MINISTÉRIO DAS FINANÇAS - Portugal · MINISTÉRIO DAS FINANÇAS 2 1. On the way to become the...

39

MINISTÉRIO DAS FINANÇAS 1 MINISTÉRIO DAS FINANÇAS Portugal: restoring credibility and confidence Vítor Gaspar Washington March 19, 2012

Transcript of MINISTÉRIO DAS FINANÇAS - Portugal · MINISTÉRIO DAS FINANÇAS 2 1. On the way to become the...

MINISTÉRIO DAS FINANÇAS 1

MINISTÉRIO DAS FINANÇAS

Portugal: restoring

credibility and confidence

Vítor Gaspar

Washington

March 19, 2012

MINISTÉRIO DAS FINANÇAS 2

1. On the way to become the difficult Portuguese case

2. The Economic Adjustment Program

3. Fiscal consolidation

4. Deleveraging and financial stability

5. Structural transformation

6. Conclusion: how will it work?

Outline

MINISTÉRIO DAS FINANÇAS 3

ON THE WAY TO BECOME THE

DIFFICULT PORTUGUESE CASE

MINISTÉRIO DAS FINANÇAS 4

Portugal’s imbalances exposed in the context of the

economic and financial crisis

Macro-

economic

imbalances

and

structural

weaknesses

that have

been

accumulated

over more

than a

decade

3. Anemic economic growth

and low productivity

1. Unsustainable public

finances

2. Over-indebtedness

10-year Government bond yields

Spread against Germany in basis points

Source: Bloomberg

0

200

400

600

800

1000

1200Austria Italy

Belgium Spain

France Ireland

Netherlands Portugal

Finland Greece

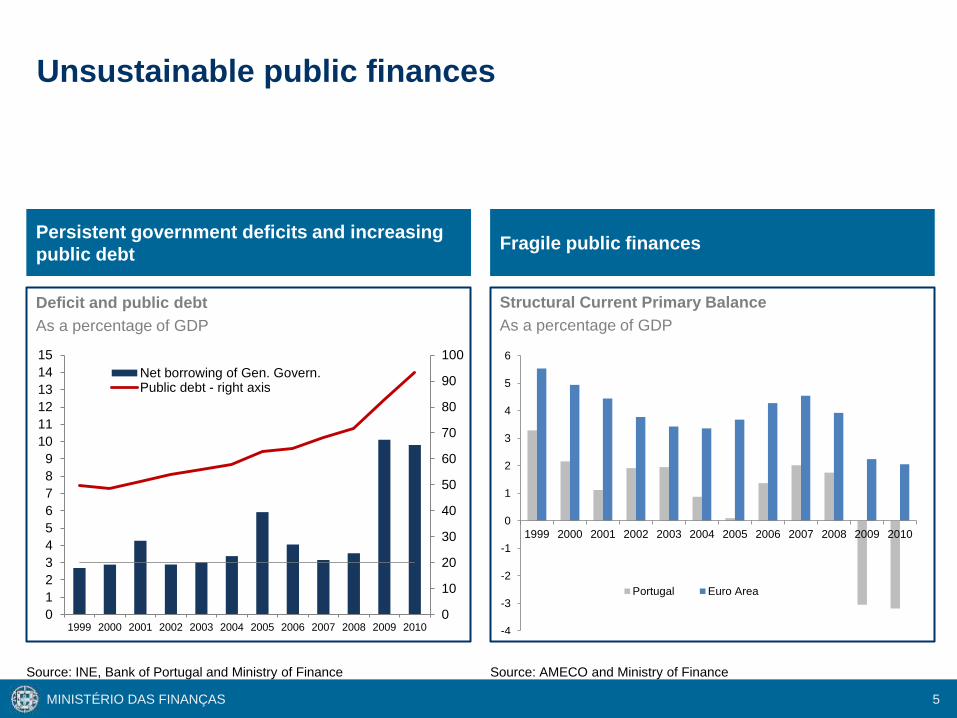

MINISTÉRIO DAS FINANÇAS 5

Persistent government deficits and increasing

public debt Fragile public finances

Structural Current Primary Balance

As a percentage of GDP

Unsustainable public finances

Deficit and public debt

As a percentage of GDP

Source: AMECO and Ministry of Finance Source: INE, Bank of Portugal and Ministry of Finance

-4

-3

-2

-1

0

1

2

3

4

5

6

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Portugal Euro Area

0

10

20

30

40

50

60

70

80

90

100

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Net borrowing of Gen. Govern.Public debt - right axis

MINISTÉRIO DAS FINANÇAS 6

0

20

40

60

80

100

120

140

160

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Non-financial corporations

Households (a)

0

50

100

150

200

250

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Increasing indebtedness of the private sector Increasing external debt

Portuguese gross external debt

As a percentage of GDP

Debt accumulation by households and firms

Debt of the Households and Non-financial Corporations

As a percentage of GDP

Source: Bank of Portugal

(*) Financial Debt

Source: Bank of Portugal

MINISTÉRIO DAS FINANÇAS 7

Insufficient attraction of direct foreign

investment

Capital accumulation in non-tradable

goods and services sectors

Lack of competition in several sectors

Low levels of innovation and

productivity growth

High levels of youth and long-term

unemployment

Restrictions on the market for

corporate control

Protection of several sectors of the

economy

Weak conditions to entrepreneurial

activity

Poor functioning of the justice

system

Rigidity of the labor market

Insufficient conditions to foster economic growth

Obstacles Consequences

MINISTÉRIO DAS FINANÇAS 8

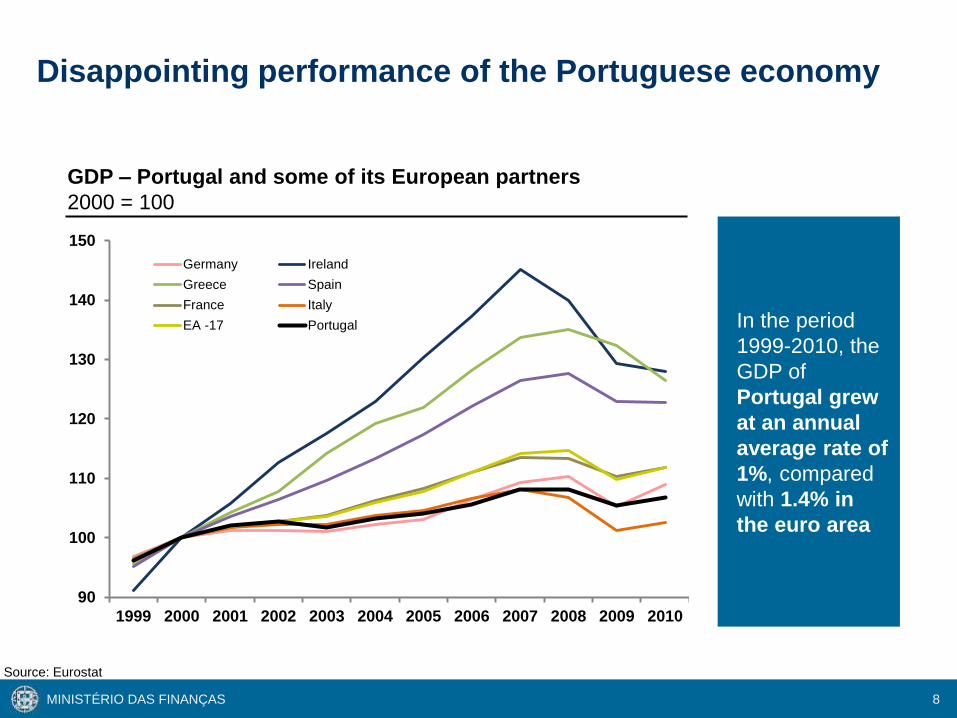

Disappointing performance of the Portuguese economy

Source: Eurostat

In the period

1999-2010, the

GDP of

Portugal grew

at an annual

average rate of

1%, compared

with 1.4% in

the euro area

GDP – Portugal and some of its European partners

2000 = 100

90

100

110

120

130

140

150

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Germany Ireland

Greece Spain

France Italy

EA -17 Portugal

MINISTÉRIO DAS FINANÇAS 9

THE ECONOMIC

ADJUSTMENT PROGRAM

MINISTÉRIO DAS FINANÇAS 10

38,5

14,9

24,6

Already disbursed(1)

4th Disbursement (April 2012)

To be disbursed

15,6

9,8

13,1

IMF

EFSF

EFSM

After the 3rd Review (completed in

February 28) the program

implementation was on track

Adjustment Program agreed with the IMF, EC and ECB in

April 2011

The Economic Adjustment Program

covers the financing needs of General

Government for the period 2011 to

mid-2014.

It comprises a financial package

amounting to EUR 78 billion in loans,

including EUR 12 billion for banking

sector recapitalization.

Each disbursement depends on the

technical mission’s quarterly

assessment about Portugal’s

performance on the implementation of

the Adjustment Program.

(1) Net issuances

Source: IGCP, February 2012

Financial package

EUR Billions Key facts

Statement by the EC, ECB, and IMF on the Third Review Mission to Portugal: http://www.imf.org/external/np/sec/pr/2012/pr1259.htm

(1)

MINISTÉRIO DAS FINANÇAS 11

A balanced Program to cope with the major challenges of

the Portuguese economy

The Economic

Adjustment Program

protects

Government

financing from

market pressures,

allowing an orderly

adjustment of

imbalances and

time to build up

confidence and

credibility.

Fiscal consolidation

Putting fiscal policy on a sustainable path

Structural transformation

Implementing structural reforms to contribute to potential growth

Deleveraging and financial stability

Reduction of debt and financing needs of the economy

The Economic Adjustment Program

MINISTÉRIO DAS FINANÇAS 12

At the start

of the

Program (in

May 2011),

Portugal

faced a very

uncertain

outlook

Reducing uncertainty: Portugal is delivering in all fronts

Weakening of political

support for the Program

Unfavorable macro-economic

developments

Missing the fiscal targets

Uncertainty regarding the

stability of the financial sector

Insufficient pace of structural

reforms

Broad political consensus

Social support to the Program

Milder recession than expected in 2011

Stronger than expected external adjustment

Dynamic exports

Major reduction in overall and structural

deficits

Progress in institutional reforms

Increase in banks’ capital

Reduction of credit-to-deposit ratio

Increase in transparency: on-site inspections

Success of privatizations process

Labor market tripartite agreement

Broad range of implemented measures

1

2

3

4

5

Main risks Major outcomes

MINISTÉRIO DAS FINANÇAS 13

A turning point in Treasury financing Portuguese Treasury Bills

Note: Auction announcement date

Source: IGCP

3 months

6 months Weighted average yield

Percentage

5,0

4,9 4,9

5,0 5,0

4,9

5,0 4,9 5,0 5,0 5,0

4,9 4,9

4,3 4,3

4,1

3,8

5,0 5,0 5,0

5,2 5,3 5,3

4,7

4,5

4,3

5,0 4,9

3,6

3,8

4,0

4,2

4,4

4,6

4,8

5,0

5,2

5,4

11 months

12 months

MINISTÉRIO DAS FINANÇAS 14

0%

10%

20%

30%

40%

50%

60%

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

A turning point in Treasury financing Portuguese Treasury Bills

(1) Weighted average of 3 and 6 months auctions

Note: Auction announcement date

Source: IGCP

Weighted(1) Bid-to-cover ratio

Weighted(1) international allocation

Percentage

2012 2011 2012 2011

MINISTÉRIO DAS FINANÇAS 15

A turning point in Treasury financing Portuguese Treasury Bonds

Source: 2 years – Bloomberg; 5 and 10 years – Reuters

2 Years, yields

Percentage 5 Years, yields

Percentage

10 Years, yields

Percentage

0

5

10

15

20

25

0

5

10

15

20

25

0

5

10

15

20

25

MINISTÉRIO DAS FINANÇAS 16

FISCAL CONSOLIDATION

MINISTÉRIO DAS FINANÇAS 17

4,0

3,0

2,3 2,0

1,5 1,5 1,3 1,2

0,8

Portugal Greece Germany Ireland Italy UnitedKingdom

Euro area Spain France

Portugal’s structural adjustment stands out

(1) Change in General Government Cyclically Adjusted Balance

Source: IMF, “Fiscal Monitor Update”, January 2012

Structural adjustment 2010-2011(1)

Percentage points of potential GDP

MINISTÉRIO DAS FINANÇAS 18

10,3

9,0 8,6

8,0

5,7

4,3 4,0 3,9

1,1

Ireland Greece UnitedKingdom

Spain France Euro area Portugal Italy Germany

Overall deficit below the average for euro area

(1) IMF, Staff report for the fourth review, 29 November 2011

(2) IMF, Staff report for the fifth review, 30 November 2011

(3) Ministry of Finance, January 2012

Source: IMF, “Fiscal Monitor Update”, January 2012 (except for PT, IR and GR for which data is not available)

Overall deficit 2011

As percentage of GDP

(1) (2) (3)

Without the partial transfer of

banks’ pension funds, overall

deficit would be 7,5% of GDP

MINISTÉRIO DAS FINANÇAS 19

93

107

116 118

116 114

112

80

90

100

110

120

130

140

150

160

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

93

107

116 118

116 114

112

145

161

152 155

152

147

142

136

131

125

120

80

90

100

110

120

130

140

150

160

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

93

106

114 118

118 115

111

93

107

116 118

116 114

112

145

161

152 155

152

147

142

136

131

125

120 119 121 120 120 119 119 118

80

90

100

110

120

130

140

150

160

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Portuguese public debt is sustainable

(1) Staff report: Second Review Under the Extended Arrangement; December, 7 2011 (2) Staff report: Fifth Review Under the Stand-By Arrangement; November, 30 2011

(3) Staff report: Fourth Review Under the Extended Arrangement; November, 29 2011 (4) Staff report for the 2011 Article IV Consultation; June, 20 2001

Source: IMF

Government Debt Sustainability Framework: Baseline

As percentage of GDP

Portugal(1) Greece(2)

Ireland(3) Italy(4)

MINISTÉRIO DAS FINANÇAS 20

90

95

100

105

110

115

120

2010 2011 2012 2013 2014 2015 2016

93

107

112

115 114

113

93

105

114

118 118

115

113

90

95

100

105

110

115

120

2010 2011 2012 2013 2014 2015 2016

Portuguese public debt is sustainable

(1) Staff report: Second Review Under the Extended Arrangement; December, 7 2011 (2) Staff report: Fourth Review Under the Extended Arrangement; November, 29 2011

(3) Third Review; February 2012 (4) Staff report: Fifth Review Under the Extended Arrangement; February, 13 2012

Source: IMF

Government Debt Sustainability Framework: Baseline

As percentage of GDP

Portugal – 3rd Review(3) Ireland – 5th Review(4)

Portugal – 2nd Review(1) Ireland – 4th Review(2)

MINISTÉRIO DAS FINANÇAS 21

Important progress in the institutional reform front

NON-EXHAUSTIVE

Public

financial

manage

ment

Public

Adminis

tration

SOEs and

PPPs

Approval of the Spending

Commitments’ Control Law

Establishment of the Portuguese

Public Finance Council

Adjustment Program for the

Autonomous Region of Madeira

Creation of the new Tax and Customs

Authority

Improve budgetary control across all

levels of Public Administration

Strategy to clear stock of arrears

Changes to national law in order to include

the golden rule and the debt reduction rule

from the Treaty on Stability,

Coordination and Governance

Next challenges Major actions

Reduction of management positions

(27%) and administrative units in

central administration (40%)

Extend streamline measures to regional

and local administration

Significant cost reductions in SOE

(e.g.: voluntary redundancy programs)

Awarded a contract to review all PPP

contracts to a top-tier accounting firm

Operational balance for SOEs as a

whole by end-2012

New fiscally-prudent PPPs institutional

framework: enhanced role of MoF

MINISTÉRIO DAS FINANÇAS 22

DELEVERAGING AND

FINANCIAL STABILITY

MINISTÉRIO DAS FINANÇAS 23

-6000

-5000

-4000

-3000

-2000

-1000

0

1000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Capital account

Current and capital accounts

Current account

-9,9

-9,0

-6,7

-4,1

-3,4 -2,7

-2,2

-10,0

-6,4

-12,0

-10,0

-8,0

-6,0

-4,0

-2,0

0,0

2010 2011 2012 2013 2014 2015 2016

Stronger than expected external adjustment

(1) Bank of Portugal, BP Stat, February 2012;

(2) IMF, Staff report: Request for a Three-Year Arrangement Under the Extended Fund Facility, May 2012

Forecast(2)

Actual(1)

Better performance of current account than

initial projections External surplus in Q4

Balance of payments

EUR Millions

Current account

As a percentage of GDP

2010 2011

MINISTÉRIO DAS FINANÇAS 24

-8,4%

-4,0%

0,1%

-12,9%

-7,2%

-3,7%

0,5%

3,5%

-9,9%

-9,0%

-6,7%

-4,1% -3,4%

-2,7%

-10,0%

-6,4%

-14,0%

-12,0%

-10,0%

-8,0%

-6,0%

-4,0%

-2,0%

0,0%

2,0%

4,0%

t-1 t t+1 t+2 t+3 t+4

1st Program (1)(t=1978)

2nd Program (1)(t=1983)

3rd Program - Forecast (2)(t= 2011)

3rd Program - Actual (3)(t= 2011)

Fast correction of external imbalances under adjustment

programs

Current account

As a percentage of GDP, t = first year of the Adjustment Programs

(1) Bank of Portugal, Long series

(2) IMF, Staff report: Request for a Three-Year Arrangement Under the Extended Fund Facility, May 2012

(3) Bank of Portugal, BP Stat, February 2012

MINISTÉRIO DAS FINANÇAS 25

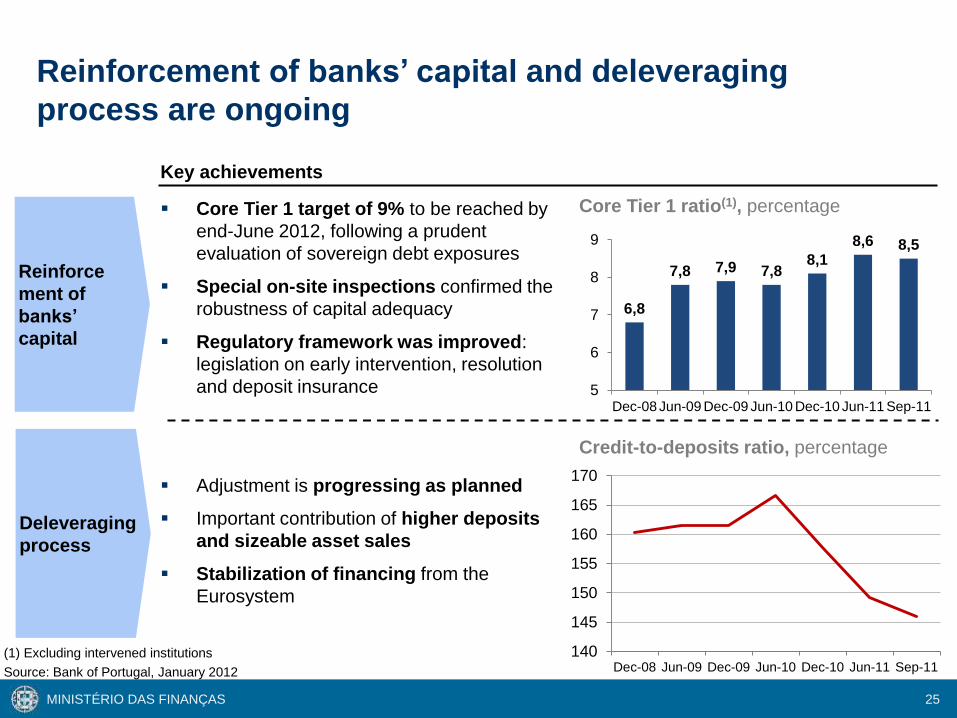

6,8

7,8 7,9 7,8 8,1

8,6 8,5

5

6

7

8

9

Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Sep-11

Reinforcement of banks’ capital and deleveraging

process are ongoing

Core Tier 1 target of 9% to be reached by

end-June 2012, following a prudent

evaluation of sovereign debt exposures

Special on-site inspections confirmed the

robustness of capital adequacy

Regulatory framework was improved:

legislation on early intervention, resolution

and deposit insurance

Adjustment is progressing as planned

Important contribution of higher deposits

and sizeable asset sales

Stabilization of financing from the

Eurosystem

Core Tier 1 ratio(1), percentage

Key achievements

(1) Excluding intervened institutions

Source: Bank of Portugal, January 2012

Reinforce

ment of

banks’

capital

Deleveraging

process

Credit-to-deposits ratio, percentage

140

145

150

155

160

165

170

Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Sep-11

MINISTÉRIO DAS FINANÇAS 26

0,00

0,25

0,50

0,75

1,00

1,25

1,50

1,75

2,00

2,25

ECB repo rate 1m

3m

12m

Reduction of the reserve requirements ratio: from 2% to 1%

Broadening of eligible collateral

Easing of bank liquidity pressures

Source: Bank of Portugal, March 2012

ECB Measures (8 December)

Euribor

Percentage

Longer-term refinancing operations: 36 months

(December 22 and March 1)

ECB LTRO 36m

MINISTÉRIO DAS FINANÇAS 27

150.000

170.000

190.000

210.000

230.000

250.000

270.000

Greece Ireland Portugal

Depositors’ trust in the Portuguese banking system

Source: ECB

Total deposits (excluding deposits from financial institutions)

EUR Millions

MINISTÉRIO DAS FINANÇAS 28

STRUCTURAL

TRANSFORMATION

MINISTÉRIO DAS FINANÇAS 29

Economic growth: importance of the Structural

Transformation Agenda

Opening to

foreign

investment and to

the challenges of

international

competition

Competitive

location for

physical and

human capital

Fully integration in

the Single

European Market

Development of a

stability culture

Judicial system

Broad range of reforms

Structural

transformation

Confidence,

credibility and

justice

Openness,

competition and

competitiveness

Entrepreneurship,

innovation and

labor market

flexibility

Limited State and

economic

democracy

Network industries: energy,

telecommunications, transports

Competition

Housing Market

Labor market

Education and training

Privatizations

Special rights of the State

Public procurement

Administrative burden

Pillars

MINISTÉRIO DAS FINANÇAS 30

Portugal needs a broad transformation agenda

(1) The heatmap is constructed based on a variety of structural indicators from alternative sources in order to flag areas where a country has the greatest need to implement structural reforms. For a

discussion of the methodology and detailed components, see IMF, 2010d, “Cross-Cutting Themes in Employment Experiences During the Crisis”, IMF Report SM/10/274

Source: OECD; World Economic Forum; Fraser Institute and IMF staff calculations

Structural reforms gaps in European economies: a heatmap(1)

Labor market inefficiency

Business regulations

Network regulation

Retail sector regulation

Profess. services regulation

Institutions and contracts

Human capital

Infrastructure

Innovation

Medium

term

Long

term

DE FR NL BE IT ES PT GR AT FI IE DK SE UK US JP

Selected comparators Euro area countries

MINISTÉRIO DAS FINANÇAS 31

0

5

10

15

20

%

Structural reforms: long-run potential impact

Source: Bouis and Duval (2011), OECD Economics Department Working Paper n.º 835; Gomes et al (2011), Banco de Portugal Working Paper n.º 13

2 empirical studies for Portugal

Approach

No model: use

empirical results

from several studies

Broad range of

reforms that include

reforms in product

and labor market

and reforms of

benefit, tax and

retirements systems

Multi-country DSGE

Model

Reforms of labor

and services market

Bouis

and

Duval

(2011)

Gomes

et al

(2011)

GDP per capita, increase in level in percent at 10-year horizon

PT ~13%

(> 5% after 5 years)

20

15

10

5

0

Results

Increase in long-term output of 7.8% , after 7 years

(8.6% in case of cross-country coordination of reforms

in the euro area)

MINISTÉRIO DAS FINANÇAS 32

In-depth labor market reform Agreement on Growth, Competitiveness and Employment

The agreement

between the

Government,

Unions and

Enterprises

Associations: an

important step to

implement reforms in

an environment of

social dialogue

Implemented measures

Tackle labor

market

segmentation

Foster job

creation

Ease

transition of

workers

across firms

and sectors

Objectives

Reduction of 4 national holidays

Elimination of 3 extra days of vacation

Decrease in 50% of compensation for

overtime work

Suspend automatic extension of collective

agreements

Implementation of individual and group

working time management mechanisms

Reduction of restrictions to individual

dismissal

Reduction of severance payments to align

with EU average

Implementation of labor arbitration

mechanisms

Reducing

labor

costs

Labor

market

flexibili

zation

NON-EXHAUSTIVE

MINISTÉRIO DAS FINANÇAS 33

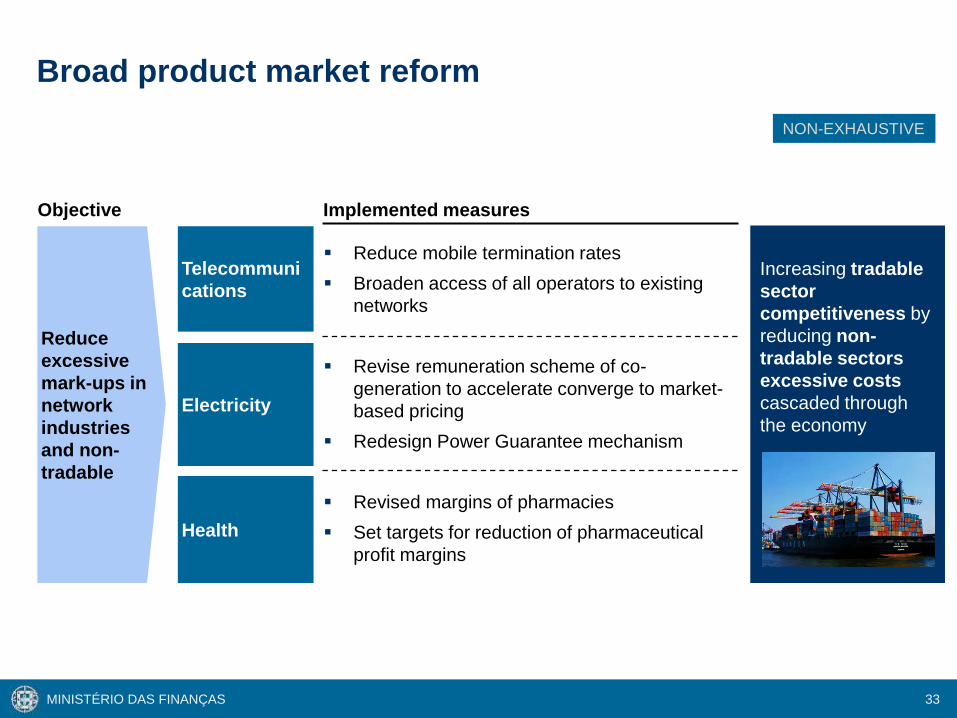

Increasing tradable

sector

competitiveness by

reducing non-

tradable sectors

excessive costs

cascaded through

the economy

Implemented measures

Broad product market reform

Reduce

excessive

mark-ups in

network

industries

and non-

tradable

Reduce mobile termination rates

Broaden access of all operators to existing

networks

Revise remuneration scheme of co-

generation to accelerate converge to market-

based pricing

Redesign Power Guarantee mechanism

Revised margins of pharmacies

Set targets for reduction of pharmaceutical

profit margins

Telecommuni

cations

Electricity

Health

Objective

NON-EXHAUSTIVE

MINISTÉRIO DAS FINANÇAS 34

Implemented measures

Improving business environment

Foster

investment

and

innovation

Incentive a

more

efficient

use of

resources

Targeted measures to accelerate the resolution of the backlog:

50,000 enforcement cleared since November

Adoption of a law on arbitration to facilitate out-of-court settlement

Proposal to amend the insolvency code and corporate recovery,

focusing on speed, simplification and creation of an extra-judicial

phase of corporate recovery

Approval of a new Competition Law harmonized with the EU legal

competition framework

Strengthen the power of the Competition Authority

Approval of a specialized court on Competition, Regulation and

Supervision

Liberalization of regulated professions’ access and exercise

Reduction of firms’ administrative burden: licensing requirements

and other legal formalities

Revision of the Urban Lease Law

Judicial

system

Competition

Other

services

Objective

NON-EXHAUSTIVE

MINISTÉRIO DAS FINANÇAS 35

Privatization program as a flagship in the agenda

Electricity

distribution

Energy retail

and production

distribution

Water

distribution

Air

infrastructure

Railway

logistics

Seguros

Insurance

Seguros

Energy retail

and production

2011 2012 2013

Q1

Air transport Television

broadcasting

(1) Sale of “Caixa Geral de Depósitos” participation of 1%

(2) Concession

(3) Expected completion date by “Caixa Geral de Depósitos”

(1) (2)

Q3 Q2

(3)

Q4

MINISTÉRIO DAS FINANÇAS 36

21,35%

Asia: China Three Gorges

Europe: E.ON

Latin America: Eletrobras

and Cemig

EUR 2,693M: premium of

53.6% per share1

EUR 2,000M through

Chinese banking entities

EUR 2,000M until 2015 in

wind farms

Privatization results above expectations

Bidders

Revenue

Financing

1 Considering the closing price of the day before the Council of Ministers decision

Investment

% Equity

The proceeds

amount to about

60% of the

estimate of

privatizations

revenues

foreseen in the

Adjustment

Program

40%

Asia: State Grid

Saudi Arabia: Oman Oil

Company

EUR 593M: average premium

of 33.6% per share1

EUR 1,000M through Chinese

banking entities

Strategic plan for national

economy development (e.g.

I&D center construction)

Selected bidders

MINISTÉRIO DAS FINANÇAS 37

CONCLUSION:

HOW WILL IT WORK?

MINISTÉRIO DAS FINANÇAS 38

The Program addresses

fundamental imbalances

and deficiencies

Restoring credibility and confidence

(1) Ministry of Finance”, February 2012

The adjustment

is inevitable

Solid starting

point for the

Program

Broad popular

and social

support for

adjustment

Elimination of budget deficit

on a durable way –

supported by a new fiscal

policy framework (at national

and European level)

Elimination of external

deficit – current and capital

account is projected to be in

surplus in 2014(1)

Deep and frontloaded

structural reform agenda that

will boost potential output

and competitiveness

Robustness of the

overall Program

The Program works

disregarding positive

impact of structural

reforms on potential

growth

Structural reforms are

likely to speed up

adjustment

Gradual credibility buildup

The Program shelters

government financing

from the vagaries of

financial markets

Quantitative objectives

and targets steered and

monitored over time

(9 reviews until Sep. 2013)

Compliance with the

Program will push for a

gradual change in

markets’ expectations

and perceptions

MINISTÉRIO DAS FINANÇAS 39

MINISTÉRIO DAS FINANÇAS

Portugal: restoring

credibility and confidence

Vítor Gaspar

Washington

March 19, 2012