Mobile financial services to emerging markets - eServGlobal · PDF fileMobile money solutions...

20

Mobile financial services to emerging markets H1 Results June 2015

Transcript of Mobile financial services to emerging markets - eServGlobal · PDF fileMobile money solutions...

Mobile financial services to emerging markets

H1 Results June 2015

2

Contents

1. Core Mobile Money business

2. Our Market

3. First half progress

4. Our Technology Advantage

5. The HomeSend Joint Venture

6. Second half 2015

3

Huge population of

working migrants need to

send money home

2 billion unbanked

working age adults want

financial services

Two different, but related markets, with enormous potential

Core Business:

Domestic mobile money, mobile

financial services

Established end-to-end technology. Distinct but complementary solutions.

International money transfer hub. JV with MasterCard & BICS

4

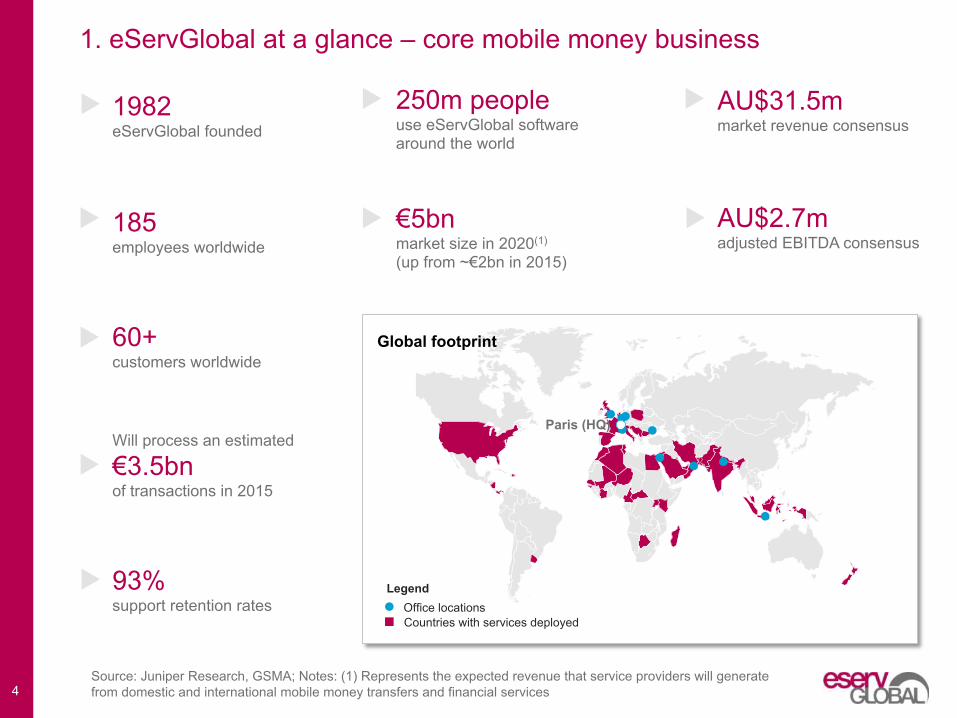

1. eServGlobal at a glance – core mobile money business

1982

eServGlobal founded

185 employees worldwide

60+ customers worldwide

250m people use eServGlobal software around the world

€5bn market size in 2020(1) (up from ~€2bn in 2015)

Will process an estimated

€3.5bn of transactions in 2015

AU$31.5m market revenue consensus

AU$2.7m adjusted EBITDA consensus

93% support retention rates

Source: Juniper Research, GSMA; Notes: (1) Represents the expected revenue that service providers will generate from domestic and international mobile money transfers and financial services

Paris (HQ)

Office locations Countries with services deployed

Legend

Global footprint

5

1. eServGlobal – where we are today

1. Reiterated on track for full year performance

2. Our new PayMobile 3.0 technology is complete and

gaining traction

3. Continued traction from HomeSend

4. Cost reductions in progress

5. Healthy market growth dynamics

6. Three new customers in 1H15

2 billion unbanked adults in emerging

markets

2. Our Market Mobile money is poised for significant growth.

5 billion mobile connections in the developing world

US$436bn estimated sent by migrants from developed to emerging

countries in 2014

Revenue from mobile money services will

grow to 5.8bn by 2020

Expected increase of 3 billion smartphones to

2020, driven by emerging markets

7

3. First half progress – Core business

} 1H15 revenue of AUD12.8M (GBP6.7M) } Recurring support & SaaS revenue of 37%

(decrease of 8% as migrate legacy VAS support contracts)

} Project backlog at the end of April totaled AUD7.1M (GBP8.7M), a 59% increase on the same period last year.

} Sales orders received in 1H15 of AUD16.5M (GBP8.7M), an increase of AUD4.6M (39%) compared to 2H14.

} The company has made rapid progress on cost-optimisation with annualised savings of over AUD1.2M (GBP0.6) actioned so far out of the full AUD2.9M (GBP1.5M) expected.

} New contracts including } Mobile money platform in Pakistan } Mobile money platform in Myanmar } Electronic top-up in UAE

} Launch of smartphone app to cater to increasing penetration of low-cost smartphones.

6 9 11 13

68 69 69 61

2012A 2013A 2014A H1 2015F

Mobile money Recharge / top-up VAS

Our customers 1H15 Highlights

The number of high value mobile money customers has more than doubled since 2012, and continues to grow at a healthy rate. Though customer numbers have declined in aggregate, these losses have generally originated from low value VAS revenues

Total customer numbers in the core business

8

4. Our technology advantage

PayMobile 3.0 is a revolution in the way eServGlobal builds and delivers its solutions. In 2014 we embarked on an ambitious project to develop a standardised technology platform to meet the needs of the rapidly evolving mobile money and advanced-recharge market.

PayMobile 3.0 is now live in Zain Saudi Arabia, Zain Jordan and Alfa Telecom Lebanon.

Objectives Outcome

Create a true, industrialised product One core-product for many customers, allow for vertical growth (indirect channels)

Create standardised platform tools Ability to use lower cost, more flexible third-party resources

Rapid deployment Customers reach project milestones faster

Reduce connection time (inbound & outbound)

Standardised connectors now reduce integration cost by two-thirds

Joint Venture of MasterCard, eServGlobal and BICS

10

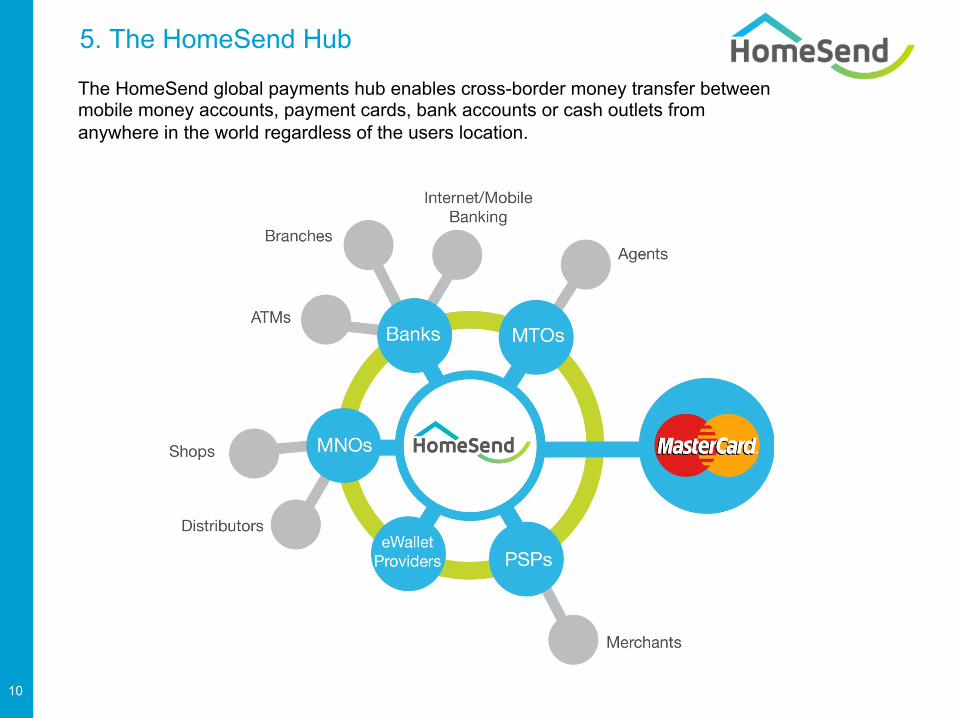

5. The HomeSend Hub

The HomeSend global payments hub enables cross-border money transfer between mobile money accounts, payment cards, bank accounts or cash outlets from anywhere in the world regardless of the users location.

11

5. HomeSend – Key performance metrics

4 17 51

486 659

1578

2011 2012 2013 2014 March 2015

June 2015

Strong growth in achieving strategy to focus on connection of live corridors. 240% increase in live corridors in 3 months. 388% YOY increase in the number of transactions compared to May 2014.

Live remittance corridors

HomeSend’s customers include several of the Top 10 MTOs (Money Transfer Organisations) worldwide. These consumer-facing services connect to HomeSend, which is a white label solution operating in the background, to reach the worldwide community of users looking for safe, cost-effective money transfer.

Connecting the top players

12

5. HomeSend highlights 1H15

} The support of MasterCard has opened new opportunities for HomeSend. HomeSend will facilitate the international remittance capabilities for MasterCard Send, an end-to-end digital platform that will leverage the industry-leading MasterCard network, paired with key capabilities from other personal payments platforms including HomeSend.

} HomeSend was recognised at the Awards for the Global Forum on Remittances and Development in Milan in June. This forum is facilitated by the IFAD (International Fund for Agricultural Development), which is an agency of the United Nations. During H1, HomeSend was also awarded Best Payment Product in Africa at the Asian Banker Middle East and Africa Awards.

} MasterCard has engaged their sales teams, already delivering results: Steward Bank in Zimabawe and eTranzact in Nigeria.

Click image to play full speech or go to: http://goo.gl/8cvQ69 To go directly to the section concerning the HomeSend JV, skip to 8mins.

} MasterCard continue to promote and discuss HomeSend as part of their emerging market strategy, including a demonstration on their booth at Mobile World Congress, Barcelona & featured in the keynote address of MasterCard CEO, Ajay Banga.

13

5. Seizing the remittance opportunity

} HomeSend is a first-mover in a substantial market. Established technology that meets an existing need.

} The HomeSend management has presented a strategy to accelerate growth to capitalise on current demand. The strategy includes:

} Co-funded marketing initiatives to stimulate subscriber demand

} Requirement for a new data centre which is PCI-DSS compliant as a pre-requisite to connect to the MasterCard network

} Acquisition of a payment institution license

} Requirement for extra capital from JV partners

} If approved maximum is €10.0M (€3.5M ESV contribution). Timing is late 2015.

333 373 392 404 436 473* 516*

2010 2011 2012 2013 2014 2015 2016

Remittances sent by migrants to developing countries US$436 billion sent in 2014 through official channels. Estimated that unofficial remittance could represent up to a further 50%

In $US Billions *forecast Source: The World Bank

14

6. Second half 2015

1. Execution

} Achieve the market consensus numbers

} Complete the delivery of cost savings

} Work more closely with HomeSend

2. Evaluation

} How to deliver sustainably higher margins

} Evaluate additional business models

} Geographic diversification

} Review Board composition

APPENDIX

16

The market is growing

Source: GSMA MMA, State of the Industry Report 2014

Continued investment in mobile money by service providers Mobile money providers are continuing to invest in improving and expanding their mobile money services, showing important commitment to the long-horizon investment required. Over 80% of service providers indicated that they had maintained or increased investment in 2014.

Growth in number of mobile money deployments 255 services now live across 89 countries. Competition is heating up between services as many markets now have 2 or more services operating. Regulators are recognising the role of mobile money to promote financial inclusion and passing reform to support the services.

17

Moving to advanced mobile financial solutions

} Mobile money solutions are generally deployed in a ‘phased’ approach with essential services launched in the initial phase building to more advanced services as the market matures.

} A mobile wallet is a ‘gateway’ to adoption of further services.

PHASE 1 PHASE 2 PHASE 3

Introductory services Growing familiarity Advanced mobile financial

services

18

Smartphones in emerging markets

eServGlobal has launched a smartphone app for mobile money services in emerging markets. The white-label app will be part of eServGlobal’s end-to-end mobile money solution, supporting deployments worldwide.

The app has already been sold to five existing eServGlobal customers including projects in Cabo Verde, Armenia, and Somalia. Service providers can easily configure the app to suit the needs and brand of their deployment. The app will be available for end users through an app store and is available for both Android and iOS devices, serving more than 95% of the market.

3.3 3.9

4.5 5.0

5.5 5.9

2015 2016 2017 2018 2019 2020 Connections

Forecasted smartphone connections & adoption rates globally (billions)

44% 50% 55% 59% 65% 62%

% Adoptioan rate (as % of population)

19

Typical customer lifecyle

eServGlobal currently has more than 60 customers worldwide with subscriber licenses covering in excess of 110M end users. The total subscriber footprint of all eServGlobal customers is significantly higher, demonstrating potential for high-margin license extensions. Currently, subscriber licenses are being used at 94% of license threshold.

RE

VE

NU

E

RE

CO

GN

ISE

D

ES

ER

VG

LOB

AL

MIL

ES

TON

E Project start phase Project live

Customer’s subscriber numbers double, exceeding

their license

Customer chooses eServGlobal for project

After X years of operation, the

platform needs to be upgraded

As the market matures, customer wants to add new features eg. Micro

Finance CU

STO

ME

R

EV

EN

TS

P P P PP PPPP

P

Solution live and eServGlobal provides

support as per contract

20

PayMobile 3.0 Technology

Retailers interacting via… Mobile network operators

Subscribers interacting via…

Other institutions

PayMobile 3.0

Transactions Software offered

Retailers network mgmt.

Promotions

Account management

Transaction processing

Reporting

Security

Administration

$ Electronic recharge / top-up

$ Voucher recharge / top-up

$ Mobile money

Billing Mobile

Web POS

Mobile

ATM Web

Intelligent network (IN)

Postpaid account

Prepaid account

Bill payments

Oracle stack ensures platform scalability

Modular approach ensures configurability and cross-sell

SOA(1) architecture ensures flexibility and reliability

SOA End-to-end platform ensures customer continuity

Banks

Salary disbursements

Government payments

Peer-to-peer transfers

Balance enquiry

Withdrawals / deposits

Highly scalable, easily deployable solution following investing in new platform