Mining Industry in Chile · 21/07/2009 1 Mining Industry in Chile Juan Carlos Guajardo B. Executive...

48

21/07/2009 1 Mining Industry in Chile Juan Carlos Guajardo B. Executive Director Friday 9 th January 2009 Center for Copper and Mining Studies •Independent think-tank, non-profit organization established in Santiago in 1984. •Contribute to the design and debate of public policies which foster the best use of the mining industry's potential for development. •CESCO has positioned itself as a meeting place for diverse sectors interested in mining --business, academia, policymakers and professionals-- •Membership of CESCO: executives or consultant for national and foreign mining companies, others as professors in local or foreign universities. •Cesco is self-funded in 100% (Cesco Week, Conferences, others)

Transcript of Mining Industry in Chile · 21/07/2009 1 Mining Industry in Chile Juan Carlos Guajardo B. Executive...

21/07/2009

1

Mining Industry in Chile

Juan Carlos Guajardo B.

Executive Director

Friday 9th January 2009

Center for Copper and Mining Studies

•Independent think-tank, non-profit organization established in Santiago in 1984.

•Contribute to the design and debate of public policies which foster the best use of the mining industry's potential for development.

•CESCO has positioned itself as a meeting place for diverse sectors interested in mining --business, academia, policymakers and professionals--

•Membership of CESCO: executives or consultant for national and foreign mining companies, others as professors in local or foreign universities.

•Cesco is self-funded in 100% (Cesco Week, Conferences, others)

21/07/2009

2

1. The Relevance of Mining to Chile

“Situación y perspectivas de la minería en chile. La visión del sector privado”. Presentación de Alvaro Merino Lacoste. Sociedad Nacional de Minería. 26 octubre 2005. “Importancia del Sector Privado en el Desarrollo Minero de Chile”. Presentación de Alberto Salas SONAMI. La Serena, 4 de Junio de 2008.

Chile in the World Mining Industry

The country has only the 0,6% of the world land and the 0,3% of the world population and income. But…

In 2007 Chile’s performance was outstanding:

1° World Copper Producer : 35%1° World Natural Nitrates Producer : 100%1° World Iodine Producer : 60%1° World Lithium Producer : 45%1° World Rhenium Producer : 44%3° World Molybdenum Producer : 21%4° World Silver Producer : 9,5%

21/07/2009

3

Source: International Copper Study Group, 2007 World Copper Factbook

Top 20 Copper Mines by Capacity, 2006(Thousand metric tonnes)

Chile:5 of the top 10

8 of the top 20

Mining Share in Current GDP and Real GDP(Base 2003)

Source: Central Bank of Chile

0

5

10

15

20

25

2003 2004 2005 2006 2007

(%)

Current Prices

Constant 2003 Prices

21/07/2009

4

0

20.000

40.000

60.000

80.000

100.000

120.000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Total Exports

Copper Exports

Source: Central Bank of Chile

Copper Exports vs. Total ExportsUS$ M

illions

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

US$ m

illions

Private Sector

Public Sector

Fiscal Revenues from the Public and Private Mining Sectors

Source: Dipres and Comisión Chilena del Cobre.

21/07/2009

5

Fiscal Revenues from the Public and Private Mining vs The Total Fiscal Income

Source: Ministry of Finance.

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

US

$ M

illio

ns

0%

5%

10%

15%

20%

25%

30%

35%

40%

Total Fiscal Revenues

% Mining

Chile’s Copper Mining Industry

Annual Production (Copper Tons)

Number of Company

Sales(US$ Millions)

Nº of Employees

(2007)

Large Mining

> 30.000 19 40.000 34.745

Medium Mining

10.000 - 30.000 29 2.500 7.560 (2)

Small Mining

< 10.000 2.050 (1) 400 8.438 (2)

1. Monthly Average 2007

2. Metals Mining

Source: Instituto de Ingenieros en Minas de Chile, ENAMI, Cochilco, SONAMI.

21/07/2009

6

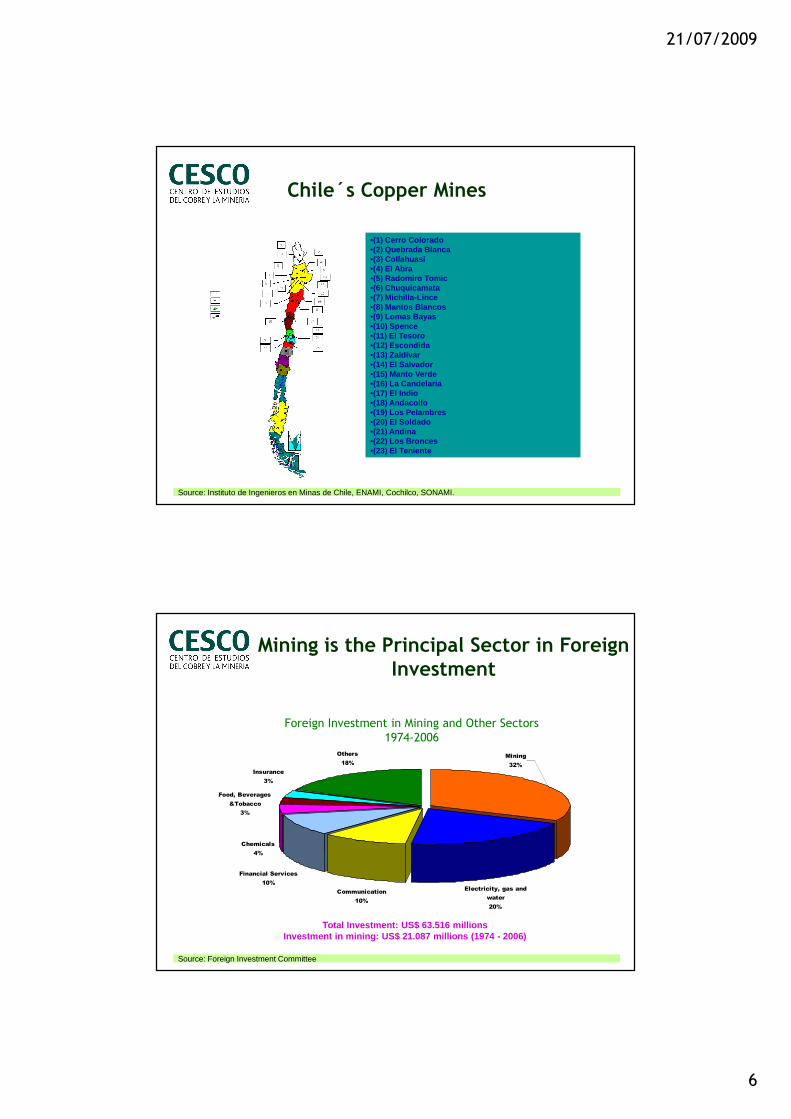

•(1) Cerro Colorado•(2) Quebrada Blanca •(3) Collahuasi •(4) El Abra •(5) Radomiro Tomic •(6) Chuquicamata •(7) Michilla-Lince •(8) Mantos Blancos•(9) Lomas Bayas•(10) Spence •(11) El Tesoro •(12) Escondida •(13) Zaldívar •(14) El Salvador •(15) Manto Verde •(16) La Candelaria •(17) El Indio •(18) Andacollo •(19) Los Pelambres•(20) El Soldado •(21) Andina •(22) Los Bronces •(23) El Teniente

Chile´s Copper Mines

Source: Instituto de Ingenieros en Minas de Chile, ENAMI, Cochilco, SONAMI.

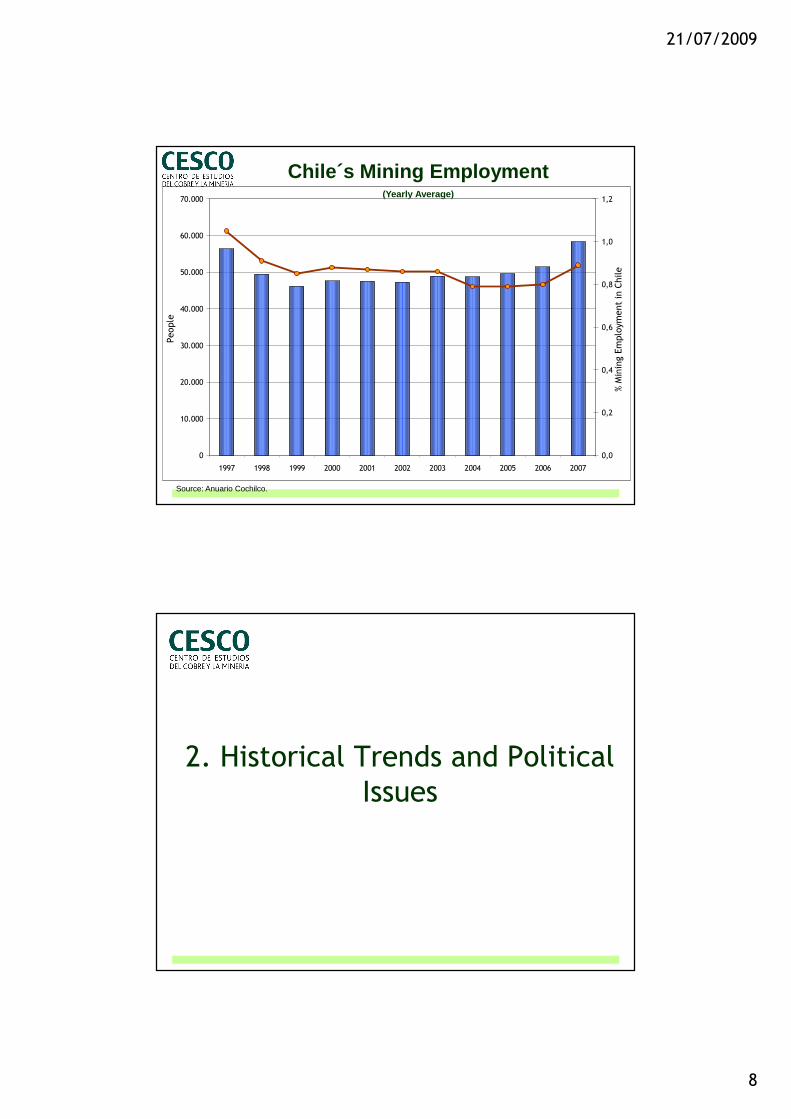

Total Investment: US$ 63.516 millionsInvestment in mining: US$ 21.087 millions (1974 - 2006)

Foreign Investment in Mining and Other Sectors1974-2006

Source: Foreign Investment Committee

Mining is the Principal Sector in Foreign Investment

Chemicals

4%

Others

18%

Mining

32%

Electricity, gas and

water

20%

Communication

10%

Financial Services

10%

Food, Beverages

&Tobacco

3%

Insurance

3%

21/07/2009

7

0%

10%

20%

30%

40%

50%

60%

70%

1999 2007

Subcontratistas Planta TotalMinería Privada 39.000 31.000 70.000Codelco 28.000 14.000 42.000Total 67.000 45.000 112.000Fuente: Compañías Mineras

Outsourcing in Mining1999-2007

Source: INE and Mining Companies

Direct Employment and Outsourcing

Source: INE

Impact of Mining Activity in Chilean Employment

21/07/2009

8

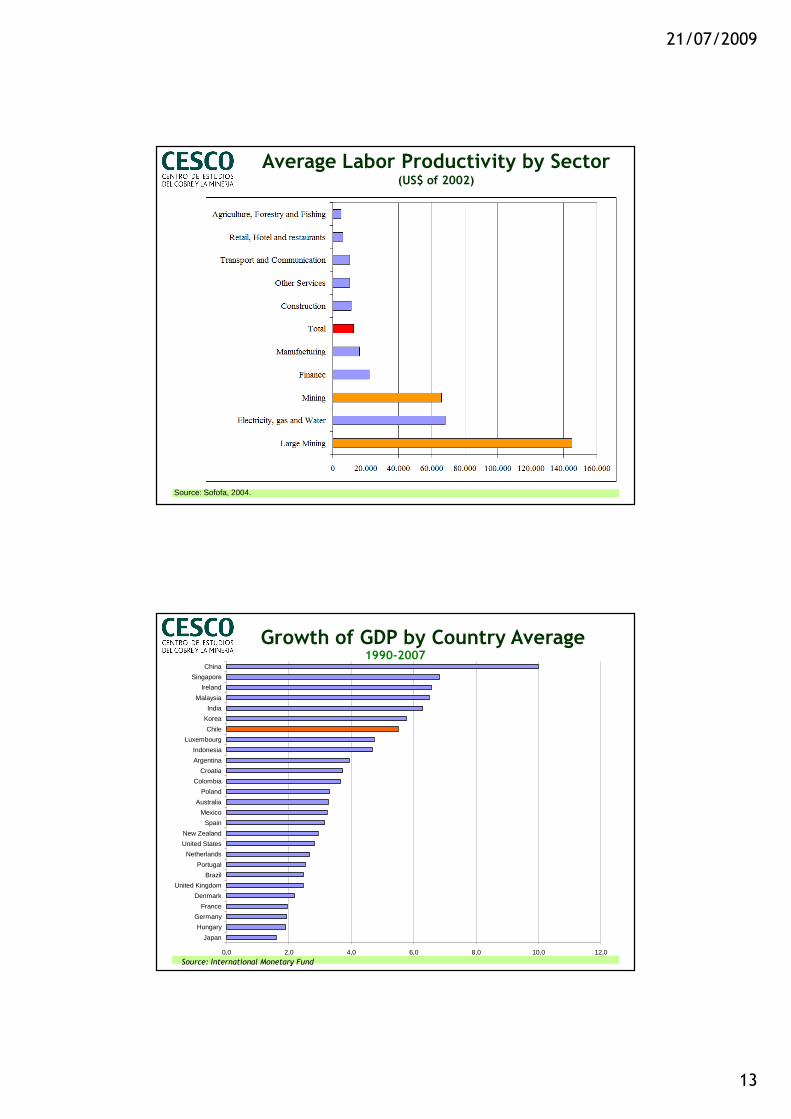

Chile´s Mining Employment(Yearly Average)

Source: Anuario Cochilco.

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

People

0,0

0,2

0,4

0,6

0,8

1,0

1,2

% Mining Employm

ent in Chile

2. Historical Trends and Political Issues

21/07/2009

9

GDP, Mining and Agriculture1860-2000

(Millions Chilean pesos of 1996)

Source: Wagner, Gert and José Díaz. 2008. Inflación y Tipo de Cambio: Chile 1810-2005. Documento de Trabajo Nº 328, Departamento de Economía Pontificia Universidad Católica de Chile.

Chilean Nitrate Production1860-2006(Tons)

Source: Wagner, Gert and José Díaz. 2008. Inflación y Tipo de Cambio: Chile 1810-2005. Documento de Trabajo Nº 328, Departamento de Economía Pontificia Universidad Católica de Chile. Anuario de Cochilco, 2007.

21/07/2009

10

Chilean Copper Production1860-2006(Tons)

Source: Wagner, Gert and José Díaz. 2008. Inflación y Tipo de Cambio: Chile 1810-2005. Documento de Trabajo Nº 328, Departamento de Economía Pontificia Universidad Católica de Chile. Anuario de Cochilco, 2007.

Chilean Copper Production by SourceState-Owned and Private

(Thousand Tons)

Source: Anuario de Cochilco, 1995 y 2007.

0

1.000

2.000

3.000

4.000

5.000

6.000

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Private Production

Codelco

21/07/2009

11

From the enclave to the Integration

Source: Presentación de Jorge Marshall en Seminario SONAMI.

Copper Mining increase it’s impact in the chilean economy

Sectoral Multipliers

(input-output matrix)

Source: Author, based on data from the Foreign Investment Committee

Foreign Investment in two periods

US$ m

illions

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

1974-1989 1990-2007

Mining Other Sectors

21/07/2009

12

Source: Superintendencia de AFP.

Salaries in Mining are high...

Annual Average of Taxable Income(USD december 2007)

Mining Regions Grow Fastest

Source: Presentación de Jorge Marshall: El Mercado del Cobre y la Economía Nacional. 7 de Agosto 2008.

GDP Growth between 1990-2006

21/07/2009

13

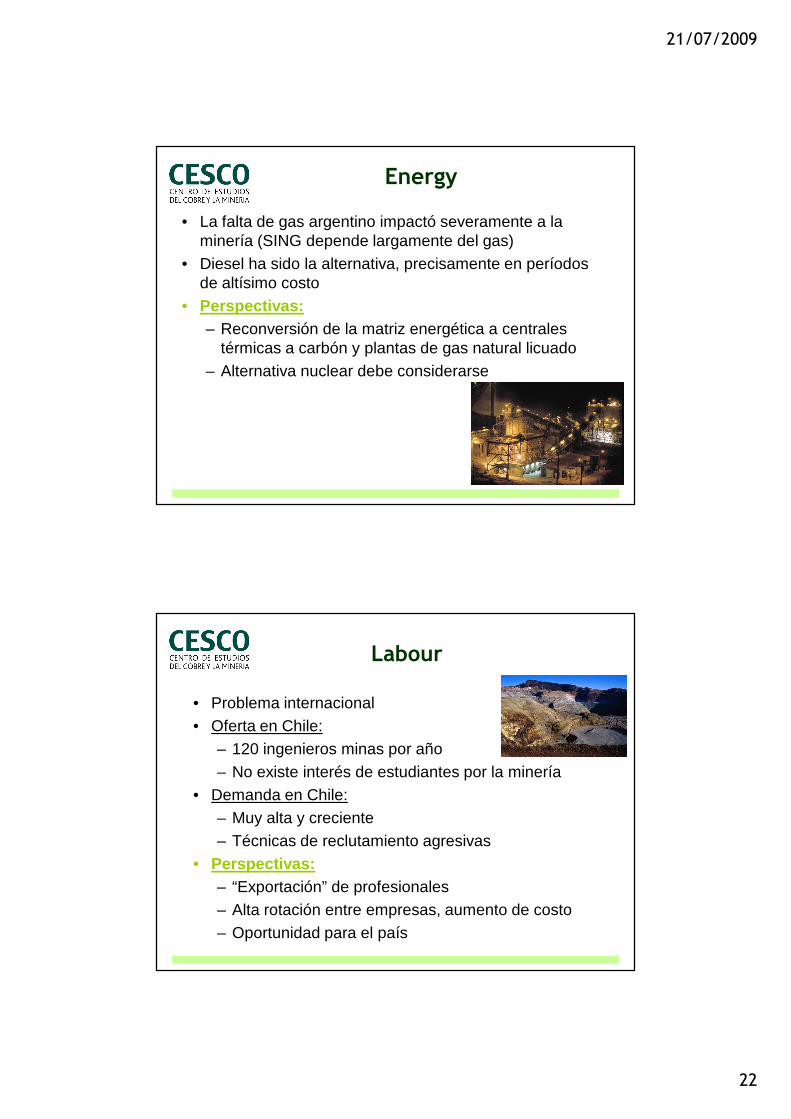

Average Labor Productivity by Sector(US$ of 2002)

Source: Sofofa, 2004.

Growth of GDP by Country Average

Source: International Monetary Fund

0,0 2,0 4,0 6,0 8,0 10,0 12,0

Japan

Hungary

Germany

France

Denmark

United Kingdom

Brazil

Portugal

Netherlands

United States

New Zealand

Spain

Mexico

Australia

Poland

Colombia

Croatia

Argentina

Indonesia

Luxembourg

Chile

Korea

India

Malaysia

Ireland

Singapore

China

1990-2007

21/07/2009

14

“All that glitters is not copper”

SQM 1.188

CAP (CMP) 1.583

Molymet 2.653

Sal Lobos 350

Source: Created in base of public information.

Large Companies from Other Industries(2007 annual sales in millions of US$)

Source: CESCO. Financial Report. Quarterly Results of Large MIning.

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

2007 Jan-Sep 2008

US

$ m

illio

ns

Income Fiscal Contributions

Chile and The Large Mining

21/07/2009

15

3. Policy Learning from Mining

Copper Price through the years

Source: Cochilco

0

50

100

150

200

250

300

350

400

450

1935

1937

1939

1941

1943

1945

1947

1949

1951

1953

1955

1957

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Precio RealDeflactor IPM EE.UU.

(base agosto 2008=100 )

Average 1935-2007:

197,9197,9

21/07/2009

16

Source: Wagner, Gert and José Díaz. 2008. Inflación y Tipo de Cambio: Chile 1810-2005. Documento de Trabajo Nº 328, Departamento de Economía Pontificia Universidad Católica de Chile

Contribution of Natural Resources to Total Fiscal Revenues

1860-1990

The Structural Balance Policy in Chile

Source: Cesco based on DIPRES.

2001

Fiscal policy based on current

fiscal position

Fiscal policy based on medium-term fiscal

outlook

“Nets out the cyclical impact of the level of economic activity and the price of

copper that affect central government income”

2006

“Cyclical adjustment of fiscal income from molybdenum also

became necessary”

Fiscal position strongly

exposed to international economy and copper price fluctuations

Fiscal policy based on medium-term fiscal

outlook

•GDP Potential Output•10-years Copper price

•GDP Potential Output•10-years Copper price•Long-term molybdenum price

21/07/2009

17

The Structural Surplus Rule

Source: Created with data from the DIPRES.

Poverty and Extreme Poverty in Chile1987-2006

Source: Ministry of Planning (Mideplan)

21/07/2009

18

Source: Informe trimestral a Junio de 2008. Dipres

Pensions Reserve FundPensions Reserve Fund

Until october 2008, total:Until october 2008, total:US$ 2.250 millionsUS$ 2.250 millions

Social and Economic Social and Economic Stabilization Fund Stabilization Fund

Until October 2008, total:Until October 2008, total:US$ 18.000 millionsUS$ 18.000 millions

Public Debt(Central Government)

Source: Dipres.

21/07/2009

19

World Bank’s Governance Indicators

Source: World Bank.

4. Challenges ahead to the Chilean Mining Industry

21/07/2009

20

• Head Grades• Water• Energy• Labour• Environment and Communities• Geology• Mining Cluster• Finance Market

Major Challenges

Copper Head Grades of the Major Chilean Mines and Projects

Source: Created in base of Brook Hunt data.

21/07/2009

21

Water

• No existen recursos hídricos para sustentar las expansiones mineras

• Los derechos de agua se pagan hasta en 200 mil dólares el litro/segundo

• Existe falta de información sobre disponibilidad de recursos hídricos

• Perspectivas: plantas desaladoras de agua de mar, uso directo de agua de mar, incremento de técnicas de recuperación

Source: Created in base of Rodolfo Camacho (Datos promedios para año 2006) presentation.

Water Consumption in Mining vs. Water Consumption in Mining vs. Other sectors is low Other sectors is low (is concentrated in the north)

Water extraction by sector

Antofagasta and Country Total

21/07/2009

22

Energy

• La falta de gas argentino impactó severamente a la minería (SING depende largamente del gas)

• Diesel ha sido la alternativa, precisamente en períodos de altísimo costo

• Perspectivas:– Reconversión de la matriz energética a centrales

térmicas a carbón y plantas de gas natural licuado– Alternativa nuclear debe considerarse

• Problema internacional• Oferta en Chile:

– 120 ingenieros minas por año– No existe interés de estudiantes por la minería

• Demanda en Chile:– Muy alta y creciente– Técnicas de reclutamiento agresivas

• Perspectivas:– “Exportación” de profesionales– Alta rotación entre empresas, aumento de costo– Oportunidad para el país

Labour

21/07/2009

23

• Existe una mayor conciencia que se refleja en mayores demandas a la minería

• Permisos cada vez más complejos de obtener (retrasos)• Incertidumbre en aplicación de criterios

• Perspectivas: Expectativa por el establecimiento del Ministerio del Medio Ambiente

Environment and Communities

• La geología no es considerada como un activo estratégico nacional. Ejemplos:– Monitoreo vulcanológico– Investigación sísmica– Información geológica

• Perspectivas: Mejorar carta geológica, acceso online y compilación de información de exploración realizada en Chile

Geology

21/07/2009

24

Mining Cluster

•Los países que se han desarrollado a partir de los recursos naturales han logrado establecer desarrollo empresarial y tecnológico en torno a ellos

•Nórdicos

•Australia

•Claves del éxito: coordinación público-privada, confianza entre actores

•Perspectivas: Difícil progreso en Chile mientras los esfuerzos se basen en el sector público y existan intereses dispersos sin liderazgo

Finance Market and MiningFinance Market and Mining

% Empresas Mineras en

Bolsas

Capitalización Bursátil

(Billones US$)

Canadá 35% 378,5

Australia 35% 320,0

Perú 10% 15,5

Chile 3% 6,3

Source: TSX, ASX, Bolsa de Lima, Bolsa de Comercio de Santiago.

Perspectivas: Arduo trabajo para superar barreras (desconocimiento, desconfianza), ley de persona competente

21/07/2009

25

5. Copper in the World

Source: International Copper Study Group, 2007 World Copper Factbook

Properties of Copper

21/07/2009

26

Source: International Copper Study Group, 2007 World Copper Factbook

Major Uses of Copper

Source: ICSG 2008 Statistical Yearbook – July 2008

Copper Mine Production(% of World Copper Mine Production)

21/07/2009

27

Source: ICSG 2008 Statistical Yearbook – July 2008

Refined Copper Production(% of World Refined Copper Production)

Source: ICSG 2008 Statistical Yearbook – July 2008

Refined Copper Usage(% of World Refined Copper Usage)

21/07/2009

28

Source: International Copper Study Group, 2007 World Copper Factbook

Refined Usage per Capita

Intensity of Refined Copper UseIntensity of Refined Copper Use

Fuente: GIEC, FMI y US Census Bureau.

Consumo per cápita de cobre refinado (kg/persona)

PIB per capita year 2006 (US$ per person)

21/07/2009

29

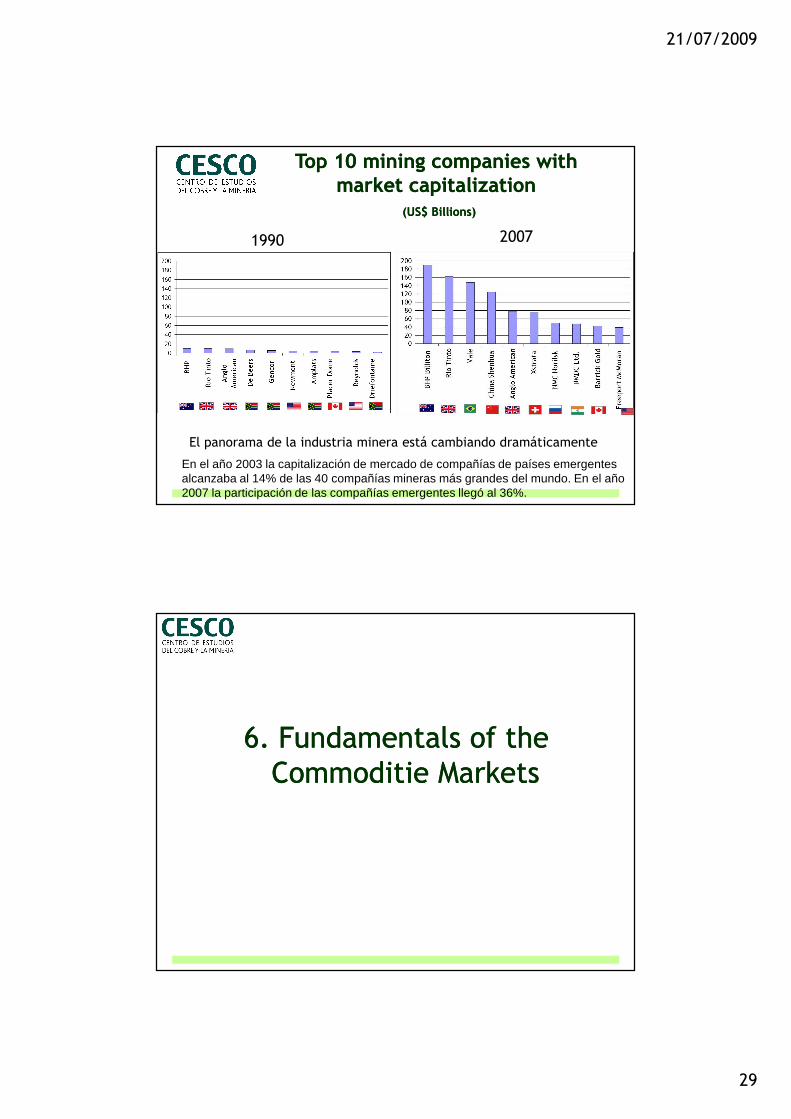

El panorama de la industria minera está cambiando dramáticamente

Top 10 mining companies with Top 10 mining companies with market capitalizationmarket capitalization

(US$ Billions)(US$ Billions)

1990 2007

En el año 2003 la capitalización de mercado de compañías de países emergentes alcanzaba al 14% de las 40 compañías mineras más grandes del mundo. En el año 2007 la participación de las compañías emergentes llegó al 36%.

6. Fundamentals of the 6. Fundamentals of the Commoditie MarketsCommoditie Markets

21/07/2009

30

There are three basic drivers of the collapse in co mmodity prices…

� The classic macro-economic cycle based on a downturn in cyclically sensitive sectors (construction, consumer durables) in the developed industrial world

� looks more like the more severe 1974/75 and 1980/82 cycles than the shallower 1990/91 or 2001/02 cycles

� note – the downturn caused the financial crisis, not vice versa

� Deliberate policy actions by the Chinese government to curb unsustainably rapid growth

� probably temporary; although structurally slower growth is not far off

� Withdrawal of commodity fund liquidity from the market

1www.crugroup.com

Source: CRU Strategies

Long expansive cycle of the OECD economies

Restricted supply

Chinese consumption

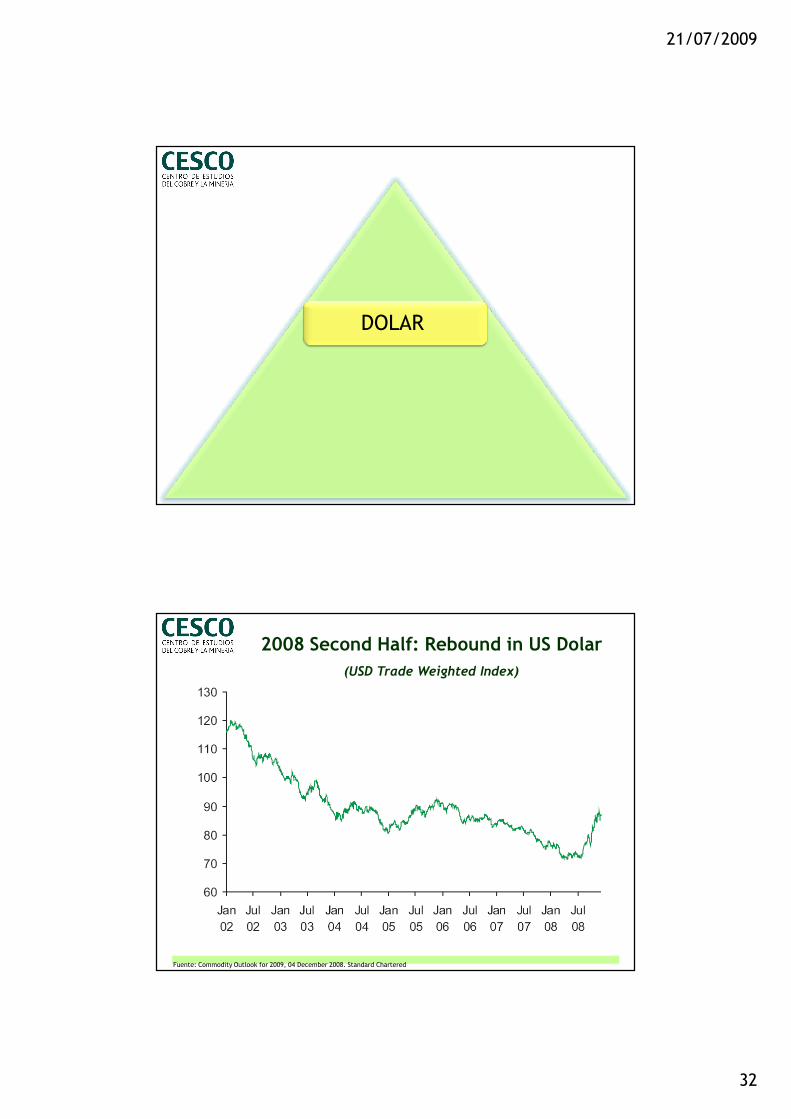

DOLAR

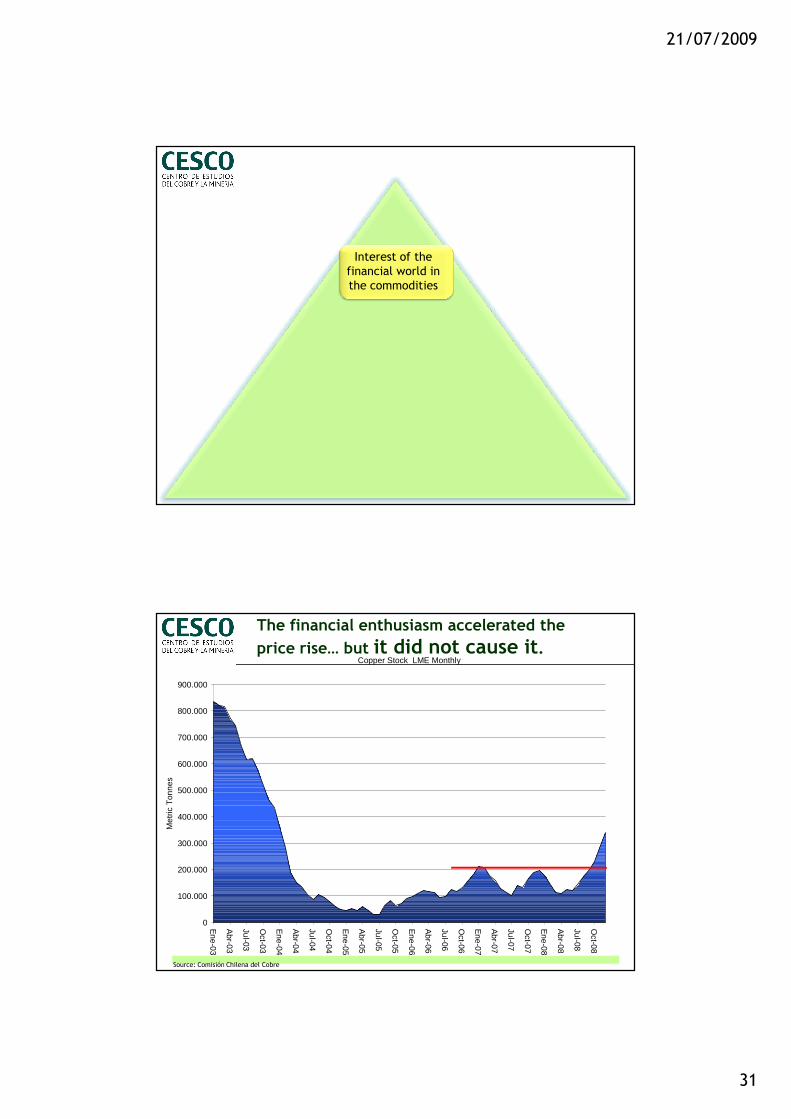

Interest of the financial world in the commodities

21/07/2009

31

Interest of the financial world in the commodities

Copper Stock LME Monthly

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

Ene-03

Abr-03

Jul-03

Oct-03

Ene-04

Abr-04

Jul-04

Oct-04

Ene-05

Abr-05

Jul-05

Oct-05

Ene-06

Abr-06

Jul-06

Oct-06

Ene-07

Abr-07

Jul-07

Oct-07

Ene-08

Abr-08

Jul-08

Oct-08

Met

ric T

onne

s

The financial enthusiasm accelerated the

price rise… but it did not cause it.

Source: Comisión Chilena del Cobre

21/07/2009

32

DOLAR

Fuente: Commodity Outlook for 2009, 04 December 2008. Standard Chartered

2008 Second Half: Rebound in US Dolar

(USD Trade Weighted Index)

21/07/2009

33

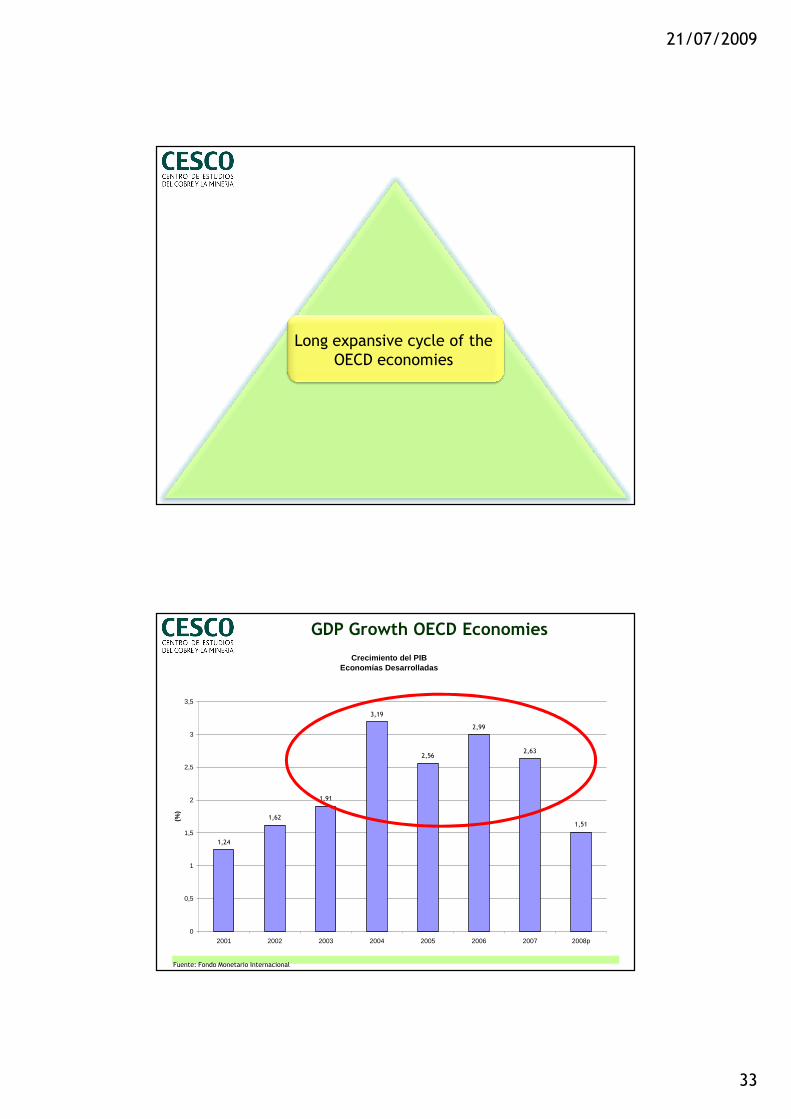

Long expansive cycle of the OECD economies

GDP Growth OECD Economies

Fuente: Fondo Monetario Internacional

Crecimiento del PIB Economías Desarrolladas

1,24

1,62

1,91

3,19

2,56

2,99

2,63

1,51

0

0,5

1

1,5

2

2,5

3

3,5

2001 2002 2003 2004 2005 2006 2007 2008p

(%)

21/07/2009

34

Restricted supply

Producción Mundial de Cobre

Fuente: En base a datos del GIEC

Var 2007-2002:

14%

21/07/2009

35

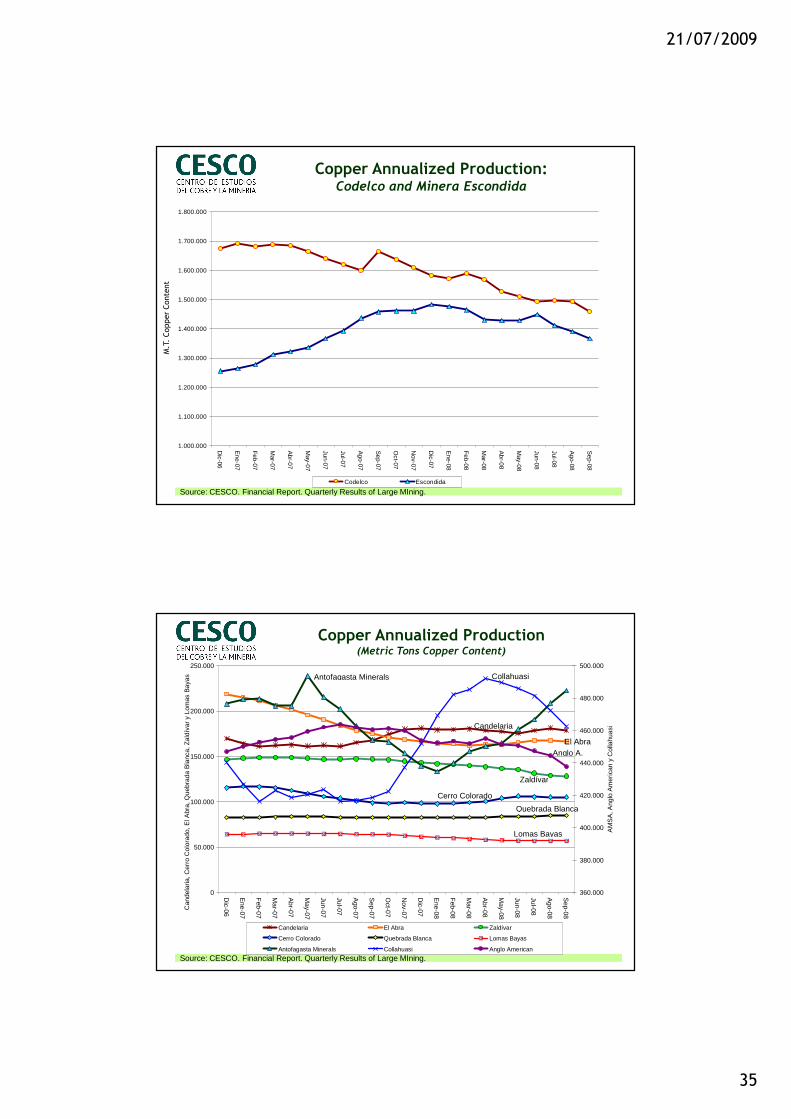

Copper Annualized Production:Codelco and Minera Escondida

Source: CESCO. Financial Report. Quarterly Results of Large MIning.

1.000.000

1.100.000

1.200.000

1.300.000

1.400.000

1.500.000

1.600.000

1.700.000

1.800.000

Dic-06

Ene-07

Feb-07

Mar-07

Abr-07

May-07

Jun-07

Jul-07

Ago-07

Sep-07

Oct-07

Nov-07

Dic-07

Ene-08

Feb-08

Mar-08

Abr-08

May-08

Jun-08

Jul-08

Ago-08

Sep-08

Codelco Escondida

M.T. Copper Content

Copper Annualized Production(Metric Tons Copper Content)

Source: CESCO. Financial Report. Quarterly Results of Large MIning.

Candelaria

El Abra

Collahuasi

0

50.000

100.000

150.000

200.000

250.000

Dic-06

Ene-07

Feb-07

Mar-07

Abr-07

May-07

Jun-07

Jul-07

Ago-07

Sep-07

Oct-07

Nov-07

Dic-07

Ene-08

Feb-08

Mar-08

Abr-08

May-08

Jun-08

Jul-08

Ago-08

Sep-08

Can

dela

ria, C

erro

Col

orad

o, E

l Abr

a, Q

uebr

ada

Bla

nca,

Zal

díva

r y

Lom

as B

ayas

360.000

380.000

400.000

420.000

440.000

460.000

480.000

500.000

AM

SA

, Ang

lo A

mer

ican

y C

olla

huas

i

Candelaria El Abra Zaldívar

Cerro Colorado Quebrada Blanca Lomas Bayas

Antofagasta Minerals Collahuasi Anglo American

Anglo A.

Zaldívar

Cerro Colorado

Quebrada Blanca

Lomas Bayas

Antofagasta Minerals

21/07/2009

36

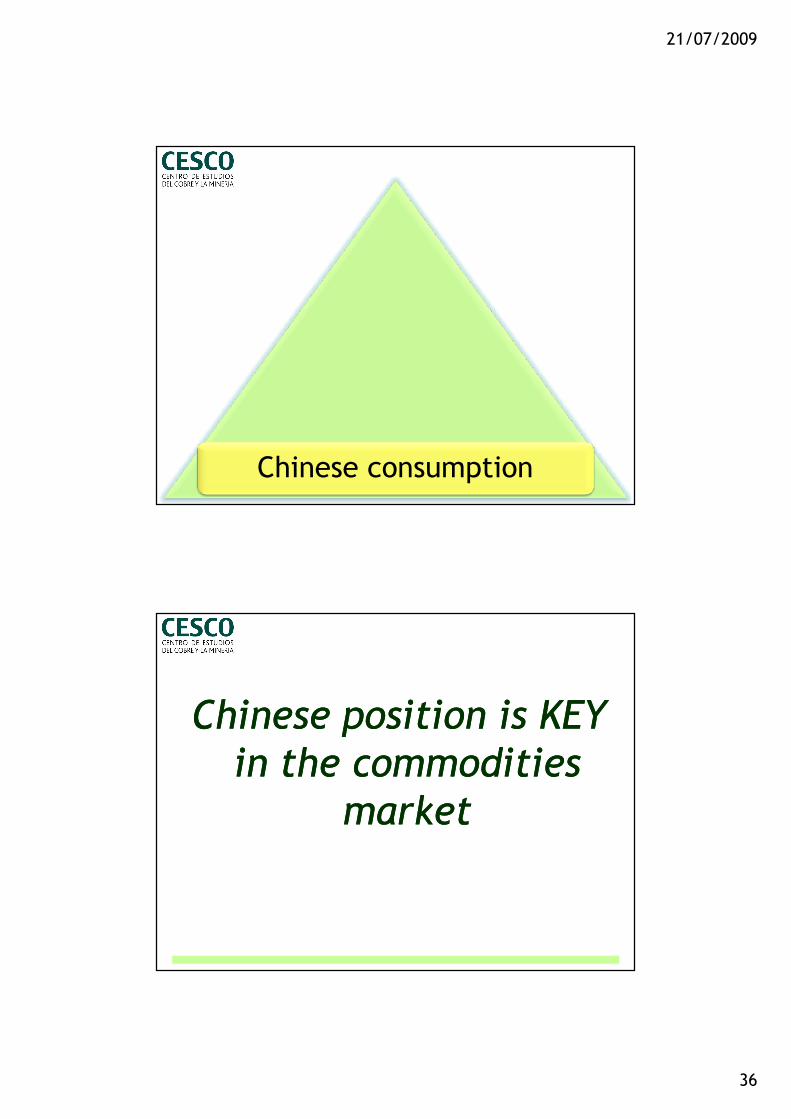

Chinese consumption

Chinese position is KEY Chinese position is KEY in the commodities in the commodities

marketmarket

21/07/2009

37

China Consumption of Commodities(Yearly)

Fuente: Presentación de Leonardo Suaréz “Monedas y precio del cobre: ¿punto de inflexión?”. LarraínVial.

Fuente: Macquarie en base a Standard Chartered, 2008.

Consumo

Inversión Exportaciones netas

Gasto del Gobierno

Contribution to the Growth of the GDP of China

21/07/2009

38

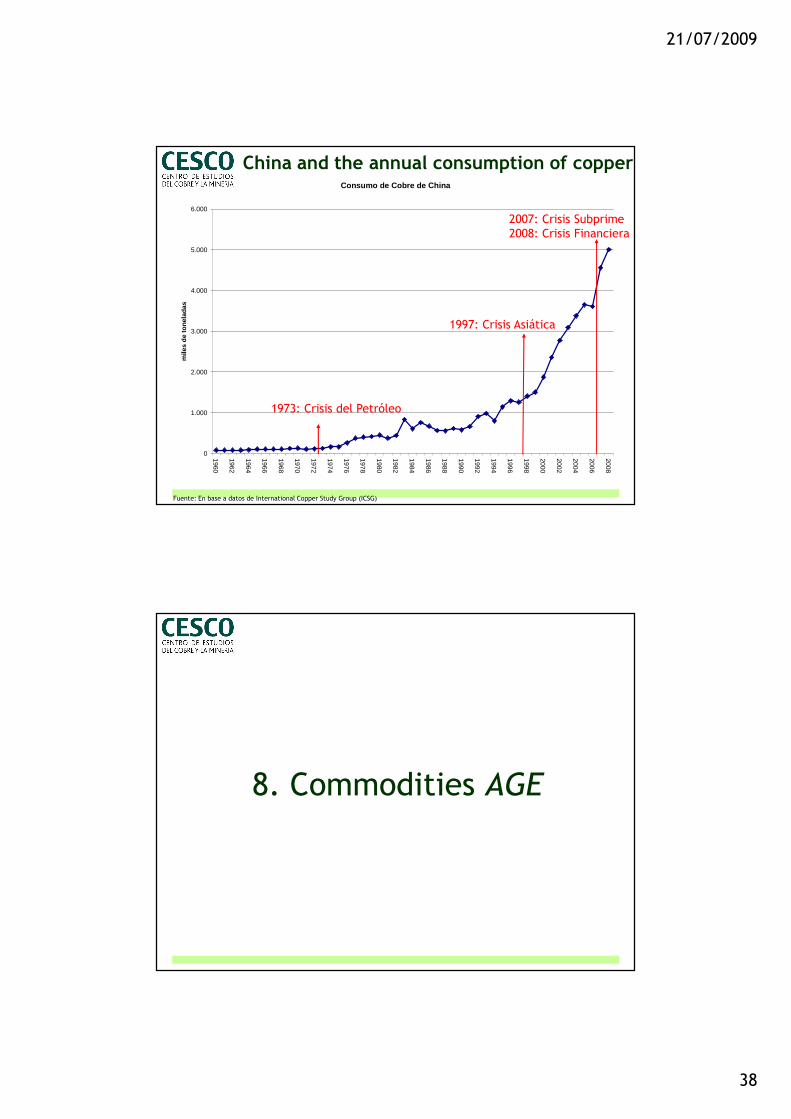

China and the annual consumption of copper

Fuente: En base a datos de International Copper Study Group (ICSG)

Consumo de Cobre de China

0

1.000

2.000

3.000

4.000

5.000

6.000

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008m

iles

de to

nela

das

1997: Crisis Asiática

1973: Crisis del Petróleo

2007: Crisis Subprime2008: Crisis Financiera

8. Commodities AGE

21/07/2009

39

Fuente: TheContaminated

Fuente: TheContaminated

21/07/2009

40

GDP World share has change between countries

Fuente: Fondo Monetario Internacional

Countries with Major Copper Consumption Countries with Major Copper Consumption 19001900--20062006

Fuente: Brook Hunt, ICSG

0

2

4

6

8

10

12

14

16

18

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2006

M to

nnes

Estados Unidos Europa Occ idental Rusia Japón China Resto Asia Otros

21/07/2009

41

Refined Copper Consumption in the World

0%

1%

2%

3%

4%

5%

6%

7%

1950 1960 1970 1980 1990 2000

0

5

10

15

20

Consumo Variac ión 10 años

Millones de TMVar (%)

1951-60: 4,8%1961-70: 4,5%

1971-80: 2,8%

1981-90: 1,5%

1991-00: 3,5%

2001-06: 3,0%

Fuente: WBMS

808 726511

484 618920

0

200

400

600

800

1.000

1.200

1.400

1.600

2003 2010 2025

Rural Urbano

Urbanización en China(millones de habitantes) Tres Factores que Incrementan el

Consumo del Cobre

1. Urbanización e infraestructura:- claves del desarrollo en China

y del consumo de metales

2. Aumento de Ingreso Per Capita:- Meta: Duplicar el Ingreso en 10

años- 2000: 900 US$ - 2010: 1,800 US$

3. Industrialización:- Rápido crecimiento del

desarrollo tecnológico

Outlook for Copper Demand in China

Fuente: China Statistics Year Book, BHP Billiton. Presentación D. Hernández “Competitividad de la Minería Chilena”

21/07/2009

42

Copper Consumption IncreaseCopper Consumption Increase

Fuente: Elaborado en base a datos del International Copper Study Group (ICSG)

50s 60s 70s 80s 90s 00s 10s 20s ...

Estados Unidos

Europa Occidental (Alemania)

Japón

China

Drivers in World Copper Consumption in the last decades

Source: Cochilco

21/07/2009

43

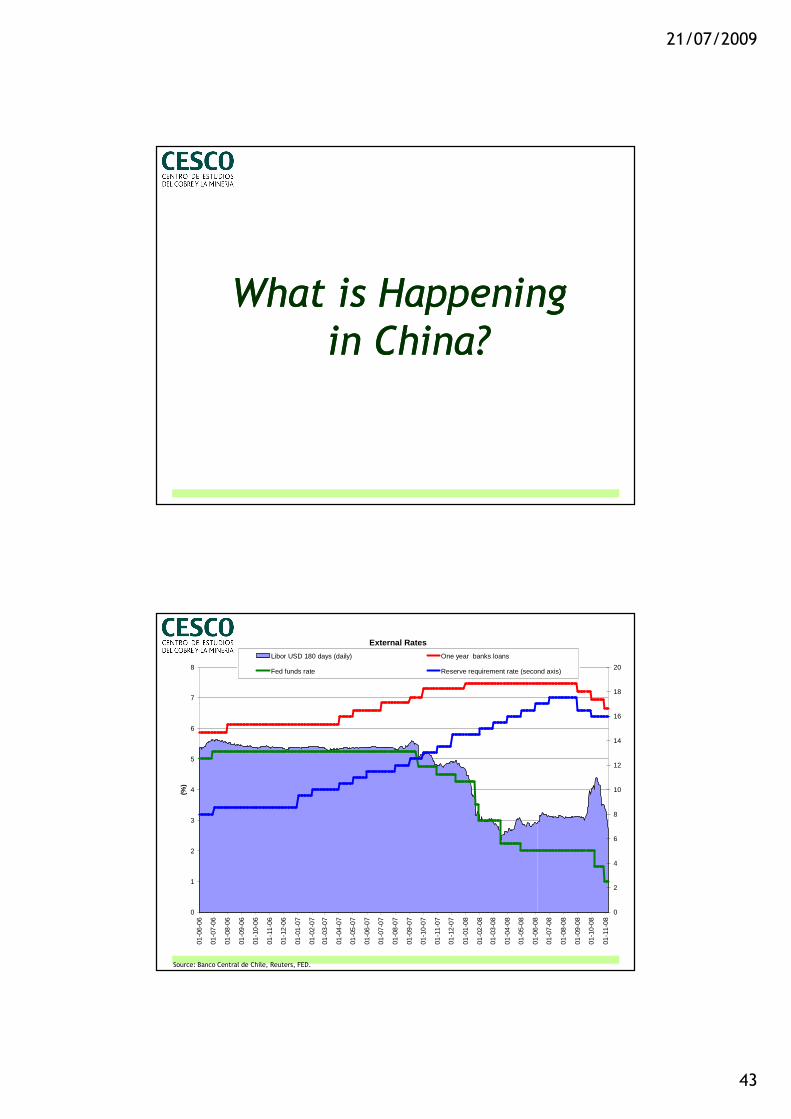

What is Happening What is Happening in China?in China?

Source: Banco Central de Chile, Reuters, FED.

External Rates

0

1

2

3

4

5

6

7

8

01-0

6-06

01-0

7-06

01-0

8-06

01-0

9-06

01-1

0-06

01-1

1-06

01-1

2-06

01-0

1-07

01-0

2-07

01-0

3-07

01-0

4-07

01-0

5-07

01-0

6-07

01-0

7-07

01-0

8-07

01-0

9-07

01-1

0-07

01-1

1-07

01-1

2-07

01-0

1-08

01-0

2-08

01-0

3-08

01-0

4-08

01-0

5-08

01-0

6-08

01-0

7-08

01-0

8-08

01-0

9-08

01-1

0-08

01-1

1-08

(%)

0

2

4

6

8

10

12

14

16

18

20

Libor USD 180 days (daily) One year banks loans

Fed funds rate Reserve requirement rate (second axis)

21/07/2009

44

Temporal de nieve

(El peor en un siglo)

Enero

Terremoto Sichuán

(segundo terremoto más desastroso de la historia de China)

Mayo

Olimpiadas

(Paralización de 3.000 obras de construcción y de industrias por motivos ambientales)

Agosto

Crisis financiera Septiembre

China 2008: Annus horribilis

Fuente: Elaborado en base a datos del International Copper Study Group (ICSG)

Copper ConsumersCopper ConsumersLeading Countries by Decades

(1960-1969)

Countries with most increase/decrease in copper con sumption

21/07/2009

45

Fuente: Elaborado en base a datos del International Copper Study Group (ICSG)

Copper ConsumersCopper ConsumersLeading Countries by Decades

(1970-1979)

Countries with most increase/decrease in copper con sumption

Fuente: Elaborado en base a datos del International Copper Study Group (ICSG)

Copper ConsumersCopper ConsumersLeading Countries by Decades

(1980-1989)

Countries with most increase/decrease in copper con sumption

21/07/2009

46

Fuente: Elaborado en base a datos del International Copper Study Group (ICSG)

Copper ConsumersCopper ConsumersLeading Countries by Decades

(1990-1999)

Countries with most increase/decrease in copper con sumption

Fuente: Elaborado en base a datos del International Copper Study Group (ICSG)

Copper ConsumersCopper ConsumersLeading Countries by Decades

(2000-2008)

Countries with most increase/decrease in copper con sumption

21/07/2009

47

Fuente: Elaborado en base a datos del International Copper Study Group (ICSG)

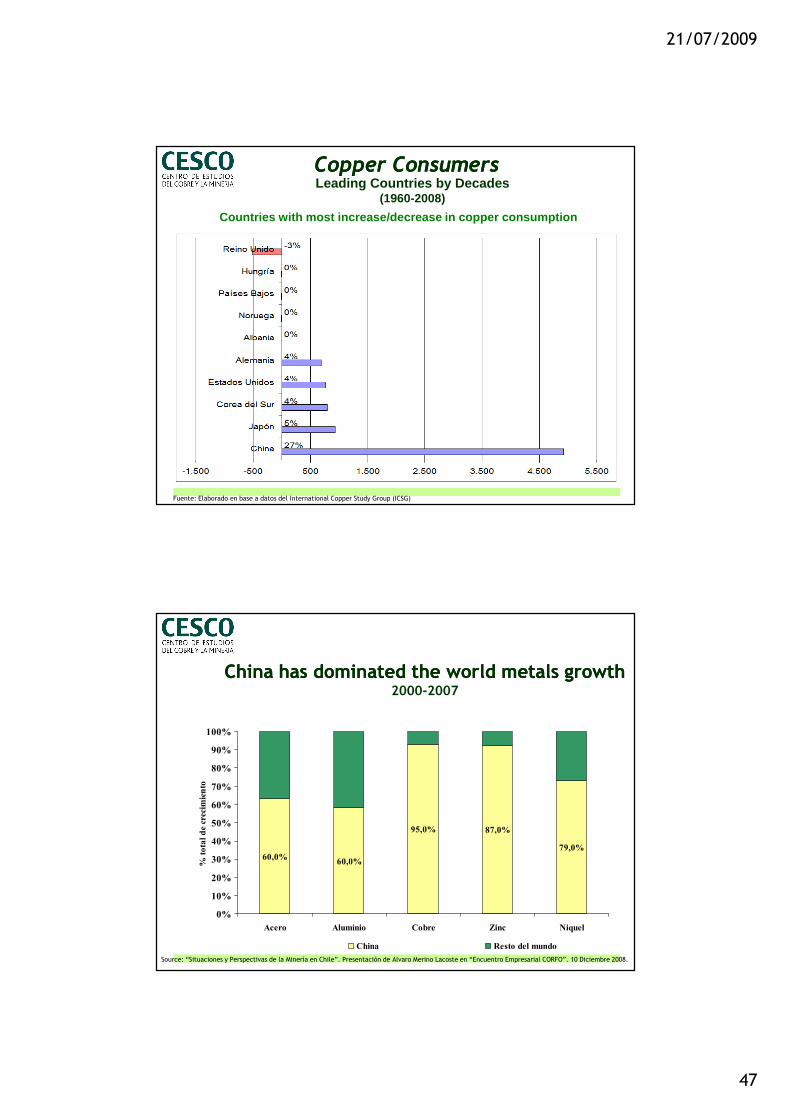

Copper ConsumersCopper ConsumersLeading Countries by Decades

(1960-2008)

Countries with most increase/decrease in copper con sumption

China has dominated the world metals growthChina has dominated the world metals growth2000-2007

60,0%60,0%

95,0% 87,0%

79,0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Acero Aluminio Cobre Zinc Niquel

% total de crecimiento

China Resto del mundo

Source: “Situaciones y Perspectivas de la Minería en Chile”. Presentación de Alvaro Merino Lacoste en “Encuentro Empresarial CORFO”. 10 Diciembre 2008.

21/07/2009

48

Mining Industry in Chile

Juan Carlos Guajardo B.

Executive Director

Friday 9th January 2009

Center for Copper and Mining Studies