon and other such particulars as may be prescribed.

A registered taxable person supplying non-taxable goods and/or services or paying tax under the provisions of

Section 8 shall issue, instead of a tax invoice, a bill of supply containing such particulars as may be prescribed.

Provisions for issuance of credit/debit notes have been introduced subject to fulfilment of certain conditions.

Analysis

The concept of debit and credit notes has been part of various VAT legislations. However, in the said legislations,

such documents have also been recommended for situations where goods are returned post sale. The model law

however does not prescribe issuance of debit/credit notes in such situations.

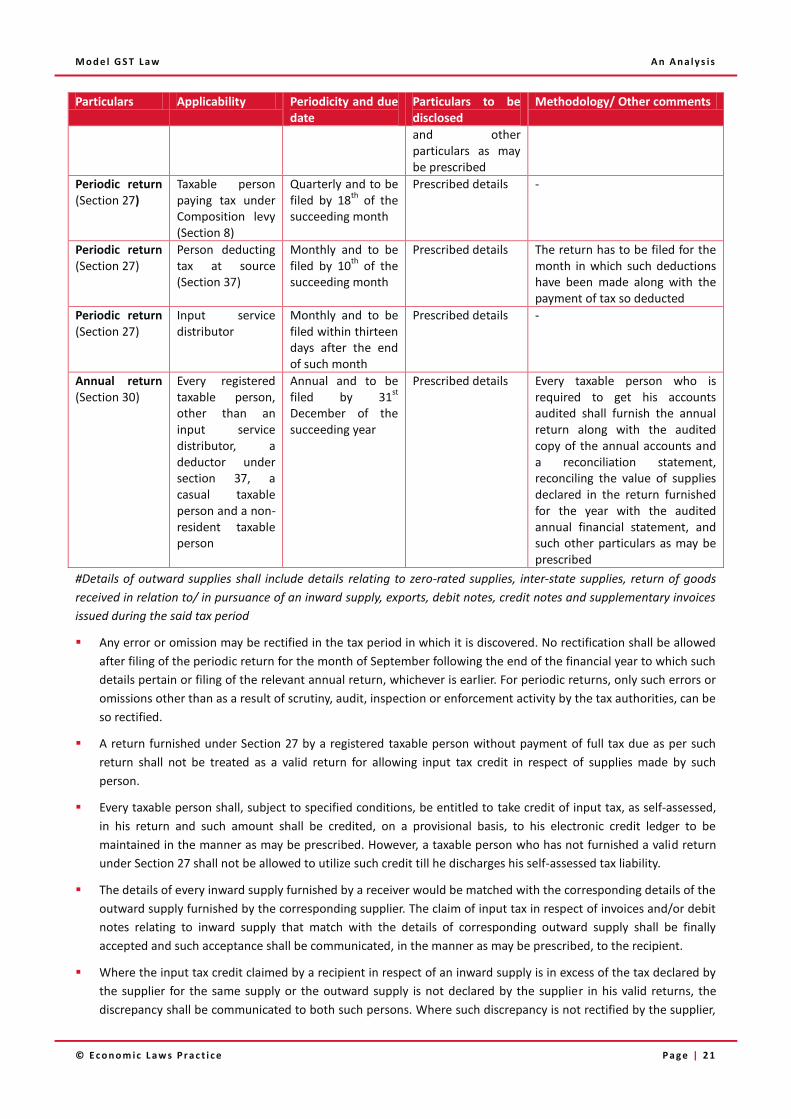

R E T U R N S [ S EC T I O N 2 5 – 3 4 ]

The provisions pertaining to the filing of various returns are tabulated below-

Particulars Applicability Periodicity and due date

Particulars to be disclosed

Methodology/ Other comments

Return of outward supplies (Section 25)

Taxable person other than those paying tax under Composition levy (Section 8) or those deducting tax at source (Section 37)

Monthly and to be filed by 10

th of the

succeeding month

Details of outward supplies# of goods and/or services effected during the said tax period

The details provided by the supplier shall be communicated to the recipient of the said supplies within the time and in the manner as may be prescribed

Return of inward supplies (Section 26)

Monthly and to be filed by 15

th of the

succeeding month

The details of inward supplies of taxable goods and/or services, received during the tax period

The taxable person shall verify, validate, modify or, if required, delete the details relating to outward supplies and credit or debit notes communicated in terms of the return filed by the corresponding supplier under (1) above, to prepare the details of his inward supplies and credit or debit notes and may include therein, the details of inward supplies and credit or debit notes received by him in respect of such supplies that have not been declared by the supplier under (1) above

Periodic return (Section 27)

Monthly and to be filed by 20

th of the

succeeding month

Details of inward and outward supplies of goods and/or services, input tax credit availed, tax payable, tax paid

-

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 2 1

Particulars Applicability Periodicity and due date

Particulars to be disclosed

Methodology/ Other comments

and other particulars as may be prescribed

Periodic return (Section 27)

Taxable person paying tax under Composition levy (Section 8)

Quarterly and to be filed by 18

th of the

succeeding month

Prescribed details -

Periodic return (Section 27)

Person deducting tax at source (Section 37)

Monthly and to be filed by 10

th of the

succeeding month

Prescribed details The return has to be filed for the month in which such deductions have been made along with the payment of tax so deducted

Periodic return (Section 27)

Input service distributor

Monthly and to be filed within thirteen days after the end of such month

Prescribed details -

Annual return (Section 30)

Every registered taxable person, other than an input service distributor, a deductor under section 37, a casual taxable person and a non-resident taxable person

Annual and to be filed by 31

st

December of the succeeding year

Prescribed details Every taxable person who is required to get his accounts audited shall furnish the annual return along with the audited copy of the annual accounts and a reconciliation statement, reconciling the value of supplies declared in the return furnished for the year with the audited annual financial statement, and such other particulars as may be prescribed

#Details of outward supplies shall include details relating to zero-rated supplies, inter-state supplies, return of goods

received in relation to/ in pursuance of an inward supply, exports, debit notes, credit notes and supplementary invoices

issued during the said tax period

Any error or omission may be rectified in the tax period in which it is discovered. No rectification shall be allowed

after filing of the periodic return for the month of September following the end of the financial year to which such

details pertain or filing of the relevant annual return, whichever is earlier. For periodic returns, only such errors or

omissions other than as a result of scrutiny, audit, inspection or enforcement activity by the tax authorities, can be

so rectified.

A return furnished under Section 27 by a registered taxable person without payment of full tax due as per such

return shall not be treated as a valid return for allowing input tax credit in respect of supplies made by such

person.

Every taxable person shall, subject to specified conditions, be entitled to take credit of input tax, as self-assessed,

in his return and such amount shall be credited, on a provisional basis, to his electronic credit ledger to be

maintained in the manner as may be prescribed. However, a taxable person who has not furnished a valid return

under Section 27 shall not be allowed to utilize such credit till he discharges his self-assessed tax liability.

The details of every inward supply furnished by a receiver would be matched with the corresponding details of the

outward supply furnished by the corresponding supplier. The claim of input tax in respect of invoices and/or debit

notes relating to inward supply that match with the details of corresponding outward supply shall be finally

accepted and such acceptance shall be communicated, in the manner as may be prescribed, to the recipient.

Where the input tax credit claimed by a recipient in respect of an inward supply is in excess of the tax declared by

the supplier for the same supply or the outward supply is not declared by the supplier in his valid returns, the

discrepancy shall be communicated to both such persons. Where such discrepancy is not rectified by the supplier,

A n A n a ly s i s M o d e l G S T La w

2 2 | P a g e © E c o n o m ic L a w s P r a c t i c e

the corresponding tax value shall be added to the output tax liability of the recipient. The amount so added may

be subsequently reduced if the supplier declares the details of the invoice and/or debit note in his valid return

within the prescribed time limit.

The duplication of claims of input tax credit shall be communicated to the recipient and the corresponding tax

value shall be added to the output tax liability of the recipient.

Similar matching will be carried out qua the credit notes relating to an outward supply, issued by the supplier, with

the corresponding reduction in the claim for input tax credit by the corresponding receiver, with similar

consequences, with the exception that additions to liability, owing to any mismatches, shall be to the account of

the supplier.

Every registered taxable person who applies for cancellation of registration shall furnish a final return within three

months of the date of cancellation or date of cancellation order, whichever is later, in such form and in such

manner as may be prescribed.

Analysis

Specific mechanism is being proposed for matching of input tax credit claimed by the recipient and tax paid by the

supplier. The said requirement was never prevalent under Central tax laws, though certain State VAT legislations

(including Maharashtra and West Bengal) incorporated such requirements. Even in such States, practically, such

requirement has resulted in denial of huge eligible input tax credits for want of documentary requirements

(pertaining to payment of tax at supplier’s end) not within the control of the assessee or owing to errors in the

Departmental database. Such conditions for availment of credit, not within the control of the credit claiming

dealer, would be detrimental to the vision of seamless GST.

PAY M E N T O F TA X A N D I N T E R E ST O N D E L AY E D PAY M E N T S [ S EC T I O N 3 5 – 3 6 ]

All deposits /payment made with respect to tax, interest, penalty, fee or any other amount by a taxable person

shall be through electronic means and shall be credited to the electronic cash ledger of such person.

The date of credit to the account of the appropriate Government in the authorized bank shall be deemed to be

the date of deposit.

The input tax credit as self-assessed in the return of a taxable person shall be credited to his electronic credit

ledger to be maintained in the manner as may be prescribed.

Every taxable person shall discharge his tax and other dues in the following order:

self-assessed tax, and other dues related to returns of previous tax periods;

self-assessed tax, and other dues related to return of current tax period;

any other amount payable under the applicable provisions.

The rate of applicable interest shall be notified, on the recommendations of the GST Council, by the Central and

State Government.

TA X D E D UC T I O N AT S O U RC E [ S E C T I O N 37 ]

Tax may be mandated to be deducted @ 1% from the payment made to the supplier of taxable goods and/or

services by the Central or State Government, Local authority, Governmental agencies, or such category of persons

as notified, if total value of such supply, under a contract, exceeds INR 10 Lakhs

Procedure for deposit of such tax and issuance of a credit certificate has been prescribed.

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 2 3

AC CO U N T S A N D R EC O R D S [ S E C T I O N 4 2 – 4 3 ]

Every registered taxable person shall be required to keep and maintain at his place of business [including the

principal place of business] a true and correct books of account including the following:

Production or manufacture of goods

Inward or outward supply of goods and/or services

Stock of goods

Input tax credit availed

Output tax payable and paid

such other particulars as may be prescribed in this behalf

Every registered taxable person whose turnover during a financial year exceeds the prescribed limit shall get his

accounts audited by a chartered accountant or a cost accountant

The time period for retaining accounts is prescribed as follows:

Particulars Time Limit

Records including books of accounts pertaining to the appeal [or revision] or any other proceeding before any Appellate Authority or Tribunal or Court

One year after final disposal of such appeal or revision or proceeding or for a time period, as may be prescribed, whichever is later

Any other case Sixty months [i.e. 5 years] from the date of filing of annual return for the year

A n A n a ly s i s M o d e l G S T La w

2 4 | P a g e © E c o n o m ic L a w s P r a c t i c e

REFUNDS

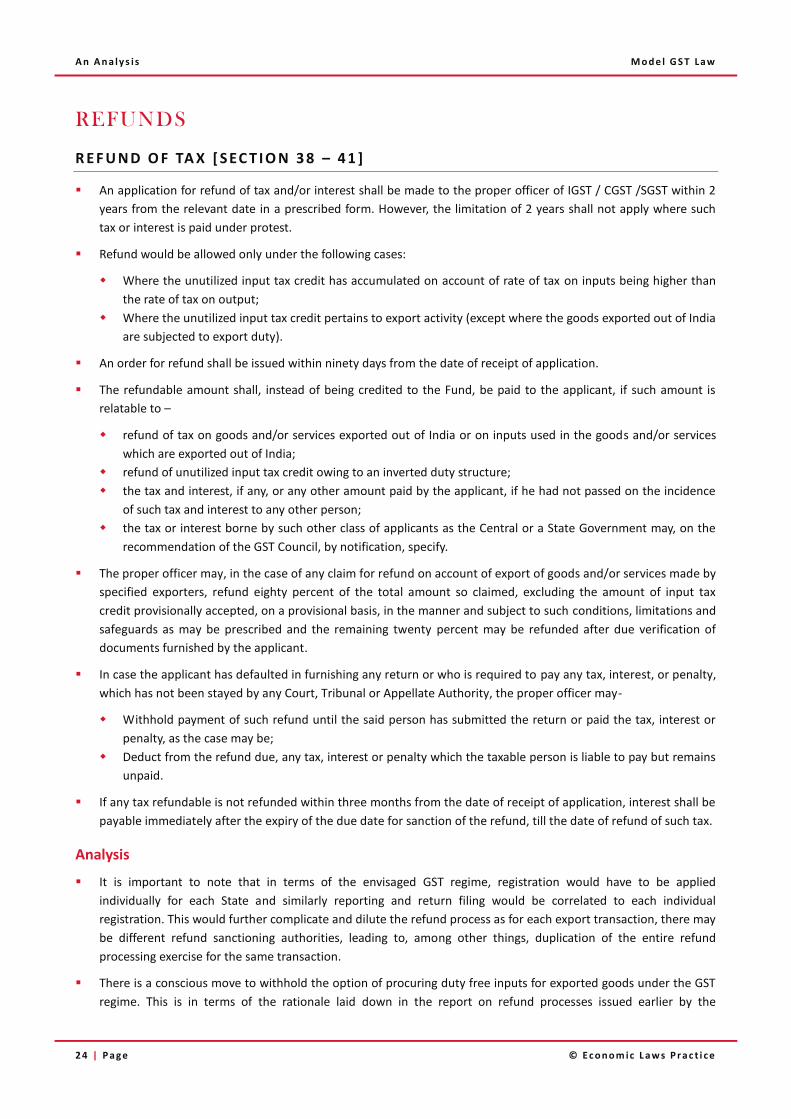

R E F U N D O F TA X [ S EC T I O N 3 8 – 4 1 ]

An application for refund of tax and/or interest shall be made to the proper officer of IGST / CGST /SGST within 2

years from the relevant date in a prescribed form. However, the limitation of 2 years shall not apply where such

tax or interest is paid under protest.

Refund would be allowed only under the following cases:

Where the unutilized input tax credit has accumulated on account of rate of tax on inputs being higher than

the rate of tax on output;

Where the unutilized input tax credit pertains to export activity (except where the goods exported out of India

are subjected to export duty).

An order for refund shall be issued within ninety days from the date of receipt of application.

The refundable amount shall, instead of being credited to the Fund, be paid to the applicant, if such amount is

relatable to –

refund of tax on goods and/or services exported out of India or on inputs used in the goods and/or services

which are exported out of India;

refund of unutilized input tax credit owing to an inverted duty structure;

the tax and interest, if any, or any other amount paid by the applicant, if he had not passed on the incidence

of such tax and interest to any other person;

the tax or interest borne by such other class of applicants as the Central or a State Government may, on the

recommendation of the GST Council, by notification, specify.

The proper officer may, in the case of any claim for refund on account of export of goods and/or services made by

specified exporters, refund eighty percent of the total amount so claimed, excluding the amount of input tax

credit provisionally accepted, on a provisional basis, in the manner and subject to such conditions, limitations and

safeguards as may be prescribed and the remaining twenty percent may be refunded after due verification of

documents furnished by the applicant.

In case the applicant has defaulted in furnishing any return or who is required to pay any tax, interest, or penalty,

which has not been stayed by any Court, Tribunal or Appellate Authority, the proper officer may-

Withhold payment of such refund until the said person has submitted the return or paid the tax, interest or

penalty, as the case may be;

Deduct from the refund due, any tax, interest or penalty which the taxable person is liable to pay but remains

unpaid.

If any tax refundable is not refunded within three months from the date of receipt of application, interest shall be

payable immediately after the expiry of the due date for sanction of the refund, till the date of refund of such tax.

Analysis

It is important to note that in terms of the envisaged GST regime, registration would have to be applied

individually for each State and similarly reporting and return filing would be correlated to each individual

registration. This would further complicate and dilute the refund process as for each export transaction, there may

be different refund sanctioning authorities, leading to, among other things, duplication of the entire refund

processing exercise for the same transaction.

There is a conscious move to withhold the option of procuring duty free inputs for exported goods under the GST

regime. This is in terms of the rationale laid down in the report on refund processes issued earlier by the

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 2 5

Empowered Committee, in terms of which refund based schemes would obviate the requirement of submission of

statutory form and the supplier of goods to the actual exporter would be required to pay the GST and will not be

required to comply with various formalities presently required for making tax free supplies.

Refund has only been allowed under two instances – i.e. when goods / services are exported and for instances of

inverted duty structure. These instances are in line with the existing provisions governing the Service tax

legislation but are restrictive when compared to the refund mechanism under Value Added Tax.

A n A n a ly s i s M o d e l G S T La w

2 6 | P a g e © E c o n o m ic L a w s P r a c t i c e

ELECTRONIC COMMERCE

R E L E VA N T D E F I N I T I O N S A N D C O L L E C T I O N O F TA X AT S O U R C E [ S E C T I O N 4 3 B A N D S E C T I O N 4 3 C ]

The term ‘electronic commerce operator’ is defined to include any person who directly or indirectly owns,

operates or manages an electronic platform that is engaged in facilitating the supply of any goods and / or services

or in providing any information or any other services incidental to or in connection there with.

An electronic commerce operator will be required to:

Collect tax at prescribed rates from the amount payable or paid to the supplier towards the supply of goods

and /or services made through the said operator and pay the said tax to the credit of the appropriate

Government within ten days after the end of the month in which such collection is made;

Furnish a statement electronically containing all prescribed particulars of amounts collected towards outward

supplies of goods and / or services effected by the said operator, within ten days after the end of such

calendar month.

The amount of tax so collected and paid by the electronic commerce operator shall be deemed to be a payment of

tax on behalf of the concerned supplier and the supplier shall claim credit of the same in his electronic cash ledger.

The term ‘aggregator’ is defined in a more restrictive manner to cover only transactions of supply of service.

‘Aggregator’ is defined to mean a person who owns and manages an electronic platform and enables a potential

customer to connect with the persons providing service of a particular kind under the brand name or trade name

of the aggregator himself.

The fact that separate provisions are introduced in respect of e-commerce transactions indicates that this

sector has received special attention in drafting of the model law;

The requirement to collect tax at source on all transactions of supply of goods and services by suppliers will

significantly increase the onus and compliance burden on electronic commerce operators. It is noteworthy that

hitherto, electronic commerce operators only act as service providers to the suppliers / sellers.

Given that the suppliers will be required to pay tax on supply to the destination State, it remains to be seen

whether an appropriate mechanism is devised to ensure a seamless and un-hindered flow of the credit of the

tax collected at source to the supplier;

Furthermore, the rate at which tax is required to be collected at source should be benign to ensure that there is

no pile-up of unutilized credit in the hands of the suppliers.

As regards aggregators, it is noteworthy that in terms of Section 3(4), the supply of service under a brand name

or trade name owned by an aggregator is deemed to be a supply of the said service by the said aggregator and

the aggregator is the person liable to pay tax on such supplies. This is in line with the existing provisions under

the Service tax law.

ELP Comments

M o d e l G S T La w A n A n a ly s i s

© E c o n o m ic L a w s P r a c t i c e P a g e | 2 7

ASSESSMENT AND AUDIT

Provision / Section Particulars / Description

Self Assessment [Section 44]

A registered taxable person shall undertake self assessment of the taxes payable and furnish a return for each tax period as specified in Section 27 which deals with returns. The usual tax period for this purpose is a calendar month.

Provisional Assessment [Section 44A]

Where taxable person is unable to determine (i) the value of goods and/or services or (ii) the rate of tax applicable, he may request the proper officer for payment of tax on a provisional basis, who shall pass an order in permitting so. Provisional assessment shall be subject to fulfilment of prescribed conditions.

Scrutiny of Returns [Section 45]

The proper officer may scrutinize the return and shall inform the taxable person of the discrepancies noticed, if any, and seek his explanation.

No further action shall be taken in case of a satisfactory response. However, in case of unsatisfactory response, the proper officer may undertake audit, special audit, inspection, search and seizure. The proper officer may subsequently determine the tax, interest and penalty due from the taxable person.

Assessment of Non – filers of Return [Section 46]

The proper officer may after allowing prescribed time to furnish the return, assess the tax liability to the best of his judgment and issue an assessment order.

In case a valid return has been furnished within thirty days of passing of the order, the proper officer may withdraw the said assessment order.

Assessment of Unregistered Persons [Section 47]

Best judgment assessment may be undertaken in respect of taxable persons who fail to obtain registration.

Summary Assessment in Certain Special Cases [Section 48]

The proper officer may, in case of sufficient grounds to believe that delay in assessment will adversely affect the interest of revenue, may proceed to assess the tax liability.

Audit [Section 49]

The Commissioner of CGST/ SGST or any officer authorized by him, at the place of business of the taxable person, may undertake audit of the business transactions.

The audit shall be completed within a period of 3 months or under certain conditions, extend the period.

On conclusion of audit, the proper officer shall notify its findings to the taxable person.

Where the audit results in detection of tax not paid or tax short paid or tax erroneously refunded or input tax credit erroneously availed, the proper officer may initiate suitable action for recovery.

A n A n a ly s i s M o d e l G S T La w

2 8 | P a g e © E c o n o m ic L a w s P r a c t i c e

INSPECTION, SEARCH, SEIZURE, ARREST; OFFENCES

& PENALTIES; PROSECUTION & COMPOUNDING

I N S P E C T I O N , S EA RC H , S E I Z U R E , S U M M O N S A N D A C C E S S TO B U S I N E S S P R E M I S E S [ S EC T I O N S 6 0 , 6 3 A N D 6 4 ]

Powers in relation to inspection, search, seizure, summons and access to business premises:

Section 60(1) deals with the power of CGST/SGST officers to inspect the places of business of - (i) taxable person,

or, (ii) persons engaged in business of transporting goods or owner or operator of warehouse or godown or any

other place, in certain circumstances.

Section 60 (2) provides that certain CGST/SGST officers who have reason to believe that goods liable to

confiscation or any documents or books or things relevant to any proceedings under the model law, are secreted,

then search and seizure can be carried out in respect of such goods, documents or books or things. The person

from whose custody any documents are seized during search and seizure shall be entitled to make copies thereof

or take extracts therefrom in presence of a CGST/SGST officer.

Section 63 empowers the CGST/SGST officers to summon any person whose attendance he considers necessary

either to give evidence or to produce a document or any other thing in an inquiry which such officer is making.

Section 64 provides for access to business premises to authorized CGST/SGST officers to inspect books of account,