MiFID II Transaction reporting: Detecting and ... · PDF fileTransaction reporting: Detecting...

9

MiFID II Transaction reporting: Detecting and investigating potential market abuse www.pwc.com July 2017

Transcript of MiFID II Transaction reporting: Detecting and ... · PDF fileTransaction reporting: Detecting...

MiFID IITransaction reporting:Detecting andinvestigating potentialmarket abuse

www.pwc.com

July 2017

PwC

Transaction reportingExecutive summary

MiFID II

1

June 2017

PwC

In 2007 MiFID I introduced the concept of a harmomisedtransaction reporting regime in Europe with the aim of detectingand investigating potential market abuse.

MiFID II significantly expands on the intention and scope ofthe existing transaction reporting regulation when it comesinto effect in 2018. Regulators will soon not only be required toguard against market abuse but must also monitor the fair andorderly functioning of the market to promote market integrity.

The regulation poses many challenges for the industry, requiring65 fields to be reported across new and existing asset classes.

This is seen as one of the priorities of the regulators,significant fines have been levied on firms for inaccurateor incomplete reporting under MiFID I and some of thenational competent authorities have indicated that firmscould expect a 50% increase in the fine per breach for theirjurisdictions. For example1

1 FCA, Financial Conduct Authority, UK’s consumer regulator

PwC

MiFID II increases the scope of the transaction reporting regime to include additional asset classespreviously outside of the scope of MiFID I but within the scope of EMIR.

MiFID II

Securityderivatives(equities/

bonds)

MiFID ICash equities

EMIRFX,

commoditiesand interest

rate derivatives

Out of scope

• Financing transactions covered under theSecurities Financing TransactionRegulation (SFTR).

• Bilateral segregated collateral transfers.

• Step-ins or Step-outs.

• Allotment, issuance or exercise ofpre-emption rights.

MiFID II broadens the definition of a transaction so that it no longer only applies to just market-sidetrades and could include any transaction with a reportable financial instrument.

The purchase or saleof a reportablefinancial instrument.

1

Entering into orclosing out aderivative contract in afinancial instrument.

2

An increase or decrease inthe notional amount for aderivative contract that isa financial instrument.

3

Hitting yourown order.

4

Transaction reporting scope

MiFID II

2

June 2017

PwC

PwC

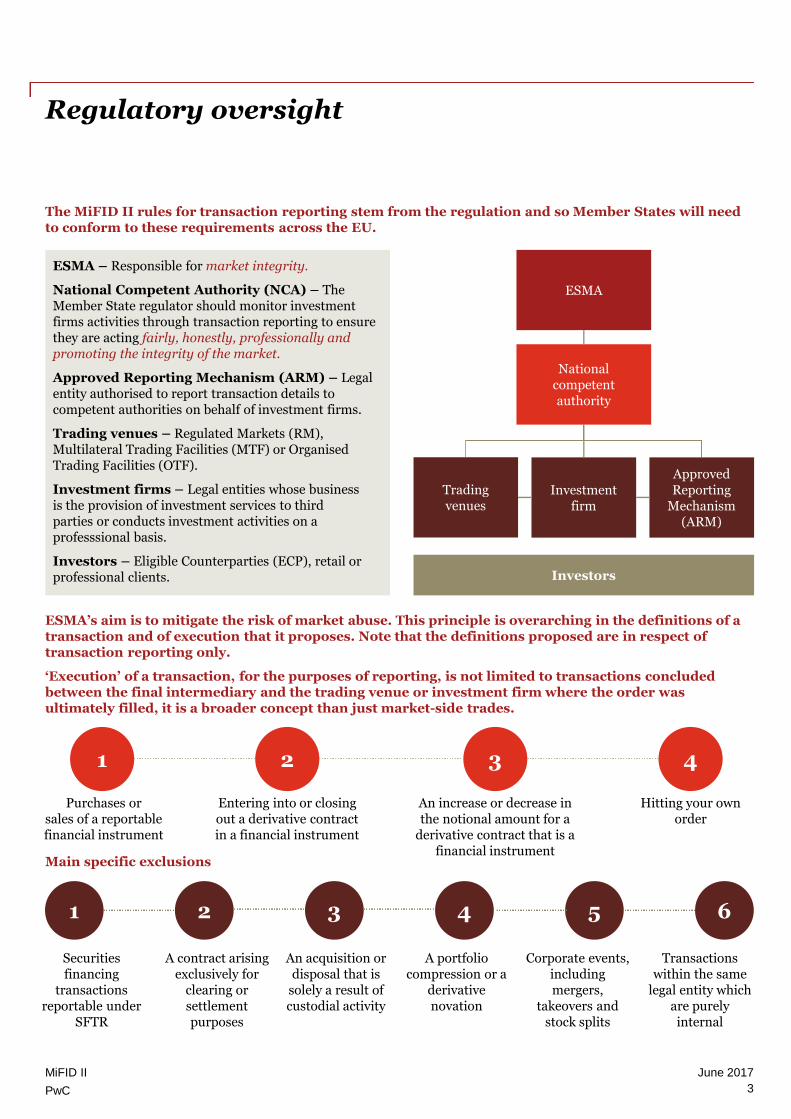

The MiFID II rules for transaction reporting stem from the regulation and so Member States will needto conform to these requirements across the EU.

Regulatory oversight

ESMA – Responsible for market integrity.

National Competent Authority (NCA) – TheMember State regulator should monitor investmentfirms activities through transaction reporting to ensurethey are acting fairly, honestly, professionally andpromoting the integrity of the market.

Approved Reporting Mechanism (ARM) – Legalentity authorised to report transaction details tocompetent authorities on behalf of investment firms.

Trading venues – Regulated Markets (RM),Multilateral Trading Facilities (MTF) or OrganisedTrading Facilities (OTF).

Investment firms – Legal entities whose businessis the provision of investment services to thirdparties or conducts investment activities on aprofesssional basis.

Investors – Eligible Counterparties (ECP), retail orprofessional clients.

ESMA

Nationalcompetentauthority

Investors

ApprovedReporting

Mechanism(ARM)

Tradingvenues

Investmentfirm

ESMA’s aim is to mitigate the risk of market abuse. This principle is overarching in the definitions of atransaction and of execution that it proposes. Note that the definitions proposed are in respect oftransaction reporting only.

‘Execution’ of a transaction, for the purposes of reporting, is not limited to transactions concludedbetween the final intermediary and the trading venue or investment firm where the order wasultimately filled, it is a broader concept than just market-side trades.

21 3 4

Purchases orsales of a reportablefinancial instrument

Entering into or closingout a derivative contractin a financial instrument

An increase or decrease inthe notional amount for a

derivative contract that is afinancial instrument

Hitting your ownorder

Main specific exclusions

21 63 54

Securitiesfinancing

transactionsreportable under

SFTR

A contract arisingexclusively for

clearing orsettlementpurposes

An acquisition ordisposal that is

solely a result ofcustodial activity

A portfoliocompression or a

derivativenovation

Corporate events,includingmergers,

takeovers andstock splits

Transactionswithin the same

legal entity whichare purelyinternal

June 2017MiFID II

3

PwC

MiFID II increases the number of reporting fields from 24 in MiFID I to 65 however, actually only 13 ofthe original fields are retained as the regulators look to standardise the requirements and make themfar more stringent.

Reporting requirements

General information

• Investment firms and Trading Venues will need toprovide the competent authority with theirtransaction report no later than T+1 at 8pm CET.

• Executing Entities and the Submitting Entity willneed to be identified using the Legal EntityIdentifier (LEI) or National ID forprivate clients.

- When investment firms are trading on behalf ofclients they will need to record and validate theLEI provided in advance of trading.

- The database of LEIs is managed and maintainedby the LEI Regulatory Oversight Committee.

• Investment firms and Trading Venues will need toassign a Transaction Reference Number(TRN) to any transactions that are executed.

Financial instruments

• It is expected that instruments will be assigned andreported using an International SecuritiesIdentification Number (ISIN).

• Instruments should be classified per theClassification of a Financial Instrument (CFI).

• Include the Market Identifier Code (MIC) whenusing a Trading Venue.

• Transaction reporting under MiFID II includes OTCderivatives and so a number of additional fields areincluded, i.e.:

- Notional increases/decreases.

- Upfront amounts.

- Optionality.

- Delivery type.

Transparency

• MiFID II requires that traders oralgorithms involved in the execution of a clientorder are identified.

• Where several persons are involved the personprimarily responsible should be recorded.

- The trader will need to record their date ofbirth and first five characters of theirgiven and last name.

• Algorithms should be assigned unique codesagainst which they can be identified upon theexecution of trades.

Regulatory flags

• Transaction reporting introduces a number of flagsto enable regulators to identify transactions that mayoverlap with other reporting regimes such as:

- Waiver indicators.

- Short selling indicator.

- OTC post-trade identifier.

- Commodity derivatives.

- Securities financing transactions.

Example indicators

Waiver Indicator

• Size – Above a specificsize transaction.

Short selling indicator

• SSEX – Short salewith exemption.

OTC post-trade indicator

• ILQD – Illiquidinstrument transaction.

June 2017MiFID II

4

PwC

New fields

What is likely to be troublesome under MiFIR?

Fields Reason

Transmissionof orders

This could be a problem for buy side firms that have traditionally relied upon their brokers toreport and for brokers that agree to receive transmitted orders. Indications are that few buy sidefirms will be able to meet the conditions for transmission for all their reportable transactions andso will have to report at least some transactions.

Short sellingindicator

The main problem is likely to impact investment banking clients that have multiple desks tradingthe same equity or sovereign debt instruments in a single legal entity. Some have indicated thatthey do not have the MI to identify short positions at the legal entity level. In addition, firmsexecuting for clients will have to report if the client is short selling.

Investmentdecisionwithin firm

Where the investment decision is made within the firm (as opposed to simply executing fora client), the person or algo must be identified. Same is true for person or algo within thefirm responsible for execution. Firms may have problems capturing this and keeping referencedata up to date.

AdditionalOTC details

With the increase in reportable products, the number of fields needed to identify an OTCderivative has expanded. Also an ETD that is traded outside the EEA needs to be identified withdetails similar to an OTC (which may cause additional problems).

Data reporting service providers/selection of ARM’s APA’s

The provision of data reporting services underMiFID II is subject to prior authorisation by therelevant Member State, which authorisation thenallows the services to be provided throughout the EU.

Different types of data reporting services mustcomply with tailored requirements which reflecttheir different roles.

• ARM’s are designed to enable investment firms toreport data to the competent authorities whereasAPAs will make public post-trade transparencyinformation required to be provided byinvestment firms, including SIs.

• As the functions performed by APAs and ARMsare not dissimilar, there is a large amount ofoverlap in the obligations which they haveto fulfil.

• Both have onerous obligations to maintain theirstatus, and both have relatively tight timelines bywhich information must be disseminated.

Despite this, ARMs tend to havelighter obligations than APAs

With ARMs, the ultimate responsibility fortrade reporting remains with the investmentfirm and there are fewer rules regarding the waydata is disseminated.

In contrast, APAs are under an obligation tostore data for a sufficient period of time and have anobligation to improve the quality of data regardingOTC contracts.

Another advantage for ARMs is the specific provisionthat they can also be trade repositories under EMIR.

The selection of an ARM is vital in meetingregulatory transaction reporting obligations,validating data, as well as assisting in the analysisof over- and under-reporting.

June 2017MiFID II

5

* Approved Reporting Mechanism (ARM)

PwC

How PwC can help

Regulation

As the MiFID II deadline of January 2018approaches investment firms are likelyto face a number of challenges in theimplementation of their transactionreporting programmes.

However, the regulators are unlikely to takea lenient position around non-compliance.

Governance

Investment firms will need to implementsystems and controls to ensure thecompleteness and accuracy of the referencedata prior to its submission and performperiodic reviews to validate its quality.

In addition firms will be required to maintainsufficient back up facilities as data omissionswould be deemed a failure.

Identifiers

MiFID II requires that entities are identifiedas an LEI which may be challenging forinvestment firms, clients will be required toprovide them with a recognised LEI andwhere one is not in place the investmentfirm may not be able to execute thetransaction on their behalf.

Investment firms may have a reliance ontheir clients to provide them with MI thatthey themselves may struggle to generate.

June 2017MiFID II

6

PwC

Contacts

Winn E Faria

Senior Manager – Risk Consulting

PwC UK

T.: +44 (0)20 7804 3843

M: 07711 562094

Elliot Hand

Manager – Risk Assurance, Bankingand Capital Markets

PwC UK

T.: +44 (0)20 7804 5724

M: 07702 697812

Ullrich Hartmann

Partner – Financial Services Risk andRegulation Leader

PwC Germany

T.: + 49 69 9585 2115

M: +349 175 2650 257

Laurent Degabriel

Partner – Financial ServicesCoE France

PwC France

T.: + 33 1 5657 8935

M: + 33 6 45 85 87 97

Are you ready for the new regime? How PwC can help

We already know that the way capital markets operate inEurope will change fundamentally. Learning both fromthe deficiencies of the original regime and from thefinancial crisis, the key goals are to radically strengthenboth market integrity and investor protection, while‘future-proofing’ the regime where possible.

Our MiFID II initiative has been established to supportyou in all aspects as the new regime comes into focus,providing insights and perspectives. As a network, wecan mobilise multi-disciplinary teams bringing togetherskilled strategy, change management, operationalefficiency, IT, tax, legal and regulatory specialists withextensive knowledge of global and European securitiesmarkets to help you address the challenges and realisethe opportunities that MiFID II can bring.

To access our suite of tools, propositions, insights andthought leadership, as well as our multi territory networkplease visit our dedicated webpage:

http://www.pwc.com/MIFIDII and our and our MiFID IIYoutube Channel

https://www.youtube.com/c/MiFIDIIPwC

About us:

PwC helps organisations and individuals create the value they’re looking for.

We’re a network of firms in 157 countries with more than 195,000 people who are committed to delivering quality inassurance, tax and advisory services.

Learn more about PwC by following us online: @PwC_LLP, YouTube, LinkedIn, Facebook and Google+.

June 2017MiFID II

7

This document has been prepared only for MiFID II and solely for the purpose and on the terms agreed with MiFID II. We accept no liability (includingfor negligence) to anyone else in connection with this document, and it may not be provided to anyone else.

© 2017 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to the UK member firm, and may sometimes refer to thePwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

170623-120931-DF-OS