Milk & Creambrakes-source.co.uk/assetfiles/Milk_and_C… · PPT file · Web view ·...

12

Milk & Cream May 2010

Transcript of Milk & Creambrakes-source.co.uk/assetfiles/Milk_and_C… · PPT file · Web view ·...

Milk & Cream

May 2010

2 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

Issues in the market

A sense of optimism has returned to the British dairy industry in 2010, with farmers and processors investing in expansion and forming producer group alliances with retailers.

Both milk and cream are performing well, with increases of 5.6% in volume and 15% in value over the last five years to an estimated 5,249 million litres valued at over £3.4 billion in 2010.

Moderated growth of 2.9% volume and 11.7% value is forecast over the next five years, projecting the total market for milk and cream to reach 5,403 million litres worth £3.8 billion in 2015.

3 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

Key themes

Health as a driver, with 1% milk set to grow in market shareFluctuating production costs are a continuing problem for the dairy industryGetting young adults to increase their milk intake poses a challenge Flavoured milk represents the fastest growing milk and cream sub-category Brand investment was low in 2009 but expected to catch up in 2010.

4 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

SummaryVolume and particularly value growth have been strong across the liquid white milk, flavoured milk and cream categories, while lack of investment has left canned and dried milk sales stagnant in 2009.

Flavoured milk is currently the most buoyant sub-category, led by chocolate variants, whilst allergy-friendly substitutes and specialist lines are driving growth in the cream market.

Within the fresh white milk segment skimmed and 1% milk have performed strongly while organic milk sales have also held up well in the recession, however, fresh speciality milks and soya-based drinks have taken a hit.

While supermarket-dedicated producer groups have been lauded by some as offering support and confidence to the British dairy industry, others are more critical of retail pricing structures.

While the recession is beginning to lift, premium categories may take some time to recover as downturn trends ranging from the growth of economy lines to more eating in the home and less wastage continue.

Austerity in advertising spend and NPD activity in 2009 looks set to give way to greater market confidence, as many milk and cream manufacturers plan major brand investment in 2010.

Health and the environment are key drivers of NPD but a double edged sword for the milk and cream categories, offering both challenges (critical attention) and opportunities (marketing potential).

While milk types gaining in usage include fresh pasteurised and organic, milk is a commodity product for many consumers and has no profile as a drink choice for a third of consumers – often women.

Fresh double cream leads usage by type, clotted and sour creams are popular choices with ABs and young Londoners respectively.

5 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

Internal market environment

Manufacturers face a challenge in communicating the many health benefits of milk to consumers, while fuller fat milks and cream have been criticised for their saturated fat content by the FSA.

The British milk industry is gaining kudos for its pro-active approach to reducing the significant carbon footprint of dairy farming and processing.

Interest in health has diminished in the recession, alongside origin and organic production, as other priorities take over but calorie counting is on the rise.

6 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

Broader market environment

While dairy sector forecasts have improved in 2010, fluctuating costs and farmgate prices remain concerns. Producer group premiums offer some comfort to farmers.

The recession may have abated for some, particularly 55+ ABs, but others are struggling with enhanced awareness of unnecessary expenditure or waste likely to continue.

Increasing numbers of elderly will boost use of milk in tea, coffee and other hot drinks, while growth among ABs supports a return to premiumisation.

7 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

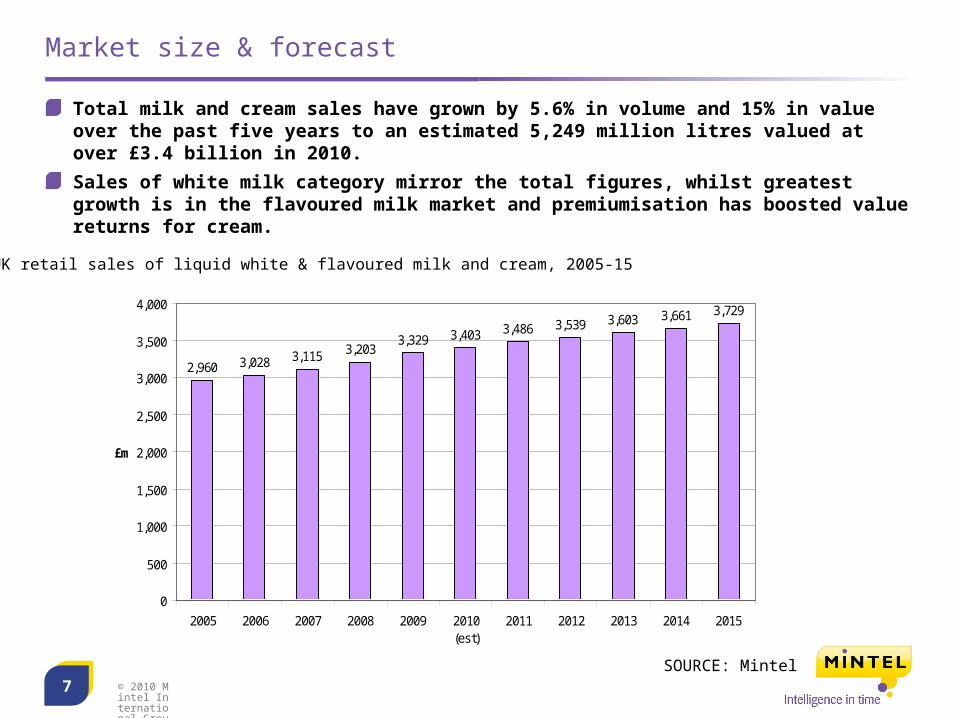

Market size & forecast

Total milk and cream sales have grown by 5.6% in volume and 15% in value over the past five years to an estimated 5,249 million litres valued at over £3.4 billion in 2010.Sales of white milk category mirror the total figures, whilst greatest growth is in the flavoured milk market and premiumisation has boosted value returns for cream.

2,960 3,028 3,115 3,2033,329 3,403 3,486 3,539 3,603 3,661 3,729

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2005 2006 2007 2008 2009 2010(est)

2011 2012 2013 2014 2015

£m

SOURCE: Mintel

UK retail sales of liquid white & flavoured milk and cream, 2005-15

8 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

Strengths and weaknesses

StrengthsThe recession brought new opportunities in economy and traditional milk and cream lines.Promoting the nutritional attributes of milk offers scope for further market opportunities.Dairy farmers and processors are going green to tackle criticism of emissions.Dedicated retail producer groups: offering confidence and stability to farmers.Positive forecasts and new market entrants are emerging in 2010.

WeaknessesThe recession has forced consumers to cut back on grocery spend and wastage.FSA campaign is targeting full-fat and semi-skimmed milk and cream.Environmental lobbyists are calling on consumers to cut back on dairy consumption due to the carbon footprint of the industry.Topline marketing spend and NPD launches have dropped in 2009: harming future growth.

9 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

Who’s innovating?

New products dominate NPD including white and flavoured milks with over a third of the market apiece, followed by non-dairy options such as soya and rice drinks.

Health is a popular driver of innovation, notably the emergent 1% milk category and widespread fortification, while green packaging has entered the mainstream.

Further NPD trends include recession-friendly budget lines boosting own-label market share, chocolate flavoured drinks and traditional-style unhomogenised milk.

10 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

Consumer usage by sub-category

Semi-skimmed is a popular choice across demographics, skimmed with older women and full-fat with families, whilst middle-aged men are the least adventurous with their milk consumption.

66

20 19

10 9 97 6 5 5

12

3

0

10

20

30

40

50

60

70

(%)

Source: Toluna/Mintel

Types of milk personally used, January 2010

11 © 2010 Mintel International Group. All rights reserved. Confidential to Mintel.

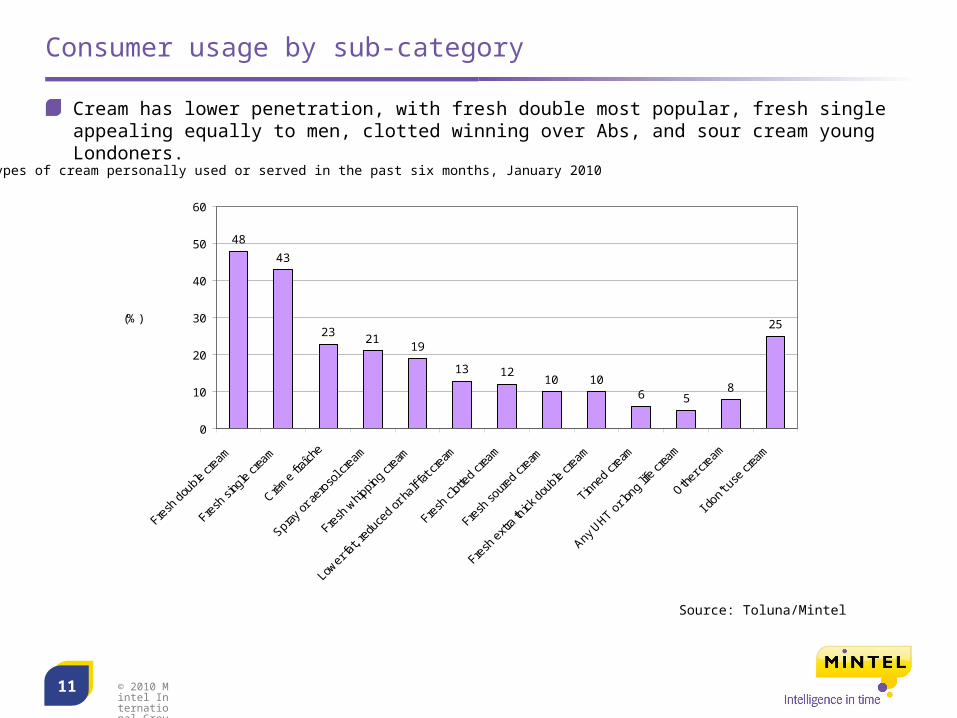

Consumer usage by sub-category

Cream has lower penetration, with fresh double most popular, fresh single appealing equally to men, clotted winning over Abs, and sour cream young Londoners.

4843

23 2119

13 1210 10

6 58

25

0

10

20

30

40

50

60

(%)

Source: Toluna/Mintel

Types of cream personally used or served in the past six months, January 2010

Your contact

tel: +44 20 7606 4533email: [email protected]

mintel.com

Head of UK Food, Drink & Foodservice Research

Ben Perkins