Managing Weather and Price Risks Using Index Insurance and Risk-Contingent Credit

Upload

hubert-marshCategory

view

216download

0

Mobilizing Private Capital: Guarantees and Contingent / Risk Finance

Workshop on Tools for Risk Mitigation in Small-Scale Clean Infrastructure Projects

November 19-20, 2003World Bank Paris Office

New lending to emerging markets was close to zero from 1998 through 2002. Total private capital flows to

emerging markets were about $112.5 billion in 2002 against an average of $185 billion / yr. during the 1990s.

From a project finance perspective, there is an increasing acknowledgement that deals simply will not get done in

emerging markets without the multilateral financial institutions (MFIs), bilateral development agencies and

export credit agencies (ECAs).

The Setting

Risk Mitigation and the MFIs

“Traditional” Political RisksWar and Civil DisturbanceExpropriation and ConfiscationCurrency Convertibility/ Transferability

Contractual and Regulatory Risks Credit Risks Foreign Exchange Risks.

Risk Mitigation and the MFIs

“Traditional” risks have changed.

EXPROPRIATION – fashionable until the 1970s / 1980s but virtually nil now. The tendency now is

to regulate rather than expropriate.

CONTRACT FRUSTRATION – probably the main problem facing foreign investors in LDCs

Risk Mitigation and the MFIs

Commercial vs. Non-Commercial Risks

When the government is the offtake buyer or regulator, their “commercial” behaviour can

result in situations that make it difficult to define whether a non-commercial or commercial risk

has materialised.

Partial (Political) Risk GuaranteesNeeds Sovereign Guarantee

IBRD PRG Debt

AsDB PRG for Public Sector Debt

IsDB Credit Insurance Debt

IsDB Master Insurance Debt

Covers War/Civil Disturbance, Expropriation/Confiscation, Currency Convertibility & Transferability

Partial (Political) Risk GuaranteeNo Sovereign Guarantee Needed

MIGA Political Risk Ins. Debt/Equity

IsDB Foreign Inv. Ins. Debt/Equity

IADB PRG (Private Sector) Debt

AsDB PRG (Private Sector) Debt

Covers War/Civil Disturbance, Expropriation/Confiscation, Currency Convertibility & Transferability

Regulatory & Contractual Risk Instruments Offered by the MFIs

Breach of Contract Changes in Law License Requirements Approval and Consents Obstruction in Process of Arbitration Non-payment of a termination amount

Products offered by MIGA are well understood but market is not as familiar with regulatory risk products offered by IBRD, AfDB, IADB, AsDB and IsDB – need more effective marketing of these

services by MFIs.

Credit Risk Instruments Offered by the MFIsPartial Credit Guarantees

IBRD (IDA) – covers latter maturities / extends tenor – will IBRD drop the sovereign counter-guarantee requirement?

IADB – covers up to 40% of project cost up to $75 million, no sovereign guarantee needed – where are the deals?

AsDB - $500 million to PSALM (Philippines) approved with sovereign guarantee in 2002.

IFC – started providing cover in 2001 and now doing the business, flexible product, mostly financial sector but also some sub-sovereign infrastructure deals.

IDA PRG: “Asia Power Deal of the Year 2002”(Project Finance International)

IDA Partial Risk Guarantee covers lenders in case the Government of Vietnam does not meet its commitments under the PPA.

ANZ, Société Générale,

Sumitomo Mitsui

Mekong Energy

Company

Government of Vietnam

Guarantee

Indemnity Agreement

Government Undertakings

Loans

World Bank

Credit Risk Instruments Offered by the MFIsPartial Credit Guarantees

Need to have viable domestic financial institutions

MFI has to evaluate commercial risk – private sector skills

Foreign Exchange RiskLocal Currency Financing Options

AsDB, AfDB, EBRD and EIB: direct local currency financing / local bond issues.

IFC, AsDB, AsDB: lending local currency and swapping

IFC & IADB: also guarantee local bond issues

Foreign Exchange RiskDevaluation Backstop Facility

World Bank recently announced intention to test a currency devaluation backstop facility in 2004/2005.

1. What are the devaluation trigger points?

2. What if the currency never bounces back and the host government can’t pay?

Credit Enhancement, Guarantees & InfrastructureMulti-Stakeholder Funds & Initiatives

Emerging Africa Infrastructure Fund

GuarantCo

DevCo

The Global Environment Facility (GEF)

“The GEF shall operate, on the basis of collaboration and partnership among the Implementing Agencies as a mechanism for international cooperation for the purpose of providing new and additional grant and concessional funding to meet the agreed incremental costs of measures to achieve agreed global environmental benefits in the following focal areas[1]:

(a) Climate Change, (b) Biological diversity, (c) International Waters, and (d) Ozone Layer Depletion.”

[1] “ Instrument for the Establishment of the Restructured Global Environment Facility” (1994, amended 2002) http://www.gefweb.org/Documents/Instrument/instrument.html

Contingent Finance - GEF

Contingent financing is conceptually attractive when there is substantial uncertainty about the

existence and extent of incremental costs.

Instead of committing to a grant which may subsequently prove to have been unnecessary,

contingent financing recognizes the potential need for support but draws on public resources only when justified later, on the basis of actual

rather than projected costs.

Contingent Financing Mechanisms - GEF

Contingent Grant:

Unlike a conventional grant, a contingent grant is repaid to the GEF if the project is successfully financed. If the project is unsuccessful, the GEF funds paid out become a grant.

Contingent or Concessional Loan

A contingent loan treated as debt and has a higher repayment priority than the converted grant. Treated as project equity or an asset unless another arrangement is negotiated. Could be forgiven if the project fails.

A concessional loan is a loan at below-market rates. The availability of the concessional loan could be contingent upon participation of other commercial lenders to achieve co-financing and leveraging of non-GEF funds.

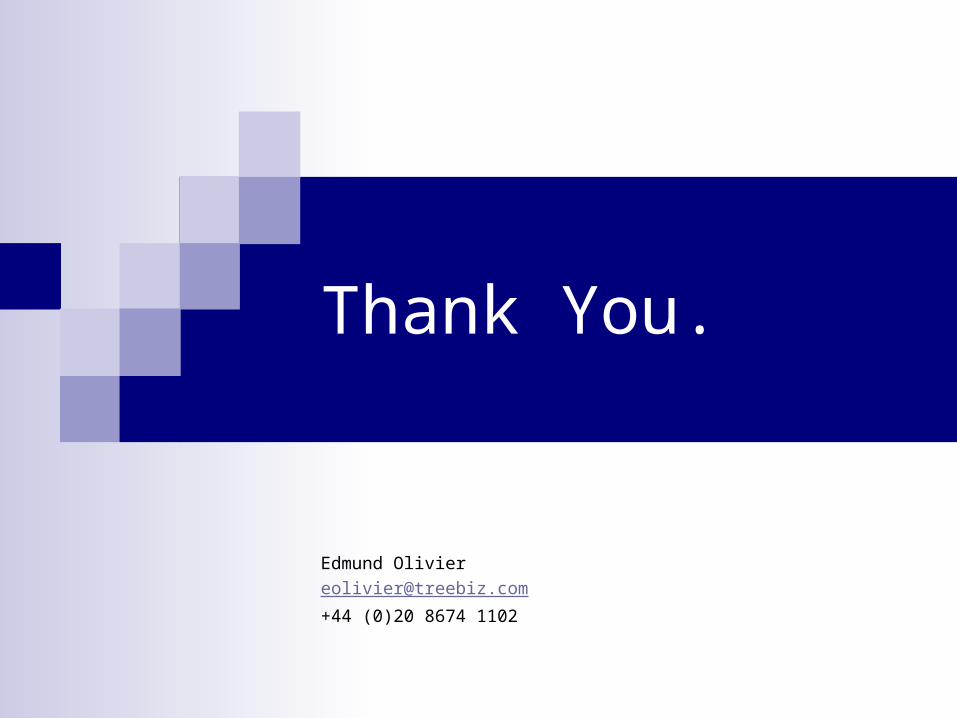

Other Financial Instruments – GEF

Partial Credit Guarantees

GEF Partial credit guarantees are similar to those provided by the multilaterals. Used encourage private-sector lenders, such as commercial banks and leasing companies, to make loans for projects that they would otherwise not lend to. The risk of the loan is shared with the private lender.

Investment Funds

For-profit, private sector, environmental funds that receive grant and/or non-grant funding from the GEF. The objective is to provide commercial or quasi-commercial financing to subprojects through a fund manager, with a possible financial return on capital.

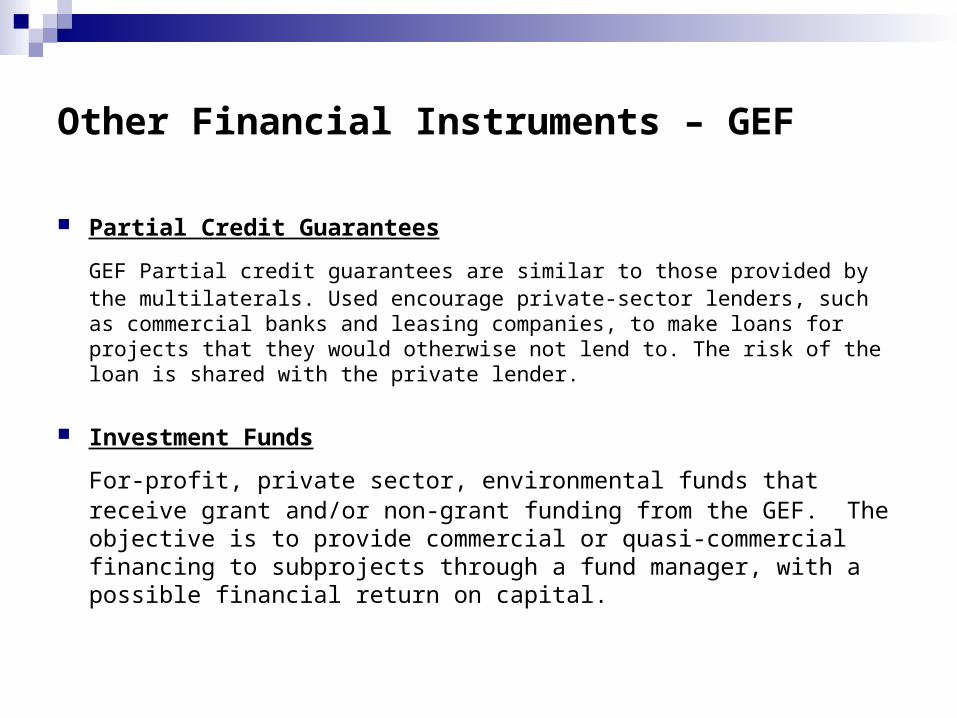

Quick Look at Insurance for RETs

1. Pre-Construction Phase Transit – marine, air, road – damage or delay

2. Construction Phase Contractor’s All Risks (CAR) CAR – Advanced Loss of Profits Business Interruption (BI) BI – Advanced loss of Profits Latent Defect / Decennial

3. Operation Phase Property Commercial All Risks

All Risks Business Interruption

Quick Look at Insurance for RETs

Example RET Risk Transfer Heat Map

Existing Insurance Products

Risk Categories

Construction All Risks

Resource Exploration

Property Damage

Business Interruption

Advance Loss of Profits

Environmental Liabilities

Performance / technology risk

Contractors overall risk

Workers Comp.

Third Party Liabilities

Wind Solar PVWave / TidalGeothermalBiogasSmall HydroBiomass

Comprehensive cover

Partial Cover

No Cover

Courtesy of Marsh

Insurance for RETs: small is beautiful

Global Sustainable Development Group

ForestRe: New Global Forestry Insurance Capacity

Need niche players with low overheads to cover small projects.

Contingent Risk Finance & ART Structures

Risk Finance vs. Risk TransferThe Retention Decision

Captives: the example of Forest Re(and the potential use of public contingent capital)

ART Deal in the Power Sector - Example

Steep rises in premiums have increased the attractiveness of these structures.

Munich Re described a double-trigger deal recently done with the power company Aquila for Business Interruption risk for gas-fired turbines in the USA as follows: IF a gas-fired turbine faced an unscheduled inoperative period THEN the reinsurer would finance the purchase of power in Aquila’s name. The two triggers for activation of the product are;

1) An unplanned outage at the facility AND

2) A spike in spot electricity prices – the contingent event for which the product would provide financial coverage.

Some Topics for the Breakout Group

Escrow Accounts Project Finance Reserve

Accounts Liquidity Facilities Structured Finance

(quanto hedges etc.) Tapping Islamic Financial

Instruments

GEF and the Private Sector

Working with the MFIs and Bilateral Agencies

Practicalities of Public-Private Interactions