Millennials’ Future · Millennials are a wave that will ripple through the economy as they...

18

Transcript of Millennials’ Future · Millennials are a wave that will ripple through the economy as they...

© 2017 Chase Intel, LLC

Conclusions

Millennials have numbers, but they will not halt the long-term trend of the weakening relative economic power of young people

Despite the size of the generation, the number of families in the US will rise only moderately through the next decade

In many ways Millennial spending patterns mimic those of prior generations, which can help you anticipate demand for family travel

Belief: Testing and applying the analyses that follow can help determine when and where to focus your efforts

© 2017 Chase Intel, LLC

Conclusions based on my analysis of Govt. estimates and millions of surveys

Social and Economic Supplement to the Current Population Survey**

Census Bureau: 1961 - 2016

American Community Survey**Census Bureau: 2005 – 2016

2014 National Population Projections DatasetsCensus Bureau: 2014

Survey of Consumer FinanceFederal Reserve: 1989 - 2016

Consumer Expenditure SurveyBureau of Labor Statistics 1996 – 2016

Natality information (Fertility Rates)Center for Disease Control: 2007 - 2016

**Steven Ruggles, Katie Genadek, Ronald Goeken, Josiah Grover, and Matthew Sobek.

Integrated Public Use Microdata Series: Version 7.0 [dataset]. Minneapolis:

University of Minnesota, 2017. https://doi.org/10.18128/D010.V7.0.

© 2017 Chase Intel, LLC

US-centric analysis, but these types of data are available in many countries

Census data for eighty-five countrieshttps://international.ipums.org/international/

Australian Bureau of Statistics [Access restricted]http://abs.gov.au/websitedbs/D3310114.nsf/

home/CURF:+About+the+ABS+Data+Laboratory+(ABSDL)

Presentation Flow

Generational income and wealth trends

Family formation and travel forecast

Suggestions for next steps

© 2017 Chase Intel, LLC

Definitions vary, but think of Millennials as a generation 9% larger than Gen X

Generation** Years # Years# People(Millions)

People/Yr(Millions)

Silent/Greatest < ‘46 29+ 28 1.0

Boomers ‘46 – ‘64 19 74 3.9

Gen X ’65 – ‘80 16 66 4.1

Millennials ’81 - 97 17 76 4.5

Gen Z > ‘97 20 82 4.1

**Generations as defined by Pew Research

Source: Summary oit States Census Bureau: 2014 National Population Projections Datasets: Table np2014-d1 :: 2017 Projections

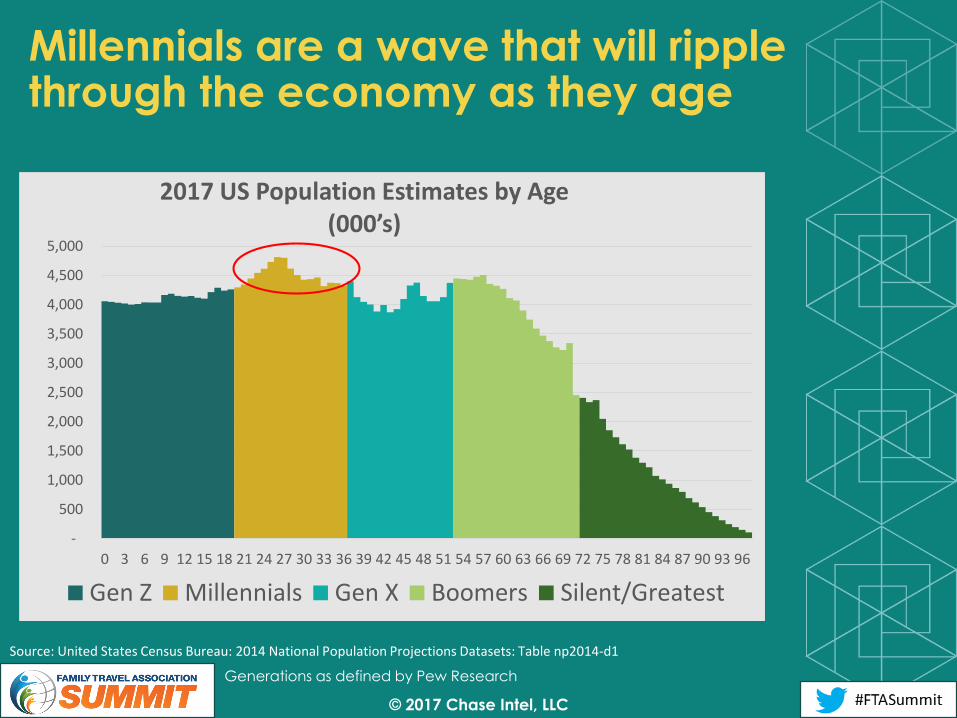

The Millennial generation has one more year of births than does Gen X• On an average, annual bases it has 4.5 million members per year• That is 9% more than Gen X’s 4.1 million

Note that Gen Z (with no defined end date) has the most members• That’s due to it having 20 years of births vs 17 for Millennials• On an adjusted basis it’s no larger than Gen X• But, it is anticipated to grow through immigration

© 2017 Chase Intel, LLC

Millennials are a wave that will ripple through the economy as they age

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96

2017 US Population Estimates by Age(000’s)

Gen Z Millennials Gen X Boomers Silent/Greatest

Source: United States Census Bureau: 2014 National Population Projections Datasets: Table np2014-d1

Generations as defined by Pew Research

© 2017 Chase Intel, LLC

Boomers are an avalanche, transforming the distribution of wealth in the US

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96

2017 US Population Estimates by Age(000’s)

Gen Z Millennials Gen X Boomers Silent/Greatest

Source: United States Census Bureau: 2014 National Population Projections Datasets: Table np2014-d1

Generations as defined by Pew Research

© 2017 Chase Intel, LLC

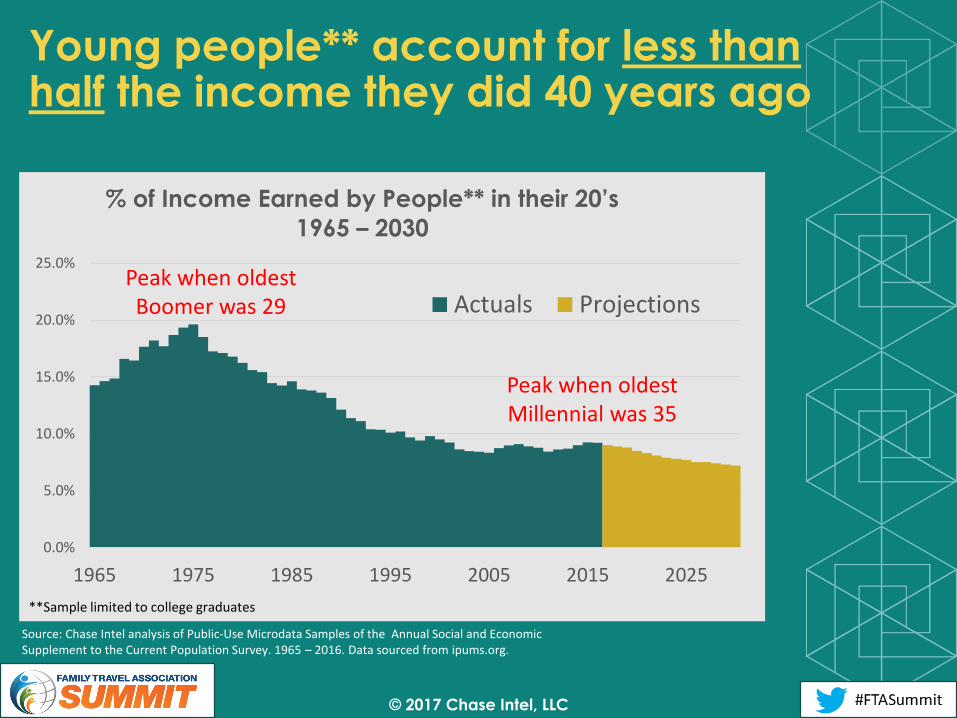

Young people** account for less than half the income they did 40 years ago

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1965 1975 1985 1995 2005 2015 2025

% of Income Earned by People** in their 20’s

1965 – 2030

Actuals ProjectionsBoomer impact

**Sample limited to college graduates

Peak when oldest Boomer was 29

Peak when oldest Millennial was 35

Source: Chase Intel analysis of Public-Use Microdata Samples of the Annual Social and Economic Supplement to the Current Population Survey. 1965 – 2016. Data sourced from ipums.org.

© 2017 Chase Intel, LLC

Their share of income will continue going to people 60 and over.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

1965 1975 1985 1995 2005 2015 2025

% of Income Earned by People** 60 and Over

1965 – 2030

Actuals ProjectionsBoomer impact

Source: Chase Intel analysis of Public-Use Microdata Samples of the Annual Social and Economic Supplement to the Current Population Survey. 1965 – 2016. Data sourced from ipums.org.

**Sample limited to college graduates

© 2017 Chase Intel, LLC

Net worth is a more extreme version of the same story; Millennials hold <3%

< 35 35 - 44 45 - 54 55 - 64 65+

1989 2016

Proportion of household net worthby age of householder

Source: Survey of Consumer Finance: Table 4. Family net worth, by selected characteristics of families, 1989–2016 surveys

Family Formation and Travel

© 2017 Chase Intel, LLC

The number of children is anticipated to grow slowly over the next decade

0

10

20

30

40

50

60

70

80

90

1970 1980 1990 2000 2010 2020 2030

Number of 0-17 Aged Children

(Millions)

1970 - 2030

Actuals Projections

Growing for first time in ten

years

Percent growth in number of

children: 2017 - 2030

• Total: 3.4%

• Annual 0.3%

Growth will be concentrated

in households with younger

children

Why is growth so moderate?

• Fertility rate is down 10%

in past ten years

• Without immigration there

would be no growth

Source: 1970 – 2016 Chase Intel analysis of the Public-Use Microdata samples of the Annual Social and

Economic Supplement to Current Population Survey 1970 – 2016. ipums.org

2017 - 2030: https://census.gov/data/datasets/2014/demo/popproj/2014-popproj.html Table 1

:

© 2017 Chase Intel, LLC

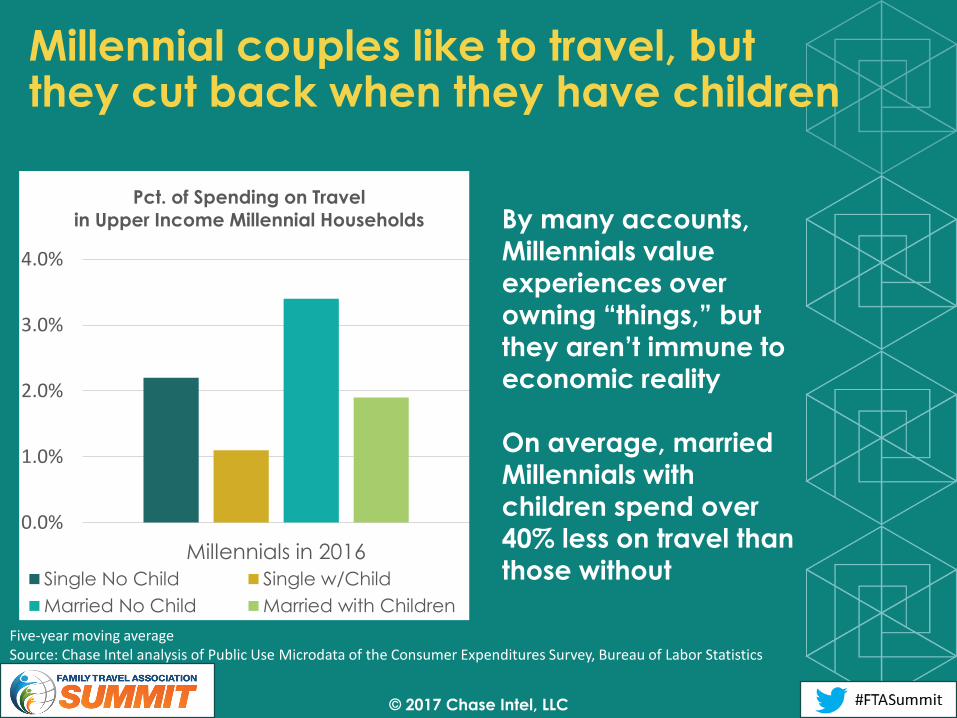

Millennial couples like to travel, butthey cut back when they have children

0.0%

1.0%

2.0%

3.0%

4.0%

Millennials in 2016

Pct. of Spending on Travel

in Upper Income Millennial Households

Single No Child Single w/Child

Married No Child Married with Children

By many accounts,

Millennials value

experiences over owning “things,” but

they aren’t immune to

economic reality

On average, married

Millennials with

children spend over

40% less on travel than

those without

Five-year moving averageSource: Chase Intel analysis of Public Use Microdata of the Consumer Expenditures Survey, Bureau of Labor Statistics

© 2017 Chase Intel, LLC

X’rs did the same thing when they were the same age as Millennials are now

0.0%

1.0%

2.0%

3.0%

4.0%

Gen X in 2000

Pct. of Spending on Travel

in Upper Income Gen X households

Single No Child Single w/Child

Married No Child Married with Children

Millennials with

children spend within

0.2% of what Gen X

did at the same age

This is true for other

categories of

spending as well

This predictability

facilitates effective

planning

Five-year moving averageSource: Chase Intel analysis of Public Use Microdata of the Consumer Expenditures Survey, Bureau of Labor Statistics

© 2017 Chase Intel, LLC

Among couples, empty-nest Boomers and Gen X families are the top travelers

-

5.00

10.00

15.00

20.00

25.00

Married No Children Married with Children

$ in

Bill

ion

s

Average Annual Travel Spend

2014 - 2016

Millennial Gen X BoomerSource: Chase Intel analysis of Public Use Microdata of the Consumer Expenditures Survey, Bureau of Labor Statistics2014-2016

© 2017 Chase Intel, LLC

Travel spending is likely to continue to shift to those with higher incomes

0%

10%

20%

30%

40%

50%

60%

70%

80%

Consumers Now Consumers of Same Age in 2000

% of Travel Spend from Upper Income

Households**

2016 v 2000

Millennial Gen X BoomerThree-Year Moving Average

** Sample includes only Married Householders with children

Source: Chase Intel analysis of Public Use Microdata of the Consumer Expenditures Survey, Bureau of Labor Statistics1998 - 2016

© 2017 Chase Intel, LLC

Concluding thoughts. . .

Set realistic goals for Millennials and other generations, timing your investments appropriately

Explore opportunities for multi-generational travel as a driver of growth

• Grandparents with money and cash-constrained parents who like to travel, sound like a match!

Monitor household formation, income and spending trends to ensure your plans remain in synch with the market

Refrain from relying on a sole source of information (including mine) to inform your decisions

• Compare these conclusions with what you see in your business and in your data

• Combined, these data can suggest insights to be tested and developed