MNC Related Doc

82

Accounting for the Growth of MNC-based T rade using a Structural Model of U.S. MNCs † Susan E. Feinberg Robert H. Smith School of Business University of Maryland 3423 Van Munching Hall College Park, MD 20742-1815 (301) 405-2251 [email protected] Michael P. Keane Department of Economics Yale University 37 Hillhouse Avenue Room 29 New Haven, CT 06520-8264 (203) 432-3548 [email protected] January, 2003 † The statistical analysis of the confidential firm-level data on U.S. multinational corporations reported in this study was conducted at the International Investment Division, Bureau of Economic Analysis, U.S. Department of Commerce, under arrangemen ts that maintained l egal confidentiality requirements. The views expressed are those o f the authors and do not necessarily reflect those of the Department of Commerce. Suggestions and assistance from William Zeile, Raymond Mataloni and Lorraine Eden are gratefully acknowledged. Comments by Keith Head, Kala Krishna, Jim Tybout, Sam Kortum, Bernie Yeung and other participants in the NBER Universities Research Conference on Firm Level Responses to Trade Policy are greatly appreciated. We have also received helpful comments from seminar participants at Yale, ASU and the U.S. International Trade Commission, especially Penny Goldberg and T.N. Srinivasan, along with Russ Hilberry, Jason Cummins and Richard Rogerso n.

-

Upload

owaiskhanm -

Category

Documents

-

view

219 -

download

0

Transcript of MNC Related Doc

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 1/82

Accounting for the Growth of MNC-based Trade

using a Structural Model of U.S. MNCs†

Susan E. FeinbergRobert H. Smith School of Business

University of Maryland

3423 Van Munching HallCollege Park, MD 20742-1815(301) 405-2251

Michael P. KeaneDepartment of Economics

Yale University37 Hillhouse Avenue Room 29 New Haven, CT 06520-8264

(203) [email protected]

January, 2003

† The statistical analysis of the confidential firm-level data on U.S. multinational corporations reported in this studywas conducted at the International Investment Division, Bureau of Economic Analysis, U.S. Department of Commerce, under arrangements that maintained legal confidentiality requirements. The views expressed are those of the authors and do not necessarily reflect those of the Department of Commerce. Suggestions and assistance fromWilliam Zeile, Raymond Mataloni and Lorraine Eden are gratefully acknowledged. Comments by Keith Head, KalaKrishna, Jim Tybout, Sam Kortum, Bernie Yeung and other participants in the NBER Universities ResearchConference on Firm Level Responses to Trade Policy are greatly appreciated. We have also received helpfulcomments from seminar participants at Yale, ASU and the U.S. International Trade Commission, especially PennyGoldberg and T.N. Srinivasan, along with Russ Hilberry, Jason Cummins and Richard Rogerson.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 2/82

Abstract

U.S. foreign trade has grown much more rapidly than GDP in recent decades. But there isno consensus as to why. More than half of U.S. foreign trade consists of arms-length and intra-firm trade activity by multinational corporations (MNCs). Thus, in order to better understand the

growth of trade, it is important to understand the reasons for the rapid growth in MNC-basedtrade.This paper uses confidential BEA data on the activities of U.S. MNCs to shed light on

this issue. Specifically, we estimate a simple structural model of the production and tradedecisions of U.S. MNCs with affiliates in Canada, the largest trading partner of the U.S., usingdata from 1983-96. We then use the model as a framework to decompose the growth in intra-firm and arms-length trade flows into components due to tariff reductions, changes intechnology, changes in wages, and other factors.

We find that tariff reductions can account for a substantial part of the increase in arms-length MNC-based trade. But our model attributes most of the growth of intra-firm trade totechnical change, with tariff reductions playing only a secondary role. Simple descriptive

statistics provide face validity for this result, since arms-length trade grew much more rapidly inindustries with the largest tariff reductions, while intra-firm trade grew rapidly even in industrieswhere tariffs were negligible to begin with.

Our work makes a number of other contributions: Our descriptive analysis of the BEAfirm level data, which has rarely been made available for research, suggests that few MNCs fitinto the neat vertical vs. horizontal dichotomy of the theoretical literature. Also, we find thatMNC decisions to engage in intra-firm and arms-length trade are unrelated to tariff levels. Thegrowth in MNC-based trade due to tariff reductions has been almost entirely on the intensivemargin, among the subset of firms already engaged in such activities.

Finally, the estimation of our model requires the development of a number of neweconometric procedures. We present new recursive importance sampling algorithms that are thecontinuous and discrete/continuous analogues of the GHK method.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 3/82

1

I. Introduction

In recent decades, trade has grown much more rapidly than GDP. Indeed, between 1982

and 1994, the growth of U.S. foreign trade (exports plus imports) averaged more than 5% per

year in real terms, while real GDP grew only 3% per year. Although the rapid growth of trade

has been widely documented, there is no consensus on its source (see Bergoeing and Kehoe

(2001) and Yi (2000) for recent discussions of this issue).

In order to understand the sources of growth of trade, it is important to understand the

behavior of multinational corporations (MNCs). According to Rugman (1988), over half of

world trade involves MNCs. Such MNC-based trade includes two components: arms-length

trade, which are shipments between a division of an MNC and unaffiliated buyers/suppliers in

other countries, and intra-firm trade, which are internal shipments between an MNC parent and

its foreign affiliates. Between 1982 and 1994, the total trade of U.S. based MNCs grew an

average of 4.5% per year. And the intra-firm component grew more rapidly than the arms-length

component.1 Indeed, between 1982 and 1994, intra-firm trade increased from 35.5% to 45% of

the total trade of US-based MNCs. What explains the rapid growth in MNC-based trade in

general, and the even faster growth of intra-firm trade between divisions of MNCs in particular?

In this paper, we analyze the sources of the growth in trade activity by U.S. MNCs with

affiliates in Canada, the largest trading partner of the U.S.. We estimate a structural model of the

MNCs’ production and trade decisions, using a confidential disaggregated panel data set from

the Bureau of Economic Analysis on more than 500 U.S. MNCs and their Canadian affiliates

from 1983-1996. We then use the model as a framework to decompose changes in intra-firm and

arms-length trade flows into components due to changes in tariffs, changes in technology,

changes in wages, and other factors (i.e., changes in prices, exchange rates, etc.).

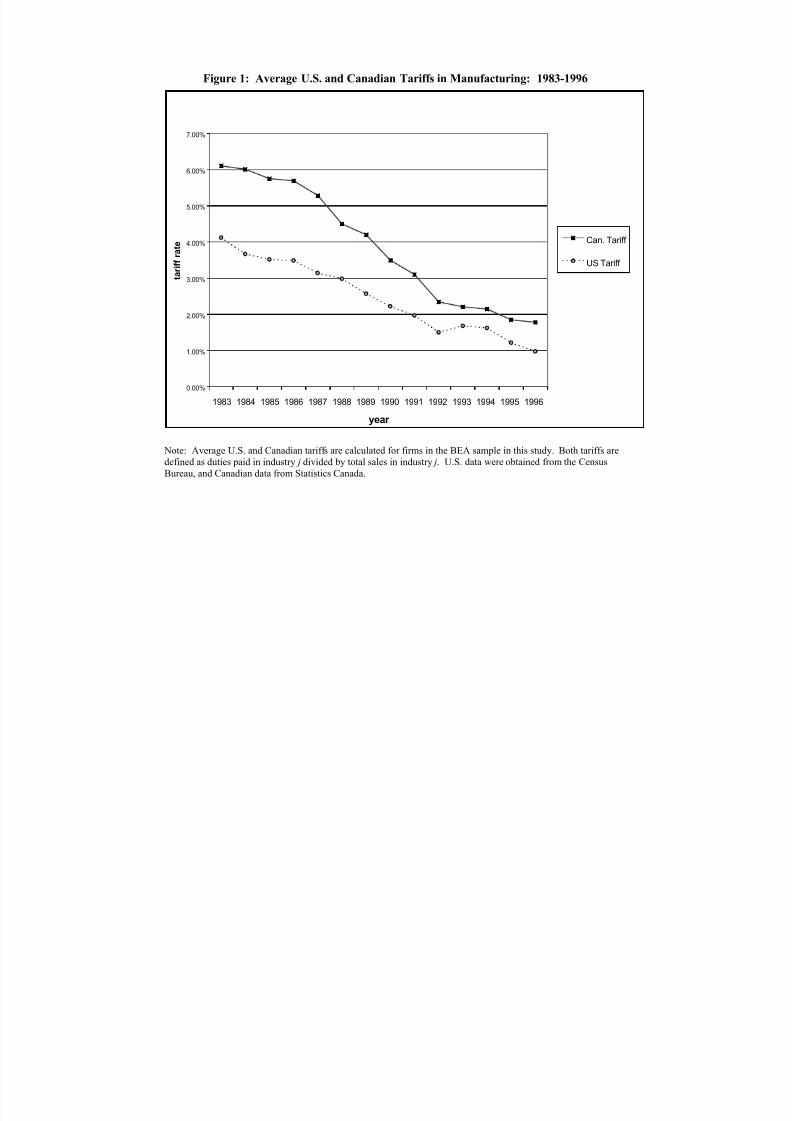

There were significant bilateral tariff reductions between the U.S. and Canada during our

sample period, arising both from the GATT/WTO and the Canada-U.S. Free Trade Agreement

(FTA) in 1989, as is shown in Figure 1. This figure makes clear that tariff reductions were

gradual, and not concentrated in the immediate aftermath of the FTA. As we will see, there was

also substantial variation across industries in the extent of tariff reductions. Thus, the U.S.-

Canada context provides an excellent opportunity to examine the contribution of trade

liberalization to the observed increases in MNC based trade.2

1 For US MNCs, these trade flows grew an average of 3.4% and 6.3% per year, respectively. We do not include inthese statistics trade to and from U.S. affiliates of foreign MNCs. All our aggregate statistics on the growth of tradeare derived from figures presented in Zeile (1997).2 As Trefler (2001) points out, most trade liberalizations are accompanied by packages of economic reforms, makingthe pure effect of tariffs difficult to isolate. A notable example is NAFTA, which included removal of constraints on

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 4/82

2

One significant contribution of our work is simply to use the confidential firm level BEA

data to provide a description of the production and trade arrangements of U.S. MNCs and their

foreign affiliates. Many aspects of MNC organization that we observe in the data are rather

surprising from the perspective of the extant theories of the MNC. As a consequence, there is no

“off-the-shelf” model of MNC behavior that we can estimate structurally on the BEA data. The

main problem is that existing theories of the MNC cannot explain the multiplicity of MNC

production arrangements we see in the data.

Markusen and Maskus (1999a, b) provide an excellent discussion of the existing theories

of the MNC. As they note, these theories can be divided into those that generate vertical vs.

horizontal MNCs. Classic examples of these two types of models are Helpman (1984) and

Markusen (1984), respectively. Vertical MNCs fragment the production process across countries

to take advantage of factor price differentials, e.g., by locating unskilled-labor intensive parts of

the process in low wage countries. Horizontal MNCs basically replicate the entire production

process in multiple countries, thus avoiding tariff and transport costs.

The MNC forms we observe in the BEA data do not, for the most part, fall into the neat

vertical/horizontal taxonomy that exists in the theories. Models of horizontal MNCs rule out

substantial intra-firm flows of intermediates essentially by definition.3 But inspection of the

BEA firm level data on US. MNC parents and their Canadian affiliates suggests that vertical

specialization – the fragmentation of production processes into parts that are performed in

different countries - is indeed pervasive. We find that the value of intermediates shipped from

U.S. parents to their Canadian affiliates is, on average, more than one-third of affiliate total sales.

And the value of intermediates shipped by affiliates to parents is, on average, 39% of affiliate

total sales. Only about 12% of the firms in the BEA data are pure “horizontal” MNCs, in the

sense of having negligible intra-firm flows of intermediates.

But standard vertical MNC models do not describe the data either. The classic models of

Helpman (1984, 1985) and Helpman and Krugman (1985) do generate intra-firm trade in

intermediates, but it goes in only one direction. For instance, in Helpman and Krugman, MNCs

foreign direct investment (FDI) in Mexico. To a great extent, the U.S.-Canada FTA did not combine tariff reductionswith other major policy changes, making it, according to Trefler, an “unusually clean trade policy exercise.”3 Obviously, simple horizontal models also fail to generate arms-length sales of final goods (either by the parent tothe host country or by the affiliate back to the home country), since FDI is used to avoid such trade in these models.But Brander (1981) showed how horizontal models can be modified to generate bilateral arms length trade in similar goods by assuming the final goods produced by the parent and affiliate are differentiated. Recently, Baldwin andOttaviano (1998) have extended Brander’s model to also generate intra-industry FDI. We note that Rugman (1985)has quantified the importance of bilateral intra-industry trade and FDI at the aggregate industry/country level.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 5/82

3

produce a differentiated product in three stages that require descending levels of capital intensity:

headquarters services, production of intermediates and production of final goods. Suppose the

factor prices are such that headquarters services and intermediate goods production are located in

the home country and final assembly is done by the foreign affiliate. This leads to a one-way

flow of intermediates from parent to affiliate.4 But a striking aspect of the BEA data is the

number of cases in which intra-firm flows actually go in both directions - 69% of observations.5

Furthermore, this prevalence of bilateral intra-firm flows of intermediates is not a special

feature of U.S.-Canada trade. While the MNC affiliates in U.S.-Canada sample tend to be more

vertically specialized than affiliates in the entire BEA population (all countries), we find broadly

similar patterns worldwide. For example, among all foreign manufacturing affiliates, nearly 34%

have some two-way trade with their U.S. parents.

Helpman and Krugman noted that the failure to generate bilateral intra-firm flows of

intermediates was a problem for their model. However, they also noted that in aggregate data,

intermediates and final goods often share the same industry code, so their model would appear to

generate two-way intra-industry trade. At the firm level, however, this does not resolve the

problem. If we define vertical MNCs only as those that exhibit a one-way flow in intermediates,

only 19% of the firms in the BEA data are purely vertical. To our knowledge, prior empirical

work has not documented the great extent of intra-firm flows in intermediates, and the fact that

less than a third of U.S. MNCs fall into the neat vertical vs. horizontal dichotomy.

An obvious way to generate bilateral intra-firm trade in intermediates in a vertical model

is to fragment the production process into additional stages. Dixit and Grossman (1982) and

Deardorff (1998) discuss this possibility. Absent a strictly descending or ascending ordering of

stages by factor intensity, this creates the possibility for bilateral flows of intermediates.

But it is not possible to estimate a multi-stage MNC production process with available (or

even prospectively available) data. The BEA data only contain the total values of the intra-firm

flows of intermediates, and do not break these down by stage of processing. Regarding other

inputs, the BEA data only contain total employment of the parent and the affiliate, and we have

no way to determine how much labor input was used in each stage of the production process.

Thus, estimation of a multi-stage process appears to be hopeless. Furthermore, the BEA data is

4 Note that, in this example, all final goods are produced by the affiliate, which it sells in both the host and homecountries. In the BEA data on U.S. MNCs and Canadian affiliates, it always the case that both the parent andaffiliate have final sales. As Helpman (1985) notes, vertical models can generate final sales by both parent andaffiliate if one adds a distribution/marketing stage that must be tied to the point of sale. Alternatively, one couldsimply assume that intermediates can be sold as final goods to third parties (which is what we assume in our model).5 It is also common for arms length flows to go in both directions - 39% of cases in the U.S.-Canada sample. Nearlyone third of the MNCs we examine have bilateral intra-firm flows and bilateral arms-length flows simultaneously.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 6/82

4

by far the best available data on MNCs, and better data is not likely to become available.

Thus, one of the key challenges we face is how to specify a model that generates bilateral

intra-firm trade, yet that is estimable given available data. We chose to do this in the most direct

possible way. We simply assume a production process in which the final good produced by the

parent may be required as an intermediate input in the affiliate’s production process, and,

simultaneously, the final good produced by the affiliate may be required as an intermediate input

in the parent’s production process. If both the parent and affiliate simultaneously require

intermediates produced by the other party, we have what might be called “parallel” or “circular”

(as opposed to “vertical”) specialization.6 If only one party needs the output of the other as an

intermediate, we obtain a traditional vertical model, and if neither party requires intermediates

produced by the other, we obtain a traditional horizontal model. Our model allows for firm

heterogeneity in terms of which of these three possible organizational structures is chosen.

Another key problem we confront is that, while the BEA data is in some ways very rich,

many basic quantities that one would like to use in estimating a structural model of MNC

behavior are not measured. One major data problem is that the BEA data do not allow one to

separate quantities of production from prices. Similarly, while one can observe values of intra-

firm flows, imports and exports – the prices and quantities for these trade flows cannot be

observed separately. Absent information on physical quantities of outputs or of intermediates

shipped intra-firm, it would be very difficult to estimate plant level returns to scale, or, for that

matter, any very flexible production technology. Griliches and Mairesse (1995) discuss the

fundamental problems in identifying returns to scale when output prices and quantities are not

observed separately and firms have market power (as is obviously the case with MNCs).

A second data problem arises because theories of the MNC stress multi-plant economies

of scale as the reason for multinational organization. These typically arise from “intangible” firm

level fixed inputs, such as a proprietary production process or a widely recognized brand name,

that serve as joint inputs for MNC operations in all countries. But the BEA data contain no

information on such intangible inputs. It is important to note however, that such firm level fixed

costs would not affect marginal production and trade decisions of the MNC (conditional on its

6 As an example of this type of circular process, consider the petroleum industry. Finished products from a petroleum refinery include fuel oil, lubricants and Naphtha. In turn, these products are also used as intermediates inoil drilling. Consider Mobil’s off shore drilling operation in the Hibernia field off Newfoundland. Since Mobil hadlittle refining capacity in Canada, the crude was primarily shipped to Mobile refineries in Texas and Louisiana.Lubricants and fuel oil were then shipped back to Hibernia as inputs to run the rig. Fuel oil requirements aresubstantial in off shore oil drilling, since all power must be generated at the rig. Similarly, Venezuelan crude oilfrom the Oronoco flow is unusually heavy. Naphtha produced at Mobil refineries in Louisiana is shipped toVenezuela and pumped into the crude oil flow to facilitate extraction.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 7/82

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 8/82

6

and trade aspects of MNC behavior.7 Soboleva (1998) models MNC decisions to locate foreign

production facilities across a portfolio of potential host countries, and also models production in

each location. But she does not examine intra-firm trade or bilateral arms-length trade.

Our main findings are as follows: First there is a clear bifurcation of MNCs into two

types: those that have intra-firm flows and those that do not. The increase in U.S.-Canada intra-

firm trade over our sample period occurred almost entirely on the intensive rather than the

extensive margin. It did not occur because more MNCs organized to trade intra-firm. A similar

pattern holds for arms-length flows. For this reason, our failure to structurally model the decision

to become an MNC, or to structurally model MNCs’ trade flow decisions on the extensive

margin, does not appear to be a significant limitation of our analysis.

Second, we find that tariff reductions explain a substantial fraction of the increase in

arms-length trade, but they can only explain a small portion of the increase in intra-firm trade.

Our estimates imply that technical change, in the form of changes in the Cobb-Douglas share

parameters, accounts for a large portion of the increase in intra-firm trade.

According to our estimates, the MNCs that were initially organized to trade intra-firm

experienced technical change that made it optimal to substantially increase intra-firm flows. In

contrast, if an MNC parent did not use intermediate inputs from the affiliate, our model is able to

explain its behavior using share parameters that are essentially fixed over time. Similarly, our

model also implies basically fixed share parameters for affiliates that did not use intermediate

inputs from the parent. These findings of stable shares are strong support for a Cobb-Douglas

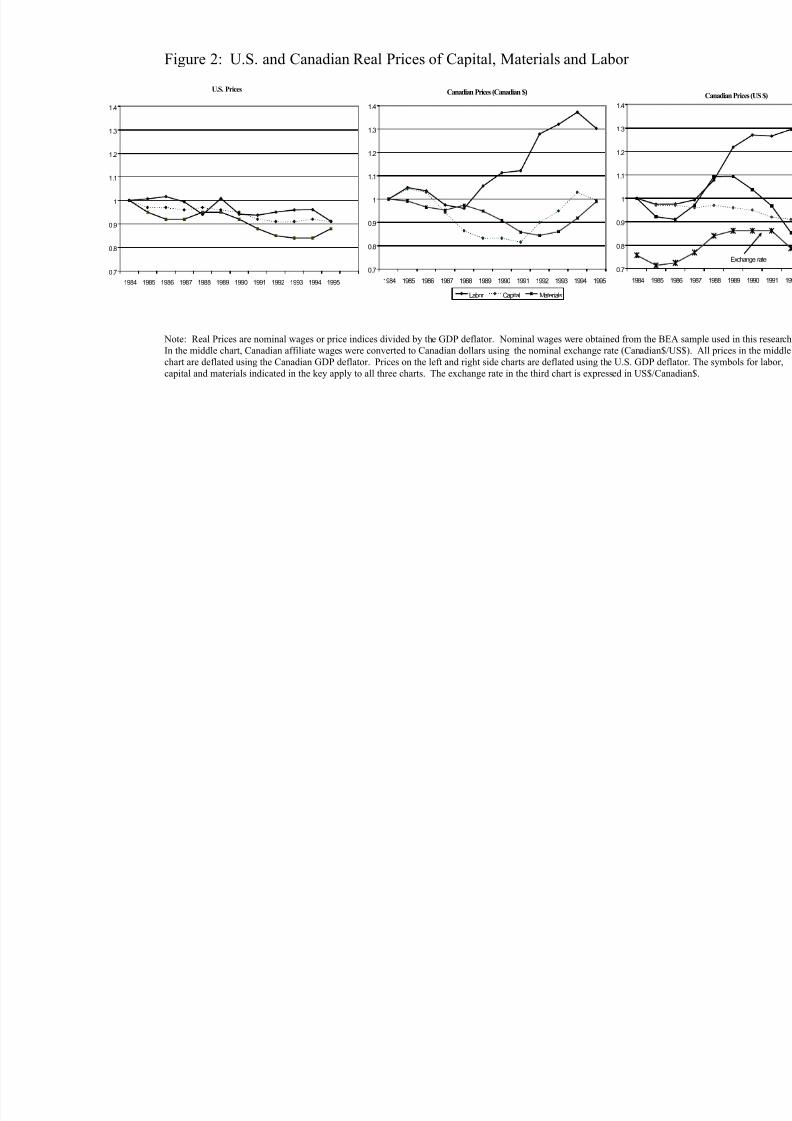

specification of technology, since as Figure 2 reveals, there were substantial changes in relative

prices of capital, labor and materials during our sample period.

An interesting question is whether our key finding - that tariff reductions can explain a

substantial increase in arms-length MNC based trade between the U.S. and Canada, but that

tariffs explain little of the growth of intra-firm trade – is an artifact of some special feature of our

model, or whether the data clearly “speaks” on this point. Figures 3 and 4, address this issue. The

left panel of Figure 3 plots the change in U.S. parent arms-length exports between 1989 (the year

of the FTA) and 1995, for four groups of firms. The firms are grouped into quartiles according to

the magnitude of the Canadian tariff reduction for their industry over the period. The figure

reveals a clear pattern whereby exports to Canada increased more in industries where Canadian

tariff reductions were greater. For industries where the Canadian tariff reductions were

7 Cummins (1995) models marginal investment decisions of U.S. parents with affiliates in Canada. He allows for capital adjustment costs that are interrelated across the parent and affiliate. Ihrig (2000) models MNC decisionsabout repatriation of profits, which we abstract from (i.e., we assume all profits are repatriated each year).

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 9/82

7

negligible, arms-length exports actually fell. In industries where tariff reductions were greatest

(4 percentage points at the median), the growth in arms-length exports was roughly 35%.

The right panel of Figure 3 reports a similar graph, except for U.S. parent intra-firm sales

to Canadian affiliates. Here, there is no clear relationship between the magnitude of the tariff

reduction and the increase in intra-firm flows. In fact, the largest increase in intra-firm trade

(roughly 140%!) occurred in the 3rd quartile industries, where Canadian tariffs reductions were

quite small. Many of these industries had very low tariffs to begin with.

Figure 4 tells a similar story for Canadian affiliate arms-length and intra-firm shipments

to the U.S.. The former are closely related to tariff changes, while the later are not. Even in the

3rd and 4th quartile industries where U.S. tariffs changed very little (and were small to begin

with), intra-firm shipments to parents grew roughly 100% and 30%, respectively. Given these

figures, it seems obvious that trade liberalization cannot explain much of the growth in intra-firm

trade. Instead, our model attributes most of this growth to technical change (i.e., an upward trend

in the Cobb-Douglas share parameters for intra-firm intermediates).8 In the conclusion we

discuss recent developments in logistics that may be inducing this technical change.

Aside from our substantive results, we also make four methodological contributions. Our

structural model is dynamic because we allow for labor force adjustment costs. Estimation using

a full solution method would require us to specify how firms form expectations of future labor

force size (which in turn depends on forecasts of future demand, technology, prices, tariffs,

exchange rates, etc.). To avoid these serious complications, we adopt the common approach of

working with the Euler conditions of the firm’s optimization problem. However, our model

contains multiple stochastic terms that enter the Euler equations non-linearly, preventing us from

obtaining moment conditions based on a single additive error. This precludes us from estimating

the model using non-linear GMM, so we instead use simulated maximum likelihood (SML).

The SML approach has no problem with multiple sources of error, but it introduces the

new problem that we must specify a distribution for forecast errors. Such an approach has

typically been avoided (in favor of GMM), because there is no clear basis for assuming a

distribution on forecast errors. However, Krussell, Ohanian, Rios-Rull and Violante (2000)

recently faced a similar problem (multiple stochastic terms) and dealt with it using an approach

somewhat similar to ours. They assumed normality for forecast errors, and implemented a

pseudo-SML procedure. We go beyond their econometric contribution in a number of ways.

Our first innovation is to show how to test the distributional assumption by simulating the

8 In a sense, our effort is analogous to the growth accounting literature (Solow, 1957). We obtain “technologicalchange” as a residual not accounted for by other factors, and we do not structurally model its ultimate source.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 10/82

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 11/82

9

(1993) finds little relation between factor endowments and patterns of FDI.

Brainard (1997) examines sales of U.S. affiliates abroad, and reaches conclusions similar

to Markusen and Maskus. Using the BEA industry level data for 1989, she notes that 64% of the

affiliates’ sales are in the host country (on average), while only 13% are back to the U.S.. She

argues that such a concentration of affiliate sales in the foreign market is consistent with

horizontal rather than vertical specialization.

On the other hand, Hanson, Mataloni and Slaughter (2001) challenge this view, arguing

that a closer look at the BEA data on U.S. affiliates abroad provides strong evidence that vertical

fragmentation is important and growing. For instance, manufacturing affiliate exports as a share

of total sales rose from 33.9% in 1992 to 44.4% in 1998. And, most obviously, more than a third

of the manufacturing affiliates are not in the same industry as the parent. Our work is related to

Hanson, Mataloni and Slaughter in that we provide an even more detailed analysis of the BEA

firm level data. But our analysis is focused exclusively on Canadian manufacturing affiliates.

Several studies have examined the impact of U.S.-Canada trade liberalization on

Canadian manufacturing. Gaston and Trefler (1997) and Trefler (2001) use industry level data to

identify the effects of tariff reductions. Their identification strategy exploits the fact that tariff

decreases differed substantially across industries. Trefler (2001) concludes that the FTA reduced

employment of production workers, increased earnings of production workers, reduced output,

and raised labor productivity. He concludes that the FTA did not affect either the number or

scale of Canadian manufacturing plants. Head and Ries (1997) show that theoretical predictions

regarding effects of tariffs on the number and scale of manufacturing plants are quite ambiguous.

Again relying on variation across industries in the extent of tariff reduction, they estimate that

the FTA had little effect on the scale of Canadian manufacturing plants.

It has often been argued that tariff jumping FDI led to inefficiently small Canadian

manufacturing plants – see Eastman and Stykolt (1967), Caves (1984, 1990), Baldwin and

Gorecki (1986). This led to concern that the FTA would “hollow out” Canadian industry, since

U.S. MNCs could most efficiently serve both markets from large U.S. plants. But our own

previous work using the BEA firm level data – Feinberg, Keane and Bognanno (1998) and

Feinberg and Keane (2001) – contradicts this view. In fact, we find that assets, employment and

value added of Canadian affiliates of U.S. MNCs actually increased following tariff reductions.

Our positive employment result may appear to contradict Gaston and Trefler, who find

(small) negative employment effects. But they examine all of Canadian manufacturing while our

results are only for affiliates of U.S. MNCs.. Since tariffs are a tax on internal flows within

MNCs, it would not be surprising if tariff reductions benefited MNCs relative to national firms.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 12/82

10

III. The Model

III.1. Overview

This subsection provides a non-mathematical overview of our model. At the outset, we

stress that we do not model an MNC’s decision to place an affiliate in Canada, which we take as

exogenous. In theoretical models of MNCs (both vertical and horizontal), a key reason for

existence of multinational operations is some firm level fixed cost that serves as a joint input (or

“public good”) for MNC operations in all countries, thus creating multi-plant economies of scale.

We simply assume there exists such a firm level fixed cost, and that it does not affect marginal

production decisions (so we can ignore it in setting up our model).9

The main assumptions of our model are as follows:

1) The parent and affiliate each produce a different good.

2) The good produced by the affiliate may serve a dual purpose: it can be sold as a final

good to third parties (in Canada or the U.S.), or it may be used as an intermediate input by the

parent. We make a symmetric assumption for the good produced by the parent.

3) Both the parent and affiliate have market power in final goods markets. They each

produce a variety of a differentiated product. These products are non-rival (i.e., not substitutes).

4) The parent and affiliate both produce output using a CRTS Cobb-Douglas production

function that takes labor, capital and materials as inputs. In addition, intermediates produced by

the affiliate may be a required input in the parent’s production process, and intermediates

produced by the parent may be a required input in the affiliate’s production process.

5) The affiliate and the parent both face iso-elastic demand functions in both the U.S. and

Canadian final goods markets.

6) The parent and affiliate both face labor force adjustment costs.

7) The MNC maximizes the expected present value of profits in U.S. dollars, converting

Canadian earnings to U.S. dollars using the nominal exchange rate.

8) The expected rate of profit is equalized across firms.

9) Parameters of technology and of demand are allowed to be heterogeneous both across

firms and within firms over time.

Tariffs and transport costs will enter the MNC’s profit function, because these costs are

levied on cross border flows. Exchange rates enter implicitly because the MNC cares about U.S.

dollar profits (and hence U.S. dollar output and input prices).

9 For instance we could assume that firms have market power by virtue of a fixed investment they have made inestablishing brand names or inventing a proprietary production process, and that licensing out of foreign operationswould potentially dissipate brand equity or risk revelation of proprietary knowledge.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 13/82

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 14/82

12

goods to third parties in both the U.S. and Canada (and vice-versa for parents).

The lack of information on stage of processing of intermediates also motivates our

assumption that the parent may potentially need output from the affiliate’s production process as

an input into its own production process, and vice-versa. As we discussed in the introduction, our

model must generate the potential for bilateral intra-firm trade in intermediates, because this is a

pervasive feature of the data. Since the data preclude modeling a multi-stage production process

explicitly, our assumption is the most direct way to generate bilateral intra-firm flows.

Finally, our assumption that the parent and affiliate produce two different goods enables

us to generate bilateral arms-length trade in finished goods, which is a pervasive feature of the

data. Our assumption that each is a variety of a differentiated product generates market power for

both the parent and affiliate in final goods markets. We must assume the goods are not

substitutable (e.g., U.S. demand facing the parent does not depend on imports from the affiliate)

in order to identify the demand elasticities given only information on revenues and costs.

Many MNCs do not utilize all four trade flows that are potentially present in our model

(i.e., arms-length imports and exports and the two intra-firm flows of intermediates). Our model

implies that these decisions should be based on expected present values of profits under each of

24 = 16 possible MNC configurations. Thus, estimation of a complete structural model would

require nested solution of a discrete/continuous stochastic dynamic programming problem with

16 discrete alternatives each period. It is well beyond available computational capacity to

implement such a model, especially given that we are required to conduct our analysis on site at

the BEA. In fact, the current state of the art in this literature is dynamic modeling of the export

decision alone, as in Das, Roberts and Tybout (1997) or Bernard and Jensen (2001).

While it is beyond the scope of our work to structurally model the firm’s decision to

engage in each of the four trade flows, we did not wish to assume that these decisions are

exogenous, in the sense of being unrelated to the stochastic terms in our structural model. As a

practical compromise, we estimate reduced form decision rules for the utilization of each flow,

and estimate these jointly with the structural model of the production process.

Preliminary investigation of the data suggests, and our results confirm, that most of the

action in increasing trade flows was at the intensive rather than the extensive margin. Loosely

speaking, the MNCs engaged in exporting, importing and trading intra-firm at the start of our

sample period were the same ones engaged in these activities at the end. Hence, fortuitously, it

turns out that a model of marginal decisions conditional on MNC structure is what is most

important for understanding changes in trade flows. Thus, to conserve on space, we relegate our

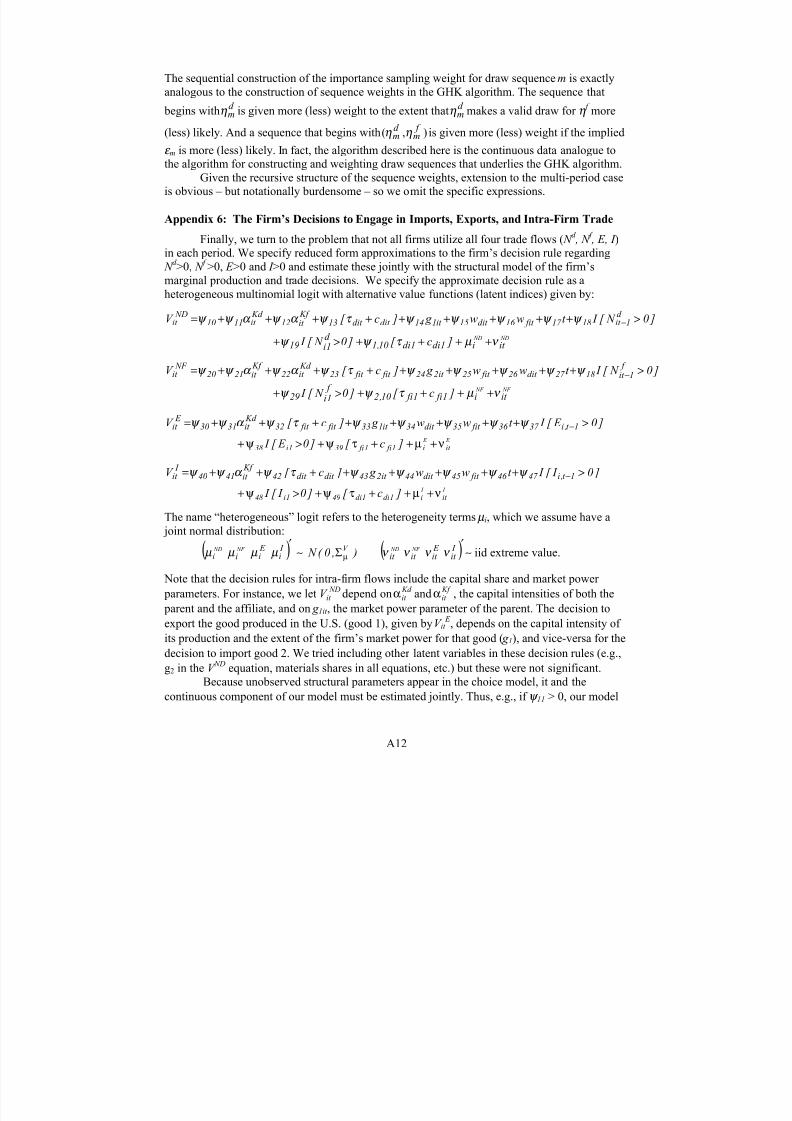

model of MNC decisions whether or not to engage in the four trade flows to Appendix 6.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 15/82

13

III.2. Basic Structure of the Model

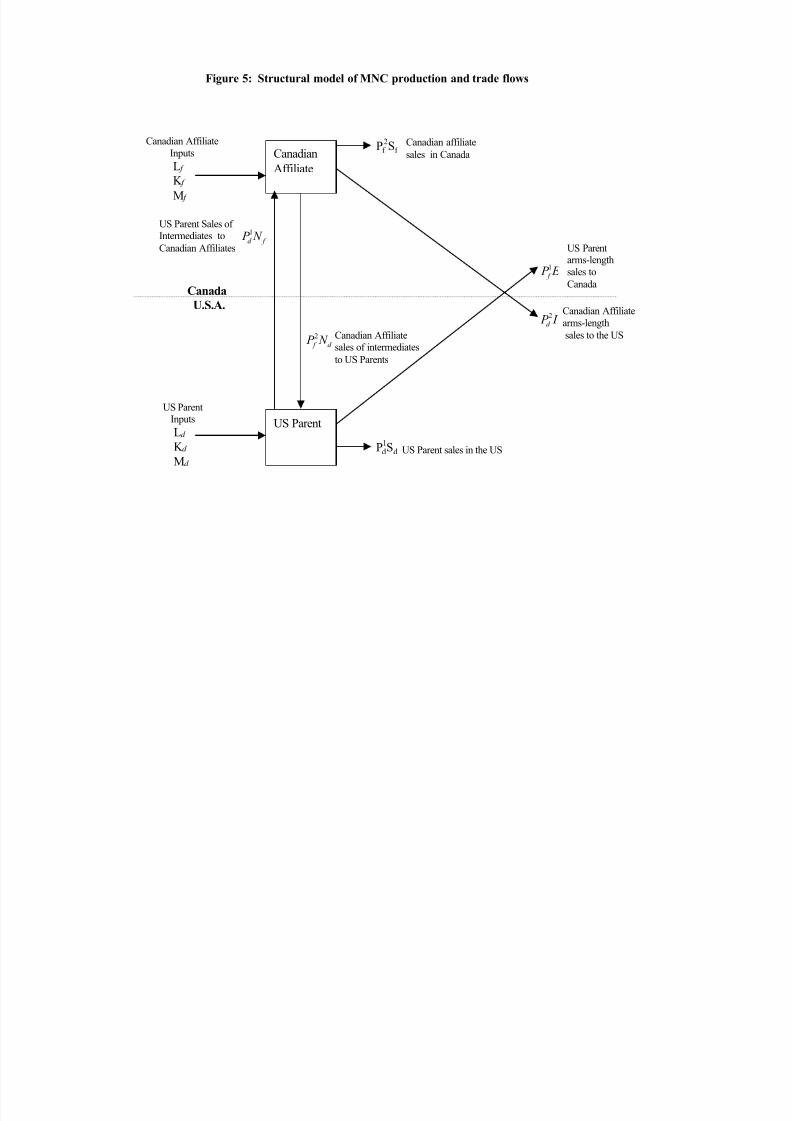

Figure 5 illustrates the most general case, in which a single MNC exhibits all four of the

potential trade flows (arms-length imports and exports and bilateral intra-firm trade). Instances

where an MNC has only a subset of these four flows are special cases. Qd and Q f denote total

output of the parent and affiliate, respectively. N d denotes the part of affiliate output shipped to

the parent for use as intermediate. Similarly, N f denotes intermediates transferred from the parent

to the affiliate. I (imports) denotes the quantity of goods sold arms-length by the Canadian

affiliate to consumers in the U.S., and E (exports) denotes arms-length exports from the U.S.

parent to consumers in Canada. Thus, S d ≡ (Qd -N f -E) is the quantity of its output the parent sells

in the U.S., and S f ≡ (Q f -N d -I) is the quantity of its output the affiliate sells in Canada.

Finally, the P denote prices, with the superscript j=1,2 denoting the good (i.e., that

produced by the parent or the affiliate) and the subscript c=d,f denoting the point of sale. Since

we do not observe prices and quantities separately in the data, we will work with the six MNC

firm-level trade and domestic sales flows, which are I P d

2 , E P f 1 , f d N P 1 , d f N P 2 , d

1d S P , and f

2 f S P .

In Figure 5, note that the price on N d , the intermediate good shipped from the Canadian

affiliate to the parent, is set equal to the price on the same good if sold to final customers in

Canada (and vice versa for N f ).10 Thus, we ignore issues of transfer price manipulation.

The corporate tax structures of the U.S. and Canada create incentives to manipulate

transfer prices to shift profits to Canada, since corporate tax rates are lower in Canada for

manufacturing firms. But transfer price manipulation is illegal under both U.S. and Canadian tax

law. IRS code section 482 and the Canadian Income Tax Code section 69 impose an “arms-

length” standard on transfer prices, meaning they should be set in the same way as prices

charged to unaffiliated buyers.

Eden (1998) reviews the empirical work on transfer price manipulation and shows that

the evidence for any such behavior by MNCs in the U.S.-Canada context is quite weak. It is

possible that MNCs avoid transfer price manipulation because they can use other means, such as

licensing fees, to shift profits. According to Eden (1998) such methods may be more common

since they are more difficult to detect than transfer price manipulation on tangible intermediate

goods. In light of this, we view our “arms-length” pricing assumption as reasonable.

The MNC’s domestic and Canadian production functions are Cobb-Douglas, given by:

(1) Md Nd Ld Kd

d d d d d d M N L K H Q α α α α =

10 Suppose we had assumed that the price on N d , the intermediate good shipped from the affiliate to the parent, was P d

2, the price on imports from the affiliate to final consumers in the U.S., rather than P d 1. This would make it

impossible to solve our model for firms with N d >0 but I =0, because then P d 2 is undefined.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 16/82

14

(2) Mf Nf Lf Kf

f f f f f f M N L K H Q α α α α =

Note that there are four factor inputs: capital ( K ), labor ( L), intermediate goods ( N ) and materials

( M ). We assume that the share parameters α sum to one for both the parent and affiliate (CRTS).

We allow the constants H d and H f to follow time trends in order to capture TFP growth.11

For the domestically produced good (good 1), the MNC faces the following iso-elastic

demand functions in the U.S. and Canada:

(3) 1 g d

1d 0

1d S P P

−= 1 g 1 f 0

1 f E P P

−= 0<g 1<1

Similarly, for the good produced in Canada (good 2), the MNC faces the demand functions:

(4) 2 g f

2 f 0

2 f S P P

−= 2 g 2d 0

2d I P P

−= 0<g 2<1

Recall that S d denotes the quantity of the U.S. produced good sold in the U.S., and S d denotes the

quantity of affiliate sales in Canada. The g 1 and g 2 are the (negative) inverses of the price

elasticities of demand for the domestic and foreign produced good, respectively.

Notice that the price elasticity of demand is a property of the good, and not the country.

For instance, the price elasticity of demand for the U.S. produced good is -1/g 1 in both the U.S.

and Canadian markets. But the demand function intercepts, 1d 0 P and 1

f 0 P , differ.12 We also

11 Interestingly, estimation of an aggregate MNC production technology can lead to misleading conclusionsregarding returns to scale. To see this, note that the production function (1) can be expressed directly in terms of capital, labor and materials inputs of the parent and affiliate, by substituting out for N d . If the decision rules for

intermediates are N d =λ Nd Q f and N f =λ Nf Qd (where, obviously, optimal λ Nd and λ Nf depend on prices), then: Nd Nf Mf Lf Kf Md Ld Kd

f f f f f Nd d d d d d N M L K H M L K H Qα

α α α α α α α λ

= .

Substituting for Nf and solving for Qd we can express (1) as:

Nd Nf Nd Mf Lf Kf Md Ld Kd Nf Nd Nd Nd 1

1

f f f d d d Nf Nd f d d M L K M L K H H Qα α α

α α α α α α α α α α λ λ −

=

Note that λ Nd and λ Nf are combined with the TFP terms H d and H f . Thus, the “aggregate” technology for the MNC as

a whole exhibits CRTS only if λ Nd and λ Nf are fixed as capital, labor and material inputs vary. However, the

aggregate technology may exhibit increasing or decreasing RTS if λ Nd and/or λ Nf vary along with capital, labor and

materials inputs as input prices, output prices and/or tariffs vary. We would expect tariff reductions to both lead toincreases in the size of MNCs (increases in K, L, M inputs) and to increases in the λ . Thus, it may appear thatMNCs have increasing RTS if an aggregate production function rather than separate parent and affiliate productionfunctions are estimated, and if intra-firm flows of intermediates are ignored. Another problem arises if one adopts a

standard approach of estimating the ln(Qd ) equation. Then, the stochastic terms will subsume changes in the λ Nd and

λ Nf terms. Since these depend on input prices, input prices will not be valid instruments for the input quantities.12 With the isoelastic functional form, gross revenue from exports is P d

2 E = P 0d 2 E (1-g1). Since 0<g 1<1, as E goes to

zero, revenue goes to zero, despite the fact that P d 2 approaches infinity. Thus, the model can rationalize a decision

not to export, although we do not model this decision structurally. The same is true with imports. See Appendix 6for a discussion of our reduced form decision rules for exports and imports that we estimate jointly with the model.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 17/82

15

assume the two goods are not substitutable. As we will see in section IV.5.B and Appendix 1,

these assumptions are critical in order to identify the price elasticities and the parameters of

technology using only information on nominal quantities.

Next, we assume the MNC faces labor force adjustment costs. It is often assumed such

costs are quadratic, e.g.: [ ]2

1, −−= t d dt d dt L L AC δ , where 0>d δ . However, we found that a

generalization of this function led to a substantial improvement in fit and could accommodate

many reasonable adjustment cost processes13:

(5) ( )( ) ∆− −

−=1,

2

1, t d L L L AC t d dt d dt

µ

δ where .0,0,0 ≥∆>> µ δ d

A similar adjustment cost function is specified for the affiliate, which will be allowed to have a

different δ parameter (δ f ). The curvature parameters µ and ∆ are assumed to be common.

We can write the MNC’s period specific profits (suppressing the time subscripts) as:

(6) )C T I ( E P )C T ( N P ) E N Q( P f f 1

f f f f 1

d f d 1

d −−++−−−=Π

)C T I ( I P )C T ( N P ) I N Q( P d d 2

d d d d 2

f d f 2

f −−++−−−+

) L , L( AC ) L , L( AC K K M M Lw Lw )1(

f f f )1(

d d d f f d d f f d d f f d d −− −−−−−−−− γ γ φ φ

Here, T f and C f are the Canadian tariff and transportation costs the MNC faces when shipping

products from the U.S. to Canada (and similarly for T d and C d ). The exchange rate enters the

problem implicitly through the fact that Canadian affiliate costs and revenues are converted into

U.S. dollars using the nominal exchange rate. wd and w f are the domestic and foreign real wagerates respectively, and φ d and φ f are the domestic and foreign materials prices. γ is the price of

capital, which we will assume is equal for the parent and the affiliate (γ d = γ f ).

The MNC’s problem is to maximize the expected present value of profits in real U.S.

dollars ∑ Π∞

=+

1τ τ

τ β t E by choice of eight control variables ft , ft , ft , ft ,dt ,dt ,dt ,dt N K M L N K M L .

The final feature of our model is the assumption that the expected rate of profit is

equalized across firms (a condition that should hold in equilibrium if there are no capital

adjustment costs – which we assume – and ignoring risk adjustments). This assumption is driven

by the problem that we do not feel there are reliable measures of the payments to capital, d d K γ

and f f K γ , for parents and affiliates in the BEA data. But, by assuming a particular profit rate,

13 For example, setting 1=µ and 0=∆ produces [ ]2

1, −− t d dt d L Lδ . Similarly,21=µ and 1=∆ gives

1,1, /)( −−− t d t d dt d L L Lδ .

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 18/82

16

we can back out the payment to capital and profit from data on total revenues and payments to

the other factors.14 Thus, we treat the profit rate, which we denote by R, as an unknown

parameter to be estimated. We discuss the intuition for its identification in Appendix 2.

This completes the exposition of our model, which is obviously very simple. As we have

discussed, the strong simplifying assumptions we have made are motivated by the need to obtain

a model that is estimable using the rather limited available data on MNC operations.

III.3 Stochastic Specification

Our model contains eight parameters ( R, β , δ d , δ f , µ , ∆ , H d and H f ) that we assume are

common across firms. Our model also contains eight technology parameters (α Kd , α Ld

, α Nd , α Md

,

α Kf , α Lf

, α Nf , α Mf ) and six demand function parameters (g1,

1d 0 P , 1

f 0 P , g2,2d 0 P and 2

f 0 P ) that we

allow to be heterogeneous both across firms and within firms over time. In the following

subsections we describe our stochastic specification for the firm specific parameters.

Since we impose CRTS, two of the share parameters (α) are determined by the other six.

Thus, we have a vector of twelve fundamental parameters that can vary independently. In section

III.3.A we describe how we let the share parameters be stochastic while still imposing CRTS. In

section III.3.B we describe the stochastic specification for the demand function parameters.

Naturally, we expect (hope) that the firm specific parameters will exhibit strong

persistence within firms over time, so we adopt a random effects specification, which we

describe in section III.3.D. Each parameter has a mean, a firm specific component, and a

firm/time specific component. This adds a substantial number of parameters to our model, since

we must estimate variance-covariance matrices for the random effects and the time varying error

components. These variance-covariance matrices are each 12×12, giving 210 unique elements.

Below we describe how we constrain these matrices in order to conserve on parameters.

14 The procedure works as follows. Denote domestic revenue by RD, domestic costs by CD* and domestic costs

excluding capital costs by CD1. These quantities are given by:

) E P )( C T 1( N P S P RD 1 f f f f

1d d

1d

−−++=

d d d d 2

f d

d d

d d

d

* AC )C T 1( N P M K LwCD ++++++= φ γ

d d K CD1CD γ −≡

Now, let R K denote the fraction of operating profit that is pure profit, leaving (1-R K ) as the fraction that is the

payment to capital. This gives Π d = R K ⋅ [RD-CD1] and thus:

]1CD RD[ ) R1( K K d d −⋅−=γ

Thus, the rate of profit for domestic operations is R = Π d / γ d K d = R K /(1-R K ). We treat R as a common parameter across firms and countries that we estimate (we also assume it is equal for the parent and the affiliate). That is, for the affiliate we have the analogous equation:

]1CF RF [ ) R1( K K f f −⋅−=γ

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 19/82

17

A key point is that we allow each of the twelve fundamental technology and demand

parameters to have a time trend. This enables the model to capture changes in production and

trade decisions that are not explicable by changes in tariffs, wages, exchange rates, etc.

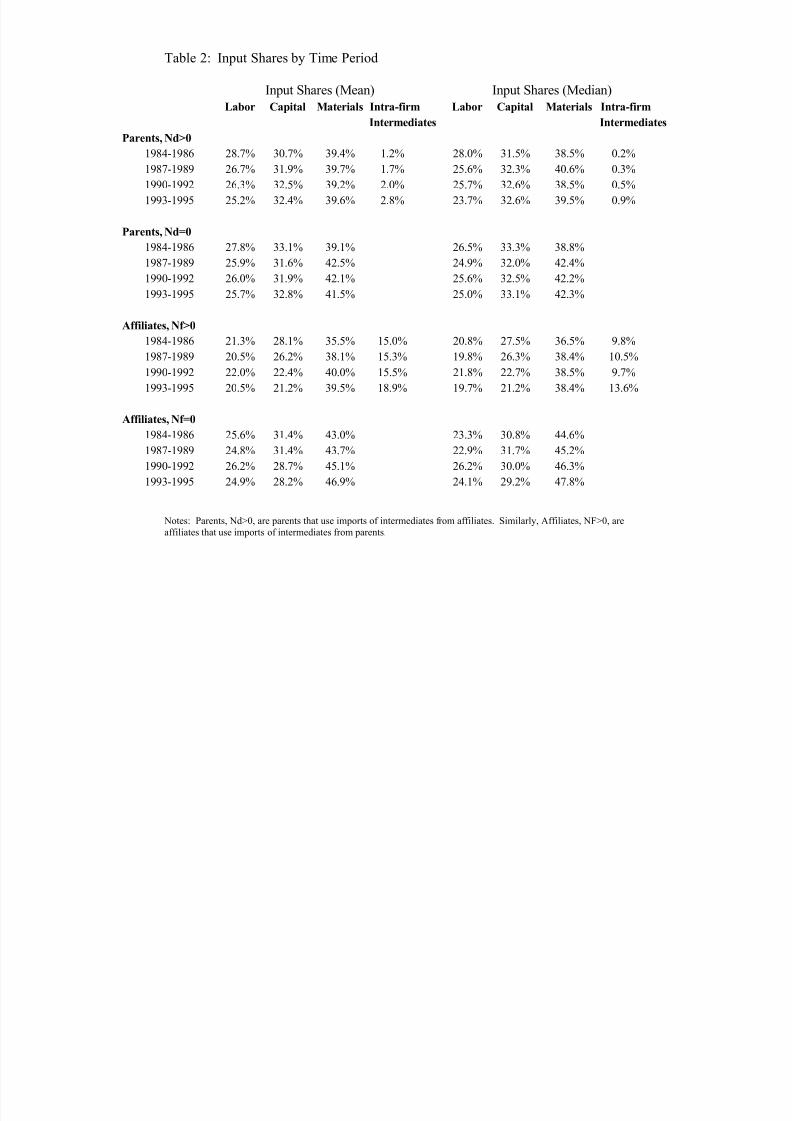

In preliminary analysis, we found that parents (affiliates) that do not use intermediate

inputs from affiliates (parents) have very stable Cobb-Douglas share parameters over time.

Given the large relative changes in factor input prices from 1984-1996 (see Figure 2), this is

striking evidence in favor of a simple Cobb-Douglas specification. But we also found that

parents and affiliates that use intermediate inputs have important time trends in the share

parameters. Therefore, we allow the time trends and base values of the technology and demand

parameters to differ across firms depending on whether or not they use intermediates.

III.3.A. Production Function Parameters

Allowing the Cobb-Douglas share parameters to be stochastic, while also imposing that

they are positive and sum to one (CRTS), is challenging. To impose these constraints, we use a

logistic transformation, treating the share parameters as analogous to choice probabilities in a

multinomial logit (MNL) model. For instance, looking at the domestic share parameters, we

have, suppressing firm and time subscripts:

(7) Ld R Kd Md Ld

Ld

1α

α α α

α ≡

−−−

Analogous expressions define Md Rα and Kd

Rα . The quantity Nd Rα is normalized to equal 1. Next, we

specify that the quantities Ld Rα , Md

Rα and Kd Rα are stochastic. As long as we choose a stochastic

specification that guarantees that the quantities Ld Rα , Md

Rα and Kd Rα are positive, then the implied

share parameters α Ld , α Kd

, α Md and Nd α will be positive and sum to one.

A natural specification would be log normality (although we generalize this below).

Then, for example, the stochastic term Ld Rα would be given by:

Ld Ld Ld R x ε α α +=ln Ld ε ~ ) ,0( N

2 Ld σ

where the vector xit includes all firm characteristics that shift the share parameters, and Ld α is a

vector of parameters. This insures that 0 Ld R >α for all Ld ε . Similar equations could be specified

for Md Rα , Kd

Rα . Then, given a vector Ld Rα , Md

Rα , Kd Rα we can solve for α Ld

and obtain:

1)8(

Kd R

Md R

Ld R

Ld R Ld

α α α

α α

+++=

{ } { } { } Kd Kd Md Md Ld Ld

Ld Ld

x x x

x

ε α ε α ε α

ε α

++++++

+=

expexpexp1

exp

Similar expressions give α Kd and α Md . Note that the expression for α Nd is:

(9){ } { } { } Kd Kd Md Md Ld Ld

Nd

x x x ε α ε α ε α α

++++++=

expexpexp1

1

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 20/82

18

So Nd α plays the role of the “base alternative” in a multinomial logit model. This specification

insures that, given any values for the xit ϖ and any draw for the ε it , the technology parameters are

guaranteed to be positive and sum to 1.

In our empirical application we allow xit to include just an intercept and a time trend t

(t=0 in 1983). But, as we noted above, we allow different intercepts and time trends for parents

(affiliates) that do and do not use intermediate inputs from affiliates (parents).

If the U.S. parent is not structured to use intermediate inputs from the affiliate, then

α Nd =0, and we must constrain the remaining three share parameters, α Ld

, α Md and α Kd

, to sum to

one. This is done just as above, except that now we let α Kd play the role of the base alternative. A

similar construct is used for affiliates that do not use intermediates from the parent. Because the

scale of the coefficients in a MNL model with three alternatives is quite different from that of a

MNL model with four alternatives, we also introduce a scaling parameter that scales down the

error terms in the three alternative case. Thus, for the α R Ld equation, we have:

(10) ln α R Ld

= α 0 Ld

+ α shift Ld

I[N d >0] + α Time Ld ⋅ t ⋅ I[N d >0] + α Time

Ld ⋅ t ⋅ I[N d =0]⋅ SC d

+ ε Ld { I[N d >0] + SC d ⋅ I[N d =0]}

Similar equations hold for α R Md and α R

Kd , except that we simply have α R Kd

=1 in the N d =0 case.

The same scaling parameter, SCd, applies in the α R Md equation in the N d =0 case. In the equations

for the affiliate parameters α R Ld , α R

Md and α R Kd , we allow for a different scaling parameter, SC f .

Originally, we estimated the model assuming log normality, but this was severely

rejected for most of the stochastic terms. So instead we turned to a Box-Cox transformation.

Using a Box-Cox transformation with parameter bc(1), equation (10) becomes:

(11)( ) Ld Ld

bc Ld R x

bcε α

α +=

−)1(

1)1(

{ I[N d >0] + SC d ⋅ I[N d =0]}

Similar expressions hold for the parameters Md Rα , Kd

Rα and also for the affiliate parameters. We

denote the Box-Cox parameters in these equations as bc(2) through bc(6). Given the Box-Cox

transformation, we only (mildly) reject normality for two of the twelve stochastic terms.15

Strictly speaking, the Box-Cox transformation does not impose positivity on the share

parameters. But, given our estimates of the Box-Cox parameters and the variances of the

stochastic terms, negative outcomes would be extreme outliers.

15 Note that we only have an equation for Kd Rα in the case of N d > 0, because if Nd = 0 we normalize

Kd Rα = 1 and if

N f = 0 we normalize α R Kf = 1. Thus, for illustration, the equation for

Kd Rα is just:

( ) Kd

d Kd time

Kd 0

)3( bc Kd R SC t aa

)3( bc

1ε

α ⋅+⋅+=

−

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 21/82

19

Turning to the correlations of the ε , we specify that

(12) ( )′ Nd Md Ld ε ε ε ~ ( )d N Σ,0 ,

where Σ d is unrestricted. Similarly, for affiliates, Σ f is unrestricted. But, in order to conserve on

parameters, we do not allow for covariances between the parent and affiliate share parameters.16

Finally, consider the TFP parameters H d and H f in equations (1) and (2). Since we do not

observe output prices and quantities separately, we cannot identify the scale of the H (either

absolutely or for the affiliate relative to the parent. However, we can identify technical progress.

Thus we normalize H d = H f = 1 at t=0 (1983) and let each have a time trend:

(13) H jt = (1 + h j )t

for j=d,f .

We could not reject a specification with equal time trends, so we set hd = h f = h.

III.3.B. Demand Function Parameters

Now, we turn to the stochastic specification for the demand function parameters. For the inverse price elasticity of demand, or market power, parameters, g 1 and g 2, we specify:

( )

( )2

1

g shift 2,time ,220

8bc2

g shift 1,time ,110

7 bc1

0]·I[Nf g t g g )8( bc

1 g

0]·I[Nd g t g g )7 ( bc

1 g

ε

ε

+>+⋅+=−

+>+⋅+=−

(14)

and, for the demand function intercepts, we specify:17

(15)

2d 0

1 f 0

2 f 0

1d 0

P 2shift 0d,

2time ,d 0

20 ,d 0

)12( bc2d 0

P 1shift 0f,

1time , f 0

10 , f 0

)11( bc1 f 0

P 2 shift 0f,

2time , f 0

20 , f 0

)10( bc2 f 0

P 1shift 0d,

1time ,d 0

10 ,d 0

)9( bc1d 0

0]·I[Nf P t P P )12( bc

1 ) P (

0]·I[Nd P t P P )11( bc

1 ) P (

0]·I[Nf P t P P )10( bc

1 ) P (

0]·I[Nd P t P P )9( bc

1 ) P (

ε

ε

ε

ε

+>+⋅+=−

+>+⋅+=−

+>+⋅+=−

+>+⋅+=−

16 Interpretation of the Σ d and Σ f terms is rather subtle. The logistic transformation already incorporates the negative

correlation among the share parameters that is generated by the CRTS assumption. If Σ d = I , we have an “IIA”setup, where if one domestic share parameter increases, the other share parameters decrease proportionately. The

correlations in Σ d and Σ f allow firms to depart from this IIA situation. For example, if Σ d 12 is very large, then we get

a pattern where firms with large domestic labor shares also have large domestic materials shares.17 Technically, we should impose that g 1 and g 2 are positive and less than 1, and that the P o terms are positive.Equations (14)-(15) do not impose these constraints. But, given our estimates, violations would be extreme outliers.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 22/82

20

Preliminary estimations of the model suggested that cross correlations between the 3 groups of

parameters (technology, price elasticities, and demand function intercepts), were not important.

Also, allowing for all possible cross correlations leads to a substantial proliferation of

parameters, which, in turn, leads to extreme difficulty in obtaining convergence of the search

algorithm. Thus, we specified 1 g ε and 2 g ε as independent of other stochastic terms and allowed

the ) , , ,( 2d 0

1 f 0

2 f 0

1d 0 P P P P

ε ε ε ε vector to be correlated within itself but not with the other stochastic

terms. We denote the covariance matrix of the latter vector by Σ P .

III.3.C Labor Force Adjustment Cost Parameters

Recall that labor force adjustment costs are given by equation (6). The parameters δ d and δ f are

allowed to vary across firms as follows:

(16) { } ]0 N [ I t wexp dt d d dt d 0 ,1d dt >⋅+⋅++= δ δ δ δ δ

]0 N [ I t wexp ft f f ft f 0 ,1 f ft >⋅+⋅++= δ δ δ δ δ

As with the other structural parameters, we allow for the possibility that adjustment costs vary

over time, and we allow for the possibility that the adjustment costs differ between firms that do

and do not have intra-firm flows. We also allow the δ to be functions of the wage rate, on the

premise that search and severance costs for high wage/highly skilled labor are higher).

III.3.D Serial Correlation

Since we have a panel, it is important to allow for serial correlation of the errors within each firm

over time. We specify a permanent-transitory (random effects) structure. Thus, e.g, for the

stochastic part of the parent labor share parameter ε Ld we have:

)()()( it Ld i Ld it Ld ν µ ε += for t=1,…T i

and similarly for the other eleven parameters. Let µ i ∼ N(0, Σ µ ) denote the 12×1 vector of random

effects for firm i, and let ν it ∼ N(0, Σ ν ) denote the 12×1 vector of firm/time specific error

components. Then, V t ≡ Var( ε it ) = Σ µ + Σ ν and C t-j, t ≡ Cov( ε it , ε i,t-j ) = Σ µ . Note that Σ µ and Σ ν

each contain 78 unique elements, but these are restricted as described earlier. For instance, the

non-zero elements of Σ µ + Σ ν consist entirely of elements of P f d , Σ Σ Σ and along

with 21 g σ and 2

2 g σ . Other cross-correlations are set to zero. Defining ) ,....,( iiT 1ii ε ε ε = we have:

(17)

=

ii T T 1

212

1

i

V C

V C

V

)( Var

!!

"#ε

So far, we have only considered the most general case where a firm has all 4 potential trade

flows. If a firm has N dt =0 (or N ft =0) at time t , then there is no value for ε Kd (it) (or ε Kf

(it)).

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 23/82

21

Similarly, if E t =0, there is no value for )it ( 1 f 0 P , and if I t =0 there is no value for )it (

2d 0 P .

Additionally, some firms are not observed for consecutive years. In such cases Var( ε i ) is

collapsed in the obvious way (by removing the relevant rows and columns).

IV. Estimation

IV. 1. Overview

In this section we describe our estimation algorithm. Although our model is quite simple,

estimation is complicated because we do not observe prices and quantities separately, and since

we allow many model parameters be heterogeneous across firms and time. Readers not interested

in the details of the estimation procedure can skip directly to section V, which discusses the data.

We base estimation on the first order conditions (FOCs) of the MNC’s optimization

problem.18 Estimation based on FOCs is usually implemented using GMM, but this option is not

open to us because we have multiple stochastic terms that enter the FOCs in highly non-linear

ways. Hence, we cannot manipulate the FOCs to obtain a single additive error term from which

to construct moments. Thus, we estimate the model using simulated maximum likelihood (SML).

In section IV.2 we present the FOCs of the model, and discuss some aspects of firm

behavior. In section IV.3 we discuss why moments based estimation is not feasible. In section

IV.4 we describe our SML alternative, which requires a specification of the stochastic process

for firms’ errors in forecasting future labor force size.

Section IV.5 shows how we construct the simulated likelihood function. The first step is

to solve the nonlinear system of equations that map the data into the stochastic terms of our

model. Section IV.5.B and Appendices 1-2 discuss this mapping and also contain an intuitive

discussion of identification of the model parameters.

Next, we obtain the joint density of these stochastic terms, and multiply it by the Jacobian

of the transformation from the joint error density to the joint data density. This process is quite

challenging for two reasons. First, the Jacobian is analytically intractable. But in section IV.5.C

we show how it can be approximated using simulation methods and numerical derivatives.

Second, the stochastic terms in our model are all continuous, yet they must fall in certain

sub-regions of a high dimensional space in order for firm behavior to be rationalizable by the

model (see section IV.5.D and in Appendix 3). As a result, a high dimensional integral must be

18 It is common to estimate production functions in levels using only nominal sales revenue data. The standardapproach is to use an industry level price index to construct real output. But this procedure is only valid in perfectlycompetitive industries, so that price is exogenous to the firms. This condition is obviously violated for MNCs.

There is an added complication in our case, because, in our model, intermediates shipped intra-firm are keyinputs in the production functions of parents and affiliates. We only observe nominal values of these intermediates.Intermediates cannot be deflated using industry price indices because they can also be sold as final goods in marketswhere the MNC has market power (making the price of intermediates endogenous). By working with the FOCs, wecan identify the Cobb-Douglas share parameters without needing to deflate either sales or input quantities.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 24/82

22

evaluated to construct the joint density of a firm’s stochastic terms. In section IV.5.E and

Appendix 4 we present a recursive importance sampling algorithm that can deal with this

integration problem. The algorithm is the discrete/continuous analogue of the GHK algorithm

(see, e.g., Keane (1994)) for discrete choice data. Just as GHK has found wide application in

discrete choice problems, the new algorithm may have wide application in discrete/continuous

problems. For instance, it would be useful in any situation where, in certain regions of the space

of stochastic terms, a firm would shut down or discontinue certain activities, etc., and where one

needs to simulate the density of marginal decisions conditional on the firm being active.

Evaluating our model’s distributional assumptions (as well as simulation of the model) is

also challenging. To do this we need a practical way to draw ex-post from the joint distribution

of the model’s stochastic terms, given our estimates. The vector of stochastic terms is 14×1, but

is constrained to lie in a 12 dimensional sub-space determined by the12×1 data vector. In section

IV.6 and Appendix 5 we present another new GHK type algorithm to draw a K

×1 vector of

continuous random variables subject to the constraint it lie in a space of dimension less than K.

Finally, in section IV.7 and Appendix 6 we present the reduced form heterogeneous logit

model that we use to model firms’ decisions about whether to engage in each of the four possible

trade flows. We allow for both heterogeneity and state dependence in these decisions using a

new approach recently suggested by Wooldridge (2001).

IV.2. Solution of the firm’s problem and Derivation of Estimable FOCs

The first order conditions for parent factor inputs and parent’s exports to Canada are:

0:

)1(

)(

)()(

1

111

1

1

=

−−−

−

∂

∂

∂

∂

−−

+−−− +

d

d

d

d

d f d d

f f f d f d d

d

d d Ld

d

d d Ld

d L

AC

L

AC

E N Q P

C T N P E N Q P

L

Q P

L

Q P

E w g L β α α

0:)(

)()(

1

111

1

1

=−

−

−−

+−−−d

f d d

f f f d f d d

d

d d Kd

d

d d Kd

d E N Q P

C T N P E N Q P

K

Q P

K

Q P g K γ α α

0:)(

)()(

1

111

1

1

=−

−

−−

+−−−d

f d d

f f f d f d d

d

d d Md

d

d d Md

d E N Q P

C T N P E N Q P

M

Q P

M

Q P g M φ α α

−

−−

+−−−

) E N Q( P

)C T ( N P ) E N Q( P

N

Q P

N

Q P

f d 1d

f f f 1d f d

1d

d

d 1d Nd

1d

d 1d Nd

d g : N α α

0 P )C T 1( P g 2 f d d

d f 2

f

d d d 2

f d f 2

f 2 f 2

) I N Q( P

)C T ( N P ) I N Q( P =++−

+

−−

+−−−

0)1()1(: 1

11

111

1

1

)(

)()(=−−−+

+

−−+−−−

f f f f d d

f f f d f d d

d d C T P g P g P E E N Q P

C T N P E N Q P

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 25/82

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 26/82

24

Similarly, the first order condition for E equates the marginal revenue from exports of the

domestically produced good to Canada with the marginal revenue from domestic (U.S.) sales.

Observe that if the Canadian tariff and transport costs are zero, ( C f + T f ) = 0, then A = 1. As a

result, the FOC for E reduces to P f 1= P d

1, which means that the MNC exports the domestically

produced good to the point where price in the US and Canada are equalized.

Tariffs and transport costs create a wedge between the U.S. and Canadian prices for final

goods. For instance, if the affiliate does not use the good produced by the parent (good 1) as an

intermediate input, then A=1, and the FOC for exports reduces to P d 1 /P f

1= (1-T f -C f )<1. Thus,

Canadian tariff and transport costs cause good 1 to cost more in Canada.19 However, if the

affiliate uses good 1 as an intermediate, then A<1. The parent then has an incentive to hold down

P d 1

because the tariff and transport cost of shipping intermediates to Canada is increasing in P d 1.

This effect is stronger the less elastic is demand (i.e., the larger is g 1) and the higher are tariffs.20

Since prices and quantities are not separately observed, we cannot take these FOCs

directly to the data. We now describe how we can manipulate the FOCs to obtain estimable

equations that contain only observed quantities and unknown model parameters. First, if we

multiply each first order condition by the associated control variable, we obtain:

0 L ) FD( E Lw )Q P )( A g 1( : L d d d d d 1d 1

Ld d =−−− δ α

0 K )Q P )( A g 1( : K d d d 1

d 1 Kd

d =γ −−α

(18) 0 M )Q P )( A g 1( : M d d 1

d 1 Md

d =φ−−α

0 ) N P )( C T 1( B ) N P ( g )Q P )( A g 1( : N d 2

f d d d 2

f 2d 1

d 1 Nd

d =++−+−α

0 ) E P )( A g 1( )C T 1 )( E P )( g 1( : E 1

d 1 f f 1

f 1 =−−−−−

Note that in the first order condition for E , the endogenous quantity ) E P ( 1d is not observable.21

However, we can exploit the fact that:

(19) ) E P ( 1d = ) E P ( 1

f 1 f

1d

P

P

= ) E P ( 1

f

1 g

1 f

d 1d

1 f 0

1d 0

E P

S P

P

P ⋅

−

19 Without our assumption that price elasticity of demand for good 1 is equal in both countries, the price ratio wouldalso depend on the difference in demand elasticities. But with equal elasticities, the incentive to raise price byreducing sales is equally strong in both countries, so price is equalized except for the tariff and transport cost wedge.20 If the parent tries to lower P d

1 too much relative to P f 1 it might create an arbitrage opportunity whereby third

parties could buy the good in the U.S. and resell it in Canada. We could invoke a segmented markets (or no resale)condition as in Brander (1981) to rule out this possibility. Such an assumption is common in trade models withdifferentiated products. Alternatively, we could assume transport costs are higher for third parties.21 Note: P d

1 E is the physical quantity of exports times their domestic (not foreign) price – an object we cannotconstruct since we do not observe prices and quantities separately

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 27/82

25

to express the first order condition for E in terms of observable quantities and the ratio of

demand function intercept parameters )1 f 0

1d 0 P P as follows:

(20) E: 0 ) E P ( ) A g 1( )C T 1 )( E P )( g 1( 1 f

1 g

1

f

d 1d

1

f 0

1d 0

1 f f 1

f 1 E P

S P

P

P =⋅

−−−−−

−

Similarly, in the FOCs for the factor inputs, the quantity )Q P ( d 1

d is also not observed. We

can rewrite this quantity as ( ) ) E P ( P P N P S P Q P 1 f

1 f

1d f

1d d

1d d

1d ++= but, again, E P 1d is not

observed. We therefore repeat the same type of substitution to obtain, for domestic labor:

(21) 0 L ) FD( E Lw ) E P ( N P S P ) A g 1( : L d d d d 1

f

g

1 f

d 1d

1 f 0

1d 0

f 1d d

1d 1

Ld d

1

E P

S P

P

P =−−

++−

−

δ α

The FOCs for K d , M d and N d are obtained similarly, so we do not repeat them. The FOCs for the

affiliate have a similar form.

We now have ten first order conditions ( Ld , K d , M d , N d , L f , K f , M f , N f , E , I ) expressed in

terms of observable quantities, unknown parameters, and an unmeasured expectation term.

Below, we show how these FOCs can be used to identify the Cobb-Douglas share parameters,

the price elasticities of demand, and the ratios of the demand function intercepts for the two

goods – i.e., ( )1 f 0

1d 0 P P and ( )2

f 02d 0 P P . We will need price indices for capital and materials in

order to identify the demand function intercepts separately (and the TFP terms). It is important to

note however, that an important subset of parameters, and hence some of our key results, are

identified without needing to deflate any of the nominal quantities we observe in the data.

IV.3. The Choice of Estimation Method

We could in principle use nonlinear GMM to estimate our model using the ten FOCs

derived in section IV.2, along with a sufficiently large set of instruments to identify all the model

parameters. Since a GMM approach is so commonly used for estimation based on FOCs, we first

describe why it is not feasible for our model. Then we describe our SML approach.

To illustrate the problems with GMM, it is useful to consider a simpler stochastic

specification than that in section III.3. Consider the Ld equation (21), which contains threestochastic terms (α it

Ld , g 1it and 1

d 0 P / 1 f 0 P ). Suppose we specify that:

)it ( Ld Ld Ld

it exp ε α α +=

)it ( 1

1it 1 g g exp g +=

( ) { } )it ( 11it

1 f 0

1d 0 pr PRexp P P +=

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 28/82

26

Here, we have only imposed that the share parameter for labor be positive. We have not imposed

CRTS. Thus, this specification is simpler than what is needed, but will suffice to make our point.

Next, to deal with the expectation term in (21), we invoke a rational expectations assumption:

(22) d it dit it dit it t L FD L ) FD( E η−=

and obtain the following equation for Ld , incorporating forecast errors, d it η :

(23)

⋅

++−

−−

− ) E P ( ee N P S P ) Aee1 )( e( e: L 1

f

ee

1 f

d 1d )it ( 1 pr 1 PR

f 1d d

1d

g 1 g d

1it g 1 g

1it

Ld it

Ld

E P

S P ε α

0=+−− d it d dit it d d d L FD Lw ηδ δ

The other equations of the model could be obtained similarly, by substituting expression for the

stochastic parameters into the other FOCs.The problem with a GMM approach in this context is obvious. The four stochastic terms,

ε it Ld , ε it

g1, ε it pr1, and ηit

d , appear in (23) in such a highly nonlinear way that it is not possible to

express the equation as a moment condition with a single additive error term. The key pr oblem is

that there are multiple stochastic terms, and also that the ε it g1

term appears in two places.22 If

there were only a single stochastic term that appeared in only one place, we could always find

appropriate transformations so that the FOC could be written in terms of a single additive error.

Krusell, Ohanian, Ríos-Rull and Violante (2000) confronted a problem similar to what

we face here when they estimated a production function that included unobserved quality of skilled and unskilled labor as two latent (stochastic) inputs. Because they had two stochastic

labor quality shocks, both of which entered nonlinearly, along with a forecast error term, the

FOCs of their model could not be written in terms of a single additive error term.

More fundamentally, even if we could implement a GMM approach successfully, it

would not be adequate for our purposes. The usual argument for GMM over ML is that one

avoids making distributional assumptions – in this case on the technology, market power and

demand shift parameters that are assumed heterogeneous across firms, and on the forecast errors

– and thereby obtains more robust estimates of model parameters. But we need to assume (andestimate) the distribution of the firm specific parameters in order to be able to simulate the

response of the population of firms to changes in tariffs or other features of the environment.

22 A second problem is that, even if we could linearize equation (23), the choice of instruments is not at all obvious.Usual candidates like input prices might well be correlated with other firm specific technology parameters if technology changes over time in response to price changes. Third, nonlinear GMM is known to often suffer fromsevere numerical instability, even in much simpler models than this.

7/29/2019 MNC Related Doc

http://slidepdf.com/reader/full/mnc-related-doc 29/82

27

IV.4 The SML Approach, and the Stochastic Process for Forecast Errors

Given the problems with a GMM approach, we decided to estimate the model by

simulated maximum likelihood (SML). SML can deal with the fact that multiple stochastic terms

enter the FOCs in (20)-(21) in a highly nonlinear way. But the use of SML raises a new problem,

which is how to handle the unmeasured expectation term in (21). In a full information ML

approach, one would specify how firms form expectations of future labor inputs. This would