Mock State Aid Project County Highway Accountant’s Conference 2015.

28

Mock State Aid Project County Highway Accountant’s Conference 2015

-

Upload

clare-alexander -

Category

Documents

-

view

216 -

download

2

Transcript of Mock State Aid Project County Highway Accountant’s Conference 2015.

Mock State Aid Project

County Highway Accountant’s Conference 2015

Obtain SAP # from District State Aid Engineer (DSAE)

Submit plan to DSAE for review and approvalAfter approval setup project in your Contract

Management system along with Engineer’s Estimate

After project has been let, enter the bid amounts into your Contract Management system

Contract is awarded to the most responsible contractor who may or may not be the lowest bidder

Steps Leading up to 1st Pay Request

Separate pay request for each SAP #Remember to include tied to Project numbers on line

belowSubmit after the award of contractMay request

95% of state aid eligible construction items95% of Right of Way appraisal costs or 100% of actual

purchase price with proof of payment100% of Engineering costs up to a cap of 25% of the

state aid eligible construction costs

Exceptions: Projects funded by State Bonds, such as bridge bonds, LRIP, special legislative bonds etc., are paid as a reimbursement only. (If tied to a DCP Project, Bond Funds will be paid with the DCP Payment Request Form.)

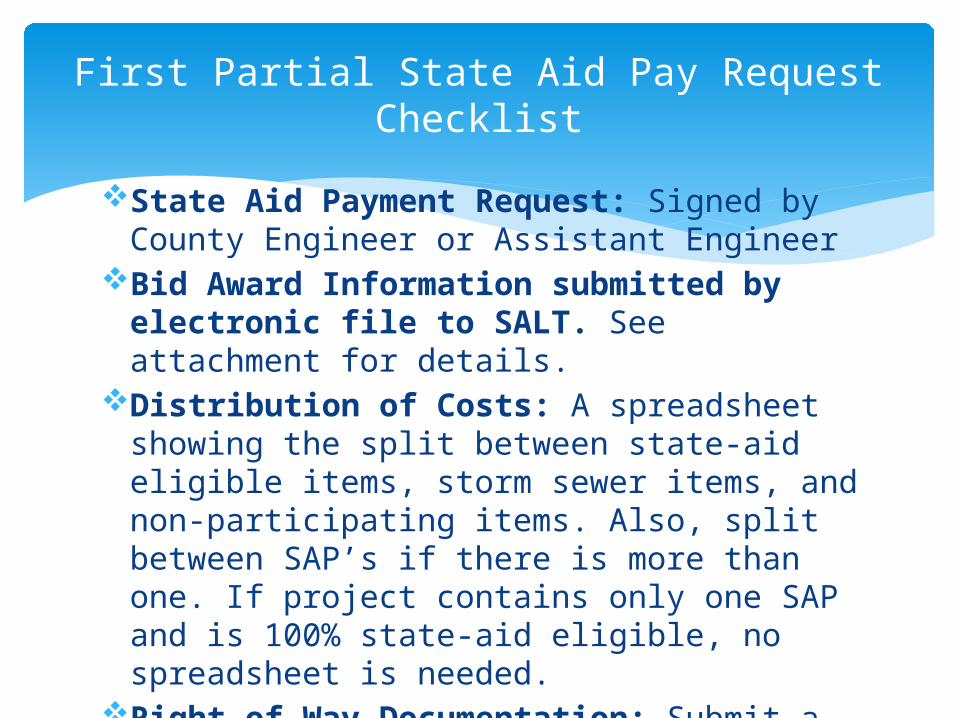

First Partial State Aid Pay Request

State Aid Payment Request: Signed by County Engineer or Assistant Engineer

Bid Award Information submitted by electronic file to SALT. See attachment for details.

Distribution of Costs: A spreadsheet showing the split between state-aid eligible items, storm sewer items, and non-participating items. Also, split between SAP’s if there is more than one. If project contains only one SAP and is 100% state-aid eligible, no spreadsheet is needed.

Right of Way Documentation: Submit a Right of Way Certificate showing actual expenditures. This must

First Partial State Aid Pay RequestChecklist

ROW cont..: Include the parcel number, price paid, person/business paid, and proof of payment (copy of checks, electronic transfer number etc.). Legal costs, title fees and other administrative costs may be lumped together and shown on one line – retain the documentation for audit purposes.

Engineering Costs: No back up documentation is required. Engineer’s signature certifies that the amount requested does not exceed the actual cost. Engineering costs cannot exceed 25% of state aid eligible items. Combine preliminary & construction engineering.

Force Account (FA) Costs: must have an executed FA on file. Payment is 95% of the Schedule of Costs shown on the FA.

First Partial State Aid Pay RequestChecklist (continued)

State Aid Payment Request: same as Initial Request

Copy of Payment Voucher to Contractor: Shows to date quantities and amounts actually paid out to contractor

Distribution of Costs: same as Initial RequestRight of Way: same as Initial RequestSupplemental Agreements/Work and Change

Orders: Include all Supplemental Agreements, Work Orders and Change Orders

Engineering Costs: same as Initial RequestForce Account Costs: same as Initial Request

Subsequent Partial State Aid Pay Request - Checklist

State Aid Payment Request: same as Initial Request except make sure Final is checked and the total project costs are equal to the total paid to the contractor

Copy of Final Payment Voucher to Contractor: Shows final quantities and amounts actually paid out to contractor

Distribution of Costs: same as Initial RequestRight of Way: same as Initial RequestSupplemental Agreements/Work and Change Orders:

Include all Supplemental Agreements, Work Orders and Change Orders

Engineering Costs: same as Initial RequestForce Account Costs: Include documentation of force labor

costs or an invoice from an external source like utilities or railroad.

Final State Aid Pay RequestChecklist

Projects using state bonds such as Bridge or special legislative programs like Local Road Improvement Program and Flood Bonds

State bond funds are “reimbursement” only funds unlike state aid funds which may be paid out before the project is started. Bond funds can only be paid up to the actual expenditure of participating costs as shown on a partial or final contractor payment voucher.

These projects need all the same documentation shown on previous checklists in addition to:Abstract of Bids on Bridge Bond funded projects sent in early so

Bridge Bond grant amount can be determined by State Aid Finance. Bridge items should be highlighted.

Bond Agreement with County Resolution: The resolution states the exact amount of the bond granted to the project and states that the local agency will return any bonds funds not used on the project and fund any excess costs

Special Bond Funds Pay RequestChecklist

For DCP projects, the state bonds are requested with the Federal DCP pay request. Do not use the SAPR (State Aid Pay Request) form for the construction bond funds. The only bond funds that may be requested, for the DCP projects on the SAPR, are engineering costs if they were approved in the bonding agreement.

Special Bond Funds Pay RequestDCP Notes

Recognize receivable from State Aid and reduce the allotment

Accounting Entries – for amount of State Aid Construction Obligation ONLY - $452,019.38

Debit: (asset) State Aid – Receivable Credit: (asset) State Aid – Allotment

NOTE: This is only for the State Aid Construction Obligation shown on the SAPR

SAPR – Contract Receivable

Accounting Entries – for 95% of State Aid Construction Obligation ONLY - $429,418.41

Debit: (asset) Cash Credit: (asset) State Aid – Receivable

NOTE: Be sure to break up the entry of your receipt by what you are being paid for (Contract Construction, Engineering, Utility Relocation and/or Right of Way)

SAPR – 95% State Aid Contract Receipt

Accounting Entries – for the amount of Engineering, Utility Relocation or Right of Way, if any - $100,000.00

Debit: (asset) Cash Credit: (asset) State Aid – Allotment

NOTE: Be sure to break up the entry of your receipt by what you are being paid for (Contract Construction, Engineering, Utility Relocation and/or Right of Way)

SAPR – Engineering, Utility Relocation and Right of Way Receipt

Accounting Entries – for the amount of Engineering, Utility Relocation or Right of Way, if any - $100,000.00

Debt: (asset) State Aid – Deferred Revenue Credit: (asset) State Aid Construction –

Revenue

SAPR – Recognize Revenue for Eng, Utility Relocation and Right of Way

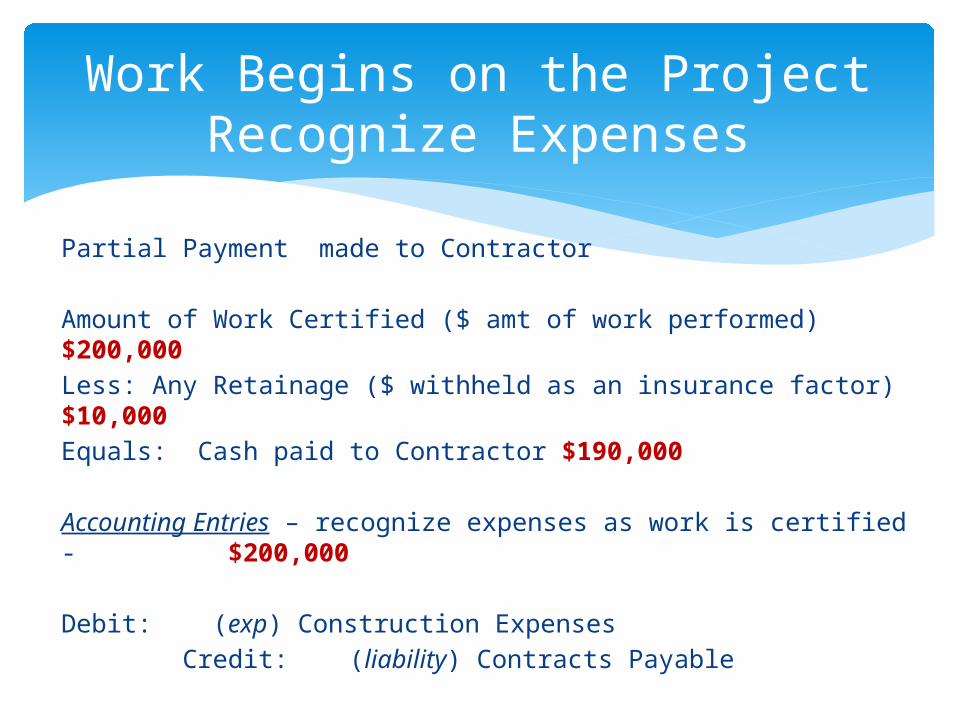

Partial Payment made to Contractor

Amount of Work Certified ($ amt of work performed) $200,000

Less: Any Retainage ($ withheld as an insurance factor) $10,000

Equals: Cash paid to Contractor $190,000

Accounting Entries – recognize expenses as work is certified - $200,000

Debit: (exp) Construction Expenses Credit: (liability) Contracts Payable

Work Begins on the ProjectRecognize Expenses

Partial Payment made to Contractor

Amount of Work Certified ($ amt of work performed) $200,000

Less: Any Retainage ($ withheld as an insurance factor) $10,000

Equals: Cash paid to Contractor $190,000

Accounting Entries – recognize earned revenue as work is certified - $200,000

Debit: (liability) State Aid – Deferred Revenue Credit: (revenue) State Aid Construction - Revenue

Work Begins on the Project (cont.)Recognize Earned Revenue

Partial Payment made to Contractor

Amount of Work Certified ($ amt of work performed) $200,000

Less: Any Retainage ($ withheld as an insurance factor) $10,000

Equals: Cash paid to Contractor $190,000

Accounting Entries – for amount of contractor disbursement - $190,000

Debit: (liability) Contracts Payable Credit: (asset) Cash

Work Begins on the Project (cont.)Disbursement to Contractor

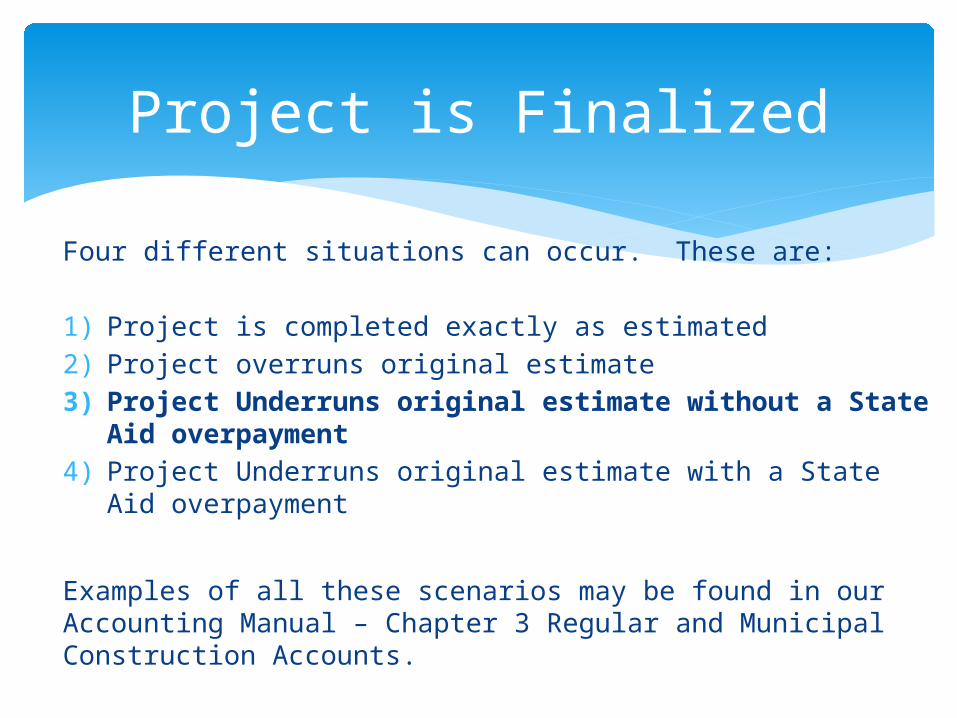

Four different situations can occur. These are:

1) Project is completed exactly as estimated2) Project overruns original estimate3) Project Underruns original estimate without a

State Aid overpayment4) Project Underruns original estimate with a State Aid

overpayment

Examples of all these scenarios may be found in our Accounting Manual – Chapter 3 Regular and Municipal Construction Accounts.

Project is Finalized

State Aid has encumbered too much and will only reimburse the portion of the encumbered amount that covers the actual project costs. Remember that the amount over the estimate will reduce your receivable & increase your allotment.

Accounting Entry - Recognize the underrun – $9,087.23 ($442,932.15 final obligated amt -

$452,019.38 original obligated amt)Debit: (asset) State Aid – Allotment Credit: (asset) State Aid – Receivable

Accounting Entry – Record State Aid Receipt - $13,513.74Debit: (asset) Cash Credit: (asset) State Aid - Receivable

Project Underruns Original Estimate without an Overpayment

There are two methods of accounting for these. We are using the one with optional entries because this method is useful to track the balance of the Bond Grant. The State Auditor’s Office may recommend these accounts be adjusted to zero at year end and re-established in the new-year.

Project is Awarded & SAPR sent inAccounting Entry – record bond grant amount -

$570,312.75

Debit: (asset) Bond Grant Credit: (liability) Bond Grand – Deferred Revenue

State Bond Grant

Accounting Entry – Recognize expense for work certified & record payable - $553,847.18

Debit: (const exp) State Bond – Expense Credit: (liability) Contracts Payable

Accounting Entry – Record disbursement to contractor - $526,154.82

Debit: (liability) Contracts Payable Credit: (asset) Cash

There will be numerous payments. This is only for the one attached to the Initial State Aid Pay Request.

State Bond Grant – Work Begins on Project

Accounting Entry – Record state bond receivable for work certified - $553,847.18

Debit: (asset) State Bond – Receivable Credit: (asset) State Bond Grant

Accounting Entry – Record state bond revenue for work certified - $553,847.18

Debit: (liability) State Bond – Deferred Revenue Credit: (revenue) State Bond – Revenue

There will be numerous payments. This is only for the one attached to the Initial State Aid Pay Request.

SAPR - State Bond Grant

Accounting Entry – Record receipt of state bond funds - $526,154.82

Debit: (asset) Cash Credit: (asset) State Bond – Receivable

NOTE: Revenue for these funds would be booked at the time it becomes certain and determinable, when work is certified.

SAPR - State Bond Grant (cont..)

CAUTION: State bond revenue can only be recognized up to the grant amount. In cases where the bond eligible items overrun the grant amount they become county expense and no revenue can be recognized. In special cases it may be possible to request and receive additional grant funds through an amendment to the bond agreement. This is rarely done

Accounting Entry – record bond grant amendment amount - $21,459.75

Debit: (asset) Bond Grant – Receivable Credit: (liability) Bond Grand – Deferred Revenue

State Bond Grant (cont..)Amendment to Bond Agreement

There are three main situations which can occur relating to the bond funds. These are:

1) Project is completed exactly as estimated2) Project overruns the original estimate3) Project underruns the original estimate

Examples of all these scenarios may be found in our Accounting Manual – Chapter 5 Special Construction Accounts.

State Bond Grant is Finalized

Accounting Entry – Recognize additional state bond revenue up to work certified - $37,925.32

Debit: (liability) State Bond – Deferred Revenue Credit: (revenue) State Bond – Revenue

Accounting Entry – Recognize expense greater than bond grant - $37,925.32

Debit: (expense) – Construction Expense Credit: (liability) – Contracts Payable

State Bond Grant is Finalized (cont..)

Accounting Entry – Record disbursement to contractor - $65,617.68

Debit: (liability) Contracts Payable Credit: (asset) Cash

Accounting Entry – Record receipt of state bond funds - $65,617.68

Debit: (asset) Cash Credit: (asset) State Bond - Receivable

State Bond Grant is Finalized (cont..)

John Fox 651-366-4854 [email protected] Degener 651-366-4850 [email protected] Martinez 651-366-4880 [email protected] Harding 651-366-4891 [email protected]

Questions on filling out SAPRWho to Call