MLP Basics Understanding MLPs Basics Understanding MLPs September 5, 2012. Confidential and...

61

Confidential and Proprietary MLP Basics Understanding MLPs September 5, 2012

Transcript of MLP Basics Understanding MLPs Basics Understanding MLPs September 5, 2012. Confidential and...

Confidential and Proprietary

MLP Basics

Understanding MLPsSeptember 5, 2012

Confidential and Proprietary

2

Today’s Panel

Capital Markets:

David Oelman

713.758.3708

Doug McWilliams

713.758.3613

Tax:

Ryan Carney

713.758.4720

Confidential and Proprietary

MLP Capital Markets Practice Group

Mike Rosenwasser David Oelman Doug McWilliamsAlan Baden Michael Swidler D. Alan Beck

Shelley Barber

Catherine Gallagher

Brenda Lenahan

Jeff Malonson

Jim FoxGillian Hobson Jim Prince Adorys VelazquezMatt PaceyE. Ramey Layne

Cheryl Jordan Will JordanSarah Morgan John Johnston Lauren Dean Dan SpelkinSteve Gill Doug Getten

Lande SpottswoodWill Burns Thomas Zentner Lauren Hunt James Brown Randi RevisoreAdam Law Matt Wiener

3

Confidential and Proprietary

4

MLP Tax Practice

MLP Finance Practice

Robert JacobsonRyan Carney Debbie DuncanBarry Miller Price Manford Judy Blissard John Lynch

Will Bos Brian Moss Brett SantoliMichael McKay

Price Manford Gary Huffman

Confidential and Proprietary

Confidential and Proprietary

5

Confidential and Proprietary

6

Contents

• MLP History

• Capital Markets

• Traditional Structure

• Governance & Accounting Issues

• Qualifying Income

• Other Tax Considerations

• Legislative Developments

• Questions and Answers

Confidential and Proprietary

MLP History

Confidential and Proprietary

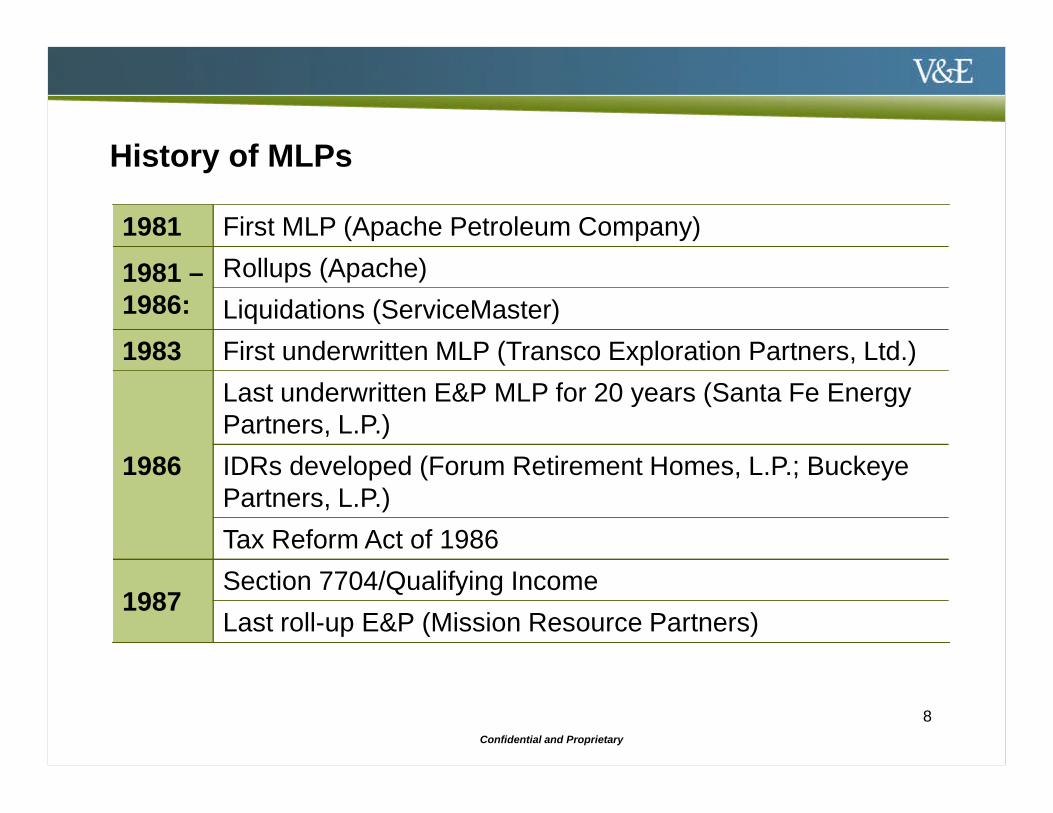

History of MLPs

1981 First MLP (Apache Petroleum Company)

1981 –1986:

Rollups (Apache)

Liquidations (ServiceMaster)

1983 First underwritten MLP (Transco Exploration Partners, Ltd.)

1986

Last underwritten E&P MLP for 20 years (Santa Fe EnergyPartners, L.P.)

IDRs developed (Forum Retirement Homes, L.P.; BuckeyePartners, L.P.)

Tax Reform Act of 1986

1987Section 7704/Qualifying Income

Last roll-up E&P (Mission Resource Partners)

8

Confidential and Proprietary

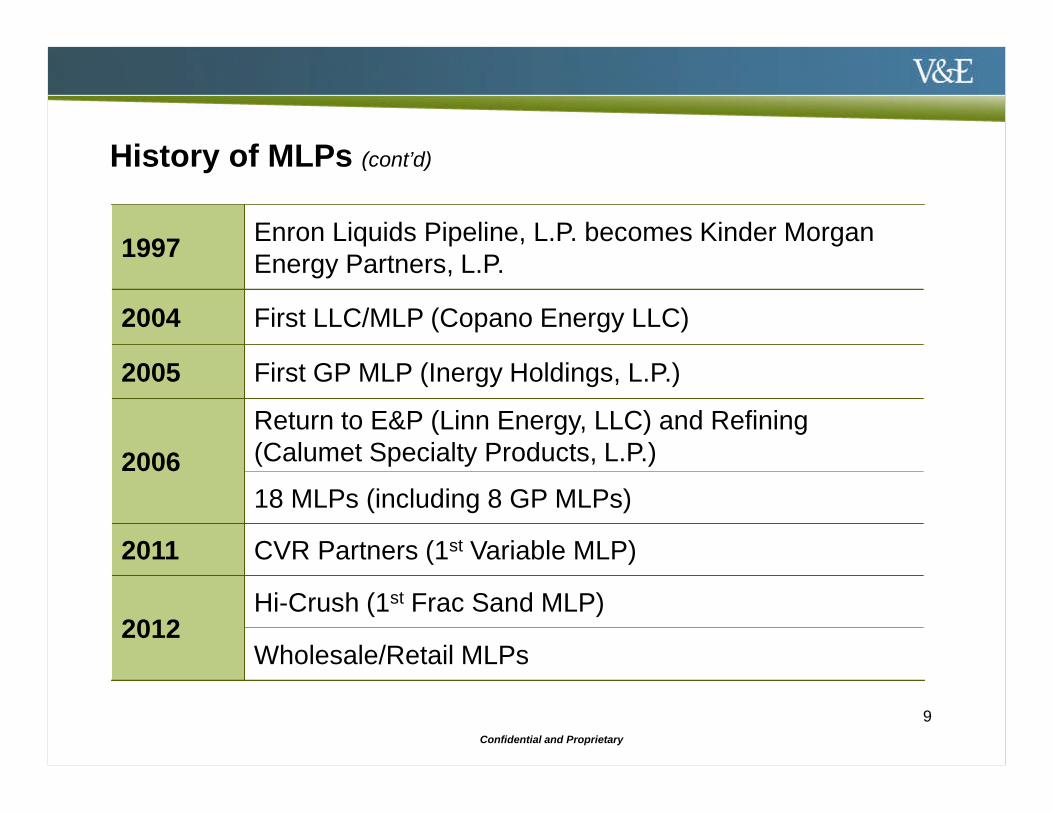

History of MLPs (cont’d)

9

1997Enron Liquids Pipeline, L.P. becomes Kinder MorganEnergy Partners, L.P.

2004 First LLC/MLP (Copano Energy LLC)

2005 First GP MLP (Inergy Holdings, L.P.)

2006

Return to E&P (Linn Energy, LLC) and Refining(Calumet Specialty Products, L.P.)

18 MLPs (including 8 GP MLPs)

2011 CVR Partners (1st Variable MLP)

2012Hi-Crush (1st Frac Sand MLP)

Wholesale/Retail MLPs

Confidential and Proprietary

Capital Markets

Confidential and Proprietary

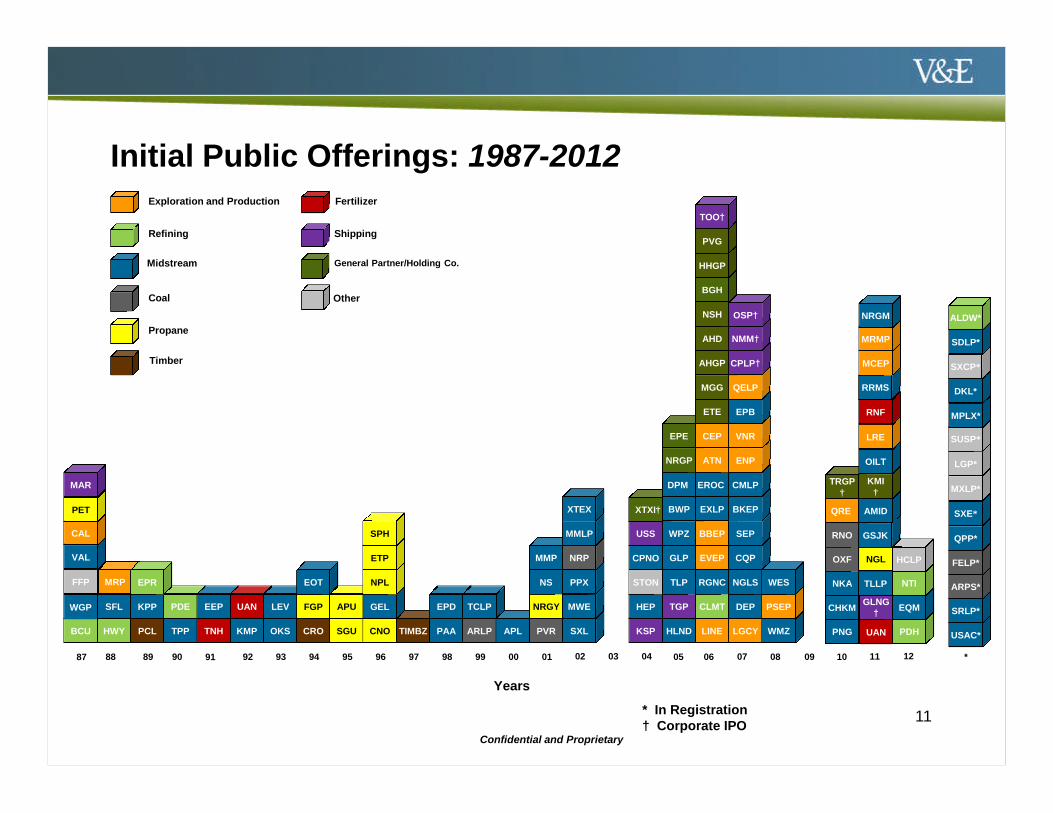

BCU

WGP

* In Registration† Corporate IPO

Years

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

KSP

HEP

STON

CPNO

USS

XTXI†

HWY

SFL

PCL

KPP

TPP

PDE

TNH

EEP

KMP

UAN

OKS

LEV

CRO

FGP

EOT

SGU

APU

CNO

GEL

NPL

ETP

SPH

TIMBZ PAA

EPD

ARLP

TCLP

APL PVR

NRGY

NS

MMP

SXL

MWE

PPX

NRP

MMLP

XTEX

HLND

TGP

TLP

GLP

WPZ

BWP

DPM

NRGP

EPE

LINE

CLMT

RGNC

EVEP

BBEP

EXLP

EROC

ATN

CEP

ETE

MGG

AHGP

AHD

NSH

BGH

HHGP

PVG

TOO†

LGCY

DEP

NGLS

CQP

SEP

BKEP

CMLP

ENP

VNR

EPB

QELP

CPLP†

NMM†

WMZ

PSEP

WES

PNG

CHKM

NKA

OXF

RNO

QRE

UAN

GLNG†

TLLP

NGL

GSJK

AMID

TRGP†

KMI†

OILT

LRE

RNF

RRMS

MCEP

MRMP

PDH

NRGM

Initial Public Offerings: 1987-2012

12

FFP

VAL

CAL

PET

MAR

Exploration and Production

Refining

Midstream

Coal

Propane

Timber

Shipping

Fertilizer

General Partner/Holding Co.

Other

MRP EPR

OSP†

EQM

USAC*

SRLP*

ARPS*

FELP*

QPP*

SXE*

MXLP*

NTI

LGP*

SUSP*

MPLX*

HCLP

DKL*

*

SXCP*

11

SDLP*

ALDW*

Confidential and Proprietary

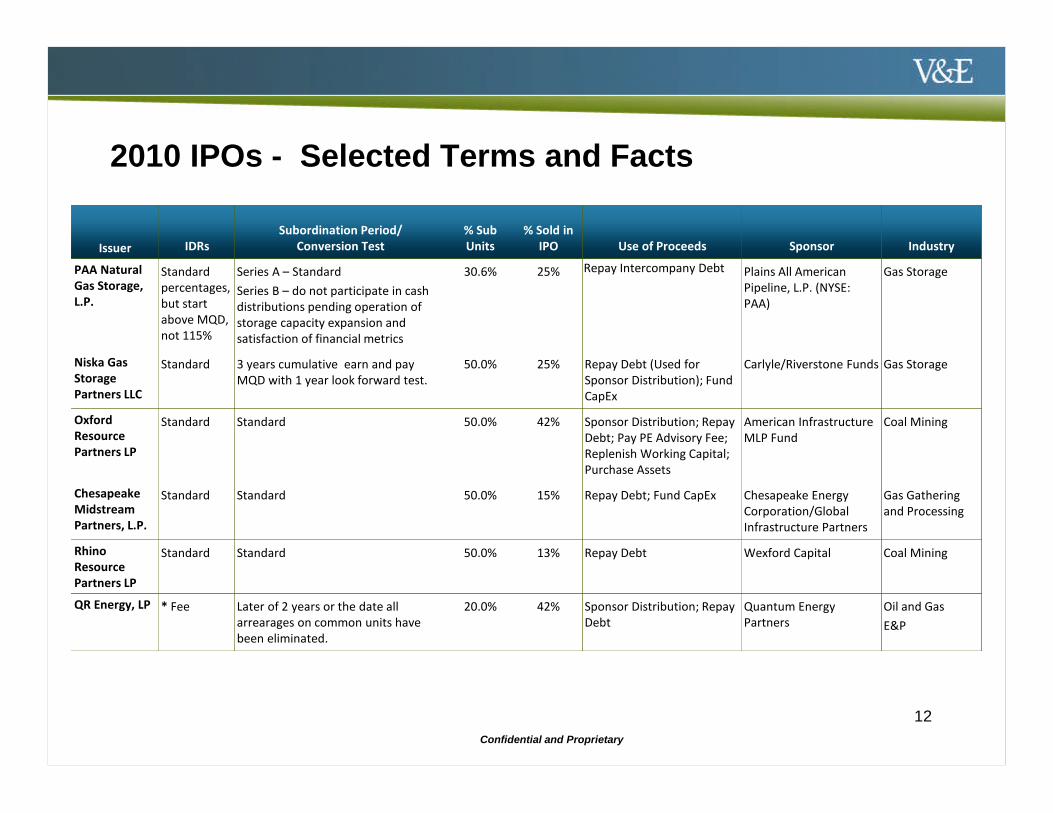

2010 IPOs - Selected Terms and Facts

Issuer IDRsSubordination Period/

Conversion Test% SubUnits

% Sold inIPO Use of Proceeds Sponsor Industry

PAA NaturalGas Storage,L.P.

Standardpercentages,but startabove MQD,not 115%

Series A – Standard

Series B – do not participate in cashdistributions pending operation ofstorage capacity expansion andsatisfaction of financial metrics

30.6% 25% Repay Intercompany Debt Plains All AmericanPipeline, L.P. (NYSE:PAA)

Gas Storage

Niska GasStoragePartners LLC

Standard 3 years cumulative earn and payMQD with 1 year look forward test.

50.0% 25% Repay Debt (Used forSponsor Distribution); FundCapEx

Carlyle/Riverstone Funds Gas Storage

OxfordResourcePartners LP

Standard Standard 50.0% 42% Sponsor Distribution; RepayDebt; Pay PE Advisory Fee;Replenish Working Capital;Purchase Assets

American InfrastructureMLP Fund

Coal Mining

ChesapeakeMidstreamPartners, L.P.

Standard Standard 50.0% 15% Repay Debt; Fund CapEx Chesapeake EnergyCorporation/GlobalInfrastructure Partners

Gas Gatheringand Processing

RhinoResourcePartners LP

Standard Standard 50.0% 13% Repay Debt Wexford Capital Coal Mining

QR Energy, LP * Fee Later of 2 years or the date allarrearages on common units havebeen eliminated.

20.0% 42% Sponsor Distribution; RepayDebt

Quantum EnergyPartners

Oil and Gas

E&P

12

Confidential and Proprietary

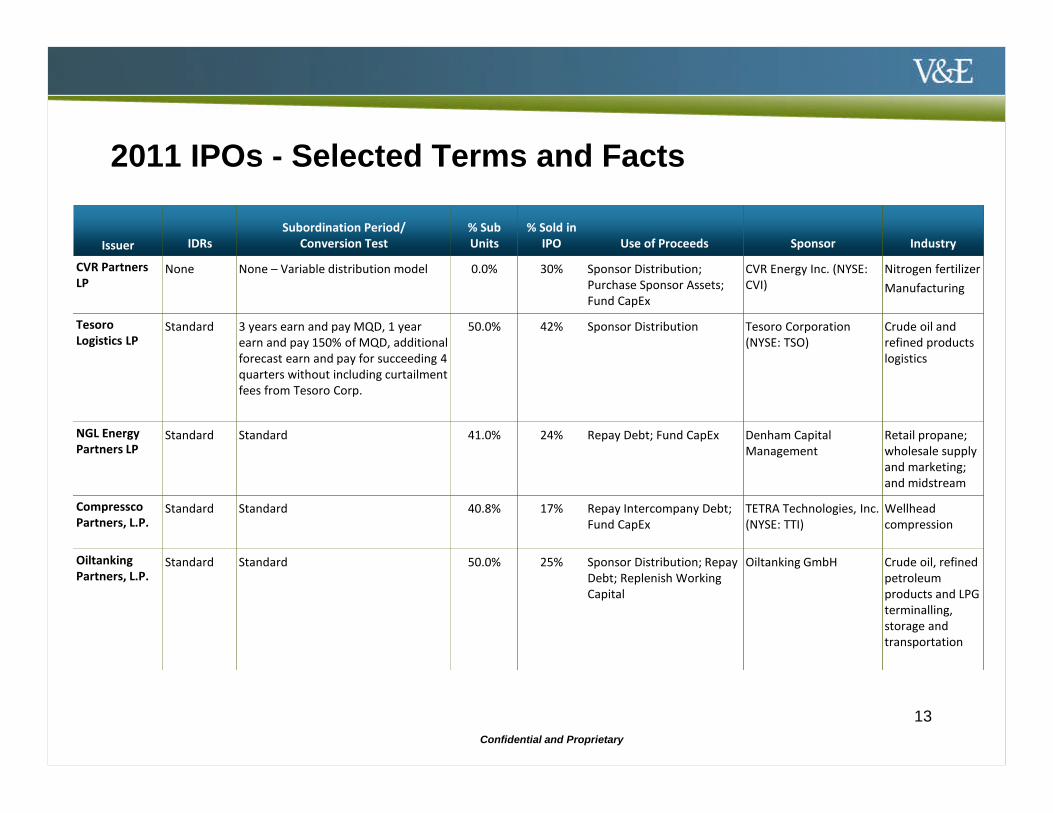

2011 IPOs - Selected Terms and Facts

Issuer IDRsSubordination Period/

Conversion Test% SubUnits

% Sold inIPO Use of Proceeds Sponsor Industry

CVR PartnersLP

None None – Variable distribution model 0.0% 30% Sponsor Distribution;Purchase Sponsor Assets;Fund CapEx

CVR Energy Inc. (NYSE:CVI)

Nitrogen fertilizer

Manufacturing

TesoroLogistics LP

Standard 3 years earn and pay MQD, 1 yearearn and pay 150% of MQD, additionalforecast earn and pay for succeeding 4quarters without including curtailmentfees from Tesoro Corp.

50.0% 42% Sponsor Distribution Tesoro Corporation(NYSE: TSO)

Crude oil andrefined productslogistics

NGL EnergyPartners LP

Standard Standard 41.0% 24% Repay Debt; Fund CapEx Denham CapitalManagement

Retail propane;wholesale supplyand marketing;and midstream

CompresscoPartners, L.P.

Standard Standard 40.8% 17% Repay Intercompany Debt;Fund CapEx

TETRA Technologies, Inc.(NYSE: TTI)

Wellheadcompression

OiltankingPartners, L.P.

Standard Standard 50.0% 25% Sponsor Distribution; RepayDebt; Replenish WorkingCapital

Oiltanking GmbH Crude oil, refinedpetroleumproducts and LPGterminalling,storage andtransportation

13

Confidential and Proprietary

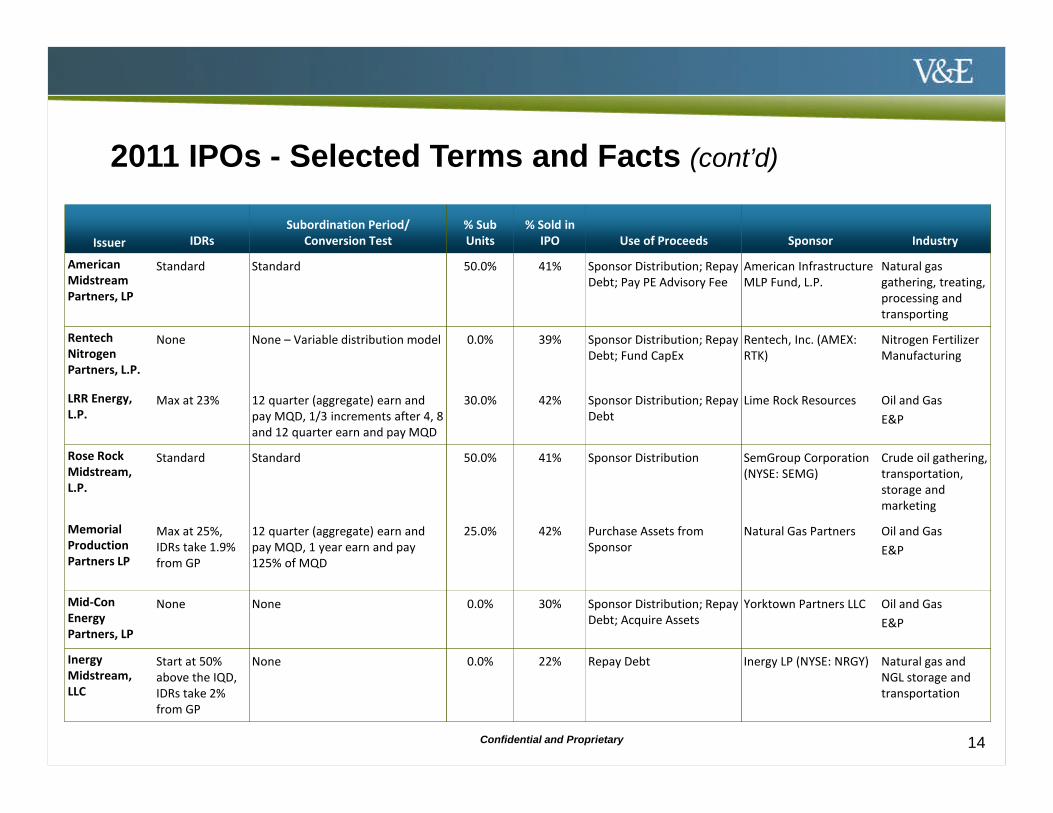

Issuer IDRsSubordination Period/

Conversion Test% SubUnits

% Sold inIPO Use of Proceeds Sponsor Industry

AmericanMidstreamPartners, LP

Standard Standard 50.0% 41% Sponsor Distribution; RepayDebt; Pay PE Advisory Fee

American InfrastructureMLP Fund, L.P.

Natural gasgathering, treating,processing andtransporting

RentechNitrogenPartners, L.P.

None None – Variable distribution model 0.0% 39% Sponsor Distribution; RepayDebt; Fund CapEx

Rentech, Inc. (AMEX:RTK)

Nitrogen FertilizerManufacturing

LRR Energy,L.P.

Max at 23% 12 quarter (aggregate) earn andpay MQD, 1/3 increments after 4, 8and 12 quarter earn and pay MQD

30.0% 42% Sponsor Distribution; RepayDebt

Lime Rock Resources Oil and Gas

E&P

Rose RockMidstream,L.P.

Standard Standard 50.0% 41% Sponsor Distribution SemGroup Corporation(NYSE: SEMG)

Crude oil gathering,transportation,storage andmarketing

MemorialProductionPartners LP

Max at 25%,IDRs take 1.9%from GP

12 quarter (aggregate) earn andpay MQD, 1 year earn and pay125% of MQD

25.0% 42% Purchase Assets fromSponsor

Natural Gas Partners Oil and Gas

E&P

Mid-ConEnergyPartners, LP

None None 0.0% 30% Sponsor Distribution; RepayDebt; Acquire Assets

Yorktown Partners LLC Oil and Gas

E&P

InergyMidstream,LLC

Start at 50%above the IQD,IDRs take 2%from GP

None 0.0% 22% Repay Debt Inergy LP (NYSE: NRGY) Natural gas andNGL storage andtransportation

14

2011 IPOs - Selected Terms and Facts (cont’d)

Confidential and Proprietary

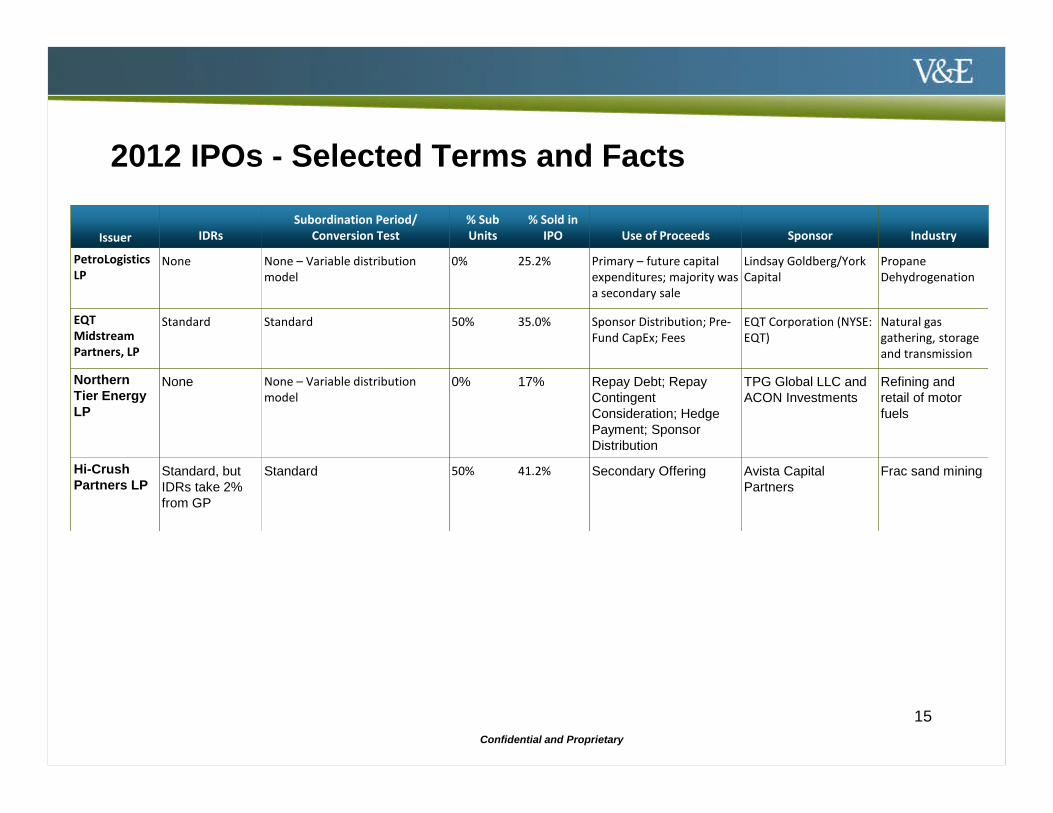

2012 IPOs - Selected Terms and Facts

Issuer IDRsSubordination Period/

Conversion Test% SubUnits

% Sold inIPO Use of Proceeds Sponsor Industry

PetroLogisticsLP

None None – Variable distributionmodel

0% 25.2% Primary – future capitalexpenditures; majority wasa secondary sale

Lindsay Goldberg/YorkCapital

PropaneDehydrogenation

EQTMidstreamPartners, LP

Standard Standard 50% 35.0% Sponsor Distribution; Pre-Fund CapEx; Fees

EQT Corporation (NYSE:EQT)

Natural gasgathering, storageand transmission

NorthernTier EnergyLP

None None – Variable distributionmodel

0% 17% Repay Debt; RepayContingentConsideration; HedgePayment; SponsorDistribution

TPG Global LLC andACON Investments

Refining andretail of motorfuels

Hi-CrushPartners LP

Standard, butIDRs take 2%from GP

Standard 50% 41.2% Secondary Offering Avista CapitalPartners

Frac sand mining

15

Confidential and Proprietary

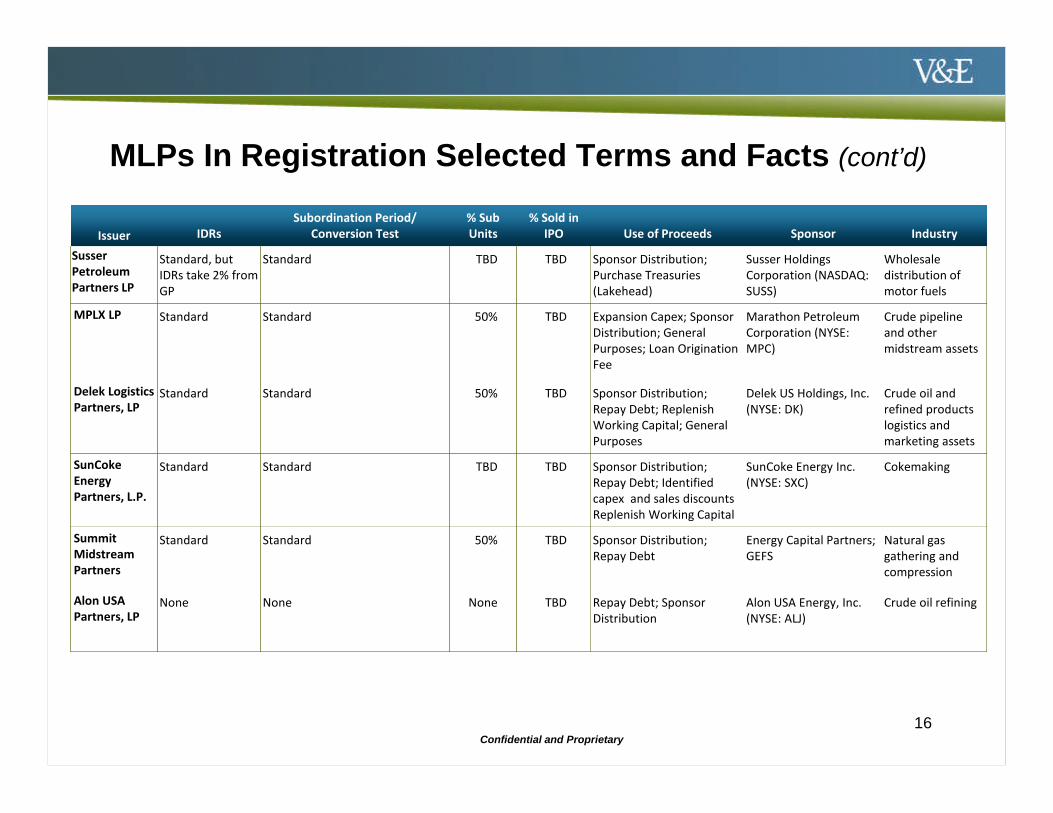

MLPs In Registration Selected Terms and Facts (cont’d)

Issuer IDRsSubordination Period/

Conversion Test% SubUnits

% Sold inIPO Use of Proceeds Sponsor Industry

SusserPetroleumPartners LP

Standard, butIDRs take 2% fromGP

Standard TBD TBD Sponsor Distribution;Purchase Treasuries(Lakehead)

Susser HoldingsCorporation (NASDAQ:SUSS)

Wholesaledistribution ofmotor fuels

MPLX LP Standard Standard 50% TBD Expansion Capex; SponsorDistribution; GeneralPurposes; Loan OriginationFee

Marathon PetroleumCorporation (NYSE:MPC)

Crude pipelineand othermidstream assets

Delek LogisticsPartners, LP

Standard Standard 50% TBD Sponsor Distribution;Repay Debt; ReplenishWorking Capital; GeneralPurposes

Delek US Holdings, Inc.(NYSE: DK)

Crude oil andrefined productslogistics andmarketing assets

SunCokeEnergyPartners, L.P.

Standard Standard TBD TBD Sponsor Distribution;Repay Debt; Identifiedcapex and sales discountsReplenish Working Capital

SunCoke Energy Inc.(NYSE: SXC)

Cokemaking

SummitMidstreamPartners

Standard Standard 50% TBD Sponsor Distribution;Repay Debt

Energy Capital Partners;GEFS

Natural gasgathering andcompression

Alon USAPartners, LP

None None None TBD Repay Debt; SponsorDistribution

Alon USA Energy, Inc.(NYSE: ALJ)

Crude oil refining

16

Confidential and Proprietary

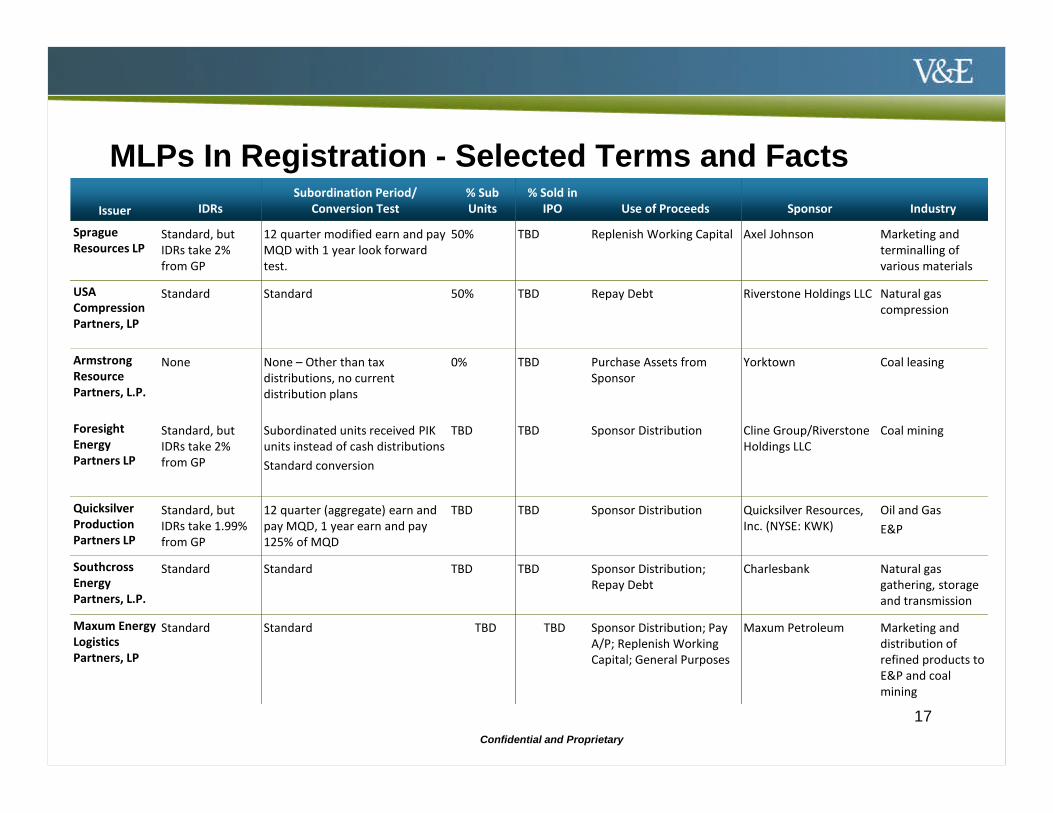

MLPs In Registration - Selected Terms and Facts

17

Issuer IDRsSubordination Period/

Conversion Test% SubUnits

% Sold inIPO Use of Proceeds Sponsor Industry

SpragueResources LP

Standard, butIDRs take 2%from GP

12 quarter modified earn and payMQD with 1 year look forwardtest.

50% TBD Replenish Working Capital Axel Johnson Marketing andterminalling ofvarious materials

USACompressionPartners, LP

Standard Standard 50% TBD Repay Debt Riverstone Holdings LLC Natural gascompression

ArmstrongResourcePartners, L.P.

None None – Other than taxdistributions, no currentdistribution plans

0% TBD Purchase Assets fromSponsor

Yorktown Coal leasing

ForesightEnergyPartners LP

Standard, butIDRs take 2%from GP

Subordinated units received PIKunits instead of cash distributions

Standard conversion

TBD TBD Sponsor Distribution Cline Group/RiverstoneHoldings LLC

Coal mining

QuicksilverProductionPartners LP

Standard, butIDRs take 1.99%from GP

12 quarter (aggregate) earn andpay MQD, 1 year earn and pay125% of MQD

TBD TBD Sponsor Distribution Quicksilver Resources,Inc. (NYSE: KWK)

Oil and Gas

E&P

SouthcrossEnergyPartners, L.P.

Standard Standard TBD TBD Sponsor Distribution;Repay Debt

Charlesbank Natural gasgathering, storageand transmission

Maxum EnergyLogisticsPartners, LP

Standard Standard TBD TBD Sponsor Distribution; PayA/P; Replenish WorkingCapital; General Purposes

Maxum Petroleum Marketing anddistribution ofrefined products toE&P and coalmining

Confidential and Proprietary

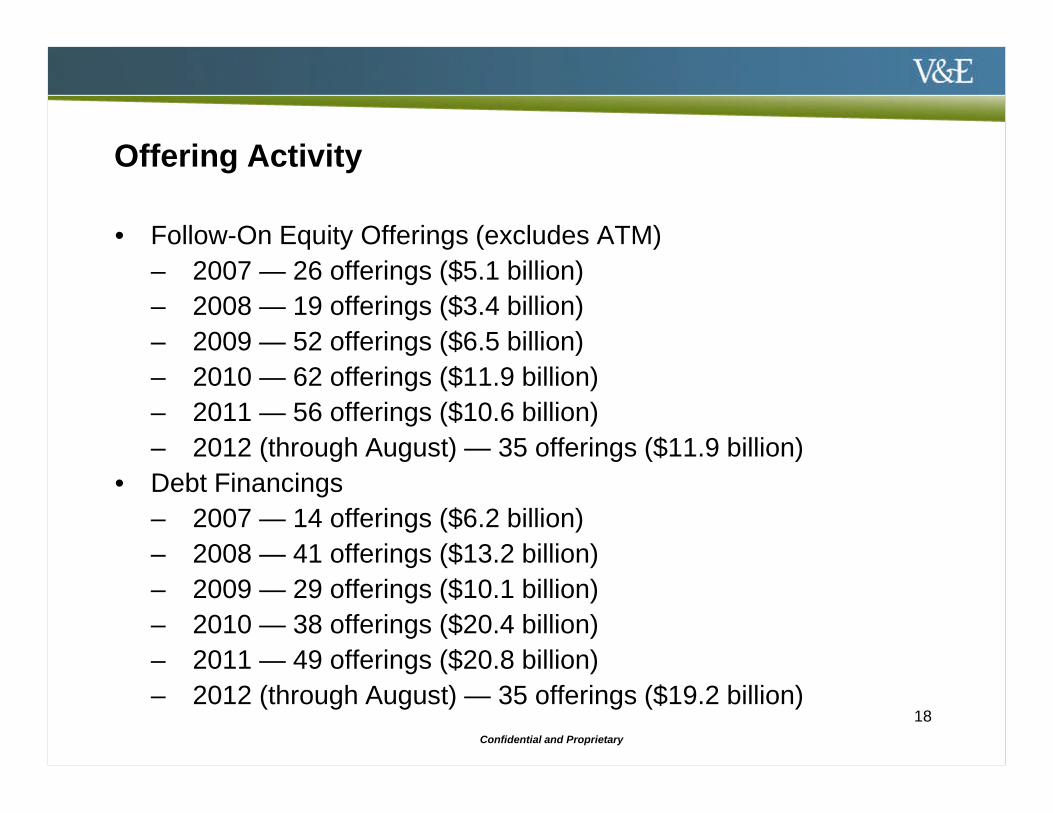

• Follow-On Equity Offerings (excludes ATM)

– 2007 — 26 offerings ($5.1 billion)

– 2008 — 19 offerings ($3.4 billion)

– 2009 — 52 offerings ($6.5 billion)

– 2010 — 62 offerings ($11.9 billion)

– 2011 — 56 offerings ($10.6 billion)

– 2012 (through August) — 35 offerings ($11.9 billion)

• Debt Financings

– 2007 — 14 offerings ($6.2 billion)

– 2008 — 41 offerings ($13.2 billion)

– 2009 — 29 offerings ($10.1 billion)

– 2010 — 38 offerings ($20.4 billion)

– 2011 — 49 offerings ($20.8 billion)

– 2012 (through August) — 35 offerings ($19.2 billion)

Offering Activity

18

Confidential and Proprietary

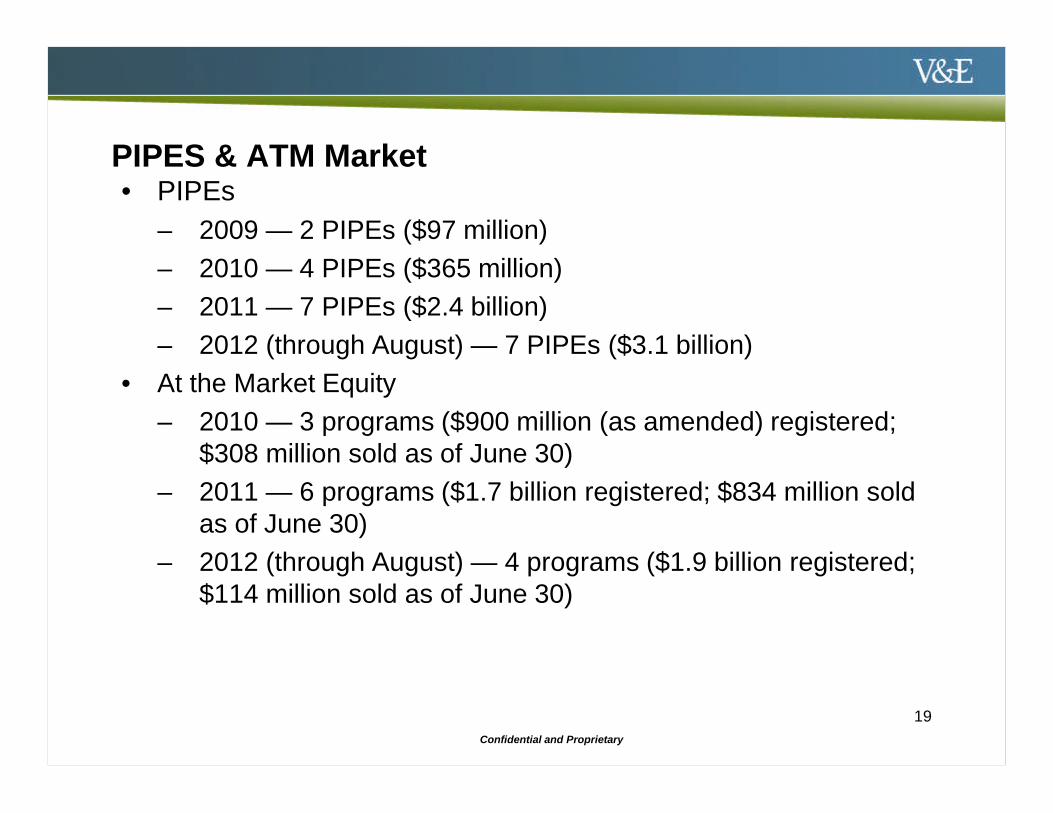

• PIPEs

– 2009 — 2 PIPEs ($97 million)

– 2010 — 4 PIPEs ($365 million)

– 2011 — 7 PIPEs ($2.4 billion)

– 2012 (through August) — 7 PIPEs ($3.1 billion)

• At the Market Equity

– 2010 — 3 programs ($900 million (as amended) registered;$308 million sold as of June 30)

– 2011 — 6 programs ($1.7 billion registered; $834 million soldas of June 30)

– 2012 (through August) — 4 programs ($1.9 billion registered;$114 million sold as of June 30)

PIPES & ATM Market

19

Confidential and Proprietary

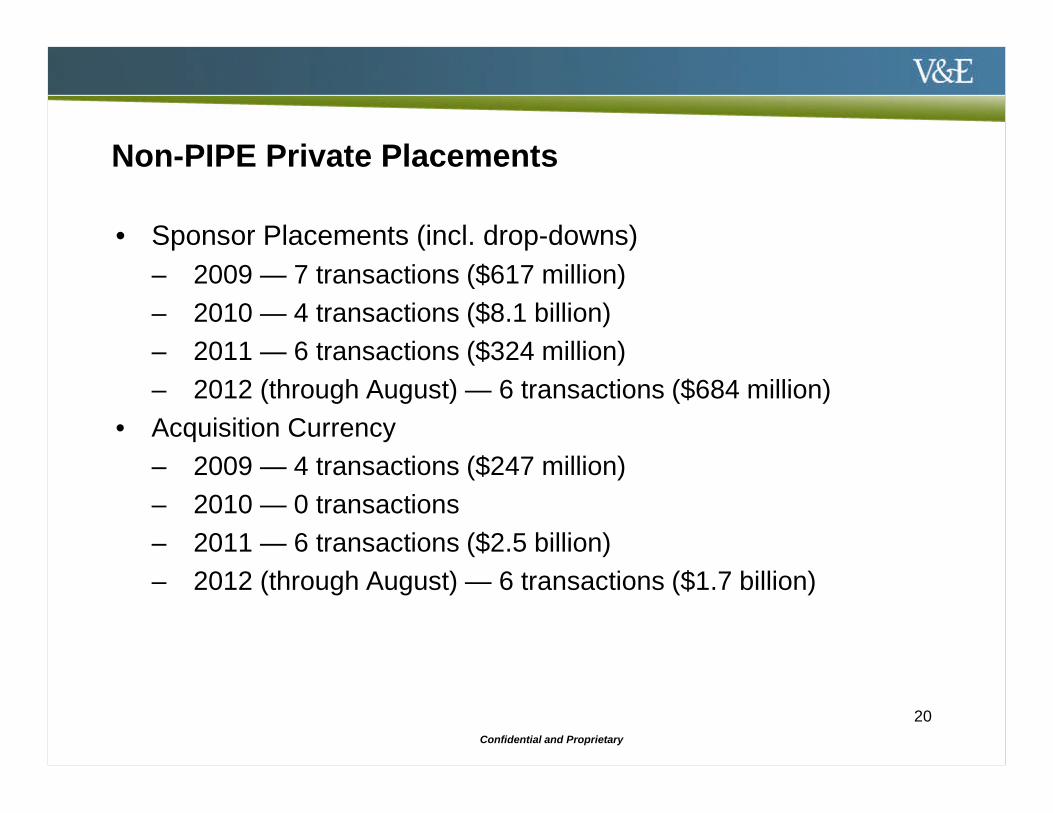

• Sponsor Placements (incl. drop-downs)

– 2009 — 7 transactions ($617 million)

– 2010 — 4 transactions ($8.1 billion)

– 2011 — 6 transactions ($324 million)

– 2012 (through August) — 6 transactions ($684 million)

• Acquisition Currency

– 2009 — 4 transactions ($247 million)

– 2010 — 0 transactions

– 2011 — 6 transactions ($2.5 billion)

– 2012 (through August) — 6 transactions ($1.7 billion)

Non-PIPE Private Placements

20

Confidential and Proprietary

Traditional Structure

Confidential and Proprietary

22

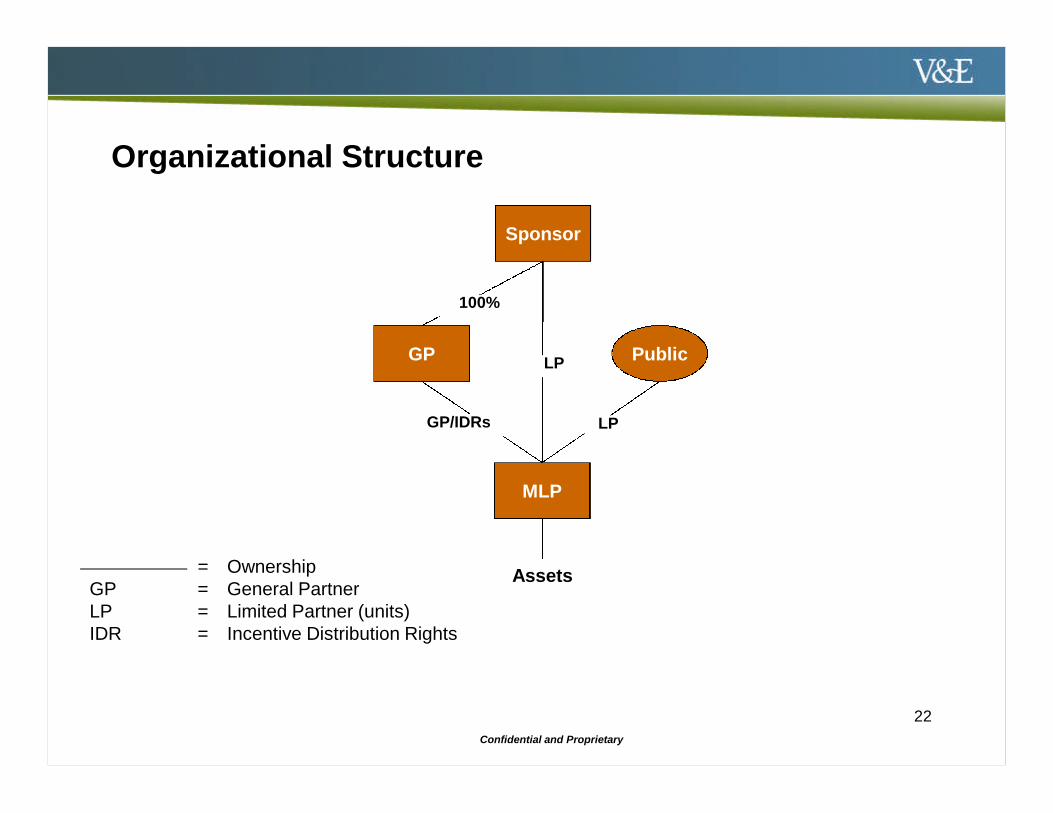

Organizational Structure

Sponsor

MLP

Public

LP

Assets= OwnershipGP = General PartnerLP = Limited Partner (units)IDR = Incentive Distribution Rights

GP LP

GP/IDRs

100%

Confidential and Proprietary

Economic Structure (Traditional MLP)

Key Concepts

• Distribution Policy

• Minimum Quarterly Distribution (“MQD”)

• Subordinated Units – Form of Distribution Support

• Incentive Distribution Rights (“IDRs”)

23

Confidential and Proprietary

24

Economic Structure (cont’d)

Distribution Policy

• The MLP’s goal is to generate stable (and increasing) cashdistributions to unitholders

• In the prospectus, the MLP makes a statement as to itsintention to distribute a specified minimum level ofdistributions on a quarterly basis (the “MQD”)

– Basis for yield at which the MLP is marketed and sold

– Basis for distribution support

– Starting point for IDRs

• Partnership agreement typically requires (in a very loosesense) distribution of 100% of “Available Cash”

• Distributions are not a tax requirement

Confidential and Proprietary

25

Economic Structure (cont’d)

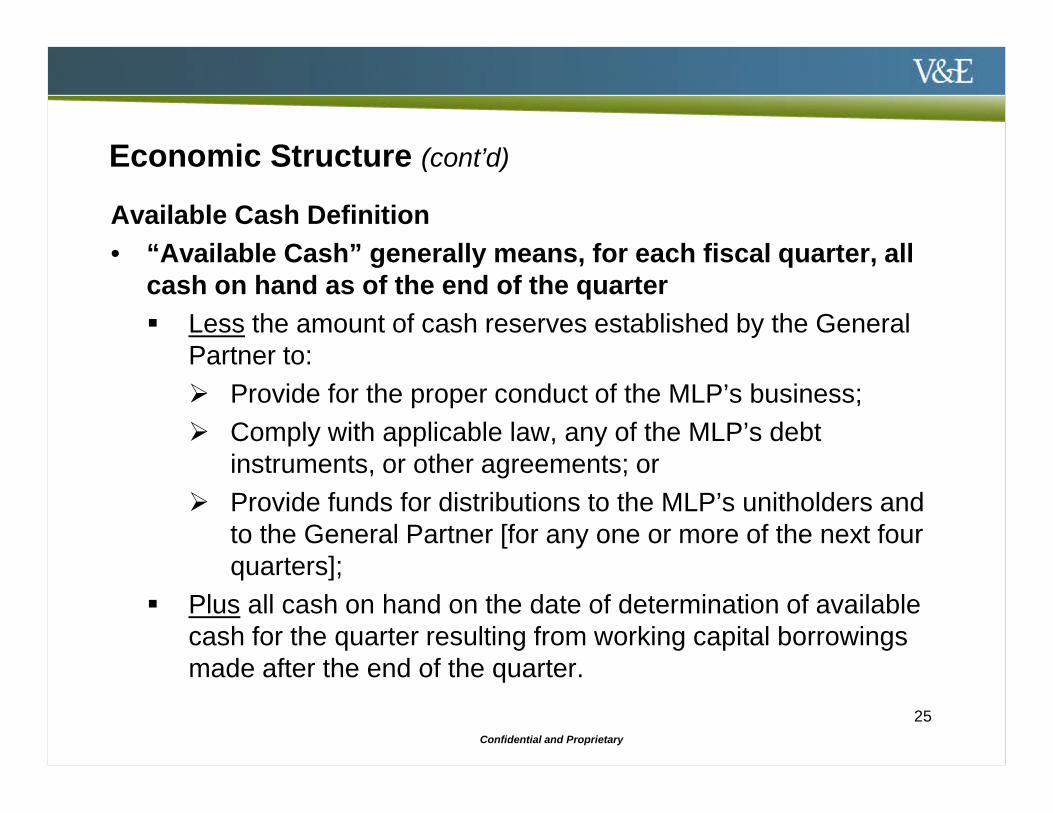

Available Cash Definition

• “Available Cash” generally means, for each fiscal quarter, allcash on hand as of the end of the quarter

Less the amount of cash reserves established by the GeneralPartner to:

Provide for the proper conduct of the MLP’s business;

Comply with applicable law, any of the MLP’s debtinstruments, or other agreements; or

Provide funds for distributions to the MLP’s unitholders andto the General Partner [for any one or more of the next fourquarters];

Plus all cash on hand on the date of determination of availablecash for the quarter resulting from working capital borrowingsmade after the end of the quarter.

Confidential and Proprietary

26

Economic Structure (cont’d)

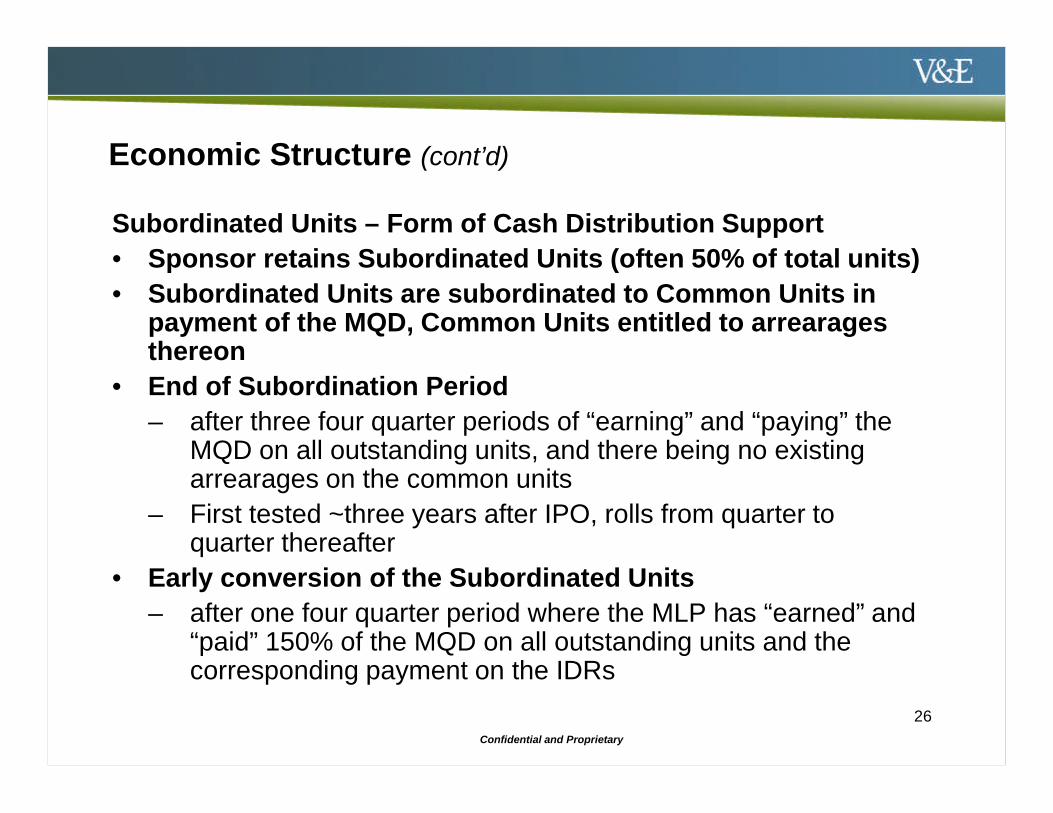

Subordinated Units – Form of Cash Distribution Support

• Sponsor retains Subordinated Units (often 50% of total units)

• Subordinated Units are subordinated to Common Units inpayment of the MQD, Common Units entitled to arrearagesthereon

• End of Subordination Period

– after three four quarter periods of “earning” and “paying” theMQD on all outstanding units, and there being no existingarrearages on the common units

– First tested ~three years after IPO, rolls from quarter toquarter thereafter

• Early conversion of the Subordinated Units

– after one four quarter period where the MLP has “earned” and“paid” 150% of the MQD on all outstanding units and thecorresponding payment on the IDRs

Confidential and Proprietary

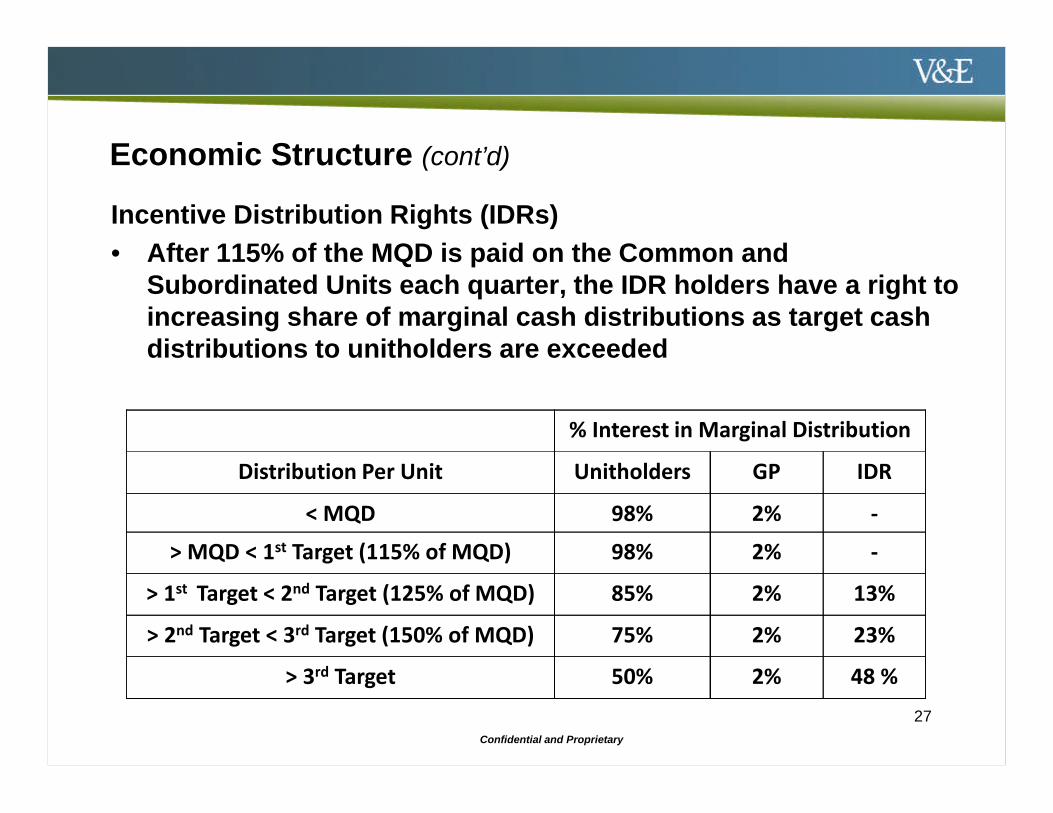

27

Economic Structure (cont’d)

Incentive Distribution Rights (IDRs)

• After 115% of the MQD is paid on the Common andSubordinated Units each quarter, the IDR holders have a right toincreasing share of marginal cash distributions as target cashdistributions to unitholders are exceeded

% Interest in Marginal Distribution

Distribution Per Unit Unitholders GP IDR

< MQD 98% 2% -

> MQD < 1st Target (115% of MQD) 98% 2% -

> 1st Target < 2nd Target (125% of MQD) 85% 2% 13%

> 2nd Target < 3rd Target (150% of MQD) 75% 2% 23%

> 3rd Target 50% 2% 48 %

Confidential and Proprietary

28

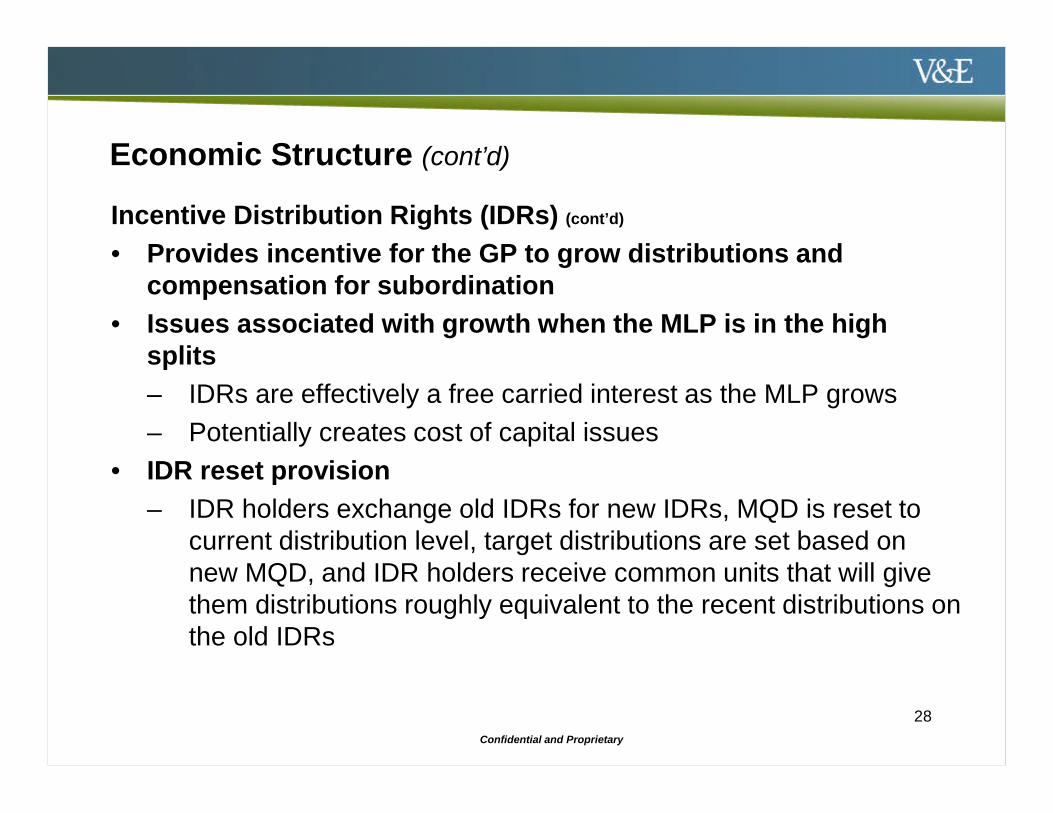

Economic Structure (cont’d)

Incentive Distribution Rights (IDRs) (cont’d)

• Provides incentive for the GP to grow distributions andcompensation for subordination

• Issues associated with growth when the MLP is in the highsplits

– IDRs are effectively a free carried interest as the MLP grows

– Potentially creates cost of capital issues

• IDR reset provision

– IDR holders exchange old IDRs for new IDRs, MQD is reset tocurrent distribution level, target distributions are set based onnew MQD, and IDR holders receive common units that will givethem distributions roughly equivalent to the recent distributions onthe old IDRs

Confidential and Proprietary

Governance &Accounting Issues

Confidential and Proprietary

30

Governance

General Partner controls the MLP

• General Partner is typically 100% owned by the sponsor

• Executive officers of the sponsor are typically designated toserve as executive officers of the MLP

Executive officers of the MLP may devote 100% of their timeto the MLP or may continue to be involved with otherbusinesses of the sponsor

• Often, the MLP and the General Partner of the MLP have noemployees

Employees can be retained by the sponsor and the allocableshare of salaries and benefits of these employees reimbursedto the sponsor by the MLP

The General Partner typically establishes new equity incentiveplans to incent employees who devote a substantial portion oftheir time to the MLP’s affairs

Confidential and Proprietary

31

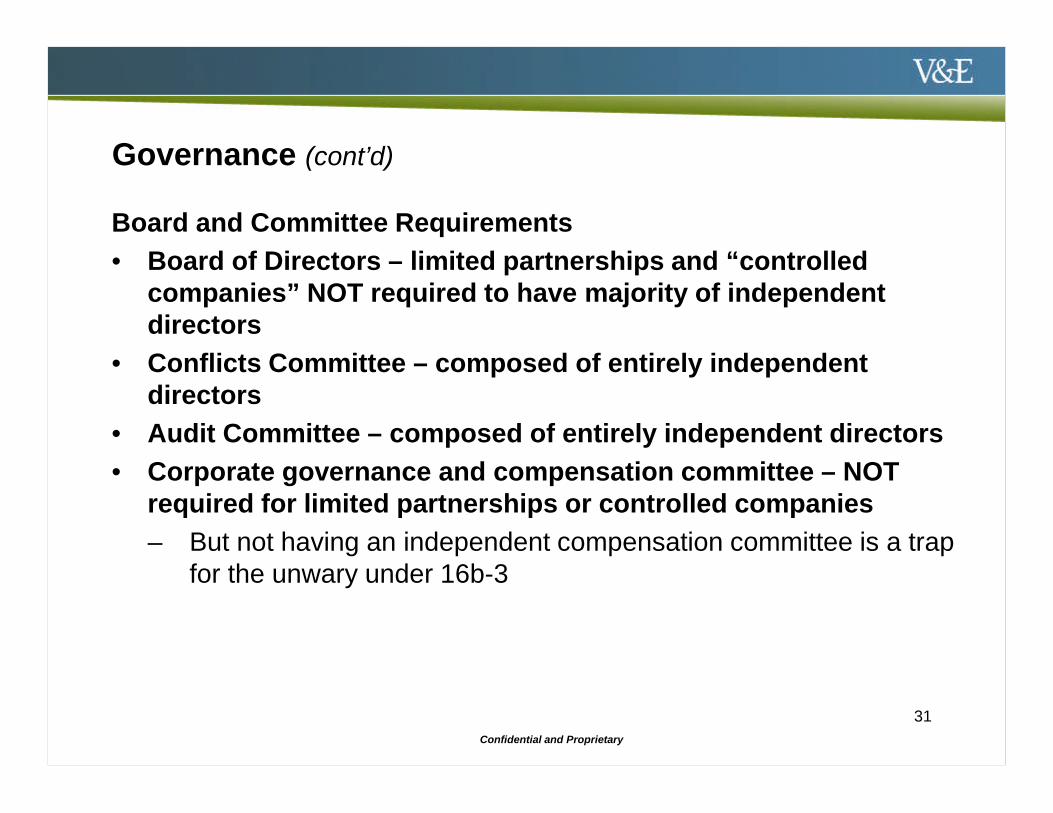

Governance (cont’d)

Board and Committee Requirements

• Board of Directors – limited partnerships and “controlledcompanies” NOT required to have majority of independentdirectors

• Conflicts Committee – composed of entirely independentdirectors

• Audit Committee – composed of entirely independent directors

• Corporate governance and compensation committee – NOTrequired for limited partnerships or controlled companies

– But not having an independent compensation committee is a trapfor the unwary under 16b-3

Confidential and Proprietary

32

Governance (cont’d)

Voting Rights of Limited Partners

• Limited Partners Do Not Elect Directors of the General Partner

– As a result, most MLPs do not have annual meetings of unitholders

– BreitBurn, Buckeye, Copano, Linn, Magellan, MarkWest, Suburbanand certain shipping MLPs are among the exceptions

• Limited Partners Vote only on Strategic Events

– Sale of all or substantially all assets

– Removal of the General Partner (upon the vote of at least 66-2/3% ofall outstanding common units and subordinated units (if any), votingtogether as a class, including units owned by the General Partnerand its affiliates)

– Certain material amendments to partnership agreement

Confidential and Proprietary

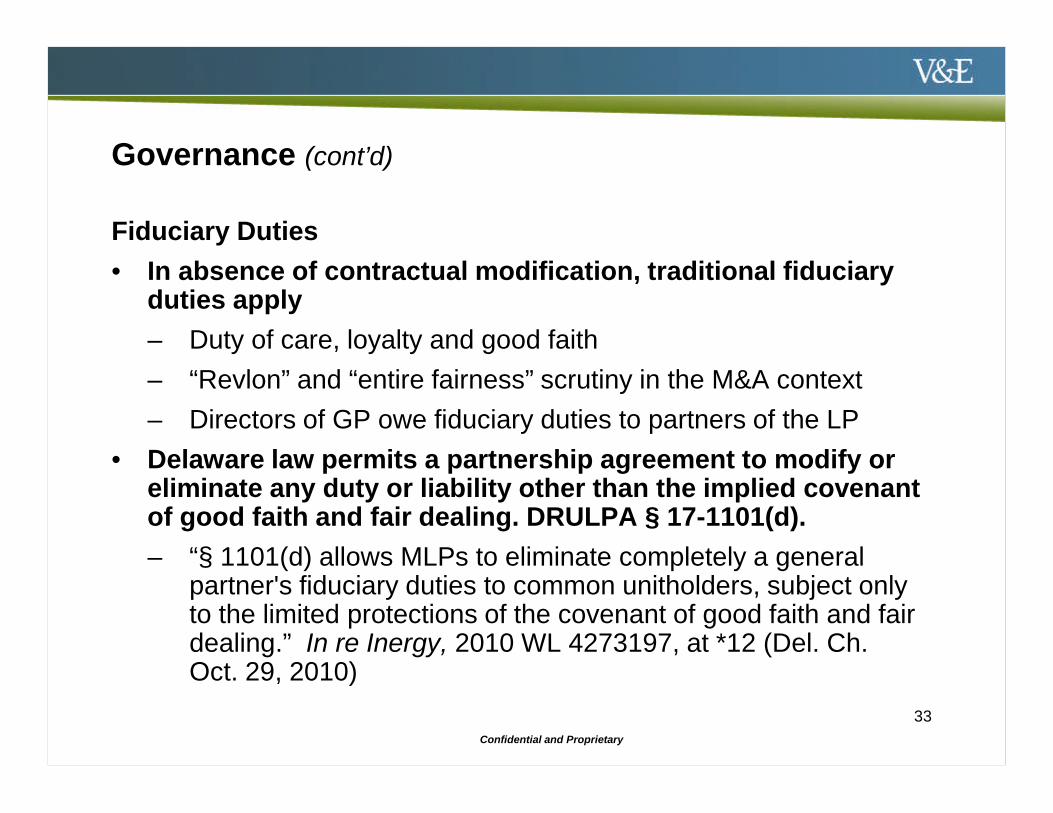

Governance (cont’d)

Fiduciary Duties

• In absence of contractual modification, traditional fiduciaryduties apply

– Duty of care, loyalty and good faith

– “Revlon” and “entire fairness” scrutiny in the M&A context

– Directors of GP owe fiduciary duties to partners of the LP

• Delaware law permits a partnership agreement to modify oreliminate any duty or liability other than the implied covenantof good faith and fair dealing. DRULPA § 17-1101(d).

– “§ 1101(d) allows MLPs to eliminate completely a generalpartner's fiduciary duties to common unitholders, subject onlyto the limited protections of the covenant of good faith and fairdealing.” In re Inergy, 2010 WL 4273197, at *12 (Del. Ch.Oct. 29, 2010)

33

Confidential and Proprietary

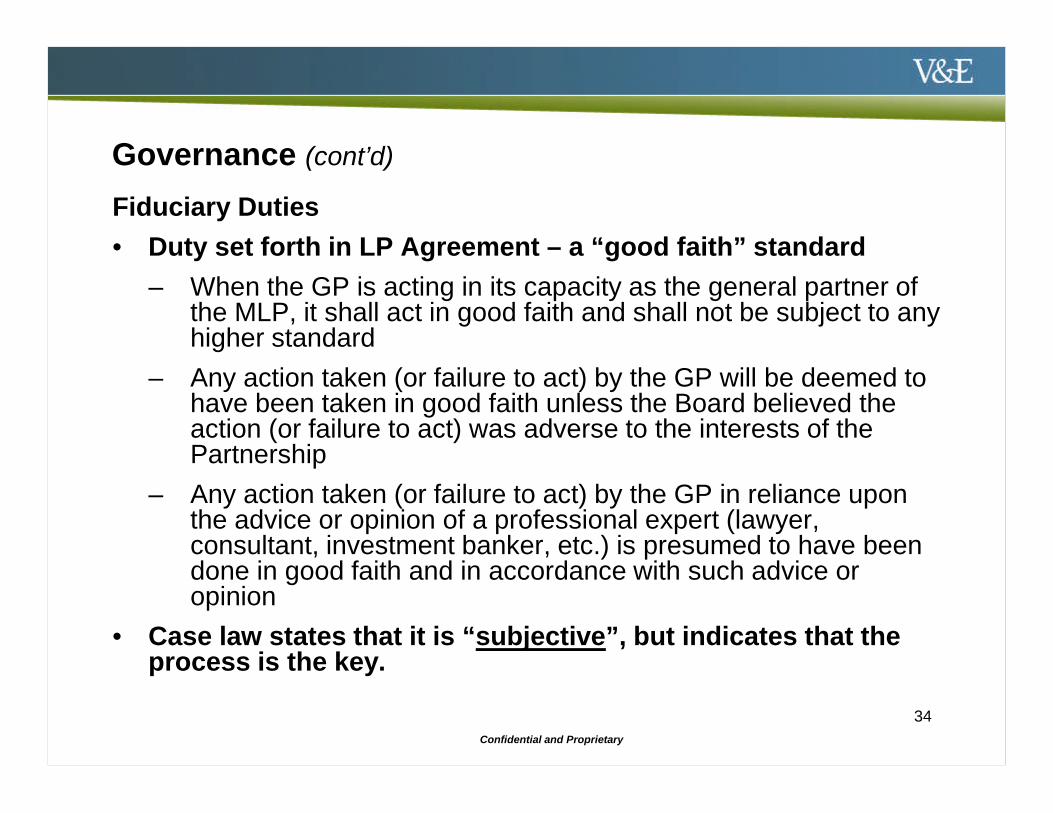

Governance (cont’d)

Fiduciary Duties

• Duty set forth in LP Agreement – a “good faith” standard

– When the GP is acting in its capacity as the general partner ofthe MLP, it shall act in good faith and shall not be subject to anyhigher standard

– Any action taken (or failure to act) by the GP will be deemed tohave been taken in good faith unless the Board believed theaction (or failure to act) was adverse to the interests of thePartnership

– Any action taken (or failure to act) by the GP in reliance uponthe advice or opinion of a professional expert (lawyer,consultant, investment banker, etc.) is presumed to have beendone in good faith and in accordance with such advice oropinion

• Case law states that it is “subjective”, but indicates that theprocess is the key.

34

Confidential and Proprietary

35

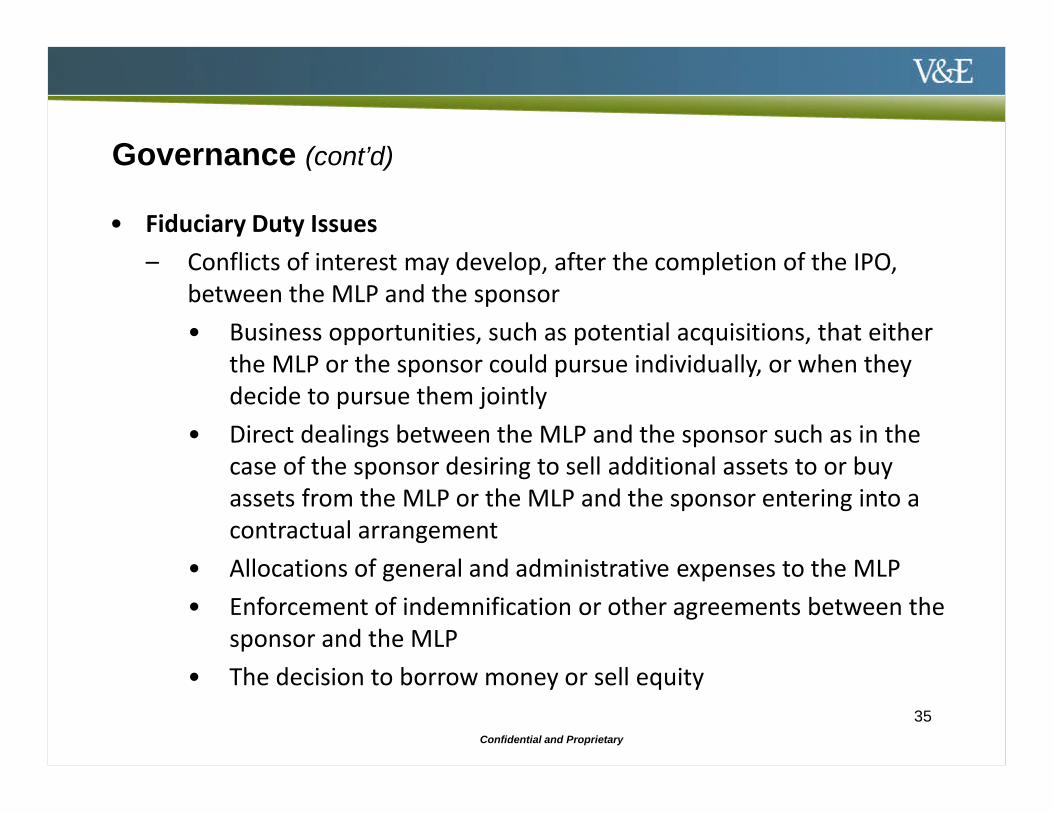

Governance (cont’d)

• Fiduciary Duty Issues

– Conflicts of interest may develop, after the completion of the IPO,between the MLP and the sponsor

• Business opportunities, such as potential acquisitions, that eitherthe MLP or the sponsor could pursue individually, or when theydecide to pursue them jointly

• Direct dealings between the MLP and the sponsor such as in thecase of the sponsor desiring to sell additional assets to or buyassets from the MLP or the MLP and the sponsor entering into acontractual arrangement

• Allocations of general and administrative expenses to the MLP

• Enforcement of indemnification or other agreements between thesponsor and the MLP

• The decision to borrow money or sell equity

Confidential and Proprietary

36

Governance (cont’d)

• The partnership agreement will contain other conflict ofinterest resolution procedures, which typically provide thatthe General Partner will not be in breach of its fiduciary dutyto the MLP or its unitholders if the resolution of the conflictis

– Approved by the Conflicts Committee of the General Partner(a committee comprised entirely of directors who areindependent from the sponsor); or

– Approved by the vote of a majority of the outstanding commonunits, excluding any common units owned by the GeneralPartner or any of its affiliates

Confidential and Proprietary

37

Governance (cont’d)

• Many MLPs enter into an Omnibus Agreement with thesponsor that, among other matters, specifies variousprocedures to deal with potential conflicts

– These provisions typically include non-compete provisionsthat require, at a minimum, the sponsor to allow the MLP thefirst opportunity to pursue an acquisition of a business that isin the same line of business as the MLP or a designatedgeographic area

– These provisions often also give the MLP a right of firstrefusal to purchase any assets of the sponsor that thesponsor is interested in selling if the assets are in the sameline of business as the MLP or a designated geographic area

Confidential and Proprietary

38

Accounting Issues

• Generally Required for all IPOs

– Audited Financial Statements

Three years’ income statement (or two for EmergingGrowth Companies)

Two years’ balance sheet

– Unaudited financial statements for any stub period

– Five years of selected financial data

• Special Requirements for MLP IPOs

– Cash Distribution Forecast (ability to pay first year’s MQD)

– Cash Distribution Backcast (pro forma ability to have paidMQD during the last year)

• Where MLP succeeds to some, but not all, of a sponsor’sbusiness, carve-out financials may be appropriate

– Preclearance letter to SEC’s Office of the Chief Accountant

Confidential and Proprietary

Qualifying Income

Confidential and Proprietary

40

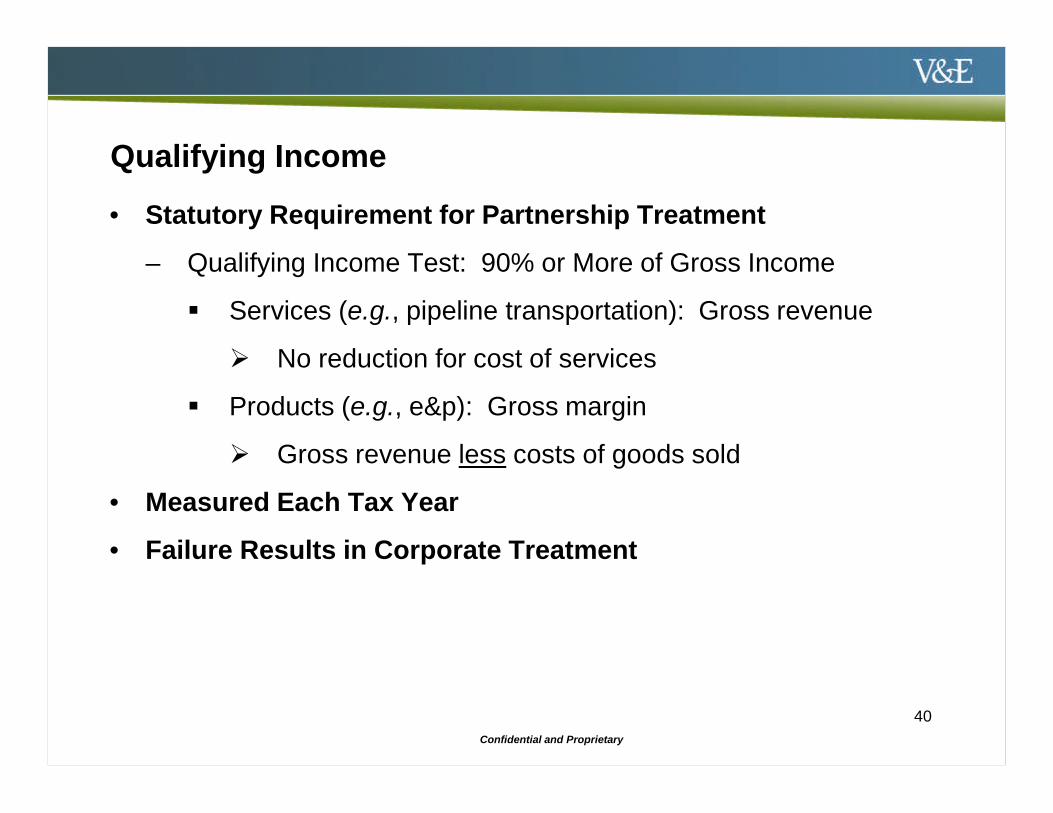

Qualifying Income

• Statutory Requirement for Partnership Treatment

– Qualifying Income Test: 90% or More of Gross Income

Services (e.g., pipeline transportation): Gross revenue

No reduction for cost of services

Products (e.g., e&p): Gross margin

Gross revenue less costs of goods sold

• Measured Each Tax Year

• Failure Results in Corporate Treatment

Confidential and Proprietary

41

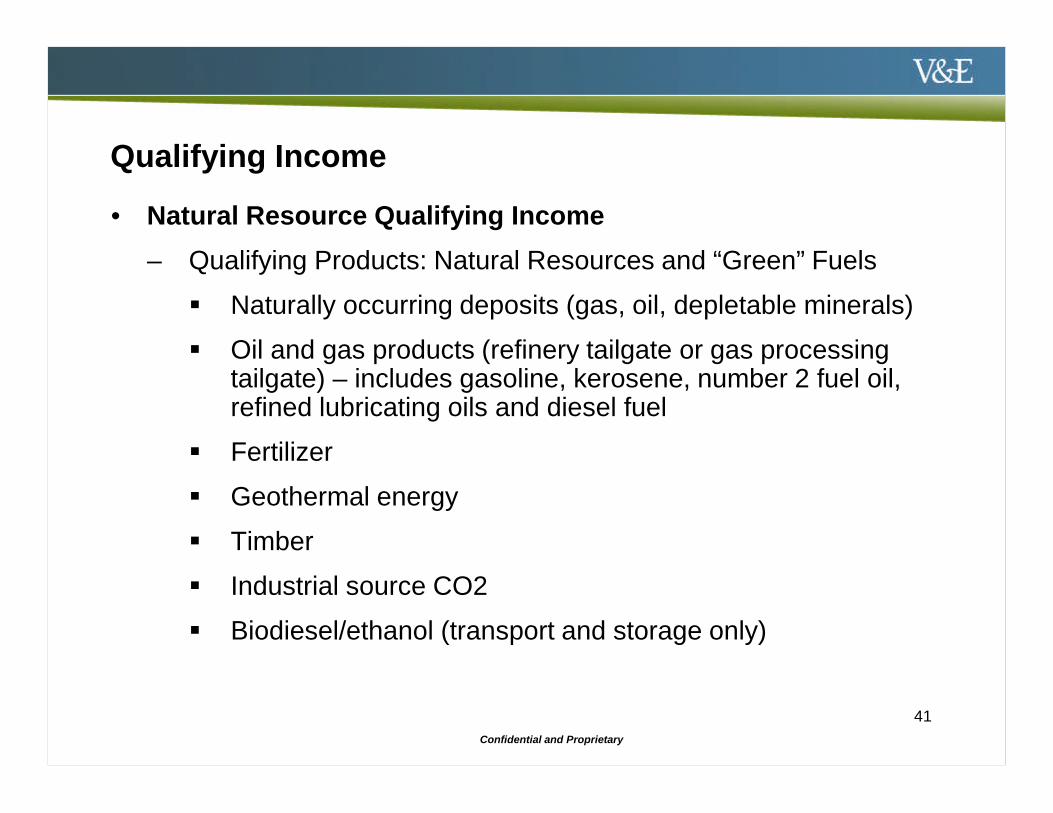

Qualifying Income

• Natural Resource Qualifying Income

– Qualifying Products: Natural Resources and “Green” Fuels

Naturally occurring deposits (gas, oil, depletable minerals)

Oil and gas products (refinery tailgate or gas processingtailgate) – includes gasoline, kerosene, number 2 fuel oil,refined lubricating oils and diesel fuel

Fertilizer

Geothermal energy

Timber

Industrial source CO2

Biodiesel/ethanol (transport and storage only)

Confidential and Proprietary

42

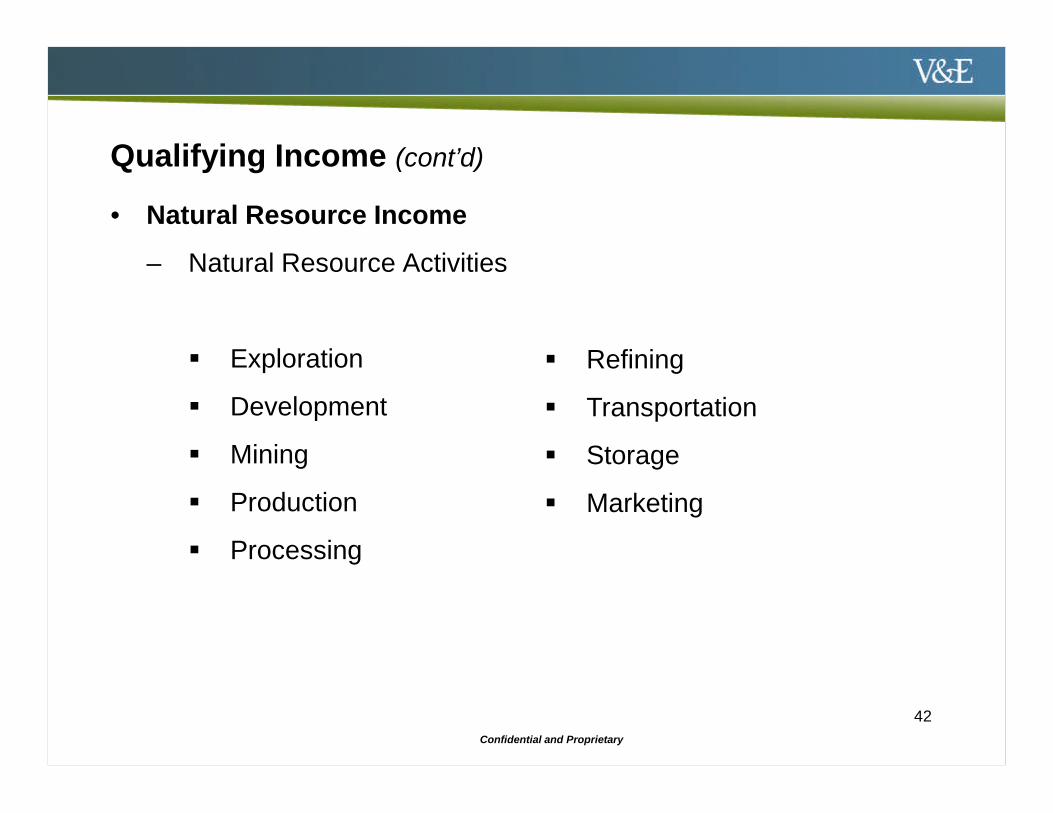

Qualifying Income (cont’d)

• Natural Resource Income

– Natural Resource Activities

Exploration

Development

Mining

Production

Processing

Refining

Transportation

Storage

Marketing

Confidential and Proprietary

43

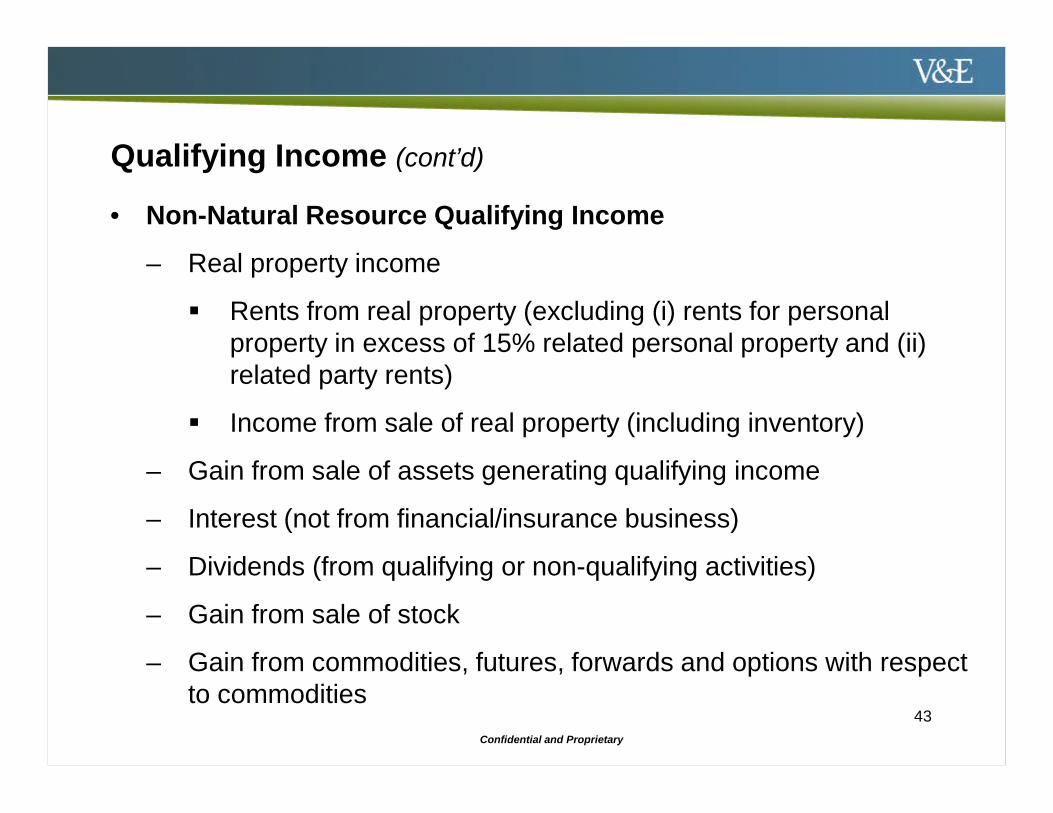

Qualifying Income (cont’d)

• Non-Natural Resource Qualifying Income

– Real property income

Rents from real property (excluding (i) rents for personalproperty in excess of 15% related personal property and (ii)related party rents)

Income from sale of real property (including inventory)

– Gain from sale of assets generating qualifying income

– Interest (not from financial/insurance business)

– Dividends (from qualifying or non-qualifying activities)

– Gain from sale of stock

– Gain from commodities, futures, forwards and options with respectto commodities

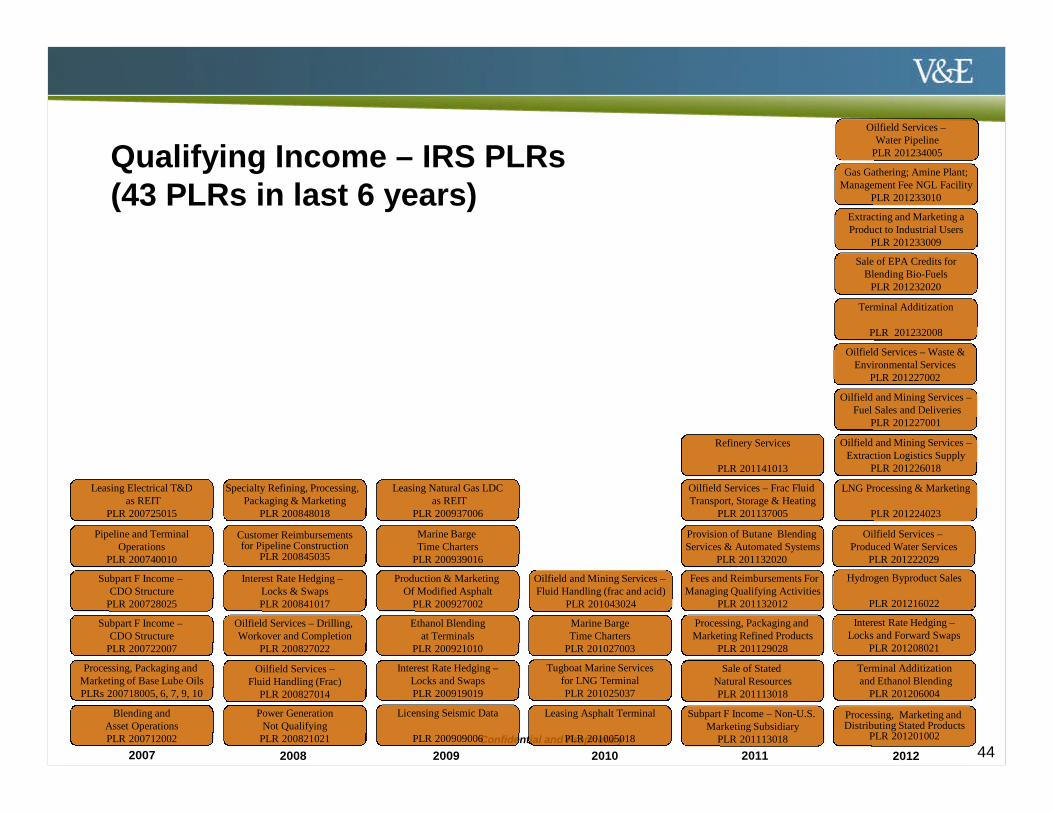

Confidential and Proprietary 4520122007 2008 2009 2010 2011 44

Leasing Electrical T&Das REIT

PLR 200725015

Pipeline and TerminalOperations

PLR 200740010

Subpart F Income –CDO Structure

PLR 200728025

Subpart F Income –CDO Structure

PLR 200722007

Processing, Packaging andMarketing of Base Lube OilsPLRs 200718005, 6, 7, 9, 10

Blending andAsset OperationsPLR 200712002

Specialty Refining, Processing,Packaging & Marketing

PLR 200848018

Customer Reimbursementsfor Pipeline Construction

PLR 200845035

Interest Rate Hedging –Locks & SwapsPLR 200841017

Oilfield Services – Drilling,Workover and Completion

PLR 200827022

Oilfield Services –Fluid Handling (Frac)

PLR 200827014

Power GenerationNot Qualifying

PLR 200821021

Leasing Natural Gas LDCas REIT

PLR 200937006

Marine BargeTime Charters

PLR 200939016

Production & MarketingOf Modified Asphalt

PLR 200927002

Ethanol Blendingat Terminals

PLR 200921010

Interest Rate Hedging –Locks and SwapsPLR 200919019

Licensing Seismic Data

PLR 200909006

Marine BargeTime Charters

PLR 201027003

Tugboat Marine Servicesfor LNG TerminalPLR 201025037

Leasing Asphalt Terminal

PLR 201005018

Oilfield and Mining Services –Fluid Handling (frac and acid)

PLR 201043024

Subpart F Income – Non-U.S.Marketing Subsidiary

PLR 201113018

Sale of StatedNatural ResourcesPLR 201113018

Processing, Packaging andMarketing Refined Products

PLR 201129028

Fees and Reimbursements ForManaging Qualifying Activities

PLR 201132012

Provision of Butane BlendingServices & Automated Systems

PLR 201132020

Oilfield Services – Frac FluidTransport, Storage & Heating

PLR 201137005

Refinery Services

PLR 201141013

Processing, Marketing andDistributing Stated Products

PLR 201201002

Terminal Additizationand Ethanol Blending

PLR 201206004

Interest Rate Hedging –Locks and Forward Swaps

PLR 201208021

Hydrogen Byproduct Sales

PLR 201216022

Oilfield Services –Produced Water Services

PLR 201222029

LNG Processing & Marketing

PLR 201224023

Oilfield and Mining Services –Extraction Logistics Supply

PLR 201226018

Oilfield and Mining Services –Fuel Sales and Deliveries

PLR 201227001

Oilfield Services – Waste &Environmental Services

PLR 201227002

Terminal Additization

PLR 201232008

Sale of EPA Credits forBlending Bio-Fuels

PLR 201232020

Extracting and Marketing aProduct to Industrial Users

PLR 201233009

Gas Gathering; Amine Plant;Management Fee NGL Facility

PLR 201233010

Oilfield Services –Water Pipeline

PLR 201234005Qualifying Income – IRS PLRs(43 PLRs in last 6 years)

Confidential and Proprietary

45

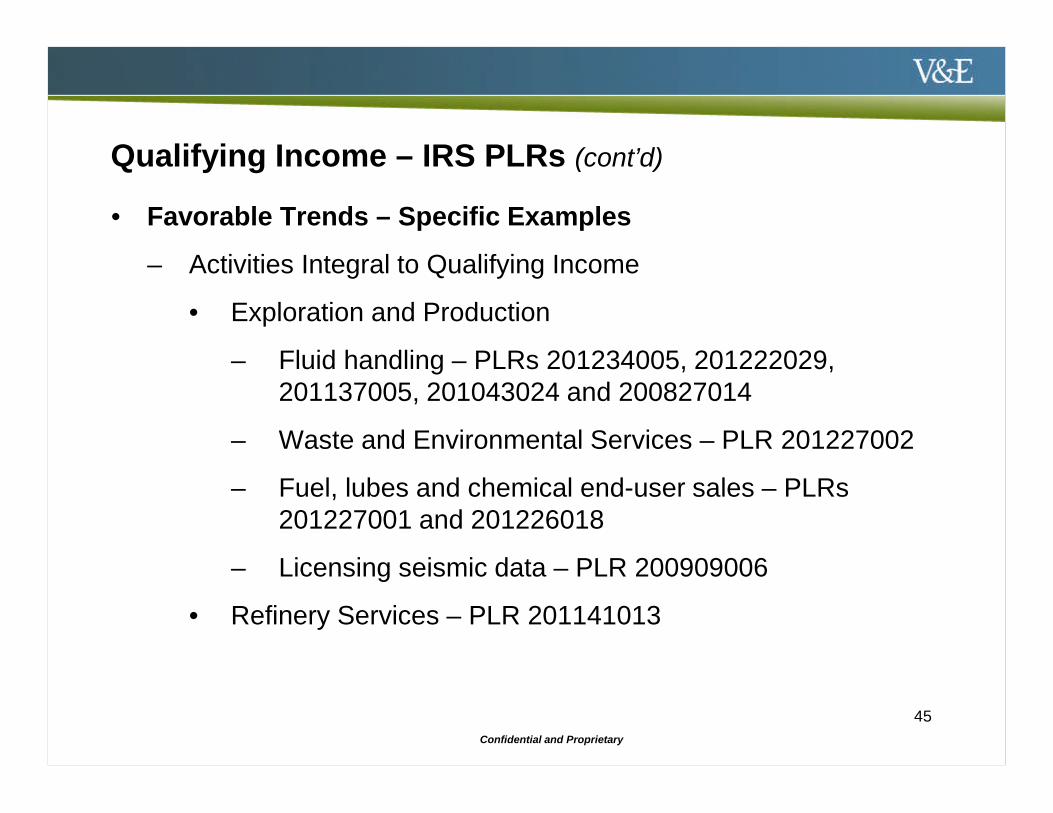

Qualifying Income – IRS PLRs (cont’d)

• Favorable Trends – Specific Examples

– Activities Integral to Qualifying Income

• Exploration and Production

– Fluid handling – PLRs 201234005, 201222029,201137005, 201043024 and 200827014

– Waste and Environmental Services – PLR 201227002

– Fuel, lubes and chemical end-user sales – PLRs201227001 and 201226018

– Licensing seismic data – PLR 200909006

• Refinery Services – PLR 201141013

Confidential and Proprietary

46

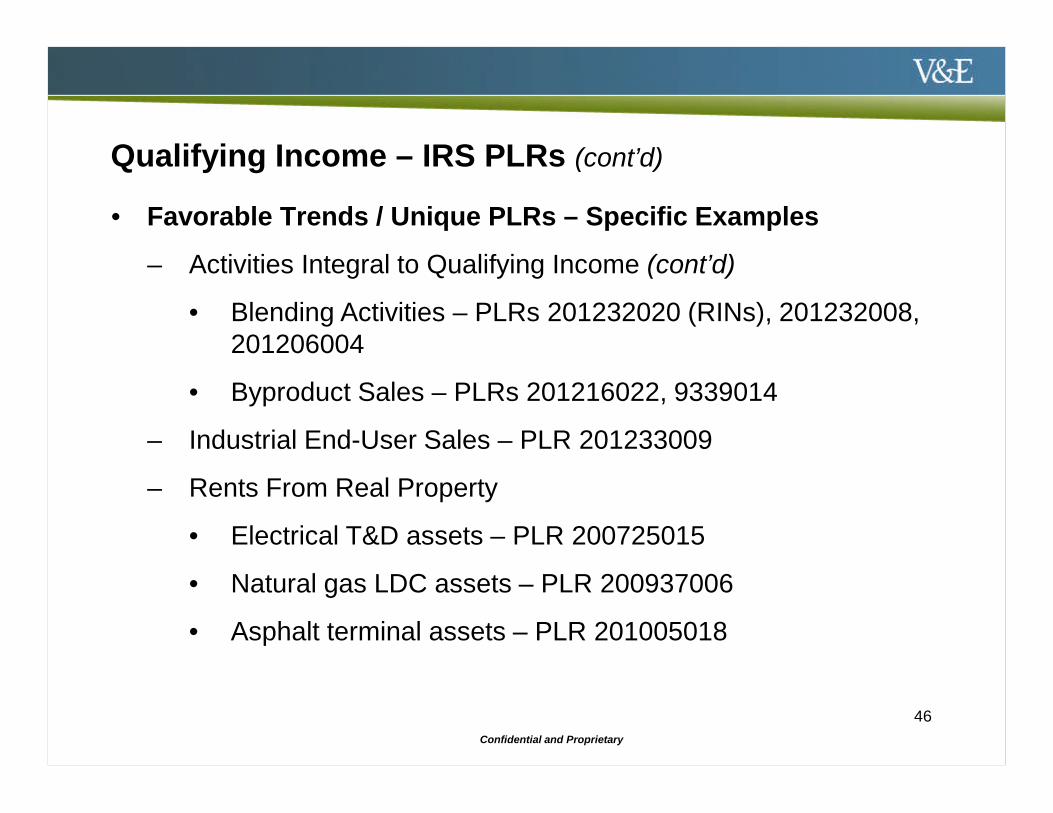

Qualifying Income – IRS PLRs (cont’d)

• Favorable Trends / Unique PLRs – Specific Examples

– Activities Integral to Qualifying Income (cont’d)

• Blending Activities – PLRs 201232020 (RINs), 201232008,201206004

• Byproduct Sales – PLRs 201216022, 9339014

– Industrial End-User Sales – PLR 201233009

– Rents From Real Property

• Electrical T&D assets – PLR 200725015

• Natural gas LDC assets – PLR 200937006

• Asphalt terminal assets – PLR 201005018

Confidential and Proprietary

Qualifying Income is Global

47

Confidential and Proprietary

Other Tax Considerations

Confidential and Proprietary

49

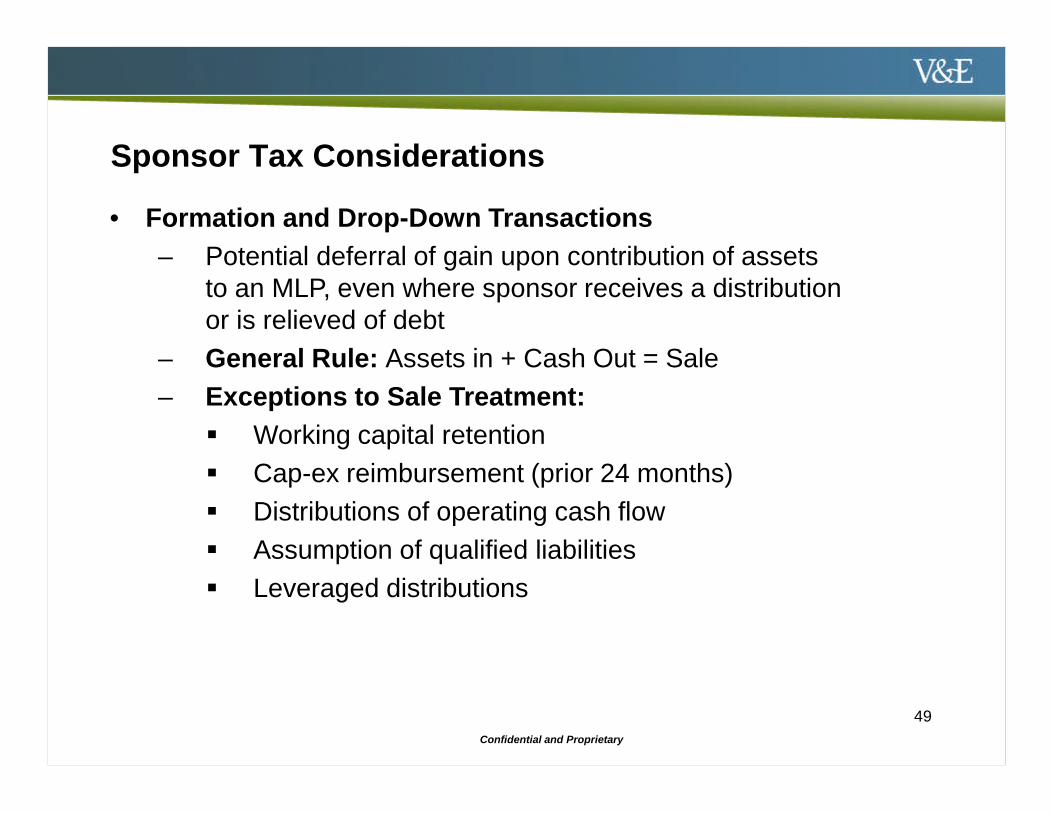

Sponsor Tax Considerations

• Formation and Drop-Down Transactions

– Potential deferral of gain upon contribution of assetsto an MLP, even where sponsor receives a distributionor is relieved of debt

– General Rule: Assets in + Cash Out = Sale

– Exceptions to Sale Treatment:

Working capital retention

Cap-ex reimbursement (prior 24 months)

Distributions of operating cash flow

Assumption of qualified liabilities

Leveraged distributions

Confidential and Proprietary

50

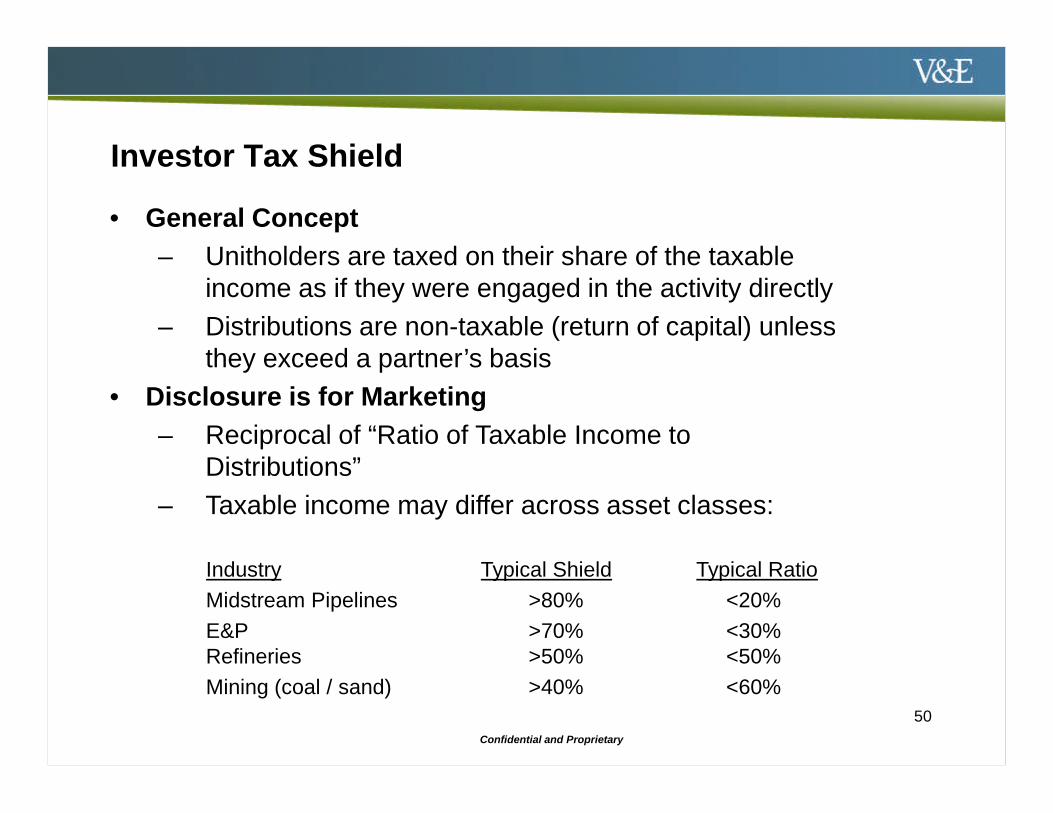

Investor Tax Shield

• General Concept

– Unitholders are taxed on their share of the taxableincome as if they were engaged in the activity directly

– Distributions are non-taxable (return of capital) unlessthey exceed a partner’s basis

• Disclosure is for Marketing

– Reciprocal of “Ratio of Taxable Income toDistributions”

– Taxable income may differ across asset classes:

Industry Typical Shield Typical Ratio

Midstream Pipelines >80% <20%

E&P >70% <30%Refineries >50% <50%

Mining (coal / sand) >40% <60%

Confidential and Proprietary

51

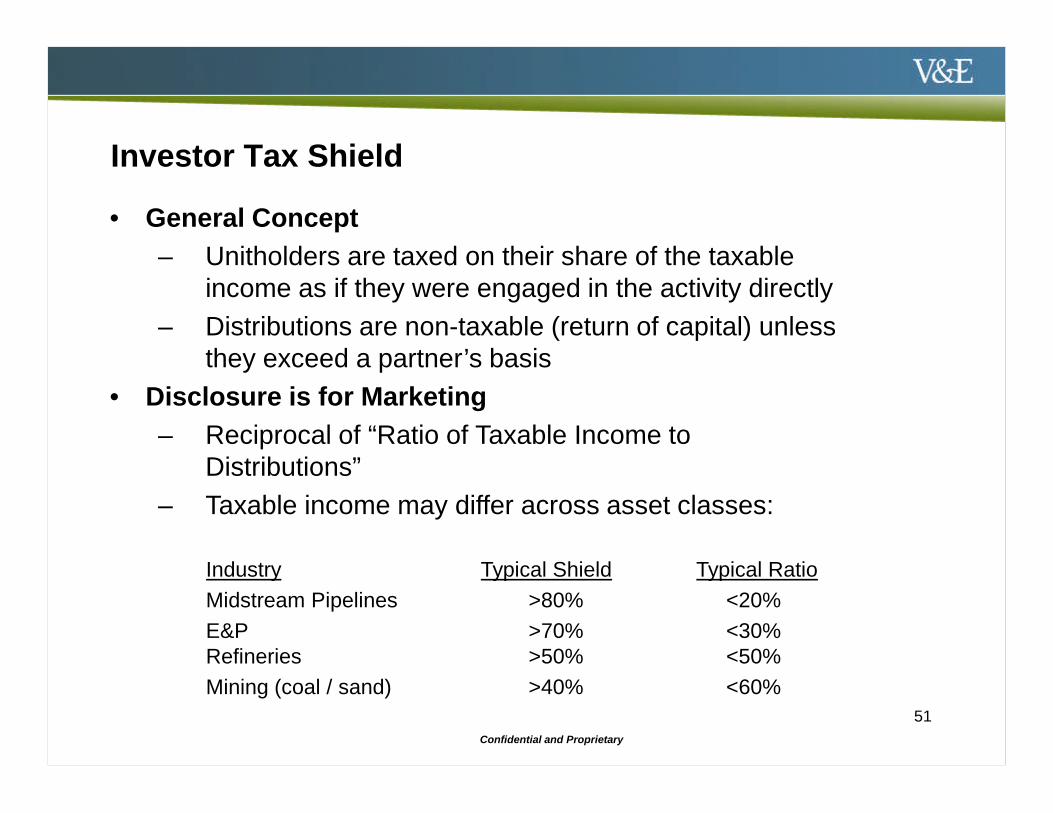

Investor Tax Shield

• General Concept

– Unitholders are taxed on their share of the taxableincome as if they were engaged in the activity directly

– Distributions are non-taxable (return of capital) unlessthey exceed a partner’s basis

• Disclosure is for Marketing

– Reciprocal of “Ratio of Taxable Income toDistributions”

– Taxable income may differ across asset classes:

Industry Typical Shield Typical Ratio

Midstream Pipelines >80% <20%

E&P >70% <30%Refineries >50% <50%

Mining (coal / sand) >40% <60%

Confidential and Proprietary

52

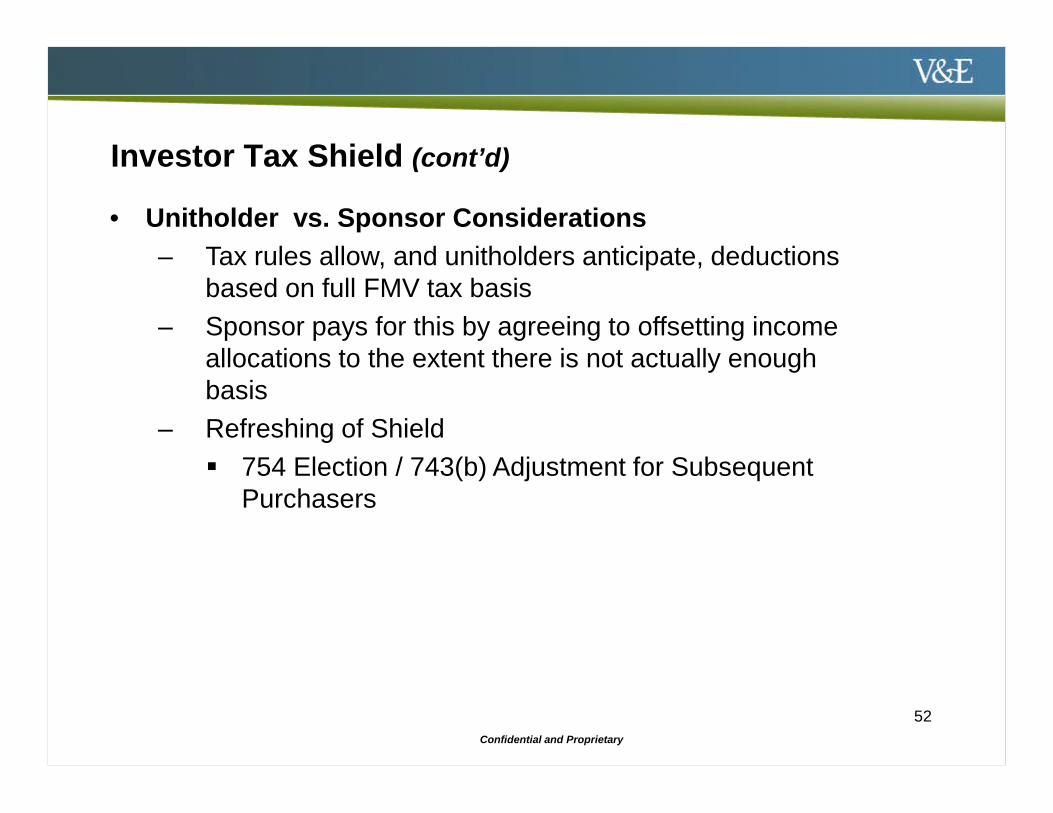

Investor Tax Shield (cont’d)

• Unitholder vs. Sponsor Considerations

– Tax rules allow, and unitholders anticipate, deductionsbased on full FMV tax basis

– Sponsor pays for this by agreeing to offsetting incomeallocations to the extent there is not actually enoughbasis

– Refreshing of Shield

754 Election / 743(b) Adjustment for SubsequentPurchasers

Confidential and Proprietary

53

• Tax Exempt Investors

– Unrelated business taxable income (“UBTI”) for tax exempts

• Non-U.S. Investors

– Effectively connected income (“ECI”) and withholding for foreignpersons

– Ownership restrictions for certain MLPs with federal O&G leasesand Jones Act shipping businesses

• Mutual Funds

– Qualifying income for mutual funds; 2004 Jobs Creation Act

– Ownership restrictions for certain MLPs with FERC regulatedpipelines

Special Investor Considerations

Confidential and Proprietary

54

State Taxes and Accounting

• State Tax Issues

– Investor filing obligations

– Company filing obligations

• Tax Accounting

– Section 754 Election

– Tax Accounting Systems / Service Providers

Confidential and Proprietary

Legislative Developments

Confidential and Proprietary

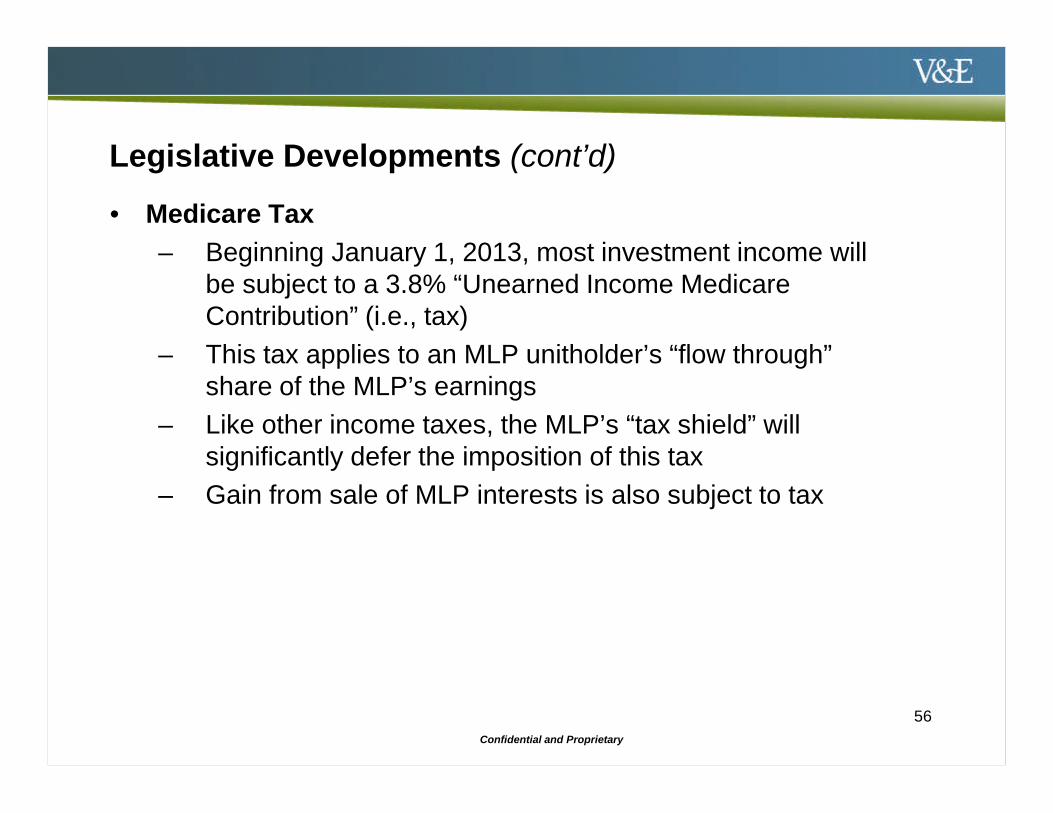

• Medicare Tax

– Beginning January 1, 2013, most investment income willbe subject to a 3.8% “Unearned Income MedicareContribution” (i.e., tax)

– This tax applies to an MLP unitholder’s “flow through”share of the MLP’s earnings

– Like other income taxes, the MLP’s “tax shield” willsignificantly defer the imposition of this tax

– Gain from sale of MLP interests is also subject to tax

Legislative Developments (cont’d)

56

Confidential and Proprietary

• Proposed Legislation

– End Welfare Polluter Act

• Excludes natural resource activities from qualifyingincome

– MLP Parity Act

• Expands qualifying income to include alternativeenergy (wind, solar, hydro-electric, solid waste, andproduction of biofuels)

– Carried Interest Legislation

• Taxes certain partnership income and sales of“carried interests” partnership interests as ordinaryincome rather than capital gains

Legislative Developments

57

Confidential and Proprietary

• Tax Reform

– Broadening the base and lowering the rate

– Closing loopholes

– Leveling the playing field

– Taxation of passthroughs

– National Association of Publicly Traded Partnerships(www.NAPTP.org)

Legislative Developments

58

Confidential and Proprietary

Question & Answers

Confidential and Proprietary

Circular 230 Notice

This presentation was written or intended to be used, andcannot be used, for the purpose of (i) avoiding penaltiesunder the Internal Revenue Code or (ii) promoting,marketing or recommending to another party anytransaction or matter addressed herein.

60