![· [MJ [M] (M] (M] (M] [MJ (MJ (M J (M] [M) [MJ [MJ [Mj [a 3rd ~pecker) [ Mj .. 2/0.t::JT.01-58 I om turning toward [point] 135. Yes, I om over [point J 136 now. {B% Roger). Roger,](https://static.fdocuments.in/doc/165x107/5c7742dc09d3f2322f8be721/-mj-m-m-m-m-mj-mj-m-j-m-m-mj-mj-mj-a-3rd-pecker-mj-.jpg)

MJ SafCom PPT

14

1 Mpesa: Mpesa: A FINANCIAL SOLUTION FINANCIAL SOLUTION for for Excellent Healthcare & Education Service Delivery in Excellent Healthcare & Education Service Delivery in Kenya and Sub Saharan Africa Kenya and Sub Saharan Africa Contact: [email protected] Caleb Opon

Transcript of MJ SafCom PPT

1

Mpesa:Mpesa: AA FINANCIAL SOLUTION FINANCIAL SOLUTION

for for

Excellent Healthcare & Education Service Delivery in Excellent Healthcare & Education Service Delivery in

Kenya and Sub Saharan AfricaKenya and Sub Saharan Africa

Contact: [email protected]

Caleb Opon

Mpesa: Turning Mpesa into an Innovative Financing Model for

Public Health & Education Institutions

The Mpesa product can provide additional funding for the sector’s

institutions without additional taxes or asking households to pay to:

1. Transform public education and health facilities in Kenya and (SSA) into world class

institutions

2. Offer excellent education and healthcare services FREE to all citizens.

3. Create huge demand (commercialize) for firms that provide health, education goods

and services and mobile phone handsets at competitive market prices

4. Expand Safaricom's subscriber base in Kenya and open new markets in SSA under

Vodafone mobile money

5. Establish Safaricom as a major player in the financial sector with over KES 318billion in

stable Mpesa deposits. (Equity Bank recently applied for a mobile phone license)

6. Use the same concept for Vodafone Mobile Money in other countries turning the

savings platform for quality education and health as the driver for overall growth2

What HEALTH SECTOR problems will Mpesa address

in Kenya?

State of Public Health Sector• Quality of healthcare is low, cost is high, equity is limited – 46% of Kenyans are

poor, (30%) 9 million absolute poor,

• 36% of total healthcare expenditure funded by households; Majority of patients

are unable to pay market prices as currently defined by the high end hospitals.

• 38% sell their assets or borrow to pay for medical bills. Many die from treatable

causes. (Maternal mortality: Kenya; 1 in every 15 women. USA; 1 in every 3,750)

The Health Care sector is unable to deliver:

• Drugs into the hands of patients

• Machines (for diagnostics as well as treatment) into the hands of doctors and

nurses at the right prices

• Doctors, nurses and technicians are expensive to train and hard to sufficiently

remunerate within the public sector or indeed the country

• There is not enough funding flowing into the sector generally 3

What EDUCATION SECTOR problems will Mpesa

address in Kenya?

4

State of Public Education Sector • Huge public spending, low educational achievements.

• Poor physical facilities and equipment, inadequate curriculum teaching and learning materials

• Facilities; the low transition rates to secondary schools and other tertiary institutions are as a result of lack of adequate places.

• Income disparities as high earners take their children to lesser affordable but more competitive private schools with better academic performance.

• From 2004 – 2010, at the secondary level, many poor parents paid USD $ 450 per year for 896,895 students classified as failures unable to go to mid-level colleges. Total lose USD $ 1.61bln (KES 137.2bln)

Estimated six million youth unemployed not just because of lack of jobs, but also lack of skills a problem that manifests itself in

lack of the skilled labour force needed for development

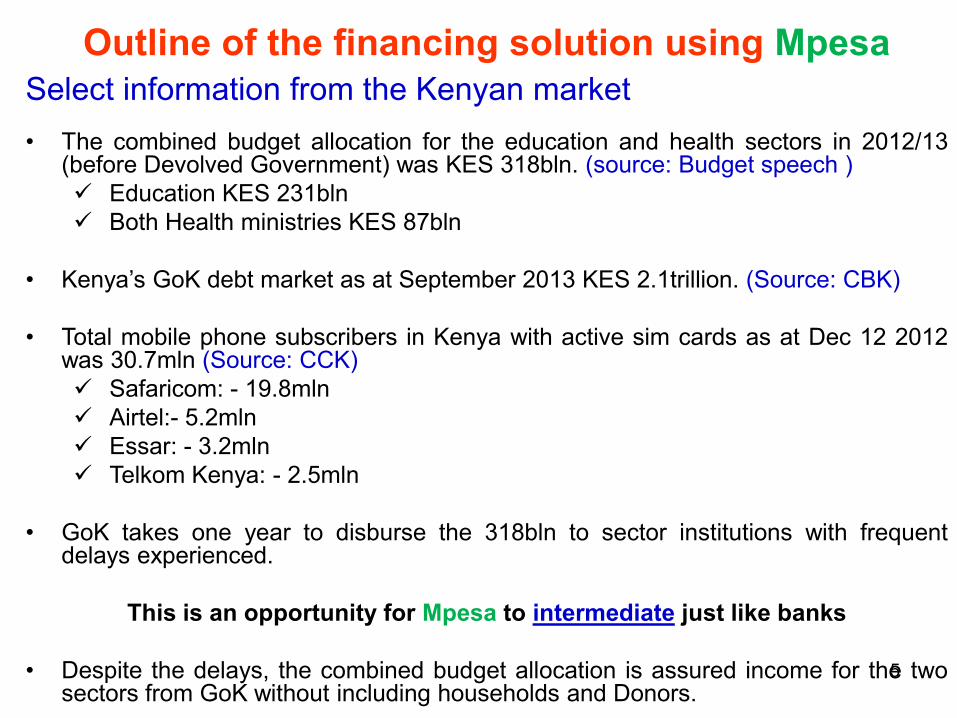

Outline of the financing solution using Mpesa

5

Select information from the Kenyan market

• The combined budget allocation for the education and health sectors in 2012/13(before Devolved Government) was KES 318bln. (source: Budget speech )

Education KES 231bln

Both Health ministries KES 87bln

• Kenya’s GoK debt market as at September 2013 KES 2.1trillion. (Source: CBK)

• Total mobile phone subscribers in Kenya with active sim cards as at Dec 12 2012was 30.7mln (Source: CCK)

Safaricom: - 19.8mln

Airtel:- 5.2mln

Essar: - 3.2mln

Telkom Kenya: - 2.5mln

• GoK takes one year to disburse the 318bln to sector institutions with frequentdelays experienced.

This is an opportunity for Mpesa to intermediate just like banks

• Despite the delays, the combined budget allocation is assured income for the twosectors from GoK without including households and Donors.

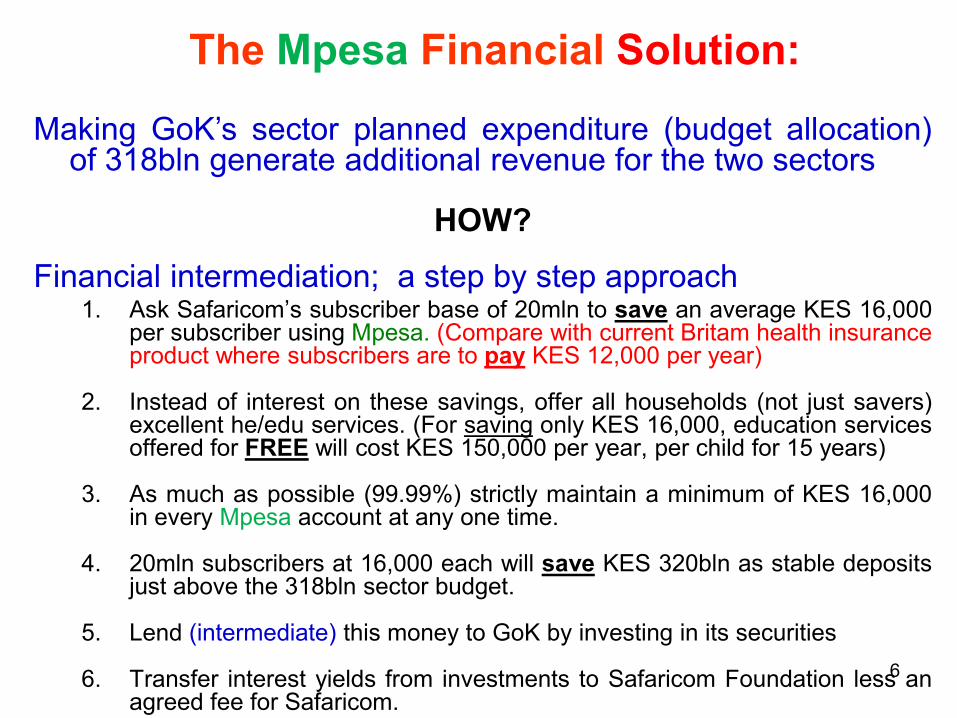

The Mpesa Financial Solution:

6

Making GoK’s sector planned expenditure (budget allocation)of 318bln generate additional revenue for the two sectors

HOW?

Financial intermediation; a step by step approach1. Ask Safaricom’s subscriber base of 20mln to save an average KES 16,000

per subscriber using Mpesa. (Compare with current Britam health insuranceproduct where subscribers are to pay KES 12,000 per year)

2. Instead of interest on these savings, offer all households (not just savers)excellent he/edu services. (For saving only KES 16,000, education servicesoffered for FREE will cost KES 150,000 per year, per child for 15 years)

3. As much as possible (99.99%) strictly maintain a minimum of KES 16,000in every Mpesa account at any one time.

4. 20mln subscribers at 16,000 each will save KES 320bln as stable depositsjust above the 318bln sector budget.

5. Lend (intermediate) this money to GoK by investing in its securities

6. Transfer interest yields from investments to Safaricom Foundation less anagreed fee for Safaricom.

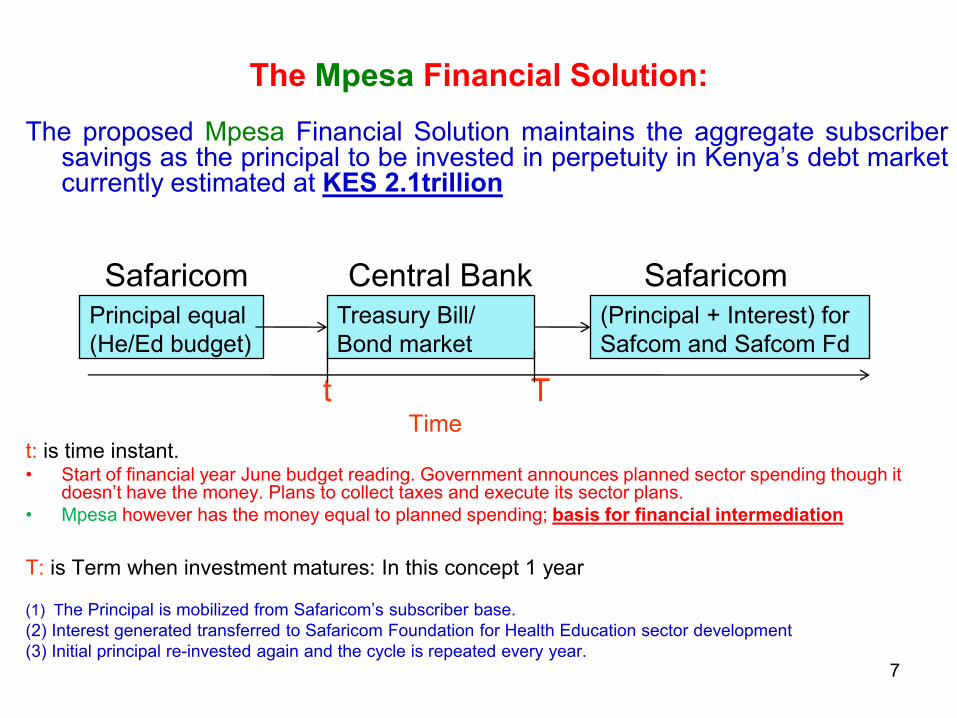

The Mpesa Financial Solution:

7

The proposed Mpesa Financial Solution maintains the aggregate subscribersavings as the principal to be invested in perpetuity in Kenya’s debt marketcurrently estimated at KES 2.1trillion

Safaricom Central Bank Safaricom

t TTime

t: is time instant. • Start of financial year June budget reading. Government announces planned sector spending though it

doesn’t have the money. Plans to collect taxes and execute its sector plans.

• Mpesa however has the money equal to planned spending; basis for financial intermediation

T: is Term when investment matures: In this concept 1 year

(1) The Principal is mobilized from Safaricom’s subscriber base.

(2) Interest generated transferred to Safaricom Foundation for Health Education sector development

(3) Initial principal re-invested again and the cycle is repeated every year.

Principal equal

(He/Ed budget)

Treasury Bill/

Bond market

(Principal + Interest) for

Safcom and Safcom Fd

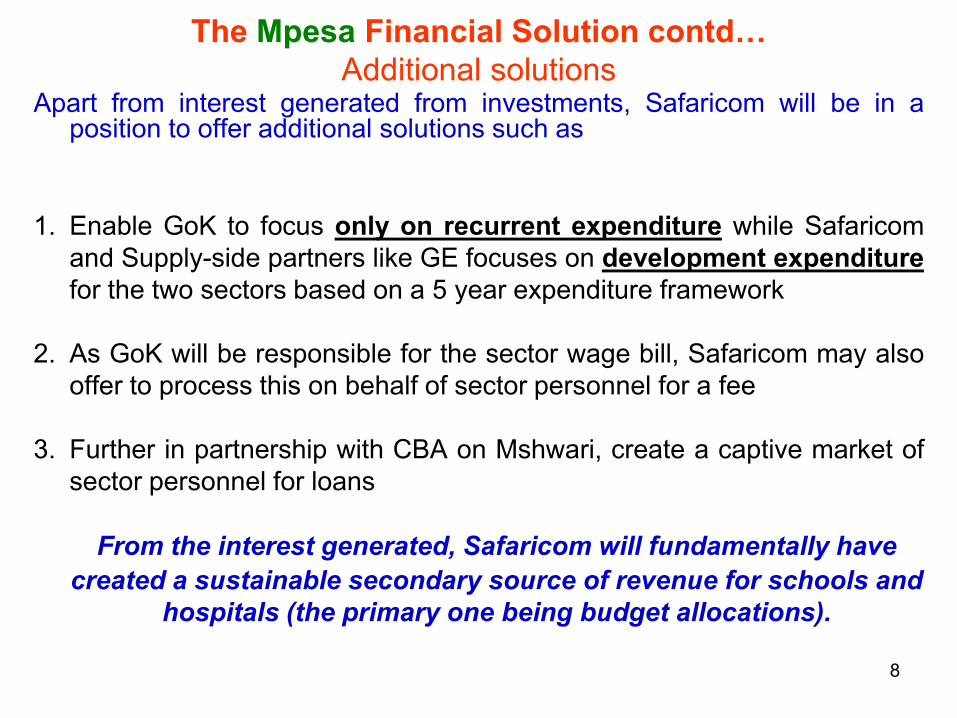

The Mpesa Financial Solution contd…

Additional solutions

8

Apart from interest generated from investments, Safaricom will be in aposition to offer additional solutions such as

1. Enable GoK to focus only on recurrent expenditure while Safaricom

and Supply-side partners like GE focuses on development expenditure

for the two sectors based on a 5 year expenditure framework

2. As GoK will be responsible for the sector wage bill, Safaricom may also

offer to process this on behalf of sector personnel for a fee

3. Further in partnership with CBA on Mshwari, create a captive market of

sector personnel for loans

From the interest generated, Safaricom will fundamentally have

created a sustainable secondary source of revenue for schools and

hospitals (the primary one being budget allocations).

9

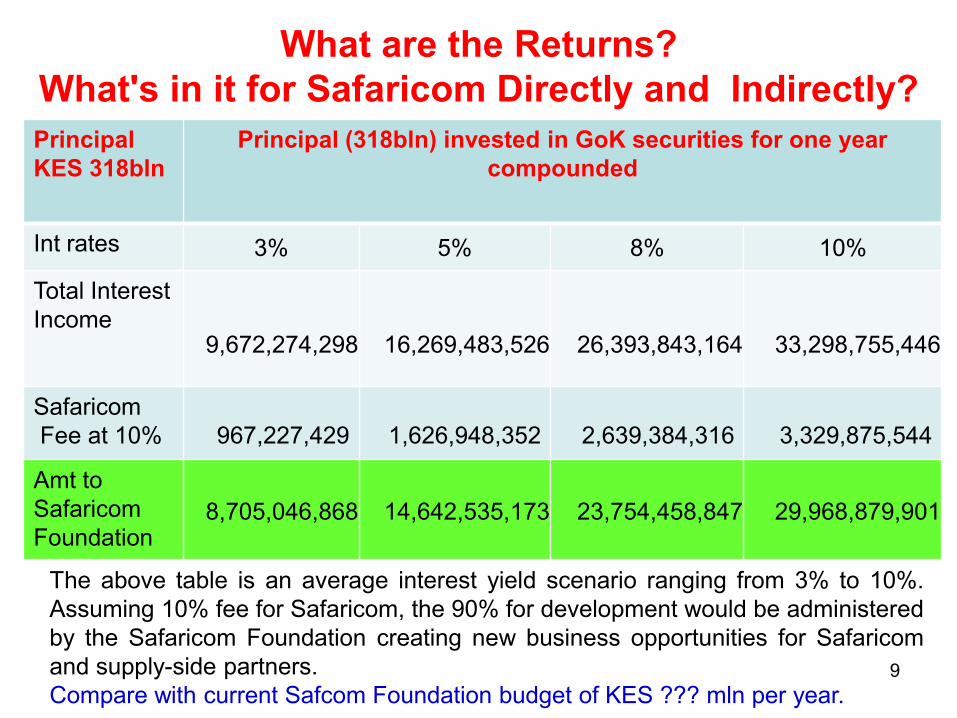

What are the Returns?

What's in it for Safaricom Directly and Indirectly?

Principal

KES 318bln

Principal (318bln) invested in GoK securities for one year

compounded

Int rates 3% 5% 8% 10%

Total Interest

Income9,672,274,298 16,269,483,526 26,393,843,164 33,298,755,446

Safaricom

Fee at 10% 967,227,429 1,626,948,352 2,639,384,316 3,329,875,544

Amt to

Safaricom

Foundation8,705,046,868 14,642,535,173 23,754,458,847 29,968,879,901

The above table is an average interest yield scenario ranging from 3% to 10%.

Assuming 10% fee for Safaricom, the 90% for development would be administered

by the Safaricom Foundation creating new business opportunities for Safaricom

and supply-side partners.

Compare with current Safcom Foundation budget of KES ??? mln per year.

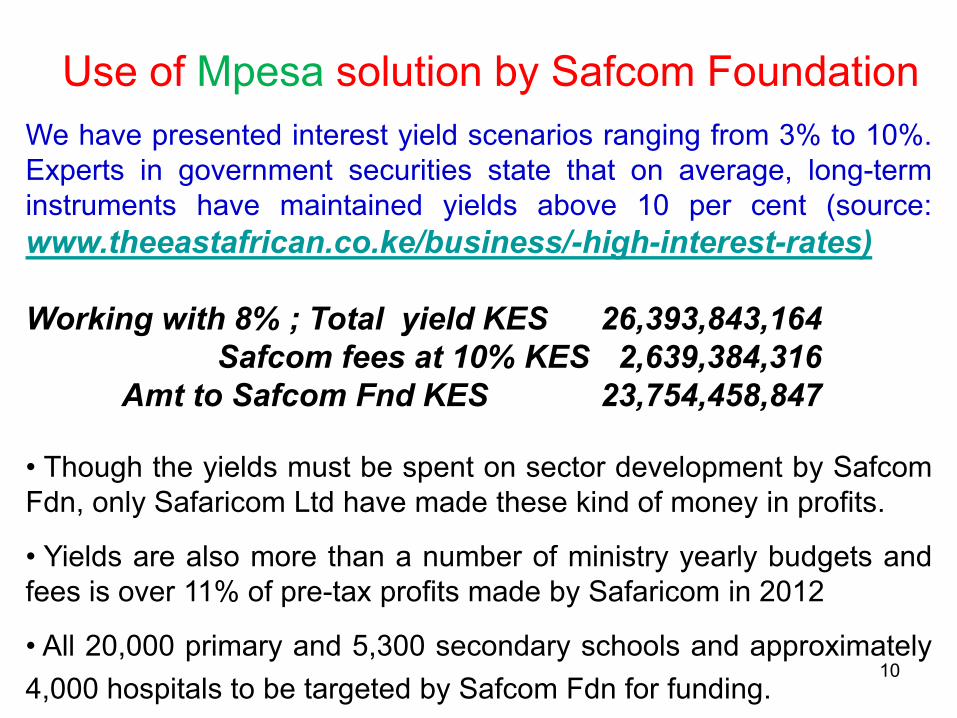

Use of Mpesa solution by Safcom Foundation

10

We have presented interest yield scenarios ranging from 3% to 10%.

Experts in government securities state that on average, long-term

instruments have maintained yields above 10 per cent (source:

www.theeastafrican.co.ke/business/-high-interest-rates)

Working with 8% ; Total yield KES 26,393,843,164

Safcom fees at 10% KES 2,639,384,316

Amt to Safcom Fnd KES 23,754,458,847

• Though the yields must be spent on sector development by Safcom

Fdn, only Safaricom Ltd have made these kind of money in profits.

• Yields are also more than a number of ministry yearly budgets and

fees is over 11% of pre-tax profits made by Safaricom in 2012

• All 20,000 primary and 5,300 secondary schools and approximately

4,000 hospitals to be targeted by Safcom Fdn for funding.

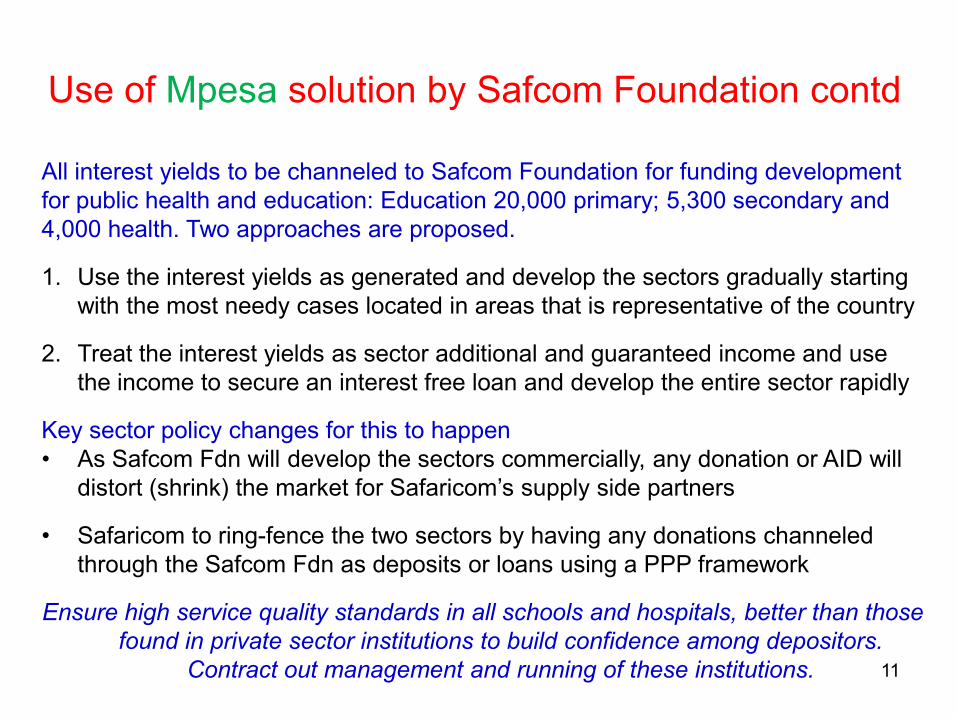

Use of Mpesa solution by Safcom Foundation contd

11

All interest yields to be channeled to Safcom Foundation for funding development

for public health and education: Education 20,000 primary; 5,300 secondary and

4,000 health. Two approaches are proposed.

1. Use the interest yields as generated and develop the sectors gradually starting

with the most needy cases located in areas that is representative of the country

2. Treat the interest yields as sector additional and guaranteed income and use

the income to secure an interest free loan and develop the entire sector rapidly

Key sector policy changes for this to happen

• As Safcom Fdn will develop the sectors commercially, any donation or AID will

distort (shrink) the market for Safaricom’s supply side partners

• Safaricom to ring-fence the two sectors by having any donations channeled

through the Safcom Fdn as deposits or loans using a PPP framework

Ensure high service quality standards in all schools and hospitals, better than those

found in private sector institutions to build confidence among depositors.

Contract out management and running of these institutions.

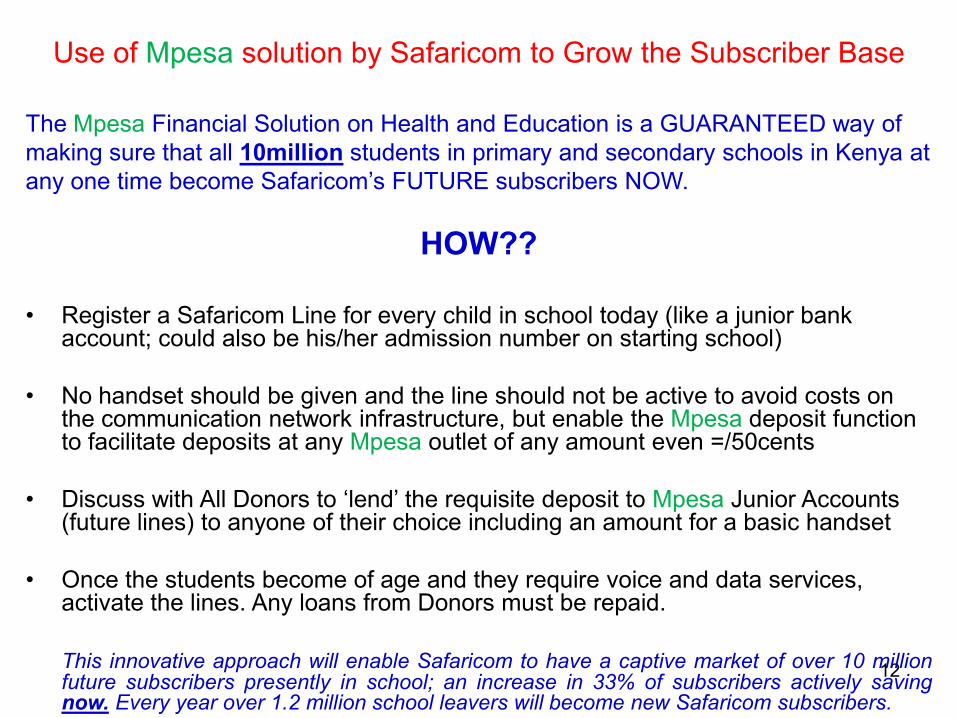

Use of Mpesa solution by Safaricom to Grow the Subscriber Base

12

The Mpesa Financial Solution on Health and Education is a GUARANTEED way of

making sure that all 10million students in primary and secondary schools in Kenya at

any one time become Safaricom’s FUTURE subscribers NOW.

HOW??

• Register a Safaricom Line for every child in school today (like a junior bank account; could also be his/her admission number on starting school)

• No handset should be given and the line should not be active to avoid costs on the communication network infrastructure, but enable the Mpesa deposit function to facilitate deposits at any Mpesa outlet of any amount even =/50cents

• Discuss with All Donors to ‘lend’ the requisite deposit to Mpesa Junior Accounts (future lines) to anyone of their choice including an amount for a basic handset

• Once the students become of age and they require voice and data services, activate the lines. Any loans from Donors must be repaid.

This innovative approach will enable Safaricom to have a captive market of over 10 millionfuture subscribers presently in school; an increase in 33% of subscribers actively savingnow. Every year over 1.2 million school leavers will become new Safaricom subscribers.

13

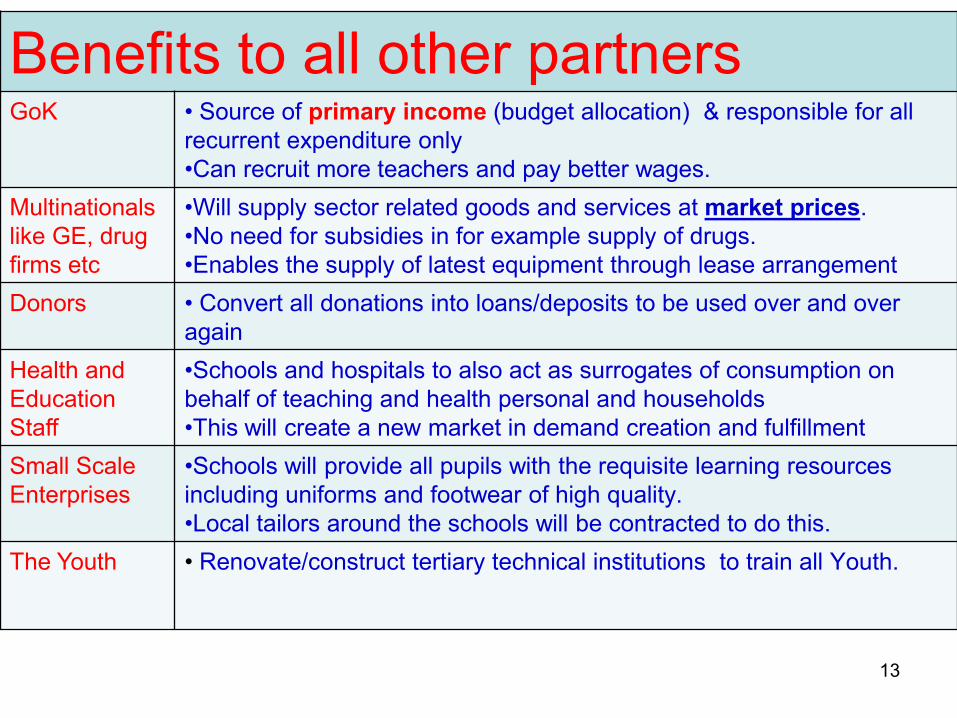

Benefits to all other partners GoK • Source of primary income (budget allocation) & responsible for all

recurrent expenditure only

•Can recruit more teachers and pay better wages.

Multinationals

like GE, drug

firms etc

•Will supply sector related goods and services at market prices.

•No need for subsidies in for example supply of drugs.

•Enables the supply of latest equipment through lease arrangement

Donors • Convert all donations into loans/deposits to be used over and over

again

Health and

Education

Staff

•Schools and hospitals to also act as surrogates of consumption on

behalf of teaching and health personal and households

•This will create a new market in demand creation and fulfillment

Small Scale

Enterprises

•Schools will provide all pupils with the requisite learning resources

including uniforms and footwear of high quality.

•Local tailors around the schools will be contracted to do this.

The Youth • Renovate/construct tertiary technical institutions to train all Youth.

In ConclusionFramework for Discussion and Development

Position the idea as a new development model for Kenya and SSA in

health and education and engage all the relevant partners.

Safaricom as lead investor to host conversations with the partners

These Partners are

1.Safaricom’s subscribers

2.Vodafone mobile money

3.Firms that supply sector-related goods and services.

4.Government leadership both local and global

5.Donors and foundations

This Mpesa Financial Solution will make Safaricom not just the

Better Option but the Only Option

Thank you. 14