Mobile Payments: Much More than In-Store | By David Hewitt, Mobile Center of Excellence Lead,...

11

DAVID HEWITT MOBILE PAYMENTS: MUCH MORE THAN IN-STORE

-

Upload

sapientnitro -

Category

Mobile

-

view

402 -

download

2

Transcript of Mobile Payments: Much More than In-Store | By David Hewitt, Mobile Center of Excellence Lead,...

2OUR PERSPECTIVES

Apple made one thing clear at their 2016 Worldwide Developers Con- ference: Mobile payments aren’t just for brick and mortar stores anymore.

The company’s decision to integrate its digital wallet service into mobile-web experiences is possibly the most important advancement the payment space has seen in the past five years. The announcement, which comes on the heels of Google’s decision to inte-grate Android Pay in much the same way, plants both organizations squarely on PayPal’s turf – and further ignites competition in an industry that has a handful of players coming from very different origins.

Significant as this announcement is, the battle to become the universal digi- tal wallet is far from decided. In 2015, transactions made from mobile phones totaled $8.7 billion in the U.S. and are expected to grow 210 percent to $27 billion by the end of 2016.1 With plans to be a preferred payment option and leverage transactional data (Google), reduce transaction fees (retailers), be the default payment card for mobile payments (banks), or be the preferred online payment platform (technology leaders), providers are unlikely to sur-render their slices of the market without a serious fight.

And, while mobile payment providers may not yet have a firm leader, com-panies ranging from retailers to banks and technology firms are all vying for position.

Notably, Apple and Google are inching ahead as they dominate the

1eMarketer. “Mobile Payments Will Triple in the US in 2016.” http://www.emarketer.com/Article/Mobile-Payments-Will-Triple-US-2016/1013147.

value of mobile transactions in 2015

$8.7B

expected value of mobile transactions in 2016

$27B

smartphone operating system market, using their direct access to the secure element in smartphones (which stores cardholder data on a chip or in the cloud).

This feature eliminates the need for consumers to find and open pay-ment apps, thereby removing two friction-filled steps to the payment process. The lack of direct access to the secure element, along with the complexities of competing business interests, likely dealt the final blow to the competitive Current-C initiative sponsored by Merchant Customer Exchange (MCX).

Current-C represented a consortium of large retailers’ efforts to launch their own mobile wallet aimed at reducing transaction fee rates from credit card companies. Yet MCX still has interest in the mobile payment space, and have now partnered with Chase Pay from JP Morgan Chase (which has 95 million active customers). Chase Pay’s soon-to-be-launched app will work on most smartphones and include some loyalty card integration, as well. Similar to the Current-C app however, the reliance on QR code scanning and app opening will likely prove too big an obstacle for widespread usage.

While retailers are losing the race of creating their own wallets, Apple’s announcement of opening up Apple Pay on mobile web will allow retailers to not only create a better experience for customers migrating to digital, but also generate significant sales through a simplified checkout process.

3OUR PERSPECTIVES

Consumer appetite for mobile payments continues to grow. Our recent survey of 800 U.S. smartphone users found that more than half (56 percent) of U.S. respondents have used mobile payments at least once (see Figure 1).

More important, mobile payments among the platform’s existing user base has increased tremendously, with 80 percent using an in-store payment op-tion several times a month, up from just 36 percent a year earlier.2

MOBILE PAYMENTS AND CONSUMERS

2Poole, David. “Banks, Brands, and Consumers: A Vision for Mobile, Payments-Driven Change.” http://www.sapientnitro.com/en-us.html#perspective/insights/insights-articles/banks-brands-and-consumers-a-vision-for-mobile-payment-driven-change.

3Among respondents who say that they’ve used mobile payments. The survey had 498 respondents, of which 56% (276) reported using mobile payments. Only those who have used mobile payments could answer the question around how often they used their smartphones for in-store payments. N = 276.

3

Among respondents who say they’ve used mobile payments, we saw a large increase in usage – from 36 percent to 80 percent (for those who use it "a few times a month" or more). The percentage of respondents who "rarely" use mobile payments, on the other hand, dropped to just 6 percent.

FIGURE01

Q: How often would you say that you currently use your mobile phone to pay for things in physical stores?3

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

Very frequently

(daily)

Frequently (2-3 times a week)

Occasionally (a few times

a month)

Seldom (every few months)

Rarely (a few times

a year)

5%

27%

39%

14%

6%

2015

13% 12%

19%

15%

49%

2016

OUR PERSPECTIVES

of consumers reported having used mobile payments at least once

56%

of mobile payment users use an in-store payment option several times a month

80%

4OUR PERSPECTIVES

Mobile checkout: Enabling a frictionless shopping experienceFor millions of smartphone users around the world, smartphones double as research tools during the shopping process. Many consumers use their device while considering a significant purchase, perhaps even in the store itself as they scan for lower prices or product availability at nearby locations.

However, while many people turn to their smartphone or tablet for answers, far fewer use a mobile device to actu-ally make a purchase. In fact, research shows that while cart abandonment is fairly common across digital channels, it’s particularly dismal for mobile with an average conversion rate of only 1.32 percent.4

Mobile’s low conversion rate can be explained, in part, by an often cumber-some and lengthy checkout process. Whether customers are using a mobile website or a native app, they are often pushed to the same checkout flow with, on average, 16 form fields and several screens required to complete a single purchase. More than one-quarter (28 percent) of mobile retail sites ask for the same information twice, instead of pre-filling fields where possible, and 3 in 10 (30 percent) do not auto-detect the type of credit card a customer is using based on the number typed.5

All of these friction points, along with typing on a small keyboard, can add up and convince a shopper to buy some-where else, or not at all.

At Apple’s 2016 Worldwide Developers Conference in June, the company announced that its mobile payment and digital wallet services can now be used to make purchases from select mobile- enabled and traditional websites, includ-ing Target, Expedia, Lululemon, Etsy, and The New York Times (see Figure 2).

Apple Pay purchases, which are au-thenticated through Apple’s Touch ID fingerprint sensor on an iPhone, iPad, or Apple Watch, eliminate the need for customers to manually enter payment and shipping information at checkout.

A full roll-out of the new Apple Pay capabilities are expected in advance of the holiday shopping season.

According to Apple, their payment system has experienced “tremendous” growth recently, with more than one million new users being added globally per week. Apple Pay is accepted at more than 2.5 million U.S. locations, as well as at 10 million contactless payment-ready locations in the U.K., Canada, Australia, and Singapore. Apple also has plans to launch the service in Switzerland, France, and Hong Kong.6

SPOTLIGHT ON APPLE PAY: EXPANDING TO ONLINE

4OUR PERSPECTIVES

4Monetate. E-commerce Quarterly (Q3 2015). http://www.monetate.com/resources/research/#ufh-i-34269668-ecommerce-quarterly-q3-2015.

5Baynard Institute. “The State of Mobile Checkout & Form Usability.” http://baymard.com/blog/mobile-ecommerce-checkout-forms.

6Apple. “Apple Special Event. June 13, 2016.” http://www.apple.com/apple-events/june-2016/.

of smartphone users download

66%66%

per month0 apps

Lululemon’s integration with Apple PayWith its recent expansion into the web, Apple Pay has already been in-tegrated by e-commerce shops across various industries – Lululemon being one of its early adopters.

FIGURE02

5OUR PERSPECTIVES

For retailers that have integrated their native apps with Apple Pay or Android Pay, the shopping experience can be far simpler, as the purchase is completed with credit card details and shipping information stored within the payment system. However, for today’s “always on” digital customer, the stark reality is that few people are interested in downloading a stand-alone retail app. In fact, two-thirds of smartphone users (66 percent) download zero new apps in a typical month.7

7comScore. The U.S. Mobile App Report. https://www.comscore.com/Insights/Presentations-and-Whitepapers/2014/The-US-Mobile-App-Report.

8Poole, David. “Banks, Brands, and Consumers: A Vision for Mobile, Payments-Driven Change.” http://www.sapientnitro.com/en-us.html#perspective/insights/insights-articles/banks-brands-and-consumers-a-vision-for-mobile-payment-driven-change.

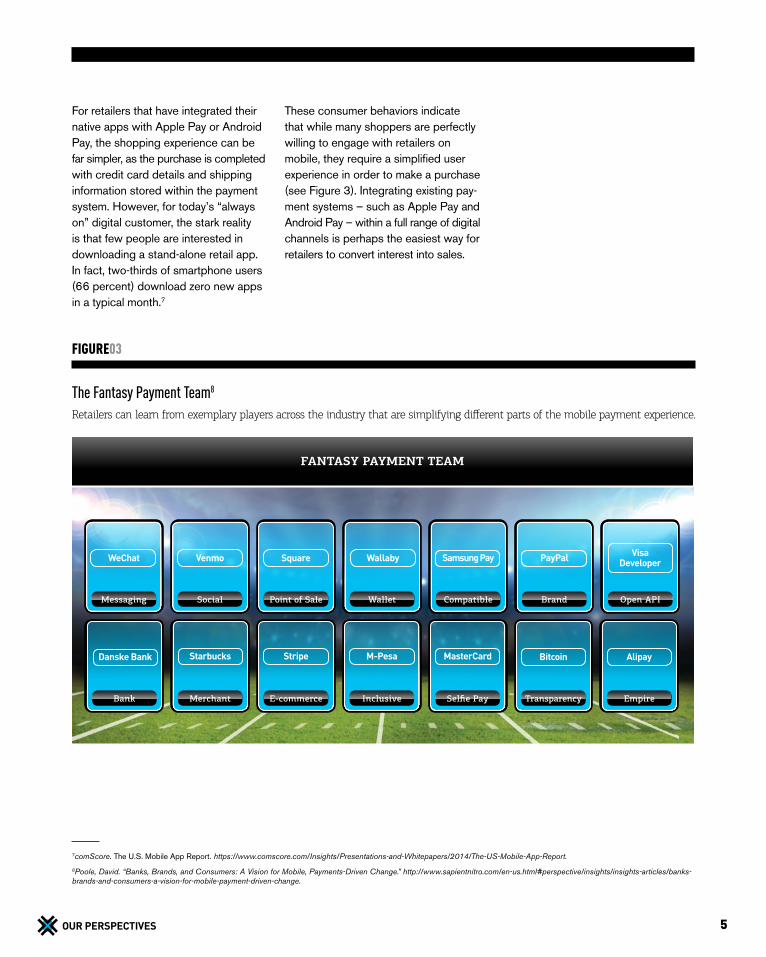

The Fantasy Payment Team8

Retailers can learn from exemplary players across the industry that are simplifying different parts of the mobile payment experience.

FIGURE03

FANTASY PAYMENT TEAM

Social Point of Sale Wallet Brand Open API

Bank Merchant Empire

CompatibleMessaging

E-commerce Inclusive Selfie Pay Transparency

Venmo Square Wallaby PayPal Visa Developer

Danske Bank Starbucks Alipay

Samsung PayWeChat

Stripe M-Pesa MasterCard Bitcoin

These consumer behaviors indicate that while many shoppers are perfectly willing to engage with retailers on mobile, they require a simplified user experience in order to make a purchase (see Figure 3). Integrating existing pay-ment systems – such as Apple Pay and Android Pay – within a full range of digital channels is perhaps the easiest way for retailers to convert interest into sales.

6OUR PERSPECTIVES

For thousands of Miami HEAT fans, game day got a lot easier with the intro-duction of a new mobile app during the 2015-16 season. The Miami HEAT app, which leverages Paydiant (now part of PayPal) technology, serves as a mobile wallet for fans, letting them buy tickets by simply scanning their smart phone while in the stadium. The app is also integrated with the team’s “Arena Bucks”, rewards program, which lets fans track their point balances and redeem them for various perks or discounts.

In the coming season there are plans to add in-seat ordering and express line busting for mobile payers. These new features will make it easier for fans to get back to enjoying the game even faster and are guaranteed to make for a happier HEAT Nation.

Going mobile has been a winning move for the HEAT as well. The app gives the organization a better sense of when, where, and how sales are made in the stadium, allowing them to better plan and staff during peak game-day periods. It also gives the team another touchpoint with fans – allowing them to reach the app users directly with flash sales and other promotions.

While the mobile app does not yet rival cash in terms of revenue generation, the average customer purchase was nearly $2 higher when made through the app during the regular season and just over $3.50 during the playoffs.

Who said there’s no such thing as a win-win?

THE MIAMI HEAT GOES MOBILE

6

The Miami HEAT app mobile wallet

FIGURE04

Easy Access to What You Need

•Customize how the app engages you with granular notification controls.

•Change your fan type and what content you see in your stream

•Access your mobile wallet and tickets

•See promotions and offers

Mobile Wallet & Loyalty

•Pay for concessions and fan gear from the HEAT store all from the app

•Add Credit and Debit cards quickly with the camera on your phone

•Earn “Arena Bucks” loyalty points with every purchase

Powered by

Mobile Wallet & Loyalty

•Pay for concessions and fan gear from the HEAT store all from the app

•Add Credit and Debit cards quickly with the camera on your phone

•Earn “Arena Bucks” loyalty points with every purchase

Powered by

OUR PERSPECTIVES

7OUR PERSPECTIVES

Consumers are migrating from general mobile web surfing patterns to anchoring their mobile behavior with on-device social platforms. With that in mind, the goal for retailers is to add features and functionality into heavily used social platforms.

Mobile messaging as a platform: Integrating bots, shopping, and paymentsFor the majority of Americans who own smartphones, time spent on mobile devices has reached an average of 4.7 hours a day.9 However, it’s not just the hours of use that have grown with mobile — how consumers are spending their time on smart devices is also changing. A recent report showed that the combined user base of the four most popular chat apps is larger than that of the four largest social networks.10 This highlights a fundamental shift in consumer behavior as they focus more on intimate connec-tions and less on broad-based social media consumption.

These findings also imply that consumers are migrating from general mobile web surfing patterns to anchoring their mobile behavior with on-device social platforms. With that in mind, the goal for retailers isn’t necessarily to create an independent app, but to add fea-tures and functionality into heavily used platforms like Facebook, Instagram, and Snapchat.

In many cases, these social media platforms are eager to engage brands in integrated campaigns. For example, in April, Facebook announced that it was introducing chatbots to its Messenger app, giving the company’s 900 million users the ability to order food, get the news, and access special deals, simply by “chatting” with the brand bots on their contact list.

9Informate. “Informate Mobile Intelligence First to Measure Smartphone Usage Internationally, Report Currently Tracks 12 Countries and Will Expand to 25 by the End of 2015.” http://www.informatemi.com/newsletter10022015.html.

10Business Insider. “Messaging apps are now bigger than social networks.” http://www.businessinsider.com/the-messaging-app-report-2015-11.

8OUR PERSPECTIVES

This trend – mobile messaging as a platform – is a huge opportunity for retailers, providing them with direct, albeit “earned” access to customers and the ability to promote flash sales, offer product suggestions, and share curated content. While in its infancy in North America, it is an established practice in other markets, most notably in China with their do-everything plat-form, “WeChat”.

Because the chatbot experience is based on a one-on-one exchange, brands can tailor the experience in a more conversational way. As such, it is a much more engaged format than display ads, yet more accessible and frictionless than native mobile apps. In comparison, most websites are also interactive, but dependent on the user to navigate a predetermined site map.

Bots, on the other hand, allow for the customer journey to be much more dynamic. The tailored conversation can lead the customer through a more consultative sales process via a com- bination of progressive navigation, such as keyword buttons (also known as “call-backs”) that appear after each response, and the ability to openly type in a command at any time. The app can also adjust its behavior so that it is not too invasive or pushy – something that

even some of the best sales associates in stores haven’t yet mastered.

For retailers interested in pursuing a mobile messaging partnership, the initial investment need not be huge. Retailers can start small – focusing on a limited customer segment or rolling out one product with pure-play mobile messaging apps such as WhatsApp, WeChat, Kik, Telegram, or, most recently, iMessage.

For example, brands can consider using a guiding selling bot for e-commerce using Apple Pay on mobile web for checkout. Or, if a brand has a personified character, then there could be some interesting activations, such as when the Muppets leveraged the Ms. Piggy persona to chat with fans on Facebook and promote the return of “The Muppet Show” to airwaves.

Finally, if there is a logical exchange of information that the brand owns in the mind of the consumer, then there could be an opportunity for the bot to offer frequent updates. For example, a ski resort could use an app to offer slope conditions during the winter on a weekly basis to customers who opt in to the service.

Mobile messaging as a platform is a huge opportunity for retailers.

9OUR PERSPECTIVES

1

Time to act: Looking ahead in the new mobile payment landscapeThe mobile payment space is far from certain. Every player – from the majors like Apple Pay and Android Pay to startups like Stripe and Square – is locked in a battle to own the space. Only time will tell how they will evolve and who will win. In the interim, there are three recommendations that retailers can consider as they navigate the changing mobile payments field.

Enable Apple Pay and Android Pay on native appsAs noted above, many retailers have native apps that allow customers to browse products and add them to their cart while in the app. However, at checkout, the customer is often taken outside the app and redirected to the mobile web purchasing page where they must enter payment and shipping information manually. This transition is generally where some customers lose interest in the purchase, and presents an opportunity for retailers to simplify and refine the process.

By integrating native apps with Apple Pay and Android Pay, retailers provide customers with a streamlined process. An automatically-populated checkout page can make consumers more likely to complete the purchase.

With Apple Pay integration for mobile websites and desktop sites available starting in Fall 2016, retailers can also consider rolling the feature through traditional online channels as well as using Apple’s Touch ID mobile web pay for mobile messaging purchases.

10OUR PERSPECTIVES

2Talk about securitySecurity is often cited as a major barrier to mobile payment adoption, and it was the leading deterrent cited by smart-phone users in our study. In fact, more than half (53 percent) of survey respon-dents reported that they would use mo-bile payments more if the transactions were secure. Unfortunately for retailers, only 1 percent of respondents cited retailers as the most trusted mobile payment provider, as compared to banks (43 percent) and alternate payment providers (14 percent) secure (see Figure 5).11

In truth, most transactions completed through mobile payments are far more secure than paying in a physical store. Between encryption of the transaction itself, security measures provided by the device, and the growing use of biometric logins on phones, consumers have relatively little to worry about when purchasing via mobile. In the coming months, it will fall to brands to help educate consumers on the security of mobile payments and the benefits of this channel.

Mobile payment users prioritize security, with 53% of respondents citing the importance of this factor.

FIGURE05

Q: Finish this sentence: I will use mobile payments more if...

It is secure

More retailers accept mobile payments

I receive exclusive offers and discounts

All of my payment cards, loyalty cards, and coupons are in one app

My purchase details are kept private

It is easy to use

None of these

It has social features, like being able to share my purchases

53%

43%

40%

36%

34%

31%

8%

3%

11Poole, David. “Banks, Brands, and Consumers: A Vision for Mobile, Payments-Driven Change.” http://www.sapientnitro.com/en-us.html#perspective/insights/insights-articles/banks-brands-and-consumers-a-vision-for-mobile-payment-driven-change.

3Experiment with mobile messagingMany retailers missed the boat when it came to mobile – having waited months or even years to develop and deploy a mobile-specific shopping ex-perience. They should be cautious not to let mobile messaging pass by in the same way. Regardless of the approach the brand takes – be it a chatbot with a “celebrity” persona or using the technology to offer real-time updates – the experience should be built with the consumer in mind. In any case, shaping for a frictionless experience with a clear value exchange is key.

David HewittMobile Center of Excellence Lead, SapientNitro Atlanta

David Hewitt leads the Mobile Center of Excellence, a full service team dedicated to designing and developing mobile experiences across the mobile web, native, and messaging plat-forms. As a global mobility strategy expert with over 20 years of experience, David helps brands take a mobile-first approach to transforming their business around tomorrow’s customer, helps shape innovation lab efforts, and connects emerging technologies to new client opportunities.

SapientNitro®, part of Publicis.Sapient, is a new breed of agency redefining storytelling for an always-on world. We’re changing the way our clients engage today’s connected consumers by uniquely creating integrated, immersive stories across brand communications, digital engagement, and omnichannel commerce. We call it our Storyscaping® approach, where art and imagination meet the power and scale of systems thinking. SapientNitro’s unique combination of creative, brand, and technology expertise results in one global team collaborating across disciplines, perspectives, and continents to create game-changing success for our Global 1000 clients, such as Chrysler, Citi, The Coca-Cola Company, Lufthansa, Target, and Vodafone, in thirty-one cities across The Americas, Europe, and Asia-Pacific. For more information, visit www.sapientnitro.com.

SapientNitro and Storyscaping are registered service marks of Sapient Corporation.

COPYRIGHT 2016 SAPIENT CORPORATION. ALL RIGHTS RESERVED.

INSIGHTS WHERE TECHNOLOGY & STORY MEETThe Insights publication features the marketing intelligence, trend forecasts, and innovative recommendations of boundary-breaking thought leaders. The SapientNitro Insights app brings that provocative collection – now in its digital form – to your on-the-go fingertips.

Download the full report at sapientnitro.com/insights and, for additional interactive and related content, download the SapientNitro Insights app.