Mobile Offshore Production Systems for Offshore Oil and ......1 Mobile Offshore Production Systems...

46

1 Mobile Offshore Production Systems for Offshore Oil and Gas Fields Presented by: Bruce Crager Rice Annual Forum XIII September 14, 2010 Houston, TX

Transcript of Mobile Offshore Production Systems for Offshore Oil and ......1 Mobile Offshore Production Systems...

1

Mobile Offshore Production

Systems for Offshore Oil and

Gas Fields

Presented by: Bruce Crager

Rice Annual Forum XIII

September 14, 2010

Houston, TX

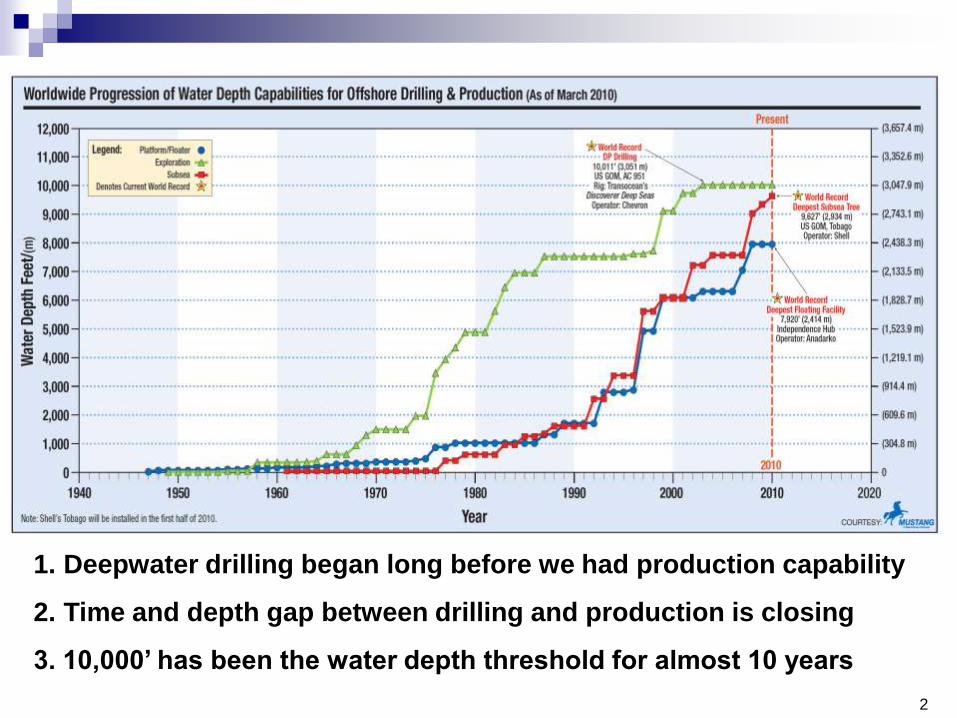

2

1. Deepwater drilling began long before we had production capability

2. Time and depth gap between drilling and production is closing

3. 10,000’ has been the water depth threshold for almost 10 years

3

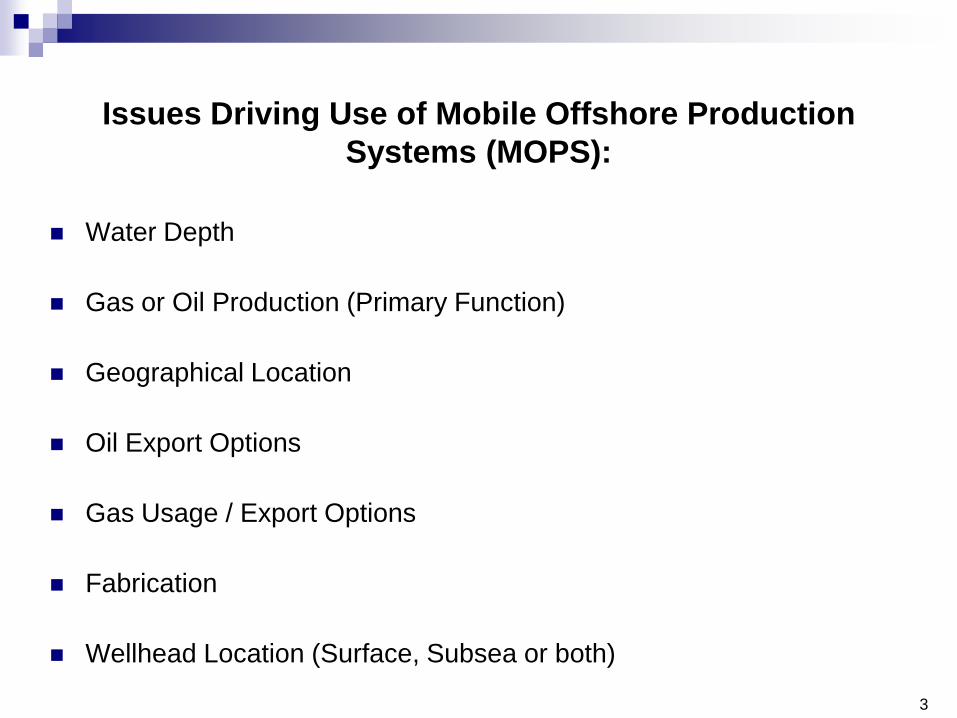

Issues Driving Use of Mobile Offshore Production

Systems (MOPS):

Water Depth

Gas or Oil Production (Primary Function)

Geographical Location

Oil Export Options

Gas Usage / Export Options

Fabrication

Wellhead Location (Surface, Subsea or both)

4

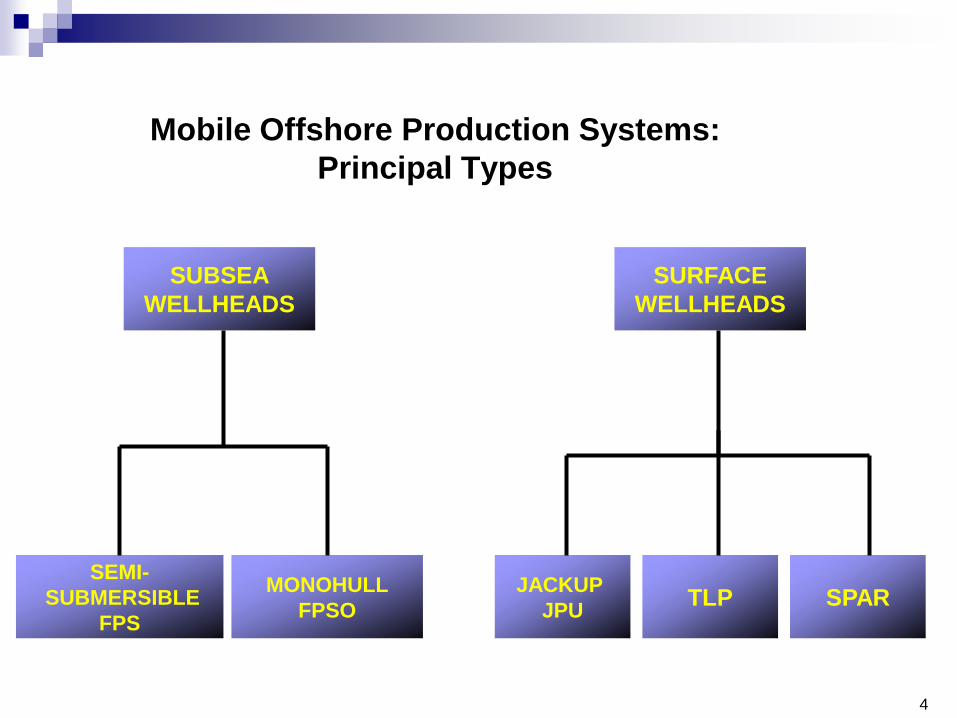

Mobile Offshore Production Systems:

Principal Types

SURFACE

WELLHEADS

JACKUP

JPUTLP SPAR

SEMI-

SUBMERSIBLE

FPS

MONOHULL

FPSO

SUBSEA

WELLHEADS

5

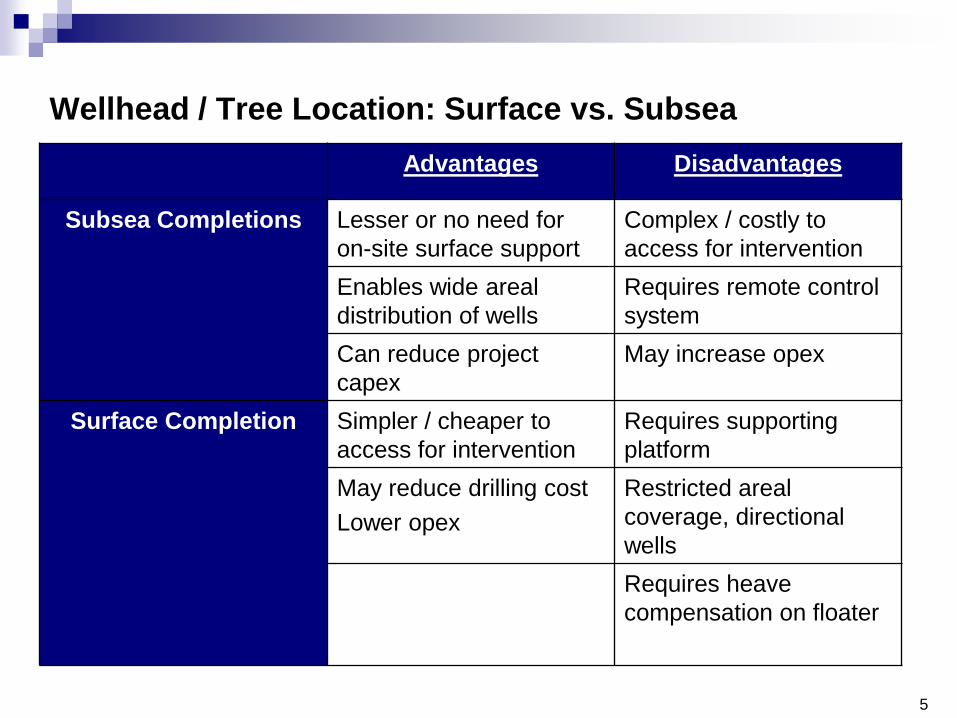

Wellhead / Tree Location: Surface vs. Subsea

Advantages Disadvantages

Subsea Completions Lesser or no need for

on-site surface support

Complex / costly to

access for intervention

Enables wide areal

distribution of wells

Requires remote control

system

Can reduce project

capex

May increase opex

Surface Completion Simpler / cheaper to

access for intervention

Requires supporting

platform

May reduce drilling cost

Lower opex

Restricted areal

coverage, directional

wells

Requires heave

compensation on floater

6

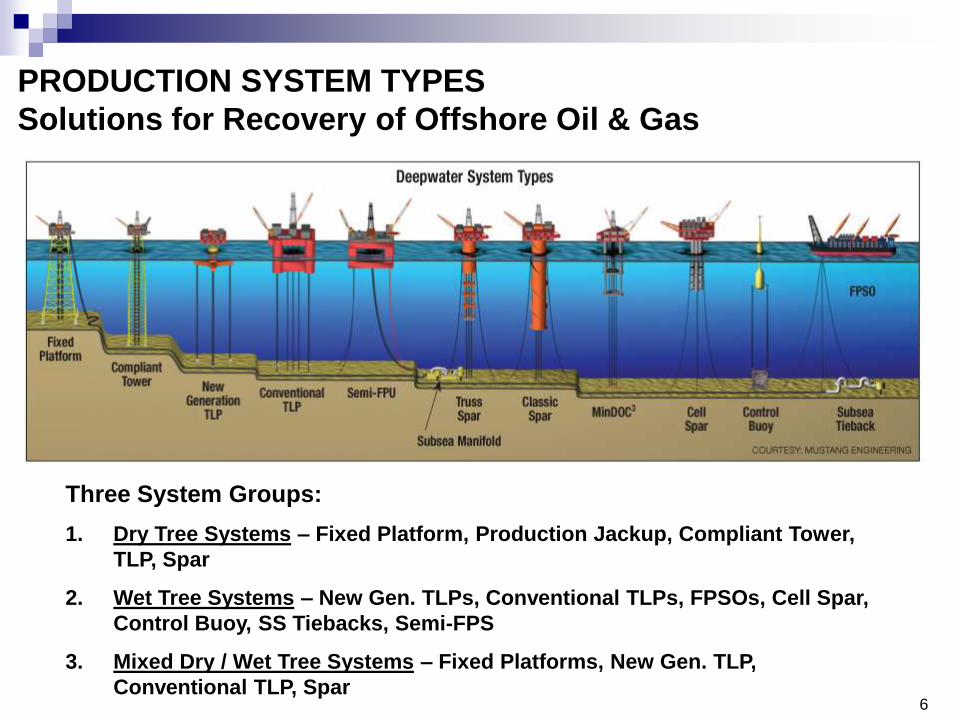

Three System Groups:

1. Dry Tree Systems – Fixed Platform, Production Jackup, Compliant Tower,

TLP, Spar

2. Wet Tree Systems – New Gen. TLPs, Conventional TLPs, FPSOs, Cell Spar,

Control Buoy, SS Tiebacks, Semi-FPS

3. Mixed Dry / Wet Tree Systems – Fixed Platforms, New Gen. TLP,

Conventional TLP, Spar

COURTESY OF: MUSTANG

ENGINEERING

PRODUCTION SYSTEM TYPES

Solutions for Recovery of Offshore Oil & Gas

7

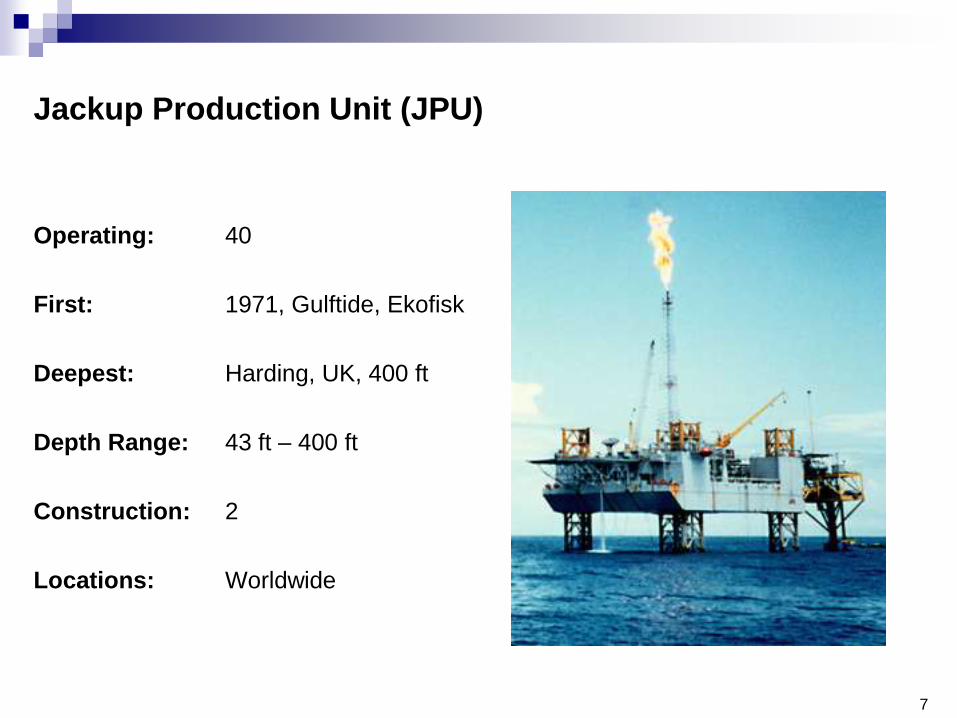

Jackup Production Unit (JPU)

Operating: 40

First: 1971, Gulftide, Ekofisk

Deepest: Harding, UK, 400 ft

Depth Range: 43 ft – 400 ft

Construction: 2

Locations: Worldwide

8

FPS - Semi Submersible

Operating : 39

Stacked: 4

First: 1975, Argyll, Hamilton

Deepest: 7,920 ft, MC920

Independence Hub

Construction: 6

Locations: Worldwide

9

FPSO

Operating : 182

Stacked: 13

First: 1977, Castellon, Shell

Deepest: 8,300 ft, Cascade

Chinook

Construction: 29

Locations: Worldwide

10

TLP

Operating : 24

First: 1984, Hutton, Conoco

Deepest: 4,674 ft, Magnolia

GB783/84

Construction: 1

Locations: North Sea, Angola,

Gulf of Mexico,

Indonesia and

Equatorial Guinea

11

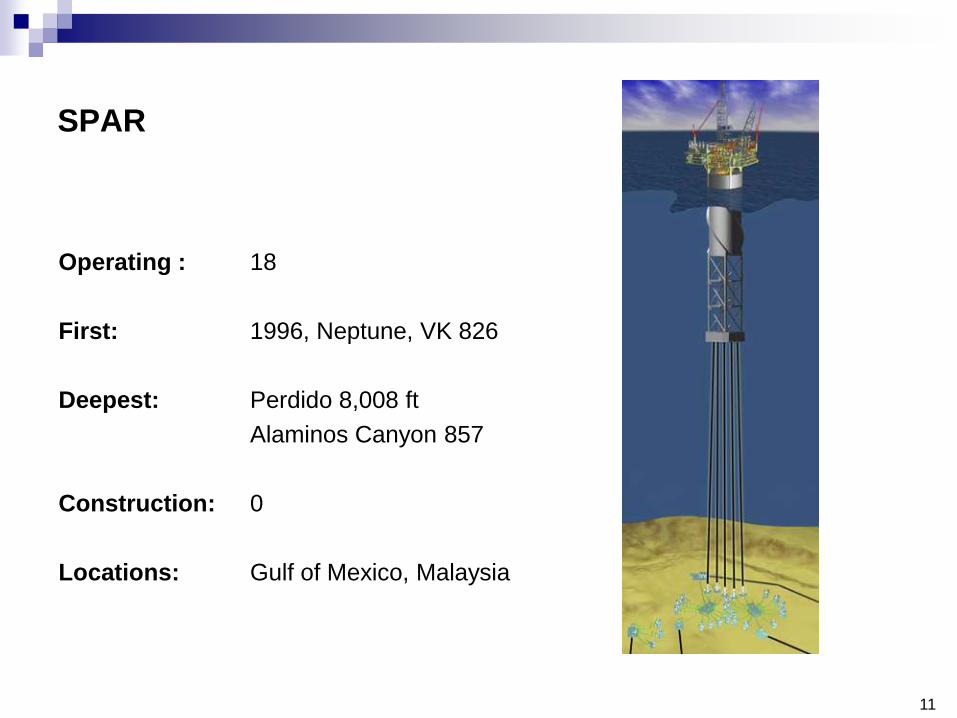

SPAR

Operating : 18

First: 1996, Neptune, VK 826

Deepest: Perdido 8,008 ft

Alaminos Canyon 857

Construction: 0

Locations: Gulf of Mexico, Malaysia

12

0

10,000

20,000

30,000

40,000

50,000

0 2,000 4,000 6,000 8,000 10,000

Water Depth (ft)

Facil

ity P

aylo

ad

(st)

Spars

Semis

TLP

Spar

Semi

TLP

Optimum Application Ranges

Source: FloaTEC

13

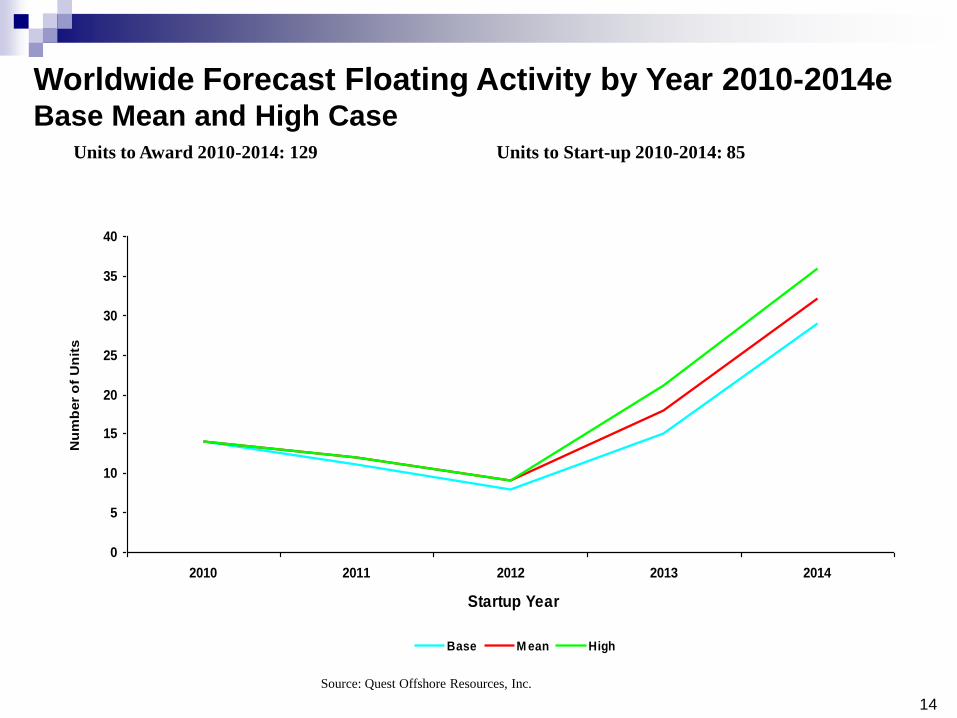

Worldwide Forecast Floating Activity by Year 2010-2014e

Units to Start-up 2010-2014: 85

Source: Quest Offshore Resources, Inc.

Units to Award 2010-2014: 129

0

5

10

15

20

25

30

35

40

2010

e

2011

e

2012

e

2013

e

2014

e

Year

Nu

mb

er

of

Un

its

Award Startup

14

Worldwide Forecast Floating Activity by Year 2010-2014eBase Mean and High Case

Units to Start-up 2010-2014: 85

Source: Quest Offshore Resources, Inc.

Units to Award 2010-2014: 129

0

5

10

15

20

25

30

35

40

2010 2011 2012 2013 2014

Startup Year

Nu

mb

er

of

Un

its

Base M ean High

15

Top Operator Analysis

16

Worldwide FPSO Top OperatorsFlowing and Under Construction Top 11 Operators (87 of 211 Units)

Source: Quest Offshore Resources, Inc.

0

5

10

15

20

25

30

35

Petro

bras

CNOO

C

Exxon

Mobil

Total

Enibp

Chev

ron

Roya

l Dutc

h/She

ll

Woodsi

de Pet

role

um

Cono

coPhill

ips

Petro

nas C

arig

ali

Operator

Nu

mb

er

of

Un

its

17

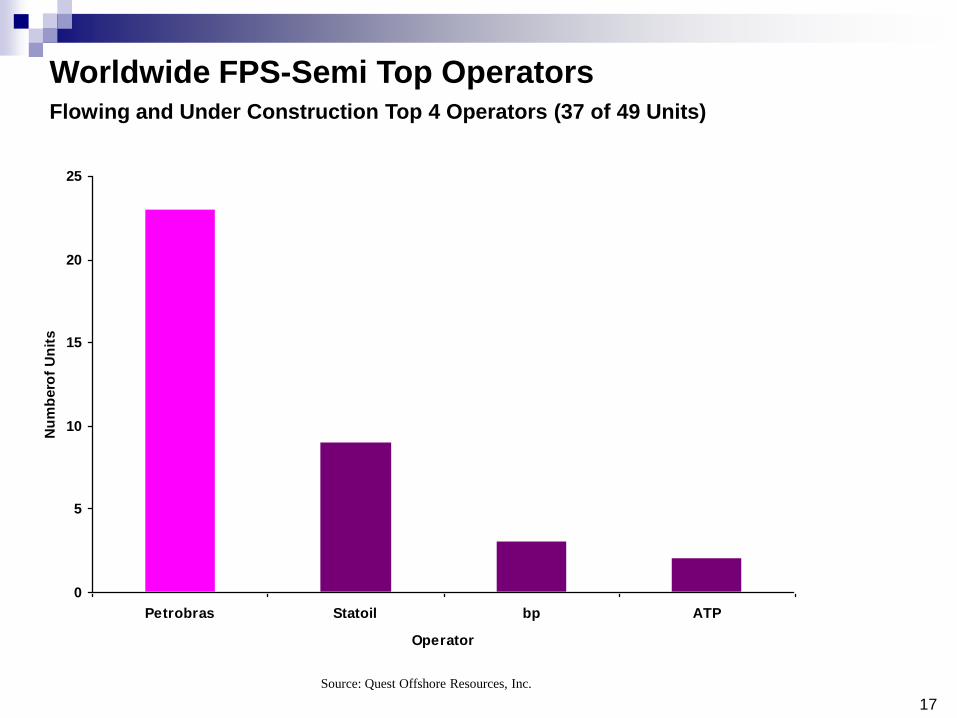

Worldwide FPS-Semi Top OperatorsFlowing and Under Construction Top 4 Operators (37 of 49 Units)

Source: Quest Offshore Resources, Inc.

0

5

10

15

20

25

Petrobras Statoil bp ATP

Operator

Nu

mb

ero

f U

nit

s

18

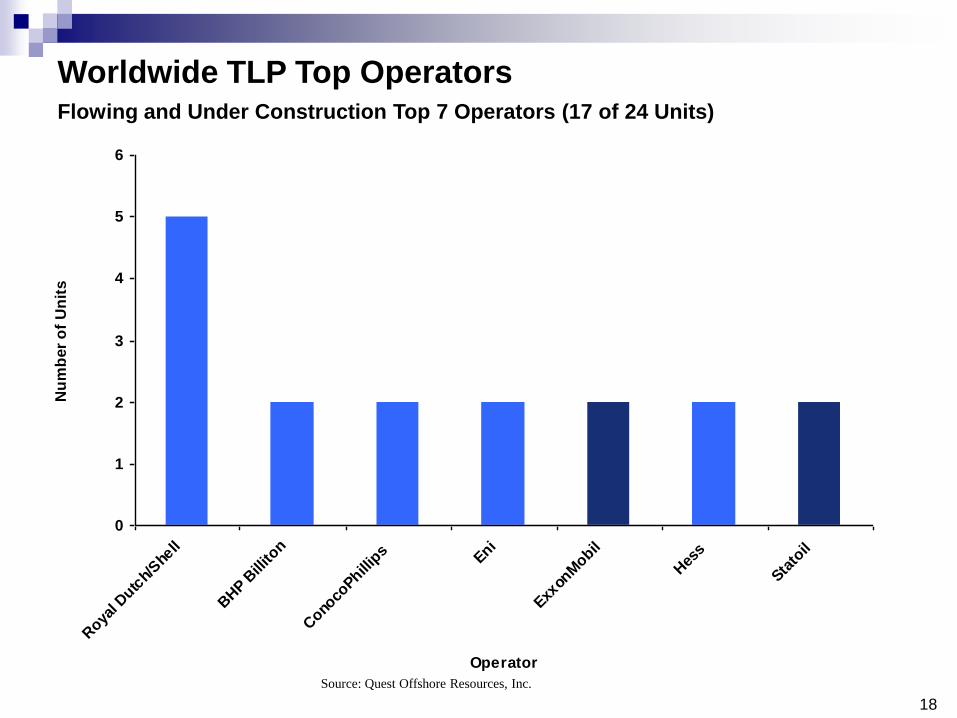

Worldwide TLP Top OperatorsFlowing and Under Construction Top 7 Operators (17 of 24 Units)

Source: Quest Offshore Resources, Inc.

0

1

2

3

4

5

6

Roya

l Dutc

h/She

ll

BHP B

illito

n

Cono

coPhill

ips Eni

Exxon

Mobil

Hes

s

Stato

il

Operator

Nu

mb

er

of

Un

its

19

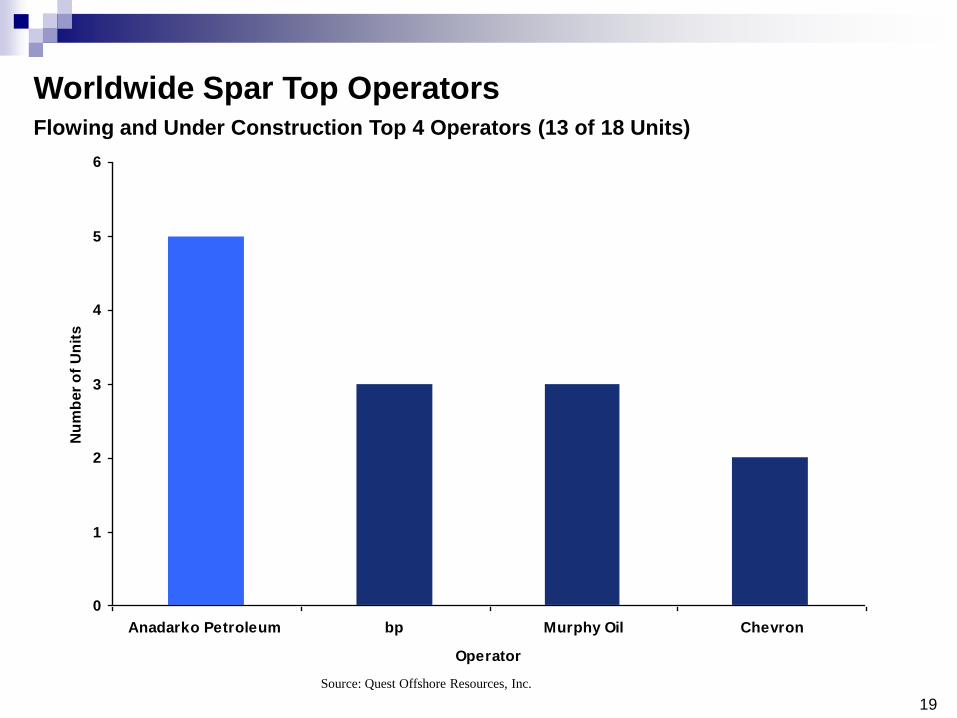

Worldwide Spar Top OperatorsFlowing and Under Construction Top 4 Operators (13 of 18 Units)

Source: Quest Offshore Resources, Inc.

0

1

2

3

4

5

6

Anadarko Petroleum bp Murphy Oil Chevron

Operator

Nu

mb

er

of

Un

its

20

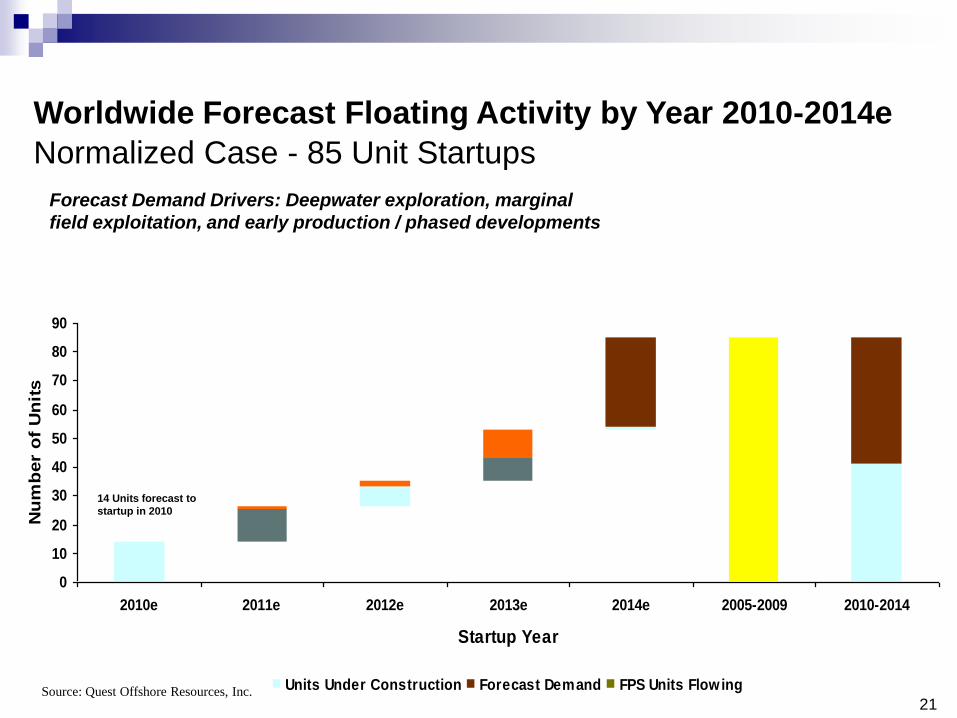

Normalized Forecast

21

0

10

20

30

40

50

60

70

80

90

2010e 2011e 2012e 2013e 2014e 2005-2009 2010-2014

Startup Year

Nu

mb

er

of

Un

its

Units Under Construction Forecast Demand FPS Units Flowing

Worldwide Forecast Floating Activity by Year 2010-2014e

Normalized Case - 85 Unit Startups

Forecast Demand Drivers: Deepwater exploration, marginal

field exploitation, and early production / phased developments

14 Units forecast to

startup in 2010

Source: Quest Offshore Resources, Inc.

22

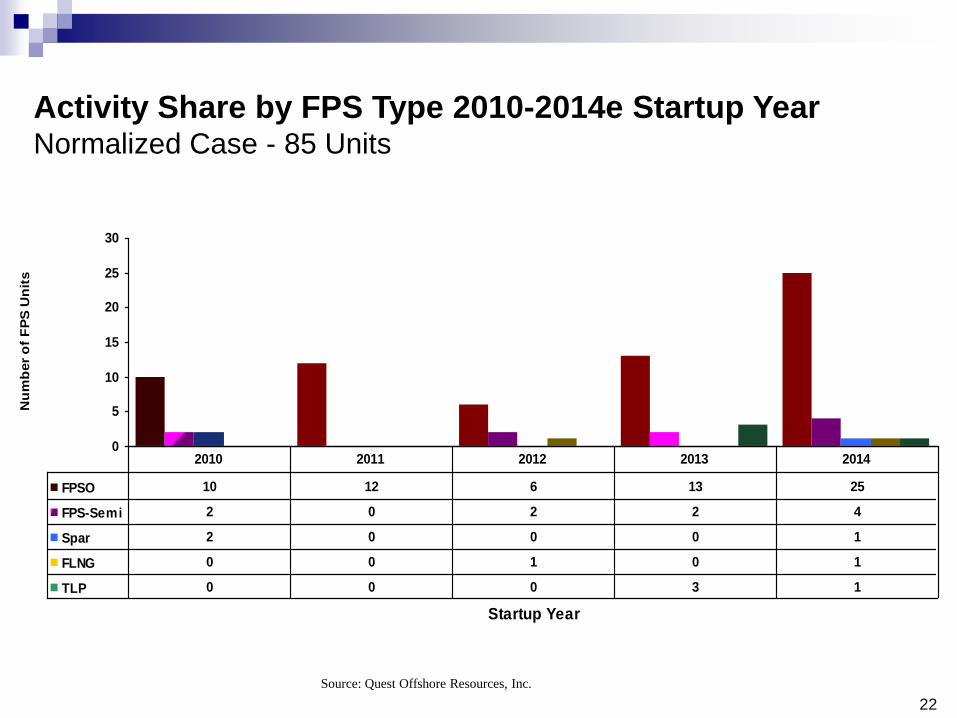

Activity Share by FPS Type 2010-2014e Startup Year Normalized Case - 85 Units

Source: Quest Offshore Resources, Inc.

0

5

10

15

20

25

30

Startup Year

Nu

mb

er

of

FP

S U

nit

s

FPSO 10 12 6 13 25

FPS-Semi 2 0 2 2 4

Spar 2 0 0 0 1

FLNG 0 0 1 0 1

TLP 0 0 0 3 1

2010 2011 2012 2013 2014

23

Global Award Analysis

24

Worldwide FPS Awards 2002 (A) – 2014 (e) (Mean Case)

Source: Quest Offshore Resources, Inc.

0

10

20

30

40

50

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hull Award Year

Nu

mb

er

of

FP

S U

nit

s

Awarded Unawarded High Case Base Case

25

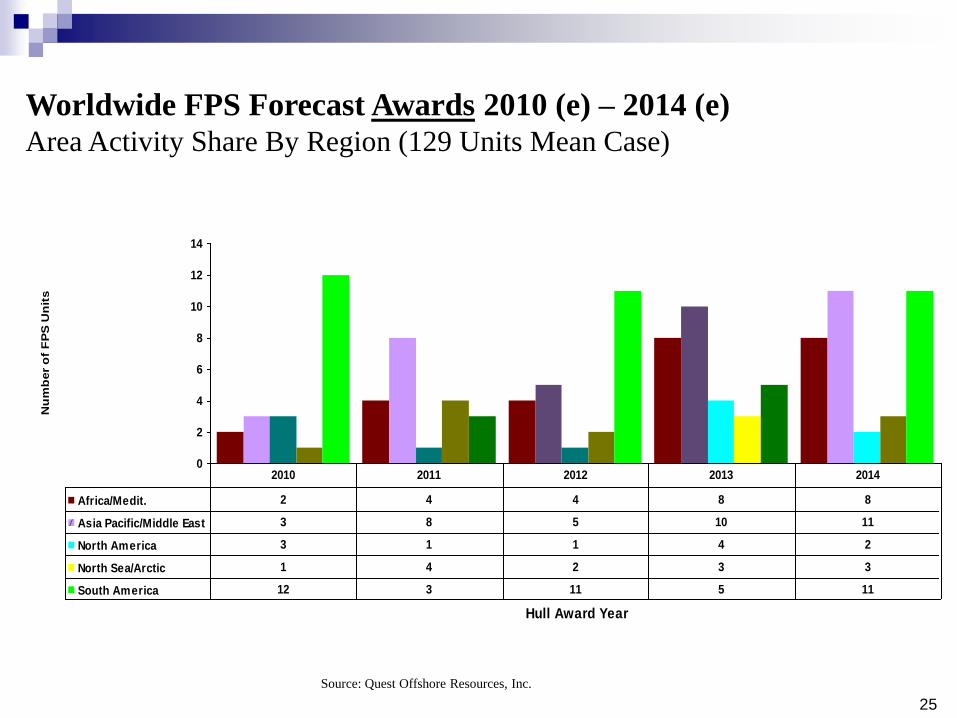

Worldwide FPS Forecast Awards 2010 (e) – 2014 (e)

Area Activity Share By Region (129 Units Mean Case)

Source: Quest Offshore Resources, Inc.

0

2

4

6

8

10

12

14

Hull Award Year

Nu

mb

er

of

FP

S U

nit

s

Africa/Medit. 2 4 4 8 8

Asia Pacific/Middle East 3 8 5 10 11

North America 3 1 1 4 2

North Sea/Arctic 1 4 2 3 3

South America 12 3 11 5 11

2010 2011 2012 2013 2014

26

Worldwide FPS Awards 2010 (A) – 2014 (e) Mean Case By FPS Type (129 Units)

Source: Quest Offshore Resources, Inc.

0

5

10

15

20

25

30

Hull Award Year

Nu

mb

er

of

FP

S U

nit

s

FPSO 17 13 20 24 26

FPS-Semi 1 3 1 2 5

Spar 0 0 0 3 1

FLNG 1 3 1 1 2

TLP 2 1 1 0 1

2010 2011 2012 2013 2014

27

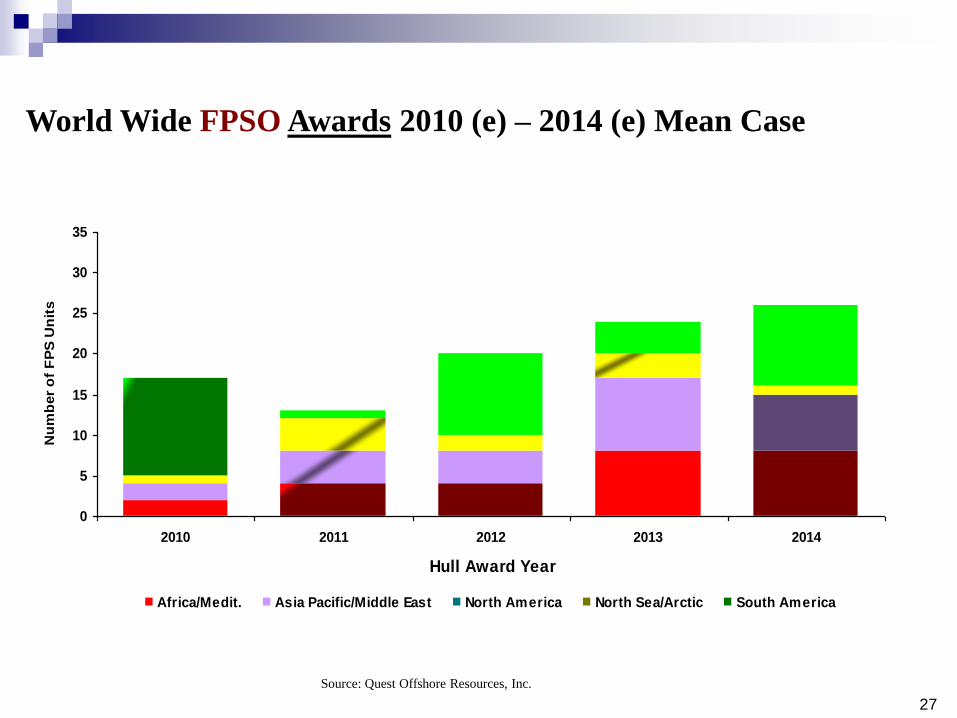

World Wide FPSO Awards 2010 (e) – 2014 (e) Mean Case

Source: Quest Offshore Resources, Inc.

0

5

10

15

20

25

30

35

2010 2011 2012 2013 2014

Hull Award Year

Nu

mb

er

of

FP

S U

nit

s

Africa/Medit. Asia Pacific/Middle East North America North Sea/Arctic South America

28

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hull Award Year

Th

ou

san

ds o

f U

S D

ollars

Africa/M edit. Asia Pacific/M iddle East

North America North Sea/Arctic

South America

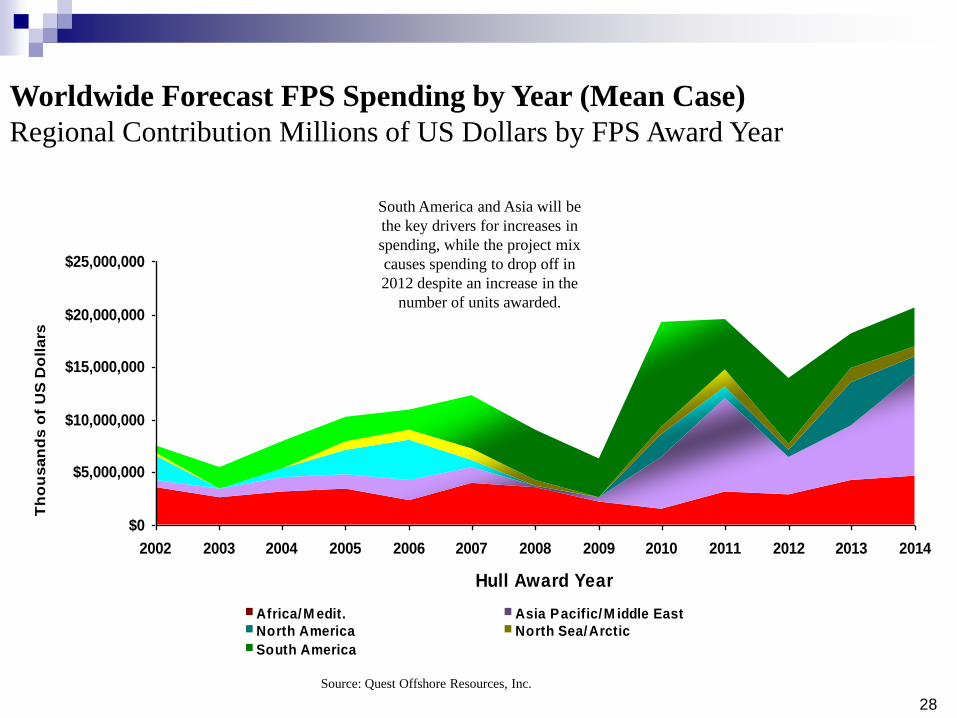

Worldwide Forecast FPS Spending by Year (Mean Case)

Regional Contribution Millions of US Dollars by FPS Award Year

South America and Asia will be

the key drivers for increases in

spending, while the project mix

causes spending to drop off in

2012 despite an increase in the

number of units awarded.

Source: Quest Offshore Resources, Inc.

29

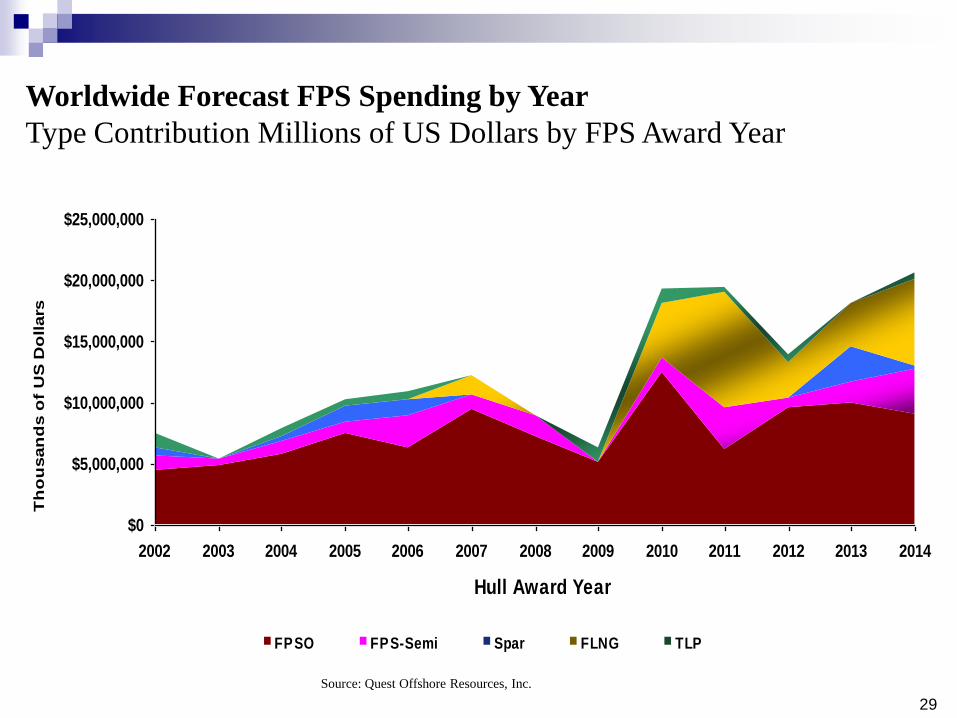

Worldwide Forecast FPS Spending by Year

Type Contribution Millions of US Dollars by FPS Award Year

Source: Quest Offshore Resources, Inc.

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hull Award Year

Th

ou

san

ds o

f U

S D

ollars

FPSO FPS-Semi Spar FLNG TLP

30

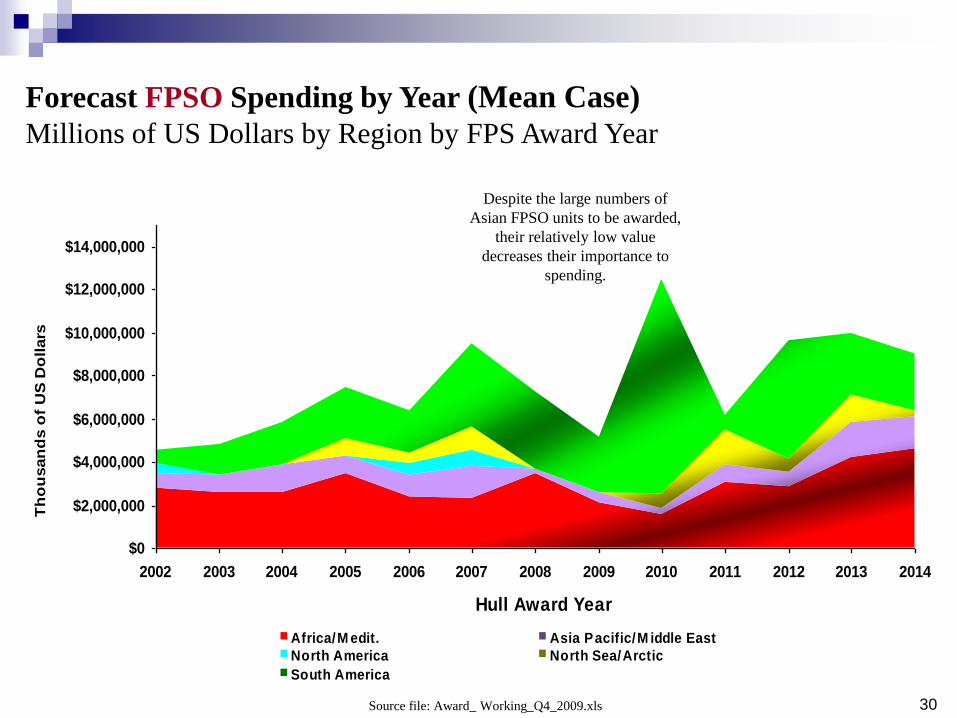

Forecast FPSO Spending by Year (Mean Case)

Millions of US Dollars by Region by FPS Award Year

Source file: Award_ Working_Q4_2009.xls

Despite the large numbers of

Asian FPSO units to be awarded,

their relatively low value

decreases their importance to

spending.

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Hull Award Year

Th

ou

san

ds o

f U

S D

ollars

Africa/M edit. Asia Pacific/M iddle East

North America North Sea/Arctic

South America

31

Leased FPS Units

32

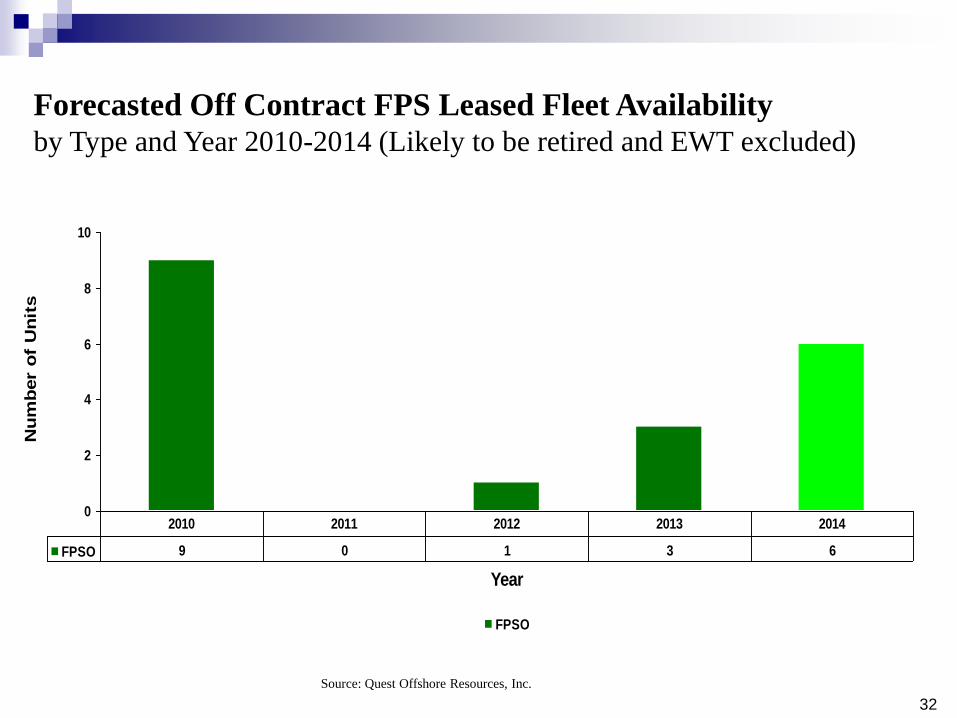

Forecasted Off Contract FPS Leased Fleet Availability

by Type and Year 2010-2014 (Likely to be retired and EWT excluded)

Source: Quest Offshore Resources, Inc.

0

2

4

6

8

10

Year

Nu

mb

er o

f U

nit

s

FPSO

FPSO 9 0 1 3 6

2010 2011 2012 2013 2014

33

5%

8%

3%

10%

3%

3%

3%

17%

3%

3%

9%

14%

3%

8%

3%5%

Aker Floating Production

Bluewater Offshore

Bumi Armada

BW Offshore

FPS Ocean

Fred Olsen Production

Maersk

MODEC

Nexus/APL

Nortech

Prosafe Production

SBM

Sea Production

Sevan Marine

Tanker Pacific

Teekay Shipping Corp

Leased FPSO Market Share by Owner

Owners with >1 Unit

Includes JV Shares

Source: Quest Offshore Resources, Inc.

34

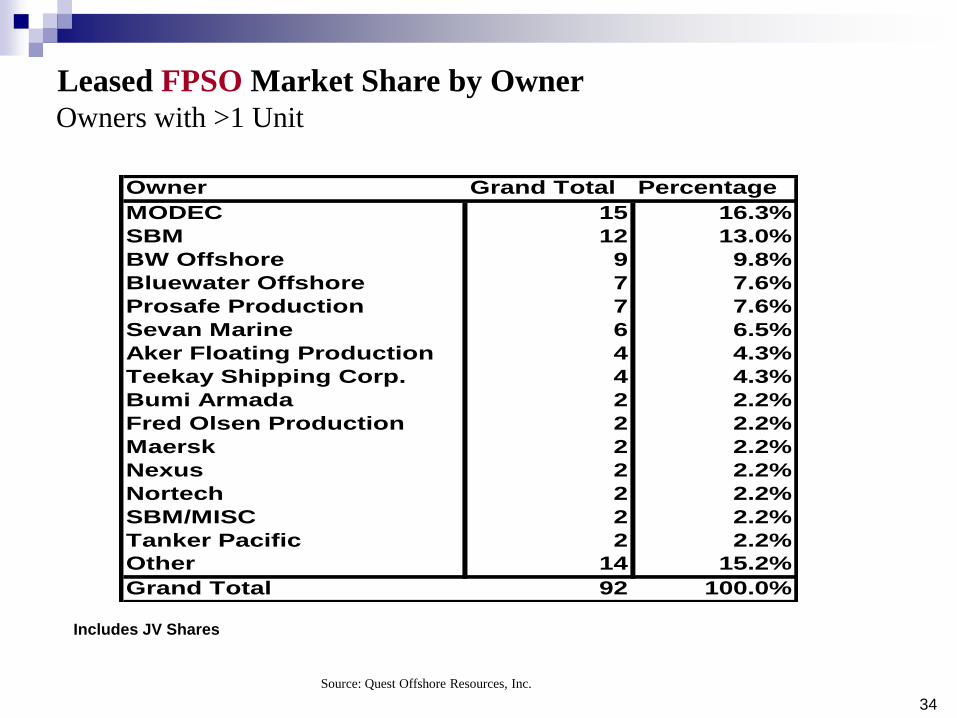

Leased FPSO Market Share by Owner

Owners with >1 Unit

Includes JV Shares

Source: Quest Offshore Resources, Inc.

Owner Grand Total Percentage

MODEC 15 16.3%

SBM 12 13.0%

BW Offshore 9 9.8%

Bluewater Offshore 7 7.6%

Prosafe Production 7 7.6%

Sevan Marine 6 6.5%

Aker Floating Production 4 4.3%

Teekay Shipping Corp. 4 4.3%

Bumi Armada 2 2.2%

Fred Olsen Production 2 2.2%

Maersk 2 2.2%

Nexus 2 2.2%

Nortech 2 2.2%

SBM/MISC 2 2.2%

Tanker Pacific 2 2.2%

Other 14 15.2%

Grand Total 92 100.0%

35

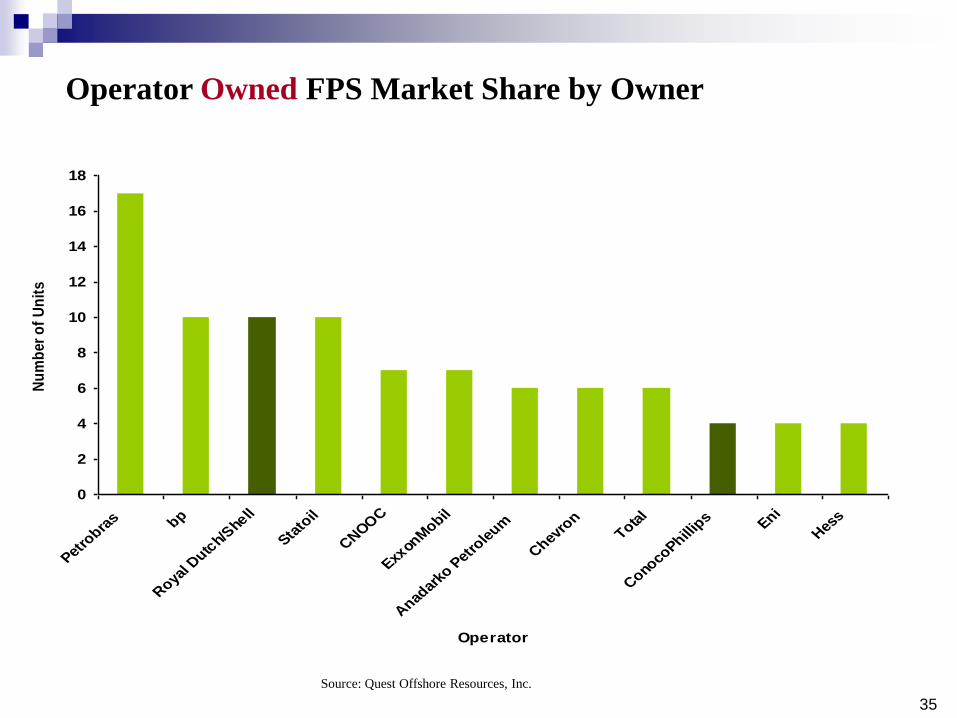

Operator Owned FPS Market Share by Owner

Source: Quest Offshore Resources, Inc.

0

2

4

6

8

10

12

14

16

18

Petro

bras bp

Roya

l Dutc

h/She

ll

Stato

il

CNOO

C

Exxon

Mobil

Anad

arko

Pet

role

um

Chev

ron

Total

Cono

coPhill

ips Eni

Hes

s

Operator

Nu

mb

er

of

Un

its

36

Global Hull Fabrication Analysis

37

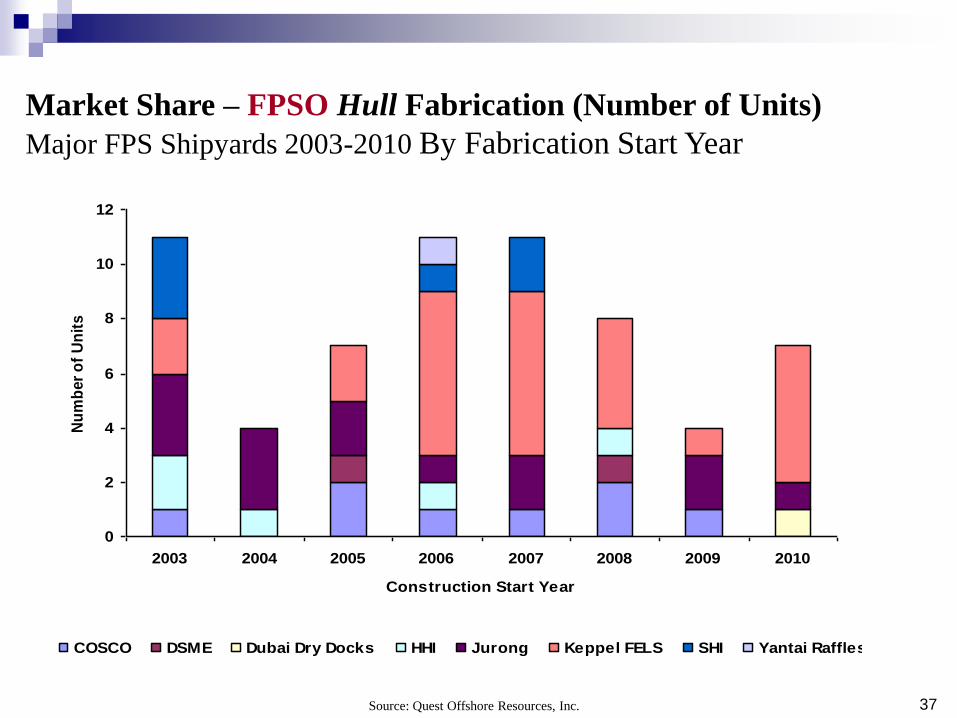

Market Share – FPSO Hull Fabrication (Number of Units)

Major FPS Shipyards 2003-2010 By Fabrication Start Year

Source: Quest Offshore Resources, Inc.

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010

Construction Start Year

Nu

mb

er

of

Un

its

COSCO DSME Dubai Dry Docks HHI Jurong Keppel FELS SHI Yantai Raffles

38

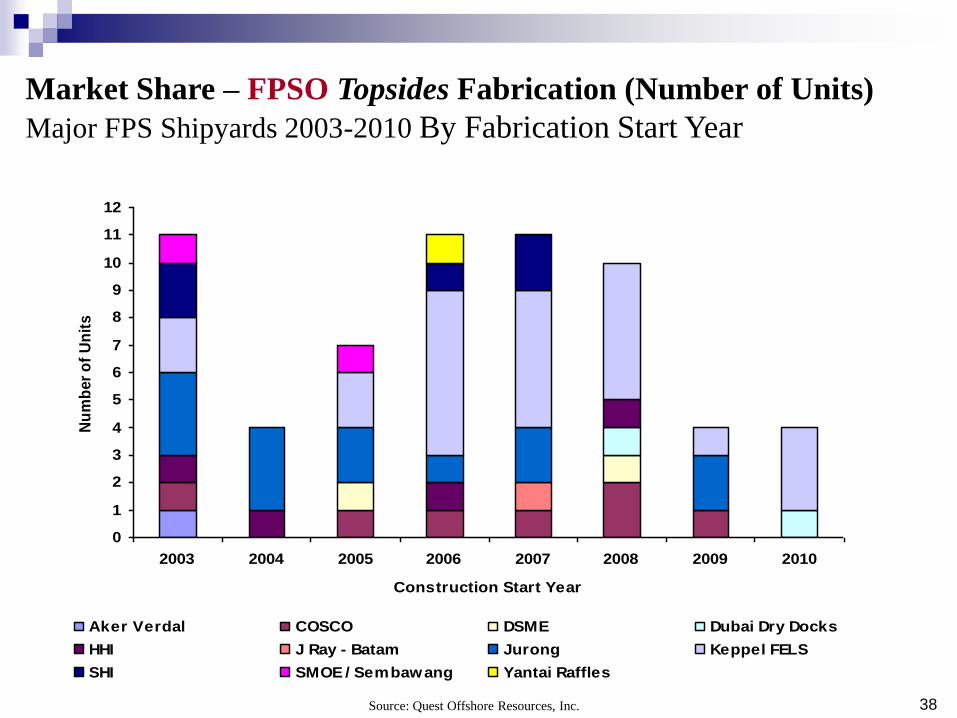

Market Share – FPSO Topsides Fabrication (Number of Units)

Major FPS Shipyards 2003-2010 By Fabrication Start Year

Source: Quest Offshore Resources, Inc.

0

1

2

3

4

5

6

7

8

9

10

11

12

2003 2004 2005 2006 2007 2008 2009 2010

Construction Start Year

Nu

mb

er

of

Un

its

Aker Verdal COSCO DSME Dubai Dry Docks

HHI J Ray - Batam Jurong Keppel FELS

SHI SMOE / Sembawang Yantai Raffles

39

Market Share – FPS-Semi Hull Fabrication (Number of Units)

Major FPS Shipyards 2003-2010 By Fabrication Start Year

Source: Quest Offshore Resources, Inc.

0

1

2

3

4

2003 2004 2005 2006 2007

Construction Start Year

Nu

mb

er

of

Un

its

Aker Verdal DSME Jurong Keppel FELS MMHE SHI

40

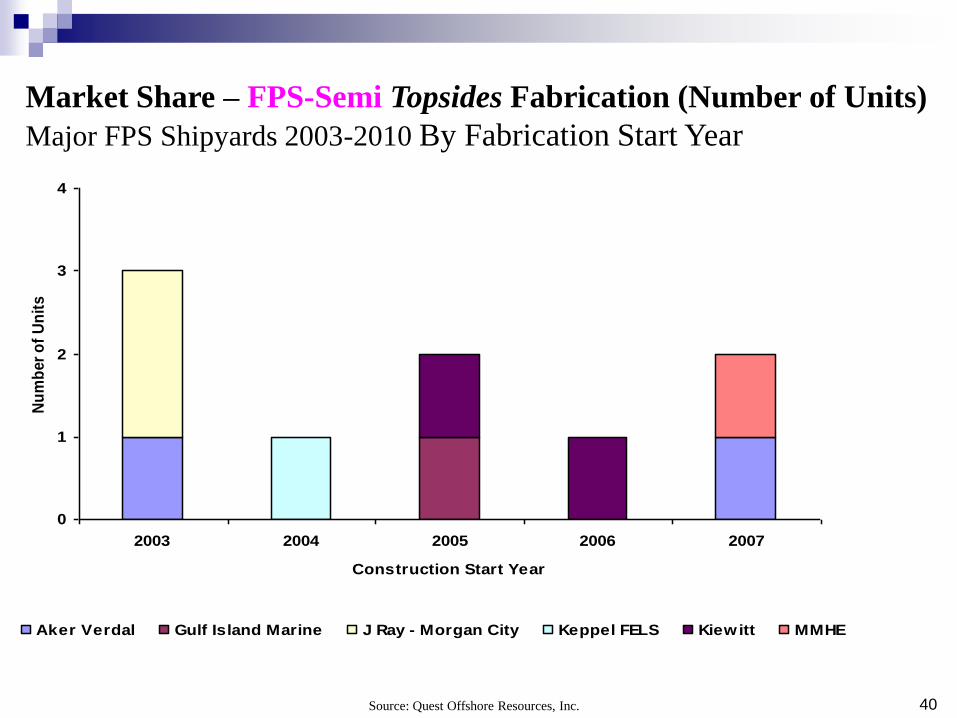

Market Share – FPS-Semi Topsides Fabrication (Number of Units)

Major FPS Shipyards 2003-2010 By Fabrication Start Year

Source: Quest Offshore Resources, Inc.

0

1

2

3

4

2003 2004 2005 2006 2007

Construction Start Year

Nu

mb

er

of

Un

its

Aker Verdal Gulf Island Marine J Ray - Morgan City Keppel FELS Kiewitt MMHE

41

Conclusions

42

Conclusions

MOPS market continues to expand

Leased FPSOs are approximately 1/2 of the FPSO market

FPSOs are by far the most common type of MOPS

A number of FPSO units are available today

Floating Production Systems are the only option for surface facilities in

water depths greater than 1,750 ft

43

Questions?

44

Selecting a MOPS Unit Type: Principal Determining

Criteria

Surface or Subsea Completions

Need for Well Access and Intervention

Drilling Program Requirements

Access to Existing Hydrocarbon Export Infrastructure

Water Depth and Environmental Regime

Size and weight of process equipment

45

Principal Operational Sensitivities

Oil Export Method / Storage and

Offloading Systems

Environmental Parameters and the

Mooring System

Permanent moorings

Disconnectable options

Weathervaning (single-point) vs.

spread moorings

Process System Sensitivities

46

Operational Considerations

System Availability / Uptime

Is redundancy required?

What cost for the final %?

Achieving Safety and

Environmental Protection

Objectives

Recruiting and Retaining

Competent Crew

Maintenance Criteria