MLP 101: INTRODUCTION TO MASTER LIMITED...

17

MLP 101: INTRODUCTION TO MASTER LIMITED P ARTNERSHIPS HOUSTON | BOSTON curbstonegroup.com

Transcript of MLP 101: INTRODUCTION TO MASTER LIMITED...

MLP 101: INTRODUCTION TO MASTER LIMITED PARTNERSHIPS

HOUSTON | BOSTON

curbstonegroup.com

|

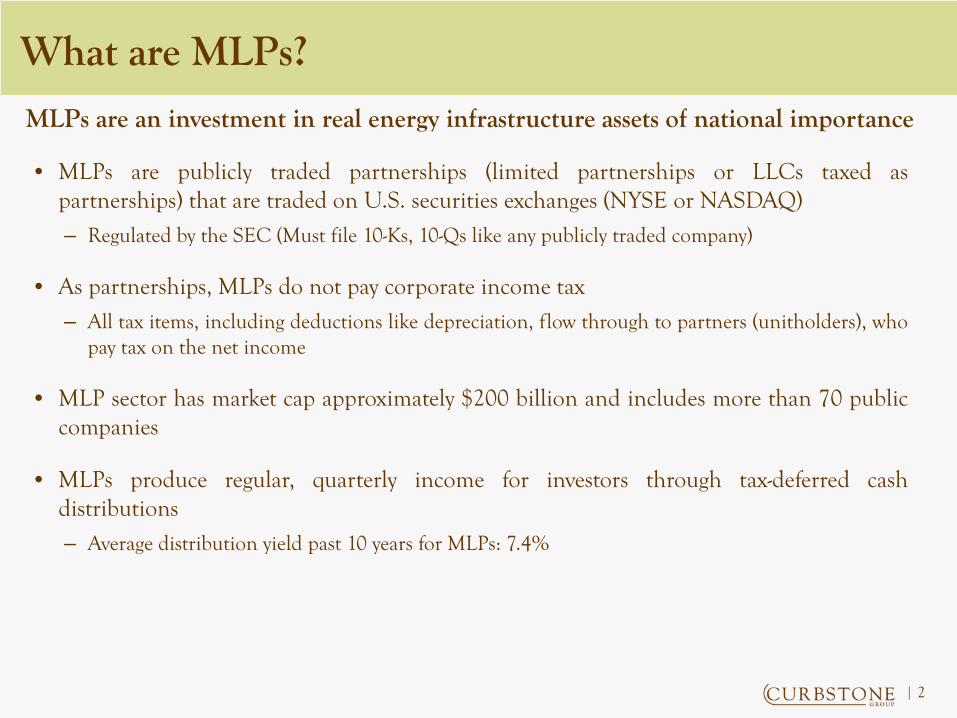

What are MLPs?

2

• MLPs are publicly traded partnerships (limited partnerships or LLCs taxed aspartnerships) that are traded on U.S. securities exchanges (NYSE or NASDAQ)

– Regulated by the SEC (Must file 10-Ks, 10-Qs like any publicly traded company)

• As partnerships, MLPs do not pay corporate income tax

– All tax items, including deductions like depreciation, flow through to partners (unitholders), whopay tax on the net income

• MLP sector has market cap approximately $200 billion and includes more than 70 publiccompanies

• MLPs produce regular, quarterly income for investors through tax-deferred cashdistributions

– Average distribution yield past 10 years for MLPs: 7.4%

MLPs are an investment in real energy infrastructure assets of national importance

|

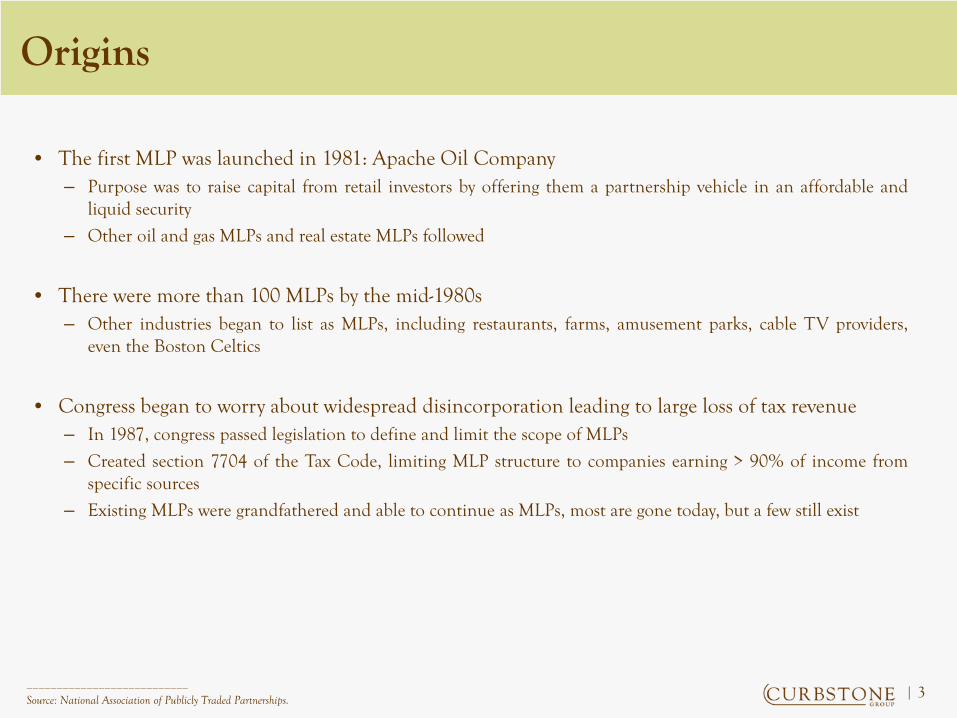

Origins

3

• The first MLP was launched in 1981: Apache Oil Company– Purpose was to raise capital from retail investors by offering them a partnership vehicle in an affordable and

liquid security

– Other oil and gas MLPs and real estate MLPs followed

• There were more than 100 MLPs by the mid-1980s– Other industries began to list as MLPs, including restaurants, farms, amusement parks, cable TV providers,

even the Boston Celtics

• Congress began to worry about widespread disincorporation leading to large loss of tax revenue– In 1987, congress passed legislation to define and limit the scope of MLPs

– Created section 7704 of the Tax Code, limiting MLP structure to companies earning > 90% of income fromspecific sources

– Existing MLPs were grandfathered and able to continue as MLPs, most are gone today, but a few still exist

___________________________Source: National Association of Publicly Traded Partnerships.

|

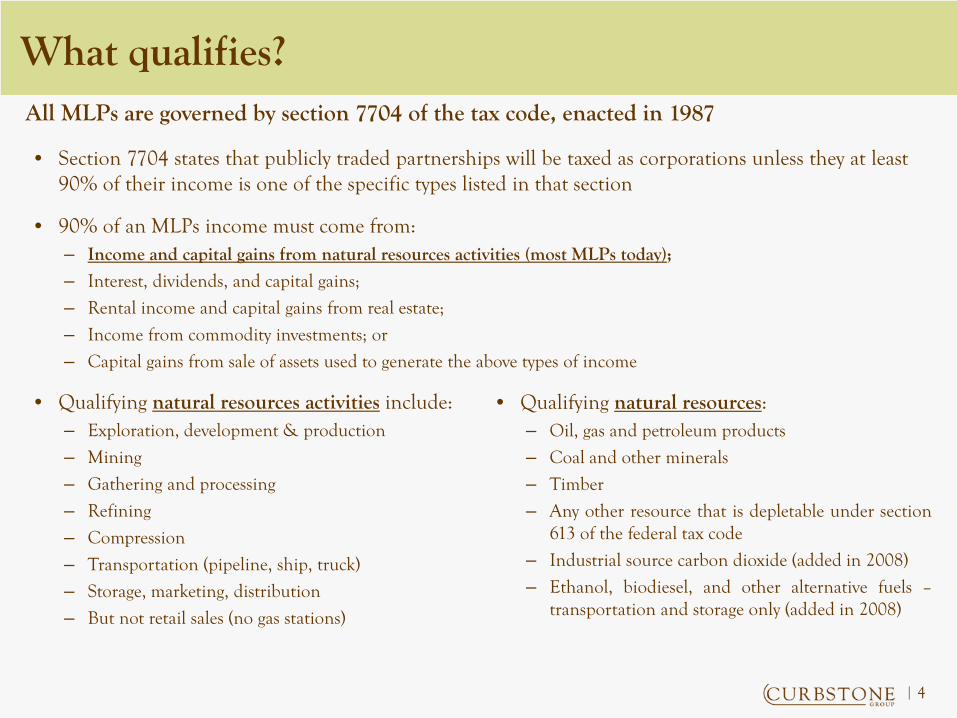

What qualifies?

4

• Section 7704 states that publicly traded partnerships will be taxed as corporations unless they at least90% of their income is one of the specific types listed in that section

• 90% of an MLPs income must come from:– Income and capital gains from natural resources activities (most MLPs today);

– Interest, dividends, and capital gains;

– Rental income and capital gains from real estate;

– Income from commodity investments; or

– Capital gains from sale of assets used to generate the above types of income

• Qualifying natural resources activities include:– Exploration, development & production

– Mining

– Gathering and processing

– Refining

– Compression

– Transportation (pipeline, ship, truck)

– Storage, marketing, distribution

– But not retail sales (no gas stations)

All MLPs are governed by section 7704 of the tax code, enacted in 1987

• Qualifying natural resources:– Oil, gas and petroleum products

– Coal and other minerals

– Timber

– Any other resource that is depletable under section613 of the federal tax code

– Industrial source carbon dioxide (added in 2008)

– Ethanol, biodiesel, and other alternative fuels –transportation and storage only (added in 2008)

|

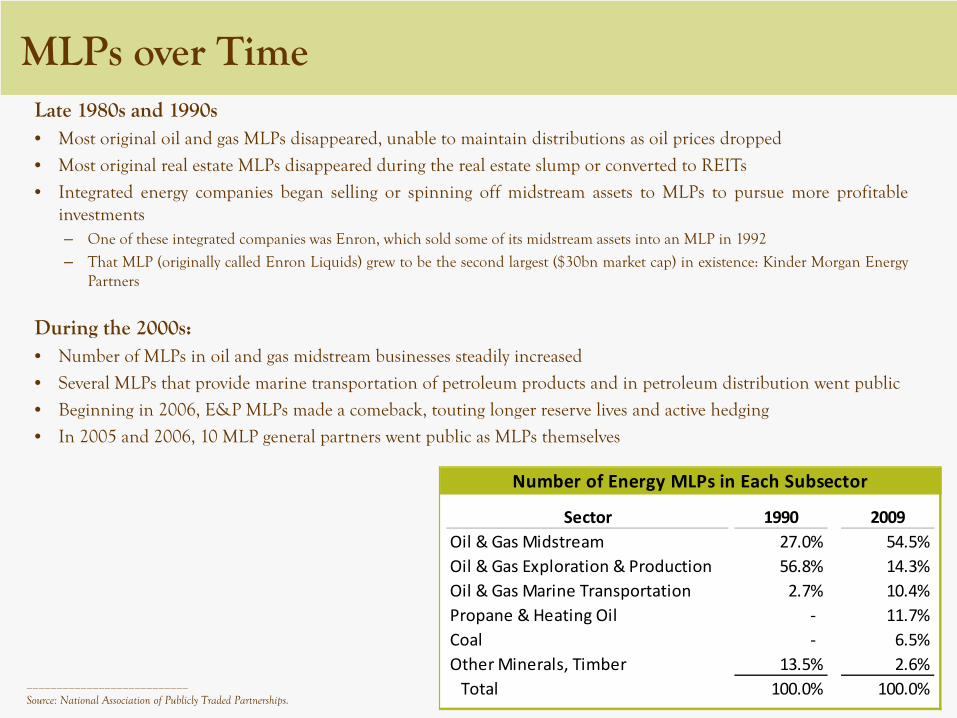

MLPs over Time

5

Late 1980s and 1990s• Most original oil and gas MLPs disappeared, unable to maintain distributions as oil prices dropped

• Most original real estate MLPs disappeared during the real estate slump or converted to REITs

• Integrated energy companies began selling or spinning off midstream assets to MLPs to pursue more profitableinvestments– One of these integrated companies was Enron, which sold some of its midstream assets into an MLP in 1992

– That MLP (originally called Enron Liquids) grew to be the second largest ($30bn market cap) in existence: Kinder Morgan EnergyPartners

During the 2000s:• Number of MLPs in oil and gas midstream businesses steadily increased

• Several MLPs that provide marine transportation of petroleum products and in petroleum distribution went public

• Beginning in 2006, E&P MLPs made a comeback, touting longer reserve lives and active hedging

• In 2005 and 2006, 10 MLP general partners went public as MLPs themselves

___________________________Source: National Association of Publicly Traded Partnerships.

Number of Energy MLPs in Each Subsector

Sector 1990 2009Oil & Gas Midstream 27.0% 54.5%Oil & Gas Exploration & Production 56.8% 14.3%Oil & Gas Marine Transportation 2.7% 10.4%Propane & Heating Oil ‐ 11.7%Coal ‐ 6.5%Other Minerals, Timber 13.5% 2.6%Total 100.0% 100.0%

|

Exploration &Production(well head)

Crude OilGathering Transportation

and Storage

RefiningFacilities Transportation

and Storage

Crude Oil Refined ProductsEnd Users

Refined Products

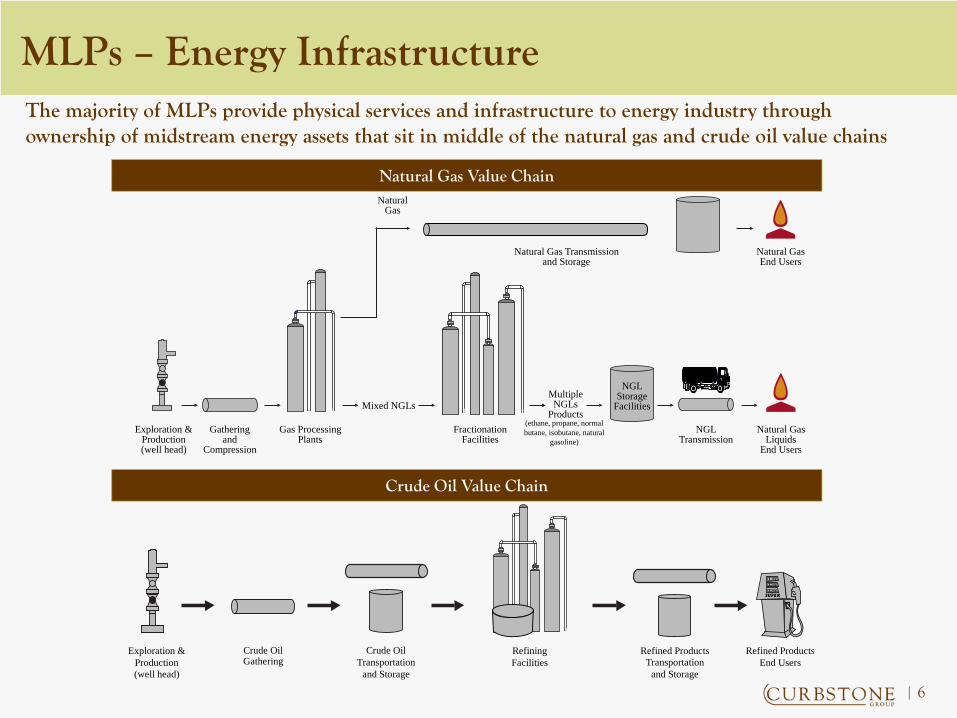

MLPs – Energy Infrastructure

6

The majority of MLPs provide physical services and infrastructure to energy industry through ownership of midstream energy assets that sit in middle of the natural gas and crude oil value chains

Natural Gas Value Chain

Crude Oil Value Chain

Exploration &Production(well head)

Gatheringand

Compression

Gas ProcessingPlants

Mixed NGLs

NaturalGas

Natural Gas Transmissionand Storage

FractionationFacilities

NGLStorage

Facilities

NGLTransmission

Natural GasEnd Users

MultipleNGLs

ProductsNatural Gas

End UsersLiquids

(ethane, propane, normal butane, isobutane, natural

gasoline)

|

MLP Structure – Typical MLP

7

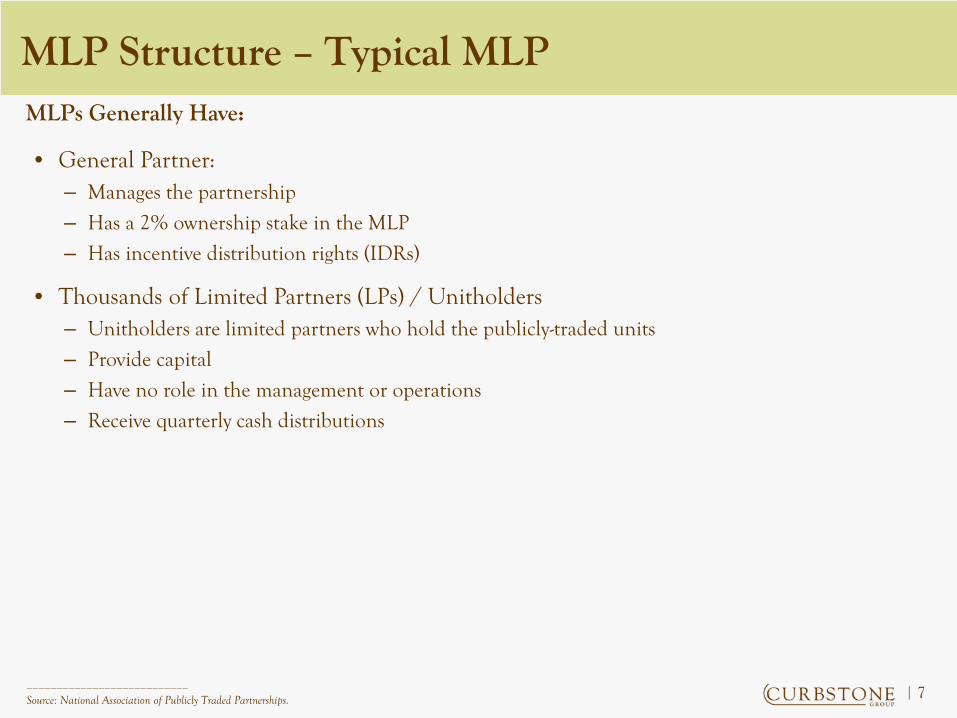

• General Partner:– Manages the partnership

– Has a 2% ownership stake in the MLP

– Has incentive distribution rights (IDRs)

• Thousands of Limited Partners (LPs) / Unitholders– Unitholders are limited partners who hold the publicly-traded units

– Provide capital

– Have no role in the management or operations

– Receive quarterly cash distributions

MLPs Generally Have:

___________________________Source: National Association of Publicly Traded Partnerships.

|

MLP Structure – Typical MLP

8

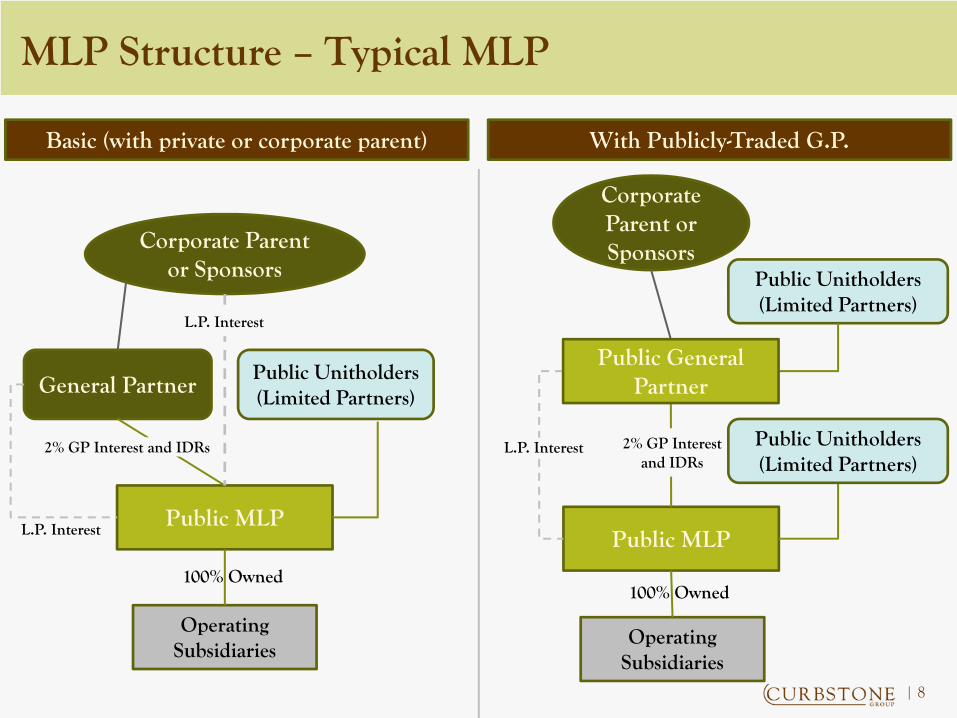

Corporate Parent or Sponsors

General Partner Public Unitholders(Limited Partners)

Public MLP

Operating Subsidiaries

100% Owned

L.P. Interest

L.P. Interest

2% GP Interest and IDRs

Corporate Parent or Sponsors

Public MLP

Operating Subsidiaries

100% Owned

L.P. Interest 2% GP Interestand IDRs

Public Unitholders(Limited Partners)

Public General Partner

Public Unitholders(Limited Partners)

Basic (with private or corporate parent) With Publicly-Traded G.P.

|

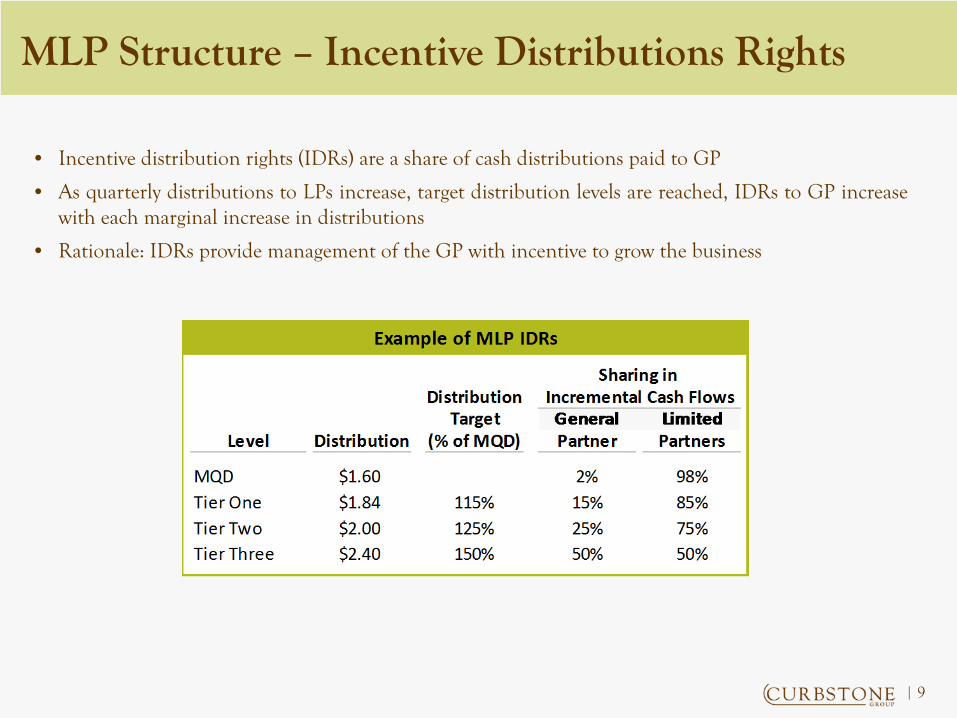

MLP Structure – Incentive Distributions Rights

9

• Incentive distribution rights (IDRs) are a share of cash distributions paid to GP

• As quarterly distributions to LPs increase, target distribution levels are reached, IDRs to GP increasewith each marginal increase in distributions

• Rationale: IDRs provide management of the GP with incentive to grow the business

|

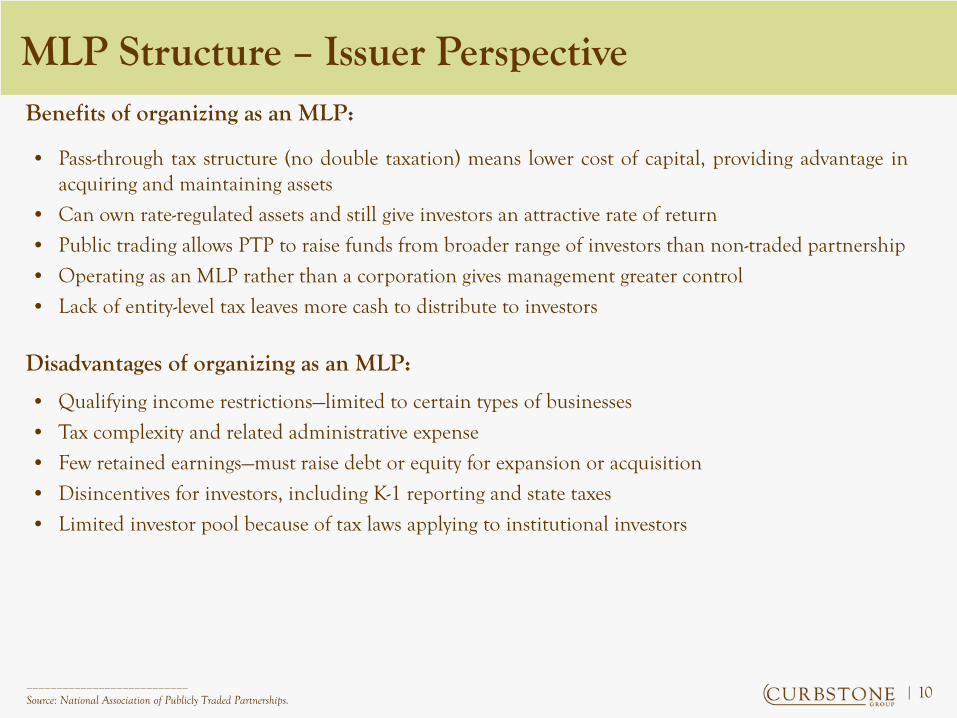

MLP Structure – Issuer Perspective

10

• Pass-through tax structure (no double taxation) means lower cost of capital, providing advantage inacquiring and maintaining assets

• Can own rate-regulated assets and still give investors an attractive rate of return

• Public trading allows PTP to raise funds from broader range of investors than non-traded partnership

• Operating as an MLP rather than a corporation gives management greater control

• Lack of entity-level tax leaves more cash to distribute to investors

Benefits of organizing as an MLP:

Disadvantages of organizing as an MLP:

• Qualifying income restrictions—limited to certain types of businesses

• Tax complexity and related administrative expense

• Few retained earnings—must raise debt or equity for expansion or acquisition

• Disincentives for investors, including K-1 reporting and state taxes

• Limited investor pool because of tax laws applying to institutional investors

___________________________Source: National Association of Publicly Traded Partnerships.

|

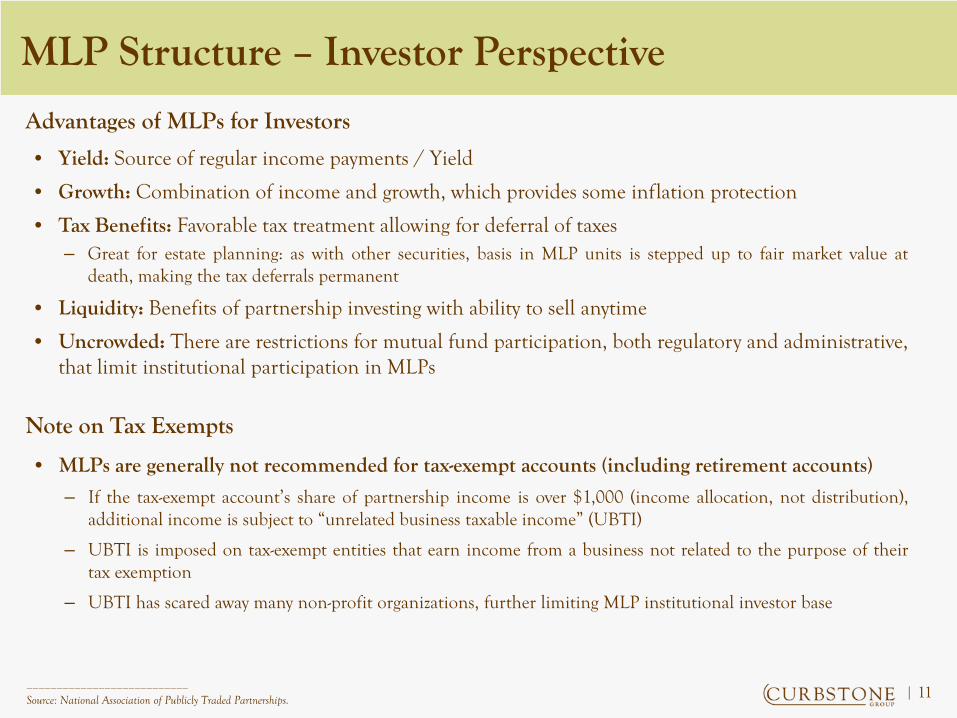

MLP Structure – Investor Perspective

11

• Yield: Source of regular income payments / Yield

• Growth: Combination of income and growth, which provides some inflation protection

• Tax Benefits: Favorable tax treatment allowing for deferral of taxes– Great for estate planning: as with other securities, basis in MLP units is stepped up to fair market value at

death, making the tax deferrals permanent

• Liquidity: Benefits of partnership investing with ability to sell anytime

• Uncrowded: There are restrictions for mutual fund participation, both regulatory and administrative,that limit institutional participation in MLPs

Advantages of MLPs for Investors

___________________________Source: National Association of Publicly Traded Partnerships.

Note on Tax Exempts

• MLPs are generally not recommended for tax-exempt accounts (including retirement accounts)

– If the tax-exempt account’s share of partnership income is over $1,000 (income allocation, not distribution),additional income is subject to “unrelated business taxable income” (UBTI)

– UBTI is imposed on tax-exempt entities that earn income from a business not related to the purpose of theirtax exemption

– UBTI has scared away many non-profit organizations, further limiting MLP institutional investor base

|

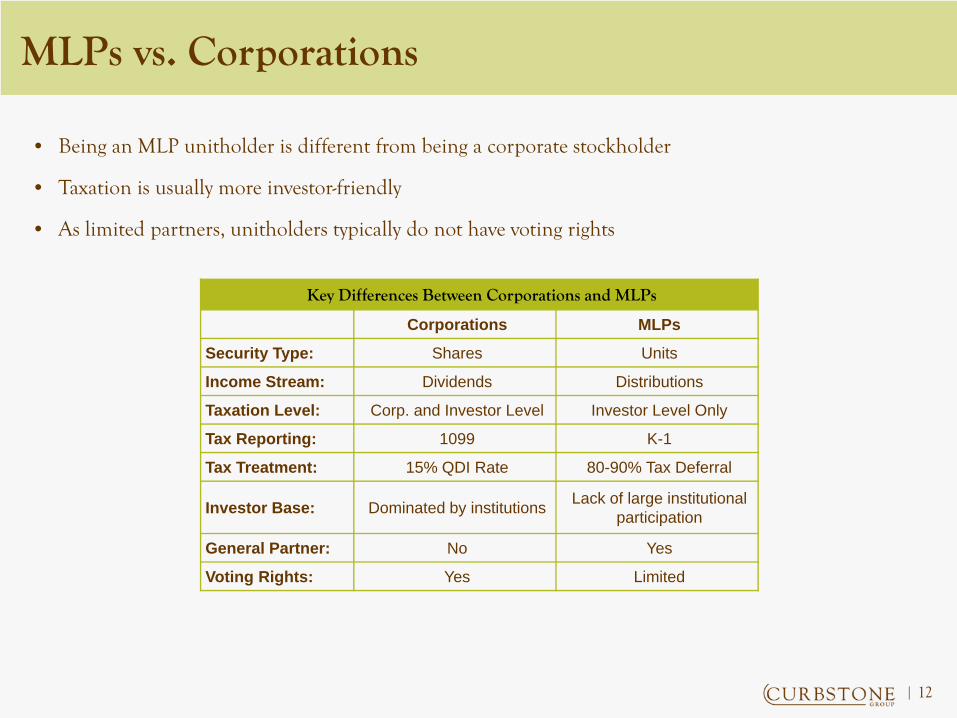

MLPs vs. Corporations

12

• Being an MLP unitholder is different from being a corporate stockholder

• Taxation is usually more investor-friendly

• As limited partners, unitholders typically do not have voting rights

Key Differences Between Corporations and MLPs

Corporations MLPs

Security Type: Shares Units

Income Stream: Dividends Distributions

Taxation Level: Corp. and Investor Level Investor Level Only

Tax Reporting: 1099 K-1

Tax Treatment: 15% QDI Rate 80-90% Tax Deferral

Investor Base: Dominated by institutions Lack of large institutional participation

General Partner: No Yes

Voting Rights: Yes Limited

|

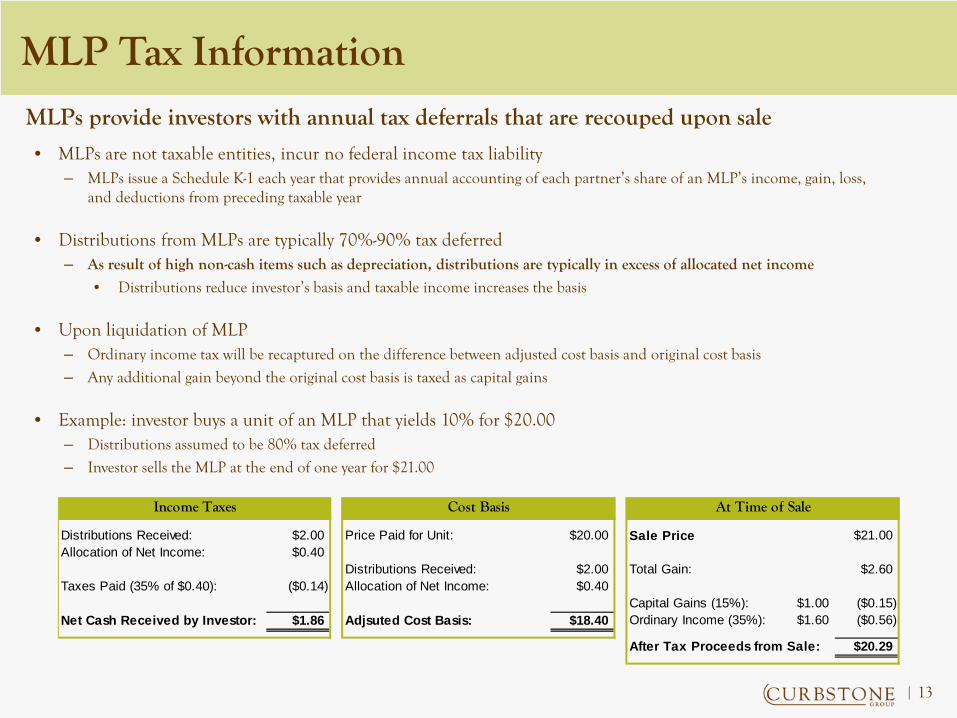

MLP Tax Information

13

• MLPs are not taxable entities, incur no federal income tax liability– MLPs issue a Schedule K-1 each year that provides annual accounting of each partner’s share of an MLP’s income, gain, loss,

and deductions from preceding taxable year

• Distributions from MLPs are typically 70%-90% tax deferred– As result of high non-cash items such as depreciation, distributions are typically in excess of allocated net income

• Distributions reduce investor’s basis and taxable income increases the basis

• Upon liquidation of MLP– Ordinary income tax will be recaptured on the difference between adjusted cost basis and original cost basis

– Any additional gain beyond the original cost basis is taxed as capital gains

• Example: investor buys a unit of an MLP that yields 10% for $20.00– Distributions assumed to be 80% tax deferred

– Investor sells the MLP at the end of one year for $21.00

MLPs provide investors with annual tax deferrals that are recouped upon sale

Income Taxes Cost Basis At Time of Sale

Distributions Received: $2.00 Price Paid for Unit: $20.00 Sale Price $21.00Allocation of Net Income: $0.40

Distributions Received: $2.00 Total Gain: $2.60Taxes Paid (35% of $0.40): ($0.14) Allocation of Net Income: $0.40

Capital Gains (15%): $1.00 ($0.15)Net Cash Received by Investor: $1.86 Adjsuted Cost Basis: $18.40 Ordinary Income (35%): $1.60 ($0.56)

After Tax Proceeds from Sale: $20.29

|

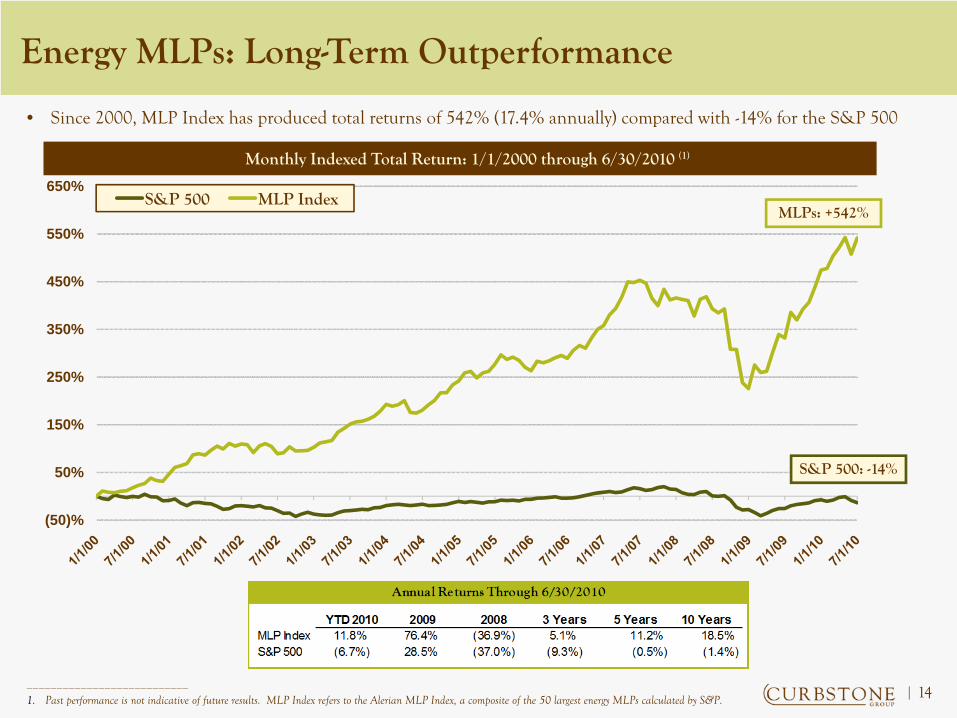

Energy MLPs: Long-Term Outperformance

14

(50)%

50%

150%

250%

350%

450%

550%

650%S&P 500 MLP Index

___________________________1. Past performance is not indicative of future results. MLP Index refers to the Alerian MLP Index, a composite of the 50 largest energy MLPs calculated by S&P.

S&P 500: -14%

MLPs: +542%

• Since 2000, MLP Index has produced total returns of 542% (17.4% annually) compared with -14% for the S&P 500

Monthly Indexed Total Return: 1/1/2000 through 6/30/2010 (1)

|

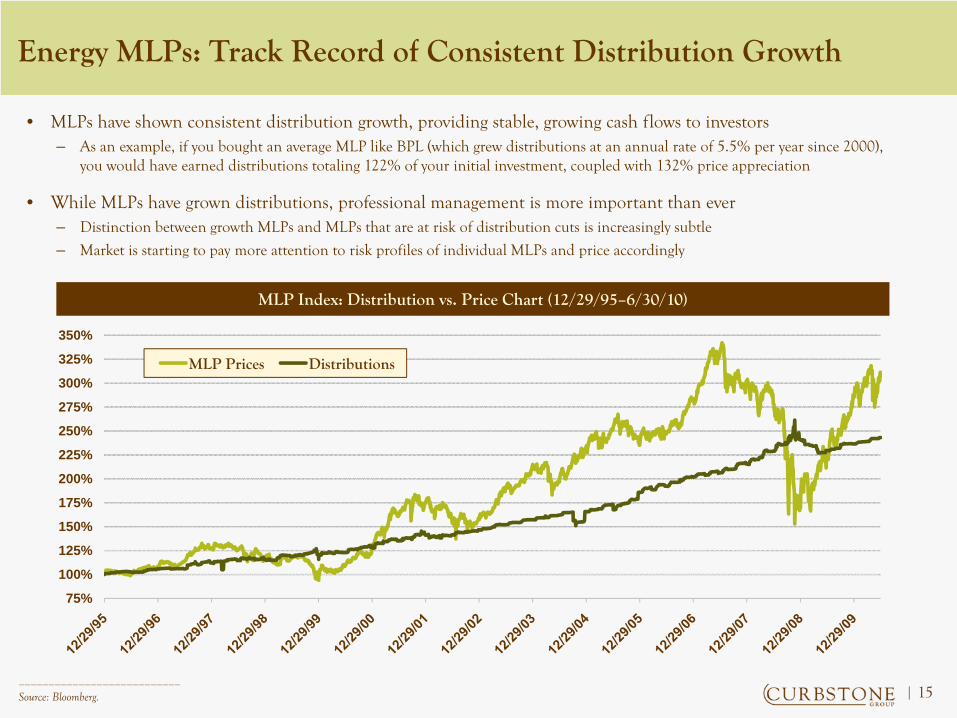

Energy MLPs: Track Record of Consistent Distribution Growth

15

• MLPs have shown consistent distribution growth, providing stable, growing cash flows to investors– As an example, if you bought an average MLP like BPL (which grew distributions at an annual rate of 5.5% per year since 2000),

you would have earned distributions totaling 122% of your initial investment, coupled with 132% price appreciation

• While MLPs have grown distributions, professional management is more important than ever– Distinction between growth MLPs and MLPs that are at risk of distribution cuts is increasingly subtle

– Market is starting to pay more attention to risk profiles of individual MLPs and price accordingly

75%

100%

125%

150%

175%

200%

225%

250%

275%

300%

325%

350%

MLP Prices Distributions

MLP Index: Distribution vs. Price Chart (12/29/95–6/30/10)

___________________________Source: Bloomberg.

|

Contact Information

16

PartnersMike [email protected]

Hinds [email protected]

Ryan [email protected]

OfficesHouston Office7700 San Felipe, Suite 461Houston, TX 77063

Boston Office1050 Winter St., Suite 1000Waltham, MA 02451(781) 333-4449

|

Disclaimers

17

Historical performance results for investment indices and/or categories generally do not reflect the deduction oftransaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of whichwould have the effect of decreasing historical performance results. Each of these indices is a Total Return index,calculated as though all cash flows from the asset are reinvested.

Any information contained herein or referenced regarding the past performance of a security is not indicative offuture results and there can be no assurance the mentioned security will achieve similar returns in the future oravoid losses. Depending on the particulars of any specific individual's account, actually investment returns mayvary materially from the returns stated in this presentation.

This information is provided for informational purposes only and does not constitute an offer to sell or asolicitation to purchase any security.

This investment evaluation is directed only to the client and/or interested party for whom this evaluation wascreated. The underlying data has been obtained from sources considered to be reliable: the information is believedto be accurate, but there is no assurance that it is so. This evaluation is for informational purposes only and is notintended to be an offer, solicitation or recommendation with respect to the purchase or sale of any security, or arecommendation of the services supplied by any money management organization. Past performance is not anindication, nor a guarantee of future results.