Minerals & Metals Presented by: Albert Chou Davis (Jinqiu) Wei Mike Bergmann Xin Lu.

170

Minerals & Metals Minerals & Metals Presented by: Presented by: Albert Chou Albert Chou Davis (Jinqiu) Wei Davis (Jinqiu) Wei Mike Bergmann Mike Bergmann Xin Lu Xin Lu

-

Upload

briana-mccarthy -

Category

Documents

-

view

214 -

download

0

Transcript of Minerals & Metals Presented by: Albert Chou Davis (Jinqiu) Wei Mike Bergmann Xin Lu.

Minerals & MetalsMinerals & Metals

Presented by:Presented by:

Albert ChouAlbert Chou

Davis (Jinqiu) WeiDavis (Jinqiu) Wei

Mike BergmannMike Bergmann

Xin LuXin Lu

Copper Mining IndustryCopper Mining Industry

Overall IntroductionOverall Introduction Product UseProduct Use Production ProcessProduction Process Structure of IndustryStructure of Industry Financial StructureFinancial Structure Risk AssessmentRisk Assessment Recommended StrategyRecommended Strategy

Overall Introduction-1Overall Introduction-1

Oldest metal known to humansOldest metal known to humans Infinite recyclable lifeInfinite recyclable life 33rdrd most widely used metal most widely used metal Sensitive to political situationSensitive to political situation Producers store copper in Producers store copper in

warehouses until it is sold and warehouses until it is sold and shipped to buyershipped to buyer

Overall Introduction-2Overall Introduction-2

Known resource 5.8 trillion poundsKnown resource 5.8 trillion pounds

Only 0.7 trillion pounds (12%) are Only 0.7 trillion pounds (12%) are minedmined

Also essential to human healthAlso essential to human health

ProductsProducts

SourcesSources OreOre ScrapsScraps

FormsForms RodsRods CathodesCathodes ConcentrateConcentrate

ProductsProducts

WiresWires SubstitutionSubstitution

Fiber OpticsFiber Optics

Pipes/TubesPipes/Tubes SubstitutionSubstitution

SteelSteel PlasticsPlastics AluminumAluminum

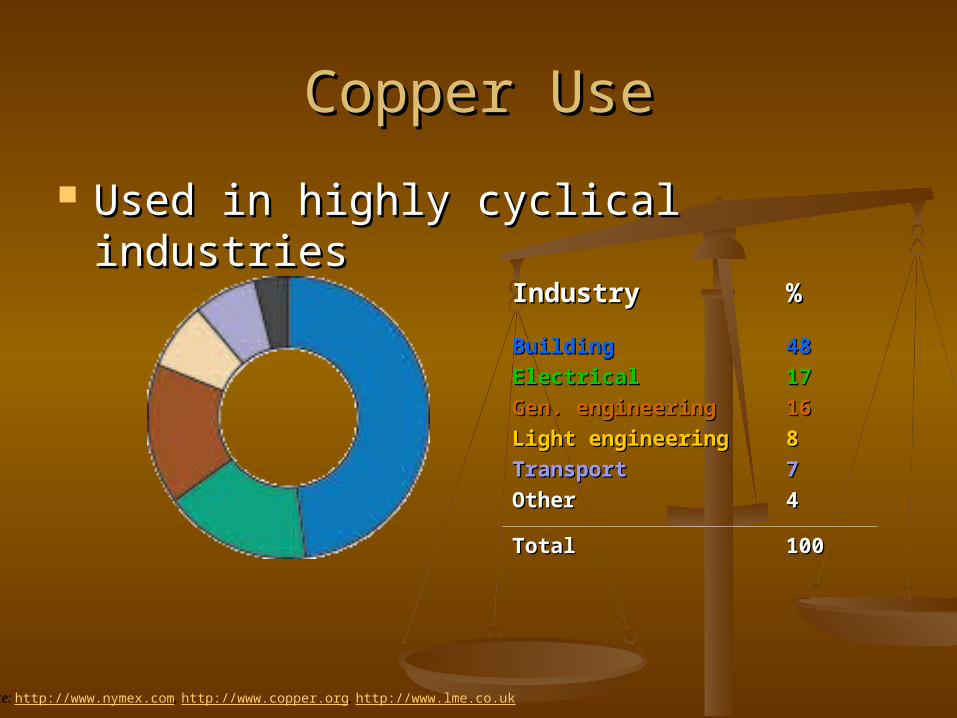

Copper UseCopper Use

Used in highly cyclical industriesUsed in highly cyclical industries

Source: http://www.nymex.com, http://www.copper.org, http://www.lme.co.uk

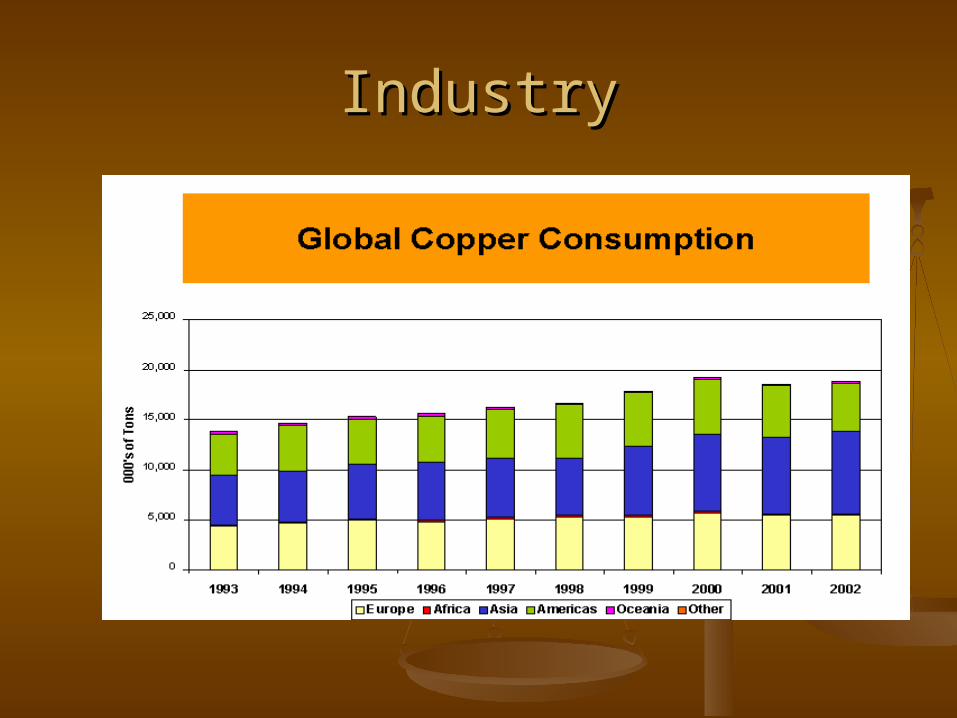

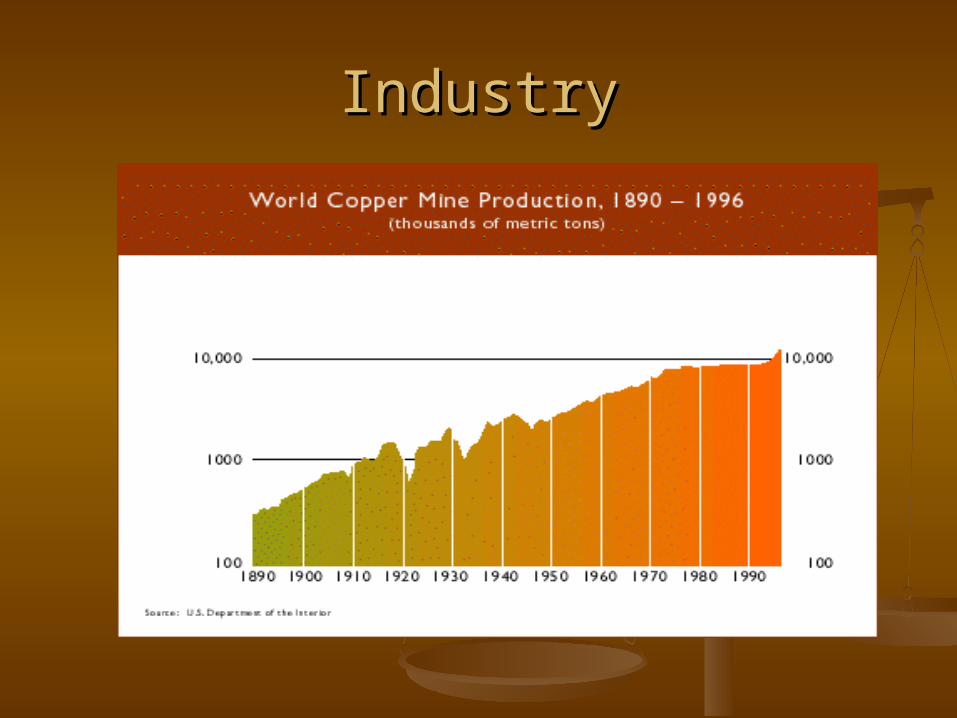

IndustryIndustry

BuildingBuilding

ElectricalElectrical

Gen. engineeringGen. engineering

Light engineeringLight engineering

TransportTransport

OtherOther

%%

4848

1717

1616

88

77

44

TotalTotal 100100

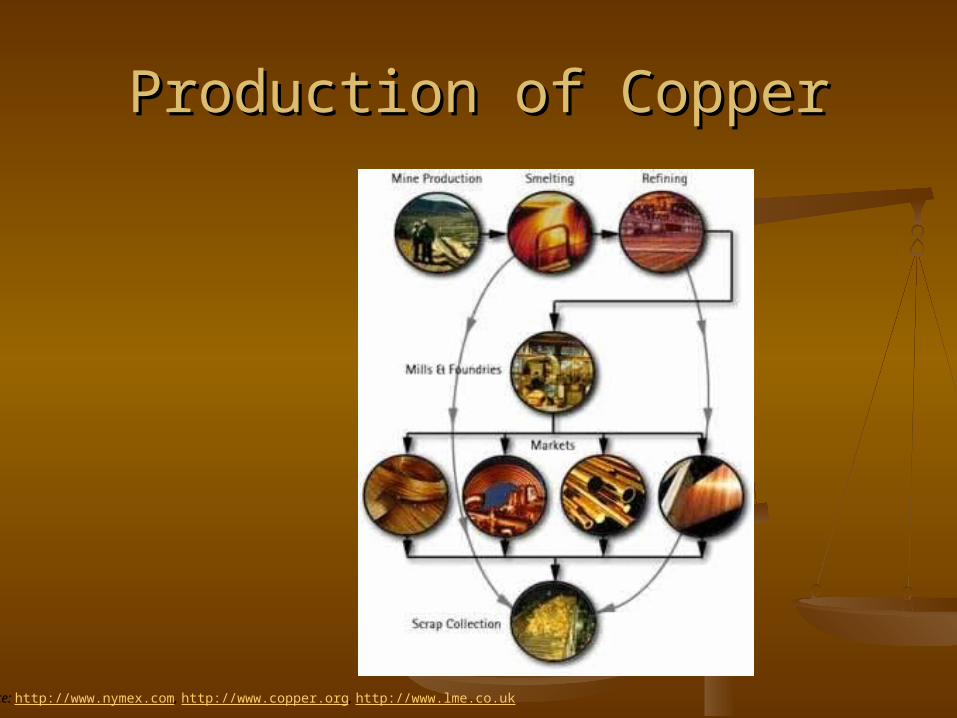

Production of CopperProduction of Copper

Source: http://www.nymex.com, http://www.copper.org, http://www.lme.co.uk

IndustryIndustry

IndustryIndustry

RivalsRivals

77 firms internationally competing77 firms internationally competing

Compete on price/low cost Compete on price/low cost productionproduction

Product QualityProduct Quality

Customer ServiceCustomer Service

Key Success FactorsKey Success Factors

Economies of ScaleEconomies of Scale

Refining technologiesRefining technologies

LocationLocation

Cost StructureCost Structure

Research and DevelopmentResearch and Development

ExplorationExploration

TransportationTransportation

StorageStorage

Cost StructureCost Structure

General Operation CostGeneral Operation Cost

Sales and AdministrativeSales and Administrative

Interest expensesInterest expenses

Depreciation, Depletion and Depreciation, Depletion and AmortizationAmortization

Risk Assessment-1Risk Assessment-1

Economic and PoliticalEconomic and Political Cyclical and Volatile price of Copper Cyclical and Volatile price of Copper

and other substitutesand other substitutes Environmental ConditionsEnvironmental Conditions Licenses and PermitsLicenses and Permits Laws and RegulationsLaws and Regulations

Risk Assessment-2Risk Assessment-2

Nature of Mineral Exploration and Nature of Mineral Exploration and MiningMining

Environmental RisksEnvironmental Risks Reserve EstimatesReserve Estimates Worldwide OperationsWorldwide Operations Licenses and PermitsLicenses and Permits

Recommended StrategyRecommended Strategy

Selection Criteria for Long Term InvestmentSelection Criteria for Long Term Investment

Larger companies with strong financial Larger companies with strong financial resourcesresources

Companies that have good access to resources Companies that have good access to resources and (potential) marketsand (potential) markets

Companies that already demonstrate superior Companies that already demonstrate superior cost structure and lower production costscost structure and lower production costs

Companies with large reserves of high grade Companies with large reserves of high grade oreore

Uranium Mining IndustryUranium Mining Industry

Overall IntroductionOverall Introduction Product UseProduct Use Production ProcessProduction Process Structure of IndustryStructure of Industry Important TrendImportant Trend Risk AssessmentRisk Assessment Recommended StrategyRecommended Strategy

Overall IntroductionOverall Introduction

15% of Canada's electricity comes 15% of Canada's electricity comes from nuclear powerfrom nuclear power

Increasing demand for nuclear fuelIncreasing demand for nuclear fuel Uranium is most commonly found in Uranium is most commonly found in

nature as an oxide, and usually as an nature as an oxide, and usually as an ore in a chemically complex bodyore in a chemically complex body

A significant amount can be found in A significant amount can be found in the oceans of the world the oceans of the world

Overall IntroductionOverall Introduction Uranium (U):Uranium (U): A mildly radioactive element with A mildly radioactive element with

two isotopes which are fissile (U-235 and U-233) two isotopes which are fissile (U-235 and U-233) and two which are fertile (U-238 and U-234). and two which are fertile (U-238 and U-234). Uranium is the basic fuel of nuclear energy. Uranium is the basic fuel of nuclear energy.

Uranium hexafluoride (UFUranium hexafluoride (UF66): ): A compound of A compound of uranium which is a gas above 56oC and is thus a uranium which is a gas above 56oC and is thus a suitable form in which to enrich the uranium. suitable form in which to enrich the uranium.

Uranium oxide concentrate (UUranium oxide concentrate (U33OO88): ): The The mixture of uranium oxides produced after milling mixture of uranium oxides produced after milling uranium ore from a mine. Sometimes loosely uranium ore from a mine. Sometimes loosely called yellowcake. It is khaki in colour and is called yellowcake. It is khaki in colour and is usually represented by the empirical formula usually represented by the empirical formula U3O8. Uranium is sold in this form. U3O8. Uranium is sold in this form.

ProductProduct ApplicationApplication

Providing electricityProviding electricity Producing medical isotopesProducing medical isotopes Using it as a weapon & armour (depleted Using it as a weapon & armour (depleted

uranium)uranium) Co-productCo-product

a co-product with copper (at Olympic a co-product with copper (at Olympic Dam in Australia)Dam in Australia)

a by-product from the treatment of other a by-product from the treatment of other ores, such as the gold-bearing ores of ores, such as the gold-bearing ores of South Africa (low concentration of South Africa (low concentration of uranium) uranium)

ProductProduct

SubstitutesSubstitutes Fossil fuel Fossil fuel CoalCoal Any other alternative fuels (solar, wind-Any other alternative fuels (solar, wind-

driven, or tidal reserves)driven, or tidal reserves)

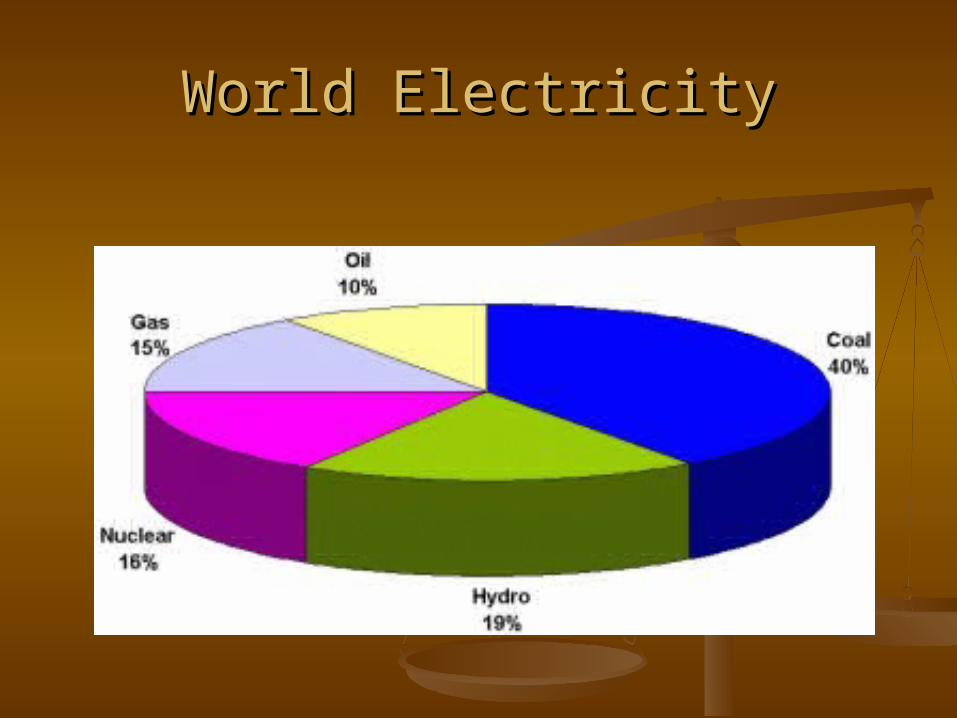

World ElectricityWorld Electricity

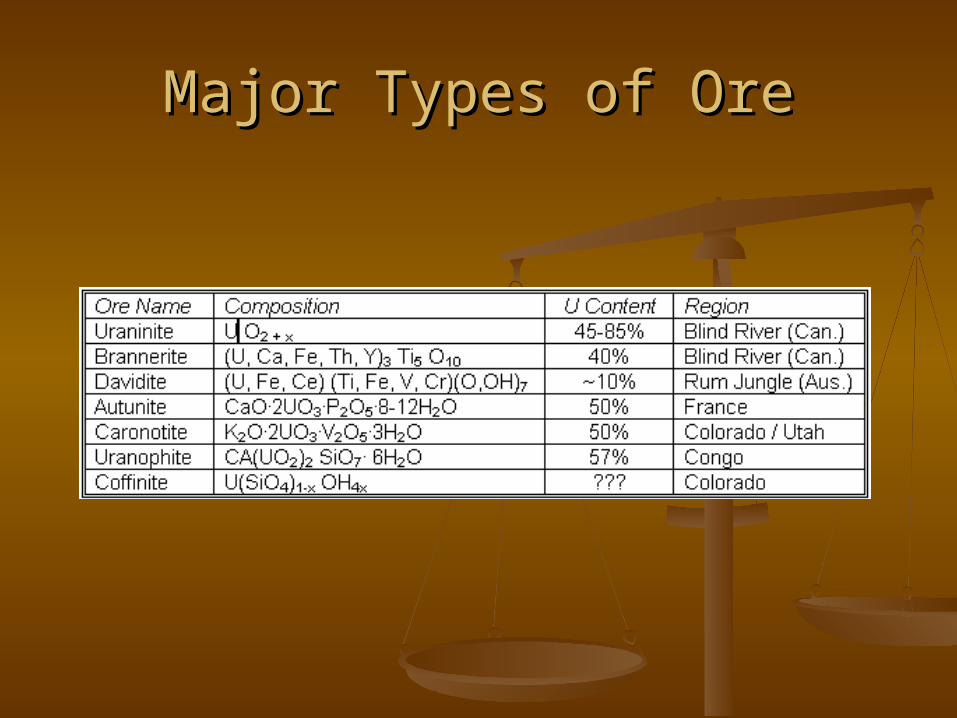

Major Types of OreMajor Types of Ore

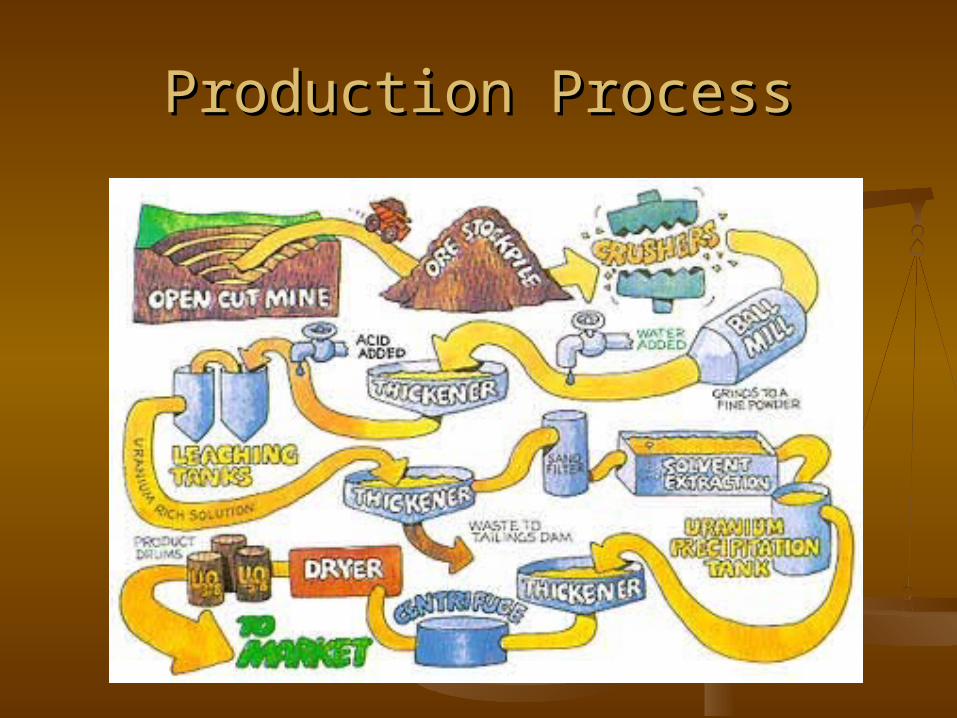

Production ProcessProduction Process

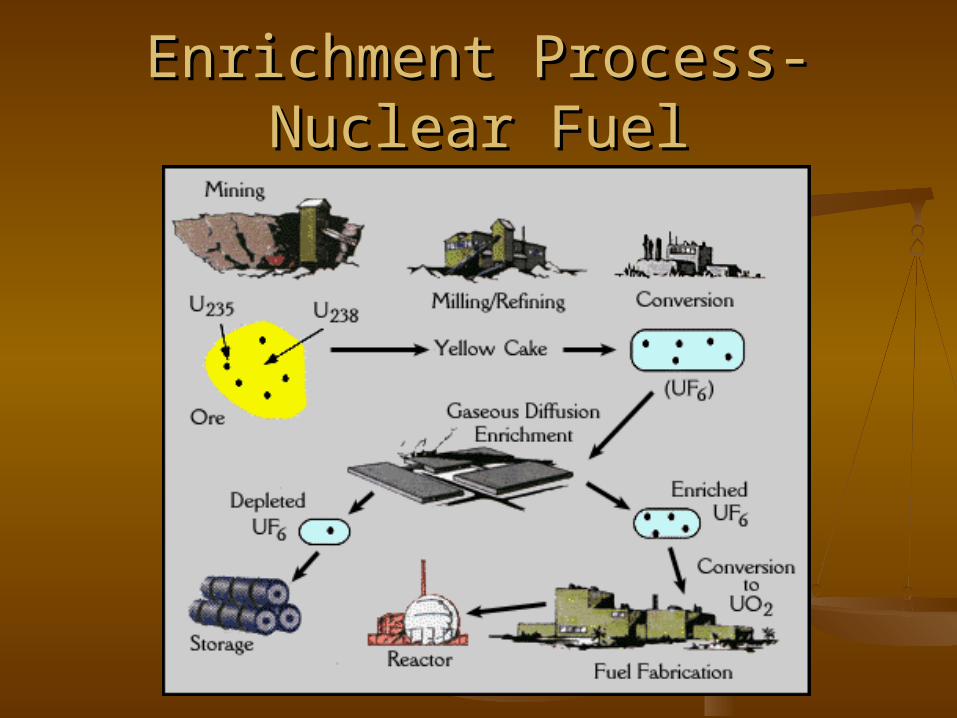

Enrichment Process-Nuclear Enrichment Process-Nuclear FuelFuel

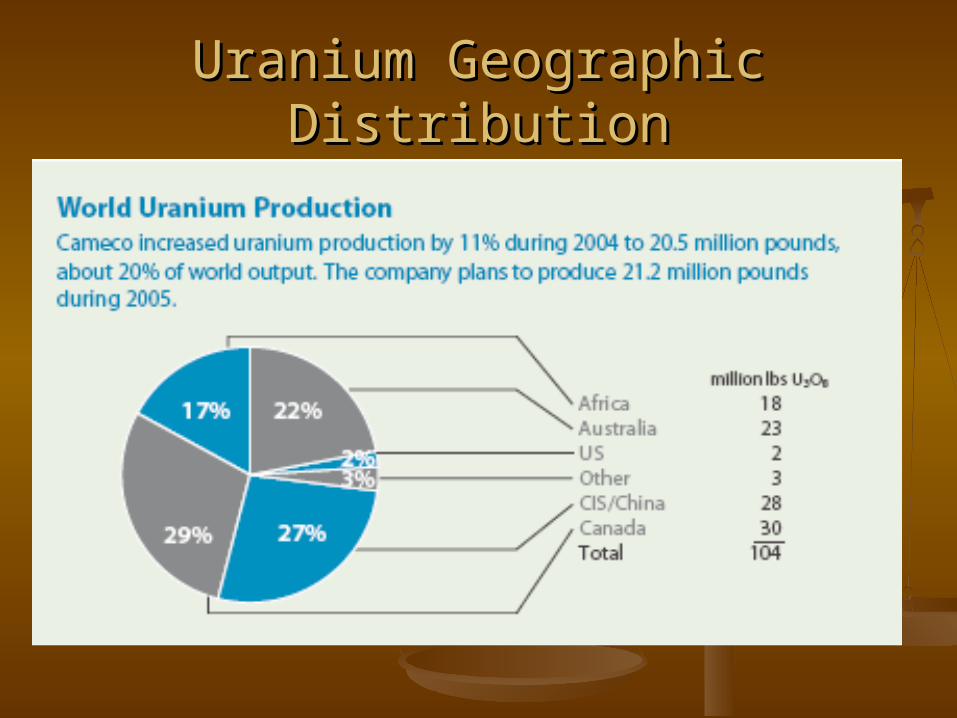

Uranium Geographic DistributionUranium Geographic Distribution

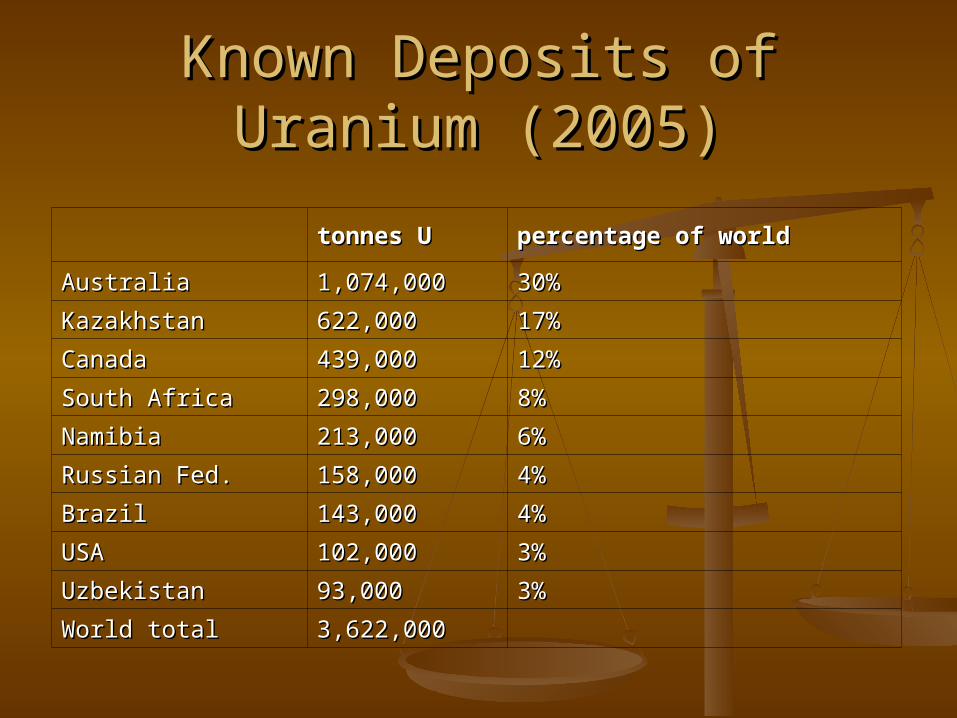

Known Deposits of Uranium Known Deposits of Uranium (2005)(2005)

tonnes Utonnes U percentage of worldpercentage of world

AustraliaAustralia 1,074,0001,074,000 30%30%

Kazakhstan Kazakhstan 622,000622,000 17%17%

Canada Canada 439,000439,000 12%12%

South Africa South Africa 298,000298,000 8%8%

Namibia Namibia 213,000213,000 6%6%

Russian Fed.Russian Fed. 158,000158,000 4%4%

Brazil Brazil 143,000143,000 4%4%

USA USA 102,000102,000 3%3%

UzbekistanUzbekistan 93,00093,000 3%3%

World total World total 3,622,0003,622,000

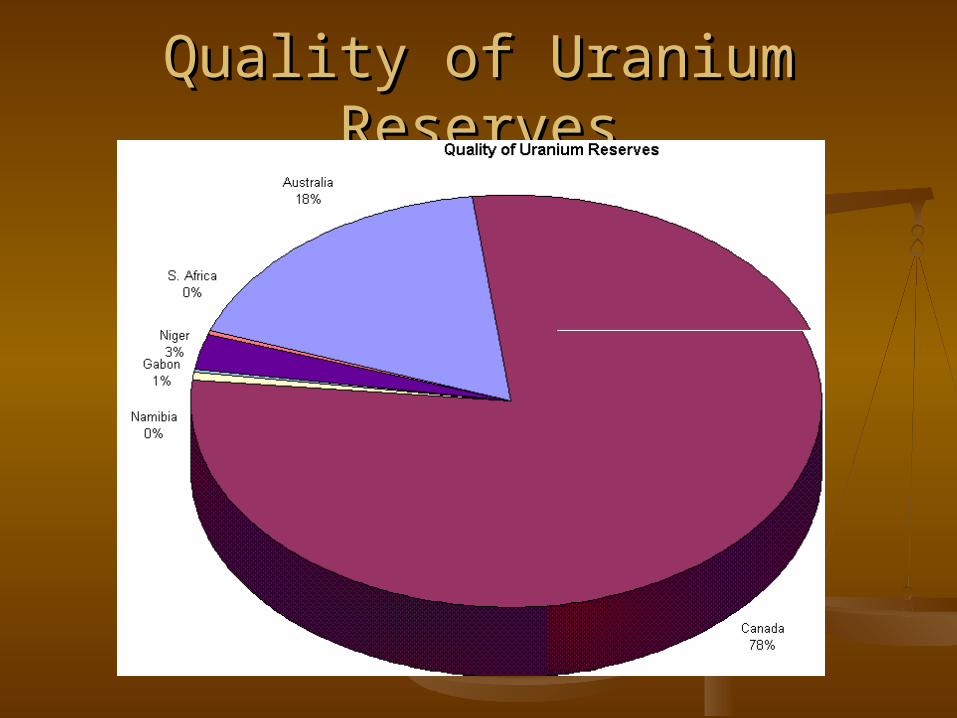

Quality of Uranium ReservesQuality of Uranium Reserves

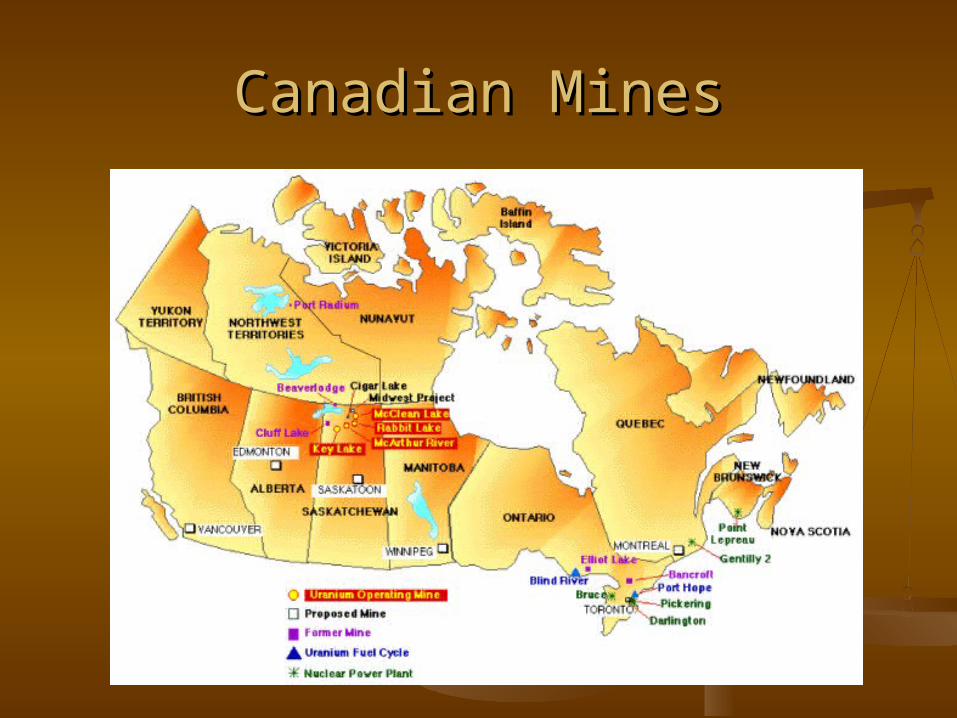

Canadian MinesCanadian Mines

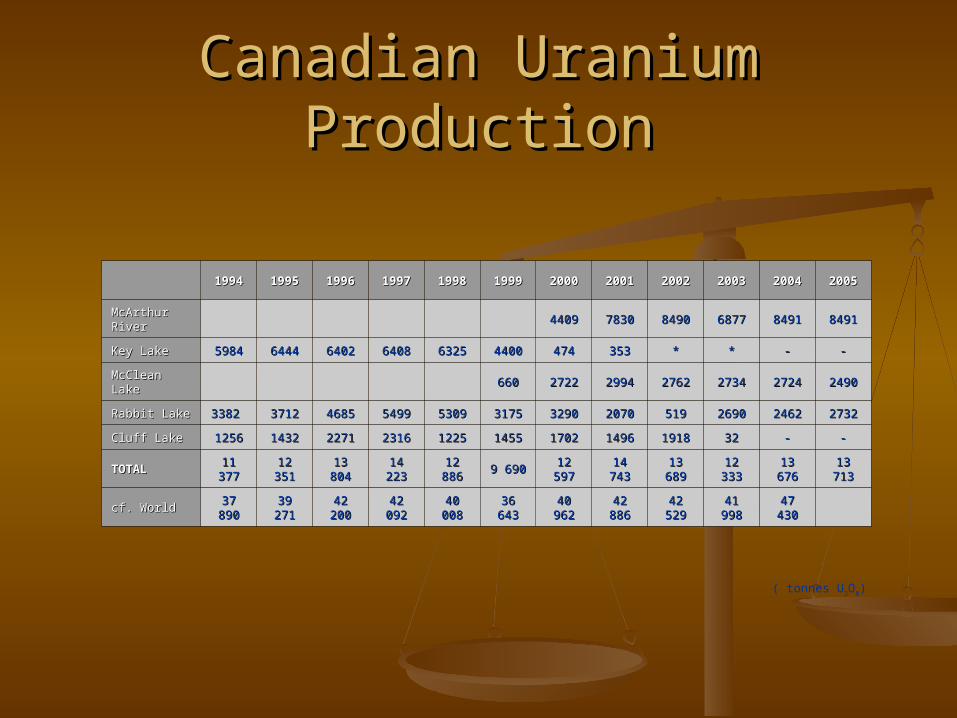

Canadian Uranium ProductionCanadian Uranium Production

( tonnes U3O8)

19941994 19951995 19961996 19971997 19981998 19991999 20002000 20012001 20022002 20032003 20042004 20052005

McArthur McArthur RiverRiver 44094409 78307830 84908490 68776877 84918491 84918491

Key Lake Key Lake 59845984 64446444 64026402 64086408 63256325 44004400 474474 353353 ** ** -- --

McClean McClean LakeLake 660660 27222722 29942994 27622762 27342734 27242724 24902490

Rabbit Lake Rabbit Lake 3382 3382 37123712 46854685 54995499 53095309 31753175 32903290 20702070 519519 26902690 24622462 27322732

Cluff Lake Cluff Lake 12561256 14321432 22712271 23162316 12251225 14551455 17021702 14961496 19181918 3232 -- --

TOTAL TOTAL 11 11 377377

12 12 351351

13 13 804804

14 14 223223

12 12 886886 9 6909 690 12 12

59759714 14

74374313 13

68968912 12

33333313 13

67667613 13

713713

cf. World cf. World 37 37 890890

39 39 271271

42 42 200200

42 42 092092

40 40 008008

36 36 643643

40 40 962962

42 42 886886

42 42 529529

41 41 998998

47 47 430430

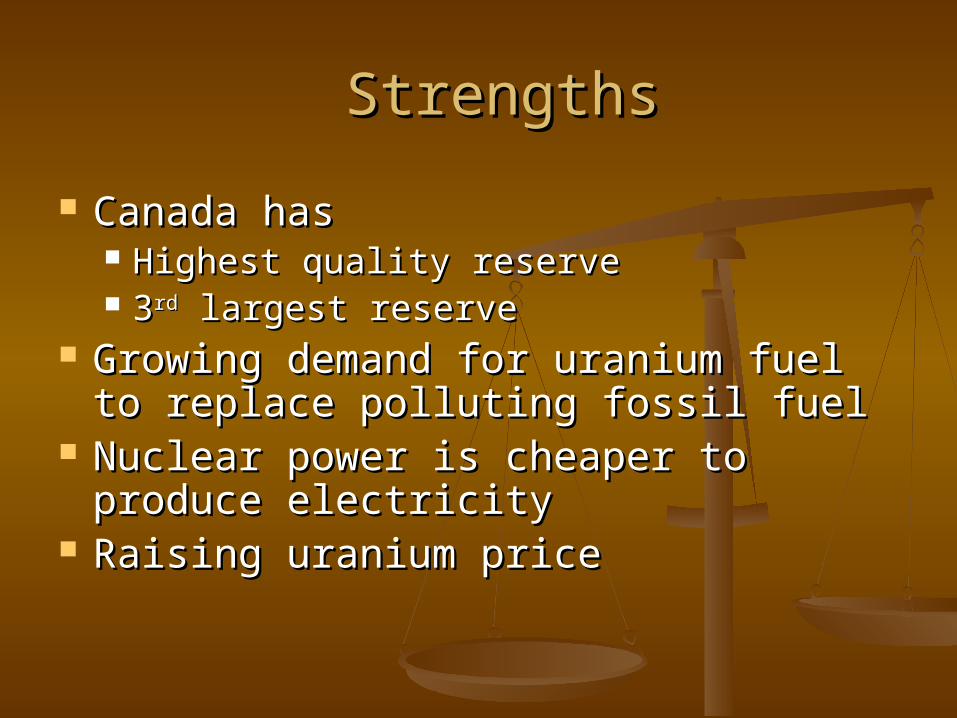

StrengthsStrengths

Canada has Canada has Highest quality reserveHighest quality reserve 33rdrd largest reserve largest reserve

Growing demand for uranium fuel to Growing demand for uranium fuel to replace polluting fossil fuelreplace polluting fossil fuel

Nuclear power is cheaper to produce Nuclear power is cheaper to produce electricityelectricity

Raising uranium priceRaising uranium price

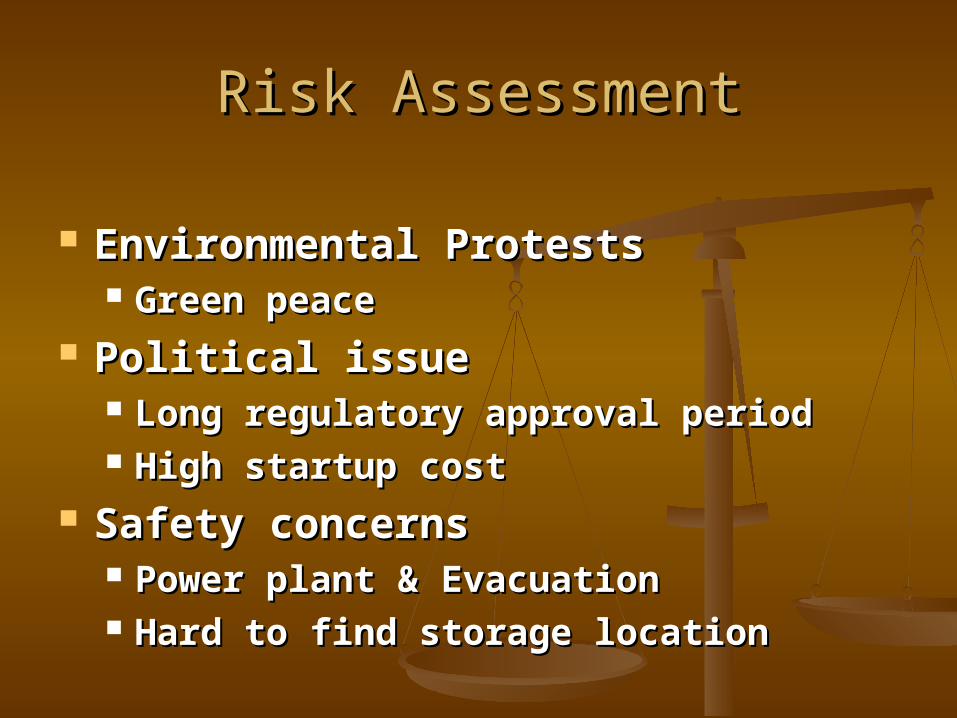

Risk AssessmentRisk Assessment

Environmental ProtestsEnvironmental Protests Green peaceGreen peace

Political issuePolitical issue Long regulatory approval periodLong regulatory approval period High startup costHigh startup cost

Safety concernsSafety concerns Power plant & Evacuation Power plant & Evacuation Hard to find storage locationHard to find storage location

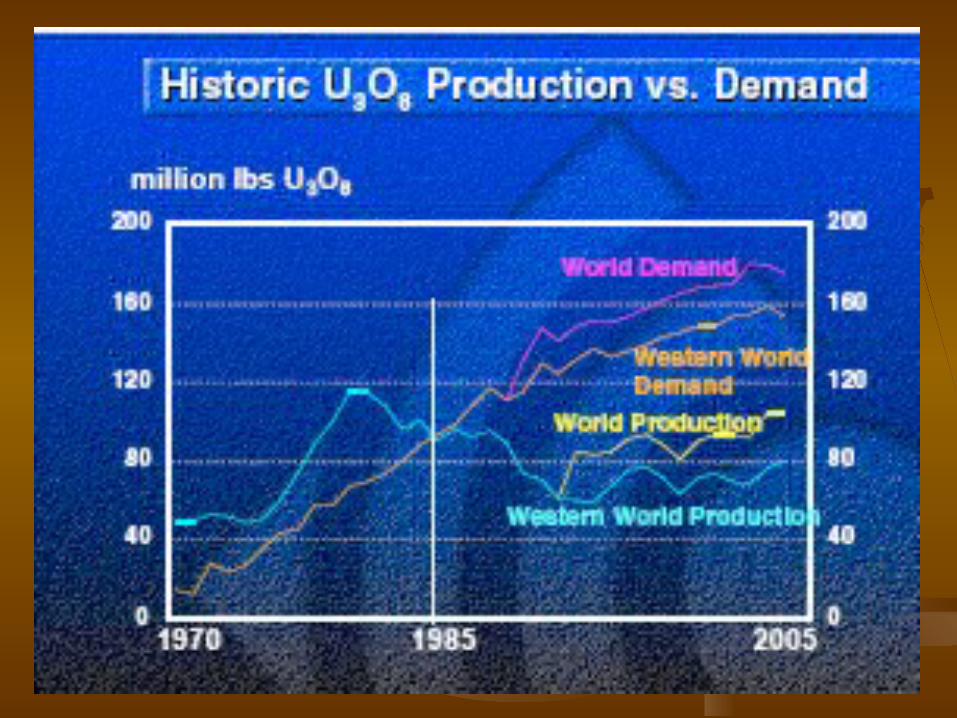

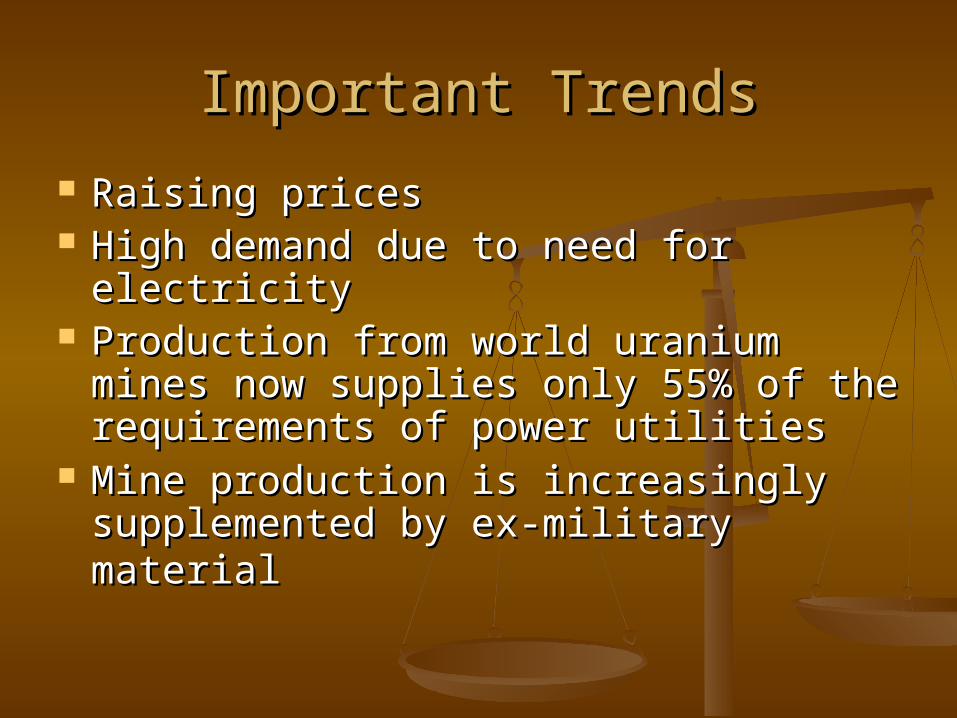

Important TrendsImportant Trends

Raising pricesRaising prices High demand due to need for High demand due to need for

electricityelectricity Production from world uranium mines Production from world uranium mines

now supplies only 55% of the now supplies only 55% of the requirements of power utilities requirements of power utilities

Mine production is increasingly Mine production is increasingly supplemented by ex-military materialsupplemented by ex-military material

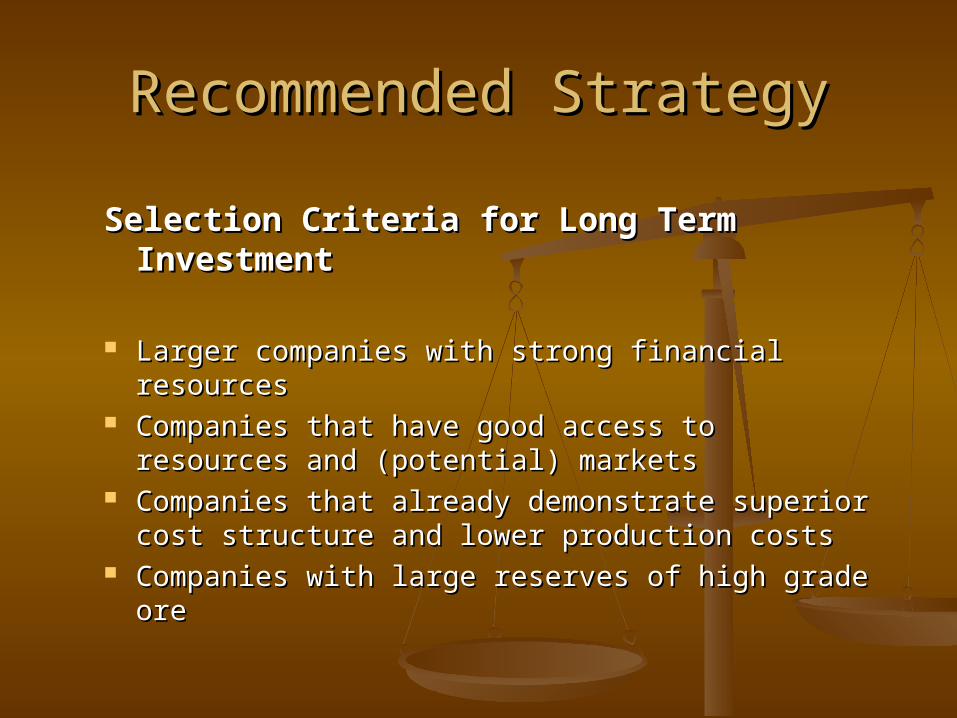

Recommended StrategyRecommended Strategy

Selection Criteria for Long Term Selection Criteria for Long Term InvestmentInvestment

Larger companies with strong financial resourcesLarger companies with strong financial resources Companies that have good access to resources Companies that have good access to resources

and (potential) marketsand (potential) markets Companies that already demonstrate superior Companies that already demonstrate superior

cost structure and lower production costscost structure and lower production costs Companies with large reserves of high grade oreCompanies with large reserves of high grade ore

Gold Mining IndustryGold Mining Industry

Overall IntroductionOverall Introduction Product UseProduct Use Production ProcessProduction Process Structure of IndustryStructure of Industry Financial StructureFinancial Structure Risk AssessmentRisk Assessment Recommended StrategyRecommended Strategy

Overall IntroductionOverall Introduction

Major ProductMajor ProductGOLDGOLD

Substitutes–Direct Substitutes

–Currency–Other precious metals

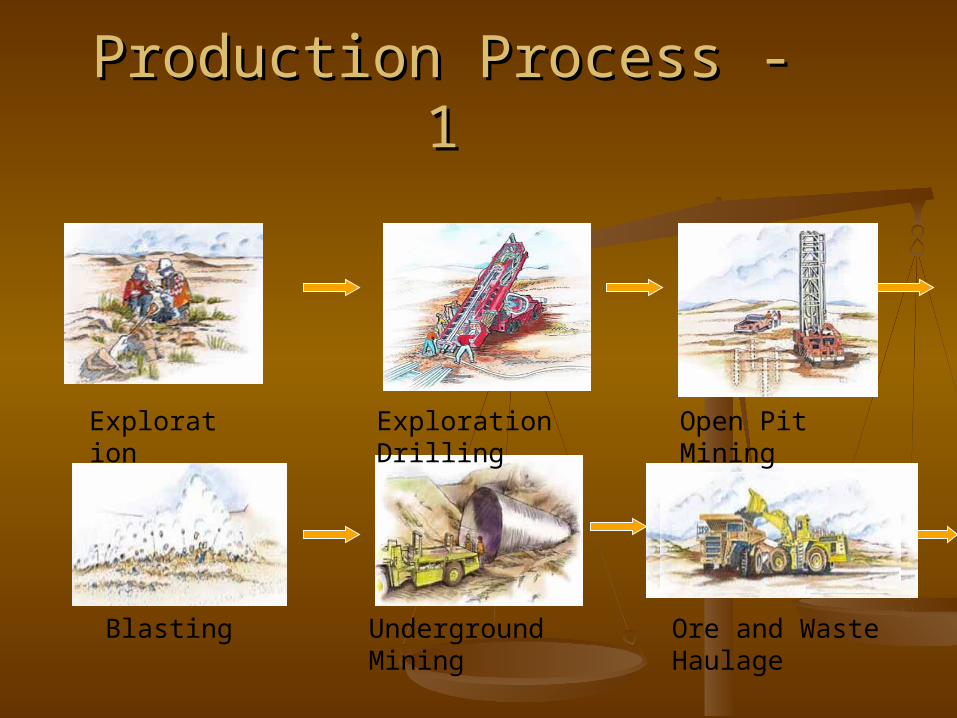

Production Process - 1Production Process - 1

Exploration Exploration Drilling Open Pit Mining

Blasting Underground Mining Ore and Waste Haulage

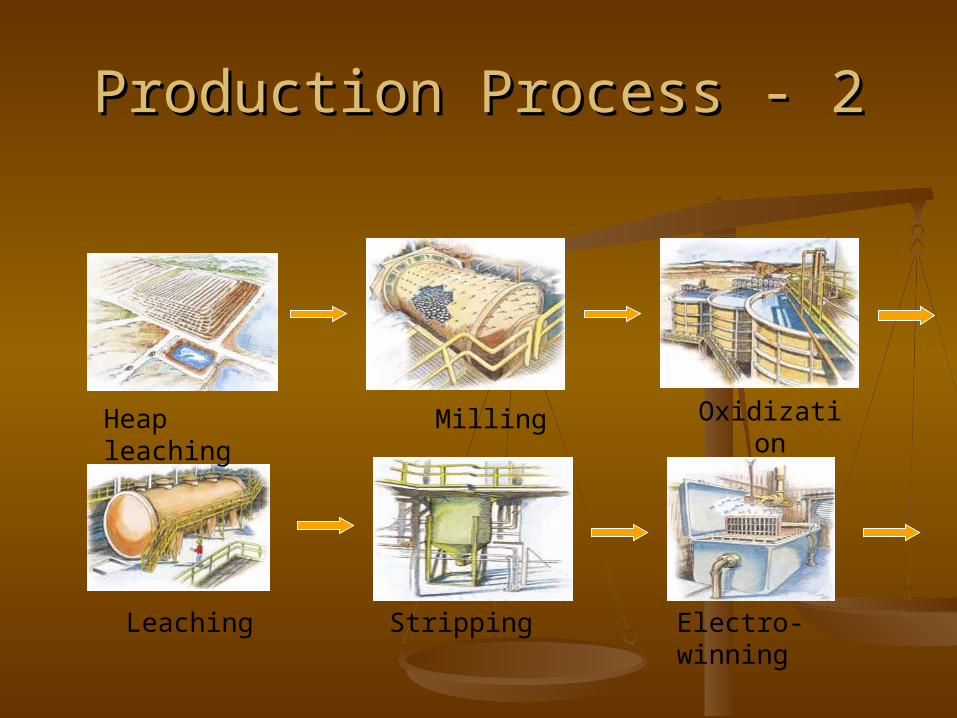

Production Process - 2Production Process - 2

Heap leaching Milling Oxidization

Leaching Stripping Electro-winning

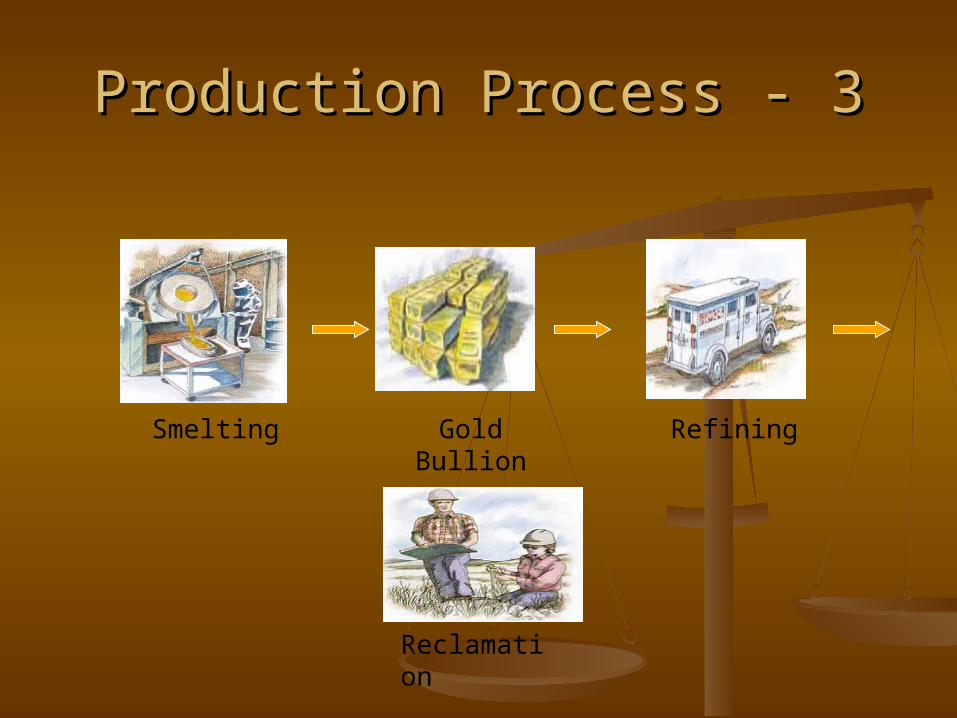

Production Process - 3Production Process - 3

Smelting Gold Bullion

Reclamation

Refining

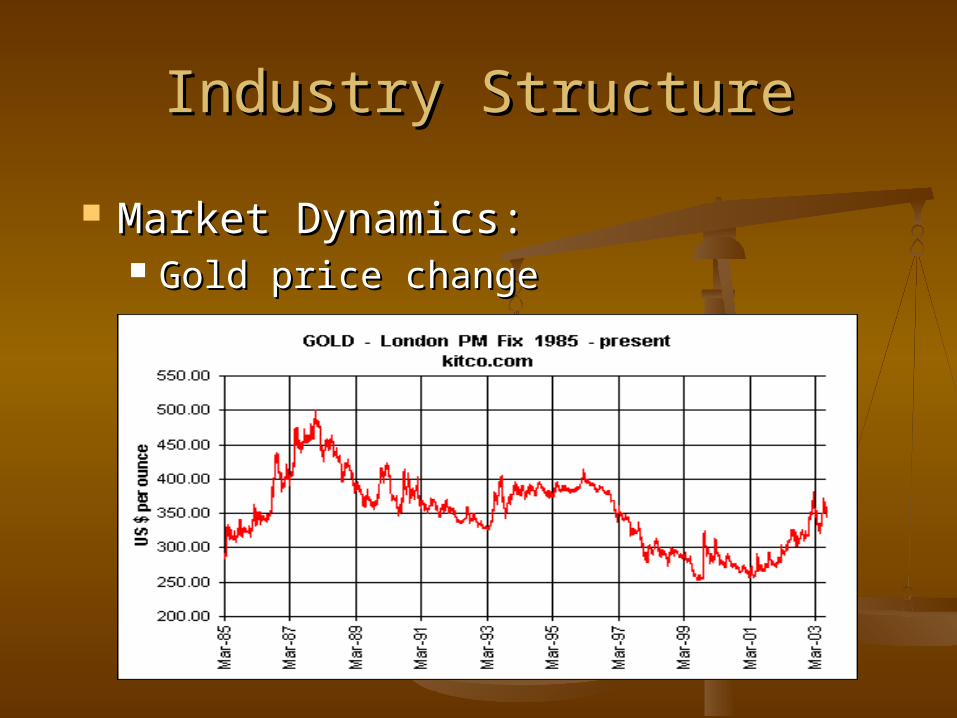

Industry StructureIndustry Structure

Market Dynamics:Market Dynamics: Gold price change Gold price change

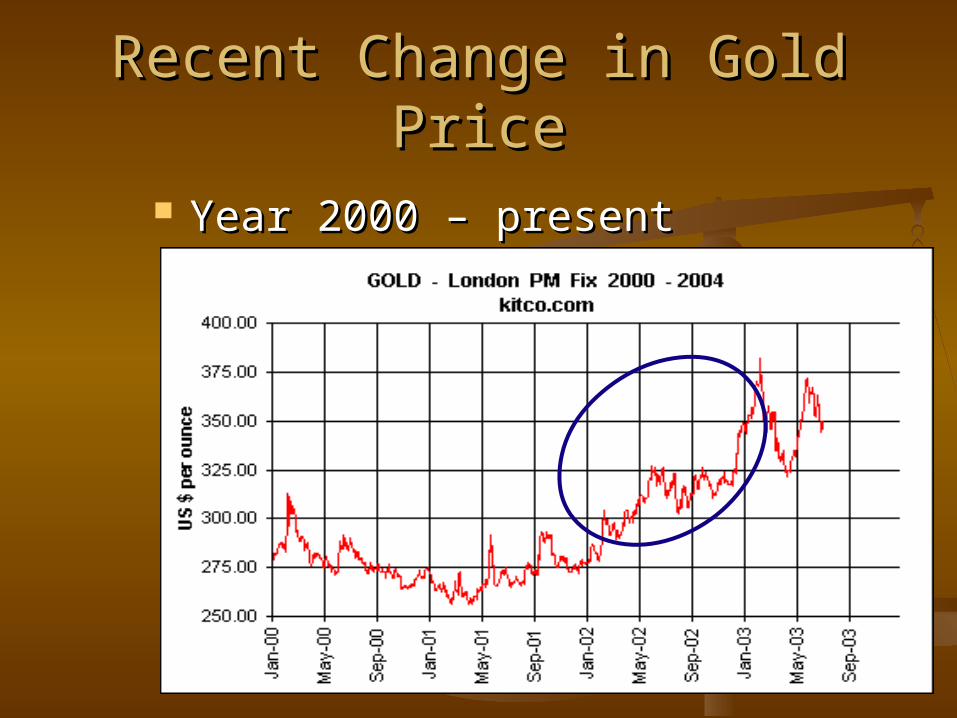

Recent Change in Gold PriceRecent Change in Gold Price

Year 2000 – presentYear 2000 – present

Industry Structure-2Industry Structure-2

Barrick Gold Corp. Barrick Gold Corp. Newmont Mining Newmont Mining Kinross Gold Corp.Kinross Gold Corp.

Meridian GoldMeridian Gold Agnico-Eagle Mines Agnico-Eagle Mines Glamis Gold Glamis Gold Goldcorp Inc. Goldcorp Inc. Cambior Inc. Cambior Inc. Ivanhoe MinesIvanhoe Mines Placer Dome Placer Dome

•Major companies (selected by assets)

Financial StructureFinancial Structure

Cost StructureCost Structure Exploration, research and developmentExploration, research and development General operation costsGeneral operation costs Depreciation, depletion and amortization Depreciation, depletion and amortization Interest expensesInterest expenses Write-down of assets Write-down of assets

Risk AssessmentRisk Assessment

Nature of Mineral Exploration and Nature of Mineral Exploration and MiningMining

Environmental RisksEnvironmental Risks Reserve EstimatesReserve Estimates Worldwide OperationsWorldwide Operations Licenses and PermitsLicenses and Permits Supply and DemandSupply and Demand

Recommended StrategyRecommended Strategy

Selection Criteria for Long Term InvestmentSelection Criteria for Long Term Investment

Larger companies with strong financial Larger companies with strong financial resourcesresources

Companies that have good access to resources Companies that have good access to resources and (potential) marketsand (potential) markets

Companies that already demonstrate superior Companies that already demonstrate superior cost structure and lower production costscost structure and lower production costs

Companies with large reserves of high grade Companies with large reserves of high grade oreore

Phelps Dodge

Phelps Dodge Corp. is one of the world’s largest copper producers

World leader in the production of molybdenum-based chemicals

Leading producers of continuous-cast copper rod

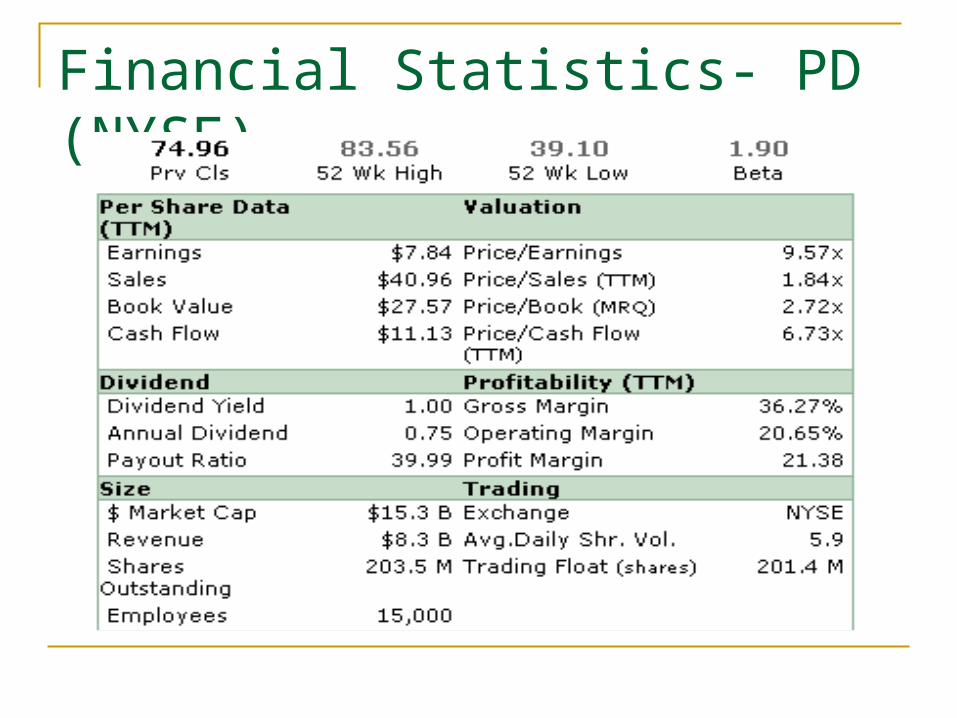

Financial Statistics- PD (NYSE)

2 years Stock Price Chart

Major Divisions

Phelps Dodge Mining Company (PDMC)

Phelps Dodge Industries (PDI)

PDMC’s Major Operations

Worldwide and vertically integrated copper operations

from mining through rod production, marketing and sales

Molybdenum operations from mining through conversion to chemical and

metallurgical products, marketing and sales Other mining operations and investment Worldwide mineral exploration, technology and

project development programs

PDMC’s Major Products

Copper related products Copper cathode Copper concentrate Copper rod

By-Products (Gold, silver, rhenium and sulfuric acid)

Molybdenum related products

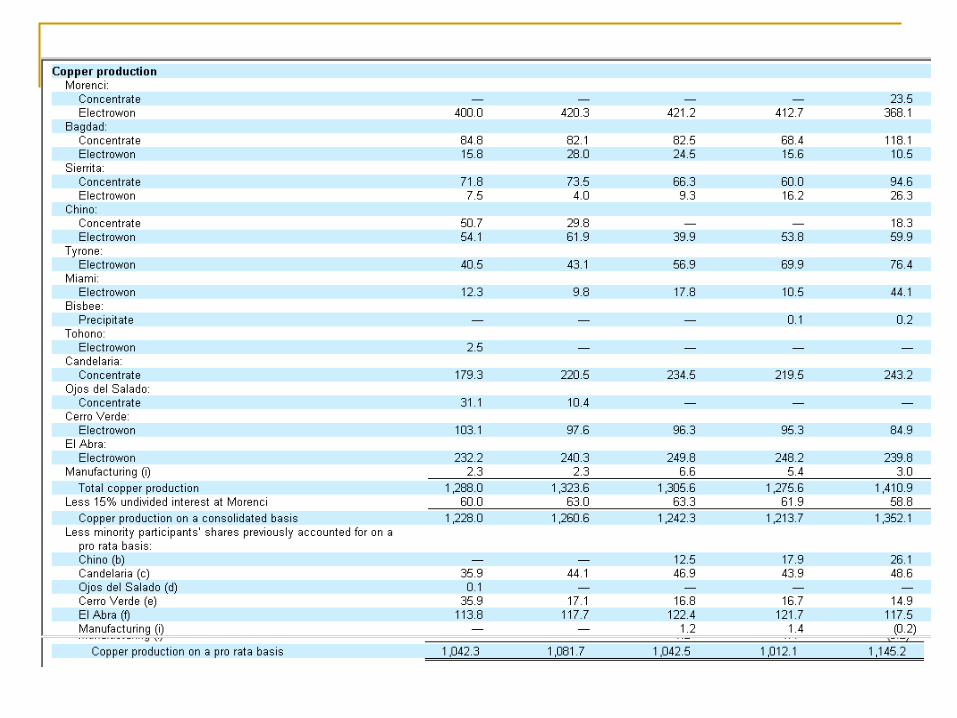

Copper

In 2005, PDMC produced 1,228,000 tons of copper on a consolidated basis (1,042,300 tons on a pro rata basis)

An additional 60,000 tons of copper for 15% undivided interest in the Morenci mine

Production of copper on pro rata basis constituted 53%of the copper mined in US

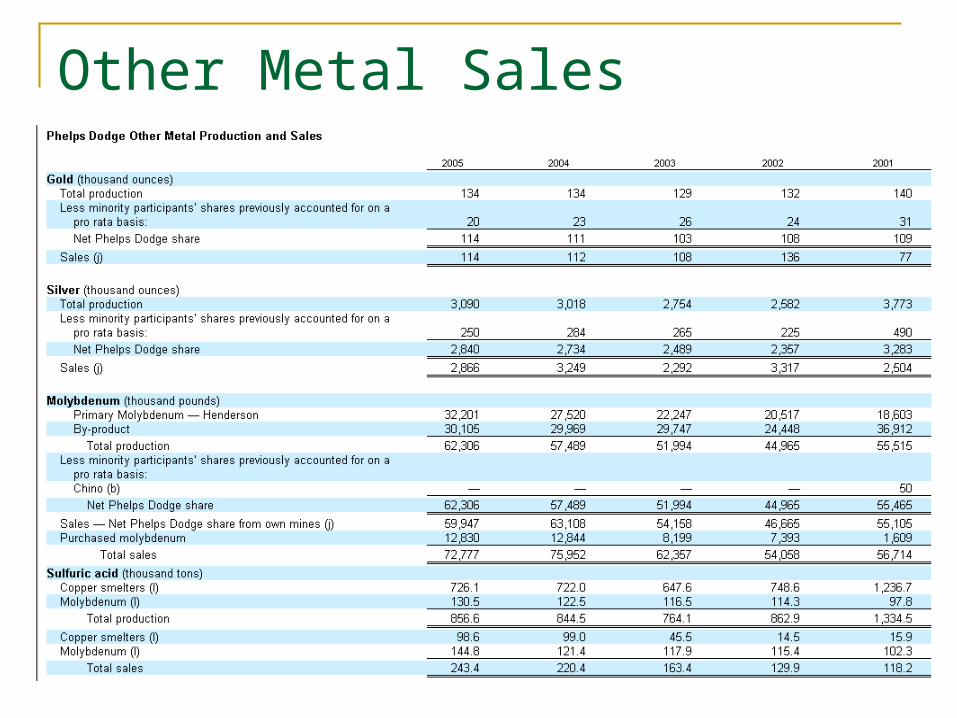

Molybdenum Concentrate

In 2005, PDMC produced 62.3 million pounds of molybdenum

High-purity, chemical-grade molybdenum concentrate is produced at Henderson mine in Colorado

Most of concentrate is produced for metallurgical markets (steel industries) to strengthen the steel and lubricant industry

PDI’s Wire and Cable

PDI produces magnet wire, copper and aluminum energy cables, specially conductors and other products for sale to original equipment manufacturers for US in electrical motors, generators, transformers, medical applications and public utilities

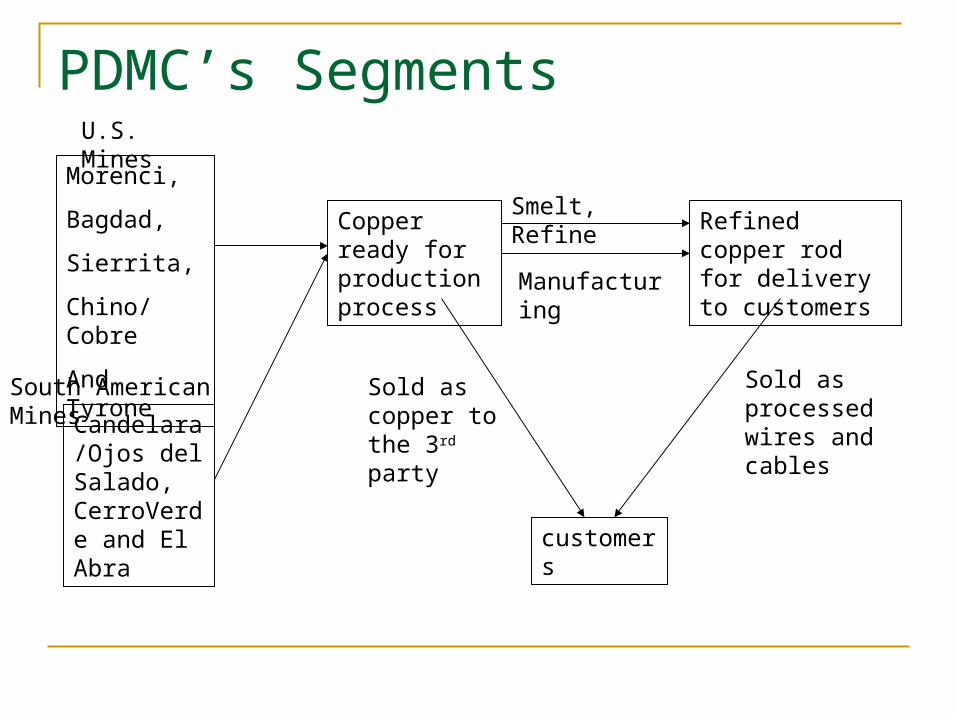

PDMC’s Segments

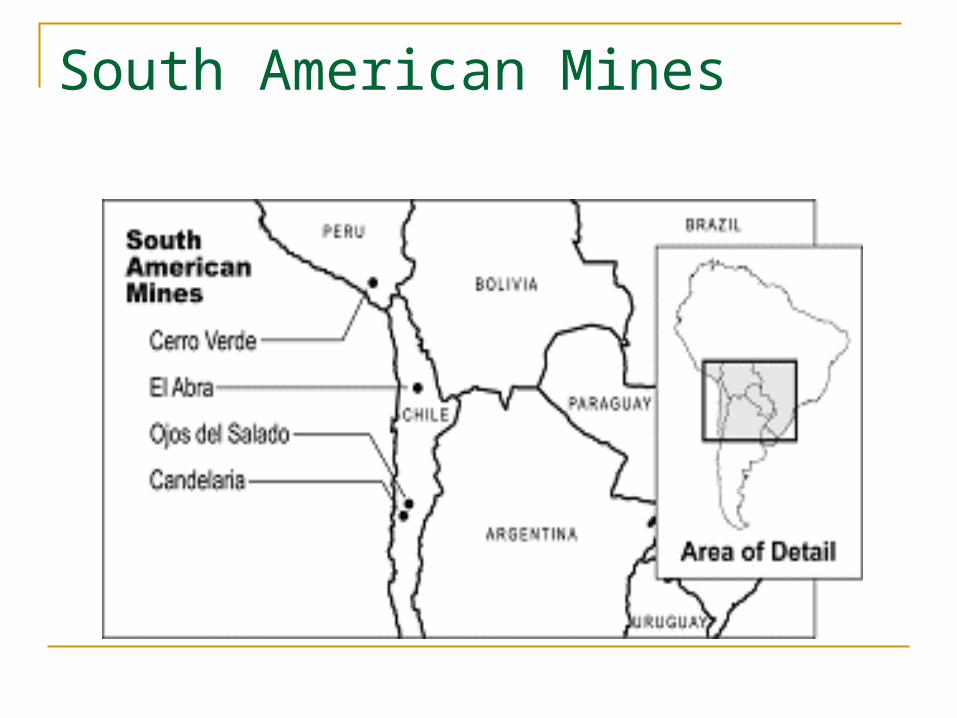

South American Mines

Morenci,

Bagdad,

Sierrita,

Chino/Cobre

And Tyrone

Candelara/Ojos del Salado, CerroVerde and El Abra

Copper ready for production process

Refined copper rod for delivery to customers

Smelt, Refine

Manufacturing

U.S. Mines

customers

Sold as copper to the 3rd party

Sold as processed wires and cables

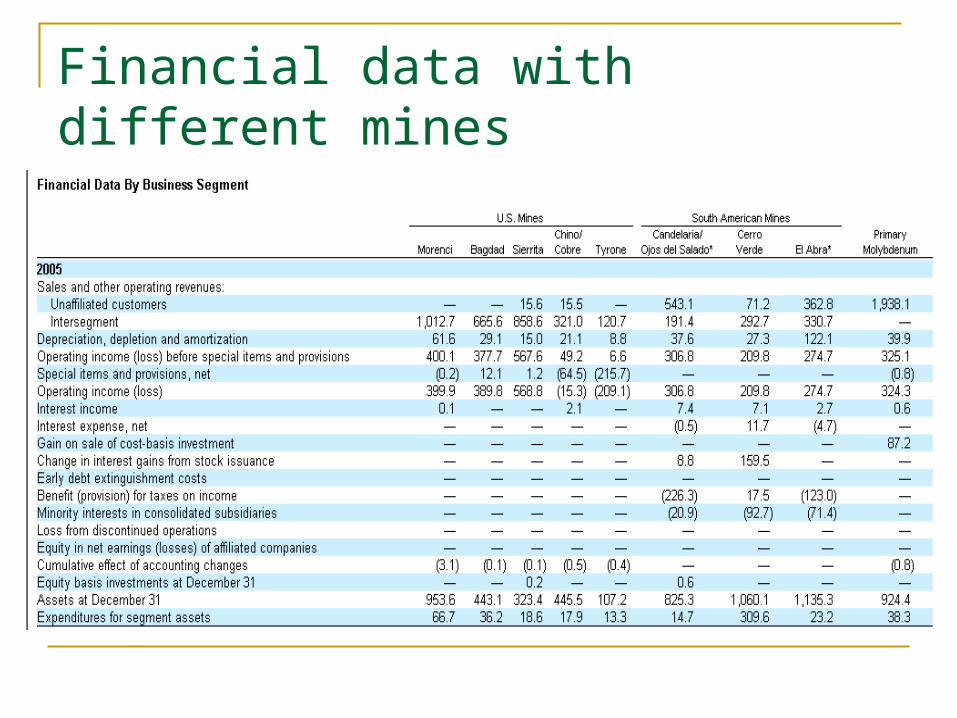

Financial data with different mines

PD’s mines segments

US Mines

South American Mines

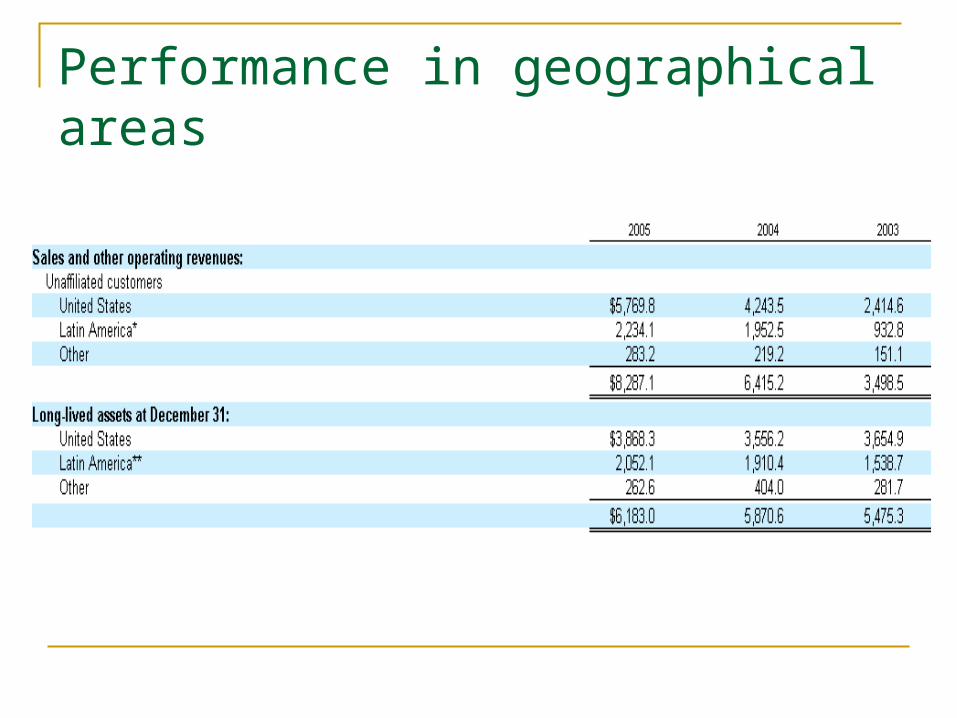

Performance in geographical areas

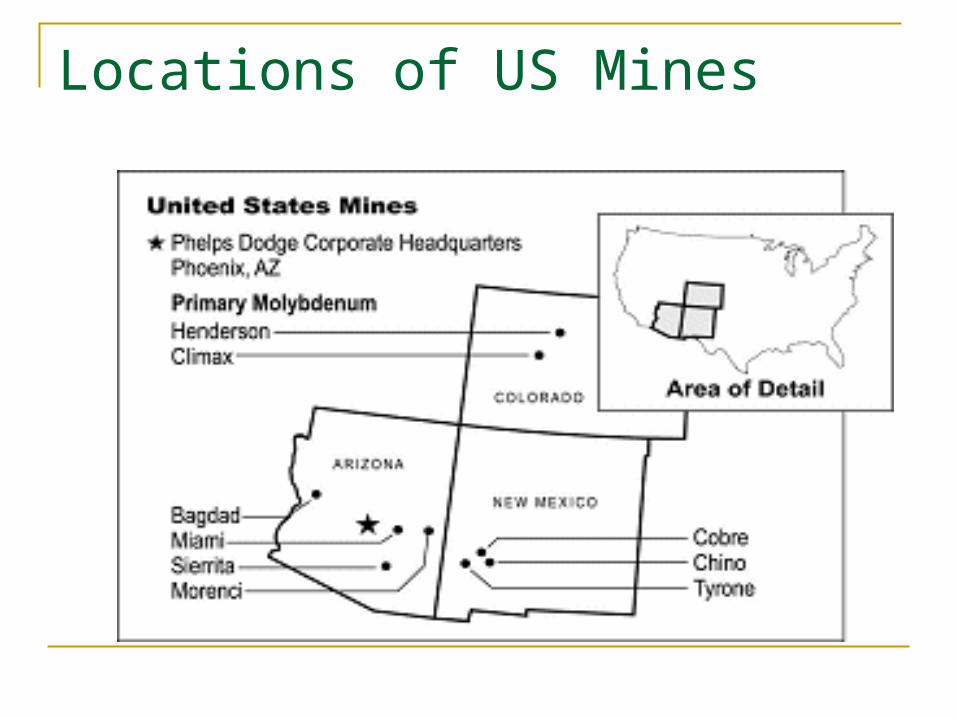

Locations of US Mines

Morenci

Leading position: the largest copper producing operation in North America

Operation Description: an open-pit mine, a concentrator, 4 solution extraction facilities 3 electronwinning tank houses.

Ownership: 85% undivided interest Annual Capacity:

410,000 tons electrowon cathode production crush-leach facility processes approximately 85,000 tons of

ore daily with the remaining ore processed through stockpile leaching.

Morenci’s Key Future Growth Factors On June 1, 2005, the Company’s board of directors

approved expenditures of $210 million to construct a concentrate-leach, direct-electrowinning facility at Morenci, and to restart its concentrator.

The concentrate-leach, direct-electrowinning facility is expected to be in operation by mid-2007, and copper production is projected to be approximately 150 million pounds per year .

Bagdad

Location: Northwestern Arizona Material: Copper Sulfide and Oxide Ore. Description of Operation:

an open-pit mine, a sulfide ore concentrator producing copper and molybdenum

concentrates a leaching system with an SX/EW operation producing copper cathode.

Ownership: 100% Undertaken an alternative technology that generates significantly less

sulfuric acid and requires less oxygen than the high-temperature process.

The benefit: Potential application in operations and projects where excess by-product

sulfuric acid cannot be beneficially used in stockpile or heap leaching operations

Lower-cost option for certain applications.

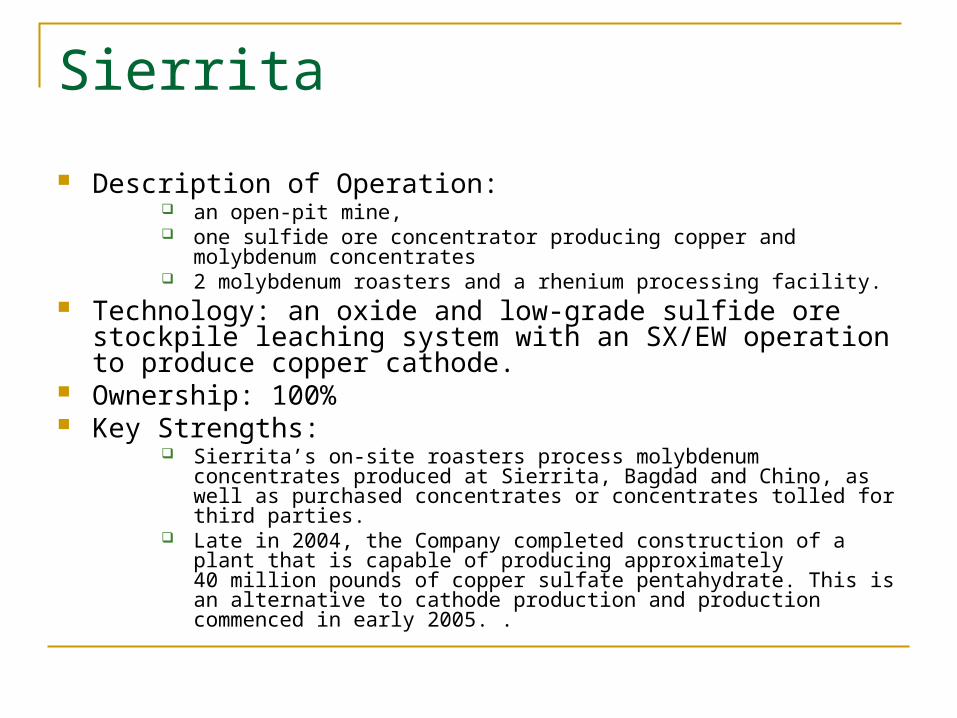

Sierrita

Description of Operation: an open-pit mine, one sulfide ore concentrator producing copper and molybdenum

concentrates 2 molybdenum roasters and a rhenium processing facility.

Technology: an oxide and low-grade sulfide ore stockpile leaching system with an SX/EW operation to produce copper cathode.

Ownership: 100% Key Strengths:

Sierrita’s on-site roasters process molybdenum concentrates produced at Sierrita, Bagdad and Chino, as well as purchased concentrates or concentrates tolled for third parties.

Late in 2004, the Company completed construction of a plant that is capable of producing approximately 40 million pounds of copper sulfate pentahydrate. This is an alternative to cathode production and production commenced in early 2005. .

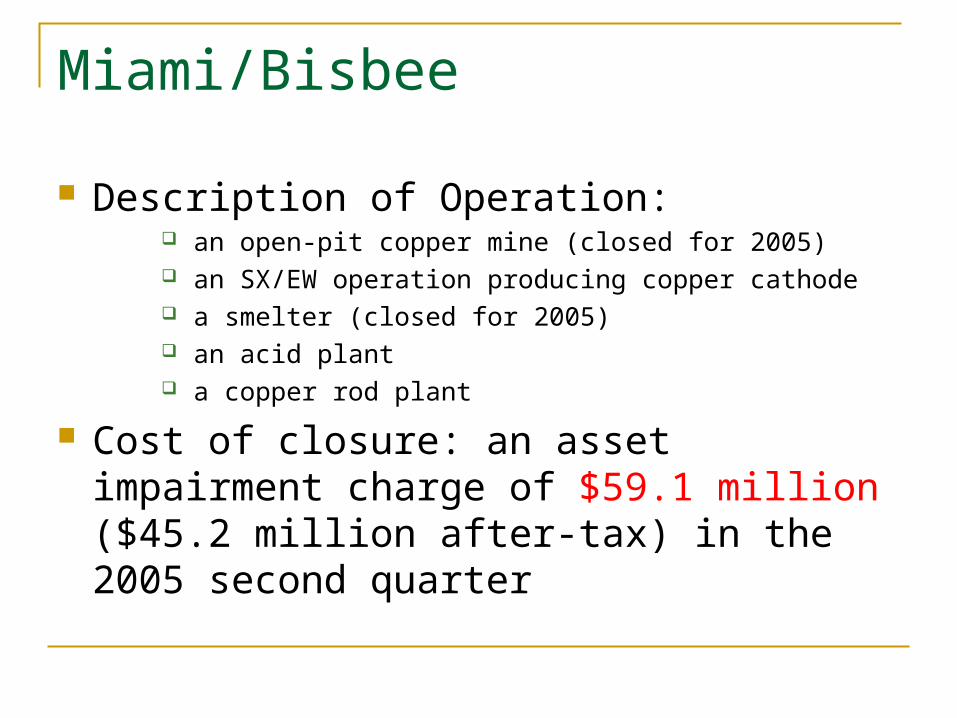

Miami/Bisbee

Description of Operation: an open-pit copper mine (closed for 2005) an SX/EW operation producing copper cathode a smelter (closed for 2005) an acid plant a copper rod plant

Cost of closure: an asset impairment charge of $59.1 million ($45.2 million after-tax) in the 2005 second quarter

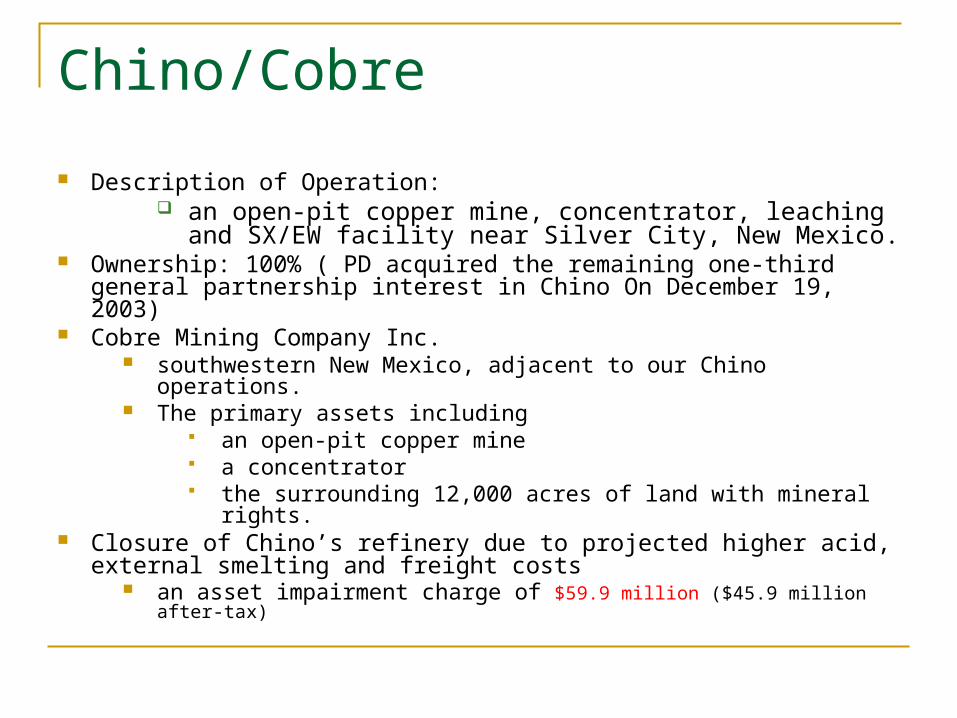

Chino/Cobre

Description of Operation: an open-pit copper mine, concentrator, leaching and

SX/EW facility near Silver City, New Mexico. Ownership: 100% ( PD acquired the remaining one-third general

partnership interest in Chino On December 19, 2003) Cobre Mining Company Inc.

southwestern New Mexico, adjacent to our Chino operations. The primary assets including

an open-pit copper mine a concentrator the surrounding 12,000 acres of land with mineral rights.

Closure of Chino’s refinery due to projected higher acid, external smelting and freight costs

an asset impairment charge of $59.9 million ($45.9 million after-tax)

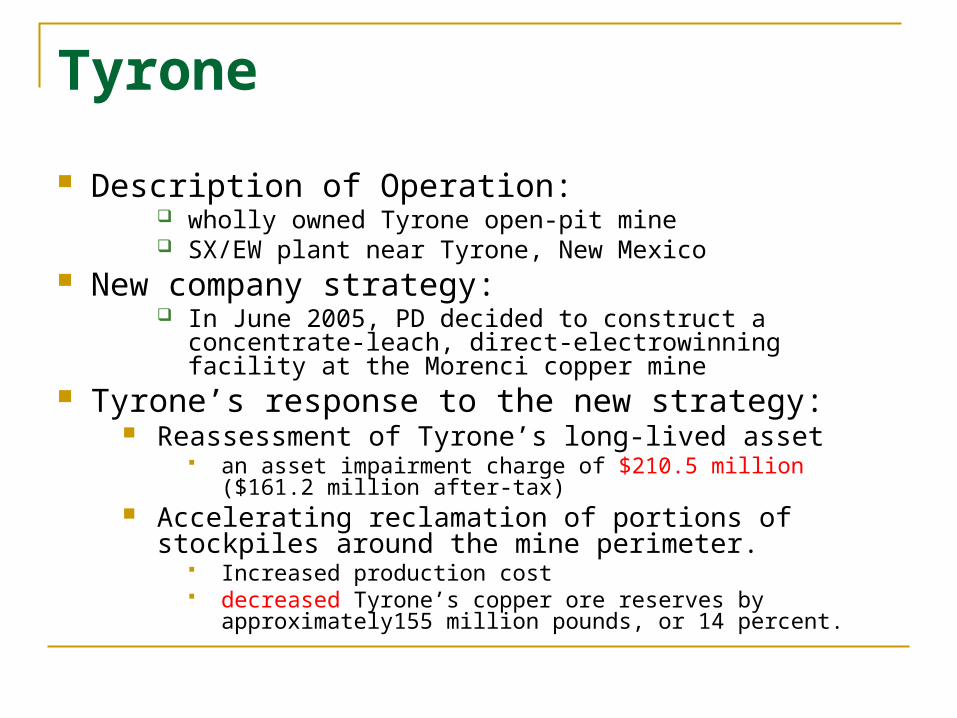

Tyrone

Description of Operation: wholly owned Tyrone open-pit mine SX/EW plant near Tyrone, New Mexico

New company strategy: In June 2005, PD decided to construct a concentrate-leach,

direct-electrowinning facility at the Morenci copper mine Tyrone’s response to the new strategy:

Reassessment of Tyrone’s long-lived asset an asset impairment charge of $210.5 million ($161.2 million

after-tax) Accelerating reclamation of portions of stockpiles around

the mine perimeter. Increased production cost decreased Tyrone’s copper ore reserves by

approximately155 million pounds, or 14 percent.

South American Mines

Candelaria/Ojos del Salado

Description of Operation: an open-pit and underground copper mines a concentrator, port and associated facilities

Ownership: 80 % partnership interest of a Chilean contractual mining

company in Candelaria Acquisition on Ojos del Salado by SMMA

On December 22, 2005, SMMA Candelaria, Inc. acquired a 20 percent equity interest in Ojos del Salado from PD Received cash of $24.8 million (net of $0.2 million of expenses) Phelps Dodge’s interest in Ojos del Salado was reduced to

80 percent from 100 percent.

El Abra

Description of Operation: Mine-for-leach, open-pit mining operation that uses three

stages of crushing prior to leaching an on/off heap leach pad an SX/EW operation to produce copper cathode

Ownership: 51 percent partnership interest in Sociedad Contractual

Minera El Abra (El Abra), a Chilean contractual mining company. The remaining 49 percent is owned by the state-owned copper enterprise Corporación Nacional del Cobre de Chile (CODELCO)

El Abra holds mining concessions over more than 33,000 acres of land near Calama in the copper-rich Second Region of northern Chile.

Cerro Verde

Location: approximately 30 kilometers southwest of Arequipa, Peru.

Description of Operation: two open-pit mines, Cerro Verde and Santa Rosa, a heap-leach operation an SX/EW operation.

Cerro Verde produces copper cathode. The ore is processed through three stages of crushing and placed on a leach pad after agglomeration.

New acquisitions led by other parties SMM Cerro Verde Netherlands B.V., acquired and increased its equity

position in Cerro Verde to 21% Compañía de Minas Buenaventura S.A. (Buenaventura), a publicly traded

Peruvian mining company, increased its ownership position in Cerro Verde to 18.2 percent.

PD’s equity position reduced from 82.5% to 53.6%

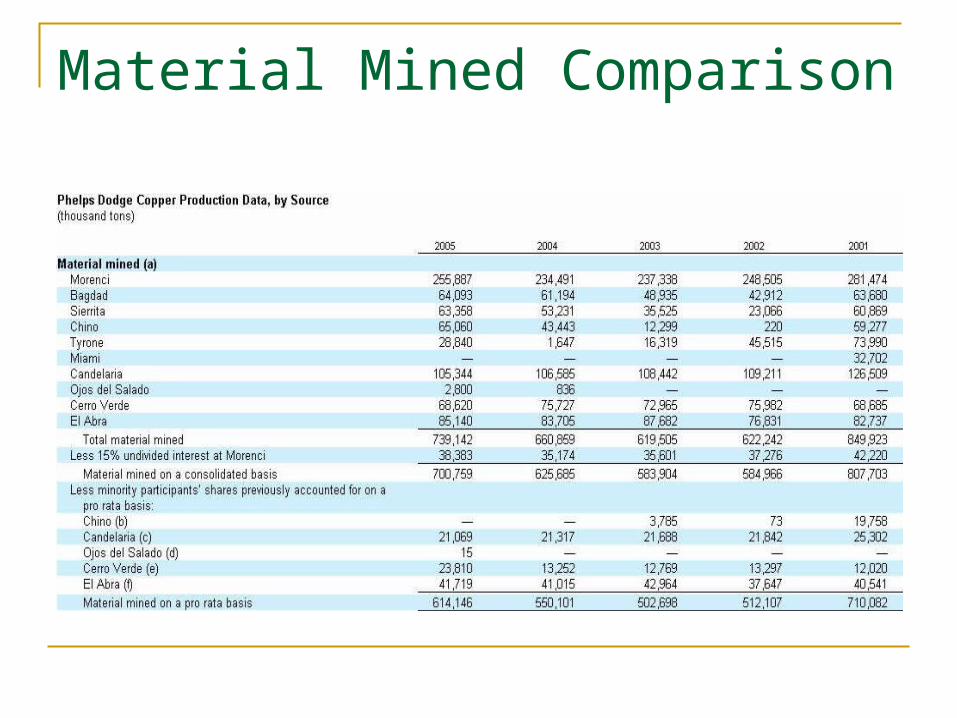

Material Mined Comparison

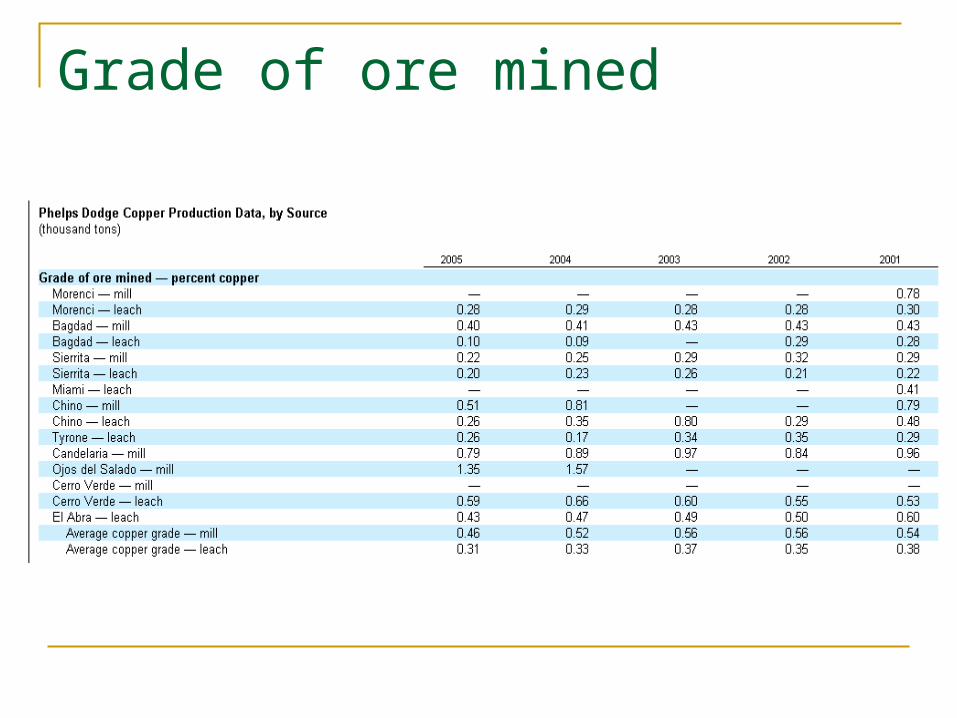

Grade of ore mined

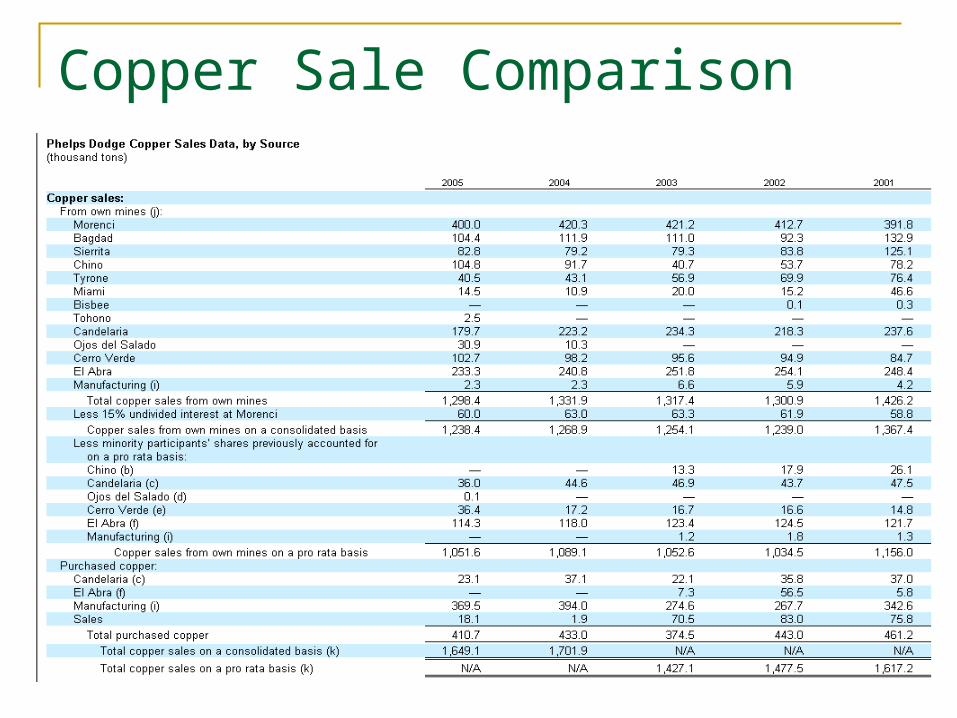

Copper Sale Comparison

Other Metal Sales

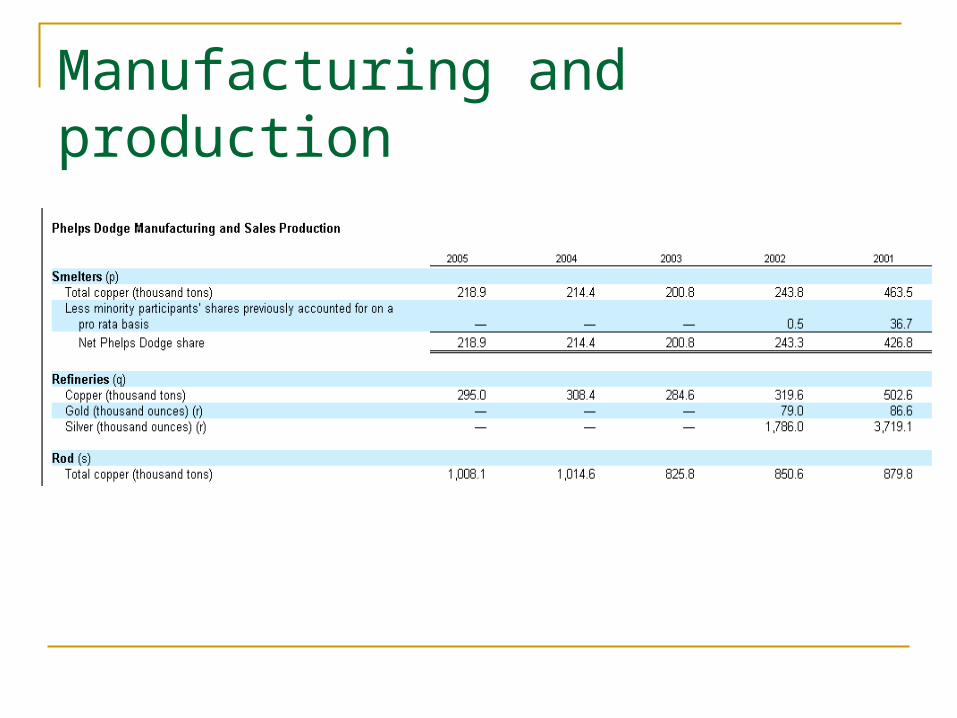

Manufacturing and production

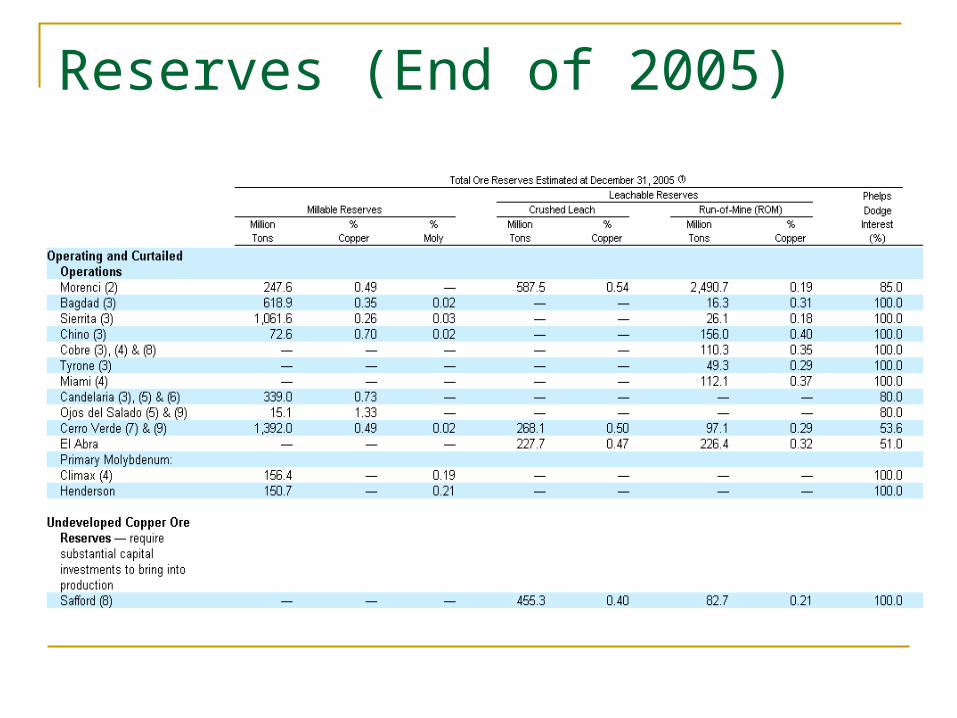

Reserves (End of 2005)

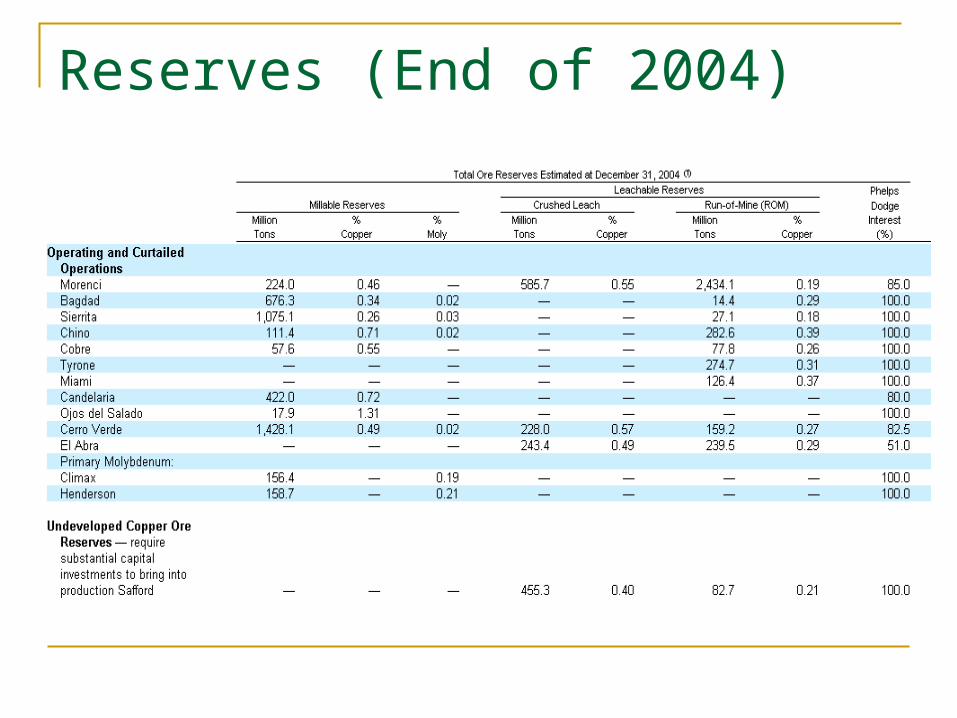

Reserves (End of 2004)

Consolidated Financial Statements

Income Statement Balance sheet statement Cash flow statement

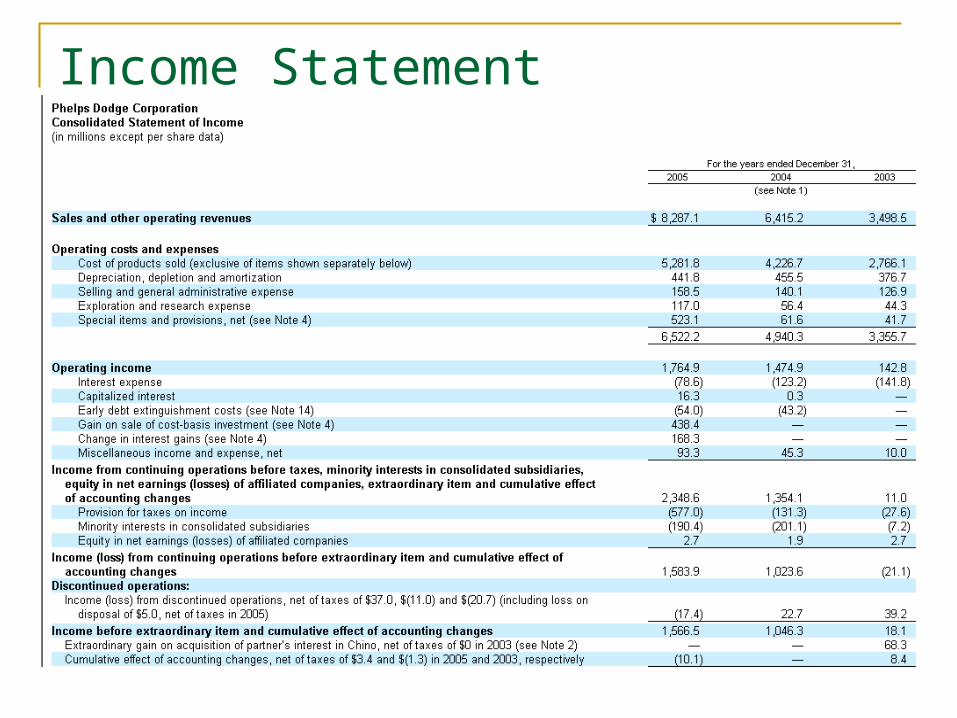

Income Statement

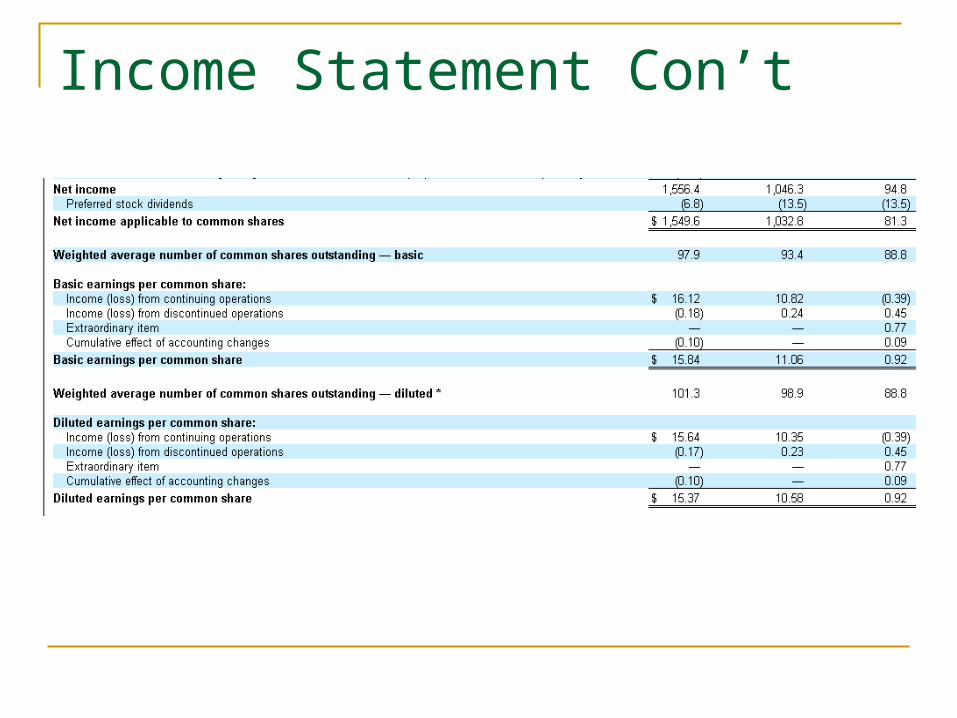

Income Statement Con’t

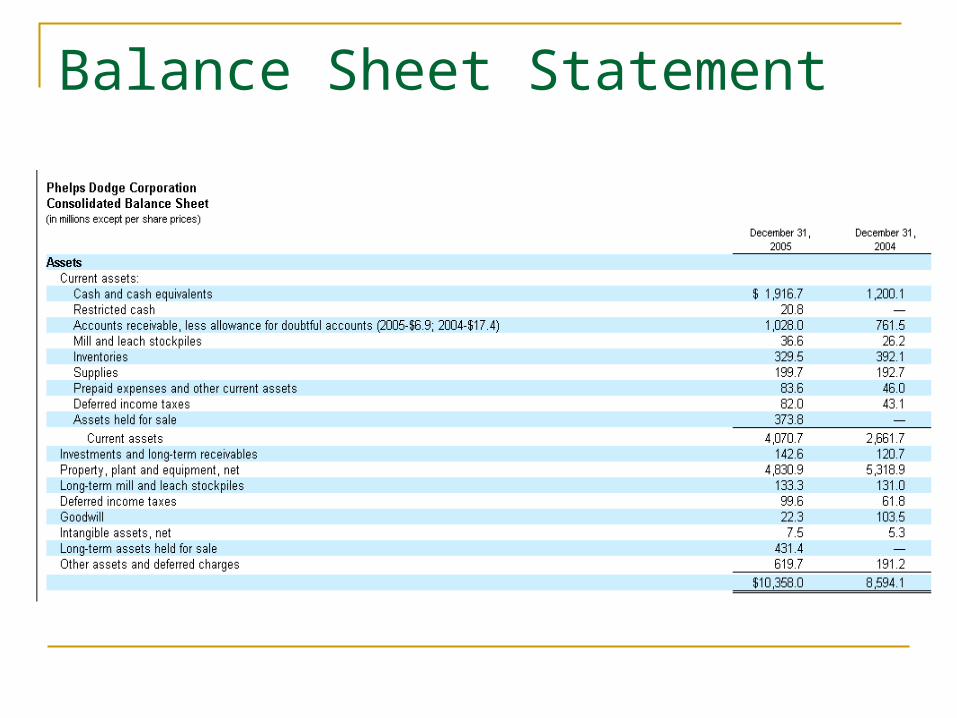

Balance Sheet Statement

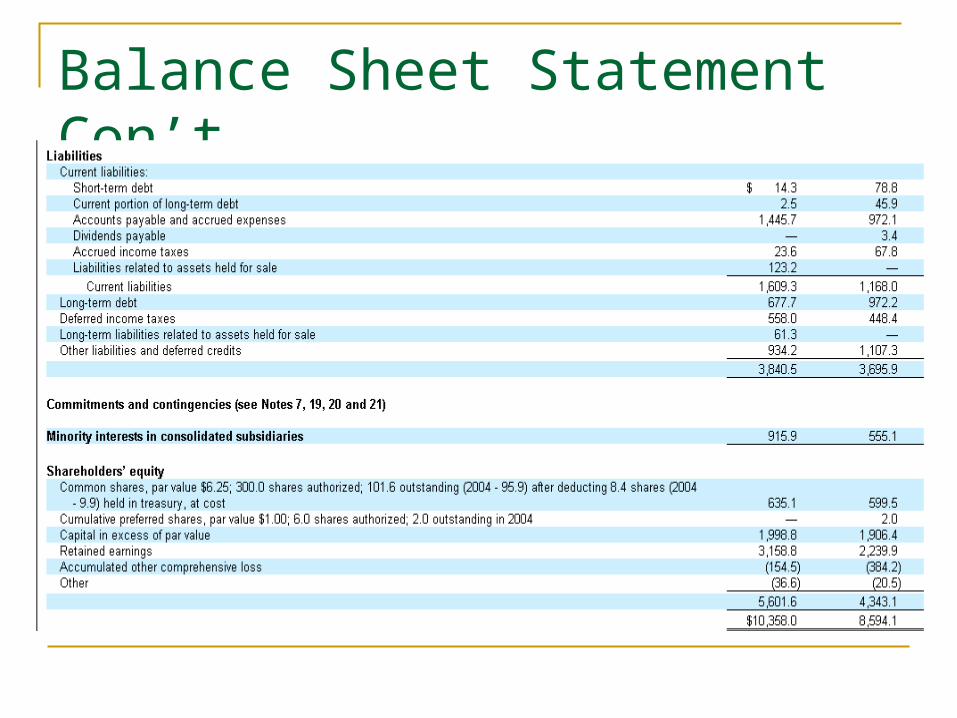

Balance Sheet Statement Con’t

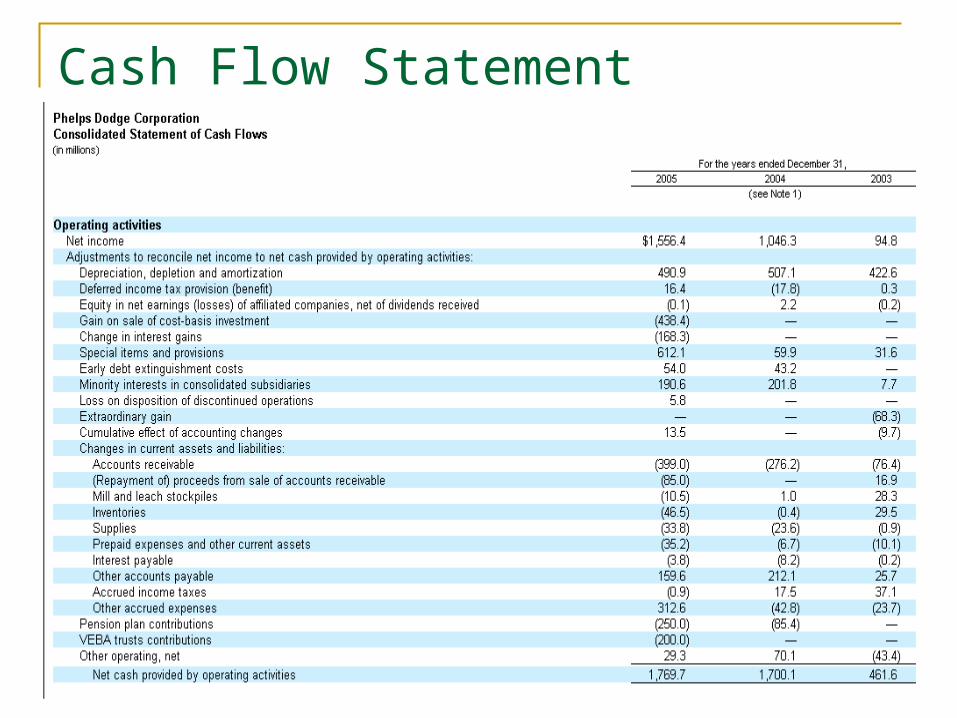

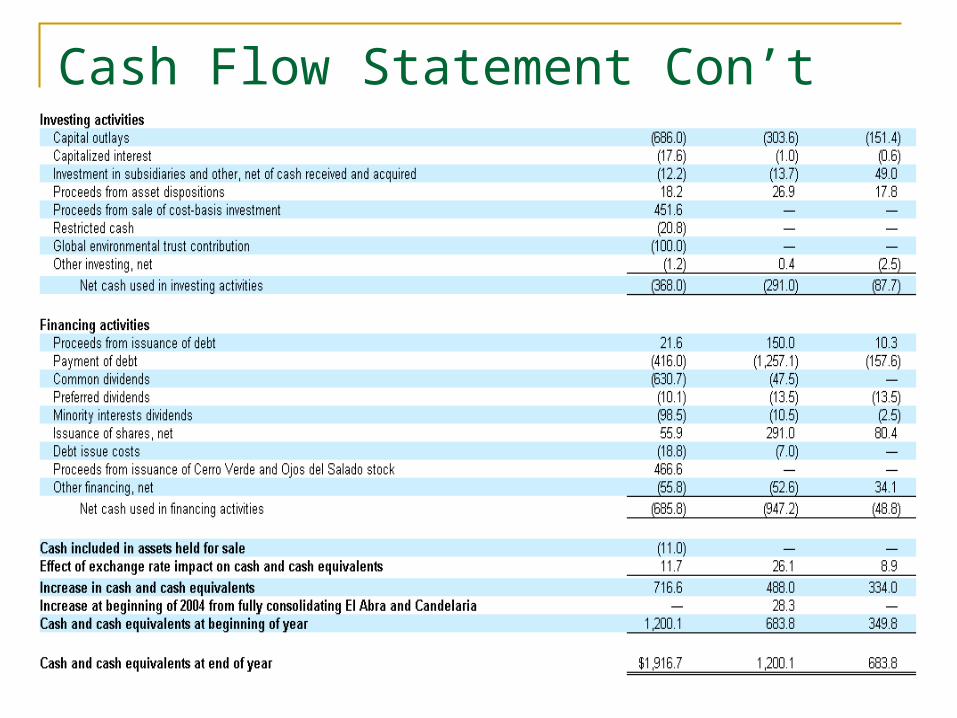

Cash Flow Statement

Cash Flow Statement Con’t

Evaluation Dimensions

Sale and Competition 2006’s Copper Price Cost Factor Level of recoverable reserves Financial Strength $ Profitability Net cash position

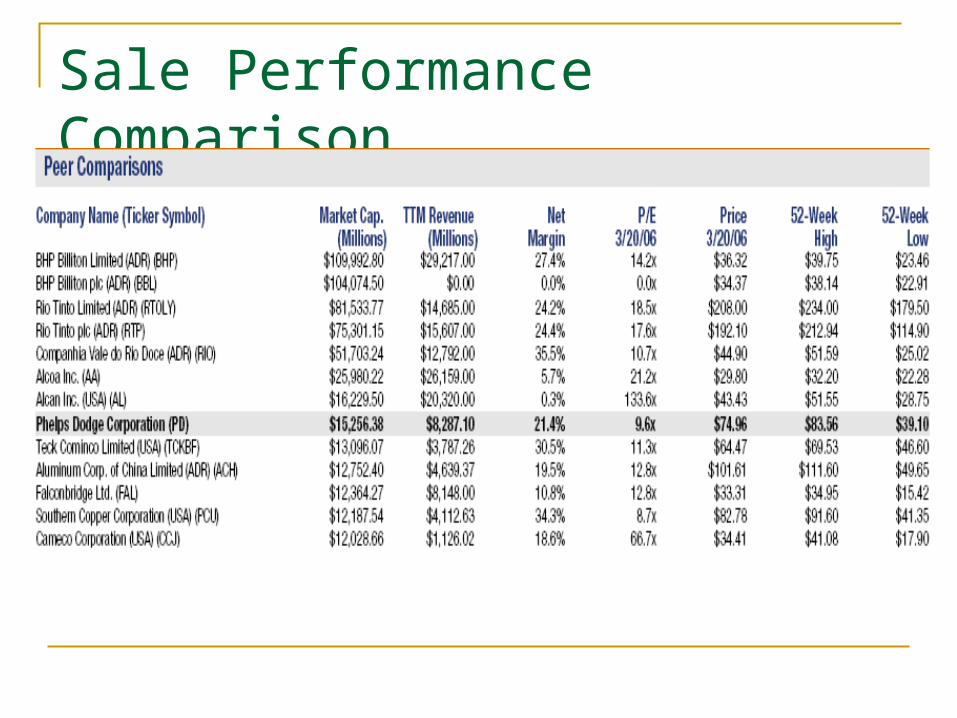

Sale Performance Comparison

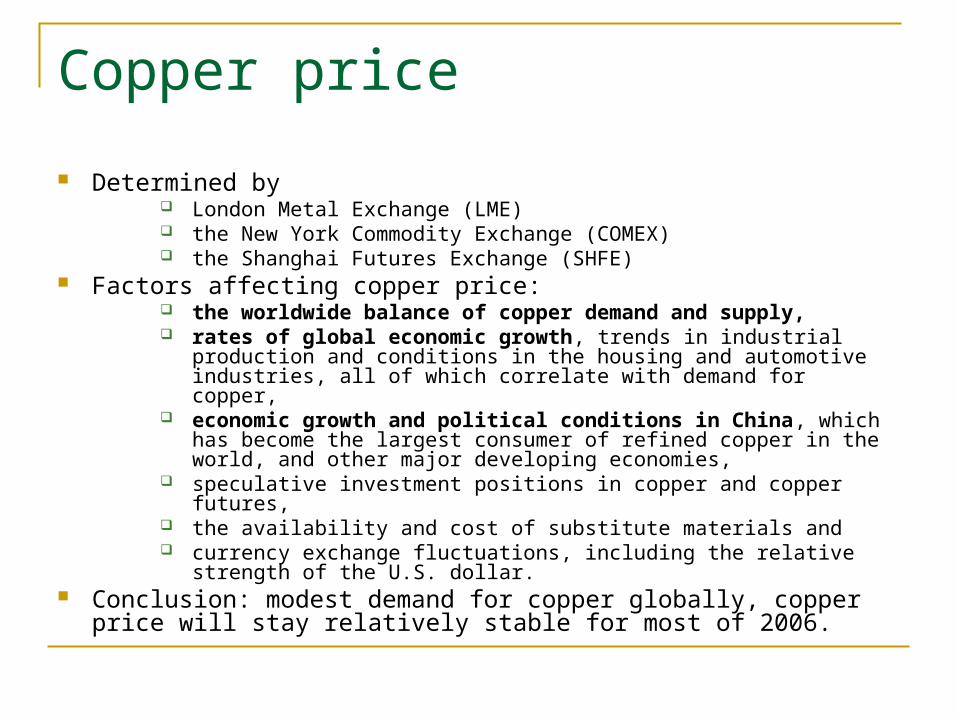

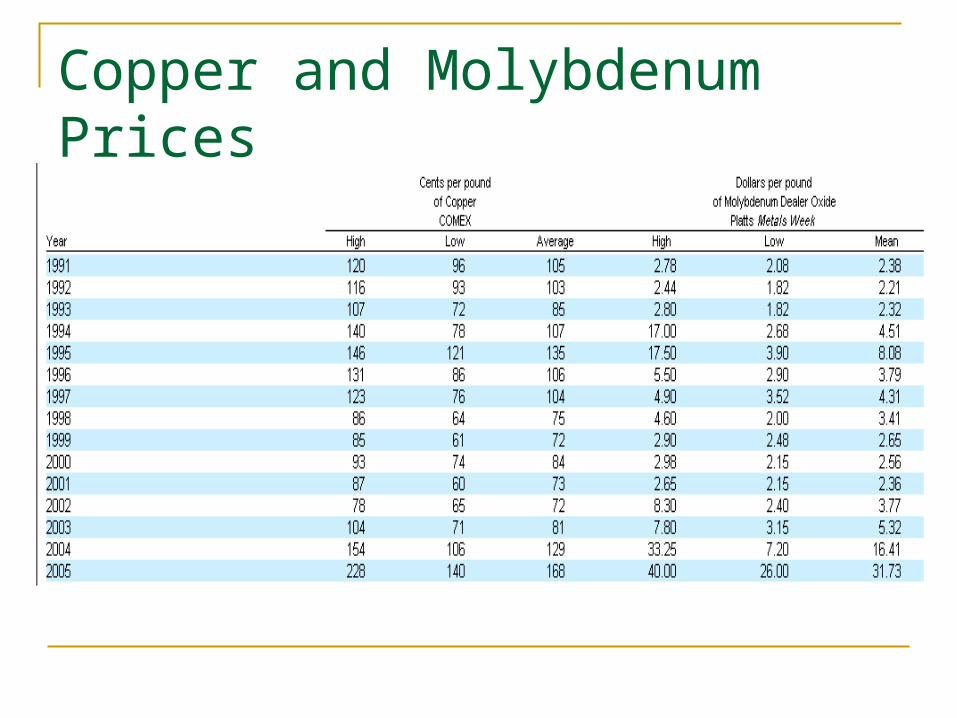

Copper price

Determined by London Metal Exchange (LME) the New York Commodity Exchange (COMEX) the Shanghai Futures Exchange (SHFE)

Factors affecting copper price: the worldwide balance of copper demand and supply, rates of global economic growth, trends in industrial production and

conditions in the housing and automotive industries, all of which correlate with demand for copper,

economic growth and political conditions in China, which has become the largest consumer of refined copper in the world, and other major developing economies,

speculative investment positions in copper and copper futures, the availability and cost of substitute materials and currency exchange fluctuations, including the relative strength of the U.S.

dollar. Conclusion: modest demand for copper globally, copper price will stay

relatively stable for most of 2006.

Copper and Molybdenum Prices

Production Cost

High energy cost: diesel fuel, natural gas, electricity, and purchased petroleum.

High copper production cost Mine closure also incurred large loss

Recoverable reserves

Levels of Ore Reserves and Mill and Leach Stockpiles Are Subject to Uncertainty and PD’s Ability to Replenish Ore Reserves Is Important for Long-Term Viability

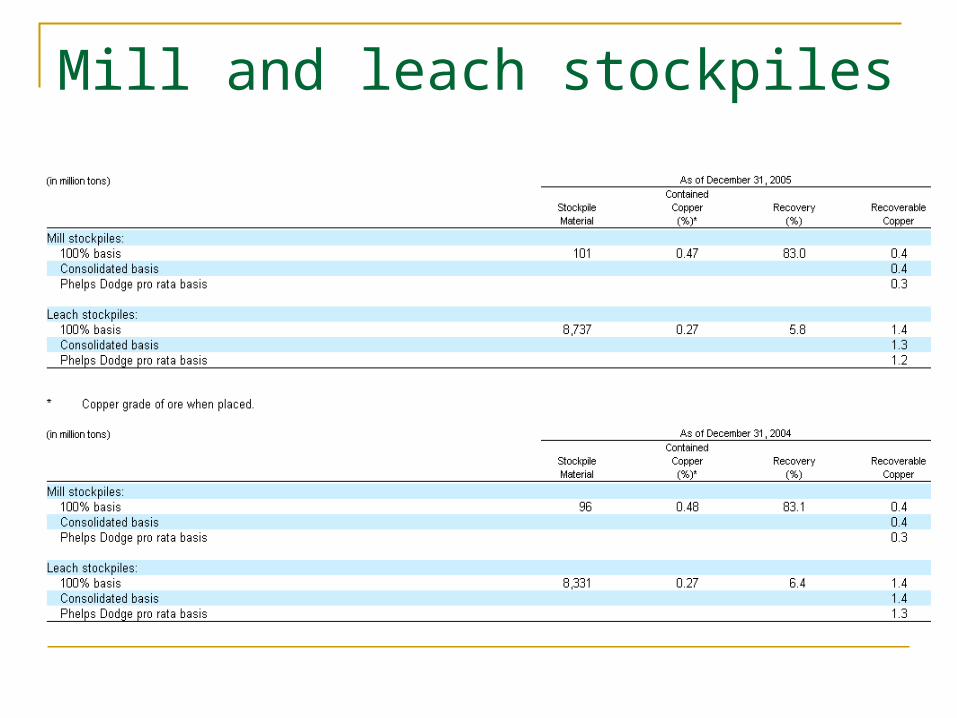

Mill and leach stockpiles

Mill Stockpiles & Leach stockpiles Mill stockpiles contain low-grade ore that has been

extracted from the mine and is available for processing to recover the contained copper by milling, concentrating, smelting and refining, or alternatively, by concentrate leaching.

Leach stockpiles contain low-grade ore that has been extracted from the mine and is available for processing to recover the contained copper through a leaching process. Leach stockpiles are exposed to acidic solutions that dissolve contained copper and deliver the copper in solution to the extraction processing facilities.

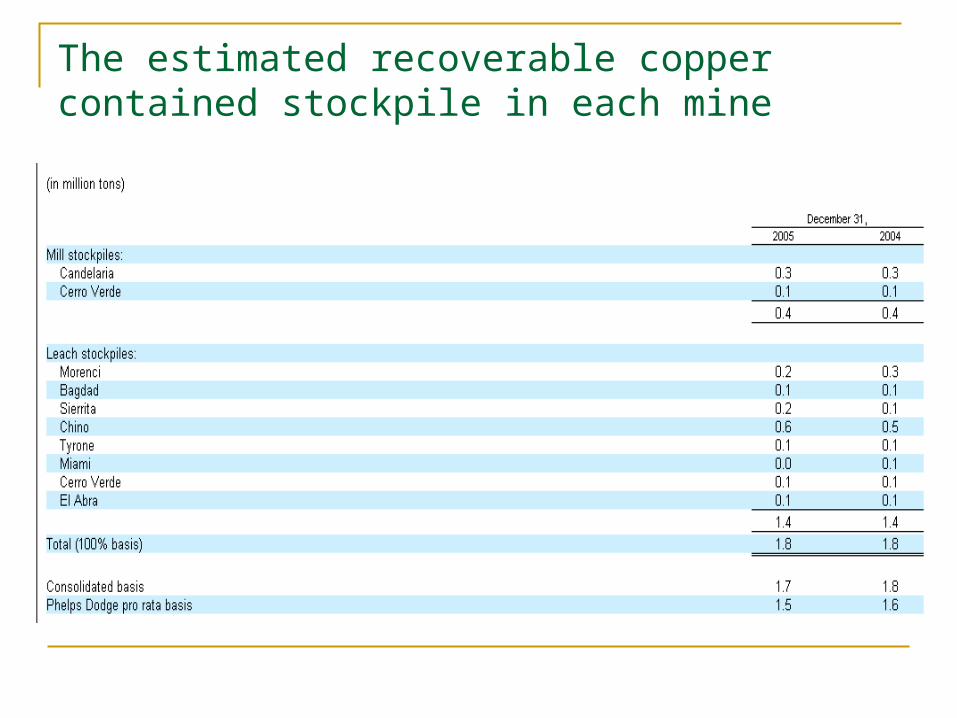

The estimated recoverable copper contained stockpile in each mine

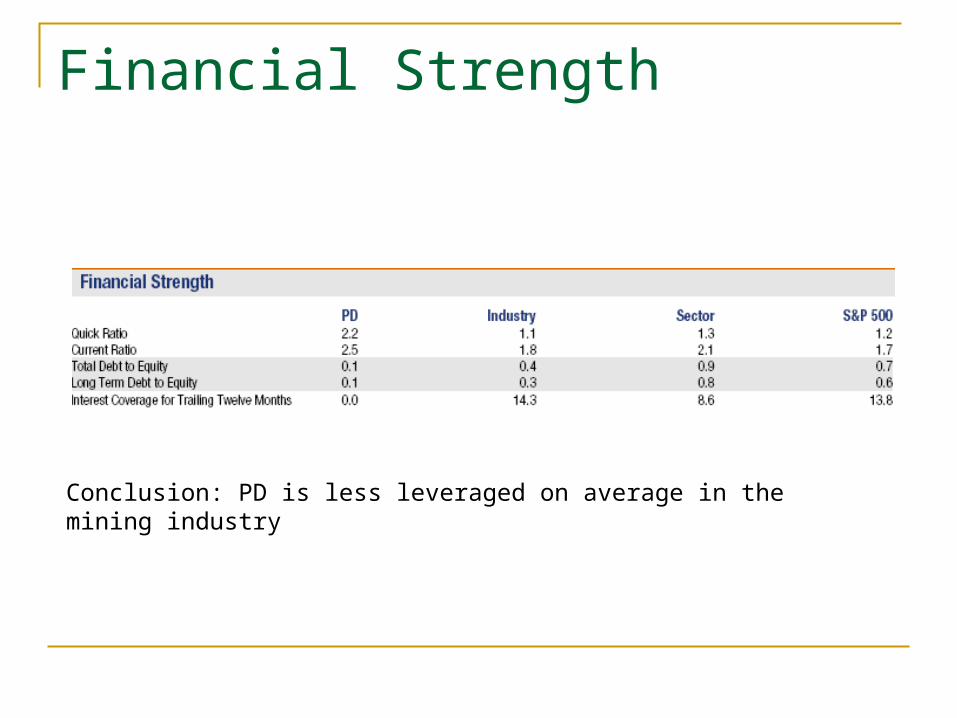

Financial Strength

Conclusion: PD is less leveraged on average in the mining industry

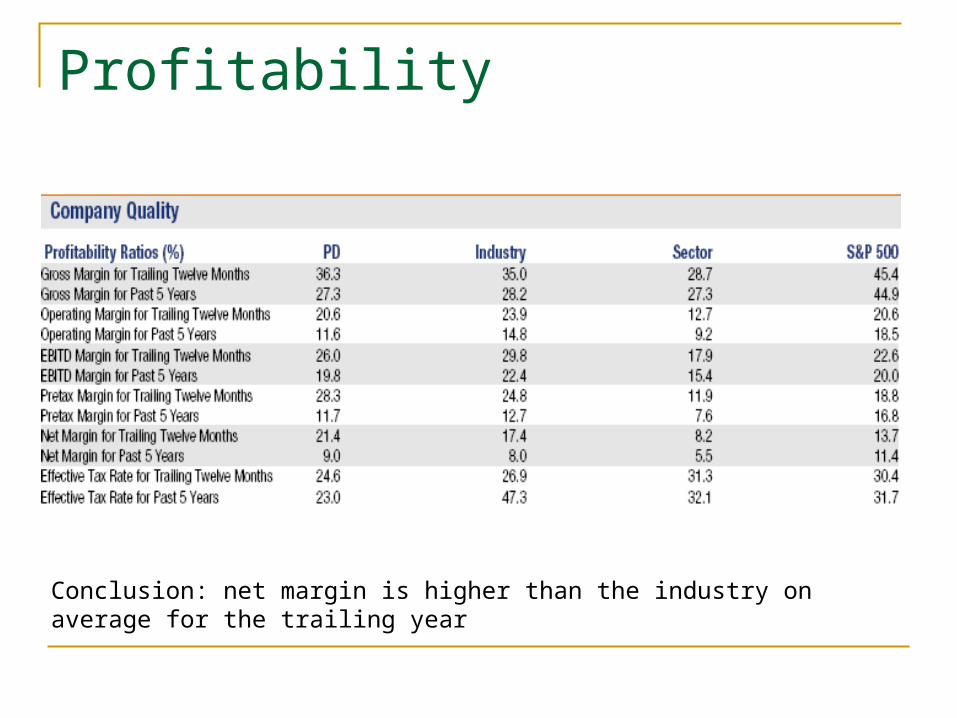

Profitability

Conclusion: net margin is higher than the industry on average for the trailing year

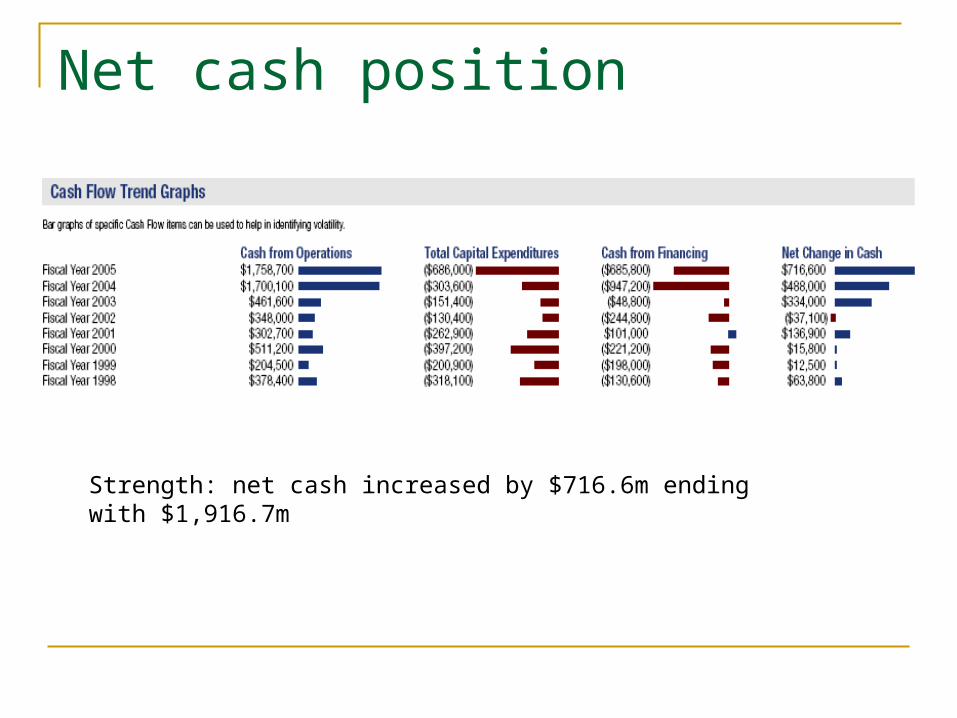

Net cash position

Strength: net cash increased by $716.6m ending with $1,916.7m

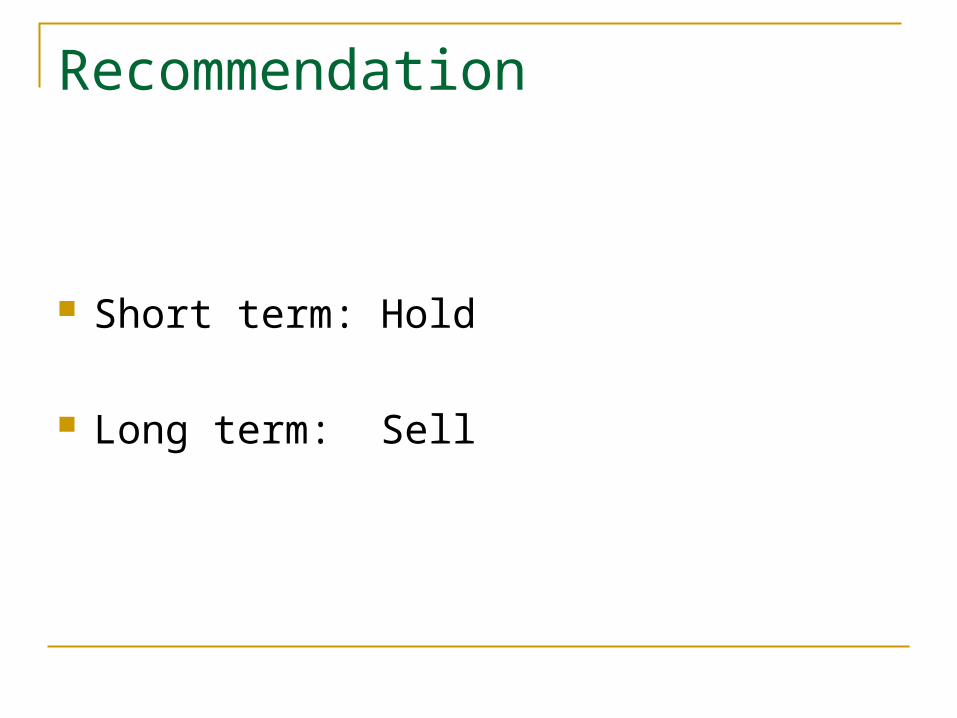

Recommendation

Short term: Hold

Long term: Sell

Section AgendaSection Agenda

Corporate ProfileCorporate Profile Stock PerformanceStock Performance Management Management Recent HistoryRecent History Competitive StrategyCompetitive Strategy Uranium OverviewUranium Overview Industry Competitors/ PositioningIndustry Competitors/ Positioning

Section AgendaSection Agenda

Core Business Properties: Uranium Core Business Properties: Uranium productionproduction

Diversified operationsDiversified operations Reserves and ResourcesReserves and Resources Segmented performance/ CAPEXSegmented performance/ CAPEX Financial statementsFinancial statements Evaluation MetricsEvaluation Metrics Recommendations/ConclusionsRecommendations/Conclusions

Corporate ProfileCorporate Profile Created Created 19881988 by the merger of two Crown by the merger of two Crown

corporations—Saskatchewan Mining Development corporations—Saskatchewan Mining Development Corporation and Eldorado Nuclear Limited. Corporation and Eldorado Nuclear Limited.

Worlds largest low cost uranium production Worlds largest low cost uranium production companycompany

Core businesses: Core businesses: Uranium production 20% of world supplyUranium production 20% of world supply Conversion services Conversion services Nuclear electricity generation, Nuclear electricity generation, Gold miningGold mining

Market Capitalization: $7.316 Billion (CAD)Market Capitalization: $7.316 Billion (CAD) Listings: Listings:

• Common Stock TSX (CCO), NYSE(CCJ)Common Stock TSX (CCO), NYSE(CCJ)• Convertible Debentures (Toronto) CCO.DBConvertible Debentures (Toronto) CCO.DB

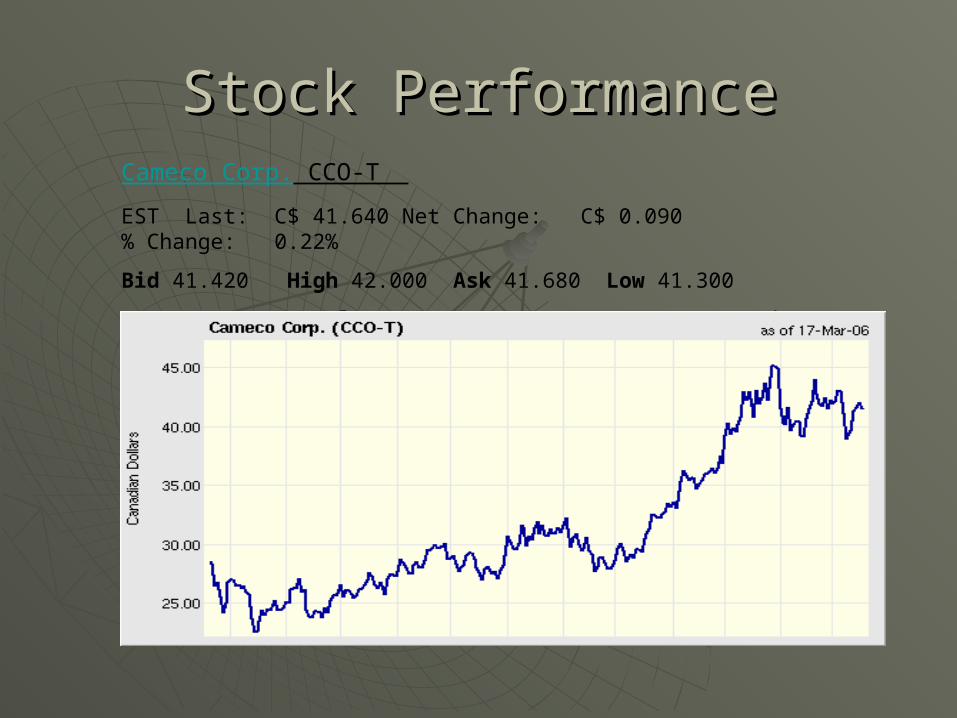

Stock PerformanceStock PerformanceCameco Corp. CCO-T

EST Last: C$ 41.640 Net Change: C$ 0.090 % Change: 0.22%

Bid 41.420 High 42.000 Ask 41.680 Low 41.300

EPS 1.26 Volume 1,272,811 P/E 33.00 52-Week High 46.820

Indicated Annual Div. 0.16 52-Week Low 22.325 Yield 0.39

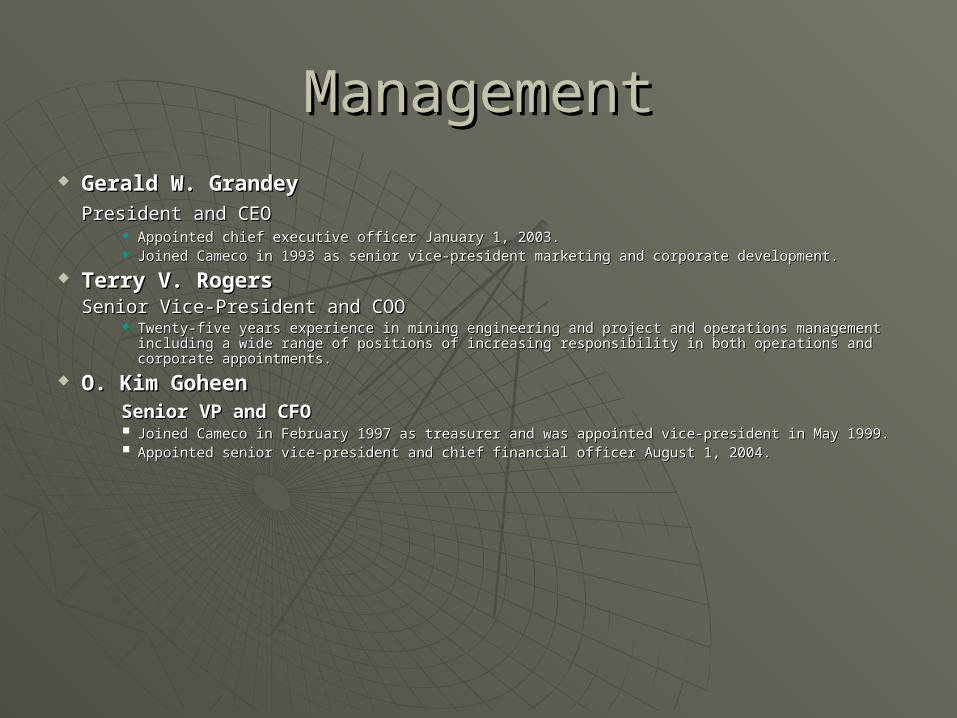

ManagementManagement Gerald W. GrandeyGerald W. Grandey

President and CEOPresident and CEO Appointed chief executive officer January 1, 2003. Appointed chief executive officer January 1, 2003. Joined Cameco in 1993 as senior vice-president marketing and corporate development.Joined Cameco in 1993 as senior vice-president marketing and corporate development.

Terry V. RogersTerry V. RogersSenior Vice-President and COOSenior Vice-President and COO

Twenty-five years experience in mining engineering and project and operations management Twenty-five years experience in mining engineering and project and operations management including a wide range of positions of increasing responsibility in both operations and corporate including a wide range of positions of increasing responsibility in both operations and corporate appointments. appointments.

O. Kim Goheen O. Kim Goheen Senior VP and CFOSenior VP and CFO

Joined Cameco in February 1997 as treasurer and was appointed vice-president in May 1999.Joined Cameco in February 1997 as treasurer and was appointed vice-president in May 1999. Appointed senior vice-president and chief financial officer August 1, 2004.Appointed senior vice-president and chief financial officer August 1, 2004.

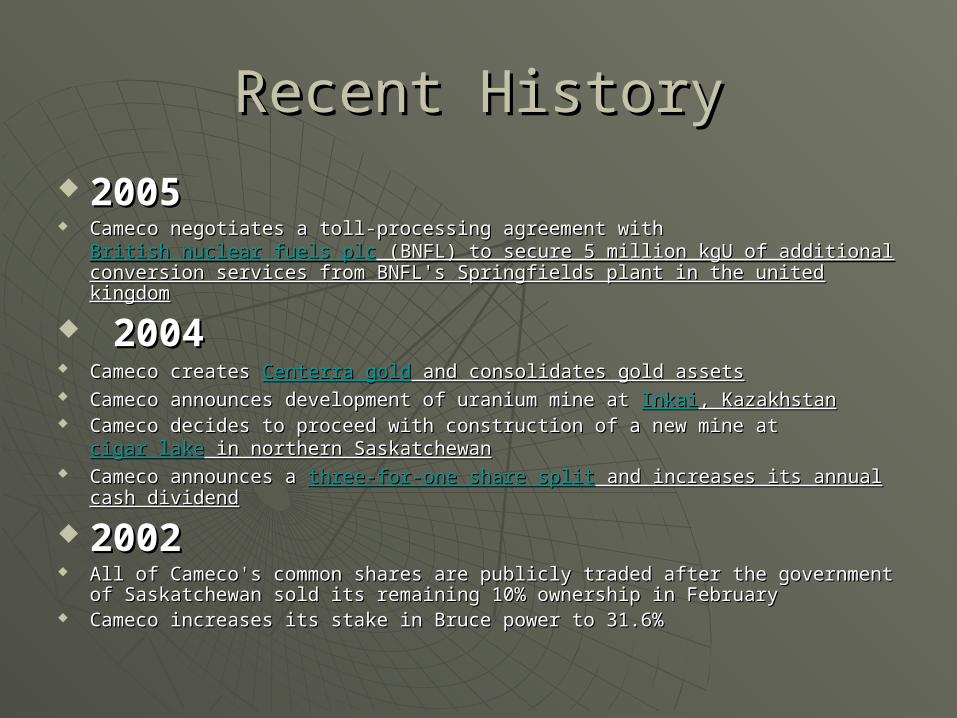

Recent HistoryRecent History

20052005 Cameco negotiates a toll-processing agreement with Cameco negotiates a toll-processing agreement with

British nuclear fuels plcBritish nuclear fuels plc (BNFL) to secure 5 million kgU of additional (BNFL) to secure 5 million kgU of additional conversion services from BNFL's Springfields plant in the united kingdomconversion services from BNFL's Springfields plant in the united kingdom

20042004 Cameco creates Cameco creates Centerra goldCenterra gold and consolidates gold assets and consolidates gold assets Cameco announces development of uranium mine at Cameco announces development of uranium mine at InkaiInkai, Kazakhstan, Kazakhstan Cameco decides to proceed with construction of a new mine at Cameco decides to proceed with construction of a new mine at cigar lakecigar lake in in

northern Saskatchewannorthern Saskatchewan Cameco announces a Cameco announces a three-for-one share splitthree-for-one share split and increases its annual and increases its annual

cash dividendcash dividend

20022002 All of Cameco's common shares are publicly traded after the government All of Cameco's common shares are publicly traded after the government

of Saskatchewan sold its remaining 10% ownership in Februaryof Saskatchewan sold its remaining 10% ownership in February Cameco increases its stake in Bruce power to 31.6%Cameco increases its stake in Bruce power to 31.6%

Competitive StrategyCompetitive Strategy

““..Simply stated it is our objective to be ..Simply stated it is our objective to be involved in involved in every stage of the every stage of the nuclear fuel cyclenuclear fuel cycle…from exploring …from exploring for, and extracting the raw uranium for, and extracting the raw uranium ore…to conversion to a purer product…ore…to conversion to a purer product…to further upgrading enrichment…to to further upgrading enrichment…to manufacturing fuel rods…and, finally, manufacturing fuel rods…and, finally, to the generation of nuclear electricity.” to the generation of nuclear electricity.” Jerry Grandey President & CEO Jerry Grandey President & CEO

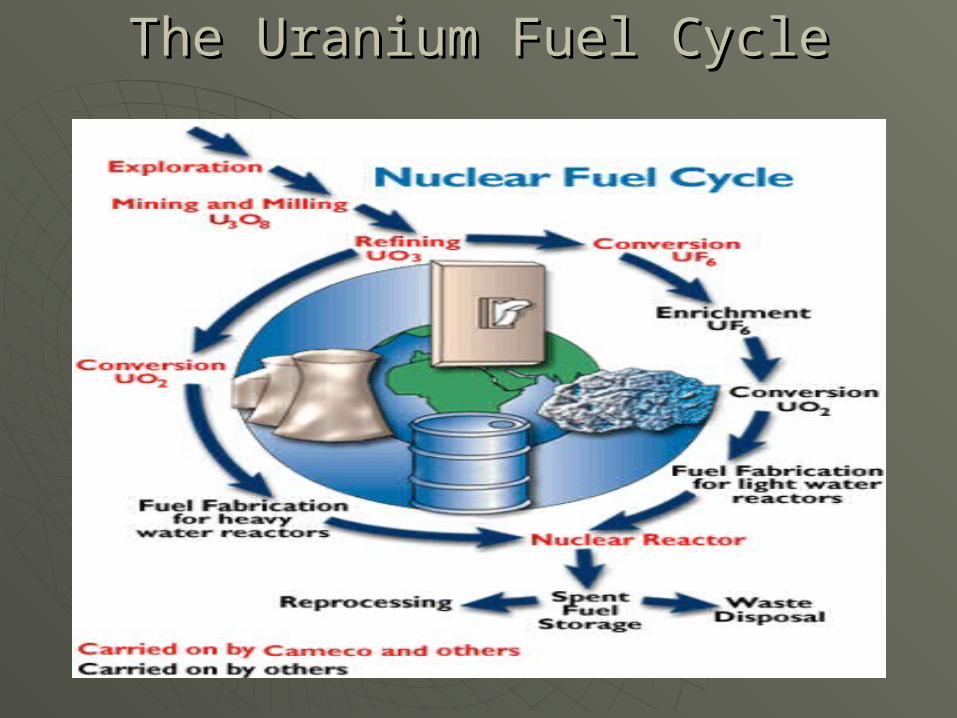

The Uranium Fuel CycleThe Uranium Fuel Cycle

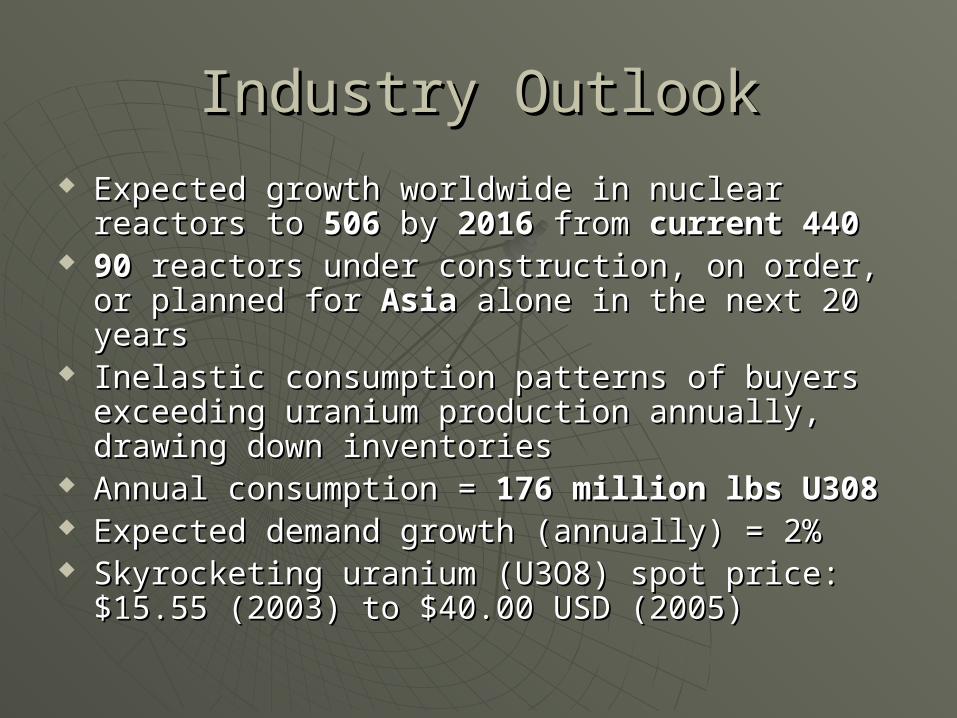

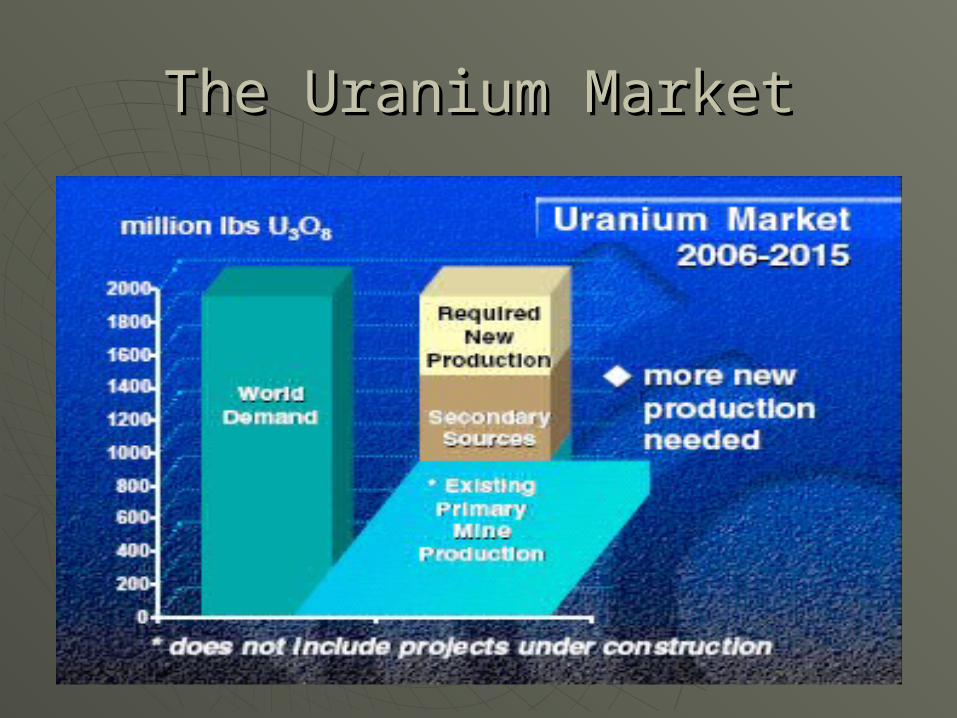

Industry OutlookIndustry Outlook Expected growth worldwide in nuclear reactors to Expected growth worldwide in nuclear reactors to

506 506 by by 2016 2016 from from current 440current 440 9090 reactors under construction, on order, or reactors under construction, on order, or

planned for planned for AsiaAsia alone in the next 20 years alone in the next 20 years Inelastic consumption patterns of buyers Inelastic consumption patterns of buyers

exceeding uranium production annually, drawing exceeding uranium production annually, drawing down inventoriesdown inventories

Annual consumption = Annual consumption = 176 million lbs U308176 million lbs U308 Expected demand growth (annually) = 2%Expected demand growth (annually) = 2% Skyrocketing uranium (U3O8) spot price: $15.55 Skyrocketing uranium (U3O8) spot price: $15.55

(2003) to $40.00 USD (2005)(2003) to $40.00 USD (2005)

The Uranium MarketThe Uranium Market

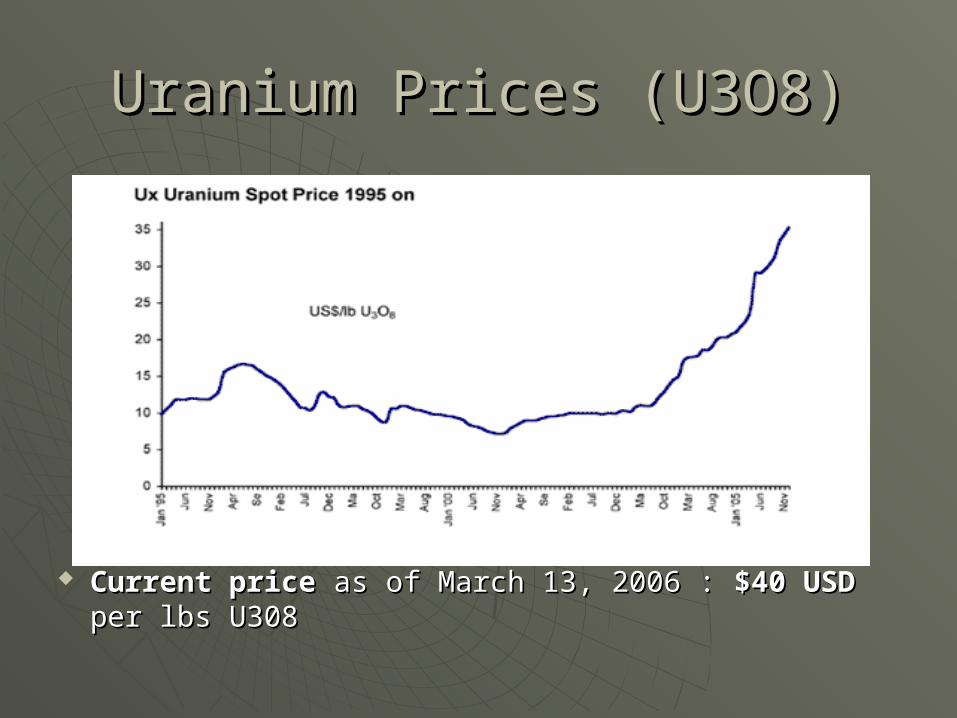

Uranium Prices (U3O8)Uranium Prices (U3O8)

Current priceCurrent price as of March 13, 2006 : as of March 13, 2006 : $40 USD$40 USD per per lbs U308lbs U308

Industry CompetitorsIndustry Competitors2004 World Production 2004 World Production

Producer Producer Million pounds UMillion pounds U33OO88

CamecoCameco 2121

CogemaCogema 1111

Energy Resources of Energy Resources of Australia Ltd.Australia Ltd.

1010

WMC Resources Ltd.WMC Resources Ltd. 99

Priargunsky Industrial Mining Priargunsky Industrial Mining and Chemical Enterprise and Chemical Enterprise (Russia)(Russia)

88

Rossing Uranium LimitedRossing Uranium Limited 55

NAVOI Mining Metallurgical NAVOI Mining Metallurgical Kombinat (Uzbekistan)Kombinat (Uzbekistan)

55

OthersOthers 2121

TOTALTOTAL 104104

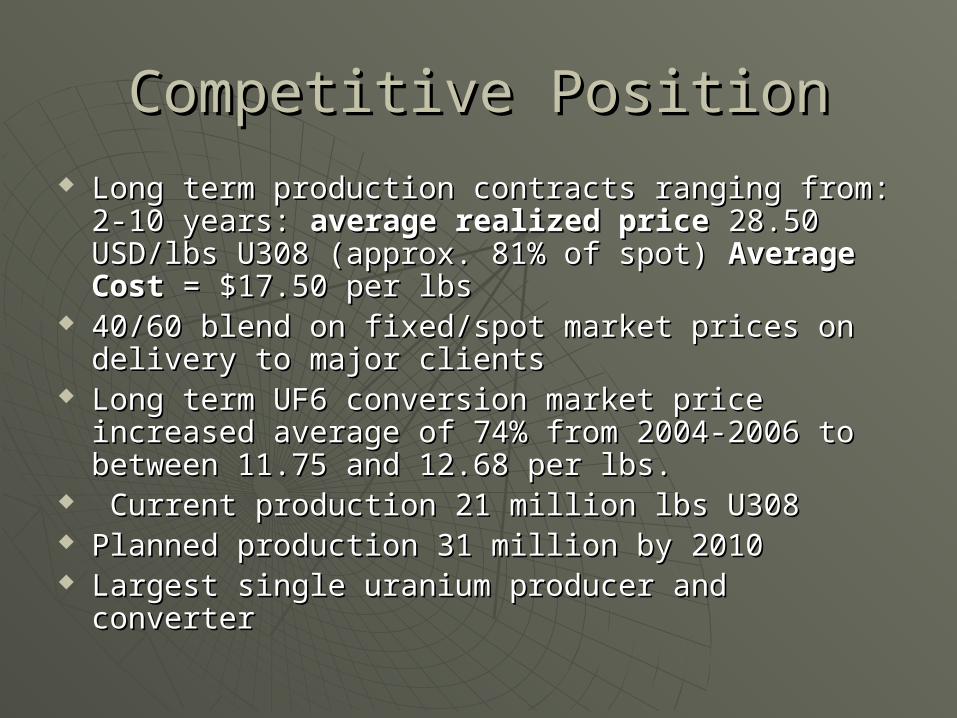

Competitive PositionCompetitive Position Long term production contracts ranging from: 2-Long term production contracts ranging from: 2-

10 years: 10 years: average realized priceaverage realized price 28.50 USD/lbs 28.50 USD/lbs U308 (approx. 81% of spot) U308 (approx. 81% of spot) Average CostAverage Cost = = $17.50 per lbs$17.50 per lbs

40/60 blend on fixed/spot market prices on 40/60 blend on fixed/spot market prices on delivery to major clientsdelivery to major clients

Long term UF6 conversion market price increased Long term UF6 conversion market price increased average of 74% from 2004-2006 to between average of 74% from 2004-2006 to between 11.75 and 12.68 per lbs.11.75 and 12.68 per lbs.

Current production 21 million lbs U308Current production 21 million lbs U308 Planned production 31 million by 2010Planned production 31 million by 2010 Largest single uranium producer and converterLargest single uranium producer and converter

Core Business: Uranium ProductionCore Business: Uranium Production

Uranium PropertiesUranium Properties• MacArthur RiverMacArthur River• Cigar LakeCigar Lake• Key LakeKey Lake• Rabbit LakeRabbit Lake• Crowe ButteCrowe Butte• Smith Ranch HighlandSmith Ranch Highland• InkaiInkai

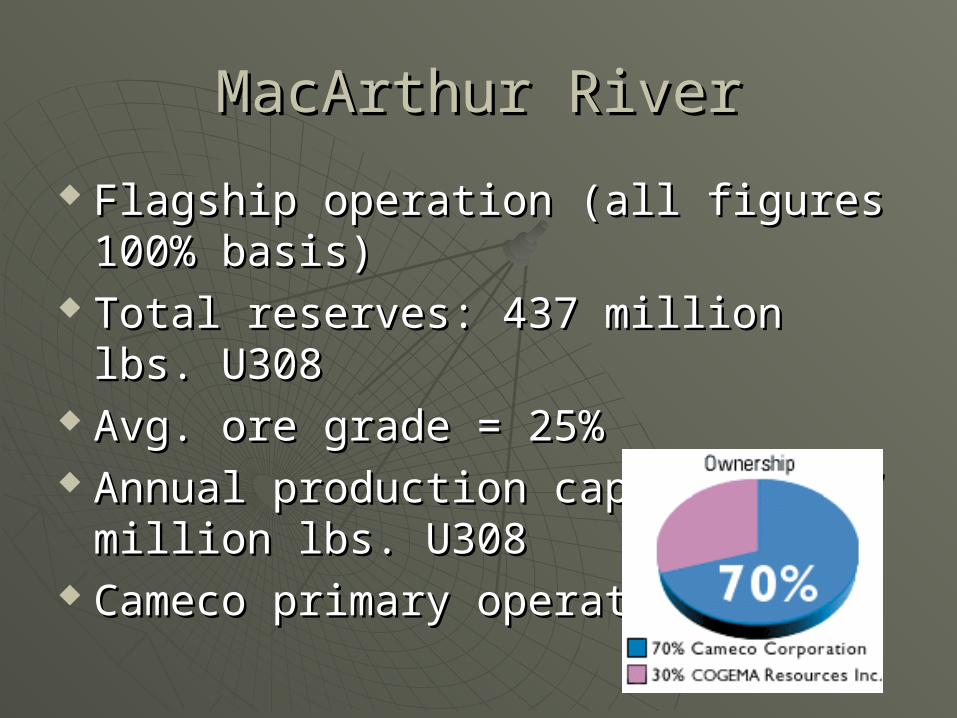

MacArthur RiverMacArthur River

Flagship operation (all figures 100% Flagship operation (all figures 100% basis)basis)

Total reserves: 437 million lbs. U308Total reserves: 437 million lbs. U308 Avg. ore grade = 25%Avg. ore grade = 25% Annual production capacity 18.7 Annual production capacity 18.7

million lbs. U308million lbs. U308 Cameco primary operator Cameco primary operator

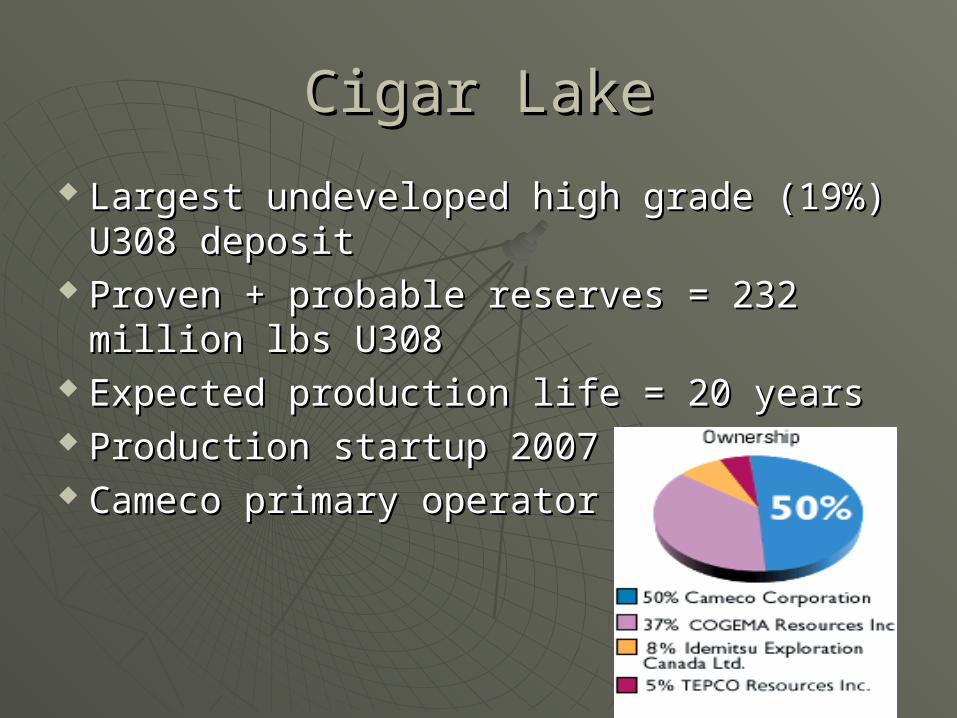

Cigar LakeCigar Lake

Largest undeveloped high grade (19%) Largest undeveloped high grade (19%) U308 depositU308 deposit

Proven + probable reserves = 232 million Proven + probable reserves = 232 million lbs U308lbs U308

Expected production life = 20 yearsExpected production life = 20 years Production startup 2007Production startup 2007 Cameco primary operatorCameco primary operator

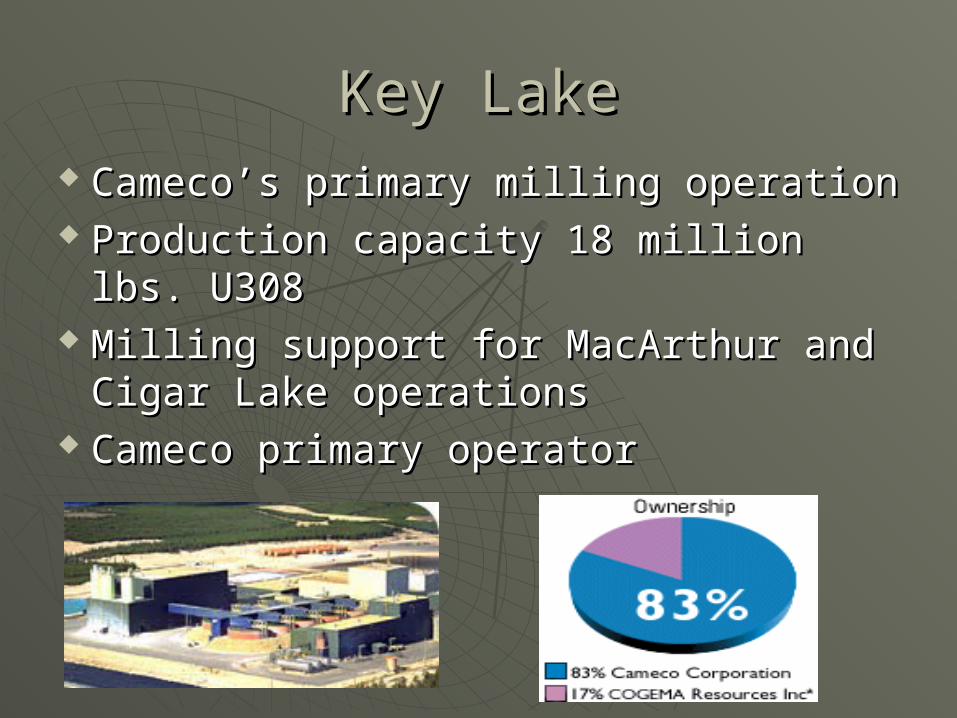

Key LakeKey Lake Cameco’s primary milling operationCameco’s primary milling operation Production capacity 18 million lbs. Production capacity 18 million lbs.

U308U308 Milling support for MacArthur and Milling support for MacArthur and

Cigar Lake operationsCigar Lake operations Cameco primary operatorCameco primary operator

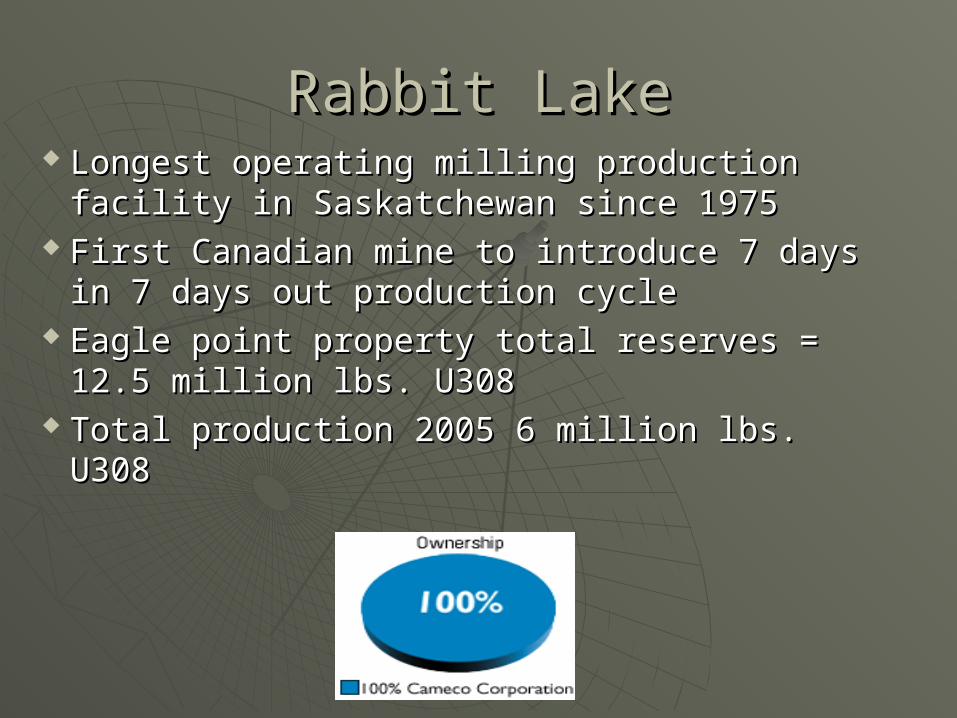

Rabbit LakeRabbit Lake Longest operating milling production Longest operating milling production

facility in Saskatchewan since 1975facility in Saskatchewan since 1975 First Canadian mine to introduce 7 days in First Canadian mine to introduce 7 days in

7 days out production cycle7 days out production cycle Eagle point property total reserves = 12.5 Eagle point property total reserves = 12.5

million lbs. U308million lbs. U308 Total production 2005 6 million lbs. U308Total production 2005 6 million lbs. U308

Crowe Butte/ Smith Highland Crowe Butte/ Smith Highland RanchRanch

United States uranium operations: United States uranium operations: total annual production = 3.1 million total annual production = 3.1 million lbs. U308lbs. U308

Total reserves proven + probable = Total reserves proven + probable = 24.9 million lbs. U30824.9 million lbs. U308

Both properties use (ISL) In situ leach Both properties use (ISL) In situ leach for extractionfor extraction

Cameco 100% operatorCameco 100% operator

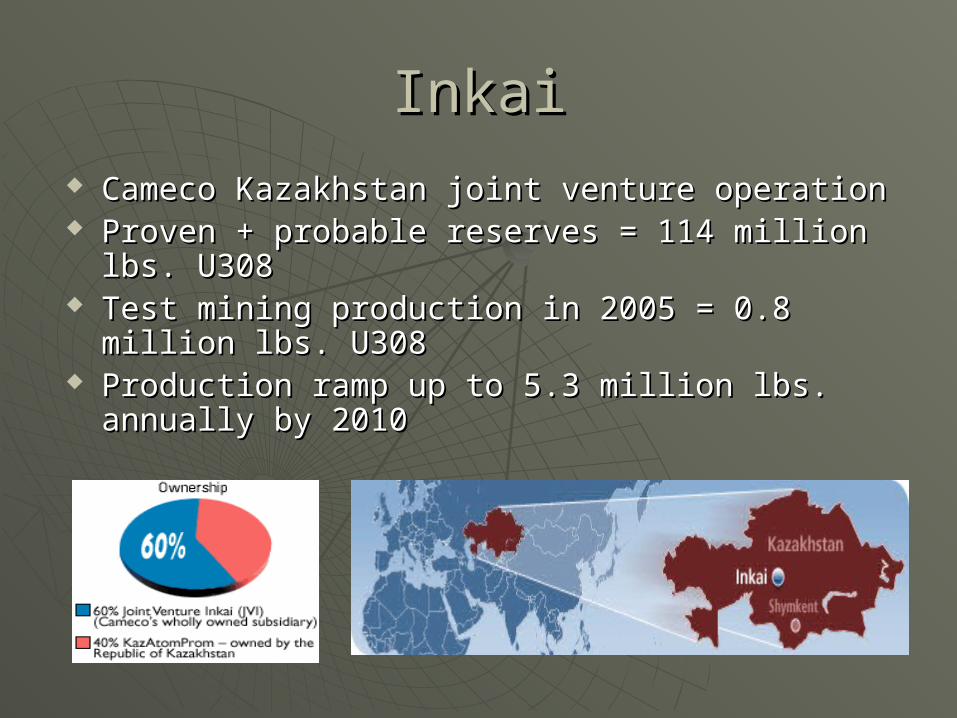

InkaiInkai Cameco Kazakhstan joint venture operationCameco Kazakhstan joint venture operation Proven + probable reserves = 114 million lbs. Proven + probable reserves = 114 million lbs.

U308U308 Test mining production in 2005 = 0.8 million lbs. Test mining production in 2005 = 0.8 million lbs.

U308U308 Production ramp up to 5.3 million lbs. annually by Production ramp up to 5.3 million lbs. annually by

20102010

Conversion OperationsConversion Operations Cameco is 100% owner and operator of Canada's only Cameco is 100% owner and operator of Canada's only

uranium refining and conversion facilities, located in Ontario. uranium refining and conversion facilities, located in Ontario. These include the Blind River refinery, the world's largest, These include the Blind River refinery, the world's largest, where uranium concentrates are processed into high-purity where uranium concentrates are processed into high-purity uranium trioxide (UOuranium trioxide (UO33), an intermediate product used as feed ), an intermediate product used as feed at the company's Port Hope conversion plants. at the company's Port Hope conversion plants.

The Port Hope facility is one of only three commercial The Port Hope facility is one of only three commercial suppliers of uranium hexafluoride (UFsuppliers of uranium hexafluoride (UF66) in the western world. ) in the western world. UFUF66 produced at the plant is delivered to others for produced at the plant is delivered to others for enrichment and fabrication into the fuel pellets used in most enrichment and fabrication into the fuel pellets used in most nuclear reactors. The Port Hope facility is also the world's nuclear reactors. The Port Hope facility is also the world's only commercial supplier of natural uranium dioxide (UOonly commercial supplier of natural uranium dioxide (UO22) ) used to manufacture fuel for the Candu reactors.used to manufacture fuel for the Candu reactors.

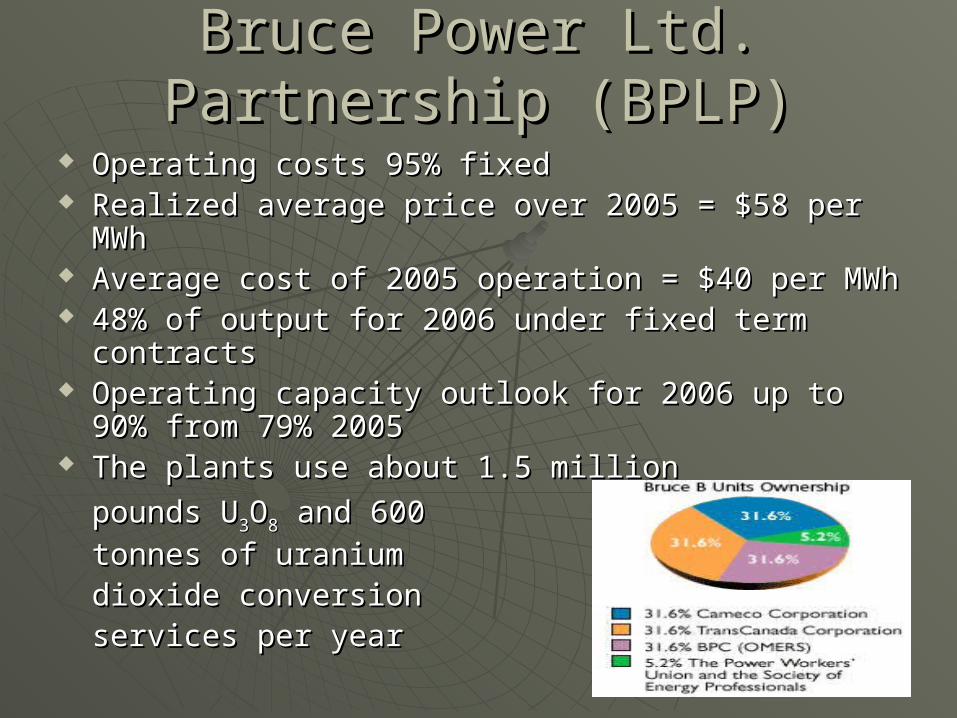

Bruce Power Ltd. Partnership Bruce Power Ltd. Partnership (BPLP)(BPLP)

Operating costs 95% fixedOperating costs 95% fixed Realized average price over 2005 = $58 per MWhRealized average price over 2005 = $58 per MWh Average cost of 2005 operation = $40 per MWhAverage cost of 2005 operation = $40 per MWh 48% of output for 2006 under fixed term 48% of output for 2006 under fixed term

contractscontracts Operating capacity outlook for 2006 up to 90% Operating capacity outlook for 2006 up to 90%

from 79% 2005from 79% 2005 The plants use about 1.5 million The plants use about 1.5 million

pounds Upounds U33OO88 and 600 and 600 tonnes of uranium tonnes of uranium dioxide conversion dioxide conversion services per yearservices per year

Centerra GoldCenterra Gold

Cameco owns 53% interest in CenterraCameco owns 53% interest in Centerra Traded on TSX under ticker “CG”Traded on TSX under ticker “CG” 100% un-hedged on Gold production..100% un-hedged on Gold production.. 4 gold production/exploration properties4 gold production/exploration properties

100% of the Kumtor mine in the Kyrgyz 100% of the Kumtor mine in the Kyrgyz Republic Republic

approximately 95% of the Boroo mine in approximately 95% of the Boroo mine in Mongolia Mongolia

73% of the Gatsuurt property in Mongolia near 73% of the Gatsuurt property in Mongolia near Boroo Boroo

62% of the REN joint venture in Nevada, U.S. 62% of the REN joint venture in Nevada, U.S.

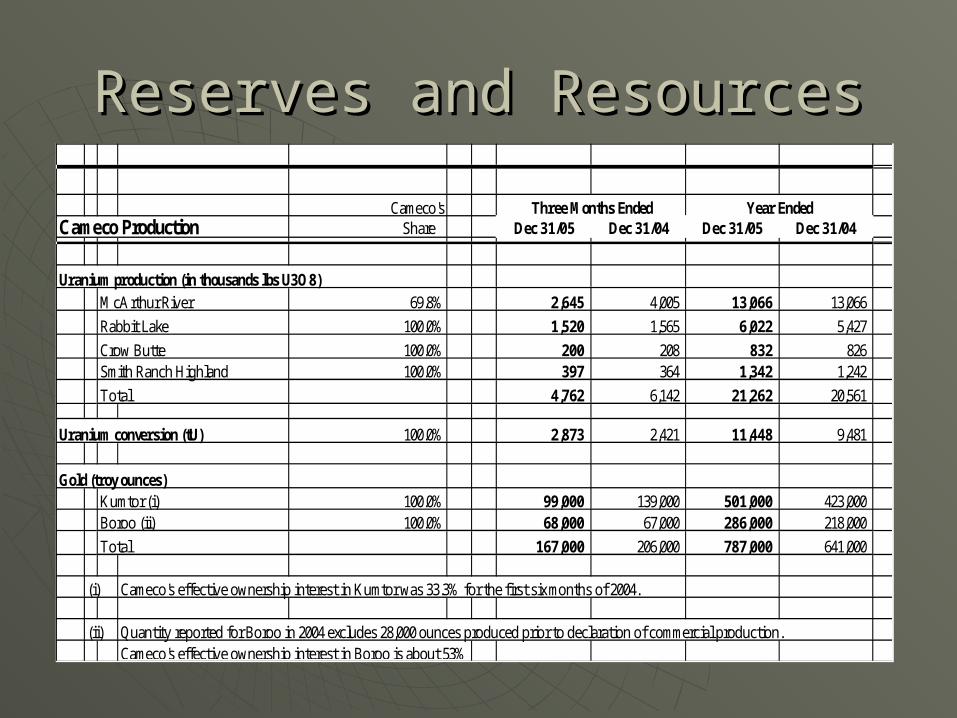

Reserves and ResourcesReserves and Resources

Cameco'sCameco Production Share Dec 31/05 Dec 31/04 Dec 31/05 Dec 31/04

Uranium production (in thousands lbs U3O8)

McArthur River 69.8% 2,645 4,005 13,066 13,066

Rabbit Lake 100.0% 1,520 1,565 6,022 5,427

Crow Butte 100.0% 200 208 832 826Smith Ranch Highland 100.0% 397 364 1,342 1,242

Total 4,762 6,142 21,262 20,561

Uranium conversion (tU) 100.0% 2,873 2,421 11,448 9,481

Gold (troy ounces)Kumtor (i) 100.0% 99,000 139,000 501,000 423,000Boroo (ii) 100.0% 68,000 67,000 286,000 218,000

Total 167,000 206,000 787,000 641,000

(i) Cameco's effective ownership interest in Kumtor was 33.3% for the first six months of 2004.

(ii) Quantity reported for Boroo in 2004 excludes 28,000 ounces produced prior to declaration of commercial production.Cameco's effective ownership interest in Boroo is about 53%.

Year EndedThree Months Ended

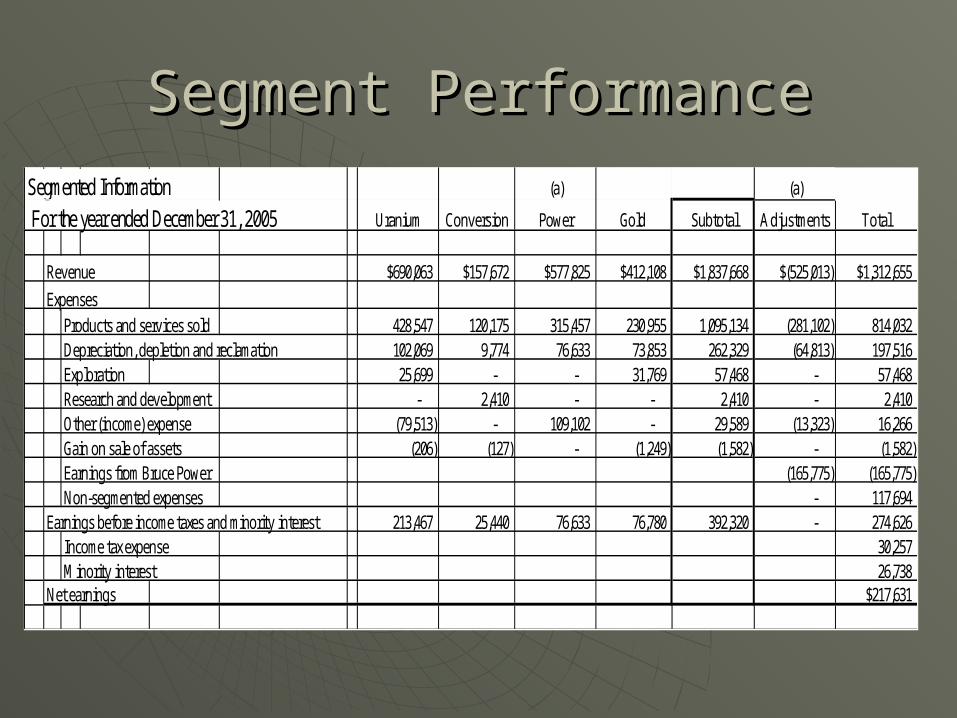

Segment PerformanceSegment PerformanceSegmented Information (a) (a)

For the year ended December 31, 2005 Uranium Conversion Power Gold Subtotal Adjustments Total

Revenue $690,063 $157,672 $577,825 $412,108 $1,837,668 $(525,013) $1,312,655

Expenses

Products and services sold 428,547 120,175 315,457 230,955 1,095,134 (281,102) 814,032 Depreciation, depletion and reclamation 102,069 9,774 76,633 73,853 262,329 (64,813) 197,516 Exploration 25,699 - - 31,769 57,468 - 57,468 Research and development - 2,410 - - 2,410 - 2,410 Other (income) expense (79,513) - 109,102 - 29,589 (13,323) 16,266 Gain on sale of assets (206) (127) - (1,249) (1,582) - (1,582) Earnings from Bruce Power (165,775) (165,775) Non-segmented expenses - 117,694

Earnings before income taxes and minority interest 213,467 25,440 76,633 76,780 392,320 - 274,626 Income tax expense 30,257 Minority interest 26,738

Net earnings $217,631

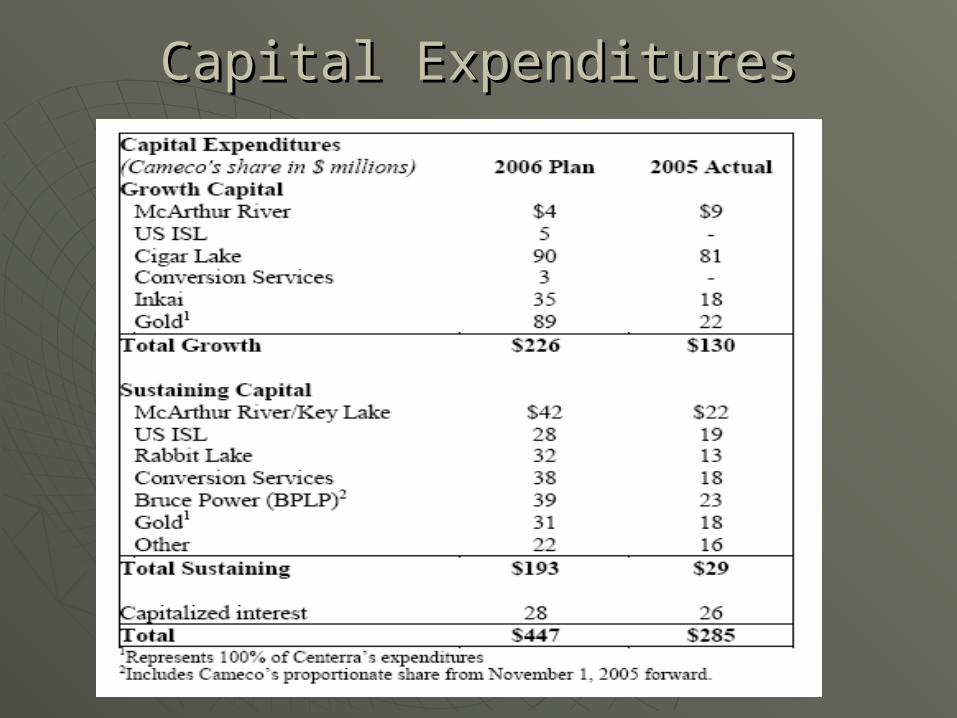

Capital ExpendituresCapital Expenditures

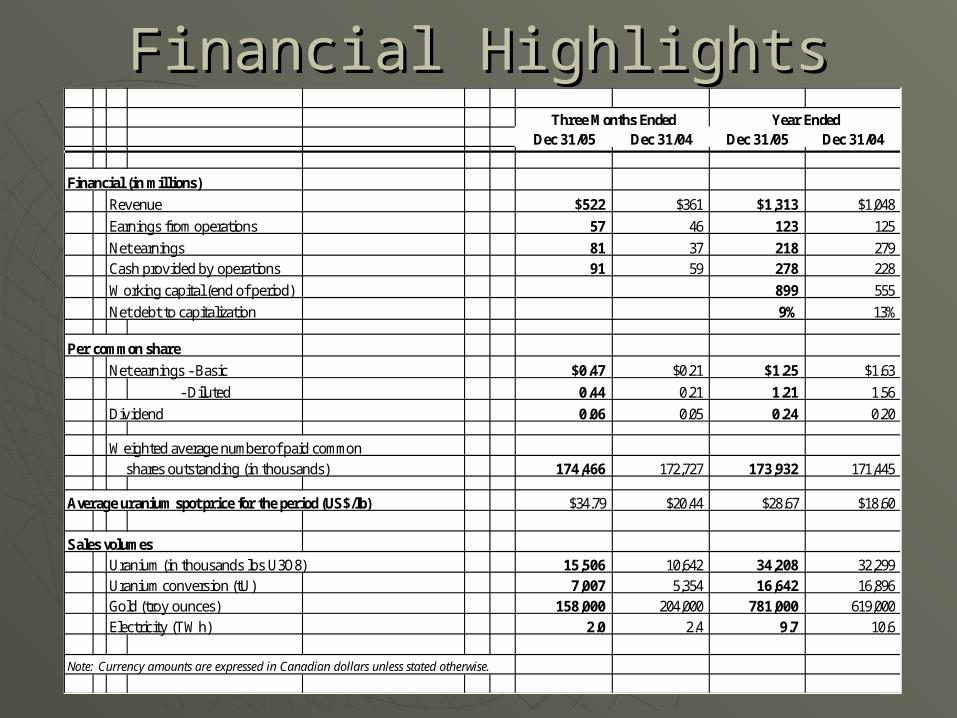

Financial HighlightsFinancial HighlightsDec 31/05 Dec 31/04 Dec 31/05 Dec 31/04

Financial (in millions)

Revenue $522 $361 $1,313 $1,048

Earnings from operations 57 46 123 125

Net earnings 81 37 218 279 Cash provided by operations 91 59 278 228

Working capital (end of period) 899 555

Net debt to capitalization 9% 13%

Per common share

Net earnings - Basic $0.47 $0.21 $1.25 $1.63

- Diluted 0.44 0.21 1.21 1.56

Dividend 0.06 0.05 0.24 0.20

Weighted average number of paid common shares outstanding (in thousands) 174,466 172,727 173,932 171,445

Average uranium spot price for the period (US$/lb) $34.79 $20.44 $28.67 $18.60

Sales volumesUranium (in thousands lbs U3O8) 15,506 10,642 34,208 32,299Uranium conversion (tU) 7,007 5,354 16,642 16,896Gold (troy ounces) 158,000 204,000 781,000 619,000Electricity (TWh) 2.0 2.4 9.7 10.6

Note: Currency amounts are expressed in Canadian dollars unless stated otherwise.

Year EndedThree Months Ended

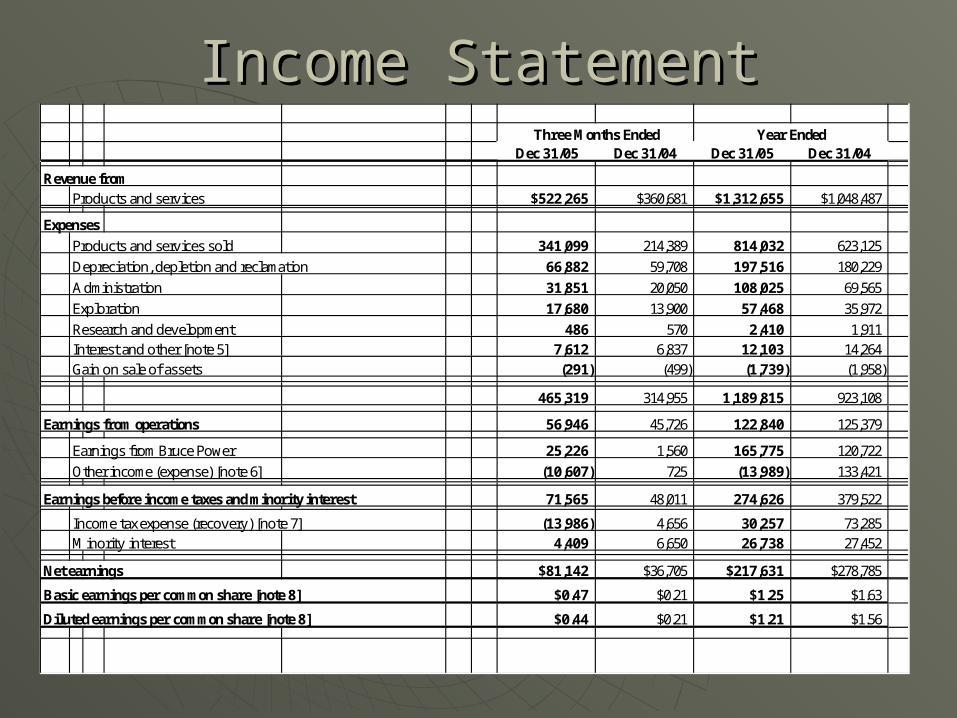

Income StatementIncome Statement

Dec 31/05 Dec 31/04 Dec 31/05 Dec 31/04

Revenue fromProducts and services $522,265 $360,681 $1,312,655 $1,048,487

Expenses

Products and services sold 341,099 214,389 814,032 623,125

Depreciation, depletion and reclamation 66,882 59,708 197,516 180,229

Administration 31,851 20,050 108,025 69,565

Exploration 17,680 13,900 57,468 35,972

Research and development 486 570 2,410 1,911Interest and other [note 5] 7,612 6,837 12,103 14,264Gain on sale of assets (291) (499) (1,739) (1,958)

465,319 314,955 1,189,815 923,108

Earnings from operations 56,946 45,726 122,840 125,379

Earnings from Bruce Power 25,226 1,560 165,775 120,722

Other income (expense) [note 6] (10,607) 725 (13,989) 133,421

Earnings before income taxes and minority interest 71,565 48,011 274,626 379,522

Income tax expense (recovery) [note 7] (13,986) 4,656 30,257 73,285Minority interest 4,409 6,650 26,738 27,452

Net earnings $81,142 $36,705 $217,631 $278,785

Basic earnings per common share [note 8] $0.47 $0.21 $1.25 $1.63

Diluted earnings per common share [note 8] $0.44 $0.21 $1.21 $1.56

Three Months Ended Year Ended

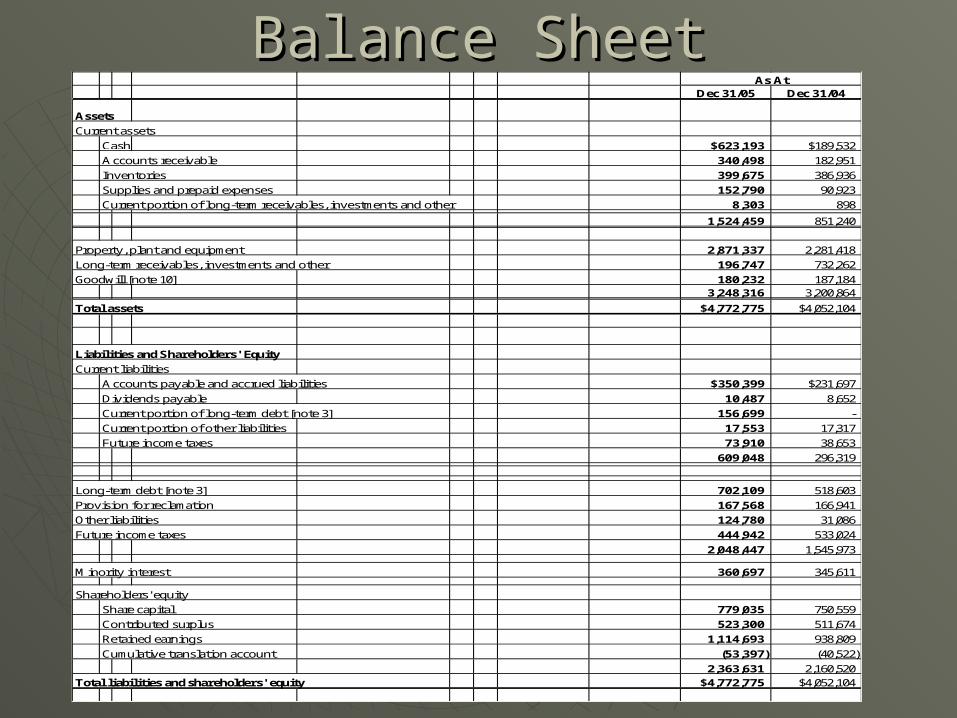

Balance SheetBalance SheetDec 31/05 Dec 31/04

Assets

Current assets

Cash $623,193 $189,532

Accounts receivable 340,498 182,951

Inventories 399,675 386,936

Supplies and prepaid expenses 152,790 90,923

Current portion of long-term receivables, investments and other 8,303 898

1,524,459 851,240

Property, plant and equipment 2,871,337 2,281,418

Long-term receivables, investments and other 196,747 732,262

Goodwill [note 10] 180,232 187,1843,248,316 3,200,864

Total assets $4,772,775 $4,052,104

Liabilities and Shareholders' Equity

Current liabilities

Accounts payable and accrued liabilities $350,399 $231,697

Dividends payable 10,487 8,652

Current portion of long-term debt [note 3] 156,699 -

Current portion of other liabilities 17,553 17,317

Future income taxes 73,910 38,653

609,048 296,319

Long-term debt [note 3] 702,109 518,603

Provision for reclamation 167,568 166,941

Other liabilities 124,780 31,086

Future income taxes 444,942 533,024

2,048,447 1,545,973

Minority interest 360,697 345,611

Shareholders' equity

Share capital 779,035 750,559

Contributed surplus 523,300 511,674

Retained earnings 1,114,693 938,809

Cumulative translation account (53,397) (40,522)

2,363,631 2,160,520

Total liabilities and shareholders' equity $4,772,775 $4,052,104

As At

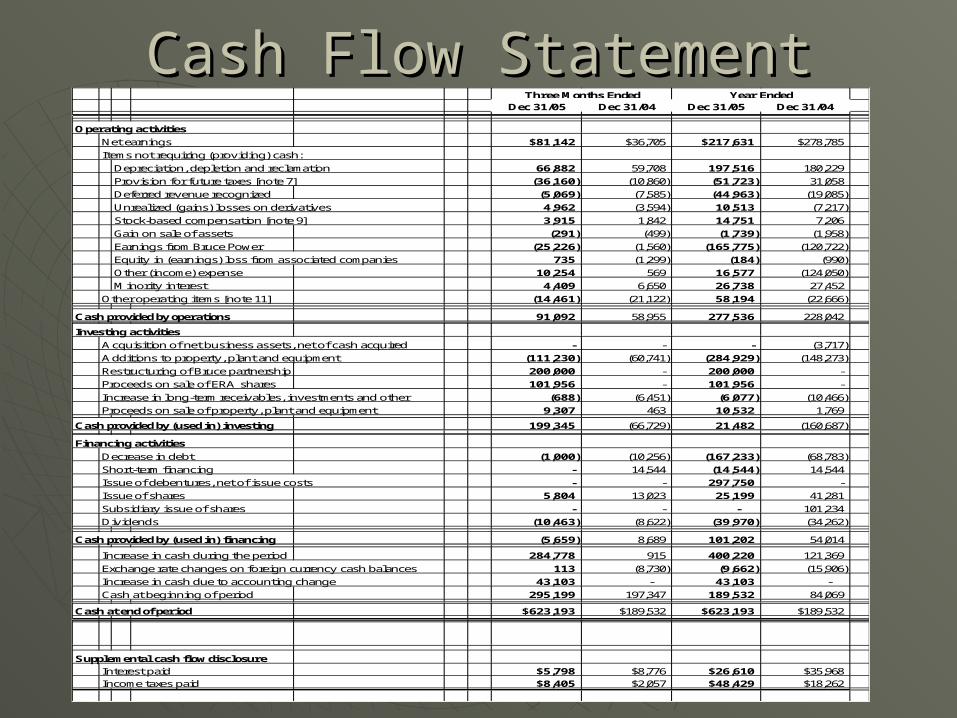

Cash Flow StatementCash Flow Statement Dec 31/05 Dec 31/04 Dec 31/05 Dec 31/04

Operating activities

Net earnings $81,142 $36,705 $217,631 $278,785

Items not requiring (providing) cash:

Depreciation, depletion and reclamation 66,882 59,708 197,516 180,229

Provision for future taxes [note 7] (36,160) (10,860) (51,723) 31,058

Deferred revenue recognized (5,069) (7,585) (44,963) (19,085)

Unrealized (gains) losses on derivatives 4,962 (3,594) 10,513 (7,217)

Stock-based compensation [note 9] 3,915 1,842 14,751 7,206

Gain on sale of assets (291) (499) (1,739) (1,958)

Earnings from Bruce Power (25,226) (1,560) (165,775) (120,722)

Equity in (earnings) loss from associated companies 735 (1,299) (184) (990)

Other (income) expense 10,254 569 16,577 (124,050)

Minority interest 4,409 6,650 26,738 27,452

Other operating items [note 11] (14,461) (21,122) 58,194 (22,666)

Cash provided by operations 91,092 58,955 277,536 228,042

Investing activities

Acquisition of net business assets, net of cash acquired - - - (3,717)

Additions to property, plant and equipment (111,230) (60,741) (284,929) (148,273)

Restructuring of Bruce partnership 200,000 - 200,000 -

Proceeds on sale of ERA shares 101,956 - 101,956 -

Increase in long-term receivables, investments and other (688) (6,451) (6,077) (10,466)

Proceeds on sale of property, plant and equipment 9,307 463 10,532 1,769

Cash provided by (used in) investing 199,345 (66,729) 21,482 (160,687)

Financing activities

Decrease in debt (1,000) (10,256) (167,233) (68,783)

Short-term financing - 14,544 (14,544) 14,544

Issue of debentures, net of issue costs - - 297,750 -

Issue of shares 5,804 13,023 25,199 41,281

Subsidiary issue of shares - - - 101,234

Dividends (10,463) (8,622) (39,970) (34,262)

Cash provided by (used in) financing (5,659) 8,689 101,202 54,014

Increase in cash during the period 284,778 915 400,220 121,369

Exchange rate changes on foreign currency cash balances 113 (8,730) (9,662) (15,906)

Increase in cash due to accounting change 43,103 - 43,103 -

Cash at beginning of period 295,199 197,347 189,532 84,069

Cash at end of period $623,193 $189,532 $623,193 $189,532

Supplemental cash flow disclosure

Interest paid $5,798 $8,776 $26,610 $35,968

Income taxes paid $8,405 $2,057 $48,429 $18,262

Three Months Ended Year Ended

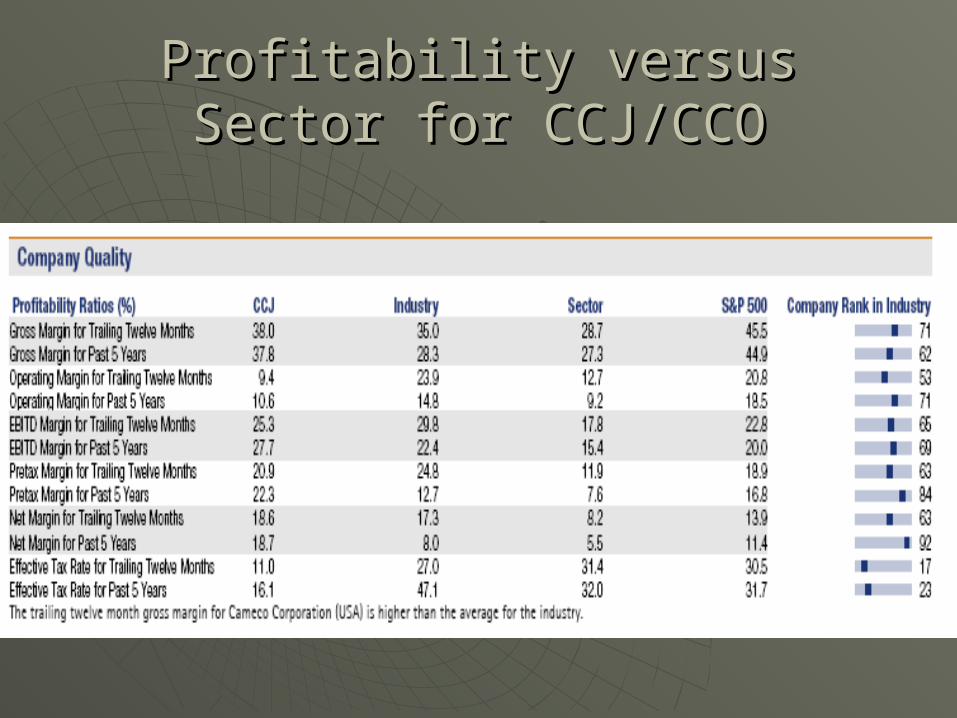

Profitability versus Sector for Profitability versus Sector for CCJ/CCOCCJ/CCO

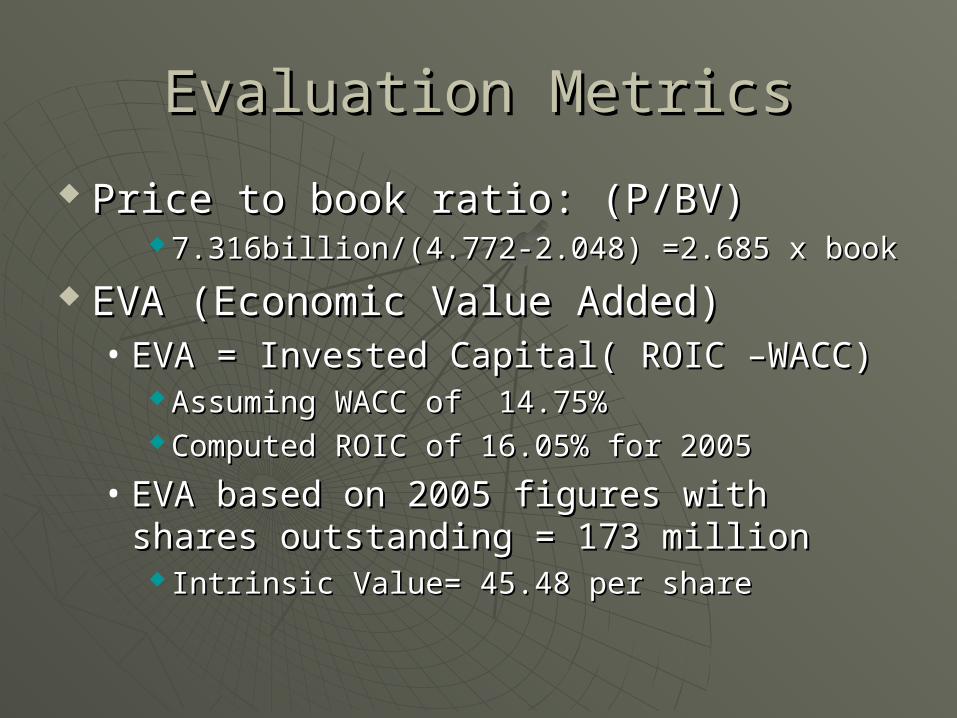

Evaluation MetricsEvaluation Metrics

Price to book ratio: (P/BV)Price to book ratio: (P/BV) 7.316billion/(4.772-2.048) =2.685 x book7.316billion/(4.772-2.048) =2.685 x book

EVA (Economic Value Added)EVA (Economic Value Added)• EVA = Invested Capital( ROIC –WACC)EVA = Invested Capital( ROIC –WACC)

Assuming WACC of 14.75%Assuming WACC of 14.75% Computed ROIC of 16.05% for 2005Computed ROIC of 16.05% for 2005

• EVA based on 2005 figures with shares EVA based on 2005 figures with shares outstanding = 173 millionoutstanding = 173 million

Intrinsic Value= 45.48 per shareIntrinsic Value= 45.48 per share

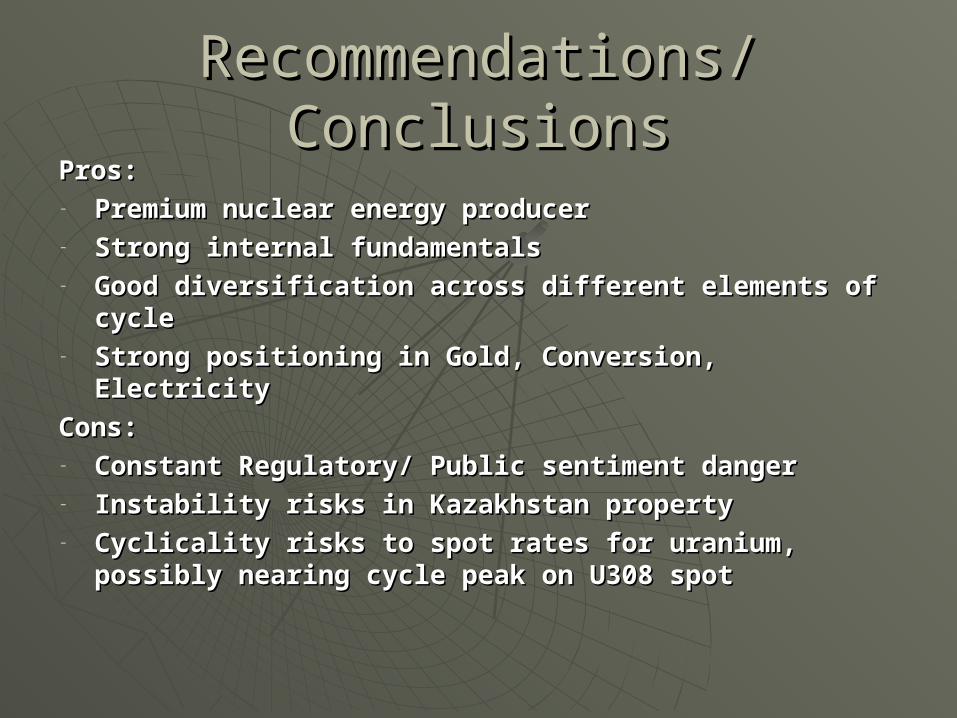

Recommendations/ConclusionsRecommendations/ConclusionsPros:Pros:- Premium nuclear energy producerPremium nuclear energy producer- Strong internal fundamentalsStrong internal fundamentals- Good diversification across different elements of Good diversification across different elements of

cycle cycle - Strong positioning in Gold, Conversion, ElectricityStrong positioning in Gold, Conversion, Electricity

Cons:Cons:- Constant Regulatory/ Public sentiment dangerConstant Regulatory/ Public sentiment danger- Instability risks in Kazakhstan propertyInstability risks in Kazakhstan property- Cyclicality risks to spot rates for uranium, possibly Cyclicality risks to spot rates for uranium, possibly

nearing cycle peak on U308 spotnearing cycle peak on U308 spot

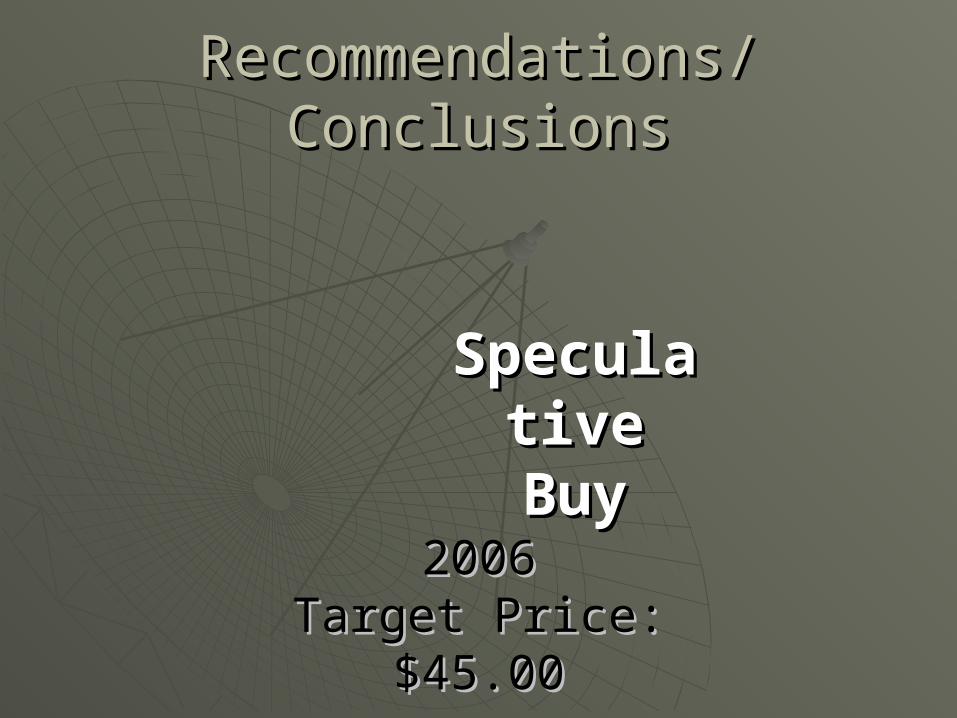

Recommendations/ConclusionsRecommendations/Conclusions

SpeculativSpeculative Buye Buy

2006 2006 Target Price: $45.00Target Price: $45.00

Newmont Mining Corporation

Creating Value with Every Ounce…

Uses of Gold

FabricationJewelry, electronics, dentistry,

industrial, decorative uses, medals (Olympic gold medal is in fact made of silver), official coins

InvestmentGold bullion, official coins, and

jewelry

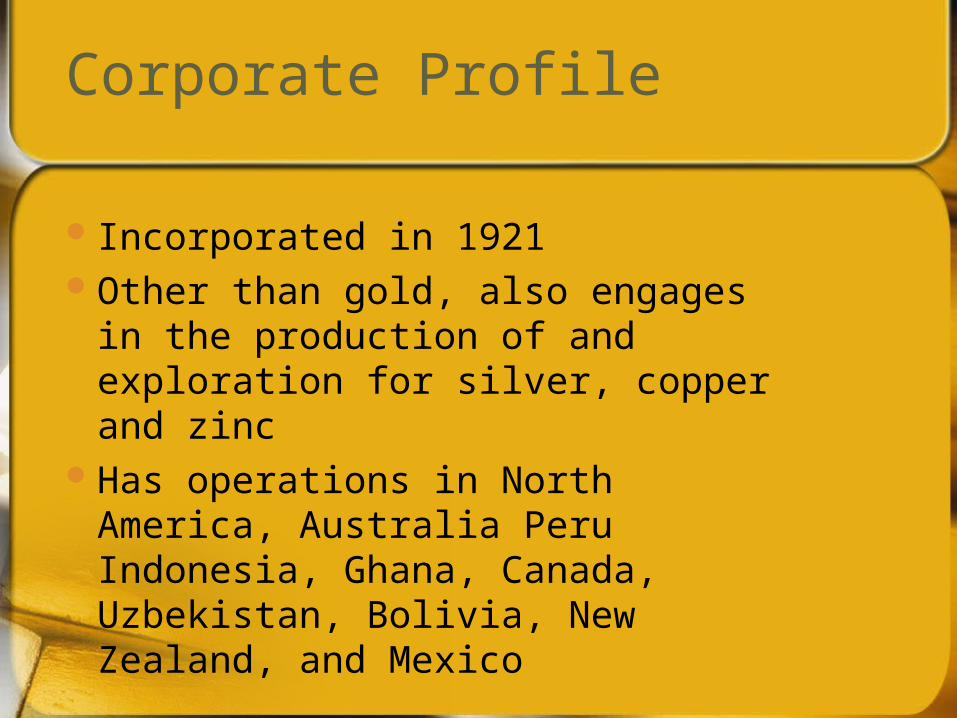

Corporate Profile

Incorporated in 1921Other than gold, also engages in

the production of and exploration for silver, copper and zinc

Has operations in North America, Australia Peru Indonesia, Ghana, Canada, Uzbekistan, Bolivia, New Zealand, and Mexico

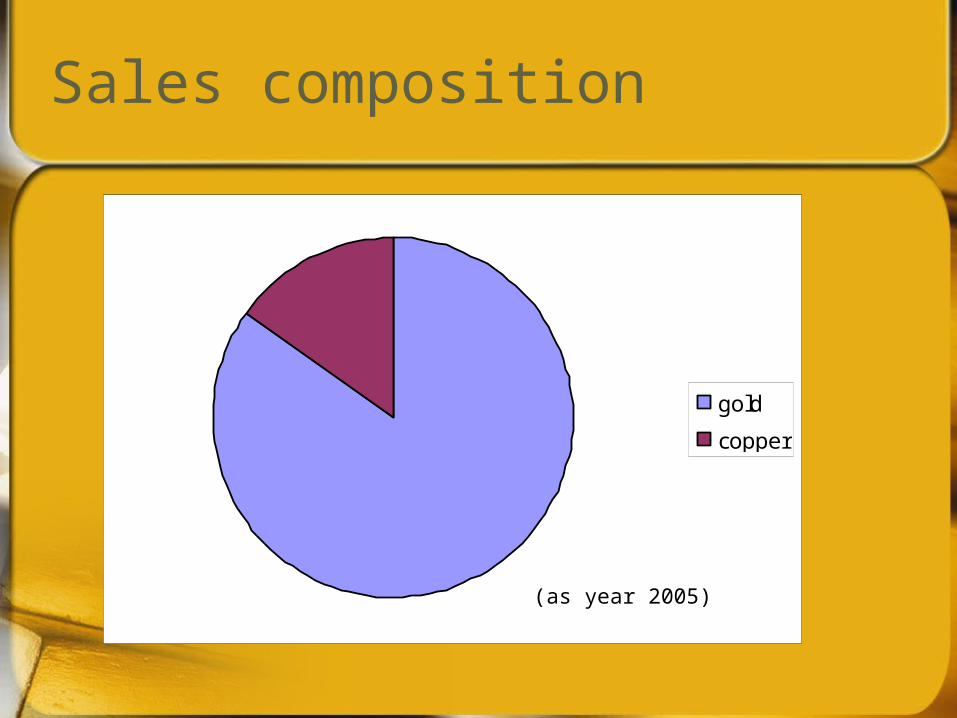

Sales composition

gold

copper

(as year 2005)

Executives

Wayne W. Murdy, Chairman and CEO (61) Pierre Lassonde, President (58) Britt D. Banks, senior VP and general

counsel (44) Thomas L. Enos, Senior VP, operations (54) Bruce D. Hansen, Senior VP, operation

services and development (48) Richard D. O’Brien, Senior VP and CFO (51)

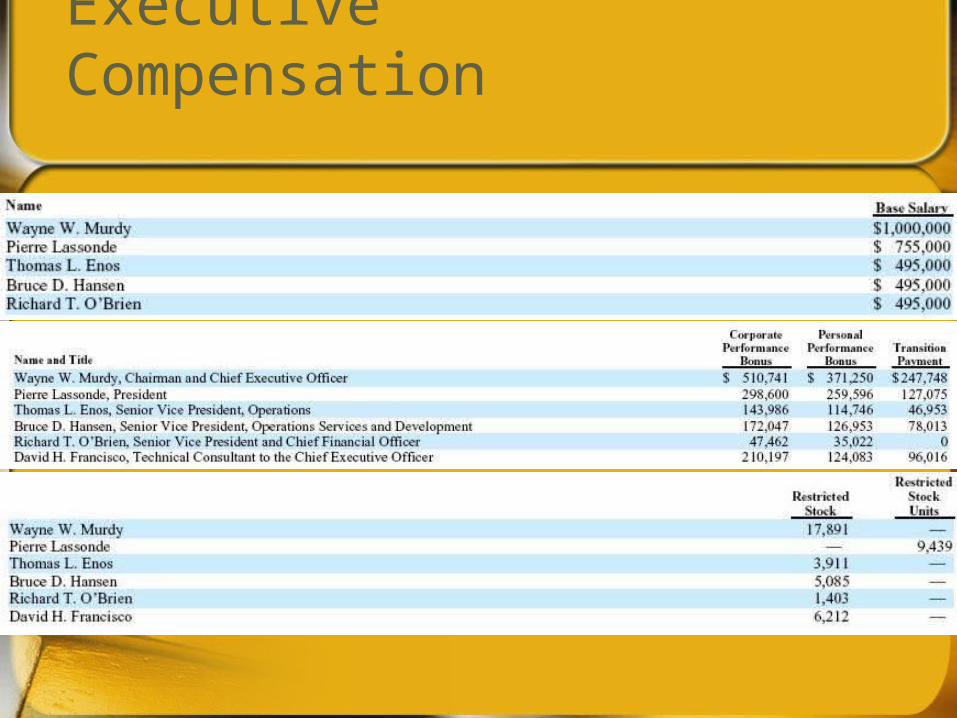

Executive Compensation

Reserves and its Value

As year 2004, Newmont reserved 92.4 million equity ounces of gold (93.2 million for year 2005) North America 35 million ounces South America 17 million ounces Africa 16 million ounces Australia/New Zealand 15.1 million ounces Indonesia 7.2 million ounces Central Asia 2.1 million ounces

Probable copper reserve was 9.1 billion equity pounds.

Newmont Properties

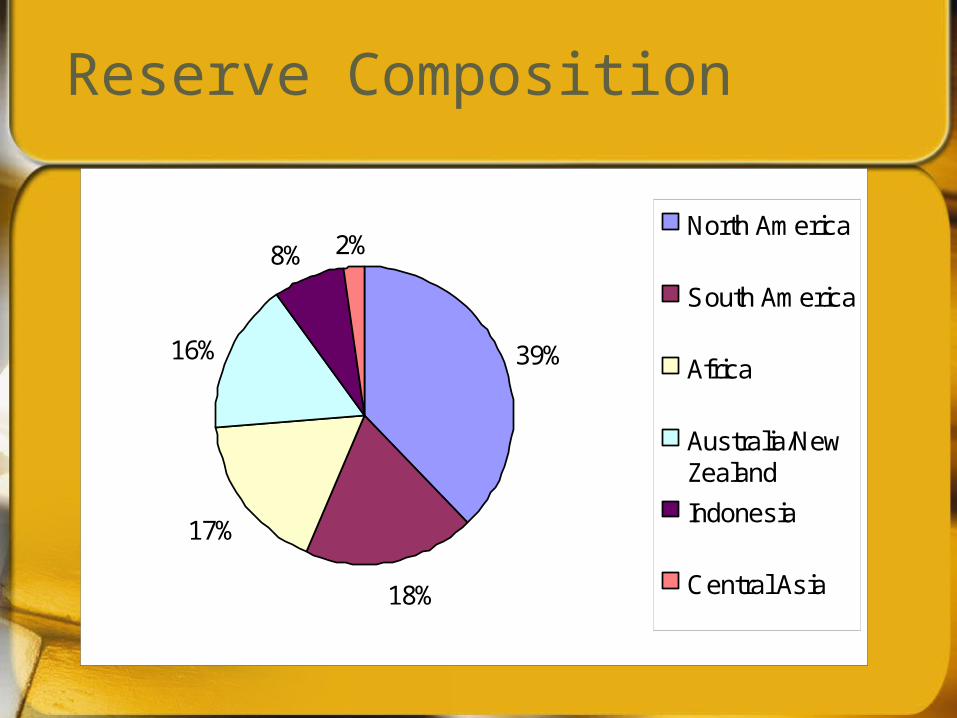

Reserve Composition

39%

18%

17%

16%

8% 2%North America

South America

Africa

Australia/NewZealand

Indonesia

Central Asia

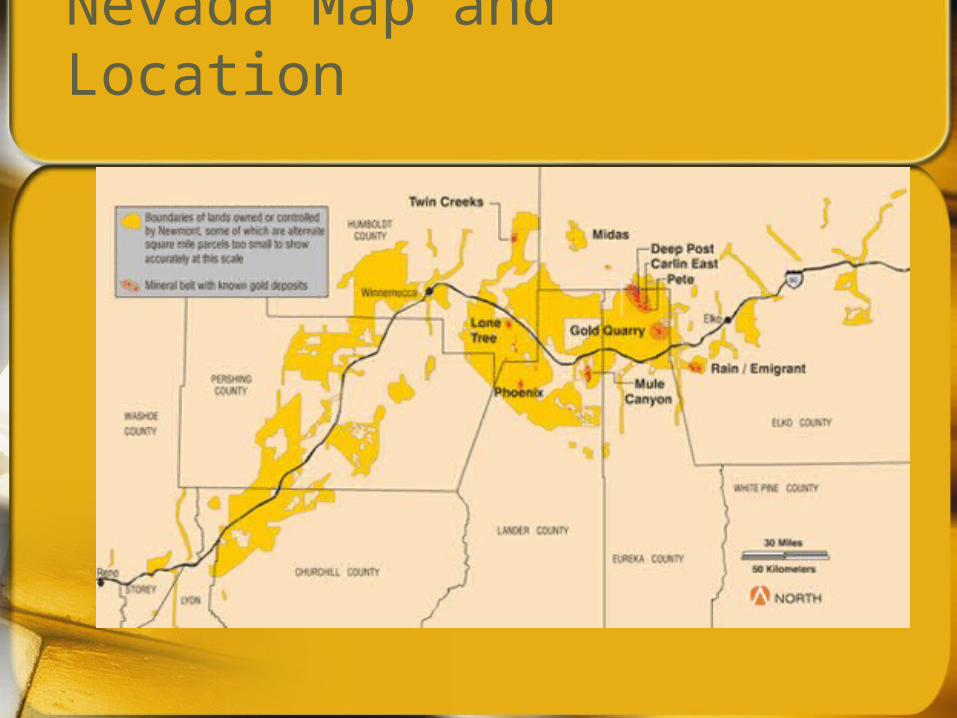

Nevada Operation

Newmont owns or controls approximately 3,056 square miles (7,915 square kilometers) of land in Nevada

Three Regions: Eastern NevadaTwin Creeks, Lone Tree and

Phoenix Midas

Nevada Map and Location

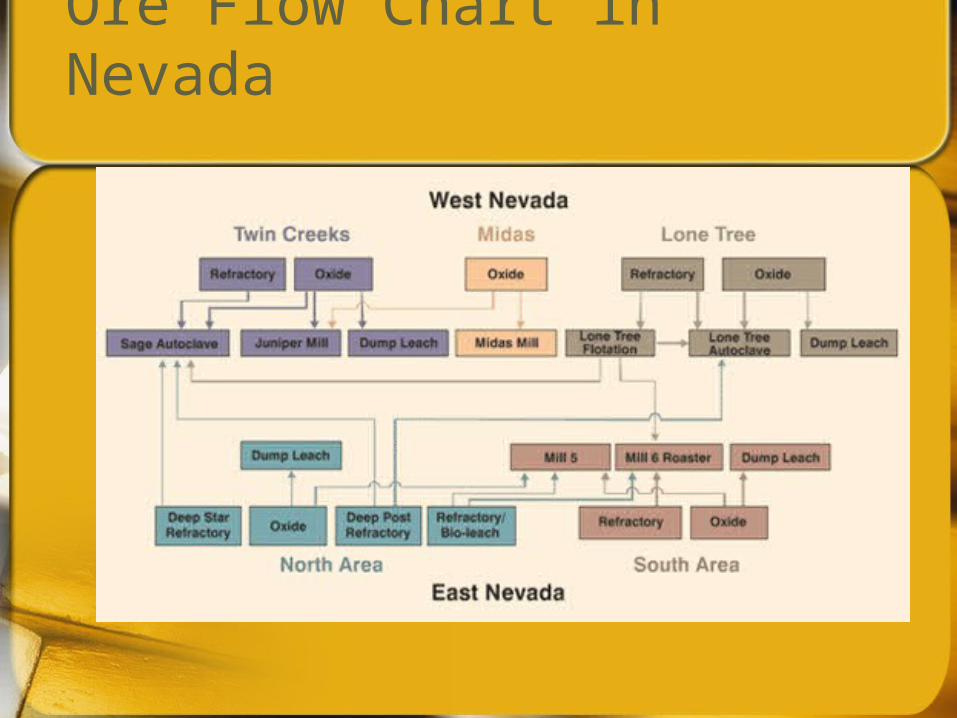

Ore Flow Chart in Nevada

Minera Yanacocha, Peru

51.35% Newmont, 43.65% Peruvian mining firm, Compania de Minas Buenaventura S.A.A , 5% International Finance Corporate

Minerta Yanaocha, Peru

Australia/New Zealand

Re-entry in year 2001After acquiring Normandy

Mining, Newmont is now the largest gold producer in Australia

Five mining operations in Western Australia, Queensland, the Northern Territory and New Zealand

Australia/NZ Map and Location

Indonesia Operation

Minahasa, started operation in 1996

Batu Hijau, a large copper-gold deposit on the island of Sumbawa, started in 1999

Recent attack on workers’ residential camp may raise security issues

Indonesia Map and Location

Central Asia

Zarafshan-Newmont Joint Venture The operation produces gold from

low grade oxide ore.

Commodity Price Risk

Metal prices fluctuateDue to demand, forward selling by

producers, central bank sales, purchases and lending, investor sentiment, and global mine production levels

Forward sales contracts with fixed and floating gold lease rates

Newmont stock and gold price

Hedging Philosophy

A non-hedgerViewing gold as an equivalent to

moneyCreating paper gold is

considered too risky

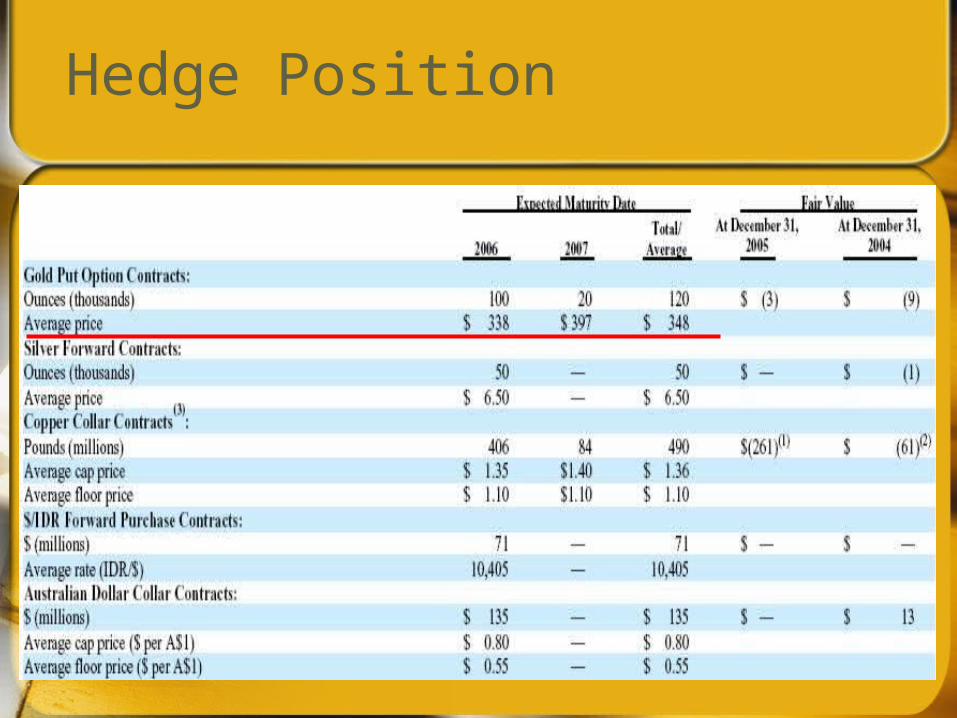

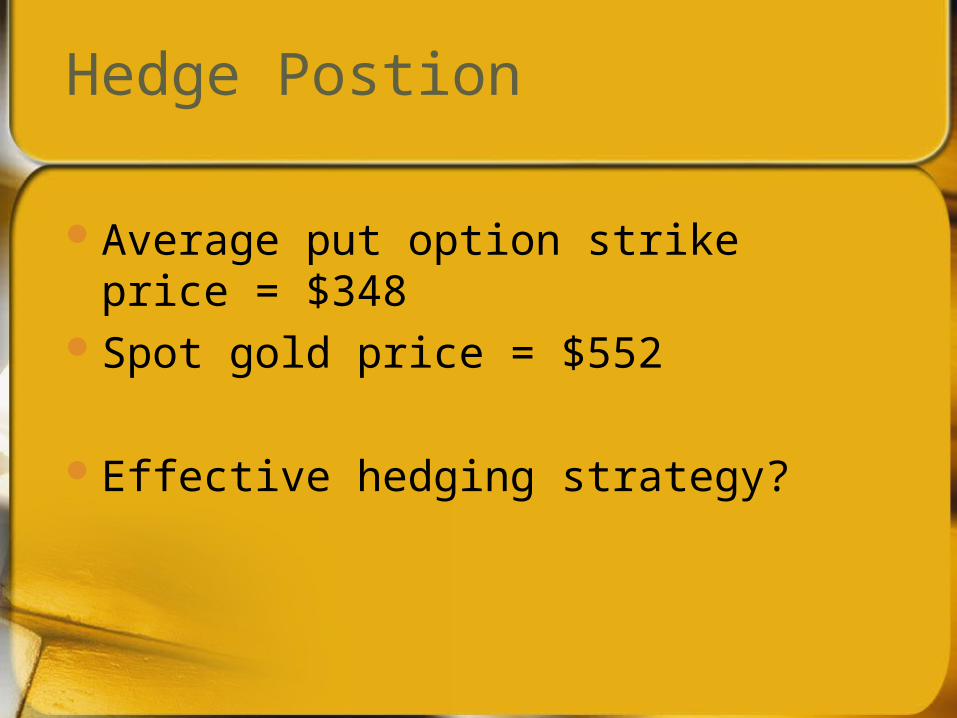

Hedge Position

Hedge Postion

Average put option strike price = $348

Spot gold price = $552

Effective hedging strategy?

Financial Statements

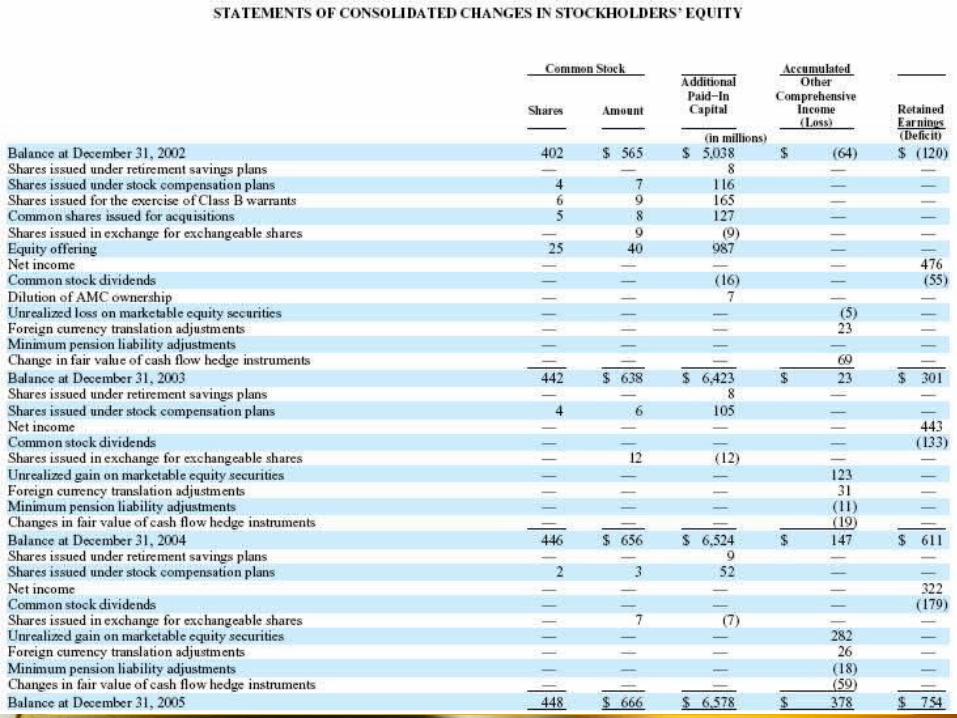

Income StatementBlance SheetStatement of Change in

Shareholder EquityStatement of Cash Flow

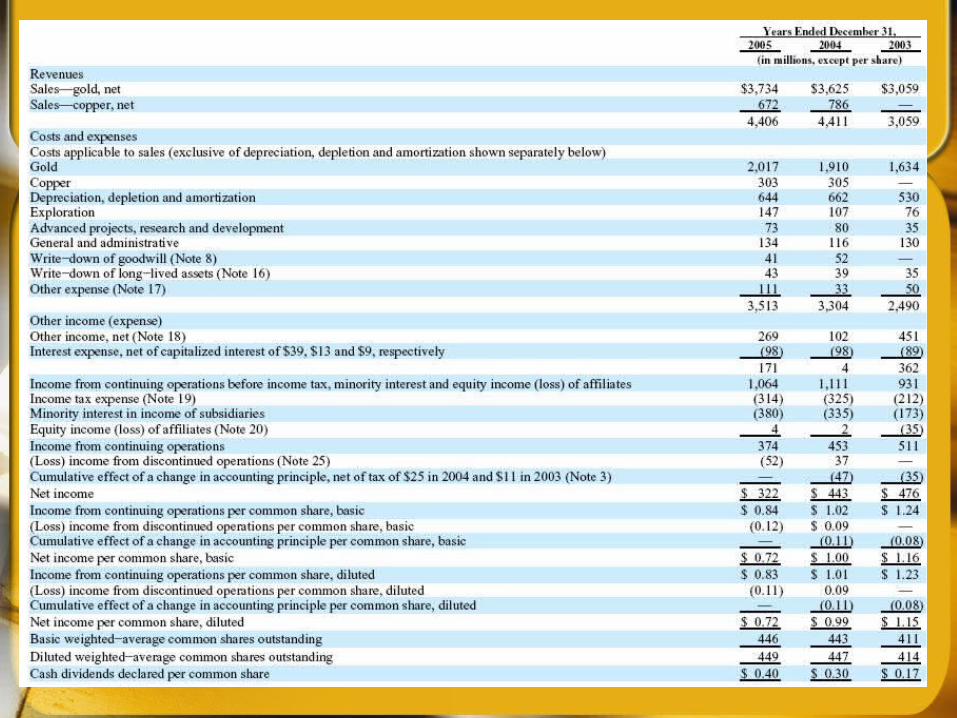

Income Statement

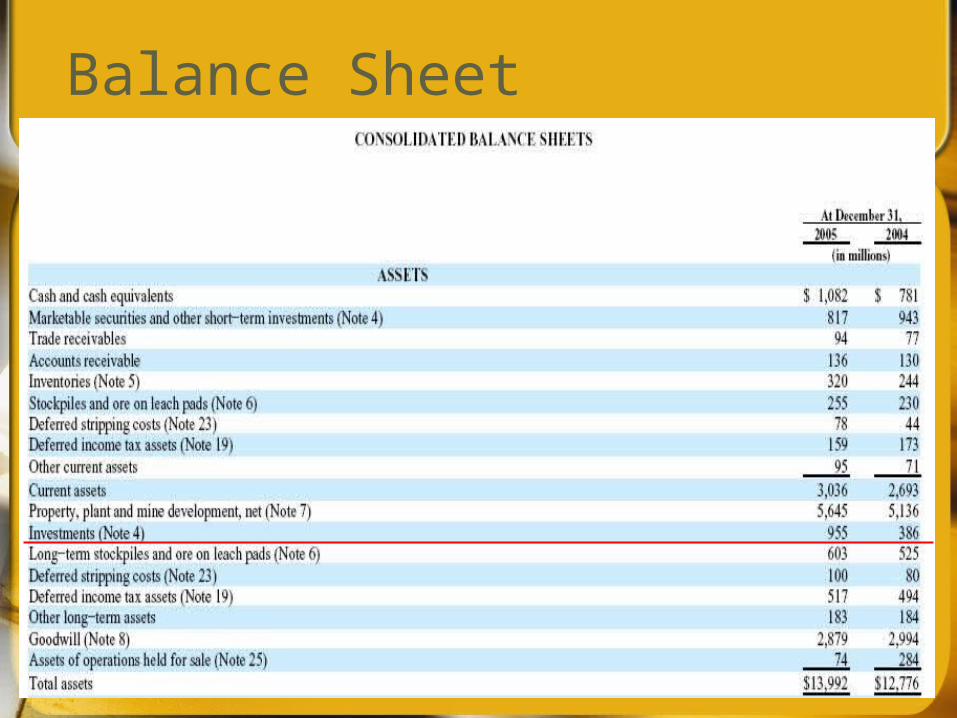

Balance Sheet

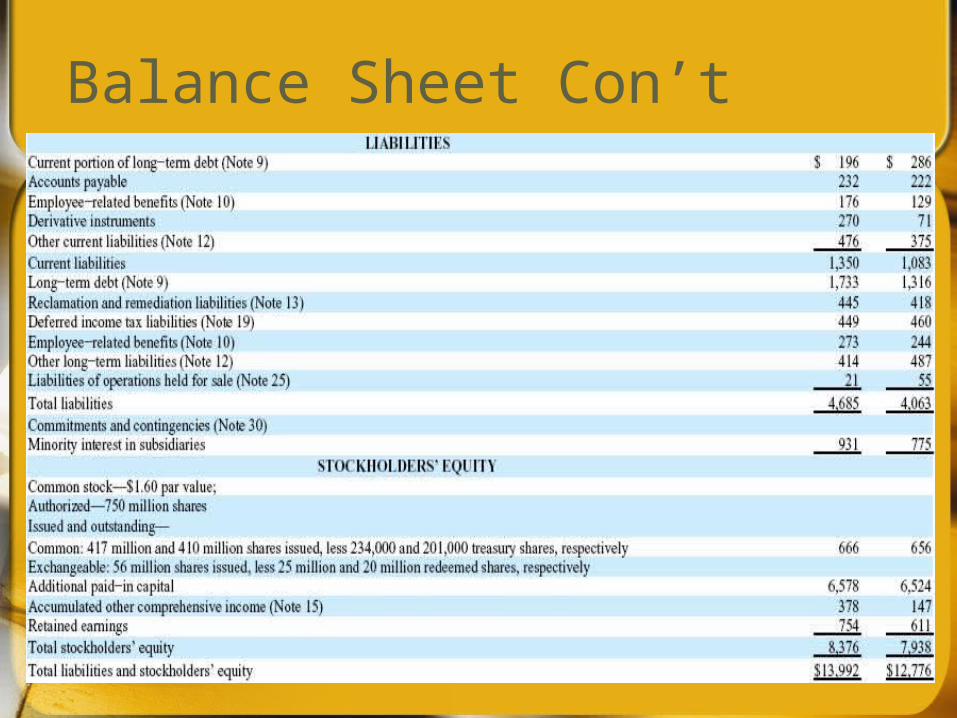

Balance Sheet Con’t

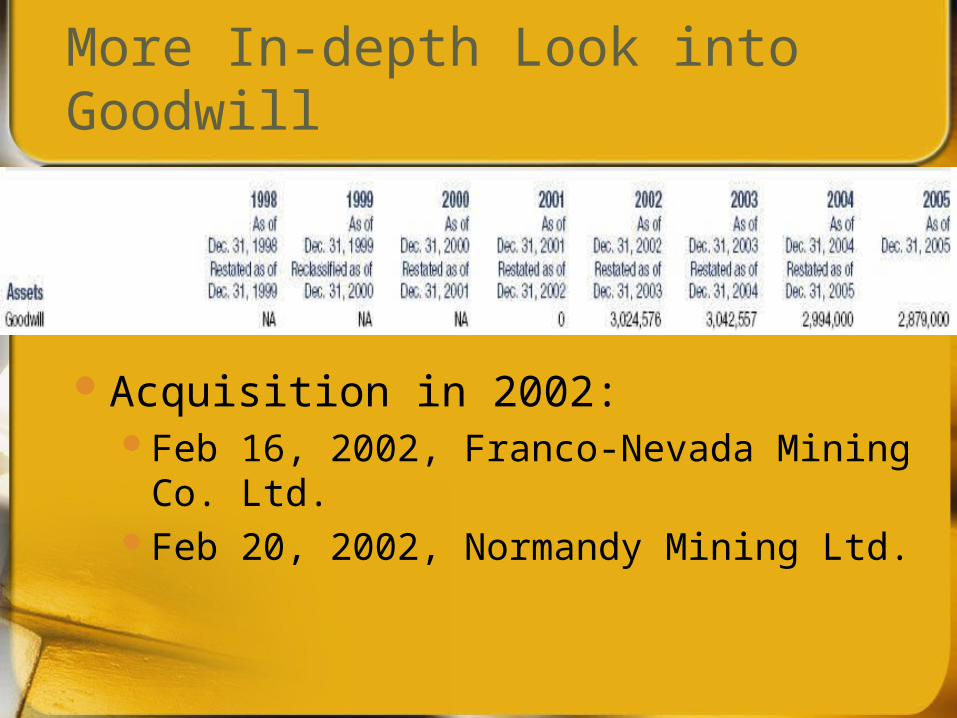

More In-depth Look into Goodwill

Acquisition in 2002:Feb 16, 2002, Franco-Nevada Mining Co.

Ltd.Feb 20, 2002, Normandy Mining Ltd.

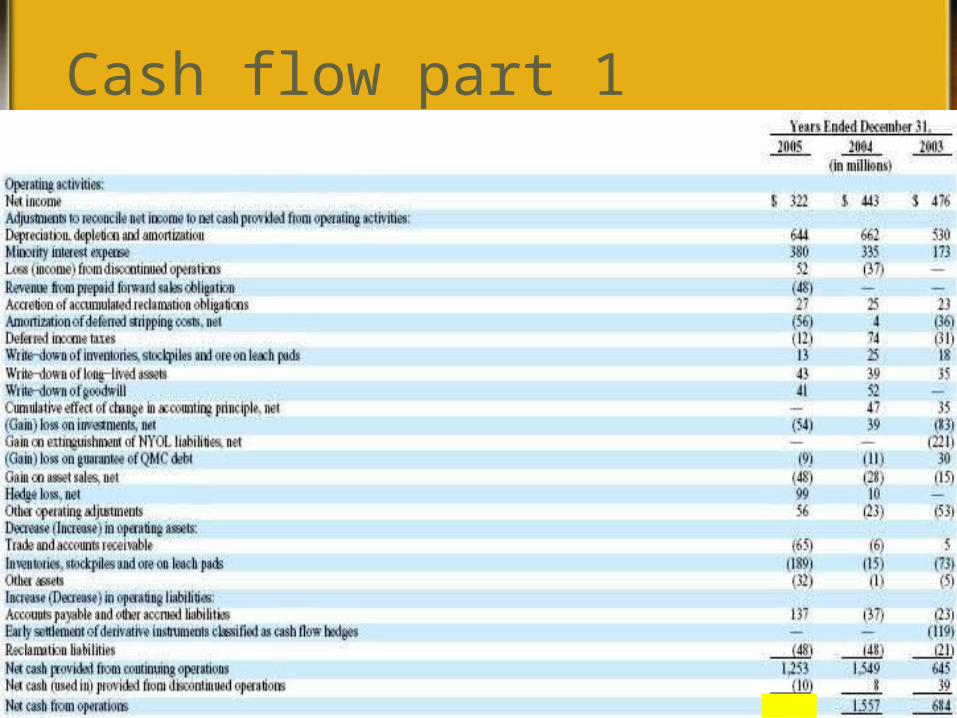

Cash flow part 1

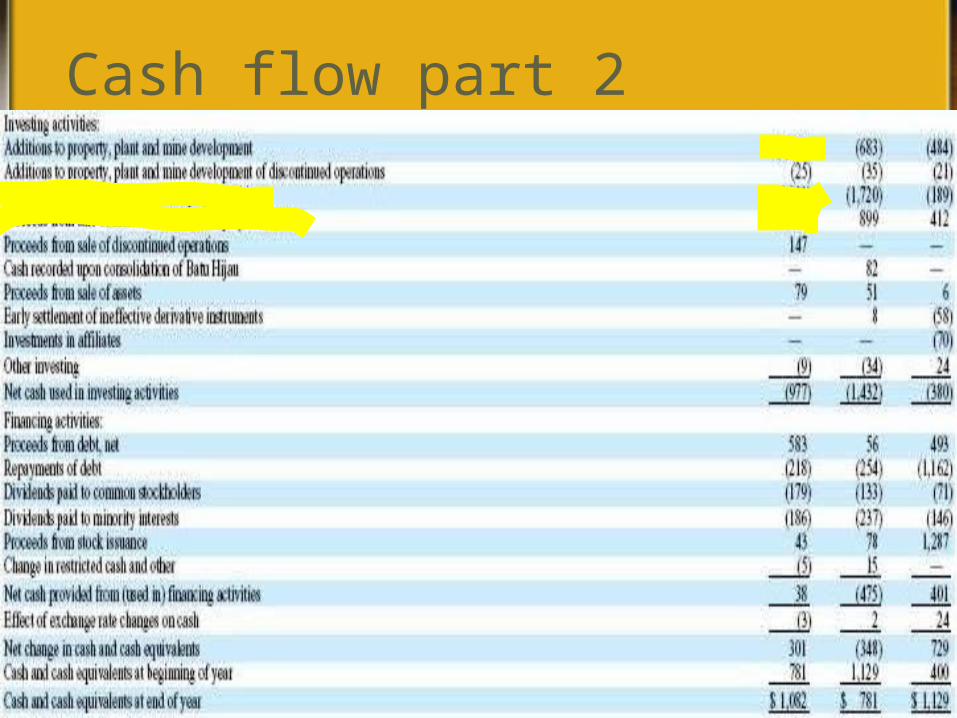

Cash flow part 2

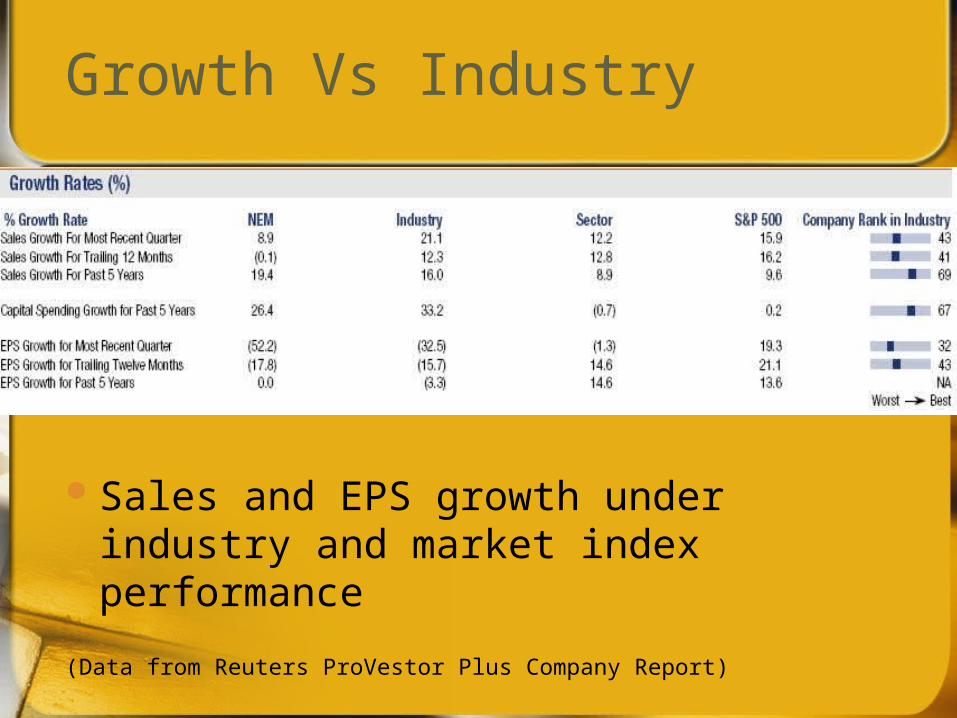

Growth Vs Industry

Sales and EPS growth under industry and market index performance

(Data from Reuters ProVestor Plus Company Report)

Recommendation

EXIT