Missouri Financial Accounting Manual · The Missouri Financial Accounting Manual’s ... Project...

58

MISSOURI FINANCIAL ACCOUNTING MANUAL Missouri Department of Elementary and Secondary Education November 2017 An Overview for School Bookkeeping and Finance Staff of Coding Basics Presented by: Tammy Lehmen Director, School Finance

Transcript of Missouri Financial Accounting Manual · The Missouri Financial Accounting Manual’s ... Project...

MISSOURI FINANCIAL ACCOUNTING MANUAL

Missouri Department of Elementary and Secondary Education November 2017

An Overview for School Bookkeeping and Finance Staff of

Coding Basics

Presented by: Tammy Lehmen

Director, School Finance

Missouri Financial Accounting Manual

The Missouri Financial Accounting Manual’s purpose is to provide guidelines for the accounting of Revenue, Expenditures, and Balance Sheet items. This is to ensure all school districts/LEAs are using the same structure to allow for Federal and State financial reporting, as well as, various calculations to be performed to analyze financial data of all districts/LEAs.

2

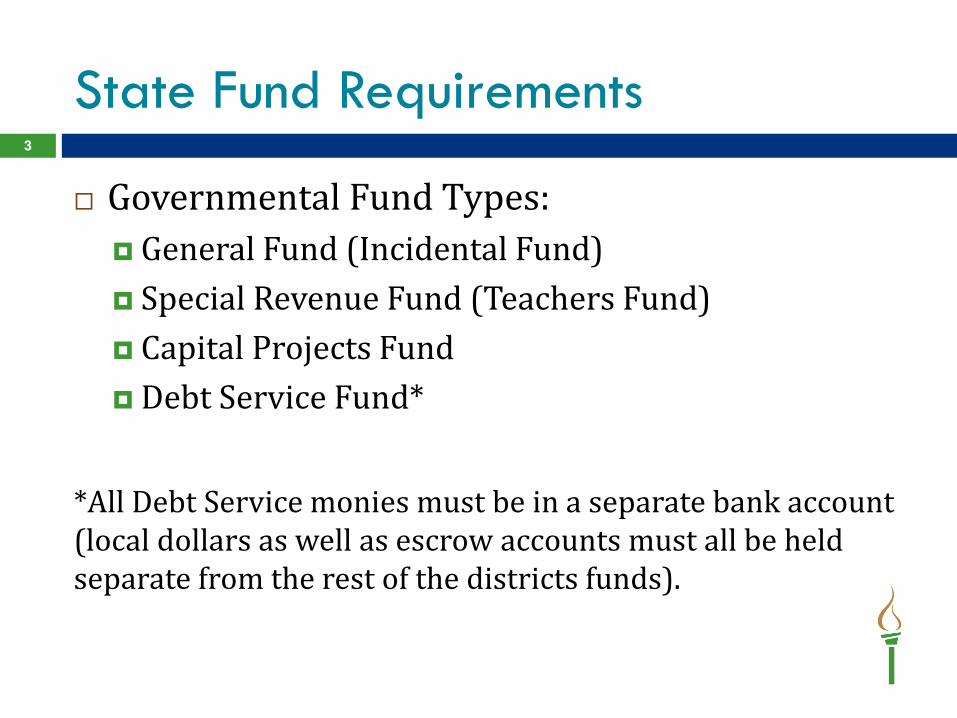

State Fund Requirements

Governmental Fund Types: General Fund (Incidental Fund) Special Revenue Fund (Teachers Fund) Capital Projects Fund Debt Service Fund*

*All Debt Service monies must be in a separate bank account (local dollars as well as escrow accounts must all be held separate from the rest of the districts funds).

3

State Fund Requirements

The General Fund also commonly includes the following sub-funds: Proprietary Funds School Food Services Self-Funded Insurance Plans Cafeteria Plan Funds

Fiduciary Funds Student Activities Scholarship Funds

4

Uses of Each Fund

Special Revenue (Teachers) Fund Used to account for revenue sources legally

restricted to expenditures for the purpose of teachers’ salaries and benefits and tuition payments to other school districts.

Capital Projects Fund Used to account for all facility acquisition,

construction, equipment, lease purchase principal and interest payments and other capital outlay expenditures.

5

Uses of Each Fund

Debt Service Fund Used to account for monies used to retire bond

debt. The General (Incidental)Fund

Used to account for all financial resources except those required to be accounted for in another fund listed previously.

6

Moving Money Between Funds

Money CANNOT just be moved between funds. Money can only be moved if there is an allowable transfer to do so.

Allowed transfers can be found on the School Finance Topics and Procedures webpage under the Coding Guidance section.

https://dese.mo.gov/financial-admin-services/school-finance/finance-topics-procedures

7

Allowed Transfers

• Area Vocational-Technical Schools • Grant Match • DNR Energy Conservation Loan • Food Services • Student Activities • $162,326 or 7% x SAT x WADA • Capital Projects Fund Interest • Unspent Bond Proceeds • Capital Projects Unrestricted Funds • FY06 Designated Levy or 5% SAT x WADA • Lease Purchase prior 01/01/1997 • Guaranteed Energy Performance Savings

8

Securing District Funds

Pursuant to Section 110.010, RSMo, the public funds of every school district and LEA which are deposited in any banking institution acting as a legal depositary of the funds under the statutes of Missouri shall be secured by the deposit of securities of the kind and character prescribed by Section 30.270, RSMo.

9

Chart of Accounts 10

New Chart of Account Changes Starting FY 2019

Order of items in the district/charter schools account entries will vary by vendor.

Fund has always been stated to be 3 digits. Not all vendors had this set up as three digits. DESE will only be collecting 1 digit for the Fund in the

ASBR.

11

Chart of Account Changes

New Chart of Account Changes Starting FY 2019

Order of items in the district/charter schools account entries will vary by vendor.

Fund has always been stated to be 3 digits. Not all vendors had this set up as three digits. DESE will only be collecting 1 digit for the Fund in the

ASBR.

12

Chart of Account Changes

Fund Code – 3 Digits – Only 1 Digit Collected on the ASBR The Fund Code represents the Fund in which the revenue

or expenditure is occurring. General Fund - 1 There could be sub funds to the General Fund, which need

to be reported as Fund 1. Teachers Fund - 2 Debt Service Fund - 3 Capital Projects Fund - 4

There is no change to the Fund Code. The change is that the Fund Code will actually be in the ASBR upload file.

13

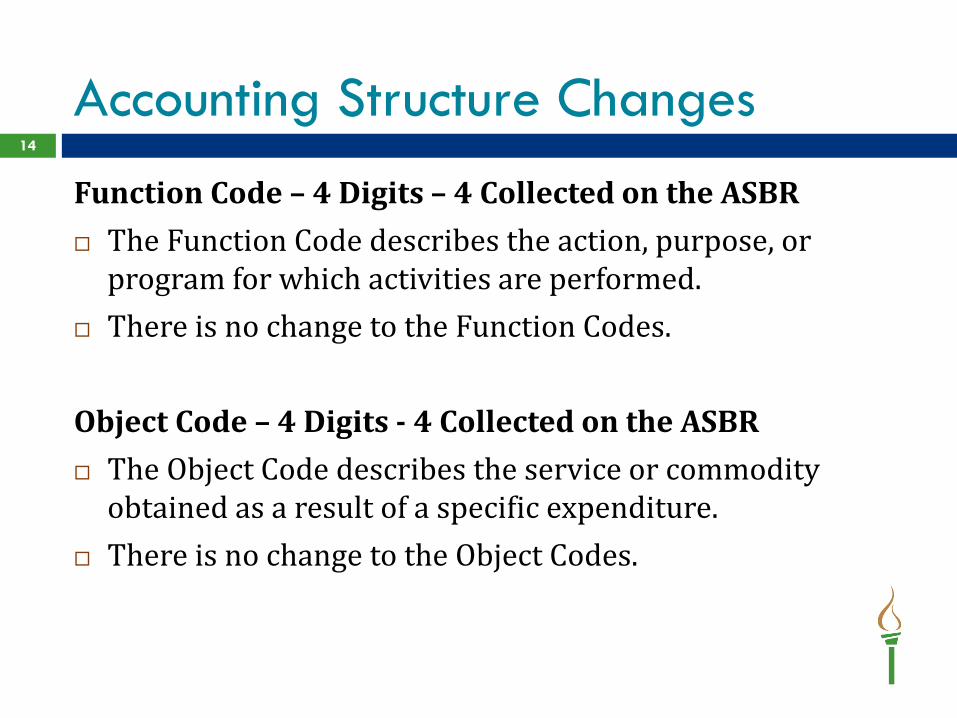

Accounting Structure Changes

Function Code – 4 Digits – 4 Collected on the ASBR The Function Code describes the action, purpose, or

program for which activities are performed. There is no change to the Function Codes. Object Code – 4 Digits - 4 Collected on the ASBR The Object Code describes the service or commodity

obtained as a result of a specific expenditure. There is no change to the Object Codes.

14

Accounting Structure Changes

Location Code – 4 Digits - 4 Collected on the ASBR The Location Code refers to individual campuses within a

district/charter school and individual components within the administration, school service, and maintenance and operation divisions. The district/charter school must use DESE’s core data building codes to distinguish separate campuses where student data is reported. The district/charter school may assign other codes that it wishes for its other operational or “cost” units.

The Location Code should tie to each of the district’s/charter school’s buildings. Example: 4020 – ABC Elementary 4030 – GHI Elementary 3020 – MNO Middle School 1050 – PQR High School

15

Accounting Structure Changes

A list of Revenue, Function, and Object Codes required to have expenditures reported at a building level can be found at: https://dese.mo.gov/financial-admin-services/school-finance/fy-2019-accounting-changes

16

Accounting Structure Changes

Source of Funds – 1 Digit - 1 Collected on the ASBR The Source of Funds Code is used to identify a subset of revenue

used to fund a specific expenditure. Districts/charter schools must assign a Source of Funds Code to expenditures funded by each type of revenue as noted below:

“1” for expenditures funded with Local Revenue (includes Non-Current Sources of Revenue)

“2” for expenditures funded with County Revenue “3” for expenditures funded with State Revenue “4” for expenditures funded with Federal Revenue

17

Accounting Structure Changes

Project Code – 5 Digits -5 Collected on the ASBR The Project Code is used to identify an expenditure paid

for with a specific source of revenue or part of a specific grant. The Project Code may also be used to aggregate costs across subfunds, such as teachers’ salaries and supplies, to construct the reports necessary for various granting agencies. The district/charter schools must use DESE’s assigned Project Codes if one is assigned for a specific Revenue Source.

18

Accounting Structure Changes

Project Code – 5 Digits -5 Collected on the ASBR

19

Accounting Structure Changes

Range of Codes Reserved for DESE Assignment

Range of Codes Open for District/Charter School Use for Other Purposes

00001-09999

10000-19999*

20000-29999*

30000-39999

40000-49999

50000-59999

60000-69999*

70000-79999

80000-89999*

90000-99999

*If a district choses to use a project code in this range it is encouraged to follow the structure shown in the Missouri Financial Accounting Manual to eliminate major changes if DESE must assign a Project Code in this range at a future date.

List of Project Codes can be found at: https://dese.mo.gov/financial-admin-services/school-finance/fy-2019-accounting-changes

20

Accounting Structure Changes

The general ledger (Balance Sheet) is comprised of assets, liabilities, and fund balances/net position.

General Ledger 21

General Ledger

The general ledger or balance sheet accounts are used to track financial transactions for each fund.

Asset codes begin with a 1xxx. Liability codes begin with a 2xxx. Fund balances/ Net Position codes begin with a

3xxx.

22

General Ledger

All entries a district/charter does will involve a general ledger code due to the requirement to use a Double-Entry Accounting System.

Normal account fund balances. Assets - Debit Liabilities - Credit Fund Balance - Credit Revenues - Credit Expenses - Debit

23

General Ledger 24

Assets = Liabilities + Fund Balance

Debit for Increase

Credit for

Decrease

Debit for

Decrease

Credit for

Increase

Debit for

Decrease

Credit for

Increase

Revenues Expenses Debit

for Decrease Credit for Increase

Debit for Increase

Credit for Decrease

General Ledger

Each separate bank account a district/charter has should be shown separately on the general ledger.

Each bank account should also be balanced each month to bank statements. Do not combined accounts and balance all

accounts in a fund as one. Even bond escrow accounts should be shown

separately on a district’s general ledger. Debt Service Funds must be held in a separate

bank account.

25

Revenue Coding 26

Revenue Coding

Revenues are broken down into five sections Local Revenues (Revenue Codes 5111-5199) County Revenues (Revenue Codes 5211-5299) State Revenues (Revenue Codes 5311-5399) Federal Revenues (Revenue Codes 5411-5499) Other Revenues (Revenue Codes 5611-5898)

Only code to Revenue Codes found in the Missouri Financial Accounting Manual.

27

Revenue Coding

Class codes (codes ending in zero) are for subtotaling purposes only and are not used for posting transactions

Subclass codes (codes ending in zero) are for subtotaling purposes only and are not used for posting transactions

Detail codes are used for posting transactions No revenue code has their own corresponding,

separate, specific function/program code

28

Revenue Coding

A description of any placement requirements can be found by each revenue code in the “Placement” column. Description of any limitations on placement Funds the revenue may be placed in. Other placement requirements

29

Common Revenue Coding Errors

Not following the “Refund and Reimbursement Policy” on the Finance Topics and Procedures webpage.

Refunds and Reimbursements - Outgoing from District Payments made by an LEA correcting or adjusting

previous revenues that were recorded in: Revenue accounts in the current year should be debited to the

same revenue account (reduces apparent revenue). Revenue account of a previous year should be debited to current

year expense (function code 2329, Executive Administration or function code 2529, Business/Central Services, object code 6398, Other Expenses).

30

Common Revenue Coding Errors

Miscoding revenue as “Other State – 5397” or “Other Federal – 5497”. To be considered state money a district would have

to have received the money from the State of Missouri. Just because Missouri is in the name does not mean the

money is from the State of Missouri. Most state deposits can be found on the State Vendor

Payment Site. https://www.vendorservices.mo.gov/vendorservices/Portal/Default.aspx

31

Common Revenue Coding Errors

To be considered federal money a district would have to have received the money from the Federal Government. Just because Federal is in the name does not mean the

money is from the Federal Government. School Finance is not aware of a federal site that districts

can look up federal payments.

32

Coding Expenditures

A major purpose of the accounting code structure is to establish the standard school district fiscal accounting system required for Missouri schools. The funds, chart of accounts, revenue, function, and object codes are to be uniformly used by all school districts in accordance with generally accepted accounting principles.

34

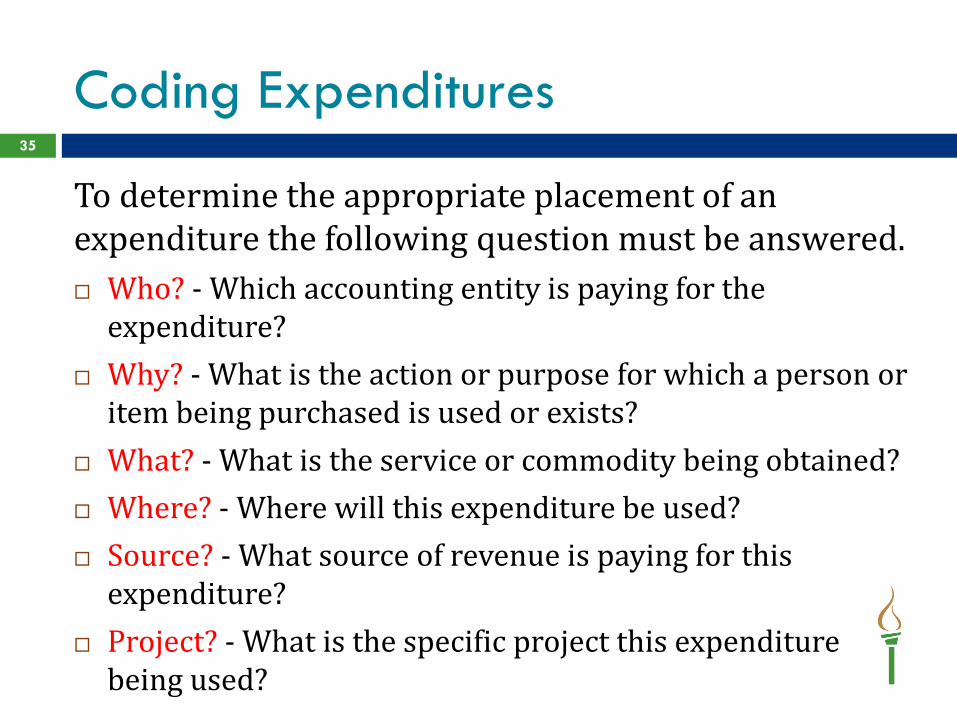

Coding Expenditures

To determine the appropriate placement of an expenditure the following question must be answered. Who? - Which accounting entity is paying for the

expenditure? Why? - What is the action or purpose for which a person or

item being purchased is used or exists? What? - What is the service or commodity being obtained? Where? - Where will this expenditure be used? Source? - What source of revenue is paying for this

expenditure? Project? - What is the specific project this expenditure

being used?

35

Coding Expenditures

Fund: The first question to ask is Who? - “Which

accounting entity is paying for the expenditure?” General Fund Teachers Fund Debt Service Capital Projects Food Service Student Activities Other……

36

Coding Expenditures

Function: The second question to ask is Why? - “What is the

action or purpose for which a person or item being purchased is used or exists?” Instruction (Instruction of Students) – 1xxx

Regular Instruction – 1111 to 1151 Other Regular Instruction – 1191 to 1192 Special Programs – 1211 to 1224 Supplemental Instruction – 1251 to 1254 Bilingual – 1271 Early Childhood Special Education – 1281 Career Education Programs – 1311 to 1391

37

Coding Expenditures

Instruction (Instruction of Students) – 1xxx (continued)

School-Sponsored Co-Curricular Activities – 1411 to 1491

Adult Education Programs - 1611 to 1691 Payments to Other Districts – 1911 to 1913 Area Career Center Fees – 1921 Tuition, Special Education Services – 1931 to 1933 Contracted Educational Services – 1941 to 1942

38

Coding Expenditures

Supporting Services – 2xxx Support Services – Pupils – 2111 to 2191 Support Services – Instructional Staff – 2211 to 2291 Support Services – General Administration – 2311 to

2331 Support Services – Building Level Administration –

2411 to 2491 Business Support Services – 2511 to 2549 Pupil Transportation – 2551 to 2559 Food Services – 2561 to 2569 Internal Services – 2571 to 2591 Support Services – Central Office – 2611 to 2691 Other Supporting Services – 2911

39

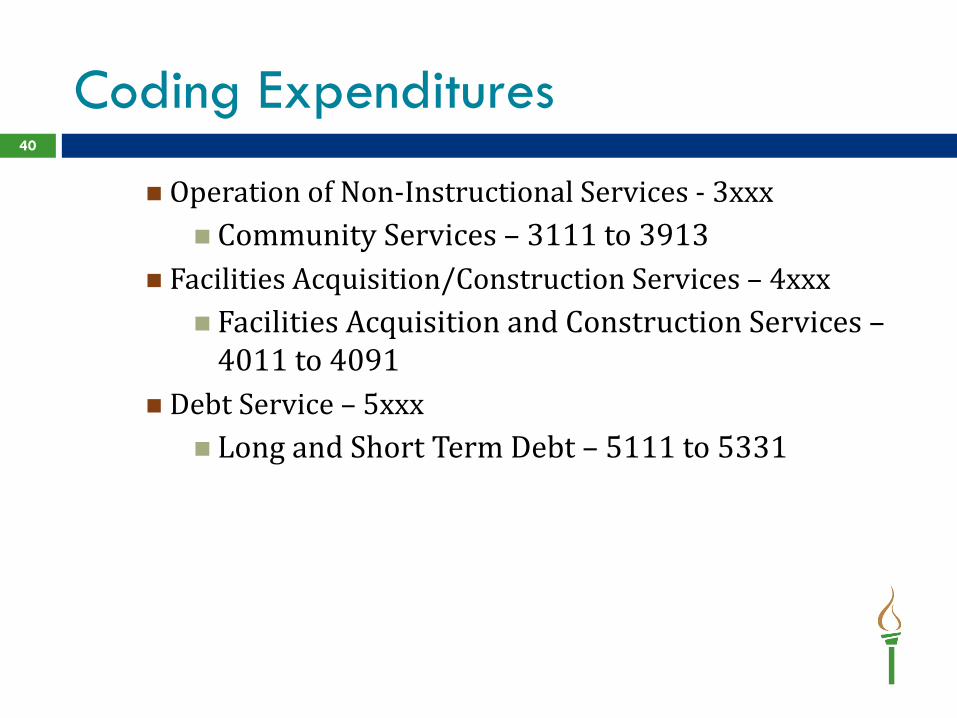

Coding Expenditures

Operation of Non-Instructional Services - 3xxx Community Services – 3111 to 3913

Facilities Acquisition/Construction Services – 4xxx Facilities Acquisition and Construction Services –

4011 to 4091 Debt Service – 5xxx

Long and Short Term Debt – 5111 to 5331

40

Coding Expenditures

Function codes that are to be used to code expenditures are the Detail codes. Class and Subclass codes are meant for subtotaling

purposes. This is becoming less necessary as time and coding requirements have become more detailed.

Detail codes end in a number between 1 and 9. Never use a code that ends in a 0. Never use a code not found in the Missouri

Financial Accounting Manual.

41

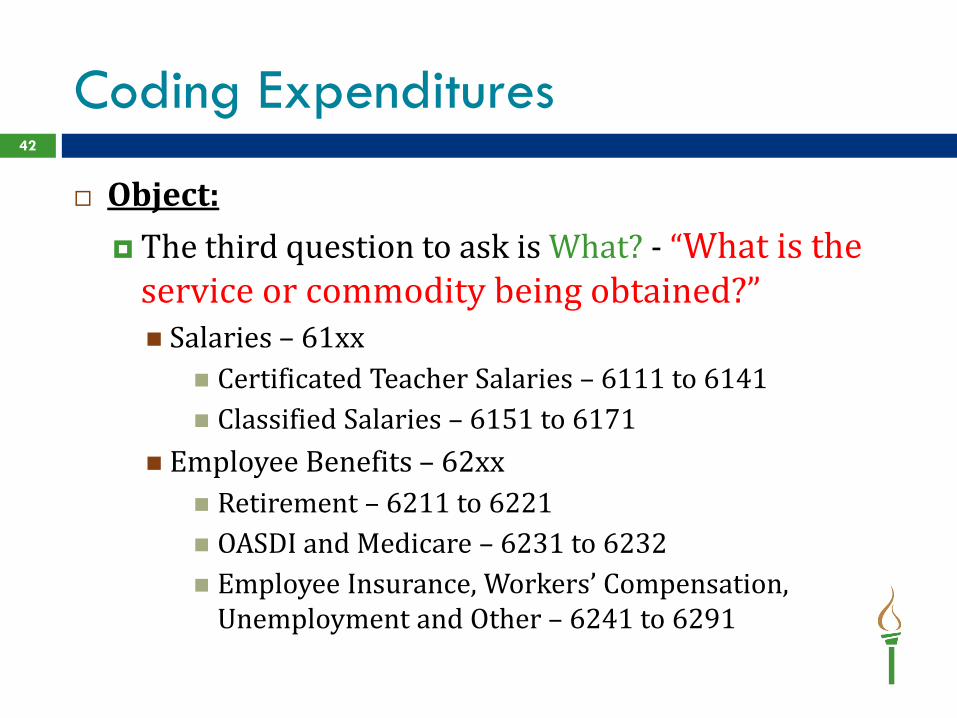

Coding Expenditures

Object: The third question to ask is What? - “What is the

service or commodity being obtained?” Salaries – 61xx

Certificated Teacher Salaries – 6111 to 6141 Classified Salaries – 6151 to 6171

Employee Benefits – 62xx Retirement – 6211 to 6221 OASDI and Medicare – 6231 to 6232 Employee Insurance, Workers’ Compensation,

Unemployment and Other – 6241 to 6291

42

Coding Expenditures

Purchased Services – 63xx Professional and Technical Services – 6311 to 6319 Property Services – 6331 to 6339 Transportation Services – 6341 to 6349 Insurance – Other Than Employee Benefits – 6351 to

6359 Communication – 6361 to 6363 Dues and Memberships 6391 to 6398

Supplies and Materials - 64xx General Supplies – 6411 to 6412 Textbooks, Library Books, and Periodicals – 6431 to

6451 Library Books – 6441

43

Coding Expenditures

Supplies and Materials - 64xx (Continued)

Warehouse Inventory Adjustment – 6461 Food – 6471 Energy – 6481 to 6486 Other Supplies - 6491

Capital Outlay – 65xx Land – 6511 Buildings – 6521 to 6531 Equipment – 6541 to 6544 Vehicles – 6551 to 6553 Other Capital Outlay - 6591

44

Coding Expenditures

Long and Short Term Debt – 66xx Principal – 6611 to 6614 Interest – 6621 to 6624 Fees – 6631 to 6634

45

Coding Expenditures

Location: The fourth question to ask is Where? - “Where will

this expenditure be used?” Example:

46

Code Location Code 4020 ABC Elementary 4025 DEF Elementary 4030 GHI Elementary 3000 JKL Middle School 3020 MNO Middle School 1050 PQR High School 0001-0999 Free for district use for other location or operational cost units.

Coding Expenditures

Source of Funds: The fifth question to ask is the Source? - “What

source of revenue is paying for this expenditure?” “1” for expenditures funded with Local (Includes Non-

Current Sources of Revenue) “2” for expenditures funded with County Revenue “3” for expenditures funded with State Revenue “4” for expenditures funded with Federal Revenue

47

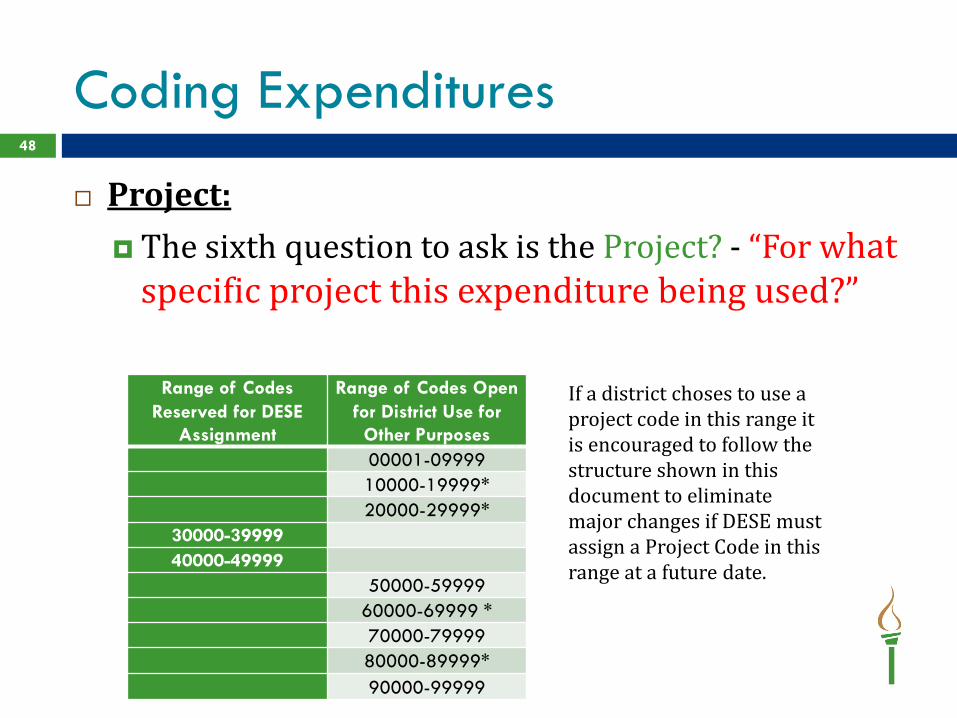

Coding Expenditures

Project: The sixth question to ask is the Project? - “For what

specific project this expenditure being used?”

48

Range of Codes Reserved for DESE

Assignment

Range of Codes Open for District Use for

Other Purposes 00001-09999 10000-19999* 20000-29999*

30000-39999 40000-49999

50000-59999 60000-69999 *

70000-79999 80000-89999*

90000-99999

If a district choses to use a project code in this range it is encouraged to follow the structure shown in this document to eliminate major changes if DESE must assign a Project Code in this range at a future date.

Coding Expenditures

Result

49

Fund Function Object Location Source Project Code

Coding Expenditures 50

Importance of Proper Coding 51

Importance of Proper Coding

Must code revenue and expenditures according to the Missouri Financial Accounting Manual.

Do not use a code that is not in the manual. Do not use a code that states it is not for posting

transactions.

52

Importance of Proper Coding

Why does this matter? Incorrect reporting occurs. Incorrectly calculates various percentages and numbers

which impact the district/charter school. Hard to compare districts’/charter schools’ data when

everyone is not reporting the same. Information publicly available.

More work trying to complete annual reporting of: ASBR FERs MOEs

53

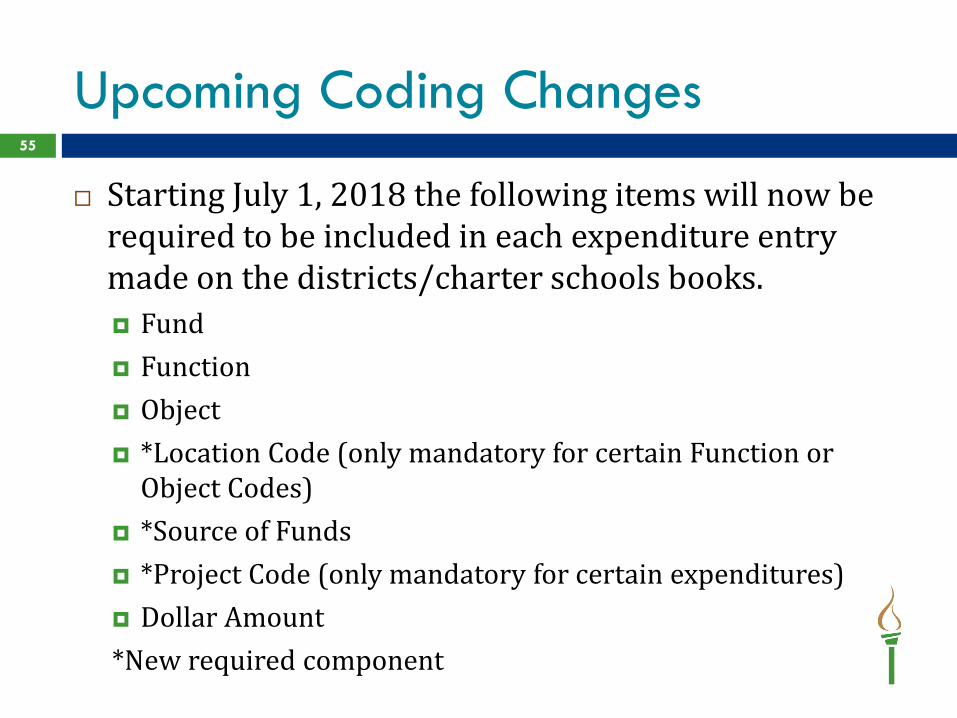

Upcoming Coding Changes 54

Upcoming Coding Changes

Starting July 1, 2018 the following items will now be required to be included in each expenditure entry made on the districts/charter schools books. Fund Function Object *Location Code (only mandatory for certain Function or

Object Codes) *Source of Funds *Project Code (only mandatory for certain expenditures) Dollar Amount *New required component

55

Upcoming Coding Changes

Questions regarding the new required components: We will be discussing internally questions that

districts ask and will be publishing future guidance.

56

School Finance 573-751-0357 57

Name Title

David Tramel David.Tramel @dese.mo.gov

Coordinator, Financial and Administrative Services

Tammy Lehmen [email protected]

Director, School Finance Contact for districts in counties 048 & Kansas City Charters, 055-079 & 347-347

Debra Clink [email protected]

Student Transportation Manager Contact for districts in counties 080-115 & St Louis Charters

Taylor Doerhoff [email protected]

School Finance Consultant Contact for districts in counties 001-047 & 049-054

Questions? 58