Mobile Access Markets throughout Europe Facts and Regulatory Aspects – Conclusions for the Polish...

18

Mobile Access Markets throughout Europe Facts and Regulatory Aspects – Conclusions for the Polish Market Dr. Joachim Haas, MLE Vice President Regulatory Affairs T-Mobile International AG & Co. KG Warszawa, 10 March 2006

-

Upload

coleen-powers -

Category

Documents

-

view

213 -

download

0

Transcript of Mobile Access Markets throughout Europe Facts and Regulatory Aspects – Conclusions for the Polish...

Mobile Access Markets throughout EuropeFacts and Regulatory Aspects – Conclusions for the Polish Market

Dr. Joachim Haas, MLEVice President Regulatory AffairsT-Mobile International AG & Co. KG

Warszawa, 10 March 2006

2

Summary The Polish mobile market – Customer is King

Mobile penetration – very strong growth since 2003, but still potential for further growth

Fierce price competition lead to very low prices for mobile services

Mobile operators face a challenging investment situation

Access Regulation is a rare exception in the EU Market 15 is effectively competitive in nearly all EU Member

States Price competition on the retail market is key indicator for

effective competition on the wholesale market EU benchmark for access regulation: Is Poland comparable?

Conclusion – Stick to competition instead of regulatory intervention

Competition warrants the best outcome on the Polish mobile market

Access agreements should create win-win situations and stick to commercial negotiations

Doing it wrong can hinder necessary investment and stop a very promising market development

3

The Polish Mobile Market –

Customer is King

4

Mobile penetration is rapidly increasing in Poland

Mobile penetration

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Market penetration (current forecast)

Market penetration (Strategia regulacyjna rządu2006 - 2007, CAS)

Market penetration (Strategia regulacyjna rządu2006 - 2007, URTIP)

Source: Era PTC, 2005

Poland has one of the fastest growing mobile markets in the whole European Union

With an increase of around 30% since 2004 Poland could already catch up with its CEE peers and close the gap

More growth ahead due to very attractive products and prices

5

Ongoing price reductions are an indicator of vital competition on the Polish market

Consumers in Poland benefited from the biggest price decreases in Europe in 2005 Prices for mobile services in Poland are now among the lowest in Europe EU-Commission recognizes fierce price competition in Poland

Source: EU-COM, European Electronic Communications Regulations and Markets 2005 (11th report, Feb. 2006)

6

0,50 zł

1,00 zł

1,50 zł

2,00 zł

2,50 zł

3,00 zł

3,50 zł

Q2'01

Q4'01

Q2'02

Q4'02

Q2'03

Q4'03

Q1'04

Q2'04

Q3'04

Q4'04

Q1'05

Q2'05

Q3'05

Q4'05

ERA IDEA PLUS Heyah

Price erosion from 2001-2005 for prepaid services shows operators competing for the lowest price on the market

POP MAX

Zrób to Sam

Fajnie!

Cały Dzień

Era Love

Happy

Jedna IdeaMono

Heyah

Heyah – nowe objawy

Simplus Team

Simplus Team 7

Happy Taniej

Orange GO

Heyah „zdrabniamy”

Basis:Offerts without price reductionsThe lowest tariffs for offnet calls are presented. Gross prices (Source: Era PTC, 2005)

7

Consumers in Poland already get a very good deal for their money spent in comparison to their peer countries

MoU/ARPU

0,00

1,00

2,00

3,00

4,00

5,00

6,00

Hu

ng

ary

De

nm

ark

Fra

nce

Po

lan

d

Po

rtug

al

Cze

ch

Italy

Gre

ece

UK

Irela

nd

Sp

ain

Ne

the

rlan

ds

Be

lgiu

m

Au

stria

Source: Merrill Lynch, Global Wireless Matrix 3Q05, 22.12.05, p. 2

Ratio of minutes of use (MoU) to the average revenues spent per user (ARPU) enables to compare different countries

Polish users enjoy very low prices for their minutes used (with 76 MoU the Polish ARPU is 18 U$; e.g. Czech Republic 85 MoU, ARPU 21 U$; Italy 125 MoU, 33 U$; Spain 155 MoU, 44 U$)

8

The highly competitive mobile market environment poses huge challenges on mobile operators

Source: Merrill Lynch, Global Wireless Matrix 3Q05, 22.12.05, p. 2

Average Revenue per minute

0,000,050,100,150,200,250,300,35

Hu

ng

ary

De

nm

ark

Fra

nce

Po

lan

d

Po

rtug

al

Cze

ch

Italy

Gre

ece

UK

Irela

nd

Sp

ain

Ne

the

rlan

ds

Be

lgiu

m

Au

stria Operators face low margins in a highly competitive Polish market Revenue per minute is one of the lowest in CEE and Western Europe

9

Access Regulation is a Rare Exception in the EU

10

Market 15 is effectively competitive in nearly all EU Member States

No remedies SMP¹ Remedies

Austria X

Cyprus X (single dominance)

Denmark X²

Finland X (X – veto EU COM)

France ? (X – withdrawn by NRA)

Hungary X

Ireland X (X – joint dominance; resolved by agreement)

Italy X

Luxembourg ? (X – withdrawn by NRA)

Netherlands X²

Slovakia ? (X – withdrawn by NRA)

Slovenia X (single dominance)

Spain X (joint dominance)

Sweden X

UK X²

¹ significant market power ² remedies withdrawn after market analysis

11

EU- benchmark: regulation of market 15 is a rare exception

Spain NRA assessment: Joint dominance for three operators; no SPs; price

competition impeded; Far lower MoU/ARPU ratio Situation not comparable with Poland

Slovenia NRA assessment: Single dominance (one operator 75 % market share, only two

operators) Large difference between market shares of operators Not comparable with

Poland where all operators compete for market leadership Cyprus

NRA assessment: Single dominance (one operator with high market share; only two operators)

Large difference between market shares of operators Not comparable with Poland where all operators compete for market leadership

Only in Spain, Slovenia and Cyprus NRAs found single or joint dominance. However, situations are not comparable with Poland

12

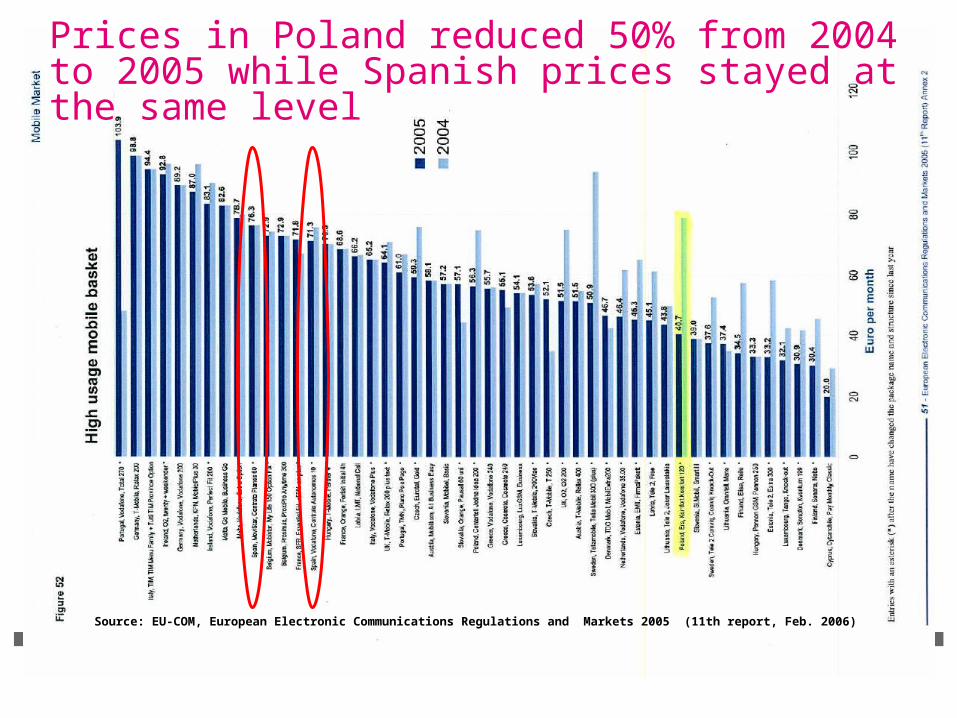

Prices in Poland reduced 50% from 2004 to 2005 while Spanish prices stayed at the same level

Source: EU-COM, European Electronic Communications Regulations and Markets 2005 (11th report, Feb. 2006)

13

Prices in Poland reduced 50% from 2004 to 2005 while Spanish prices stayed at the same level

Source: EU-COM, European Electronic Communications Regulations and Markets 2005 (11th report, Feb. 2006)

14

Need for regulation on market 15 hard to proveSeveral NRAs decided to or were forced to withdraw their decision to regulate the access market

Finland: FICORA found single dominance of mobile operator with more than 60% market share EU-COM vetoed the decision for failure to take market dynamics into consideration FICORA had not referred to economic incentives to provide access to SPs and improve

capacity utilisation ratios No regulation of market 15 in Finland

Ireland: ComReg applied EU-COM “Airtours” criteria and found joint dominance; EU-COM did not

veto However, despite a long and indepth analysis by ComReg the subsequent appeal of

operators has been resolved by agreement: ComReg stepped back and agreed not to defend the case! No regulation of market 15 in

Ireland

France, Slovakia, Luxembourg: ARCEP notified MVNO obligations to the EU-COM EU-COM challenged ARCEP`s assessment. ARCEP decided to withdraw before receiving a veto from EU-COM Comparable situations in Slovakia and Luxembourg

Spain – the latest ambiguous decision to regulate the access market: Although GD Info and GD Comp could not agree to veto the NRA decision on EU-level,

the EU-COM’s press release revealed serious doubts on the NRA’s decision

15

Price competition on retail market is key indicator of effective competition on the wholesale market

Two factors decisive in assessing whether a market is effectively competitive:

Price competition or Presence of SPs/MVNOs now or in the foreseeable future

Hungary and Italy as benchmarks NRAs - confirmed by the EU-Commission - refrained from access regulation due

to price competition on the retail market irrespective of any existing SP/MVNO landscape

Conclusions for the Polish market Poland already has a fierce price competition and prices are among the lowest in

Europe 4th Operator Netia auctioned UMTS licence in summer 2005 and is about to enter

the market with further competition potential

16

Conclusion

17

Conclusion - Competition Warrants the Best Outcome on the Polish Mobile Market

A decision to regulate market 15 in Poland would be legally flawed because the market is effectively competitive

Prices are constantly falling due to intensive competition on retail markets

Impressive record of market penetration growth MoU/ARPU ratio better than peers

Concerns coming along with regulatory intervention in the Polish market:

Regulation will stifle the positive development on the Polish mobile market

Risk of doing it wrong: Necessary incentives for investment in expanding innovative networks such as 3G are at stake

No incentive for voluntary wholesale agreements because of risk of annulment after regulatory intervention

Thank you for your attention

Dr. Joachim Haas, MLE T-Mobile International AG & Co. KG Vice President Regulatory Affairs [email protected]